Embed Size (px)

Citation preview

MARY FRANCES CHARLTONLEGAL AID JUSTICE CENTER

The Affordable Care Act in

Virginia

Overview

Affordable Care Act, aka “Obamacare”

Goals Affordable Insurance Coverage Private Insurance Reform Better Health Delivery System

Eligibility Guidelines&

Enrollment Process

Health Insurance Marketplace

Federally Facilitated Marketplace (FFM)To compare / purchase private health

insurance Qualified Health Plans (QHPs) Premium Tax Credits only available with FFM plans

Also available to small employers Fewer than 50 “full time equivalent” employees Small Business Health Options

Program “SHOP”

Open Enrollment

November 15, 2014-February 15, 2015If enrolled by December 15, coverage can begin

January 1, 2015“Special Enrollment” after February 15 to

enroll/change plan Loss of other coverage (except for non-payment, rescission) Birth, adoption, marriage Change in immigration status Error by FFM Other exceptional circumstances

• Note: Medicaid/FAMIS applications accepted & processed all year

Eligibility for Premium Tax Credits

Marketplace eligibility requires you to:Live in its service areaBe a US citizen or national, or be a non-citizen

who is lawfully present in the US for the entire time coverage is sought. Exception: DACA recipients not eligible.

Not be incarcerated Can apply for Marketplace if pending disposition of charge Can apply for Medicaid/CHIP at any time

Not have access to affordable and adequate insurance

The ACA and Imigration

Those lawfully present for the year they seek coverage (i.e. for this enrollment period those present 1/1/14 - 12/31/14) can access and benefit on the Marketplace. Exception: DACA

Undocumented persons cannot. Those who have been present <5 years may be

precluded from accessing Medicaid/Medicare and are therefore eligible.

Note: Unlawful presence is an exception to penalties under the mandate, but often other exceptions will apply and can be claimed instead.

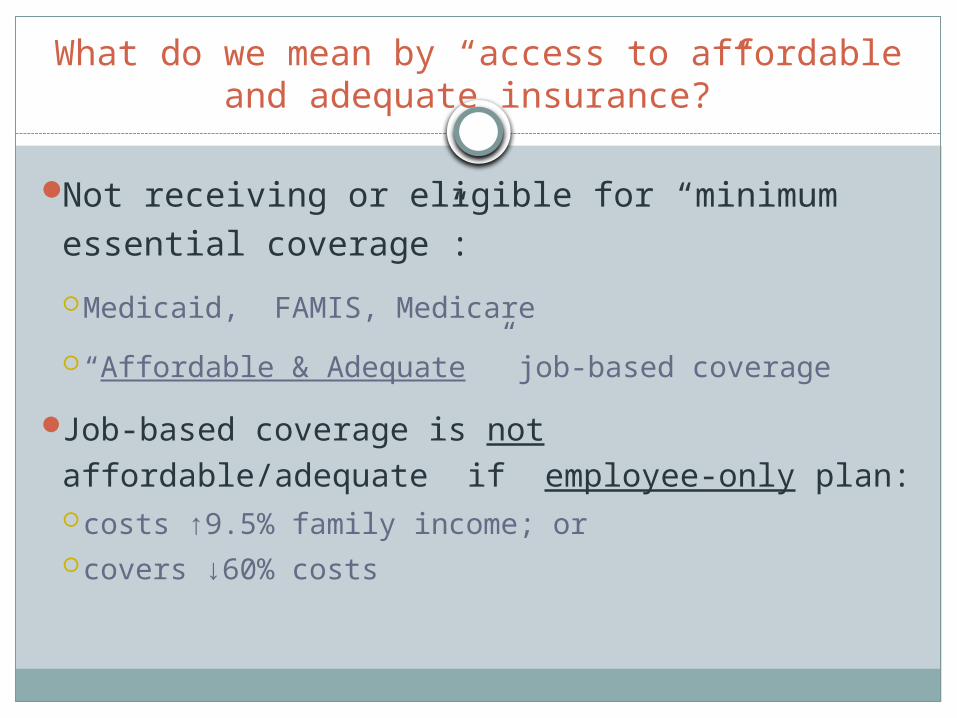

What do we mean by “access to affordable and adequate insurance?”

Not receiving or eligible for “minimum essential coverage”:

Medicaid, FAMIS, Medicare

“Affordable & Adequate ” job-based coverage

Job-based coverage is not affordable/adequate if employee-only plan: costs ↑9.5% family income; or covers ↓60% costs

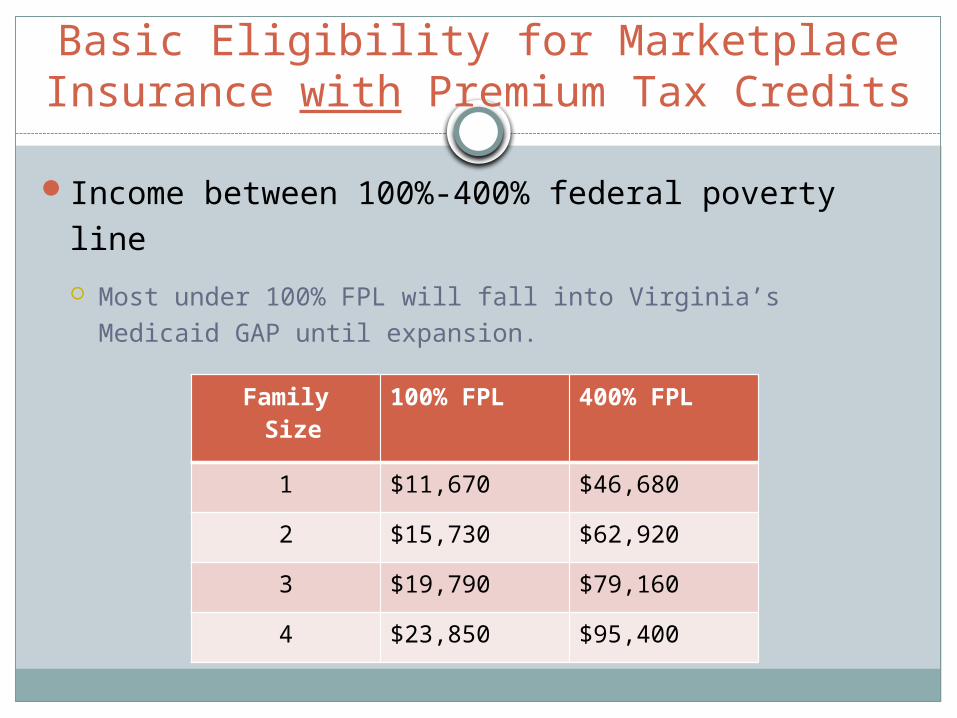

Basic Eligibility for Marketplace Insurance with Premium Tax Credits

Income between 100%-400% federal poverty line

Most under 100% FPL will fall into Virginia’s Medicaid GAP until expansion.

Family Size

100% FPL 400% FPL

1 $11,670 $46,680

2 $15,730 $62,920

3 $19,790 $79,160

4 $23,850 $95,400

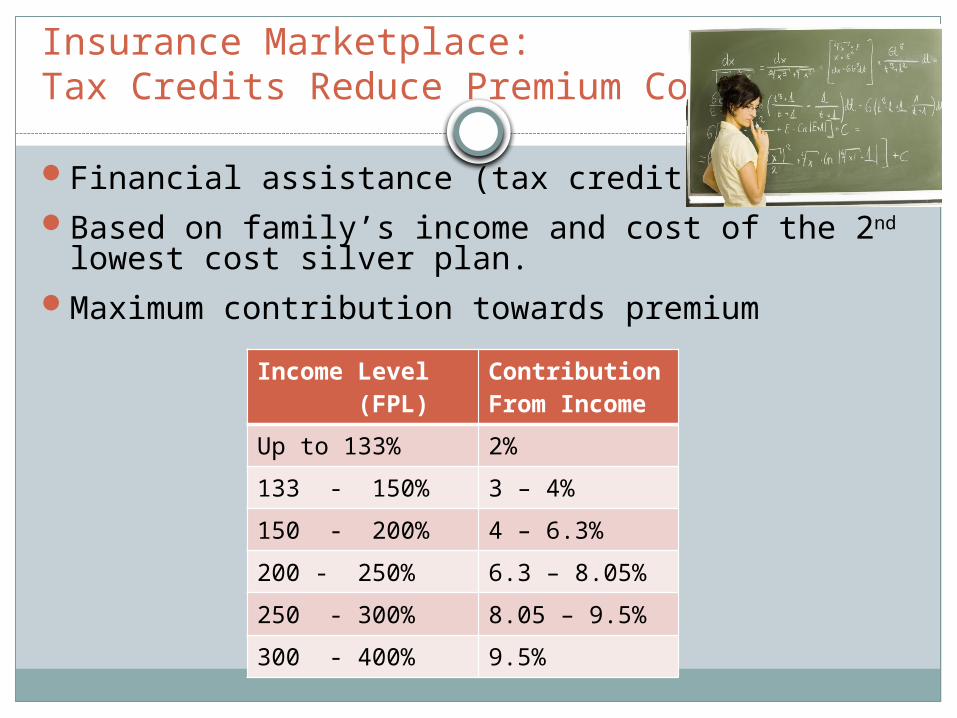

Insurance Marketplace: Tax Credits Reduce Premium Costs

Financial assistance (tax credits)Based on family’s income and cost of the 2nd lowest

cost silver plan. Maximum contribution towards premium

Income Level (FPL)

Contribution From Income

Up to 133% 2%

133 - 150% 3 – 4%

150 - 200% 4 – 6.3%

200 - 250% 6.3 – 8.05%

250 - 300% 8.05 – 9.5%

300 - 400% 9.5%

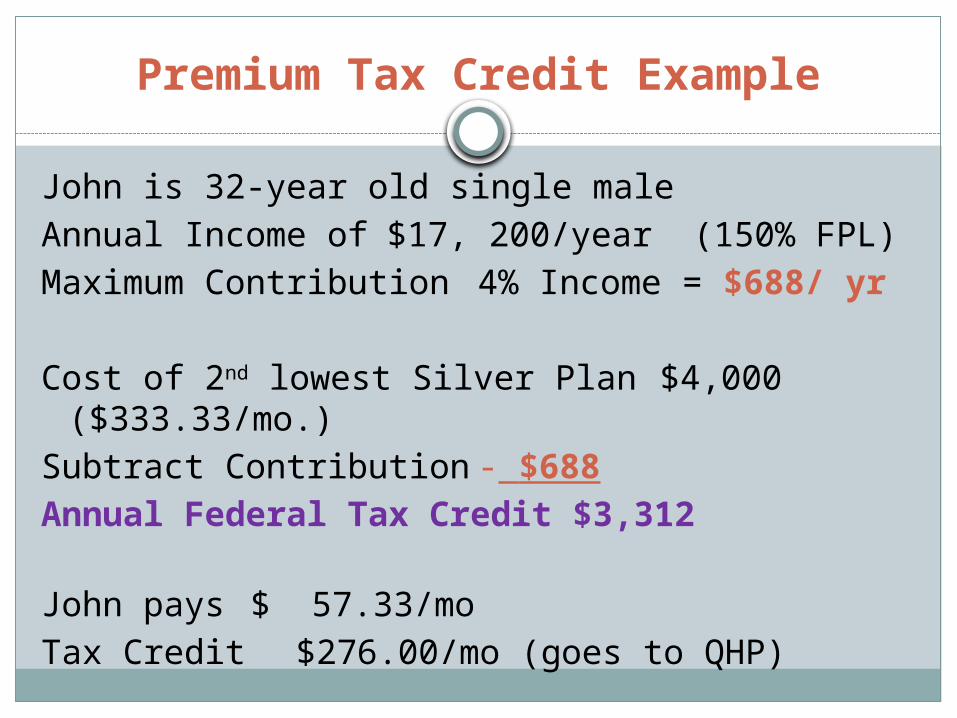

Premium Tax Credit Example

John is 32-year old single maleAnnual Income of $17, 200/year (150% FPL)Maximum Contribution 4% Income = $688/ yr

Cost of 2nd lowest Silver Plan $4,000 ($333.33/mo.)

Subtract Contribution - $688Annual Federal Tax Credit $3,312

John pays $ 57.33/moTax Credit $276.00/mo (goes to QHP)

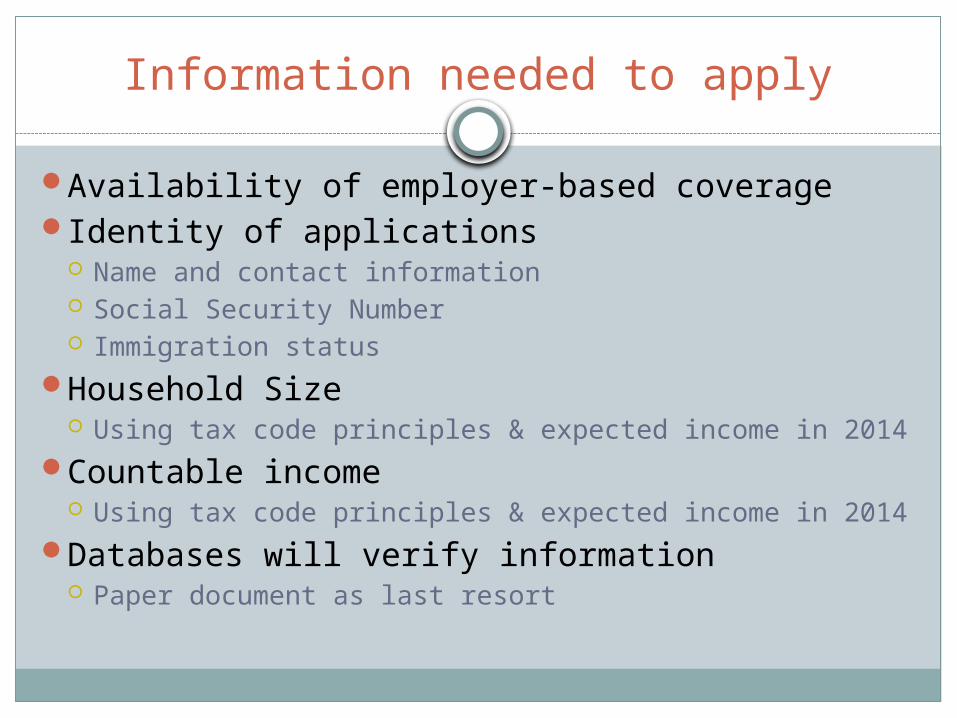

Information needed to apply

Availability of employer-based coverageIdentity of applications

Name and contact information Social Security Number Immigration status

Household Size Using tax code principles & expected income in 2014

Countable income Using tax code principles & expected income in 2014

Databases will verify information Paper document as last resort

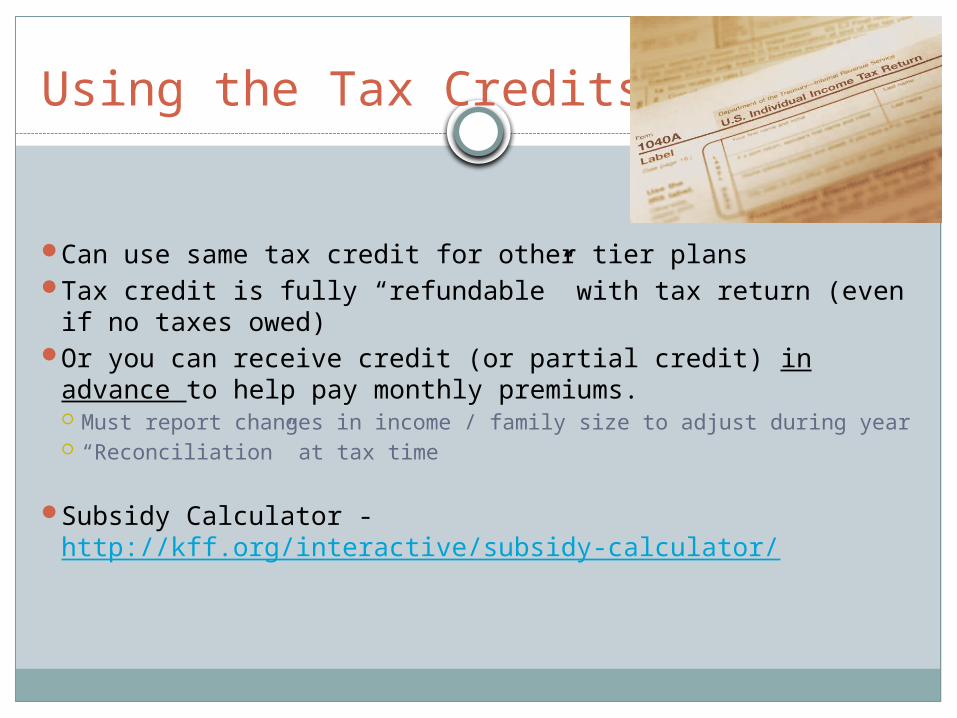

Using the Tax Credits

Can use same tax credit for other tier plansTax credit is fully “refundable” with tax return (even if

no taxes owed)Or you can receive credit (or partial credit) in advance to

help pay monthly premiums. Must report changes in income / family size to adjust during year “Reconciliation” at tax time

Subsidy Calculator - http://kff.org/interactive/subsidy-calculator/

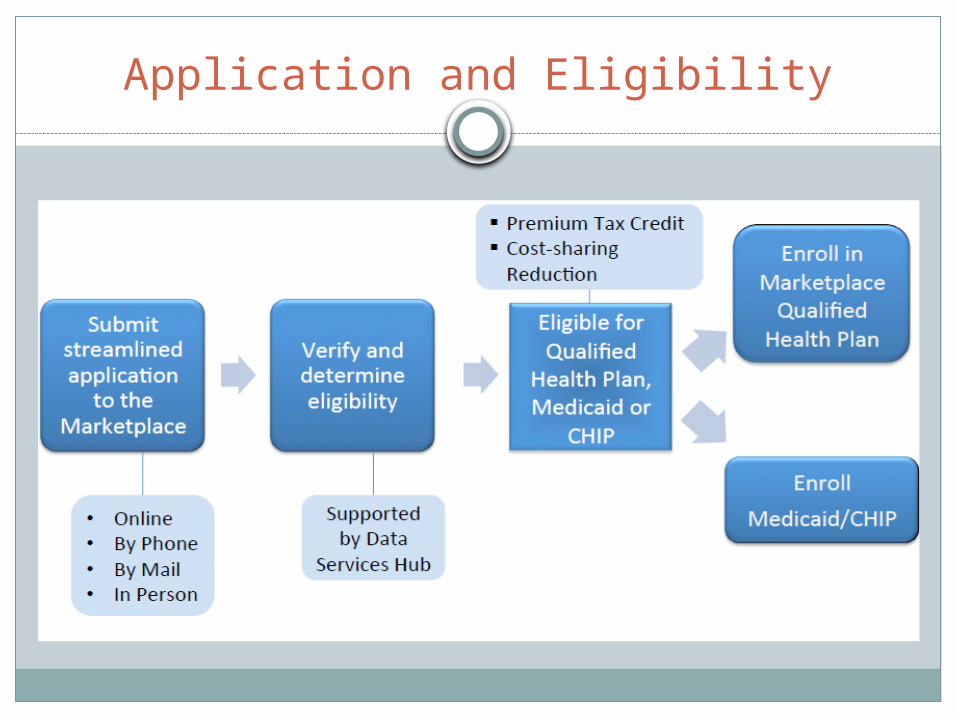

Application and Eligibility

What to Consider When Choosing a Plan

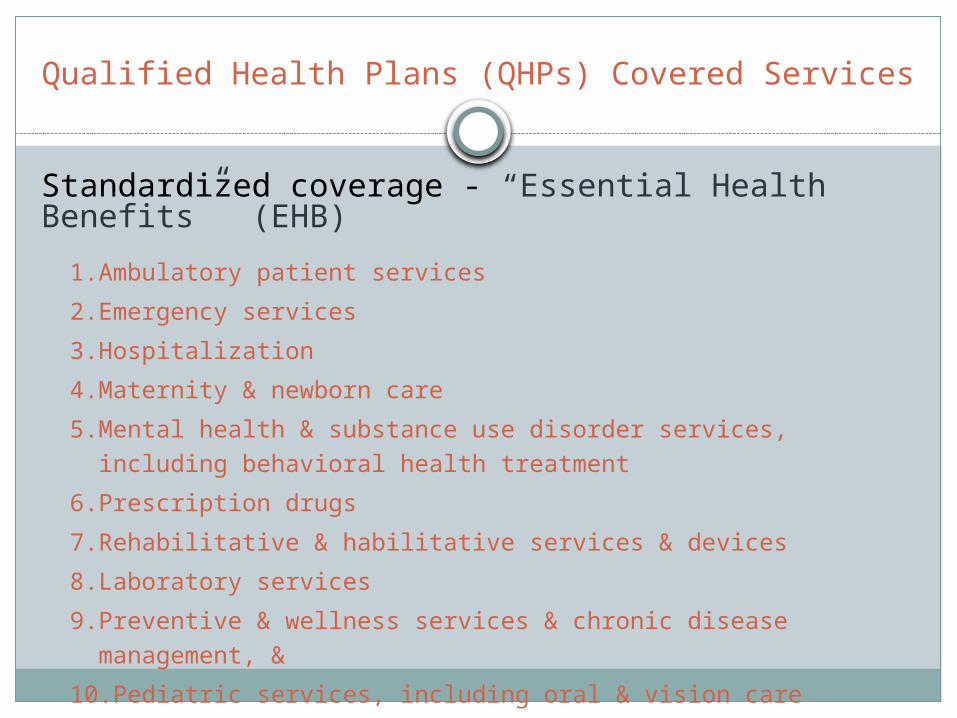

Qualified Health Plans (QHPs) Covered Services

Standardized coverage - “Essential Health Benefits” (EHB)

1.Ambulatory patient services

2.Emergency services

3.Hospitalization

4.Maternity & newborn care

5.Mental health & substance use disorder services, including behavioral health treatment

6.Prescription drugs

7.Rehabilitative & habilitative services & devices

8.Laboratory services

9.Preventive & wellness services & chronic disease management, &

10.Pediatric services, including oral & vision care

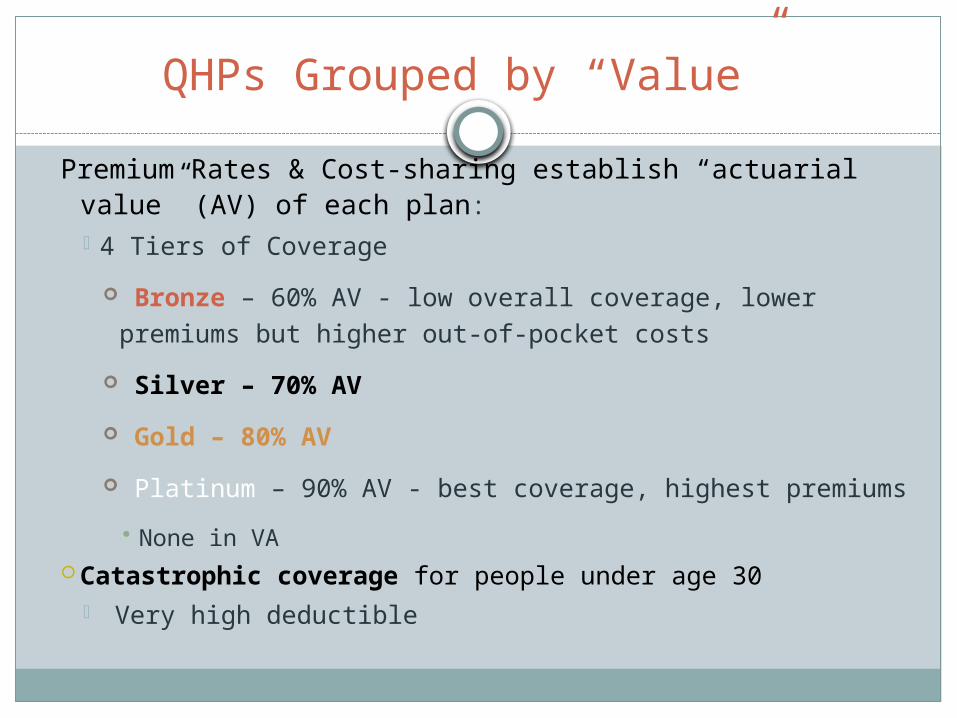

QHPs Grouped by “Value”

Premium Rates & Cost-sharing establish “actuarial value” (AV) of each plan: 4 Tiers of Coverage

Bronze – 60% AV - low overall coverage, lower premiums but higher out-of-pocket costs

Silver – 70% AV

Gold – 80% AV

Platinum – 90% AV - best coverage, highest premiums

• None in VA Catastrophic coverage for people under age 30

Very high deductible

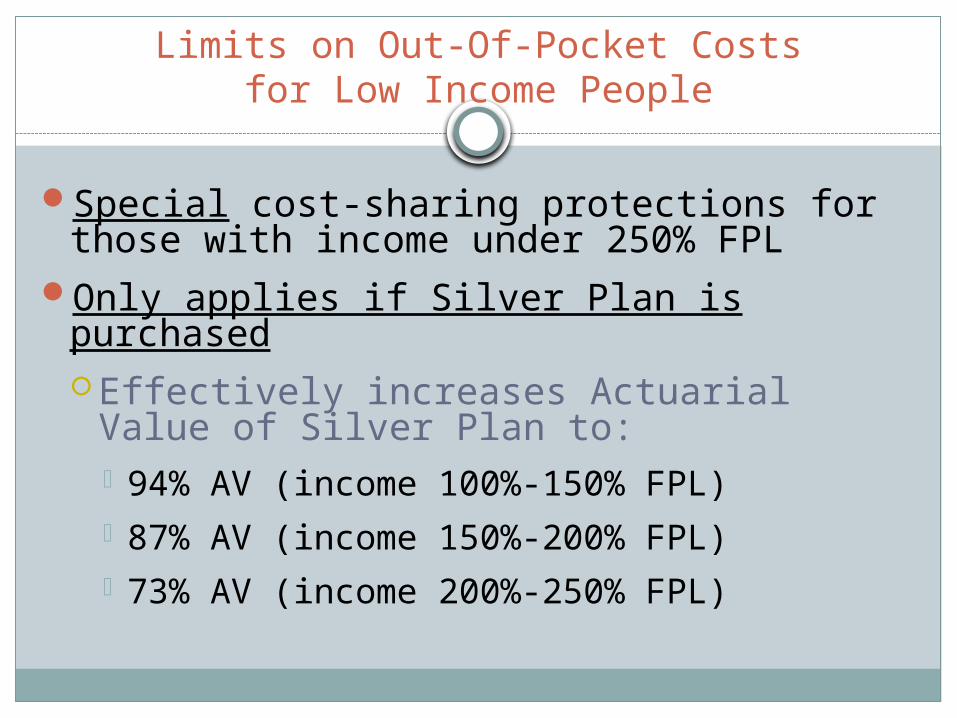

Limits on Out-Of-Pocket Costs for Low Income People

Special cost-sharing protections for those with income under 250% FPL

Only applies if Silver Plan is purchased Effectively increases Actuarial Value of

Silver Plan to: 94% AV (income 100%-150% FPL) 87% AV (income 150%-200% FPL) 73% AV (income 200%-250% FPL)

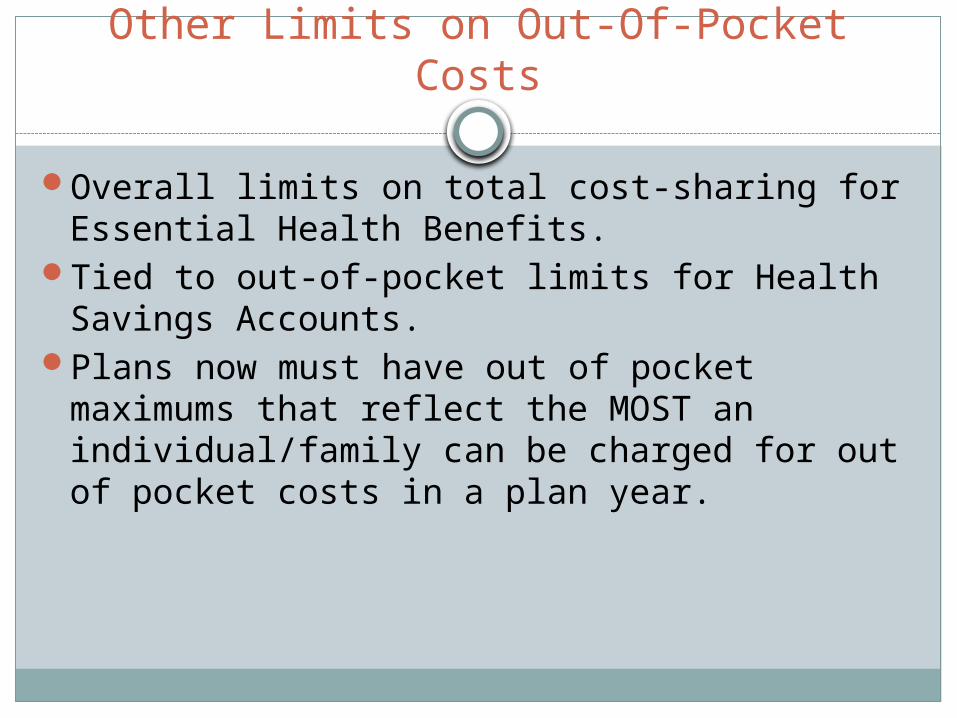

Other Limits on Out-Of-Pocket Costs

Overall limits on total cost-sharing for Essential Health Benefits.

Tied to out-of-pocket limits for Health Savings Accounts.

Plans now must have out of pocket maximums that reflect the MOST an individual/family can be charged for out of pocket costs in a plan year.

Minimum Coverage Requirements Tax Penalties

• Individual / Family penalty is much less than cost of insurance.

• Penalty is the greater of: 2014 - $95 /adult + $47.50 /child (up to $285) or 1%

family income* 2015 - $325/adult + $165.50/child (up to $975) or 2%

family income* 2016 - $695/adult + $347.50/child (up to $2085) or 2.5%

family income*• Large Employer Penalty in 2015 if affordable coveragenot offered.

[*Income is amount over taxfiling threshold]

If you signed up for a plan in 2013-2014 Open Enrollment…

To continue health coverage in 2015, you can renew your current health plan or choose a new health plan through the Marketplace during the 2015 Open Enrollment period.

Your insurance company will send you information this Fall about updated premiums and benefits.

If you’re happy with your current plan and want to keep it--and your income or household size haven’t changed - you don’t need to do anything. The Marketplace will auto-enroll you in the same plan for 2015.

If you signed up for a plan in 2013-2014 Open Enrollment…(continued)

If you want to change plans, you can: Choose any other Marketplace health plan your

company offers in your service area if you want to stay with your current insurance company.

Choose a new health plan from a different insurance company through the Marketplace.

Buy a new private health plan outside of the Marketplace. If you do this, you won’t be eligible for premium tax credits and cost-sharing reductions offered through the Marketplace

Questions?ENROLL Virginia! is a nonprofit, nonpartisan entity that assists individuals and small businesses to obtain health insurance including commercial health coverage through the federally facilitated health insurance marketplace, to qualify for applicable tax subsidies, and to comply with the U.S. Patient Protection and Affordable Care Act and avoid penalties for failure to do so. The program is paid for by a federal grant (Funding Opportunity Number CA-NAV-13-001 from the U.S. Department of Health and Human Services, Centers for Medicare & Medicaid Services) and administered by the Virginia Poverty Law Center. The contents provided here are solely the responsibility of the authors and do not necessarily represent the official views of HHS or any of its agencies.