Embed Size (px)

Citation preview

CHAPTER V

MARKETING STRATEGY OF COMMERCIAL BANKS – AN APPRAISAL

CONTENTS

1. Marketing – the Concept

2. Marketing of Banking Services

3. Bank Marketing Objectives

4. Bank Marketing in India

5. Bank Marketing Strategy

6. Primary Data Analysis

a) Socio-Economic Profile of Customer

Respondents

b) Opinion of Customers on Marketing

Strategy

c) Opinion of Bank Personnel on Marketing

Strategy

References

CHAPTER V

MARKETING STRATEGY OF COMMERCIAL

BANKS – AN APPRAISAL

Marketing – the Concept

Years back, the concept of marketing centred around the selling and buying

activities and, therefore, the functional areas of marketing were totally related with

the management of sales and purchases. Today there is a sea change in this

concept of marketing and its functional areas. Now all organisations either

producing goods or generating services give significant consideration for customer

satisfaction while shaping organisational policies i.e., a basic shift from selling-

oriented to customer-oriented business. Selling focuses on the needs of the seller

while modern marketing focuses on the needs of the buyer.

Marketing management is the function of managing the marketing

activities. “Marketing management is the process of planning and executing the

conception, pricing, promotion and distribution of ideas, goods and services to

create exchanges that satisfy individual and organizational objectives”1. Basically

marketing is a business technique devised to sell products and services keeping in

mind the needs and requirements of existing and prospective customers. Thus

marketing becomes a customer satisfaction engineering in which marketer’s efforts

assign due weightage to customer satisfaction.

Marketing of Banking Services

The concept of marketing of banking services is of recent origin. It is only

during 1950s banks came to accept the marketing concept for bank services. Bank

marketing is the aggregate of functions directed at providing services to satisfy

customers’ financial needs and wants more efficiently and effectively than the

148

competitors in consonance with the organisational objectives.2 In a true sense, it is

the application of marketing techniques in the banking services. Application of

marketing techniques in banking, in simple terms, means a coordinated

organisational effort to reach the customer to fulfill his specific needs for getting

his patronage, through utilisation of people, products or services, price, promotion,

branch outlets and distribution policies for maximising customer satisfaction.3 In a

competitive situation banks sell their services through branch counters throughout

the entire country through the employees who act as salesmen recruited by the

management.

Bank Marketing Objectives

In this stage it is fruitful to have a discussion on the objectives of Bank

Marketing. The basic objectives of marketing are applicable in the case of bank

marketing also. They are:

• Maximising the profitability

• Providing high return to investors

• Development of an image and reputation and

• Developing new products to meet emerging customer requirements.

But the specific objectives of bank marketing are:

• increase in deposits

• increase in loans

• diversification of products and

• directing customers to specific products

The achievement of these objectives necessitates that the marketing

department should undertake the following functions:

1. analysis of the customer behaviour, attitudes and market segmentation.

2. market research to collect, investigate analyse and interpret customers’

attitudes and market developments to contribute to the maximum attainment

of objectives.

149

3. development of new products and/or services

4. advertising, publicity and promotion

5. pricing

6. defining strategies, administering and controlling the marketing programme

7. forecasting changing customer profiles and consequent product changes.4

Bank Marketing in India

Originally the marketing concept came into the Indian banking sector in the

form of advertising and promotion. The first major step in the direction of bank

marketing was initiated by State Bank of India in 1971. Groupwise segmentation

was introduced by SBI to assess and understand the specific needs of groups of

customers. It recognised itself on the basis of major market segments, dividing the

borrowing customers on the basis of activity and set up four major market

segments viz., commercial and institutional, small industries and business,

agriculture and personal and services banking segments. A few need based

schemes like home loan accounts, education loans, installment credit etc. were

added to the traditional services range.

The example of SBI was followed by a few other banks. Canara Bank is a

pioneer in this respect which showed how an Indian Bank could be market

innovative and could manage and respond to the changes in the banking

environment so quickly and efficiently. Foreign banks also used different

marketing techniques successfully in India in fund mobilisation and promotion of

consumer credit.

As a result of liberalisation there was an all round growth in competition in

the financial sector, especially in the banking sector. Along with the existing

Public Sector Banks and Old Private Sector Banks, some New Generation Banks

and Foreign Banks entered the scene. As the bank customers got a chance to make

choice from among different offers from different banks and other financial

agencies they became very selective and compelled bankers to project their

presence enthusiastically. This led to acute competition in the sector. Customers

150

are always selective. So the degree of success in this respect depends directly on

the degree of understanding of each group of customers. Also the mounting

intensity of competition results in quality gap5 as some competitors in the field,

especially foreign banks and new private banks, excel others in providing core and

peripheral services using advanced information technologies and develop human

resources accordingly.

Foreign Banks in India have been the pioneers in the field to apply the

quality difference in their services. Aggressive marketing and technological

advancement help them to make inroads into the bank market. Though concerted

efforts were there on the part of Indian banks, they, especially public sector banks,

were far behind in applying the marketing strategies. The technological advantages

of Foreign Banks and New Generation Banks were not available for majority of

other Indian Banks. Technological obsolescence was also a major hindrance in

this respect.

The reform process started in the beginning of 1990s led the management

and staff to the real situations. The opening of new private sector banks and

foreign banks and their application of marketing techniques made management and

staff think about marketing in their banks. They identified the need for product

laboratories for designing and developing new products. But the problem was, in

most banks, management personnel had little knowledge and experience about

marketing in a competitive environment. Their previous experience was mainly in

deposit mobilisation and in achieving deposit targets. But the situation has

changed. The emphasis has further shifted away from deposits to capturing prime

customers wanting credit facilities, raising funds from the market, offering more

and more technology oriented products and even recruiting and retaining skilled

personnel. Perhaps the most significant change is the pursuit of asset-led growth.6

The marketing of loans becomes a major occupation of management at all levels-

senior to junior. The efficiency of an officer as a banking professional is measured

in terms of his success as a loan officer. Of course, this does not mean that the need

151

for cheap funds or deposits does not exist but there is need for value addition as a

result of these efforts.7

Bank Marketing Strategy

The marketing strategy of a business consists of certain components which,

as a blend is named as marketing mix. The marketing mix of a bank is considered

as its marketing strategy as this mix or the combination of this mix varies with the

situation or environment.

The marketing mix of a bank consists of seven component sub mixes:

product, price, place, promotion, process, people and physical evidence. These are

considered as the 7 P’s or 7 elements of bank marketing strategy. In addition to

the first 4 P’s of ordinary marketing, 3 more P’s are applicable in the case of bank

marketing. These seven P’s are not much effective in isolation. An appropriate

blend of these P’s is necessary for a well orchestrated marketing strategy. Banking

professionals’ excellence in blending these sub-mixes gives the best result in the

form of satisfaction to customers and profit to the organisation.

Product – The First ‘P’

A product is anything that can be offered to a market for attention,

acquisition, use or consumption that might satisfy a want or need.8 It is a bundle of

utilities consisting of various product attributes and accompanying services. The

services are of intangible nature and banking services are of that nature. The

banking professionals are expected to develop different dimensions of products so

that the banking services are made attractive, innovative and competitive. Since

banks have customers from different walks of life, a single product specification

will not be attractive for all. Service/product of an optimal mix of core and

peripheral dimensions will raise the attraction of the product. Generally banking

products are grouped under three different heads: Core products, Formal products

and Augmented products/Peripheral services. Core products are those products in

which a banker is engaged in business. For a bank, core products are savings

152

banks, term deposits, current accounts, cash credits, overdrafts, term loans and so

on. Formal products are made up of a combination of two or more core products

and they have a strong marketing content to meet some customer needs. Unfixed

Deposit scheme 9 of Citi Bank is an example for this. The Augmented product is a

Formal product with some ancillary benefits or peripheral services attached to it.

For example in many banks when one opens a savings bank account he gets an

ATM Card or Credit Card. The different services of a bank form the product mix

of the bank. The formulation of a sound product mix is very essential to survive

and compete in the market.

Price – The Second ‘P’

Price is the interest, fees and commission charged and paid by the bank.

Price will determine the profitability of the banks. In a highly regulated market,

banks have little option in deciding the prices. In the regulated market, the RBI

prescribed deposit and lending interest rates and the Indian Banks Association took

decision regarding other charges. Naturally, Indian Banks have not felt any need

to develop their own pricing strategy. But the situation has steadily changed to

deregulated market due to liberalisation. Through RBI’s credit policy

commencements substantial deregulation has brought in, and now banks have

flexibility in their pricing policy. Thus, liberalisation has brought in almost

complete freedom to the banks to decide the price according to market situations.

Place – The Third ‘P’

This ‘P’ signifies placing or distribution of services to the ultimate

customers. The service mix of banks moves through different distribution

channels, such as, the branches, the executives and the staff. A suitable location/

point for the establishment of a bank branch is very important. It should give

conveniences and comfort to the customers. As far as possible, services should

reach the doorsteps of the customers. The behavioral profile and efficiency of the

bank personnel is also equally important. No gap in the distribution process would

153

occur that will hinder smooth flow of services since inconveniences to customers

would act as a demotivational tool that will result in deserting a bank.

Conveniences inside the premises also attract customers to the bank. It

should be neat, clean and well furnished. There are many well equipped and air-

conditioned branches for many banks. But many others lack proper space, filled

with old and worn-out furniture and look unattractive. Effective marketing requires

good appearance and comfortable surroundings.

Technology has been in extensive use to reach customers now (Refer

Ch. II). Strategic alliance with other players in the field for providing banking

services is another strategy under place mix. Through this, there is a possibility for

covering wider geographical area through other established banks, especially for

new banks with limited number of branches. Special counters for certain segments

of customers like pensioners, specialized branches for special customers like Non-

Resident Indians, exporters etc. and single window concept are now in the offing.

Mobile offices and officers which are reaching to customers are in use in many

banks.

Promotion – the Fourth ‘P’

The fourth ‘P’, promotion plays an important role in promoting banking

business. It communicates with the customers/prospective customers on almost all

the aspects of the marketing mix like advantages of different products, details of

how it is delivered, details on the interest and commission paid and charged by the

bank etc. Simultaneously, it persuades the prospective customers to bank’s

products. Thus marketing promotion has two basic objectives – first one to inform

the prospective customers and second one to persuade them. This could be in

various shapes like advertisement, personal interaction and sales campaign. Or this

could be a combination of various promotional instruments. Basically there are

four important components for promotion strategy, such as:

154

Advertising

Sales Promotion

Publicity and

Personal Selling

While formulating a promotion mix, optimal blending of all the four

elements is necessary to succeed in informing, persuading, reminding and

reinforcing customers.

Advertising

Traditional meaning of advertising is that it is a paid form of non-personal

presentation and promotion of ideas, goods and services by an identified sponsor.

It is a paid form of persuasive communication. In bank marketing it is the bank

which directly talks about itself, and pays for doing so. Here the bank tells the

prospective customer the merits of its products and how it satisfies the customer.

Earlier public sector banks were prohibited from advertising through media. But

now they have the freedom to advertise, along with private and foreign banks, their

product launch, brand building and their corporate philosophy.

Sales Promotion

Sales promotion, the next component of the promotion mix, is found

effective in motivating the customers and the employees of the bank. It comprises

of short term activities intending to boost the banking business. It helps a bank in

increasing its market share by helping to launch a new scheme/service or by

supporting an ailing or modified one. Moreover, sales promotion activities are

attention-raisers that will influence prospective customers. If advertising is aimed

to increase loyalty towards a brand, sales promotion techniques are intended to

increase the actual immediate purchase by existing or prospective buyers. The

tools of sales promotion in banks may be in the form of gifts, contests, fairs and

shows, discounts and commissions, low interest financing, entertainment and

traveling and additional allowance.

155

Personal selling

Personal selling10 is an important component of promotion mix. It is very

much instrumental in promoting banking business. It is a function of informing the

prospective customers and persuading them to purchase products through personal

communication in an exchange situation. In personal selling inter-personal or

two–way communication happens and that makes way for a feedback. Moreover,

personal selling may be interchanged with persuasion, in meaning, and persuasion

has an effective role in the banking business. Personal selling becomes very much

effective in improving the quality of banking services since the bankers have a

command on it. This art of telling-and-selling is known as personal selling in

which an individual, based on his/her expertise, attempts to transform the prospects

into customers.11 It is a form of direct selling.

Public Relations and Publicity

The next component, public relations, occupies an outstanding place in the

promotion of banking services. In banking services the development of rapport

with customers plays an incremental role in getting the business or keeping the

business. It is a two–way communication system to develop mutual understanding

between a banking organisation and its customer. It is the way to inform the public

about the organisational programmes and activities, so as to create the best public

reputation. Most probably it is in the form of a press release to newspapers and

banking magazines or financial news so as to create the interest of customers. In

banks there is a Public Relations Department and Public Relations Officers. The

other components of public relations are press bits distributed during press

conference, speeches, seminars, annual reports, charitable donations, sponsorships,

community relations and lobbying the noted personalities, VIPs etc.

Process – the Fifth ‘P’

The organisational activities or processes of a typical banking concern were

mostly designed during the traditional banking period. In the present scenario of

156

reforms basic changes in banking systems and procedures are necessary for

achieving customer satisfaction. The need of the hour is more customer-friendly

and marketing-oriented processes that will give uniqueness to the product. For this

the work-flow in a bank branch should be customer-oriented so as to give

maximum convenience to the customers. Similarly, the present reporting system

of sending too many reports/statements should be abolished to reduce the workload

of the bank staff. Some bankers have already taken this issue in their consideration

while introducing information and communication technology based systems and

procedures.

People - The Sixth ‘P’

People are an important component of bank marketing strategy as human

factor is very influential in services marketing. As the inseparability principle is

applicable in bank marketing, the services and service providers are not separable

in banks. So the quality of service provided by a bank depends on the quality of

people available to the bank. Only quality people can generate efficiency ad

improve productivity. A fair synchronisation of dedicated and committed team of

efficient professionals and new information technology could perform fantastically

to produce the best result as in some foreign banks and private banks. Human

resource development is the way for the formation of human capital. Since the

banking services are intended for customer satisfaction, it is imperative that the top

executives at the apex level should give due consideration for their human capital

and the people at the counter.

Physical Evidence –The Seventh ‘P’

Like all service products, banking products are also intangible. Making it

tangible is a major duty of the banker and for that he uses the instrument of

physical evidence in different forms in banks. Proper upkeep of branch premises

and interior decoration of branches are originally part of place strategy but which

have relevance from the standpoint of physical evidence also. Most of the banks in

157

India accepted this fact with enthusiasm and there is a new look and convenience

for many bank branches. Another area of physical evidence is the stationery items

like cheque book, pass book supplied to customers and other stationery materials

in use. These items may be redesigned to look attractive, clear and convenient to

customers. An attractively designed product brochure, a catchy brand name for a

product, timely supply of statement of account etc. will make the products tangible.

PRIMARY DATA ANALYSIS

In the background of the above said details, enquiry was made with

customers and personnel of commercial banks to know their opinion and

perception on various marketing strategies of their banks.

SOCIO - ECONOMIC PROFILE OF CUSTOMER RESPONDENTS

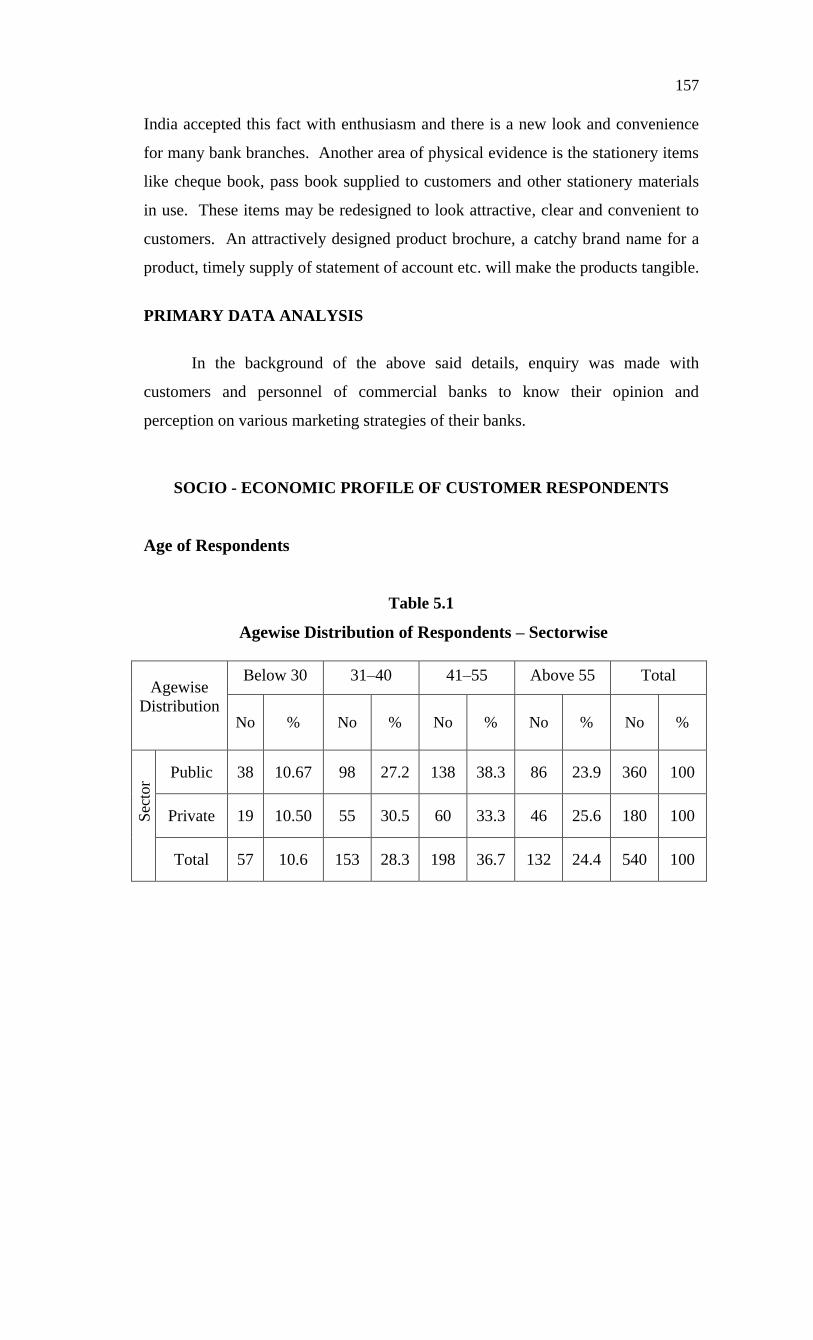

Age of Respondents

Table 5.1

Agewise Distribution of Respondents – Sectorwise

Agewise

Distribution

Below 30 31–40 41–55 Above 55 Total

No

%

No

%

No

%

No

%

No

%

Public 38 10.67 98 27.2 138 38.3 86 23.9 360 100

Private 19 10.50 55 30.5 60 33.3 46 25.6 180 100

Total 57 10.6 153 28.3 198 36.7 132 24.4 540 100

Sec

tor

158

Table 5.2

Agewise Distribution of Respondents – Locationwise

Agewise

Distribution

Below 30 31–40 41–55 Above 55 Total

No

%

No

%

No

%

No

%

No

%

Urban 22 12.2 65 36.1 63 35 30 16.7 180 100

Semi

Urban

19 10.5 45 25 72 40 44 24.4 180 100

Rural 16 8.9 43 23.9 63 35 58 32.2 180 100

Total 57 10.6 153 28.3 198 36.7 132 24.4 540 100

Table 5.1 and Table 5.2 reveal that out of the 540 respondents, 153 i.e., 28.3

percent belonged to the age category of 31–40 years, 198 respondents i.e., 36.7

percent were in the 41–55 years category and 132 persons i.e., 24.4 percent were in

the above 55 years category. Only 57 i.e., 10.6 percent of the respondents

belonged to below 30 years category. The sector wise distribution also revealed

more or less same picture.

In location wise distribution, it can be observed that in urban branches 12.2

percent belonged to below 30 years category, 36.1 percent belonged to 31-40

category, 35 percent belonged to 41-55 category and 16.7 percent belonged to

above 55 category. In semi-urban branches, they were 10.5 percent, 25 percent, 40

percent and 24.4 percent, respectively. In rural branches 8.9 percent, 23.9 percent,

35 percent and 32.2 percent were the corresponding figures.

Loca

tion

159

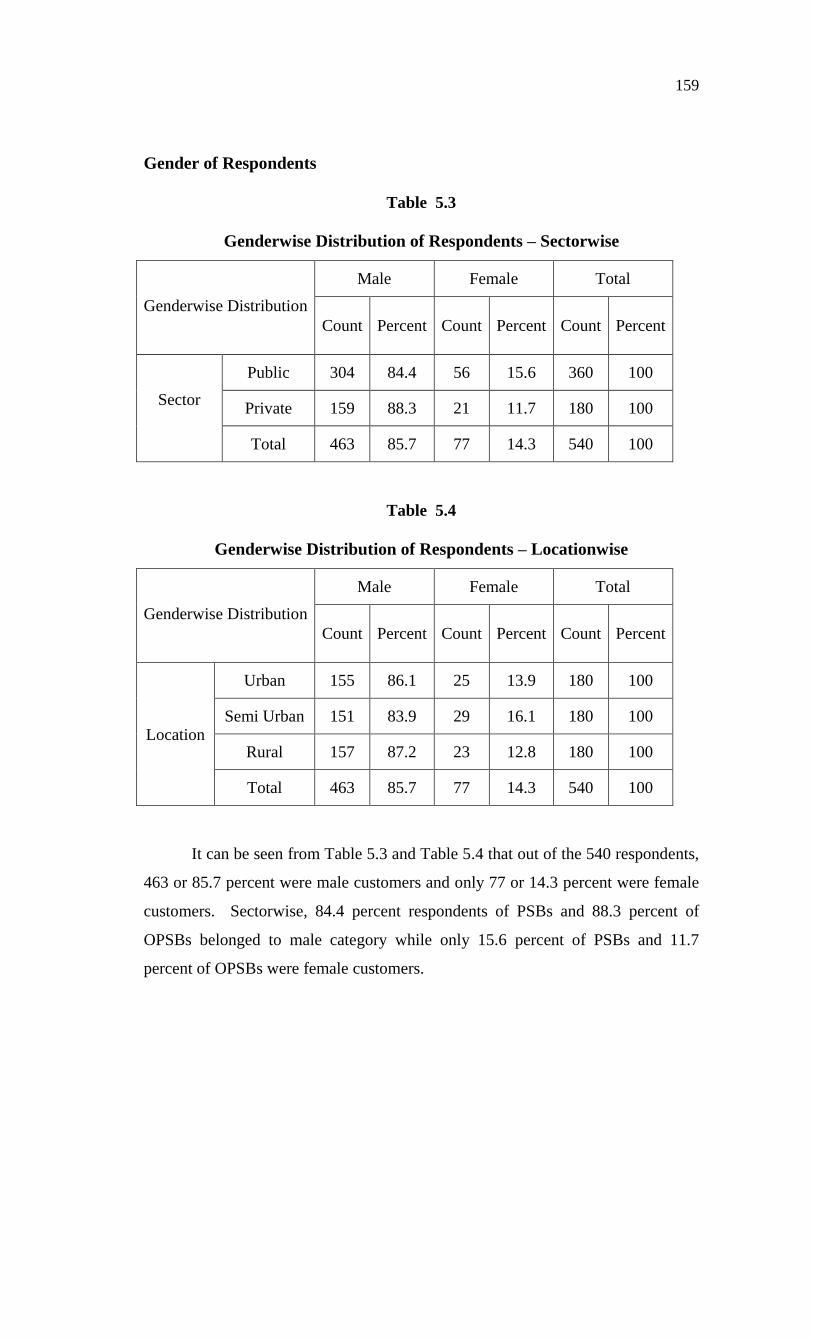

Gender of Respondents

Table 5.3

Genderwise Distribution of Respondents – Sectorwise

Genderwise Distribution

Male Female Total

Count

Percent

Count

Percent

Count

Percent

Sector

Public 304 84.4 56 15.6 360 100

Private 159 88.3 21 11.7 180 100

Total 463 85.7 77 14.3 540 100

Table 5.4

Genderwise Distribution of Respondents – Locationwise

Genderwise Distribution

Male Female Total

Count

Percent

Count

Percent

Count

Percent

Location

Urban 155 86.1 25 13.9 180 100

Semi Urban 151 83.9 29 16.1 180 100

Rural 157 87.2 23 12.8 180 100

Total 463 85.7 77 14.3 540 100

It can be seen from Table 5.3 and Table 5.4 that out of the 540 respondents,

463 or 85.7 percent were male customers and only 77 or 14.3 percent were female

customers. Sectorwise, 84.4 percent respondents of PSBs and 88.3 percent of

OPSBs belonged to male category while only 15.6 percent of PSBs and 11.7

percent of OPSBs were female customers.

160

Locationwise, almost same picture was revealed. The female customers

were 13.9 percent, 16.1 percent, and 12.8 percent, respectively, in urban, semi-

urban and rural branches. This situation indicates that though women literacy and

employment rates are high in the state, female folk is reluctant to become

customers of a bank. Interaction with officials also revealed this.

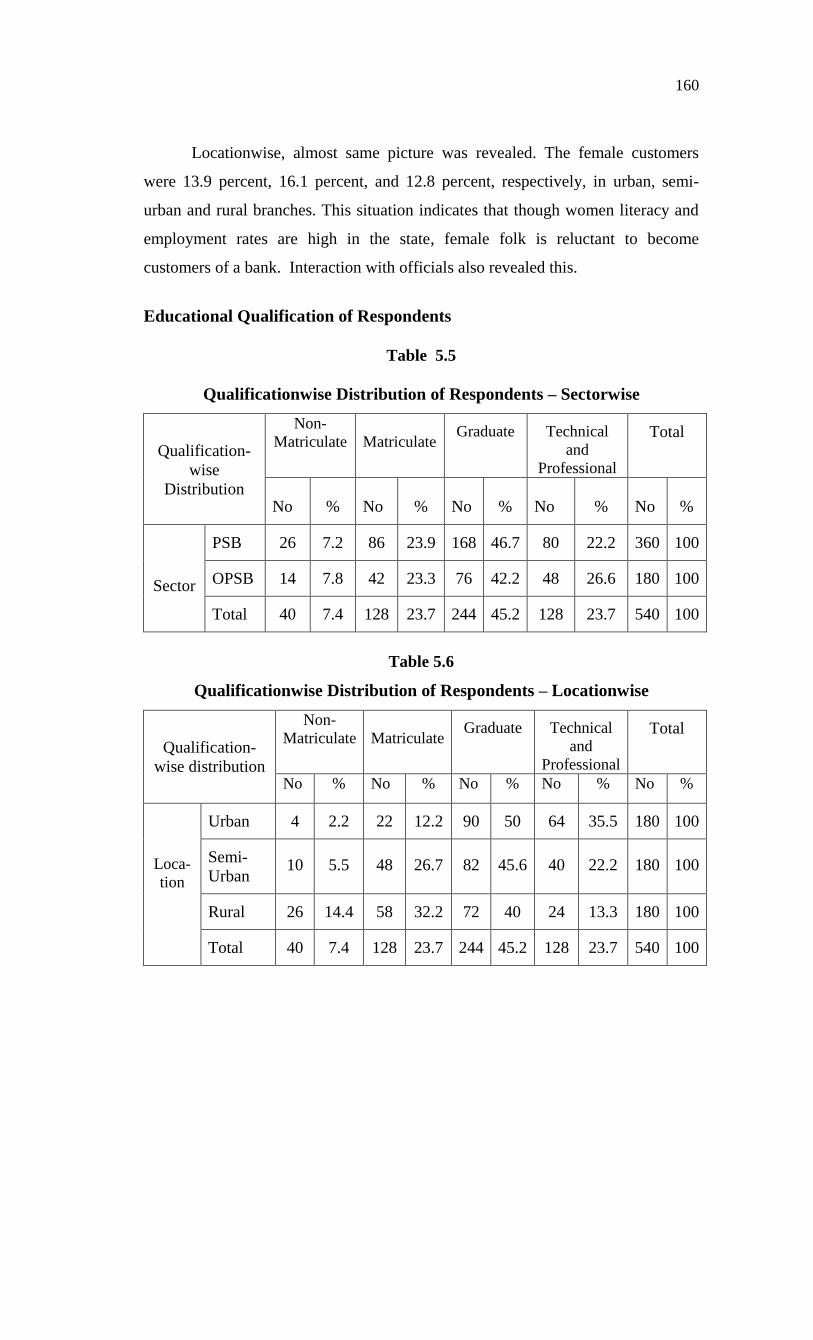

Educational Qualification of Respondents

Table 5.5

Qualificationwise Distribution of Respondents – Sectorwise

Qualification-

wise

Distribution

Non-

Matriculate

Matriculate Graduate Technical

and

Professional

Total

No

%

No

%

No

%

No

%

No

%

Sector

PSB 26 7.2 86 23.9 168 46.7 80 22.2 360 100

OPSB 14 7.8 42 23.3 76 42.2 48 26.6 180 100

Total 40 7.4 128 23.7 244 45.2 128 23.7 540 100

Table 5.6

Qualificationwise Distribution of Respondents – Locationwise

Qualification-

wise distribution

Non-

Matriculate

Matriculate Graduate Technical

and

Professional

Total

No % No % No % No % No %

Loca-

tion

Urban 4 2.2 22 12.2 90 50 64 35.5 180 100

Semi-

Urban 10 5.5 48 26.7 82 45.6 40 22.2 180 100

Rural 26 14.4 58 32.2 72 40 24 13.3 180 100

Total 40 7.4 128 23.7 244 45.2 128 23.7 540 100

161

Table 5.5 and Table 5.6 reveal that of the sample 7.4 percent respondents

were non-matriculates, 23.7 percent were matriculates, 45.2 percent were

graduates, and 23.7 percent were professionally or technically qualified.

In sectorwise analysis, the percentage of graduates of PSBs was 46.7

percent while that of OPSBs was 42.2 percent. The percentage of technically

qualified and professionally qualified persons in OPSBs was higher than in PSBs.

While considering the literacy level in Kerala, it can be assumed that participation

of non-matriculate population in commercial banking is not up to the expected

level.

In locationwise analysis, in urban branches graduates were 50 percent,

matriculates were 12.2 percent, and technically and professionally qualified were

35.5 percent of the respondents. The respective rates in semi-urban branches were

45.6 percent, 26.7 percent and 22.2 percent, and in rural branches these were 40

percent, 32.2 percent and 13.3 percent. The non-matriculates were higher (14.4

percent) in rural branches.

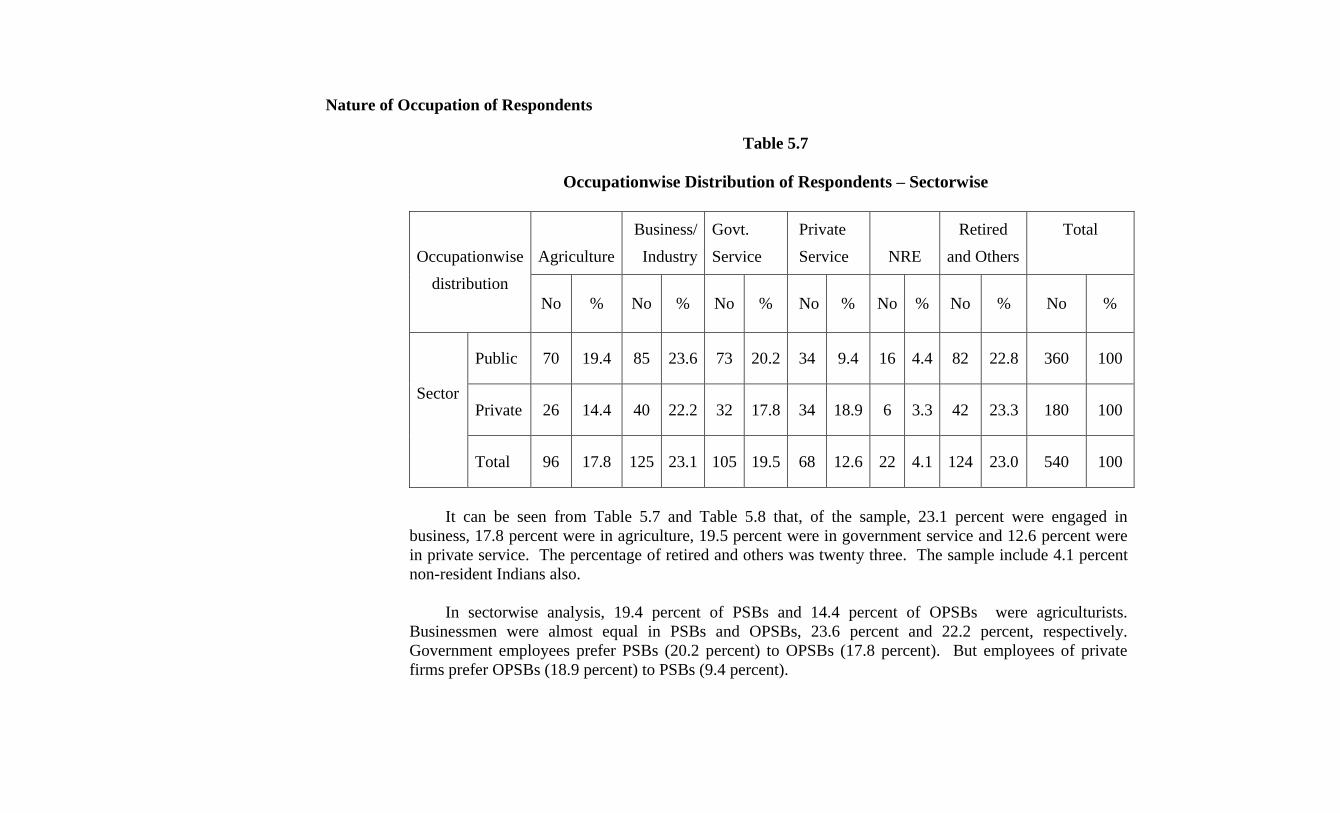

Nature of Occupation of Respondents

Table 5.7

Occupationwise Distribution of Respondents – Sectorwise

Occupationwise

distribution

Agriculture

Business/

Industry

Govt.

Service

Private

Service

NRE

Retired

and Others

Total

No

%

No

%

No

%

No

%

No

%

No

%

No

%

Sector

Public 70 19.4 85 23.6 73 20.2 34 9.4 16 4.4 82 22.8 360 100

Private 26 14.4 40 22.2 32 17.8 34 18.9 6 3.3 42 23.3 180 100

Total 96 17.8 125 23.1 105 19.5 68 12.6 22 4.1 124 23.0 540 100

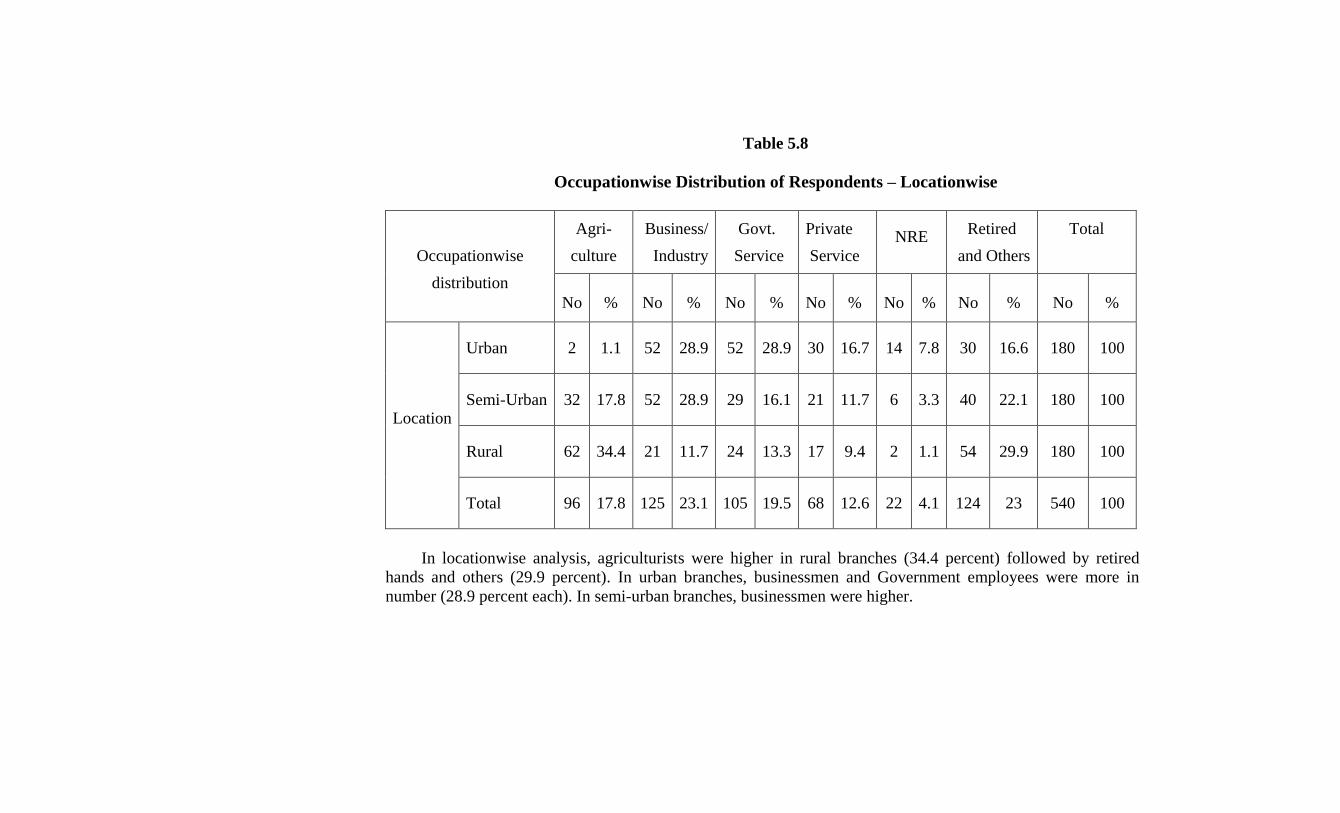

It can be seen from Table 5.7 and Table 5.8 that, of the sample, 23.1 percent were engaged in

business, 17.8 percent were in agriculture, 19.5 percent were in government service and 12.6 percent were

in private service. The percentage of retired and others was twenty three. The sample include 4.1 percent

non-resident Indians also.

In sectorwise analysis, 19.4 percent of PSBs and 14.4 percent of OPSBs were agriculturists.

Businessmen were almost equal in PSBs and OPSBs, 23.6 percent and 22.2 percent, respectively.

Government employees prefer PSBs (20.2 percent) to OPSBs (17.8 percent). But employees of private

firms prefer OPSBs (18.9 percent) to PSBs (9.4 percent).

Table 5.8

Occupationwise Distribution of Respondents – Locationwise

Occupationwise

distribution

Agri-

culture

Business/

Industry

Govt.

Service

Private

Service

NRE Retired

and Others

Total

No

%

No

%

No

%

No

%

No

%

No

%

No

%

Location

Urban 2 1.1 52 28.9 52 28.9 30 16.7 14 7.8 30 16.6 180 100

Semi-Urban 32 17.8 52 28.9 29 16.1 21 11.7 6 3.3 40 22.1 180 100

Rural 62 34.4 21 11.7 24 13.3 17 9.4 2 1.1 54 29.9 180 100

Total 96 17.8 125 23.1 105 19.5 68 12.6 22 4.1 124 23 540 100

In locationwise analysis, agriculturists were higher in rural branches (34.4 percent) followed by retired

hands and others (29.9 percent). In urban branches, businessmen and Government employees were more in

number (28.9 percent each). In semi-urban branches, businessmen were higher.

164

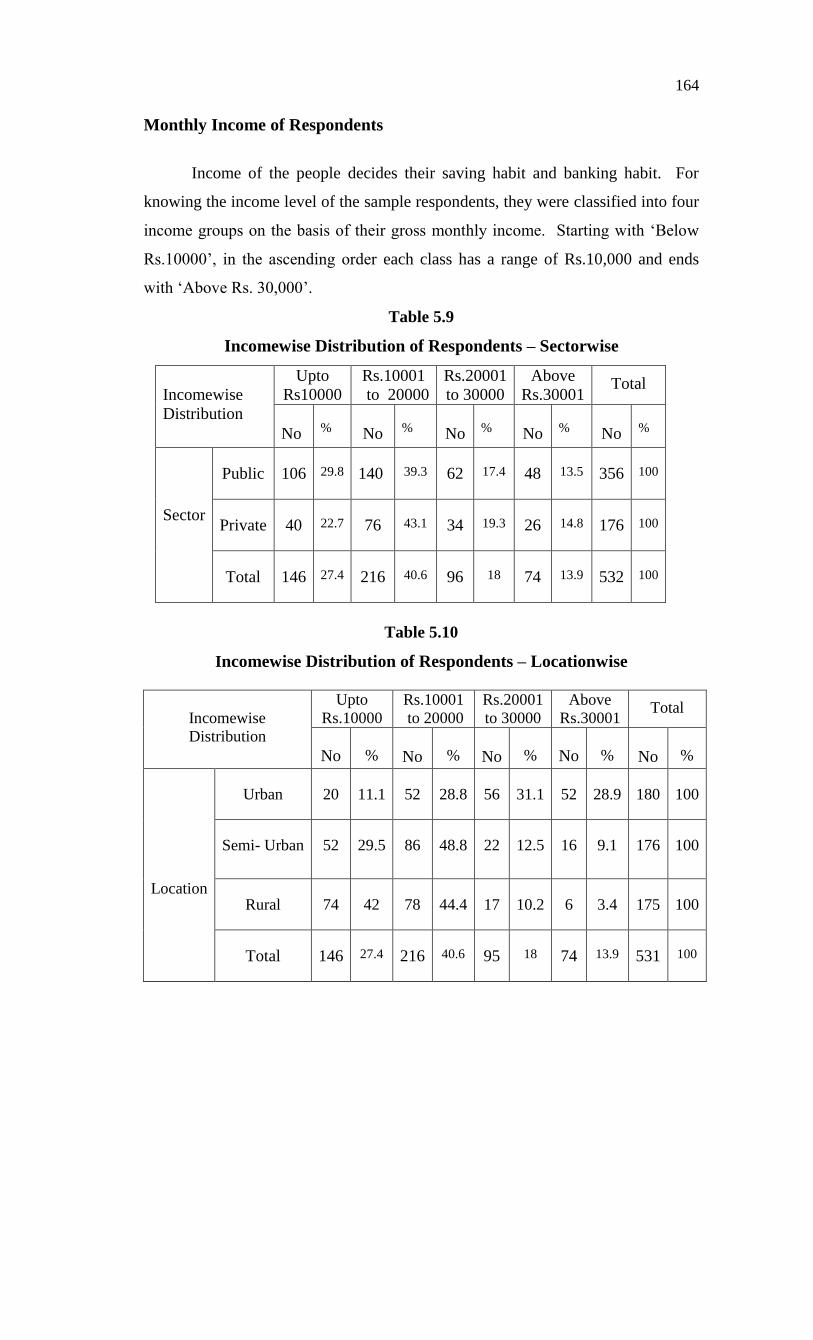

Monthly Income of Respondents

Income of the people decides their saving habit and banking habit. For

knowing the income level of the sample respondents, they were classified into four

income groups on the basis of their gross monthly income. Starting with ‘Below

Rs.10000’, in the ascending order each class has a range of Rs.10,000 and ends

with ‘Above Rs. 30,000’.

Table 5.9

Incomewise Distribution of Respondents – Sectorwise

Incomewise

Distribution

Upto

Rs10000

Rs.10001

to 20000

Rs.20001

to 30000

Above

Rs.30001 Total

No

%

No

%

No

%

No

%

No

%

Sector

Public 106 29.8 140 39.3 62 17.4 48 13.5 356 100

Private 40 22.7 76 43.1 34 19.3 26 14.8 176 100

Total 146 27.4 216 40.6 96 18 74 13.9 532 100

Table 5.10

Incomewise Distribution of Respondents – Locationwise

Incomewise

Distribution

Upto

Rs.10000

Rs.10001

to 20000

Rs.20001

to 30000

Above

Rs.30001 Total

No

%

No

%

No

%

No

%

No

%

Location

Urban 20 11.1 52 28.8 56 31.1 52 28.9 180 100

Semi- Urban 52 29.5 86 48.8 22 12.5 16 9.1 176 100

Rural 74 42 78 44.4 17 10.2 6 3.4 175 100

Total 146 27.4 216 40.6 95 18 74 13.9 531 100

165

Above given Tables 5.9 and 5.10 reveal that out of the sample respondents,

146 (27.4 percent) earned a gross monthly income less than Rs.10,000. While 216

(40.6 percent) belonged to Rs.10,001–20,000 income group, 96 (18 percent)

belonged to Rs.20,001–30,000 income group and the remaining 74 (13.9 percent)

respondents belonged to the above Rs.30,000 category.

In sectorwise analysis, 29.8 percent respondents of PSBs belonged to

‘Below Rs. 10,000’ category and that of OPSBs was 22.7 percent. Further, 39.3

percent respondents of PSBs and 43.1 percent of OPSBs belonged to the income

group Rs.10001–20,000. In the ‘Above Rs. 30,000’ category, 13.5 percent

respondents of PSBs and 14.8 percent of OPSBs were included.

In locationwise analysis, 42 percent of the rural respondents and 29.5

percent of the semi-urban respondents belonged to the income category ‘Below

Rs.10,000’, while only 11.1 percent of urban respondents belonged to this

category. In Rs.10001–20,000 income group, 44.4 percent of rural respondents,

48.8 percent of semi-urban respondents, and 28.8 percent urban respondents were

included. Among the urban customers, 31.1 percent belonged to the Rs.20001-

30000 category and 28.9 percent to above Rs.30001 category.

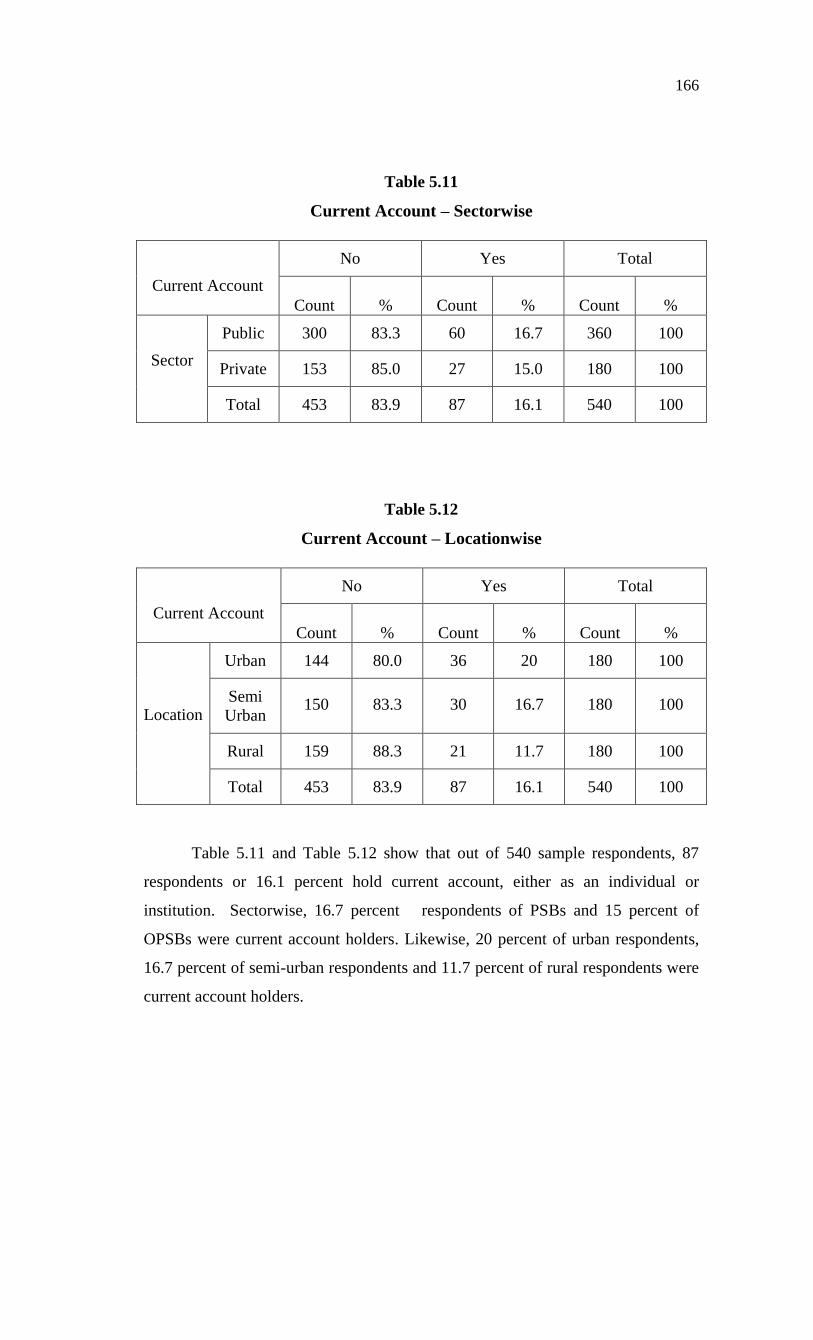

Type of Account of Respondents

The type of account of a customer decides his relationship with the banker.

A customer has either a deposit account or a loan account and sometime both

accounts, simultaneously, with the same banker. A non-resident Indian holds a

Non-Resident External (NRE) Account with a banker. Usually a current account is

operated by a business man or an institution and savings bank account and fixed

deposit account by ordinary people/fixed income earning people. A loan account

may be operated by both.

166

Table 5.11

Current Account – Sectorwise

Current Account

No Yes Total

Count

%

Count

%

Count

%

Sector

Public 300 83.3 60 16.7 360 100

Private 153 85.0 27 15.0 180 100

Total 453 83.9 87 16.1 540 100

Table 5.12

Current Account – Locationwise

Current Account

No Yes Total

Count

%

Count

%

Count

%

Location

Urban 144 80.0 36 20 180 100

Semi

Urban 150 83.3 30 16.7 180 100

Rural 159 88.3 21 11.7 180 100

Total 453 83.9 87 16.1 540 100

Table 5.11 and Table 5.12 show that out of 540 sample respondents, 87

respondents or 16.1 percent hold current account, either as an individual or

institution. Sectorwise, 16.7 percent respondents of PSBs and 15 percent of

OPSBs were current account holders. Likewise, 20 percent of urban respondents,

16.7 percent of semi-urban respondents and 11.7 percent of rural respondents were

current account holders.

167

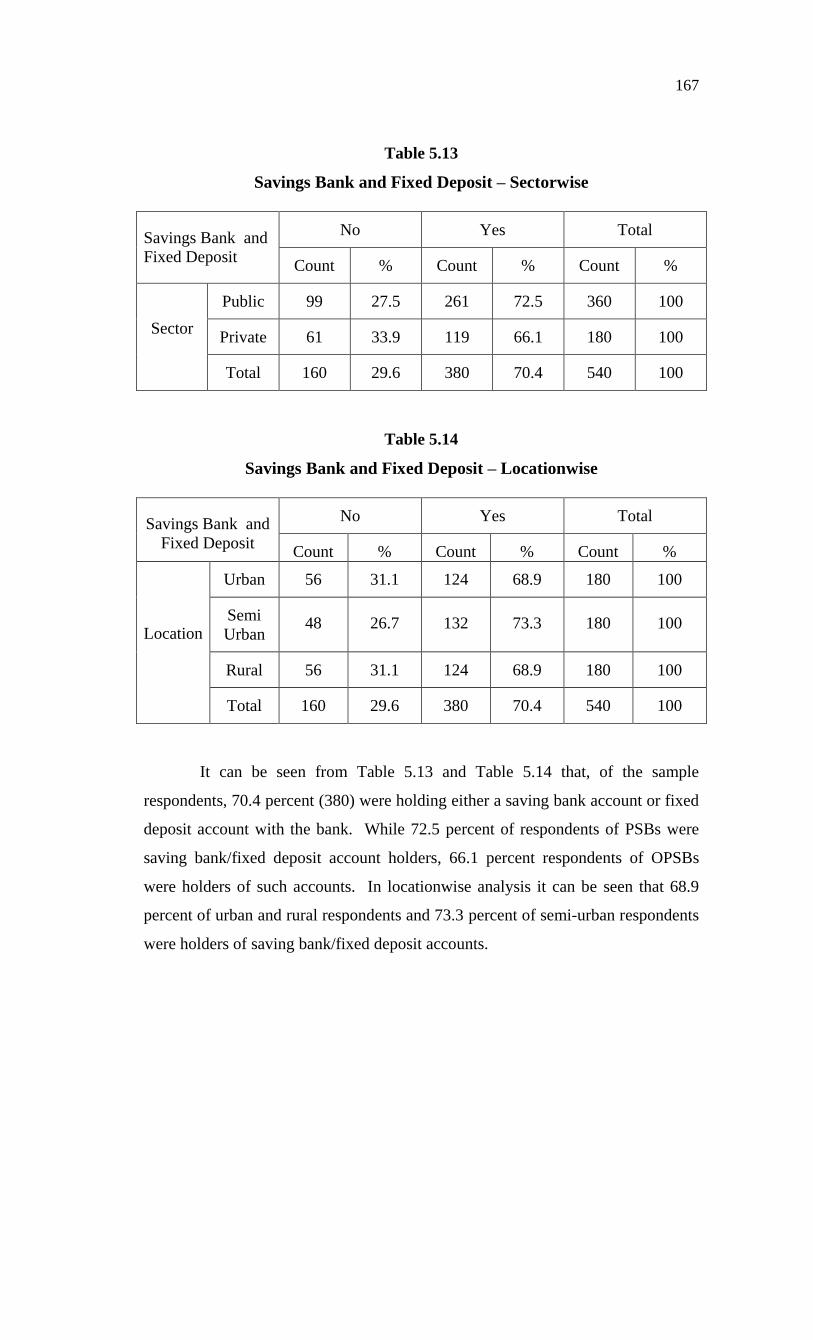

Table 5.13

Savings Bank and Fixed Deposit – Sectorwise

Savings Bank and

Fixed Deposit

No Yes Total

Count % Count % Count %

Sector

Public 99 27.5 261 72.5 360 100

Private 61 33.9 119 66.1 180 100

Total 160 29.6 380 70.4 540 100

Table 5.14

Savings Bank and Fixed Deposit – Locationwise

Savings Bank and

Fixed Deposit

No Yes Total

Count % Count % Count %

Location

Urban 56 31.1 124 68.9 180 100

Semi

Urban 48 26.7 132 73.3 180 100

Rural 56 31.1 124 68.9 180 100

Total 160 29.6 380 70.4 540 100

It can be seen from Table 5.13 and Table 5.14 that, of the sample

respondents, 70.4 percent (380) were holding either a saving bank account or fixed

deposit account with the bank. While 72.5 percent of respondents of PSBs were

saving bank/fixed deposit account holders, 66.1 percent respondents of OPSBs

were holders of such accounts. In locationwise analysis it can be seen that 68.9

percent of urban and rural respondents and 73.3 percent of semi-urban respondents

were holders of saving bank/fixed deposit accounts.

168

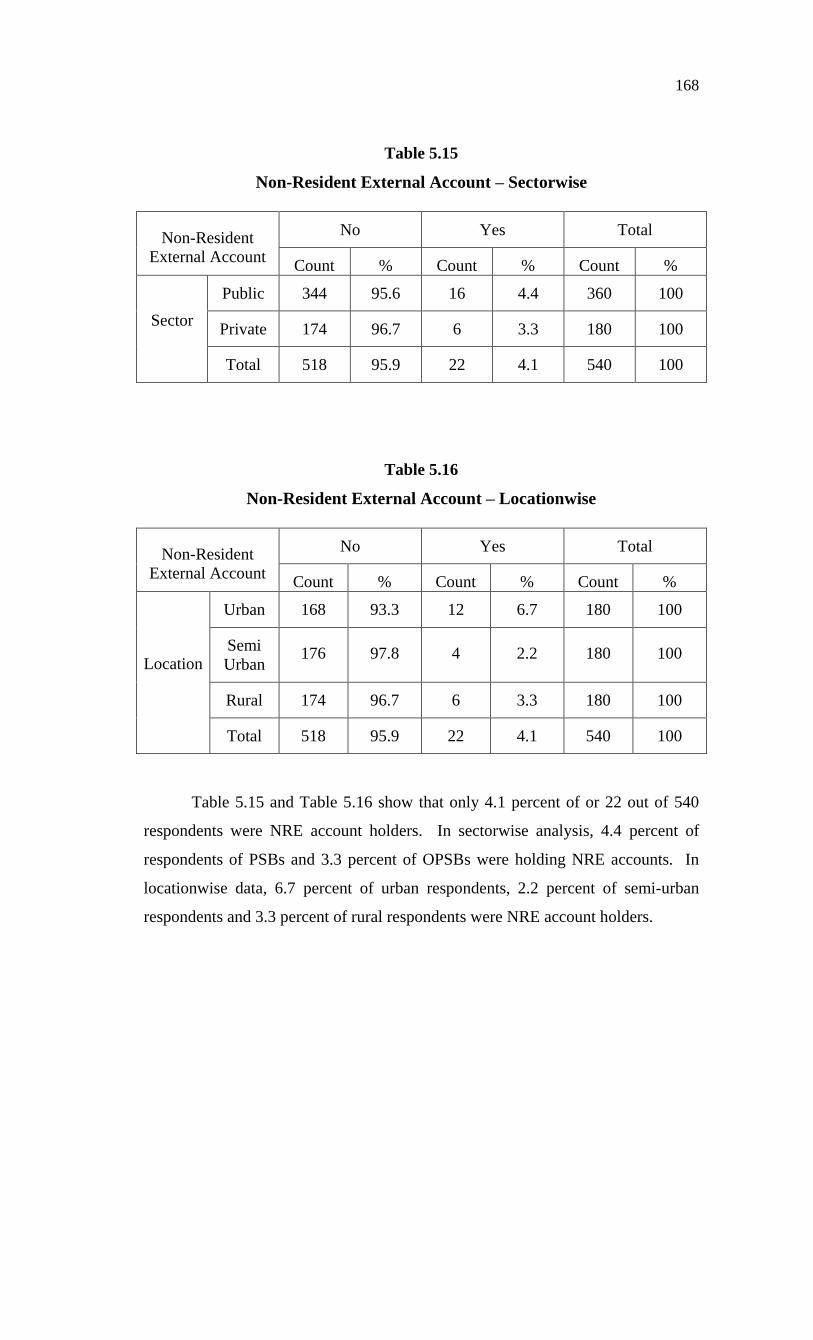

Table 5.15

Non-Resident External Account – Sectorwise

Non-Resident

External Account

No Yes Total

Count % Count % Count %

Sector

Public 344 95.6 16 4.4 360 100

Private 174 96.7 6 3.3 180 100

Total 518 95.9 22 4.1 540 100

Table 5.16

Non-Resident External Account – Locationwise

Non-Resident

External Account

No Yes Total

Count % Count % Count %

Location

Urban 168 93.3 12 6.7 180 100

Semi

Urban 176 97.8 4 2.2 180 100

Rural 174 96.7 6 3.3 180 100

Total 518 95.9 22 4.1 540 100

Table 5.15 and Table 5.16 show that only 4.1 percent of or 22 out of 540

respondents were NRE account holders. In sectorwise analysis, 4.4 percent of

respondents of PSBs and 3.3 percent of OPSBs were holding NRE accounts. In

locationwise data, 6.7 percent of urban respondents, 2.2 percent of semi-urban

respondents and 3.3 percent of rural respondents were NRE account holders.

169

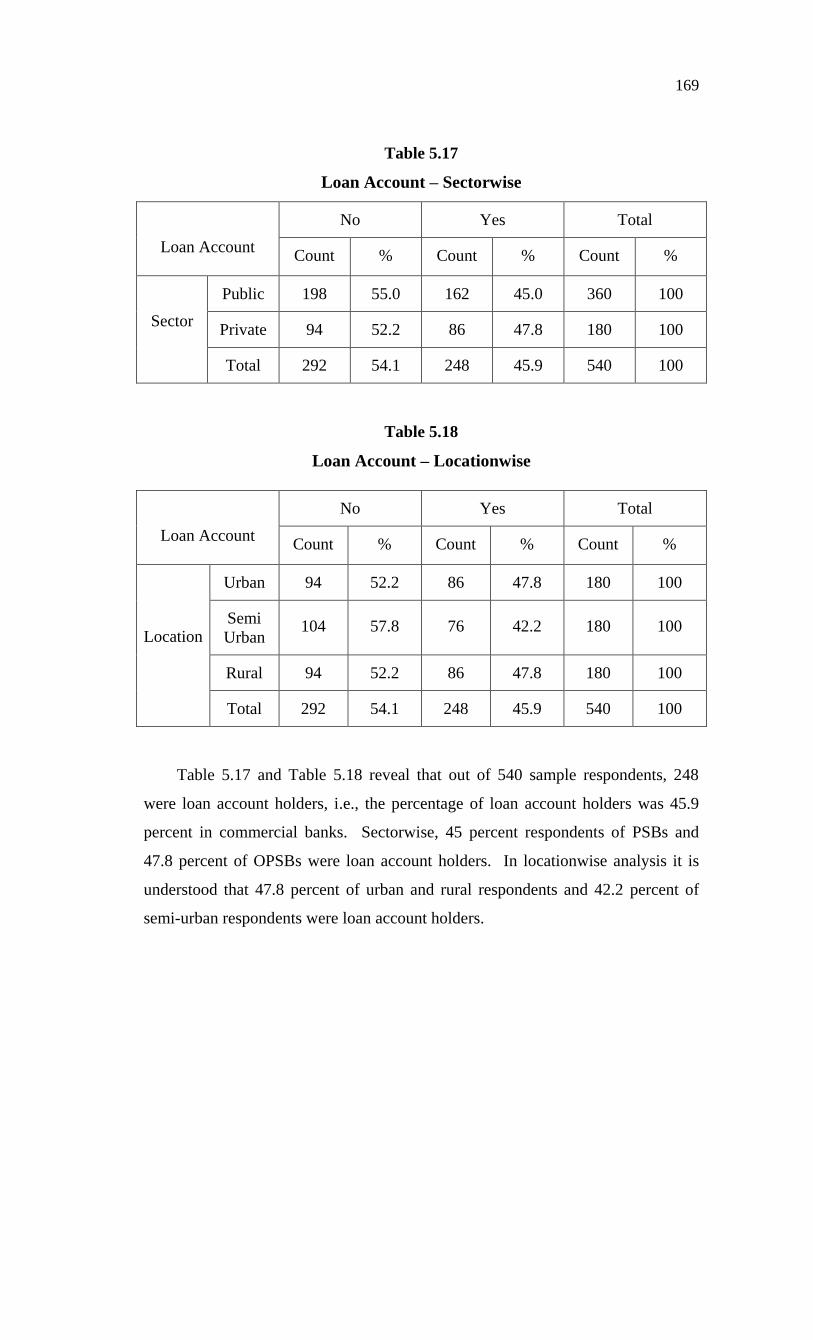

Table 5.17

Loan Account – Sectorwise

Loan Account

No Yes Total

Count % Count % Count %

Sector

Public 198 55.0 162 45.0 360 100

Private 94 52.2 86 47.8 180 100

Total 292 54.1 248 45.9 540 100

Table 5.18

Loan Account – Locationwise

Loan Account

No Yes Total

Count % Count % Count %

Location

Urban 94 52.2 86 47.8 180 100

Semi

Urban 104 57.8 76 42.2 180 100

Rural 94 52.2 86 47.8 180 100

Total 292 54.1 248 45.9 540 100

Table 5.17 and Table 5.18 reveal that out of 540 sample respondents, 248

were loan account holders, i.e., the percentage of loan account holders was 45.9

percent in commercial banks. Sectorwise, 45 percent respondents of PSBs and

47.8 percent of OPSBs were loan account holders. In locationwise analysis it is

understood that 47.8 percent of urban and rural respondents and 42.2 percent of

semi-urban respondents were loan account holders.

170

Opinion of Customers on Marketing Strategy

Awareness on New Marketing Strategies during Liberalisation Period

Commercial banks have been given the freedom to compete with each other

and with other financial agencies during the post liberalisation period. Naturally

they have been compelled to apply new marketing strategies during this period. To

check the awareness of customers regarding new marketing strategies, an enquiry

was made among them.

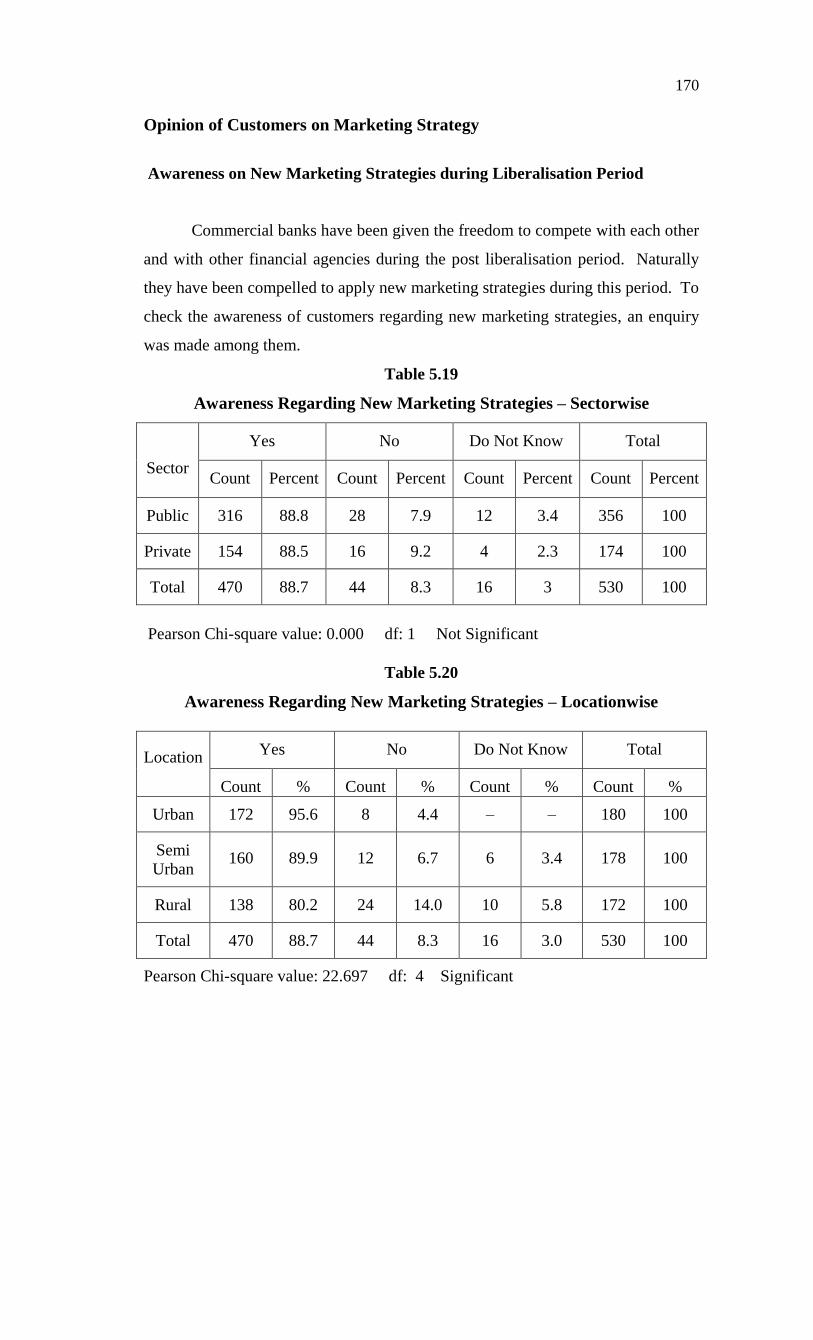

Table 5.19

Awareness Regarding New Marketing Strategies – Sectorwise

Sector

Yes No Do Not Know Total

Count Percent Count Percent Count Percent Count Percent

Public 316 88.8 28 7.9 12 3.4 356 100

Private 154 88.5 16 9.2 4 2.3 174 100

Total 470 88.7 44 8.3 16 3 530 100

Pearson Chi-square value: 0.000 df: 1 Not Significant

Table 5.20

Awareness Regarding New Marketing Strategies – Locationwise

Location Yes No Do Not Know Total

Count % Count % Count % Count %

Urban 172 95.6 8 4.4 – – 180 100

Semi

Urban 160 89.9 12 6.7 6 3.4 178 100

Rural 138 80.2 24 14.0 10 5.8 172 100

Total 470 88.7 44 8.3 16 3.0 530 100

Pearson Chi-square value: 22.697 df: 4 Significant

171

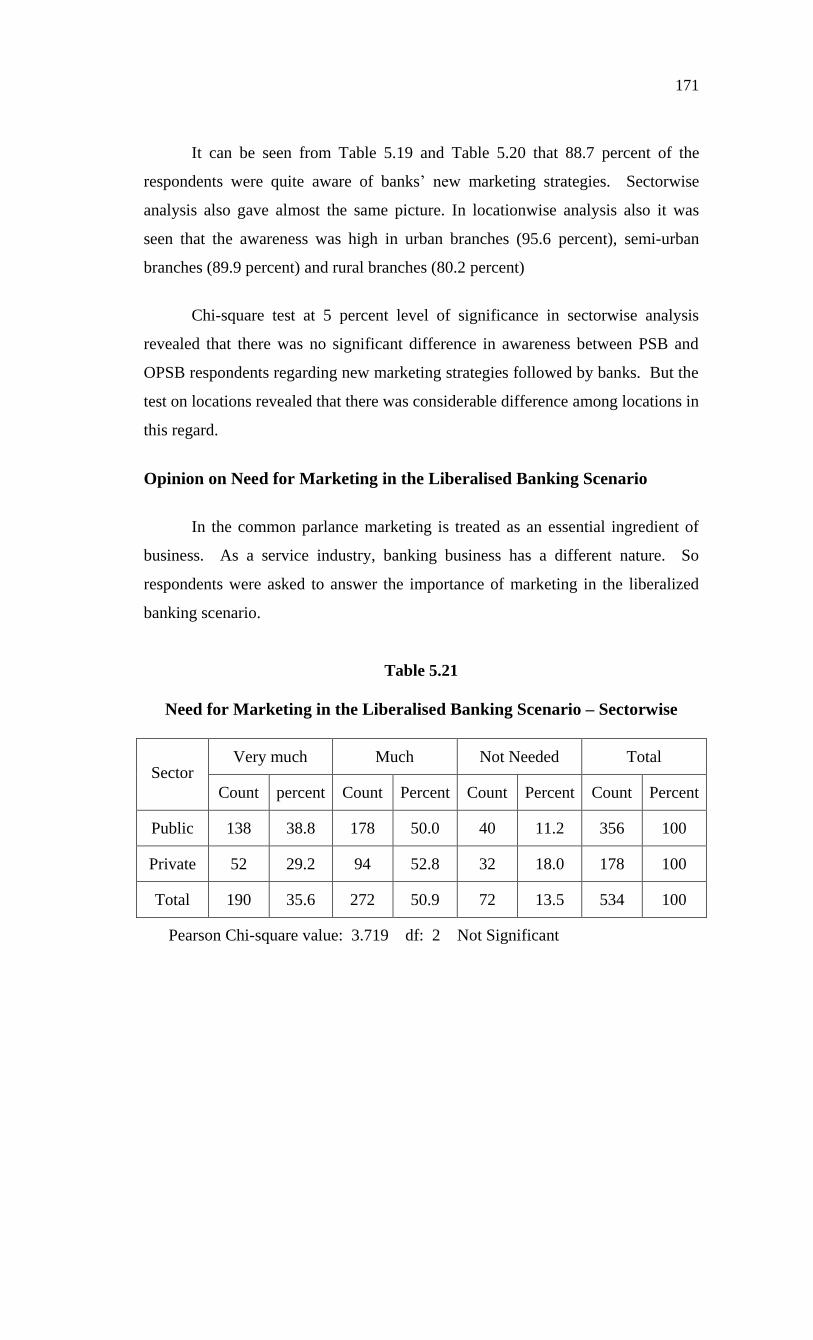

It can be seen from Table 5.19 and Table 5.20 that 88.7 percent of the

respondents were quite aware of banks’ new marketing strategies. Sectorwise

analysis also gave almost the same picture. In locationwise analysis also it was

seen that the awareness was high in urban branches (95.6 percent), semi-urban

branches (89.9 percent) and rural branches (80.2 percent)

Chi-square test at 5 percent level of significance in sectorwise analysis

revealed that there was no significant difference in awareness between PSB and

OPSB respondents regarding new marketing strategies followed by banks. But the

test on locations revealed that there was considerable difference among locations in

this regard.

Opinion on Need for Marketing in the Liberalised Banking Scenario

In the common parlance marketing is treated as an essential ingredient of

business. As a service industry, banking business has a different nature. So

respondents were asked to answer the importance of marketing in the liberalized

banking scenario.

Table 5.21

Need for Marketing in the Liberalised Banking Scenario – Sectorwise

Sector Very much Much Not Needed Total

Count percent Count Percent Count Percent Count Percent

Public 138 38.8 178 50.0 40 11.2 356 100

Private 52 29.2 94 52.8 32 18.0 178 100

Total 190 35.6 272 50.9 72 13.5 534 100

Pearson Chi-square value: 3.719 df: 2 Not Significant

172

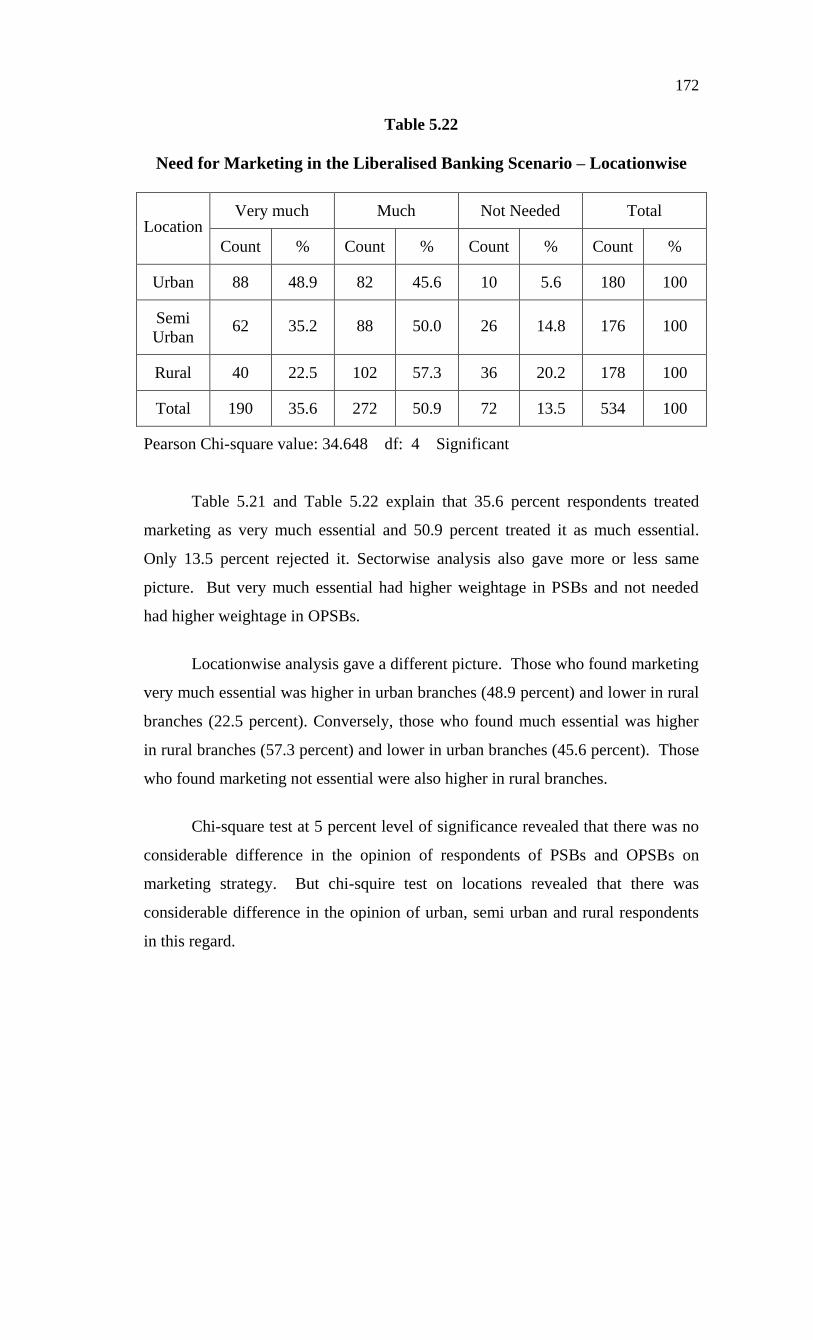

Table 5.22

Need for Marketing in the Liberalised Banking Scenario – Locationwise

Location Very much Much Not Needed Total

Count % Count % Count % Count %

Urban 88 48.9 82 45.6 10 5.6 180 100

Semi

Urban 62 35.2 88 50.0 26 14.8 176 100

Rural 40 22.5 102 57.3 36 20.2 178 100

Total 190 35.6 272 50.9 72 13.5 534 100

Pearson Chi-square value: 34.648 df: 4 Significant

Table 5.21 and Table 5.22 explain that 35.6 percent respondents treated

marketing as very much essential and 50.9 percent treated it as much essential.

Only 13.5 percent rejected it. Sectorwise analysis also gave more or less same

picture. But very much essential had higher weightage in PSBs and not needed

had higher weightage in OPSBs.

Locationwise analysis gave a different picture. Those who found marketing

very much essential was higher in urban branches (48.9 percent) and lower in rural

branches (22.5 percent). Conversely, those who found much essential was higher

in rural branches (57.3 percent) and lower in urban branches (45.6 percent). Those

who found marketing not essential were also higher in rural branches.

Chi-square test at 5 percent level of significance revealed that there was no

considerable difference in the opinion of respondents of PSBs and OPSBs on

marketing strategy. But chi-squire test on locations revealed that there was

considerable difference in the opinion of urban, semi urban and rural respondents

in this regard.

173

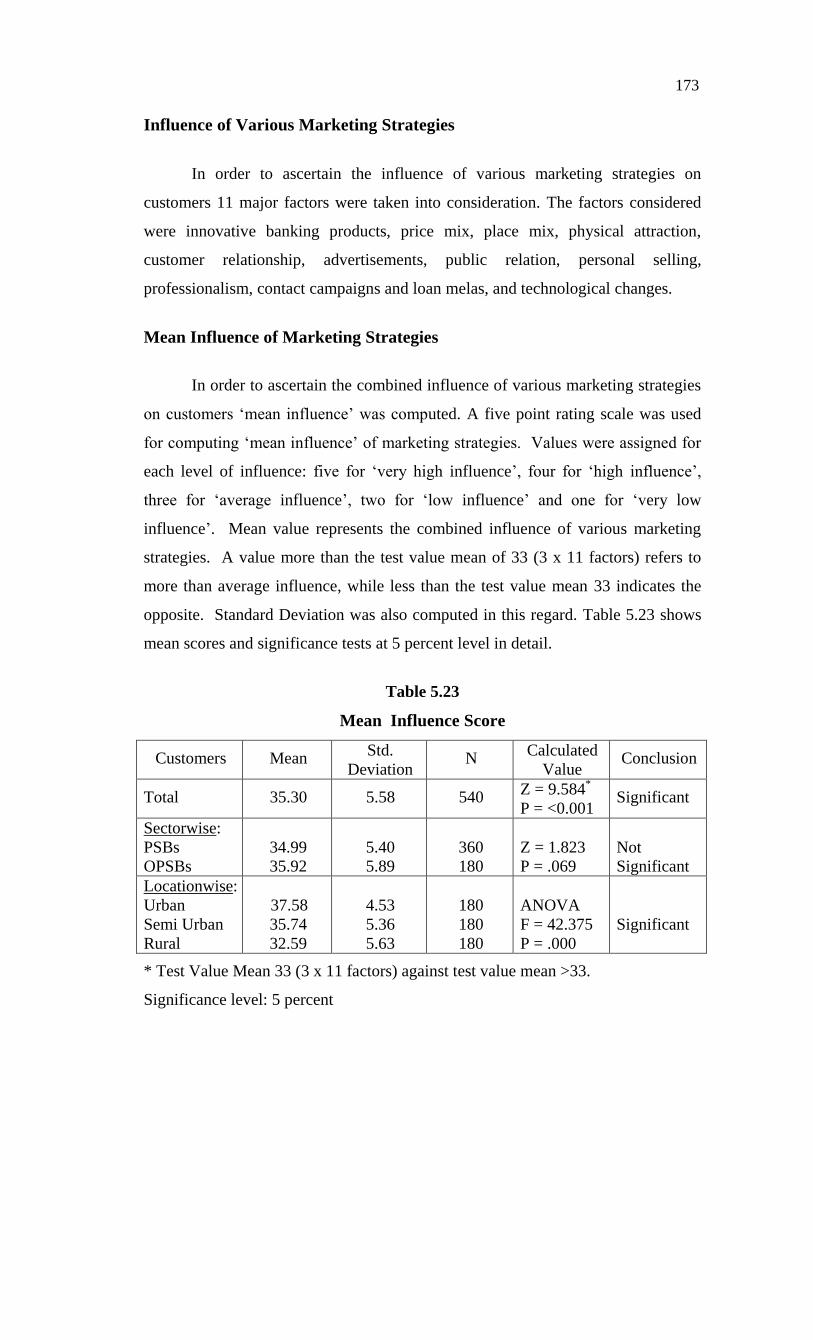

Influence of Various Marketing Strategies

In order to ascertain the influence of various marketing strategies on

customers 11 major factors were taken into consideration. The factors considered

were innovative banking products, price mix, place mix, physical attraction,

customer relationship, advertisements, public relation, personal selling,

professionalism, contact campaigns and loan melas, and technological changes.

Mean Influence of Marketing Strategies

In order to ascertain the combined influence of various marketing strategies

on customers ‘mean influence’ was computed. A five point rating scale was used

for computing ‘mean influence’ of marketing strategies. Values were assigned for

each level of influence: five for ‘very high influence’, four for ‘high influence’,

three for ‘average influence’, two for ‘low influence’ and one for ‘very low

influence’. Mean value represents the combined influence of various marketing

strategies. A value more than the test value mean of 33 (3 x 11 factors) refers to

more than average influence, while less than the test value mean 33 indicates the

opposite. Standard Deviation was also computed in this regard. Table 5.23 shows

mean scores and significance tests at 5 percent level in detail.

Table 5.23

Mean Influence Score

Customers Mean Std.

Deviation N

Calculated

Value Conclusion

Total 35.30 5.58 540 Z = 9.584*

P = <0.001 Significant

Sectorwise:

PSBs

OPSBs

34.99

35.92

5.40

5.89

360

180

Z = 1.823

P = .069

Not

Significant

Locationwise:

Urban

Semi Urban

Rural

37.58

35.74

32.59

4.53

5.36

5.63

180

180

180

ANOVA

F = 42.375

P = .000

Significant

* Test Value Mean 33 (3 x 11 factors) against test value mean >33.

Significance level: 5 percent

174

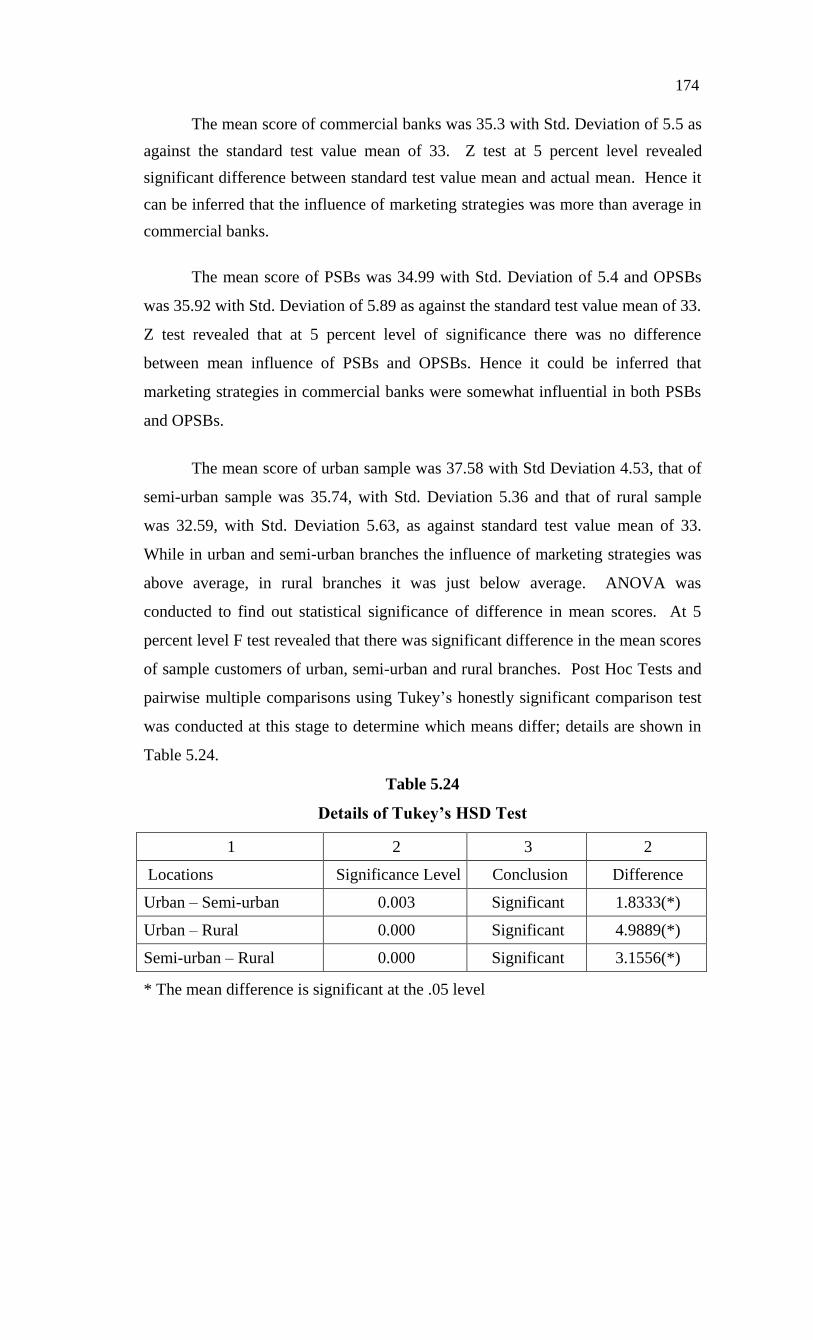

The mean score of commercial banks was 35.3 with Std. Deviation of 5.5 as

against the standard test value mean of 33. Z test at 5 percent level revealed

significant difference between standard test value mean and actual mean. Hence it

can be inferred that the influence of marketing strategies was more than average in

commercial banks.

The mean score of PSBs was 34.99 with Std. Deviation of 5.4 and OPSBs

was 35.92 with Std. Deviation of 5.89 as against the standard test value mean of 33.

Z test revealed that at 5 percent level of significance there was no difference

between mean influence of PSBs and OPSBs. Hence it could be inferred that

marketing strategies in commercial banks were somewhat influential in both PSBs

and OPSBs.

The mean score of urban sample was 37.58 with Std Deviation 4.53, that of

semi-urban sample was 35.74, with Std. Deviation 5.36 and that of rural sample

was 32.59, with Std. Deviation 5.63, as against standard test value mean of 33.

While in urban and semi-urban branches the influence of marketing strategies was

above average, in rural branches it was just below average. ANOVA was

conducted to find out statistical significance of difference in mean scores. At 5

percent level F test revealed that there was significant difference in the mean scores

of sample customers of urban, semi-urban and rural branches. Post Hoc Tests and

pairwise multiple comparisons using Tukey’s honestly significant comparison test

was conducted at this stage to determine which means differ; details are shown in

Table 5.24.

Table 5.24

Details of Tukey’s HSD Test

1 2 3 2

Locations Significance Level Conclusion Difference

Urban – Semi-urban 0.003 Significant 1.8333(*)

Urban – Rural 0.000 Significant 4.9889(*)

Semi-urban – Rural 0.000 Significant 3.1556(*)

* The mean difference is significant at the .05 level

175

Tukey test also revealed that the difference in mean between urban and

semi-urban, urban and rural and semi-urban and rural branches were statistically

significant at the .05 level. Hence it can be inferred that the influence of marketing

strategies was significantly different in different locations.

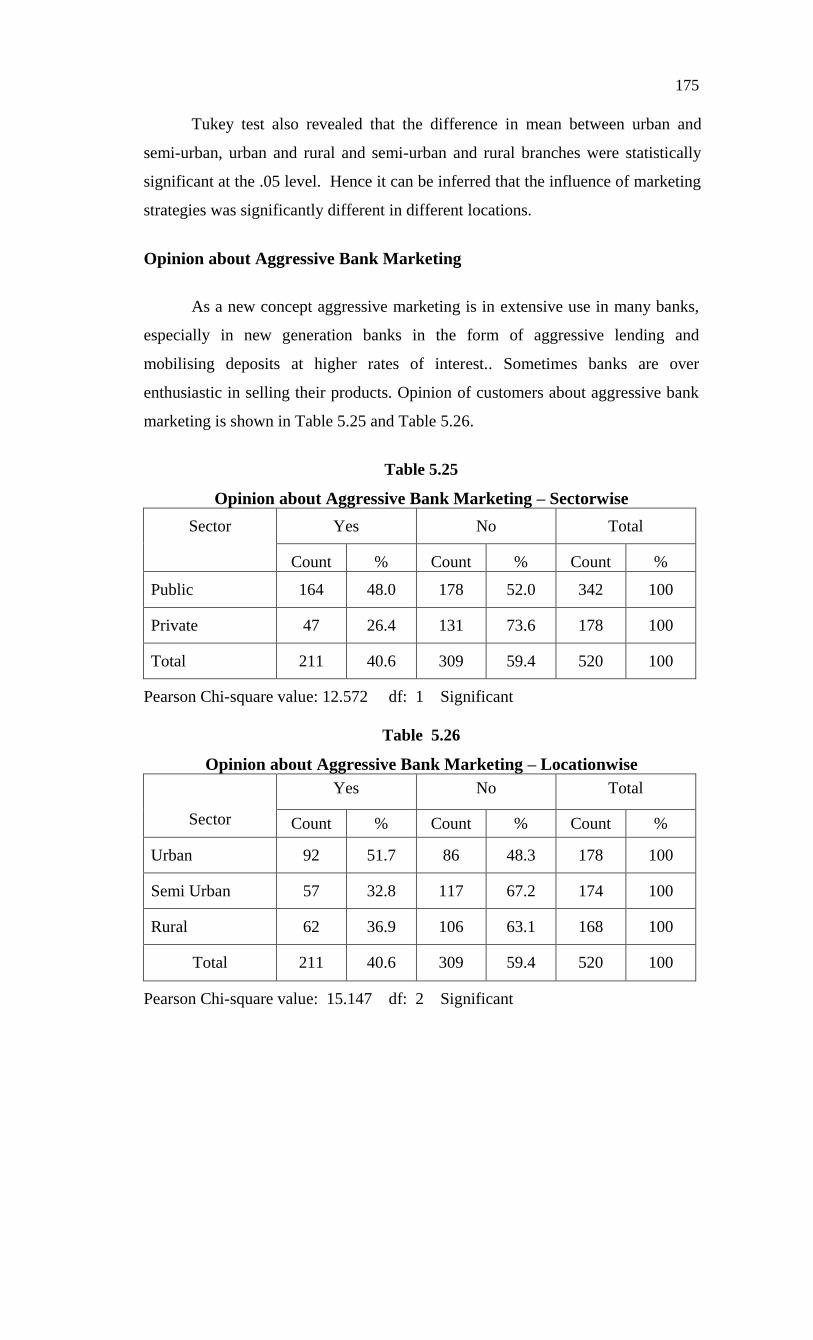

Opinion about Aggressive Bank Marketing

As a new concept aggressive marketing is in extensive use in many banks,

especially in new generation banks in the form of aggressive lending and

mobilising deposits at higher rates of interest.. Sometimes banks are over

enthusiastic in selling their products. Opinion of customers about aggressive bank

marketing is shown in Table 5.25 and Table 5.26.

Table 5.25

Opinion about Aggressive Bank Marketing – Sectorwise

Sector

Yes No Total

Count % Count % Count %

Public 164 48.0 178 52.0 342 100

Private 47 26.4 131 73.6 178 100

Total 211 40.6 309 59.4 520 100

Pearson Chi-square value: 12.572 df: 1 Significant

Table 5.26

Opinion about Aggressive Bank Marketing – Locationwise

Sector

Yes No Total

Count % Count % Count %

Urban 92 51.7 86 48.3 178 100

Semi Urban 57 32.8 117 67.2 174 100

Rural 62 36.9 106 63.1 168 100

Total 211 40.6 309 59.4 520 100

Pearson Chi-square value: 15.147 df: 2 Significant

176

Of the sample, 40.6 percent favoured aggressive bank marketing while 59.4

percent opposed it. Sectorwise analysis also showed a picture that majority were

against aggressive marketing in banking. While 52 percent in PSBs opposed it, a

higher percentage i.e., 73.6 percent, in OPSBs opposed it.

In locationwise analysis almost majority (51.7 percent) in urban branches

favoured it. But majority in semi-urban branches (67.2 percent) and rural branches

(63.1 percent) opposed it. Many of them treated aggressive bank marketing of

New Generation Banks as encroachment into their freedom. So they oppose its

application in old commercial banks. Instead of aggressive marketing customers

expect proper and timely services and relationship marketing.

Chi-square test of independence at 5 percent level of significance revealed

that there was considerable difference in opinion in between respondents of PSBs

and OPSBs with regard to aggressive bank marketing. Chi-square test on locations

also revealed that there was considerable difference among urban, semi-urban and

rural branches with regard to it.

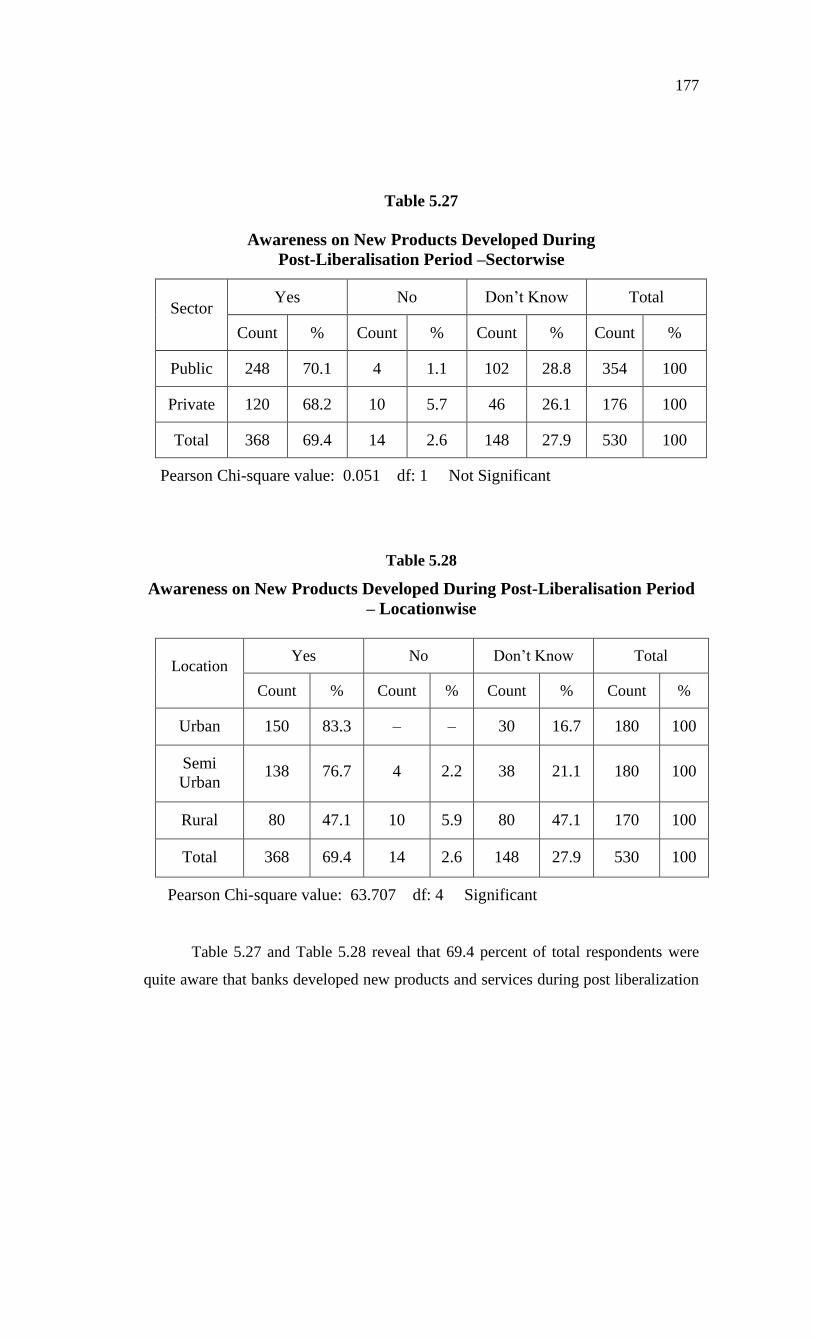

Awareness on New Products Developed During Post-Liberalisation Period

Many new products and services were developed by commercial banks for

facing competition and to attract customers during the post-liberalization period. An

enquiry was made with customers to find out their awareness level regarding new

products.

177

Table 5.27

Awareness on New Products Developed During

Post-Liberalisation Period –Sectorwise

Sector Yes No Don’t Know Total

Count % Count % Count % Count %

Public 248 70.1 4 1.1 102 28.8 354 100

Private 120 68.2 10 5.7 46 26.1 176 100

Total 368 69.4 14 2.6 148 27.9 530 100

Pearson Chi-square value: 0.051 df: 1 Not Significant

Table 5.28

Awareness on New Products Developed During Post-Liberalisation Period

– Locationwise

Location Yes No Don’t Know Total

Count % Count % Count % Count %

Urban 150 83.3 – – 30 16.7 180 100

Semi

Urban 138 76.7 4 2.2 38 21.1 180 100

Rural 80 47.1 10 5.9 80 47.1 170 100

Total 368 69.4 14 2.6 148 27.9 530 100

Pearson Chi-square value: 63.707 df: 4 Significant

Table 5.27 and Table 5.28 reveal that 69.4 percent of total respondents were

quite aware that banks developed new products and services during post liberalization

178

period. But 27.9 percent respondents were not aware about it. Sectorwise analysis

also show similar picture. In locationwise analysis it was found that the awareness of

rural respondents was quiet low (47.1 percent) and urban respondents were high (83.3

percent)

Chi-square test of independence at 5 percent level of significance revealed

that there was no considerable difference in the awareness of respondents of PSBs

and OPSBs. But chi-square test in location wise analysis revealed that the

difference was considerable among urban semi-urban, rural respondents.

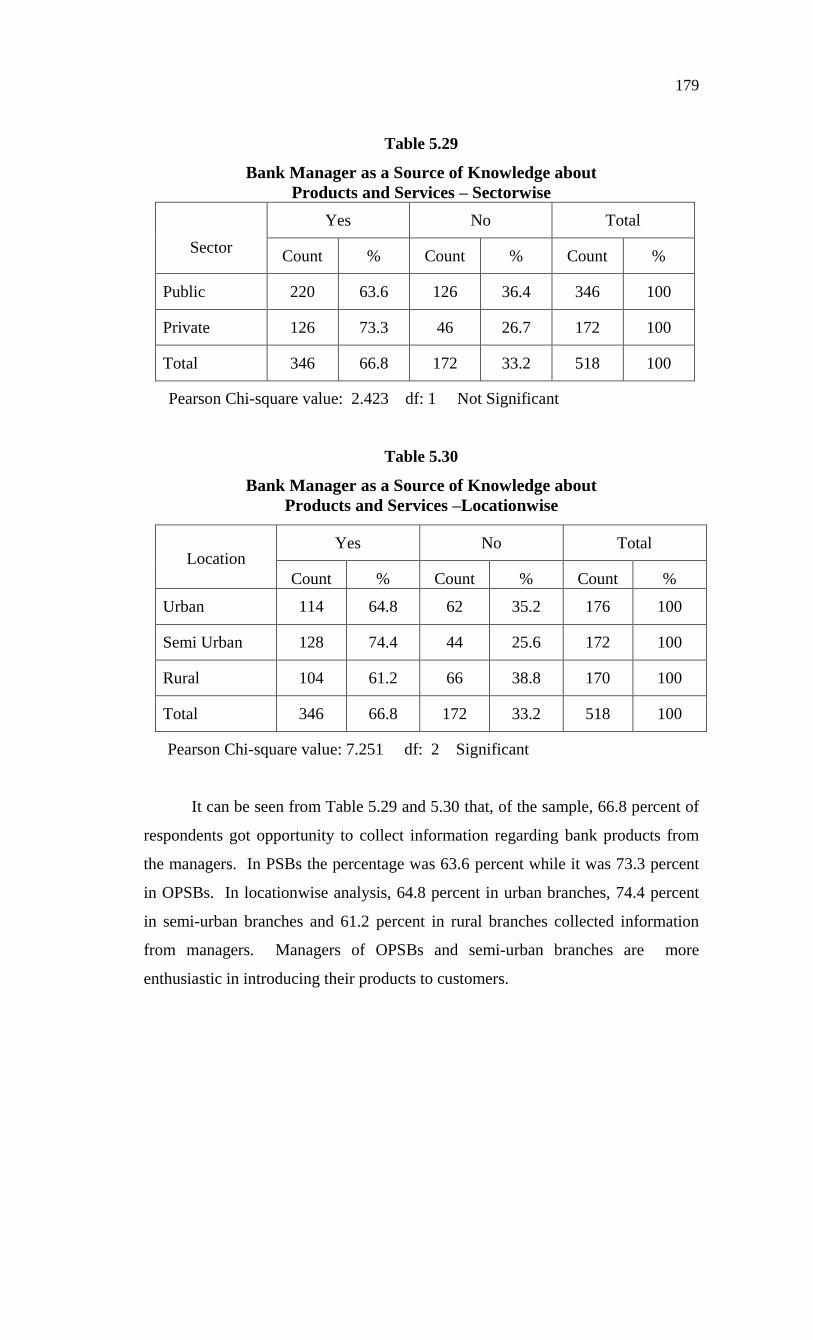

Source of Knowledge about Products and Services Offered by the Bank

Banks are selling, simultaneously, their old or conventional products and

some new products. For many customers even old products are new for them.

Sometimes old products may be reshaped and presented as new products. Anyway

these are to be presented before prospective users in a convincing way. Sometimes

customers’ own initiatives pave the way for presentation of new products before

them, especially by the bank managers and other staff. To test the source of

knowledge, an enquiry was made to respondents regarding this. Many of the

respondents got knowledge from multiple sources. These responses were analysed

case by case on a multi response basis and percentages in each case reveal

proportion of respondents who got opportunity to get knowledge from different

sources.

Bank Manager as a Source of Knowledge

In many banks there are special managers in addition to the Chief Manager

or Senior Manager, especially in urban and semi-urban branches, to deal, interact,

with customers.

179

Table 5.29

Bank Manager as a Source of Knowledge about

Products and Services – Sectorwise

Sector

Yes No Total

Count % Count % Count %

Public 220 63.6 126 36.4 346 100

Private 126 73.3 46 26.7 172 100

Total 346 66.8 172 33.2 518 100

Pearson Chi-square value: 2.423 df: 1 Not Significant

Table 5.30

Bank Manager as a Source of Knowledge about

Products and Services –Locationwise

Location Yes No Total

Count % Count % Count %

Urban 114 64.8 62 35.2 176 100

Semi Urban 128 74.4 44 25.6 172 100

Rural 104 61.2 66 38.8 170 100

Total 346 66.8 172 33.2 518 100

Pearson Chi-square value: 7.251 df: 2 Significant

It can be seen from Table 5.29 and 5.30 that, of the sample, 66.8 percent of

respondents got opportunity to collect information regarding bank products from

the managers. In PSBs the percentage was 63.6 percent while it was 73.3 percent

in OPSBs. In locationwise analysis, 64.8 percent in urban branches, 74.4 percent

in semi-urban branches and 61.2 percent in rural branches collected information

from managers. Managers of OPSBs and semi-urban branches are more

enthusiastic in introducing their products to customers.

180

Chi-square test of independence at 5 percent level of significance revealed

that there was no considerable difference between opinions of PSBs and OPSBs

with regard to manager as a source of knowledge about banking products. But chi-

square test on locations revealed that there was considerable difference in opinion

about managers of urban, semi-urban and rural branches with regard to this.

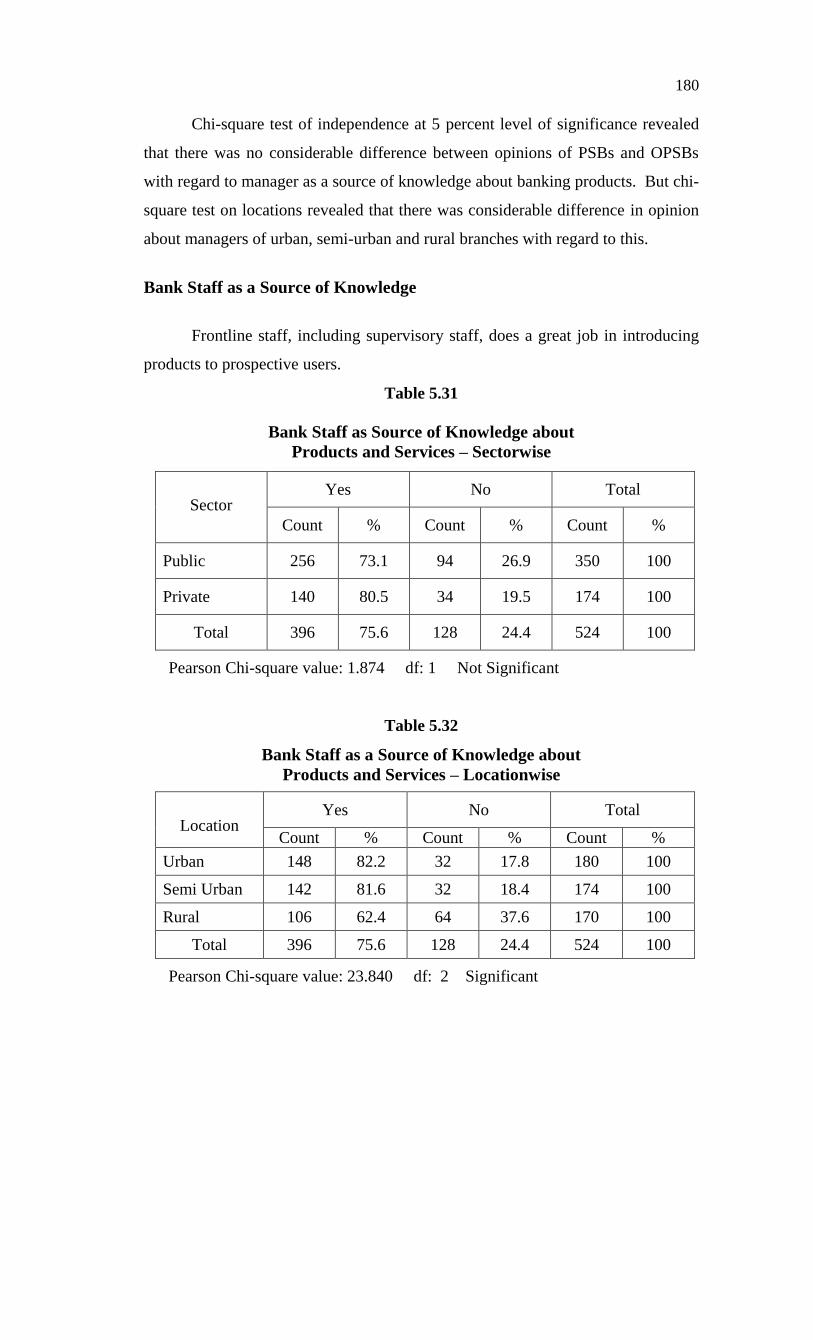

Bank Staff as a Source of Knowledge

Frontline staff, including supervisory staff, does a great job in introducing

products to prospective users.

Table 5.31

Bank Staff as Source of Knowledge about

Products and Services – Sectorwise

Sector Yes No Total

Count % Count % Count %

Public 256 73.1 94 26.9 350 100

Private 140 80.5 34 19.5 174 100

Total 396 75.6 128 24.4 524 100

Pearson Chi-square value: 1.874 df: 1 Not Significant

Table 5.32

Bank Staff as a Source of Knowledge about

Products and Services – Locationwise

Location Yes No Total

Count % Count % Count %

Urban 148 82.2 32 17.8 180 100

Semi Urban 142 81.6 32 18.4 174 100

Rural 106 62.4 64 37.6 170 100

Total 396 75.6 128 24.4 524 100

Pearson Chi-square value: 23.840 df: 2 Significant

181

Table 5.31 and 5.32 exhibit that 75.6 percent respondents got opportunity to

collect information regarding products from frontline staff, supervisory and

clerical. In PSBs 73.1 percent collected information from bank staff, while in

OPSBs 80.5 percent got this opportunity. This indicates that to some extent OPSB

staff is more active in introducing their products.

In locationwise analysis, it can be seen that 82.2 percent and 81.6 percent in

urban and semi–urban branches, respectively, got this opportunity. But only 62.4

percent in rural branches got it. The reason for this may be that sometime staff

members are not ready to explain things well to customers.

Chi-square test of independence 5 percent at level of significance revealed

that there was no considerable difference in the opinion of respondents of PSBs

and OPSBs with regard to bank staff as a source of knowledge. But in location

wise analysis, chi-square test revealed that there was significant difference among

urban, semi-urban and rural branches with regard to this.

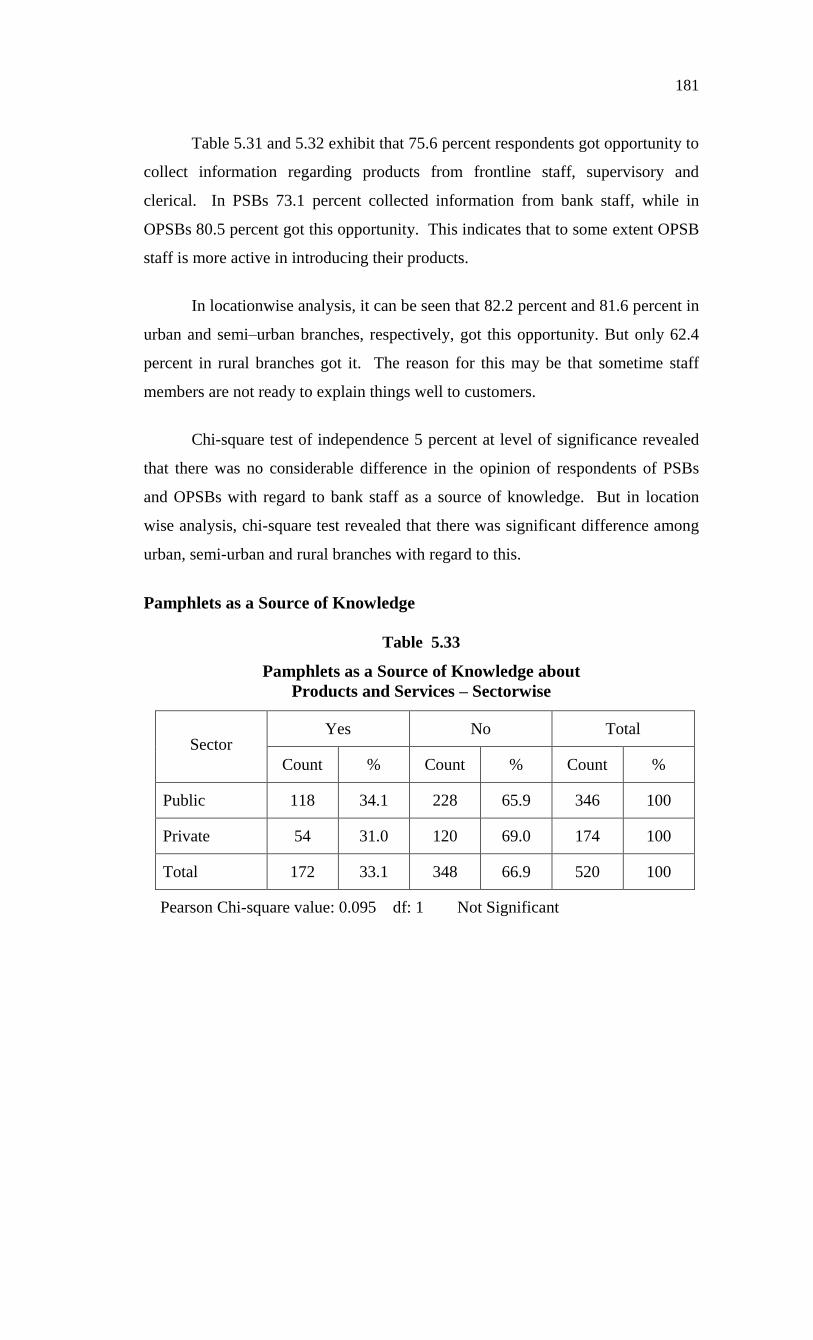

Pamphlets as a Source of Knowledge

Table 5.33

Pamphlets as a Source of Knowledge about

Products and Services – Sectorwise

Sector Yes No Total

Count % Count % Count %

Public 118 34.1 228 65.9 346 100

Private 54 31.0 120 69.0 174 100

Total 172 33.1 348 66.9 520 100

Pearson Chi-square value: 0.095 df: 1 Not Significant

182

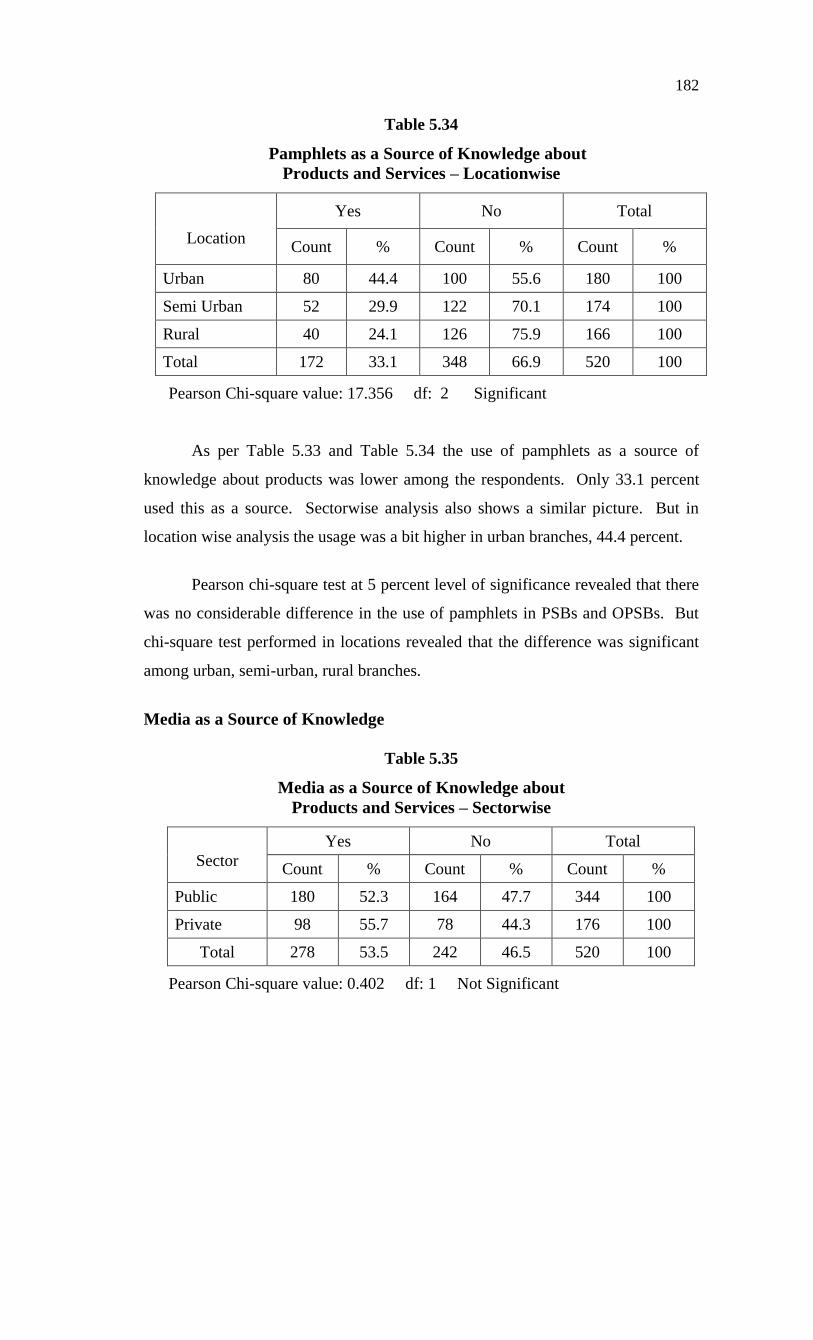

Table 5.34

Pamphlets as a Source of Knowledge about

Products and Services – Locationwise

Location

Yes No Total

Count % Count % Count %

Urban 80 44.4 100 55.6 180 100

Semi Urban 52 29.9 122 70.1 174 100

Rural 40 24.1 126 75.9 166 100

Total 172 33.1 348 66.9 520 100

Pearson Chi-square value: 17.356 df: 2 Significant

As per Table 5.33 and Table 5.34 the use of pamphlets as a source of

knowledge about products was lower among the respondents. Only 33.1 percent

used this as a source. Sectorwise analysis also shows a similar picture. But in

location wise analysis the usage was a bit higher in urban branches, 44.4 percent.

Pearson chi-square test at 5 percent level of significance revealed that there

was no considerable difference in the use of pamphlets in PSBs and OPSBs. But

chi-square test performed in locations revealed that the difference was significant

among urban, semi-urban, rural branches.

Media as a Source of Knowledge

Table 5.35

Media as a Source of Knowledge about

Products and Services – Sectorwise

Sector

Yes No Total

Count % Count % Count %

Public 180 52.3 164 47.7 344 100

Private 98 55.7 78 44.3 176 100

Total 278 53.5 242 46.5 520 100

Pearson Chi-square value: 0.402 df: 1 Not Significant

183

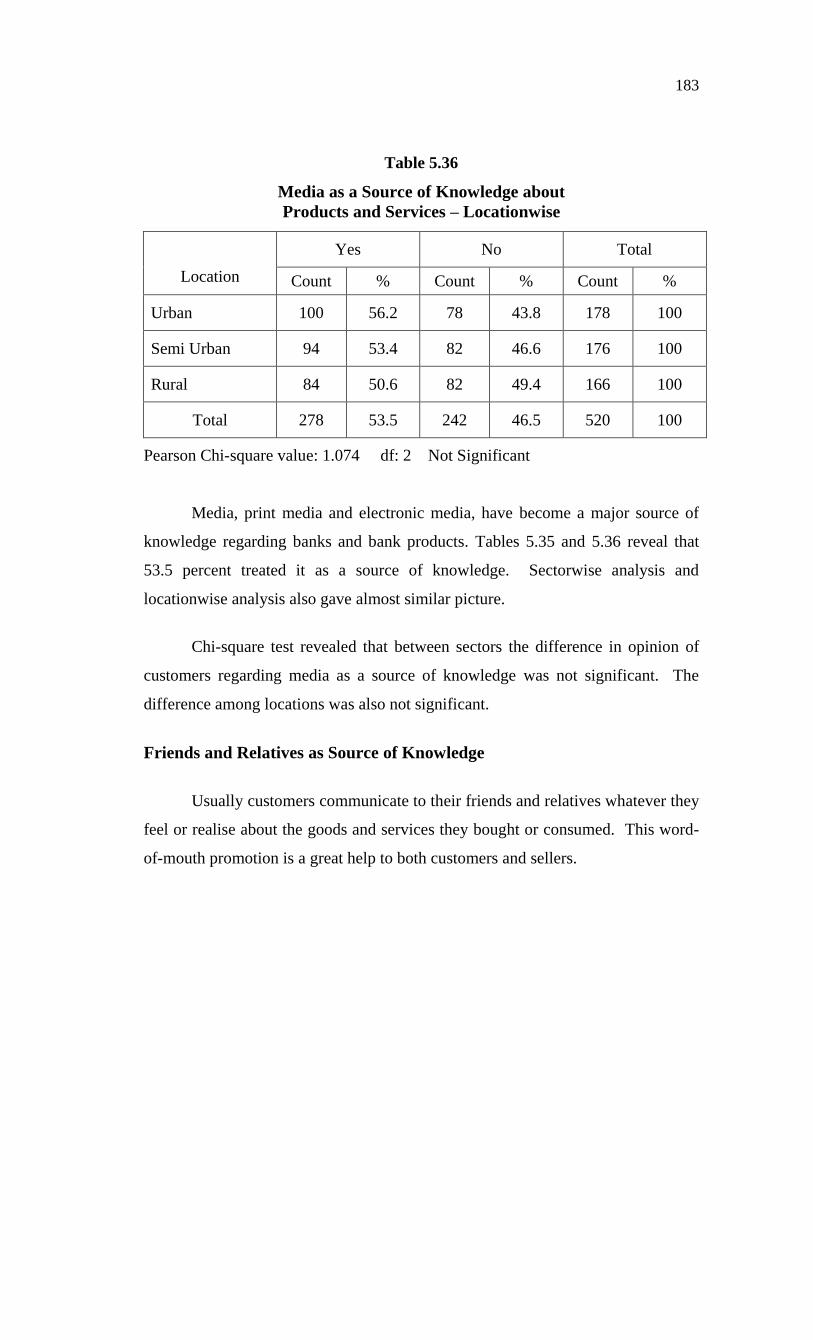

Table 5.36

Media as a Source of Knowledge about

Products and Services – Locationwise

Location

Yes No Total

Count % Count % Count %

Urban 100 56.2 78 43.8 178 100

Semi Urban 94 53.4 82 46.6 176 100

Rural 84 50.6 82 49.4 166 100

Total 278 53.5 242 46.5 520 100

Pearson Chi-square value: 1.074 df: 2 Not Significant

Media, print media and electronic media, have become a major source of

knowledge regarding banks and bank products. Tables 5.35 and 5.36 reveal that

53.5 percent treated it as a source of knowledge. Sectorwise analysis and

locationwise analysis also gave almost similar picture.

Chi-square test revealed that between sectors the difference in opinion of

customers regarding media as a source of knowledge was not significant. The

difference among locations was also not significant.

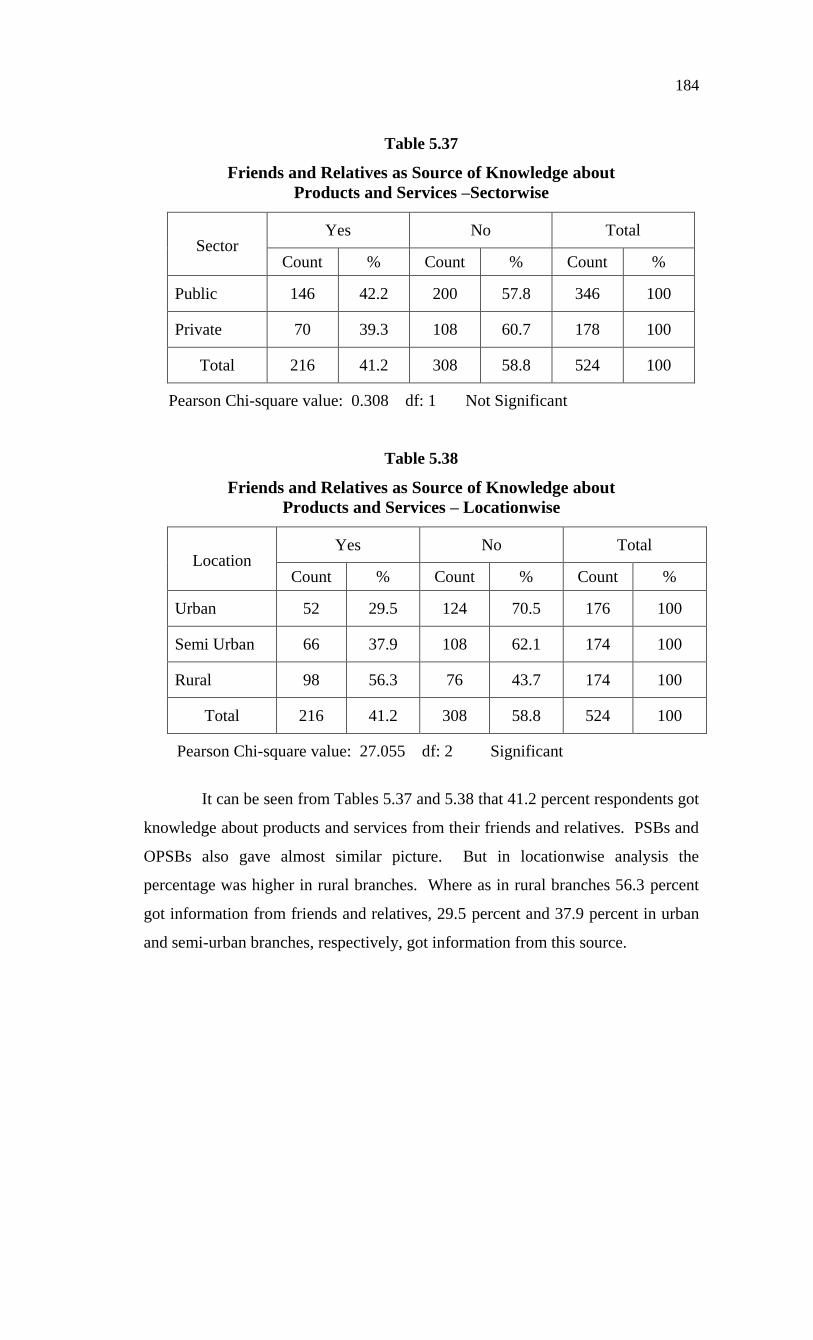

Friends and Relatives as Source of Knowledge

Usually customers communicate to their friends and relatives whatever they

feel or realise about the goods and services they bought or consumed. This word-

of-mouth promotion is a great help to both customers and sellers.

184

Table 5.37

Friends and Relatives as Source of Knowledge about

Products and Services –Sectorwise

Sector Yes No Total

Count % Count % Count %

Public 146 42.2 200 57.8 346 100

Private 70 39.3 108 60.7 178 100

Total 216 41.2 308 58.8 524 100

Pearson Chi-square value: 0.308 df: 1 Not Significant

Table 5.38

Friends and Relatives as Source of Knowledge about

Products and Services – Locationwise

Location Yes No Total

Count % Count % Count %

Urban 52 29.5 124 70.5 176 100

Semi Urban 66 37.9 108 62.1 174 100

Rural 98 56.3 76 43.7 174 100

Total 216 41.2 308 58.8 524 100

Pearson Chi-square value: 27.055 df: 2 Significant

It can be seen from Tables 5.37 and 5.38 that 41.2 percent respondents got

knowledge about products and services from their friends and relatives. PSBs and

OPSBs also gave almost similar picture. But in locationwise analysis the

percentage was higher in rural branches. Where as in rural branches 56.3 percent

got information from friends and relatives, 29.5 percent and 37.9 percent in urban

and semi-urban branches, respectively, got information from this source.

185

Chi-square test of independence at 5 percent level of significance revealed

that there was no difference in the opinion of PSB and OPSB personnel regarding

friends and relatives as a source of knowledge. But the chi-square test performed

on location analysis revealed that there was considerable difference among urban,

semi-urban, rural personnel with regard to friends and relatives as a source of

knowledge.

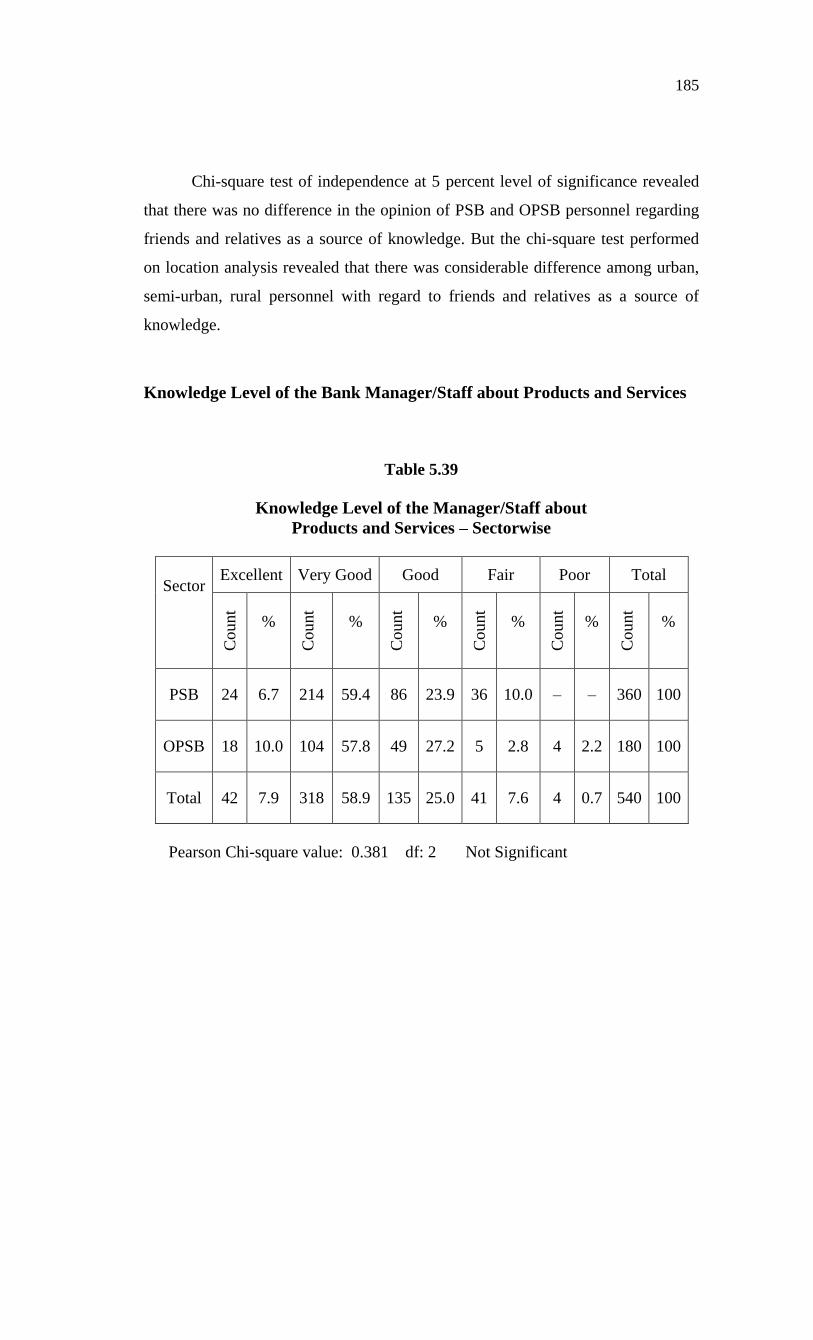

Knowledge Level of the Bank Manager/Staff about Products and Services

Table 5.39

Knowledge Level of the Manager/Staff about

Products and Services – Sectorwise

Sector Excellent Very Good Good Fair Poor Total

Count

%

Count

%

Count

%

Count

%

Count

%

Count

%

PSB 24 6.7 214 59.4 86 23.9 36 10.0 – – 360 100

OPSB 18 10.0 104 57.8 49 27.2 5 2.8 4 2.2 180 100

Total 42 7.9 318 58.9 135 25.0 41 7.6 4 0.7 540 100

Pearson Chi-square value: 0.381 df: 2 Not Significant

186

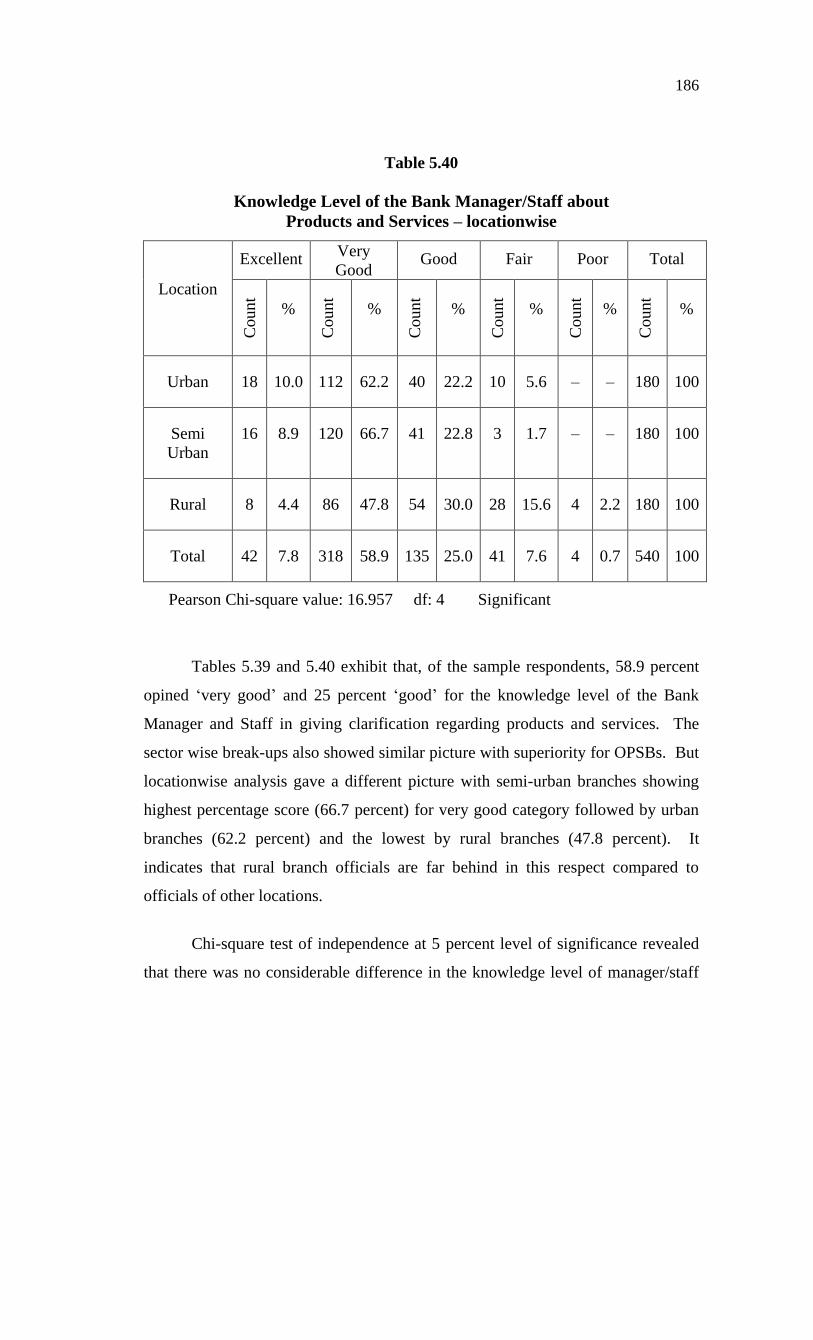

Table 5.40

Knowledge Level of the Bank Manager/Staff about

Products and Services – locationwise

Location

Excellent Very

Good Good Fair Poor Total

Count

%

Count

%

Count

%

Count

%

Count

%

Count

%

Urban 18 10.0 112 62.2 40 22.2 10 5.6 – – 180 100

Semi

Urban

16 8.9 120 66.7 41 22.8 3 1.7 – – 180 100

Rural 8 4.4 86 47.8 54 30.0 28 15.6 4 2.2 180 100

Total 42 7.8 318 58.9 135 25.0 41 7.6 4 0.7 540 100

Pearson Chi-square value: 16.957 df: 4 Significant

Tables 5.39 and 5.40 exhibit that, of the sample respondents, 58.9 percent

opined ‘very good’ and 25 percent ‘good’ for the knowledge level of the Bank

Manager and Staff in giving clarification regarding products and services. The

sector wise break-ups also showed similar picture with superiority for OPSBs. But

locationwise analysis gave a different picture with semi-urban branches showing

highest percentage score (66.7 percent) for very good category followed by urban

branches (62.2 percent) and the lowest by rural branches (47.8 percent). It

indicates that rural branch officials are far behind in this respect compared to

officials of other locations.

Chi-square test of independence at 5 percent level of significance revealed

that there was no considerable difference in the knowledge level of manager/staff

187

of PSBs and OPSBs. But chi-square test on locations revealed that there was

considerable difference among urban, semi-urban and rural branches in this regard.

Opinion of Bank Personnel on Marketing Strategy

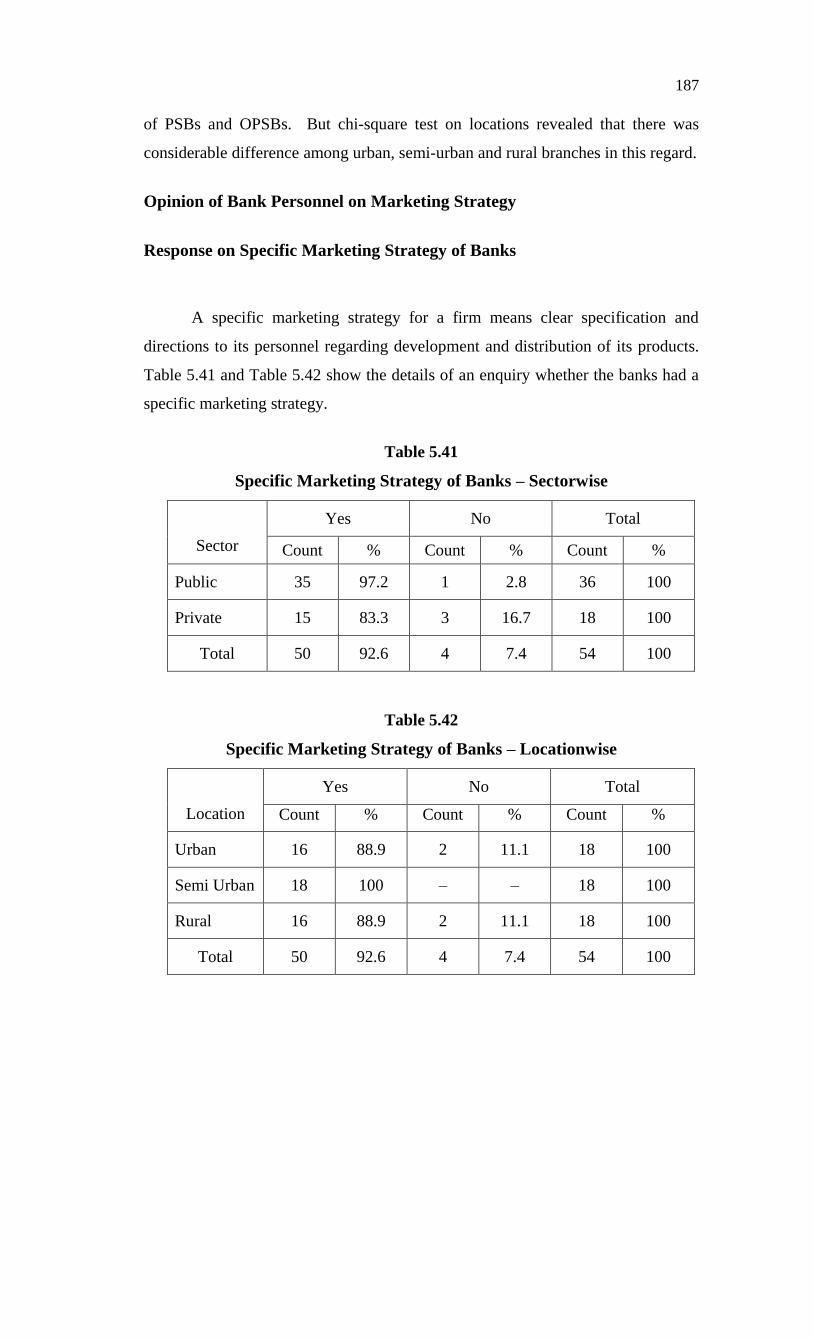

Response on Specific Marketing Strategy of Banks

A specific marketing strategy for a firm means clear specification and

directions to its personnel regarding development and distribution of its products.

Table 5.41 and Table 5.42 show the details of an enquiry whether the banks had a

specific marketing strategy.

Table 5.41

Specific Marketing Strategy of Banks – Sectorwise

Sector

Yes No Total

Count % Count % Count %

Public 35 97.2 1 2.8 36 100

Private 15 83.3 3 16.7 18 100

Total 50 92.6 4 7.4 54 100

Table 5.42

Specific Marketing Strategy of Banks – Locationwise

Location

Yes No Total

Count % Count % Count %

Urban 16 88.9 2 11.1 18 100

Semi Urban 18 100 – – 18 100

Rural 16 88.9 2 11.1 18 100

Total 50 92.6 4 7.4 54 100

188

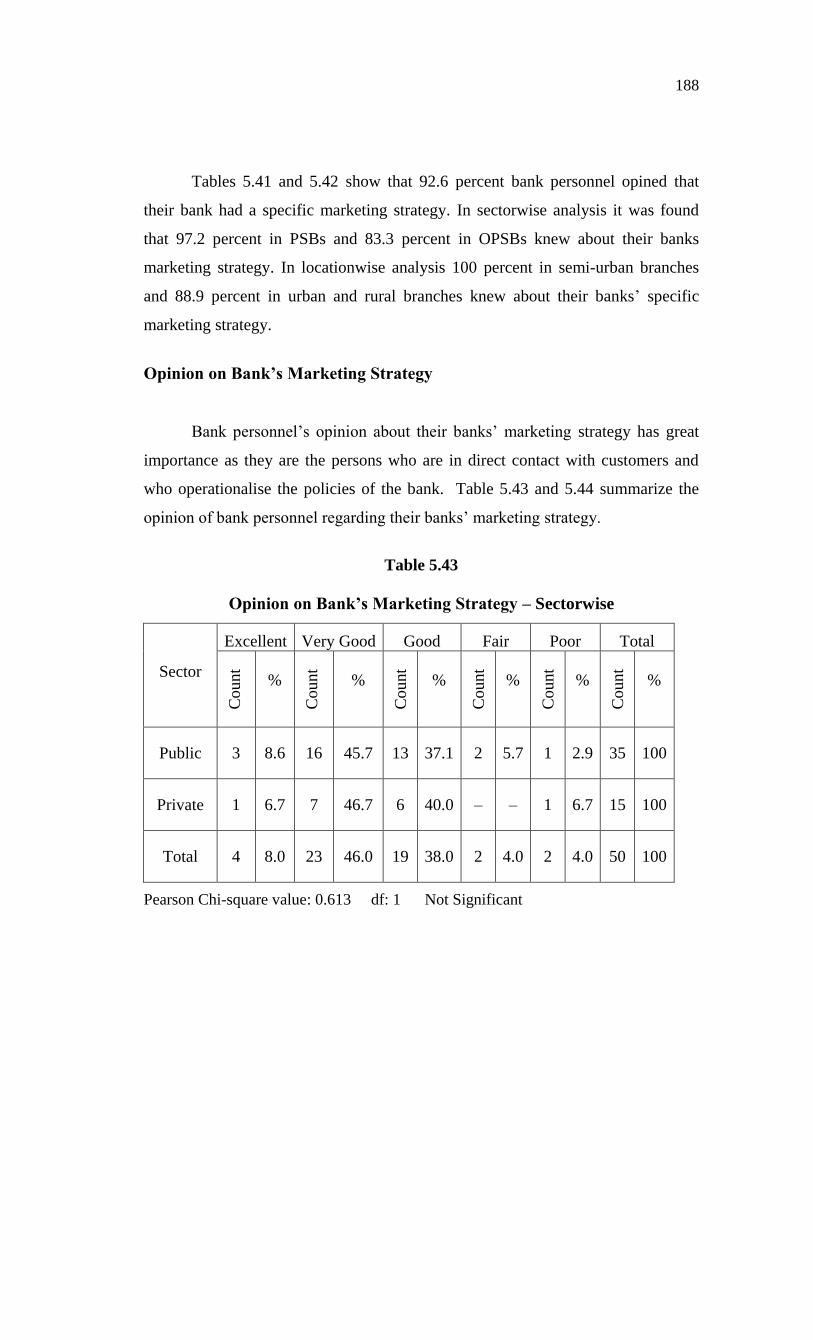

Tables 5.41 and 5.42 show that 92.6 percent bank personnel opined that

their bank had a specific marketing strategy. In sectorwise analysis it was found

that 97.2 percent in PSBs and 83.3 percent in OPSBs knew about their banks

marketing strategy. In locationwise analysis 100 percent in semi-urban branches

and 88.9 percent in urban and rural branches knew about their banks’ specific

marketing strategy.

Opinion on Bank’s Marketing Strategy

Bank personnel’s opinion about their banks’ marketing strategy has great

importance as they are the persons who are in direct contact with customers and

who operationalise the policies of the bank. Table 5.43 and 5.44 summarize the

opinion of bank personnel regarding their banks’ marketing strategy.

Table 5.43

Opinion on Bank’s Marketing Strategy – Sectorwise

Sector

Excellent Very Good Good Fair Poor Total

Count

%

Count

%

Count

%

Count

%

Count

%

Count

%

Public 3 8.6 16 45.7 13 37.1 2 5.7 1 2.9 35 100

Private 1 6.7 7 46.7 6 40.0 – – 1 6.7 15 100

Total 4 8.0 23 46.0 19 38.0 2 4.0 2 4.0 50 100

Pearson Chi-square value: 0.613 df: 1 Not Significant

189

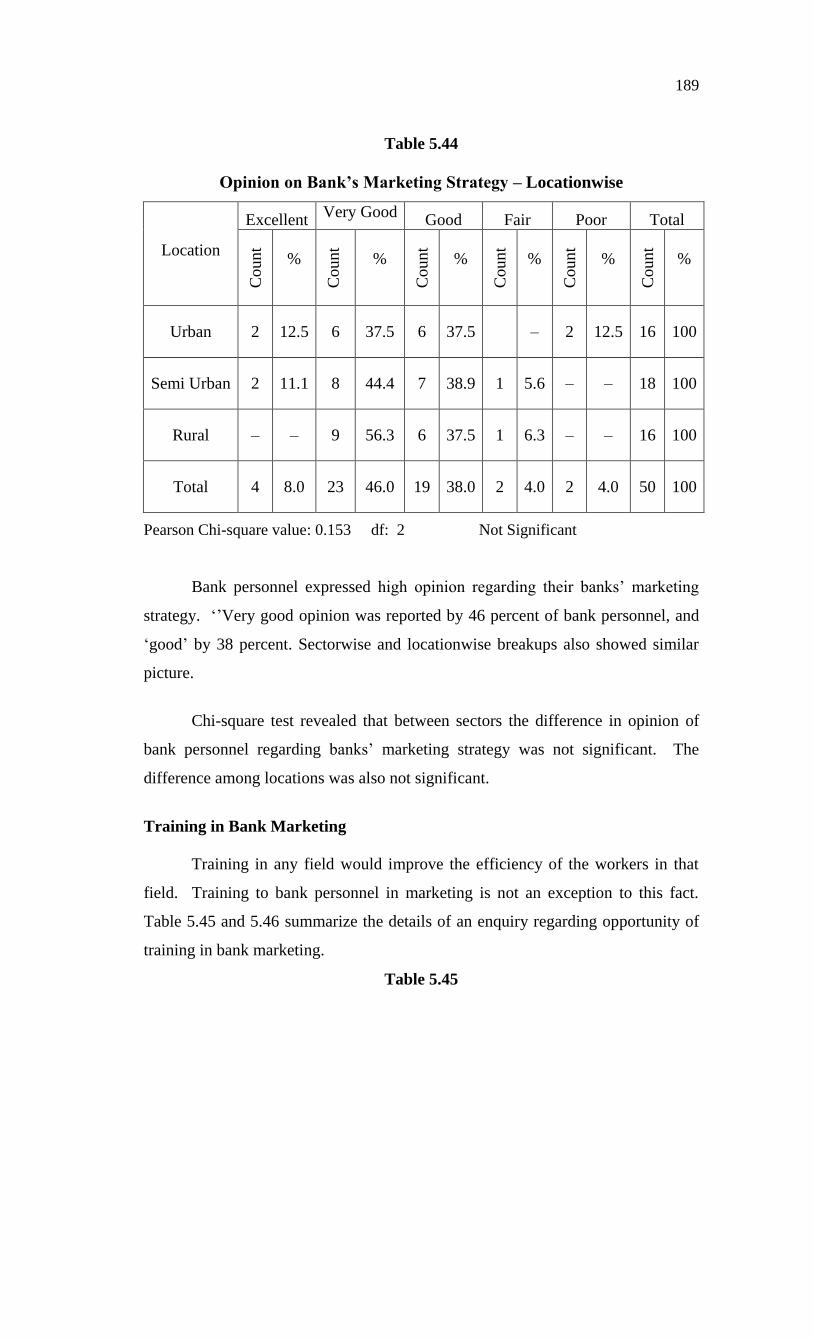

Table 5.44

Opinion on Bank’s Marketing Strategy – Locationwise

Location

Excellent Very Good

Good Fair Poor Total

Count

%

Count

%

Count

%

Count

%

Count

%

Count

%

Urban 2 12.5 6 37.5 6 37.5 – 2 12.5 16 100

Semi Urban 2 11.1 8 44.4 7 38.9 1 5.6 – – 18 100

Rural – – 9 56.3 6 37.5 1 6.3 – – 16 100

Total 4 8.0 23 46.0 19 38.0 2 4.0 2 4.0 50 100

Pearson Chi-square value: 0.153 df: 2 Not Significant

Bank personnel expressed high opinion regarding their banks’ marketing

strategy. ‘’Very good opinion was reported by 46 percent of bank personnel, and

‘good’ by 38 percent. Sectorwise and locationwise breakups also showed similar

picture.

Chi-square test revealed that between sectors the difference in opinion of

bank personnel regarding banks’ marketing strategy was not significant. The

difference among locations was also not significant.

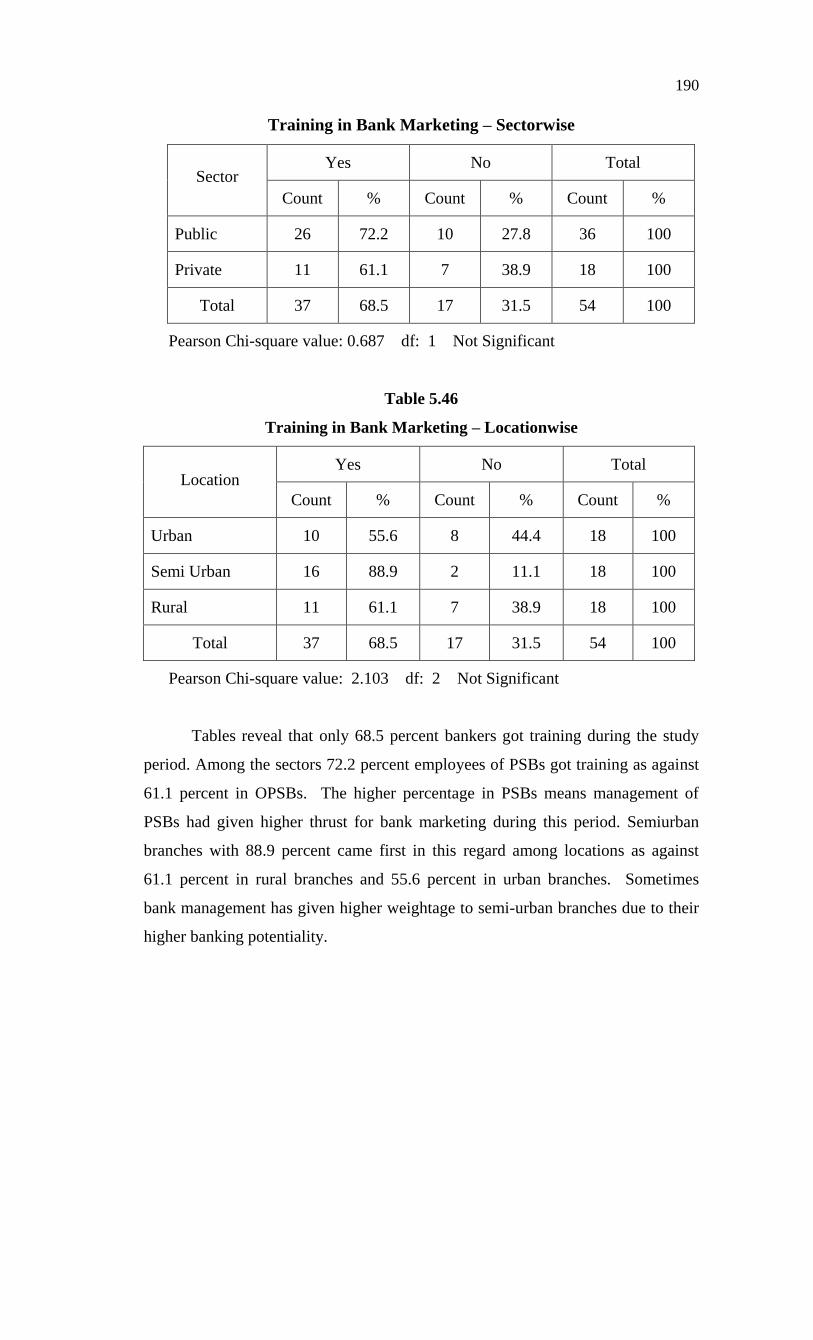

Training in Bank Marketing

Training in any field would improve the efficiency of the workers in that

field. Training to bank personnel in marketing is not an exception to this fact.

Table 5.45 and 5.46 summarize the details of an enquiry regarding opportunity of

training in bank marketing.

Table 5.45

190

Training in Bank Marketing – Sectorwise

Sector Yes No Total

Count % Count % Count %

Public 26 72.2 10 27.8 36 100

Private 11 61.1 7 38.9 18 100

Total 37 68.5 17 31.5 54 100

Pearson Chi-square value: 0.687 df: 1 Not Significant

Table 5.46

Training in Bank Marketing – Locationwise

Location Yes No Total

Count % Count % Count %

Urban 10 55.6 8 44.4 18 100

Semi Urban 16 88.9 2 11.1 18 100

Rural 11 61.1 7 38.9 18 100

Total 37 68.5 17 31.5 54 100

Pearson Chi-square value: 2.103 df: 2 Not Significant

Tables reveal that only 68.5 percent bankers got training during the study

period. Among the sectors 72.2 percent employees of PSBs got training as against

61.1 percent in OPSBs. The higher percentage in PSBs means management of

PSBs had given higher thrust for bank marketing during this period. Semiurban

branches with 88.9 percent came first in this regard among locations as against

61.1 percent in rural branches and 55.6 percent in urban branches. Sometimes

bank management has given higher weightage to semi-urban branches due to their

higher banking potentiality.

191

Chi-square test on sectors revealed that there was no significant difference

between PSBs and OPSBs regarding training to bank personnel. Likewise, the

difference among locations was also not considerable.

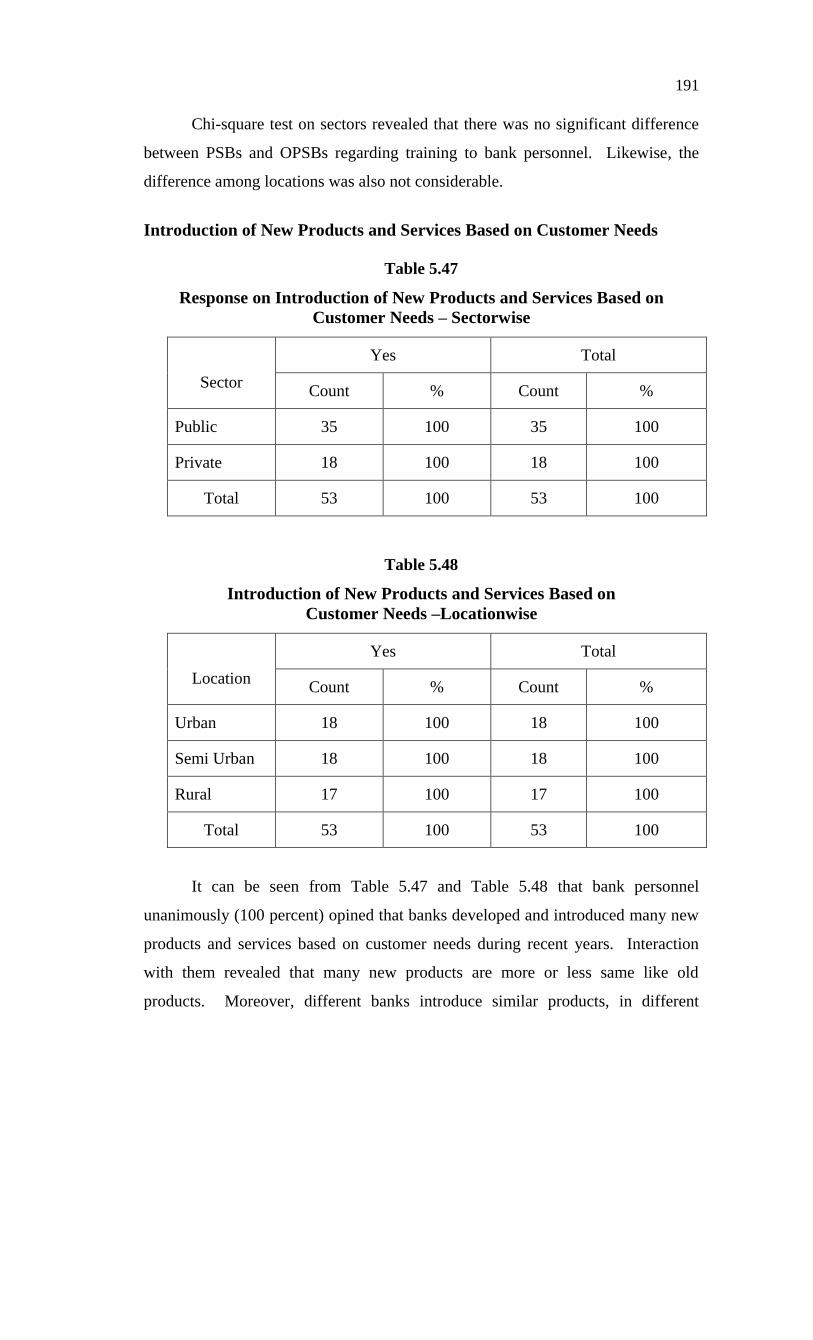

Introduction of New Products and Services Based on Customer Needs

Table 5.47

Response on Introduction of New Products and Services Based on

Customer Needs – Sectorwise

Sector

Yes Total

Count % Count %

Public 35 100 35 100

Private 18 100 18 100

Total 53 100 53 100

Table 5.48

Introduction of New Products and Services Based on

Customer Needs –Locationwise

Location

Yes Total

Count % Count %

Urban 18 100 18 100

Semi Urban 18 100 18 100

Rural 17 100 17 100

Total 53 100 53 100

It can be seen from Table 5.47 and Table 5.48 that bank personnel

unanimously (100 percent) opined that banks developed and introduced many new

products and services based on customer needs during recent years. Interaction

with them revealed that many new products are more or less same like old

products. Moreover, different banks introduce similar products, in different

192

names. Even then they have a special charm in attracting customers. However,

customization of products i.e., developing products according to an individual

customer’s needs, as in new generation banks, is not yet in practice in old

commercial banks.

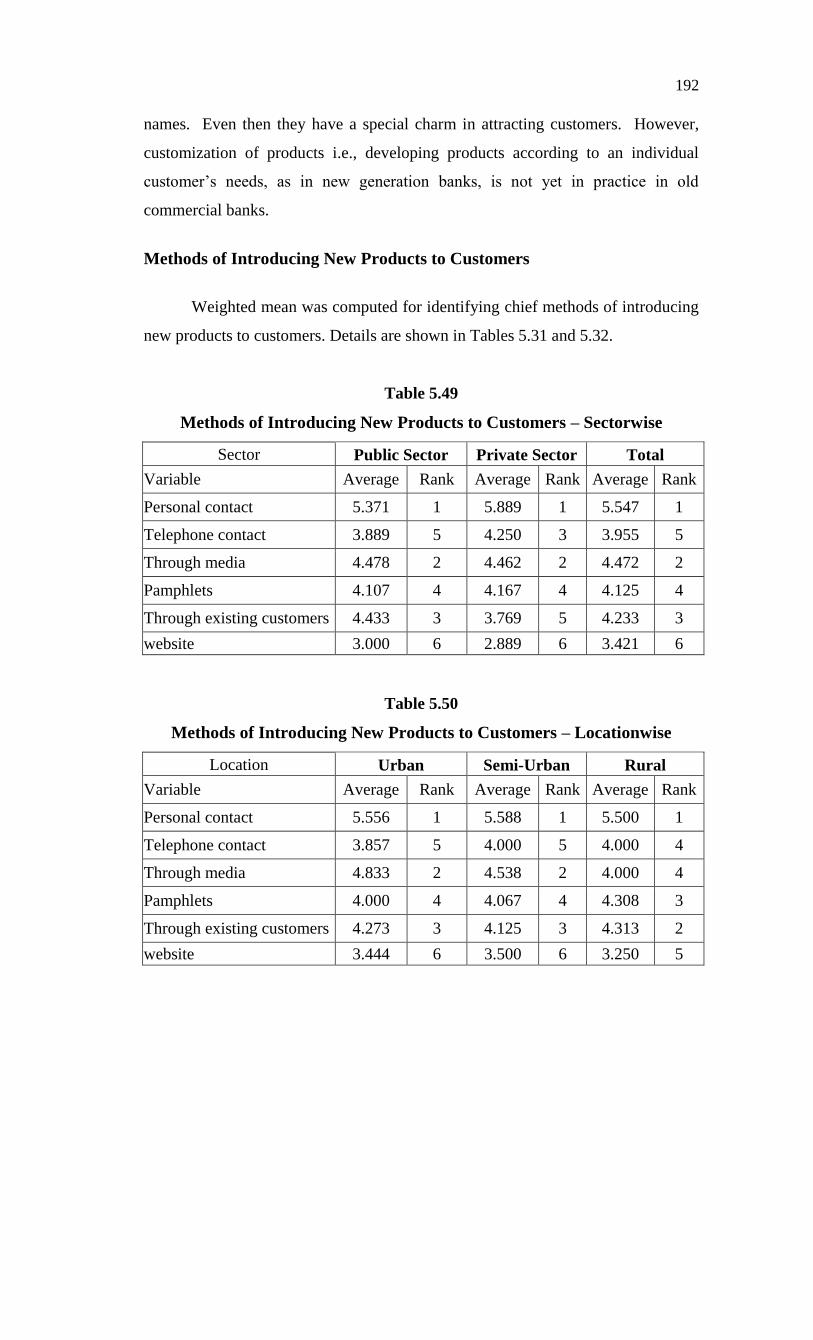

Methods of Introducing New Products to Customers

Weighted mean was computed for identifying chief methods of introducing

new products to customers. Details are shown in Tables 5.31 and 5.32.

Table 5.49

Methods of Introducing New Products to Customers – Sectorwise

Sector Public Sector Private Sector Total

Variable Average Rank Average Rank Average Rank

Personal contact 5.371 1 5.889 1 5.547 1

Telephone contact 3.889 5 4.250 3 3.955 5

Through media 4.478 2 4.462 2 4.472 2

Pamphlets 4.107 4 4.167 4 4.125 4

Through existing customers 4.433 3 3.769 5 4.233 3

website 3.000 6 2.889 6 3.421 6

Table 5.50

Methods of Introducing New Products to Customers – Locationwise

Location Urban Semi-Urban Rural

Variable Average Rank Average Rank Average Rank

Personal contact 5.556 1 5.588 1 5.500 1

Telephone contact 3.857 5 4.000 5 4.000 4

Through media 4.833 2 4.538 2 4.000 4

Pamphlets 4.000 4 4.067 4 4.308 3

Through existing customers 4.273 3 4.125 3 4.313 2

website 3.444 6 3.500 6 3.250 5

193

The first method selected was ‘Personal contact’, second ‘Media’, third

‘Existing customers’ and fourth place for ‘Pamphlets’. Even in sectorwise break

ups ‘Personal contact’ and ‘Media’ ranked first and second in both PSBs and

OPSBs. The third position was for ‘Existing customers’ in PSBs and ‘Telephone

contact’ in OPSBs. ‘Pamphlets’ ranked fourth in both sectors.

Locationwise analysis revealed that in all locations ‘personal contact’ was

the first method. With regard to second position in urban and semi-urban branches

‘Media’ was the choice as against ‘Existing customers’ in rural branches. The

third choice was ‘Existing customers’ in urban and semi-urban branches while

‘Pamphlets’ was in rural branches.

Effectiveness of Various Marketing Strategies

Bank personnel are in direct contact with customers and so they are

competent to talk about the effectiveness of various marketing strategies

efficiently. In order to measure the effectiveness of various marketing strategies

11 major factors were taken into consideration. A five point rate scale with Very

high, High, Average, Low and Very Low as points, was used to express

employees’ opinion on each strategy. The marketing strategies considered in this

regard were innovative banking products, price mix, place mix, physical attraction,

customer relationship, advertisements, public relation, personal selling,

professionalism, contact campaigns and loan melas and technological changes.

Mean Effectiveness of Marketing Strategies

In order to measure the combined effectiveness of various marketing

strategies according to bank personnel, ‘mean effectiveness’ was computed. Five

point rating scale was used for computing ‘mean effectiveness’ of marketing

strategies. Values were assigned for each level of effectiveness – five for ‘very high

effectiveness’, four for ‘high effectiveness’, three for ‘average effectiveness’, two

194

for ‘low effectiveness’ and one for ‘very low effectiveness’. Mean value represents

the combined effectiveness of various marketing strategies. A value more than the

standard test value mean of 33 (3 x 11 factors) refers to more than average

effectiveness, while less than the test value mean 33 indicates the opposite.

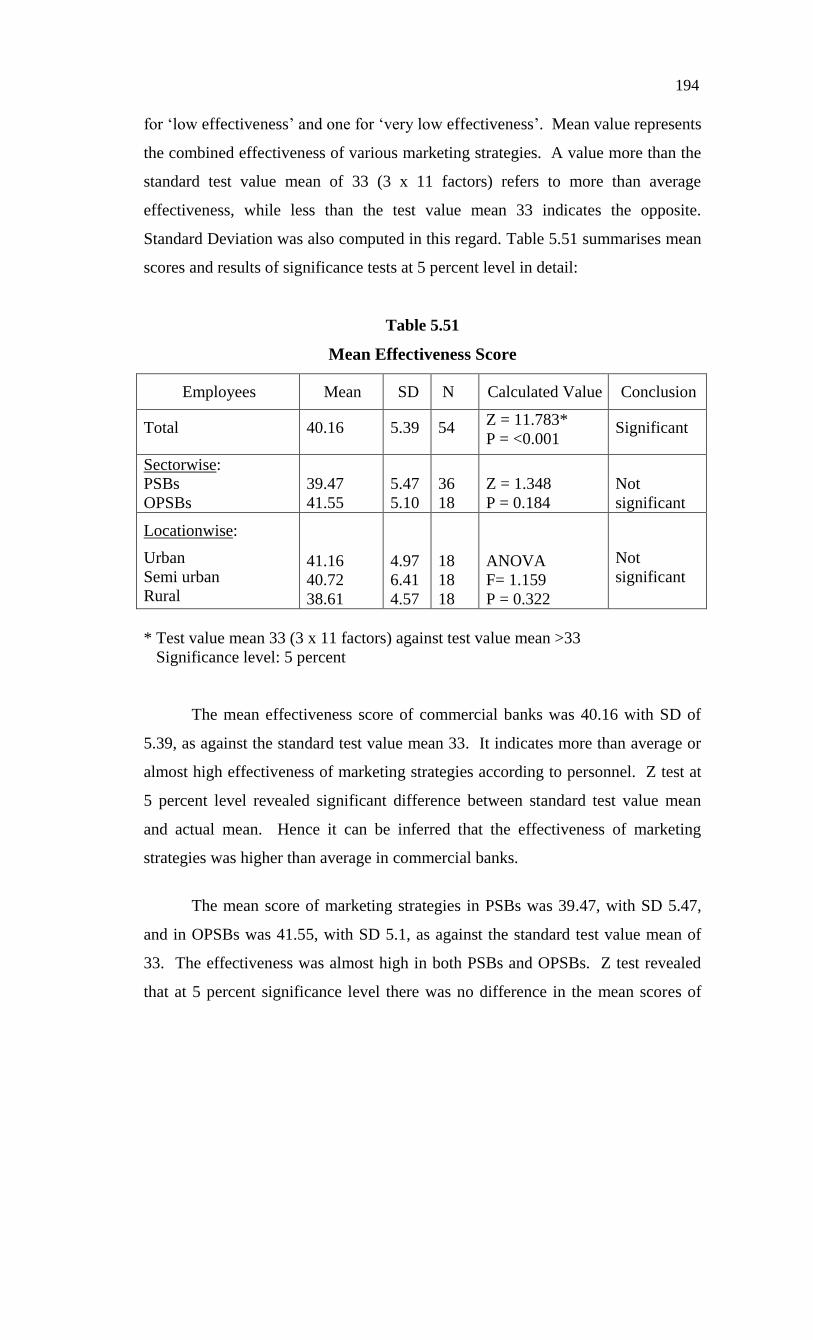

Standard Deviation was also computed in this regard. Table 5.51 summarises mean

scores and results of significance tests at 5 percent level in detail:

Table 5.51

Mean Effectiveness Score

Employees Mean SD N Calculated Value Conclusion

Total 40.16 5.39 54 Z = 11.783*

P = <0.001 Significant

Sectorwise:

PSBs

OPSBs

39.47

41.55

5.47

5.10

36

18

Z = 1.348

P = 0.184

Not

significant

Locationwise:

Urban

Semi urban

Rural

41.16

40.72

38.61

4.97

6.41

4.57

18

18

18

ANOVA

F= 1.159

P = 0.322

Not

significant

* Test value mean 33 (3 x 11 factors) against test value mean >33

Significance level: 5 percent

The mean effectiveness score of commercial banks was 40.16 with SD of

5.39, as against the standard test value mean 33. It indicates more than average or

almost high effectiveness of marketing strategies according to personnel. Z test at

5 percent level revealed significant difference between standard test value mean

and actual mean. Hence it can be inferred that the effectiveness of marketing

strategies was higher than average in commercial banks.

The mean score of marketing strategies in PSBs was 39.47, with SD 5.47,

and in OPSBs was 41.55, with SD 5.1, as against the standard test value mean of

33. The effectiveness was almost high in both PSBs and OPSBs. Z test revealed

that at 5 percent significance level there was no difference in the mean scores of

195

PSBs and OPSBs. Hence it can be inferred that marketing strategies are effective in

both PSBs and OPSBs and the effectiveness was not significantly different in

sectors.

The mean score of marketing strategies in urban branches was 41.16, with

SD 4.97, in semi-urban branches was 40.72, with SD 6.41, and in rural branches

was 38.61, with S.D. 4.57, as against the standard test value mean of 33. It

indicates that the effectiveness of marketing strategies was almost high in all

locations. ANOVA at 5 percent level revealed that there was no significant

difference in the mean scores of urban, semi-urban and rural branches with regard

to effectiveness of marketing strategies. Hence it can be inferred that marketing

strategies are effective in urban, semi-urban and rural branches and the

effectiveness was not significantly different in locations. This is quite different

from the opinion of customers.

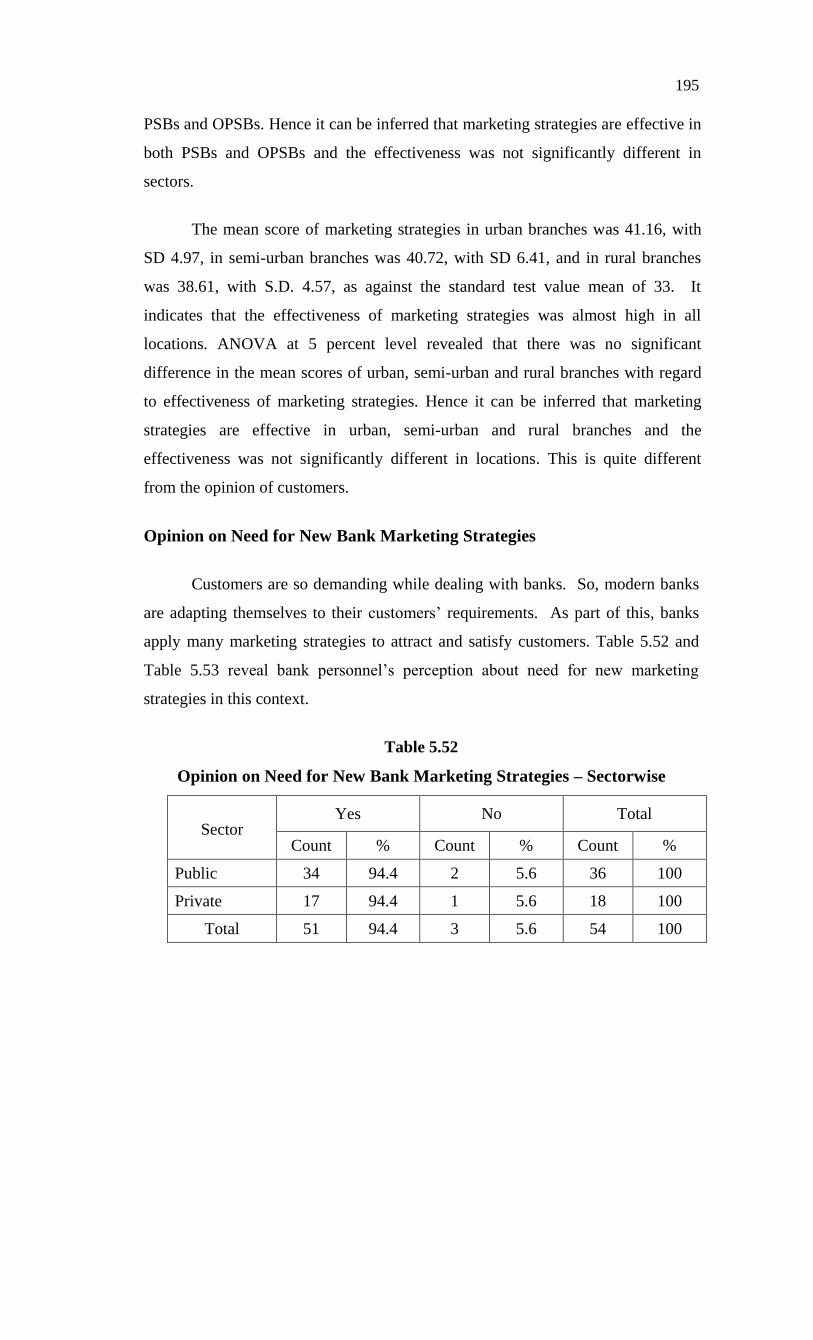

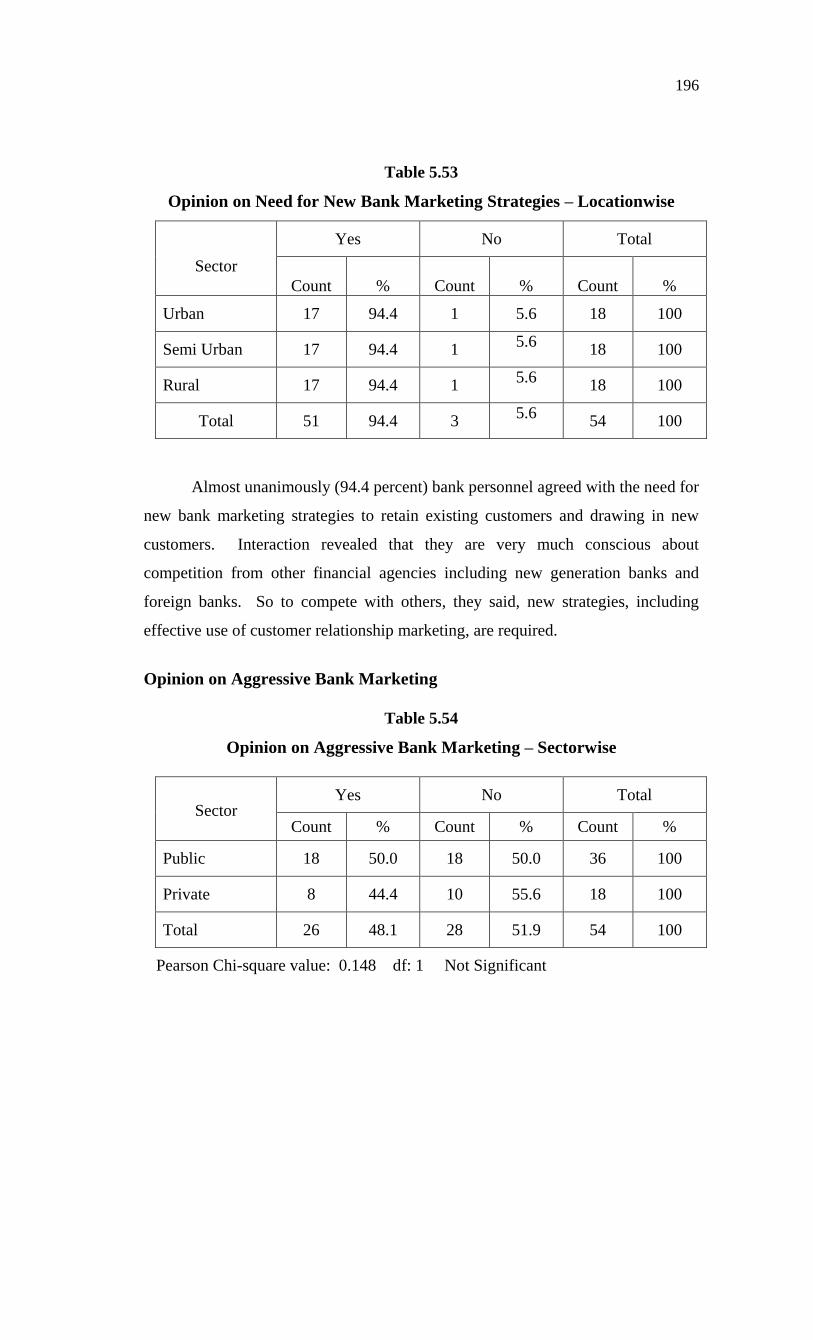

Opinion on Need for New Bank Marketing Strategies

Customers are so demanding while dealing with banks. So, modern banks

are adapting themselves to their customers’ requirements. As part of this, banks

apply many marketing strategies to attract and satisfy customers. Table 5.52 and

Table 5.53 reveal bank personnel’s perception about need for new marketing

strategies in this context.

Table 5.52

Opinion on Need for New Bank Marketing Strategies – Sectorwise

Sector Yes No Total

Count % Count % Count %

Public 34 94.4 2 5.6 36 100

Private 17 94.4 1 5.6 18 100

Total 51 94.4 3 5.6 54 100

196

Table 5.53

Opinion on Need for New Bank Marketing Strategies – Locationwise

Sector

Yes No Total

Count

%

Count

%

Count

%

Urban 17 94.4 1 5.6 18 100

Semi Urban 17 94.4 1 5.6

18 100

Rural 17 94.4 1 5.6

18 100

Total 51 94.4 3 5.6

54 100

Almost unanimously (94.4 percent) bank personnel agreed with the need for

new bank marketing strategies to retain existing customers and drawing in new

customers. Interaction revealed that they are very much conscious about

competition from other financial agencies including new generation banks and

foreign banks. So to compete with others, they said, new strategies, including

effective use of customer relationship marketing, are required.

Opinion on Aggressive Bank Marketing

Table 5.54

Opinion on Aggressive Bank Marketing – Sectorwise

Sector Yes No Total

Count % Count % Count %

Public 18 50.0 18 50.0 36 100

Private 8 44.4 10 55.6 18 100

Total 26 48.1 28 51.9 54 100

Pearson Chi-square value: 0.148 df: 1 Not Significant

197

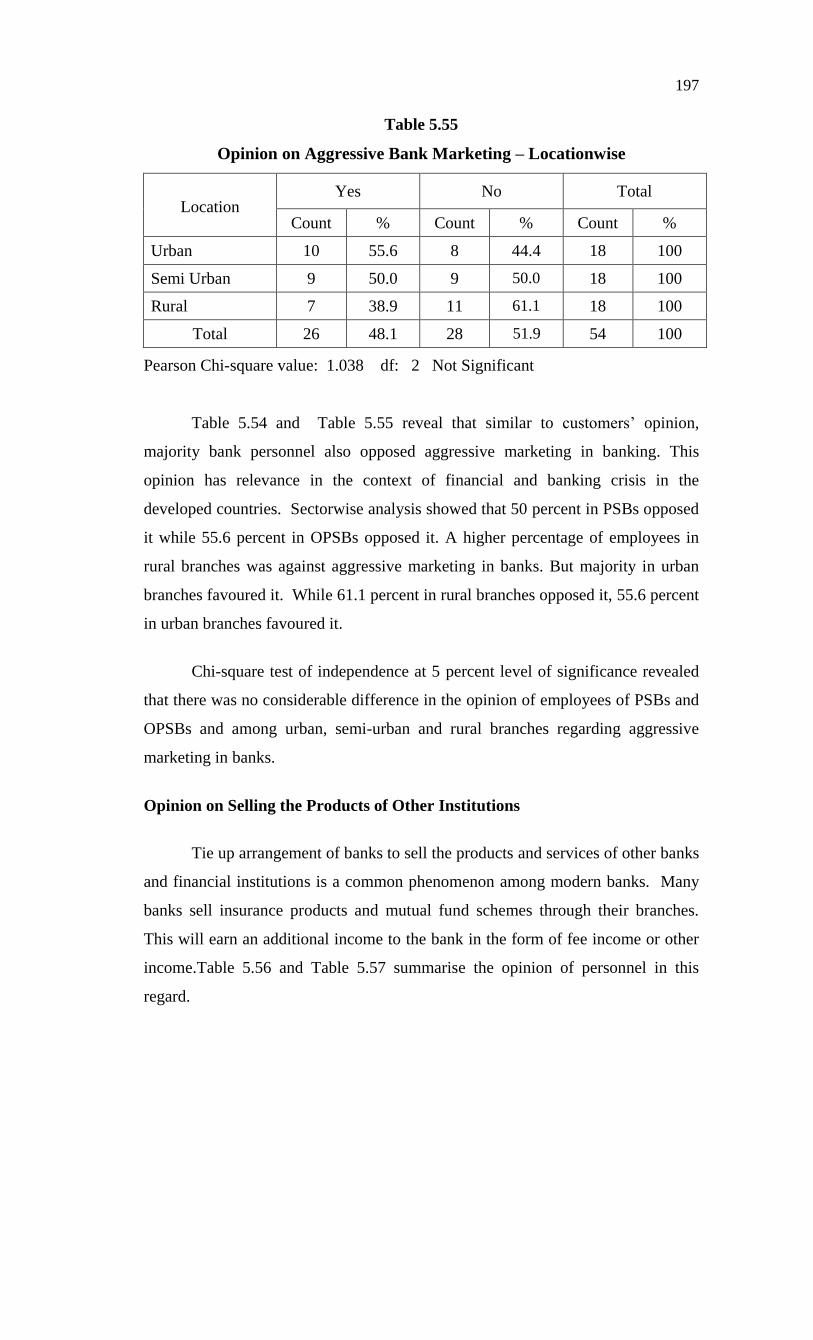

Table 5.55

Opinion on Aggressive Bank Marketing – Locationwise

Location Yes No Total

Count % Count % Count %

Urban 10 55.6 8 44.4 18 100

Semi Urban 9 50.0 9 50.0 18 100

Rural 7 38.9 11 61.1 18 100

Total 26 48.1 28 51.9 54 100

Pearson Chi-square value: 1.038 df: 2 Not Significant

Table 5.54 and Table 5.55 reveal that similar to customers’ opinion,

majority bank personnel also opposed aggressive marketing in banking. This

opinion has relevance in the context of financial and banking crisis in the

developed countries. Sectorwise analysis showed that 50 percent in PSBs opposed

it while 55.6 percent in OPSBs opposed it. A higher percentage of employees in

rural branches was against aggressive marketing in banks. But majority in urban

branches favoured it. While 61.1 percent in rural branches opposed it, 55.6 percent

in urban branches favoured it.

Chi-square test of independence at 5 percent level of significance revealed

that there was no considerable difference in the opinion of employees of PSBs and

OPSBs and among urban, semi-urban and rural branches regarding aggressive

marketing in banks.

Opinion on Selling the Products of Other Institutions

Tie up arrangement of banks to sell the products and services of other banks

and financial institutions is a common phenomenon among modern banks. Many

banks sell insurance products and mutual fund schemes through their branches.

This will earn an additional income to the bank in the form of fee income or other

income.Table 5.56 and Table 5.57 summarise the opinion of personnel in this

regard.

198

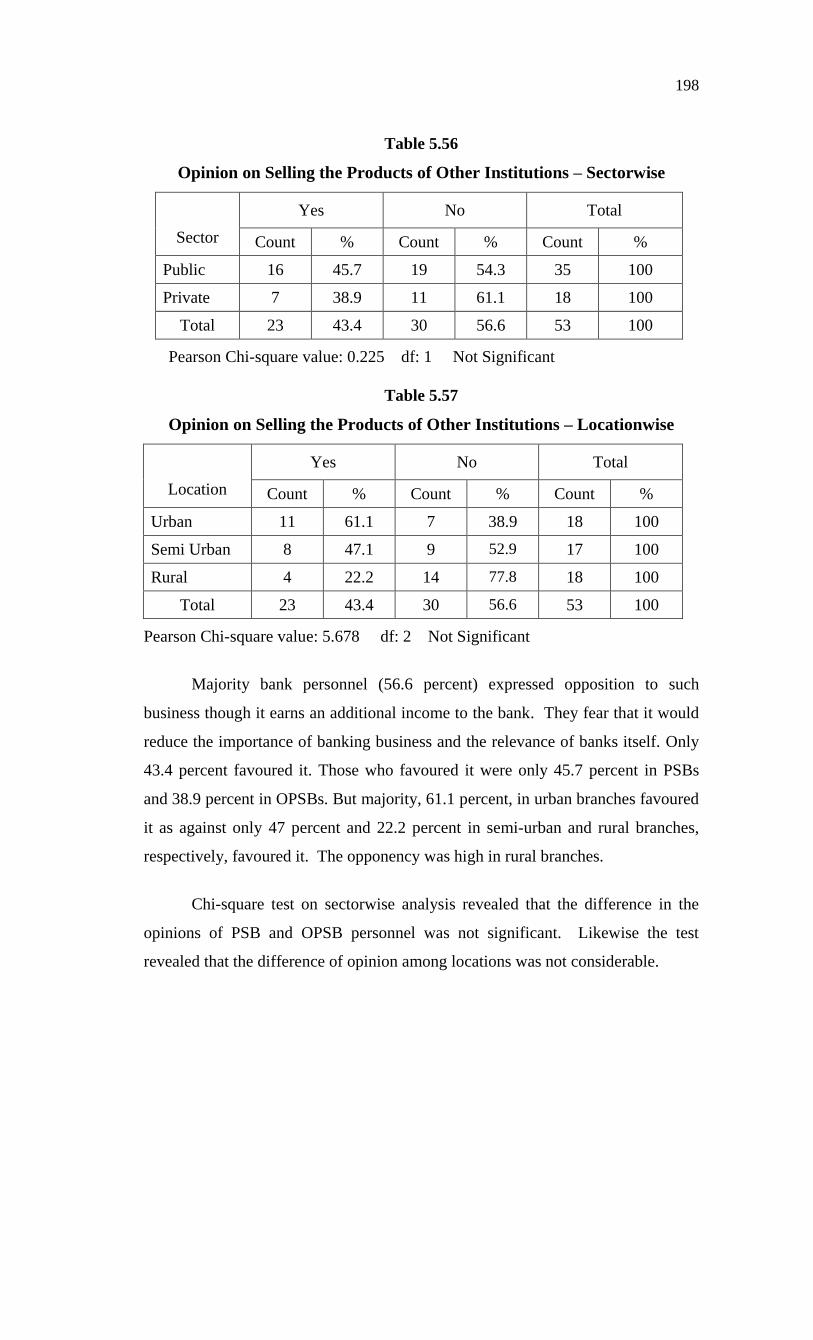

Table 5.56

Opinion on Selling the Products of Other Institutions – Sectorwise

Sector

Yes No Total

Count % Count % Count %

Public 16 45.7 19 54.3 35 100

Private 7 38.9 11 61.1 18 100

Total 23 43.4 30 56.6 53 100

Pearson Chi-square value: 0.225 df: 1 Not Significant

Table 5.57

Opinion on Selling the Products of Other Institutions – Locationwise

Location

Yes No Total

Count % Count % Count %

Urban 11 61.1 7 38.9 18 100

Semi Urban 8 47.1 9 52.9 17 100

Rural 4 22.2 14 77.8 18 100

Total 23 43.4 30 56.6 53 100