Embed Size (px)

Citation preview

Market Outlook of N-Type TechnologyChief Analyst Corrine Lin Dec. 2018

ONE

MARKET

OVERVIEW

TWO

DRIVING FORCE OF

N-TYPE MARKET

THREE

COMPARISON OF

N-TYPE

TECHNOLOGY

FOUR

CONCLUSION

CONTENTS

During the 2018 SNEC, Chinese manufacturers continually announced HJT expansion plans.

However, after China announced the 531 Policy, P-type cell prices plummeted. Price of N-type cell remained high because it’s

difficult to lower N-type cell cost. There’s barely any demand for Chinese N-type products, leading to a postponement in

expansion plans.

How to develop future N-type market?

PV InfoLink will discuss the future outlook of the N-type market with the industry at the Asian Chemical Congress.

ONE

MARKET OVERVIEW

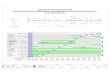

• After global module demand dropped to 88GW in 2018, module demand is projected to rebound to 112GW in 2019.

• The US and European markets that have strong demand for high-efficiency products will witness a significant growth in

2019 demand. It’s difficult for Chinese capacities to be shipped to the US due to the Section 201 tax rate together with the

anti-dumping and countervailing tariff rate. Yet, Chinese capacities can be shipped to Europe directly since there is no

more trade war limitation.

• Other major high-efficiency markets: demand in Australia and Japan have slightly declined.

Forecast of Global Demand

01

-

50

100

150

200

250

2017 2018 2019 2020 2021 2022 2023 2024 2025

2017 - 2025 Module Demand Forecast, Unit: GW

Expected Scenario Optimistic Scenario

110GW+Optimistic Scenario could reach over 150GW

2018 2019

2018-2019 Global Module Demand Forecast

• Overall, the low season this time will last till mid-2019. Moreover, new capacities of each sector of the

supply chain will be continuously released, leading to serious oversupply in 1Q19. The overall supply chain

prices may go down further. Considering manufacturers will start to conduct procurement in 2H19, the

market will witness the lowest price of the year in April 2019.

• The polysilicon sector has more newly-added capacity in the 4Q18-4Q19. A market knockout has begun

for this sector in 2H18. As of mono wafers, lots of manufacturers have left the market, resulting in mono

wafer supply may tight at 2019Q3.

02

0

10

20

30

40

50

2017Q1 2017Q2 2017Q3 2017Q4 2018Q1 2018Q2 2018Q3 2018Q4 2019Q1 2019Q2 2019Q3 2019Q4

2017-2019 Supply Forecast by Quarter, Unit: GW

Polysilicon Wafer Cell Module Expected Demand

Market Supply and Demand

*Shows only first-tier companies (Capacities>10,000MT/1GW)

TWO

DRIVING FORCE OF

N-TYPE MARKET

03

• The 2017 “Top Runner Program” (installed in 2018) not just planned to boost installation scale but also increased efficiency

threshold. Manufacturers have continually won the bid with a “full score”, pushing up the power output of 60-cell PERC

modules to 310W.

• The requirement of the “General Top Runner Program” can be achieved easier with any mono & multi products in combine

with the PERC technology. However, a “full score” standard of the “Super Top Runner Program” needs forward-looking

technologies. Aside from module technologies, cell has to achieve a conversion efficiency of 23% too.

➢ In order to encourage technology upgrade, the Chinese government released PV plant demonstration projects. Only products that match the

efficiency threshold can join the bid.

➢ Scale in the previous years 2015: 1GW/ 2016: 5.5GW/ 2017: 8GW

➢ Efficiency Threshold:

Top Runner Program

Efficiency Level Multi Module Mono Module

First 17.5% or more 18.0% or more

Second 16.5 - 17.5% 17.0 - 18.0%

Corresponding

Module Wattage60pc:270W or more 60pc:280W or more

Corresponding

Cell Efficiency>18.5% >19.6%

2015 - 2016

Program TypeModule

Efficiency

Corresponding

Module WattageCell Efficiency*

General Top

Runner Program

(lower score)

Multi Module 17.0% 280W or more 19.50% or more

Mono Module 17.8% 295W or more 20.80% or more

General Top

Runner Program

(highest score-

full score)

Multi Module 17.9% 295W or more 20.00% or more

Mono Module 18.7% 310W or more 21.50% or more

Super Top Runner

Program

(lower score)

Multi Module 18.0% 295W or more 20.00% or more

Mono Module 18.9% 310W or more 21.50% or more

Super Top Runner

Program

(highest score-

full score)

Multi Module 19.4% 320W or more 21.05% or more

Mono Module 20.4% 335W or more 23.00% or more

2017

*Cell efficiency of the “General Top Runner Program” is an estimation.

The 2017 “Top Runner Program” Encouraged 310W+

*Module calculated by 1650*992mm area.

• In the “General Top Runner Program” this time, due to capacity and cost effectiveness limitation,manufacturers ended up using mono PERC cells for projects that can be completed with both P and N-type products. N-type products only took up 10% of the total products. As for the “Super Top RunnerProgram” that requests higher efficiency, N-type products represented 1/3 portion.

• A new round for next year’s “Top Runner Program” will request higher efficiencies and more advancedtechnologies. This may make P-type products more difficult to finish the projects, and perhaps it willstimulate more manufacturers to use N-type products instead.

Driving Force of N-type Market – 1 – Policy Support

04

Mono PERC44%

Mono PERC-Bifacial23%

Mono PERC-HalfCut

4%

N-Type-Bifacial2%

N-Type8%

Multi-MWT7%

Multi PERC-Black Silicon

6%

Bidding Result of Top Runner by Product Type

• Mono PERC cell has become a mainstream product this year. Most of the expansion this year focuses on mono PERC. This

led to a higher-than-expected total PERC capacity in the world, rising from 33.6GW in the end of last year to 66.7GW in late-

2018. Total PERC expansion reached 33GW in this year. It’s estimated that global PERC capacity will further extend over

26GW by the end of next year, boosting global PERC capacity to more than 92GW.

• There will be 25-30GW of PERC capacity expansion in the next two years. Due to the rapid rise in PERC efficiency and

uncertain mainstream route in the future, N-type production is not likely to be released substantially until after 2020 despite the

higher capacity every year.

05

Driving Force of N-type Market – 2 – SE-PERC Becomes Conventional;

In Need to Search for Next-Generation High-Efficiency Product

8 10 15 17

20 22 22

27 53 78 101 106 109 110

0

50

100

150

200

250

2017 2018 2019 2020 2021 2022 2023

Cell Capacity Forecast, Unit: GW

Multi Normal Multi PERC Mono Normal Mono PERC N-type Mono MWT Thin Film

3

5 9 12 1520 22

11

2854 70 76 78 82

4

4

56

8 11 16

0

20

40

60

80

100

120

140

160

2017 2018 2019 2020 2021 2022 2023

2017 – 2023 Module Shipment Forecast, Unit: GW

Multi Multi PERC P-type Mono P-type Mono PERC N-type Mono Thin Film

Cell Price Trend

• Before SNEC took place this May, many Chinese manufacturers continually announced theexpansion plans of HJT, including GS Solar, CIE Power, Hanergy, Tongwei, Akcome, and SunLinkPV.

• P-type product prices plummeted after China announced the 531 Policy, widening the price gapbetween P and N-type modules. It’s more difficult to sell N-type products, leading to apostponement or suspension of HJT expansion plans. Therefore, shipment of N-type productsshould not grow significantly next year.

0.10

0.17

0.25

0.32

Cell Price Trend, Unit: USD/W

Multi Cell Mono PERC Cell N-PERT Cell HJT Cell

?

06

0 1 2 3 4 5 6

2017

2018

2019

Shipment Forecast of N-Type Products, Unit: GW

N PERT TOPCon HJT IBC

Driving Force of N-type Market – 3 –

A Decisive Battle of Cell Efficiency of over 22%

07

• SE-PERC has becomestandard equipment forproductions this year. AfterSE-PERC pushing up thecell efficiency to 22% nextyear, the definition of “high-efficiency” will be anefficiency of over 22%.

• After achieving anefficiency of 22%, PERCefficiency growth will slowdown. Aside from workingwith module technologies,many top-tiermanufacturers have startedto think about how tomaintain “high-efficiency”product competitivenessthrough cell.

18

19

20

21

22

23

24

25

2016 2017 2018 2019 2020 2021 2022 2023

Cell Efficiency and Module Wattage Growth Trend (60pcs), Unit: %

Multi Multi PERC Mono Mono PERC HJT / TOPCon

320

325

345

340345

345

300305

310

320 320 320

285 290

280285

290 295 300 305

270 275 280 285290285

Cell Eff. (%)

M4

Wet Etching

P TOPCon?315

158.75 / Half Cut

330

315

THREE

COMPARISON OF N-TYPE

TECHNOLOGY

High-Efficiency Battlefield of a Cell Efficiency of over 22%

08

• After equipping with the SE technology this year, mainstream mono PERC efficiencies haveincreased to 21.5-21.8%, limiting the future improvement of technology and efficiency for P-type multi/mono cells. Top-tier manufacturers and new capacities need to evaluate the C/Pratio if the existing technologies continue to be upgraded and the development of next-generation N-type technology.

• It’s difficult for N-PERT to gain profits, while the difficulty to implement the IBC and cost aretoo high. Therefore, HJT and TOPCon will be the two major focuses for N-type technology inthe next two years.

P-Type

Multi P-Type PERC Black Silicon✚

Mono

N-Type

PERC

IBC

HJT

PERT ✚ TOPCon

HBC

✚ SE ✚

✚

TOPCon?

Mono-Like ?

Comparison of Cell Efficiency, Cost, and Sale Price

09

• Comparing the efficiency and costbetween mono PERC and N-PERT, thecost effectiveness is lower for N-PERT.N-PERT manufacturers will continuallyupgrade the productions lines toTOPCon.

• Comparing TOPCon and HJT, becausethe rapid decline in mono PERC priceshave drove down the overall high-efficiency market price, with prices ofTOPCon and HJT remaining flat orslightly higher than cost, it’s difficult forthese technologies to gain too manyprofits. Therefore, the next priority is toreduce more cost!

• Although the IBC technology can gainhigher profits at the moment, thepower output has far exceeded theconventional products and thus theIBC technology can only go for theniche market.

0.1

0.3

0.5

0.7

0.9

18

20

22

24

26

Multi PERC Mono PERC N PERT N PERT + TOPCon HJT IBC

Comparison of Cell Efficiency, Cost, and Sale Price, Unit: % & US$ / W

Cell Efficiency Cell Cost Cell Price (Dec, 2018)

Comparison of N-Type Technology

10

• More and more manufacturershave started to MP bi-facial P-PERC, forcing N-PERT withmuch higher cost to beginupgrade.

• If N-type cell can’t achieve anefficiency of 23.5% or over24%, it’s difficult to widen thewattage gap. As a result, 2019will be a year for N-typeTOPCon and HJT to competewith each other. The twotechnologies’ equipmentmaturity and possibility toreduce cost are likely to beclearer next year.

Conclusion –

Status Quo and Strategy of Major Manufacturers for Different Technologies

11

Common Strategy

• Reduce cost and

reduce cost further!

• Expand capacities to

motivate the

localization of

equipment, paste,

and other auxiliary

materials will be the

primary goal in the

near future.

• Cost reduction and

efficiency increase

brought by capacity

expansion.

• The process of

unifying the size of

the wafers

HJT

TOPCon

• Panasonic faces quite a lot of pressure due to the lower

PERC prices and shrinkage in the Japanese market.

• 5-inch version for capacities outside of the US, which is not

obvious compared to the wattage advantage. The bargaining

power of wafers is limited too.

Status Quo

• Many manufacturers including Sunpreme, Jinergy, CIE Power

and GS Solar have started to go into mass production. However,

the market price has plummeted after China announced the 531

Policy, leading to a postponement or suspension of HJT

expansion plans. But there are still many new entrants.

• MP efficiency of 22.5-23%

• LG boosted the wattage using the brand advantage with M4 wafers

and MBB, widening the wattage gap with HJT and PERC products.

However, a comparison still needs to be conducted between high-

efficiency product and PERC prices and thus LG is confronted by

profit challenge.

• REC has also started to equip with the TOPCon technology in Q3

this year.

• Jolywood will be the first manufacturer to mass produce

TOPCon in China. The initial MP efficiency reached

22.5%.

• Vertically-integrated manufacturers including Jinko,

Trina, JA Solar, and Longi will continually put research

into TOPCon.

1) New Entrants

2) New capacities

Prefer HJT

1) PERT

manufacturers

2) Vertically-

integrated

manufacturers

Prefer TOPCon

In the initial

development

period of the

N-type

market, the

two

technologies

will be

collateral.

The actual

market trend

will depend

on the

equipment

maturity and

cost

reduction

next year.

Overseas

Overseas

China

China

FOUR

CONCLUSION

• Export of N-type modules andcells from China remainedweak at below 30MW,respectively, for January toOctober 2018.

• N-type cell export has begunto rise stably starting fromlate-2Q18. There was also asmall amount of HJT cellexport.

• N-type module export mainlywent to the Netherlands, theUS, Japan, Thailand, andMexico.

• HJT cell and module exportmainly went to the US andThailand.

• Current mainstream poweroutput: 360-375W (72-cell)/300-315W (60-cell) for PERTand 370-400W (72-cell)/ 310-315W (60-cell) for HJT.

Export Distribution of Chinese N-type Modules and Cells

12

2018 N-type Module and Cell Export Distribution

HJT Cell

PERT Cell

Italy

UAE

Philippines

US

Source: PV InfoLink Customs export analysis

**Collection from January to October

Japan

United States

Conclusion

13

• SE-PERC is the product with the best cost effectiveness at the moment, with the market share expanding rapidly. SE-PERC will be the most

mainstream “high-efficiency” product before 2020. Overall, mono PERC will continue to dominate the market before 2020, while N-type can only

maintain a market share of 4-6%. Meanwhile, because cost is higher and price drop is limited for TOPCon and HJT, it’s difficult for these two

technologies to gain too many profits with a price slightly higher or flat from cost.

• The N-type technology can’t expand too quickly since PERC has had outstanding performances in terms of quantity, price, and efficiency. Although

it’s difficult for the N-type market share to increase significantly before 2020, the market will eventually have to find PERC’s next generation products,

which allows N-type capacities to slowly rise every year.

• Newer production lines may be able to equip with the N-type

TOPCon technology without adding too many production

processes. When all manufacturers are largely investing in

PERC machines, they also have to think about the

possibilities of equipping with future technologies.

• HJT has only 4-5 of production processes and has potential

in further efficiency growth. More manufacturers are likely to

put into research and development in the HJT technology.

• What type of technology will become a mainstream

technology for N-type products remains to be seen. But

judging from now, in the initial stage of N-type development

in China, TOPCon and HJT will coexist in the market and

develop.

0

5

10

15

20

25

30

2015 2016 2017 2018 2019 2020 2021 2022 2023

Capacity Forecast of N-Type Technology, Unit: GW

IBC HJT TOPCon PERT

ABOUT US

PV InfoLink focuses on the Asian markets and mainly conducts market research on

the Chinese, Korean, Taiwanese, Indian, Japanese, and Southeast Asian

markets. We provide the most up-to-date solar PV market information, including price

tracking of PV products, database establishing of global PV market supply/demand,

report publishing of market analysis, and providing customized consulting services.

PV InfoLink was established in March 2017. Although we are a new company, our

analysts have plenty of experiences in the PV industry. Our analysts have working

experiences in solar energy companies or have more than five years of analyzing

experiences in solar energy industry.

PV InfoLink provides the most up-to-date solar PV market information, including price

tracking of PV products, database establishing of global PV market supply/demand,

report publishing of market analysis, and providing customized consulting services.

www.pvinfolink.com

If you have any question concerning this report, please contact