Embed Size (px)

Citation preview

California Dairy report

Market report - eggs

flour faCts

proDuCe Market upDate

neil Jones Crop upDate

Cheese & Butter

Market upDate

Market News

Click on the link below to view updates:

oil Market WatCh

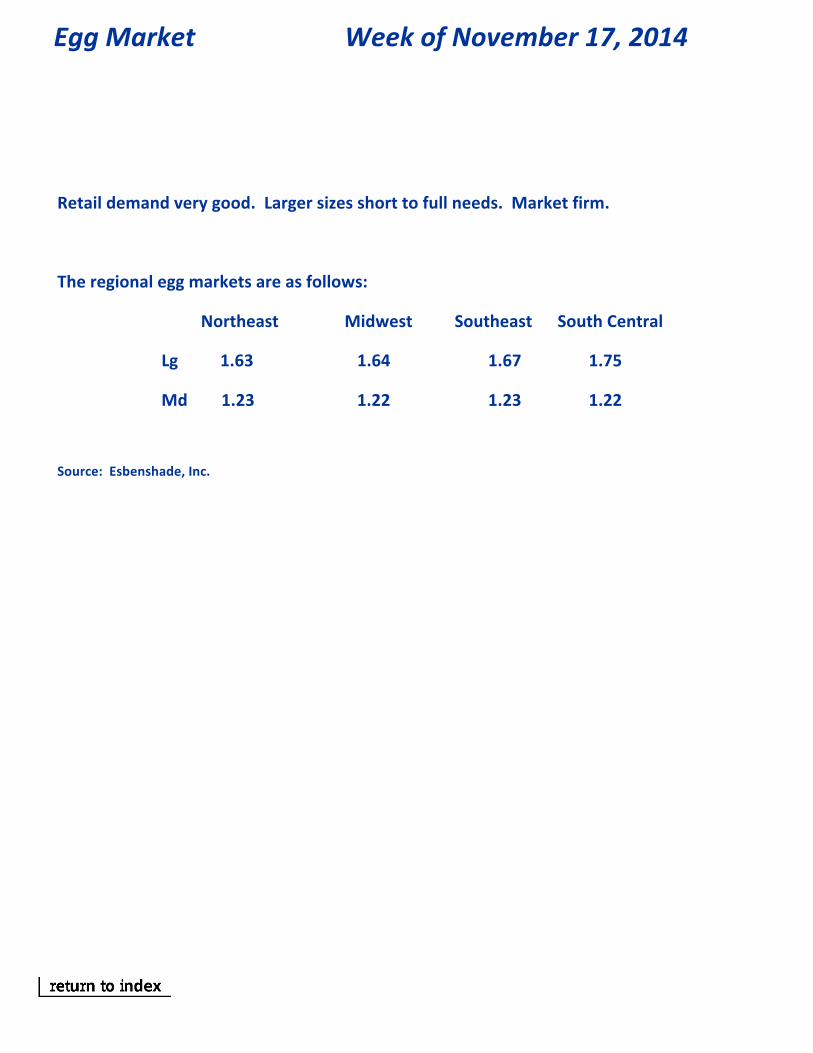

Egg Market Week of November 17, 2014

Retail demand very good. Larger sizes short to full needs. Market firm.

The regional egg markets are as follows:

Northeast Midwest Southeast South Central

Lg 1.63 1.64 1.67 1.75

Md 1.23 1.22 1.23 1.22

Source: Esbenshade, Inc.

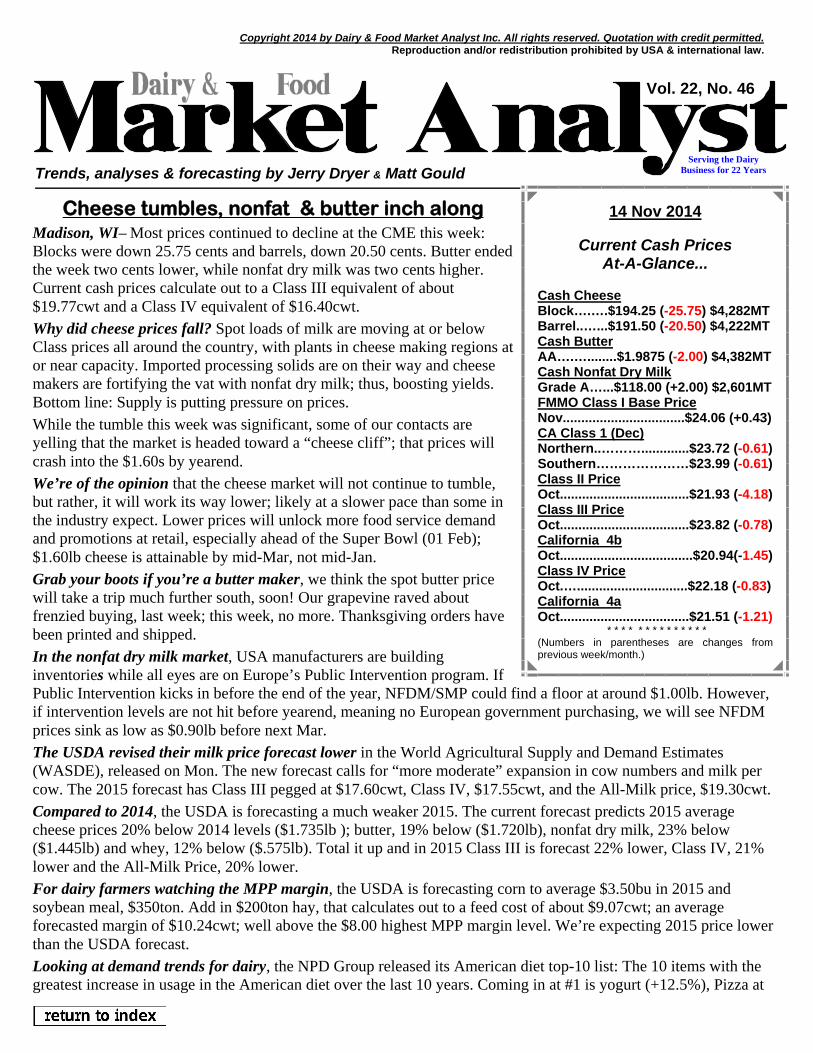

Cheese tumbles, nonfat & butter inch along Madison, WI– Most prices continued to decline at the CME this week: Blocks were down 25.75 cents and barrels, down 20.50 cents. Butter ended the week two cents lower, while nonfat dry milk was two cents higher. Current cash prices calculate out to a Class III equivalent of about $19.77cwt and a Class IV equivalent of $16.40cwt.

Why did cheese prices fall? Spot loads of milk are moving at or below Class prices all around the country, with plants in cheese making regions at or near capacity. Imported processing solids are on their way and cheese makers are fortifying the vat with nonfat dry milk; thus, boosting yields. Bottom line: Supply is putting pressure on prices.

While the tumble this week was significant, some of our contacts are yelling that the market is headed toward a “cheese cliff”; that prices will crash into the $1.60s by yearend.

We’re of the opinion that the cheese market will not continue to tumble, but rather, it will work its way lower; likely at a slower pace than some in the industry expect. Lower prices will unlock more food service demand and promotions at retail, especially ahead of the Super Bowl (01 Feb); $1.60lb cheese is attainable by mid-Mar, not mid-Jan.

Grab your boots if you’re a butter maker, we think the spot butter price will take a trip much further south, soon! Our grapevine raved about frenzied buying, last week; this week, no more. Thanksgiving orders have been printed and shipped.

In the nonfat dry milk market, USA manufacturers are building inventories while all eyes are on Europe’s Public Intervention program. If Public Intervention kicks in before the end of the year, NFDM/SMP could find a floor at around $1.00lb. However, if intervention levels are not hit before yearend, meaning no European government purchasing, we will see NFDM prices sink as low as $0.90lb before next Mar.

The USDA revised their milk price forecast lower in the World Agricultural Supply and Demand Estimates (WASDE), released on Mon. The new forecast calls for “more moderate” expansion in cow numbers and milk per cow. The 2015 forecast has Class III pegged at $17.60cwt, Class IV, $17.55cwt, and the All-Milk price, $19.30cwt.

Compared to 2014, the USDA is forecasting a much weaker 2015. The current forecast predicts 2015 average cheese prices 20% below 2014 levels ($1.735lb ); butter, 19% below ($1.720lb), nonfat dry milk, 23% below ($1.445lb) and whey, 12% below ($.575lb). Total it up and in 2015 Class III is forecast 22% lower, Class IV, 21% lower and the All-Milk Price, 20% lower.

For dairy farmers watching the MPP margin, the USDA is forecasting corn to average $3.50bu in 2015 and soybean meal, $350ton. Add in $200ton hay, that calculates out to a feed cost of about $9.07cwt; an average forecasted margin of $10.24cwt; well above the $8.00 highest MPP margin level. We’re expecting 2015 price lower than the USDA forecast.

Looking at demand trends for dairy, the NPD Group released its American diet top-10 list: The 10 items with the greatest increase in usage in the American diet over the last 10 years. Coming in at #1 is yogurt (+12.5%), Pizza at

Vol. 22, No. 46

Trends, analyses & forecasting by Jerry Dryer & Matt Gould

Copyright 2014 by Dairy & Food Market Analyst Inc. All rights reserved. Quotation with credit permitted. Reproduction and/or redistribution prohibited by USA & international law.

14 Nov 2014

Current Cash Prices At-A-Glance...

Cash Cheese Block….….$194.25 (-25.75) $4,282MT Barrel..…...$191.50 (-20.50) $4,222MT Cash Butter AA….…........$1.9875 (-2.00) $4,382MT Cash Nonfat Dry Milk Grade A…...$118.00 (+2.00) $2,601MT FMMO Class I Base Price Nov.................................$24.06 (+0.43) CA Class 1 (Dec) Northern..……….............$23.72 (-0.61) Southern…………………$23.99 (-0.61) Class II Price Oct...................................$21.93 (-4.18) Class III Price Oct...................................$23.82 (-0.78) California 4b Oct....................................$20.94(-1.45) Class IV Price Oct.…..............................$22.18 (-0.83) California 4a Oct...................................$21.51 (-1.21)

* * * * * * * * * * * * * * (Numbers in parentheses are changes from previous week/month.)

Serving the Dairy Business for 22 Years

Page 2 of 3 14 Nov 2014

Nothing in this report shall be deemed to constitute an offer or solicitation for an offer for the purchase or sale of any commodity or security. Dairy & Food Market Analyst Inc. uses sources that it believes to be reliable, but it cannot warrant the accuracy of any of the data or forecasts included in this report. Copyright 2014 by Dairy & Food Market Analyst Inc. All rights reserved. Quotation with credit permitted. Reproduction or redistribution prohibited by international law. Individual, group and corporate subscription rates are available. Contact Jerry Dryer at (561) 445.1074 or [email protected].

Block Barrels Butter Nonfat Whey

11/08/14 2.2198 2.0912 1.9672 1.4633 0.6454

1 Year Ago 1.8248 1.8203 1.4949 1.8633 0.5800

52-Week Low 1.8419 1.8105 1.4828 1.4427 0.5592

52-Week High 2.4212 2.4756 3.0130 2.1026 0.6971

$0.0000$0.2000$0.4000$0.6000$0.8000$1.0000$1.2000$1.4000$1.6000$1.8000$2.0000$2.2000$2.4000$2.6000$2.8000$3.0000

AMS/NASS Price Analysis #3 (+9.6%) and Mexican food at #8 (+8.3%). McDonald’s showed weak comparable sales during Oct, down 3.4% YoY system-wide, with the CEO commenting, “Today’s consumers increasingly prefer customizable food options” (Analyst’s note: Not yet available in McDonald’s restaurants, but in the works.) USA sales were down 1.0%, Europe sales were down 0.7%; Asia/Pacific, Middle East and Africa (APMEA) sales were 4.2% lower YoY, a recovery from the 9.9% YoY decline experienced in 3Q14 due to a supplier issue.

Meanwhile, Pizza Hut, a cheese-friendly business, has announced a complete brand overhaul in the USA, adding customizability to its menus. Set to hit stores 19 Nov, the transformation includes a new logo, a new slogan (“The Flavor of Now”), new uniforms, and of course, a new menu with “exotic” toppings like Peruvian cherry peppers and fresh spinach. Dean Foods reported a fluid milk sales declines of 1% in the third quarter, according to their 3Q14 earnings report; noting that consumers are trading away from their branded product lines to generic, private label.

Across the entire dairy beverage category at retail stores, branded products account for about 58% of volume; private label, 42%, according to IRI data. Whitewave reported that their Silk almond milk grew 30% during 3Q14; Whitewave organic fluid milk sales were up 8% during the quarter.

Around the world, milk production continues to grow. We estimate European milk production up 4.4% YoY during Sep, after being up 4.4% during Aug. The latest data out of New Zealand show Fonterra’s reported NZ milk intakes up 4.0% during Oct, while official NZ production was up 5.2% the month before, according to just released data out of DCANZ. Australian production was up 4.2% YoY during Sep.

Milk production in Russia has turned positive, up 0.05%,

during Sep, after running negative all year; Belarus milk production was up 4.2% during the same month. Consistent with the need for “Emergency” imports, the only production slowdown was in Japan, down 1.25% during Aug (latest data available).

How are the European processors coping with the Russian ban? By sending milk away from the cheese vat and into the drier! EU skim milk powder production was up 32% YoY in Aug after being 25% higher in Jul. Meanwhile, cheese production turned negative; down 1% YoY during Aug after being up 1% in Jul. European butter production also declined during Aug, down 4% YoY while whole milk powder production was flat during the month

For the eternal bear, the risk of the El Niño weather system has been revised lower by NOAA; from a 66% chance to a 58% chance by this winter, despite borderline conditions already existing. The signals do remain mixed, however; with analysts citing record warm water off the coast of Baja California up to San Francisco, fantastic fishing seasons off the coast of Mexico and warmth in the Indian Ocean. Remember: A weak El Niño increases the likelihood of rains in southern California and the high plains; warmth and drought in Southeast Australia (Australia’s dairy region) and

Page 3 of 3 14 Nov 2014

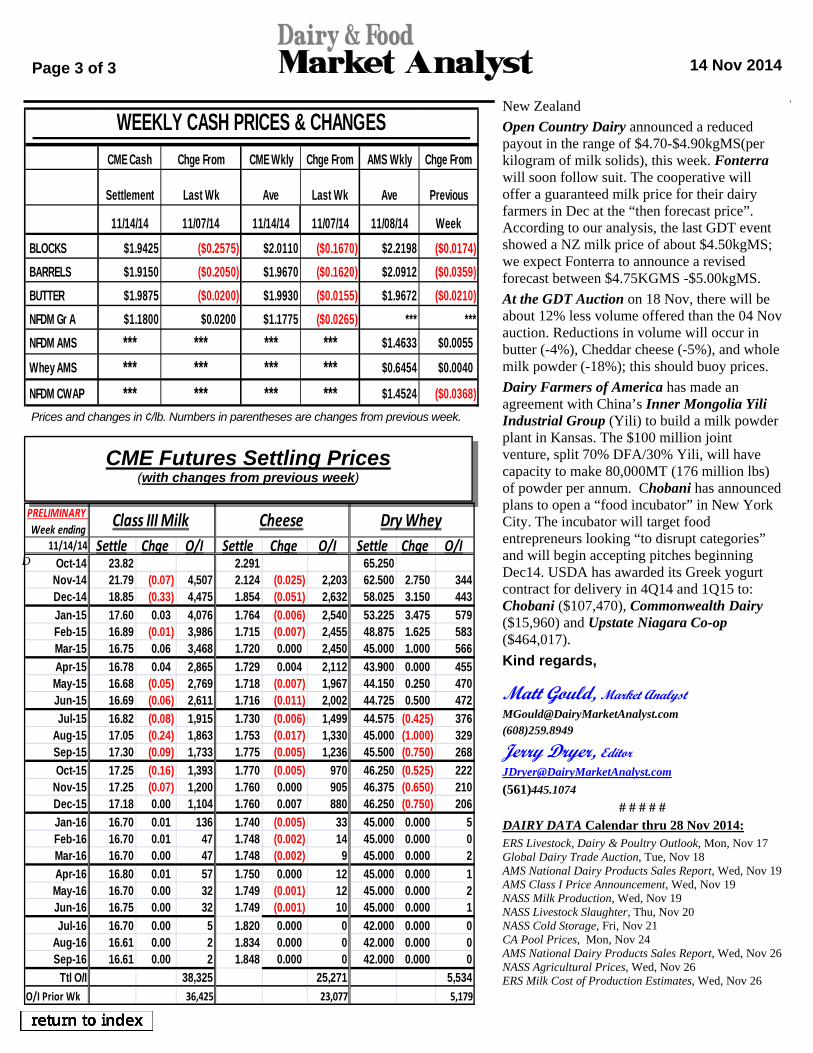

Prices and changes in ¢/lb. Numbers in parentheses are changes from previous week.

CME Futures Settling Prices (with changes from previous week)

New Zealand

Open Country Dairy announced a reduced payout in the range of $4.70-$4.90kgMS(per kilogram of milk solids), this week. Fonterra will soon follow suit. The cooperative will offer a guaranteed milk price for their dairy farmers in Dec at the “then forecast price”. According to our analysis, the last GDT event showed a NZ milk price of about $4.50kgMS; we expect Fonterra to announce a revised forecast between $4.75KGMS -$5.00kgMS.

At the GDT Auction on 18 Nov, there will be about 12% less volume offered than the 04 Nov auction. Reductions in volume will occur in butter (-4%), Cheddar cheese (-5%), and whole milk powder (-18%); this should buoy prices.

Dairy Farmers of America has made an agreement with China’s Inner Mongolia Yili Industrial Group (Yili) to build a milk powder plant in Kansas. The $100 million joint venture, split 70% DFA/30% Yili, will have capacity to make 80,000MT (176 million lbs) of powder per annum. Chobani has announced plans to open a “food incubator” in New York City. The incubator will target food entrepreneurs looking “to disrupt categories” and will begin accepting pitches beginning Dec14. USDA has awarded its Greek yogurt contract for delivery in 4Q14 and 1Q15 to: Chobani ($107,470), Commonwealth Dairy ($15,960) and Upstate Niagara Co-op ($464,017).

Kind regards,

Matt Gould, Market Analyst [email protected] (608)259.8949

Jerry Dryer, Editor [email protected]

(561)445.1074 # # # # #

DAIRY DATA Calendar thru 28 Nov 2014: ERS Livestock, Dairy & Poultry Outlook, Mon, Nov 17 Global Dairy Trade Auction, Tue, Nov 18 AMS National Dairy Products Sales Report, Wed, Nov 19 AMS Class I Price Announcement, Wed, Nov 19 NASS Milk Production, Wed, Nov 19 NASS Livestock Slaughter, Thu, Nov 20 NASS Cold Storage, Fri, Nov 21 CA Pool Prices, Mon, Nov 24 AMS National Dairy Products Sales Report, Wed, Nov 26 NASS Agricultural Prices, Wed, Nov 26 ERS Milk Cost of Production Estimates, Wed, Nov 26

D

CME Cash Chge From CME Wkly Chge From AMS Wkly Chge From

Settlement Last Wk Ave Last Wk Ave Previous

11/14/14 11/07/14 11/14/14 11/07/14 11/08/14 Week

BLOCKS $1.9425 ($0.2575) $2.0110 ($0.1670) $2.2198 ($0.0174)

BARRELS $1.9150 ($0.2050) $1.9670 ($0.1620) $2.0912 ($0.0359)

BUTTER $1.9875 ($0.0200) $1.9930 ($0.0155) $1.9672 ($0.0210)

NFDM Gr A $1.1800 $0.0200 $1.1775 ($0.0265) *** ***

NFDM AMS *** *** *** *** $1.4633 $0.0055

Whey AMS *** *** *** *** $0.6454 $0.0040

NFDM CWAP *** *** *** *** $1.4524 ($0.0368)

WEEKLY CASH PRICES & CHANGES

PRELIMINARY

Week ending11/14/14 Settle Chge O/I Settle Chge O/I Settle Chge O/I

Oct-14 23.82 2.291 65.250Nov-14 21.79 (0.07) 4,507 2.124 (0.025) 2,203 62.500 2.750 344Dec-14 18.85 (0.33) 4,475 1.854 (0.051) 2,632 58.025 3.150 443

Jan-15 17.60 0.03 4,076 1.764 (0.006) 2,540 53.225 3.475 579Feb-15 16.89 (0.01) 3,986 1.715 (0.007) 2,455 48.875 1.625 583Mar-15 16.75 0.06 3,468 1.720 0.000 2,450 45.000 1.000 566

Apr-15 16.78 0.04 2,865 1.729 0.004 2,112 43.900 0.000 455May-15 16.68 (0.05) 2,769 1.718 (0.007) 1,967 44.150 0.250 470Jun-15 16.69 (0.06) 2,611 1.716 (0.011) 2,002 44.725 0.500 472

Jul-15 16.82 (0.08) 1,915 1.730 (0.006) 1,499 44.575 (0.425) 376Aug-15 17.05 (0.24) 1,863 1.753 (0.017) 1,330 45.000 (1.000) 329Sep-15 17.30 (0.09) 1,733 1.775 (0.005) 1,236 45.500 (0.750) 268

Oct-15 17.25 (0.16) 1,393 1.770 (0.005) 970 46.250 (0.525) 222Nov-15 17.25 (0.07) 1,200 1.760 0.000 905 46.375 (0.650) 210Dec-15 17.18 0.00 1,104 1.760 0.007 880 46.250 (0.750) 206

Jan-16 16.70 0.01 136 1.740 (0.005) 33 45.000 0.000 5Feb-16 16.70 0.01 47 1.748 (0.002) 14 45.000 0.000 0Mar-16 16.70 0.00 47 1.748 (0.002) 9 45.000 0.000 2

Apr-16 16.80 0.01 57 1.750 0.000 12 45.000 0.000 1May-16 16.70 0.00 32 1.749 (0.001) 12 45.000 0.000 2Jun-16 16.75 0.00 32 1.749 (0.001) 10 45.000 0.000 1

Jul-16 16.70 0.00 5 1.820 0.000 0 42.000 0.000 0Aug-16 16.61 0.00 2 1.834 0.000 0 42.000 0.000 0Sep-16 16.61 0.00 2 1.848 0.000 0 42.000 0.000 0

Ttl O/I 38,325 25,271 5,534

O/I Prior Wk 36,425 23,077 5,179

Class III Milk Cheese Dry Whey

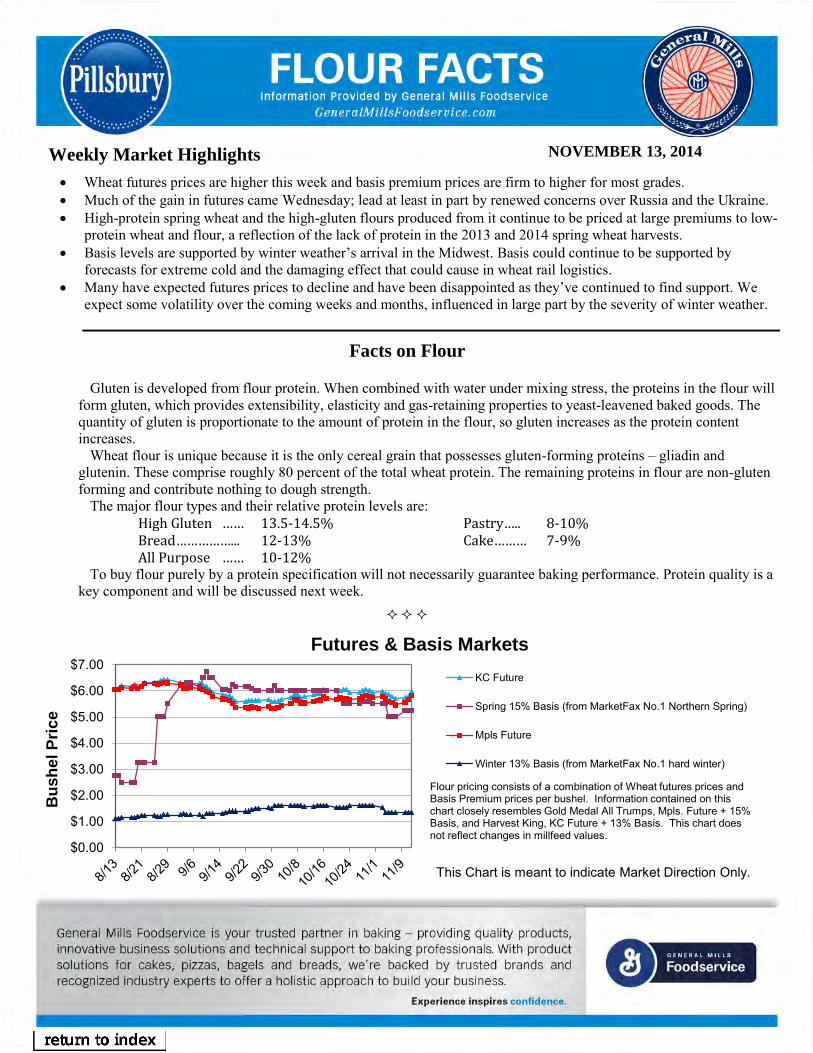

Weekly Market Highlights

Wheat futures prices are higher this week and basis premium prices are firm to higher for most grades. Much of the gain in futures came Wednesday; lead at least in part by renewed concerns over Russia and the Ukraine. High-protein spring wheat and the high-gluten flours produced from it continue to be priced at large premiums to low-

protein wheat and flour, a reflection of the lack of protein in the 2013 and 2014 spring wheat harvests. Basis levels are supported by winter weather’s arrival in the Midwest. Basis could continue to be supported by

forecasts for extreme cold and the damaging effect that could cause in wheat rail logistics. Many have expected futures prices to decline and have been disappointed as they’ve continued to find support. We

expect some volatility over the coming weeks and months, influenced in large part by the severity of winter weather.

Facts on Flour

Gluten is developed from flour protein. When combined with water under mixing stress, the proteins in the flour will form gluten, which provides extensibility, elasticity and gas-retaining properties to yeast-leavened baked goods. The quantity of gluten is proportionate to the amount of protein in the flour, so gluten increases as the protein content increases.

Wheat flour is unique because it is the only cereal grain that possesses gluten-forming proteins – gliadin and glutenin. These comprise roughly 80 percent of the total wheat protein. The remaining proteins in flour are non-gluten forming and contribute nothing to dough strength.

The major flour types and their relative protein levels are: High Gluten …… 13.5-14.5% Pastry….. 8-10% Bread……………... 12-13% Cake……… 7-9% All Purpose …… 10-12%

To buy flour purely by a protein specification will not necessarily guarantee baking performance. Protein quality is a key component and will be discussed next week.

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

Bu

sh

el P

ric

e

Futures & Basis Markets

KC Future

Spring 15% Basis (from MarketFax No.1 Northern Spring)

Mpls Future

Winter 13% Basis (from MarketFax No.1 hard winter)

Flour pricing consists of a combination of Wheat futures prices and Basis Premium prices per bushel. Information contained on this chart closely resembles Gold Medal All Trumps, Mpls. Future + 15% Basis, and Harvest King, KC Future + 13% Basis. This chart does not reflect changes in millfeed values.

This Chart is meant to indicate Market Direction Only.

NOVEMBER 13, 2014

11.05.14

Crop Update/Neil Jones Food Company Valued Customers: California Tomatoes: Pack has now concluded for all Processors and official tonnage will finish at just over 14 MM tons for the 2014 season. Total global production for 2014 is forecast at 39.12 MM metric tons. The early start and late finish contributed to what will be the largest tomato crop in California history. It is important to note that the majority of this tonnage will go to industrial drums and bins with most of that going to paste. Global paste consumption continues to outpace supply and 2013 carryover paste inventories were extremely low. We anticipate domestic Foodservice inventories to be balanced for the year. Our 2014 total cost per ton increased 18% from $70.50 to $83. All Processors and Growers have significant concerns about the continued California drought conditions. Our growing region suffered the least rainfall in 163 years for 2014. Pending federal legislation, and the projected El Nino for the 2015 season, offer further cause for concern. Northwest Sweet Cherries: Washington, Oregon, Idaho, Montana and Utah have concluded the cherry harvest and we continue to be in a strong supply position with premium Dark Sweet Cherries and are offering truckload incentives. Northwest Bartlett Pears: As with last year, the high quality of fruit and fresh demand has made it difficult for processors to secure the tonnage needed to fulfill all contracts, bookings and domestic demand for the year. The season started with virtually no inventory on 6/10 fruit and very limited retail availability. Growers elected this year to move the majority of a near perfect crop to the fresh market to maximize their price per ton, leaving processors at least 30,000 tons short and with higher overall production costs to spread over fewer cases. Final tonnage numbers have not been calculated but we estimate total crop at about 117-120K tons. We have concluded our pack for the year and have allocated to contracted customers. Northwest Plums: Both the Willamette Valley and Yakima orchards had strong crops this year with nice quality fruit. We don’t always get enough or great quality fruit and we’re pleased that this year we have both! We are in a great inventory position with this exceptional crop and are accepting all bid solicitations and contracted opportunities for incremental volume now. Contact Meghan at extension 1139- (800.543.4356). Northwest Cranberries: Bandon, Oregon cranberries are currently giving us good production and are projected to be still in the 40-45 million pound range for the year. We are well stocked with 6/10 Cranberries and retail pack, both Whole Berry and Jellied. Component Cost Adjustments: Utilities: Labor/Obamacare: Tomatoes cost per ton: +18% Natural Gas: 18-20% Healthcare: + 15.9% Pears cost per ton: +10.3% Water: 15-20% Direct labor: +2.2% Ingredients: + 3-5%; Electricity: 15-20% Fiber: +1-3%

Tinplate: +3% Supply Chain: Intermodal Rates +2-3% Union Pacific Rail + 4-5% Warehousing +2-4% Thanks as always for your continued partnership in the year ahead!

Jon Jon K. Holt Global Sales & Marketing Director The Neil Jones Food Company

Pro News Market Update

“Produce from the Ground Up”

For the week of: November 16th 2014

Whipped Idaho® Potatoes with Basil Oil Photo by: someone Armand Lobato knows

Ingredients • Idaho potatoes, peeled • 2½ cups hot milk • ¾ cup extra virgin olive oil • ¾ cup melted butter • Salt and pepper to taste

For the Garnish: • Cracked black pepper • Basil Oil (see recipe) • Chives For the Basil Oil: • 2 bunches fresh basil • 2½ cups virgin olive oil

Directions

1. Steam or boil the potatoes in lightly salted water (if boiling, less milk may be needed) until for tender, approximately 30 minutes. Drain.

2. Place potatoes in mixing bowl and beat with electric mixer on “whip” or in a Kitchen Aid mixer with whip attachment. Slowly start beating potatoes, gradually adding the hot milk. When milk is mixed in, slowly drizzle in olive oil and follow the melted butter, salt and pepper. Garnish with pepper, Basil Oil and chives. Serve immediately. For the Basil Oil:

1. Plunge basil into an ample amount of boiling salted water for 20 to 30 seconds, and shock in lightly salted ice bath. Squeeze all water out thoroughly.

2. Put basil in standard blender and cover with ½ cup olive oil. Run blender on “high” and gradually add remaining olive oil as the mixture is blending.

3. Pour into glass bottle or jar and leave to decant for one day. Strain basil puree off through cheesecloth or fine sieve and store in refrigerator.

Recipe from

ASPARAGUS -- Although prices are level, the market is expected to climb later in November due to holiday demand. AVOCADOES -- The market is unchanged. Although Chilean stocks are tight, there is an ample supply of Mexican fruit. Large, 48-count avocados are limited, but there are plenty of 60- and 70-count supplies on the market. It is normal for fruit to take longer to ripen at this time of the season; skins may remain greener than normal when mature. BROCOLLI -- Supplies this week on broccoli will be very light and should remain lighter for the coming weeks as transition takes place to the Yuma/Brawley growing regions. The quality over the last few weeks continues to improve allowing for more harvest on a daily ba-sis. Quality is good with the exception of some with larg-er stalk size and a slightly knuckled appearance de-pending on the location. Expect the market to continue to be active over the next few weeks as Thanks-giving demand picks up with local broccoli being done for the season. CARROTS -- Availability has tightened for jumbo carrots in California as size and yield have declined the result of a slower growth cycle during the late season fall harvest at higher elevation (2,150 ft.) in the Cuyama Valley of Southern California. Prices will trend higher until the harvest returns to the Southern San Joaquin Valley (Bakersfield). CAULIFLOWER -- The raw quality has been improving for the past few weeks with less bruising by leaving jacket on. We do occasionally see some raw with ricing and sunburn scars. We have also made a few adjustments at the plant level toward handling the product more gently which should positively impact our shelf-life performance. The cauliflower supply will tighten up during the transition period into Yuma AZ. Quality issue may raise if we start seeing high moisture or rain enter at the field level. We will continue taking all precautions necessary to keep maintain the best available quality. CELERY -- Demand continues mostly steady. Oxnard is scheduled to start production next week with predicted good quality. Weights are ranging in the low to upper 50’s depending on shipper and field location. Quality is generally good with some bow, crack at node and light insect damage showing up. Pith has become an issue with some shippers and not a problem for others. Flagging continues to be an issue in some fields. LETTUCE -- While the ongoing drought in California is a major long-term concern, it is the short-term weather that has caused immediate concern. Ice-berg lettuce is in short sup-ply and prices have been much higher than normal for the past few weeks. Increased nighttime temperatures have caused let-tuce plants to grow at a much faster rate than expected, creating both quality and quantity problems. Tight availability and high prices will continue through the month of November. LEAF LETTUCE / ROMAINE – The market is slowly climbing. California supplies remain ample, but growers are moving to Yuma. Quality is very good, yet insect pressure and outer leaf decay are minor issues. PEPPERS/CUCUMBERS/SQUASH -- Peppers -- The market is moderately active. In the West, Coachella is finishing on green bell peppers, while new shippers are gradually entering the market in Nogales, with Mexico in full production by late November. Florida is now the primary district in the East. Red bells will be in extremely tight supply through early January. Oxnard is winding down, and in addition to fewer planted acres, Coachella is behind harvest schedules. Prices will continue to advance. Cucumbers -- A wide range in quality and price exists in Nogales, with rain damaged cucumbers selling at a discount to premium quality product. Florida has good supplies with good quality

Squash -- Zucchini & Yellow: Production in Florida is limited due to previous adverse weather conditions causing bloom drop. Production is below normal in Nogales, and the increased demand from Easter buyers is pushing prices higher for both zucchini and yellow squash. Acorn, Butternut, & Spaghetti – The hard freeze has hit the mid-west [22 in Jefferson city, MO with 1 – 3 inches of snow for week end.] You will not see the local squash any longer POTATOES -- All size cartons have tightened up as harvest is winding down, and growers are focusing on storing the remainder of their crop. Mid-range and smaller sizes are in better supply than larger size cartons. We are seeing a two-tiered pricing structure as both Burbank’s and Norkotah varieties are being shipped, with Burbank’s garnering higher returns. ONIONS -- Everything is undercover and it's a bumper crop. Due to excellent growing conditions quality and appearance is outstanding. The irony here is that unless there is a global hiccup- look for very promotable pricing for the year on Yellow onions. Good news for the consumer; bad news for the grower. Reds may have a bit of a boost due to demand from Mexico. White onion market steady on a very nice looking crop. Market is generally steady to lower. TOMATOES – Rounds: Markets will continue to be strong but should start coming down as the crops return to normal production over the next few weeks barring any additional weather events. Due to severe weather in all areas, the crops are producing lighter yields and weaker fruit. We expect that this will be the case over the next few weeks. As the weather returns to normal, crops should start to improve around late November or early December. Cherry and Grape: Palmetto/Ruskin, Florida: This area is just starting with mature greens, Roma’s, cherry tomatoes and grape tomatoes. This area won’t have any real volume until late November or early December. The area received a lot of rain on the early plantings which has caused the first pickings to be light. Roma: Roma tomatoes are scarce out of all growing regions. The Eastern shore does not plant an early fall crop of Romas. The rain in Mexico has knocked growers out of production for a several days; the summertime regional growing areas are winding down, leaving Central California to bare the brunt of the demand of the country.

APPLES -- Apple market continues to remain active. Domestic sales remain strong with the sale of large fruit being the focus of most shippers. There is still a concern about the lack of storage bins & rooms for the apples. The shortage in labor is also being discussed. With a record crop being harvested this year there is more storage rooms still being built. Gala apples are now being exported with other varieties just a few weeks away from meeting the required time in storage for export. STRAWBERRIES -- Cindy Jewell, director of marketing at Watsonville, Calif.-based California said “Strawberries are definitely tight right now in California, and we expect Florida and Mexico to kick in closer to Thanksgiving.” There are several reasons for the strong markets, Jewell said. A heat wave in early October brought fruit on faster than normal. In addition, workers have largely been occupied with plantings for the 2015 season, slowing down harvests. Finally, Jewell said, cooler weather in November is cutting into California volumes. “The fruit still looks great and sizing is consistent, there’s just not a lot to go around.”

CITRUS Lemons: Expect prices to inch down through December; new crop stocks are ample. Domestic quality is excellent: fruit is tart and juicy. Oranges: The California Navel market is easing; new crop supplies are increasing. Texas fruit is also on the market; this fruit is not as visually appealing, but flavor is sweet. Limes: I wonder, other than Creighton for his gin and tonic, does anyone else really care? Please advise. GRAPES – The grape movement is very good. Most shippers have little to no inventory on red seedless grapes. The predominant variety on green seedless is Autumn King, and they are moving very well at this time. The market is very firm on all varieties. It appears there is still a good amount of grapes to pick, but waiting for color and sugars. There are good supplies of Red Globes and fair supplies of Autumn Royals. MELONS -- Cantaloupe -- The current supply of melons overall is extremely short. The market is climbing fast on all sizes. The Westside district is done now. The desert is starting off extremely slow with rains last week hampering supplies. Quality is fair to good on the new crop from the desert. Honeydew: The Westside district has finished. The market is picking up on all sizes. Good demand along with lower supplies has created a rising market. Mexico and the desert have started and are heavy towards 4’s, 5’s and 6’s. Quality is fair to good. Watermelon -- Prices will remain high until supplies from mainland Mexico (into Nogales and South Texas) increase in late November. This fall’s hurricanes destroyed many crops. Ron Orr Executive Director Pro Mark [573] 680-1066 [email protected]

Market Watch . . . . . . .

Market Watch

November 14, 2014

Market Watch . . . . . . .

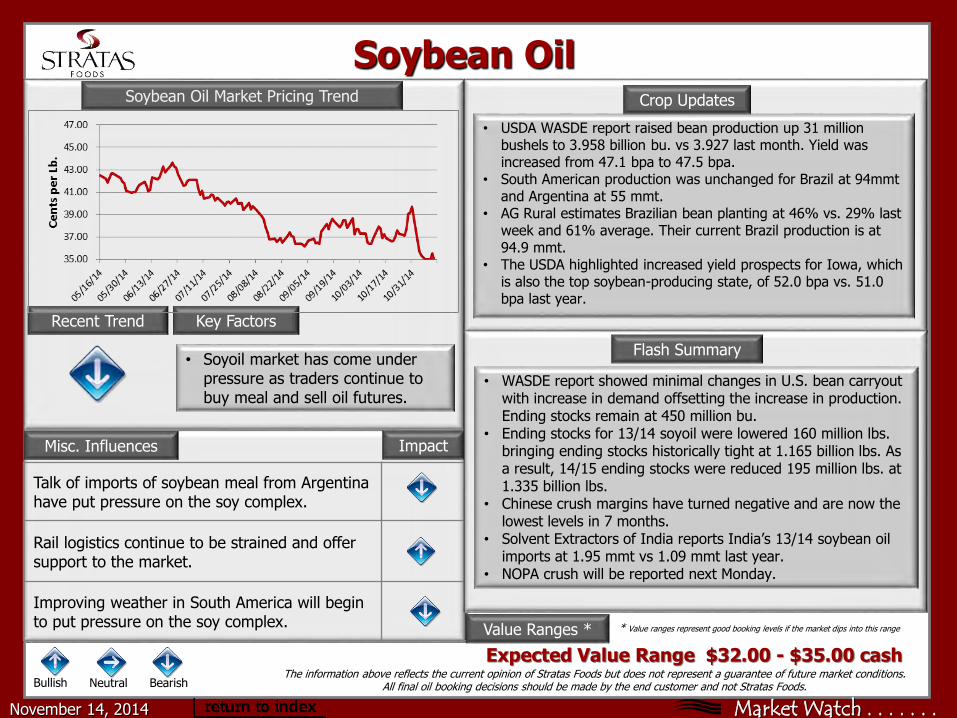

Talk of imports of soybean meal from Argentinahave put pressure on the soy complex.

Rail logistics continue to be strained and offer support to the market.

Improving weather in South America will begin to put pressure on the soy complex.

• Soyoil market has come under pressure as traders continue to buy meal and sell oil futures.

Soybean Oil

• USDA WASDE report raised bean production up 31 million bushels to 3.958 billion bu. vs 3.927 last month. Yield was increased from 47.1 bpa to 47.5 bpa.

• South American production was unchanged for Brazil at 94mmt and Argentina at 55 mmt.

• AG Rural estimates Brazilian bean planting at 46% vs. 29% last week and 61% average. Their current Brazil production is at 94.9 mmt.

• The USDA highlighted increased yield prospects for Iowa, which is also the top soybean-producing state, of 52.0 bpa vs. 51.0 bpa last year.

Crop Updates

Expected Value Range $32.00 - $35.00 cash

Soybean Oil Market Pricing Trend

Value Ranges *

The information above reflects the current opinion of Stratas Foods but does not represent a guarantee of future market conditions. All final oil booking decisions should be made by the end customer and not Stratas Foods.

* Value ranges represent good booking levels if the market dips into this range

Misc. Influences Impact

Key FactorsRecent Trend

November 14, 2014

BearishBullish Neutral

• WASDE report showed minimal changes in U.S. bean carryout with increase in demand offsetting the increase in production. Ending stocks remain at 450 million bu.

• Ending stocks for 13/14 soyoil were lowered 160 million lbs. bringing ending stocks historically tight at 1.165 billion lbs. As a result, 14/15 ending stocks were reduced 195 million lbs. at 1.335 billion lbs.

• Chinese crush margins have turned negative and are now the lowest levels in 7 months.

• Solvent Extractors of India reports India’s 13/14 soybean oil imports at 1.95 mmt vs 1.09 mmt last year.

• NOPA crush will be reported next Monday.

Flash Summary

Market Watch . . . . . . .

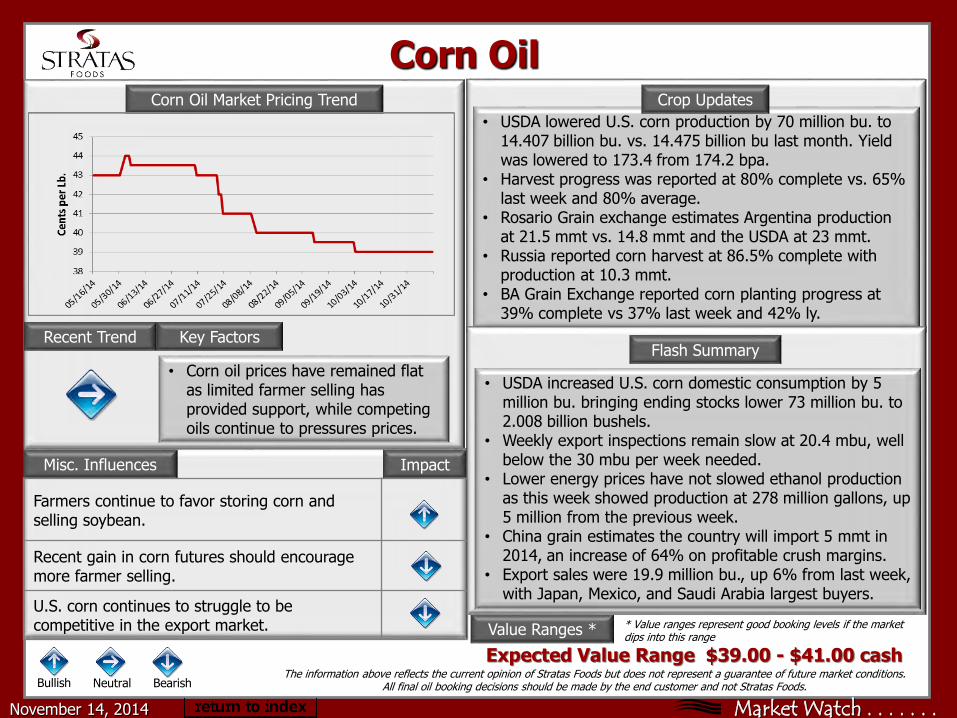

• Corn oil prices have remained flat as limited farmer selling has provided support, while competing oils continue to pressures prices.

Corn Oil

• USDA lowered U.S. corn production by 70 million bu. to 14.407 billion bu. vs. 14.475 billion bu last month. Yield was lowered to 173.4 from 174.2 bpa.

• Harvest progress was reported at 80% complete vs. 65% last week and 80% average.

• Rosario Grain exchange estimates Argentina production at 21.5 mmt vs. 14.8 mmt and the USDA at 23 mmt.

• Russia reported corn harvest at 86.5% complete with production at 10.3 mmt.

• BA Grain Exchange reported corn planting progress at 39% complete vs 37% last week and 42% ly.

Crop Updates

Expected Value Range $39.00 - $41.00 cash

Corn Oil Market Pricing Trend

Value Ranges *

The information above reflects the current opinion of Stratas Foods but does not represent a guarantee of future market conditions. All final oil booking decisions should be made by the end customer and not Stratas Foods.

* Value ranges represent good booking levels if the market dips into this range

Misc. Influences Impact

Key FactorsRecent Trend

• USDA increased U.S. corn domestic consumption by 5 million bu. bringing ending stocks lower 73 million bu. to 2.008 billion bushels.

• Weekly export inspections remain slow at 20.4 mbu, well below the 30 mbu per week needed.

• Lower energy prices have not slowed ethanol production as this week showed production at 278 million gallons, up 5 million from the previous week.

• China grain estimates the country will import 5 mmt in 2014, an increase of 64% on profitable crush margins.

• Export sales were 19.9 million bu., up 6% from last week, with Japan, Mexico, and Saudi Arabia largest buyers.

Flash Summary

BearishBullish Neutral

Farmers continue to favor storing corn and selling soybean.

Recent gain in corn futures should encourage more farmer selling.

U.S. corn continues to struggle to be competitive in the export market.

November 14, 2014

Market Watch . . . . . . .

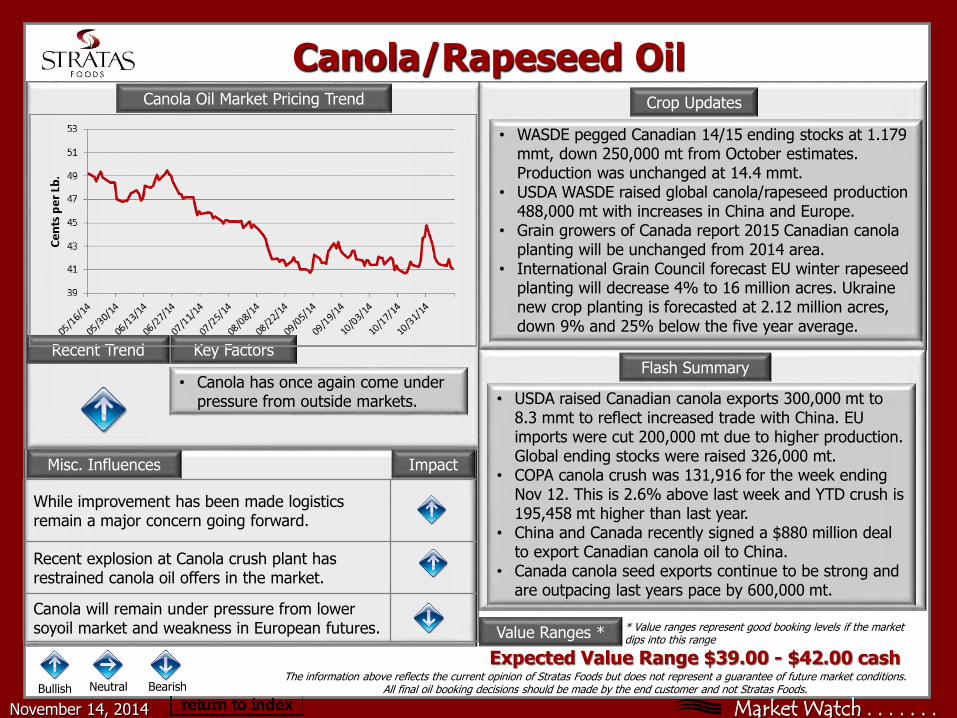

While improvement has been made logistics remain a major concern going forward.

Recent explosion at Canola crush plant has restrained canola oil offers in the market.

Canola will remain under pressure from lower soyoil market and weakness in European futures.

• Canola has once again come under pressure from outside markets.

Canola/Rapeseed Oil

• WASDE pegged Canadian 14/15 ending stocks at 1.179 mmt, down 250,000 mt from October estimates. Production was unchanged at 14.4 mmt.

• USDA WASDE raised global canola/rapeseed production 488,000 mt with increases in China and Europe.

• Grain growers of Canada report 2015 Canadian canola planting will be unchanged from 2014 area.

• International Grain Council forecast EU winter rapeseed planting will decrease 4% to 16 million acres. Ukraine new crop planting is forecasted at 2.12 million acres, down 9% and 25% below the five year average.

Crop Updates

Expected Value Range $39.00 - $42.00 cash

Canola Oil Market Pricing Trend

Value Ranges *

The information above reflects the current opinion of Stratas Foods but does not represent a guarantee of future market conditions. All final oil booking decisions should be made by the end customer and not Stratas Foods.

* Value ranges represent good booking levels if the market dips into this range

Misc. Influences Impact

Key FactorsRecent Trend

• USDA raised Canadian canola exports 300,000 mt to 8.3 mmt to reflect increased trade with China. EU imports were cut 200,000 mt due to higher production. Global ending stocks were raised 326,000 mt.

• COPA canola crush was 131,916 for the week ending Nov 12. This is 2.6% above last week and YTD crush is 195,458 mt higher than last year.

• China and Canada recently signed a $880 million deal to export Canadian canola oil to China.

• Canada canola seed exports continue to be strong and are outpacing last years pace by 600,000 mt.

Flash Summary

BearishBullish Neutral

November 14, 2014

Market Watch . . . . . . .

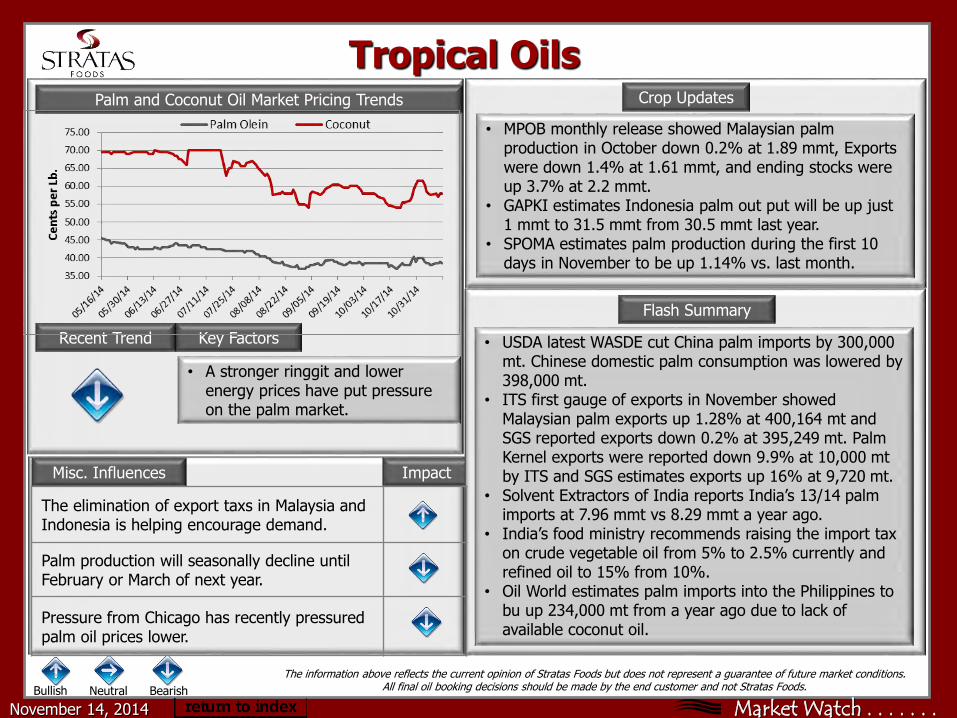

• A stronger ringgit and lower energy prices have put pressure on the palm market.

Tropical Oils

• MPOB monthly release showed Malaysian palm production in October down 0.2% at 1.89 mmt, Exports were down 1.4% at 1.61 mmt, and ending stocks were up 3.7% at 2.2 mmt.

• GAPKI estimates Indonesia palm out put will be up just 1 mmt to 31.5 mmt from 30.5 mmt last year.

• SPOMA estimates palm production during the first 10 days in November to be up 1.14% vs. last month.

Crop UpdatesPalm and Coconut Oil Market Pricing Trends

The information above reflects the current opinion of Stratas Foods but does not represent a guarantee of future market conditions. All final oil booking decisions should be made by the end customer and not Stratas Foods.

Misc. Influences Impact

Key FactorsRecent Trend

BearishBullish Neutral

The elimination of export taxs in Malaysia and Indonesia is helping encourage demand.

Palm production will seasonally decline untilFebruary or March of next year.

Pressure from Chicago has recently pressured palm oil prices lower.

November 14, 2014

• USDA latest WASDE cut China palm imports by 300,000 mt. Chinese domestic palm consumption was lowered by 398,000 mt.

• ITS first gauge of exports in November showed Malaysian palm exports up 1.28% at 400,164 mt and SGS reported exports down 0.2% at 395,249 mt. Palm Kernel exports were reported down 9.9% at 10,000 mt by ITS and SGS estimates exports up 16% at 9,720 mt.

• Solvent Extractors of India reports India’s 13/14 palm imports at 7.96 mmt vs 8.29 mmt a year ago.

• India’s food ministry recommends raising the import tax on crude vegetable oil from 5% to 2.5% currently and refined oil to 15% from 10%.

• Oil World estimates palm imports into the Philippines to bu up 234,000 mt from a year ago due to lack of available coconut oil.

Flash Summary