Embed Size (px)

Citation preview

Market development strategy

September 2009

Market development strategy NHS Northamptonshire 1

NHS Northamptonshire is committed to providing the highest levels of healthcare for our population. This can only be achieved through a detailed and comprehensive understanding of commissioned services and a commitment to contract with only those providers who commit to delivering exceptional clinical outcomes.

I am therefore delighted to present NHS Northamptonshire’s Market Development Strategy, a document that describes the approach this organisation will adopt in the analysis and management of the health system in our county. This strategy will ensure that a systematic approach is taken to understand the needs of our population and to determine future market priorities. It will inform our investment decisions in future years as we drive further improvements in quality outcomes, choice, and service redesign. We will work with a range of responsive and high quality providers to deliver our ambition. These providers could be existing organisations who share our commitment to delivering the very highest standards of healthcare in the county, or new market entrants.

Where new services are needed we will deliver these through a clear and transparent procurement process that ensures compliance with legal and policy requirements.

Our strategy represents a new approach to system management for NHS Northamptonshire which can be summarised as:

A renewed commitment to continuous and yymeaningful engagement with patients and the public

A redesigned approach to stimulating the market yyto secure the highest quality services whilst fostering a partnership approach to service improvement

A new approach to the procurement processes yyfor clinical services that will result in contracts which clearly specify quality standards and outcomes

I am excited by this new direction for the management of services in the county and I commend this Strategy to you

John Parkes Chief Executive NHS Northamptonshire

Foreword

Market development strategy NHS Northamptonshire 3

ContentsIntroduction and strategic purpose 4

Setting the context 5

Market Development as Part of World Class Commissioning

7

Northamptonshire context 8

A systematic and transparent approach to Market Analysis

12

NHS Northamptonshire’s market priorities 16

Prioritisation outcome 17

Programme interdependencies and risks 27

Turning Strategy In To Action – Next Steps 33

Appendix A List of current providers from whom NHS Northamptonshire commissions services (2007/08)

36

Appendix B Defining health care markets

39

Appendix C NHS Northamptonshire’s Market Taxonomy

40

Appendix D Example of Potential Provider Dialogue script

42

4 NHS Northamptonshire Market development strategy

This Market Development Strategy for NHS Northamptonshire is central to its emergence as a PCT at the leading-edge of World Class Commissioning competence (see figure 1 below). The objectives of the strategy are to:

Describe the systematic and transparent approach yythat NHS Northamptonshire has developed to enable the analysis, prioritisation and intervention within the healthcare markets it manages;

Identify the priority healthcare markets that NHS yyNorthamptonshire will focus on developing over the short, medium and longer term in order that better quality and improved value for money are delivered for the local population;

Outline the governance framework within which yyNHS Northamptonshire will manage and monitor healthcare markets, and in so doing continue its development as a world class commissioner; and

Recognise the interdependencies and dependencies yythat exist in relation to market management and other essential programmes that contribute to delivering our vision of:

Reducing the overall mortality rate y—within Northamptonshire;Helping people live healthier lives, reducing y—inequalities and improving their wellbeing; andImproving patient satisfaction with NHS services.y—

Introduction and strategic purpose

Healthneed

Individualrisk

register

Causalpathways

Personalisedtargeted

intervention

KPIs

Healthoutcomes

Carepathwayreview

ROI

TheIndividual

Figure 1: World Class Commissioning: putting patients at the centre of all that we do. ROI = return on investment; KPI = Key performance indicators

Market development strategy NHS Northamptonshire 5

Setting the context

National contextThe existing NHS policy framework locates the application of market principles at the centre of the current reform programme. The application of market principles to healthcare, however, needs to recognise the inherent complexities not only of the services that are offered across a range of providers, but also those that exist in relation to different service user requirements and different commissioner requirements.

PCTs are therefore required to transition from a traditional commissioning model that has historically focused on contracting, to an effective market management model where commissioners work with healthcare partners to secure the delivery of higher quality and better value for money services (summarised in figure 2 below).

Any market-based reforms will clearly need to be considered against the Principles and Rules for Co-operation and Competition (2007)1 and Necessity - not nicety: A new commercial operating model for the NHS and Department of Health (2009)2, requiring NHS Northamptonshire to ensure that not only the Board but also officers of the PCT fully understand the context within which change will need to be managed.

The way in which healthcare is both planned and delivered is changing and NHS Northamptonshire is committed to being at the forefront of these changes. High Quality Care for All (2008)3 sets bold and ambitious plans for the future shape of NHS funded services. Greater public and patient involvement in the design and evaluation of services are obligations that are set out in section 242 of the NHS Act 2006. Alongside transparent, non-discriminatory, and proportionate procurement activity we will, among other activities, contribute to the delivery of better quality services and better use of the resources made available to the PCT.

1 Department of Health (2007) The NHS in England: The operating framework for 2008/9 Annex D – Principles and rules for co-operation and competition, Department of Health2 Department of Health (2009) Necessity – not nicety: A new commercial operating model for the NHS and Department of Health3 Lord Darzi (2008) High quality care for all: NHS Next Stage Review final report

Figure 2: Working towards Healthcare Partnerships

6 NHS Northamptonshire Market development strategy

The way in which contracting authorities interact locally and regionally will be influenced by the likely financial context in which the NHS will be operating. David Nicholson has recently signalled that £15-20 billion will need to be saved over the next comprehensive spending review period (source: NHS Chief Executive’s Annual Report 2008/09).

By establishing a clear strategy underpinned by detailed and robust delivery plans, NHS Northamptonshire will shape the future of healthcare delivery and in so doing, strengthen its standing as a world class commissioner.

Market development strategy NHS Northamptonshire 7

Recipients of this strategy will clearly see the "product development" elements of market theory and practice strongly emphasised.

Elements of broader market reform run through the strategy but these must be seen in the context of the whole commissioning cycle and World Class Commissioning competencies. Together these frameworks provide the basis for prioritisation, harnessing of new technology and its market implications, stakeholder and supplier engagement and ultimately procurement and contract management.

Figure 3 illustrates the commissioning cycle and how the process of service review and prioritisation illustrated within this strategy fits within the wider context of service and product change. The blue “call out” boxes within the diagram illustrate the elements of market reform that run through the whole cycle, aside from the clear focus on product development that this strategy provides.

Market Development as Part of World Class Commissioning

Figure 3:

8 NHS Northamptonshire Market development strategy

Northamptonshire context

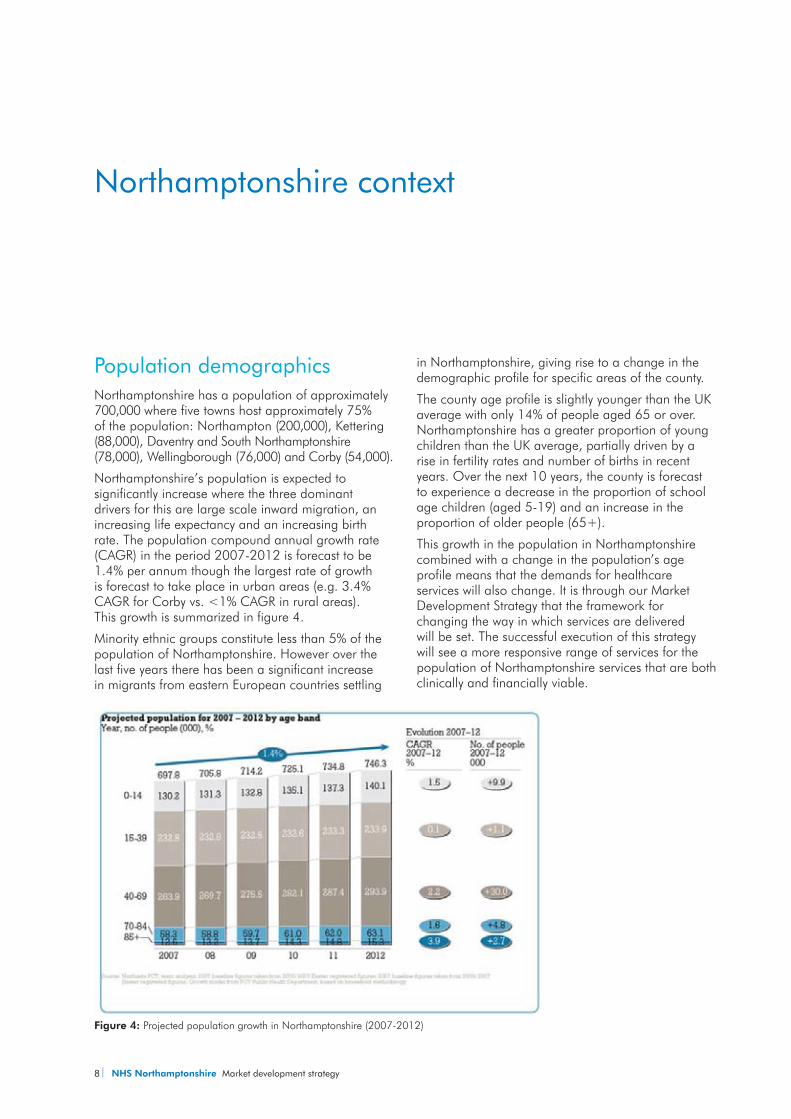

Population demographicsNorthamptonshire has a population of approximately 700,000 where five towns host approximately 75% of the population: Northampton (200,000), Kettering (88,000), Daventry and South Northamptonshire (78,000), Wellingborough (76,000) and Corby (54,000).

Northamptonshire’s population is expected to significantly increase where the three dominant drivers for this are large scale inward migration, an increasing life expectancy and an increasing birth rate. The population compound annual growth rate (CAGR) in the period 2007-2012 is forecast to be 1.4% per annum though the largest rate of growth is forecast to take place in urban areas (e.g. 3.4% CAGR for Corby vs. <1% CAGR in rural areas). This growth is summarized in figure 4.

Minority ethnic groups constitute less than 5% of the population of Northamptonshire. However over the last five years there has been a significant increase in migrants from eastern European countries settling

in Northamptonshire, giving rise to a change in the demographic profile for specific areas of the county.

The county age profile is slightly younger than the UK average with only 14% of people aged 65 or over. Northamptonshire has a greater proportion of young children than the UK average, partially driven by a rise in fertility rates and number of births in recent years. Over the next 10 years, the county is forecast to experience a decrease in the proportion of school age children (aged 5-19) and an increase in the proportion of older people (65+).

This growth in the population in Northamptonshire combined with a change in the population’s age profile means that the demands for healthcare services will also change. It is through our Market Development Strategy that the framework for changing the way in which services are delivered will be set. The successful execution of this strategy will see a more responsive range of services for the population of Northamptonshire services that are both clinically and financially viable.

Figure 4: Projected population growth in Northamptonshire (2007-2012)

Market development strategy NHS Northamptonshire 9

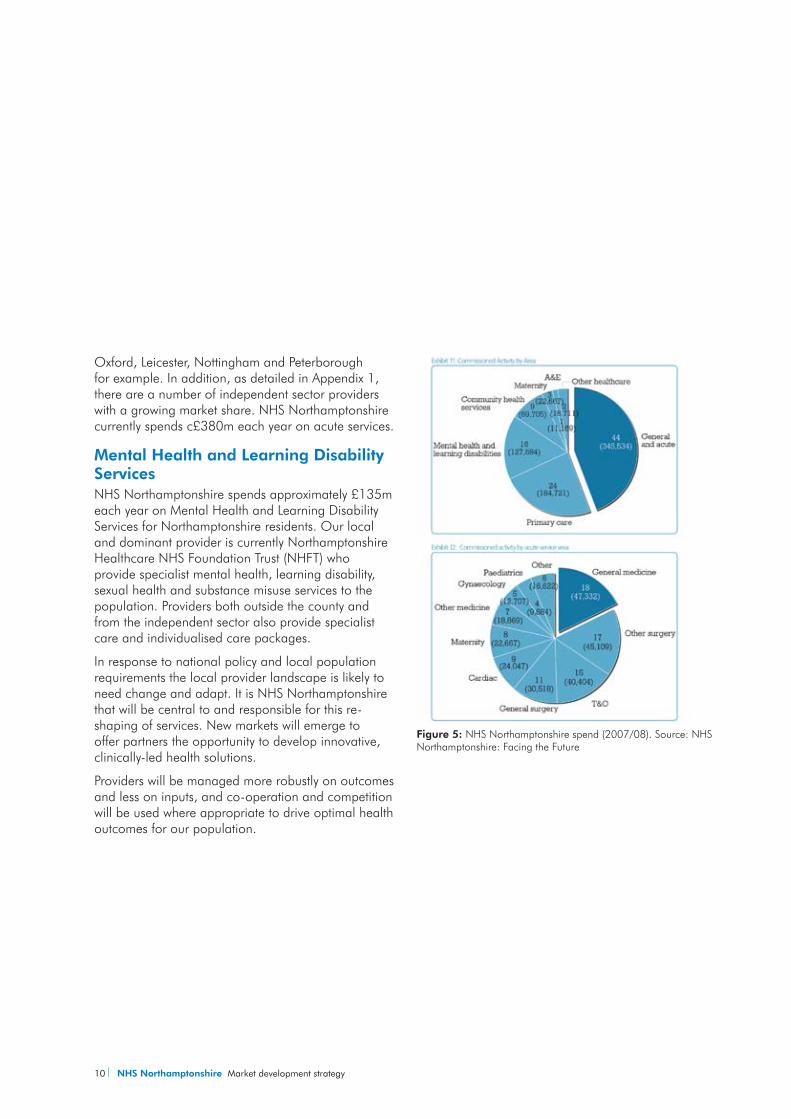

Local providersNHS Northamptonshire commissions services from a range of providers (see appendix 1), spending in excess of £900 million each year, and in several cases commissions collaboratively with Northamptonshire County Council (for example some Mental Health services) and East Midlands Specialist Commissioning Group.

Primary CareThe county currently has 83 GP surgeries, 84 dental practices, 115 pharmacies, and 59 optical premises, attracting approximately a quarter of NHS Northamptonshire’s total annual spend (c£220m).

Community-based careThe majority of community services are currently provided by the PCT’s Provider Services where NHS Northamptonshire spends around 9% of its total budget per annum (c£70 million).

Acute CareAcute care is currently provided by Kettering General Hospital (KGH) and Northampton General Hospital (NGH), as well as in a number of smaller community hospitals. Essentially KGH serves the population in the north of the county while NGH serves the centre and south of the county. Patients also access providers outside of the county at Milton Keynes,

10 NHS Northamptonshire Market development strategy

Oxford, Leicester, Nottingham and Peterborough for example. In addition, as detailed in Appendix 1, there are a number of independent sector providers with a growing market share. NHS Northamptonshire currently spends c£380m each year on acute services.

Mental Health and Learning Disability ServicesNHS Northamptonshire spends approximately £135m each year on Mental Health and Learning Disability Services for Northamptonshire residents. Our local and dominant provider is currently Northamptonshire Healthcare NHS Foundation Trust (NHFT) who provide specialist mental health, learning disability, sexual health and substance misuse services to the population. Providers both outside the county and from the independent sector also provide specialist care and individualised care packages.

In response to national policy and local population requirements the local provider landscape is likely to need change and adapt. It is NHS Northamptonshire that will be central to and responsible for this re-shaping of services. New markets will emerge to offer partners the opportunity to develop innovative, clinically-led health solutions.

Providers will be managed more robustly on outcomes and less on inputs, and co-operation and competition will be used where appropriate to drive optimal health outcomes for our population.

Figure 5: NHS Northamptonshire spend (2007/08). Source: NHS Northamptonshire: Facing the Future

Market development strategy NHS Northamptonshire 11

Drawing on an established and tested framework that is set out in section 2, NHS Northamptonshire has already begun the process of identifying the priority areas for immediate action (see section 3).

Section 4 then sets out the governance surrounding these market-based reforms and identifies the interdependencies that exist, both in terms of current (Transforming Community Services for example) and future programmes of work.

12 NHS Northamptonshire Market development strategy

A systematic and transparent approach to Market Analysis

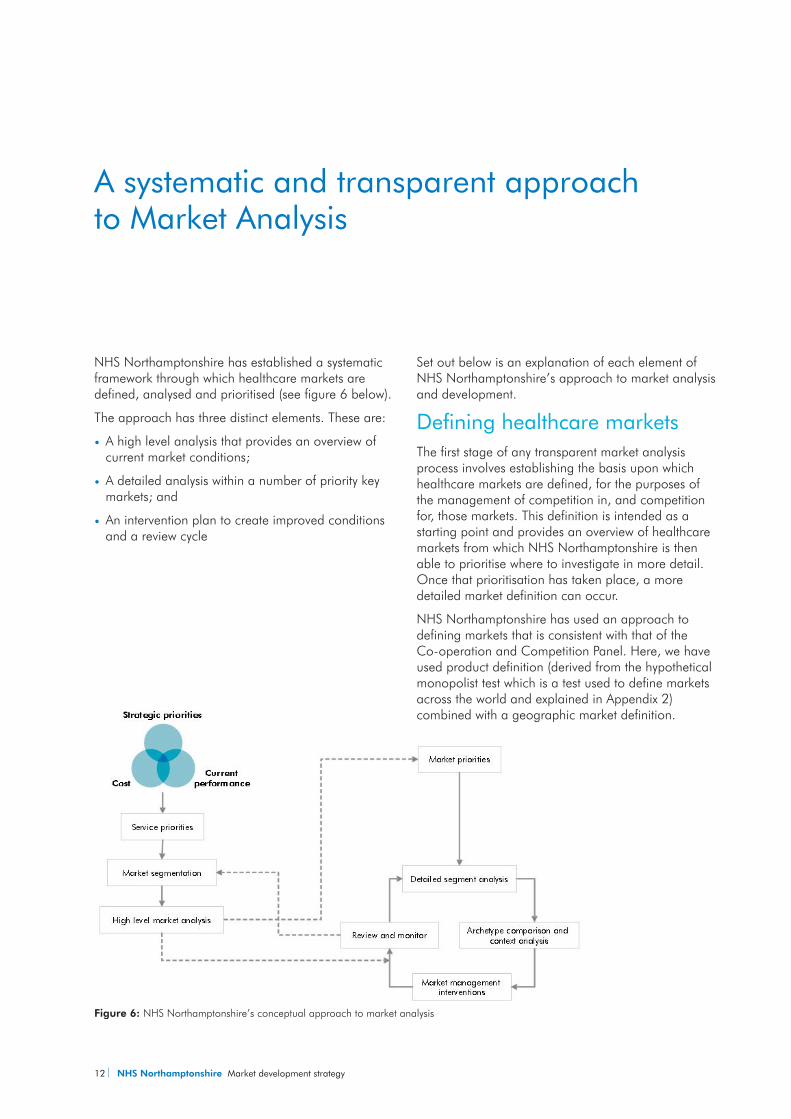

NHS Northamptonshire has established a systematic framework through which healthcare markets are defined, analysed and prioritised (see figure 6 below).

The approach has three distinct elements. These are:

A high level analysis that provides an overview of yycurrent market conditions;

A detailed analysis within a number of priority key yymarkets; and

An intervention plan to create improved conditions yyand a review cycle

Set out below is an explanation of each element of NHS Northamptonshire’s approach to market analysis and development.

Defining healthcare marketsThe first stage of any transparent market analysis process involves establishing the basis upon which healthcare markets are defined, for the purposes of the management of competition in, and competition for, those markets. This definition is intended as a starting point and provides an overview of healthcare markets from which NHS Northamptonshire is then able to prioritise where to investigate in more detail. Once that prioritisation has taken place, a more detailed market definition can occur.

NHS Northamptonshire has used an approach to defining markets that is consistent with that of the Co-operation and Competition Panel. Here, we have used product definition (derived from the hypothetical monopolist test which is a test used to define markets across the world and explained in Appendix 2) combined with a geographic market definition.

Figure 6: NHS Northamptonshire’s conceptual approach to market analysis

Market development strategy NHS Northamptonshire 13

Product market definitionThe definition of “a market” does not imply that competition is the only, or the most appropriate, way in which particular objectives can be met. The definition of NHS healthcare markets is inevitably influenced by current structures and behaviours.

In particular, the prominent divide between primary and secondary care (e.g. in the contexts of commissioning and referrals) has a strong influence over the definition of healthcare markets today.

The theory and detail behind product definition is described in Appendix 2.

Defining healthcare markets in this way has enabled NHS Northamptonshire to analyse the current level of quality and competition within each market and to locate markets within the relevant care pathways and strategic programmes, recognising the extent and importance of market interdependencies.

Geographical market definitionThe geography of a market is defined by an understanding as to how far a patient is willing to travel to receive care. This will vary by the patient need in question and by the nature of the service. Through using the travel times (listed in appendix 3) outlined in our Facing the Future document we have established travel times for each ‘product’ market that has been defined.

Ensuring the market definitions remain currentNHS Northamptonshire has identified an initial 90 markets (these are set out in Appendix 3). Any ‘future’ market definitions will likely be influenced by three key factors:

Settingyy – as the current divide between community, primary and secondary care is broken down further, the size and scope of product markets will also change;

Informationyy – as the information available to the public, patients and their advisers (e.g. GPs) and commissioners changes, so too will the size and scope of product markets; and

Flexibilityyy – of staff and physical resources: as training and technology change, so too will the size and scope of product markets.

The Strategy and System Management Directorate will therefore, review the taxonomy to ensure currency on an annual basis and at the start of the cyclical high level market analysis refresh (April to June).

High Level Analysis of NHS Northamptonshire’s Markets NHS Northamptonshire has completed a high level analysis of each market. The purpose of this analysis is to provide an overview of the current performance and determine where competition in or for the market may be appropriate. Competition in the market is where providers compete to attract patients directly whereas; competition for the market is where providers compete to attract commissioners.

This analysis has considered service quality and four dimensions of competition (choice, concentration, switching and rivalry) where the following sections describe more specifically how each element has been assessed.

QualityThe metric(s) used to assess quality differ by market. However, NHS Northamptonshire has used the categories set out below (where the data permits), which are based on those identified by the Organisation for Economic Co-Operation and Development (OECD)5 as the basis for an assessment of quality:

Effectivenessyy – degree of achieving desirable outcomes

14 NHS Northamptonshire Market development strategy

Safetyyy – degree to which adverse outcomes are avoided, prevented and ameliorated

Responsivenessyy – how patients needs/wants are met

Accessibilityyy – ease with which services are accessed (physical, financial or psychological)

Equityyy – extent to which the service deals with people fairly or the distribution of healthcare benefits among the population

Efficiencyyy – optimal use of available resource to deliver maximum benefit(s)

Where data is limited or unavailable, NHS Northamptonshire will seek to understand the dimensions of quality using either proxy or qualitative indices, recognising the associated limitations.5 OECD (2006) , Health Care Quality Indicators Project Conceptual Framework Paper

Theoretical choiceTheoretical choice (the number of providers of a specific product or service within the geographical market) is defined by a particular travel time. Relevant travel times have been applied to each market (e.g. 10 minutes for Primary Care GP services).

Choice is now a right that patients have. This measure simply represents a theoretical level of choice – it does not capture whether or not these choices are taken up by many or even any patients. However, it allows NHS Northamptonshire to consider whether an appropriate level of choice exists within each market. For non-elective markets, access rather than theoretical choice has been considered.

The levels of choice observed are likely to vary by market archetype. For example, the amount of choice available within patient-led choice markets (e.g. Orthopaedics) is likely to be much greater than that observed within non-elective or highly specialised markets (e.g. bariatric surgery).

ConcentrationThe level of concentration has been evaluated to allow NHS Northamptonshire to determine the structure of each of the markets. Defined by the market shares of the providers serving the population, a common summary measure of the market shares for all providers serving a population is the Herfindahl Hirschman Index (HHI).

The HHI ranges from 10,000 for a monopoly market (with one provider having 100% market share) to 100 for a market with a large number of very small providers, where UK competition authorities define concentration at two levels:

A HHI over 1,000 indicates that a market is yyconcentrated

A HHI over 1,800 indicates that a market is highly yyconcentrated

Concentration within healthcare markets in England is typically much higher than the levels considered ‘high’ by competition authorities. Therefore, NHS Northamptonshire will consider levels of concentration alongside quality and other economic measures before drawing specific conclusions about the state of the any given market.

Again, the level of concentration observed within local markets is likely to vary between the different types of market that exist. For example, it would be unsurprising to see that the level of concentration for bariatric surgery (where the number of providers is relatively low and it typically considered a regional service) being much higher than that seen in the General Practice market.

The important consideration, particularly where higher levels of concentration are observed, will be the level of quality experienced by patients (and in some cases, the price paid by commissioners).

Market development strategy NHS Northamptonshire 15

Where data is not readily available, NHS Northamptonshire will use approximate activity levels to develop a considered view on the current market shares of providers.

Patient switchingNHS Northamptonshire has defined switching as the number of people moving from one provider to another in a given time period (e.g. over the course of a year). In some healthcare markets this can be observed directly, for example most acute services have data that can provide values of switching levels. In others it has been necessary to approximate by looking at the change in market share of the providers, which may be the result of patients choosing to switch from one provider to another.

Switching provides the stimulus for providers to improve or maintain the quality of their service. Where the quality of services provided is uneven (i.e. some providers offer poorer services than others) a dynamic market would be characterised by switching from poor providers to better ones. However, patients (and their general practitioners) need reliable information upon which to base any switching decision.

An alternative measure of switching involves tracking changes in individual patient choices, capturing patients who move between hospitals. This ‘gross switching’ is particularly difficult to achieve currently. However, as the quality and availability of patient level information improves, and as NHS Northamptonshire and its providers engage effectively with patients, so analysis can move away from ‘net switching’ (the difference between the number of patients switching to a provider and the number of patients switching away) to gross switching’ measures.

This will also provide NHS Northamptonshire with the opportunity to monitor whether patients switch within their care pathway, for example using a different provider of physiotherapy to that which provided their elective orthopaedic operation.

RivalryRivalry is the degree of actual or potential entry into and exit from a market. Rivalry is a useful measure of competition because competitive markets are characterised by real entry and exit as well as the threat of entry and exit.

The degree of rivalry is influenced by factors such as the extent of any barriers of entry (such as fixed costs or the ability to access patients, obtain a contract etc). For example, low barriers to entry could be considered to exist where set -up costs are relatively low. Conversely where barriers to entry are high, the market may need to have highly skilled specialised staff.

In practice, in healthcare, rivalry is generally measured qualitatively through interviews with both current and potential providers. While the observation regarding the level of barriers to entry and exit may be valid, NHS Northamptonshire will consider whether the barriers to entry and exit can be addressed, rather than simply considering them a ‘fixed’ variable.

The results of our high level analysisFollowing the completion of the high level analysis, NHS Northamptonshire has considered the potential range of levers that can be applied to address the specific issues identified within each analysis. However, and more fundamentally, the analysis itself has allowed NHS Northamptonshire to complete a prioritisation exercise, detailed in the section below, which has identified the markets within which phased market reform is necessary over a short, medium and longer term timescale.

16 NHS Northamptonshire Market development strategy

NHS Northamptonshire’s market priorities

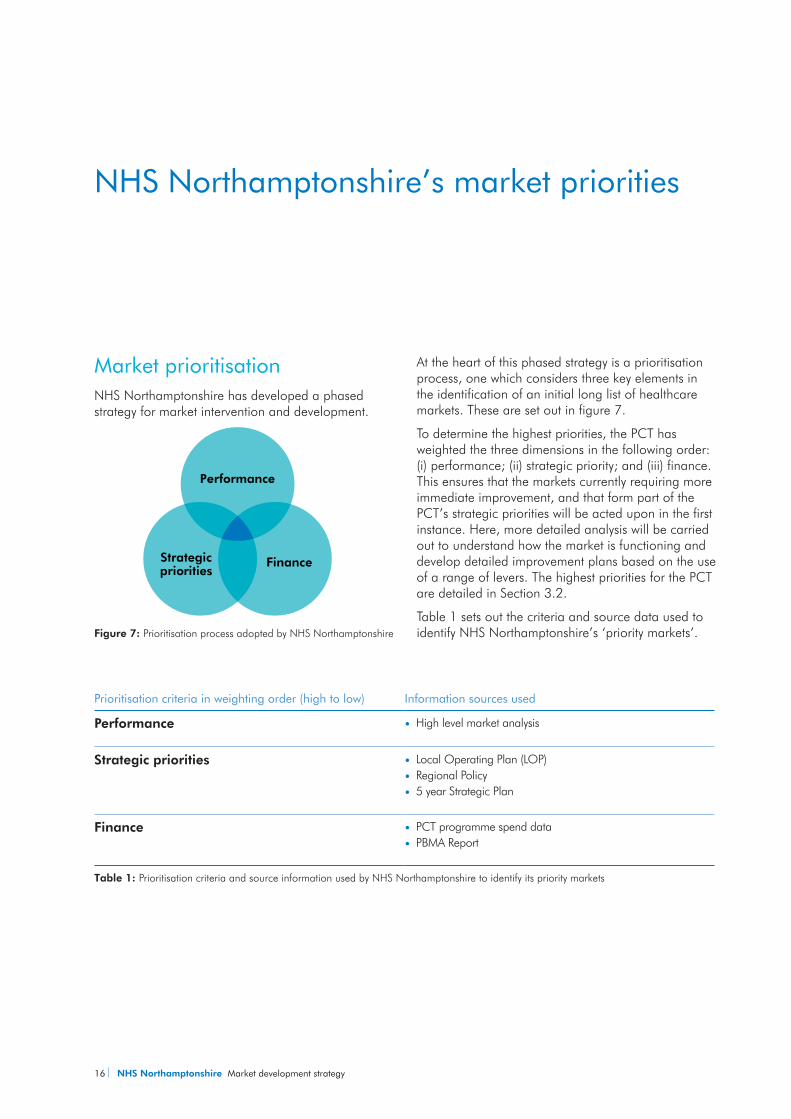

Market prioritisationNHS Northamptonshire has developed a phased strategy for market intervention and development.

At the heart of this phased strategy is a prioritisation process, one which considers three key elements in the identification of an initial long list of healthcare markets. These are set out in figure 7.

To determine the highest priorities, the PCT has weighted the three dimensions in the following order: (i) performance; (ii) strategic priority; and (iii) finance. This ensures that the markets currently requiring more immediate improvement, and that form part of the PCT’s strategic priorities will be acted upon in the first instance. Here, more detailed analysis will be carried out to understand how the market is functioning and develop detailed improvement plans based on the use of a range of levers. The highest priorities for the PCT are detailed in Section 3.2.

Table 1 sets out the criteria and source data used to identify NHS Northamptonshire’s ‘priority markets’.

Prioritisation criteria in weighting order (high to low) Information sources used

Performance High level market analysisyy

Strategic priorities Local Operating Plan (LOP)yyRegional Policyyy5 year Strategic Planyy

Finance PCT programme spend datayyPBMA Reportyy

Table 1: Prioritisation criteria and source information used by NHS Northamptonshire to identify its priority markets

Performance

FinanceStrategicpriorities

Figure 7: Prioritisation process adopted by NHS Northamptonshire

Market development strategy NHS Northamptonshire 17

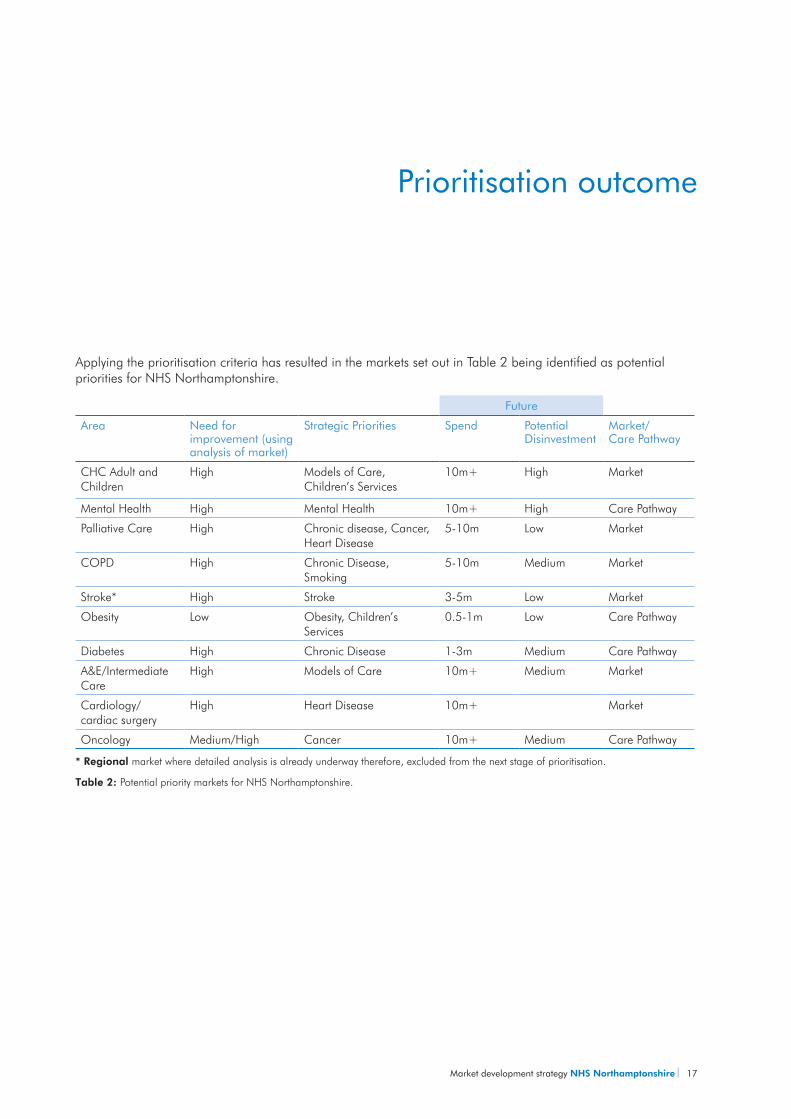

Applying the prioritisation criteria has resulted in the markets set out in Table 2 being identified as potential priorities for NHS Northamptonshire.

Future

Area Need for improvement (using analysis of market)

Strategic Priorities Spend Potential Disinvestment

Market/ Care Pathway

CHC Adult and Children

High Models of Care, Children’s Services

10m+ High Market

Mental Health High Mental Health 10m+ High Care Pathway

Palliative Care High Chronic disease, Cancer, Heart Disease

5-10m Low Market

COPD High Chronic Disease, Smoking

5-10m Medium Market

Stroke* High Stroke 3-5m Low Market

Obesity Low Obesity, Children’s Services

0.5-1m Low Care Pathway

Diabetes High Chronic Disease 1-3m Medium Care Pathway

A&E/Intermediate Care

High Models of Care 10m+ Medium Market

Cardiology/ cardiac surgery

High Heart Disease 10m+ Market

Oncology Medium/High Cancer 10m+ Medium Care Pathway

* Regional market where detailed analysis is already underway therefore, excluded from the next stage of prioritisation.

Table 2: Potential priority markets for NHS Northamptonshire.

Prioritisation outcome

18 NHS Northamptonshire Market development strategy

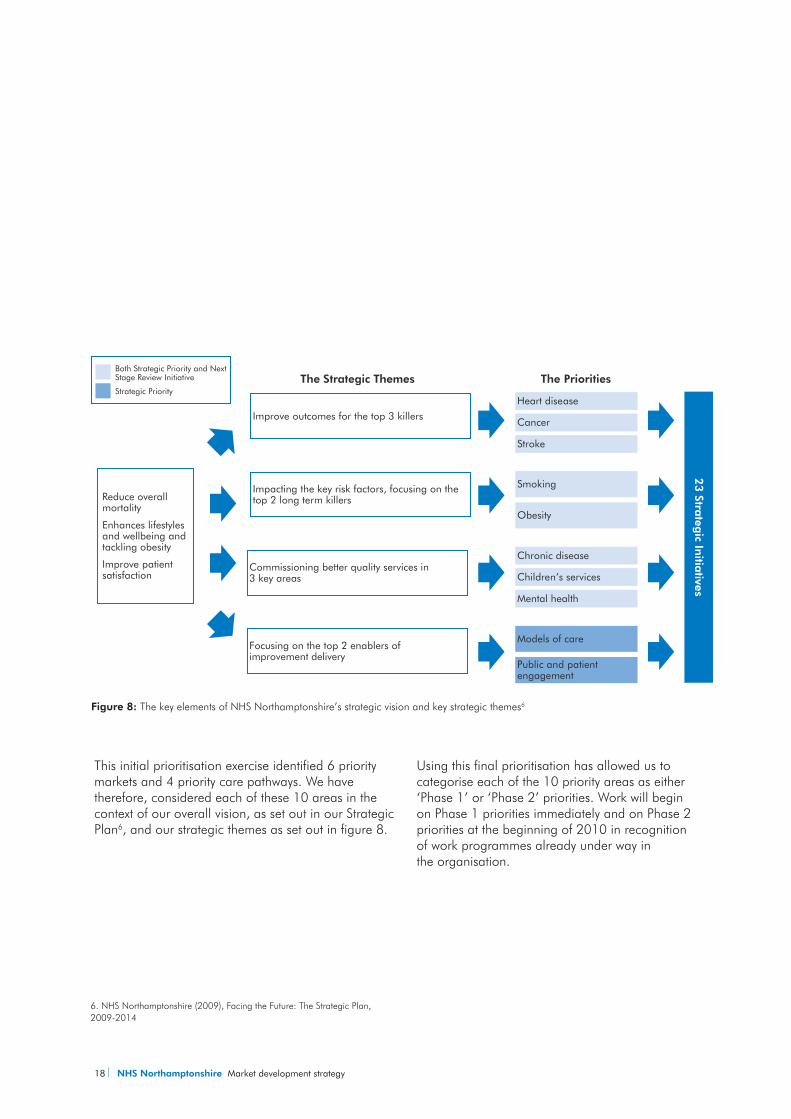

This initial prioritisation exercise identified 6 priority markets and 4 priority care pathways. We have therefore, considered each of these 10 areas in the context of our overall vision, as set out in our Strategic Plan6, and our strategic themes as set out in figure 8.

Using this final prioritisation has allowed us to categorise each of the 10 priority areas as either ‘Phase 1’ or ‘Phase 2’ priorities. Work will begin on Phase 1 priorities immediately and on Phase 2 priorities at the beginning of 2010 in recognition of work programmes already under way in the organisation.

Figure 8: The key elements of NHS Northamptonshire’s strategic vision and key strategic themes6

6. NHS Northamptonshire (2009), Facing the Future: The Strategic Plan, 2009-2014

Reduce overall mortality

Enhances lifestyles and wellbeing and tackling obesity

Improve patient satisfaction

Improve outcomes for the top 3 killers

Commissioning better quality services in 3 key areas

Focusing on the top 2 enablers of improvement delivery

Impacting the key risk factors, focusing on the top 2 long term killers

Heart disease

Cancer

Stroke

Chronic disease

Children’s services

Mental health

Smoking

Obesity

Models of care

Public and patient engagement

23 Stra

tegic In

itiatives

The Strategic Themes The PrioritiesBoth Strategic Priority and Next Stage Review Initiative

Strategic Priority

Market development strategy NHS Northamptonshire 19

Phase 1 priorities Phase 2 priorities

Obesity A&E / Intermediate Care

Palliative Care Oncology

COPD Cardiology/cardiac surgery

Mental Health

Diabetes

CHC (Adult and Children)

Table 3: Phase 1 and Phase 2 priority markets for NHS Northamptonshire

Market analysis is not an end in itself; it exists to guide our action. While the analysis identifies areas where action should be taken together with a desired direction of travel, it is market management interventions themselves that will deliver the required changes.

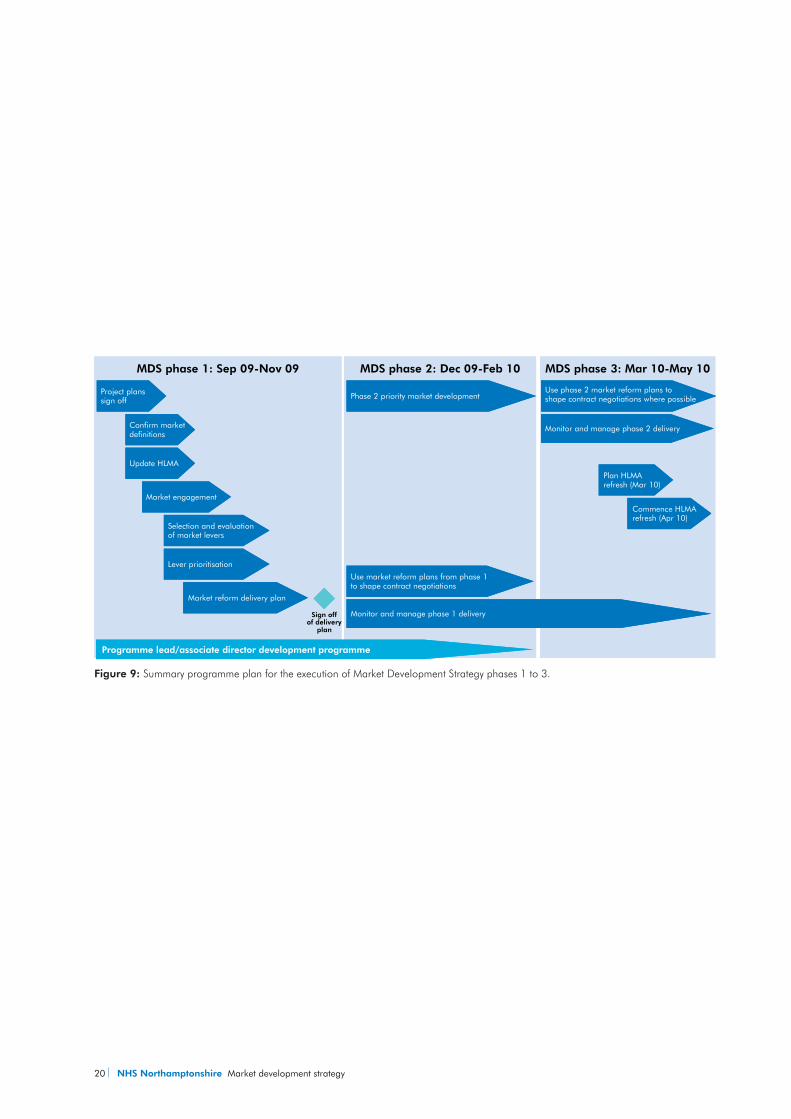

NHS Northamptonshire has identified the markets that are important in terms of requiring improvement and the approach that will be taken, which is described in section 3.3. A summary programme plan is set out in Figure 9.

Market Development Strategy delivery Phase 1Three streams of activity will begin during Phase 1 of the Market Development Strategy delivery. These are:

Detailed market analysis;yy

Programme Leads and Associate Director yydevelopment; and

Competition Governance development.yy

Detailed market analysisNHS Northamptonshire will complete an in-depth analysis of each Phase 1 priority market to understand prevailing market conditions in more detail, including relevant local context (for example, local demographic or geographic conditions that impact on the distribution and use of services) where a more detailed definition of the market will be undertaken (e.g. collecting evidence on willingness to travel).

As highlighted in the diagram above, this process will take 8-12 weeks based on experience from other sectors and will be underpinned by a detailed project plan.

20 NHS Northamptonshire Market development strategy

Figure 9: Summary programme plan for the execution of Market Development Strategy phases 1 to 3.

MDS phase 1: Sep 09-Nov 09

Project planssign off

Confirm marketdefinitions

Market engagement

Selection and evaluationof market levers

Update HLMA

Lever prioritisation

Market reform delivery plan

Monitor and manage phase 1 delivery

Use market reform plans from phase 1 to shape contract negotiations

Sign off of delivery

plan

Board sign off

Programme lead/associate director development programme

Phase 2 priority market development

Plan HLMArefresh (Mar 10)

Commence HLMArefresh (Apr 10)

Monitor and manage phase 2 delivery

Use phase 2 market reform plans to shape contract negotiations where possible

Strengthen competition governance

MDS phase 2: Dec 09-Feb 10 MDS phase 3: Mar 10-May 10

Market development strategy NHS Northamptonshire 21

Demand sidelevers

• Activities by PBC/PCT to influence care seeking behaviours by patients• Making available comparative data on providers to inform patient choices• Formal dialogue with patients to inform development of new market options

(such as new care pathways)• Use of patient ‘voice’ within providers (e.g. members of FT)

• Demand shaping and education

• Provision of information• Consumer engagement

• Stimulating competition where monopoly exists• Introducing greater range of providers in existing market• Decommissioning existing providers• Altering key performance indicators and other quality drivers in contract

Supply sidelevers

• Market creation• Market development• Market exit• Contracting

• PCT requiring additional licensing requirements as community services markets are established

• Removal of licences granted by PCTs• Provision of information to formal licensing authorities

Regulation • Licensing• De-licensing• Regulatory influence

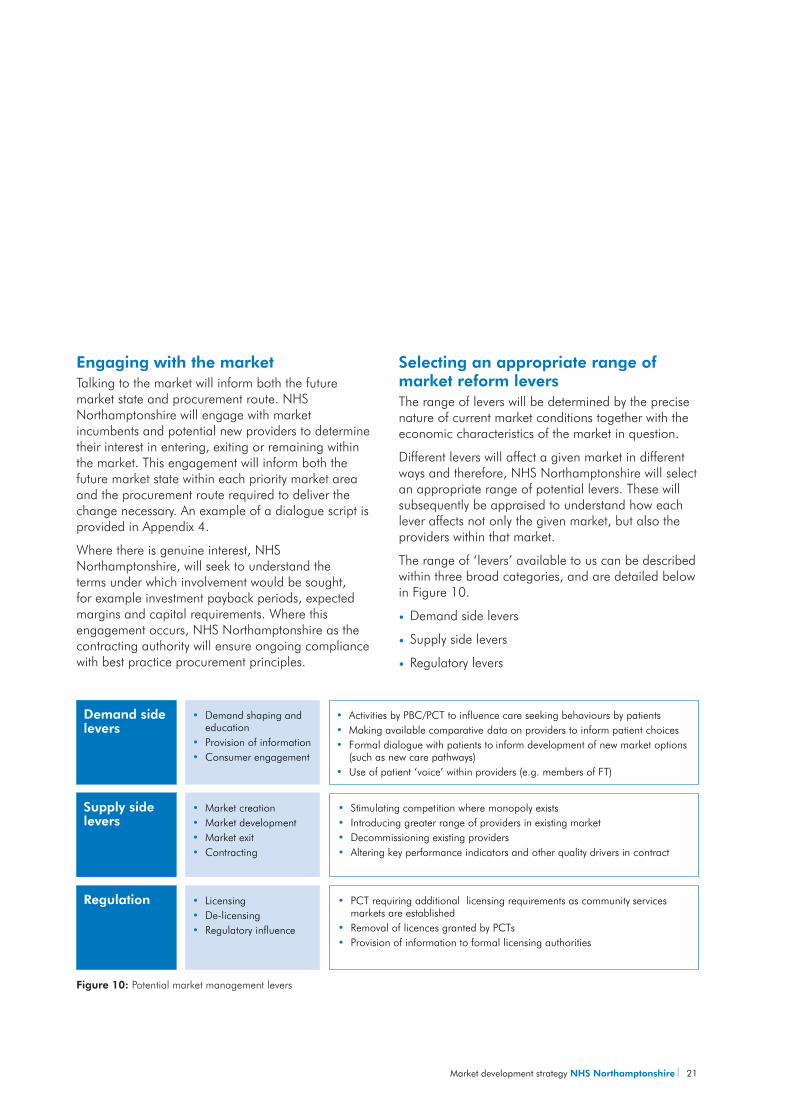

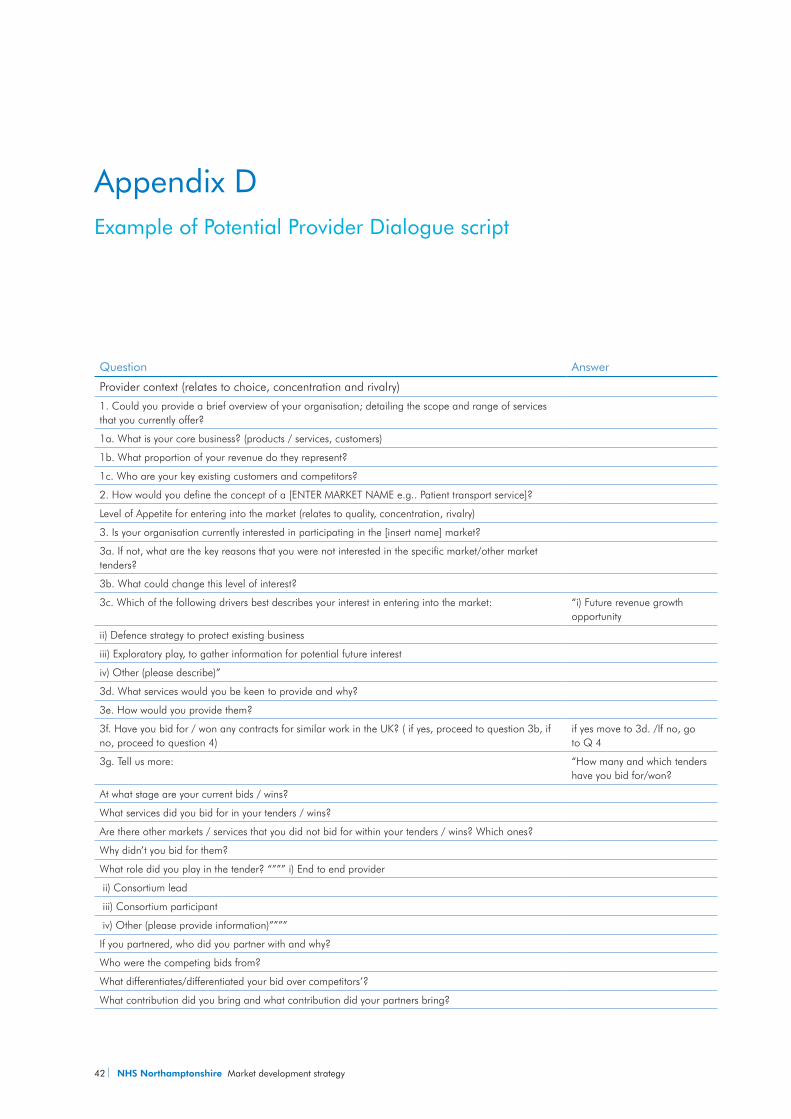

Engaging with the marketTalking to the market will inform both the future market state and procurement route. NHS Northamptonshire will engage with market incumbents and potential new providers to determine their interest in entering, exiting or remaining within the market. This engagement will inform both the future market state within each priority market area and the procurement route required to deliver the change necessary. An example of a dialogue script is provided in Appendix 4.

Where there is genuine interest, NHS Northamptonshire, will seek to understand the terms under which involvement would be sought, for example investment payback periods, expected margins and capital requirements. Where this engagement occurs, NHS Northamptonshire as the contracting authority will ensure ongoing compliance with best practice procurement principles.

Selecting an appropriate range of market reform leversThe range of levers will be determined by the precise nature of current market conditions together with the economic characteristics of the market in question.

Different levers will affect a given market in different ways and therefore, NHS Northamptonshire will select an appropriate range of potential levers. These will subsequently be appraised to understand how each lever affects not only the given market, but also the providers within that market.

The range of ‘levers’ available to us can be described within three broad categories, and are detailed below in Figure 10.

Demand side leversyy

Supply side leversyy

Regulatory leversyy

Figure 10: Potential market management levers

22 NHS Northamptonshire Market development strategy

For segments that conform mostly to competition ‘for-the-market’, action will most likely focus on supply side and regulatory levers (although some demand side levers such as the encouragement of the patient and public ‘voice’ may also be relevant).

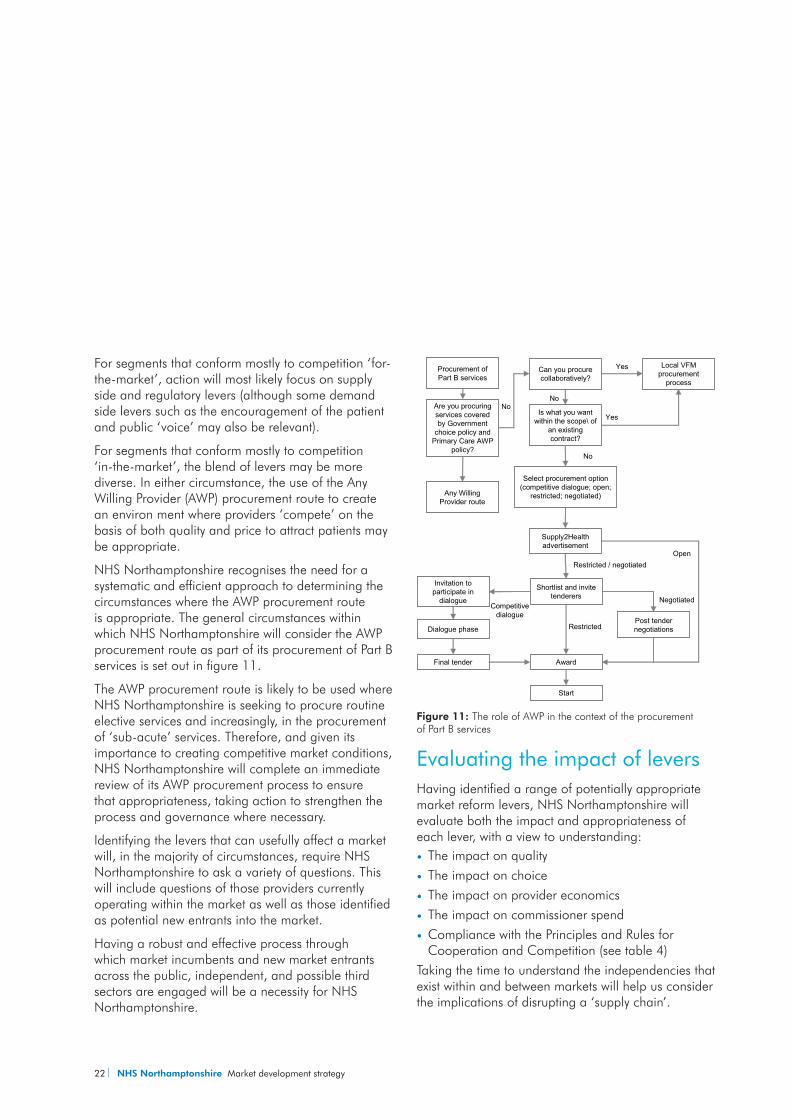

For segments that conform mostly to competition ‘in-the-market’, the blend of levers may be more diverse. In either circumstance, the use of the Any Willing Provider (AWP) procurement route to create an environ ment where providers ‘compete’ on the basis of both quality and price to attract patients may be appropriate.

NHS Northamptonshire recognises the need for a systematic and efficient approach to determining the circumstances where the AWP procurement route is appropriate. The general circumstances within which NHS Northamptonshire will consider the AWP procurement route as part of its procurement of Part B services is set out in figure 11.

The AWP procurement route is likely to be used where NHS Northamptonshire is seeking to procure routine elective services and increasingly, in the procurement of ‘sub-acute’ services. Therefore, and given its importance to creating competitive market conditions, NHS Northamptonshire will complete an immediate review of its AWP procurement process to ensure that appropriateness, taking action to strengthen the process and governance where necessary.

Identifying the levers that can usefully affect a market will, in the majority of circumstances, require NHS Northamptonshire to ask a variety of questions. This will include questions of those providers currently operating within the market as well as those identified as potential new entrants into the market.

Having a robust and effective process through which market incumbents and new market entrants across the public, independent, and possible third sectors are engaged will be a necessity for NHS Northamptonshire.

Evaluating the impact of leversHaving identified a range of potentially appropriate market reform levers, NHS Northamptonshire will evaluate both the impact and appropriateness of each lever, with a view to understanding:

The impact on qualityyy

The impact on choiceyy

The impact on provider economicsyy

The impact on commissioner spendyy

Compliance with the Principles and Rules for yyCooperation and Competition (see table 4)

Taking the time to understand the independencies that exist within and between markets will help us consider the implications of disrupting a ‘supply chain’.

Are you procuring services covered by Government

choice policy and Primary Care AWP

policy?

Any Willing Provider route

Can you procure collaboratively?

Is what you want within the scope\ of

an existing contract?

No

No

Local VFM procurement

process

Yes

Yes

Select procurement option (competitive dialogue; open;

restricted; negotiated)

Supply2Health advertisement

Shortlist and invite tenderers

Post tender negotiations

Award

Start

Restricted / negotiatedOpen

Restricted

Negotiated

Invitation to participate in

dialogue

Dialogue phase

Final tender

Competitivedialogue

Procurement of Part B services

No

Figure 11: The role of AWP in the context of the procurement of Part B services

Market development strategy NHS Northamptonshire 23

1. Commissioners should commission services from the providers who are best placed to deliver the needs of their patients and population.

2. Providers and commissioners must cooperate to ensure that the patient experience is of a seamless health service, regardless of organisational boundaries, and to ensure service continuity and sustainability.

3. Commissioning and procurement should be transparent and non-discriminatory.

4. Commissioners and providers should foster patient choice and ensure that patients have accurate and reliable information to exercise more choice and control over their healthcare.

5. Appropriate promotional activity is encouraged so long as it remains consistent with patients’ best interests and the brand and reputation of the NHS.

6. Providers must not discriminate against patients and promote equality.

7. Payment regimes must be transparent and fair.

8. Financial intervention in the system must be transparent and fair.

9. Mergers, acquisitions, de-mergers and joint ventures are acceptable and permissible when demonstrated to be in patient and taxpayers’ best interests and there remains sufficient choice and competition to ensure high quality standards of care and value for money.

10. Vertical integration is permissible when demonstrated to be in patient and taxpayers’ best interest and protects the primacy of the GP gatekeeper function; and there remains sufficient choice and competition to ensure high quality standards of care and value of money.

Table 4: The Principles and Rules for Cooperation and Competition

Having evaluated the potential benefit of each of the levers available, and the timing of their both application and likely market response, the future market state and implementation plans will then be developed.

Delivery planNHS Northamptonshire will focus relentlessly on the delivery of this strategy and therefore, the market reform delivery plans that sit within in it. The delivery plans that are developed as a result of appropriate engagement will set out precisely:

What actions will happen to deliver the agreed yyvision for each market

When each action will happen (start and yycompletion date)

Who is accountable and responsible for the delivery yyof each action

Delivery plans will be signed off in October 2009.yy

24 NHS Northamptonshire Market development strategy

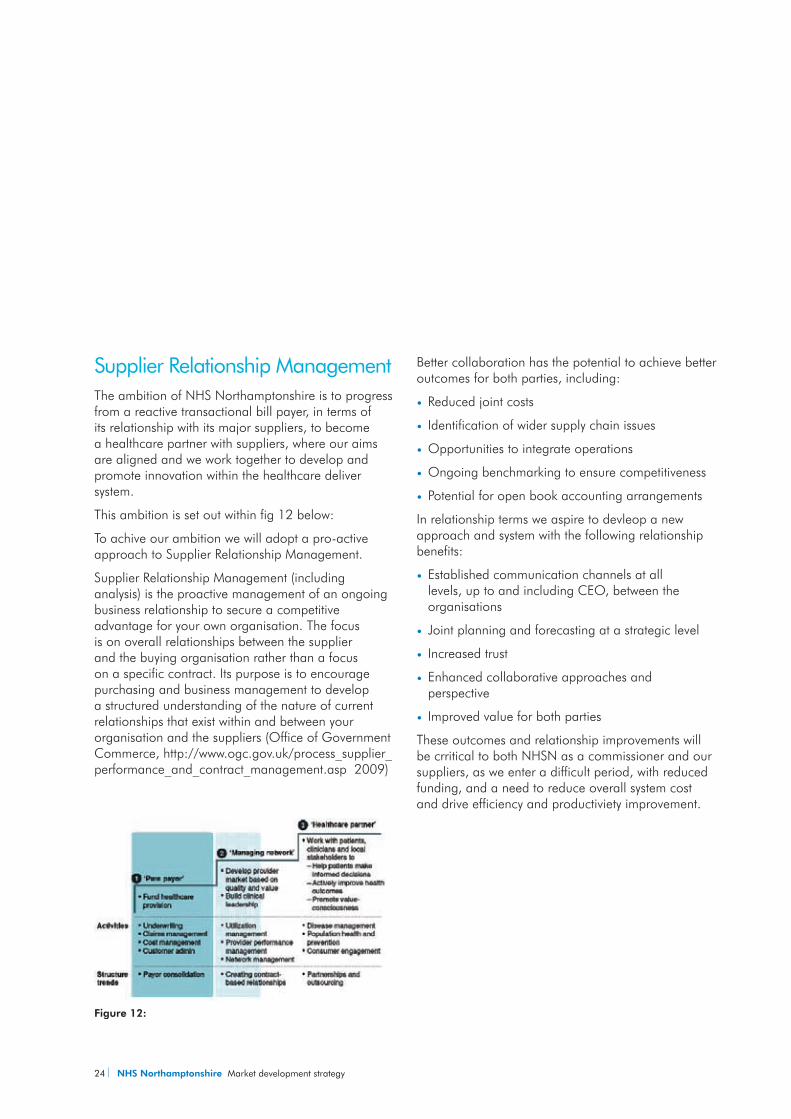

Supplier Relationship ManagementThe ambition of NHS Northamptonshire is to progress from a reactive transactional bill payer, in terms of its relationship with its major suppliers, to become a healthcare partner with suppliers, where our aims are aligned and we work together to develop and promote innovation within the healthcare deliver system.

This ambition is set out within fig 12 below:

To achive our ambition we will adopt a pro-active approach to Supplier Relationship Management.

Supplier Relationship Management (including analysis) is the proactive management of an ongoing business relationship to secure a competitive advantage for your own organisation. The focus is on overall relationships between the supplier and the buying organisation rather than a focus on a specific contract. Its purpose is to encourage purchasing and business management to develop a structured understanding of the nature of current relationships that exist within and between your organisation and the suppliers (Office of Government Commerce, http://www.ogc.gov.uk/process_supplier_performance_and_contract_management.asp 2009)

Better collaboration has the potential to achieve better outcomes for both parties, including:

Reduced joint costs yy

Identification of wider supply chain issues yy

Opportunities to integrate operations yy

Ongoing benchmarking to ensure competitiveness yy

Potential for open book accounting arrangementsyy

In relationship terms we aspire to devleop a new approach and system with the following relationship benefits:

Established communication channels at all yylevels, up to and including CEO, between the organisations

Joint planning and forecasting at a strategic level yy

Increased trust yy

Enhanced collaborative approaches and yyperspective

Improved value for both partiesyy

These outcomes and relationship improvements will be crritical to both NHSN as a commissioner and our suppliers, as we enter a difficult period, with reduced funding, and a need to reduce overall system cost and drive efficiency and productiviety improvement.

Figure 12:

Market development strategy NHS Northamptonshire 25

Programme lead and associate director developmentNHS Northamptonshire has undertaken a diagnostic review of current capability in relation to competencies 3, 7, 9, and 10 among a specifically selected group of respondents. Twenty seven individuals were selected by NHS Northamptonshire from within the Strategy and System Management, Contracting, and Public Health departments including Directors, Associate Directors, and Programme Leads. These individuals were selected because of their involvement in and contribution to significant service change programmes.

The results from a diagnostic survey were used to structure 1-2-1 interviews with each individual where emergent themes were identified; where the data collection and analysis was completed prior to our completing work to support the organisation deliver a Market Development Strategy, Primary Care Market Development Plan and Procurement Plan.

The emergent themes have enabled us to begin the process of developing tailored development programmes for both Programme Leads and Associate Directors.

While the programme will, when finalised, consider the role that the local Commercial Support Unit (East Midlands Collaborative Commissioning and Procurement or “EMCCAP”) will play moving forward, it is essential that Programme Leads and Associate Directors have core competence in relation to a number of tasks.

The key modules of the development programme will be agreed by September 2009, with the delivery of these training modules commencing in October 2009, running through until January 2010. Importantly, individual attendance at these modules and performance following attendance will form part of the overall performance management process in

place within the PCT. This development programme will embrace the key elements of competition governance outlined in the subsequent section.

Competition governance developmentThe Principles and Rules for Cooperation and Competition, in place since April 2008, set out clearly the considerations for both commissioners and providers with respect to service reconfiguration and market reform plans. It is therefore, implicit that commissioners have appropriate evaluative systems, processes and controls in place that supports a Board reaching conclusions on the extent to which activities are PRCC compliant.

Following a review of the NHS Northamptonshire’s existing competition governance arrangements, a programme of work to strengthen these arrangements has begun. This work will be lead by the Director of Operations and Policy, with development proposals being made to the Board in September 2009.

3.4 Market Development Strategy delivery phase 2

Detailed market analysisPhase 2 of Market Development Strategy delivery has two core elements:

Using the market reform plans developed during 1.

phase 1 to shape contract negotiations with existing providers while monitoring and managing the delivery of the phase 1 plans; and

Applying the process deployed during phase 1 2.

to examine in detail the phase 2 priority markets.

It is our expectation that phase 2 will begin in November 2009, completing in January 2010.

26 NHS Northamptonshire Market development strategy

3.5 Market Development Strategy delivery phase 3It is our expectation that phase 3 will begin in February 2010, completing in April 2010 and will have three core elements:

Using the market reform plans developed during 1.

phase 1 to shape contract negotiations with existing providers while monitoring and managing the delivery of the phase 2 plans.

Applying the process deployed during phases 1 2.

and 2 to examine in detail the phase 2 priority markets.

Planning and delivering the high level market 3.

analysis ‘refresh’ exercise.

It is our expectation that the process of refreshing our high level analysis of the healthcare markets that we manage, identifying the priority markets within which reforms are necessary, and continually monitoring staff development and organisational governance form part of a cyclical process. Therefore, the processes outlined here are complimentary to the commissioning process in the way that it had traditionally been considered.

Detailed analysis of prioritymarkets (July to September)

Planned execution of market reform

(October to January)

Revisit definitions of the local healthcare market (February to March)

High level analysis of allmarkets (April to June) Deep

dive

Marketreform

Marketdefinition

HLMA

Quality andvalue for

money

Figure 13: The cyclical market management process

Market development strategy NHS Northamptonshire 27

Programme interdependencies and risks

The strategy and therefore framework within which NHS Northamptonshire will monitor and manage markets effectively on an on-going basis is dependent on a number of enablers and the capacity within the PCT to carry out this work.

4.1 Interdependencies

Work programme interdependenciesTransforming Community Services (TCS) programme

The TCS Programme has been established for three main reasons:

Ensure that the care provided within community 1.

settings is of the highest quality and responsive to the needs of both patients and local communities;

Enable transformation practices that drive quality 2.

of better value for money; and

Strengthen PCT’s capacity by through the 3.

establishment of Alternative Provider Organisations (APrO’s) following the disaggregation of PCT’s Provider Arm services.

NHS Northamptonshire is engaged with the programme management approach to TCS that is underway across NHS East Midlands. Therefore, and in relation to the execution of this Market Development Strategy, NHS Northamptonshire will need to:

Establishing an APrO is compliant with the Principles yyand Rules for Cooperation and Competition;

Consider the APrO (once established) and PCT yyProvider Arm (as it is currently established) as a provider across healthcare markets, where the impact of specific market reforms (including decommissioning, new market entry and market development) will need to considered in relation to whether the current and/or new organisation is best placed to deliver care to the local population.

28 NHS Northamptonshire Market development strategy

DisinvestmentThe current economic recession will impact significantly and adversely on NHS funding and is likely also to increase demand for health care. The government will demand that the NHS improve efficiency to help balance its books. A rising demand for healthcare, driven by an aging population, technological advances and lifestyle diseases will lead to mounting cost pressures in the future.

NHS Northamptonshire recognises that managed and transformational change is required if we are to meet the challenge and to deliver better value from constrained resources. At the heart of this commissioning transformation is the capability to

deliver greater technical efficiency (doing current things better) and allocative efficiency (doing the right things).

Therefore, and in relation to the execution of this Market Development Strategy, NHS Northamptonshire will need to:

Recognise that any potential disinvestment yyopportunities are likely to change the nature of the markets as they are currently defined; and

Consider the impact of any decisions to disinvest yyin specific markets on interdependent markets, within and across care pathways and strategic programmes.

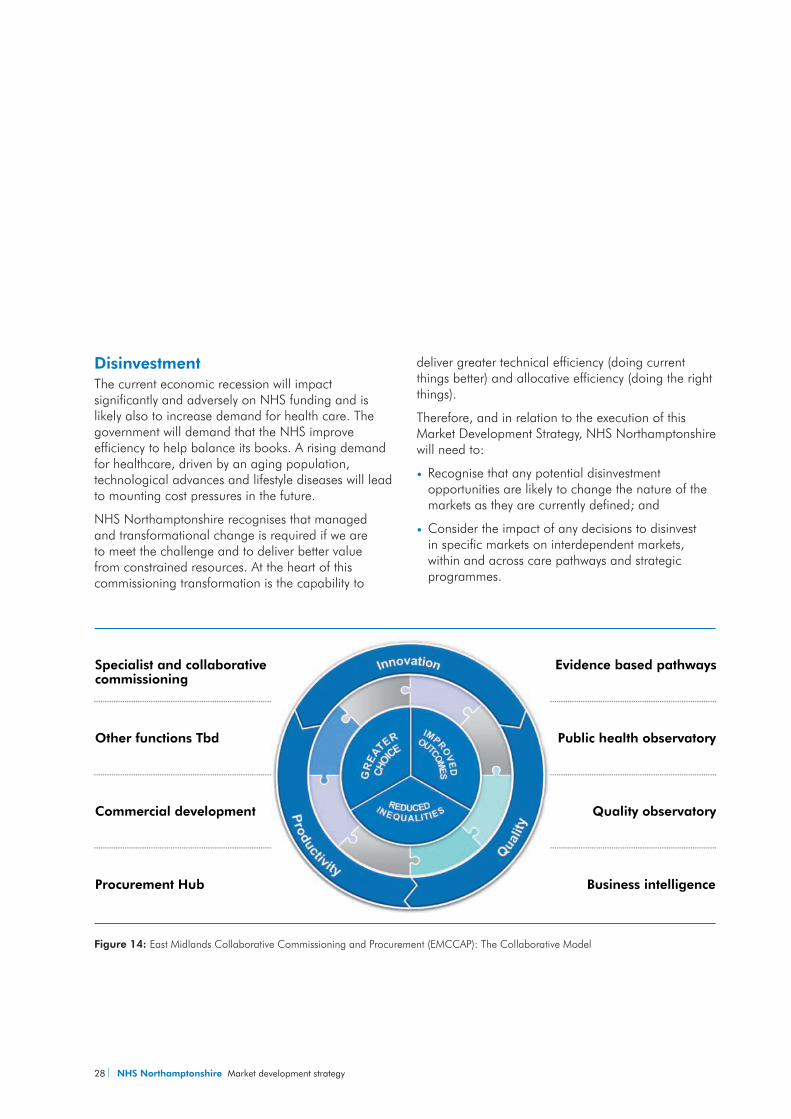

Figure 14: East Midlands Collaborative Commissioning and Procurement (EMCCAP): The Collaborative Model

Evidence based pathways

Public health observatory

Commercial development

Procurement Hub Business intelligence

Quality observatory

Other functions Tbd

Specialist and collaborativecommissioning

Market development strategy NHS Northamptonshire 29

East Midlands Commercial Support UnitHigh-quality commercial skills, deployed in the right way and in the right place, will be instrumental in meeting this challenge outlined above in relation to disinvestment. Therefore, Commercial Support Units (CSUs) are expected to provide a focused and efficient grouping of commercial skills that are currently spread across the environment and provided from a range of internal and external sources.

While the precise form and function of the CSU solution within NHS East Midlands has yet to be agreed (the diagram below illustrates the proposed collaboarative model), it is likely that it will focus on commercial skills transfer and development in PCTs. This will accelerate the drive towards the vision of local commercially enabled organisations, supporting rapid improvement against the relevant World Class Commissioning capabilities (in particular 7, 9 and 10). Furthermore, and where necessary, CSUs may also be involved in undertaking commercial activity on behalf of PCTs – for example where PCTs have taken an early and informed decision to pool commercial activities (e.g. market-making or business intelligence).

In relation to the execution of this Market Development Strategy, NHS Northamptonshire will therefore, need to:

Ensure that it retains a clear view on both the form yyand function of the East Midlands CSU solution, for which John Parkes is the Senior Responsible Officer.

Adapt and update existing systems, processes yyand controls to cater for the changing role and responsibilities retained by NHS Northamptonshire as a result of the introduction of the CSU.

Organisational interdependenciesProviders

The market analysis process will lead to a range of interventions that NHS Northamptonshire can adopt to deliver improvements in healthcare services. Before moving on to implement these interventions, it is important that we work in dialogue with providers to develop an understanding of the impact of changes on existing service providers.

Market interventions will lead to changes in activity and funding flows across service providers. While this can be beneficial in terms of creating competitive tension and driving responsiveness, NHS Northamptonshire will need to guard against any unintended consequence of changes which could threaten the viability and sustainability of key services.

This will inevitably require NHS Northamptonshire to develop a framework that relies on both detailed economic analysis as well as qualitative information sources to understand this, which:

recognises the implications of any proposed 1.

change to activity type or volume in financial, quality and choice terms by provider;

recognises how and where the interdependencies 2.

between services within providers mean that stimulating the market is more likely to adversely affect the financial viability of a provider, the quality of service offered, or the amount of choice available;

recognises how and where the interdependencies 3.

between services within providers mean that stimulating the market is less likely to adversely affect the financial viability of a provider, the quality of service offered, or the amount of choice available.

30 NHS Northamptonshire Market development strategy

Without developing the framework, it is possible to set out the main issues that NHS Northamptonshire has to understand to be able to decide on the impact of increased competition (in or for the market) on incumbent providers. The main areas to understand are:

Cost structure:yy the balance between fixed and variable costs, which requires understanding of which costs can be decreased if demand falls. This analysis should encompass both the ability to alter particular inputs in response to changes in demand and also the ability to shift those inputs to alternative uses within the trust (ie the flexibility of inputs).

Extent of cross-subsidies:yy which services, treatments or procedures are loss making on a fully-allocated cost basis or under current tariffs, their importance in the total trust budget and how they are funded,

Service being open to competition:yy mapping how the service(s) opened to competition relate to the different cost structures set out above.

Understanding each of these areas will allow NHS Northamptonshire to build a picture of the impact on trust finances of new competition, either in or for the market. Any changes are not necessarily bad, however any anticipated negative impacts on particular providers will be weighed against any positive impacts on health outcomes.

Implications of commissioning from a broad range of types of provider

Market stimulation and the introduction of competition means that NHS Northamptonshire may increasingly commission services from a range of different types of providers.

Some of these providers may be public sector institutions, private corporations, other partnerships, charities and other third sector institutions. At the same time, they are all operating in the same system. It is important therefore, that NHS Northamptonshire is aware of this range of different business models and the implications for effective commissioning and the operation of the healthcare system.

One important example arises in the context of competition for the market. If the aim of competition for the market is to help drive improvements in quality it is important that the different types of providers highlighted previously, who may be interested in competing, are able to compete fairly. If the design of the tender is such that one type of provider is favoured over others, then the benefits of real competition will not emerge due to a lack of competitive tension.

Different types of providers will have significant differences in the costs that they face in providing NHS services for example, a private sector provider competing against a public sector institution for a particular contract. These differences can have either a positive or negative impact on costs. The areas of cost that may differ include:

Corporation tax:yy private providers must pay corporation tax if making taxable profits overall, but public institutions do notVAT:yy private providers must charge VAT where this applies, but public institutions have different rules and reduced liability

Market development strategy NHS Northamptonshire 31

Central overheads:yy public institutions have access to certain central administrative and support that private providers would have to pay forCost of capital: yy private providers must earn a competitive rate of return; public providers have to make a return on capital, but this is less onerousClinical negligence scheme:yy there are differences in the costs and coverage of the clinical negligence scheme between public and private providersCensions:yy the treatment of pension costs is different between public and private providers although if a private provider does not operate a pension scheme then their costs would actually be lowerFinancing:yy The private sector has an ability to borrow to finance capital which the NHS does not have which could mean that the necessary assets are financed cheaper and quickerThe private sector has an ability to subsidise one yycontract from another and create loss leaders

To ensure that all providers can compete fairly for work it is important for NHS Northamptonshire to consider whether these, or other, issues distort competition and prevent it from driving performance improvement. This could, for example, involve adjusting (or asking bidders to adjust) prices for particular cost categories (e.g. requiring public providers to include corporation tax costs in their bids). It could simply require all competitors to use fully-allocated cost approaches to their pricing (e.g. ensuring public providers include costs of central overheads, pensions and other services properly within their bids).

In summary, when considering approaches to stimulate or manage a market, NHS Northamptonshire will consider the range of providers in the market and their different economic models. This will allow us to assess whether some providers have systematic advantages and whether any adjustments are required to ensure competition can effectively drive improved performance.

Developing an understanding of provider economics is a key requirement for NHS Northamptonshire in an increasingly dynamic healthcare system. World Class Commissioning Competency 9a sets out the expectations on PCTs in this area and NHS Northamptonshire will need to consider its ability to carry out the analysis set out above, working in partnership with new and existing providers and where necessary develop new skills in this area.

Local commissioners

Where appropriate, NHS Northamptonshire will look to collaborative procurement solutions for specific services. The approach to considering where this may be appropriate is summarised within the PCT’s Procurement Policy for Clinical Services.

NHS East Midlands

NHS Northamptonshire recognises the importance of maintaining its effective relationship with NHS East Midlands, particularly where competition issues are being considered.

32 NHS Northamptonshire Market development strategy

4.2 Strategic risksKey strategic risks will be managed and monitored in accordance with the established approach to risk management within the PCT. In terms of delivering the Market Development Strategy, three strategic risks have been identified and are outlined below.

Delivery governance

NHS Northamptonshire recognises the need to ensure that the infrastructure surrounding the execution of the Market Development Strategy is robust. In this regard, the recommendations made following a review of the existing competition governance framework will be accelerated while good practice project management disciplines will form the basis for all delivery activity.

Organisational capacity and capability

To ensure effective delivery of the Market Development Strategy, NHS Northamptonshire recognises that the organisation will need to ensure that sufficient capacity exists and that this capacity is appropriately skilled. To mitigate this risk, NHS Northamptonshire is currently developing a development programme for the key staff groups involved in delivery market-based reforms and analysis.

Compliance with PRCC

In reforming healthcare markets, NHS Northamptonshire recognises the risks of non-compliance with the PRCC. Therefore, NHS Northamptonshire will update the existing governance framework to ensure commissioning, procurement and tender activities are considered against the relevant principles and rules.

Market development strategy NHS Northamptonshire 33

The production of this strategy, the high level market analysis of all our healthcare markets (product lines), and the commercial skills devleopment associated with this work are important first steps, but first steps nonetheless in the devleopment of a more commercial approach to commissioning and procurement.

A number of market activities and procurements are in train, or planned as a result of the work undertaken.

In the future we will focus market intervention activity in areas of strategic importance (our service priorities form our 5 year strategy), where our analysis shows outcomes to be poorer than expected, care pathways to be sub optimal, or where value for money is poor.

Turning Strategy In To Action – Next Steps

34 NHS Northamptonshire Market development strategy

Market development strategy NHS Northamptonshire 35

Appendices

36 NHS Northamptonshire Market development strategy

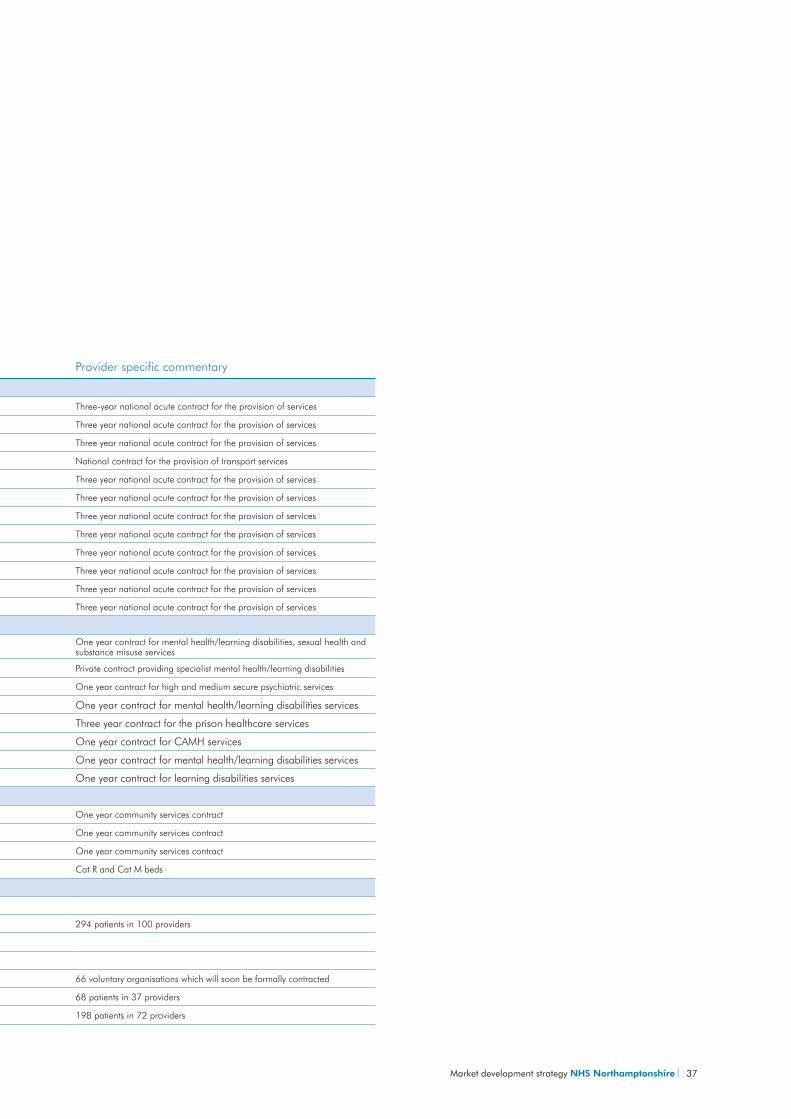

Current key provider Value activity commissioned Provider specific commentary

Acute

Northampton General Hospital NHS Trust £139,386,776 Three-year national acute contract for the provision of services

Kettering General Hospital NHS Trust £116,594,924 Three year national acute contract for the provision of services

East Midlands Specialist Services £67,654,230 Three year national acute contract for the provision of services

East Midlands Ambulance Service NHS Trust £13,156,213 National contract for the provision of transport services

Oxford Radcliffe Hospitals NHS Foundation Trust £13,052,597 Three year national acute contract for the provision of services

University Hospital of Leicester £8,780,323 Three year national acute contract for the provision of services

Peterborough & Stamford Hospitals NHS Foundation Trust £5,235,635 Three year national acute contract for the provision of services

University Hospitals of Coventry and Warwickshire NHS Trust £3,508,399 Three year national acute contract for the provision of services

Milton Keynes Hospital NHS Foundation Trust £2,241,611 Three year national acute contract for the provision of services

Hinchingbrooke Health Care NHS Trust £698,345 Three year national acute contract for the provision of services

Bedford General Hospital NHS Trust £592,493 Three year national acute contract for the provision of services

British Pregnancy Advisory Service £405,867 Three year national acute contract for the provision of services

Mental Health

Northamptonshire Healthcare NHS Trust £88,011,762 One year contract for mental health/learning disabilities, sexual health and substance misuse services

St. Andrew’s Healthcare £5,763,413 Private contract providing specialist mental health/learning disabilities

Secure Mental Health Services – Leicestershire County and Rutland PCT £5,671,308 One year contract for high and medium secure psychiatric services

Oxford & Buckinghamshire Mental Health Trust £837,372 One year contract for mental health/learning disabilities services

Care UK Clinical Services Ltd £682,453 Three year contract for the prison healthcare services

Cambridgeshire & Peterborough Mental Health Foundation Trust £363,500 One year contract for CAMH services

Leicestershire Partnership NHS Trust £342,489 One year contract for mental health/learning disabilities services

Oxfordshire Learning Disability NHS Trust £56,965 One year contract for learning disabilities services

Community

Northamptonshire tPCT Provider Services £74,788,408 One year community services contract

Oxfordshire PCT £1,071,236 One year community services contract

Peterborough Provider Services £969,701 One year community services contract

Brackley Cottage Hospital Trust £389,841 Cat R and Cat M beds

Other provider organisations

Adult Mental Health IPC £13,784,348

Physical Disability IPCs £7,869,726 294 patients in 100 providers

Non Adult IPCs £7,090,564

High Cost Placement Reviews £4,347,881

Voluntary and community sector £4,341,710 66 voluntary organisations which will soon be formally contracted

Associated Brain Injury IPCs £4,123,820 68 patients in 37 providers

Palliative Care IPCs £2,144,398 198 patients in 72 providers

Appendix A List of current providers from whom NHS Northamptonshire commissions services (2007/08)

Market development strategy NHS Northamptonshire 37

Current key provider Value activity commissioned Provider specific commentary

Acute

Northampton General Hospital NHS Trust £139,386,776 Three-year national acute contract for the provision of services

Kettering General Hospital NHS Trust £116,594,924 Three year national acute contract for the provision of services

East Midlands Specialist Services £67,654,230 Three year national acute contract for the provision of services

East Midlands Ambulance Service NHS Trust £13,156,213 National contract for the provision of transport services

Oxford Radcliffe Hospitals NHS Foundation Trust £13,052,597 Three year national acute contract for the provision of services

University Hospital of Leicester £8,780,323 Three year national acute contract for the provision of services

Peterborough & Stamford Hospitals NHS Foundation Trust £5,235,635 Three year national acute contract for the provision of services

University Hospitals of Coventry and Warwickshire NHS Trust £3,508,399 Three year national acute contract for the provision of services

Milton Keynes Hospital NHS Foundation Trust £2,241,611 Three year national acute contract for the provision of services

Hinchingbrooke Health Care NHS Trust £698,345 Three year national acute contract for the provision of services

Bedford General Hospital NHS Trust £592,493 Three year national acute contract for the provision of services

British Pregnancy Advisory Service £405,867 Three year national acute contract for the provision of services

Mental Health

Northamptonshire Healthcare NHS Trust £88,011,762 One year contract for mental health/learning disabilities, sexual health and substance misuse services

St. Andrew’s Healthcare £5,763,413 Private contract providing specialist mental health/learning disabilities

Secure Mental Health Services – Leicestershire County and Rutland PCT £5,671,308 One year contract for high and medium secure psychiatric services

Oxford & Buckinghamshire Mental Health Trust £837,372 One year contract for mental health/learning disabilities services

Care UK Clinical Services Ltd £682,453 Three year contract for the prison healthcare services

Cambridgeshire & Peterborough Mental Health Foundation Trust £363,500 One year contract for CAMH services

Leicestershire Partnership NHS Trust £342,489 One year contract for mental health/learning disabilities services

Oxfordshire Learning Disability NHS Trust £56,965 One year contract for learning disabilities services

Community

Northamptonshire tPCT Provider Services £74,788,408 One year community services contract

Oxfordshire PCT £1,071,236 One year community services contract

Peterborough Provider Services £969,701 One year community services contract

Brackley Cottage Hospital Trust £389,841 Cat R and Cat M beds

Other provider organisations

Adult Mental Health IPC £13,784,348

Physical Disability IPCs £7,869,726 294 patients in 100 providers

Non Adult IPCs £7,090,564

High Cost Placement Reviews £4,347,881

Voluntary and community sector £4,341,710 66 voluntary organisations which will soon be formally contracted

Associated Brain Injury IPCs £4,123,820 68 patients in 37 providers

Palliative Care IPCs £2,144,398 198 patients in 72 providers

38 NHS Northamptonshire Market development strategy

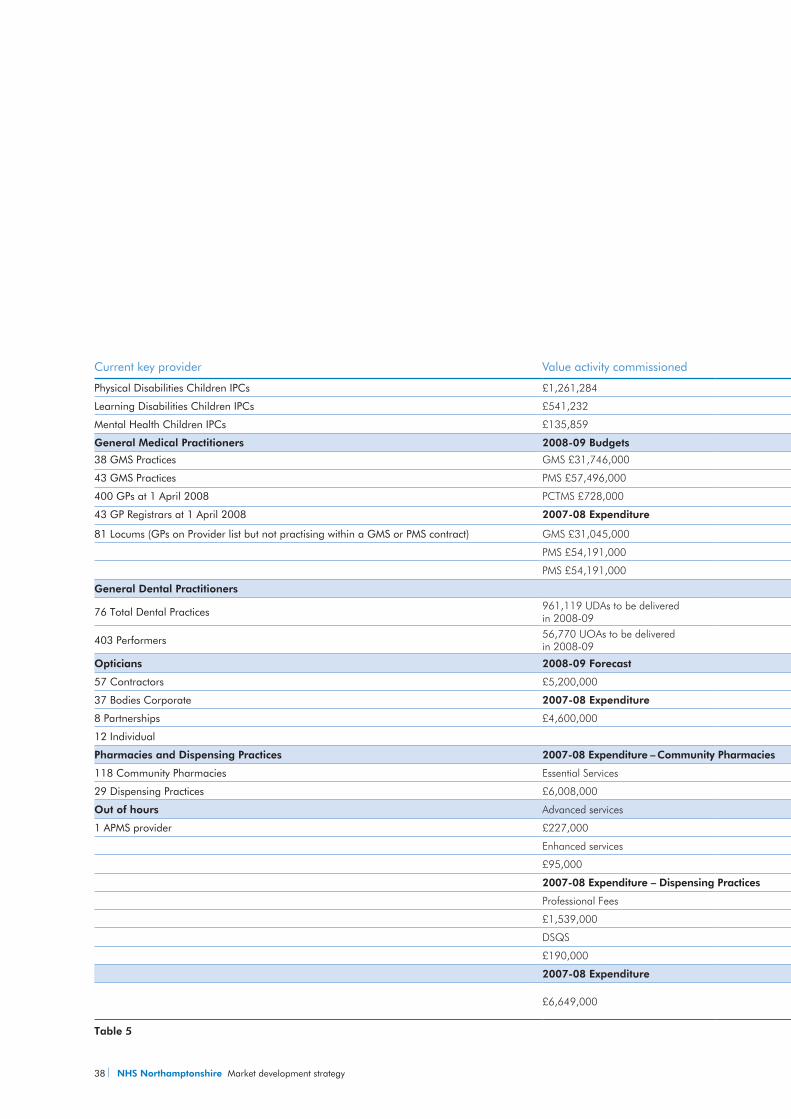

Current key provider Value activity commissioned Provider specific commentary

Physical Disabilities Children IPCs £1,261,284 29 children in 18 providers

Learning Disabilities Children IPCs £541,232 18 children in 14 providers

Mental Health Children IPCs £135,859 2 children in 2 providers

General Medical Practitioners 2008-09 Budgets

38 GMS Practices GMS £31,746,000

The PCT has a total of 81 GMS/PMS contracts providing a full range of essential services and the majority of practices provide all enhanced services too. The range of enhanced services provided varies from contract to contract

43 GMS Practices PMS £57,496,000

400 GPs at 1 April 2008 PCTMS £728,000

43 GP Registrars at 1 April 2008 2007-08 Expenditure

81 Locums (GPs on Provider list but not practising within a GMS or PMS contract) GMS £31,045,000

PMS £54,191,000

PMS £54,191,000

General Dental Practitioners

76 Total Dental Practices 961,119 UDAs to be delivered in 2008-09

The PCT has 59 General Dental Services Contracts (GDS) and 38 Personal Dental Services contracts (PDS) covering 76 Dental practices. The PCT has 3 Additional Advance services contracts covering Paedodontic Services, Minor Oral Services and Out of Hours services403 Performers 56,770 UOAs to be delivered

in 2008-09

Opticians 2008-09 Forecast

57 Contractors £5,200,000New Ophthalmic contract 1 August 200877 Contracts issued

50 Mandatoryyy27 Additional Servicesyy

(33 requested to be NHS Bodies)

37 Bodies Corporate 2007-08 Expenditure

8 Partnerships £4,600,000

12 Individual

Pharmacies and Dispensing Practices 2007-08 Expenditure – Community Pharmacies

118 Community Pharmacies Essential Services

Northamptonshire currently has 118 Community Pharmacies comprising of 49 Large Multiples; 63 Independent Contractors and 6 Supermarkets. There is one internet supplier providing services in the county. Of these 7 practices are contracted to open 100 hours per week. Community Pharmacies dispense on average 800,000 prescriptions per week

29 Dispensing Practices £6,008,000

Out of hours Advanced services

1 APMS provider £227,000

Enhanced services

£95,000

2007-08 Expenditure – Dispensing Practices

Professional Fees

£1,539,000

DSQS

£190,000

2007-08 Expenditure The majority of Out of Hours services are provided through 1 main APMS contract. The PCT also operates an OOH service through its Provider arm covering the West and South of the county. The north and south extremes of the county are covered through arrangements with Peterborough and Oxfordshire PCTs respectively

£6,649,000

Table 5

Market development strategy NHS Northamptonshire 39

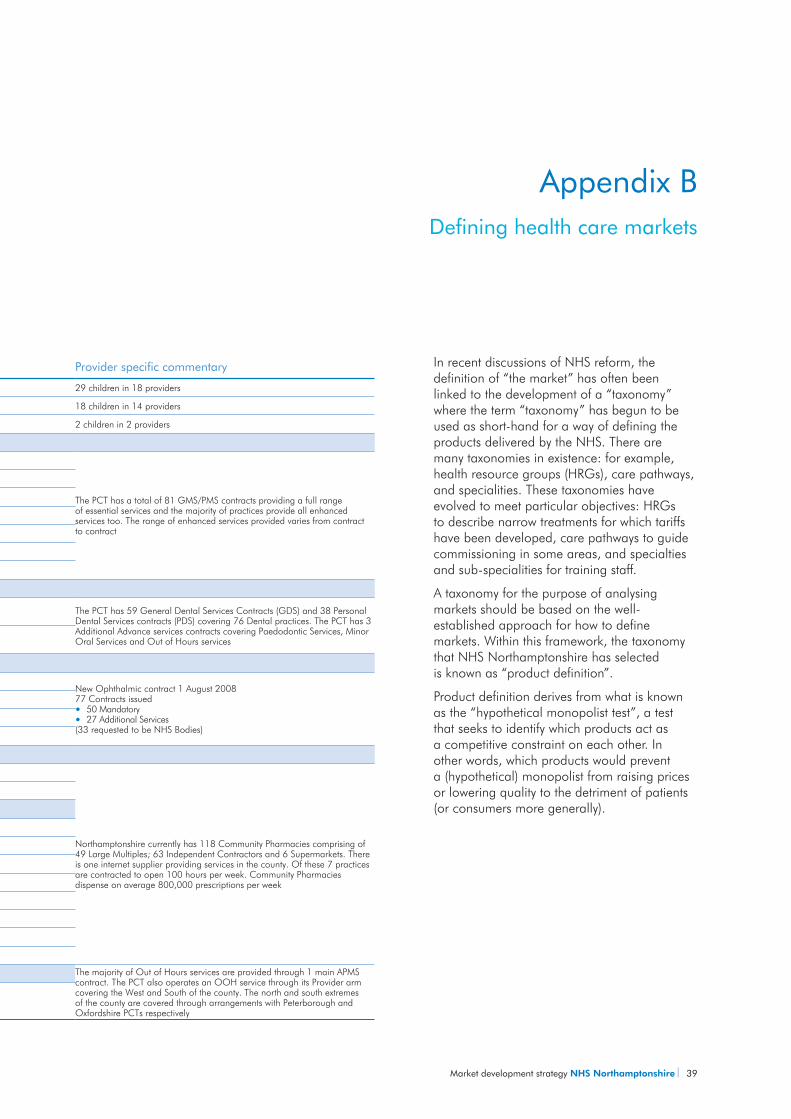

In recent discussions of NHS reform, the definition of “the market” has often been linked to the development of a “taxonomy” where the term “taxonomy” has begun to be used as short-hand for a way of defining the products delivered by the NHS. There are many taxonomies in existence: for example, health resource groups (HRGs), care pathways, and specialities. These taxonomies have evolved to meet particular objectives: HRGs to describe narrow treatments for which tariffs have been developed, care pathways to guide commissioning in some areas, and specialties and sub-specialities for training staff.

A taxonomy for the purpose of analysing markets should be based on the well-established approach for how to define markets. Within this framework, the taxonomy that NHS Northamptonshire has selected is known as “product definition”.

Product definition derives from what is known as the “hypothetical monopolist test”, a test that seeks to identify which products act as a competitive constraint on each other. In other words, which products would prevent a (hypothetical) monopolist from raising prices or lowering quality to the detriment of patients (or consumers more generally).

Appendix BDefining health care markets

Current key provider Value activity commissioned Provider specific commentary

Physical Disabilities Children IPCs £1,261,284 29 children in 18 providers

Learning Disabilities Children IPCs £541,232 18 children in 14 providers

Mental Health Children IPCs £135,859 2 children in 2 providers

General Medical Practitioners 2008-09 Budgets

38 GMS Practices GMS £31,746,000

The PCT has a total of 81 GMS/PMS contracts providing a full range of essential services and the majority of practices provide all enhanced services too. The range of enhanced services provided varies from contract to contract

43 GMS Practices PMS £57,496,000

400 GPs at 1 April 2008 PCTMS £728,000

43 GP Registrars at 1 April 2008 2007-08 Expenditure

81 Locums (GPs on Provider list but not practising within a GMS or PMS contract) GMS £31,045,000

PMS £54,191,000

PMS £54,191,000

General Dental Practitioners

76 Total Dental Practices 961,119 UDAs to be delivered in 2008-09

The PCT has 59 General Dental Services Contracts (GDS) and 38 Personal Dental Services contracts (PDS) covering 76 Dental practices. The PCT has 3 Additional Advance services contracts covering Paedodontic Services, Minor Oral Services and Out of Hours services403 Performers 56,770 UOAs to be delivered

in 2008-09

Opticians 2008-09 Forecast

57 Contractors £5,200,000New Ophthalmic contract 1 August 200877 Contracts issued

50 Mandatoryyy27 Additional Servicesyy

(33 requested to be NHS Bodies)

37 Bodies Corporate 2007-08 Expenditure

8 Partnerships £4,600,000

12 Individual

Pharmacies and Dispensing Practices 2007-08 Expenditure – Community Pharmacies

118 Community Pharmacies Essential Services

Northamptonshire currently has 118 Community Pharmacies comprising of 49 Large Multiples; 63 Independent Contractors and 6 Supermarkets. There is one internet supplier providing services in the county. Of these 7 practices are contracted to open 100 hours per week. Community Pharmacies dispense on average 800,000 prescriptions per week

29 Dispensing Practices £6,008,000

Out of hours Advanced services

1 APMS provider £227,000

Enhanced services

£95,000

2007-08 Expenditure – Dispensing Practices

Professional Fees

£1,539,000

DSQS

£190,000

2007-08 Expenditure The majority of Out of Hours services are provided through 1 main APMS contract. The PCT also operates an OOH service through its Provider arm covering the West and South of the county. The north and south extremes of the county are covered through arrangements with Peterborough and Oxfordshire PCTs respectively

£6,649,000

40 NHS Northamptonshire Market development strategy

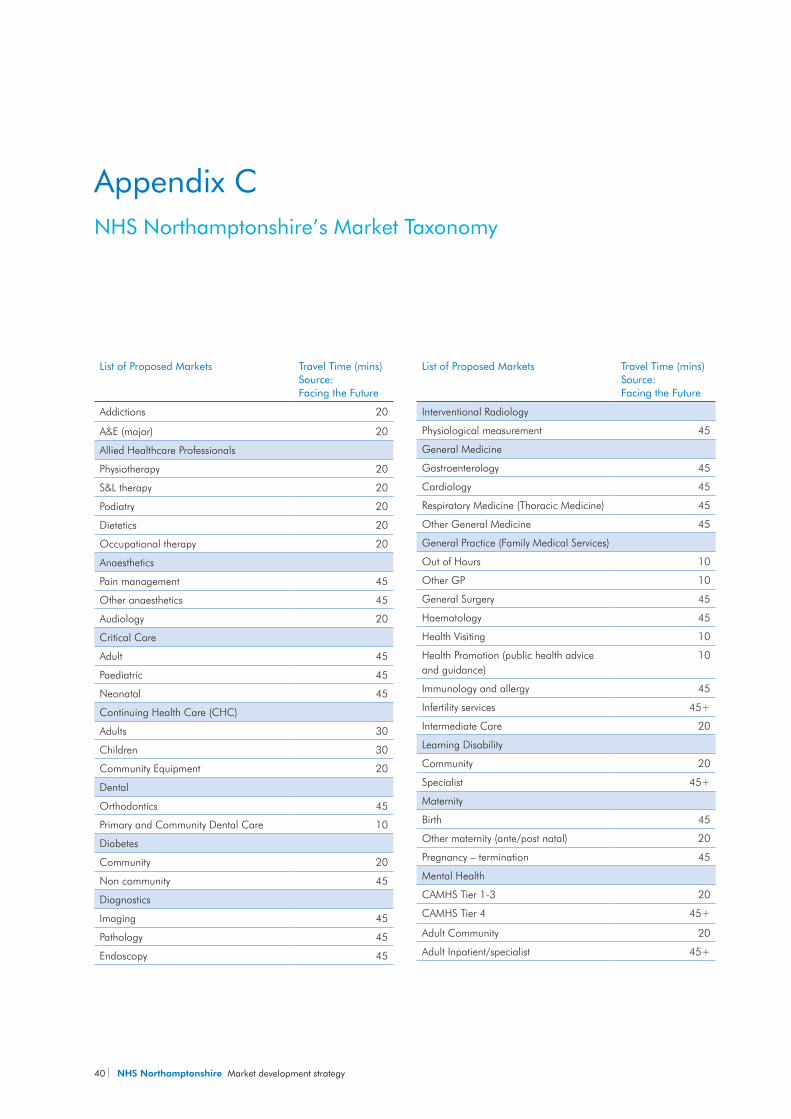

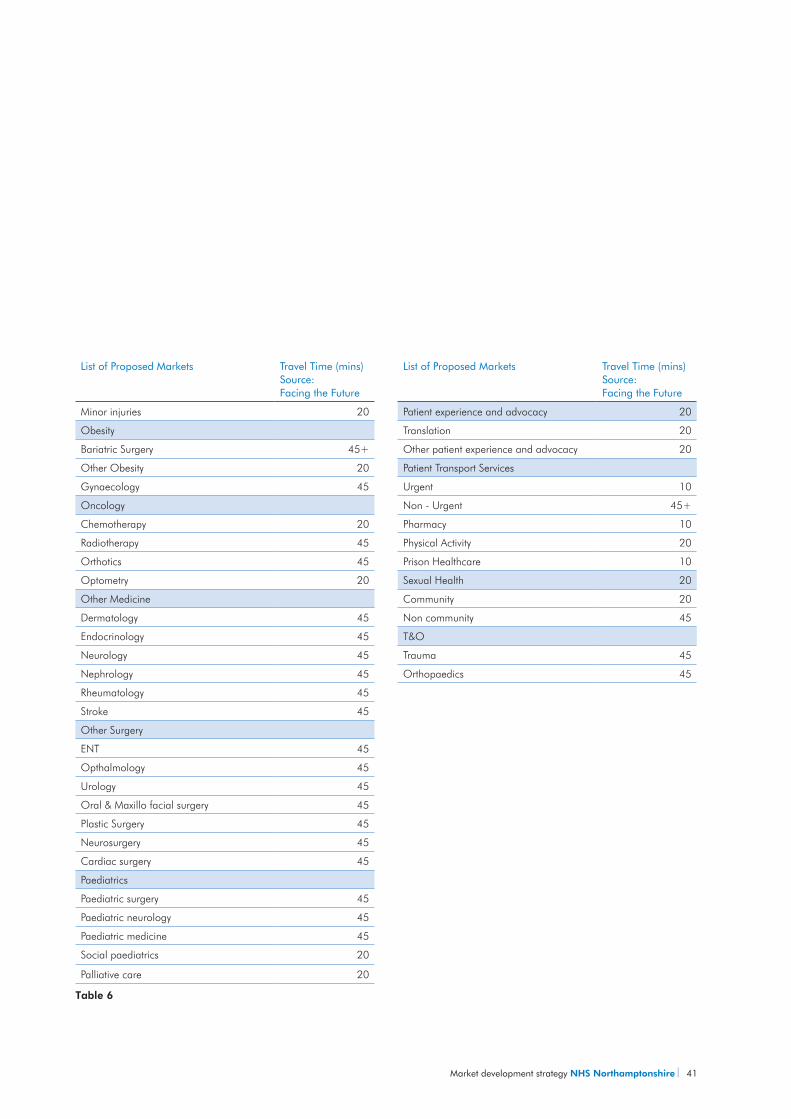

List of Proposed Markets Travel Time (mins) Source: Facing the Future

Addictions 20

A&E (major) 20

Allied Healthcare Professionals

Physiotherapy 20

S&L therapy 20

Podiatry 20

Dietetics 20

Occupational therapy 20

Anaesthetics

Pain management 45

Other anaesthetics 45

Audiology 20

Critical Care

Adult 45

Paediatric 45

Neonatal 45

Continuing Health Care (CHC)

Adults 30

Children 30

Community Equipment 20

Dental

Orthodontics 45

Primary and Community Dental Care 10

Diabetes

Community 20

Non community 45

Diagnostics

Imaging 45

Pathology 45

Endoscopy 45

List of Proposed Markets Travel Time (mins) Source: Facing the Future

Interventional Radiology

Physiological measurement 45

General Medicine

Gastroenterology 45

Cardiology 45

Respiratory Medicine (Thoracic Medicine) 45

Other General Medicine 45

General Practice (Family Medical Services)

Out of Hours 10

Other GP 10

General Surgery 45

Haematology 45

Health Visiting 10

Health Promotion (public health advice and guidance)

10

Immunology and allergy 45

Infertility services 45+

Intermediate Care 20

Learning Disability

Community 20

Specialist 45+

Maternity

Birth 45

Other maternity (ante/post natal) 20

Pregnancy – termination 45

Mental Health

CAMHS Tier 1-3 20

CAMHS Tier 4 45+

Adult Community 20

Adult Inpatient/specialist 45+

Appendix CNHS Northamptonshire’s Market Taxonomy

Market development strategy NHS Northamptonshire 41

List of Proposed Markets Travel Time (mins) Source: Facing the Future

Minor injuries 20

Obesity

Bariatric Surgery 45+