Embed Size (px)

Citation preview

8/6/2019 Low Income Household Improvement

http://slidepdf.com/reader/full/low-income-household-improvement 1/46

EARD Special Studies

Low-Income Households’

Access to Financial Services

International Experience, Measures forImprovement, and the Future

Nimal A. Fernando

8/6/2019 Low Income Household Improvement

http://slidepdf.com/reader/full/low-income-household-improvement 2/46

Nimal A. Fernando

Low-Income Households’ Access to Financial Services

International Experience, Measures forImprovement, and the Future

EARD Special Studies

October 2007

8/6/2019 Low Income Household Improvement

http://slidepdf.com/reader/full/low-income-household-improvement 3/46

ii

© 2007 Asian Development Bank

All rights reserved. Published 2007.

Printed in the Philippines.

Publication Stock No. 080907

Cataloging-In-Publication Data

ADB study on the access to nancial services or low-income households.

1. Access to nance 2. Low-income households

The views expressed in this paper are those o the author and do not necessarily refect the views and policies

o the Asian Development Bank, or its Board o Governors or the governments they represent.

The Asian Development Bank does not guarantee the accuracy o the data included in this publication and

accepts no responsibility or any consequences o their use.

Use o the term “country” does not imply any judgment by the author or the Asian Development Bank as to

the legal or other status o any territorial entity.

This publication is available on the Asian Develoment Bank’s micronance web site:

http://www.adb.org/micronance

Nimal A. Fernando is Practice Leader (Micronance) in the East Asia Department

o the Asian Development Bank

8/6/2019 Low Income Household Improvement

http://slidepdf.com/reader/full/low-income-household-improvement 4/46

iii

CONTENTS

Page

Abbreviations

Foreword v

Abstract

I. Introduction 1

II. Low-Income Households’ Demand or Financial Services 3

III. Dimensions o the Access Problem 4

IV. Factors Underlying Low Access 11

V. Overview o Cross-Country Experience 15

VI. Measures to Improve Access to Finance 26

VII. The Future o Access to Finance 30

VIII. Conclusions

Reerences and Websites 34

8/6/2019 Low Income Household Improvement

http://slidepdf.com/reader/full/low-income-household-improvement 5/46

iv

ABBREVIATIONS

ADB – Asian Development Bank

ASA – Association or Social Advancement

BRI – Bank Rakyat Indonesia

IRDA Insurance Regulatory and Development Authority (India)

MFI – micronance institution

NGO – nongovernment organization

PRC – People’s Republic o China

RFAS – Rural Finance Access Survey

ROA – return on assets

ROE – return on equity

SHG – sel-help group

SMEs – small and medium-size enterprises

WOCCU – World Council o Credit Unions

8/6/2019 Low Income Household Improvement

http://slidepdf.com/reader/full/low-income-household-improvement 6/46

v

FOREWORD

A

ccess to nancial services plays an important role

in inclusive development. Broader access makes

it possible or low-income households to not only

make use o economic opportunities but also improve

their health, education, and other social indicators

thus signiicantly improving their socioeconomic

well-being. However, in most developing countries,

a majority o the population, low-income people in

particular, do not have access to nancial services

rom ormal and semiormal sources. Even those who

have gained access owing to recent developments in

nancial services or the low-income people are oten

underserved. In the Asia and Pacic region alone, more

than 300 million households suer rom lack o access

to nancial services rom the ormal and semiormal

sectors. As a result, many o these households are

compelled to rely on inormal sources o nance. I

inclusive development is to become a reality, this

problem must be addressed head-on and as early as

possible.

This paper discusses dierent dimensions o the

problem o access to nance o low-income people

and provides cross-country experience in improving

access to highlight the diversity o approaches that

dierent countries ollow. In addition, the paper

proposes a number o measures to trigger a more

powerul process toward improved access.

The Asian Development Bank hopes that the

paper will help not only policy makers but also

practitioners to gain a better understanding o the

gravity o the problem o access to nance o low-

income households, and ormulate and implement

policies and other measures to make a signicant dent

in the problem, thus enabling millions o unserved

and underserved low-income households to actively

participate in, and benet rom, the development

process.

H. Satish Rao

Director General

East Asia Department

Asian Development Bank

8/6/2019 Low Income Household Improvement

http://slidepdf.com/reader/full/low-income-household-improvement 7/46

vi

ABSTRACT

Formal inancial sectors in most developing

economies serve only a minority, oten no more

than 20–30% o the population. Most households

do not have access to even basic nancial services.

A majority o those who do not have access are

concentrated in low-income categories. Even

those low-income households who have access to

nance are underserved both in terms o quantity

and quality o products and services. Access to

nance is not a magic bullet capable o liting poor

people out o poverty. However, there is consensus

that better access can play a potentially key role

in inclusive growth and development. Hence, the

problem o lack o access to nance or a majority

o the people deserves a great deal o attention and

must be addressed head-on. This paper discusses

dierent dimensions o the access problem and

provides global experience in improving access or

low-income households. The paper highlights the

diversity o approaches adopted and the institutional

modalities used by dierent countries. It concludes

that the global experience provides useul insights or

policy makers and practitioners who are committed

to address the issue. While many stakeholders have

to participate in the eorts to improve access to

nance in quantitative and qualitative terms, the

cross-country experience and the gravity o the access

problem suggest that governments have a major role

to play. Government role, however, must be ocused

on promoting the important role that private sector

nancial institutions could play in this task.

8/6/2019 Low Income Household Improvement

http://slidepdf.com/reader/full/low-income-household-improvement 8/46

vii

“The biggest challenge or developing economies

is to get the banks to the unbanked, rather thanto get the unbanked to the banks.”

Brian Richardson

Managing Director

Wizzit (cellphone-based banking acility)

South Arica

“Poorly unctioning banks that simply unnel credit

to connected parties and elites slow growth and

exert a disproportionately negative infuence on the

poor and small businesses by depriving them o thecapital they need to succeed. Unortunately, billions

o people live in countries with poorly unctioning

banks. Thus, banking policies matter because banks

infuence the ability o people, rich and poor, to

improve their living standards”.

James R. Barth, Gerard Caprio, Jr., and Ross Levine. 2006.

Rethinking Bank Regulation: Till Angels Govern. New York:

Cambridge University Press. 2.

8/6/2019 Low Income Household Improvement

http://slidepdf.com/reader/full/low-income-household-improvement 9/46

viii

8/6/2019 Low Income Household Improvement

http://slidepdf.com/reader/full/low-income-household-improvement 10/46

I. INTRODUCTION1

I

n developed economies, ormal nancial sectors

serve a majority. For example, 99% o the population

o Denmark, 96% o the population o Germany, 91%

o the population o the Unites States o America, and

96% o the population o France has a bank account

(Peachy and Roe. 2004, 31). The opposite is true,

unortunately, or developing countries. According

to the World Savings Banks Institute (2004), only 20%

o the population in most developing economies

has access to ormal nancial services. In a typical

developing economy in the Asia and Pacic region, the

ormal nancial system at best serves no more than

20–30% o the population, and excludes 70–80%, the

vast majority o whom are low-income households in

rural areas. With rapid urbanization, rural-to-urban

migration, and increasing urban poverty, the share o

low-income people without access to nance in urban

areas is also increasing in many countries.

Although access to nance is a seemingly simple

concept, measuring access to nance is not easy partly

because it is dierent rom actual usage o nancial

services. A person may be said to have access to

nancial services i he or she is able to use ormal or

semiormal nancial services in an appropriate orm

at reasonable prices when such services are required.

Thus, some o those who do not use nancial services

at a given time may actually have access, whereas other

nonusers do not. At the same time, some people may

have only partial access in terms o scope o services

or institutional types. Similarly, certain occupational

groups or ethnic groups may have access while others

may not (gure 1). However, because data on access

to nance and its various dimensions are dicult to

collect and extremely limited, it is common to use data

on usage as a proxy. Although the usage data may not

tell the ull story, they can illustrate many aspects o

the multidimensional access problem.

Introduction

1 The author grateully acknowledges the comments and suggestions o Nimal Sanderatne, Geetha Nagarajan and Ying Qian on an earlierversion o this paper. Secretarial assistance was provided by Emmalou Guillarte and Presentacion Lorena. The paper was edited by Ma.Priscilla Del Rosario. The author is responsible or any errors o omission or interpretations in the paper.

• Apersonwhorequiresuseofformalorsemiformalfinancialservicesisabletousetheserviceswhenhe/shewantstodoso.

• Apersonhasaccessonlytosomeproductsandservicesprovidedbytheformalandsemiformalsources.Forexample,somepeoplemayhaveaccesstodepositfacilitiesbutnoaccesstocreditfacilitiesorinsuranceproducts.

• Somepeoplemayhaveaccesstoservicesthatsemiformalinstitutionsprovidebutnoaccesstothoseprovidedbymainstreambankinginstitutions.Orsomepeoplemayhaveaccessonlytoservicesofstate-ownedfinancialinstitutions.

• Apersonmayhaveaccessonlytoapre-specifiedsmallamountofcreditwhichdoesnotfullymeetthedemand.

• Apersonmayhaveaccessbutnotatcompetitiveprices.

• Apersonmayhaveaccessonlytopoorqualityproductsandservices.

• Onlymenmayhaveaccesswhilewomenmaynot.

• Youthandelderlypersonsmaynothaveaccesswhileothersmay.

• Onlycertainoccupationalorethnicgroupsandliteratepersonsmayhaveaccess

Full Access

Partial Access

Scope dimension

Institutional dimension

Quantity dimension

Price dimension

Quality dimension

Gender dimension

Age dimension

Other dimensions

Figure 1: Dimensions of Access to Finance

8/6/2019 Low Income Household Improvement

http://slidepdf.com/reader/full/low-income-household-improvement 11/46

Given that inclusive development is a widely

accepted development objective, the lack o access

to nance or a majority o the population o these

countries must be considered a undamental faw in

the ormal nancial systems because it reinorces the

vicious circle o both income and non-income poverty.

Access to nance, though

not a magic bullet by any

measure, could play a

potentially signiicant

role in eorts to reduce

poverty. Like the rich,

poor households can

ben e it r o m c r edit ,

savings, payment and

insurance services, and

money transer acilities. Rutherord (2000) in his

excellent book, The Poor and Their Money, even

argues that the poor need access to nancial services

much more than the rich simply because the poor

have little money. Such services help the poor manage

their risks, smoothen consumption, take advantage

o protable economic opportunities, build income-

earning and other assets, and improve their standards

o living (ADB 2005; Helms 2006; United Nations

2006). Thus, access to ormal nancial services can

prooundly impact on

the quality o lie o low-

income households. AsRajan and Zingales (2004,

28) noted, “the limited

access to nance severely

r edu c es the c ho ic es

citizens have in determining the way they work and

live.” Without broader access to nance, only the rich

and connected people are able to take advantage o

economic opportunities. Also, when a majority o

the population is excluded rom access to nancial

services, it can signicantly and adversely impact

on the ecient allocation o nancial and physical

resources, economic growth, income and non-income

inequalities, and the distribution o benets in an

economy. Households rom Indian villages without

access to credit markets tend to reduce their children’s

schooling when they receive transitory shocks

more than households

with greater access to

nancial services ( Jacoby

and Skouias1997). The

adverse eects o lack

o access to inancial

s e r v i c e s c o u l d a l s o

s p i l l o v e r t o u t u r e

generations. In general,

lack o access to nancial

services imposes signicant direct and indirect costs

on low-income households and the economy.

The twin purposes o this paper are to briefy

discuss international experience on eorts to expand

the access to nance or low-income households and

draw some lessons rom that experience. Section 2 o

this paper describes the demand or nancial services

by the poor and low-income households. Section

3 ocuses on dierent dimensions o the access

problem. Section 4 discusses actors underlying low

access. Section 5 looks at

cross-country experience

on expanding inancialservices or low-income

households and explain

c o u n tr ies tha t ha ve

signicantly progressed

on this ront and the strategies they have adopted.

The section also discusses why some other countries

have ailed to make signicant progress. Section 6

discusses measures to improve access while section

7 looks into the uture o access to nance. Section 8

presents conclusions.

Access to nance, though not a magic bullet by

any measure, could play a potentially signicant

role in eorts to reduce poverty. Like the rich,

poor households can beneit rom credit,

savings, payment and insurance services, and

money transer acilities.

As Rajan and Zingales (2004, 28) noted, “the

limited access to nance severely reduces the

choices citizens have in determining the way

they work and live.”

8/6/2019 Low Income Household Improvement

http://slidepdf.com/reader/full/low-income-household-improvement 12/46

Low-Income Households’ Demand or Financial Services

II. LOW-INCOME HOUSEHOLDS’ DEMAND

FOR FINANCIAL SERVICES

Since the early 1980s, the conventional ormalinancial sectors have experienced a dramatic

growth. But the growth has been highly uneven and

occurred mainly at the middle and upper ends o the

nancial markets. This lop-sided growth, however,

has not been a result o lack o demand or nancial

services at the low end

o the markets. In the

Asia and Paciic region

alone, about 1.9 billion

are poor, near-poor, and

vulnerable in about 380

mil l io n ho u seho l ds,

mostly concentrated in

rural areas. The demand

or nancial services rom

these low-income households is substantial, and their

demand covers a wide range o products and services.

First, these households demand access to sae,

convenient, and appropriate deposit acilities. Second,

they demand access to credit at minimum transaction

costs and at reasonable prices or a wide range o

purposes. Third, they demand access to payment and

money transer services. In many countries, rural-to-

urban migration has resulted in signicant remittance

fows rom urban to rural areas. This is true or large

countries such as the People’s Republic o China (PRC)

and India as well as or relatively small countries

such as Cambodia and Viet Nam. Fourth, emerging

evidence suggests that demand or microinsurance

products and services is signicant. A recent study

(United Nations Development Programme [UNDP]

2007, 1), or example, estimated that the potential

market or microinsurance in India could exceed $1.4

billion in value terms. Fith, the demand or nancial

literacy services among low-income households is

also vast.

A signiicant part o the demand or depositservices and credit is generally directed at the inormal

markets. Lacking access to the kind o products

and convenient services they require rom ormal

sources, many households keep their cash at home,

with inormal savings clubs or in the orm o various

nonnancial assets such

as livestock as most rural

households do in the

Lao People’s Democratic

Republic (Lao PDR).

Similarly, households

also rely on sel-savings

or inormal sources to

nance investments and

smooth consumption.

For insurance, they rely on inormal arrangements

which rest on reciprocity in many cases. For money

transers also, they use inormal mechanisms. In

general, the eective prices that the poor and low-

income households pay in inormal markets or these

services tend to be high. Many people who save cash in

inormal markets suer signicant losses. Those who

borrow rom inormal commercial credit markets oten

have to pay very high interest rates and are unable to

get medium- to long-term loans. In addition, inormal

markets are inecient in nancial intermediation.

While many admit the drawbacks o inormal

sources o nancial services, their extensive nature

and persistent role in meeting the demand or nancial

services among low-income households conirm

beyond any doubt the importance o nancial services

in the lives o these households. Also, the widespread

existence o inormal markets conrms the act that

there are important supply-side constraints in the

ormal nancial system on the access to nancial

services or those at the low end o the market.

In the Asia and Pacic region alone, about 1.9

billion are poor, near-poor, and vulnerable

in about 380 million households, mostly

concentrated in rural areas. The demand orinancial services rom these low-income

households is substantial, and their demand

covers a wide range o products and services.

8/6/2019 Low Income Household Improvement

http://slidepdf.com/reader/full/low-income-household-improvement 13/46

III. DIMENSIONS OF THE ACCESS PROBLEM

The problem o access to nance or low-incomehouseholds has dierent dimensions (gure 2).

It is necessary to look at these to better understand

the gravity o the problem. The most conspicuous

dimension is that a majority o the low-income

population in developing countries do not have

access at all even to very basic nancial services. The

second dimension is that a large majority o the limited

number o those who have access are underserved in

terms o quality and quantity o products and services.

In many developing countries in the region, in

aggregate terms, more low-income people have accessto deposit services than nondeposit nancial services.

A third dimension is that access to a signiicant

proportion o low-income households is dependent

on unsustainable, subsidy-dependent, and poorly

perorming institutions.

Reliable and up-to-date data on dierentdimensions o access to nance in developing countries

are scanty. However, available country-level evidence

o access to ormal nancial services is revealing: In

India, about 73% o 89 million armer-households have

no access to ormal sources o credit (Thorat 2007). The

World Bank-National Council o Applied Economic

Research, Rural Finance Access Survey (RFAS) 2003 in

India2 (World Bank 2004), indicated that 79% o the

households do not have access to ormal loans and

59% do not have access to a savings account in the

ormal sector. The access problem was more severe orthe poorer households: 87% o the poorest households

surveyed did not have access to a loan and 71% did

not have access to a savings account rom the ormal

nancial system. The problem was not insignicant

even among small armers—68% without access to

2 This survey covered 6,000 households and microenterprises in two states, Andhra Pradesh and Uttar Pradesh.

Figure 2: Dimensions of the Access Problem

Low-income households andtheir micro- and small enterprises

Majority with no access to nance at all A small minority with access to nance

Very large proportion is underserved Very small proportion with ull access

Many have access todeposit services o state-

owned fnancial institutions

and cooperatives

A signicant proportionhave access only to

credit rom microcredit

institutions

Signicant numberdepend on services

o unsustainable

institutions

Proportion with accessto banking services is

very limited

Access to insuranceservices is extremely

limited

• Clients have to pay high transactions costs

• Withdrawing unds isnot always easy

• Transactions costs arehigh

• Poor credit quality • Client transactionscosts are high

• Processing time long • High minimum loan

requirements• Banks are geared to

serve high-incomegroups

• Productincompatability ishigh

• Transparency low

8/6/2019 Low Income Household Improvement

http://slidepdf.com/reader/full/low-income-household-improvement 14/46

Dimensions o the Access Problem

a loan and 45% without access to a savings account.

Over 82% o the households surveyed in RFAS 2003

also did not have any insurance. Another study by

Diamond Management and Technology Consultants

(2006) concluded that less than 20% o rural Indians

have access to ormal nancial services, and about 185

million “potentially bankable” people in rural India

do not have a bank account. However, the problem

o access to nance is not conned to rural areas.

According to the Banking Ombudsman o Karnataka

State (Business Line 2006), 63% o the people in the

country do not have the benet o banking acilities.

The nancially excluded sections largely comprise

marginal armers, landless laborers, sel-employed and

unorganized sector enterprises, urban slum dwellers,

ethnic minorities, migrants, and women. Most o the

excluded people are concentrated in the North East,

Eastern, and Central regions (Thorat 2007). Access to nance is no better in Pakistan. Only

about 30% o adults have bank accounts and the

total number o borrowers rom banking institutions

constitutes only 3% o the population. There are only

171 deposit accounts and 30 loan accounts per 1,000

people. Agriculture and small and medium enterprise

credit reaches only 1.6 million and 0.3 million

borrowers, respectively (Akhtar 2007, 36). Formal

and semiormal nancial institutions reach no more

than 10% o the potential market at the low end. The

number o active borrowers served by micronanceinstitutions at the end o 2005 was estimated at 6% o

the potential market o 10 million people (Burki and

Chen 2006, 7). Rural people suer the most rom the

lack o access to nance.

According to Akhtar (2007,

36) who is the Governor o

the State Bank o Pakistan

(central bank), 67% o

the rural population

is underserved by the

ormal banking systembecause only 6% o bank branch networks reach into

rural areas.

Nepal is another country with acute problems

in access to nance. A recent survey (2006) on access

to inancial services estimated that only 52.3% o

Nepalese households are served by a ormal or

semiormal nancial institution while about 27.6%

are served by inormal sources. An estimated 19.6%

remained nancially excluded, with no service rom

the ormal or inormal inancial sector. The same

survey ound that only 26% o households have a

bank account. However, banks ocus on urban areas

and the wealthiest. In rural Nepal, only 16% o the

households have a bank account, or example. Again

this is heavily concentrated in the upper income

groups. Only 49% o the households have a deposit

account with any nancial institution. An estimated

69% o oreign remittances come through inormal

channels—usually amily and riends—even among

households with a bank account. Despite government

eorts, ormal nancial institutions do not serve the

needs o most o the Nepalese population, particularly

the low-income people (Ferrari et. al. 2007).

A large number o rural people in the PRC also do

not have access to banking services. The Organisation

or Economic Co-operation and Development (2004)reports the results o a recent national survey showing

that only 16% o armers in the PRC have access to

ormal or inormal credit. The People’s Bank o China

(the central bank) estimates (www.undp.org.cn)

that 36% (82 million) o Chinese rural households

currently have access to nancial services, primarily

through Rural Credit Cooperatives (RCCs). However,

according to the members o the agriculture and

rural development task orce at the China Council

or International Cooperation on Environment and

Development (CCICED), although RCCs cover a vastarea o the countryside with an extensive network, their

provision o loans to small-arm households is limited.

Only 25% o smallholders nationwide have obtained

a RCC loan (CCICED

Agriculture and Rural

Development Task Force

Members 2005. 356). The

small and medium-sized

enterprises (SMEs) in

the PRC also receive less

than 10% o bank creditthough their share in gross domestic product is about

50%, and 40% o SMEs have no debt mainly because

they have no easy access to ormal sources (OECD

2005).

A recent national survey showed that more than

90% o the rural population in the Lao PDR do not have

access to ormal nancial services. The main service

provider, the state-owned Agricultural Promotion

According to the Governor o the State Bank

o Pakistan, 67% o the rural population is

underserved by the ormal banking system

because only 6% o bank branch networks reach

into rural areas.

8/6/2019 Low Income Household Improvement

http://slidepdf.com/reader/full/low-income-household-improvement 15/46

Bank, serves about 5% o rural households while

another 5% are served by semiormal institutions.

With little access to reliable ormal sector acilities,

most people in rural areas o the Lao PDR continue to

hold cash at home or save in nonnancial assets. In

early 2004, rural households held an estimated $216

million equivalent in cash savings, and cash in hand

accounted or about 40% o this amount. The estimated

total noncash savings o rural households—savings in

the orm o livestock, gold, jewelry, housing materials,

etc.—were much higher, exceeding the cash savings

by a actor o 2.75 (Coleman and Wynne-Williams

2006, 46–50).

Surprisingly, even in such countries as Indonesia

where nancial services

o r t h e p o o r h a v e

expanded because o

successul institutions,the access problems

remain signiicant. A

household survey that the

Bank Rakyat Indonesia

(BRI) and a group o

researchers rom Harvard

University carried out in

October 2000 concluded

that 68% o the sample

h o u s e h o l d s d i d n o t

have credit rom any ormal or inormal inancialinstitutions, and that 62% o the sample households

did not have savings accounts in any ormal or

inormal nancial institutions. The same survey also

showed that the proportions were high even or the

group o households with viable enterprises: 58% had

no loans rom nancial institutions and 52% had no

savings in a nancial institution (BRI 2001, 36–37).

While the proportion o the sel-excluded among these

is not clear, the data tend to show that the number o

households without access to nancial services could

be large.The other dimension o the access problem is

that a large majority o the low-income households

with access are simply underserved both in terms

o quality and quantity o products and services.

The underserved category suers rom a number o

problems.

A signiicant proportion o those with access

depend on the services provided by inancially

unsustainable, heavily subsidy-dependent, and poorly

perorming institutions. Whether these institutions

can maintain, let alone increase, their outreach and

the quality o the services they provide in the uture

remains uncertain. Perhaps one o the best examples

or this is provided by the state-owned agricultural

development bank in Bangladesh.3 This bank claims

to reach over 3 million borrowers. However, the bank

relies excessively on resources provided by the central

bank to continue its operations and is saddled with

too many operational

p r o b l e m s . T h e

nonperorming assets

o the bank amountedto 50% o total assets at

the end o June 2006.

Similarly, the Bangladesh

R u r a l D e v e l o p m e n t

Board (BRDB) claims

to reach over 4 million

clients. However, the

nancial and operational

perormance o BRDB is

extremely unsatisactory:

its operations lack transparency; are characterized by poor loan recovery rates; and involve large government

subsidies, being a state agency. In addition, rent seeking

is widespread among its eld-level employees.

Viet Nam also has a large-scale state-owned

institution—Vietnam Bank or Social Policies (VBSP)—

that provides access to credit or low-income

households at highly subsidized interest rates. VBSP

reported 4.195 million active borrowers with a total o

$1.149 billion in gross loans outstanding at the end o

2006. However, its return on assets (ROA) and return

on equity (ROE) have continued to be signicantly negative in the last 3 years or which data are available

(table 1). At the end o 2006, ROA and ROE were –4.04%

and –13.69%. The continued operations o VBSP as a

large-scale credit agency is thus dependent on whether

3 The bank started commercial operations in 1973. In 2007, it had 948 branches, 818 o which are in rural areas. According to its proft andloss account (unadjusted or subsidies, etc.), its losses amounted to about $26 million equivalent or the fnancial year ended 30 June 2006.Its gross loans outstanding amounted to about $1.1 billion.

Surprisingly, even in such countries as Indonesia

where inancial services or the poor have

expanded because o successul institutions, the

access problems remain signicant.

A signicant proportion o those with access

depend on the services provided by nancially

unsustainable, heavily subsidy-dependent, and

poorly perorming institutions.

8/6/2019 Low Income Household Improvement

http://slidepdf.com/reader/full/low-income-household-improvement 16/46

Dimensions o the Access Problem

it is able to obtain government subsidies without

interruption.

The rural credit cooperatives (RCCs) in the

PRC provide deposit

and lending services to

a large number o low-

in c o me ho u seho l ds.

But RCCs have seriousn o n per o r min g l o a n

( N P L ) p r o b l e m s —

according to dierent

estimates their average

NPL ratio ranged rom 26% to 50% (Dolven and Kuhn

2004). They are also beset with serious governance and

viability problems. The Government has initiated a

nationwide reorm program to address their nancial

and operational problems. The same is true or most

primary agricultural credit societies in India which

claim to have over 90 million members. A recent pressreport (Financial Express 2006) stated that majority

o these societies are in shambles or want o sound

nancial practices. Sri Lanka’s cooperative rural banks

provide basic lending and deposit services to over 1.5

million low-income households. But they also suer

rom severe governance and operational problems

(ADB 2003). India Post has a network o over 155,000

post oces, 89% o which are located in rural areas.

India Post is India’s largest savings institution with

more than $60 billion in outstanding deposits and

over 116 million savings accounts, mostly rom low-income households. However, India Post continues

to make substantial losses and relies on government

subsidies. Postal savings banks in many other Asian

developing economies such as Bangladesh, Pakistan,4

and Indonesia have similar problems.

4 Pakistan’s post ofce network consists o 12,343 post ofces. These ofces manage 4 million savings accounts (Akhtar 2007, 37).

While more low-income households have access

to deposit services than to other nancial services, the

quality o deposit services provided by most ormal

and semiormal institutions remains questionable.

First, the transaction costs associated with the

deposit services o most ormal institutions remain

too high or the users rom low-income households.

Most rural people have to spend time and money to

make deposits—walking, cycling, or riding to bank

oces. In some countries, depositors have to incur

other expenses. For example, in Cambodia, “savers

who make deposits in banking institutions expect to

pay a commission to the teller or the sae deposit o

their money” (Clark 2006,

111). Second, restrictions

on withdrawal o unds

reduce their value as

a source o liquidity.Third, most developing

countries have a long way

to go in ensuring saety o

poor people’s deposits

in nancial institutions including cooperatives that

they rely on.

The proportion o low-income people with

access to credit rom mainstream banking institutions

continues to be insigniicant in most developing

countries. Also, transaction costs that poor and

low-income households have to bear when they usethe acilities provided by these institutions remain

high. Generally, to obtain a loan rom a bank, a low-

income person has to visit the institution several times

and go through cumbersome procedures. Banks in

Bangladesh, Pakistan, and Philippines take more than

one month to process an SME loan application (Beck

et. al. 2007, 14). In many countries, low-income clients

have to pay bribes to have access to ormal nancial

services, particularly to credit rom state-owned banks.

According to some studies, in India, bribe payments

are estimated to be around 10% o the loan amount(Diamond Management and Technology Consultants

2006, 9). The RFAS 2003 estimated the bribe payments

to be in the range o 10–20% o the loan amount. On

average, 27% o sample households who borrowed

rom a regional rural bank report having to pay a

00 00 00

Numberofactiveborrowers 3,740,179 4,125,264 4,695,986

Loansbelow$300(%) 80.00 70.00 50.00

Clientsbelowpovertyline(%) 86.00 86.00 83.00

ROA (4.21) (4.56) (4.04)

ROE (12.89) (15.29) (13.69)

Table 1: Vietnam Bank for Social Policiesa

ROA=returnonassets,ROE=returnonequity.aPositionatendofeachyear.

Source:www.mixmarket.org.

While more low-income households have

access to deposit services than to other nancial

services, the quality o deposit services providedby most ormal and semiormal institutions

remains questionable.

8/6/2019 Low Income Household Improvement

http://slidepdf.com/reader/full/low-income-household-improvement 17/46

bribe to get the loan; a little under 27% o households

who borrowed rom a commercial bank paid a bribe,

and 10% o households who borrowed rom a credit

cooperative paid a bribe (World Bank 2004, 15). In

Azerbaijan, “corruption in the banking sector has been

observed to be signicant. Bankers charge ees as a

bribe that can sometimes account or 20–30% o the

loans” (Lamberte and Fitchett 2006, 110). Although

data are not available, one should not assume that this

problem does not exist or low-income households in

other developing countries.

Low-income people with access to credit are too

heavily dependent on the services that specialized

microinance institutions (MFIs) provide. While

MFIs have signiicantly

improved access to credit

or low-income people,

women in particular, withew exceptions, much

o the credit provided

by MFIs is or short-

term income-generating

activities. Little is provided or housing improvements,

education, health, consumption smoothing, and

emergencies. Credit quality remains generally low.

Beyond credit, other basic inancial services such

as deposit and domestic money transer services

remain peripheral in the case o most MFIs, although

there are exceptions such as the unit desas o the BRI,Grameen Bank, and ACLEDA Bank, which have made

signiicant progress in broadening their inancial

services (Rutherord 2006; Clark 2006).

In most countries, majority o the population do

not have access to ormal insurance services, although

microinsurance services in a number o countries

have begun to expand in recent years. About 86% o

Indonesians were not covered by any health insurance

scheme in 2001. In India, about 90% o the population

is not served by the insurance industry. The exclusion

rates in other countries are also alarmingly high: 97%in Bangladesh, 97% in Pakistan, and 95% in Nepal.

5 Insurance penetration ratio is an indicator used to measure the level o risk awareness in the population and signifcance o insurance inan economy.

A recent global study estimated the number o lives

covered by ormal insurance policies in 100 poorest

countries at no more than 78 million (Roth et. al. 2007).

The comparatively low insurance penetration ratios5

in developing countries shown in table 2 refect the

access problem.

A majority o the population in most developing

countries in the Pacic sub-region also do not have

access to ormal or semi-ormal nancial services.

A recent inancial sector assessment covering the

Solomon Islands, Vanuatu, Samoa, Tuvalu and Kiribati

noted that only about 20% o the population o these

ve countries have access to nancial services. Most

o the banking is conducted in the capital cities.

In the Solomon Islands,

about 90% o all banking

sector savings accounts

and loan are based in thebranches o the capital

city. The percentage o

the rural population that

can access the branches

in the provinces is small because o logistic constraints

(Flaming and Mathison 2007).

aInsurancepenetrationisgrossinsurance premiumas a% ofgrossdomestic

product.Source:SwissRe.2006.

Table 2: Insurance Penetration Ratioa:Selected Countries, 2005

Developing Countries Insurance Penetration(%)

Bangladesh 0.61

People’sRepublicofChina 2.70

India 3.14

Indonesia 1.52

Pakistan 0.67

Philippines 1.48

SriLanka 1.46

Developed Countries

Japan 10.54

UnitedKingdom 12.45

UnitedStatesofAmerica 9.15

RepublicofKorea 10.25

Low-income people with access to credit are

too heavily dependent on the services that

specialized microinance institutions (MFIs)

provide.

8/6/2019 Low Income Household Improvement

http://slidepdf.com/reader/full/low-income-household-improvement 18/46

Dimensions o the Access Problem

Thus, developing Asia clearly suers rom a

massive nancial access problem quantitatively and

qualitatively. The problem

is more acute in large

countries such as the

PRC, India, and Pakistan.

As a result, vast numbers

o poor and low-income

people in the region are

unable to take advantage

o economic opportunities and gainully employ

themselves and their amily members, and create

employment opportunities or others; unable to build

assets that increase their income-earning capacity and

quality o lie; unable to ensure that their children get

basic primary and secondary education; and unable

to manage the risks o vulnerabilities resulting rom

various types o external shocks that adversely aecttheir already low living standards. Many small armers

and small nonarm enterprise operators who are just

above the poverty line also suer rom lack o access

to nancial services. Faced with credit constraints

many small armers use ewer cash inputs leading

to lower incomes. They are also compelled to rely on

sel-nance6 and inormal markets. Many o these

people are orced by the circumstances to pay a

“poverty premium” when they access the services o

commercial inormal markets. Although it is not the

only cause, lack o access to nancial services lies at

the root o the persistent

poverty and inequality

p r o b l e m s i n m o s t

developing societies.

Given the severity o

the problem, widespread

a n d a r - r e a c h i n g

economic and social

implications o lack o access to nancial services

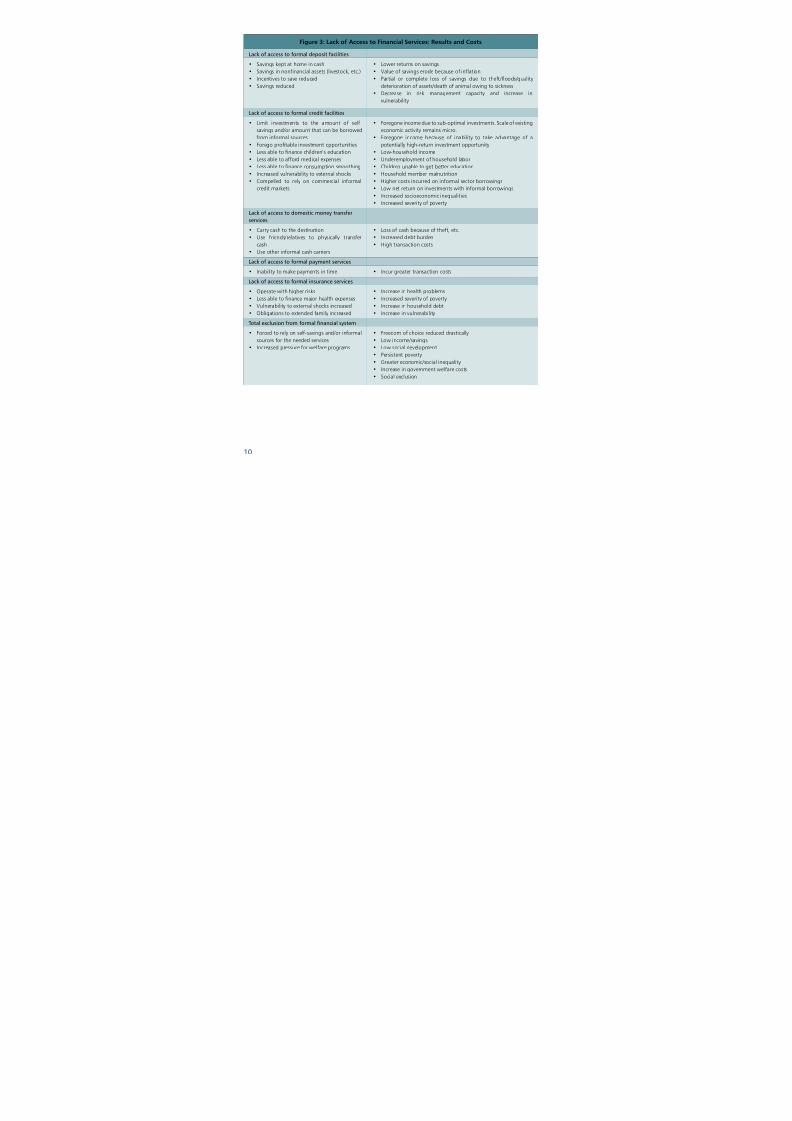

(gure 3) and the potentially critical role that nance

can play in inclusive development, closing the huge

gap between the demand or nancial services rom

low-income households and its supply rom the

ormal and semiormal sources in both quantitative

and qualitative terms may be considered one o

the biggest development challenges acing mostdeveloping countries in Asia and other regions. The

international experience provides that some countries

have remarkably progressed in improving access to

nance or low-income households while some others

have not been able to achieve relatively successul

results. An examination o these dierent experiences

suggests insights and lessons or the policy makers

and practitioners who are serious about addressing

this important development issue.

Developing Asia clearly suers rom a massive

inancial access problem quantitatively and

qualitatively. The problem is more acute in large

countries such as the PRC, India, and Pakistan.

6 McKinnon (1973, 30) defnes sel-fnance “as the investment within a particular enterprise (or economic unit) o savings accumulated inthat enterprise.” Sel-fnance takes place in all types o households and enterprises, rom rich to poor people, and rom microenterprisesto the very large-scale multinational frms. The main disadvantage o sel-fnance is that a household’s or enterprise’s resources may notmatch those required to harness an investment opportunity within a reasonable time rame. Thus, a household or an enterprise may not

be able to take advantage o a high-productivity investment opportunity. The scale o an economic activity or an enterprise will have to belimited by the amount o sel-fnance. The shortcomings o sel-fnance will be more pronounced when investments are characterized by indivisibilities. A poor household may require unds to buy cattle, a sewing machine, or a bag o ertilizer. The amount o unds required may be large relative to the income o a household living at subsistence level. Hence, the household may not be able to fnance the investment inone lump sum but may be able to do so in installments. A poor household that is not able to sel-fnance discrete increases in investments

will be compelled to use traditional technology and continue with low-productivity activities. Thus, McKinnon (1973, 13) noted that “poverty and the inability to borrow can be ormidable barriers to the adoption o even the simplest and most productive innovations. The importantpoint, however, is the virtual impossibility o a poor armer’s fnancing rom his current savings the whole o the balanced investmentneeded to adopt the new technology. Access to external fnancial resources is likely to be necessary over the one or two years when thechanges take place. Without this access, the constraint o sel-fnance sharply biases investment strategy toward marginal variations withinthe traditional technology.” Sel-fnance limits specialization, adoption o better technology, growth in productivity, and thus economicgrowth and development (ADB 2000, 44–45). Conversely, access to fnance promotes these.

8/6/2019 Low Income Household Improvement

http://slidepdf.com/reader/full/low-income-household-improvement 19/46

0

Figure 3: Lack of Access to Financial Services: Results and Costs

• Lowerreturnsonsavings

• Valueofsavingserodebecauseofinflation

• Partial or complete loss of savings due to theft/floods/quality

deteriorationofassets/deathofanimalowingtosickness

• Decrease in risk management capacity and increase invulnerability

• Foregoneincomeduetosub-optimalinvestments.Scaleofexisting

economicactivityremainsmicro.

• Foregone income because of inability to take advantage of a

potentiallyhigh-returninvestmentopportunity

• Low-householdincome

• Underemploymentofhouseholdlabor

• Childrenunabletogetbettereducation

• Householdmembermalnutrition

• Highercostsincurredoninformalsectorborrowings

• Lownetreturnoninvestmentswithinformalborrowings

• Increasedsocioeconomicinequalities

• Increasedseverityofpoverty

• Lossofcashbecauseoftheft,etc.

• Increaseddebtburden

• Hightransactioncosts

• Incurgreatertransactioncosts

• Increaseinhealthproblems

• Increasedseverityofpoverty

• Increaseinhouseholddebt

• Increaseinvulnerability

• Freedomofchoicereduceddrastically

• Lowincome/savings

• Lowsocialdevelopment

• Persistentpoverty

• Greatereconomic/socialinequality

• Increaseingovernmentwelfarecosts• Socialexclusion

Lack of access to formal deposit facilities

• Savingskeptathomeincash

• Savingsinnonfinancialassets(livestock,etc.)

• Incentivestosavereduced

• Savingsreduced

Lack of access to formal credit facilities

• Limit investments to the amount of self-

savingsand/oramountthatcanbeborrowed

frominformalsources

• Foregoprofitableinvestmentopportunities

• Lessabletofinancechildren’seducation

• Lessabletoaffordmedicalexpenses

• Lessabletofinanceconsumptionsmoothing

• Increasedvulnerabilitytoexternalshocks

• Compelled to rely on commercial informal

creditmarkets

Lack of access to domestic money transfer

services

• Carrycashtothedestination

• Use friends/relatives to physically transfer

cash

• Useotherinformalcashcarriers

Lack of access to formal payment services

• Inabilitytomakepaymentsintime

Lack of access to formal insurance services

• Operatewithhigherrisks

• Lessabletofinancemajorhealthexpenses

• Vulnerabilitytoexternalshocksincreased

• Obligationstoextendedfamilyincreased

Total exclusion from formal financial system

• Forcedtorelyonself-savingsand/orinformal

sourcesfortheneededservices

• Increasedpressureforwelfareprograms

8/6/2019 Low Income Household Improvement

http://slidepdf.com/reader/full/low-income-household-improvement 20/46

Factors Underlying Low Access

IV. FACTORS UNDERLYING LOW ACCESS

A signicant proportion o people excluded romthe ormal nancial system have access to and use

nancial services o the inormal sector. This indicates

that the limited access to ormal or semiormal sources

o inance cannot be solely explained in terms o

market ailure. The persistence o the inormal markets

not only suggests the

importance o inancial

services rom the demand

side, but also reveals

undamental supply-side

constraints in the ormalinancial system. These

constraints vary across countries and are infuenced

by a host o actors such as the stage o nancial sector

development, perceptions o dominant inancial

institutions regarding the business case or providing

nancial services or the excluded, nancial policy and

regulatory system, and the institutional composition

o the nancial system.

A root cause o supply-side constraints is the

conventional view o the potential market consisting

o poor and low-income people. Two interrelated ideasdominate the conventional view. First is that given low-

income levels and lagging social development, there

is little prot potential in the low end o the nancial

markets; hence, the conclusion that market-based

solutions cannot lead to improved nancial services or

low-income people and that the private sector has no

signicant role in this market segment. Second is that

because this market consists o low-income people,

it must be served through government programs and

programs o charitable institutions including social-

mission-oriented nongovernment organizations.Most ormal-sector-established nancial institutions,

international development agencies, and government

policy makers including those working in ministries

o nance, central banks, and national planning andimplementing agencies share these views. Even low-

income people hold similar views, with their deep

suspicion o the intentions and the role o the private

sector. Most o the supply-side actors that contribute to

low access to nance nd their roots in these conventional,

deep-rooted, and widely

held views. This dominant

thinking has contributed

to a “business ailure”

in serving this market,

although much o thelimited access to ormal

inancial services or low-income households is

generally described as “market ailure.”

Perhaps, the most obvious supply-side actor is

the absence o ormal nancial institutions in close

proximity. Thus, many low-income people in remote

rural areas where such acilities are not available

within a reasonable distance tend to rely more on

inormal markets than those in other areas. However,

availability o retail outlets in close proximity does

not oten help i these institutions are not seriously committed to serve the low-end market taking it as a

business proposition, and their core business does not

include products and services that low-income people

demand at reasonable prices. The geographic (spatial)

access does not necessarily mean economic access

in such cases. India seems to provide an example o

this. Over 95 commercial banks operating in India

have some 47,000 branches located in semiurban

and rural areas while 196 regional rural banks also

have over 14,372 branches in rural areas. In addition,

there are 105,000 primary agricultural credit societies.Despite this extensive retail network, access to nance

continues to be dismally low in rural India, particularly

or low-income households, as noted earlier.7 Similarly,

7 However, it is important to note that some studies have highlighted major banking inrastructure defciencies in rural India. For example,according to Diamond Management and Technology Consultants (2006), only 7% o villages have a bank branch and 67% do not even havea post ofce. Availability o brick and mortar acilities may be important, although its signifcance or access to fnance is likely to decreasesignifcantly with new inormation and communication technology that would connect remote rural areas to semiurban or urban-basedacilities.

The persistence o the inormal markets not

only suggests the importance o inancial

services rom the demand side, but also reveals

undamental supply-side constraints in the

ormal nancial system.

8/6/2019 Low Income Household Improvement

http://slidepdf.com/reader/full/low-income-household-improvement 21/46

in all developing countries, urban areas have much

better banking inrastructure but the majority o low-

income households do not have access to the services

provided by these institutions.

Another major reason or the limited supply is that

established medium- and large-scale conventional

nancial institutions have not yet become major players

in the low end o the nancial markets. First, these

institutions have not been established and organized

to serve the low-end markets. They do not have access

to low-cost inormation on the potential clients at

the low-end markets. Their organizational structures,

cost structures, and products are geared to serve

up-market clients. Given

the higher costs generally

associated with serving

low-income clients, these

nancial institutions ndthat the impetus to move

urther up market is more

powerul than that or

moving down-market. Hence, established, large-scale

conventional nancial institutions seldom attempt

to serve low-income households because the relative

contribution that such a move can make to prot is

smaller.8 The long-held, deep-rooted presumption

that prot is small at the

bottom o the pyramid

market and meeting theirdemand or inancial

(and other) services is the

primary responsibility

o the governments and

charitable organizations

seems to have reinorced this incentive asymmetry.

Managers o conventional medium- and large-scale

institutions who would like to introduce innovative

technology and processes to serve poor clients or

prot will oten nd it dicult to get their proposals

through the resource allocation processes and systems within their institutions.

The incompatibility o services and products

oered by the suppliers with the product and service

requirements o those in the low-end markets has

aggravated the access problem. Oten even low-

income people living in close proximity to ormal

nancial institutions do not have access to products

and services or this reason. The incompatibility may

stem rom a number o actors. The products may have

eatures that are not in line with the socioeconomic

characteristics o clients. A loan product requiring

weekly repayments may not be suitable or a

household whose cash fow does not enable such

repayments. An insurance product whose terms and

conditions are not readily transparent and simple may

not be suitable or people with limited literacy skills.

I having an account with

the bank is required to use

its payment services, some

people may not be able to

actually use those services.The eective price o a

product including client

transaction costs may be

too high. Most migrant workers have been using

inormal money transer services to remit money

because they are relatively cheaper and more

convenient than most ormal mechanisms. Most banks

require high minimum balances or savings accounts,

do not accept savings in

small amounts, and have

restrictions on requency o withdrawals. These

actors have kept millions

o small savers rom using

their deposit acilities

(Rutherord 2000), driving

them to save under the mattress despite the risks such

practices entail. In Nepal, the high required minimum

balance and the cumbersome documentation

requirements to open a savings account limit many

low-income people’s access to deposit services o

banks.In most developing countries procedures

associated with transactions are too complex,

cumbersome, and intimidating or most low-income

8 As Christensen et. al. (2004, 36) noted, “an opportunity that is attractive to a frm that has $50 million in sales and seeks 10 percent top-linegrowth would be unattractive to a frm that has $5 billion in sales and seeks 10 percent top-line growth. A $2.5 million opportunity meets50 percent o the frst frm’s growth needs but only 0.5 percent o the second frm’s growth needs. Which company do you think will placea higher priority on going ater a $2.5 million market?”

The incompatibility o services and products

oered by the suppliers with the product and

service requirements o those in the low-end

markets has aggravated the access problem.

In most developing countries procedures

associated with transactions are too complex,

cumbersome, and intimidating or most low-

income clients, particularly those with low

literacy levels and or poor women.

8/6/2019 Low Income Household Improvement

http://slidepdf.com/reader/full/low-income-household-improvement 22/46

Factors Underlying Low Access

clients, particularly those with low literacy levels and

or poor women. Most institutions do not have simple,

low-end-market-riendly systems and procedures. In

Bangladesh, more than three documents are required

to open a savings account in a bank and minimum

loan requirements o banks are too high in relation to

the typical requirements o low-income households.

Banks also take more than a month to process a

small enterprise loan application. In some states

o India, a commercial bank takes, on average, 33

weeks to approve a loan (World Bank 2004, 15). More

importantly, banks require marketable collateral or

loans which most low-

income households are

unable to provide. In some

countries, the collateral

requirements are so high

that even middle-classclients are unable to meet

them. In Azerbaijan, or

example, banks usually

require 125–200% collateral as guarantees or loans

and accept only real estate properties in Baku city

as collateral (Lamberte and Fitchett 2006, 110). Most

nancial institutions, including MFIs, do not provide

emergency loans and loans or lie-cycle events or

which eective demand at

the base o the economic

pyramid is substantial. Although poor and low-

income clients demand

simple, no-nonsense, easy

to understand inancial

products and services,

most conventional nancial institutions do not oer

such products and services.

Most supply-side constraints have been reinorced

by, i they are not rooted in, what may be described as

“government ailure.” The global experience provides

ample support to this hypothesis. In general, accessis much lower in countries where governments have

not adopted market-riendly policies toward access

to inance. Where governments have signiicantly

restricted the potential role o the private sector

including NGOs, and restricted the operational

autonomy o nancial services providers (including

that o state-owned inancial institutions with a

social mission to serve the poor) through interest rate

ceilings and other measures, the growth in supply o

services has been sluggish. Also, in countries where

governments have imposed regulatory barriers on,

or not provided adequate legal space to acilitate,

integration o nancial services or the poor into the

mainstream o nance, the growth in supply has been

lackluster. Restrictive government policies on oreign

investments in nancial services or the poor have also

retarded the supply.

Demand-side actors

also explain the limited

access to nance or low-

income people. First, many

poor and low-incomepeople cannot aord to

bear the high eective

costs involved in using

ormal nancial services. In Nepal, an estimated 34%

o the population cannot aord the ees and charges

associated with a bank savings account (Beck et. al.

2007). While a signicant proportion o the excluded

people use services provided by a range o inormal

sources o nance, some

people are even excluded

rom inormal commercialmarkets.9 Many experts

i n m i c r o e n t e r p r i s e

development tend to

assume that millions and

millions o high-return

economic activities in which poor people can invest

their loan proceeds exist. This is ar rom reality. A

closer look at dierent segments o the market or

nancial services or the poor suggests that many

poor households do not have viable economic

opportunities that can generate high enough real rateso return to repay loans at interest rates that enable

nancial institutions to cover their costs, make an

adequate prot, and save some money or a rainy day.

In a typical developing economy in the region, the

9 Inormal fnancial markets consist o two subtypes: noncommercial and commercial. Friends and relatives who provide fnancial serviceson reciprocal arrangements without a proft motive are noncommercial while those who provide loans or proft are commercial.

More importantly, banks require marketable

collateral or loans which most low-income

households are unable to provide. In some

countries, the collateral requirements are so

high that even middle-class clients are unable

to meet them.

Many experts in microenterprise development

tend to assume that millions and millions o high-return economic activities in which poor

people can invest their loan proceeds exist. This

is ar rom reality.

8/6/2019 Low Income Household Improvement

http://slidepdf.com/reader/full/low-income-household-improvement 23/46

best available investments or many poor households

involve those with moderate real returns (Fernando

2006, 8). Thus, many people who belong to this

category tend to sel-exclude

rom ormal nancial markets

and rely on sel-savings or

reciprocal arrangements to

meet their demand or credit.

Most small and marginal

armers, particularly those in

what is generally described

as less-avored areas all into

this category. As Rajan and Zingales (2004, 113) noted,

“nance cannot create opportunities. It only makes it

easier to exploit them.”

High transaction costs o using ormal nancial

services severely limit the access o low-income people

to ormal nancial services because the incidence o transaction costs is too high on small value transactions.

Transaction costs are the costs o establishing and

conducting nancial relationships: hence, they are

admission tickets to nancial markets (Von Pischke

1991, 11). High transaction costs arise rom a variety

o actors such as lack o retail outlets in close

proximity, complex and cumbersome requirements

and procedures o the ormal institutions, and corrupt

practices adopted by

sta o some ormal

institutions, as noted

earlier.

L o w i n a n c i a l

l i t e r a c y o p o o r

a n d l o w - i n c o m e

people signiicantly

contributes to nancial

exclusion in general and sel-exclusion in particular.

Many low-income households do not access insurance

services and deposit acilities, among many other

nancial services, because o this actor. The impact

o this is reinorced by the complex procedures and

requirements o ormal nancial institutions. In mosto the Pacic developing countries, nancial illiteracy

is considered a major actor limiting access to nance

because most o the population have conducted

transactions without using nancial institutions or

generations (Flaming and Mathison 2007, 4).

Overview o Cross-Country Experience

High transaction costs o using ormal nancial

services severely limit the access o low-income

people to ormal nancial services because the

incidence o transaction costs is too high on

small value transactions.

8/6/2019 Low Income Household Improvement

http://slidepdf.com/reader/full/low-income-household-improvement 24/46

Overview o Cross-Country Experience

10 India began nationalization o banks in 1969. The regional rural banks were established in 1976 to service the rural poor, small and marginalarmers, rural artisans, landless workers, and small entrepreneurs. The Integrated Rural Development Program (IRDP) provided highly subsidized credit to rural households in the 1980s and 1990s.

11 According to the World Bank (2006, 15) “the two decades o IRDP experience in the 1980s and 1990s aected the credibility o microborrowersin the view o bankers and ultimately hindered the access o low-income clients to banking services.”

12 In October 2002, ADBP was incorporated as Zarai Taraqiati Bank Ltd. as an initial step o a government-initiated restructuring programsupported by ADB. However, implementation o the program has been patchy, and much o its deep-rooted problems remain.

V. OVERVIEW OF CROSS-COUNTRY EXPERIENCE

Historically governments in many Asian andother countries have intervened on the supply

side to address access to nancial services in various

ways. These measures include nationalizing private

banks; establishing and promoting specialized banks

including national savings banks and postal banks,

branching regulations or directives, directives on

portolio composition, interest rate ceilings on credit

to low-income households, and provision o credit

at subsidized interest rates to what was considered

priority sectors o the economy or priority segments

o the society. For example, India, Sri Lanka, andPakistan nationalized private-owned banks to expand

banking services to the excluded and established new

state-owned banks to serve low-income segments.10

India’s social banking program and priority sector

lending program meant to increas e banking services

to the poor and low-income households and rural

people. While an evaluation o the eectiveness o

these measures is beyond the scope o this paper, it is

correct to say that some o these did produce positive

results (Burgess and Pande 2005) while some did, in

eect, urther curtail the supply contrary to the policy makers’ expectations.11

In most cases, newly established state-owned

inancial institutions

a i l e d t o m a k e a

sustainable dent in the

problem despite the large

amount o unds used or

the purpose. Pakistan’s

Agricultural Development

Bank (ADBP)12 is one o

many examples. These institutions have also createdtheir own constituency o supporters making their

reorms a politically more daunting task and ensuring their persistence despite continuing nancial bleeding,

ineciency, dismally low outreach, and poor quality

o services. More importantly, these institutions have

ailed to serve their stated target groups. Similarly,

nationalized nancial institutions have ailed to live up

to the stated objectives o policy makers and inficted

signicant costs on the society. The operations o

both categories o institutions have promoted rent-

seeking behavior among their sta and clients and

damaged development o a disciplined credit culture.

There is general agreement that in most countriesthe conventional supply-side measures contributed

to the weakening o nancial institutions and their

implementation involved huge nancial costs (Meyer

and Nagarajan 2000). Whether they produced benets

proportional to the costs remain controversial. Many

people who are keen to improve access to nance

agree that the old approach o direct interventions

to provide the services by government-owned or

controlled institutions and to orce the private sector

institutions to provide the services is no longer relevant

and eective, even i it has worked to some extent inthe past. A new, more market-riendly and market-

supportive demand-driven approach has gained

increasing support at

global, regional, and

national levels.

The countries that

adopted a more market-

riendly approach to

access to inance have

achieved sustainable

results. These countries have essentially taken anumber o bold initiatives to implement such an

The countries that adopted a more market-

riendly approach to access to inance have

achieved sustainable results. These countries

have essentially taken a number o bold

initiatives to implement such an approach.

8/6/2019 Low Income Household Improvement

http://slidepdf.com/reader/full/low-income-household-improvement 25/46

(Position as of December 00)

Khan Bank BRI

NumberofActiveBorrowers 234,715 3,455,894

NumberofSavingsAccounts 717,824 30,907,566

GrossLoanPortfolio($million) 201.90 3,035.70TotalSavings($million) 250.00 4,869.70

TotalAssets($million) 295.90 5,498.30

ReturnonAssets(%) 4.45 6.88

ReturnonEquity(%) 51.32 129.86

Portfolioatrisk–over30days(%) – 5.07

Operatingexpenseratio(%) – 8.26

Costperborrower($) 123.80 65.30

Table 3: Khan Bank (Mongolia) and Bank RakyatIndonesia (BRI) Selected Performance Indicators

Source:www.mixmarket.org

approach. Some o these countries have eectively

reormed existing state-owned nancial institutions

with a mandate to serve low-income clients and

given those institutions the reedom to adopt market-

oriented, demand-driven policies and practices. These

policies and reorms have produced robust and viable

nancial institutions serving the poor and low-income

households. Indonesia and Mongolia belong to this

category. In the case o Mongolia, the state-owned

Agricultural Bank o Mongolia was insolvent in 1995,

illiquid in 1999, and plagued by unrecoverable loans

that government oicials promoted prior to the

reorms. The cost o operating this bank was borne by

the Government. The bank’s operational and nancial

problems were so acute that most analysts presumed

reorming this bank was impossible. With external

assistance, the Government successully reormed this

bank during 2000–2002 and sold it to a oreign-ownedprivate sector company

in 2003 (Dyer et. al. 2004).

Contrary to many people’s

skepticism that it will

not continue, let alone

expand, rural inancial

services under the private

ownership, Khan Bank

(new name o the ormer

bank) has signiicantly

improved access to a wide range o nancial servicesor previously unserved and underserved clients in

urban and rural areas. It has also achieved remarkable

results in mobilizing deposits by providing quality,

reliable, and sae deposit services to a wide range o

clients. At the end o August 2007, outstanding deposits

amounted to $390.5 million in 1,528,879 accounts.

The previously nonviable, poor-quality, credit-only

nancial institution has become a viable nancial

intermediary that adds value to the nancial system

and increases people’s choices. Khan Bank’s return on

equity was 51.3% at the end o 2006 (table 3). The bank serves about 80% o the households in the country.

In Indonesia, during 1983–1986, the Government

successully reormed the unit desa system o the Bank

Rakyat Indonesia (BRI) which was about to collapse

because o political intervention, poor management,

and high deault rates, among other things. The reorms

led to the emergence o one o the most successul

state-owned rural nancial institutions in the world. A

major element o the reorm program was the reedom

given to BRI management to set cost-recovery and

market-oriented interest rates on loans and deposits.

The Government also ensured elimination o political

interventions in the operation o the unit desa system

and access to high-quality technical assistance to

carry out the necessary reorms in operations. The

reorms transormed the unit desa system into a viable

operation and a robust entity by 1987. It has continued

to generate proits with increasing outreach ever

since on a continuing basis. In 2002, the Government

allowed private sector ownership o this bank through

an initial public oering. Currently, private sector

shareholders account or about 48% o its share

capital. At the end o 2006, BRI units had 4,112 outlets

with over 3.45 million borrowers and 30.9 million

savings accounts. The value o their outstanding loansamounted to $3.04 billion

while deposits amounted

to $4.87 billion, indicating

a deposit-to-loan ratio o

160%. BRI continues to

expand its services to

the poor and low-income

h o u s e h o l d s , a m o n g

others, on a proitable

basis. The average annual

prots o BRI unit desas amounted to $199 millionin 2001–2006 while in 2006 the units reported $329

million in prots. At the end o 2006, the ROA and ROE

were 6.9% and 130%, respectively (table 3).

Contrary to many people’s skepticism that

it will not continue, let alone expand, rural

nancial services under the private ownership,

Khan Bank (new name o the ormer bank) has

signicantly improved access to a wide range o

nancial services or previously unserved and

underserved clients in urban and rural areas.

8/6/2019 Low Income Household Improvement

http://slidepdf.com/reader/full/low-income-household-improvement 26/46

Overview o Cross-Country Experience

Indonesia’s market-oriented and liberal approach

to nancial services is urther refected in its policy

toward the operations o the state-owned pawning

company, Perum Pegadaian. Again the Government

has given operational and management autonomy

to this institution to adopt market-oriented pricing

policies. The company provides services throughout

the country to a wide range o clients through its branch

network o 840 branches and 13 regional oces. In

2003, it provided over $1.0 billion in 21 million loans

and was the major supplier o microcredit in terms o

the number o clients served (ADB 2005, 9).

Another country which has achieved a remarkably

improved access to nance

is Cambodia. The war-

torn Cambodia did not

have existing inancial

institutions to reorm in thelate 1980s. But Cambodia

allowed new microcredit

institutions to emerge

and nurtured their growth

through liberal policies.

The Government allowed

oreign investments to the

microinance sector and

micronance institutions

(MFIs) to adopt cost-

recovery interest rates without restrictions. These

two policy measures laid

the oundation or a solid

microinance sector to

emerge and grow. Two o the many such institutions

have become major players in the sector in recent

years.

ACLEDA Bank is one o these two. This institution

which had an NGO origin

is one o the ew fagship

micronance commercialbanks in the region and

serves over 150,000 poor

and low-income clients.

ACLEDA provides a wide

range o quality and reliable services protably to an

increasing number o people in the country. According