Embed Size (px)

Citation preview

Long Term Care Planning Solutions

Helping Make Sense of It All

Jack Morrone, CPA, CFP®, PFS®

Today’s Agenda

When Is Long Term Care Insurance Right for You?

Most Asked Questions about LTC

• What is LTC?

• Facts and Stats

Which LTC Solution is right for you?

Next Steps

Baby boomers and Long Term Care

Most Current Data Available

3 What to Know About Long-term Care and Medicaid- The Wealth Channel- 2011. 4 The 2011 Sourcebook for Long-term Care Insurance Information – AALTCI 2011, U.S. Census Bureau. 5 What to Know About Long-term Care and Medicaid — The Wealth Channel — 2011.

Let’s Talk –Having the LTC Discussion

… or their financial advisor

Most Current Data Available

73% – Genworth 2011 Financial Reality Check Study 59% Genworth/Age Wave. November 2010. Our Family, Our Future: The Heart of Long Term Care Planning Study 90% – Genworth/Age Wave, Our Family, Our Future, November 2010

Is Long Term Care Insurance Right for

YOU?

Are you:

• Age 40-80?

• Someone who has funds set aside as your “just in case” money?

• Concerned about what could happen to your to your retirement income?

• Concerned about who would take care of you if you needed extended health care?

• Concerned about protecting the amount of money you would like to leave for your

loved ones?

If you answered “yes” to any of the above,

Long Term Care Insurance may be right for you.

What is Long-Term Care (LTC)?

The need for care is created by two impairments…

Physical: A chronic medical condition that compromises the individual’s ability to get through the most basic of daily routines

Cognitive: A measurable decline in intellect that compromises a client’s ability to safely interact with his environment

The operative word is compromise

What Triggers Long Term Care?

Requiring assistance with Activities of Daily Living (ADL’s):

• Bathing

• Dressing

• Eating

• Continence

• Toileting

• Transferring

• Severe cognitive impairment

(mental deterioration)

Long Term Care – Where is care provided?

Assisted Living Facilities provides supervision or assistance with (ADLs); coordination of services

by outside providers; and monitoring of resident activities to help to

ensure their health, safety, and well-being.

Nursing homes

provide the most comprehensive range of services, including

nursing care and 24-hour supervision

Home Care • Unpaid caregiver (family members and friends) • Home Maker Services • A Nurse, Home Care Aide, and/or therapist

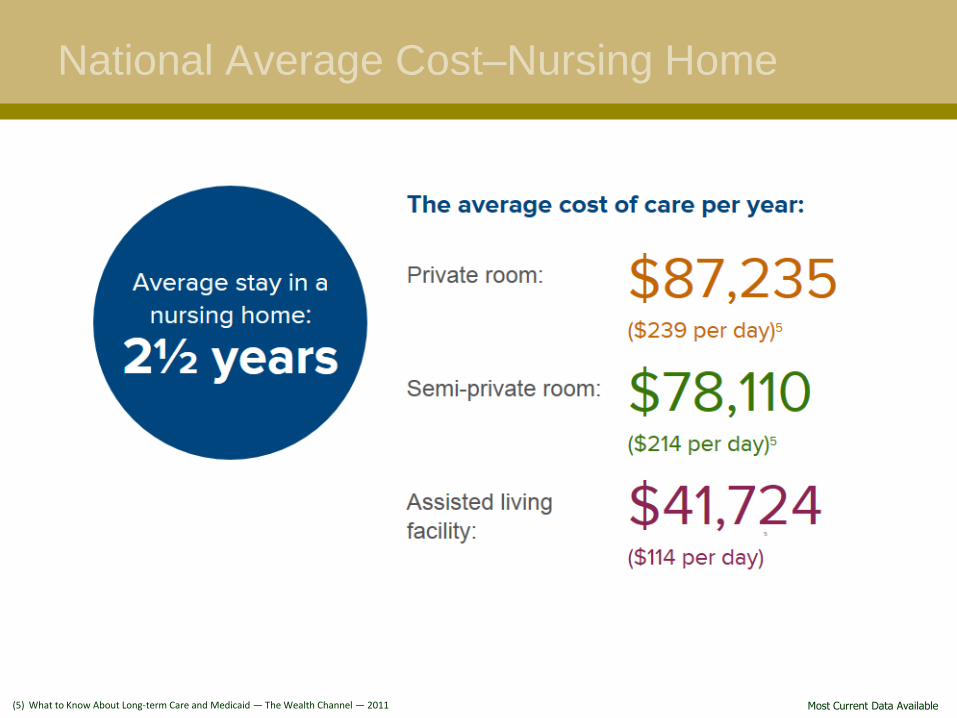

National Average Cost–Nursing Home

Most Current Data Available (5) What to Know About Long-term Care and Medicaid — The Wealth Channel — 2011

Average Cost Care – Outside of NH

Most Current Data Available (6) NCPC- National Care Planning Council - October 2012.

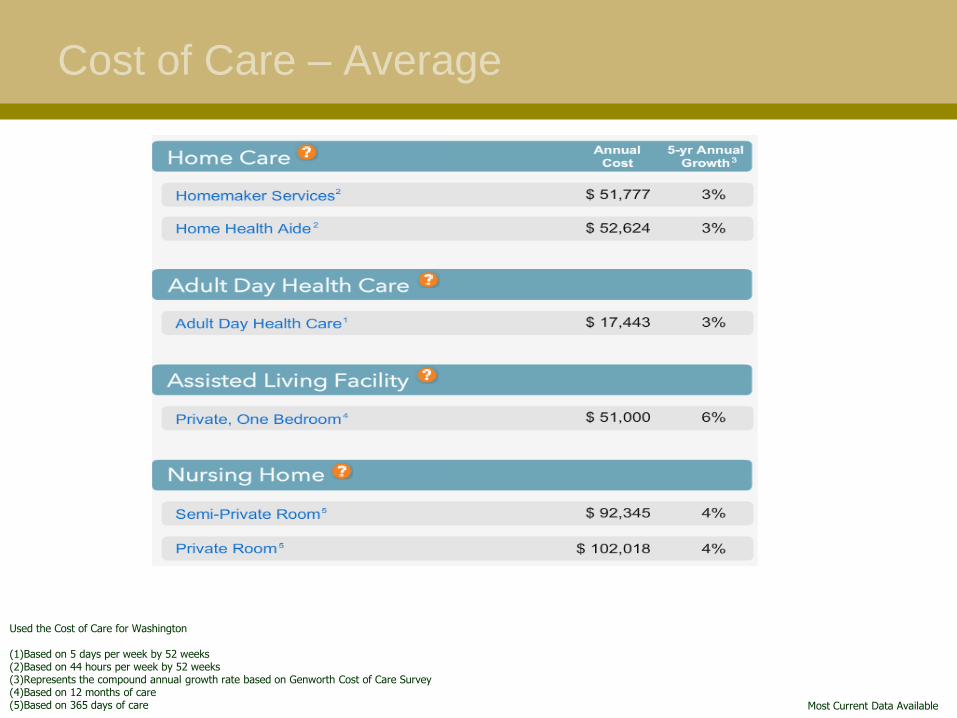

Cost of Care – Average

Most Current Data Available

Used the Cost of Care for Washington (1)Based on 5 days per week by 52 weeks (2)Based on 44 hours per week by 52 weeks (3)Represents the compound annual growth rate based on Genworth Cost of Care Survey (4)Based on 12 months of care (5)Based on 365 days of care

Who Covers What

Most Current Data Available

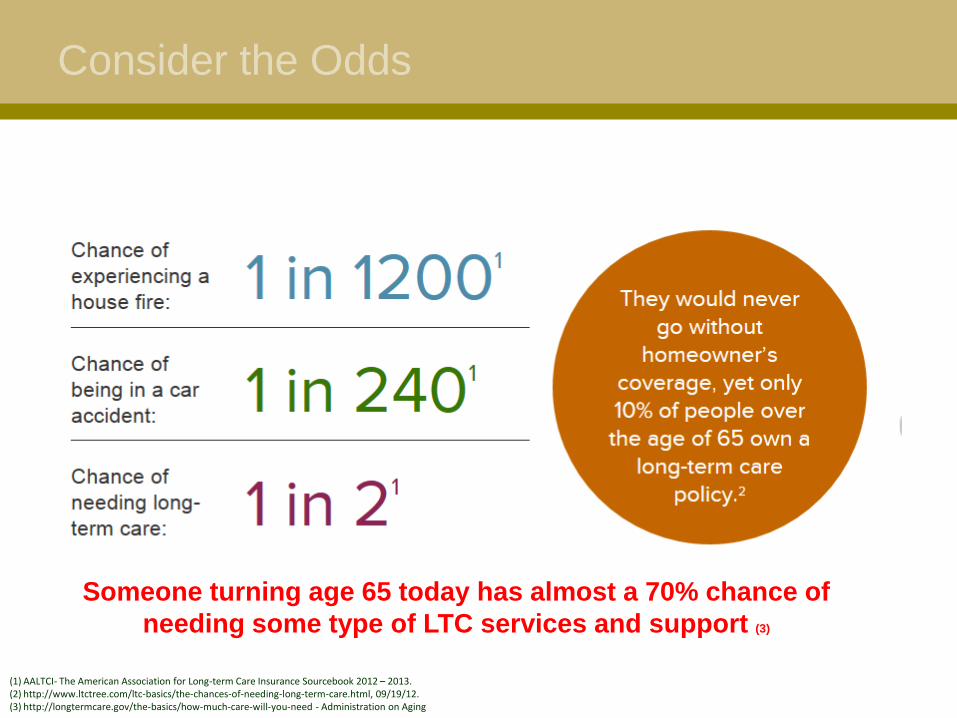

Consider the Odds

Someone turning age 65 today has almost a 70% chance of

needing some type of LTC services and support (3)

(1) AALTCI- The American Association for Long-term Care Insurance Sourcebook 2012 – 2013. (2) http://www.ltctree.com/ltc-basics/the-chances-of-needing-long-term-care.html, 09/19/12. (3) http://longtermcare.gov/the-basics/how-much-care-will-you-need - Administration on Aging

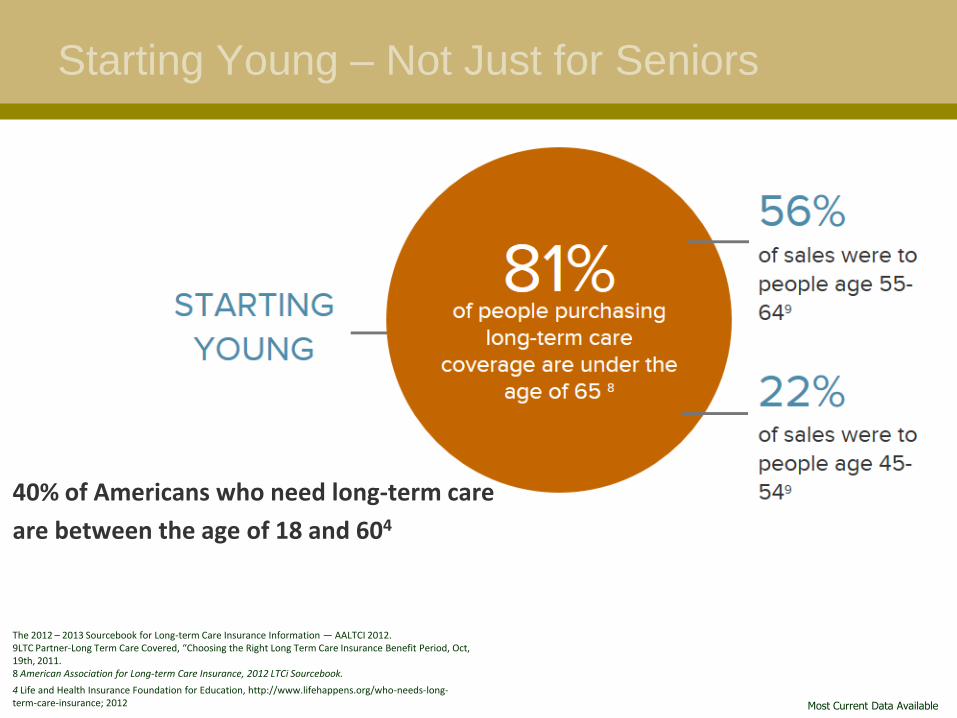

Starting Young – Not Just for Seniors

40% of Americans who need long-term care

are between the age of 18 and 604

Most Current Data Available

The 2012 – 2013 Sourcebook for Long-term Care Insurance Information — AALTCI 2012. 9LTC Partner-Long Term Care Covered, “Choosing the Right Long Term Care Insurance Benefit Period, Oct, 19th, 2011. 8 American Association for Long-term Care Insurance, 2012 LTCi Sourcebook.

4 Life and Health Insurance Foundation for Education, http://www.lifehappens.org/who-needs-long-term-care-insurance; 2012

It’s a woman thing

Most Current Data Available

8 http://www.wiserwomen.org/index.php?id=184, 09/20/12. 9 Completelongtermcare.com, August 2012. 10 Healthcare Costs in Retirement, Feb 2012, Harris Interactive.

The Need for a Plan

Most Current Data Available (7) LifeHealthPRO, “This Isn’t Your Parent’s Retirement,” October 4, 2012.

Your Long-Term Care Experiences

Who?

Where?

How was it paid for?

Who provided the care?

How long did the person need care?

Was the care expected or unexpected?

How did long-term care affect the family?

PLEASE SHARE YOUR STORIES

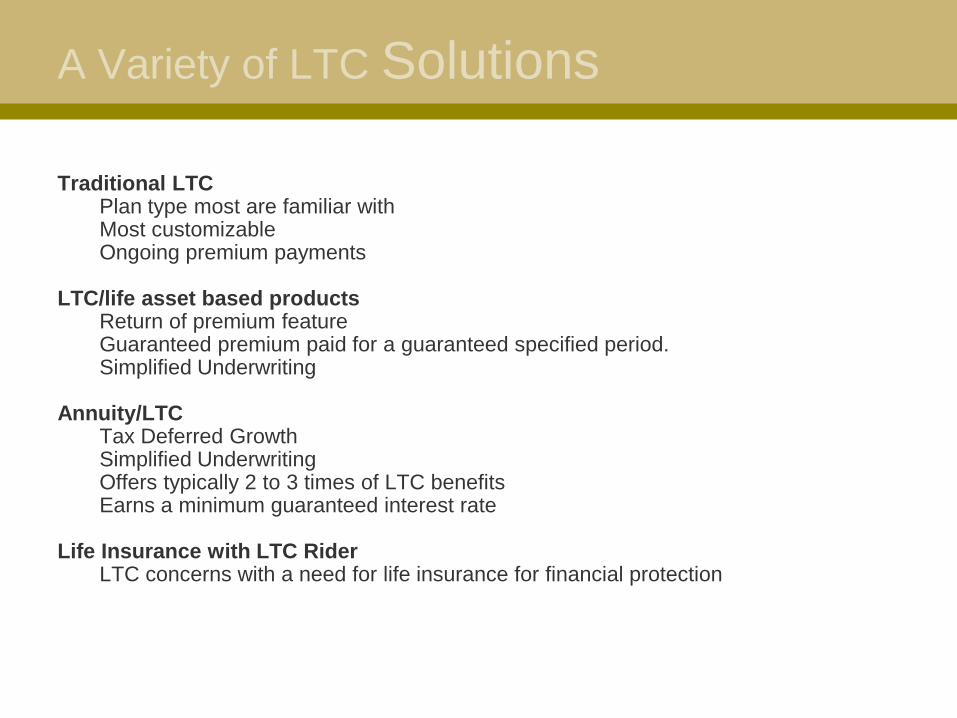

A Variety of LTC Solutions

Traditional LTC Plan type most are familiar with Most customizable Ongoing premium payments

LTC/life asset based products Return of premium feature Guaranteed premium paid for a guaranteed specified period. Simplified Underwriting

Annuity/LTC Tax Deferred Growth Simplified Underwriting Offers typically 2 to 3 times of LTC benefits Earns a minimum guaranteed interest rate

Life Insurance with LTC Rider LTC concerns with a need for life insurance for financial protection

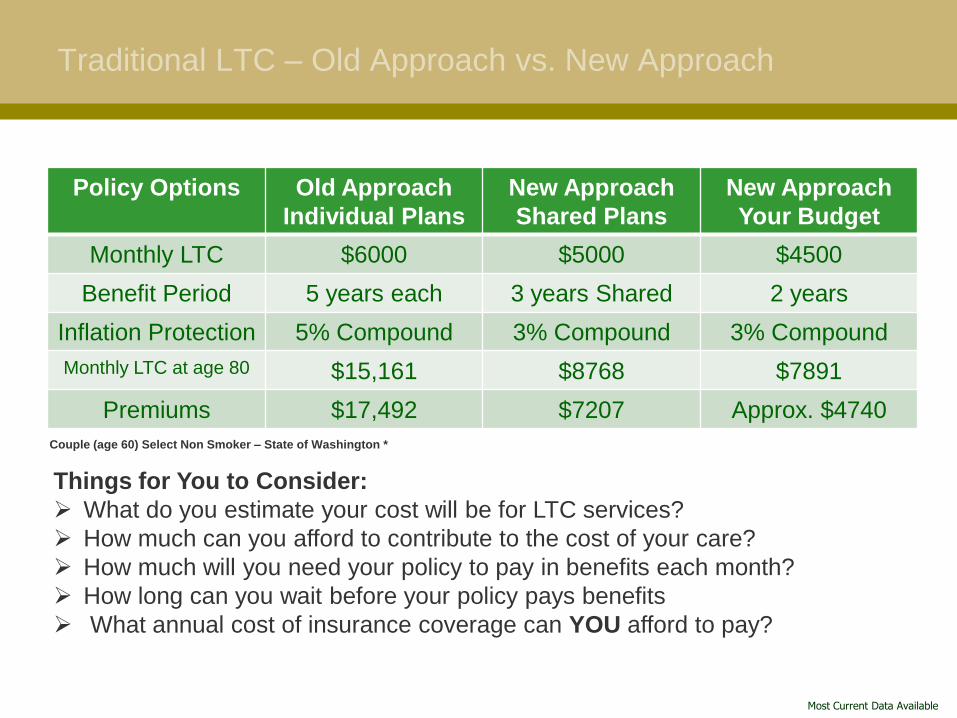

Traditional LTC – Old Approach vs. New Approach

Policy Options Old Approach

Individual Plans

New Approach

Shared Plans

New Approach

Your Budget

Monthly LTC $6000 $5000 $4500

Benefit Period 5 years each 3 years Shared 2 years

Inflation Protection 5% Compound 3% Compound 3% Compound

Monthly LTC at age 80 $15,161 $8768 $7891

Premiums $17,492 $7207 Approx. $4740

Things for You to Consider:

What do you estimate your cost will be for LTC services?

How much can you afford to contribute to the cost of your care?

How much will you need your policy to pay in benefits each month?

How long can you wait before your policy pays benefits

What annual cost of insurance coverage can YOU afford to pay?

Couple (age 60) Select Non Smoker – State of Washington *

Most Current Data Available

LTCI: Why Not Self Insure?

Most Current Data Available This is a hypothetical example and is not representative of any specific situation. Your results will vary. The hypothetical rates of return used do not reflect the deduction of fees and charges inherent to investing

Source: http://www.guidetolongtermcare.com/selfinsurechart.html

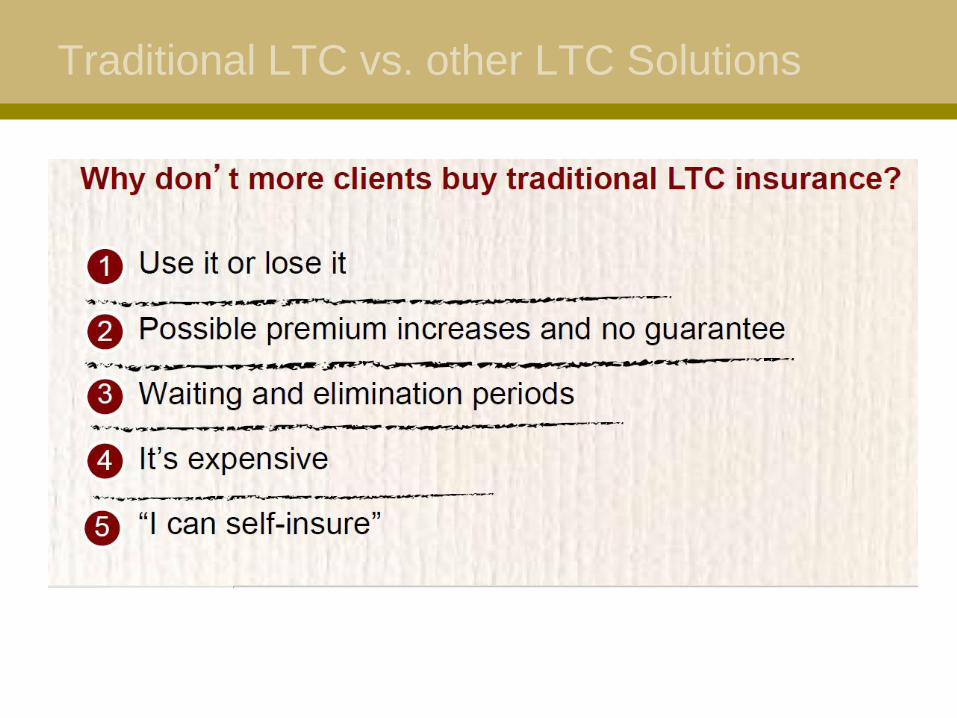

Traditional LTC vs. other LTC Solutions

Life Insurance with LTC Riders (Hybrids)

* Varies based on carriers, state and clients age

Riders are additional guarantee options that are available to an annuity or life insurance contract holder. While some riders are part of an existing contract, many others may carry additional fees, charges and restrictions, and the policy holder should review their contract carefully before purchasing. Guarantees are based on the claims paying ability of the issuing insurance company.

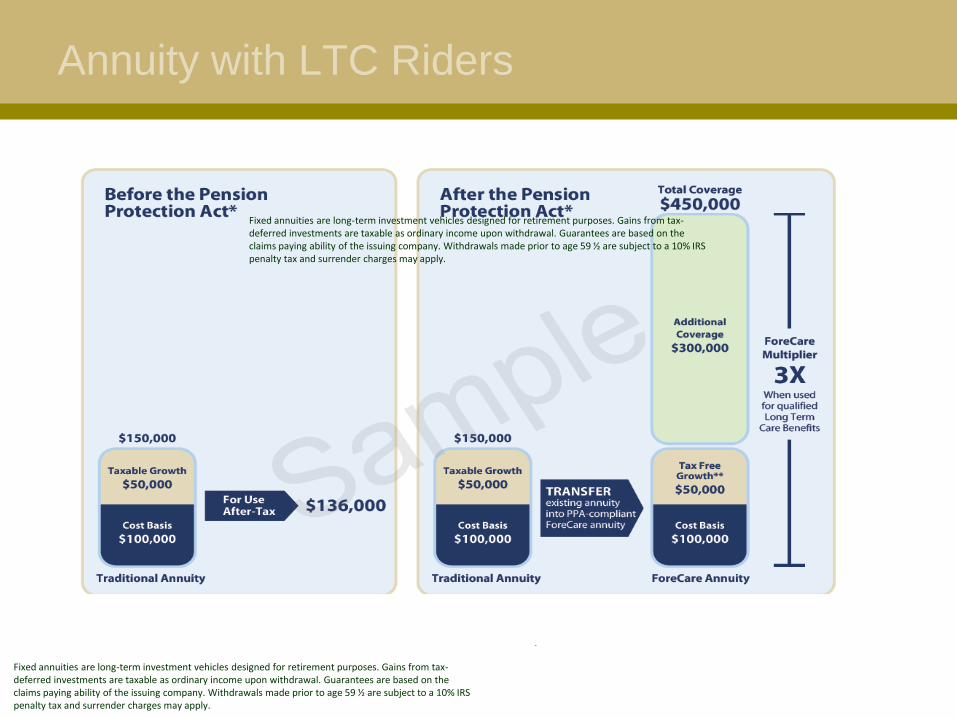

Annuity with LTC Riders

Fixed annuities are long-term investment vehicles designed for retirement purposes. Gains from tax-deferred investments are taxable as ordinary income upon withdrawal. Guarantees are based on the claims paying ability of the issuing company. Withdrawals made prior to age 59 ½ are subject to a 10% IRS penalty tax and surrender charges may apply.

Fixed annuities are long-term investment vehicles designed for retirement purposes. Gains from tax-deferred investments are taxable as ordinary income upon withdrawal. Guarantees are based on the claims paying ability of the issuing company. Withdrawals made prior to age 59 ½ are subject to a 10% IRS penalty tax and surrender charges may apply.

In Summary

The likelihood of needing long-term care is significant

The cost of such care can be financially devastating

Not covered by heath insurance

Not covered by Medicare after 100 days

Long-term care coverage is another piece in financial

and retirement considerations

Purchasing LTC insurance coverage may help preserve

financial well-being and provide peace of mind

What’s the Next Step?

DISCLOSURES:

The opinions voiced in this material are for general information only and not intended to provide specific advice or recommendations for any individual. To determine which investment (s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly.

Life insurance policies contain exclusions, limitations, reductions of benefits, and terms from keeping them in-force. Your financial professional can provide you with costs and complete details.

[Add one of the disclosures listed in the notes (Tahoma 16) to meet compliance requirements: IAS – IS – Bank/Credit Union - Hybrid.]

Insurance guarantees are based upon the claims paying ability of the issuing company. Securities offered through LPL Financial. Member FINRA/SIPC.