Embed Size (px)

Citation preview

Loganville High Loganville High SchoolSchool

4/20/20104/20/2010

Bill Inabinet, AVPBill Inabinet, AVP

Athens First Bank & TrustAthens First Bank & Trust

Outline of DiscussionOutline of Discussion

• Account OpeningAccount Opening• SavingSaving• What does a Bank Provide?What does a Bank Provide?• What goes into a Credit Score?What goes into a Credit Score?

Account OpeningAccount OpeningWhat to ExpectWhat to Expect

• What should I bring with me to open What should I bring with me to open an account?an account?– Are you 18 years of age or older?Are you 18 years of age or older?

• NO? – Parent or GuardianNO? – Parent or Guardian

– Bring two forms of identificationBring two forms of identification• Driver’s LicenseDriver’s License• Social Security Card, Student ID, etc.Social Security Card, Student ID, etc.

– Know your essential informationKnow your essential information• Social Security Number, Mother’s Maiden Social Security Number, Mother’s Maiden

NameName

Account OpeningAccount OpeningWhat to ExpectWhat to Expect

• Bring a list of Questions about the Bring a list of Questions about the account you are wanting to open…account you are wanting to open…– What does the bank charge for the account?What does the bank charge for the account?– Am I limited to any number of transactions or Am I limited to any number of transactions or

any style of banking?any style of banking?– When will I receive my statement?When will I receive my statement?– Is there a charge to view my account on-line?Is there a charge to view my account on-line?– Can I get a check card or checks or both?Can I get a check card or checks or both?– What do I do if I lose my check card or What do I do if I lose my check card or

checks?checks?

Account OpeningAccount OpeningWhat to ExpectWhat to Expect

• A bank will pull your credit before A bank will pull your credit before they allow you to have an account…they allow you to have an account…– Know what is on your credit before Know what is on your credit before

someone else looks at itsomeone else looks at it– No surprise is a good surpriseNo surprise is a good surprise– Pull your credit report annuallyPull your credit report annually

• www.annualcreditreport.com

– If your credit is poor you may not be If your credit is poor you may not be allowed to open a checking accountallowed to open a checking account

Account OpeningAccount OpeningWhat to ExpectWhat to Expect

• Standard DocumentationStandard Documentation– Signature CardSignature Card

• Lists the signers of an accountLists the signers of an account– Limits the individuals that can sign checks or Limits the individuals that can sign checks or

make withdrawals on your accountmake withdrawals on your account

• A Bank’s way to verify signaturesA Bank’s way to verify signatures– You should sign any financial information the You should sign any financial information the

way you sign your signature cardway you sign your signature card

• The legal account agreementThe legal account agreement

Signature CardSignature Card

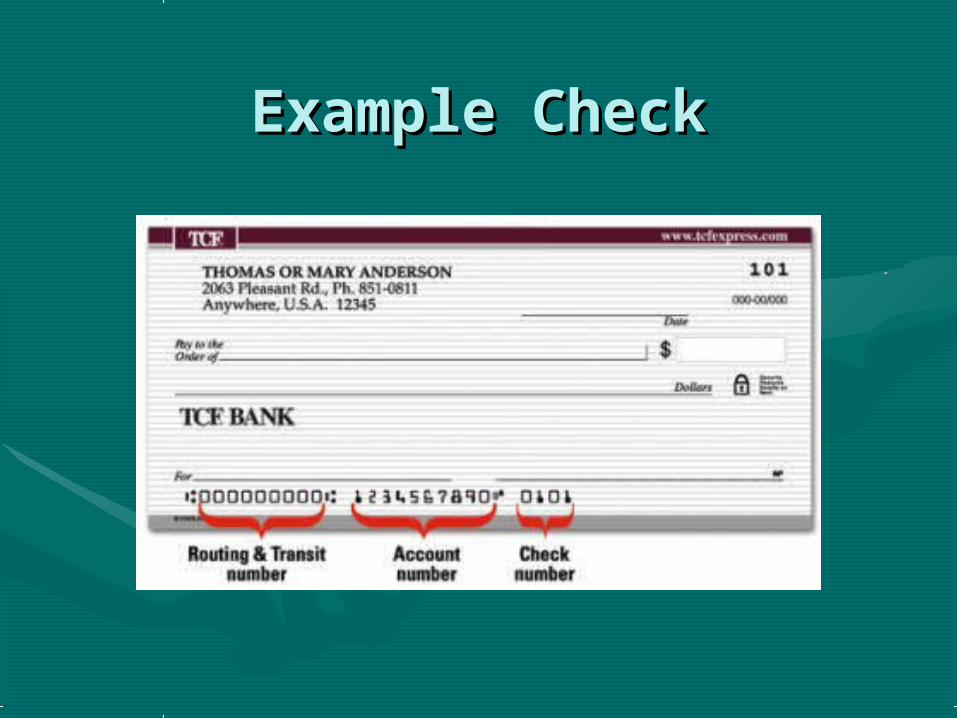

Example CheckExample Check

Example Deposit SlipExample Deposit Slip

Personal Record KeepingPersonal Record KeepingHow to keep a Check How to keep a Check

RegisterRegister• You spend $50 on gas, $45 on groceries, You spend $50 on gas, $45 on groceries,

$150 on rent, $250 on a car payment and $150 on rent, $250 on a car payment and $100 at Wal-Mart in one month$100 at Wal-Mart in one month

• What is the balance in your account at What is the balance in your account at the end of the month?the end of the month?

How can you know where you’re How can you know where you’re going if you don’t know where going if you don’t know where

you’ve started?you’ve started?

Personal Record KeepingPersonal Record KeepingHow to keep a Check How to keep a Check

RegisterRegister• Important steps to keeping a Check Important steps to keeping a Check

RegisterRegister– Be consistentBe consistent– Have a good starting pointHave a good starting point– Do the math as you goDo the math as you go– Write down everything!Write down everything!– Reconcile your bank statements monthlyReconcile your bank statements monthly– Utilize the tools you are givenUtilize the tools you are given– Just because it’s not a check or a deposit Just because it’s not a check or a deposit

doesn’t mean you don’t have to write it doesn’t mean you don’t have to write it downdown

• Keeping a check register will save Keeping a check register will save you moneyyou money– By knowing what is in your account you By knowing what is in your account you

won’t have to worry about spending won’t have to worry about spending more than you havemore than you have

– If you spend more money than you If you spend more money than you have, your account will become have, your account will become “overdrawn” causing “Overdraft” fees “overdrawn” causing “Overdraft” fees from the bank which can be as much as from the bank which can be as much as $36 per occurrence$36 per occurrence

Personal Record KeepingPersonal Record KeepingHow to keep a Check How to keep a Check

RegisterRegister

Personal Record KeepingPersonal Record KeepingHow to keep a Check How to keep a Check

RegisterRegister

Check Number

DateCompany or Person you are paying or “Cash” or “ATM”

Debit AmountReconcil

ed

Fee?Credit Amount

Balance

850 9/4 Loganville High School 10 00

515 00 505 00

Personal Record KeepingPersonal Record KeepingStatements & ReconcilingStatements & Reconciling

• When you receive you statements you When you receive you statements you should:should:– Check the transactions on your statement Check the transactions on your statement

against the transactions in your check registeragainst the transactions in your check register– Use the “Reconciled” column to check off Use the “Reconciled” column to check off

items that appear on the statement and make items that appear on the statement and make a check mark next to each transaction on your a check mark next to each transaction on your statement that is in your registerstatement that is in your register

– Add/Subtract missing itemsAdd/Subtract missing items– Shred your statements when you’re finishedShred your statements when you’re finished

Save or Borrow??Save or Borrow??

Save or Borrow??Save or Borrow??

Save or Borrow??Save or Borrow??

Save or Borrow??Save or Borrow??

Save or Borrow??Save or Borrow??

Save or Borrow??Save or Borrow??

SavingSaving

• The Starbuck’s ScenarioThe Starbuck’s Scenario• If my wife was to save $3.85 every school If my wife was to save $3.85 every school

day, that’s $19.25 a week and $1,000 per day, that’s $19.25 a week and $1,000 per year.year.

• If she was to save $3.85 per day every If she was to save $3.85 per day every day in a savings account for 25 years day in a savings account for 25 years until she’s ready to retire, how much until she’s ready to retire, how much money would she have?money would she have?

$52,580$52,580

Ways To SaveWays To Save

0100200300400500600700800900

1000

No Saving

IncomeSpending

0500

10001500

IncreaseIncome

IncomeSpending0

500

1000

DecreaseSpending

IncomeSpending

BudgetingBudgeting

• There is nothing more frustrating There is nothing more frustrating than not being in control of your than not being in control of your finances.finances.

• Budgeting is planning where each Budgeting is planning where each and every dollar should be allocated and every dollar should be allocated and tracking your finances based on and tracking your finances based on a period of a month, week, etc.a period of a month, week, etc.

Creating a BudgetCreating a Budget• To create a budget you must look at To create a budget you must look at

what you spend your money on. what you spend your money on. • Come up with as many specific Come up with as many specific

categories as possible, i.e. Housing, categories as possible, i.e. Housing, Car, Gas, Groceries, Entertainment, etc.Car, Gas, Groceries, Entertainment, etc.

• Allocate a specific dollar amount to Allocate a specific dollar amount to each category; track it, and stick to it.each category; track it, and stick to it.

• Budgeting is normally viewed Budgeting is normally viewed negatively. However, if you stick to it negatively. However, if you stick to it you can find ways to save money or find you can find ways to save money or find that you can spend more money on that you can spend more money on things that you enjoy.things that you enjoy.

Other Banking SolutionsOther Banking SolutionsDepositsDeposits

• Checking Accounts – accounts used for Checking Accounts – accounts used for day-to-day expensesday-to-day expenses

• Savings Accounts – a place to store Savings Accounts – a place to store money that you may not need money that you may not need immediately, interest bearingimmediately, interest bearing

• Money Market Accounts – like savings Money Market Accounts – like savings accounts that earns more interest but accounts that earns more interest but are limited to the number of times that are limited to the number of times that you can make withdrawals or write you can make withdrawals or write checkschecks

Other Banking SolutionsOther Banking SolutionsDepositsDeposits

• Certificate of Deposit (CD) – More Certificate of Deposit (CD) – More interest than a money market interest than a money market account with penalties for account with penalties for withdrawal before maturity.withdrawal before maturity.

• Individual Retirement Account (IRA) Individual Retirement Account (IRA) – a CD that you contribute money to – a CD that you contribute money to tax free with government penalties tax free with government penalties for withdrawal before retirement for withdrawal before retirement ageage

Other Banking SolutionsOther Banking SolutionsServicesServices

• Checks – Documents that serve as Checks – Documents that serve as payment bearing your signaturepayment bearing your signature

• Automated Teller Machines (ATMs) – Automated Teller Machines (ATMs) – Machines that allow you to withdraw Machines that allow you to withdraw cash from your bank account using cash from your bank account using an ATM or Check Cardan ATM or Check Card

• Check Cards (Debit Cards) – Plastic Check Cards (Debit Cards) – Plastic cards that allow you access to your cards that allow you access to your accounts without checks.accounts without checks.

Other Banking SolutionsOther Banking SolutionsTechnologyTechnology

• Online Banking – The most popular Online Banking – The most popular mode of banking today. mode of banking today. – You can pay bills, check balances at 2 AM You can pay bills, check balances at 2 AM

and make transfers between accountsand make transfers between accounts

• Mobile Banking – Online Banking for Mobile Banking – Online Banking for your cell phoneyour cell phone– Allows you to view online statements, Allows you to view online statements,

transfer funds, pay bills and even receive transfer funds, pay bills and even receive text messages to your cell phonetext messages to your cell phone

Other Banking SolutionsOther Banking SolutionsLoansLoans

• Credit Cards – Lines of credit Credit Cards – Lines of credit accessible through a plastic card. accessible through a plastic card. – These carry higher interest rates since These carry higher interest rates since

there is no form of collateral – there is no form of collateral – “unsecured”“unsecured”

• Car Loans – A loan that holds an Car Loans – A loan that holds an automobile as collateralautomobile as collateral– These carry middle range interest rates These carry middle range interest rates

since they are “secured” with a physical since they are “secured” with a physical objectobject

Other Banking SolutionsOther Banking SolutionsLoansLoans

• Mortgage – A home loanMortgage – A home loan– Low interest rates being secured by real Low interest rates being secured by real

estate (previously “very low risk” loans estate (previously “very low risk” loans since real estate values had consistently since real estate values had consistently risen annually)risen annually)

• Home Equity Lines of Credit – allow Home Equity Lines of Credit – allow you to take advantage of the value that you to take advantage of the value that you have in your homeyou have in your home– A Credit card with your home as collateralA Credit card with your home as collateral

How to Create/Maintain How to Create/Maintain Good CreditGood Credit

CreditCredit

““Good Credit is better than money”Good Credit is better than money” Credit Scores are determined by Fair Isaac Credit Scores are determined by Fair Isaac

& Co (FICO)& Co (FICO) Range from 300-850Range from 300-850 Why do I need good credit?Why do I need good credit?

• Connecting electricityConnecting electricity• Opening bank accountsOpening bank accounts• Telephone/Cell Phone serviceTelephone/Cell Phone service• LoansLoans• Applying for a jobApplying for a job

Why is good credit better than Why is good credit better than money?money?

Two people come in to Athens First Bank & Trust Two people come in to Athens First Bank & Trust to apply for a $10,000 car loan for 3 yearsto apply for a $10,000 car loan for 3 years

Person A has a credit score of 600 and person B Person A has a credit score of 600 and person B has a credit score of 750has a credit score of 750

Person A might get an interest rate of 9%, while Person A might get an interest rate of 9%, while person B might get a rate of 6.5%person B might get a rate of 6.5%

Person A has a payment of $318/monthPerson A has a payment of $318/month Person B has a payment of $306/monthPerson B has a payment of $306/month $12/month is a lot of money, right?$12/month is a lot of money, right?

Person B has just saved…Person B has just saved…

$432$432

Ways to Build/Strengthen CreditWays to Build/Strengthen Credit

11 Paying Bills on Time Paying Bills on Time• The most heavily weighted factor in The most heavily weighted factor in

building/maintaining creditbuilding/maintaining credit• 35% of your credit score35% of your credit score• Payment history is used as an indicator Payment history is used as an indicator

for payment of future bills/loansfor payment of future bills/loans

““Forgetting” is no longer an excuse Forgetting” is no longer an excuse with so many tools todaywith so many tools today• Write it down on a calendarWrite it down on a calendar• Electronic DraftsElectronic Drafts• Automatic Payments from your accountsAutomatic Payments from your accounts

Ways to Build/Strengthen CreditWays to Build/Strengthen Credit

22 Keeping your Lines of Credit low Keeping your Lines of Credit low• Make sure that you do not go over 50% Make sure that you do not go over 50%

of your credit limitsof your credit limits• 30% of your credit score is how well you 30% of your credit score is how well you

utilize all of your credit limitsutilize all of your credit limits $10,000 limit, $8,000 used = $10,000 limit, $8,000 used =

negative impact on your credit scorenegative impact on your credit score

Ways to Build/Strengthen CreditWays to Build/Strengthen Credit

33 Age of Debts Age of Debts• The longer you have established well The longer you have established well

paying credit on your credit report the paying credit on your credit report the betterbetter

• 15% of your credit score15% of your credit score• Don’t go out and sign up for every credit Don’t go out and sign up for every credit

card or loan offered to youcard or loan offered to you• Manage one to two lines of credit to Manage one to two lines of credit to

build/strengthen your credit scorebuild/strengthen your credit score

Ways to Build/Strengthen CreditWays to Build/Strengthen Credit

44 New Debt and Inquiries New Debt and Inquiries• Keep your debt only to what you needKeep your debt only to what you need• 10% of your credit score10% of your credit score• Inquiries – each time your credit is Inquiries – each time your credit is

pulledpulled Each inquiry shows up on your credit report Each inquiry shows up on your credit report Store Credit CardsStore Credit Cards Car Dealer financingCar Dealer financing

Ways to Build/Strengthen CreditWays to Build/Strengthen Credit

55 Mixtures of Different Types of Credit Mixtures of Different Types of Credit• Credit reporting agencies like to see that Credit reporting agencies like to see that

you can manage different types of credityou can manage different types of credit• 10% of your score10% of your score

Installment loans Installment loans • With a set payment and a maturity dateWith a set payment and a maturity date

Revolving loansRevolving loans• Like Credit CardsLike Credit Cards

• Good to have at least one of eachGood to have at least one of each

Ways to Build/Strengthen CreditWays to Build/Strengthen Credit

QUESTIONS?QUESTIONS?

151413121110987654321

$1 Million$500,000$250,000$125,000$64,000$32,000$16,000$8,000$4,000$2,000$1,000$500$300$200$100

Welcome to

Who Wants to be a Millionaire

50:50

Presentation

Loganville High SchoolLoganville High School

151413121110987654321

$1 Million$500,000$250,000$125,000$64,000$32,000$16,000$8,000$4,000$2,000$1,000$500$300$200$100

A: Life History

C: First Born Child

B: Mother’s Maiden Name

D: $1,000,000

50:50

151413121110987654321

$1 Million$500,000$250,000$125,000$64,000$32,000$16,000$8,000$4,000$2,000$1,000$500$300$200$100

What do you need to give a bank to open an account?

151413121110987654321

$1 Million$500,000$250,000$125,000$64,000$32,000$16,000$8,000$4,000$2,000$1,000$500$300$200$100

A: Who has good credit?

C: You can borrow and not pay back

B: You won’t have any friends

D: You may not be able to open a bank account

50:50

151413121110987654321

$1 Million$500,000$250,000$125,000$64,000$32,000$16,000$8,000$4,000$2,000$1,000$500$300$200$100

If you have bad credit…

151413121110987654321

$1 Million$500,000$250,000$125,000$64,000$32,000$16,000$8,000$4,000$2,000$1,000$500$300$200$100

A: Your signature

C: Your legal name

B: Your account number

D: All of the above

50:50

151413121110987654321

$1 Million$500,000$250,000$125,000$64,000$32,000$16,000$8,000$4,000$2,000$1,000$500$300$200$100

What is on a Signature Card?

151413121110987654321

$1 Million$500,000$250,000$125,000$64,000$32,000$16,000$8,000$4,000$2,000$1,000$500$300$200$100

A: New Television

C: New Car

B: New House

D: Lawn mower

50:50

151413121110987654321

$1 Million$500,000$250,000$125,000$64,000$32,000$16,000$8,000$4,000$2,000$1,000$500$300$200$100

What should you not buy unless you have 100% saved for?

(More than 1)

151413121110987654321

$1 Million$500,000$250,000$125,000$64,000$32,000$16,000$8,000$4,000$2,000$1,000$500$300$200$100

A: Checking Account

C: College Saving Account

B: Certificate of Deposit

D: Lay Away

50:50

151413121110987654321

$1 Million$500,000$250,000$125,000$64,000$32,000$16,000$8,000$4,000$2,000$1,000$500$300$200$100

A bank does NOT offer this account…

Congratulations!

You’ve ReachedYou’ve Reached

the $1,000the $1,000

Milestone!Milestone!

Congratulations!Congratulations!

151413121110987654321

$1 Million$500,000$250,000$125,000$64,000$32,000$16,000$8,000$4,000$2,000$1,000$500$300$200$100

A: You dip below $100

C: You take out a loan

B: You spend more money than you have

D: On the 1st of the month

50:50

151413121110987654321

$1 Million$500,000$250,000$125,000$64,000$32,000$16,000$8,000$4,000$2,000$1,000$500$300$200$100

When would you get an Overdraft Fee?

151413121110987654321

$1 Million$500,000$250,000$125,000$64,000$32,000$16,000$8,000$4,000$2,000$1,000$500$300$200$100

A: Interest you earn

C: Only applies to a CD

B: Interest that accrues more interest

D: Only applies to a loan

50:50

151413121110987654321

$1 Million$500,000$250,000$125,000$64,000$32,000$16,000$8,000$4,000$2,000$1,000$500$300$200$100

What is compounding interest?

151413121110987654321

$1 Million$500,000$250,000$125,000$64,000$32,000$16,000$8,000$4,000$2,000$1,000$500$300$200$100

A: 15

C: 18

B: 16

D: 21

50:50

151413121110987654321

$1 Million$500,000$250,000$125,000$64,000$32,000$16,000$8,000$4,000$2,000$1,000$500$300$200$100

How old do you have to be to have yourown bank account?

151413121110987654321

$1 Million$500,000$250,000$125,000$64,000$32,000$16,000$8,000$4,000$2,000$1,000$500$300$200$100

A: Advertising

C: Stockholders

B: Interest on the balance

D: Selling Credit Cards to banks

50:50

151413121110987654321

$1 Million$500,000$250,000$125,000$64,000$32,000$16,000$8,000$4,000$2,000$1,000$500$300$200$100

How do credit card companies make money?

151413121110987654321

$1 Million$500,000$250,000$125,000$64,000$32,000$16,000$8,000$4,000$2,000$1,000$500$300$200$100

A: 3%

C: $20,000

B: 20%

D: 1 Arm 2 Legs

50:50

151413121110987654321

$1 Million$500,000$250,000$125,000$64,000$32,000$16,000$8,000$4,000$2,000$1,000$500$300$200$100

What is a typical down payment for a house?

Congratulations!

You’ve ReachedYou’ve Reached

the $32,000the $32,000

Milestone!Milestone!

Congratulations!Congratulations!

151413121110987654321

$1 Million$500,000$250,000$125,000$64,000$32,000$16,000$8,000$4,000$2,000$1,000$500$300$200$100

A: 300-850

C: 300-800

B: 350-800

D: 350-850

50:50

151413121110987654321

$1 Million$500,000$250,000$125,000$64,000$32,000$16,000$8,000$4,000$2,000$1,000$500$300$200$100

What is the high and low range of a credit score?

151413121110987654321

$1 Million$500,000$250,000$125,000$64,000$32,000$16,000$8,000$4,000$2,000$1,000$500$300$200$100

To jumpA: Pay bills on time

C: Pay cash for everything

B: Keeping Lines of Credit low

D: Limit credit inquiries

50:50

151413121110987654321

$1 Million$500,000$250,000$125,000$64,000$32,000$16,000$8,000$4,000$2,000$1,000$500$300$200$100

Which is NOT a way to build your credit score?

151413121110987654321

$1 Million$500,000$250,000$125,000$64,000$32,000$16,000$8,000$4,000$2,000$1,000$500$300$200$100

A: Don’t buy anything

C: Avoid impulse buys

B: Steal

D: Create a budget

50:50

151413121110987654321

$1 Million$500,000$250,000$125,000$64,000$32,000$16,000$8,000$4,000$2,000$1,000$500$300$200$100

Which are NOT smart ways to save money?

151413121110987654321

$1 Million$500,000$250,000$125,000$64,000$32,000$16,000$8,000$4,000$2,000$1,000$500$300$200$100

A: Kim is smart because she values time to herself

C: Bob will get a lower interest rate

B: Bob is smart for buying a used car

D: Kim and Bob’s interest rates will be identical

50:50

151413121110987654321

$1 Million$500,000$250,000$125,000$64,000$32,000$16,000$8,000$4,000$2,000$1,000$500$300$200$100

Kim and Bob go in to apply for loans, Kim is wanting the loan to go on a vacation,

Bob is wanting to buy a car. Which is true?

151413121110987654321

$1 Million$500,000$250,000$125,000$64,000$32,000$16,000$8,000$4,000$2,000$1,000$500$300$200$100

A: www.freecreditreport.com

C: www.google.com

B:www.annualcreditreport.com

D: www.givememycreditreport.com

50:50

151413121110987654321

$1 Million$500,000$250,000$125,000$64,000$32,000$16,000$8,000$4,000$2,000$1,000$500$300$200$100

What website offers you a truly FREE creditreport each year?

YOU WIN $1 MILLION DOLLARS!

Questions?Questions?