Embed Size (px)

Citation preview

©2015 First American Financial Corporation and/or its affiliates. All rights reserved. NYSE: FAF

Loan Estimate (LE) TILA-RESPA Integrated Disclosure (TRID) Rule Requirements

©2015 First American Financial Corporation and/or its affiliates. All rights reserved. NYSE: FAF

• New Rule creates new definition of – Covered Loan – Loan Application – Consummation (Closing)

• New Rule creates new work flow – More documentation – Tighter time lines

• New Rule creates new forms – Loan Estimate – Closing Disclosure

New Definitions; New Forms New Work Flow

©2015 First American Financial Corporation and/or its affiliates. All rights reserved. NYSE: FAF

• No longer RESPA definition • All TILA and Regulation Z

– Loan to natural person (includes trusts) – Proceeds for personal, family of household use – Collateral is dwelling attached to land

• Includes 25 acres or more if above applies

Covered Loan

©2015 First American Financial Corporation and/or its affiliates. All rights reserved. NYSE: FAF

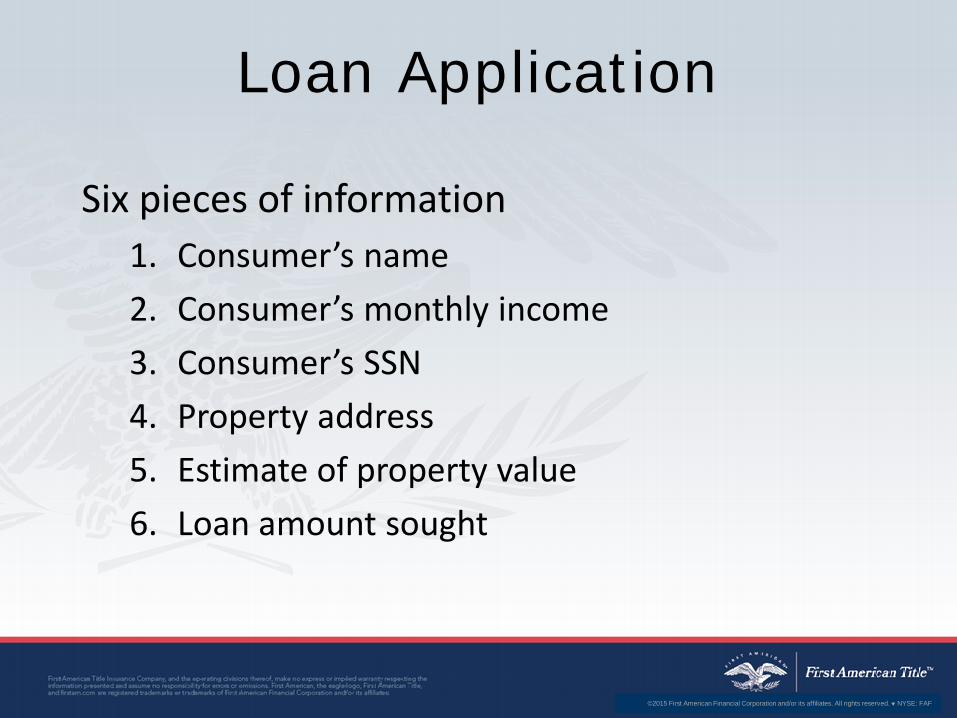

Loan Application

Six pieces of information 1. Consumer’s name 2. Consumer’s monthly income 3. Consumer’s SSN 4. Property address 5. Estimate of property value 6. Loan amount sought

©2015 First American Financial Corporation and/or its affiliates. All rights reserved. NYSE: FAF

Consummation

• The target date around which disclosure requirements revolve

• CFPB explains: – Commonly occurs at closing or settlement – Legally distinct event:

• “Occurs when the consumer becomes contractually obligated to the creditor on the loan”

• Lender will likely dictate the date of consummation

©2015 First American Financial Corporation and/or its affiliates. All rights reserved. NYSE: FAF

• Lender and Broker fees must be exact • All other fees quoted

– Including Homeowner Association Dues if known (example)

• Must be in Good Faith – Best information reasonably available to the

creditor – Obtained through due diligence

Accuracy of Disclosures

©2015 First American Financial Corporation and/or its affiliates. All rights reserved. NYSE: FAF

Loan Estimate (LE) Provision

Provided to the consumer by: • Creditor/Lender • Mortgage broker Delivery • 3 business days after application • 7 business days before consummation • If mailed add 3 days for receipt

©2015 First American Financial Corporation and/or its affiliates. All rights reserved. NYSE: FAF

SUNDAY MONDAY TUESDAY WEDNESDAY THURSDAY FRIDAY SATURDAY

16

17 18 19 Application Received Can be either creditor or broker 6 specific items

20 Customer can withdraw/Lender can reject Application

21 Customer can withdraw/Lender can reject Application

22 Lender is not open for customer facing business so Saturday does not count for Loan Estimate preparation

23 Sunday doesn’t count

24 Loan Estimate must be mailed or hand delivered If in hand= LE Delivery Date

25 LE Mail Day 1 Earliest Day Closing Disclosure can be mailed or delivered in hand If in hand= CD Delivery Date

26 LE Mail Day 2 CD Mail Day 1 CD In hand Disclosure Day 1

27 LE Mail Day 3= Delivery Date (presumed) CD Mail Day 2 CD In hand Disclosure Day 2

28 CD Mail Day 3= Delivery Date (presumed) CD in hand Disclosure Day 3

1 CD Mail Disclosure Day 1

2 Sunday doesn’t count

3 CD Mail Disclosure Day 2

4 CD Mail Disclosure Day 3= okay to close Earliest day for closing assuming LE mailed or delivered on 24th

5 6 7 8 LE expires

Application Timeline

©2015 First American Financial Corporation and/or its affiliates. All rights reserved. NYSE: FAF

Page One

©2015 First American Financial Corporation and/or its affiliates. All rights reserved. NYSE: FAF

General

©2015 First American Financial Corporation and/or its affiliates. All rights reserved. NYSE: FAF

Loan Terms & Projected Payments

©2015 First American Financial Corporation and/or its affiliates. All rights reserved. NYSE: FAF

• Refinance transaction – Includes check boxes From and To Borrower

Costs at Closing

©2015 First American Financial Corporation and/or its affiliates. All rights reserved. NYSE: FAF

Page Two

©2015 First American Financial Corporation and/or its affiliates. All rights reserved. NYSE: FAF

Loan Costs

©2015 First American Financial Corporation and/or its affiliates. All rights reserved. NYSE: FAF

Other Costs

©2015 First American Financial Corporation and/or its affiliates. All rights reserved. NYSE: FAF

Calculating Cash to Close

©2015 First American Financial Corporation and/or its affiliates. All rights reserved. NYSE: FAF

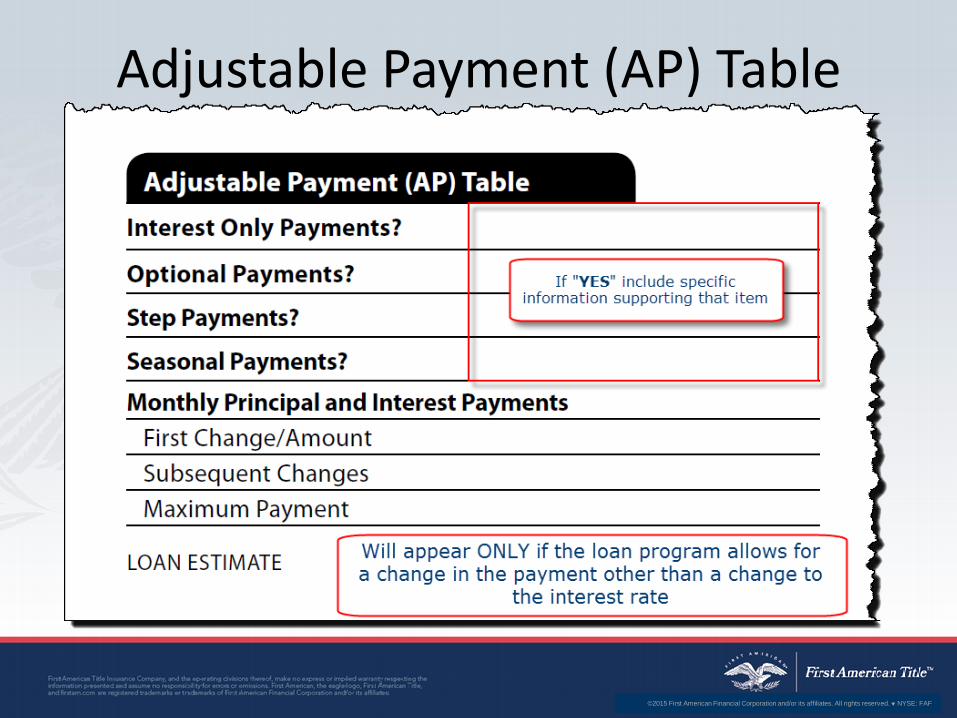

Adjustable Payment (AP) Table

©2015 First American Financial Corporation and/or its affiliates. All rights reserved. NYSE: FAF

Adjustable Interest Rate (AIR) Table

©2015 First American Financial Corporation and/or its affiliates. All rights reserved. NYSE: FAF

Page Three

©2015 First American Financial Corporation and/or its affiliates. All rights reserved. NYSE: FAF

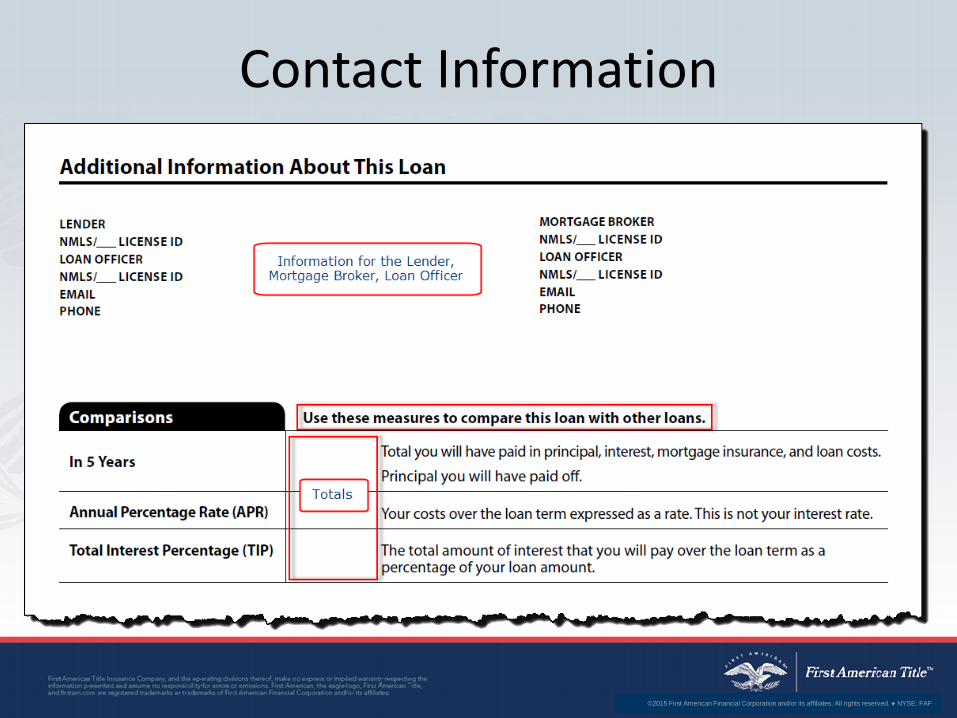

Contact Information

©2015 First American Financial Corporation and/or its affiliates. All rights reserved. NYSE: FAF

Other Considerations & Receipt

©2015 First American Financial Corporation and/or its affiliates. All rights reserved. NYSE: FAF

Shopping Service Providers

• Can Shop For a settlement service, subject to reasonable requirements

• It’s NOT shopping for a provider when – Consumer is required to choose from a written

list of providers – OR – If consumer voluntarily chooses from a written

list of providers

©2015 First American Financial Corporation and/or its affiliates. All rights reserved. NYSE: FAF

Revised Loan Estimate (LE)

• Six different types of changes 1. Changed circumstances affecting settlement

charges 2. Changed circumstances affecting eligibility 3. Revisions requested by consumer 4. Interest rate dependent changes 5. Loan Estimate expires 6. Delayed settlement date on a construction

loan

©2015 First American Financial Corporation and/or its affiliates. All rights reserved. NYSE: FAF

• If a Changed Circumstance/ Tolerance exceeded – However cannot be ‘piece-meal’ – Must be provided to consumer within three

business days of receiving information sufficient to establish the changed circumstance.

– Consumer must receive the revision no later than 4 days before closing

– May not issue after Closing Disclosure

Revised Disclosure-Loan Estimate

©2015 First American Financial Corporation and/or its affiliates. All rights reserved. NYSE: FAF

New Tolerances

Rule Expands zero tolerance group: • Amounts disclosed on the Loan Estimate for the following

services cannot increase (Zero Tolerance): 1. Transfer Taxes 2. Fees paid to the creditor or broker 3. Fees paid to an affiliate of the creditor or broker 4. Fees paid for services for which the lender or broker does not permit

the consumer to shop

©2015 First American Financial Corporation and/or its affiliates. All rights reserved. NYSE: FAF

Tolerances

The 10% group: • Amounts disclosed on the Loan Estimate for the following

services cannot increase by more than 10 percent (aggregate):

1. Third Party Fees for services: – Required by the Lender – The Lender provides a written list – Where the Consumer may shop for the service provider, (not on

the list) and – The Consumer selects a provider from the Lender’s written list

of provider's

2. Recording Fees

©2015 First American Financial Corporation and/or its affiliates. All rights reserved. NYSE: FAF

Tolerances

Unlimited Tolerance • Amounts disclosed on the Loan Estimate for the following services may

increase: 1. Prepaid Interest 2. Property Insurance Premiums 3. Amounts in Escrow 4. Third Party Fees for services:

– Required by the Lender – Where the Consumer may shop for the service provider, and – The Consumer selects a provider not on the Lender’s written list of provider's

5. Third Party Fees for services – Not required by the Lender – Even if paid to an affiliate

The creditor may still impose reasonable qualifications for providers.

– Example: Provider must be licensed

©2015 First American Financial Corporation and/or its affiliates. All rights reserved. NYSE: FAF

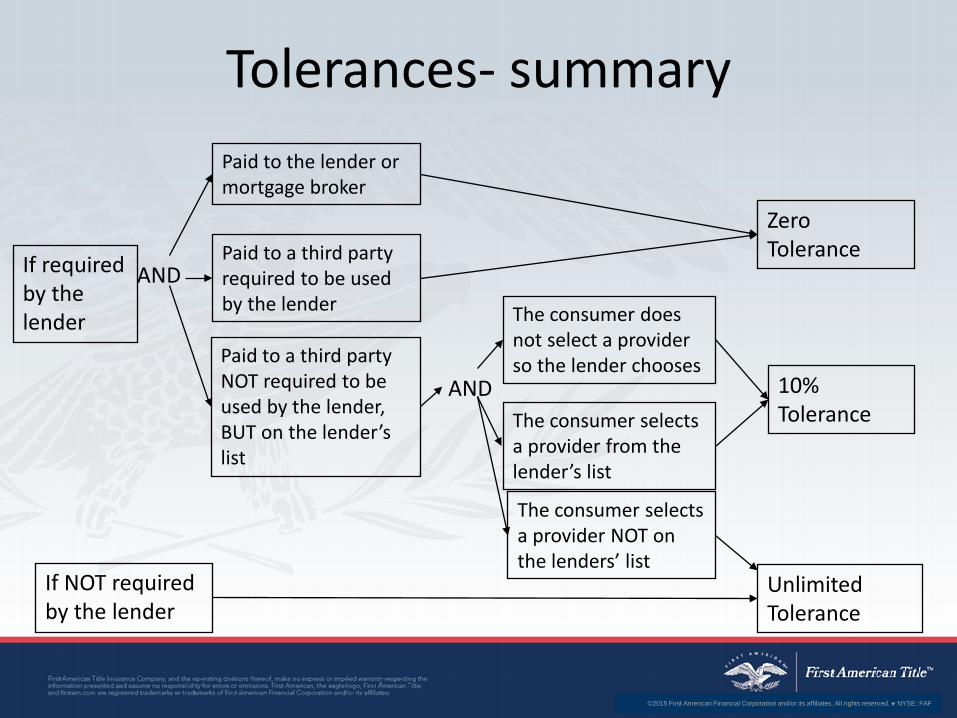

Tolerances- summary Paid to the lender or mortgage broker

If required by the lender

Paid to a third party required to be used by the lender

Paid to a third party NOT required to be used by the lender, BUT on the lender’s list

The consumer selects a provider from the lender’s list

The consumer does not select a provider so the lender chooses

AND

If NOT required by the lender

Unlimited Tolerance

The consumer selects a provider NOT on the lenders’ list

Zero Tolerance

10% Tolerance

AND

©2015 First American Financial Corporation and/or its affiliates. All rights reserved. NYSE: FAF

• TILA ▫ Private right of action for violations (with attorney’s fees and costs)

▫ Statutory penalties of up to $4,000 for failures to properly provide certain disclosures (including finance charge and APR)

• RESPA ▫ No private right of action for GFE and HUD-1 disclosures

• Dodd-Frank ▫ CFPB enforcement of consumer financial laws (incl. TILA and RESPA)

▫ $5,000 per day per violation; $25,000 per day for reckless violations; $1M per day for knowing violations

Liability

©2015 First American Financial Corporation and/or its affiliates. All rights reserved. NYSE: FAF

Thank you! Questions?