Embed Size (px)

Citation preview

German Institute for Economic Research

LNG and Natural Gas Perspectives -Competition – Contracts – Cartel

Christian von HirschhausenTogether with Steven A. Gabriel, Ruud Egging (University of Maryland),

Franziska Holz, Daniel Huppmann (DIW Berlin),Sophia Rüster, Anne Neumann (TU Dresden)

Add picture on dark green area(see slide 9 for an example)

32nd IAEE International ConferenceSan Francisco, CA, June 23, 2009

Picture: Roar Lindefjeld, StatoilHydro – Arctic Discoverer docked at Cove Point – commons.wikimedia.org

- 2 -

Background: EE2 / DIW Program“The Globalization of Natural Gas Markets”

- Jointly between Dresden University of Technology, Chair of Energy Economics and Public Sector Management, and DIW Berlin

- Research and advice to policy makers and the corporate sector, three modules:1) Computational model of the European (and trans-Atlantic) natural gas market

- Competition/oligopoly, effect on prices, quantities- Infrastructure bottlenecks (pipelines, LNG-terminals)- Role of Russia …

2) Institutional economic modeling on governance structures and contracts- Nexus between regulation and contracts- Changing role of long-term contracts- Vertical integration along the LNG value added chain

3) Econometric analysis of energy price developments- Relation between North American, European, Asian gas and oil prices- Cointegration and/or convergence of trans-Atlantic natural gas prices ?

globalgas.ee2.biz

- 3 -

Agenda

1. Introduction

2. Competition – Competition for LNG in the Atlantic Basin

3. Contracts – Vertical Integration and Investments

4. Cartel and Other Scenarios – A Modeling Analysis

5. Conclusions

- 4 -

1. Introduction: Is Global Natural Gas Trade Still Relevant?The (Short-Term) Future of LNG Looks Unpromising

• EIA International Energy Outlook LNG Imports: 2007 versus 2008

• Recent forecasts expect:- Lower net imports from Canada- Increasing domestic production, Alaska, but mainly shale gas- “Oversupply” of LNG due to economic crisis

Significantly lower imports in the form of LNG

1,000 bcm ~ 35 Tcf

$ 100 tcm ~ 3.5$/Mcf

- 5 -

Will We Need Natural Gas in 2050?POLES – 2050: Yes (~20% of World Primary Energy Demand)

Source: EC (2006) WETO H2

Carbon-Constraint Case

- Although “CO2-intensive”, natural gas has a role to play in the “transition” to whatever the new energy system will look like

- Natural gas is needed as back-up for a super-smart-grid (combining large-scaledistributed resources, concentrating solar power, wind, etc.)

- 6 -

Agenda

1. Introduction

2. Competition – Competition for LNG in the Atlantic Basin

3. Contracts – Vertical Integration and Investments

4. Cartel and Other Scenarios – A Modeling Analysis

5. Conclusions

- 7 -

4 Hypotheses

As international markets are increasingly integrated, and regional markets are restructured, competition on natural gas markets is intensifying

Contract structures are also evolving towards more flexible arrangements; corporate structures depend upon specific strategy options

Upstream markets tend to be more oligopolistic in nature, but the risk of a “GECF cartel” or Russian dominance seem to be manageable

The integration of “unconventional” natural gas reserves (mainly shale gas, but also coalbed-methane, tight gas) may change the medium-term outlook of international LNG-trade, in particular the role of the U.S., significantly

- 8 -

Price Relations in the Atlantic Basin

Published in:

• Anne Neumann (2009): Is LNG Doing Its Job? The Energy Journal, Vol. 30, Special Issue “World Natural Gas Markets and Trade: A Multi-ModelingPerspective”, pp. 187-199.

• Boriss Siliverstovs, Anne Neumann, Guillaume L'Hegaret, and Christian von Hirschhausen (2005): International Market Integration for Natural Gas? A Cointegration Analysis of Gas Prices in Europe, North America and Japan. Energy Economics, Vol. 27, No. 4, pp. 603-615.

• Also as Discussion Papers: www.ee2.biz

- 9 -

Natural Gas Trade Flows 2006 / 2030

Source: IEA World Energy Outlook 2008

1,000 bcm ~ 35 Tcf

$ 100 kcm ~ 3.5$/Mcf

- 10 -

Infrastructure Investment is Forthcoming, but is it Efficient?Comparison of the three Main Regions

U.S. Europe

Highly diversified Concentrated, butdiversificationpossible

Quasi-verticalintegration

National regulation, little European coordination

National prices, fewhubs, low liquidity

RoR based, Art. 22, TPA exemptions, etc.

Unbundled

Truly integratedinter-state market, FERC regulation

Nodal pricing, ~ 25 market centers(U.S. and Canada)

RoR based, TPA exemptionspossible for LNG-terminals(Hackberry)

Asia(Japan/Korea)

Supply structure Highly importdependent

Monopolistic

Regulated prices

Includes high riskpremium

Long-term planningapproach

Market structure

Regulatory structure

Pricing

Investment incentives

- 11 -

North America: Coordinated Spot Market:Bid-Based, Security-Constrained, Economic Dispatch with Nodal Prices

- 12 -

… But the Pricing System Allows Efficient Decisions on Investment Financing: Example of the Rockies Express Pipeline Project

• I ~ 5 bn. USD, 2,700 km, 15-18 bcm

• FERC-filing, open season, nodal pricing, etc. identification of bottlenecks

• TPA with „regulated“ ROR, secondary trading, etc. efficient capacity allocation

Source map:: IEA Natural Gas Market Review 2008

- 13 -

Europe: The Main Obstacles to the Internal Market are intra-EuropeanGasmod Results

France→ Spain

UK ↔Continent

Norway→Europe

Between BL, NL, GER and Fr

- 14 -

European LNG Import Capacities are Rapidly Expanding

Existing

Planned /underdiscussion

Under construction

• Money (rate-of-return) is no object

• UK and Spain examples show that investments in LNG terminals are forthcoming

• This holds most likely for other countries/terminals as well

- 15 -

Asia: Sustained, though Uncertain (LNG) Demand, andGradually More Competitive Markets

• Japan and South Korea:- Remain the backbone of intenational LNG demand- Gradually moving towards more gas-to-gas competition

• China: LNG boom not yet materialized, but growth is likely

• India/Indonesia: Depends upon price of coal/carbon policy

Asia will remain a major competitor for LNG

- 16 -

Towards LNG Competition in the Atlantic Basin

3

4

5

6

7

8

9

10

11

12

Jan-

05

Mar

-05

May

-05

Jul-0

5

Sep

-05

Nov

-05

Jan-

06

Mar

-06

May

-06

Jul-0

6

Sep

-06

Nov

-06

$/MbtuLNG from Algeria to SpainLNG from Qatar to SpainHenry Hub

LNG cargoes to USLNG cargoes to Europe

- 17 -

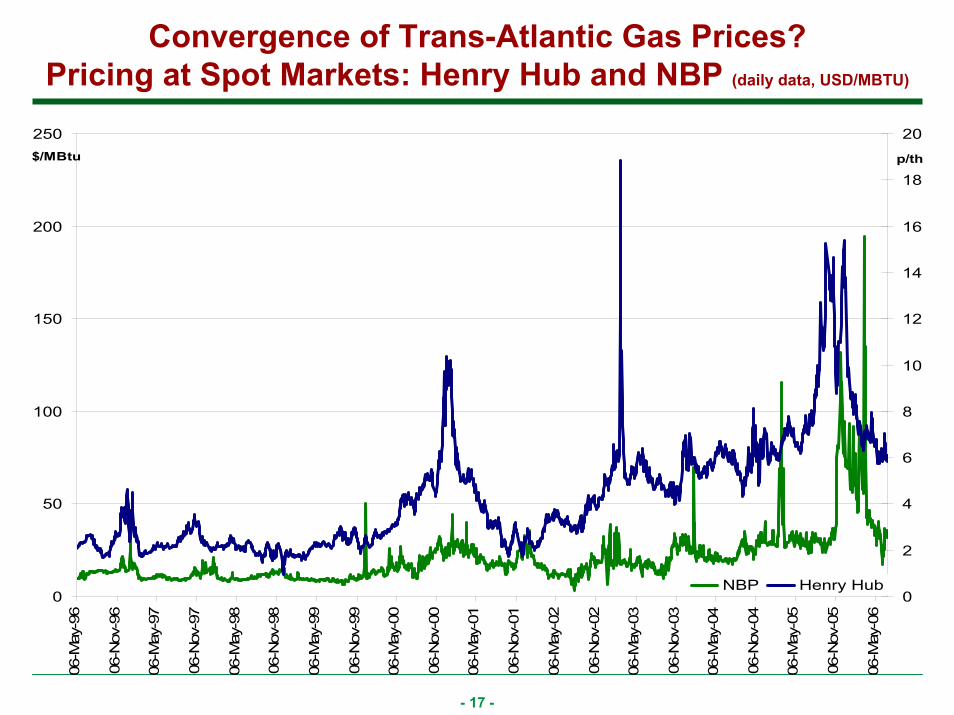

Convergence of Trans-Atlantic Gas Prices?Pricing at Spot Markets: Henry Hub and NBP (daily data, USD/MBTU)

0

50

100

150

200

250

06-M

ay-9

6

06-N

ov-9

6

06-M

ay-9

7

06-N

ov-9

7

06-M

ay-9

8

06-N

ov-9

8

06-M

ay-9

9

06-N

ov-9

9

06-M

ay-0

0

06-N

ov-0

0

06-M

ay-0

1

06-N

ov-0

1

06-M

ay-0

2

06-N

ov-0

2

06-M

ay-0

3

06-N

ov-0

3

06-M

ay-0

4

06-N

ov-0

4

06-M

ay-0

5

06-N

ov-0

5

06-M

ay-0

6

$/MBtu

0

2

4

6

8

10

12

14

16

18

20

p/th

NBP Henry Hub

- 18 -

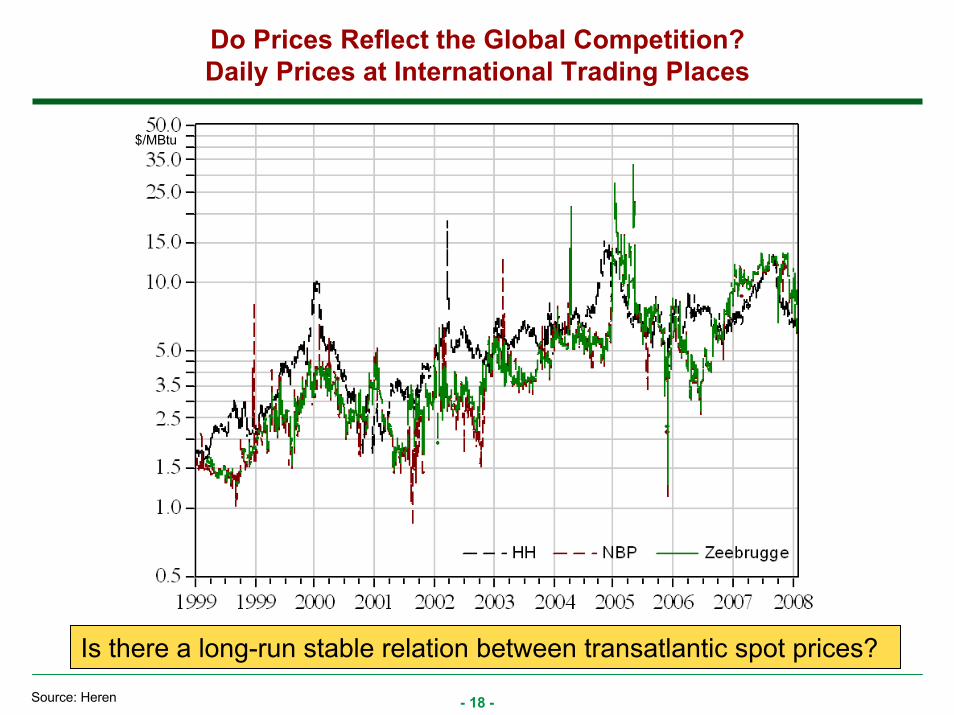

Do Prices Reflect the Global Competition?Daily Prices at International Trading Places

Source: Heren

Is there a long-run stable relation between transatlantic spot prices?

$/MBtu

- 19 -

• No stable cointegration relation between prices (yet?)

• Market integration understood as dynamic concept, hence movingtowards price integration

- Restructured natural gas markets in North America and Europe- High proportion of spot trading - Increasing integration of former regional unconnected natural gas markets - Active LNG arbitrage in the Atlantic Basin

• Kalman Filter - dynamic structural change, time-varying coefficient models- βt contains information on price relationship

β = 0 no market integrationβ = 1 LOP holds; markets are fully integratedβ 1 increasing market integration over time

Methodological Approach: Price Convergence

lnp1t = α + βt*lnp2t + et

βt = βt-1 + ut

- 20 -

Estimated Beta-Coefficient for Transatlantic Prices

- Results indicate increasing convergence over time

- Including more recent data supports the existing trend

- Seasonal trend: higher coefficient in winter (~ January)

- Confirmed by anecdotal evidence (~$22/MBTu in Japan)

- 21 -

Agenda

1. Introduction

2. Competition – Competition for LNG in the Atlantic Basin

3. Contracts – Vertical Integration and Investments

4. Cartel and Other Scenarios – A Modeling Analysis

5. Conclusions

- 22 -

Contracts and Vertical Integration in the LNG Value Chain

Published in:

• Christian von Hirschhausen and Anne Neumann (2008): Long-Term Contracts and Asset Specificity Revisited: An Empirical Analysis of Producer-Importer Relations in the Natural Gas Industry. Review of Industrial Organization, Vol. 32, No. 2, pp. 131-143.

• Sophia Rüster and Anne Neumann (2009): Linking Alternative Theories of the Firm – A First Empirical Application to the Liquefied Natural Gas Industry. Journal of Institutional Economics, Vol. 5, No. 1, pp. 47-64.

• Sophia Rüster (2009): Relational Contracting in the LNG Industry – An Empirical Analysis. Presented at 32nd IAEE Conference.

• Also as Discussion Papers: www.ee2.biz

- 23 -

Existing Literature

Transaction cost economics and agency theory:- Long-term contracts minimize transaction cost when significant specific assets are required

- Overcome the hold-up problem without vertical integration (Klein, Crawford, and Alchian, 1978, Williamson, 1979)

- Asset-specificity, uncertainty, opportunism, bounded rationality (Williamson, 1975, 1985)

- Sufficient investment incentives and inexpensive ex- post renegotiation

Incomplete contracts:- Reduce inefficiencies in ex-ante investments or ex-post exchange (Grossmann / Hart,

1986, Hart / Moore, 1988)

Empirical evidence:- Work by Joskow (1987) on contract duration and asset-specificity in American coal industry

- Masten / Crocker (1985) and Crocker / Masten (1988) focus on the US natural gas industry, contractual take-obligations relate negatively with contract duration

- Influence of US governmental regulation on long-term contracts in natural gas sector (Mulherin, 1986, Hubbard / Weiner, 1986, Doane / Spulber, 1994)

- Flexibility and price trends in contract negotiations (Parsons, 1986); increasing use of spot transactions in LNG industry (Hartley / Brito, 2002)

- 24 -

Structural Changes in the International Natural Gas Industry

- Relative cost reduction in the LNG value-added chain- Economies of scale in liquefaction- Lower costs for shipping- Economies of scale in regas

- Diminishing asset specificity of investments- Formerly: field-specific contracts- Nowadays: infrastructure developed, less hold-up risk, more general country-

focused contracts- More players on both sides (producers, traders, importers)

- Development of spot markets and shorter-term trading

- Increased number of market participants- Producers- Buyers

Less need for long-term contracts to overcome the hold-up problem

- 25 -

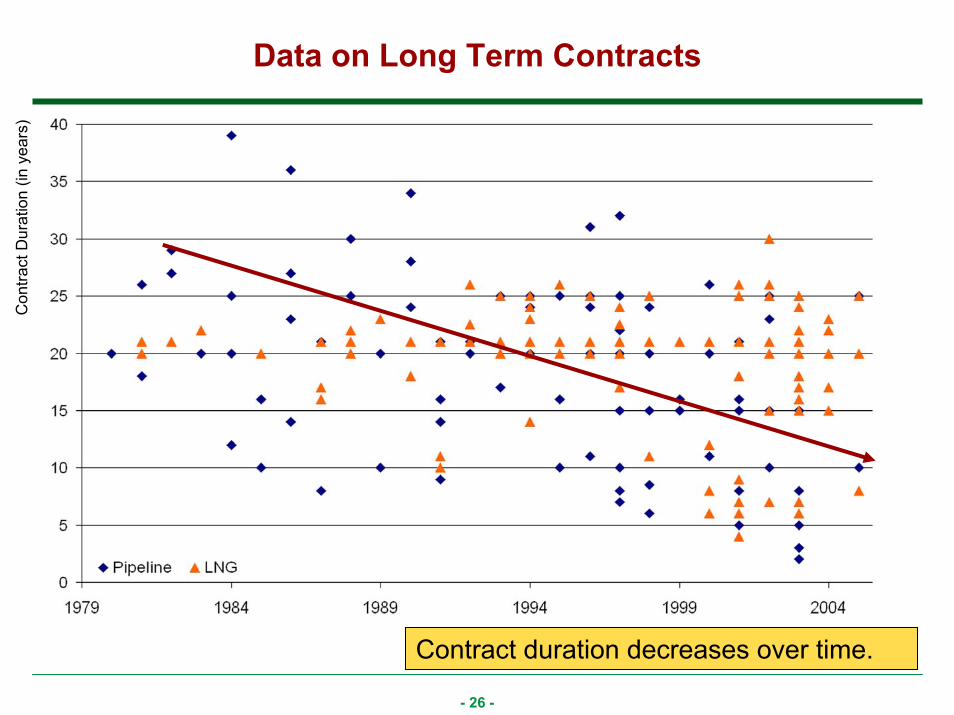

Data – Sample Size

All contracts

European contracts

Number of contracts

Number of contracts Contract duration (in years)

Contract duration (in years)

0

4

8

12

16

20

5 10 15 20 25 30 35 40

Series: CDSample 1 135Observations 135

Mean 18.95926Median 20.00000Maximum 39.00000Minimum 2.000000Std. Dev. 8.170079Skewness 0.165087Kurtosis 2.697388

Jarque-Bera 1.128311Probability 0.568840

0

10

20

30

40

50

60

5 10 15 20 25 30 35 40

Series: CDSample 1 262Observations 262

Mean 19.28435Median 20.00000Maximum 39.00000Minimum 2.000000Std. Dev. 6.678600Skewness -0.084494Kurtosis 3.464052

Jarque-Bera 2.662583Probability 0.264136

- 26 -

Con

tract

Dur

atio

n(in

yea

rs)

Data on Long Term Contracts

Contract duration decreases over time.

- 27 -

An Econometric Specification ...... Taking into Account Project Specificity

Contract Duration = c + β1TVol + β2PROJECT + β3ENTRANT

+ β4RENEGO + β5EU_post98 + β6C_US_UK + β7P_AFRICA

+ β8P_Eurasia + β9P_Russia + β10P_ME + β11P_Oceania + εi

CD – contract duration RENEGO – extension/renegotiationTVOL – total contracted volume EU_post98 – deliveries to Europe since 1998 PROJECT – related to investments in a concrete project C_US_UK - exports to competitive marketsENTRANT – importing incumbent companies P_Eurasia –gas producing regions

H1: Market restructuring and emergence of a global natural gas marketreduces the duration of long-term contracts;

H2: Other things being equal, contracts that imply large-scale, asset-specific investments will have longer contract duration than do othercontracts.

- 28 -

Results (311 observations, as of 2006)

Reported are estimated coefficients and p-values. ***, **,* indicate significance at 1%, 5%, and 10% level

Specification Level

C 20.54***(0.0000)

TVOL 0.04***(0.0000)

PROJECT 3.09***(0.0000)

ENTRANT -3.09***(0.0001)

RENEGO -4.36***(0.0000)

EU_post98 -1.50**(0.0416)

C_US_UK -2.42**(0.0502)

P_regions Negative, significant

R2 0.326

Adjusted R2 0.301

H1: Contract duration negatively related with variablesrepresenting market restructuring.

H2: Positive relation between contract duration and asset-specificity of the investments linked to a particular contract.

- 29 -

Agenda

1. Introduction

2. Competition – Competition for LNG in the Atlantic Basin

3. Contracts – Vertical Integration and Investments

4. Cartel and Other Scenarios – A Modeling Analysis1. The World Gas Model (WGM), Model & Data2. „Upstream Withholding“3. „Eastern Promises“4. „Barnett Shale“

5. Conclusions

- 30 -

References

• Egging, Ruud, Franziska Holz, Christian von Hirschhausen, Steven A. Gabriel (2009):Representing GASPEC With the World Gas Model. The Energy Journal, Vol. 30, Special Issue “World Natural Gas Markets and Trade: A Multi-Modeling Perspective”, pp. 97-117.

• Egging, Ruud, Franziska Holz, and Daniel Huppmann (2009): Pretty Coast California: Implications of an LNG Import Terminal Ban for the US Pacific Coast Up To 2030. Presented at 28th USAEE conference, Dec 5, 2008 New Orleans, LA

• Egging, Ruud, Steven A. Gabriel, Franziska Holz and Jifang Zhuang: A Complementarity Model for the European Natural Gas Market. Energy Policy, Vol. 36(7), 2385-2414, July 2008.

• Holz, Franziska, Christian von Hirschhausen, and Claudia Kemfert (2009): International Gas Markets: Modeling Results with the GASMOD-Model. The Energy Journal, Vol. 30, Special Issue “World Natural Gas Markets and Trade: A Multi-Modeling Perspective”.

• Franziska Holz, Christian von Hirschhausen, and Claudia Kemfert (2008): GASMOD –A Model for the European Natural Gas Market. Energy Economics, Vol. 32, No. 3.

• Holz, Franziska, Christian von Hirschhausen, Daniel Huppmann, Sophia Ruester, Steven Gabriel, and Ruud Egging (2008): The World Gas Market in 2030: Policy Scenario Analysis Using the World Gas Model. Presentation at the 8th Infraday, Berlin.

• Also as Discussion Papers: www.ee2.biz

- 31 -

The World Gas Model (WGM)University of Maryland – TU Dresden – DIW Berlin

• WGM is a simulation model of the global natural gas market- Partial market equilibrium model with optimization problems for individual players- Mixed complementarity problem

• Features:- More than 70 countries, 95% of world natural gas production and consumption- Time horizon until 2030 in 5-year intervals, with three seasons per period- Market power for traders in pipeline market and regasifiers- Limited capacities in production, storage, pipeline and LNG transport- Endogenous investments in pipeline, storage and LNG capacity- LNG contract database, not just spot market

• Calibration to projections of energy markets (PRIMES, POLES)- POLES projections include a worldwide increase in natural gas production and

consumption by 70% until 2030, followed by stagnation in demand- PRIMES price forecast of an annual increase by 3%

- 32 -

The World Gas Model – Countries in the Model

Countries included in the WGM (light green: consumption only)

- 33 -

The World Gas Model – Structure

Players and natural gas flows in the WGM

- 34 -

The World Gas Model – Players

• Producer

• Trader- one trader per producer- in charge of exports via pipeline

• Liquefier

• Regasifier

• Storage Operator- arbitrageur between low, high and peak demand seasons

• (Pipeline Operator)- to allocate pipeline capacity to traders- „Third Party Access“

• (Marketer)- represented by inverse demand function of final consumers (industry,

households/commercial, electricity)- players in brackets are modelled implicitely

- 35 -

Base Case – Global Natural Gas Market Development

Global natural gas volumes and world average wholesale price, in bcm/y and $/kcm

1,000 bcm ~ 35 Tcf

$ 100 tcm ~ 3.5$/Mcf

- 36 -

Base Case – Global Natural Gas Flows in 2030Natural gas flows in 2030 by region, in bcm/y

Truly integrated, globalized natural gas markets

Middle East and Russia/Turkmenistan as “swing suppliers”

Values not yet “updated” with economic crisis, shale gas, etc.

1,000 bcm ~ 35 Tcf

$ 100 tcm ~ 3.5$/Mcf

- 37 -

4 Hypotheses

As international markets are increasingly integrated, and regional markets are restructured, competition on natural gas markets is intensifying

Contract structures are also evolving towards more flexible arrangements; corporate structures depend upon specific strategy options

Upstream markets tend to be more oligopolistic in nature, but the risk of a “GECF cartel” or Russian dominance seem to be manageable

The integration of “unconventional” natural gas reserves (mainly shale gas, but also coalbed-methane, tight gas) may change the medium-term outlook of international LNG-trade, in particular the role of the U.S., significantly

- 38 -

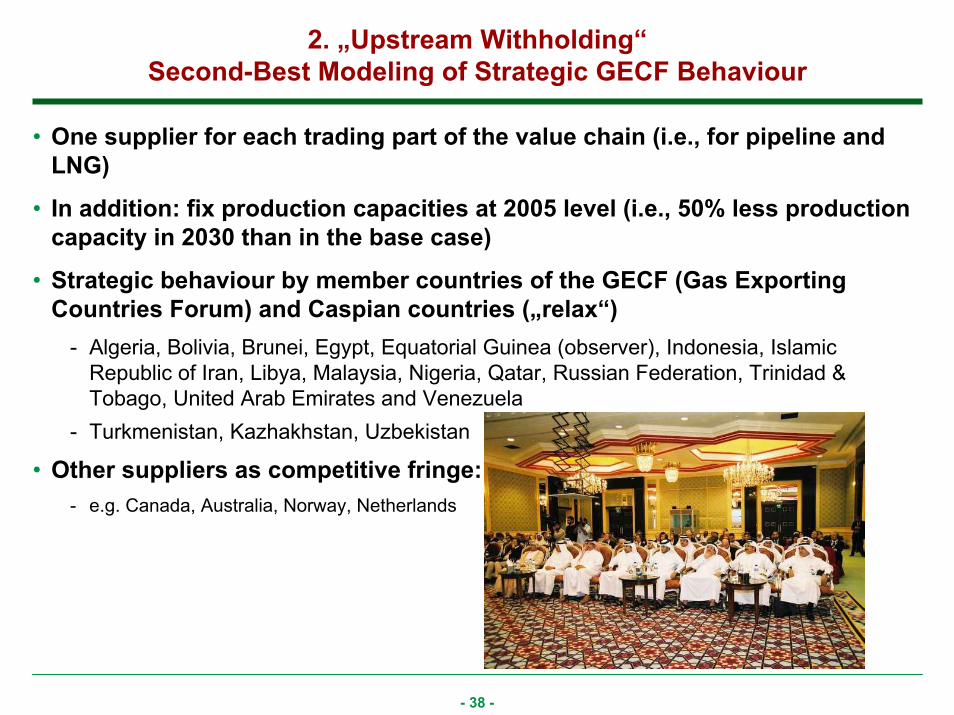

2. „Upstream Withholding“Second-Best Modeling of Strategic GECF Behaviour

• One supplier for each trading part of the value chain (i.e., for pipeline and LNG)

• In addition: fix production capacities at 2005 level (i.e., 50% less productioncapacity in 2030 than in the base case)

• Strategic behaviour by member countries of the GECF (Gas ExportingCountries Forum) and Caspian countries („relax“)

- Algeria, Bolivia, Brunei, Egypt, Equatorial Guinea (observer), Indonesia, Islamic Republic of Iran, Libya, Malaysia, Nigeria, Qatar, Russian Federation, Trinidad & Tobago, United Arab Emirates and Venezuela

- Turkmenistan, Kazhakhstan, Uzbekistan

• Other suppliers as competitive fringe:- e.g. Canada, Australia, Norway, Netherlands

- 39 -

„Upstream Withholding“: Scenario Results

• Total world production lower than in base case, despite compensation of withheld capacities by competitive fringe

• However, quite some resilience in the global system (i.e., failing suppliescan to a large extend be replaced), constrained in some cases by lackingtransport infrastructure

0

500

1000

1500

2000

2500

3000

3500

4000

4500

CC+ BC CC+ BC CC+ BC

2010 2020 2030

year

ly p

rodu

ctio

n (b

cm)

OtherGEC

- 40 -

„Upstream Withholding“: Significant Price Markups

• Price increase is significant, increases over time due to withholding in capacities (less investments)

$-

$100

$200

$300

$400

$500

$600

2005 2010 2015 2020 2025 2030

pric

e (2

005$

/kcm

)

BCCCCC+

- 41 -

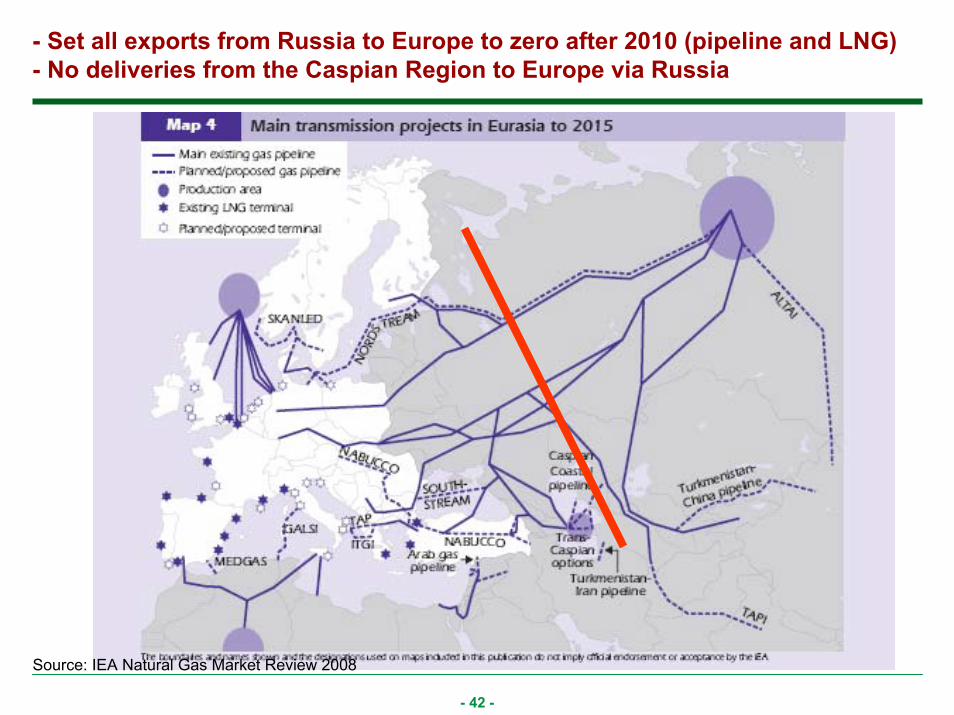

3. „Eastern Promises“ –Russian Embargo towards Europe

Source: APwww.mosnews.com

- 42 -

- Set all exports from Russia to Europe to zero after 2010 (pipeline and LNG)- No deliveries from the Caspian Region to Europe via Russia

Source: IEA Natural Gas Market Review 2008

- 43 -

„Eastern Promises“ – Russian Exports

Russian Natural Gas Distribution, in bcm/y, (Base Case/Scenario)

- 44 -

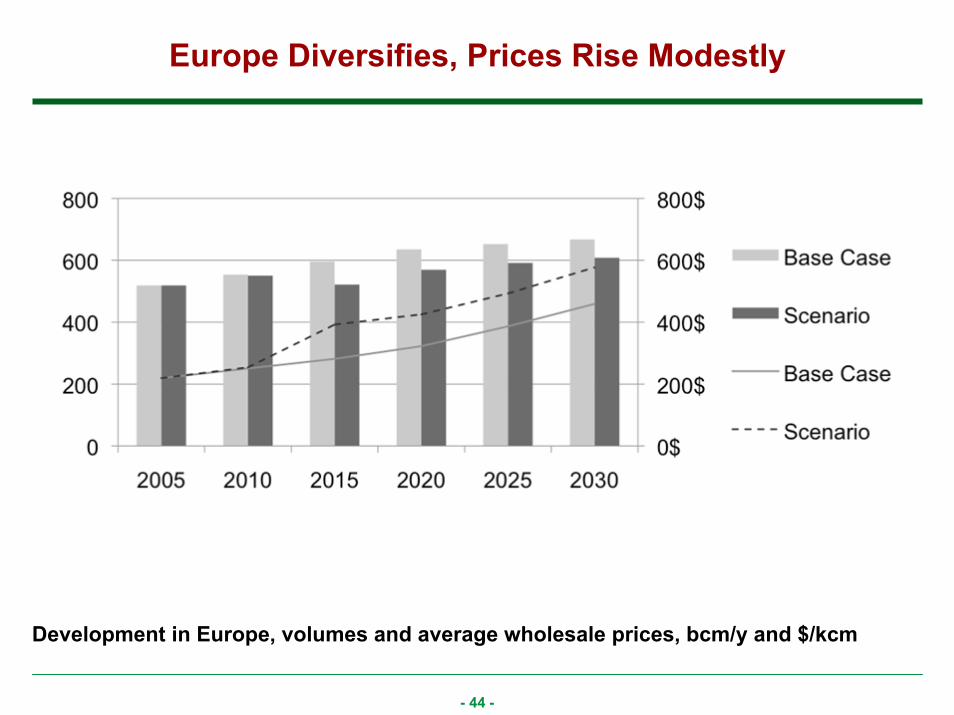

Europe Diversifies, Prices Rise Modestly

Development in Europe, volumes and average wholesale prices, bcm/y and $/kcm

- 45 -

Diversification of the European Natural Gas Supplies (incl. with LNG) Reduces the Dominance of Individual Suppliers such as Russia

• Expected increase of natural gas exports over time comes with anincreasing diversification of supplies, in favor of LNG

• High demand for LNG: mainly comes from North Africa, Africa, partly also from the Caribbean

0

100

200

300

400

500

600

2003 2010 2015 2020 2025

Exp

orts

to E

urop

e in

bcm

per

yea

r

Venezuela

Trinidad

Nigeria

UK

Netherlands

Norway

Russia

Middle East

Iran

Iraq

Egypt

Lybia

Algeria

EMF Reference Scenario, calculated with GASMOD

- 46 -

4 Hypotheses

As international markets are increasingly integrated, and regional markets are restructured, competition on natural gas markets is intensifying

Contract structures are also evolving towards more flexible arrangements; corporate structures depend upon specific strategy options

Upstream markets tend to be more oligopolistic in nature, but the risk of a “GECF cartel” or Russian dominance seem to be manageable

The integration of “unconventional” natural gas reserves (mainly shale gas, but also coalbed-methane, tight gas) may change the medium-term outlook of international LNG-trade, in particular the role of the U.S., significantly

- 47 -

4. „Barnett Shale“:Significant Increase in the Use of Shale Gas Across the Country

Source: IEA Natural Gas Market Review 2008

BarnetShale

- 48 -

Base Case – Global Natural Gas Flows in 2030Natural gas flows in 2030 by region, in bcm/y

Truly integrated, globalized natural gas markets

Middle East and Russia/Turkmenistan as “swing suppliers”

Values not yet “updated” with economic crisis, shale gas, etc.

1,000 bcm ~ 35 Tcf

$ 100 tcm ~ 3.5$/Mcf

- 49 -

„Barnett Shale“ and the Global LNG Market:Include unconventional reserves in the U.S. and Canada in production capacity

-12

-13 -10-34

-38

-49

- 50 -

„Barnett Shale“: Price Effects

• Price effects are mainly local:- in North America - in the Middle East (source of a major share of the U.S. LNG imports in the base

case)

- 51 -

- 52 -

Agenda

1. Introduction

2. Competition – Competition for LNG in the Atlantic Basin

3. Contracts – Vertical Integration and Investments

4. Cartel and Other Scenarios – A Modeling Analysis

5. Conclusions

- 53 -

4 Hypotheses

As international markets are increasingly integrated, and regional markets are restructured, competition on natural gas markets is intensifying

Contract structures are also evolving towards more flexible arrangements; corporate structures depend upon specific strategy options

Upstream markets tend to be more oligopolistic in nature, but the risk of a “GECF cartel” or Russian dominance seem to be manageable

The integration of “unconventional” natural gas reserves (mainly shale gas, but also coalbed-methane, tight gas) may change the medium-term outlook of international LNG-trade, in particular the role of the U.S., significantly