Embed Size (px)

Citation preview

LinksLinks

HOMEHOMEOptions PricingOptions Pricing

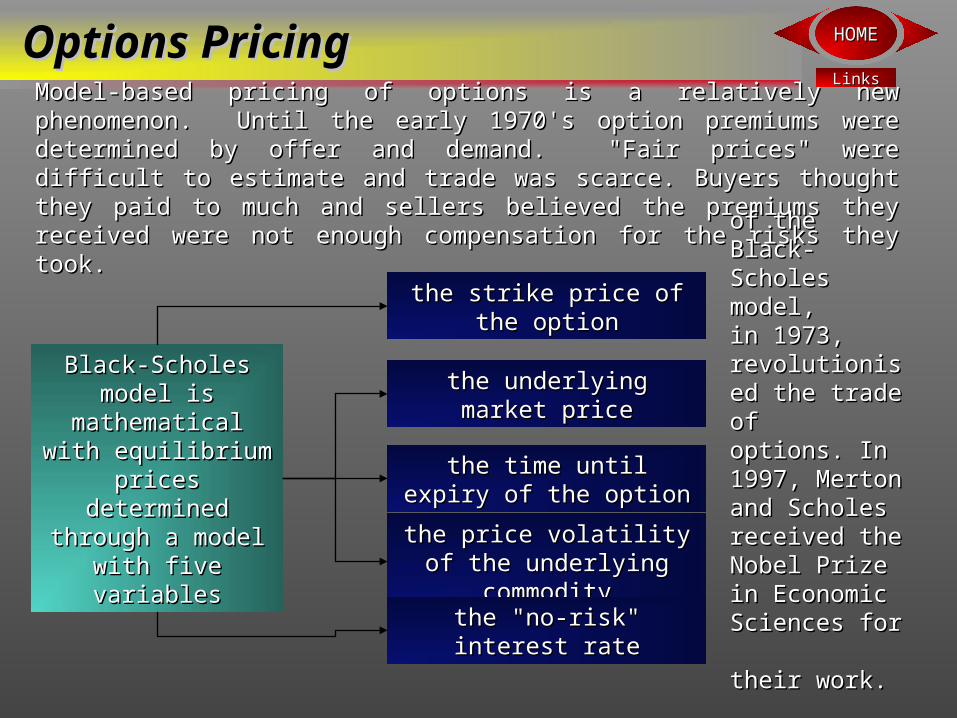

Model-based pricing of options is a relatively new phenomenon. Until the early Model-based pricing of options is a relatively new phenomenon. Until the early 1970's option premiums were determined by offer and demand. "Fair prices" 1970's option premiums were determined by offer and demand. "Fair prices" were difficult to estimate and trade was scarce. Buyers thought they paid to much were difficult to estimate and trade was scarce. Buyers thought they paid to much and sellers believed the premiums they received were not enough compensation and sellers believed the premiums they received were not enough compensation for the risks they took. for the risks they took.

Black-Scholes model Black-Scholes model is mathematical with is mathematical with

equilibrium prices equilibrium prices determined through a determined through a

model with five model with five variablesvariables

the strike price of the optionthe strike price of the option

the underlying market pricethe underlying market price

the time until expiry of the the time until expiry of the optionoption

the price volatility of the the price volatility of the underlying commodityunderlying commodity

the "no-risk" interest ratethe "no-risk" interest rate

of the Black-of the Black-Scholes model,Scholes model,in 1973, in 1973, revolutionised revolutionised the trade of the trade of options. In 1997, options. In 1997, Merton and Merton and Scholes received Scholes received the Nobel Prize the Nobel Prize in Economic in Economic Sciences for Sciences for their work. their work.

LinksLinks

HOMEHOME

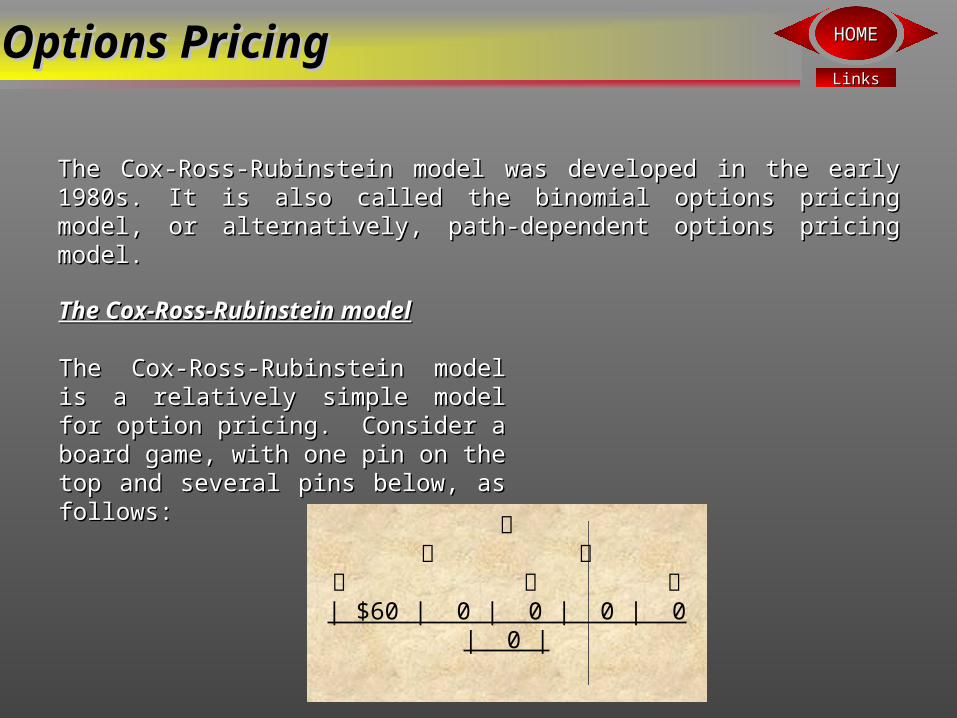

The Cox-Ross-Rubinstein model was developed in the early 1980s. It The Cox-Ross-Rubinstein model was developed in the early 1980s. It is also called the binomial options pricing model, or alternatively, is also called the binomial options pricing model, or alternatively, path-dependent options pricing model.path-dependent options pricing model.

The Cox-Ross-Rubinstein modelThe Cox-Ross-Rubinstein model

The Cox-Ross-Rubinstein model is a The Cox-Ross-Rubinstein model is a relatively simple model for option relatively simple model for option pricing. Consider a board game, pricing. Consider a board game, with one pin on the top and several with one pin on the top and several pins below, as follows:pins below, as follows:

| $60 | 0 | 0 | 0 | 0 | 0 |

Options PricingOptions Pricing

LinksLinks

HOMEHOME

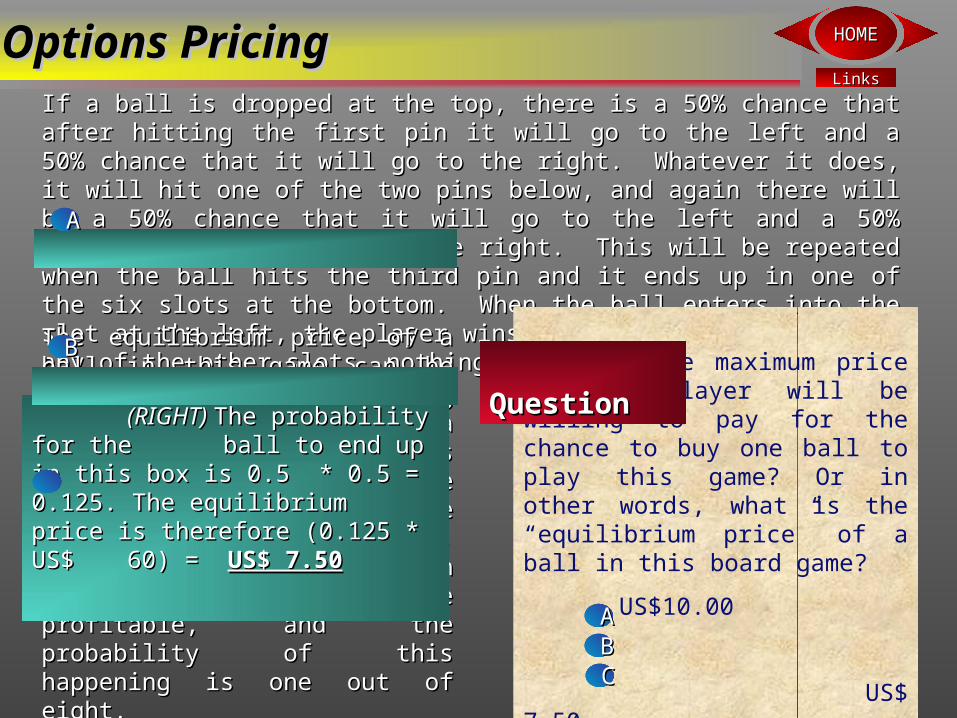

If a ball is dropped at the top, there is a 50% chance that after hitting If a ball is dropped at the top, there is a 50% chance that after hitting the first pin it will go to the left and a 50% chance that it will go to the the first pin it will go to the left and a 50% chance that it will go to the right. Whatever it does, it will hit one of the two pins below, and again right. Whatever it does, it will hit one of the two pins below, and again there will be a 50% chance that it will go to the left and a 50% chance there will be a 50% chance that it will go to the left and a 50% chance that it will go to the right. This will be repeated when the ball hits the that it will go to the right. This will be repeated when the ball hits the third pin and it ends up in one of the six slots at the bottom. When the third pin and it ends up in one of the six slots at the bottom. When the ball enters into the slot at the left, the player wins US$ 60. If it ends ball enters into the slot at the left, the player wins US$ 60. If it ends up in any of the other slots, nothing would be won.up in any of the other slots, nothing would be won.

The equilibrium price of a ball in The equilibrium price of a ball in this game can be calculated by this game can be calculated by multiplying the probability that a multiplying the probability that a profitable outcome is reached profitable outcome is reached with the profits one would have in with the profits one would have in a profitable case. In the game a profitable case. In the game above, there is only one situation above, there is only one situation in which the outcome will be in which the outcome will be profitable, and the probability of profitable, and the probability of this happening is one out of eight. this happening is one out of eight.

What is the maximum price that a player will be willing to pay for the chance to buy one ball to play this game? Or in other words, what is the “equilibrium price” of a ball in this board game?

US$10.00 US$ 7.50US$ 5.00

AABBCC

QuestionQuestion

Options PricingOptions Pricing

AA

(RIGHT) (RIGHT) The probability for the The probability for the ball to end up in this box is 0.5 ball to end up in this box is 0.5 * 0.5 = 0.125. The equilibrium * 0.5 = 0.125. The equilibrium price is therefore (0.125 * US$ price is therefore (0.125 * US$ 60) = 60) = US$ 7.50US$ 7.50

BB

LinksLinks

HOMEHOME

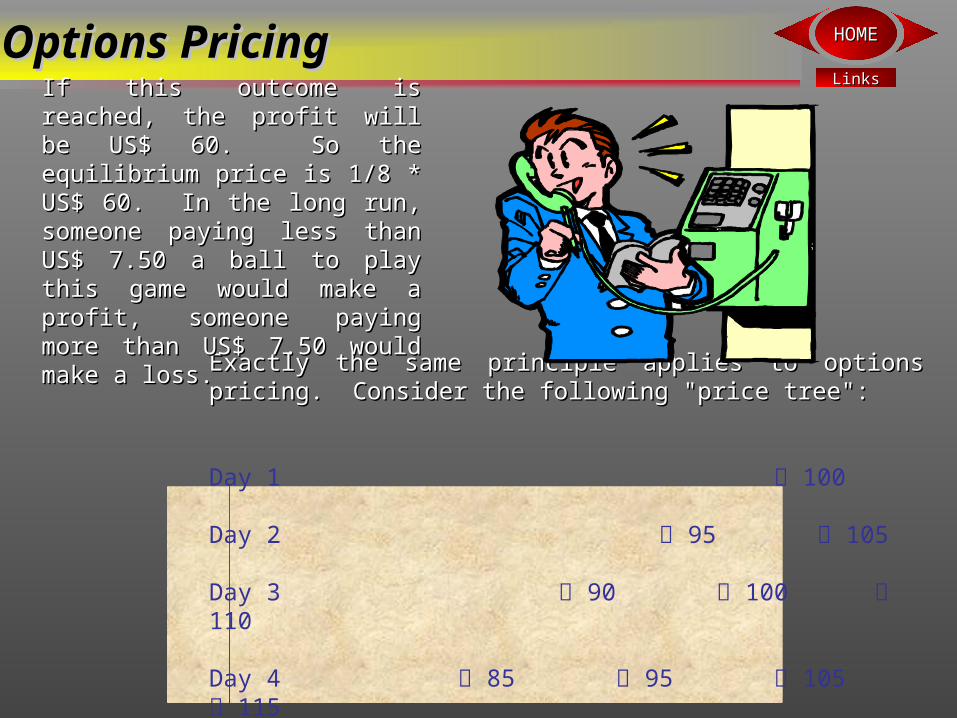

Exactly the same principle applies to options pricing. Exactly the same principle applies to options pricing. Consider the following "price tree":Consider the following "price tree":

Day 1 100

Day 2 95 105

Day 3 90 100 110

Day 4 85 95 105 115

If this outcome is reached, the If this outcome is reached, the profit will be US$ 60. So the profit will be US$ 60. So the equilibrium price is 1/8 * US$ equilibrium price is 1/8 * US$ 60. In the long run, someone 60. In the long run, someone paying less than US$ 7.50 a paying less than US$ 7.50 a ball to play this game would ball to play this game would make a profit, someone paying make a profit, someone paying more than US$ 7.50 would more than US$ 7.50 would make a loss.make a loss.

Options PricingOptions Pricing

LinksLinks

HOMEHOME

On the first day, the price is US$ On the first day, the price is US$ 100. There is a 50% chance that 100. There is a 50% chance that prices increase to 105, and a 50% prices increase to 105, and a 50% chance that prices decrease to US$ chance that prices decrease to US$ 95. Whatever happens, the next 95. Whatever happens, the next day there is again a probability of day there is again a probability of the price moving US$ 5 up (50%) the price moving US$ 5 up (50%) or down (50%), and the same or down (50%), and the same again on day 3. On day four, the again on day 3. On day four, the price is US$ 85, US$ 95, US$ 105 price is US$ 85, US$ 95, US$ 105 or US$ 115 - now, on day 1, it is or US$ 115 - now, on day 1, it is simply not known which of these simply not known which of these four prices will be reached on day four prices will be reached on day 4.4.

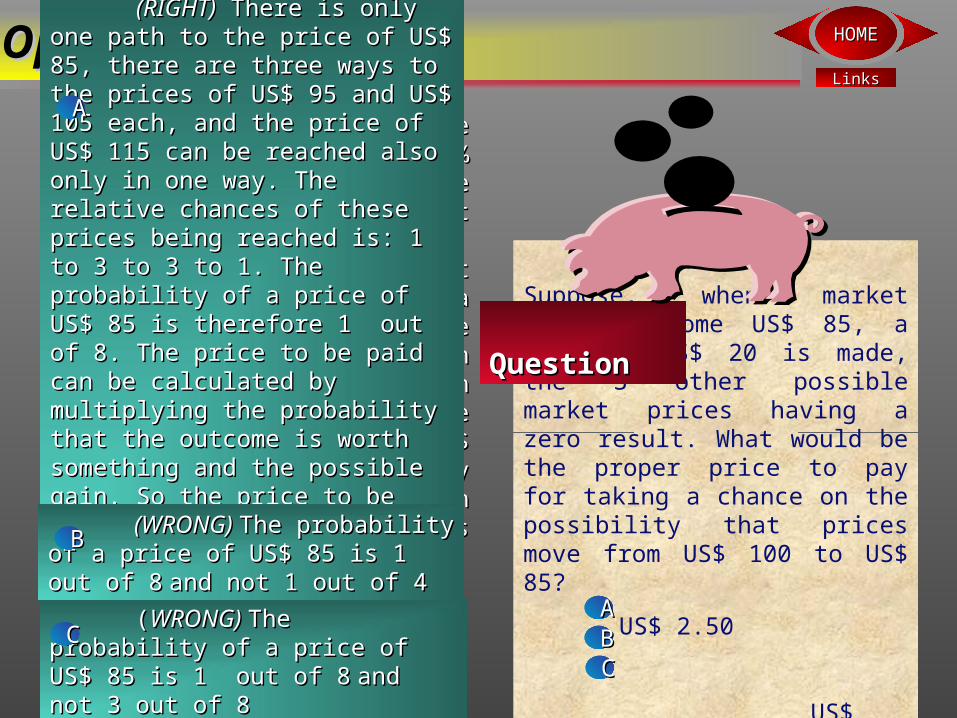

Suppose, when market prices become US$ 85, a gain of US$ 20 is made, the 3 other possible market prices having a zero result. What would be the proper price to pay for taking a chance on the possibility that prices move from US$ 100 to US$ 85?

US$ 2.50 US$ 5.00US$ 7.50

AABBCC

QuestionQuestion

Options PricingOptions Pricing (RIGHT)(RIGHT) There is only one path to the There is only one path to the price of US$ 85, there are three ways to price of US$ 85, there are three ways to the prices of US$ 95 and US$ 105 each, the prices of US$ 95 and US$ 105 each, and the price of US$ 115 can be reached and the price of US$ 115 can be reached also only in one way. The relative also only in one way. The relative chances of these prices being reached is: chances of these prices being reached is: 1 to 3 to 3 to 1. The probability of a price 1 to 3 to 3 to 1. The probability of a price of US$ 85 is therefore 1 out of 8. The of US$ 85 is therefore 1 out of 8. The price to be paid can be calculated by price to be paid can be calculated by multiplying the probability that the multiplying the probability that the outcome is worth something and the outcome is worth something and the possible gain. So the price to be paid is possible gain. So the price to be paid is 0.125 x US$ 20 = US$ 2.500.125 x US$ 20 = US$ 2.50

AA

((WRONG) WRONG) The probability of a price The probability of a price of US$ 85 is 1 out of 8of US$ 85 is 1 out of 8 and not 3 out of 8and not 3 out of 8

CC

(WRONG) (WRONG) The probability of a price The probability of a price of US$ 85 is 1 out of 8of US$ 85 is 1 out of 8 and not 1 out of 4and not 1 out of 4

BB

LinksLinks

HOMEHOME

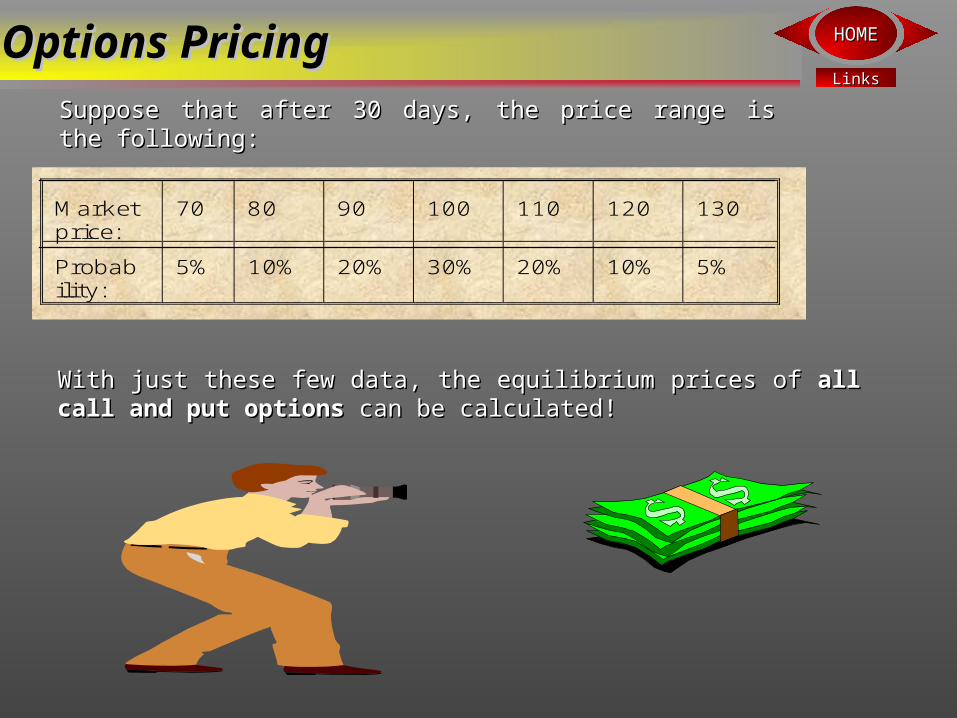

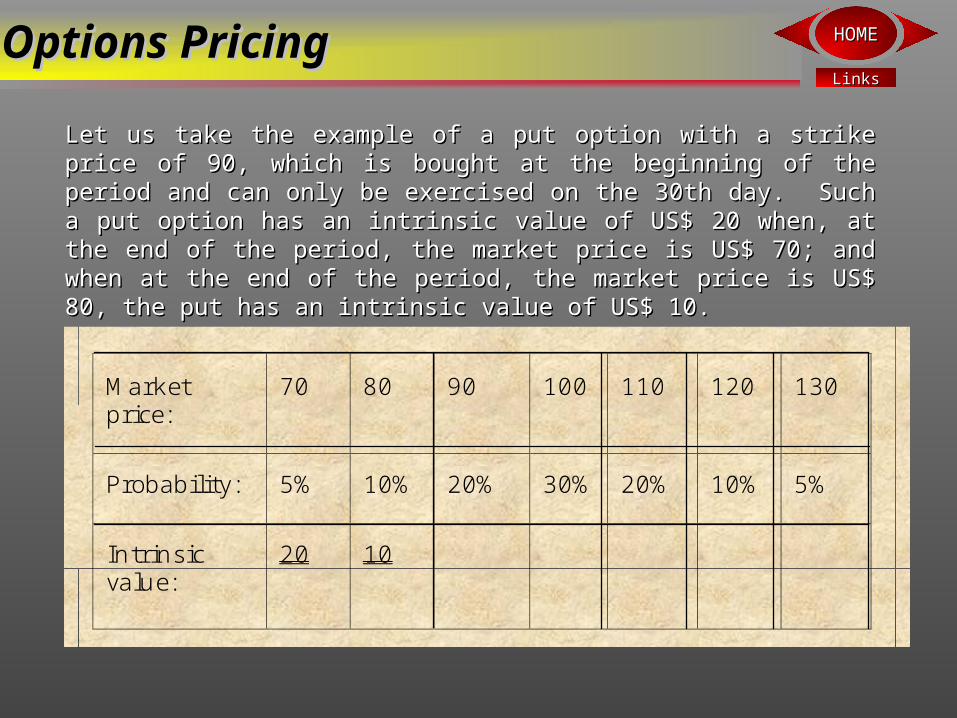

Marketprice:

70 80 90 100 110 120 130

Probability:

5% 10% 20% 30% 20% 10% 5%

Suppose that after 30 days, the price range is the Suppose that after 30 days, the price range is the following:following:

With just these few data, the equilibrium prices of With just these few data, the equilibrium prices of all call and all call and put optionsput options can be calculated! can be calculated!

Options PricingOptions Pricing

LinksLinks

HOMEHOME

Marketprice:

70 80 90 100 110 120 130

Probability: 5% 10% 20% 30% 20% 10% 5%

Intrinsicvalue:

20 10

Let us take the example of a put option with a strike price of 90, Let us take the example of a put option with a strike price of 90, which is bought at the beginning of the period and can only be which is bought at the beginning of the period and can only be exercised on the 30th day. Such a put option has an intrinsic exercised on the 30th day. Such a put option has an intrinsic value of US$ 20 when, at the end of the period, the market price is value of US$ 20 when, at the end of the period, the market price is US$ 70; and when at the end of the period, the market price is US$ US$ 70; and when at the end of the period, the market price is US$ 80, the put has an intrinsic value of US$ 10.80, the put has an intrinsic value of US$ 10.

Options PricingOptions Pricing

LinksLinks

HOMEHOME

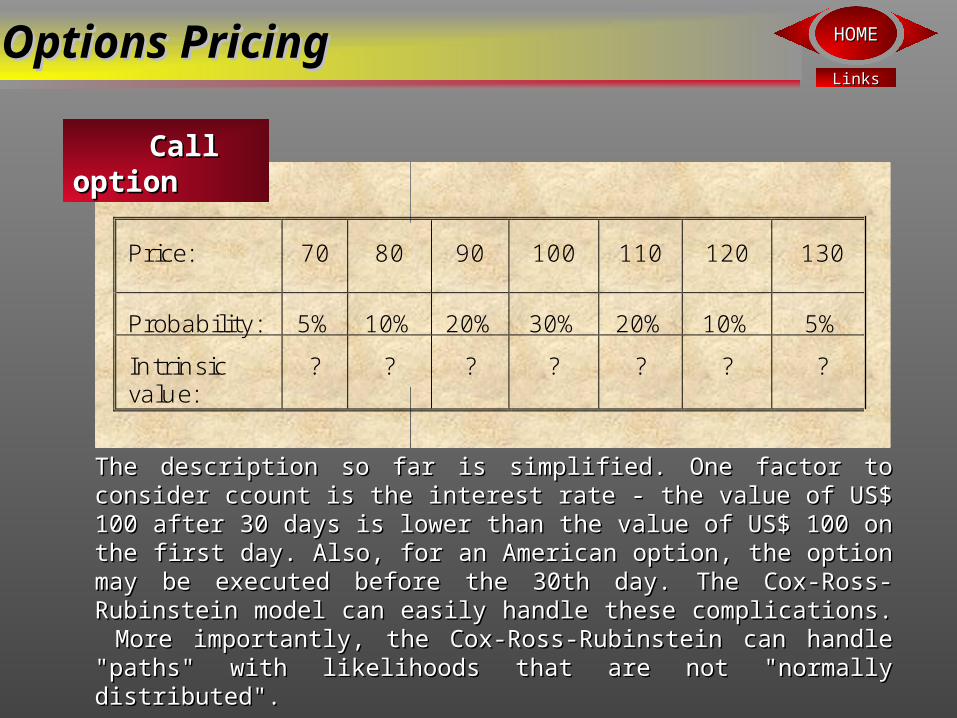

Price: 70 80 90 100 110 120 130

Probability: 5% 10% 20% 30% 20% 10% 5%

Intrinsicvalue:

? ? ? ? ? ? ?

Call optionCall option

The description so far is simplified. One factor to consider ccount The description so far is simplified. One factor to consider ccount is the interest rate - the value of US$ 100 after 30 days is lower is the interest rate - the value of US$ 100 after 30 days is lower than the value of US$ 100 on the first day. Also, for an American than the value of US$ 100 on the first day. Also, for an American option, the option may be executed before the 30th day. The Cox-option, the option may be executed before the 30th day. The Cox-Ross-Rubinstein model can easily handle these complications. Ross-Rubinstein model can easily handle these complications. More importantly, the Cox-Ross-Rubinstein can handle "paths" More importantly, the Cox-Ross-Rubinstein can handle "paths" with likelihoods that are not "normally distributed". with likelihoods that are not "normally distributed".

Options PricingOptions Pricing

LinksLinks

HOMEHOME

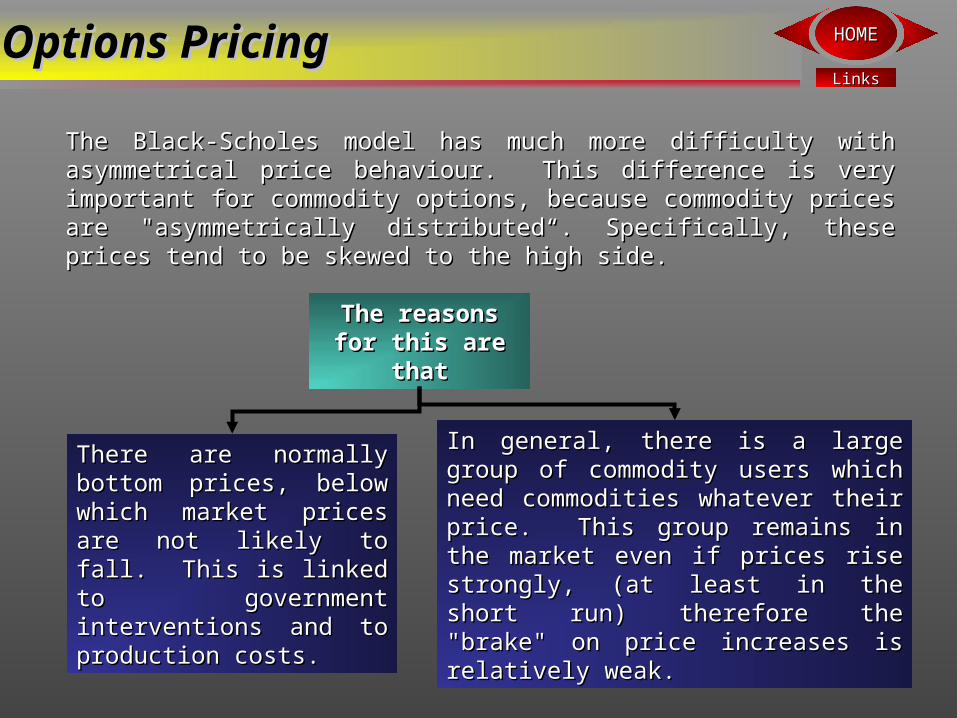

The Black-Scholes model has much more difficulty with The Black-Scholes model has much more difficulty with asymmetrical price behaviour. This difference is very important for asymmetrical price behaviour. This difference is very important for commodity options, because commodity prices are "asymmetrically commodity options, because commodity prices are "asymmetrically distributed“. Specifically, these prices tend to be skewed to the high distributed“. Specifically, these prices tend to be skewed to the high side. side.

There are normally There are normally bottom prices, below bottom prices, below which market prices are which market prices are not likely to fall. This is not likely to fall. This is linked to government linked to government interventions and to interventions and to production costs.production costs.

In general, there is a large group of In general, there is a large group of commodity users which need commodity users which need commodities whatever their price. commodities whatever their price. This group remains in the market This group remains in the market even if prices rise strongly, (at least even if prices rise strongly, (at least in the short run) therefore the in the short run) therefore the "brake" on price increases is "brake" on price increases is relatively weak. relatively weak.

The reasons The reasons for this are for this are

thatthat

Options PricingOptions Pricing

LinksLinks

HOMEHOMEOptions PricingOptions Pricing

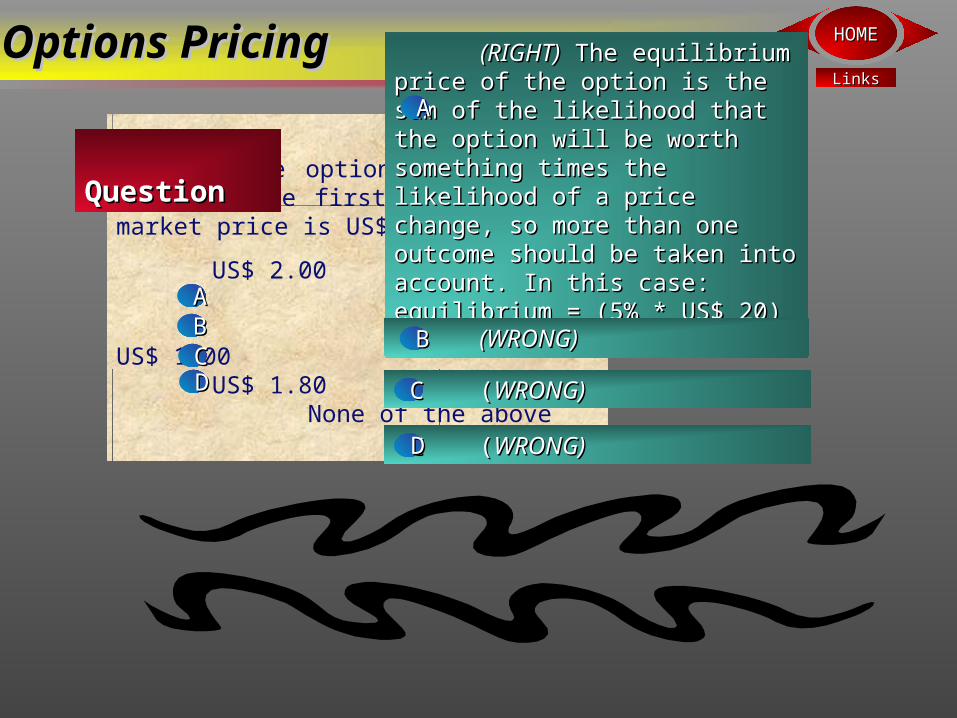

What is the option’s equilibrium price on the first day, when the market price is US$ 100?

US$ 2.00 US$ 1.00

US$ 1.80None of the above

AABBCC

QuestionQuestion

DD

(RIGHT)(RIGHT) The equilibrium price of the The equilibrium price of the option is the sum of the likelihood that option is the sum of the likelihood that the option will be worth something times the option will be worth something times the likelihood of a price change, so more the likelihood of a price change, so more than one outcome should be taken into than one outcome should be taken into account. In this case: equilibrium = (5% * account. In this case: equilibrium = (5% * US$ 20) + (10% * US$ 10) = US$ 2.00.US$ 20) + (10% * US$ 10) = US$ 2.00.

AA

((WRONG)WRONG)CC

(WRONG)(WRONG)BB

((WRONG)WRONG)CCDD

LinksLinks

HOMEHOME

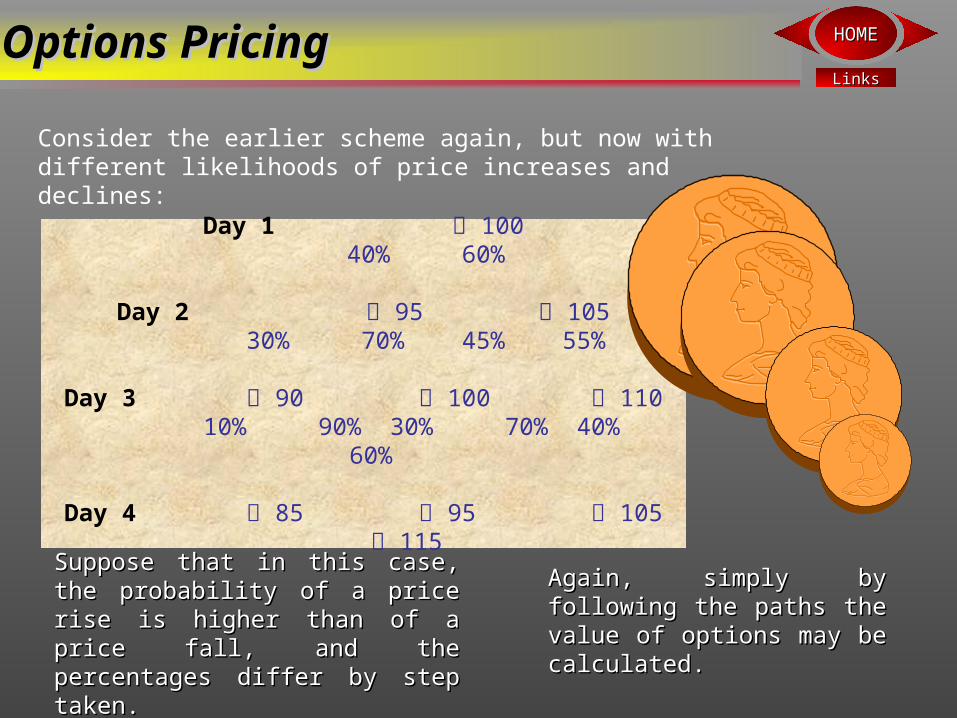

Consider the earlier scheme again, but now with different likelihoods of price increases and declines:

Day 1 100 40% 60%

Day 2 95 105 30% 70% 45% 55%

Day 3 90 100 110 10% 90% 30% 70% 40% 60%

Day 4 85 95 105 115

Again, simply by following Again, simply by following the paths the value of the paths the value of options may be calculated.options may be calculated.

Suppose that in this case, the Suppose that in this case, the probability of a price rise is probability of a price rise is higher than of a price fall, and higher than of a price fall, and the percentages differ by step the percentages differ by step taken.taken.

Options PricingOptions Pricing

LinksLinks

HOMEHOME

Consider an at-the-money call option which can only be executed on the 30th day, the market price on the first day still being US$ 100. What is its equilibrium price?

US$ 2.00 US$ 5.50

US$ 30.00

AABBCC

Question Question

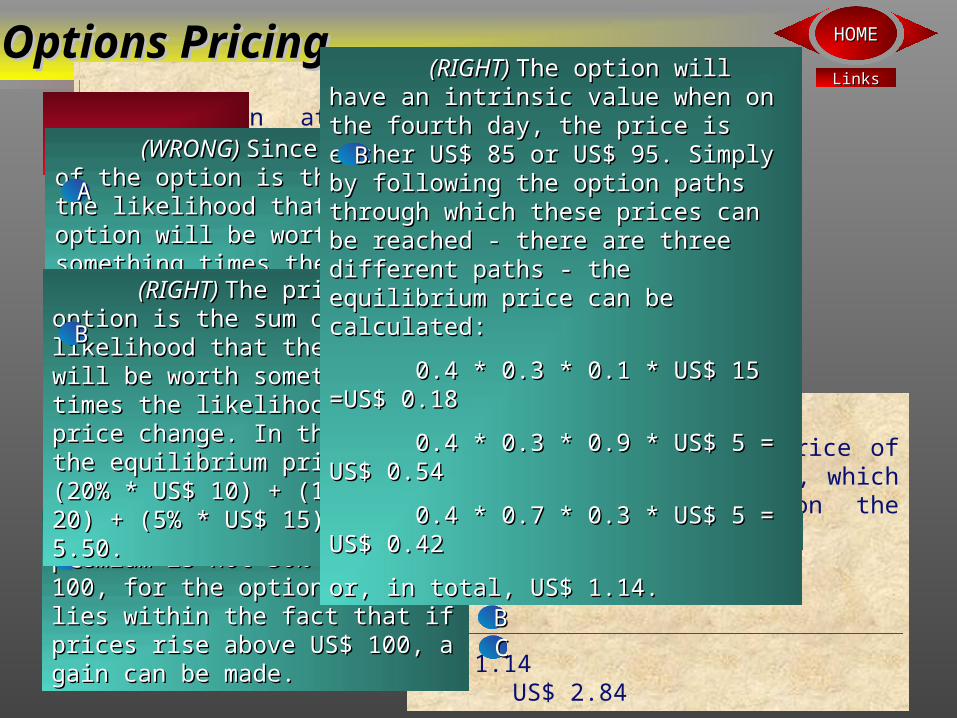

What is the equilibrium price of an at-the-money put option, which can only be executed on the fourth day?

US$ 0.72 US$ 1.14

US$ 2.84

AABBCC

Question Question

Options PricingOptions Pricing

(WRONG) (WRONG) SinceSince the price of the the price of the option is the sum of the likelihood that option is the sum of the likelihood that the option will be worth something times the option will be worth something times the likelihood of a price change. the likelihood of a price change.

AA

((WRONG) WRONG) Since the premium is not Since the premium is not 30% of US$ 100, for the option’s value 30% of US$ 100, for the option’s value lies within the fact that if prices rise lies within the fact that if prices rise above US$ 100, a gain can be made.above US$ 100, a gain can be made.

CC

(RIGHT) (RIGHT) The price of the option is the The price of the option is the sum of the likelihood that the option will sum of the likelihood that the option will be worth something times the likelihood be worth something times the likelihood of a price change. In this case, the of a price change. In this case, the equilibrium price is (20% * US$ 10) + equilibrium price is (20% * US$ 10) + (10% * US$ 20) + (5% * US$ 15) = US$ (10% * US$ 20) + (5% * US$ 15) = US$ 5.50.5.50.

BB

(WRONG)(WRONG)AA

((WRONG)WRONG)CC

(RIGHT) (RIGHT) The option will have an intrinsic The option will have an intrinsic value when on the fourth day, the price is either value when on the fourth day, the price is either US$ 85 or US$ 95. Simply by following the US$ 85 or US$ 95. Simply by following the option paths through which these prices can be option paths through which these prices can be reached - there are three different paths - the reached - there are three different paths - the equilibrium price can be calculated:equilibrium price can be calculated:

0.4 * 0.3 * 0.1 * US$ 15 =US$ 0.180.4 * 0.3 * 0.1 * US$ 15 =US$ 0.18

0.4 * 0.3 * 0.9 * US$ 5 = US$ 0.540.4 * 0.3 * 0.9 * US$ 5 = US$ 0.54

0.4 * 0.7 * 0.3 * US$ 5 = US$ 0.420.4 * 0.7 * 0.3 * US$ 5 = US$ 0.42

or, in total, US$ 1.14.or, in total, US$ 1.14.

BB