Embed Size (px)

Citation preview

Limerick Solicitors Bar Association

Professional Indemnity Insurance

Learning from 2010 and preparing for 2011

14th April 2011

David Rowe & Pauline McNamara

AgendaProfessional Indemnity Insurance – learning from 2010 and preparing for 2011

•What is Risk Management?•The 2010 renewal•How the underwriters arrive at a premium•How to move on from a claims history•Preparing for 2011

Where does Risk Management fit in

Running a law firm was relatively easy• You only had to worry about getting the work• Then managing the cost base became a requirement to

survive• Then getting paid became an issue and firms were

forced to improve their procedures• Now Risk Management has become a necessity – lack

of Risk Management can prevent a firm trading (no cover) or render it not viable (premium prohibitive)

What is Risk Management?What can go wrong and what is the potential damage caused?

How can I limit the number of things going wrong?

Accepting that things will go wrong - what systems and control can I put in place to limit the effect of things that do go wrong?

Risk Management – the build up

• Volumes of business up year on year (until 2007)

• PI insurance premiums fell (less premium for more risk)

• Firms found it difficult to service the volume - shortcuts taken

• The financial dynamics of property markets changed almost overnight

the build up cont’d• Clients and financial institutions started

looking for potential escape routes and made claims

• The profession saw a significant increase in claims against it

• The insurers began incurring significant losses

• Premiums increased

• Insurance companies began to take a more selective approach

the build up cont’d

• Insurance companies became interested in the risk profile of the profession

• When they looked they did not like what they saw and regard the profession as high risk and substantially unmanaged

• Now likely to insist on firms managing risk

• Encouraged by the number of firms who have voluntarily attained risk management accreditation, but legacy problems persist.

The stakeholders - the insurance companies

• See solicitors as high risk, following high claims

• Will pick and choose

• Will look for systems to mitigate risk

• Will audit their clients

• Want to work with firms to improve their risk profile

• Accept that problems occur, looking for post loss corrective actions

The stakeholders - the profession

• Trading conditions difficult and feel they cannot take more of a burden

• Renewal in December 2010 very difficult, multiple forms, uncertainties in getting cover at all and huge premium increases

• Feel overregulated and see risk management as more of the same

• Practitioners who are claims free struggle to see the value in this, most accept the insurers hold all the cards

The Insurance Market• XL through AON

• SMDF

• Chartis Insurance • Liberty International Insurance

• UK General Insurance Ireland (UKGII)

• Axis Insurance

• Assigned Risks Pool (ARP)

Challenges• Late exit of RSA and Quinn Insurance

• Chartis heavy handed approach to existing book and not in the market for new business

• AON/XL very aggressive/ large primary limits

• New entrants to the market very late in process – last week in November – looked for risk management reports/file audits

• New entrants required supplementary forms

• Lack of consistency in underwriting criteria applied – Chartis in particular

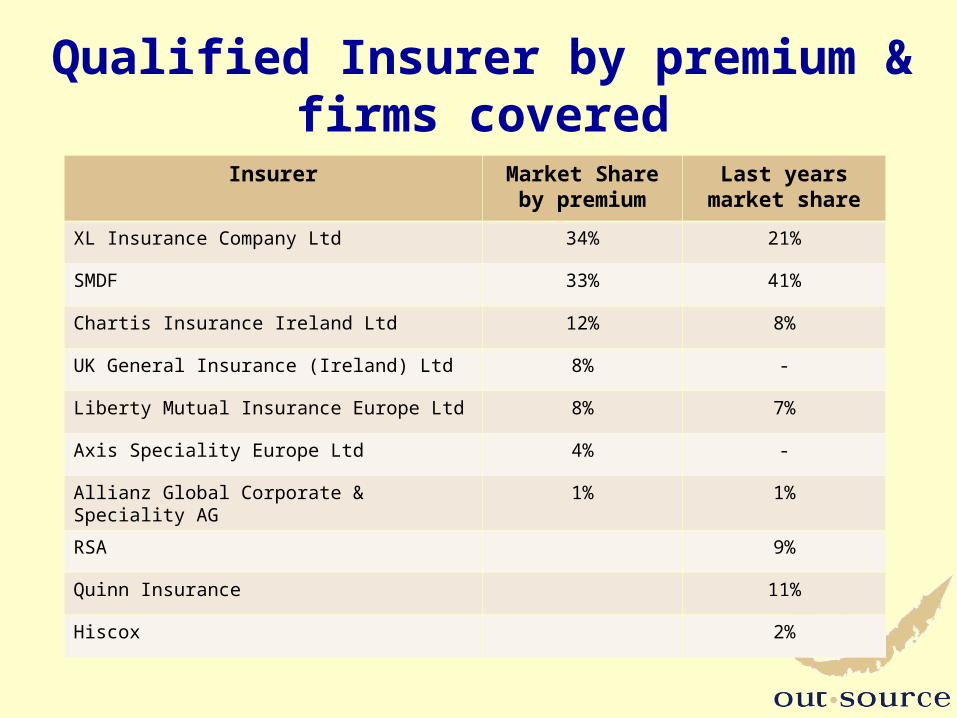

Qualified Insurer by premium & firms covered

Insurer Market Share by premium

Last years market share

XL Insurance Company Ltd 34% 21%

SMDF 33% 41%

Chartis Insurance Ireland Ltd 12% 8%

UK General Insurance (Ireland) Ltd 8% -

Liberty Mutual Insurance Europe Ltd 8% 7%

Axis Speciality Europe Ltd 4% -

Allianz Global Corporate & Speciality AG 1% 1%

RSA 9%

Quinn Insurance 11%

Hiscox 2%

Pricing - 2010

• Up 14% overall

• Low risk firms (per solicitor)– Start ups - €6K to €10K– Established firms - €10K to €15K– Larger established firms - €7k to €10K

• High Risk– Up to €50K to €100K

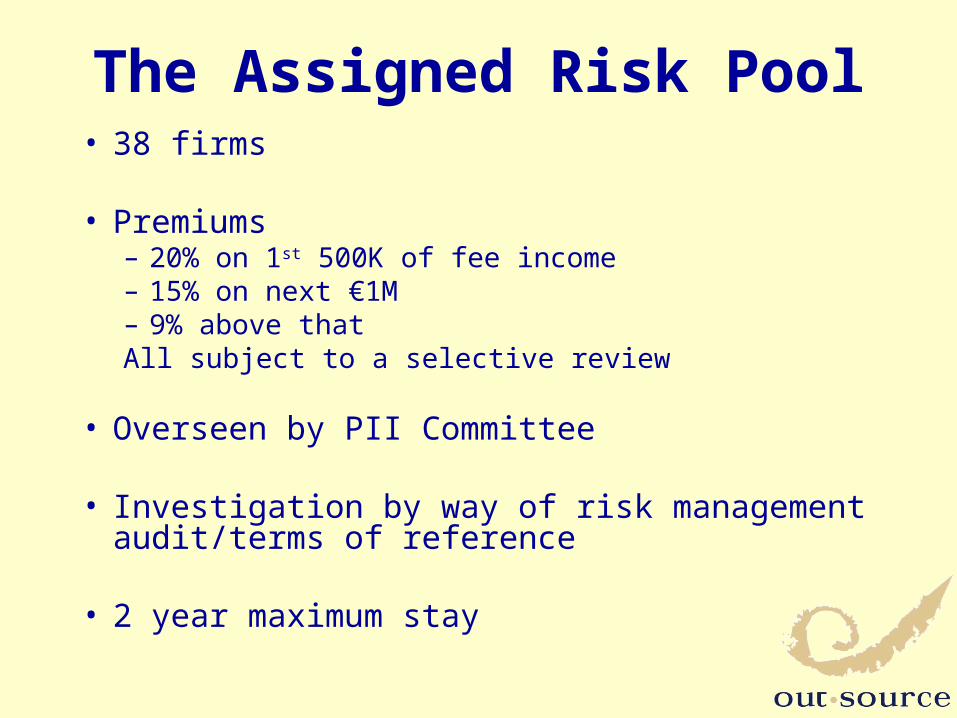

The Assigned Risk Pool• 38 firms

• Premiums– 20% on 1st 500K of fee income– 15% on next €1M– 9% above thatAll subject to a selective review

• Overseen by PII Committee

• Investigation by way of risk management audit/terms of reference

• 2 year maximum stay

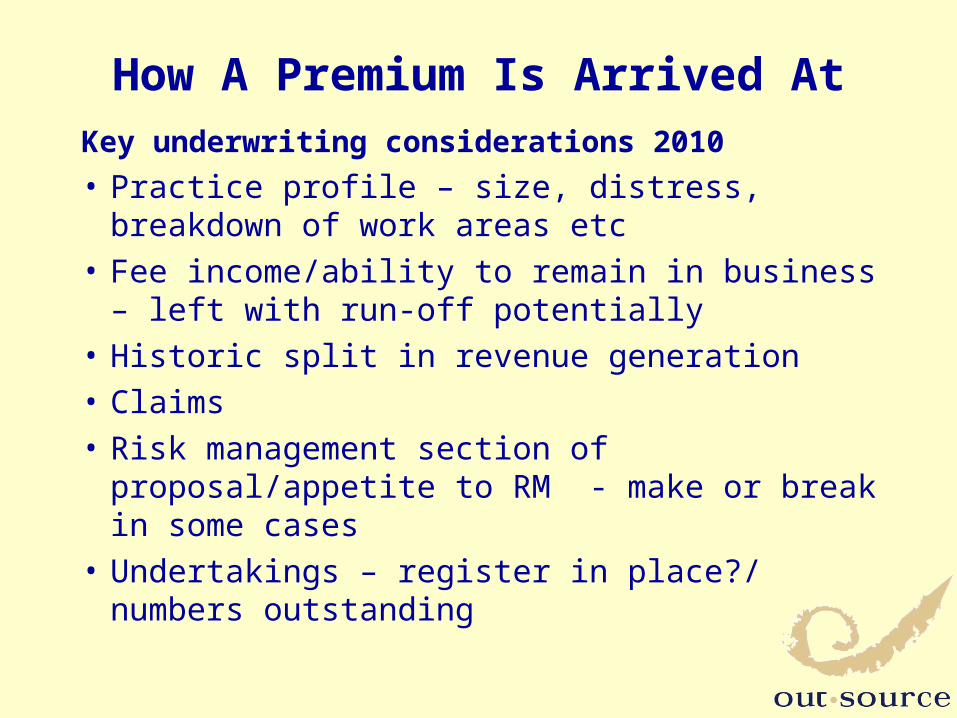

How A Premium Is Arrived At

Key underwriting considerations 2010

• Practice profile – size, distress, breakdown of work areas etc

• Fee income/ability to remain in business – left with run-off potentially

• Historic split in revenue generation• Claims• Risk management section of proposal/appetite to

RM - make or break in some cases• Undertakings – register in place?/ numbers

outstanding

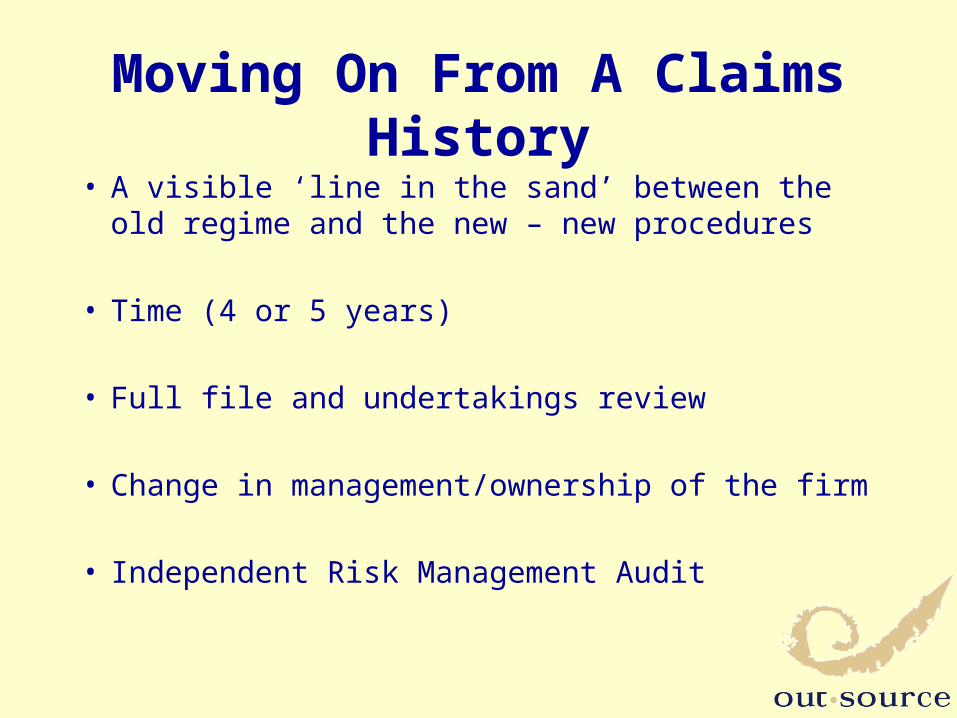

Moving On From A Claims History

• A visible ‘line in the sand’ between the old regime and the new – new procedures

• Time (4 or 5 years)

• Full file and undertakings review

• Change in management/ownership of the firm

• Independent Risk Management Audit

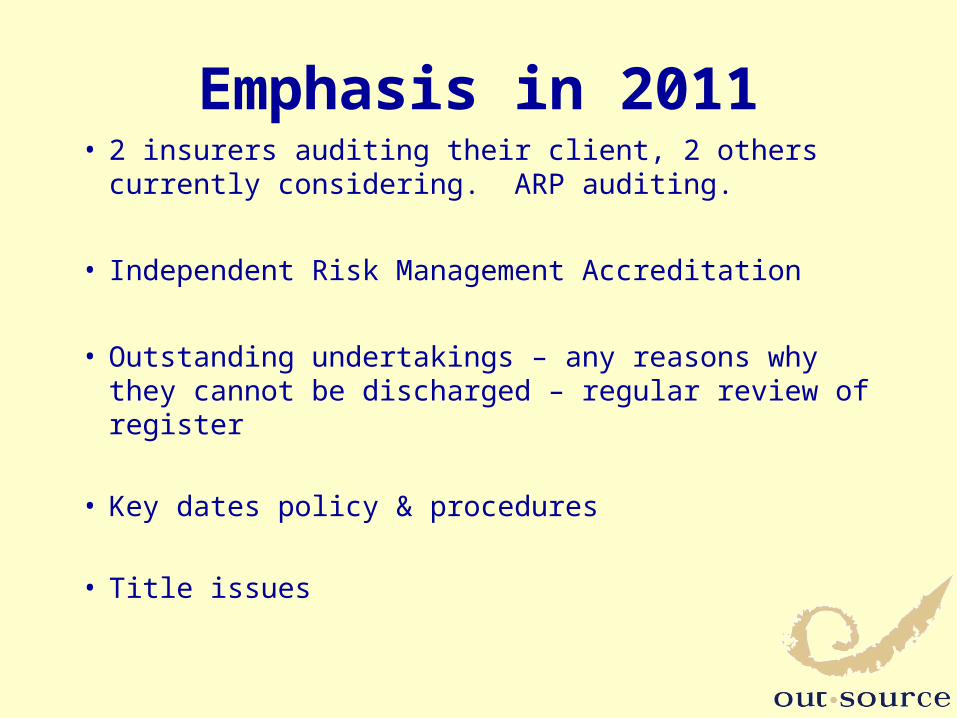

Emphasis in 2011• 2 insurers auditing their client, 2 others currently

considering. ARP auditing.

• Independent Risk Management Accreditation

• Outstanding undertakings – any reasons why they cannot be discharged – regular review of register

• Key dates policy & procedures

• Title issues

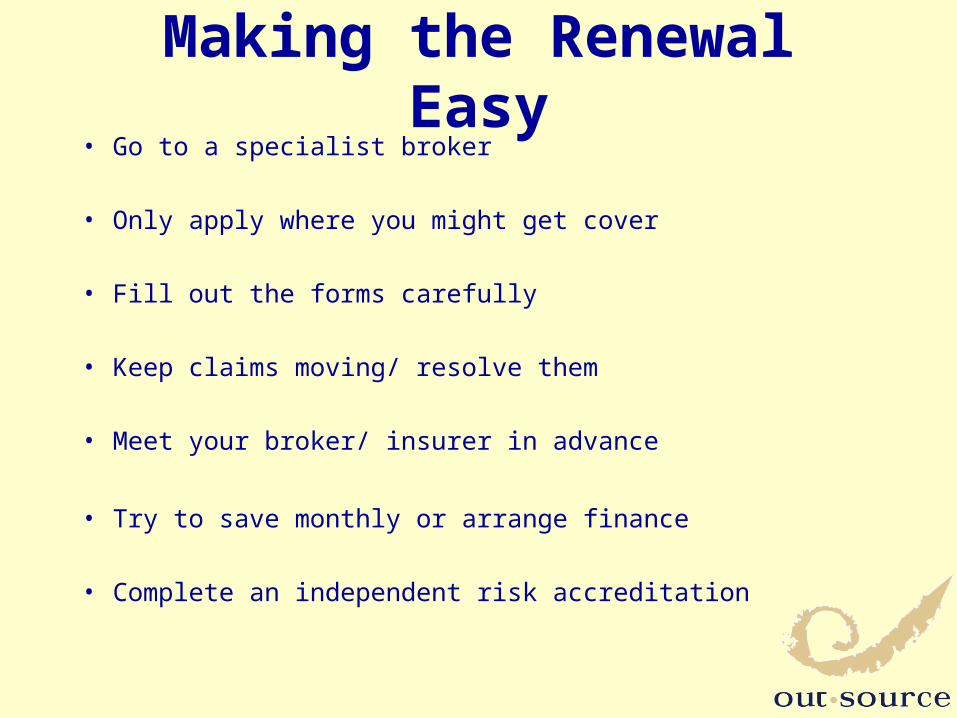

Making the Renewal Easy• Go to a specialist broker

• Only apply where you might get cover

• Fill out the forms carefully

• Keep claims moving/ resolve them

• Meet your broker/ insurer in advance

• Try to save monthly or arrange finance

• Complete an independent risk accreditation

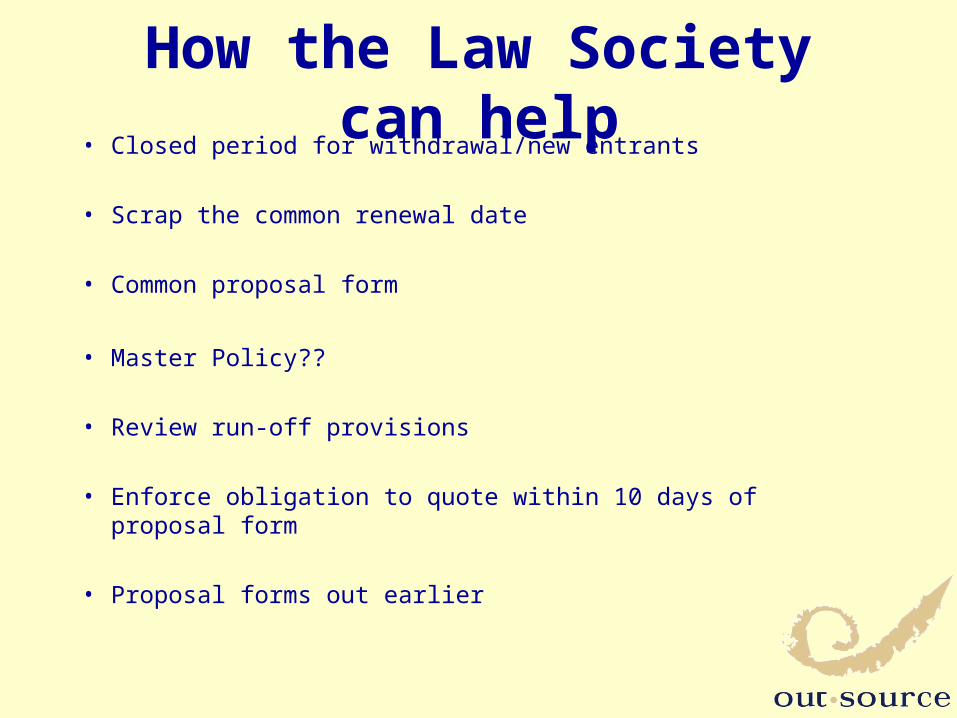

How the Law Society can help• Closed period for withdrawal/new entrants

• Scrap the common renewal date

• Common proposal form

• Master Policy??

• Review run-off provisions

• Enforce obligation to quote within 10 days of proposal form

• Proposal forms out earlier

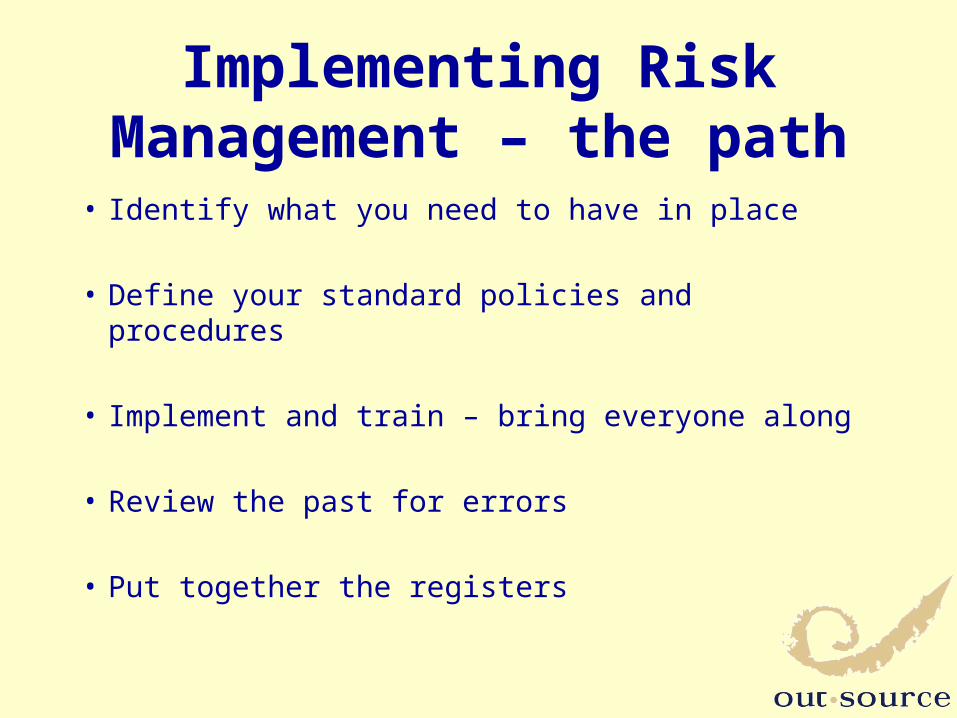

Implementing Risk Management – the path

• Identify what you need to have in place

• Define your standard policies and procedures

• Implement and train – bring everyone along

• Review the past for errors

• Put together the registers

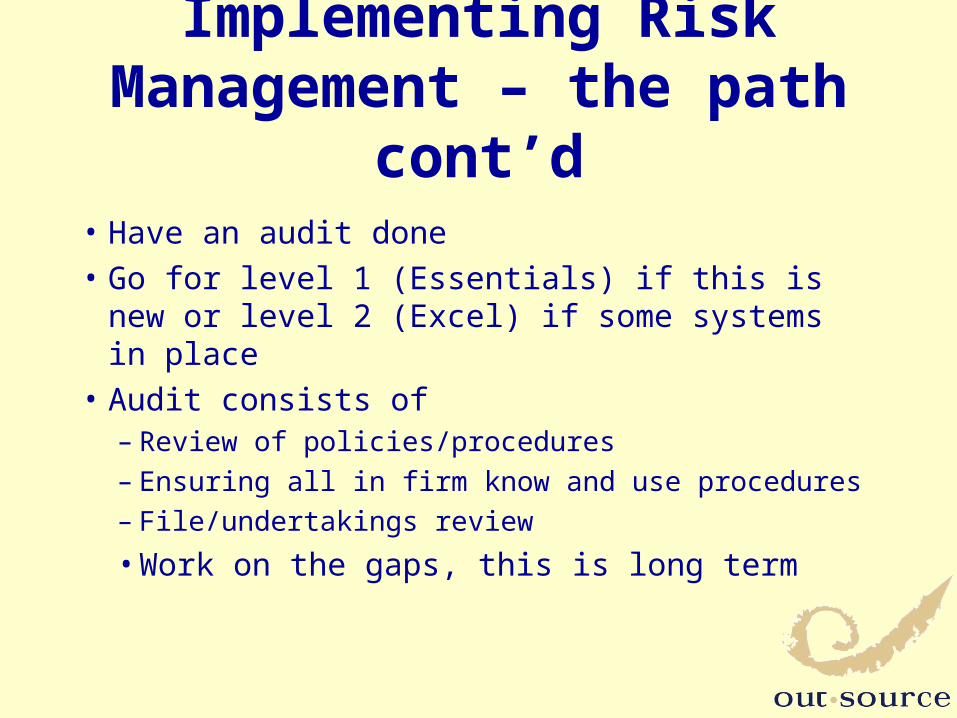

Implementing Risk Management – the path cont’d

• Have an audit done

• Go for level 1 (Essentials) if this is new or level 2 (Excel) if some systems in place

• Audit consists of – Review of policies/procedures– Ensuring all in firm know and use procedures– File/undertakings review

• Work on the gaps, this is long term

Implementing a risk management strategy

Practical Tips• Allocate sufficient time and resources – a partner

needs to lead the effort

• Risk management is a culture not an event – it is long term

• Very few firms in Ireland would pass the standard without preparation – this is as expected

• Make it an office wide project, the benefits come from eyes and ears throughout

• Remove the fear factor – this is a positive step and the benefits are significant

How to start - choices

• Do it yourself

• Take it on with external assistance, pre-audit, policies and procedures, experienced help.

Sample of RequirementsClient Management (1 out of 8 standards)• Formal procedures required for engaging new

clients, limitation of liabilities etc• Who and on what terms

– Review creditworthiness

• Can we do the work?– Resources and expertise

• How do we staff it?• Partner involvement from the start

Client Management (1 out of 8 standards) cont’d

Policies needed- Partner sign-off of file matter opening forms (ensure

compliance going forward)- Engagement letter/S68 letter put in place – but

standardised where possible- Conflicts of interest policy- Anti-money laundering policy- Complaints policy (ensure you are aware of and adhere

to the policy)- Disengagement procedures (in place – but use of

disengagement letters recently introduced)

Common myths• Risk management is a bureaucratic exercise of no

value• Risk management is an event you have to comply

with once a year (passing the exam)• Doing nothing is an option• This is a contentious process where the Risk

Management Auditor wants to highlight your weaknesses

Conclusions

Benefits from the practitioners perspective

• Achievement of an approved quality standard

• Improved efficiency

• Reduction in complaints and potential claims

• Lower insurance premium

• Savings in time, worry and expenditure

• Greater profitability

• Potentially a win/win situation

Conclusions• Insurance is now the 3rd biggest cost in running a

firm

• 2010 renewal very difficult, 2011 unlikely to be any better

• Pricing levels to remain at current levels

• Now part of staying in business – can be fatal

• Being pro-active is key, don’t just wait for it to happen

• Has become part of doing business and making a living

For further information contact:

David Rowe

Managing Director

Outsource

Ph: 01 6788490

Email: [email protected]