Embed Size (px)

Citation preview

LandDevelopment

TransportInvestment

AccessibiAccessibilitylity

The Role of Transportation Investments inThe Role of Transportation Investments inShaping Land DevelopmentShaping Land Development

Robert CerveroRobert CerveroUC BerkeleyUC Berkeley

Five Points (“Truths”?)Five Points (“Truths”?)

1) Regionally, impacts are mainly Redistributive.

Highways:Highways: California County Investments (Boarnet) Beltway Studies

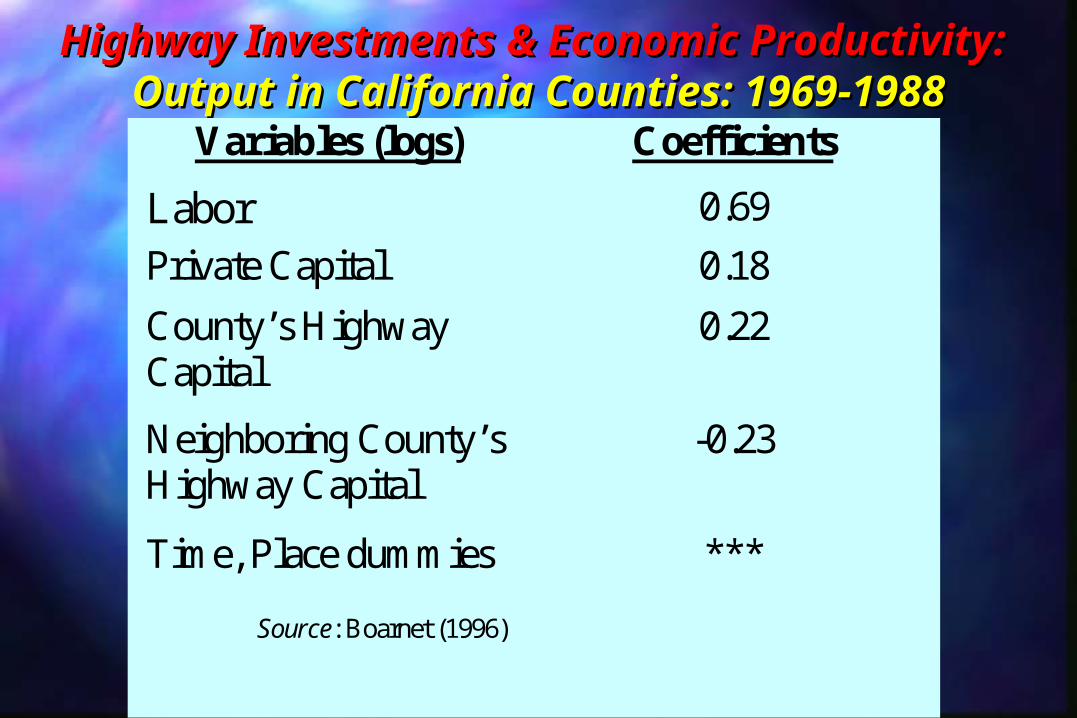

Highway Investments & Economic Highway Investments & Economic Productivity: Productivity:

Output in California Counties: 1969-1988Output in California Counties: 1969-1988Variables (logs) Coefficients

Labor 0.69

Private Capital 0.18

County’s Highway Capital

0.22

Neighboring County’s Highway Capital

-0.23

Time, Place dummies ***

Source: Boarnet (1996)

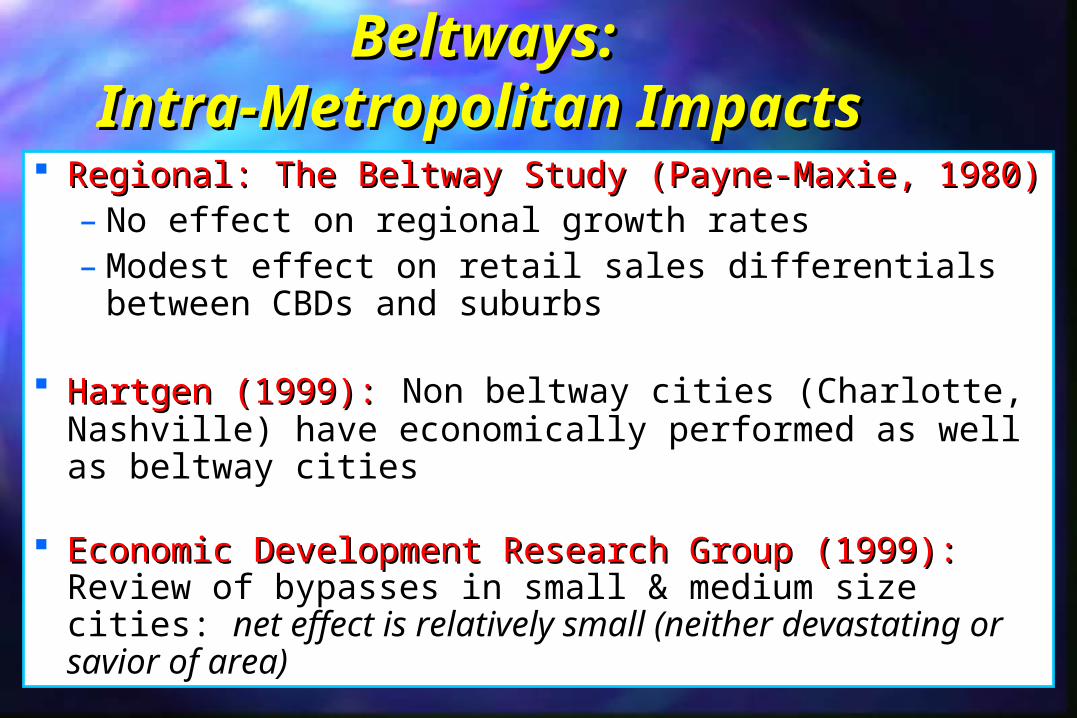

Beltways: Beltways: Intra-Metropolitan ImpactsIntra-Metropolitan Impacts

Regional: The Beltway Study (Payne-Maxie, 1980)Regional: The Beltway Study (Payne-Maxie, 1980)– No effect on regional growth rates – Modest effect on retail sales differentials between

CBDs and suburbs

Hartgen (1999):Hartgen (1999): Non beltway cities (Charlotte, Nashville) have economically performed as well as beltway cities

Economic Development Research Group (1999): Economic Development Research Group (1999): Review of bypasses in small & medium size cities: net effect is relatively small (neither devastating or savior of area)

22ndnd Point Point

2) Growth is a Prerequisite for “Big” Land Use Changes (i.e., has to be something to redistribute).

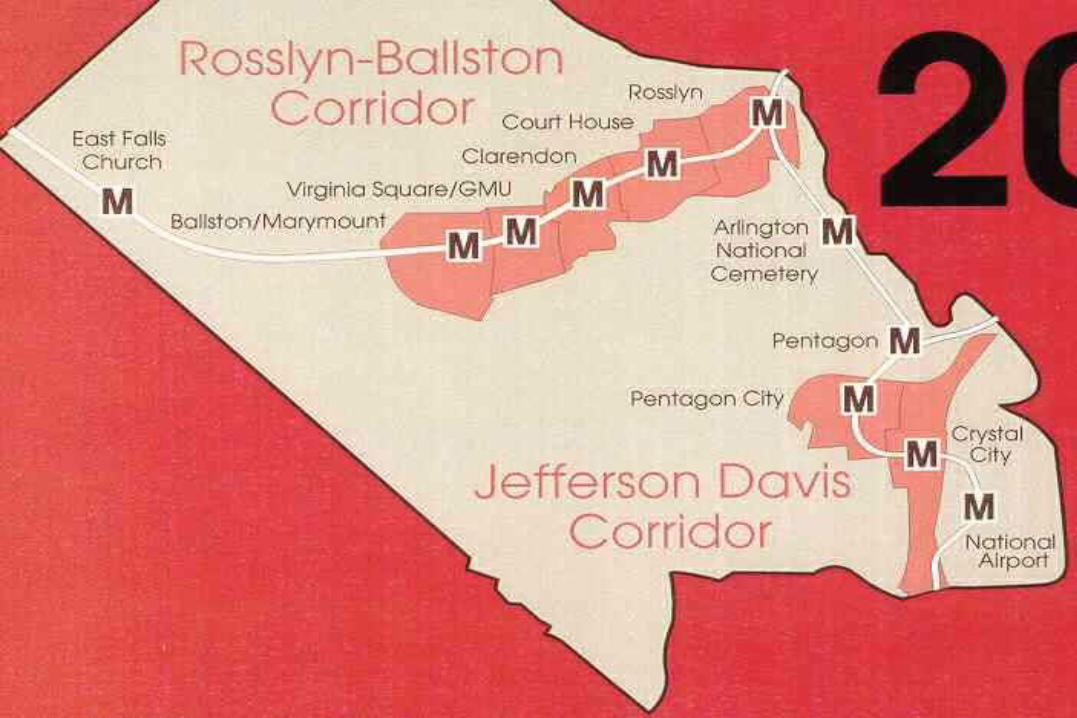

Transit (New Growth Nodes):Transit (New Growth Nodes): Arlington County’s Metrorail

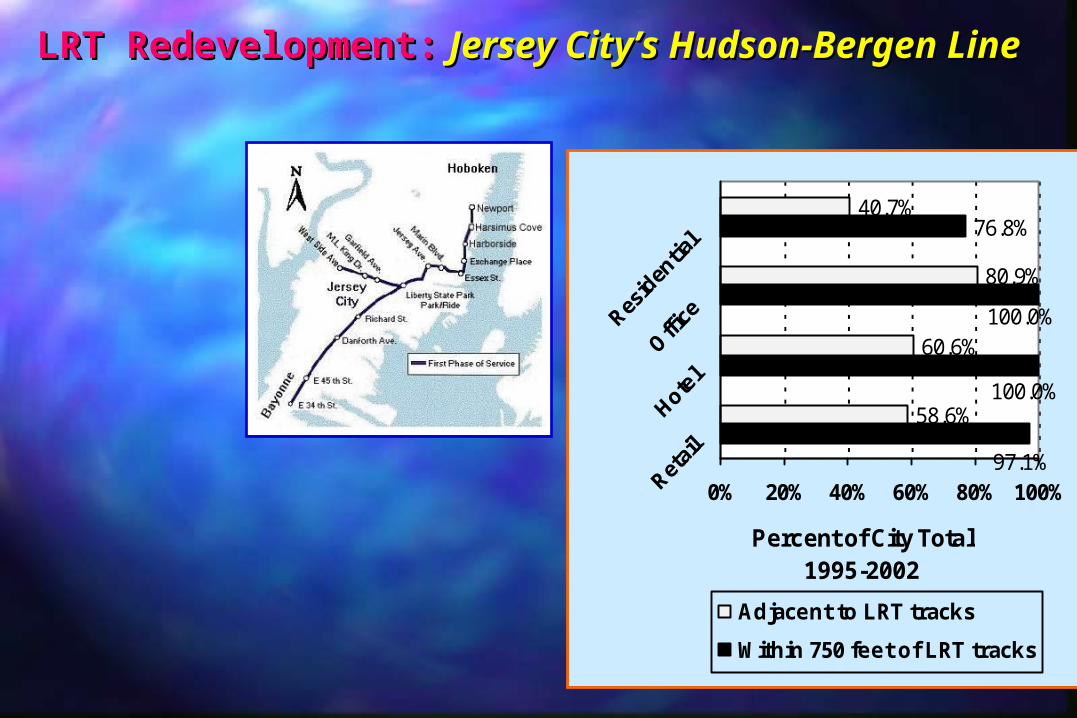

Transit (Redevelopment):Transit (Redevelopment): New Jersey (Jersey City; Commuter Rail Towns)

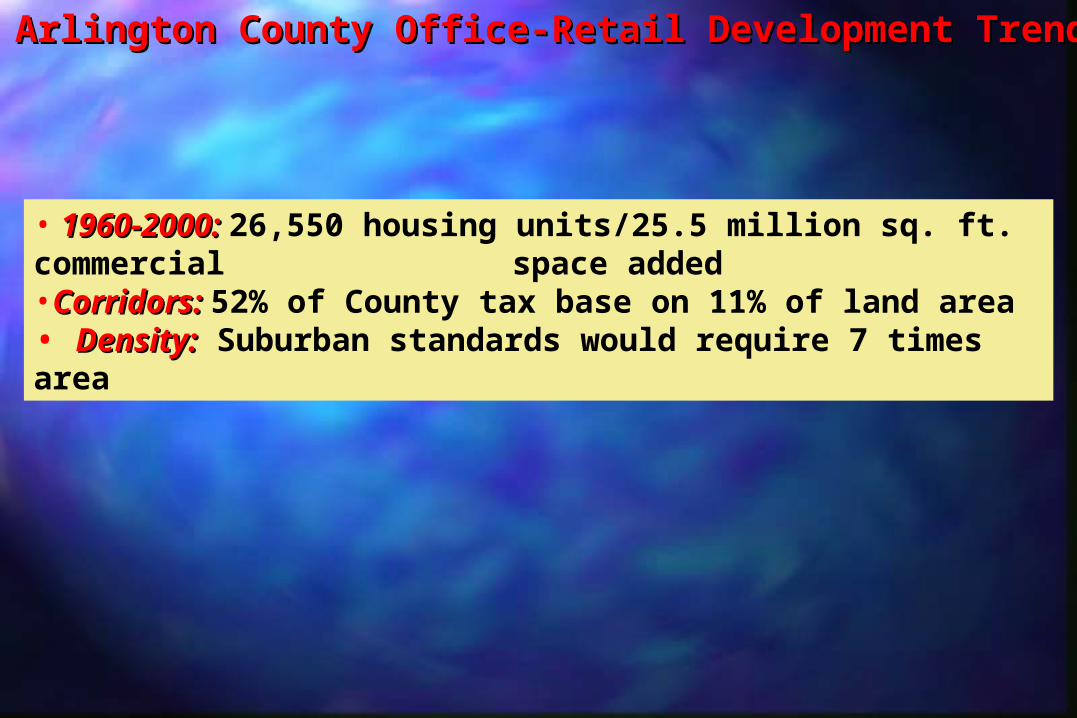

Arlington County Office-Retail Development TrendsArlington County Office-Retail Development Trends

• 1960-2000:1960-2000: 26,550 housing units/25.5 million sq. ft. commercial space added •Corridors:Corridors: 52% of County tax base on 11% of land area• Density:Density: Suburban standards would require 7 times area

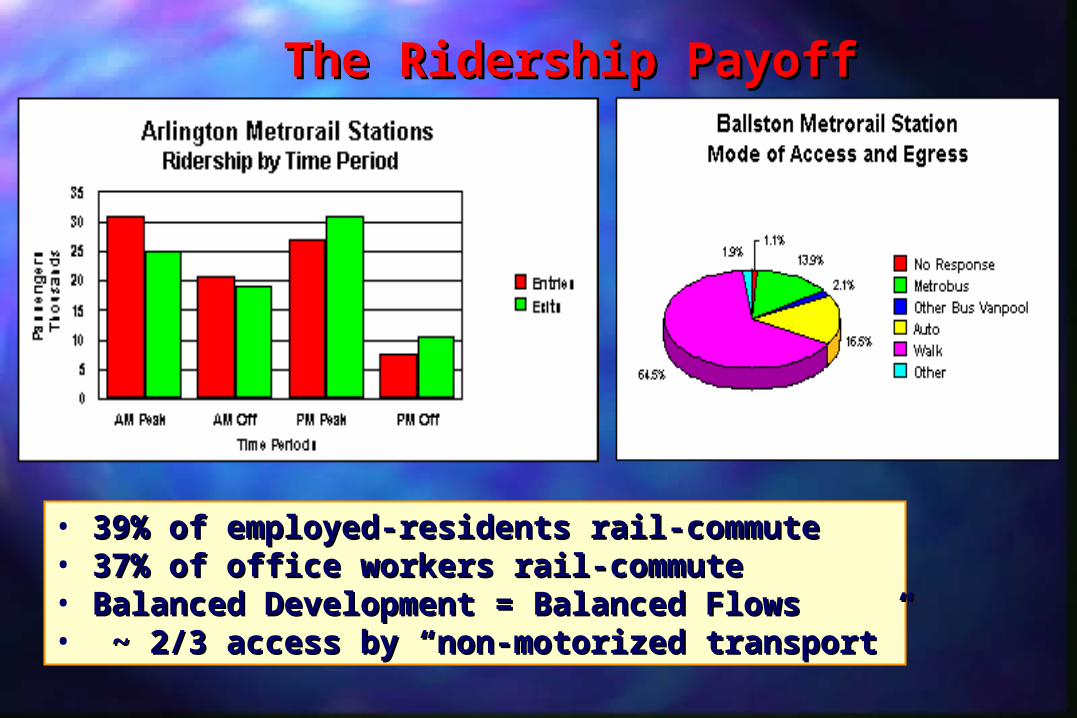

The Ridership Payoff The Ridership Payoff

• 39% of employed-residents rail-commute 39% of employed-residents rail-commute • 37% of office workers rail-commute37% of office workers rail-commute• Balanced Development = Balanced FlowsBalanced Development = Balanced Flows• ~ 2/3 access by “non-motorized transport”~ 2/3 access by “non-motorized transport”

76.8%

58.6%

60.6%

80.9%

40.7%

97.1%

100.0%

100.0%

0% 20% 40% 60% 80% 100%

Percent of City Total1995-2002

Adjacent to LRT tracks

Within 750 feet of LRT tracks

LRT Redevelopment:LRT Redevelopment: Jersey City’s Hudson-Bergen Line Jersey City’s Hudson-Bergen Line

33rdrd Point Point

3) Timing/Congestion Levels Matter

Transit:Transit: Santa Clara County’s Land-Value Premiuims

Highways: Highways: California: Freeway Expansions Induce Big

Land Use Changes Ohio: Road investment have little impact

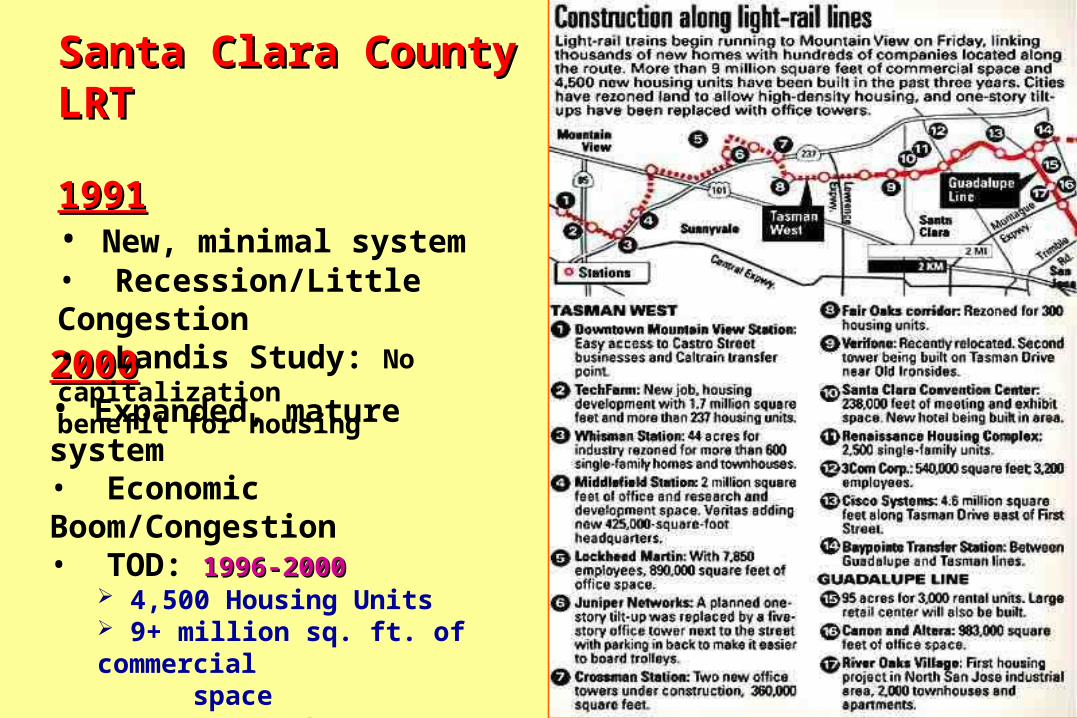

20002000• Expanded, mature system• Economic Boom/Congestion• TOD: 1996-20001996-2000

4,500 Housing Units 9+ million sq. ft. of commercial space

• Cervero Study: AppreciableCapitalization benefits

Santa Clara Santa Clara County LRTCounty LRT

19911991• New, minimal system• Recession/Little Congestion• Landis Study: No capitalization benefit for housing

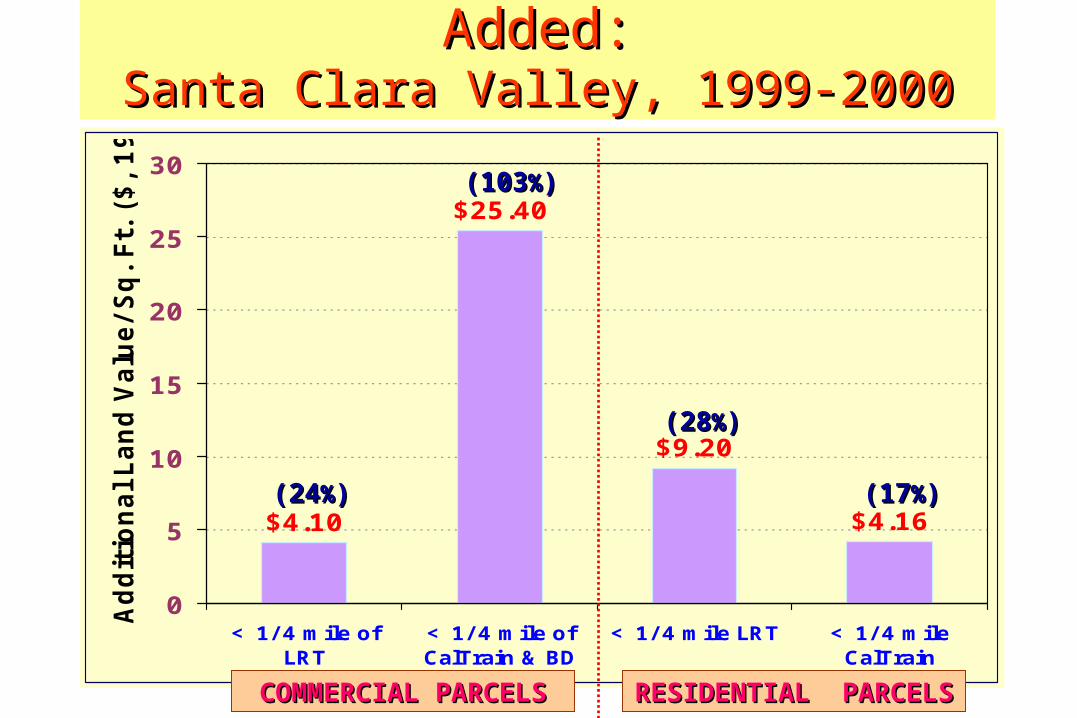

Transit Proximity & Value-Added:Transit Proximity & Value-Added:Santa Clara Valley, 1999-2000Santa Clara Valley, 1999-2000

$4.10

$25.40

$9.20

$4.16

0

5

10

15

20

25

30

< 1/ 4 mile ofLRT

< 1/ 4 mile ofCalTrain & BD

< 1/ 4 mile LRT < 1/ 4 mileCalTrain

Addit

ional Land V

alu

e/Sq. Ft.

($, 1999)

(24(24%%))

(103(103%%))

(28(28%%))

(17(17%%))

COMMERCIAL COMMERCIAL PARCELSPARCELS

RESIDENTIAL RESIDENTIAL PARCELSPARCELS

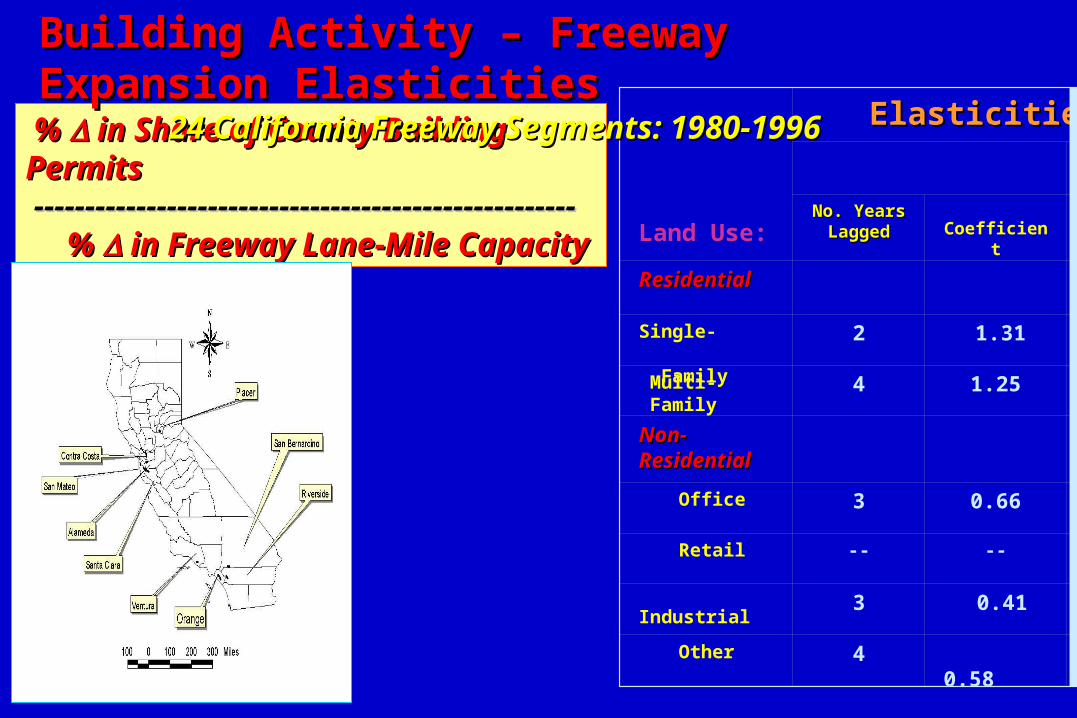

Land Use:

Elasticities Elasticities

No. YearsNo. YearsLaggedLagged

Coefficient

ResidentialResidential

Single- Family

2 1.31

Multi- Family

4 1.25

Non-Non-ResidentialResidential

Office 3 0.66

Retail -- --

Industrial 3 0.41

Other 4 0.58

% % in Share of County in Share of County Building Permits Building Permits ---------------------------------------------------------------------------------------------------------- % % in Freeway Lane-Mile in Freeway Lane-Mile CapacityCapacity

Building Activity – Freeway Expansion Building Activity – Freeway Expansion ElasticitiesElasticities

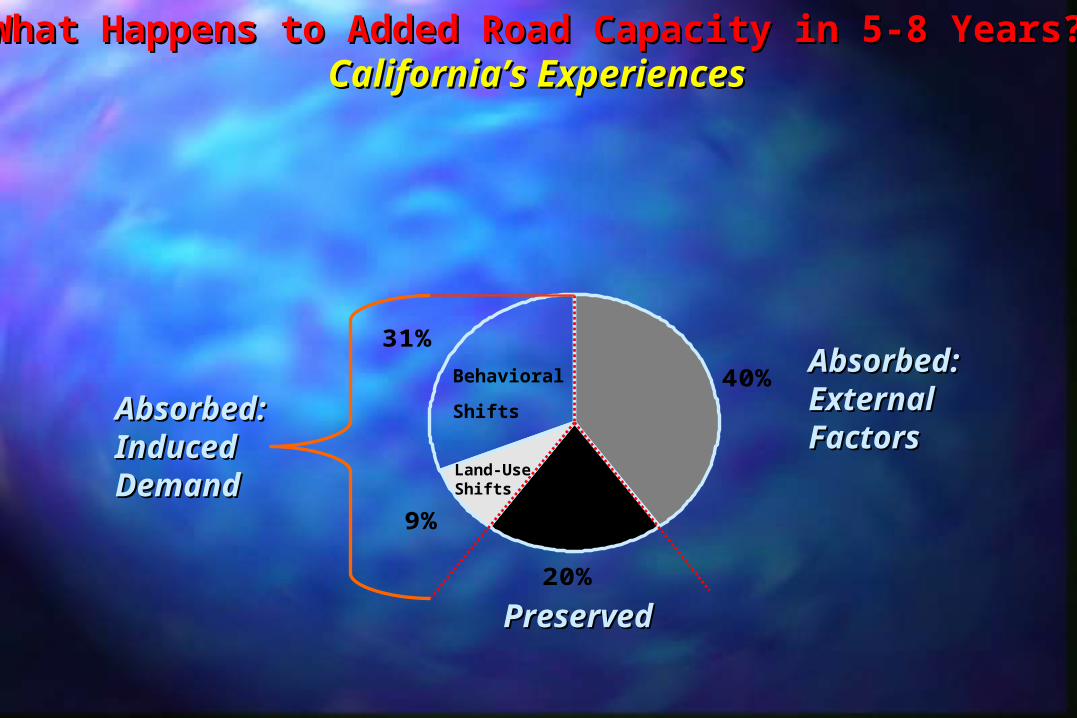

24 California Freeway Segments: 1980-199624 California Freeway Segments: 1980-1996

40%

20%

9%

31%

Land-UseShifts

Behavioral

Shifts Absorbed:Absorbed:Induced Induced DemandDemand

PreservePreservedd

AbsorbeAbsorbed:d:ExternalExternalFactors Factors

What Happens to Added Road Capacity in 5-8 Years?What Happens to Added Road Capacity in 5-8 Years?California’s ExperiencesCalifornia’s Experiences

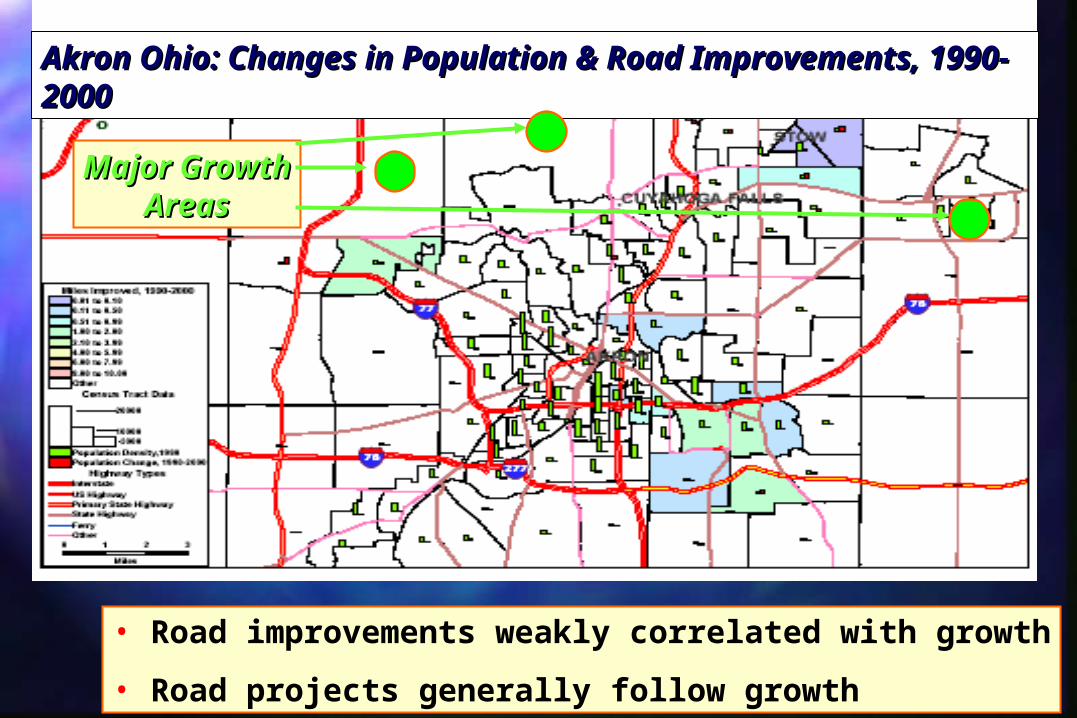

• Road improvements weakly correlated with growth

• Road projects generally follow growth

Akron Ohio: Changes in Population & Road Akron Ohio: Changes in Population & Road Improvements, 1990-2000Improvements, 1990-2000

Major GrowthMajor GrowthAreasAreas

44thth Point Point

4) Given Growth, Proactive Planning is Key to Leveraging “Smart Growth” Outcomes

Transit: San DiegoTransit: San Diego “Tiajuana Corridor”: No Growth, Little

Planning, No Impacts Mission Valley Corridor: Substantial Growth,

Proactivism, Big Impacts

San DiegoSan DiegoRail StationsRail Stations

4 6 .1 %

2 .2 %

3 .0 %

6 .4 %

3 .5 %

0 % 5 % 1 0 % 1 5 % 2 0 % 2 5 % 3 0 % 3 5 % 4 0 % 4 5 % 5 0 %

La nd V a lue P re m ium /Dis c ount, P e rc e nt

T ro lle y : S o u th L in e

T ro lle y : E a s t L in e

T ro lle y : N o rth L in e

T ro lle y : D o w n to w n

C o a s te r

MF HousingMF Housing

38.5%

-4.2%

1.9%

30.4%

-0.5%

-3.9%

-10% -5% 0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

La nd V a lue P re m ium /Discount, P e rce nt

Tro lley: South L ine

Tro lley: East L ine

Tro lley: N orth L ine

Tro lley: D ow ntow n

C oaster

C oaster: D ow ntow n

CommercialCommercial

SAN DIEGOSAN DIEGOTROLLEY & COASTER’s VALUE-ADDEDTROLLEY & COASTER’s VALUE-ADDED

55thth Point Point

5) Finance Connection: Value Capture – Makes Sense in Theory, Hard in Practice

Happens: Happens: Indirectly: Property Tax Intake More directly: Joint Development Most directly: Benefit Assessment

-1 .6%

-6 .0%

3 .4%

1.2%

0.5%

-3 .4%

3 .7%

-3 .5%

6 .1%

-8% -6% -4% -2% 0% 2% 4% 6% 8%

Land Value P re mium/D iscount, P e rce nt

M etro R ed S ubw ay L ine

M etro link Antelope V a lley L ine

M etro link R iverside L ine

M etro link S an B ernard ino L ine

M etro link V entura L in e

M etro LR T B lue L ine

M etro LR T G reen L in e

M etro R ap id V entura B R T L ine

M etro R ap id W ilsh ire -W hittier B R T L ine

Los Angeles: Mixed ExperiencesLos Angeles: Mixed ExperiencesMulti-Family Housing Premium/Discount

Benefit Benefit AssessmentAssessment

9% of funds to retire Red Line Capital

Bonds

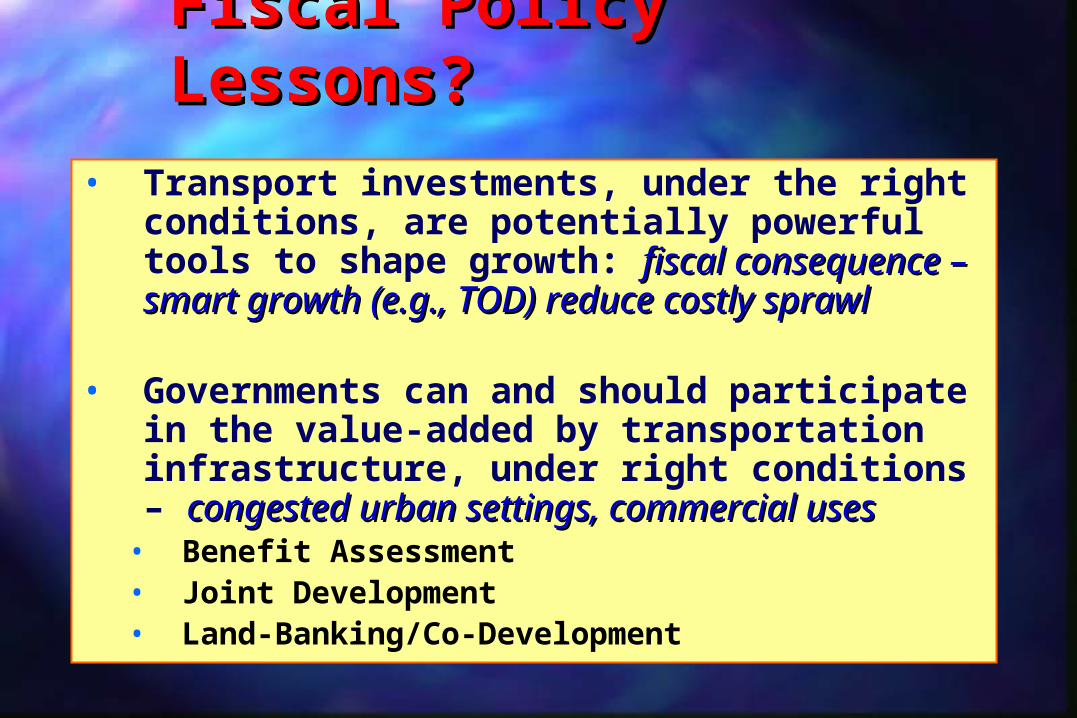

Fiscal Policy Lessons? Fiscal Policy Lessons?

• Transport investments, under the right conditions, are potentially powerful tools to shape growth: fiscal consequence – fiscal consequence – smart growth (e.g., TOD) reduce costly sprawlsmart growth (e.g., TOD) reduce costly sprawl

• Governments can and should participate in the value-added by transportation infrastructure, under right conditions – congested urban settings, commercial usescongested urban settings, commercial uses

• Benefit Assessment• Joint Development• Land-Banking/Co-Development

![robert c.PPT [Read-Only] - · PDF fileRobert Cervero University of California, ... Sears Warehouse ... Pleasant Hill BART 2nd Generation TODGeneration TOD b](https://img.pdfslide.us/doc/110x75/5ab2020f7f8b9a7e1d8d141e/robert-cppt-read-only-cervero-university-of-california-sears-warehouse.jpg)