Embed Size (px)

Citation preview

CHAPTER-1

INTRODUCTION

INTRODUCTION TO FINANCIAL STATEMENTS:

Financial statements are generally prepared on the basis of

recorded facts. The recorded facts are those which can be

expressed only in monetary terms. All the transactions are

recorded in a chronological order throughout the year. Financial

statements are prepared from the records which are based on

historical costs.

The financial statements are summarizes of the items recorded

in the business and these statements are prepared periodically,

generally for the accounting period.

The financial statements are prepared mainly for decision-

making purposes. The information given in the financial

statements is of immense use is making decisions through

analysis and interpretation of financial statements.

OBJECTIVES OF FINANCIAL STATEMENTS :

To provide reliable financial information about economic resources and

obligations of a business firm.

To provide other needed information about changes in such economic

resources and obligations.

To provide reliable information about changes in net resources (resources

less obligations) arising out of business activities.

To provide financial information that assists in estimating the earning

potential of business.

To disclose to the extent possible, other information related to the

financial statement i.e. relevant to the need of the users of these

statements.

INTRODUCTION TO FINANCIAL ANALYSIS :

Analysis is the process of critically examining in detail accounting

information given in the financial statements. For the purpose of analysis,

individuals items are studied, their interrelationships with other elated figures

established, the data is sometimes rearranged to have better understanding of the

information with the help of different techniques or tools for ht purpose.

Analyzing financial statements is a process of evaluating relationship between

component parts of financial statements to obtain a better understanding of

firm’s position and performance.

Financial analysis is the process of identifying the financial strengths and

weaknesses of a firm by properly establishing relationship between the items of

the balance sheet and profit and loss account.

From the definition, it is clear that analysis and interpretation of financial

statement is the methodical classification of the data given in the financial

statement into simple component parts of elements, and evaluation of the

significance of the relationship between the classified component parts of

elements, with a view to provide a full diagnosis of the profitability and

financial statement of an enterprise.

SIGNIFICANCE OF FINANCIAL ANALYSIS:

1. HELPS IN SCREENING:

Financial statements can serve as a preliminary tool on the selection of

investments. It greatly helps the investors in studying 3p’s i.e. prospects,

payment and protection. The prospects of a firm can be judge by looking to both

its presenting and future profitability. The capacity can be judge on the basis of

present and prospective rigidity of the firms. The protection can be judged on

the basis of tangible assets backing, which the firm enjoys.

2. HELPS IN FORECASTING:

It can be used as a forecasting tool for future profitability and financial

soundness of business.

3. HELPS IN DIAGNOSIS:

It helps the management to identifying the factors responsible for creating

managerial, operating and other problems.

INTRODUCTION TO FINANCIAL STATEMENTS ANALYSIS:

Financial statement analysis is a process of evaluations of

the relationship between components parts of a financial

statement to obtain a better understanding of a firm’s position

and performance. In this way, the main objective of financial

statement analysis is to analyse and evaluate the information

contained in financial statements to judge the profitability,

solvency and financial soundness of a firm.

A financial analyst analyses the financial statements with

various tools of analysis before commenting upon the financial

health or weakness of an enterprise. The analysis and

interpretation of financial statements is essential to bring out

the mystery behind the figures in financial statements.

MEANING OF FINANCIAL STATEMENTS ANALYSIS:

The term financial statements analysis refers to" the process of

determining financial strengths and weaknesses of the firm by

establishing relationship between the items of the balance sheet and

profit and loss account".

OBJECTIVES OF FINANCIAL STATEMENTS ANALYSIS:

The basic objective of the analysis statements is to understand the information

contained in financial statements with a view to know the weaknesses and

strengths of the firm and to make a forecast about the future prospects of the

firm and thereby enabling the financial analyst to take different decisions

regarding the operation of the firm.

However, some of the specific objectives of the analysis of financial

statements can be identified as;

To asses the current profitability position and operating efficiency of the

firm and as of different departments.

To find out the relative importance of different components of the

financial position of the firm.

To identify the reasons for change in the profitability position of the firm.

To assess the short as well as long-term liquidity position of the firm

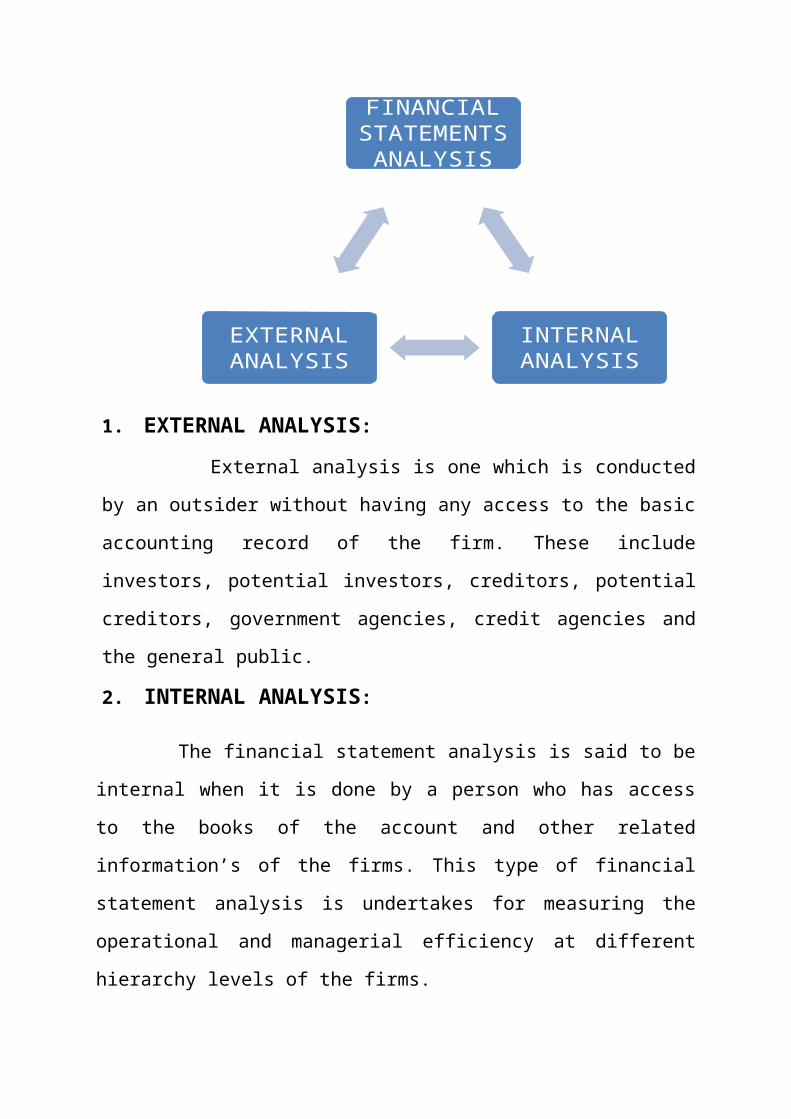

TYPES OF FINANCIAL STATEMENTS ANALYSIS :

1. EXTERNAL ANALYSIS:

External analysis is one which is conducted by an outsider without having

any access to the basic accounting record of the firm. These include investors,

potential investors, creditors, potential creditors, government agencies, credit

agencies and the general public.

2. INTERNAL ANALYSIS:

The financial statement analysis is said to be internal when it is done by a

person who has access to the books of the account and other related

information’s of the firms. This type of financial statement analysis is

undertakes for measuring the operational and managerial efficiency at different

hierarchy levels of the firms.

FINANCIAL STATEMENTS

ANALYSIS

INTERNAL ANALYSIS

EXTERNAL ANALYSIS

CHAPTER-2

RESEARCH DESIGN

STATEMENT OF THE PROBLEM :

Financial statement analysis is very important in financial management;

this requires deep study on the analysis of the available statement and

interpretation. It is very crucial to analyze the performance of a manufacturing

industry.

Analysis of financial performance is one of the major requirements for

planning because owners, management, creditors, prospective investors, and

employees are involved in the decision making process. Government and

financial institutions require it, as they are interested to know the financial

soundness of the company.

Financial statements exhibit the occurrences in a given period of time.

But there are certain important financial matters, which can be known only

through analysis of these financial statements. Thus, it is important to know the

behavior of items in the financial statements. This underlines the importance of

financial statement analysis and the current study is conducted to investigate

into financial statements to evaluate the performance and profitability of

Karnataka Soaps and Detergents Ltd.

OBJECTIVES OF THE STUDY:

Following are the objectives of analyzing the financial statements:

To analyze present and future earning capacity of profitability of

KS&DL,

To understand the short-term and long term solvency of KS&DL for

the benefit of the debenture holders and trade creditors.

To evaluate financial stability of KS&DL.

To study the significance of financial data, and long term liquidity of

its funds.

To evaluate operational efficiency of KS&DL as a whole and of its

various parts or departments.

SCOPE OF THE STUDY :

The scope of the study covers evaluating the financial performance by

analyzing the financial statement of Karnataka Soaps and Detergent Limited

which were collected from the present record and from discussion with the

company’s accountant. The study aims at analyzing the financial statement of

Karnataka Soaps and Detergent Limited over last five years and interpreting

the different ratios and suggesting remedies for better performance

RESEARCH METHODOLOGY

TITLE OF THE STUDY

"A STUDY ON THE ANALYSIS AND INTERPRETATION OF

FINANCIAL STATEMENTS WITH SPECIAL REFRENCE TO

KARNATAKA SOAPS AND DETERGENTS LIMITED”

Research Methodology :

The purpose of methodology is to describe the process involved in research work. This includes the overall research design, data collection method, the field survey and the analysis of data

RESEARCH DESIGN

A research design is a logically and systematic plan prepared for directing a research study. It specifies the objectives of the study, the methodology and the techniques to be adopted for achieving the objectives. It constitutes the blue print for the collection, measurement and analysis of data

It is an outline that specifies the sources and the types of information

relevant to the research question.

It is a blue print specifying the methods to be adopted for gathering and

analysis the data.

It should facilitate in obtaining required information.

It should suit to the availability of resources and time.

TYPE OF STUDY

The research is made in a descriptive way of study. The financial statements

are analyzed through various tools of financial statements analyses. Analytical

study which helps to analyze financial statement of the company.

SOURCES OF DATA

1. Primary data

Primary data can collected through the information within the

organization and through references of the officials of the company.

2. Secondary data

Secondary data is obtained through the use of statistical techniques which

are further used for planning of analysis.

PLAN OF ANALYSIS

The data collected from the secondary sources have to be processed &

interpreted systematically it includes such as:

Interpretation of the study for 5years.

Application of ratio analysis for the period of the study

Identification of the changes in the working capital with the increase or

decrease of the amount in the balance sheet of 5 years.

Calculation of various ratios reflecting the current ratio, quick ratio, cash

ratio, inventory turnover ratio, creditors turnover ratio, average payment

period, working capital ratio etc..

LIMITATION OF THE STUDY

The information is based on data supplied by factory personnel and the data

restricted to KS&DL.

Analysis in the study will be depended on the information provided by the

company.

The study is done only on the basis of financial statement of 5years only.

CHAPTER SCHEME

I. INTRODUCTION: This chapter includes definition of financial

analysis, types of financial analysis, significance of financial analysis.

Introduction, meaning, objectives, types, procedure, methods of

financial statements analysis.

II. RESEARCH DESIGN:

Introduction, meaning, definition of research design.Nature/essential

of a good research design. It also includes Title of the project,

statement of the problem, objective of the study, research technique,

sampling design, methods of data collection, tools of data collection,

plan of analysis, limitations of the study, chapter scheme.

III. COMPANY PROFILE:

This chapter gives us the profile of KS&DL. It provides details

regarding KS&DL, nature of its activities, organizational structure,

functional departments, its vision and mission, business operations,

product profile, market status, competitors, a brief SWOT analysis

and future prospects for the growth of KS&DL.

IV. ANALYSIS AND INTERPRETATION:

This chapter focuses upon the data which is collected to know the

liquidity position, comparative balance sheet and common size

balance sheet. This chapter also shows various ratios like current ratio,

liquidity ratio, turnover ratios and the liquidity position of KS&DL.

V. FINDINGS AND RECOMMENDATIONS:

This chapter of the study includes the findings of the overall study at

KS&DL on basis of data analysis and the conclusion which is online

with objectives of the research.

CHAPTER-3

COMPANY PROFILE

INDUSTRY PROFILE:

Soap is one of the commodities which have become an indispensable part of the life of modern world. Since it is non durable consumer goods, there is a large market for it. The whole soap industry is experiencing changes due to innumerable reasons such as government relations environment and energy problems increase in cost of raw material etc. The changing technology and ever existing desire by the individual and the organization to produce a better product at a more economical rate has also acted as catalyst for the dynamic process of change. More and more soap manufactures are trying to capture a commanding market share by introducing new products. The soap industry in India faces a cut throat competition with mult inat ional companies dominate the market . They are also facing severe threat fromdynamic and enterprising new entrance especially during 1991-92.If we look back into the history of soaps & detergents, mankind knew about soaps nearly 2000 years back i.e. in 70 A.D. when Mr. Elder accidentally discovered the soap, when roasted meat over f lowed on the glow in ashes. This lump l ike product was soap & had foaming & cleansing character. In 1192 A.D. the first commercial batch of soaps was made &marketed by M/s Bristol soap market in London, from there in 1662A.D. the first patent for making soap was taken in London. The world consumption of soap in 1884A.D. was said to be 2 lakh tonnes p.a.

HISTORY OF THE SOAP:

Soap manufacturing was started in North America. Some American companies with well known names were started 200 years ago. During middle age soap was made at various places in Italy, France, England & other countries. France became famous & many small factories were established there.

In India the first soap industry was established by North West soap company in1897 at Meerut following the swadeshi movement. From 1905 on wards few more factories were setup. They are,

Mysore soap factory at Bangalore Godrej soap at Bombay Bengal chemicals Tata oil mills 1930 lever brothers comp

THE INDIAN SOAP INDUSTRY SCENARIO:

The Indian soap industry has long been dominated by hand full of companies such as:

1. Hindustan levers limited2. Tata oil mills (taken over by HLL)3. Godrej soaps private limited.

The Indian soap industry continued to flourish very well until 1967-68, but began to stagnate & soon it started to recover & experienced a short upswing in 1974. This increase in demand can be attributed due to;1 . G r o w t h o f p o p u l a t i o n .2. Income & consumption increase.3 . I n c r e a s e i n u r b a n i z a t i o n .4. Growth in degree of personal hygiene.

PRESENT STATUS:

Market scenario:

India is the ideal market for cleaning products. Hindustan liver, which towers over the cleaning business, sells in all over the cleaning business but the tiniest of Indian settlements. The 7.4 lakhs tons per annum soap market in India in crawling along at 4%The hope lies in raising Rupee worth, the potential for

which is high because the Indian soap market is pseudo in nature & it is amazingly complex being segmented not only on the basis of price benefits, but even a range of emotions within that outlining framework.

PROBLEMS OF SOAP INDUSTRY:

Soap industry faces some problems in case of raw materials.

The major ingredients are soap ash l inear alkyl , benzene& sodium. Tripoli phosphate poses number of serious problems in terms of availability. The demand supply gap for vegetable oil is 1.5 to 2 lakh tons & is met through imports. In recent times, caustic soda and soap ashes in the cheaper varieties of soaps are quite high.

COMPANY PROFILE

THE FOUNDERS OF MYSORE SANDAL SOAP:

Sir M. Visvesvaraya Nalwadi krishnaraja Wodeyar

Sri S. G. Shastri

ABOUT KARNATAKA SOAPS AND DETERGENTS LIMITED:

Karnataka soaps and detergents limited [KS&DL] – a Government of

Karnataka undertaking is involved in the extraction of sandalwood oil and in the

manufacture of soaps, Detergents, Incense sticks and sandal Talc, having over 9

decades of experience in this field. KS&DL today is one of the largest

producers of sandalwood oil and sandal soap in the world, with a turnover of

Rs.125crs. The sandal soaps of KS&DL have a definite niche in the soap market

with the oldest known perfumery material sandalwood as its main ingredient.

Sandal Soaps of KS&DL are probably the only soap in the world with pure

natural sandalwood oil.

KS&DL is the true inheritor of India’s golden sandalwood legacy, the

sandalwood oil which is also known as Liquid Gold. Sandal wood oil is

recommended in ancient ayurvedic texts for skin care, has excellent antiseptic

properties and soothes prickly heat and other skin rashes too. This is the reason

why soaps made out of sandalwood oil are used all over the world for

nourishing and softening the skin. It was the availability of sandal wood oil,

which became a reason to set up a soap factory.

“Government soap Factory” in Bangalore was established by the

Maharaja of Mysore Nalwadi Krishna raja Wodeyar and Diwan Sir M.

Visvesvaraya during the year 1916. The soap making process was perfected

under the stewardship of eminent scientist Shri S. G. Shastri. The sandalwood

Oil Division in Mysore was established during the year 1916 and Sandalwood

Oil Division at Shimoga was established during the year 1944.

RENAMING:

On 1st October 1980, the Government Soap Factory was renamed as

“Karnataka Soaps and Detergent Limited” by integrating sandal oil factories at

Mysore, Shimoga and Bangalore. The Company was registered as a public

limited company. Today Company produces varieties of products in the toilet

soaps, detergent, agarbathies and Cosmetics.

TRADEMAR OF KS & DL : -

THE “ SHARABHA ”

The carving on the cover is the Sharabha, the trademark of KS & DL.

The Sharabha is a mythological creation from the “puranas” which has a

body of a lion and head of elephant, which embodies the combined virtues of

wisdom and strength. It is adopted as an official emblem of KS& DL to

symbolize the philosophy of the company.The Sharabha thus symbolized a

power that removes imperfections and impurities.

SLOGAN :-

“NATURAL PRODUCTS WITH EXOTIC FRAGRANCES”

VISION STATEMENT :

Keeping pace with globalization, global trends and the state’s policy for

technology in every aspect of governance.

Ensuring global presence of Mysore Sandal products while leveraging its

unique strengths to take advantage of the current technology scenario by

intelligent and selective diversification.

Further, ensure Karnataka’s pre-eminent status as a proponent and

provider of technology services to the world, nation, other states public

and private sectors.

Making all out efforts to achieve reasonable profits.

Most importantly to earn the invaluable foreign exchange, both to the

state and to the country.

MISSION STATEMENT :-

To serve the National economy.

To attain self-reliance.

To promote purity & quality products

To maintain the Brand loyalty of its customers.

To build upon the reputation of Mysore sandal soap based on pure sandal

oil.

OBJECTIVES OF KS & DL: -

To attain self – reliance.

To promote and uphold its image as symbol of traditional products

To promote purity and quality products and thus enhance age old – charm

of Sandalwood Oil.

To build upon the reputation of Mysore Sandal soap based on pure sandal

oil.

To maintain the brand loyalty of its customer.

To supply the products mentioned above at most reasonable and

competitive rate.

POLICY OF KS&DL:-

Seek purchase of goods and services from environment responsible

suppliers.

Communicate its environment policy and best practices to all its

employees’ implications.

Set targets and monitor progress through internal and external audits.

Strive to design and develop products, which have friendly environmental

impact during manufacturing.

. Reuse and recycle materials wherever possible and minimize energy

consumption and waste.

COMPETITORS OF KS&DL PRODUCT AND SERVICES:-

KS&DL is facing cut-throat competition in national and international market.

Some of its main competitors are:-

M/S. Hindustan Unilever Ltd

M/S. Godrej Soaps Private Ltd

M/S. Proctor& Gamble

M/S. Wipro

M/S. Nirma Soaps Private Ltd

M/S. Jyothi Laboratories

DEPARTMENTS OF KS&DL:

Human Resources Department

Production Department

Marketing Department

Finance\Accounts Department

Research & Development Department

Stores Department

Welfare Department

Maintenance Department

Materials Department

Management Information System Department

AN ISO-9001 AND ISO-14001 COMPANY :

KS & DL with a tradition of excellence of over eight decades is

committed to customer delight, through total quality management and

continuous improvement through the involvement of all employees. KS&DL

has got ISO 9002 certificate.The Company got itself upgraded to ISO-9001-

2004, Quality Systems in the year 2004-05

The company is located in the heart of the Bangalore city. The management

of the company took a decision to get the ISO-14001 and become model to

other public sector for the techniques used and also to other Government units

to spread the message of maintenance of environment.

ISO-14001 and ISO-9001 will facilitate to improve the corporate brands

in the global market and it will help the company to improve the profits, year

after year on long-term basis. The environment management system adopted in

the company through this motive as follows:

Conservation of energy

Conservation of Surrounding

Conservation of resources

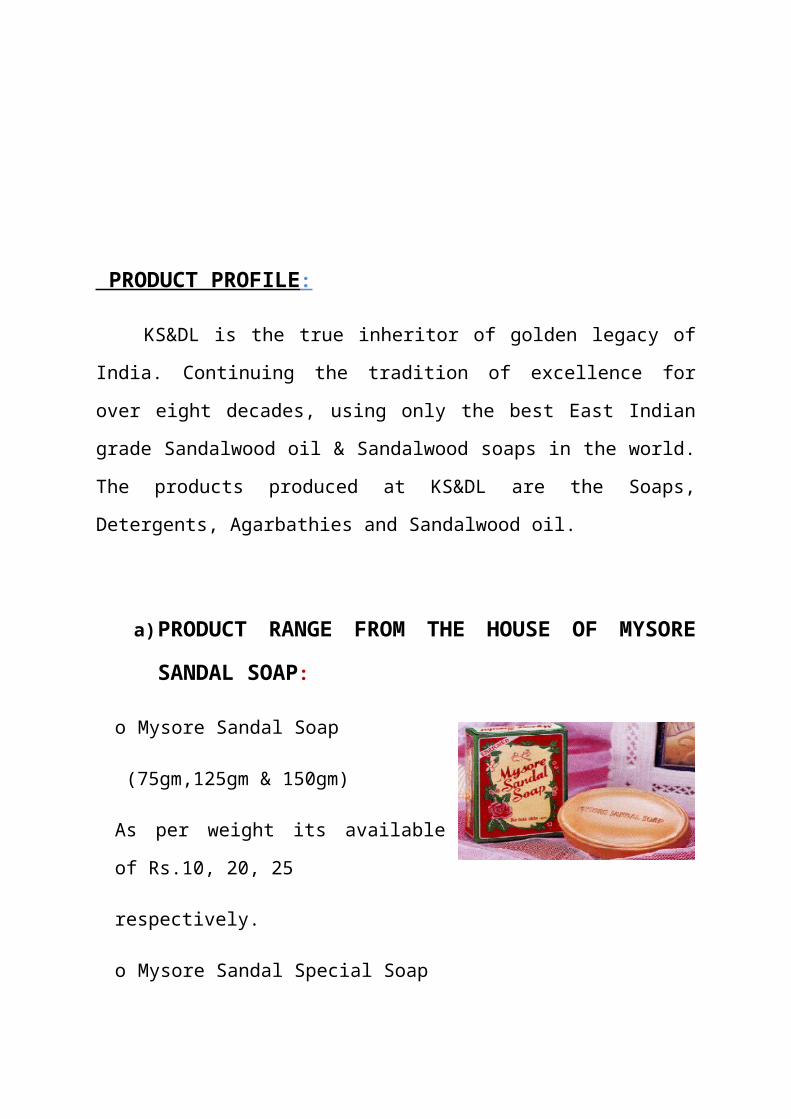

PRODUCT PROFILE :

KS&DL is the true inheritor of golden legacy of India. Continuing the

tradition of excellence for over eight decades, using only the best East Indian

grade Sandalwood oil & Sandalwood soaps in the world. The products produced

at KS&DL are the Soaps, Detergents, Agarbathies and Sandalwood oil.

a)PRODUCT RANGE FROM THE HOUSE OF MYSORE

SANDAL SOAP:

o Mysore Sandal Soap

(75gm,125gm & 150gm)

As per weight its available of Rs.10, 20, 25

respectively.

o Mysore Sandal Special Soap

Available mostly in 75 grms pack and having sandalwood and almond oil

as ingrediants.

o Mysore Sandal Baby Soap

This soap is mainly for babies made of ingredients suitable for babies soft

and sensitive skin.

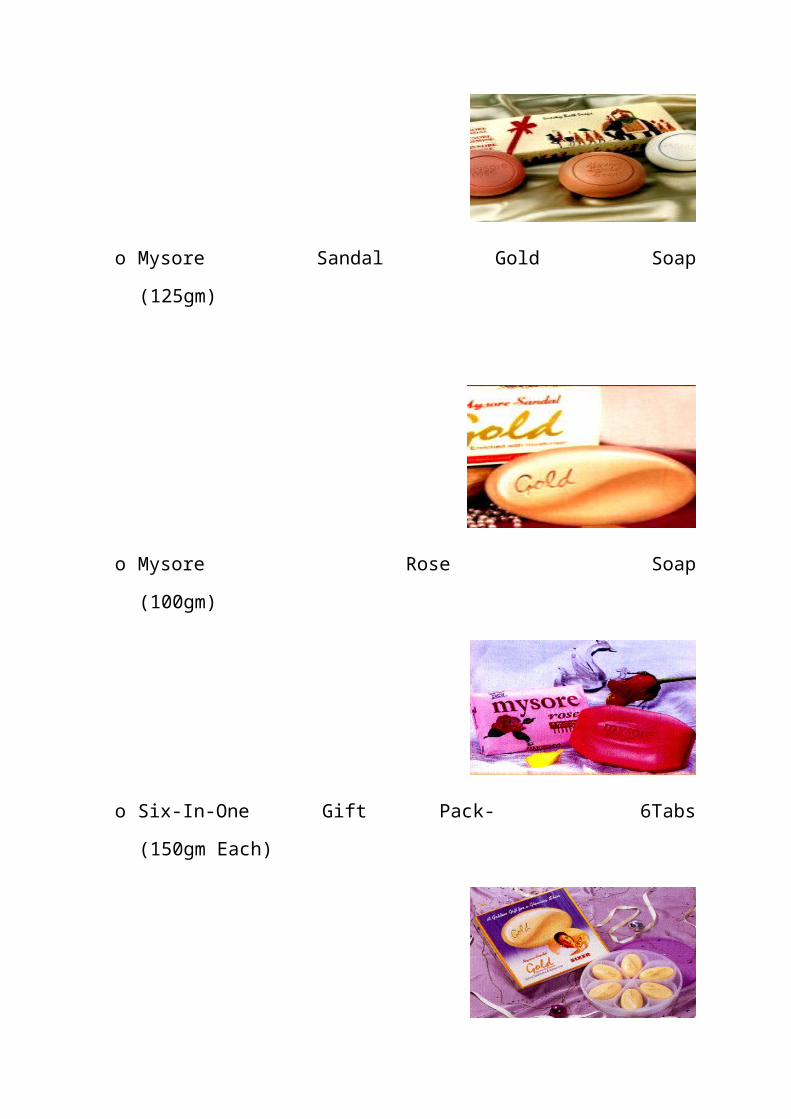

o Three-In-One Gift Pack –(SJR) 3Tabs (150gm Each)

o Mysore Sandal Gold Soap (125gm)

o Mysore Rose Soap (100gm)

o Six-In-One Gift Pack- 6Tabs (150gm Each)

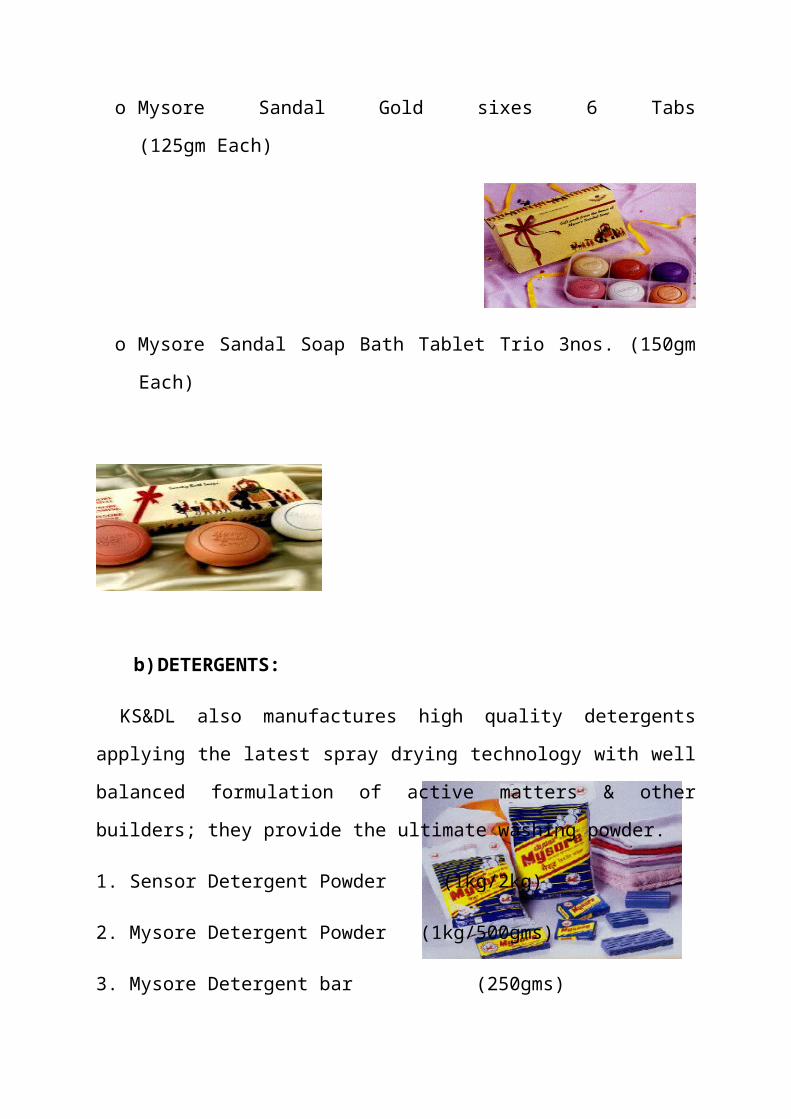

o Mysore Sandal Gold sixes 6 Tabs (125gm Each)

o Mysore Sandal Soap Bath Tablet Trio 3nos. (150gm Each)

b) DETERGENTS:

KS&DL also manufactures high quality detergents applying the latest spray

drying technology with well balanced formulation of active matters & other

builders; they provide the ultimate washing powder.

1. Sensor Detergent Powder (1kg/2kg)

2. Mysore Detergent Powder (1kg/500gms)

3. Mysore Detergent bar (250gms)

4. Mysore Detergent Cake (125gms/250gms)

c) AGARBATHIS:

1. Mysore Sandal premium

2. Mysore Rose

3. Suprabath

4. Parijata

5. Venkateshwar

6. Ayyappa

7. Chandhana

8. Mysore sandal

9. Nagachampa

10.sMysore Jasmine

11.Bodhisattva

12.Durga

13.Alif Laila

d) SANDALWOOD OIL:

In 5ml, 10ml,20ml, 100ml,500ml,2kg,5kg,20kg,and 25kg packing.

e) POWDERS:

1. Mysore Sandal Talk: Cooling & Healing, Fragrant freshness, Net. Wt

20gm, 60gm, 300gm and 1kg.

2. Mysore Sandal Baby Powder: Tender loving care for baby…& Mummy.

Net wt 100-400gms.

EXPORTS FROM KS&DL:

1. Middle East Countries.

2. Asian Countries.

3. American Countries.

4. European Countries.

5. Australia and New Zealand.

6. African countries.

PLANTS SITUATION:

Plants at Bangalore

Soaps, Detergents,Fatty Acid,

Plants at Mysore

Sandalwood oil,Agarbathies

Plants at Shimoga

OWNERSHIP PATTERN:

“Wholly owned by Government of Karnataka”.

PRESENT STATUS:

1. The company has entered into shampoo, dish wash, detergent bar & room

refresher.

2. The company is striving to develop new perfumes for soaps detergents,

agarbathies & shampoo.

3. The company wants to improve the existing products in terms of quality.

ACHIEVEMENTS AND AWARDS OF KARNATAKA SOAPS

AND DETERGENTS LIMITED :

Government of Karnataka

Dept of Industries and commerce

State Export Promotion Advisory Board. “EXPORT AWARD” 1974-75

Geographical Indication GI-2005

ISO 9001-2000 in the year 1999

ISO 14001-2004 in the year 2000

FUTURE GROWTH AND PROSPECTUS :

Introduction of anti-bacteria, herbal transparent soap, made out of 33

essential oil based Timely introduction and implementation of market

driven decisions.

Improvement in existing products Mysore Sandal classic improved

moisturizers & skin conditions.

Introduction of sandalwood powder in 50gms, 100gms to meet the

growing demand for religious purpose.

Introduction of new higher powered detergent powder for institutional

sales in bulk packaging.

To attain market leadership.

Introduction of new trade schemes to increase sales.

Aggressive advertisement and publicity as part of sales promotion.

Reduction in distribution expenses.

Cost-reduction in all areas.

BANKERS:

“KARNATAKA SOAPS AND DETERGENTS LIMITED” being a

huge organization, should possess better banking facilitates to meet the timely

requirements of capital of the company & to fulfill the financial obligations of

supplies, customers & other personnel having relationship with the company.

The Bankers of the company are:

STATE BANK OF MYSORE

CANARA BANK

VIJAYA BANK

SYNDICATE BANK

ORGANISATION CHART OF FINANCE FUNCTION :

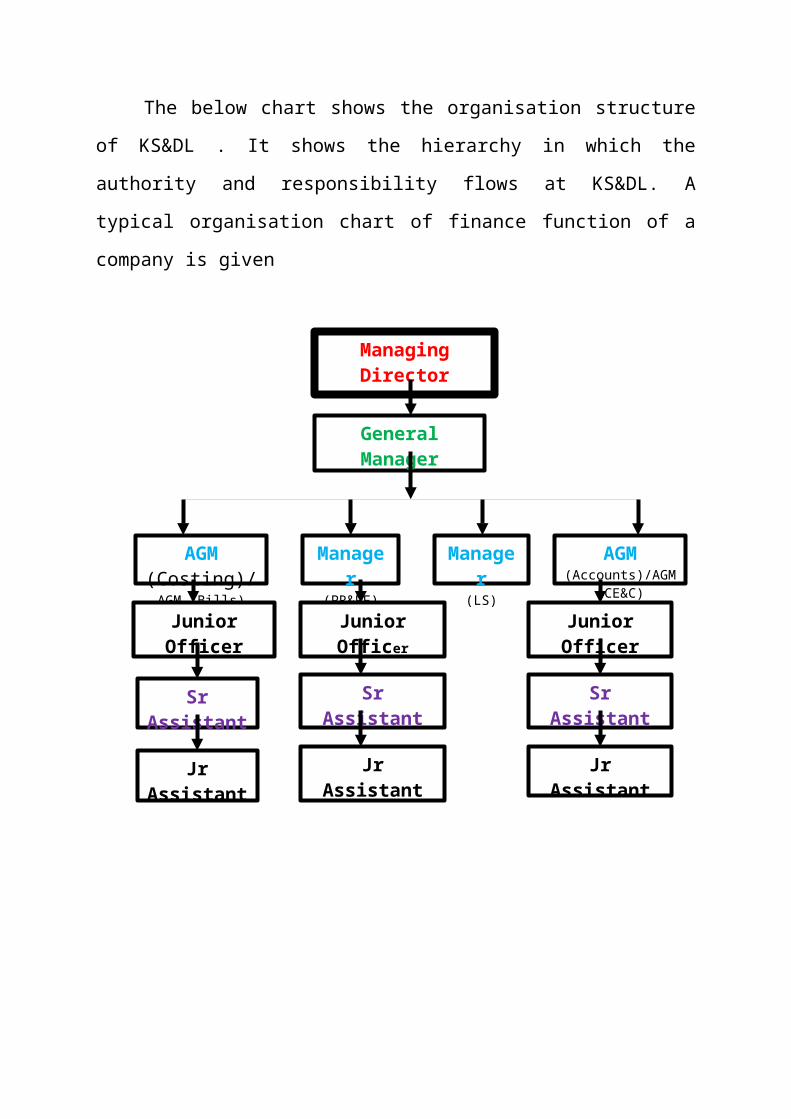

The below chart shows the organisation structure of KS&DL . It shows

the hierarchy in which the authority and responsibility flows at KS&DL. A

typical organisation chart of finance function of a company is given

Managing Director

General Manager

AGM (Costing)/

AGM (Bills)

Manager(PR&PF)

Manager(LS)

AGM (Accounts)/AGM

(CE&C)

Junior Officer

Sr Assistant

Jr Assistant

Junior Officer

Sr Assistant

Jr Assistant

Junior Officer

Sr Assistant

Jr Assistant

LEVELS OF ORGANISATION :

The organization of KS&DL consists of 4 levels, they are

TOP LEVEL consisting of BOD’s and M.D

SECOND LEVEL consisting of Directors of Finance and Special officers

THIRD LEVEL consisting of senior managers, deputy managers and

officers.

FOURTH LEVEL consisting of clerks, Assistants and Attendees.

SWOT ANALYSIS:

1. STRENGTHS :

The Mysore sandal soap contains pure sandal and almond oil.

Certified by ISO.

World’s largest production of sandalwood oil.

Brand name from decades in soap market.

It has very good dealership network in south which ensures that the

products reach every customer.

Diversified product range helps the company to maintain stability.

2. WEAKNESSESS:

Distribution network is weak in north and east.

Absence of television advertisement.

High oriented cost due to excessive labour force.

Neglecting freshness aspect.

Low turnover resulting in low profit.

3. OPPORTUNITIES :

Traditional benefits that sandal is good for skin.

Skin care is just gaining importance among consumers

As a soap attribute.

Government support and large production capacity.

Advantages of being in the industry for a long time.

Existence of vast market and huge demand.

4. THREATS :

There are other competitors such as Rexona, Moti, Santoor etc

There is a need for renovation of plant and machinery.

Government policy may reduce growth potential.

Other sandal soaps in the market.

Entry of new multinational in soap business.

CHAPTER-4

DATA ANALYSIS AND INTERPRETATION

DATA ANALYSIS AND INTERPRETATION

MEANING OF ANALYSIS:

Analysis is the process by which, the whole body of gathered data,

facts, figures and ideas, is converted into meaningful and usable

information.

MEANING OF INTERPRETATION:

Interpretation refers to the task of drawing inferences from the

collected facts after analytical and/or experimental study. In short, it is a

search for broader meaning of research findings.

MEANING OF ANALYSIS AND INTERPRETATION:

In the words of Kennedy and Memullar, "The analysis and

interpretation of financial statements are an attempt to determine the

significance and meaning of the financial statements data so, that a forecast

may be made of the prospects for future earnings"

TECHNIQUES/TOOLS OF ANALYSIS AND INTERPETATION :

1. COMPARITIVE FINANCIAL STATEMENTS

2. COMMON MEASUREMENT STATEMENTS

3. TREND PERCENTAGE ANALYSIS

4. FUNDS FLOW STATEMENTS

5. CASH FLOW STATEMENTS

6. NET WORKING CAPITAL ANALYSIS

7. RATIO ANALYSIS

Among the various above techniques two tools have been selected in

order to analyze the financial statement of KS&DL , the tools used are:

1. COMPARATIVE FINANCIAL STATEMENTS

2. RATIO ANALYSIS

1. COMPARATIVE FINANCIAL STATEMENTS:

In comparative financial statements two or more balance sheets and or the

income statement of a firm are presented simultaneously in columnar form. The

financial data for two or more years are placed and presented

in adjacent columns and thereby the financial data is provided a times

perspective in order to facilitate periodic comparison. In comparative financial

statements, the balance sheet and the income statements for a number of years

are presented in condensed form for year comparison and to exhibit the

magnitude and direction of changes.

The comparative financial statements may be prepared to show;

The absolute amount of different items in monetary forms.

The amount of periodic changes in monetary terms.

The percentage of periodic changes to reveal the proportionate changes.

The comparative financial statement can be prepared for both balance

sheet and the income statement.

The analysts are able to draw useful conclusions when figures are given

in a comparative position.

The figures of sales for a quarter or half year or one year may tell only the

present position of sales efforts.

COMPARATIVE BALANCE SHEET:

The comparative balance sheet analysis is the study of the trend of the

same items, group of items and computed items in two or more balance sheets

of the same business enterprise on different dates. The changes in periodic

balance sheet items reflect the conduct of a business. The changes can be

observed by comparison of the balance sheet at the beginning of the year and at

the end of the year.

These changes will help in forming an opinion about the progress of an

enterprise. The comparative balance sheet has two columns for the data of

columns for the data of original balance sheets. A third column is used to show

increase in figures. The fourth and last column may be added for showing

percentages of increases or decreases.

This statement prepared on two or more different dates can be used for

comparing sources of funds under that secured loans, unsecured loans and

reserves & surplus.

These statements also used to compare fixed and current assets, liabilities

& provision and to find out increase/decrease in these items.

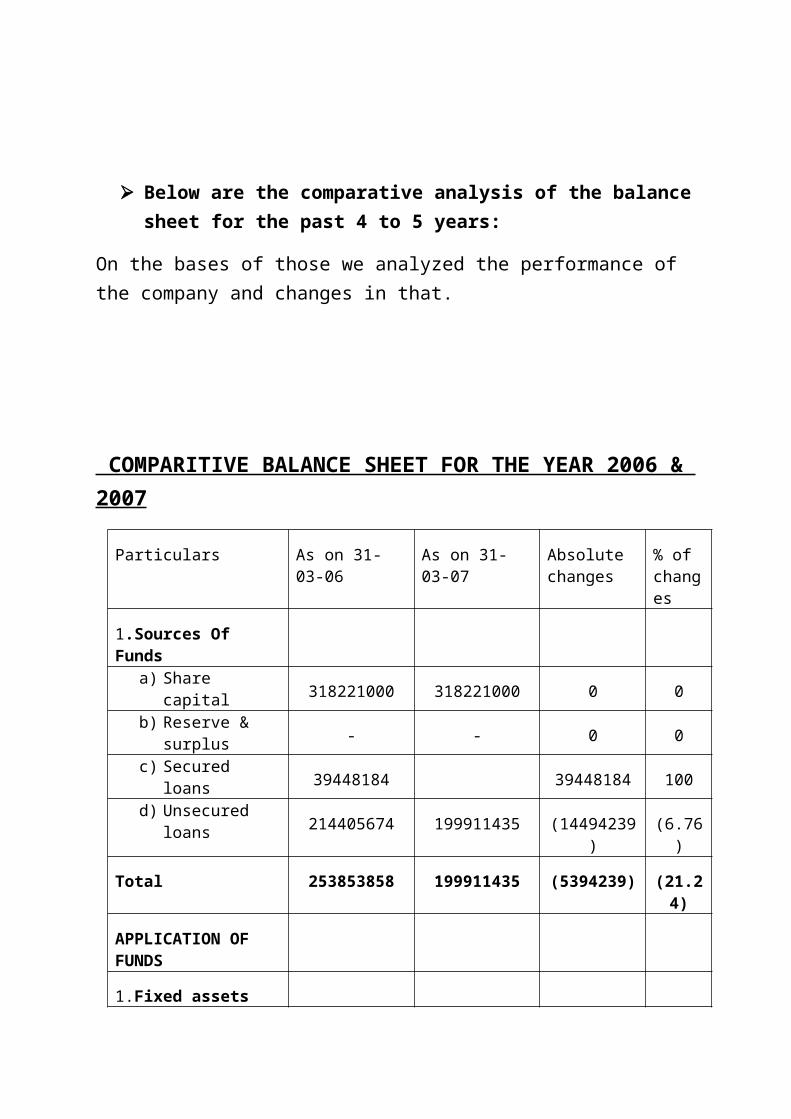

Below are the comparative analysis of the balance sheet for the past 4 to 5 years:

On the bases of those we analyzed the performance of the company and changes in that.

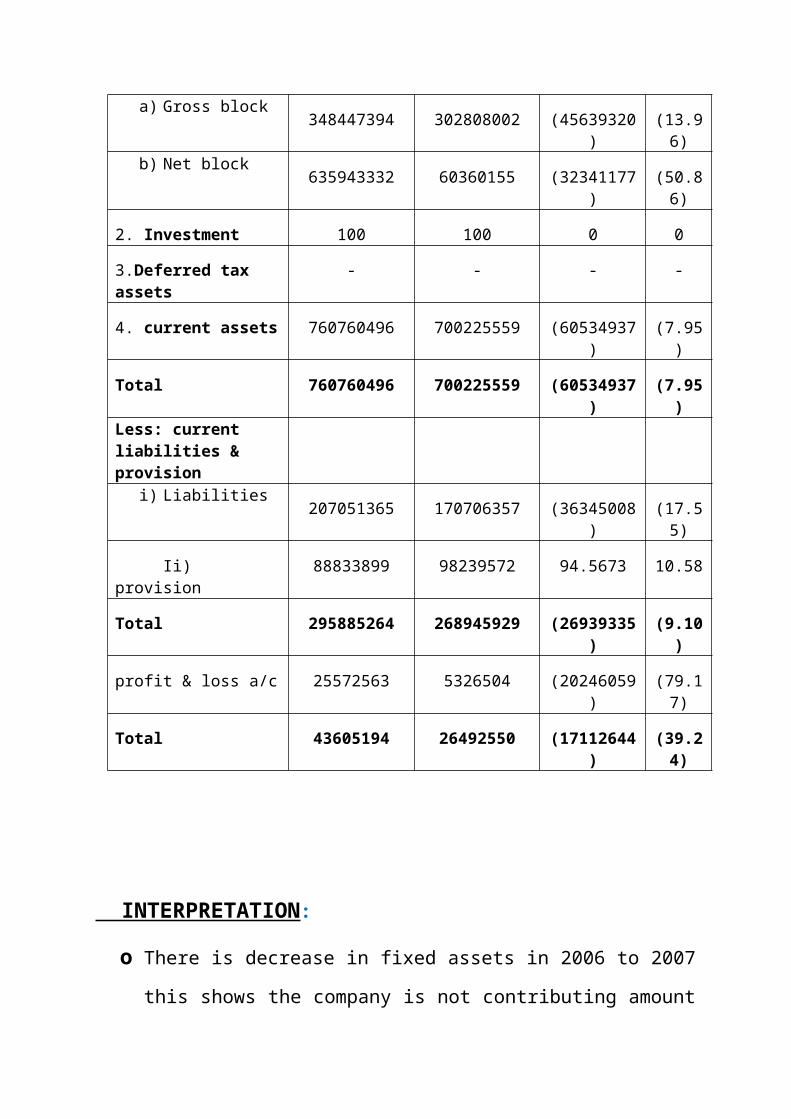

COMPARITIVE BALANCE SHEET FOR THE YEAR 2006 & 2007

Particulars As on 31-03-06 As on 31-03-07 Absolute changes

% of changes

1.Sources Of Fundsa) Share capital

318221000 318221000 0 0b) Reserve & surplus

- - 0 0c) Secured loans

39448184 39448184 100d) Unsecured loans

214405674 199911435 (14494239) (6.76)

Total 253853858 199911435 (5394239) (21.24)

APPLICATION OF FUNDS

1.Fixed assetsa) Gross block

348447394 302808002 (45639320) (13.96)b) Net block

635943332 60360155 (32341177) (50.86)

2. Investment 100 100 0 0

3.Deferred tax assets - - - -

4. current assets 760760496 700225559 (60534937) (7.95)

Total 760760496 700225559 (60534937) (7.95)Less: current liabilities & provision

i) Liabilities207051365 170706357 (36345008) (17.55)

Ii) provision 88833899 98239572 94.5673 10.58

Total 295885264 268945929 (26939335) (9.10)

profit & loss a/c 25572563 5326504 (20246059) (79.17)

Total 43605194 26492550 (17112644) (39.24)

INTERPRETATION:

o There is decrease in fixed assets in 2006 to 2007 this shows the company

is not contributing amount for fixed assets out of profit and the

company’s liquidity position is not good when compare to 2006 as the

company is concentrating on earning profit.

The decreased %age of fixed assets is 13.96 and 50.86 in gross and net

block respectively.

o In the sources of funds secured and unsecured loans are decreasing in the

year 2007 as compared to 2006 which is a good sign for the company.

Secured loans are decreasing to zero and unsecured loans are decreased

by 6.76%.

Share capital of the firm remains constant.

There are no reserve and surplus with the firm in both the years i.e 2006

& 2007.

o There is a decrease in the current assets from 2006 to 2007 with a percent

of 7.95 which shows a loss to the company.

o As seen in current liabilities companies position is good as they are

decreasing in the year 2007 as compared to 2006 with a percentage of

changes 17.55, which is again good for the company.

o In the profit and loss account, in 2006 company had Rs.25572563 of

profit which become Rs.5326504 in the year 2007 i.e 79.17% of change .

Overall company`s performance is satisfactory but company needs to

give attention to some of its major areas like current assets and fixed

assets as there is a decrease in current and fixed assets with a percentage

change of 13.96 % and 50.86% respectively. There

is a decrease in secured and unsecured loans with a percentage change of

100% and 6.76% respectively which is on the benefit side of the company

.

COMPARITIVE BALANCE SHEET FOR THE YEAR 2007 & 2008

Particulars As on 31-03-07 As on 31-03-08 Absolute changes

% of changes

1.Sources Of Fundse) Share capital

318221000 318221000 - -f) Reserve &

surplus - 15070293 15070293 100

g) Secured loans16629120 16629120 0

h) Unsecured loans 199911435 129995436 (6691599) (34.97)

Total 199911435 479915849 53286879 (26.66)

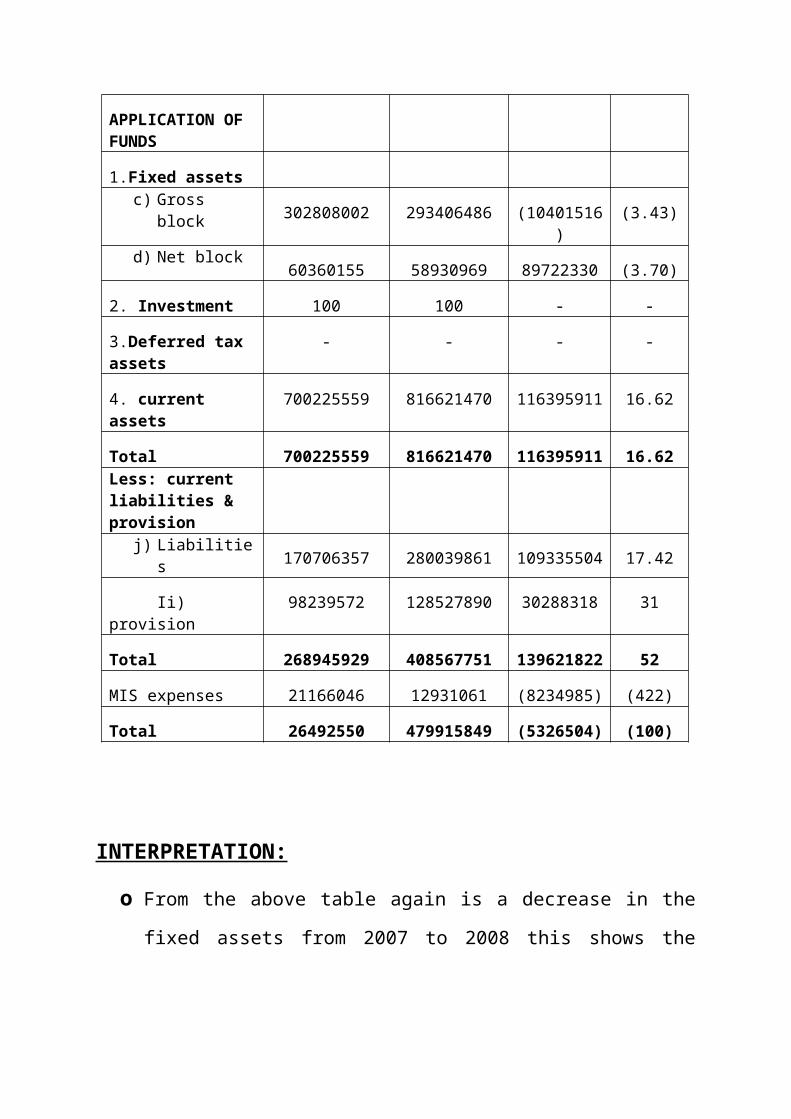

APPLICATION OF FUNDS

1.Fixed assetsc) Gross block

302808002 293406486 (10401516) (3.43)d) Net block

60360155 58930969 89722330 (3.70)

2. Investment 100 100 - -

3.Deferred tax assets - - - -

4. current assets 700225559 816621470 116395911 16.62

Total 700225559 816621470 116395911 16.62Less: current liabilities & provision

j) Liabilities170706357 280039861 109335504 17.42

Ii) provision 98239572 128527890 30288318 31

Total 268945929 408567751 139621822 52

MIS expenses 21166046 12931061 (8234985) (422)

Total 26492550 479915849 (5326504) (100)

INTERPRETATION:

o From the above table again is a decrease in the fixed assets from 2007 to

2008 this shows the company is not contributing amount for fixed assets

out of profit.

The decreased %age of fixed assets is 3.43 and 3.70 in gross and net

block respectively.

o In the sources of funds secured and unsecured loans are increasing in the

year 2008 as compared to 2007 which is a not a good sign for the

company.

Secured loans are increased from zero to Rs.16629120 and unsecured

loans are increased by 34.97%.

Reserve and surplus are also increased by 100% from 2007 to 2008.

Share capital of the firm remains constant.

o There is a increase in the current assets from 2007 to 2008 with a percent

of 16.62 which shows that the company`s liquidation position is

becoming good.

o As seen in current liabilities companies position is not much better as

they are increasing in the year 2008 as compared to 2007 with a

percentage of changes 17.42, which is again not good for the company.

Overall the company`s performance is satisfactory as compared to the

performance of 2007 as there is a decrease in unsecured loans but

increase in secured loans with a percentage change of (34.97)% and 0%

respectively. There is an increase in the current assets but decrease in

fixed assets with a percentage change of 16.62% and (3.43) which is good

on the side of current assets but not good in reference of fixed assets.

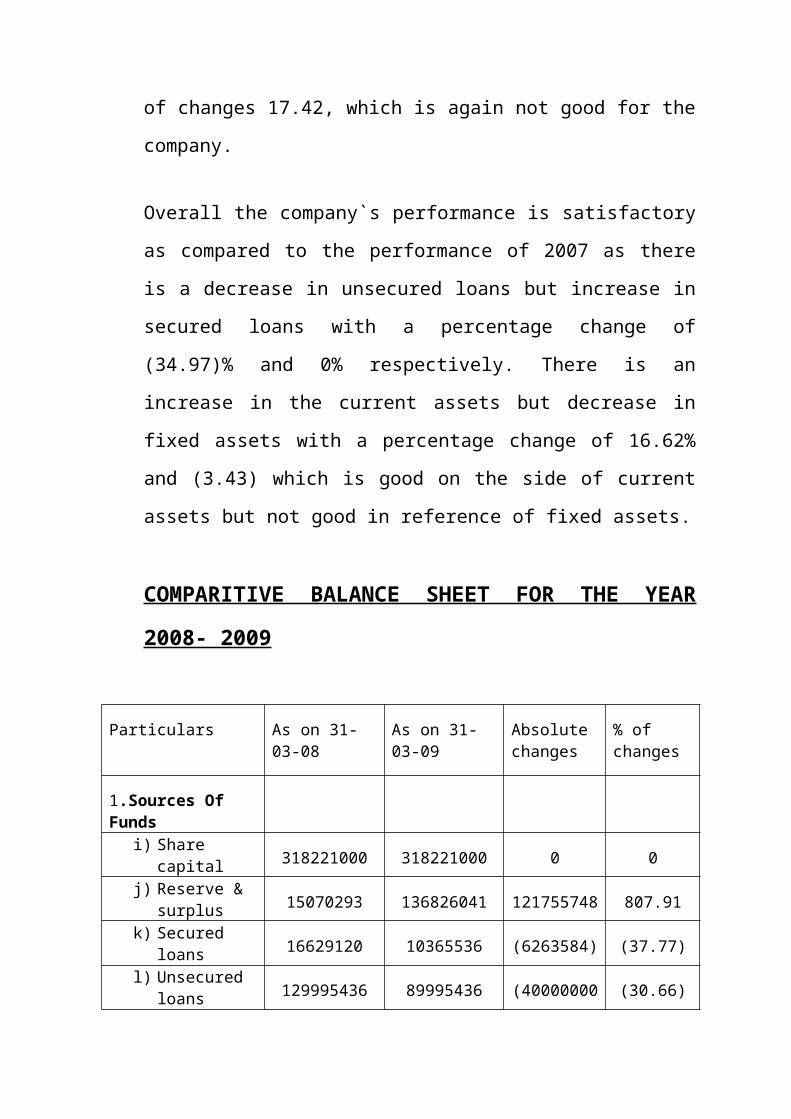

COMPARITIVE BALANCE SHEET FOR THE YEAR

2008- 2009

Particulars As on 31-03-08 As on 31-03-09 Absolute changes

% of changes

1.Sources Of Fundsi) Share capital

318221000 318221000 0 0j) Reserve &

surplus 15070293 136826041 121755748 807.91

k) Secured loans16629120 10365536 (6263584) (37.77)

l) Unsecured loans 129995436 89995436 (40000000) (30.66)

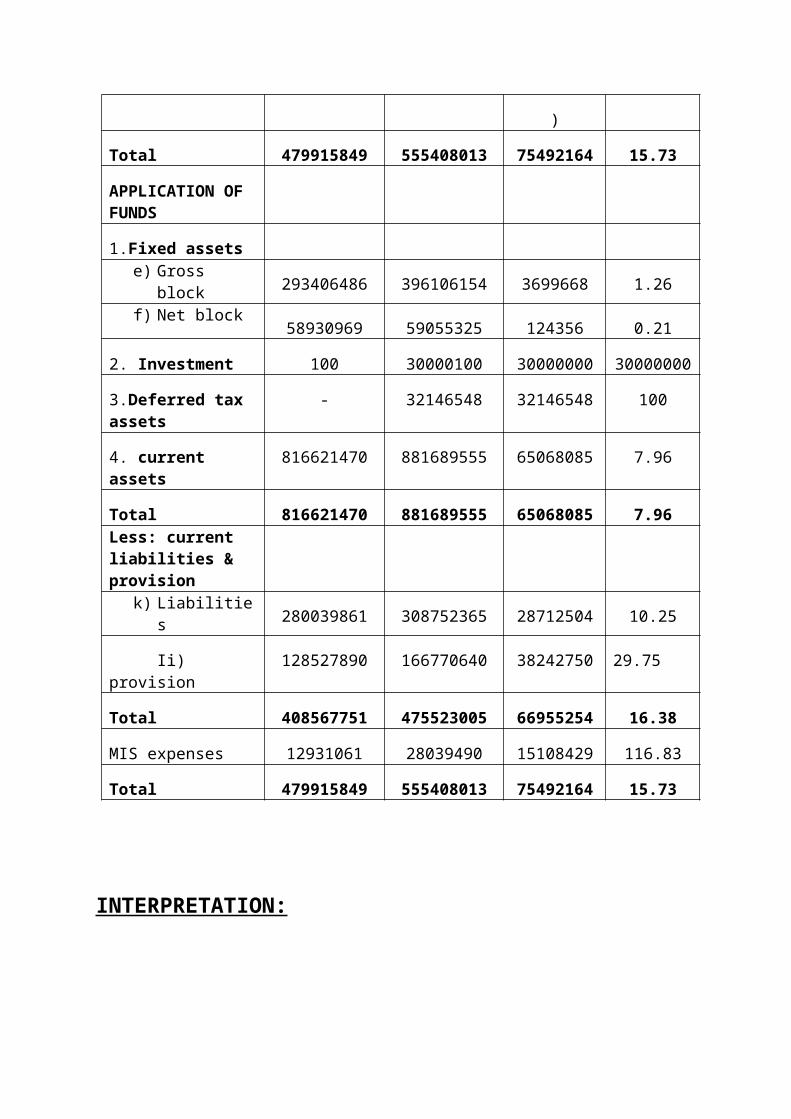

Total 479915849 555408013 75492164 15.73

APPLICATION OF FUNDS

1.Fixed assetse) Gross block

293406486 396106154 3699668 1.26f) Net block

58930969 59055325 124356 0.21

2. Investment 100 30000100 30000000 30000000

3.Deferred tax assets - 32146548 32146548 100

4. current assets 816621470 881689555 65068085 7.96

Total 816621470 881689555 65068085 7.96Less: current liabilities & provision

k) Liabilities280039861 308752365 28712504 10.25

Ii) provision 128527890 166770640 38242750 29.75

Total 408567751 475523005 66955254 16.38

MIS expenses 12931061 28039490 15108429 116.83

Total 479915849 555408013 75492164 15.73

INTERPRETATION:

o In the sources of funds secured and unsecured loans are decreasing in the

year 2009 as compared to 2008 which is a good sign for the company.

Secured loans are decreasing by 37.77 and unsecured loans are decreased

by 30.66%.

Share capital of the firm remains constant.

Reserve and surplus are increased with an absolute change of

Rs.121755748 the firm in the year 2009.

o The above table is showing a increase in the fixed assets from 2008 to

2009 this shows the company is contributing amount for fixed assets out

of profit.

The increased %age of fixed assets is 1.26 and 0.21 in gross and net block

respectively.

o From the above table, in the year 2009 the position of

current assets is 88.16 which was 81.66 in 2008 and

current liabilities is 30.87 and 28.00 in the year 2009 and

2008 respectively. All this is showing good results for the

firm in accordance of current assets but not good in

current liabilities position.

o In 2009 company`s MIS expenses are increasing with a

absolute changes of Rs. 15108429 and percent change of

116.83, it means company should control its undesired

expenses.

Overall the performance of KS&DL is pretty satisfactory,

when compare to the year 2008.It indicate that, in

both the year 2008-2009 the company has a good liquidity

position as there`s an increase in the fixed and current

assets with a percentage change of 1.26% & 7.96% .The

firm position also increasing in the side of sources of funds

as there is a decrease in the secured loans with a change

of (37.77)% and also decrease in the unsecured loans with

(30.66)%.

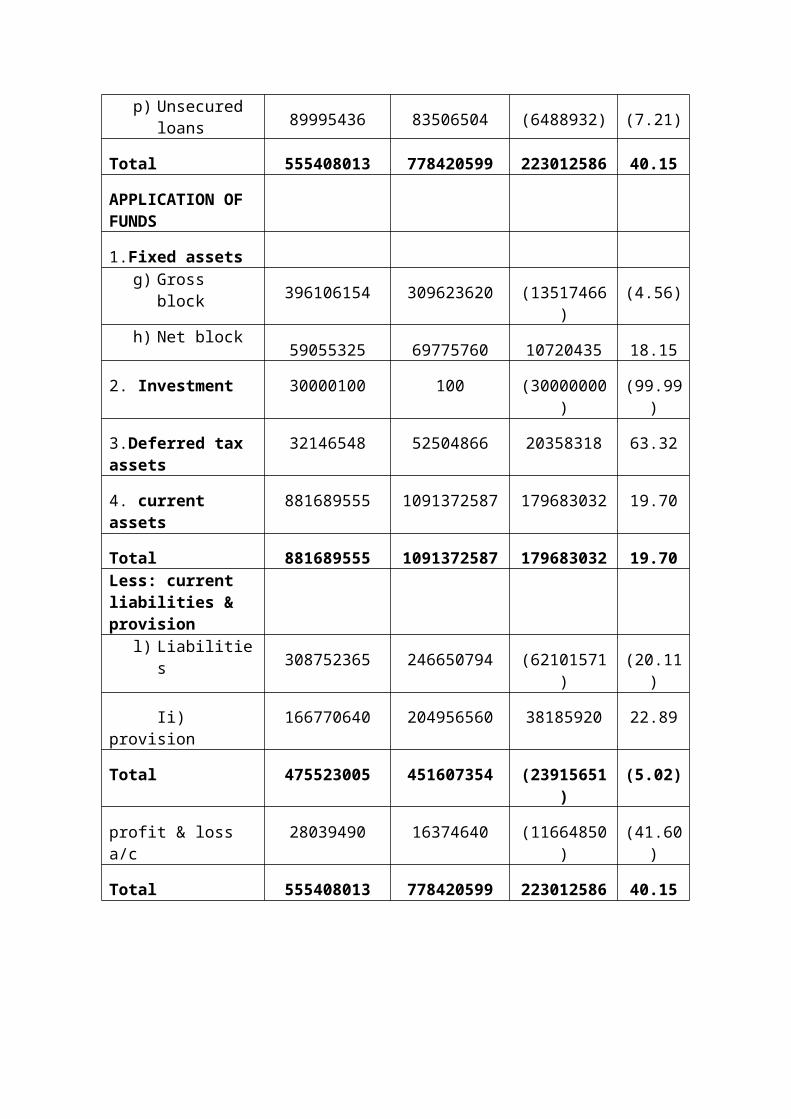

COMPARITVE BALANCE SHEET FOR THE YEAR 2009- 2010

Particular As on 31-03-09 As on 31-03-10 Absolute changes

% of changes

1.Sources Of Fundsm) Share capital

318221000 318221000 0 0n) Reserve &

surplus 136826041 267719129 130893088 95.66

o) Secured loans10365536 107204608 96839072 934.24

p) Unsecured loans 89995436 83506504 (6488932) (7.21)

Total 555408013 778420599 223012586 40.15

APPLICATION OF FUNDS

1.Fixed assetsg) Gross block

396106154 309623620 (13517466) (4.56)h) Net block

59055325 69775760 10720435 18.15

2. Investment 30000100 100 (30000000) (99.99)

3.Deferred tax assets 32146548 52504866 20358318 63.32

4. current assets 881689555 1091372587 179683032 19.70

Total 881689555 1091372587 179683032 19.70Less: current liabilities & provision

l) Liabilities308752365 246650794 (62101571) (20.11)

Ii) provision 166770640 204956560 38185920 22.89

Total 475523005 451607354 (23915651) (5.02)

profit & loss a/c 28039490 16374640 (11664850) (41.60)

Total 555408013 778420599 223012586 40.15

INTERPRETATION:

From the table of comparative balance sheet of year

2009-2010

o In the sources of funds secured loans are increasing highly and unsecured

loans are decreasing in the year 2010 as compared to 2009 which is a not

good for the company.

Secured loans are increased by 934.247 and unsecured loans are

decreased by (7.21). Reserve and surplus are increased with an absolute

change of Rs.130893088 of the firm in year 2010.

Share capital of the firm remains constant.

o The above table is showing a decrease in the fixed assets from 2009 to

2010 this shows the company is not contributing enough amount for fixed

assets out of profit.

The decreased %age of fixed assets is 4.56.

o From the above table, in the year 2010 the position of

current assets is 109.13 which was 88.16 in 2009 i.e

there`s a increase and current liabilities is 30.87 and 24.66

in the year 2009 and 2010 respectively. All this is showing

good results for the firm in both the cases, current assets

and current liabilities.

Overall the performance of KS&DL is satisfactory but when

compared to 2009 it`s not good enough as there is an

increase in secured loans but decrease in unsecured loans

with a percentage change of 934.24% and (7.21)%

respectively. company’s liquidity position is also not

satisfactory when compared to the year 2009 as there is a

decrease in fixed assets gross block with a change of

4.56% but increase in current assets with a percentage of

19.70%.company`s current liabilities are also decreasing

with a absolute changes of Rs.62101571 & percentage

change of (20.11)% which is a good sign for the company.

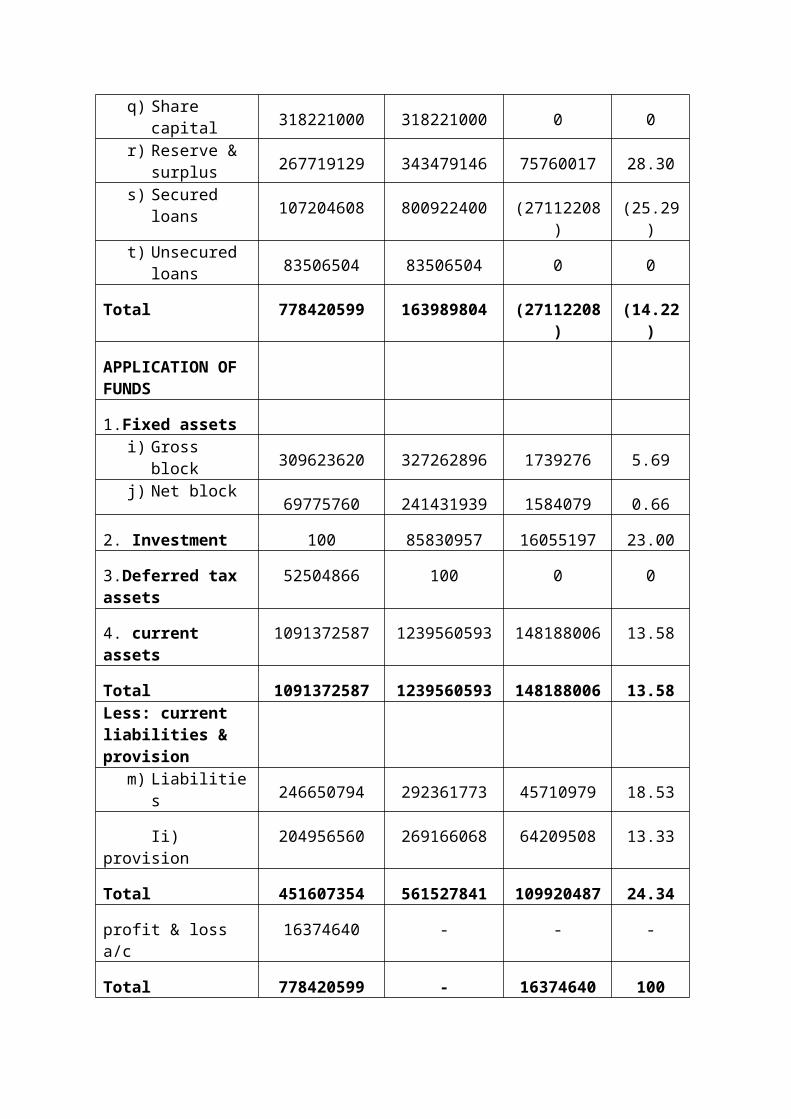

COMPARITVE BALANCE SHEET FOR THE YEAR 2010- 2011

Particular As on 31-03-10 As on 31-03-11 Absolute changes

% of changes

1.Sources Of Fundsq) Share capital

318221000 318221000 0 0r) Reserve &

surplus 267719129 343479146 75760017 28.30

s) Secured loans107204608 800922400 (27112208) (25.29)

t) Unsecured loans 83506504 83506504 0 0

Total 778420599 163989804 (27112208) (14.22)

APPLICATION OF FUNDS

1.Fixed assetsi) Gross block

309623620 327262896 1739276 5.69j) Net block

69775760 241431939 1584079 0.66

2. Investment 100 85830957 16055197 23.00

3.Deferred tax assets 52504866 100 0 0

4. current assets 1091372587 1239560593 148188006 13.58

Total 1091372587 1239560593 148188006 13.58Less: current liabilities & provision

m) Liabilities246650794 292361773 45710979 18.53

Ii) provision 204956560 269166068 64209508 13.33

Total 451607354 561527841 109920487 24.34

profit & loss a/c 16374640 - - -

Total 778420599 - 16374640 100

INTERPRETATION:

From the above table of 2010-2011

o In the sources of funds secured loans are decreasing and unsecured loans

are also decreasing in the year 2011 as compared to 2010 which is good

for the company.

Secured loans are decreased by 25.29 and unsecured loans are decreased

to zero (0). Reserve and surplus are increased with an absolute change of

Rs.75760017 in the year 2011.

Share capital of the firm remains constant.

o The above table is showing an increase in the fixed assets from 2010 to

2011 this shows the company is contributing enough amount for fixed

assets out of profit.

The increased %age of fixed assets is 5.69.

o In the year 2011 the current assets are increasing with a percentage

change of 13.58 and current liabilities are also increasing with a absolute

change of Rs. 45710979 and a percentage change of 18-53.

The overall performance of the firm is comparatively good in the last year

as it has covered all of its unsecured loans and there is a decrease in the

percentage of secured loans i.e 25.29%. Company is also contributing a

good amount toward its assets as both of current and fixed assets are

increased in the year 2011. So, the company`s liquidity position is good

and the performance of the organization is also satisfactory.

2.RATIO ANALYSIS:

RATIO:

Ratios are guides or shortcuts that are useful in evaluating the financial

position and operations of a company and in comparing them to previous years

or other companies. The primary purpose of ratios is to point out areas for

further investigation. They should be used in connection with a general

understanding of the company and its environment.

RATIO ANALYSIS:

Ratio analysis is an important means of expressing the relationship

between two numbers. A ratio can be computed form any pair of numbers. To

be useful, a ratio must represent a meaningful relationship, but use of ratios

cannot take the place of studying the underlying data.

IMPORTANCE OF RATIO ANALYSIS:

Useful in financial position analysis

Useful in simplifying accounting figures

Useful in assessing the operational efficiency

Useful in forecasting purposes

Useful in locating the weak spots of the business

Useful in comparison of performance

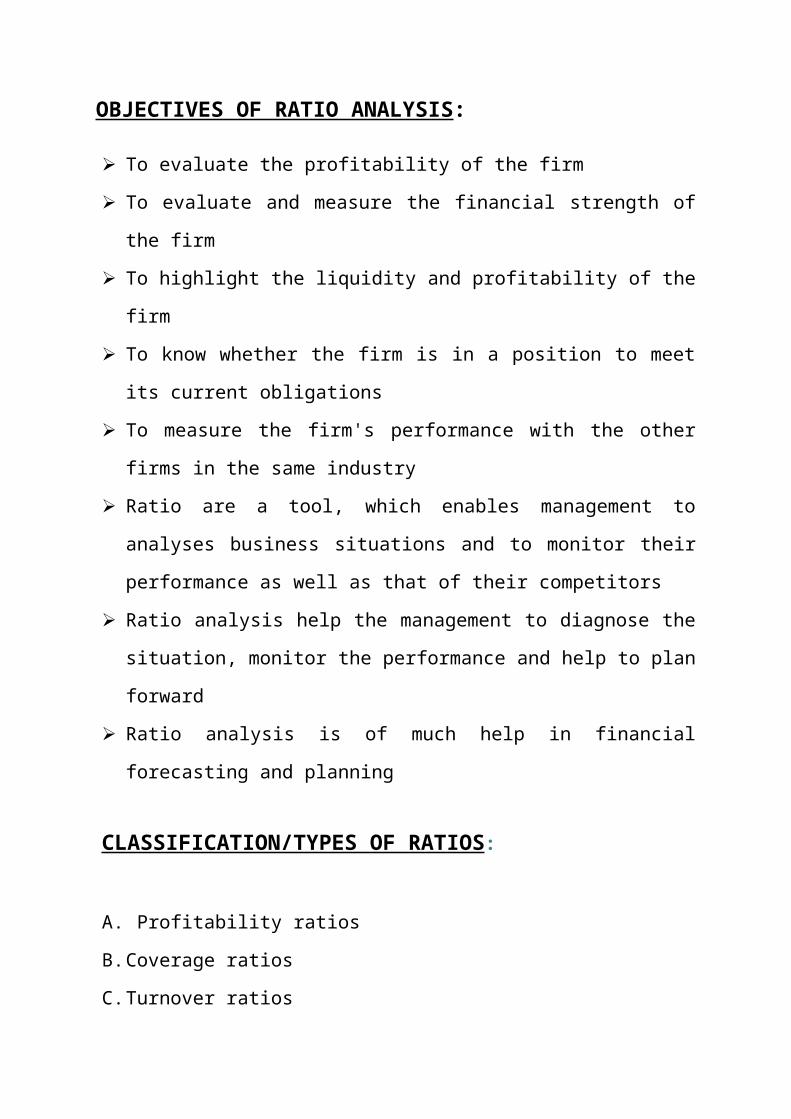

OBJECTIVES OF RATIO ANALYSIS:

To evaluate the profitability of the firm

To evaluate and measure the financial strength of the firm

To highlight the liquidity and profitability of the firm

To know whether the firm is in a position to meet its current obligations

To measure the firm's performance with the other firms in the same industry

Ratio are a tool, which enables management to analyses business situations

and to monitor their performance as well as that of their competitors

Ratio analysis help the management to diagnose the situation, monitor the

performance and help to plan forward

Ratio analysis is of much help in financial forecasting and planning

CLASSIFICATION/TYPES OF RATIOS:

A. Profitability ratios

B. Coverage ratios

C. Turnover ratios

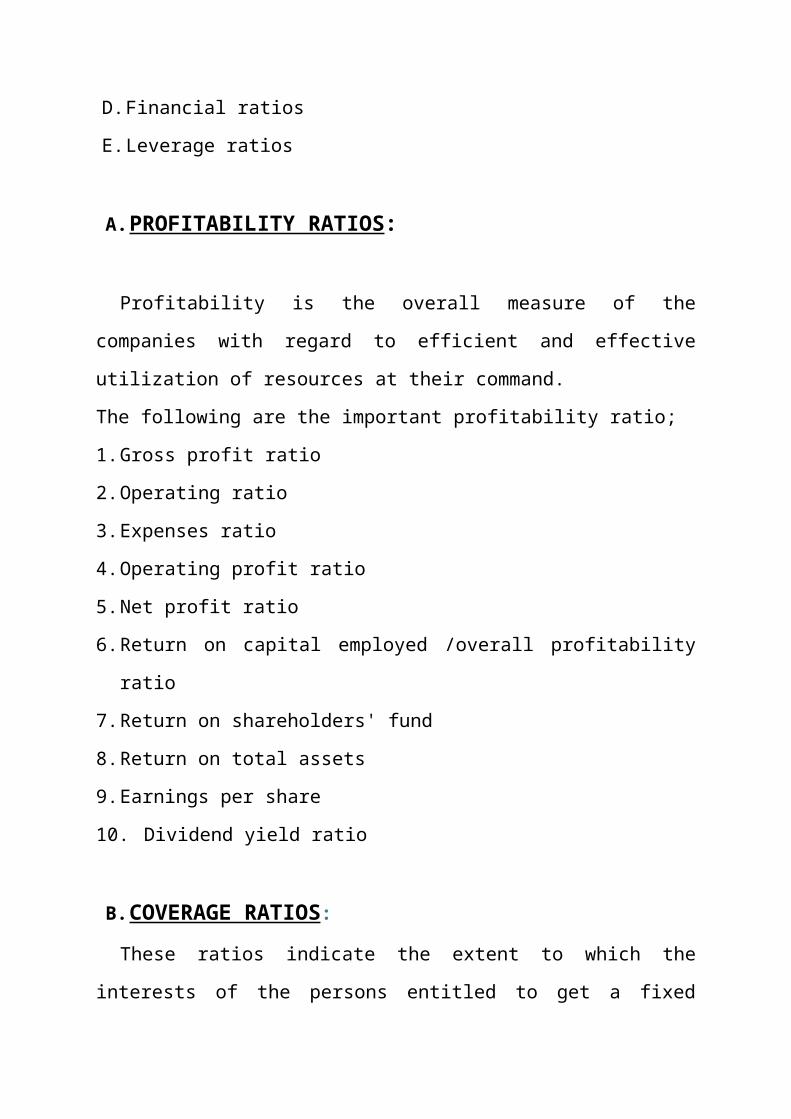

D. Financial ratios

E. Leverage ratios

A. PROFITABILITY RATIOS :

Profitability is the overall measure of the companies with regard to efficient

and effective utilization of resources at their command.

The following are the important profitability ratio;

1. Gross profit ratio

2. Operating ratio

3. Expenses ratio

4. Operating profit ratio

5. Net profit ratio

6. Return on capital employed /overall profitability ratio

7. Return on shareholders' fund

8. Return on total assets

9. Earnings per share

10.Dividend yield ratio

B. COVERAGE RATIOS :

These ratios indicate the extent to which the interests of the persons entitled

to get a fixed return (i.e., interest or dividend) or a scheduled repayment as per

agreed terms are safe.

The following are the important coverage ratio;

1. Fixed interest cover

2. Fixed dividend cover

3. Debt service coverage ratio

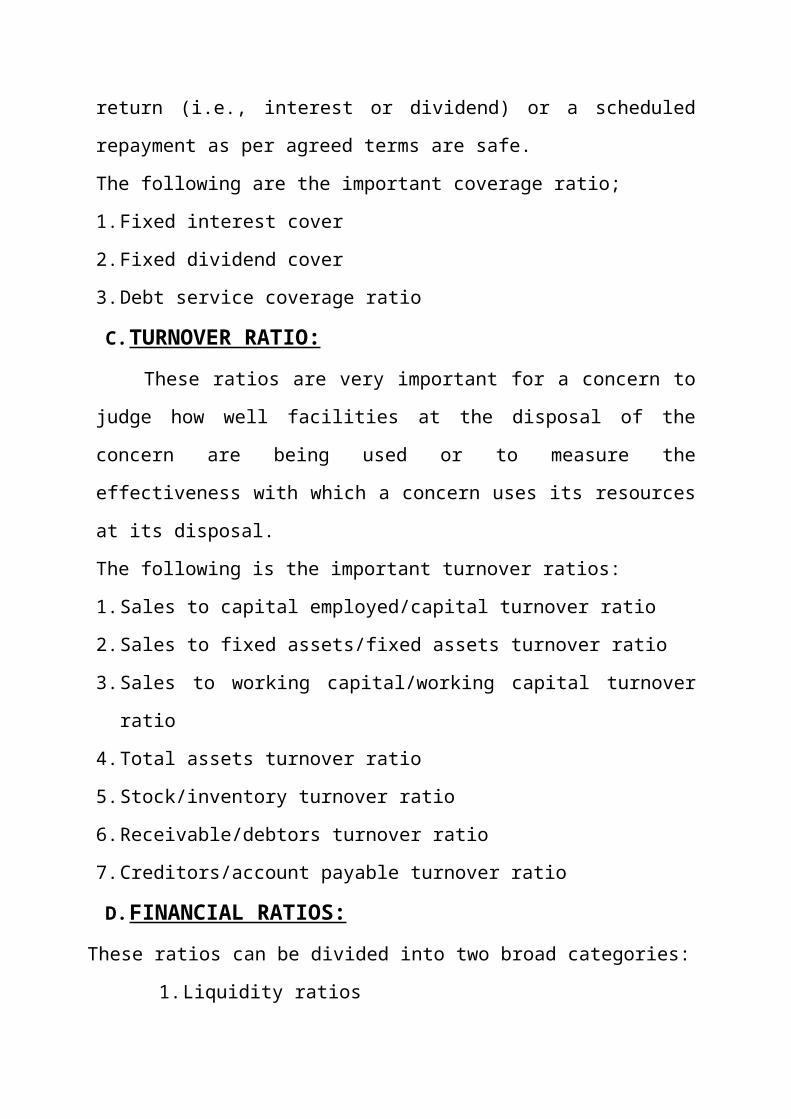

C. TURNOVER RATIO:

These ratios are very important for a concern to judge how well facilities

at the disposal of the concern are being used or to measure the effectiveness

with which a concern uses its resources at its disposal.

The following is the important turnover ratios:

1. Sales to capital employed/capital turnover ratio

2. Sales to fixed assets/fixed assets turnover ratio

3. Sales to working capital/working capital turnover ratio

4. Total assets turnover ratio

5. Stock/inventory turnover ratio

6. Receivable/debtors turnover ratio

7. Creditors/account payable turnover ratio

D. FINANCIAL RATIOS:

These ratios can be divided into two broad categories:

1. Liquidity ratios

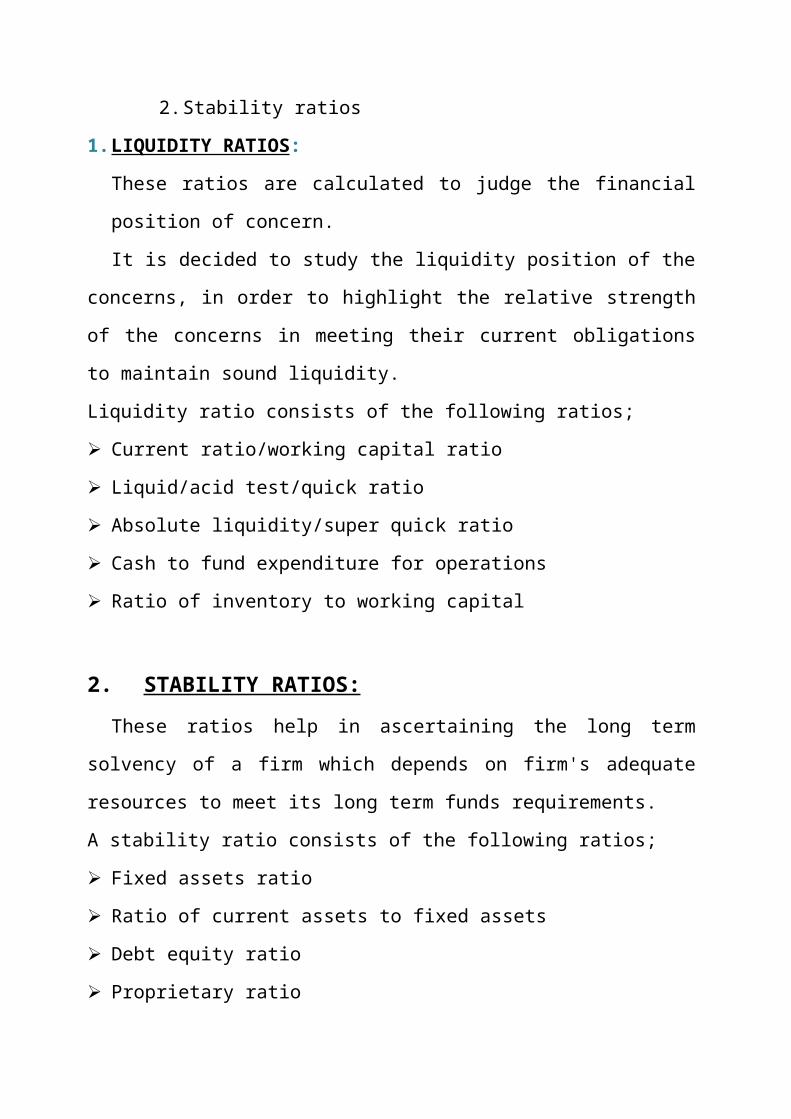

2. Stability ratios

1. LIQUIDITY RATIOS :

These ratios are calculated to judge the financial position of concern.

It is decided to study the liquidity position of the concerns, in order to

highlight the relative strength of the concerns in meeting their current obligations

to maintain sound liquidity.

Liquidity ratio consists of the following ratios;

Current ratio/working capital ratio

Liquid/acid test/quick ratio

Absolute liquidity/super quick ratio

Cash to fund expenditure for operations

Ratio of inventory to working capital

2. STABILITY RATIOS:

These ratios help in ascertaining the long term solvency of a firm which

depends on firm's adequate resources to meet its long term funds requirements.

A stability ratio consists of the following ratios;

Fixed assets ratio

Ratio of current assets to fixed assets

Debt equity ratio

Proprietary ratio

Capital gearing ratio

E. LEVERAGE RATIOS :

The leverage ratios explain the extent to which the debt is employed in the

capital structure of the concerns.

The leverage ratios are divided in two broad categories.

1. Operating leverage

2. Financial leverage

CURRENT RATIO :

This is the most widely used ratio. It is the ratio of current assets to

current liabilities. It shows a firm's ability to cover its current liabilities with its

current assets.

Current ratio is sometimes to as working capital ratio or banker's ratio. Current

ratio expresses the relationship of current assets to current liabilities. It is widely

used as a broad indicator of a company's liquidity and short term debt paying

ability.

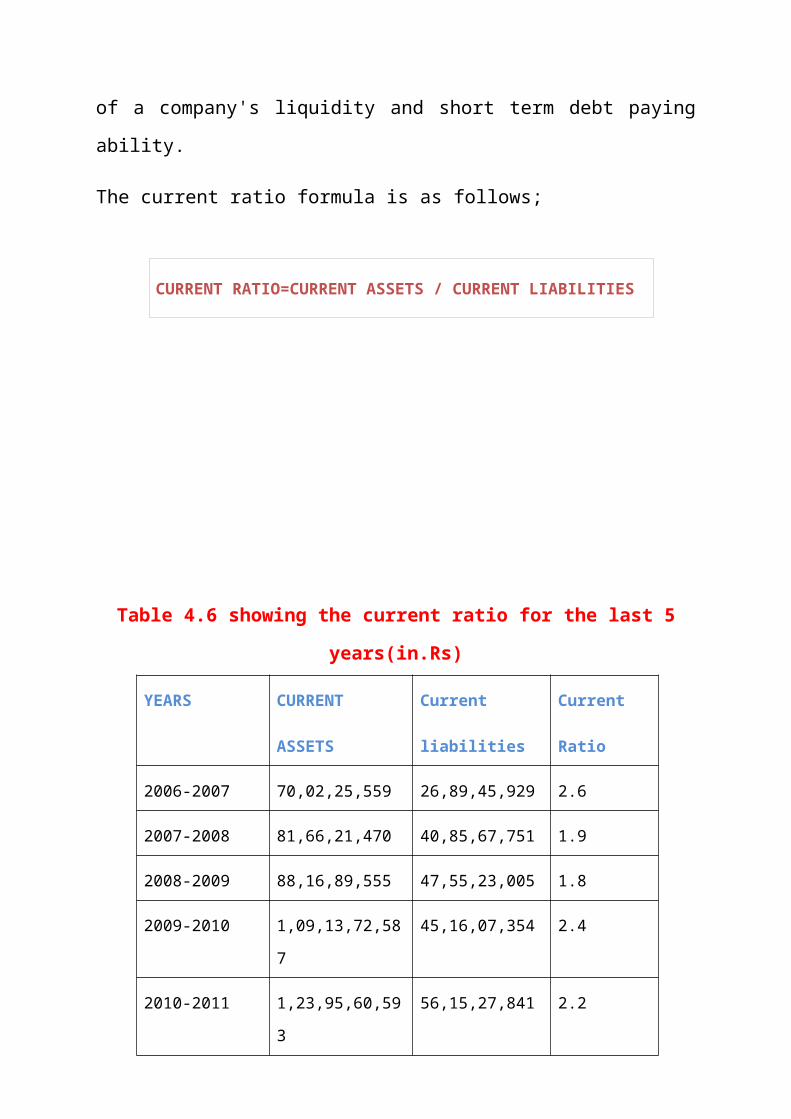

The current ratio formula is as follows;

Table 4.6 showing the current ratio for the last 5 years(in.Rs)

H

CURRENT RATIO=CURRENT ASSETS / CURRENT LIABILITIES

YEARS CURRENT

ASSETS

Current

liabilities

Current

Ratio

2006-2007 70,02,25,559 26,89,45,929 2.6

2007-2008 81,66,21,470 40,85,67,751 1.9

2008-2009 88,16,89,555 47,55,23,005 1.8

2009-2010 1,09,13,72,587 45,16,07,354 2.4

2010-2011 1,23,95,60,593 56,15,27,841 2.2

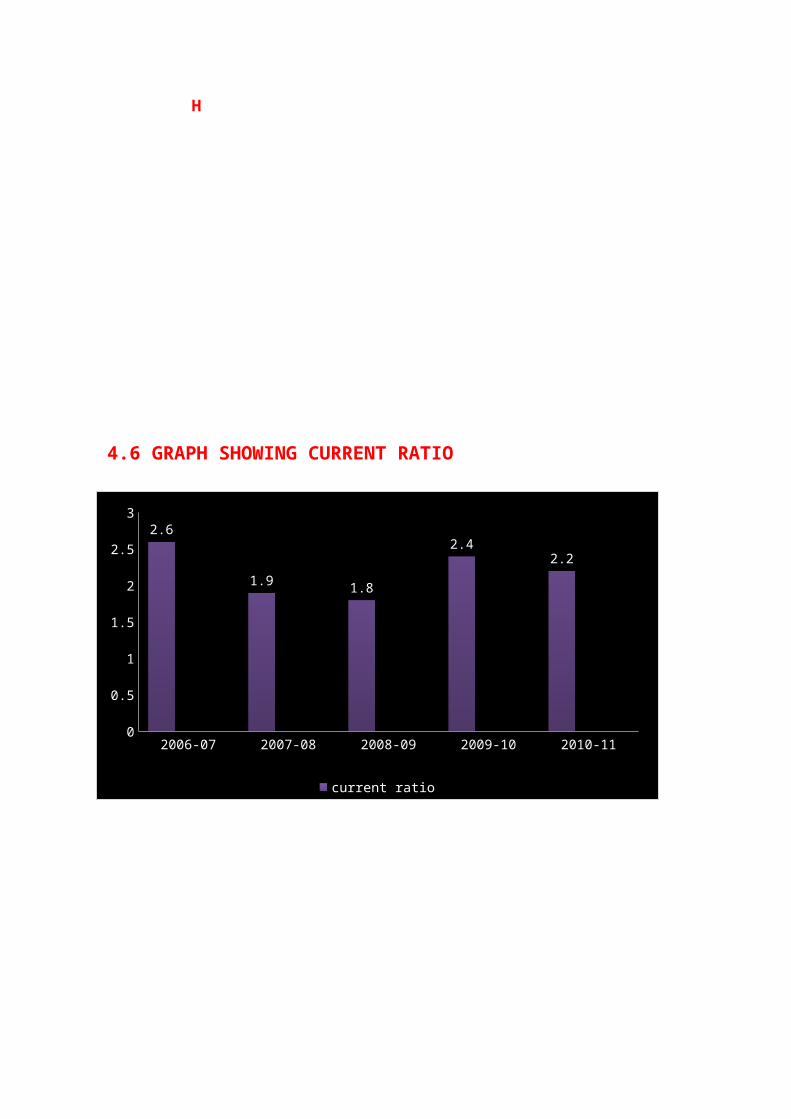

4.6 GRAPH SHOWING CURRENT RATIO

ANALYSIS:

A Relatively high current ratio is an indication that the firm is liquid and has

the ability to pay its current obligations in time as and when they become due.

On the other hand, a relatively low current ratio represents that the liquidity

position of the firm is not good and the firm shall not be able to pay its current

liabilities in time without facing difficulties. The ratio equal or near to the rule

of thumb is 2:1, i.e. current assets double the current liabilities is considered

satisfactory.

INTERPRETATION:

It is inferred that current ratio was up to the standard in the year 2006-07,

2009-10, 2010-11 due to decrease in inventory and debtors. For the two years it

is showing a decreasing trend due to drastic increase in current liabilities.

QUICK RATIO :

It is the ratio that expresses the relationship between quick or liquid assets

and quick or liquid liabilities. Any asset is called liquid if it can be converted to

cash without loss in value. Cash is the most liquid assets. They include all

current assets except inventories or stocks and prepaid expenses since these are

not easily available for the payment of current liabilities. It shows a firm's

ability to meet current liabilities with its most liquid assets. 1:1 ratio is

considered ideal ratio for a concern because it is wise to keep the liquid assets at

least equal to the liquid liabilities at all times.

Current liabilities include all those liabilities, which should necessarily be

paid within a short period of one year.

The quick ratio formula is as fallows;

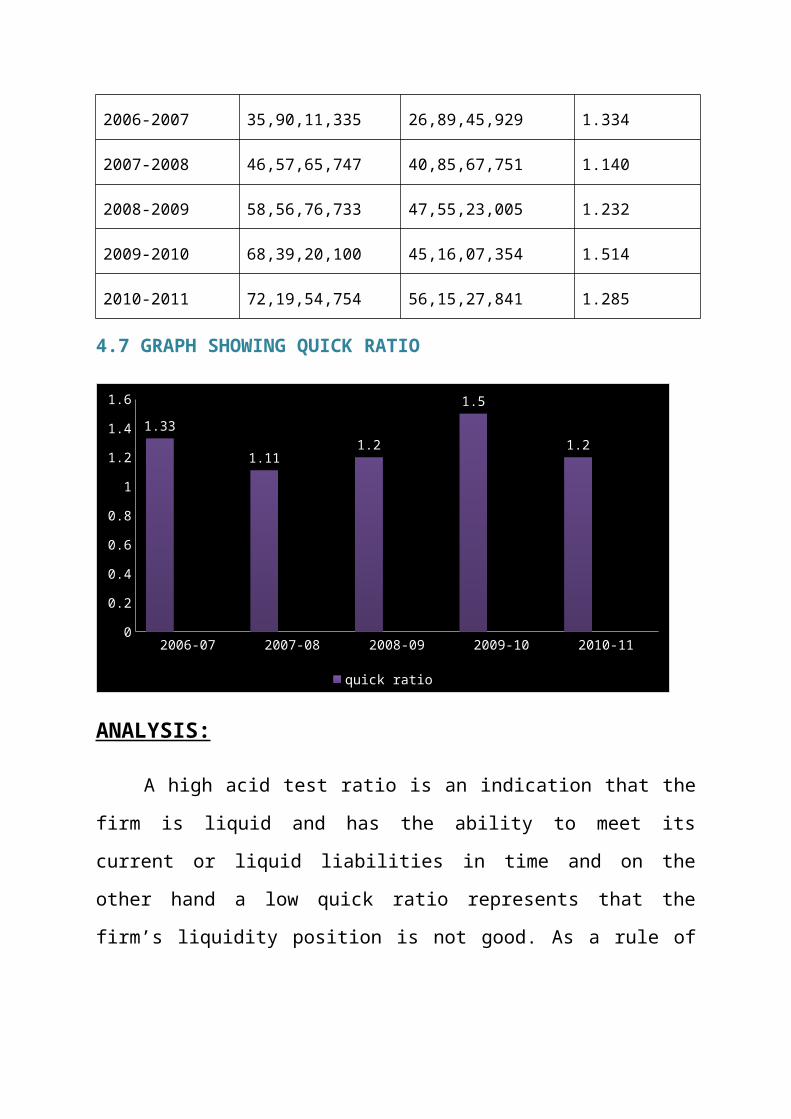

Table 4.7 showing the quick ratio for the last 5 years(in.Rs)

YEARS QUICK

ASSETS

QUICK LIABILITIES QUICK

RATIO

QUICK RATIO= QUICK OR LIQUID ASSETS / CURRENT LIABILITIES

2006-2007 35,90,11,335 26,89,45,929 1.334

2007-2008 46,57,65,747 40,85,67,751 1.140

2008-2009 58,56,76,733 47,55,23,005 1.232

2009-2010 68,39,20,100 45,16,07,354 1.514

2010-2011 72,19,54,754 56,15,27,841 1.285

4.7 GRAPH SHOWING QUICK RATIO

2006-07 2007-08 2008-09 2009-10 2010-110

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.33

1.111.2

1.5

1.2

quick ratio

ANALYSIS:

A high acid test ratio is an indication that the firm is liquid and has the

ability to meet its current or liquid liabilities in time and on the other hand a low

quick ratio represents that the firm’s liquidity position is not good. As a rule of

thumb or as a convention quick ratio of 1:1 is considered satisfactory.

INTERPRETATION:

It is inferred that the company has the ability to meet its current liquid

liabilities as and when they become due as it has pretty good quick ratio above

the normal standard of 1:1.

ABSOLUTE LIQUIDITY RATIO OR CASH RATIO :

Liquidity of a firm can be viewed from an extremely conservative point

of view and the short term liquidity of a company may be measured through

cash ratio.

Cash ratio or absolute liquid ratio is the ratio which expresses the

relationship between liquid assets and quick liabilities. Absolute liquid ratio is

the most rigorous ratio to measure the liquidity of the firm.

Absolute liquid assets include cash in hand and at bank and marketable

securities or temporary investments.

The absolute liquid ratio formula is as follows;

Table 4.8 showing the cash ratio for the last 5 years

YEAR ABSOLUTE

LIQUID ASSETS

CURRENT

LIABILITIES

RATIO

2006-2007 19,57,15,651 26,89,45,929 0.727

2007-2008 31,23,45,581 40,85,67,751 0.765

2008-2009 33,43,85,423 47,55,23,005 0.703

2009-2010 25,51,32,909 45,16,07,354 0.565

2010-2011 28,53,59,727 56,15,27,841 0.508

CASH RATIO= ABSOLUTE LIQUID ASSETS / CURRENT LIABILITIES

4.8 GRAPH SHOWING CASH RATIO

2006-07 2007-08 2008-09 2009-10 2010-110

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

0.727000000000001

0.765000000000008 0.703000000000

001

0.5650.508

cash ratio

ANALYSIS:

The acceptable norm for this ratio is 50% or 0.5:1 or 1:2 i.e. Re.1 worth

absolute liquid assets are considered adequate to pay Rs.2 worth current

liabilities in time as all the creditors are not expected to demand cash at the

same time and then cash may also be realized form debtors and investors.

INTERPRETATION:

It is inferred that there was an increasing trend in first four years that is

from 2006-2009. But in the previous year it has decreased to 0.508 which was a

result of decrease in cash and bank balance accompanied with increase in

creditors where company won’t be able to meet its short term financial

obligations. So it has to take steps to decrease creditors and also speed up its

collection from debtors to improve its cash reserves.

STOCK OR INVENTORY TURNOVER RATIO :

The inventory turnover ratio also known as stock turnover ratio indicates

whether inventory has been efficiently used or not. The purpose is to see

whether only the required minimum funds have been locked up in inventory.

Inventory turnover during the period and evaluates the efficiency with which a

firm is able to manage its inventory.It denotes the speed at which the inventory

will be converted into sales, thereby contributing for the profits of the concern.

Here cost of goods include ( opening stock + purchases + manufacturing

expenses - closing stock or sales - Gross profit)

And average stock includes opening stock + closing stock

2

Inventory turnover ratio can be calculated as fallows;

Table 4.9 showing the Stock Turnover Ratio for the last 5 years

YEARS SALES AVERAGE

STOCK

RATIO

2006-2007 98,81,11,423 39,24,94,368 2.518

2007-2008 104,43,74,470 34,60,34,973 3.018

2008-2009 1,28,64,62,008 32,34,34,273 3.978

2009-2010 1,53,37,03,531 35,17,32,655 4.360

INVENTORY TURNOVER RATIO= SALES / AVERAGE STOCK

2010-2011 16,47,77,47,37 46,25,29,163 3.562

4.9 GRAPH SHOWING INVENTORY TURNOVER RATIO

2006-07 2007-08 2008-09 2009-10 2010-110

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5

2.518

3.018

3.9784.36

3.562

Inventory turnover ratio

ANALYSIS:

Inventory Turnover Ratio measures the velocity of conversion of stock

into sales. A high inventory turnover/stock velocity indicates efficient

management of inventory because more frequently the stocks are sold, the lesser

amount of money is required to finance the inventory.

A low inventory turnover indicates over-investment in inventory, dull

business, poor quality of goods, stock accumulations, accumulations of obsolete

and slow moving goods and low profits as compared to total investments. There

are no ‘rules of thumb’ or ‘standard inventory turnover ratio’ for interpreting the

inventory turnover ratio.

INTERPRETATION:

It is inferred that the inventory turnover ratio has been showing an

increasing trend from past four years but there was a slight decrease in the

previous year, which indicates that there is an efficient management of

inventory and stocks are sold out within short span of time which reduces the

warehouse cost and avoids the chances of obsolescence of stocks.

DEBTORS OR RECEIVABLE TURNOVER RATIO :

Debtor's turnover ratio indicates the velocity of data collection of firm. In

simple words, it indicated the number of times average debtors are turned over

during a year. This ratio indicates the speed at which the debtors are converted

into cash. Usually a high ratio will be referred to high efficiency in debt

collection and a low ratio for lower efficiency. High ratios indicates that debts

are collected in short time period (i.e., there is little time gap between sales and

payments.

The ratio is obtained by dividing the net credit sales by average debtors

outstanding during that year.

Debtors' turnover ratio can be calculated as fallows:

Table 4.10 showing the Debtors Turnover Ratio for the last 5 years(in.Rs)

YEARS NET CREDIT

SALES

AVERAGE

DEBTORS

RATIO

DEBTORS TURNOVER RATIO= NET CREDIT SALES / AVERAGE DEBTORS

2006-2007 98,81,11,423 7,45,79,779 13.249

2007-2008 1,04,43,74,470 7,48,55,399 13.95

2008-2009 1,28,64,62,008 11,36,10,155 11.323

2009-2010 1,53,37,03,531 15,49,38,144 9.899

2010-2011 16,47,77,47,37 16,80,85,689 9.803

4.10 GRAPH SHOWING DEBTORS TURNOVER RATIO

2006-07 2007-08 2008-09 2009-10 2010-110

2

4

6

8

10

12

14

16

13.24913.95

11.323

9.899 9.803

Debtors turnover ratio

ANALYSIS:

The debtors’ turnover ratio indicates the number of times the debtors

are turned over a year. Generally, the higher the debtors’ turnover the more

efficient is the management of debtors similarly; low debtors turnover implies

inefficient management of debtors or sales.

INTERPRETATION:

From the above table, it is seen that KS&DL has increased by almost

50% for the two years to 13.249 and 13.952 respectively. But in the year 2008-

2009, 2009-2010 & 2010-11 it has gradually decreased to 11.323, 9.899 &

9.803.

It is inferred that it shows a decreasing trend from past three years which is not

a good sign for a company. So it has to take steps to manage debtors through

prompt collection so that it will be able to sell the goods on credit and there by

gaining sales and profit.

CREDITORS OR ACCOUNT RECIEVABLE TURNOVER

RATIO :

Debtor's turnover ratio indicates the velocity of data collection of firm. In

simple words, it indicated the number of times average debtors are turned over

during a year. This ratio indicates the credit facility enjoyed by a firm. It is

calculated by taking into account the net purchase and average creditors.

Creditors' turnover ratio can be calculated as fallows:

Table 4.11 showing the Creditors Turnover Ratio for the last 5 years(in.Rs)

YEARS NET PURCHASE AVERAGE

CREDITORS

RATIO

2006-2007 36,72,38,387 4,53,54,445 8.09

2007-2008 50,70,94,587 4,75,84,558 10.65

2008-2009 54,14,33,115 7,01,84,312 07.71

2009-2010 80,19,28,342 6,97,71,274 11.49

2010-2011 77,53,83,439 6,44,60,999 12.02

4.11 GRAPH SHOWING CREDITORS TURNOVER RATIO

CREDITORS TURNOVER RATIO= NET PURCHASE / AVERAGE CREDITORS

2006-07 2007-08 2008-09 2009-10 2010-110

2

4

6

8

10

12

14

8.09

10.65

7.71

11.4912.02

Creditors turnover ratio

ANALYSIS:

Generally higher the creditors velocity better it is or otherwise lower the

creditors velocity less favorable are results.

INTERPRETATION

From the above table it has seen that KS&DL exhibits high creditors turnover

ratio from 2006-08 where it has decreased gradually in the year 2008-09 and

increased in 2009-10,2010-11 to 11.49 and 12.02 respectively.

WORKING CAPITAL TURNOVER RATIO:

Working capital turnover ratio indicates the velocity of the utilization of

working capital. This ratio indicates the number of times the working capital is

turned over in the course of a year. This measures the efficiency with which the

working capital is being used by the firm. A higher ratio indicates efficient

utilization of working capital and a low ratio indicates otherwise.

Working capital turnover ratio can be calculated as fallows:

Table 4.12 showing the Working Capital Turnover Ratio

GRAPH SHOWING WORKING CAPITAL TURNOVER

RATIO

WORKING CAPITAL TURNOVER RATIO= SALES / NET WORKING CAPITAL

YEARS SALES NET WORKING

CAPITAL

RATIO

2006-2007 98,81,11,423 43,12,79,630 2.291

2007-2008 1,04,43,74,470 40,80,53,719 2.559

2008-2009 1,28,64,62,008 40,61,66,550 3.167

2009-2010 1,53,37,03,531 63,97,65,233 2.397

2010-2011 16,47,77,47,37 67,80,32,752 2.430

2006-07 2007-08 2008-09 2009-10 2010-110

0.5

1

1.5

2

2.5

3

3.5

2.291

2.559

3.167

2.397 2.43

ANALYSIS:

A higher working capital ratio indicates efficient utilization of working capital

and low ratio indicates otherwise.

From the above table, KS&DL working capital turnover ratio in the year

2006-2007 was 2.291 and for next two years it has shown an increasing trend. It

increased in the year 2008-2009 to 3.167 and decreased in the year 2009-2010

to 2.397 & 2010-11 to 2.430.

INTERPRETATION:It is inferred that working capital turnover ratio

shows an increasing trend, but it has decreased in the year 2009-2010 & 2010-

11 which shows there is inefficient management of working capital in the

previous year. The company should take steps to invest in current assets and

other short term investment opportunities.

Chapter-5

Findings, suggestion and conclusion

5.FINDINGS, SUGGESTION AND CONCLUSION

FINDINGS :

1. The Current Ratio of KS&DL even though it shows a decreasing trend in

the years 2007-2008 and 2008-2009, it has increased in the year 2009-

2010 to 2.417 which is above the standard or rule of thumb. The liquidity

position of the organization is satisfactory as it is taking steps to improve

its liquidity position and it has the ability to pay its current obligations in

time.

2. The Quick Ratio of KS&DL has remained stable during all the years. It is

just above the standard which shows that the company has ability to meet

its current liquid liabilities.

3. During the year 2006-2009, the cash ratio has increased gradually for

three years. But it decreased in the year 2009-2010 to 0.565 , 2010-2011

to 0.508 which is just above the standard rule and it has to improve its

short term financial position.The reason for decrease is decreasing cash in

the year 2009-2010, 2010-2011 and due to increase in creditors on the

current liabilities side.

4. The Inventory Turnover Ratio of KS&DL in the year 2006-2007 was

2.518. Thereafter, inventory turnover ratio is showing an increasing trend

which indicates efficient management of inventory as more frequently the

stocks are sold, the lesser amount of money is required to finance the

inventory.

5. The Debtors Turnover Ratio at KS&DL showed an increasing trend in the

next two years. But in the year 2009-2010 and in the year 2010-2011 its

showing a decreasing trend which indicates inefficient management of

debtors.

6. The creditor`s turnover ratio at KS&DL in the year 2006-07 was 8.097

and later on it shows an increasing trend in the year 2007-08 and there

was a constant increase in the year 2009-10 & 2010-11 as it indicates the

creditors are paid in time and this earns a good reputation to company in

the market.

7. The Working Capital Turnover Ratio of KS&DL was 2.291 2006-2007.

Later it showed an increasing trend from 2007-2008 to 2008-2009. But in

the year 2009-2010, the Working Capital Turnover Ratio has decreased to

2.40 which imply inefficient management of working capital. This is due

to decrease in cash and bank balance.

SUGGESTIONS/RECOMMONDATIONS :

1. The liquidity position is showing relatively more the company can go for

reducing the current assets and try to invest it in long term assets or long

term revenue earning investments.

2. The company is suggested to have a continuous check of all cash and bank

balance. In case if the cash is idle it can be brought to the notice and can be

invested in various short term investment opportunities to earn returns.

Forecasting of cash should be made to meet requirements of business.

3. Due to the shortage in cash the company is unable to have adequate

inventory reserves which are hampering its optimum production capacity.

So the company has to have efficient inventory reserves to increase its

production.

4. The company is not able to generate income from other sources due to lack

of skills of the investment analyst. So, the company should try improving

its investment decisions to generate income from other sources.

5. As a part of recommendation it is advisable if KS&DL diverts a little

portion of funds in undertaking expansion activities and ultimately

enhancing its sales and profitability.

6. By adopting good planning towards recovery of debt that is by adopting

Good Credit policy, Proper assessment of credit worthiness of its debtors,

by adopting strict collection measures etc. the company can get into more

profitability.

7. It is suggested to control over and under stocking of raw material using

technical auditors and maintain a coordination between production

processes department and inventory handling department for efficient

outcomes.

8. If the company maintains a favorable cash and bank balance it will help in

smooth running of business and maintain balanced working capital.

CONCLUSION :

The overall performance of the organization is satisfactory, particularly the

last two years trading profit is good but the trading profit is fluctuating every

year. The company can increase its clientele base by doing certain promotional

campaigns such as organizing corporate parties and advertising in a better

manner.

As a part of the study it can be concluded that the quick ratio overall the year

have remains stable which is the good indication for the company`s position,

since its able to meet its current liabilities. Also the creditor`s turnover ratio is a

good indicator that the company is able to meet a timely payments and hence is

enjoying a good reputation in the market. However as per the debtors position

in the balance sheet effective management is required, so that a favorable trend

and position can be observed overall the years.

Also KSDL should try to have an efficient inventory reserve so that its

productivity is increase and hence improve the investment decision and increase

the income level from other sources.

Last but not the least the company can device a competitive pricing strategy

so that it can overcome price related hurdles that it has been facing over the

years and hence leads to a successful organization, fulfilling its operational

objectives.

BIBLIOGRAPHY:

REFERENCE

BOOKS

AUTHOR EDITION PUBLISHER

BBM Financial

Management

Reddy, Appannaiah,

Satyaprasad

1st Edition Himalaya Publishing House,

Delhi

Business Research

Methods

Ramachandra,

Chandrasekhar

1st Edition Himalaya Publishing House,

Delhi

Cost and financial

analysis

Jawahar lal 1st Edition Himalaya publishing

house,delhi

Annual Reports

Journals

Internet references

Company Web Site: www.mysoresandal.co.in

www .KSDL. com

APPENDIX AND ANNEXURE

BALACE SHEET AS AT 31ST MARCH (AMOUNT IN CRORES)

Particulars 2007 2008 2009 2010 2011

1.Sources Of Fundsu) Share capital

31.82 31.82 31.82 31.82 31.82v) Reserve & surplus

- 1.51 13.68 26.77 34.34w) Secured loans

- 1.66 1.04 10.72 8.00x) Unsecured loans

19.99

13.00 9.00 8.35 8.35

Deferred tax liability (Net) - - 3.21 5.25 6.14

1.Fixed assetsGross block

30.28 29.24 29.61 30.96 32.72Less depreciation

24.24 23.35 23.71 23.98 24.14

Net block 6.03 5.89 5.91 6.98 8.85

Capital work in progress - - - - -

Total 6.03 5.89 5.91 6.98 8.85

2. current Assets Loans and Advances Inventories

34.12 35.09 29.60 40.75 51.76Sundary Debtors

6.88 8.09 14.63 16.35 17.29

Cash and Bank Balance 19.57 31.23 33.43 25.51 28.53

Loans and Advances 9.44 7.25 10.49 21.53 21.39

Investments in gratuity fund - - - - -

Total 70.02 81.66 88.17 109.14 123.95

Less: Current Liabilities and Provision

Current Liabilities 17.07 29.26 30.88 24.67 29.23

Provision 9.82 11.59 16.67 20.50 26.91

Net Curerent Assets (6) Less (7) 43.13 40.81 40.62 63.98 67.80

Miscellaneous Expenditure 2.12 1.29 2.80 1.64 -

Total Assets (Net) 51.81 47.99 61.96 77.84 82.52

PROFIT AND LOSS ACCOUNT (RS.IN LAKHS)

PARTICULARS AMOUNT AMOUNT AMOUNT AMOUNT

INCOME(year) 2008 2009 2010 2011

Net Sales 1,04,43,74,470

1,28,64,62,008

1,53,37,03,531

1,64,77,74,737

Other income 1,90,04,300 2,09,85,305 6,06,23,797 2,22,88,309

1,06,33,78,770

1,30,74,47,313

1,59,43,27,328

1,67,00,63,047

Increase/(-) Decrease in stock

4,73,09,343 2,64,66,726 7,03,74,213 5,32,86,174

1,11,06,88,113

1,28,09,80,587

1,66,47,01,541

1,72,33,49,221

EXPENDITURE

Materials Consumed (include trading items)

50,70,94,583

54,13,33,115

80,19,28,343

77,53,83,439

Other Expenditure 55,19,82,573

61,35,25,868

73,44,42,910

79,97,99,905

Depreciation 36,05,016 35,77,430 39,69,038 49,82,474

1,06,26,82,573

1,15,85,36,413

1,54,03,40,291

1,58,01,65,818

Operating Profit/Loss 4,80,05,540 12,24,44,174

12,43,61,250

14,31,83,402

Less: Interest and Finance charges

46,08,734 45,08,734 72,76,261 82,97,546

PROFIT BEFORE TAX 4,33,57,146 11,79,35,440

11,70,89,988

13,48,85,857

Less: Provision

for Taxation

Current Tax 52,00,000 1,80,00,000 1,85,00,000 4,80,00,000

Fringe Benefit Tax 23,01,452 70,98,690 21,28,828 -

Deferred Tax Asset 3,21,46,548 2,03,58,318 89,30,375

Dividend Tax 45,96,941 - 87,04,083

PROFIT AFTER TAX 3,58,55,694 8,82,39,809 11,68,14,478

9,31,12,149

Prior period income/(-) Expenditure

66,40,886 1,40,78,609 14,41,082

Proposed dividend 2,70,48,785 - 1,59,11,050

Tax of earlier year 2,20,99,794 1,37,30,643 - -

2,03,96,797 12,17,55,748

13,08,93,087

7,57,60,017

Profit/loss brought forward previous year

(53,26,504) 1,50,70,293 13,68,26,041

26,77,19,129

Profit/loss Carried to Balance sheet

1,50,70,293 13,68,26,041

26,77,19,129

34,34,79,146

![Presentation1 1 [repaired]](https://img.pdfslide.us/doc/110x75/588869671a28abad0d8b641f/presentation1-1-repaired.jpg)

![Blank jeopardy template[1] [repaired]](https://img.pdfslide.us/doc/110x75/548824e7b47959ce0c8b5626/blank-jeopardy-template1-repaired.jpg)

![BANKING_BASICSMini[1] (Repaired).doc](https://img.pdfslide.us/doc/110x75/577cdf0b1a28ab9e78b05cb2/bankingbasicsmini1-repaireddoc.jpg)

![Tripddy htbas 1 [repaired]](https://img.pdfslide.us/doc/110x75/55c28657bb61eb7d608b45b1/tripddy-htbas-1-repaired.jpg)