Embed Size (px)

Citation preview

Colliers International | Kansas City colliersmultifamilyeast.com

KANSAS CITY1Q17 | MULTIFAMILY

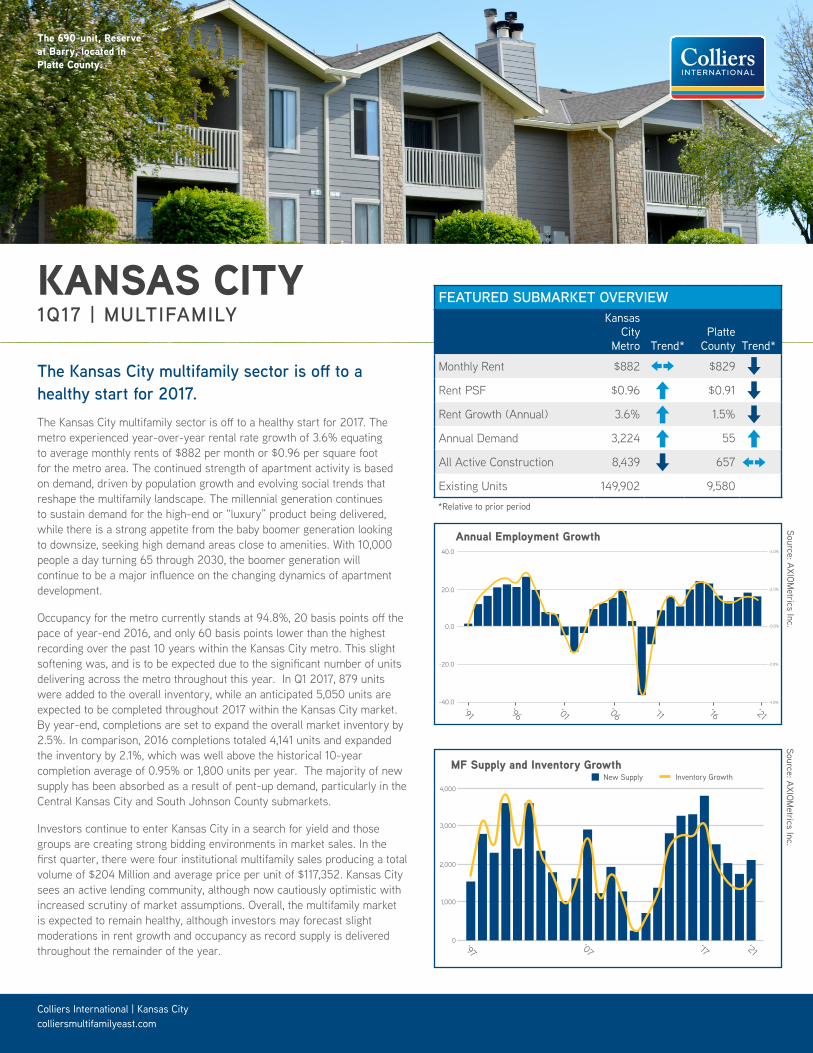

The Kansas City multifamily sector is off to a healthy start for 2017.The Kansas City multifamily sector is off to a healthy start for 2017. The metro experienced year-over-year rental rate growth of 3.6% equating to average monthly rents of $882 per month or $0.96 per square foot for the metro area. The continued strength of apartment activity is based on demand, driven by population growth and evolving social trends that reshape the multifamily landscape. The millennial generation continues to sustain demand for the high-end or “luxury” product being delivered, while there is a strong appetite from the baby boomer generation looking to downsize, seeking high demand areas close to amenities. With 10,000 people a day turning 65 through 2030, the boomer generation will continue to be a major influence on the changing dynamics of apartment development.

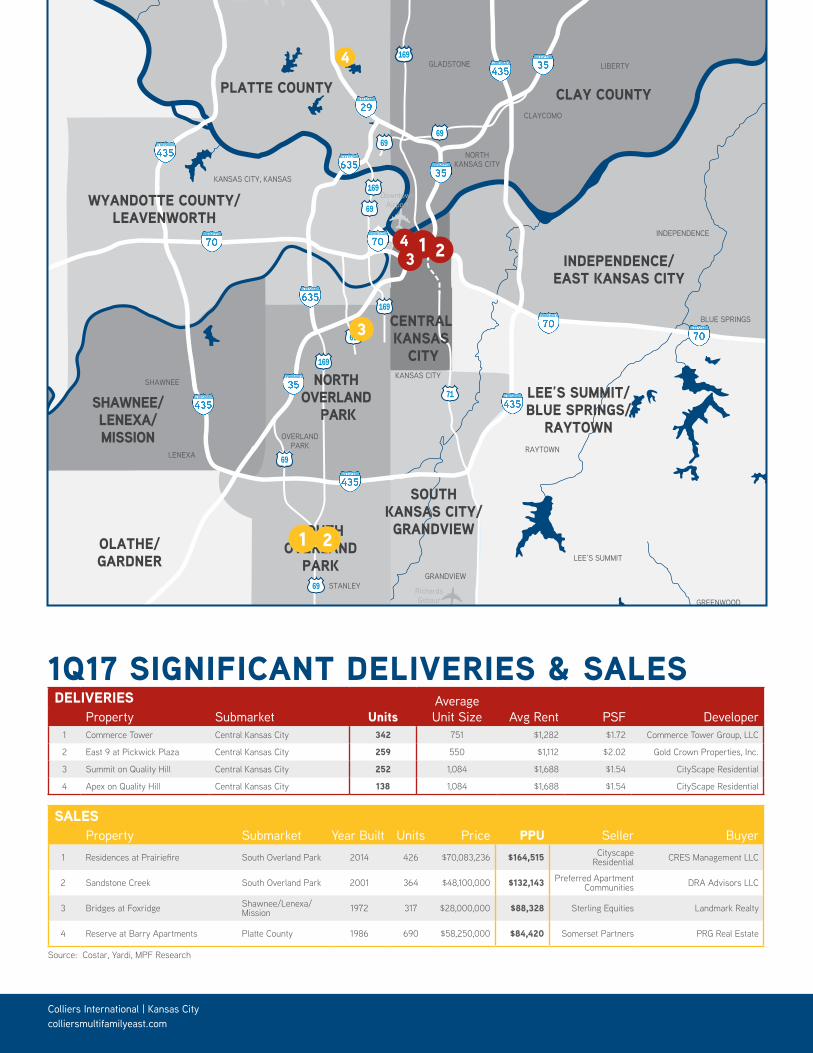

Occupancy for the metro currently stands at 94.8%, 20 basis points off the pace of year-end 2016, and only 60 basis points lower than the highest recording over the past 10 years within the Kansas City metro. This slight softening was, and is to be expected due to the significant number of units delivering across the metro throughout this year. In Q1 2017, 879 units were added to the overall inventory, while an anticipated 5,050 units are expected to be completed throughout 2017 within the Kansas City market. By year-end, completions are set to expand the overall market inventory by 2.5%. In comparison, 2016 completions totaled 4,141 units and expanded the inventory by 2.1%, which was well above the historical 10-year completion average of 0.95% or 1,800 units per year. The majority of new supply has been absorbed as a result of pent-up demand, particularly in the Central Kansas City and South Johnson County submarkets.

Investors continue to enter Kansas City in a search for yield and those groups are creating strong bidding environments in market sales. In the first quarter, there were four institutional multifamily sales producing a total volume of $204 Million and average price per unit of $117,352. Kansas City sees an active lending community, although now cautiously optimistic with increased scrutiny of market assumptions. Overall, the multifamily market is expected to remain healthy, although investors may forecast slight moderations in rent growth and occupancy as record supply is delivered throughout the remainder of the year.

FEATURED SUBMARKET OVERVIEWKansas

City Metro Trend*

Platte County Trend*

Monthly Rent $882 $829

Rent PSF $0.96 $0.91

Rent Growth (Annual) 3.6% 1.5%

Annual Demand 3,224 55

All Active Construction 8,439 657

Existing Units 149,902 9,580

The 690-unit, Reserve at Barry, located in Platte County.

Source: AXIOMetrics Inc.

Source: AXIOMetrics Inc.

*Relative to prior period

-40.0

0

1,000

2,000

3,000

4,000

Annual Employment Growth

New Supply Inventory GrowthMF Supply and Inventory Growth

-4.0%

-20.0

0.0

20.0

40.0

-2.0%

-0.0%

-2.0%

-4.0%

‘91

‘97‘07 ‘17 ‘21

‘96 ‘01 ‘06 ‘11 ‘16 ‘21

Colliers International | Kansas Citycolliersmultifamilyeast.com

SOUTHOVERLAND

PARK

CENTRAL KANSAS

CITY

SOUTHKANSAS CITY/GRANDVIEW

LEE’S SUMMIT/BLUE SPRINGS/

RAYTOWN

CLAY COUNTY

WYANDOTTE COUNTY/LEAVENWORTH

NORTH OVERLAND

PARK

Sherman Army Airfield Clay

CountyRegional Airfield

RichardsGebaurAirport

Kansas CityInternational

Airport

DowntownAirport

KANSAS CITY, KANSAS

SHAWNEE

OVERLANDPARK

STANLEYGRANDVIEW

BELTON

PECULIAR

RAYMORE

LEE’S SUMMIT

RAYTOWN

BLUE SPRINGS

INDEPENDENCE

LIBERTY

CLAYCOMO

GLADSTONE

KANSAS CITY

PLATTE CITY

KEARNEY

EXCELSIORSPRINGS

NORTHKANSAS CITY

KANSAS CITY

GREENWOOD

LENEXA

Kansas City MetroOffice Submarkets

Colliers International4520 Main Street, Suite 1000Kansas City, Missouri 64111www.colliers.com

PLATTE COUNTY

SHAWNEE/LENEXA/MISSION

INDEPENDENCE/EAST KANSAS CITY

OLATHE/GARDNER

1 243

1 2

3

4

DELIVERIES Average Unit Size Property Submarket Units Avg Rent PSF Developer

1 Commerce Tower Central Kansas City 342 751 $1,282 $1.72 Commerce Tower Group, LLC

2 East 9 at Pickwick Plaza Central Kansas City 259 550 $1,112 $2.02 Gold Crown Properties, Inc.

3 Summit on Quality Hill Central Kansas City 252 1,084 $1,688 $1.54 CityScape Residential

4 Apex on Quality Hill Central Kansas City 138 1,084 $1,688 $1.54 CityScape Residential

1Q17 SIGNIFICANT DELIVERIES & SALES

Source: Costar, Yardi, MPF Research

SALESYear Built PPU Property Submarket Units Price Seller Buyer

1 Residences at Prairiefire South Overland Park 2014 426 $70,083,236 $164,515 Cityscape Residential CRES Management LLC

2 Sandstone Creek South Overland Park 2001 364 $48,100,000 $132,143 Preferred Apartment Communities DRA Advisors LLC

3 Bridges at Foxridge Shawnee/Lenexa/Mission 1972 317 $28,000,000 $88,328 Sterling Equities Landmark Realty

4 Reserve at Barry Apartments Platte County 1986 690 $58,250,000 $84,420 Somerset Partners PRG Real Estate

Colliers International | Kansas City

Martin Maguire cprcSenior Research Director | Kansas City

+1 816 556 [email protected]

Colliers International | Kansas City | 4520 Main Street, Suite 1000, Kansas City, Missouri 64111 | +1 816 531 5303 | colliers.com

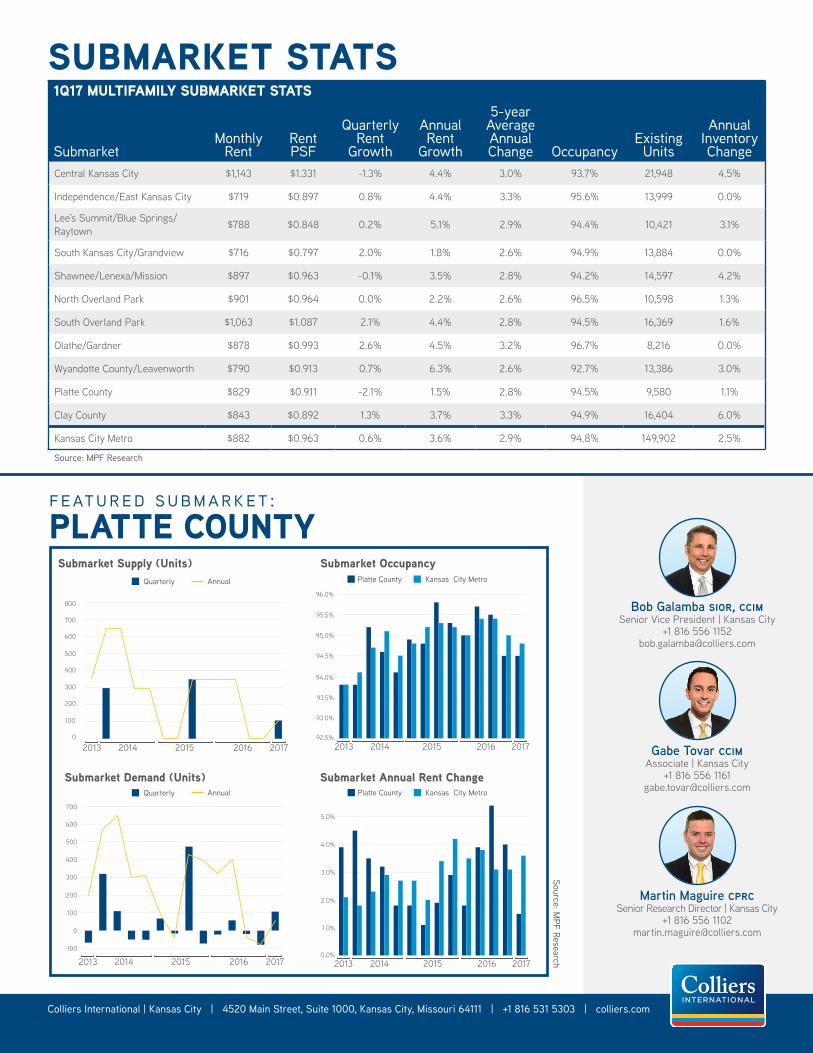

SUBMARKET STATS1Q17 MULTIFAMILY SUBMARKET STATS

SubmarketMonthly

RentRent PSF

Quarterly Rent

Growth

Annual Rent

Growth

5-year Average Annual Change Occupancy

Existing Units

Annual Inventory Change

Central Kansas City $1,143 $1.331 -1.3% 4.4% 3.0% 93.7% 21,948 4.5%

Independence/East Kansas City $719 $0.897 0.8% 4.4% 3.3% 95.6% 13,999 0.0%

Lee's Summit/Blue Springs/Raytown $788 $0.848 0.2% 5.1% 2.9% 94.4% 10,421 3.1%

South Kansas City/Grandview $716 $0.797 2.0% 1.8% 2.6% 94.9% 13,884 0.0%

Shawnee/Lenexa/Mission $897 $0.963 -0.1% 3.5% 2.8% 94.2% 14,597 4.2%

North Overland Park $901 $0.964 0.0% 2.2% 2.6% 96.5% 10,598 1.3%

South Overland Park $1,063 $1.087 2.1% 4.4% 2.8% 94.5% 16,369 1.6%

Olathe/Gardner $878 $0.993 2.6% 4.5% 3.2% 96.7% 8,216 0.0%

Wyandotte County/Leavenworth $790 $0.913 0.7% 6.3% 2.6% 92.7% 13,386 3.0%

Platte County $829 $0.911 -2.1% 1.5% 2.8% 94.5% 9,580 1.1%

Clay County $843 $0.892 1.3% 3.7% 3.3% 94.9% 16,404 6.0%

Kansas City Metro $882 $0.963 0.6% 3.6% 2.9% 94.8% 149,902 2.5%

Gabe Tovar ccimAssociate | Kansas City

+1 816 556 [email protected]

Bob Galamba sior, ccimSenior Vice President | Kansas City

+1 816 556 [email protected]

featured submarket:PLATTE COUNTY

Source: MPF Research

Submarket Supply (Units)

0

100

200

300

Quarterly Annual

Submarket Annual Rent Change

0.0%

1.0%

2.0%

3.0%

4.0%

92.5%

93.0%

93.5%

94.0%

94.5%

95.0%

95.5%

96.0%

Platte County

Submarket OccupancyKansas City Metro

Submarket Demand (Units)

400

300

200

100

0

-100

400

500

600

700

800

500

600

7005.0%

0

100

200

300

400

500

600

700

800

900

1,000

2013 Q4 2014 Q1 2014 Q2 2014 Q3 2014 Q4 2015 Q1 2015 Q2 2015 Q3 2015 Q4 2016 Q1 2016 Q2 2016 Q3 2016 Q4 2017 Q1

Source: MPF Research

Platte County Supply (Units)

Quarterly Annual

2014 2015 2016 2017201392.5%

93.0%

93.5%

94.0%

94.5%

95.0%

95.5%

96.0%

2013 Q4 2014 Q1 2014 Q2 2014 Q3 2014 Q4 2015 Q1 2015 Q2 2015 Q3 2015 Q4 2016 Q1 2016 Q2 2016 Q3 2016 Q4 2017 Q1Source: MPF Research

Submarket Occupancy

Platte County Kansas City Metro

2014 2015 2016 20172013

-300

-200

-100

0

100

200

300

400

500

600

700

2013 Q4 2014 Q1 2014 Q2 2014 Q3 2014 Q4 2015 Q1 2015 Q2 2015 Q3 2015 Q4 2016 Q1 2016 Q2 2016 Q3 2016 Q4 2017 Q1

Source: MPF Research

Platte County Demand (Units)

Quarterly Annual

2014 2015 2016 20172013

Quarterly Annual

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

2013 Q4 2014 Q1 2014 Q2 2014 Q3 2014 Q4 2015 Q1 2015 Q2 2015 Q3 2015 Q4 2016 Q1 2016 Q2 2016 Q3 2016 Q4 2017 Q1Source: MPF Research

Submarket Annual Rent Change

Platte County Kansas City MetroPlatte County Kansas City Metro

2014 2015 2016 20172013

Source: MPF Research