Embed Size (px)

Citation preview

Colliers International | Kansas City colliersmultifamilyeast.com

KANSAS CITY2Q17 | MULTIFAMILY

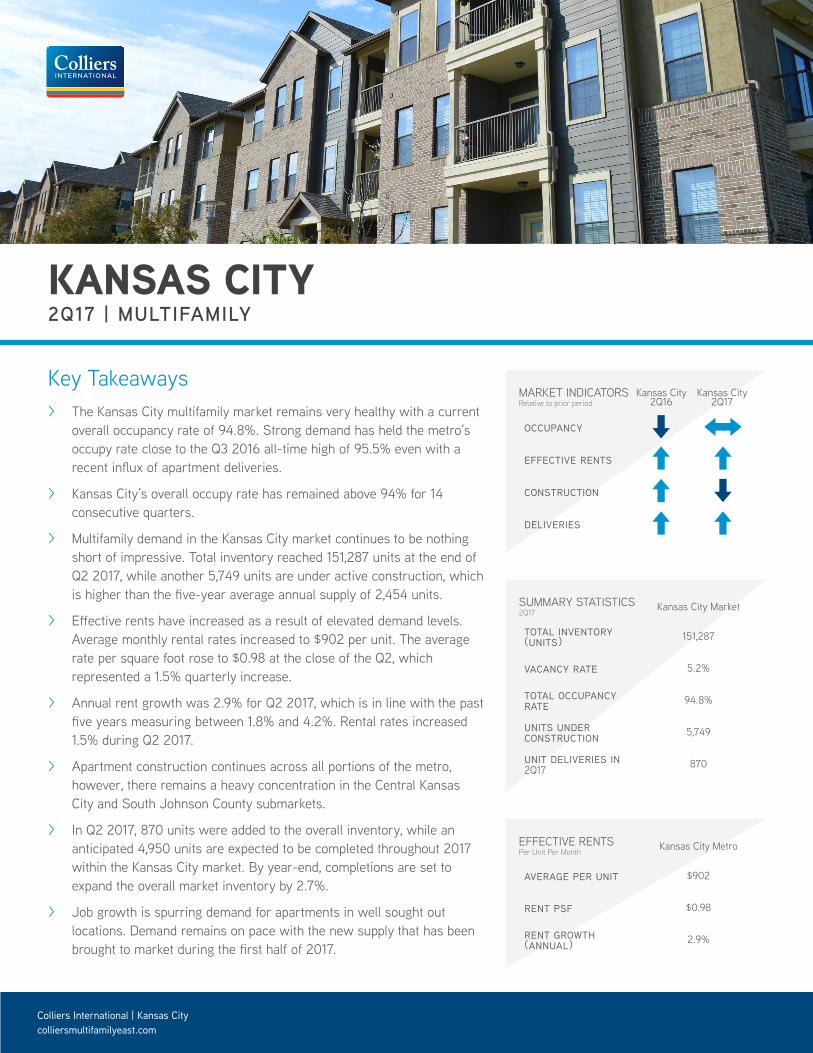

Key Takeaways > The Kansas City multifamily market remains very healthy with a current

overall occupancy rate of 94.8%. Strong demand has held the metro’s occupy rate close to the Q3 2016 all-time high of 95.5% even with a recent influx of apartment deliveries.

> Kansas City’s overall occupy rate has remained above 94% for 14 consecutive quarters.

> Multifamily demand in the Kansas City market continues to be nothing short of impressive. Total inventory reached 151,287 units at the end of Q2 2017, while another 5,749 units are under active construction, which is higher than the five-year average annual supply of 2,454 units.

> Effective rents have increased as a result of elevated demand levels. Average monthly rental rates increased to $902 per unit. The average rate per square foot rose to $0.98 at the close of the Q2, which represented a 1.5% quarterly increase.

> Annual rent growth was 2.9% for Q2 2017, which is in line with the past five years measuring between 1.8% and 4.2%. Rental rates increased 1.5% during Q2 2017.

> Apartment construction continues across all portions of the metro, however, there remains a heavy concentration in the Central Kansas City and South Johnson County submarkets.

> In Q2 2017, 870 units were added to the overall inventory, while an anticipated 4,950 units are expected to be completed throughout 2017 within the Kansas City market. By year-end, completions are set to expand the overall market inventory by 2.7%.

> Job growth is spurring demand for apartments in well sought out locations. Demand remains on pace with the new supply that has been brought to market during the first half of 2017.

MARKET INDICATORSRelative to prior period

Kansas City2Q16

Kansas City2Q17

occupancy

effective rents

construction

deliveries

SUMMARY STATISTICS2Q17

Kansas City Market

total inventory (units) 151,287

vacancy rate 5.2%

total occupancy rate 94.8%

units under construction 5,749

unit deliveries in 2Q17 870

EFFECTIVE RENTSPer Unit Per Month

Kansas City Metro

average per unit $902

rent psf $0.98

rent growth (annual) 2.9%

93.0%

93.5%

94.0%

94.5%

95.0%

95.5%

96.0%

2013 Q4 2014 Q1 2014 Q2 2014 Q3 2014 Q4 2015 Q1 2015 Q2 2015 Q3 2015 Q4 2016 Q1 2016 Q2 2016 Q3 2016 Q4 2017 Q1 2017 Q2Source: MPF Research

Kansas City Metro Occupancy

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

4Q2011

1Q2012

2Q2012

3Q2012

4Q2012

1Q2013

2Q2013

3Q2013

4Q2013

1Q2014

2Q2014

3Q2014

4Q2014

1Q2015

2Q2015

3Q2015

4Q2015

1Q2016

2Q2016

3Q2016

4Q2016

1Q2017

2Q2017

Source: MPF Research

Annual Rent Change ComparisonUnited States Midwest Kansas City

Rental Rates

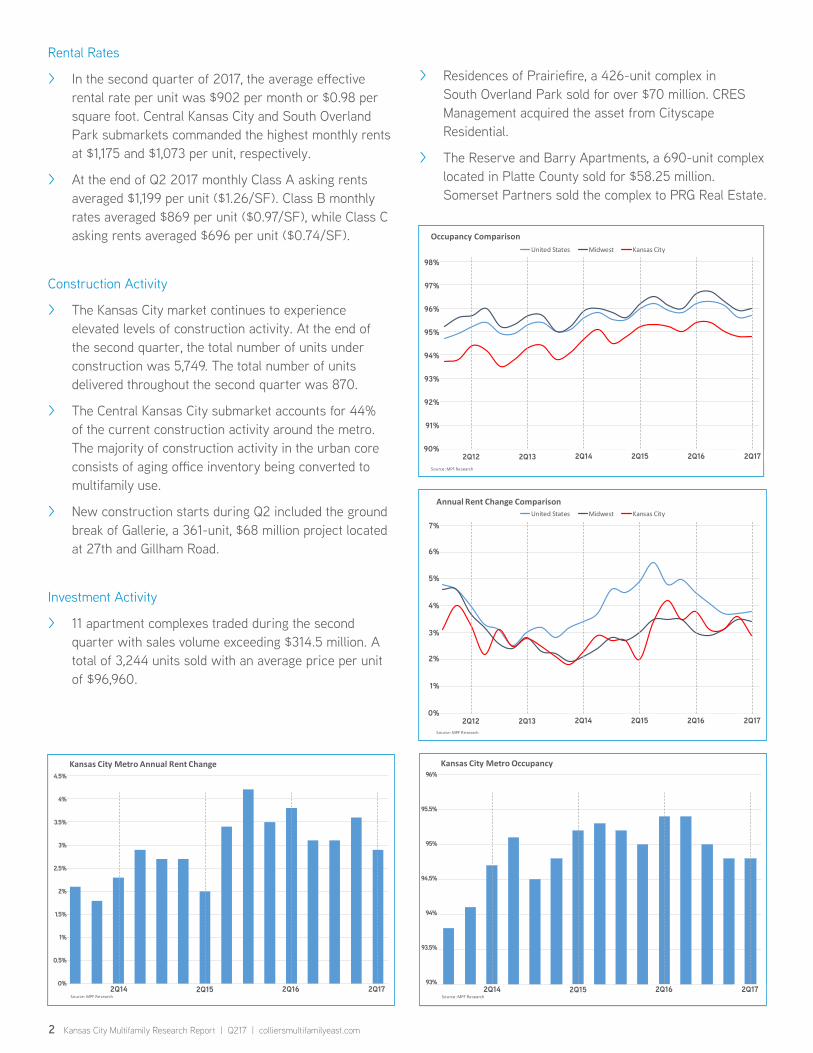

> In the second quarter of 2017, the average effective rental rate per unit was $902 per month or $0.98 per square foot. Central Kansas City and South Overland Park submarkets commanded the highest monthly rents at $1,175 and $1,073 per unit, respectively.

> At the end of Q2 2017 monthly Class A asking rents averaged $1,199 per unit ($1.26/SF). Class B monthly rates averaged $869 per unit ($0.97/SF), while Class C asking rents averaged $696 per unit ($0.74/SF).

Construction Activity

> The Kansas City market continues to experience elevated levels of construction activity. At the end of the second quarter, the total number of units under construction was 5,749. The total number of units delivered throughout the second quarter was 870.

> The Central Kansas City submarket accounts for 44% of the current construction activity around the metro. The majority of construction activity in the urban core consists of aging office inventory being converted to multifamily use.

> New construction starts during Q2 included the ground break of Gallerie, a 361-unit, $68 million project located at 27th and Gillham Road.

Investment Activity

> 11 apartment complexes traded during the second quarter with sales volume exceeding $314.5 million. A total of 3,244 units sold with an average price per unit of $96,960.

2 Kansas City Multifamily Research Report | Q217 | colliersmultifamilyeast.com

90.0%

91.0%

92.0%

93.0%

94.0%

95.0%

96.0%

97.0%

98.0%

4Q2011

1Q2012

2Q2012

3Q2012

4Q2012

1Q2013

2Q2013

3Q2013

4Q2013

1Q2014

2Q2014

3Q2014

4Q2014

1Q2015

2Q2015

3Q2015

4Q2015

1Q2016

2Q2016

3Q2016

4Q2016

1Q2017

2Q2017

Source: MPF Research

Occupancy ComparisonUnited States Midwest Kansas City

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

2013 Q4 2014 Q1 2014 Q2 2014 Q3 2014 Q4 2015 Q1 2015 Q2 2015 Q3 2015 Q4 2016 Q1 2016 Q2 2016 Q3 2016 Q4 2017 Q1 2017 Q2Source: MPF Research

Kansas City Metro Annual Rent Change

> Residences of Prairiefire, a 426-unit complex in South Overland Park sold for over $70 million. CRES Management acquired the asset from Cityscape Residential.

> The Reserve and Barry Apartments, a 690-unit complex located in Platte County sold for $58.25 million. Somerset Partners sold the complex to PRG Real Estate.

2Q12 2Q13 2Q14 2Q15 2Q16 2Q17

7%

6%

5%

4%

3%

2%

1%

0%

98%

97%

96%

95%

94%

93%

92%

91%

2Q12 2Q13 2Q14 2Q15 2Q16 2Q1790%

2Q14 2Q15 2Q16 2Q17

96%

95.5%

95%

94.5%

94%

93.5%

93%2Q14 2Q15 2Q16 2Q17

3.5%

3%

2.5%

2%

1.5%

1%

0.5%

0%

4.5%

4%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2013 Q4 2014 Q1 2014 Q2 2014 Q3 2014 Q4 2015 Q1 2015 Q2 2015 Q3 2015 Q4 2016 Q1 2016 Q2 2016 Q3 2016 Q4 2017 Q1 2017 Q2

Source: MPF Research

Kansas City Metro Supply (Units)

Quarterly Annual

NOTABLE DELIVERIESproperty submarket units avg unit size avg rent psf developer Altitude 970 Platte County 289 1,018 $1,395 $1.49 AG Spanos

East 9 at Pickwick Plaza Central Kansas City 259 550 $1,120 $2.04 Gold Crown Properties, Inc.

The Denton - Phase II Platte County 154 1,025 $1,261 $1.23 NorthPoint Development

3435 Main Central Kansas City 80 593 $1,006 $1.70 Antheus Capital

911 & 915 Broadway Central Kansas City 44 846 $1,142 $1.35 Yarco Development Co.

InterUrban Lofts North Overland Park 41 975 $1,453 $1.49 REAL Property Group, LLC

NOTABLE SALESproperty submarket yr built units price price per unit seller buyerResidences at Prairiefire South Overland Park 2014 426 $70,083,236 $164,515 Cityscape Residential CRES Management LLC

Manor Homes of Arborwalk Lee's Summit/Blue Springs/Raytown 2006 280 $39,124,960 $139,732 Starwood Capital Milestone Apartments

REIT

Sandstone Creek South Overland Park 2001 364 $48,100,000 $132,143 Preferred Apartment Communities DRA Advisors

West End at City Center Shawnee/Lenexa/Mission 2009 309 $31,950,000 $103,398 TA Realty Blackstone

Reserve at Barry Apartments Platte County 1986 690 $58,250,000 $84,420 Somerset Partners PRG Real Estate

The Meadows Shawnee/Lenexa/Mission 1974 434 $28,000,000 $64,516 Banner Property Management

BH Equities LLC/L5 Investments

Carlyle Apartments Shawnee/Lenexa/Mission 1971 436 $27,550,000 $63,188 TriVest McNeil BH Equities LLC/L5 Investments

3 Kansas City Multifamily Research Report | Q217 | colliersmultifamilyeast.com

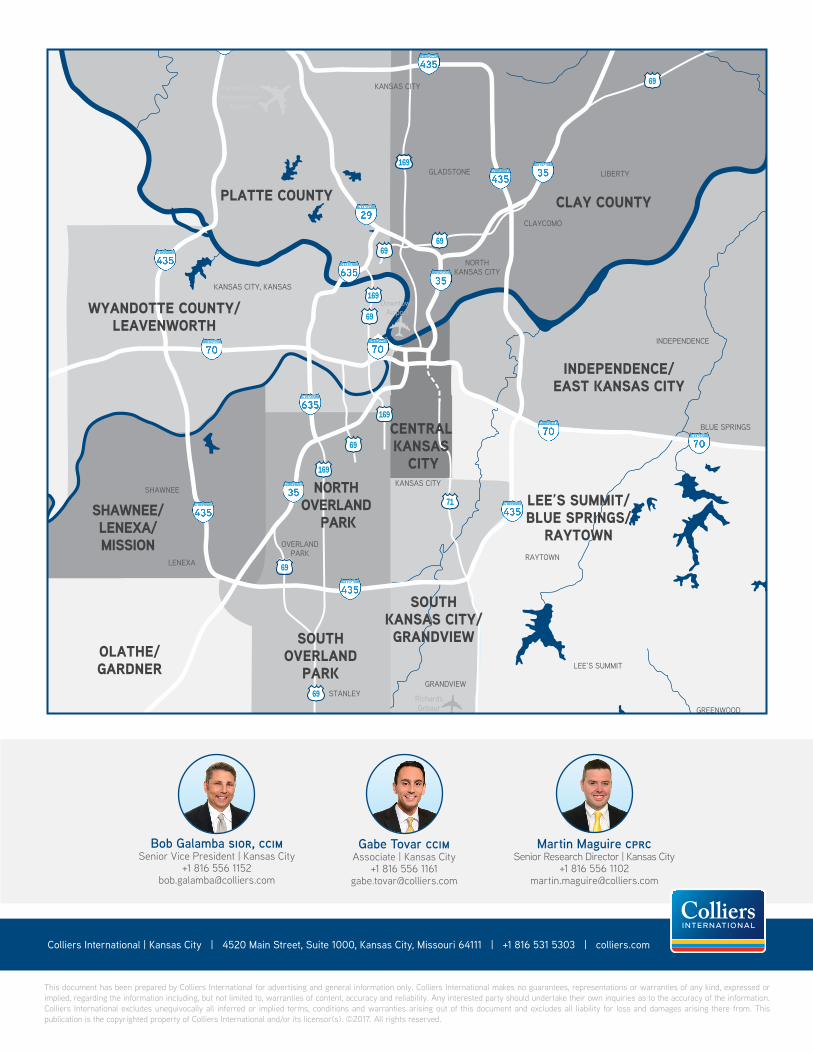

SUBMARKET BREAKDOWN

submarketmonthly

rent rent psfquarterly

rent growthannual rent

growth

five-year avg annual

change occupancyexisting

units

annual inventory change %

Central Kansas City $1,175 $1.36 0.3% 3.0% 3.0% 93.7% 22,605 7.7%

Independence/East Kansas City $747 $0.91 0.5% 2.8% 3.5% 97.1% 13,999 0.0%

Lee's Summit/Blue Springs/Raytown $816 $0.88 3.1% 5.8% 3.1% 94.2% 10,421 3.1%

South Kansas City/Grandview $724 $0.81 0.8% 1.0% 2.4% 93.2% 13,884 0.0%

Shawnee/Lenexa/Mission $932 $1.00 2.1% 4.2% 2.8% 95.6% 14,663 1.6%

North Overland Park $906 $0.97 1.7% 2.8% 2.7% 97.0% 10,639 0.4%

South Overland Park $1,073 $1.10 0.8% 1.5% 2.6% 95.6% 17,104 3.2%

Olathe/Gardner $890 $1.02 1.9% 5.1% 3.2% 96.9% 8,216 0.0%

Wyandotte County/Leavenworth $799 $0.91 2.1% 4.7% 2.8% 95.0% 13,386 3.0%

Platte County $848 $0.94 3.2% 2.3% 2.8% 95.3% 9,580 1.1%

Clay County $868 $0.92 1.1% 2.4% 3.2% 91.6% 16,790 8.4%

Kansas City Metro $902 $0.98 1.5% 2.9% 2.9% 94.8% 151,287 2.9%

-300

700

1,700

2,700

3,700

4,700

5,700

2013 Q4 2014 Q1 2014 Q2 2014 Q3 2014 Q4 2015 Q1 2015 Q2 2015 Q3 2015 Q4 2016 Q1 2016 Q2 2016 Q3 2016 Q4 2017 Q1 2017 Q2

Source: MPF Research

Kansas City Metro Demand (Units)

Quarterly Annual

2Q14 2Q15 2Q16 2Q17

5,700

4,700

3,700

2,700

1,700

700

-3002Q14 2Q15 2Q16 2Q17

3,500

3,000

2,500

2,000

1,000

500

-0

5,000

4,500

4,000

1,500

SOUTHOVERLAND

PARK

CENTRAL KANSAS

CITY

SOUTHKANSAS CITY/GRANDVIEW

LEE’S SUMMIT/BLUE SPRINGS/

RAYTOWN

CLAY COUNTY

WYANDOTTE COUNTY/LEAVENWORTH

NORTH OVERLAND

PARK

Sherman Army Airfield Clay

CountyRegional Airfield

RichardsGebaurAirport

Kansas CityInternational

Airport

DowntownAirport

KANSAS CITY, KANSAS

SHAWNEE

OVERLANDPARK

STANLEYGRANDVIEW

BELTON

PECULIAR

RAYMORE

LEE’S SUMMIT

RAYTOWN

BLUE SPRINGS

INDEPENDENCE

LIBERTY

CLAYCOMO

GLADSTONE

KANSAS CITY

PLATTE CITY

KEARNEY

EXCELSIORSPRINGS

NORTHKANSAS CITY

KANSAS CITY

GREENWOOD

LENEXA

Kansas City MetroOffice Submarkets

Colliers International4520 Main Street, Suite 1000Kansas City, Missouri 64111www.colliers.com

PLATTE COUNTY

SHAWNEE/LENEXA/MISSION

INDEPENDENCE/EAST KANSAS CITY

OLATHE/GARDNER

Martin Maguire cprcSenior Research Director | Kansas City

+1 816 556 [email protected]

Gabe Tovar ccimAssociate | Kansas City

+1 816 556 [email protected]

Bob Galamba sior, ccimSenior Vice President | Kansas City

+1 816 556 [email protected]

Colliers International | Kansas City | 4520 Main Street, Suite 1000, Kansas City, Missouri 64111 | +1 816 531 5303 | colliers.com

This document has been prepared by Colliers International for advertising and general information only. Colliers International makes no guarantees, representations or warranties of any kind, expressed or implied, regarding the information including, but not limited to, warranties of content, accuracy and reliability. Any interested party should undertake their own inquiries as to the accuracy of the information. Colliers International excludes unequivocally all inferred or implied terms, conditions and warranties arising out of this document and excludes all liability for loss and damages arising there from. This publication is the copyrighted property of Colliers International and/or its licensor(s). ©2017. All rights reserved.

![[15] Planetary Geology (10/19/17)miller/teaching/astr120f17/class15.pdf · Maximum height of Mountains •Earth: 8.8 km •Venus: 11 km; surface gravity 0.91 times Earth’s 8.8 km/0.91~10](https://img.pdfslide.us/doc/110x75/5fb83964df9a3259956fc5a7/15-planetary-geology-101917-millerteachingastr120f17-maximum-height.jpg)