Embed Size (px)

Citation preview

Jones Lang LaSalle – Investment Outlook – Q4 2013 1

Russian Real Estate Investment Outlook February 2014

Jones Lang LaSalle – Investment Outlook – Q4 2013 2 Economic sentiment is poor

Source: Jones Lang Lasalle, IMF, Rosstat

30

35

40

45

50

55

60

65

Jan-

05

Jun-

05

Nov

-05

Apr

-06

Sep

-06

Feb

-07

Jul-0

7

Dec

-07

May

-08

Oct

-08

Mar

-09

Aug

-09

Jan-

10

Jun-

10

Nov

-10

Apr

-11

Sep

-11

Feb

-12

Jul-1

2

Dec

-12

May

-13

Oct

-13

Index

Russia PMI Services Russia PMI Manufacturing

PMI (Services and Manufacturing)

Cumulative revisions to 2014-15 GDP growth (bps))

-10

-5

0

5

10

15

20

YoY %

Construction Fixed investment

Construction vs Investment

-150

-100

-50

0

50

100

-12

-10

-8

-6

-4

-2

0

2

4

6

8

YoY %

Industrial production Mining

Infrastructure Manufacturing

Industrial production

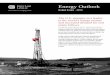

Jones Lang LaSalle – Investment Outlook – Q4 2013 3 Consumption has been the backbone of growth

Source: Jones Lang Lasalle, IMF, Rosstat

Corporate versus retail lending , YoY, %

-20%

-10%

0%

10%

20%

30%

40%

50%

Total lending Retail lending Corporate lending

10%

12%

14%

16%

18%

20%

22%

24%

Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12 Jan-13 Jul-13

Househould debt / annual income

13.5

16.2

9.7

-2.8

4.22.8

7.8

4.0 3.8

-5.0

0.0

5.0

10.0

15.0

20.0

2006 2007 2008 2009 2010 2011 2012 2013E 2014F

-0.2

0.7

0.50.4

0.0

0.5

1.0

1.5

2.0

-0.5

0.0

0.5

1.0

1.5

2.0

Q1 2013 Q2 2013 Q3 2013

%%

Agriculture, hunting and forestry Mineral extraction

Processing industry Construction

Wholesale and retail trade; vehicle repair Financial services

Real estate services Other sectors

GDP growth

Retail sales, YoY, %

Constribution to YoY growth, %

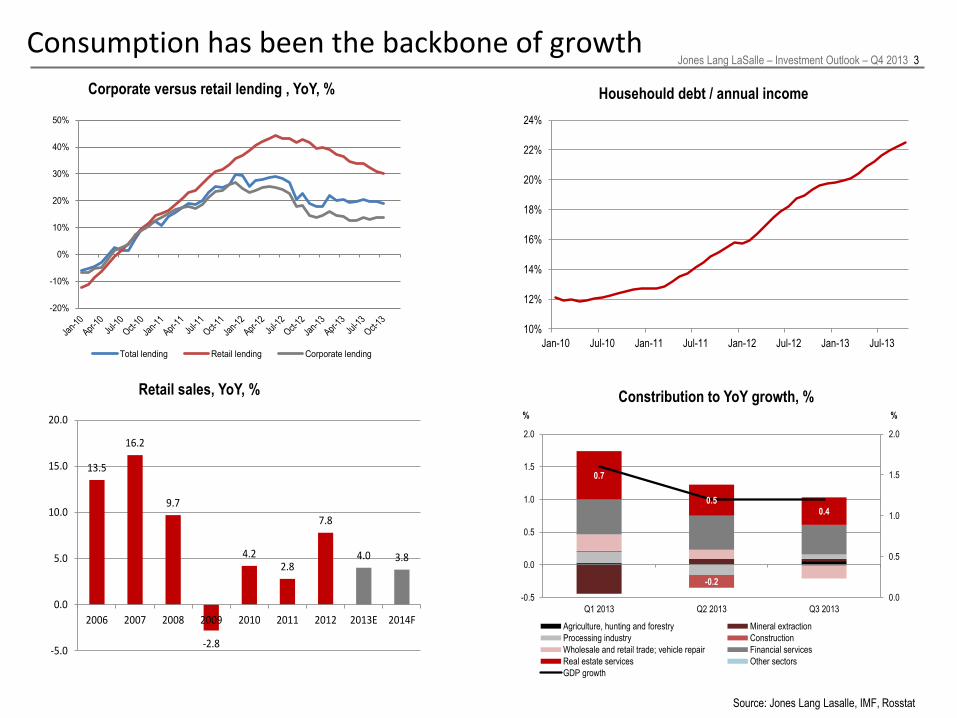

Jones Lang LaSalle – Investment Outlook – Q4 2013 4 Expect rate cuts and a weaker ruble

Source: Jones Lang Lasalle, IMF, Rosstat

9.0

11.9

13.3

8.8 8.8

6.16.6 6.5

5.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

2006 2007 2008 2009 2010 2011 2012 2013E 2014F

CPI growth, YoY, %

6.00

9.00

6.00

5.00 5.25 5.50 5.505.00

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.00

2007 2008 2009 2010 2011 2012 2013E 2014F

Key policy rate

26.3324.55

29.38 30.24 30.4832.20

30.37

33.5035.00

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

2006 2007 2008 2009 2010 2011 2012 2013E 2014F

Ruble/USD

Jones Lang LaSalle – Investment Outlook – Q4 2013 5 Investment market is strong, despite weak GDP

2011 2012 2013

Real estate investment volume, USD m* 8,499 8,772 8,135

Moscow share 69% 88% 84%

St. Petersburg share 27% 10% 6%

* Investment deals, excluding land acquisitions, JVs, direct residential sales to end-users. Source: Jones Lang LaSalle

Investment volume dynamics, USD bn* Investment volume: European comparison, 2012

2.1%

0.9%0.8%

0.4%

0.7%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

0

10

20

30

40

50

60

UK Germany France Russia Poland

Investm

ent vo

lum

e, % o

f GD

P

USD bn

Country Capital8.5

8.1

0.1 0.30.8

4.0 3.9

5.1

3.2

4.9

8.8

7.0

0

2

4

6

8

10

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014F

USD bn

Q4 Q3 Q2 Q1

Jones Lang LaSalle – Investment Outlook – Q4 2013 6

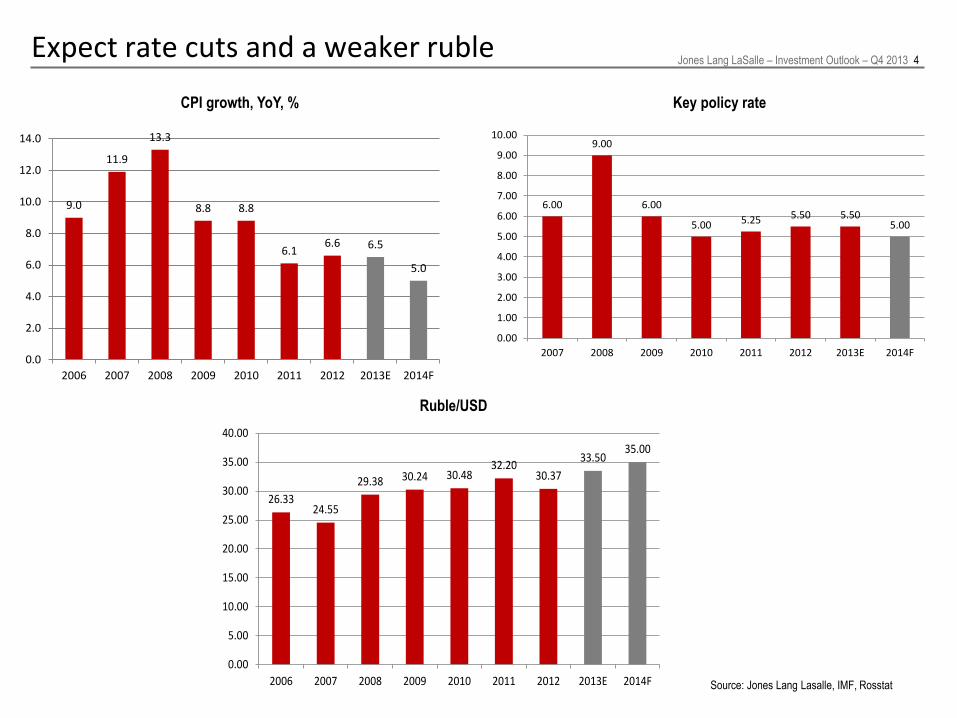

Yield compression unlikely in 2014

Source: Jones Lang LaSalle

Yields, Q4 2013 Moscow St. Petersburg

Office 8.75% 10.0%

Retail 9.0% 10.0%

Warehouse 11.00% 13.0%

8.0%

19.0%

17.0%

11.5%

8.5%

10.0%

12.5%

16.0%

11.0%

14.5%

9.0%

8.75%

6%

8%

10%

12%

14%

16%

18%

20%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Warehouse Shopping centre Office

Jones Lang LaSalle – Investment Outlook – Q4 2013 7

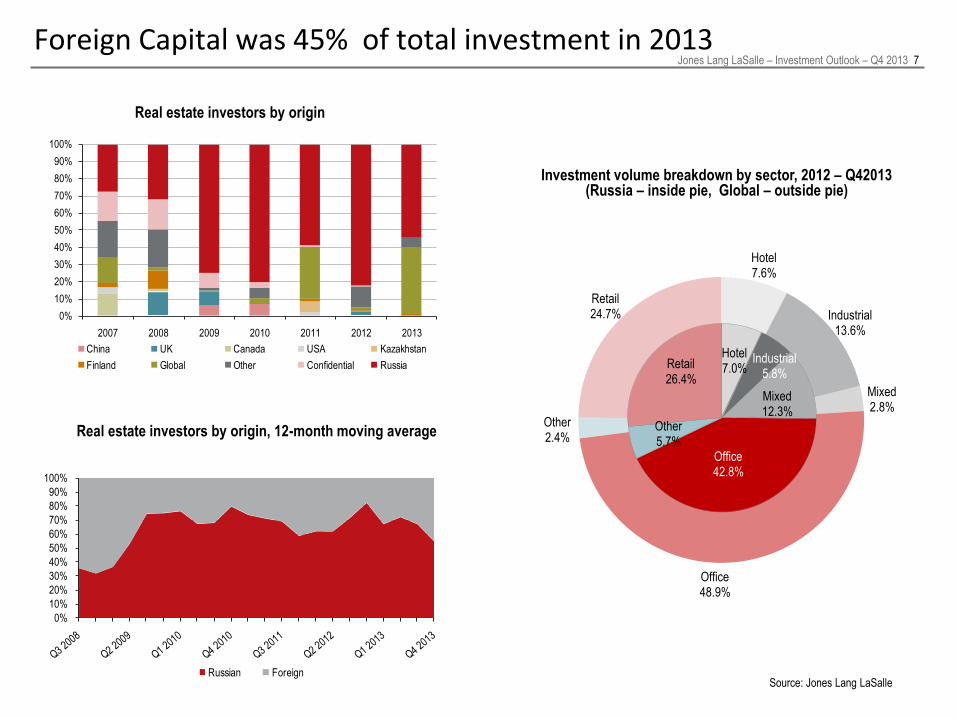

Foreign Capital was 45% of total investment in 2013

Real estate investors by origin

Source: Jones Lang LaSalle

Real estate investors by origin, 12-month moving average

Investment volume breakdown by sector, 2012 – Q42013 (Russia – inside pie, Global – outside pie)

Hotel7.6%

Industrial13.6%

Mixed2.8%

Office48.9%

Other2.4%

Retail24.7%

Hotel7.0%

Industrial5.8%

Mixed12.3%

Office42.8%

Other5.7%

Retail26.4%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2007 2008 2009 2010 2011 2012 2013

China UK Canada USA Kazakhstan

Finland Global Other Confidential Russia

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Russian Foreign

Jones Lang LaSalle – Investment Outlook – Q4 2013 8

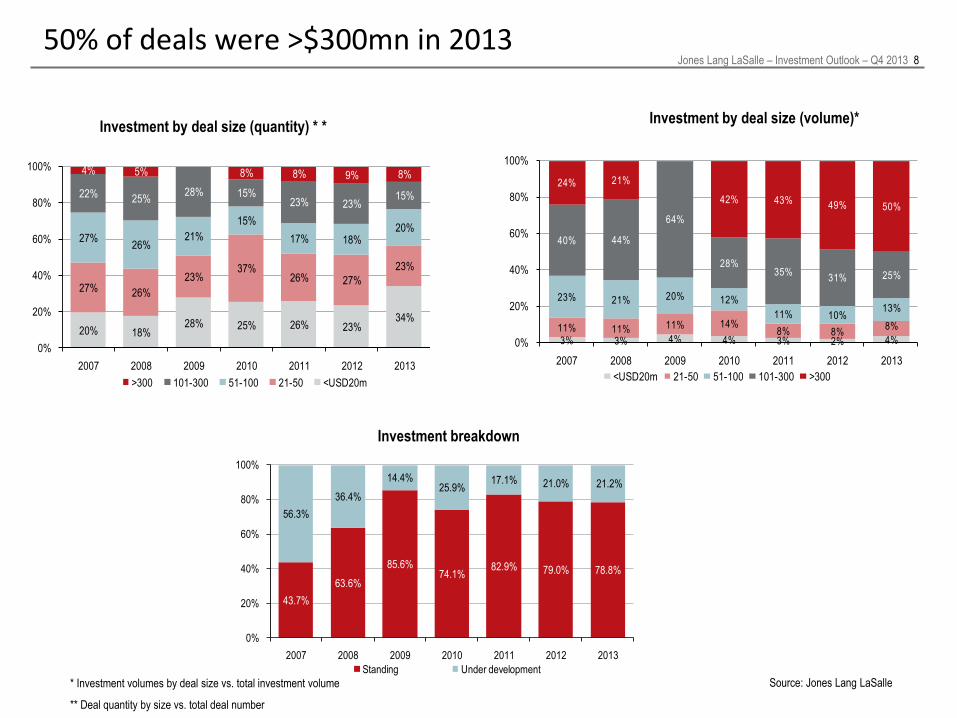

50% of deals were >$300mn in 2013

Source: Jones Lang LaSalle

Investment breakdown

Investment by deal size (volume)* Investment by deal size (quantity) * *

* Investment volumes by deal size vs. total investment volume

** Deal quantity by size vs. total deal number

43.7%

63.6%

85.6%74.1%

82.9% 79.0% 78.8%

56.3%

36.4%

14.4%25.9%

17.1% 21.0% 21.2%

0%

20%

40%

60%

80%

100%

2007 2008 2009 2010 2011 2012 2013

Standing Under development

3% 3% 4% 4% 3% 2% 4%11% 11% 11% 14%

8% 8%8%

23% 21% 20% 12%

11% 10%13%

40% 44%

64%

28%35%

31% 25%

24% 21%

42% 43% 49% 50%

0%

20%

40%

60%

80%

100%

2007 2008 2009 2010 2011 2012 2013

<USD20m 21-50 51-100 101-300 >300

20% 18%28% 25% 26% 23%

34%

27% 26%

23%37%

26% 27%

23%

27%26%

21%

15%

17% 18%20%

22% 25%28% 15%

23% 23%15%

4% 5% 8% 8% 9% 8%

0%

20%

40%

60%

80%

100%

2007 2008 2009 2010 2011 2012 2013

>300 101-300 51-100 21-50 <USD20m

Jones Lang LaSalle – Investment Outlook – Q4 2013 9

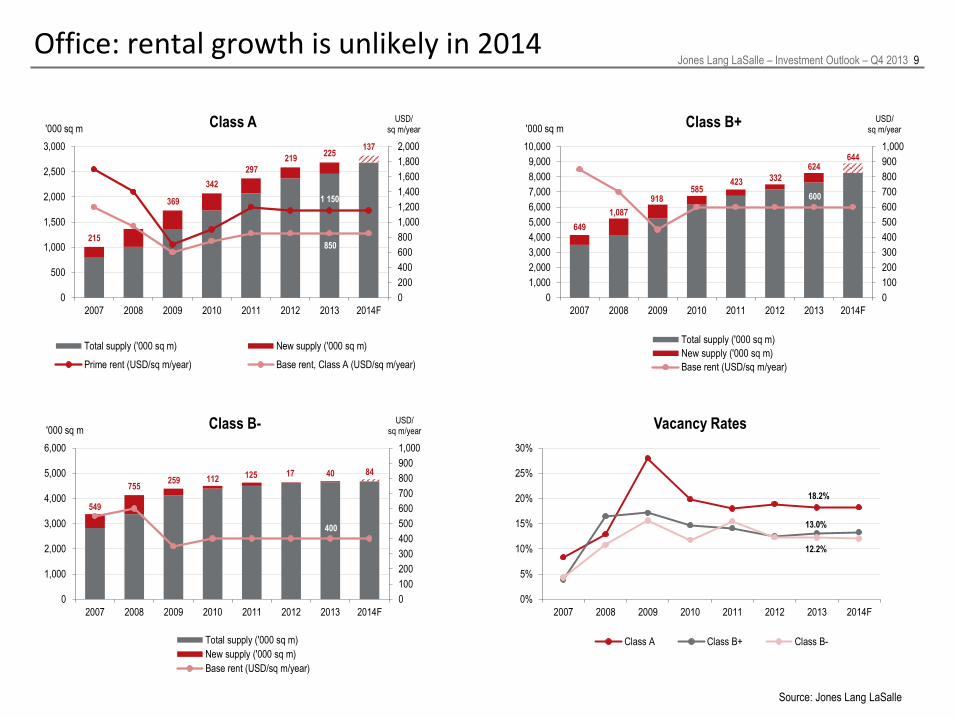

215

369

342

297

219225

137

1 150

850

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

0

500

1,000

1,500

2,000

2,500

3,000

2007 2008 2009 2010 2011 2012 2013 2014F

USD/sq m/year'000 sq m

Class A

Total supply ('000 sq m) New supply ('000 sq m)

Prime rent (USD/sq m/year) Base rent, Class A (USD/sq m/year)

649

1,087

918585

423 332

624644

600

0

100

200

300

400

500

600

700

800

900

1,000

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

2007 2008 2009 2010 2011 2012 2013 2014F

USD/sq m/year'000 sq m

Class B+

Total supply ('000 sq m)

New supply ('000 sq m)

Base rent (USD/sq m/year)

549

755259 112 125 17 40 84

400

0

100

200

300

400

500

600

700

800

900

1,000

0

1,000

2,000

3,000

4,000

5,000

6,000

2007 2008 2009 2010 2011 2012 2013 2014F

USD/sq m/year'000 sq m

Class B-

Total supply ('000 sq m)

New supply ('000 sq m)

Base rent (USD/sq m/year)

18.2%

13.0%

12.2%

0%

5%

10%

15%

20%

25%

30%

2007 2008 2009 2010 2011 2012 2013 2014F

Vacancy Rates

Class A Class B+ Class B-

Office: rental growth is unlikely in 2014

Source: Jones Lang LaSalle

Jones Lang LaSalle – Investment Outlook – Q4 2013 10

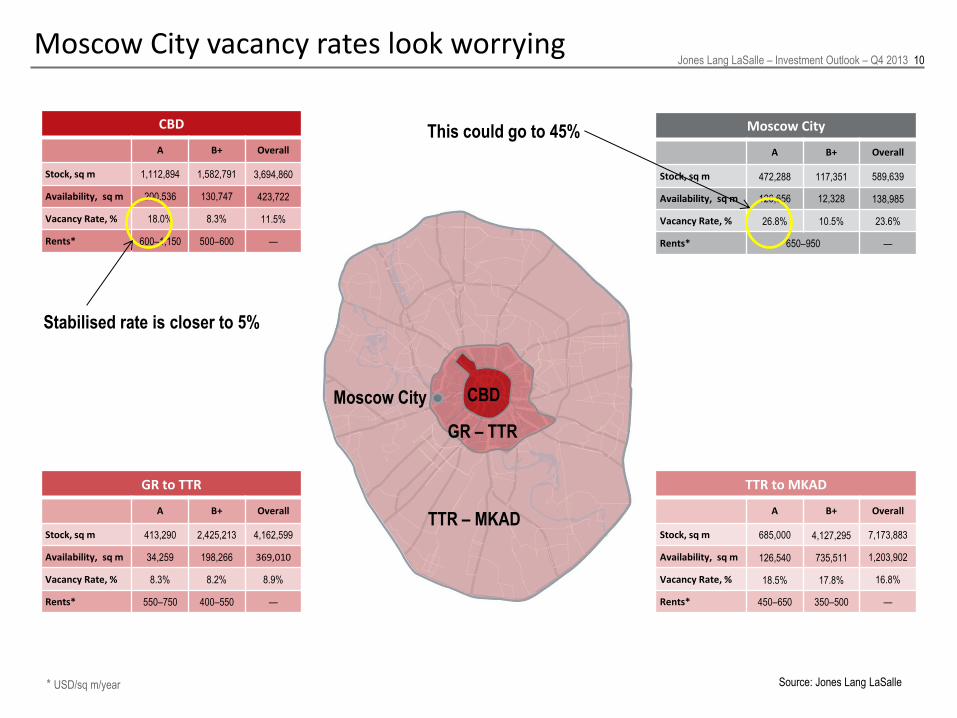

CBD

TTR – MKAD

GR – TTR

Moscow City

CBD

A B+ Overall

Stock, sq m 1,112,894 1,582,791 3,694,860

Availability, sq m 200,536 130,747 423,722

Vacancy Rate, % 18.0% 8.3% 11.5%

Rents* 600–1,150 500–600 —

Moscow City

A B+ Overall

Stock, sq m 472,288 117,351 589,639

Availability, sq m 126,656 12,328 138,985

Vacancy Rate, % 26.8% 10.5% 23.6%

Rents* 650–950 —

GR to TTR

A B+ Overall

Stock, sq m 413,290 2,425,213 4,162,599

Availability, sq m 34,259 198,266 369,010

Vacancy Rate, % 8.3% 8.2% 8.9%

Rents* 550–750 400–550 —

TTR to MKAD

A B+ Overall

Stock, sq m 685,000 4,127,295 7,173,883

Availability, sq m 126,540 735,511 1,203,902

Vacancy Rate, % 18.5% 17.8% 16.8%

Rents* 450–650 350–500 —

Source: Jones Lang LaSalle

Moscow City vacancy rates look worrying

* USD/sq m/year

This could go to 45%

Stabilised rate is closer to 5%

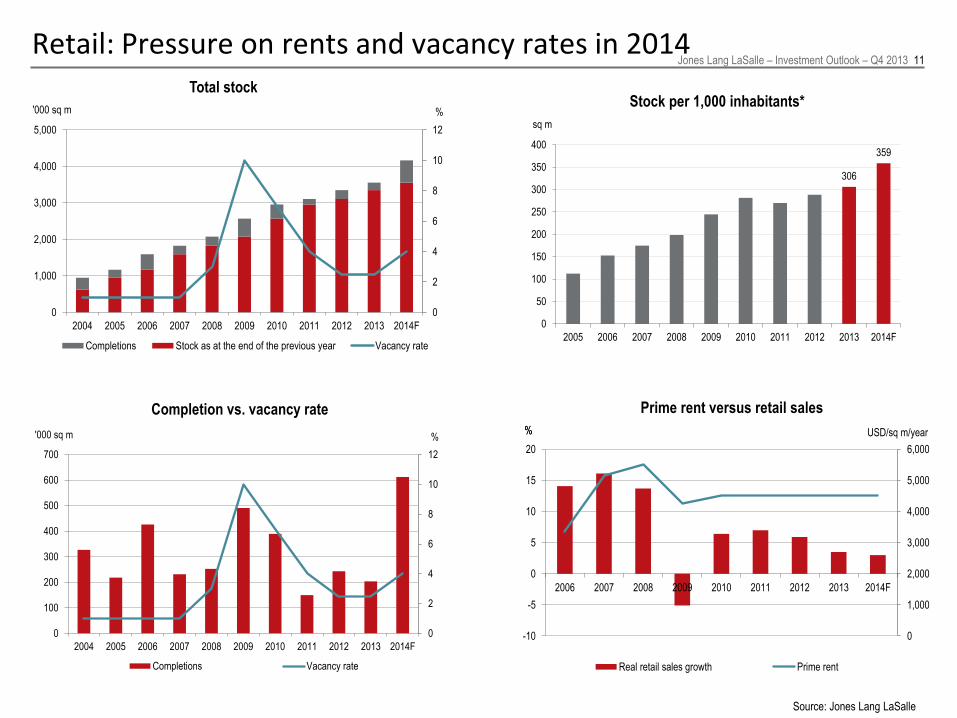

Jones Lang LaSalle – Investment Outlook – Q4 2013 11 Retail: Pressure on rents and vacancy rates in 2014

Source: Jones Lang LaSalle

Total stock Stock per 1,000 inhabitants*

0

2

4

6

8

10

12

0

1,000

2,000

3,000

4,000

5,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014F

%'000 sq m

Completions Stock as at the end of the previous year Vacancy rate

306

359

0

50

100

150

200

250

300

350

400

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014F

sq m

0

2

4

6

8

10

12

0

100

200

300

400

500

600

700

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014F

%'000 sq m

Completions Vacancy rate

Completion vs. vacancy rate Prime rent versus retail sales

0

1,000

2,000

3,000

4,000

5,000

6,000

-10

-5

0

5

10

15

20

2006 2007 2008 2009 2010 2011 2012 2013 2014F

Real retail sales growth Prime rent

%% USD/sq m/year

Jones Lang LaSalle – Investment Outlook – Q4 2013 12

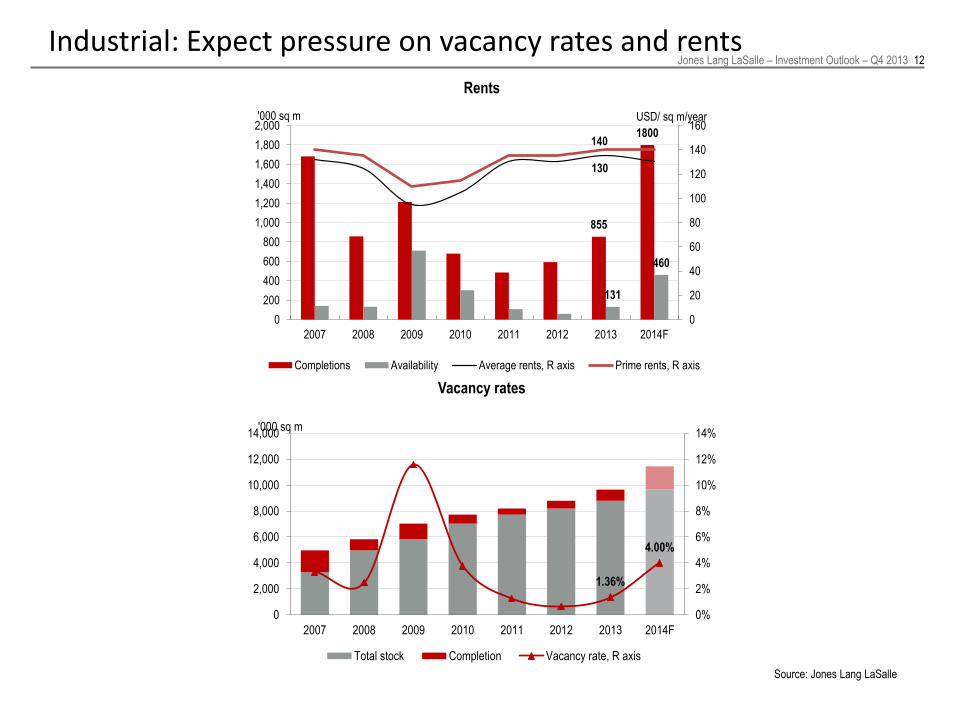

Source: Jones Lang LaSalle

Industrial: Expect pressure on vacancy rates and rents

855

1800

131

460

130

140

0

20

40

60

80

100

120

140

160

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2007 2008 2009 2010 2011 2012 2013 2014F

USD/ sq m/year '000 sq m

Completions Availability Average rents, R axis Prime rents, R axis

1.36%

4.00%

0%

2%

4%

6%

8%

10%

12%

14%

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2007 2008 2009 2010 2011 2012 2013 2014F

'000 sq m

Total stock Completion Vacancy rate, R axis

Vacancy rates

Rents

Jones Lang LaSalle – Investment Outlook – Q4 2013 13

COPYRIGHT © JONES LANG LASALLE IP, INC. 2014. No part of this publication may be reproduced or transmitted in any form or by any means without prior written consent of Jones Lang LaSalle. It is

based on material that we believe to be reliable. Whilst every effort has been made to ensure its accuracy, we cannot offer any warranty that it contains no factual errors. We would like to be told of any such

errors in order to correct them.

Tom Mundy Head of Research Jones Lang LaSalle, Russia & CIS Office: +7 (495) 737 8000 ext. 441 Fax: +7 (495) 737 8011 Mobile: +7 (903) 213-54-37 Email: [email protected] Web: www.joneslanglasalle.ru Jones Lang LaSalle, Russia voted Consultant of the Year in 2004, 2006-2012 and 2013 at Commercial Real Estate Awards