Embed Size (px)

Citation preview

JOHN HESSCHAIRMAN OF THE BOARD CHIEF EXECUTIVE OFFICER

JOHN HESSCHAIRMAN OF THE BOARD CHIEF EXECUTIVE OFFICER

3

StrategyStrategy

CORPORATE

• Grow the company long term through Exploration and Production• Operate Marketing and Refining for near term returns and cash flow

EXPLORATION AND PRODUCTION

• Build a global franchise• Create value through exploration, developments and technology

MARKETING AND REFINING

• Expand Hess brand in Retail and Energy Marketing on East Coast• Maximize free cash flow from refining assets

FINANCE

• Ensure capital availability to fund growth• Deliver first quartile financial and shareholder returns

CORPORATE

• Grow the company long term through Exploration and Production• Operate Marketing and Refining for near term returns and cash flow

EXPLORATION AND PRODUCTION

• Build a global franchise• Create value through exploration, developments and technology

MARKETING AND REFINING

• Expand Hess brand in Retail and Energy Marketing on East Coast• Maximize free cash flow from refining assets

FINANCE

• Ensure capital availability to fund growth• Deliver first quartile financial and shareholder returns

4

SpeakersSpeakers

NameName TitleTitleJoinedHess

JoinedHess

John O’ConnorJohn O’Connor President, Worldwide E&PPresident, Worldwide E&P 20012001

George SandisonGeorge Sandison SVP, ProductionSVP, Production 20012001

Keith HunterKeith Hunter SVP, Major ProjectsSVP, Major Projects 20042004

Bob StrodeBob Strode SVP, Exploration & New VenturesSVP, Exploration & New Ventures 20002000

Borden WalkerBorden Walker President, Marketing & RefiningPresident, Marketing & Refining 19961996

John RiellyJohn Rielly SVP, Chief Financial OfficerSVP, Chief Financial Officer 20012001

Jay WilsonJay Wilson VP, Investor RelationsVP, Investor Relations 20032003

JOHN O’CONNORPRESIDENT

WORLDWIDE E&P

JOHN O’CONNORPRESIDENT

WORLDWIDE E&P

6

E&P Vision in 2002E&P Vision in 2002

Build a global franchise that delivers sustainable growthBuild a global franchise that delivers sustainable growth

7

Goals

Grow Production by 3-5% p.a.

Grow Reserves by 5-8% p.a.

Goals

Grow Production by 3-5% p.a.

Grow Reserves by 5-8% p.a.

Strategy

Exit short-life assets

Acquire interests in long-life properties

Extract more value from core fields

Build an impactful exploration program

Apply innovative technologies

Strategy

Exit short-life assets

Acquire interests in long-life properties

Extract more value from core fields

Build an impactful exploration program

Apply innovative technologies

E&P GoalsE&P Goals and Strategyand Strategy

8

2002 – 2005: Actions Taken2002 – 2005: Actions Taken

Recruited top talent

Instituted a disciplined investment process

Actively high-graded portfolio

Sanctioned 10 profitable new projects

Built attractive exploration program

Recruited top talent

Instituted a disciplined investment process

Actively high-graded portfolio

Sanctioned 10 profitable new projects

Built attractive exploration program

9

Recruited Top TalentRecruited Top Talent

Implemented a global functional organization

Leveraged best practices and technology

Hired top tier industry talent

80% of top 100 E&P leaders new to Hess since 2002

Implemented a global functional organization

Leveraged best practices and technology

Hired top tier industry talent

80% of top 100 E&P leaders new to Hess since 2002

10

Instituted a Disciplined Investment ProcessInstituted a Disciplined Investment Process

Global prioritization of investment opportunities

Multi-stage project review and approval

Formal risk assessment and mitigation

Returns exceed WACC even at $25/bbl WTI

Global prioritization of investment opportunities

Multi-stage project review and approval

Formal risk assessment and mitigation

Returns exceed WACC even at $25/bbl WTI

11

Actively High-Graded PortfolioActively High-Graded Portfolio

6

8

10

02 03 04 05

Reserve Life (Years)

Reserve Life (Years)

ACQUIRED

JDAPangkah

LlanoWest Med

LibyaRussia

ACQUIRED

JDAPangkah

LlanoWest Med

LibyaRussia

DISPOSED

ColombiaHudsonScott

PermianGOM ShelfMont / Arb

Jabung

DISPOSED

ColombiaHudsonScott

PermianGOM ShelfMont / Arb

Jabung

12

Sanctioned 10 Profitable New ProjectsSanctioned 10 Profitable New Projects

ACG Phase 2

ACG Phase 3

Atlantic / Cromarty

GEA Phase 2

JDA Phase 2

ACG Phase 2

ACG Phase 3

Atlantic / Cromarty

GEA Phase 2

JDA Phase 2

Llano

Okume Complex

Pangkah Gas

Phu Horm

Toucan

Llano

Okume Complex

Pangkah Gas

Phu Horm

Toucan

13

Built Attractive Exploration ProgramBuilt Attractive Exploration Program

Exited marginal plays

Farmed into impact opportunities in Gulf of Mexico

Acquired attractive acreage globally

Developed technology capability

Drilled 11 wildcat successes

Exited marginal plays

Farmed into impact opportunities in Gulf of Mexico

Acquired attractive acreage globally

Developed technology capability

Drilled 11 wildcat successes

14

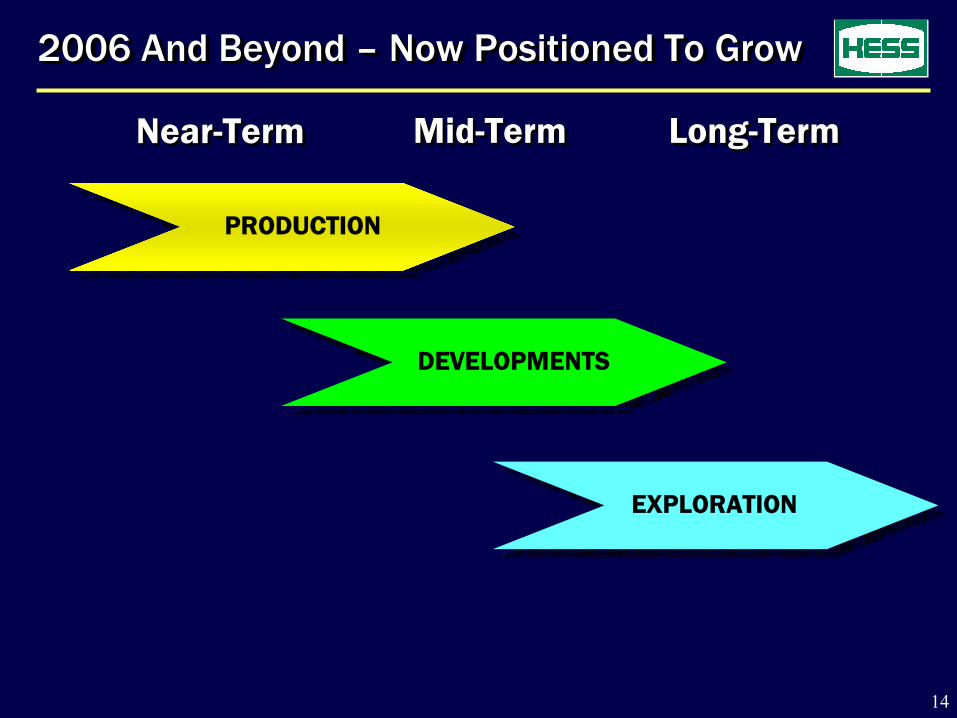

2006 And Beyond – Now Positioned To Grow2006 And Beyond – Now Positioned To Grow

EXPLORATION

Long-TermLong-TermNear-TermNear-Term

PRODUCTION

Mid-TermMid-Term

DEVELOPMENTS

GEORGE SANDISONSENIOR VICE PRESIDENT

PRODUCTION

GEORGE SANDISONSENIOR VICE PRESIDENT

PRODUCTION

16

Global Production Portfolio

UNITED STATES ALGERIA

UNITED KINGDOM

LIBYA

RUSSIA

EQUATORIAL GUINEA

GABON

THAILAND

INDONESIA

MALAYSIA

NORWAYDENMARK

AZERBAIJAN

17

Production BaseProduction Base

0

100

200

300

400

05 06 07 08 09 10

MBOED (Net)MBOED (Net)

2004 Producing Assets2004 Producing Assets

2005 Start-Ups2005 Start-UpsLibyaLibya

Excludes divestitures 05-06

3%

– Modest Decline– Modest Decline

18

Competitive Costs and Margins - 2005Competitive Costs and Margins - 2005

0 10 20

NXY

PCZ

OXY

APA

TLM

MRO

APC

WPL

MUR

NHY

BG

Production Costs $ / BOEProduction Costs $ / BOE

HES

0 10 20

NHY

NXY

BG

TLM

WPL

PCZ

MRO

APA

MUR

APC

OXY

HES

A-Tax Net Margin $ / BOEA-Tax Net Margin $ / BOE

Source: Company FilingsSource: Company Filings Adjusted for A-Tax effects of hedgingAdjusted for A-Tax effects of hedging

19

Producing Asset BaseProducing Asset Base

0

100

200

300

400

05 06 07 08 09 10

Europe

USA

Asia

Africa

Excludes divestitures 05-06

MBOED (Net)MBOED (Net)

20

AsiaAsia

Long-life assets

Substantial growth

$6 / BOE production costs 1Q06

Highly attractive economics

Long-life assets

Substantial growth

$6 / BOE production costs 1Q06

Highly attractive economics

JDAJDA

Phu Horm

PailinPailin

Natuna ANatuna A

PangkahPangkah

JambiMerang

21

JDAJDA

120 MMSCFD net production in 2006

10 discovered fields

Largest reserve holding in portfolio

PSC through 2029

Attractive economics

120 MMSCFD net production in 2006

10 discovered fields

Largest reserve holding in portfolio

PSC through 2029

Attractive economicsBUMIEAST

BULAN

Current production fromCakerawala only

SURIYA

BUMI

10 km

CAKERAWALA

Block A-18

22

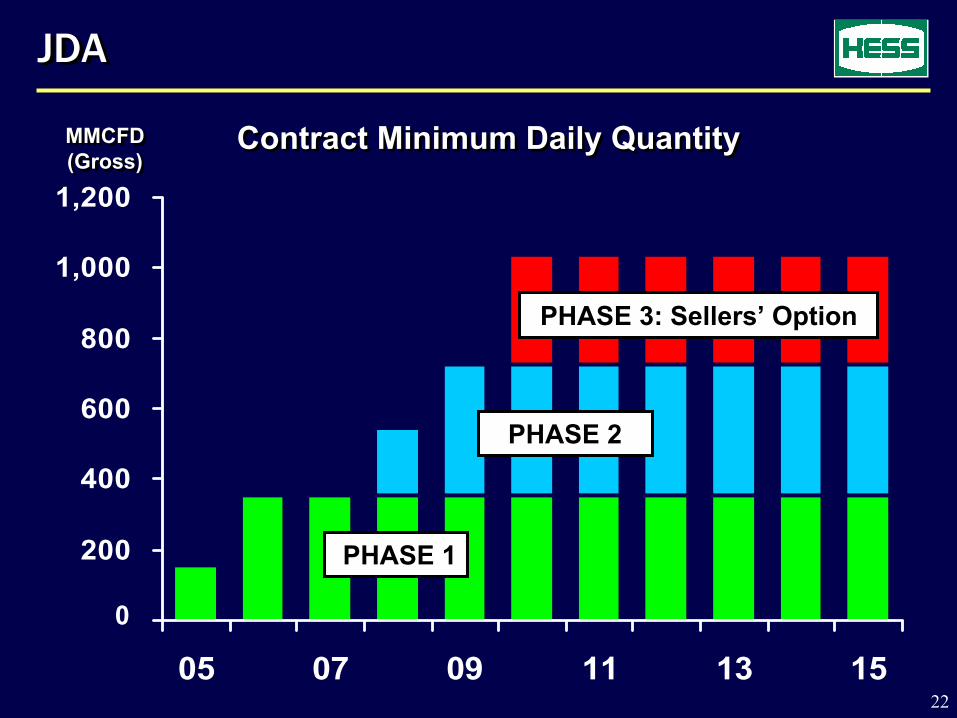

JDAJDA

-

200

400

600

800

1,000

1,200

05 07 09 11 13 15

MMCFD(Gross)MMCFD(Gross)

PHASE 1

PHASE 2

PHASE 3: Sellers’ Option

Contract Minimum Daily QuantityContract Minimum Daily Quantity

0

23

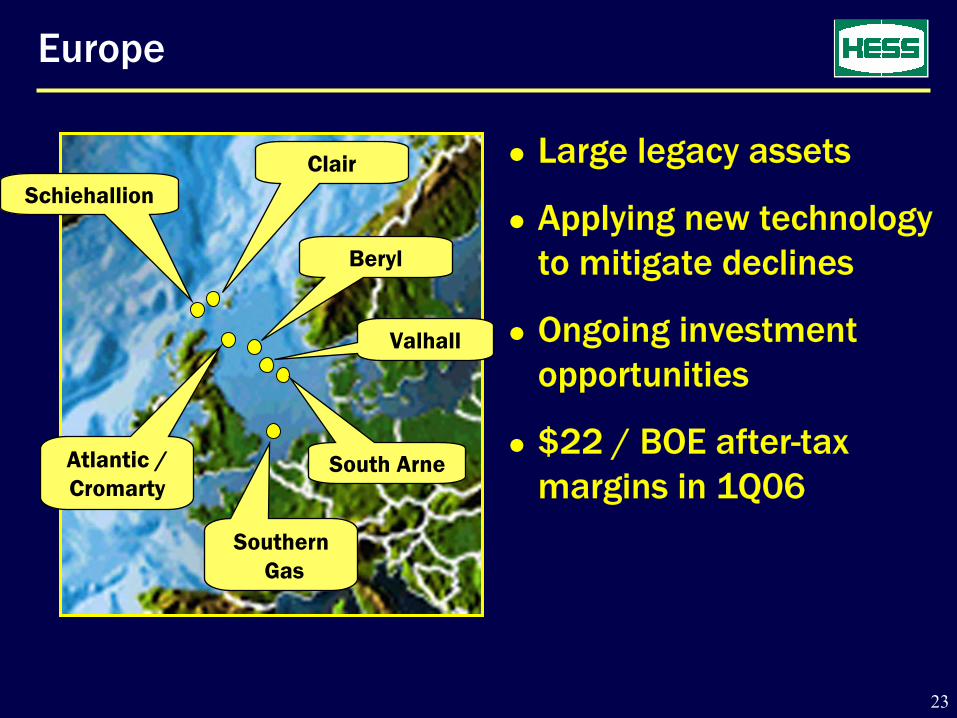

Europe

Large legacy assets

Applying new technology to mitigate declines

Ongoing investment opportunities

$22 / BOE after-tax margins in 1Q06

SouthernGas

Atlantic /Cromarty

Beryl

Valhall

South Arne

ClairSchiehallion

24

ValhallValhall

0

20

40

06 07 08 09 10

28 MBOED net production

40+ years remaining field life

Technology enables growth

Multi-year drilling program

28 MBOED net production

40+ years remaining field life

Technology enables growth

Multi-year drilling program

Base

WaterfloodPotential

MBOED (Net)MBOED (Net)

25

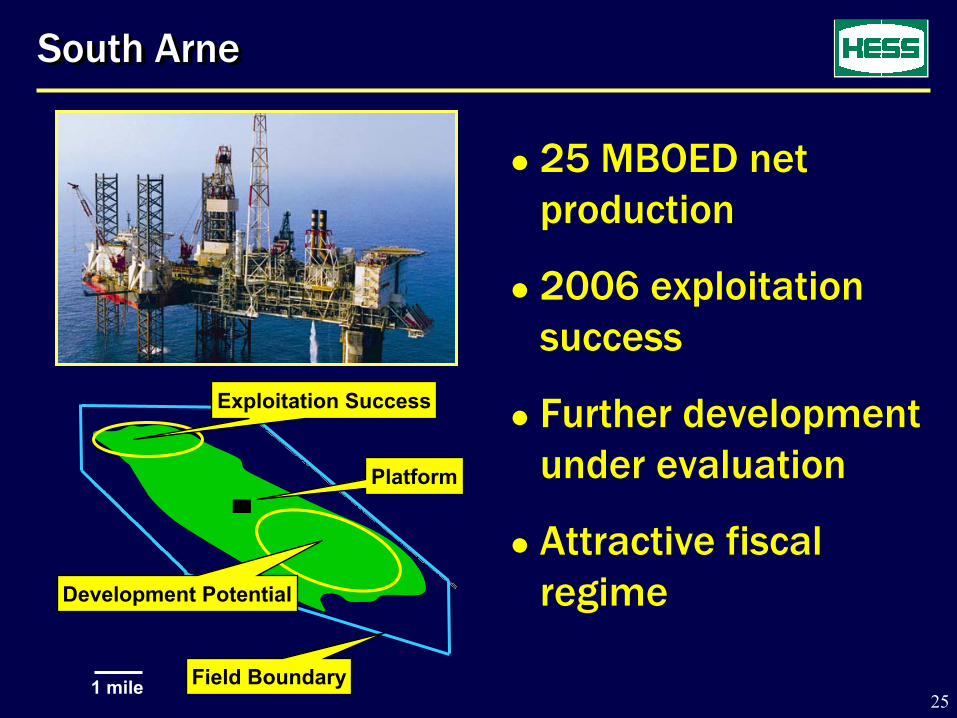

South ArneSouth Arne

25 MBOED net production

2006 exploitation success

Further development under evaluation

Attractive fiscal regime

25 MBOED net production

2006 exploitation success

Further development under evaluation

Attractive fiscal regime

1 mile

Development Potential

Platform

Exploitation Success

Field Boundary

26

Beryl

Nevis

TayTayNess

Linnhe

Katrine

Beryl AreaBeryl Area

20 MBOED net production

Multiple fields

Long-life asset

Successful ongoing exploitation

Attractive returns

20 MBOED net production

Multiple fields

Long-life asset

Successful ongoing exploitation

Attractive returns

27

Atlantic / Cromarty

120 MMSCFD net plateau

First gas May 2006

Short-life, but highly profitableATLANTIC

CROMARTY

St FERGUSTERMINAL

GOLDENEYE

28

Russia

16 MBOED net production

Investment to date of $400 MM

Active drilling program

Phased development

RUSSIARUSSIA

25 miles

Licenses

SamaraVOLGARIVER

29

Positioned in large assets

$7.50 / BOE 1Q06 production costs

Substantial near-term growth

Positioned in large assets

$7.50 / BOE 1Q06 production costs

Substantial near-term growth

AfricaAfrica

Toucan

GEA

Ceiba

EgyptLibyaAlgeria

GabonGabonE.G.E.G.

Waha

30

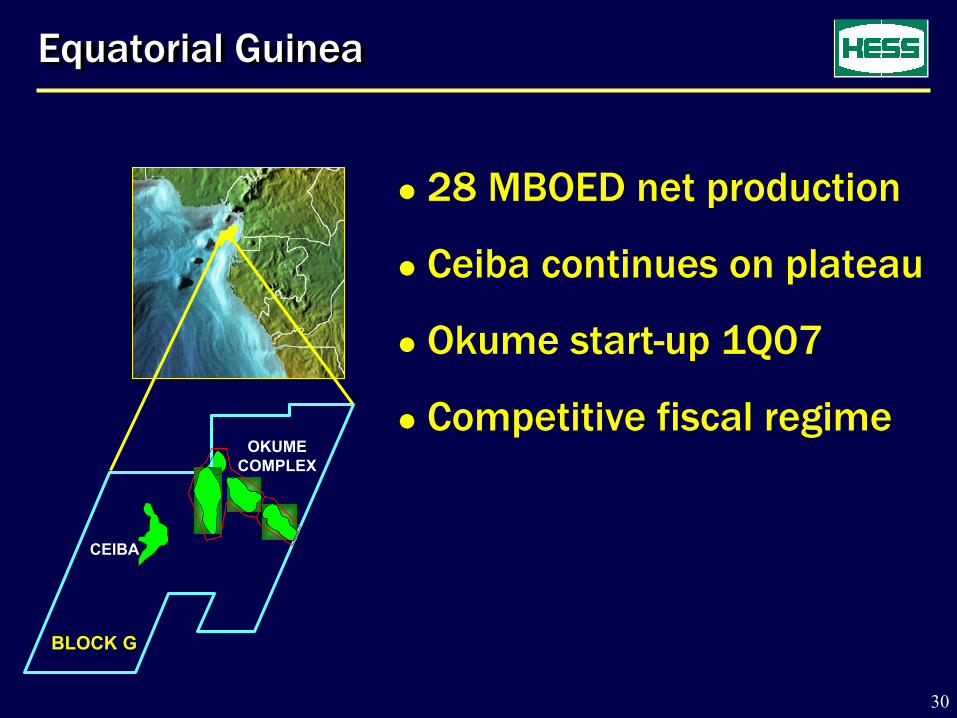

Equatorial Guinea Equatorial Guinea

28 MBOED net production

Ceiba continues on plateau

Okume start-up 1Q07

Competitive fiscal regime

28 MBOED net production

Ceiba continues on plateau

Okume start-up 1Q07

Competitive fiscal regime

BLOCK G

OKUME COMPLEX

CEIBA

31

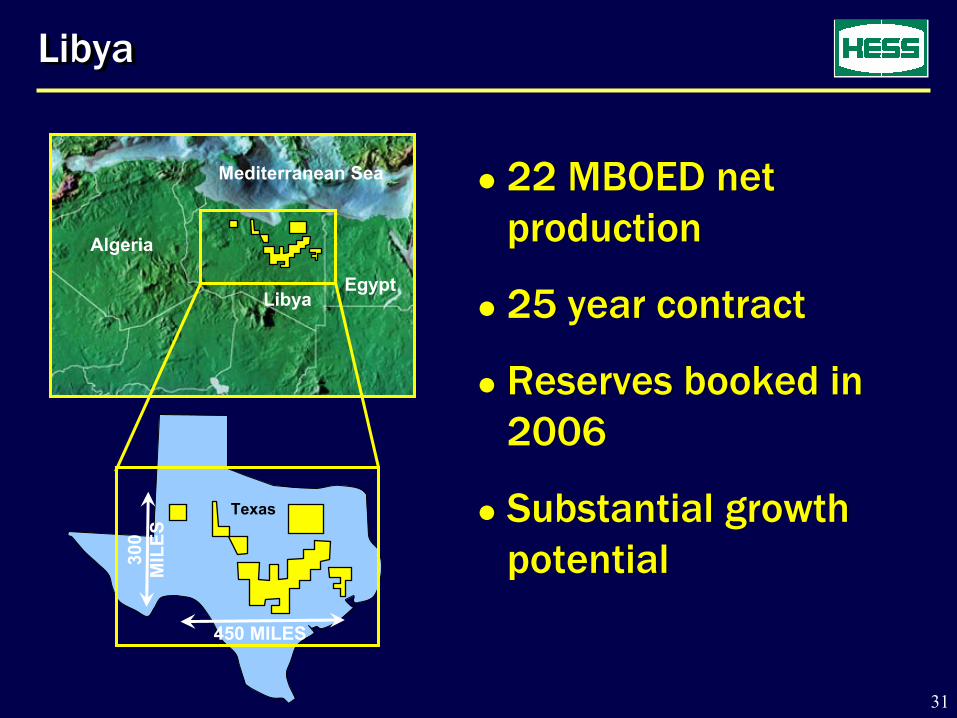

LibyaLibya

22 MBOED net production

25 year contract

Reserves booked in 2006

Substantial growth potential

22 MBOED net production

25 year contract

Reserves booked in 2006

Substantial growth potential

LibyaEgypt

Algeria

Mediterranean Sea

450 MILES

Texas

300

MIL

ES

32

United StatesUnited States

Technology driving sustainability

20% of total Hess production

Moderate declines onshore

$24 / BOE after tax margins in 1Q06

Technology driving sustainability

20% of total Hess production

Moderate declines onshore

$24 / BOE after tax margins in 1Q06

Williston Basin

PermianBasin

Deepwater

33

US DeepwaterUS Deepwater

35 MBOED net production

Active drilling program

$2 / BOE operating costs

Outstanding economics

35 MBOED net production

Active drilling program

$2 / BOE operating costs

Outstanding economics

Louisiana

Garden Banks

PENNSTATE

BALDPATE

LLANO

NORTHWESTERN

CONGER

TULANE

34

Williston BasinWilliston Basin

20 MBOED net; stable production for last 25 years

180,000 acres in Bakken play where technology is key

Evaluating deep gas potential

20 MBOED net; stable production for last 25 years

180,000 acres in Bakken play where technology is key

Evaluating deep gas potential

NEW HESS LEASES

NESSONANTICLINE

EXISTING HESS

LEASES

35

Production Portfolio - SummaryProduction Portfolio - Summary

Material positions in high quality legacy assets

Competitive costs and margins

Moderate decline in production base

Substantial resource base

Development projects drive growth

Material positions in high quality legacy assets

Competitive costs and margins

Moderate decline in production base

Substantial resource base

Development projects drive growth

KEITH HUNTERSENIOR VICE PRESIDENT

MAJOR PROJECTS

37

BMS

PANGKAH

ACG

ATLANTIC/CROMARTY

PHU HORM

OKUME COMPLEX

SHENZI

JDA PHASE 2

WEST MED

Global Developments

SNØHVIT

JAMBI MERANG

PERMIAN EOR

VALHALL REDEV

38

2006 – 2007Atlantic/Cromarty Okume Complex

Phu HormPangkah Gas

SnøhvitACG Phase 2

Strong Slate Of DevelopmentsStrong Slate Of Developments

AppraisalConstruction

2008 - 2009JDA Phase 2ACG Phase 3

ShenziPangkah Oil

Permian EORJambi Merang

West Med Phase 1BMS

2010+Valhall RedevClair Ridge

T BellsSitucheBelud

Bakken

Engineering

39

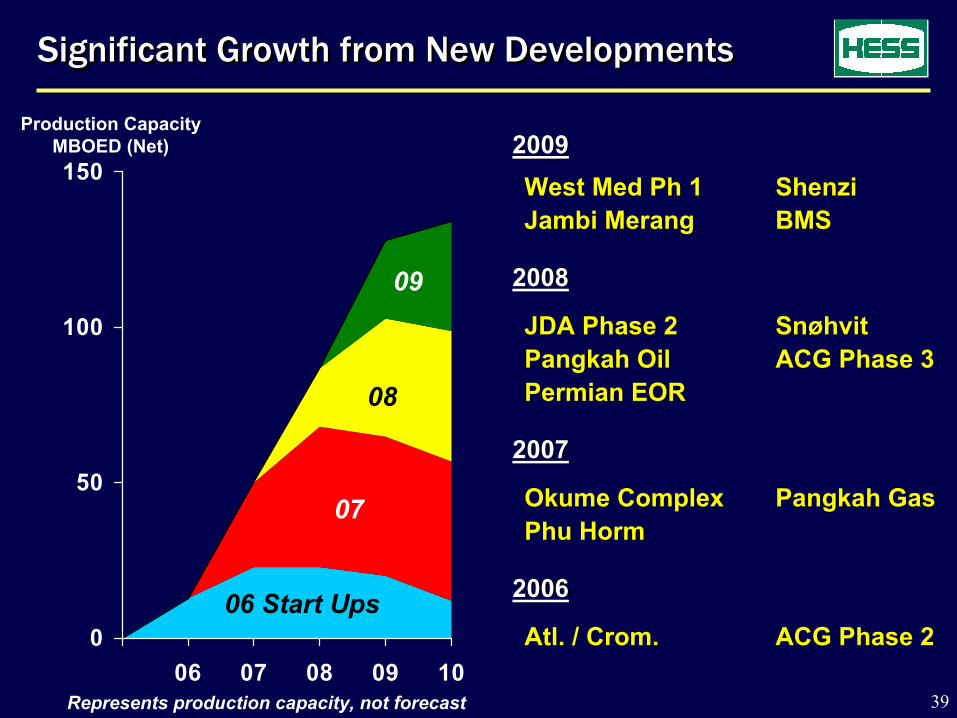

Significant Growth from New DevelopmentsSignificant Growth from New Developments

0

50

100

150

06 07 08 09 10

2009West Med Ph 1 ShenziJambi Merang BMS

2008

JDA Phase 2 SnøhvitPangkah Oil ACG Phase 3Permian EOR

2007

Okume Complex Pangkah Gas Phu Horm

2006

Atl. / Crom. ACG Phase 2

2009West Med Ph 1 ShenziJambi Merang BMS

2008

JDA Phase 2 SnøhvitPangkah Oil ACG Phase 3Permian EOR

2007

Okume Complex Pangkah Gas Phu Horm

2006

Atl. / Crom. ACG Phase 2

Production CapacityMBOED (Net)

06 Start Ups

07

08

09

Represents production capacity, not forecast

40

0 10 20 30 40

NXY

MUR

TLM

PCZ

WPL

APC

NHY

APA

OXY

BG

MRO

FD&A Costs Now Competitive

2000 - 2002 2003 - 2005

0 10

WPL*

MRO

NXY

APC

MUR

TLM

APA

PCZ

OXY

BG

NHY

*WPL is 2001-2003 average

HES

Source: Company Filings

$/BOE

HES

41

Okume Complex

85% WI, Hess operator

$1Bn net investment

125 - 150 MMBOE net resources

First oil in 1Q07

40 MBOED net peak production

85% WI, Hess operator

$1Bn net investment

125 - 150 MMBOE net resources

First oil in 1Q07

40 MBOED net peak production

Okume TLP

42

Okume Complex

Central Processing

Facility

Central Processing

Facility

Satellite 1Satellite 1

Satellite 2Satellite 2

Satellite 3Satellite 3Sendje Ceiba

FPSOSendje Ceiba

FPSO

OkumeMini-TLPOkume

Mini-TLPOveng

Mini-TLPOveng

Mini-TLP

ElonElon

• 43 WELLS (26 Prod, 17 Injection)• 60 MBOED Capacity• 135 MBOED Water Injection• 15 MMSCFD Gas Injection• Full Field Gas Lift

43

Okume: On Time, On Budget

Drilling

Commissioning

Start-Up

Installation

Construction

4Q2Q 3Q 1Q1Q

2006 2007

44

Pangkah

75% WI, Hess operator

$650 MM net investment

80 - 120 MMBOE net resources

First gas in 1H07

First oil in 2H08

20 MBOED net peak production

75% WI, Hess operator

$650 MM net investment

80 - 120 MMBOE net resources

First gas in 1H07

First oil in 2H08

20 MBOED net peak production

PangkahPangkah

45

Liquid StorageLiquid Storage

Central Platform

OPFGas SalesGas Sales

Pangkah

Phase 1 Gas8 Wells150 MMSCFD GasPhase 2 Liquids26 Wells6 MBLPD LPG 25 MBOPD Oil

Phase 1 Gas8 Wells150 MMSCFD GasPhase 2 Liquids26 Wells6 MBLPD LPG 25 MBOPD Oil

East Java

46

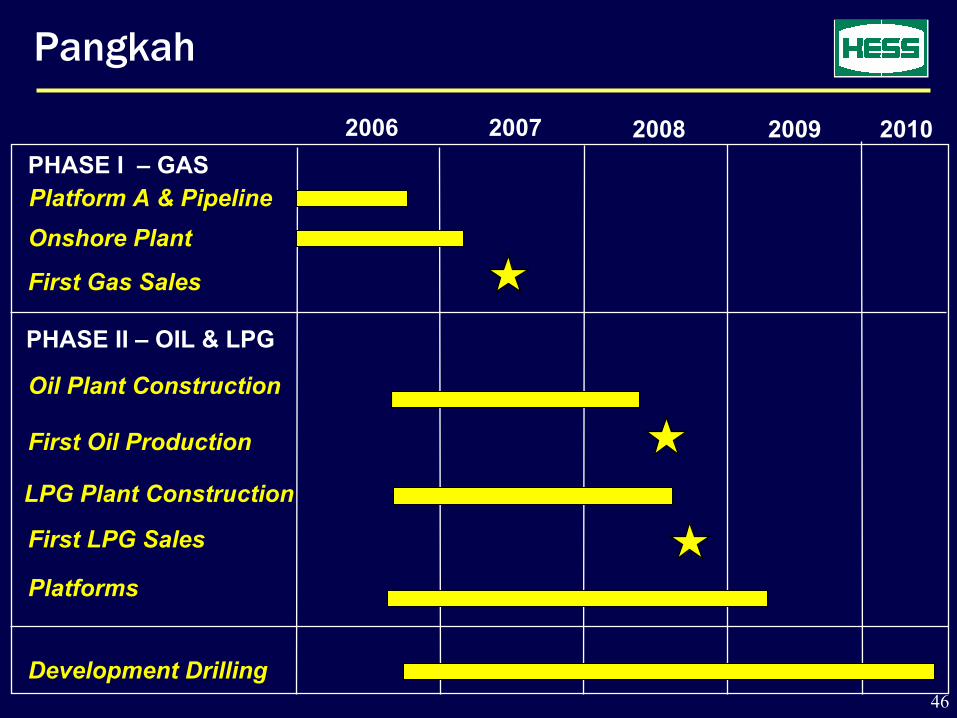

2006 2007 2008 2009 2010PHASE I – GASPlatform A & PipelineOnshore Plant

First Gas Sales

PHASE II – OIL & LPG

Oil Plant Construction

First Oil Production

LPG Plant Construction

First LPG Sales

Platforms

Development Drilling

Pangkah

47

Shenzi

28% WI

$1 Bn net investment

100-150 MMBOE net resources

First oil in 2H09

25 MBOED net peak production

28% WI

$1 Bn net investment

100-150 MMBOE net resources

First oil in 2H09

25 MBOED net peak productionTahiti

Mad DogAtlantis

K2 Area

Puma

Tonga

Neptune

Knotty Head

Miocene Foldbelt

Miocene Fields

Green Canyon Area Shenzi

48

Shenzi

TLP Design

15 subseaproduction wells

100 MBOPD

50-80 MMCFD gas lift

130 MBWD water injection capacity

TLP Design

15 subseaproduction wells

100 MBOPD

50-80 MMCFD gas lift

130 MBWD water injection capacity

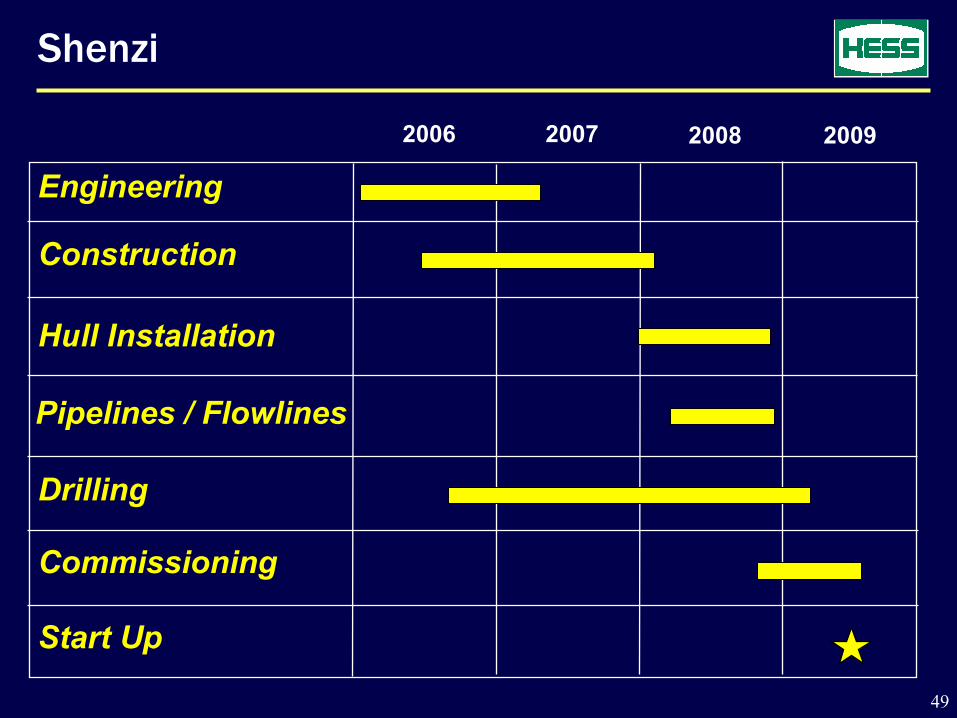

49

Shenzi

2006 2007 2008 2009

Engineering

Construction

Hull Installation

Pipelines / Flowlines

Drilling

Commissioning

Start Up

50

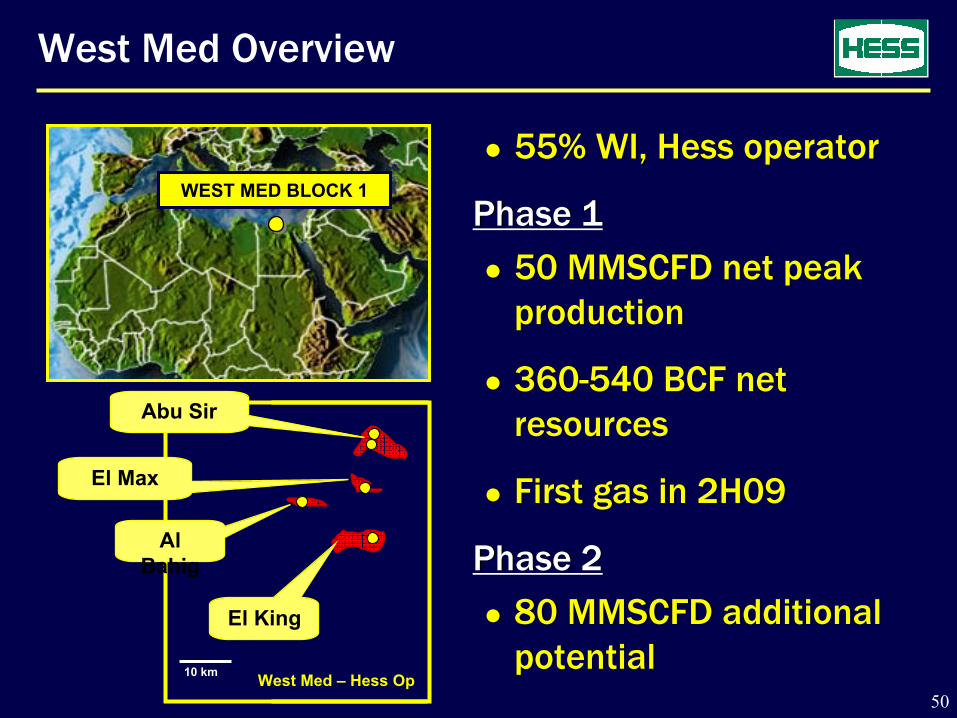

West Med Overview

55% WI, Hess operator

Phase 1

50 MMSCFD net peak production

360-540 BCF net resources

First gas in 2H09

Phase 2

80 MMSCFD additional potential

55% WI, Hess operator

Phase 1

50 MMSCFD net peak production

360-540 BCF net resources

First gas in 2H09

Phase 2

80 MMSCFD additional potential

WEST MED BLOCK 1

10 km West Med – Hess Op

Abu Sir

El Max

Al Bahig

El King

51

West Med

Development of 4 existing fields

3,000’- 4,000’ water depth

6-10 subsea wells

Domestic sales secured

Development plan being finalized

Development of 4 existing fields

3,000’- 4,000’ water depth

6-10 subsea wells

Domestic sales secured

Development plan being finalized

Abu QirGas Plant

Egypt LNG Plant

Abu Sir

El KingAl Bahig

El Max

52

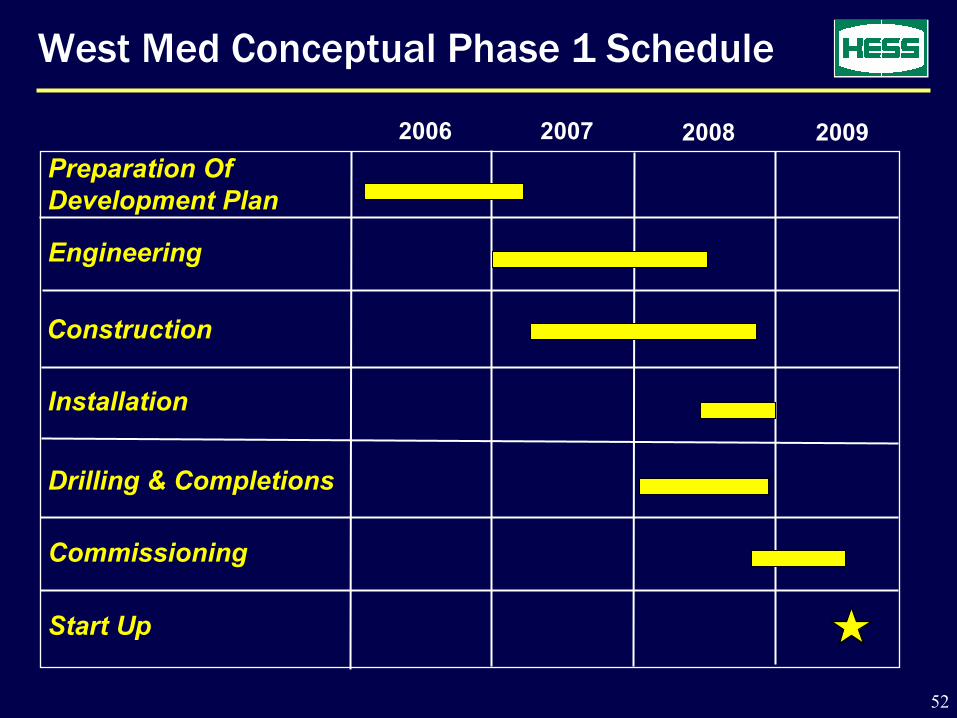

West Med Conceptual Phase 1 Schedule

2006 2007 2008 2009Preparation Of Development Plan

Engineering

Installation

Drilling & Completions

Commissioning

Start Up

Construction

53

Balanced Portfolio of Developments

Hess OperatedBMS

Okume Complex

Pangkah Gas

Pangkah Oil

Permian EOR

Phu Horm

West Med

Hess OperatedBMS

Okume Complex

Pangkah Gas

Pangkah Oil

Permian EOR

Phu Horm

West Med

Outside Operated ACG Phase 2

ACG Phase 3

Atlantic / Cromarty

JDA Phase 2

Jambi Merang

Shenzi

Snøhvit

Valhall Redev

Outside Operated ACG Phase 2

ACG Phase 3

Atlantic / Cromarty

JDA Phase 2

Jambi Merang

Shenzi

Snøhvit

Valhall Redev

54

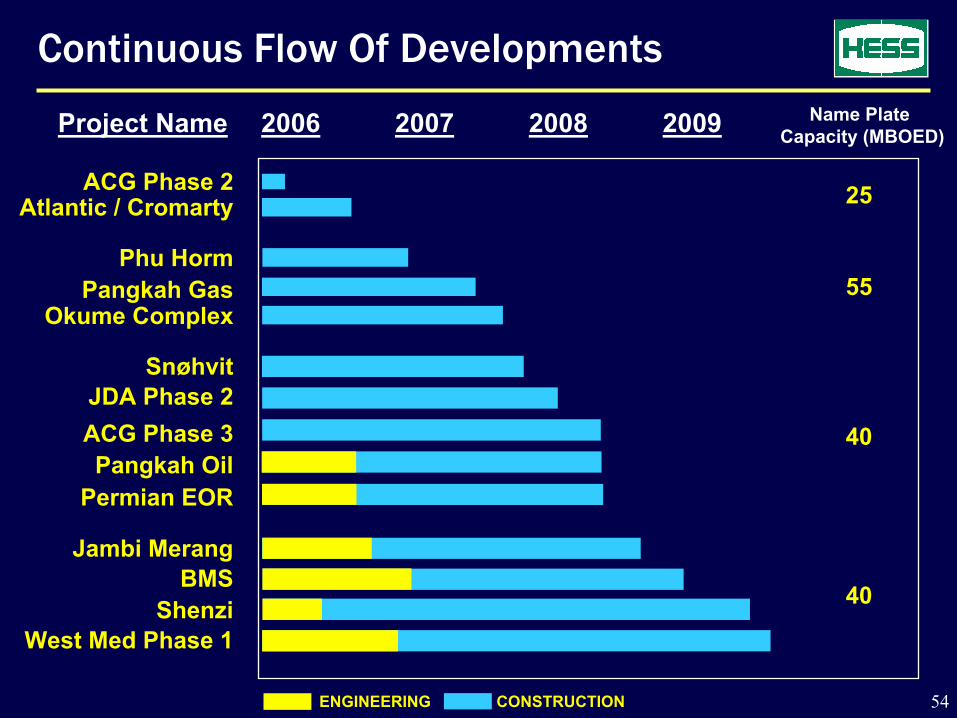

Continuous Flow Of Developments

CONSTRUCTIONENGINEERING

Name Plate Capacity (MBOED)Project Name 2006 2007 2008 2009

ACG Phase 2Atlantic / Cromarty

Phu HormPangkah Gas

Okume Complex

JDA Phase 2ACG Phase 3Pangkah Oil

Snøhvit

Permian EOR

Jambi MerangBMS

ShenziWest Med Phase 1

25

55

40

40

55

Major Projects: Summary

Strong slate of developments

World class project teams assembled

Hess operated projects on time and on budget

Building global execution capability

Exploration success feeds future developments

Strong slate of developments

World class project teams assembled

Hess operated projects on time and on budget

Building global execution capability

Exploration success feeds future developments

BOB STRODESENIOR VICE PRESIDENT

EXPLORATION AND NEW VENTURES

57

RECON ACREAGE PORTFOLIO DRILLING RESULTS

Exploration Strategy

Add resources and create value

Drill 8 – 10 impact wells per year

Apply leading-edge technology

Add resources and create value

Drill 8 – 10 impact wells per year

Apply leading-edge technology

58

Exploration Results: 2002 - 2005

11 wildcat successes

Discovered >400 MMBOE net resources

Created >$2 Bn value at $50/bbl WTI

Added 7.5 million net acres to portfolio

11 wildcat successes

Discovered >400 MMBOE net resources

Created >$2 Bn value at $50/bbl WTI

Added 7.5 million net acres to portfolio

59

-2 0 2 4

BG

TLM

OXY

NHY

MRO

KMG

WPL

NXY

APC

MUR

APA

Industry Value Creation

1999 - 2001 2002 - 2004

-2 0 2 4 6

MRO

APC

NHY

MUR

OXY

APA

TLM

NXY

WPL

BG

KMG

Source: Wood Mackenzie – Exploration Strategy & Performance ~ $ 40/bbl in real 2005 terms

$ Bn $ Bn

HES

HES

60

0

5

10

15

20

25

02 03 04 05

World Class Geoscience Capability

Global expertise in petroleum system basin modeling

Proprietary seismic imaging

Significant increase in 3D seismic processing output

Global expertise in petroleum system basin modeling

Proprietary seismic imaging

Significant increase in 3D seismic processing output

Processing Output (Thousands of 3D Sq. Km)

61

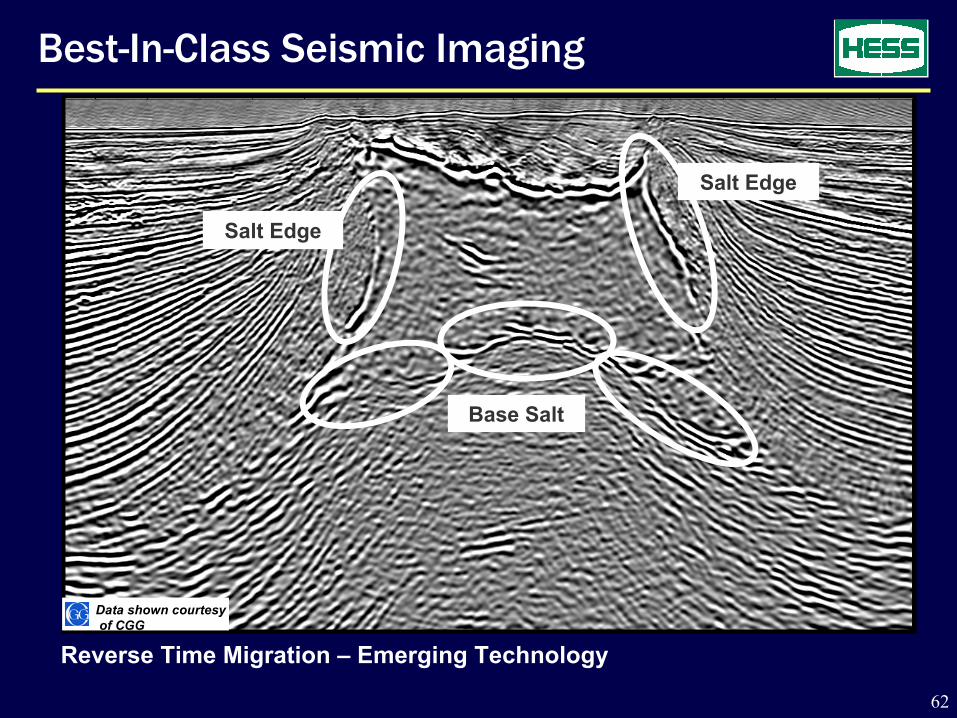

Wave Equation 3D Migration – Recent Technology

Technology Example – Seismic Imaging

Base Salt?

Salt Edge?

Salt Edge?

Data shown courtesyof CGG

Data shown courtesyof CGG

62

Reverse Time Migration – Emerging Technology

Best-In-Class Seismic Imaging

Salt Edge

Salt Edge

Base Salt

Data shown courtesyof CGG

Data shown courtesyof CGG

63

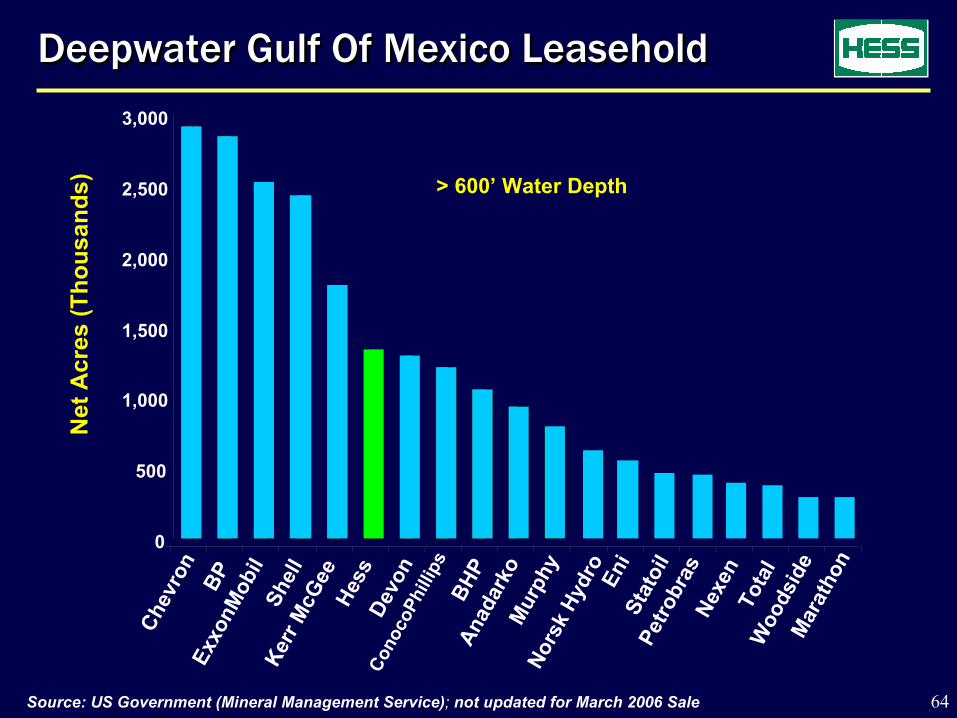

GOM Exploration Strategy

Major petroleum system

Material acreage position

50 named prospects

Deepwater rigs under contract

• Ocean Baroness thru Nov 09

• Noble Max Smith thru May 08

Major petroleum system

Material acreage position

50 named prospects

Deepwater rigs under contract

• Ocean Baroness thru Nov 09

• Noble Max Smith thru May 08

0.0

0.5

1.0

1.5

02 03 04 05 06

Total Net Acres(Million)

64Source: US Government (Mineral Management Service); not updated for March 2006 Sale

Deepwater Gulf Of Mexico LeaseholdDeepwater Gulf Of Mexico Leasehold

> 600’ Water Depth

0

500

1,000

1,500

2,000

2,500

3,000Ch

evro

nBP

Ex

xonM

obil

Shel

lKe

rr M

cGee

Hess

Devo

nCo

noco

Phill

ips

BHP

Anad

arko

Mur

phy

Nors

kHy

dro

Eni

Stat

oil

Petro

bras

Nexe

nTo

tal

Woo

dsid

eM

arat

hon

Net

Acr

es (T

hous

ands

)

65

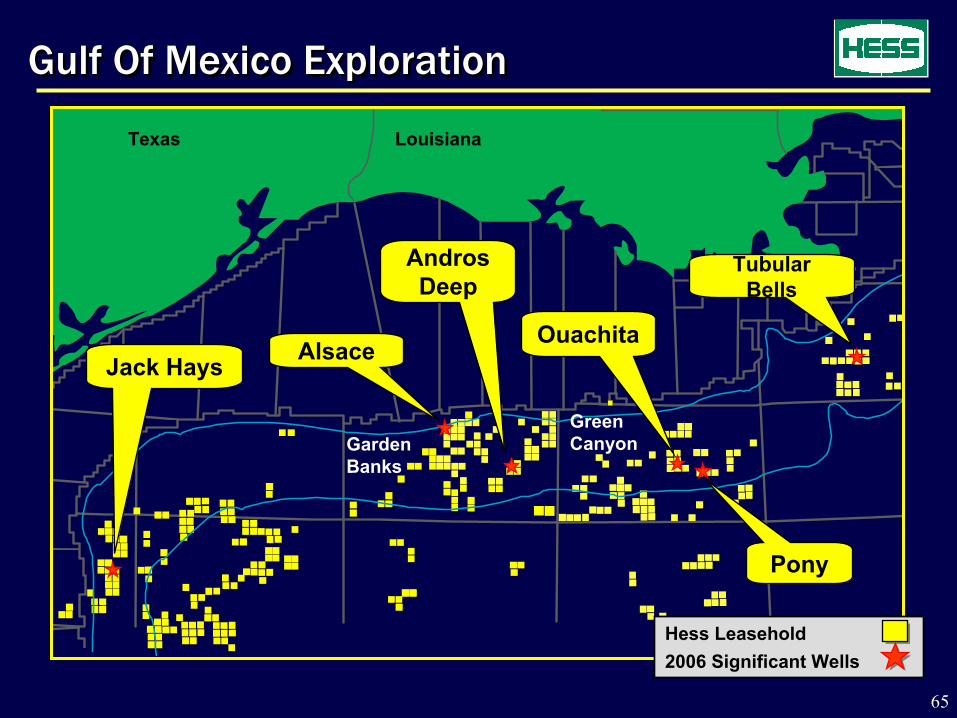

Gulf Of Mexico ExplorationGulf Of Mexico Exploration

Hess Leasehold2006 Significant Wells

Texas Louisiana

Garden Banks

Green Canyon

Jack Hays Alsace

AndrosDeep

Ouachita

Pony

Tubular Bells

66

Regional View – Miocene FoldbeltRegional View – Miocene Foldbelt

Tahiti

Mad DogPuma

Knotty Head

Miocene FoldbeltSeismic Line

15 Miles

A

B

Hess Leasehold2006 Key WellsMiocene Fields

Shenzi

Atlantis

Pony

Vancouver

Ouachita

Data shown courtesyof CGG

Data shown courtesyof CGG

67

Hess Prospects on TrendHess Prospects on Trend

Pony Knotty Head TahitiOuachitaVancouver

SaltSaltSaltSalt

SaltSalt

CretaceousCretaceous

Lower MioceneLower MioceneMiddle MioceneMiddle Miocene

Two significant discoveries (Tahiti and Knotty Head) on trend with three Hess prospects

AA BB

Data shown courtesyof CGG

Data shown courtesyof CGG

68

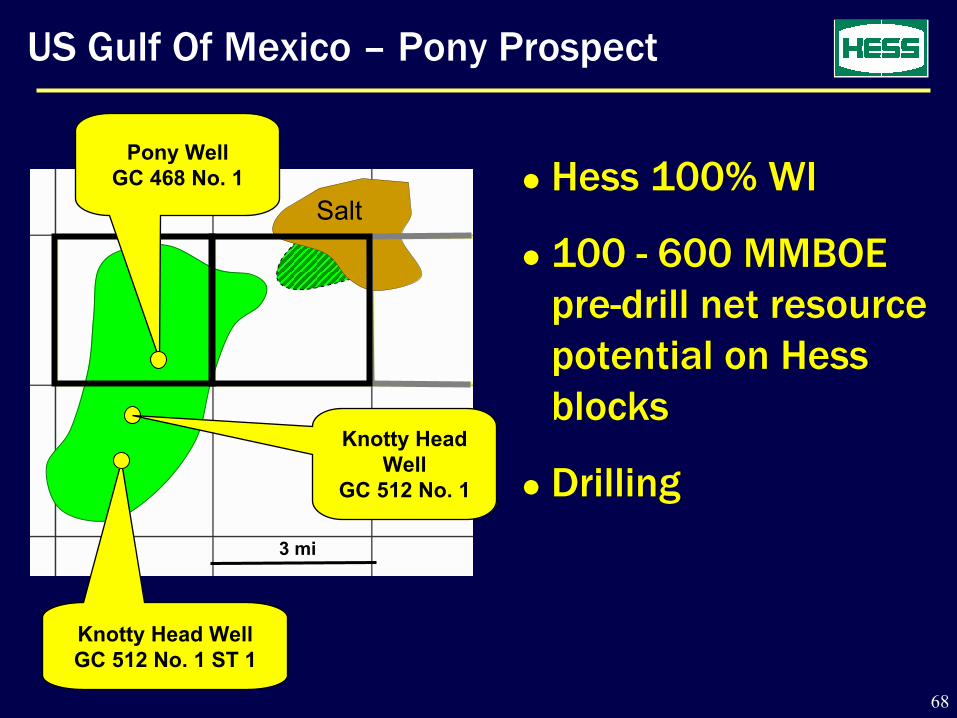

US Gulf Of Mexico – Pony Prospect

Hess 100% WI

100 - 600 MMBOE pre-drill net resource potential on Hess blocks

Drilling

Hess 100% WI

100 - 600 MMBOE pre-drill net resource potential on Hess blocks

Drilling

Salt

3 mi

Knotty Head WellGC 512 No. 1 ST 1

Pony WellGC 468 No. 1

Knotty Head Well

GC 512 No. 1

69

US Gulf Of Mexico – Ouachita Prospect

• Hess 66.6% WI

• 100 – 400 MMBOEpre-drill gross resource potential

•Middle & Lower Miocene objectives

• Drilling

OuachitaGC 376 No. 1

3 miles

Salt

70

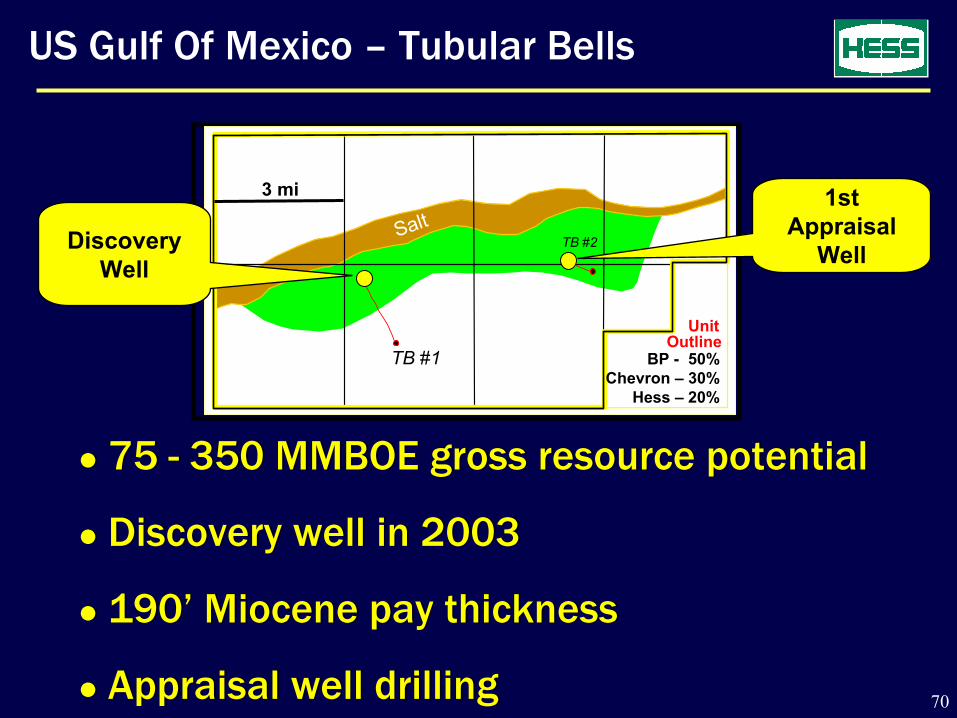

US Gulf Of Mexico – Tubular Bells

75 - 350 MMBOE gross resource potential

Discovery well in 2003

190’ Miocene pay thickness

Appraisal well drilling

75 - 350 MMBOE gross resource potential

Discovery well in 2003

190’ Miocene pay thickness

Appraisal well drilling

3 Miles3 MilesBP - 50%

Chevron – 30%Hess – 20%

TB #1 MC 727 #1

Salt

Discovery Well

Discovery Well

1st Appraisal WellSpudded April 2006

1st Appraisal WellSpudded April 2006

UnitOutline

MC 725MC 724 MC 726 MC 727

MC 682 MC 683MC 681MC 680

TB #2

TB #1

Salt

UnitOutline

TB #2Discovery Well

1st Appraisal

Well

BP - 50%Chevron – 30%

Hess – 20%

3 mi

71

North Africa Exploration Strategy

Major petroleum systems

Significant position established in key plays

Multiple material prospects

Major petroleum systems

Significant position established in key plays

Multiple material prospects

Total Net Acres (Million)

0

5

10

02 03 04 05 06

AlgeriaAlgeria LibyaLibya EgyptEgypt

Hess AcreageHess Acreage

Blks 428, 429Block 54

West Med

N. Red Sea

72

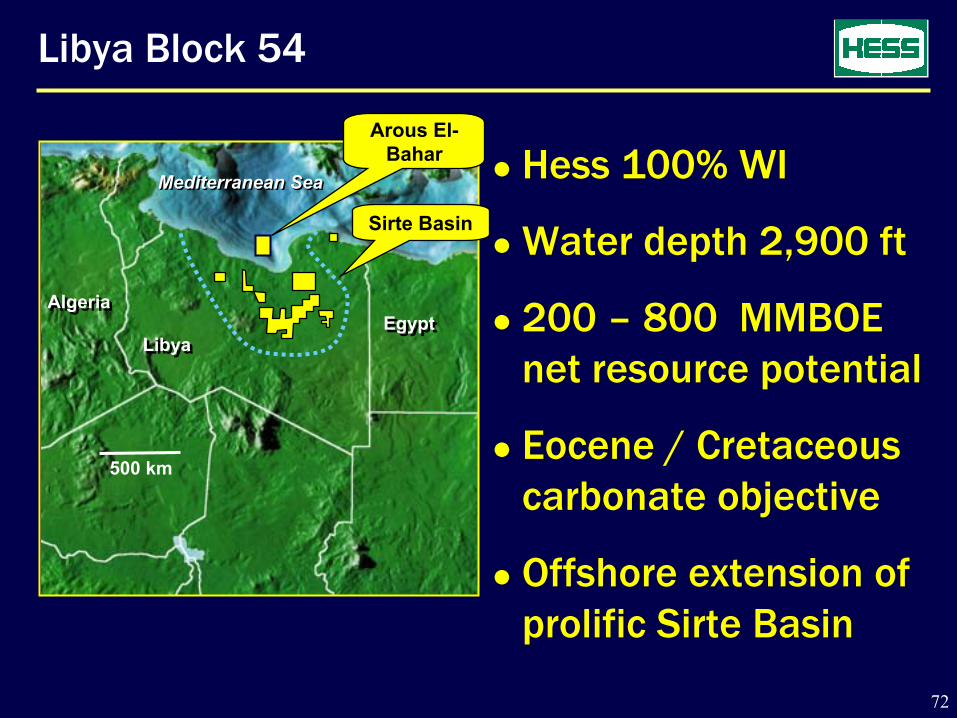

Libya Block 54

Hess 100% WI

Water depth 2,900 ft

200 – 800 MMBOEnet resource potential

Eocene / Cretaceous carbonate objective

Offshore extension of prolific Sirte Basin

Hess 100% WI

Water depth 2,900 ft

200 – 800 MMBOEnet resource potential

Eocene / Cretaceous carbonate objective

Offshore extension of prolific Sirte Basin

500 km

LibyaLibyaEgyptEgypt

AlgeriaAlgeria

Mediterranean SeaMediterranean Sea

Arous El-Bahar

Sirte Basin

73

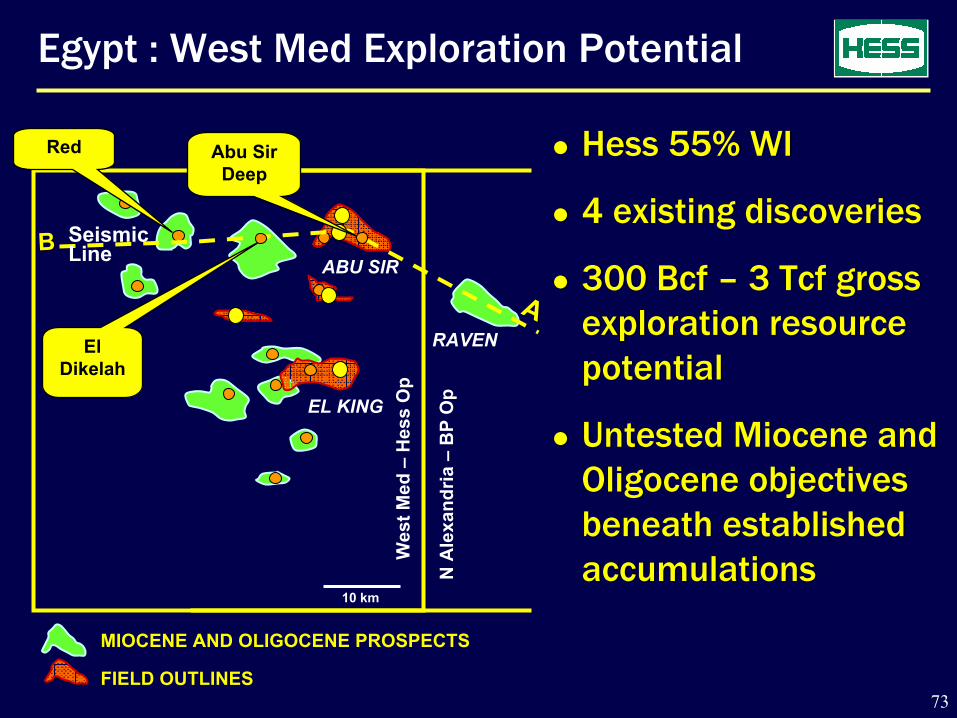

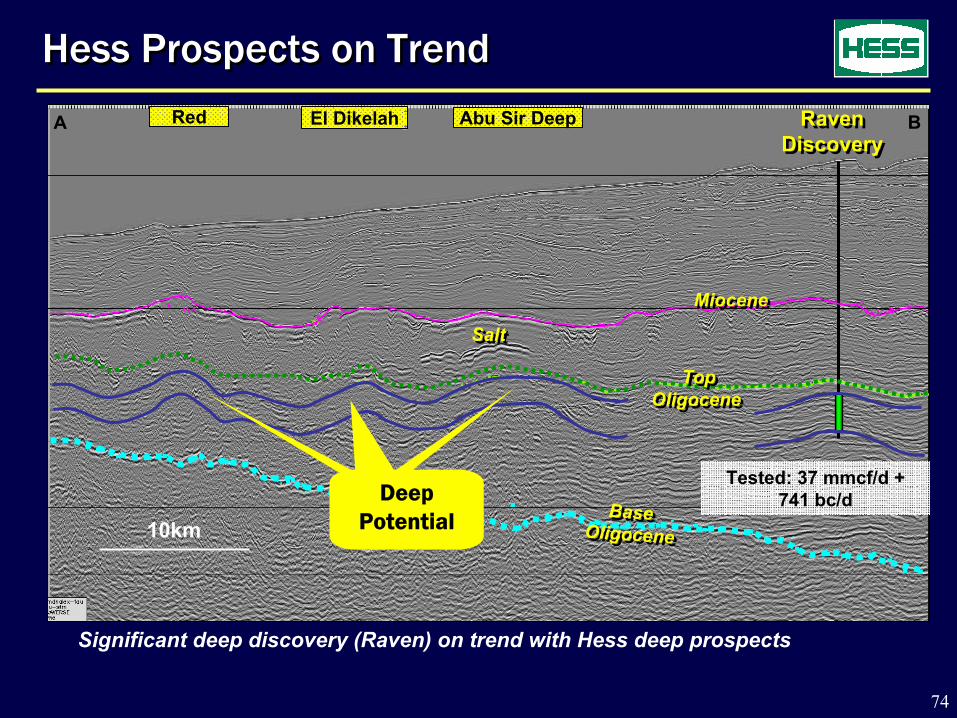

Egypt : West Med Exploration Potential

Hess 55% WI

4 existing discoveries

300 Bcf – 3 Tcf gross exploration resource potential

Untested Miocene and Oligocene objectives beneath established accumulations

Hess 55% WI

4 existing discoveries

300 Bcf – 3 Tcf gross exploration resource potential

Untested Miocene and Oligocene objectives beneath established accumulations

MIOCENE AND OLIGOCENE PROSPECTS

FIELD OUTLINES

10 km

EL KING

ABU SIR

RAVENEl Dikelah

AA

BB Seismic Line

Abu Sir Deep

Red

Wes

t Med

–H

ess

Op

N A

lexa

ndria

–B

P O

p

74

Hess Prospects on TrendHess Prospects on Trend

Significant deep discovery (Raven) on trend with Hess deep prospects

Red El Dikelah Abu Sir DeepA B

10km

Raven Discovery

Raven Discovery

SaltSaltMioceneMiocene

Top Oligocene

Top Oligocene

Base Oligocene

Base Oligocene

Tested: 37 mmcf/d + 741 bc/dDeep Deep

PotentialPotentialDeep Deep

PotentialPotentialDeep

Potential

75

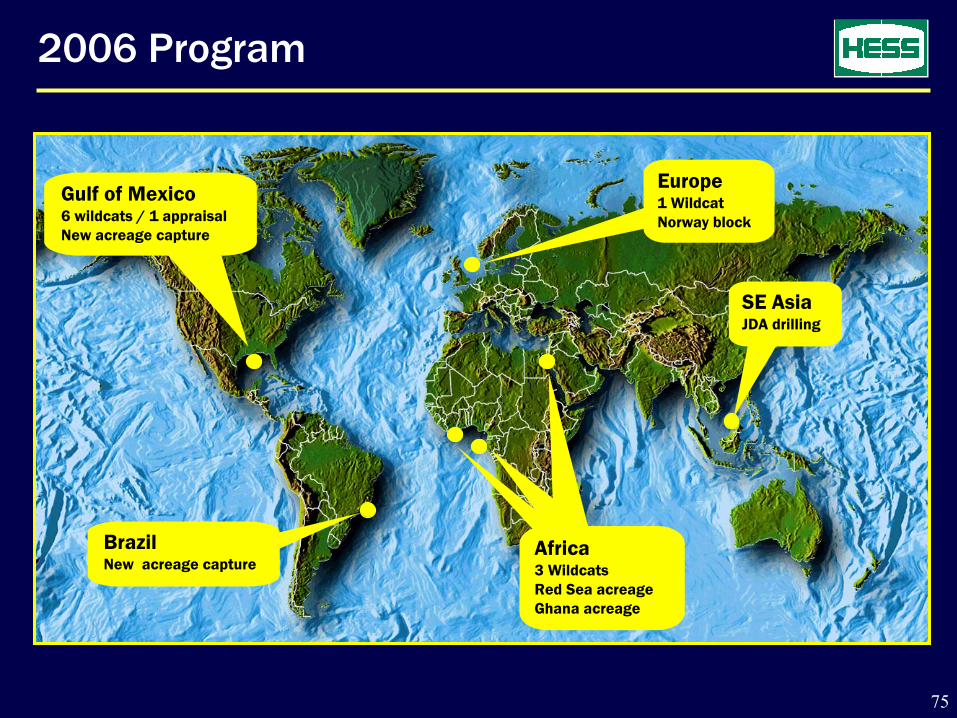

2006 Program

Gulf of Mexico6 wildcats / 1 appraisalNew acreage capture

Europe1 WildcatNorway block

Africa 3 WildcatsRed Sea acreageGhana acreage

SE AsiaJDA drilling

BrazilNew acreage capture

76

2007 – 2008 Outlook

Gulf of Mexico8 - 10 Wildcats / Appraisals

NW EuropeCambo AppraisalNorway Wildcat

Africa West Med Arous El-Bahar2 - 3 Wildcats

SE AsiaBelud AppraisalMalaysian Wildcat

South AmericaPeru AppraisalBrazil Wildcat

77

Exploration - Summary

Adding resources and creating value

Global inventory of 19 million net acres

80 named prospects globally

Drilling 8 – 10 impact wells per year

Leading-edge technology

Adding resources and creating value

Global inventory of 19 million net acres

80 named prospects globally

Drilling 8 – 10 impact wells per year

Leading-edge technology

E&P – CONCLUSION

79

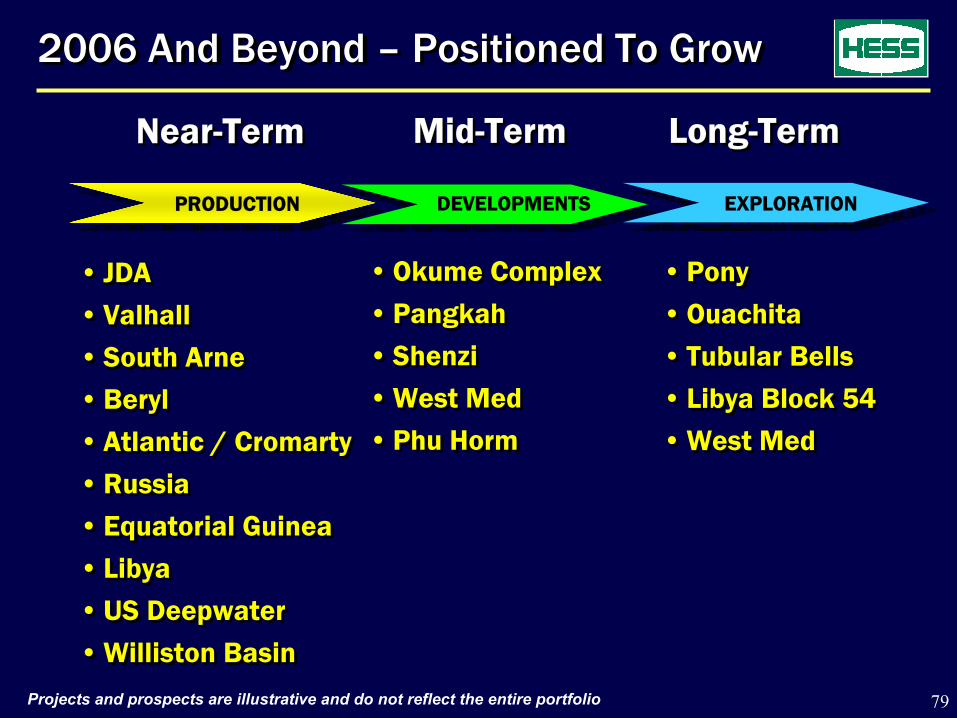

2006 And Beyond – Positioned To Grow2006 And Beyond – Positioned To Grow

• Pony• Ouachita• Tubular Bells• Libya Block 54• West Med

• Pony• Ouachita• Tubular Bells• Libya Block 54• West Med

• JDA• Valhall• South Arne• Beryl• Atlantic / Cromarty• Russia• Equatorial Guinea• Libya• US Deepwater• Williston Basin

• JDA• Valhall• South Arne• Beryl• Atlantic / Cromarty• Russia• Equatorial Guinea• Libya• US Deepwater• Williston Basin

• Okume Complex• Pangkah• Shenzi• West Med• Phu Horm

• Okume Complex• Pangkah• Shenzi• West Med• Phu Horm

EXPLORATION

Long-TermLong-TermNear-TermNear-Term

PRODUCTION

Mid-TermMid-Term

DEVELOPMENTS

Projects and prospects are illustrative and do not reflect the entire portfolio

80

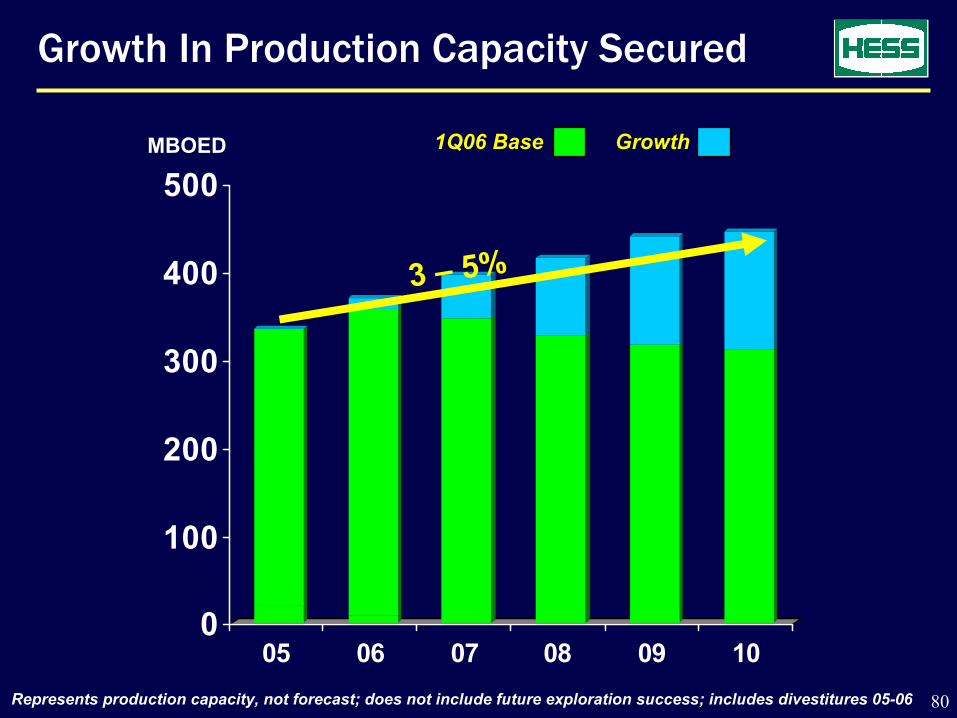

Growth In Production Capacity Secured

0

100

200

300

400

500

05 06 07 08 09 10

MBOED 1Q06 Base Growth

Represents production capacity, not forecast; does not include future exploration success; includes divestitures 05-06

3 – 5%

81

Longer-Life Assets, Geographically Balanced

0

100

200

300

400

500

05 06 07 08 09 10

ProductionCapacityMBOED

Long

Medium

Short

05 06 07 08 09 10

By Reserve Life By Region

Europe

USA

Asia

Africa

Represents production capacity, not forecast; does not include future exploration success; includes divestitures 05-06

82

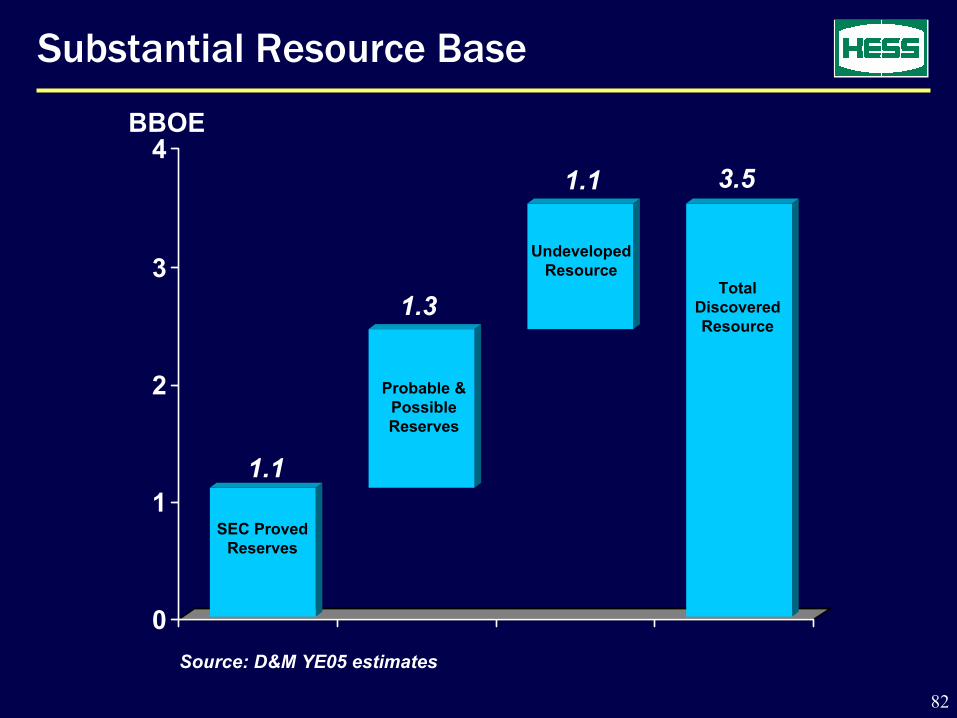

Substantial Resource Base

0

1

2

3

4BBOE

SEC Proved Reserves

Probable & Possible Reserves

UndevelopedResource

Total Discovered Resource

1.1

1.3

1.1 3.5

Source: D&M YE05 estimates

83

0

1

2

2005 2010

ValhallWest Med Pailin

Waha JDA NatunaShenzi Okume Clair RidgePangkah S. Arne BakkenPhu Horm Russia BerylPermian EOR Schiehallion Snøhvit

Reserve Growth Potential Identified

BBOE

5% - 8% Growth Rate

84

E&P – Summary

…that is delivering sustainable growth.

Building a global franchise…

Building a global franchise…

BREAK

BORDEN WALKERPRESIDENT

MARKETING AND REFINING

BORDEN WALKERPRESIDENT

MARKETING AND REFINING

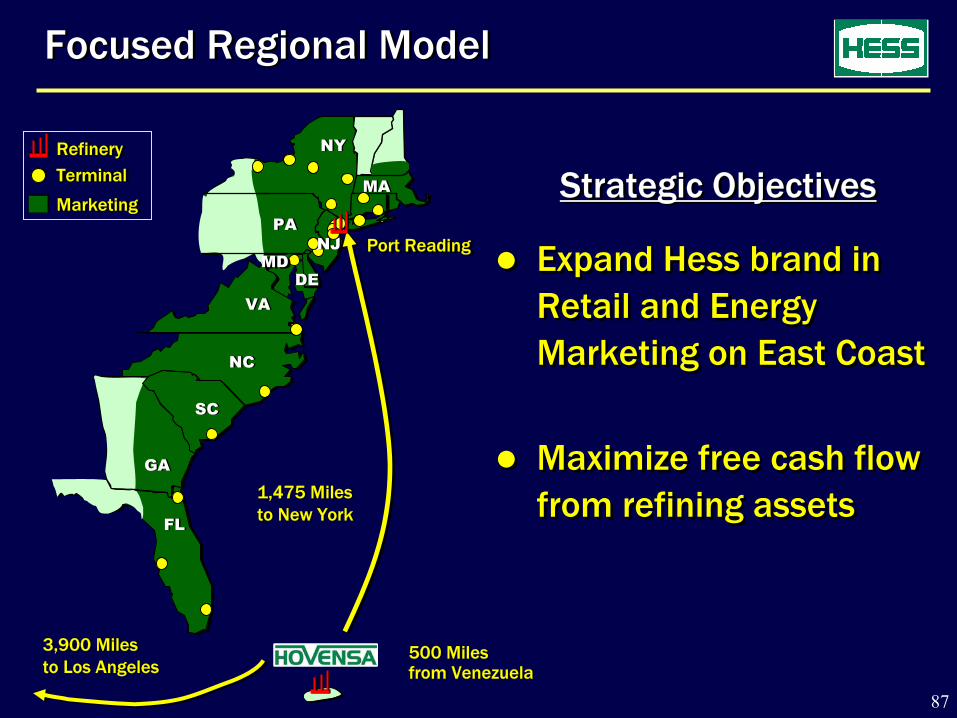

87

DEDE

3,900 Milesto Los Angeles3,900 Milesto Los Angeles

500 Milesfrom Venezuela500 Milesfrom Venezuela

RefineryRefineryTerminalTerminal

MarketingMarketing

1,475 Miles to New York1,475 Miles to New York

Focused Regional ModelFocused Regional Model

Expand Hess brand in Retail and Energy Marketing on East Coast

Maximize free cash flow from refining assets

Expand Hess brand in Retail and Energy Marketing on East Coast

Maximize free cash flow from refining assets

Strategic ObjectivesStrategic Objectives

Port ReadingPort Reading

FL

PAPA

MAMA

VA

NC

SC

NYNY

VAVA

NCNC

GAGA

FLFL

SCSC

MDMDNJNJ

88

EstMarket

# Sites Share (%)

Florida 344 10.5 New York 267 9.9 North Carolina 238 8.9 Pennsylvania 109 5.6 Massachusetts 101 8.2 New Jersey 85 5.4 South Carolina 73 9.0 Virginia 56 4.7 Other 81 N/A

TOTAL 1,354

EstMarket

# Sites Share (%)

Florida 344 10.5 New York 267 9.9 North Carolina 238 8.9 Pennsylvania 109 5.6 Massachusetts 101 8.2 New Jersey 85 5.4 South Carolina 73 9.0 Virginia 56 4.7 Other 81 N/A

TOTAL 1,354

Retail Station NetworkRetail Station NetworkNY

MD

NC

Year-End 2005Year-End 2005

Source: EIA total gallons by stateSource: EIA total gallons by state

89

794

151

242

807

155

233

836

202

216

855

309

190

0

500

1,000

1,500

02 03 04 05

794

151

242

807

155

233

836

202

216

855

309

190

0

500

1,000

1,500

02 03 04 05

Convenience Stores:

Merchandise Sales ($MM)

Gross Margin ($MM)

Convenience Stores:

Merchandise Sales ($MM)

Gross Margin ($MM)

772

187

772

187

862

206

862

206

932

215

932

215

973

232

973

232

Branded / Dealer

WilcoHess

Hess Operated

Branded / Dealer

WilcoHess

Hess Operated

Site Count (Year End)Site Count (Year End)

1,1871,187 1,1951,1951,2541,254

1,3541,354

Growth in Company Operated ModelGrowth in Company Operated Model

86% Co-op86% Co-op

90

Industry Leading PerformanceIndustry Leading Performance

96

104

113114

50

75

100

125

02 03 04 05

96

104

113114

50

75

100

125

02 03 04 05

170178

191

204

100

125

150

175

200

225

02 03 04 05

170178

191

204

100

125

150

175

200

225

02 03 04 05

Typical Major Source: New Image Marketing SurveysTypical Major Source: New Image Marketing Surveys

Per Site AveragesPer Site Averages

Volume (Mg/Mo)Volume (Mg/Mo)

C-Store Sales ($M/Mo)C-Store Sales ($M/Mo)

91

Recent AcquisitionsRecent Acquisitions

Successful Acquisition StrategySuccessful Acquisition Strategy

Hess Rebranded Disney SitesHess Rebranded Disney Sites

Numberof Sites Before After Before After

Disney World 3 110 510 70 187

DB Marts 19 74 175 68 121

Servco 50 101 164 49 77

Fuel Volume C-Store Sales(Mgals/Site/Mo) ($M/Site/Mo)Number

of Sites Before After Before After

Disney World 3 110 510 70 187

DB Marts 19 74 175 68 121

Servco 50 101 164 49 77

Fuel Volume C-Store Sales(Mgals/Site/Mo) ($M/Site/Mo)

92

Strong brand and reputation

Scale advantage

More than 10,000 customers

• Fuel Oil Sales: 130 MB/D

• Natural Gas Sales: 1.5 BCF/D

Selective Growth

Strong brand and reputation

Scale advantage

More than 10,000 customers

• Fuel Oil Sales: 130 MB/D

• Natural Gas Sales: 1.5 BCF/D

Selective Growth

Energy MarketingEnergy Marketing

93

C&I Volume (MDth/d) 185

Ohio Valley

Leading C&I Natural Gas SupplierLeading C&I Natural Gas Supplier

Market ShareMarket Share

15%15%

17%17%

28%28%40%40%

C&I Volume (MDth/d) 110

Upstate New York

C&I Volume (MDth/d) 90

New England

C&I = Commercial and Industrial

28%28%

Mid Atlantic / SE115C&I Volume (MDth/d)

C&I Volume (MDth/d) 260

Metro NY/New Jersey

94

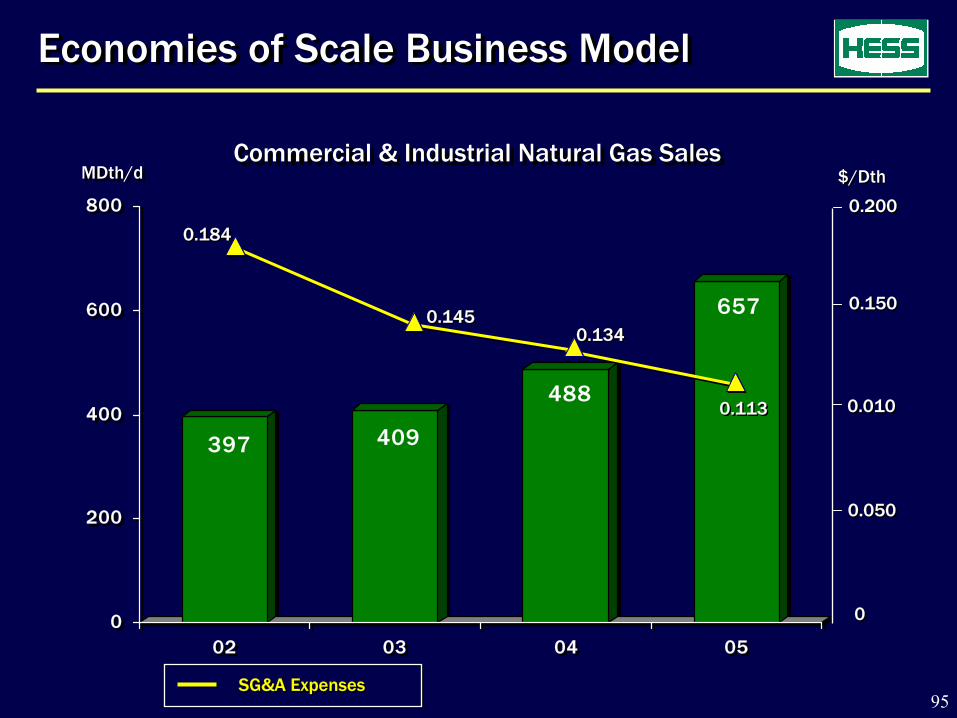

Sales Volume GrowthSales Volume Growth

397 409

488

657

0

200

400

600

800

02 03 04 05

397 409

488

657

0

200

400

600

800

02 03 04 05

MDth/dMDth/dCommercial & Industrial Natural Gas SalesCommercial & Industrial Natural Gas Sales

95

Commercial & Industrial Natural Gas SalesCommercial & Industrial Natural Gas Sales

397 409

488

657

0

200

400

600

800

02 03 04 05

397 409

488

657

0

200

400

600

800

02 03 04 05

Economies of Scale Business ModelEconomies of Scale Business Model

MDth/dMDth/d

0.1450.145

0.1840.184

0.1340.134

00

0.0500.050

0.0100.010

0.1500.150

0.2000.200

0.1130.113

$/Dth$/Dth

SG&A ExpensesSG&A Expenses

96

Hovensa RefineryHovensa Refinery

50/50 JV formed in 1998 by Hess and PDVSA

Capacity

• Crude 500 MB/D

• FCC 150 MB/D

• Coker 58 MB/D

World Class Merchant Refinery

•Competitive Geographic Position

•Economies of Scale

•Long Term PDVSA Crude Supply

50/50 JV formed in 1998 by Hess and PDVSA

Capacity

• Crude 500 MB/D

• FCC 150 MB/D

• Coker 58 MB/D

World Class Merchant Refinery

•Competitive Geographic Position

•Economies of Scale

•Long Term PDVSA Crude Supply

97

Hovensa: Strong Financial ReturnsHovensa: Strong Financial Returns

1.88

0.93 0.92

0.51

0.0

0.5

1.0

1.5

2.0

02 03 04 05

1.88

0.93 0.92

0.51

0.0

0.5

1.0

1.5

2.0

02 03 04 05

OSHA Recordable RateOSHA Recordable Rate

361

440484

461

0

100

200

300

400

500

02 03 04 05

361

440484

461

0

100

200

300

400

500

02 03 04 05

(12)

147

238 244

(50)

0

50

100

150

200

250

300

02 03 04 05

(12)

147

238 244

(50)

0

50

100

150

200

250

300

02 03 04 05

83 90

174

281

0

50

100

150

200

250

300

02 03 04 05

83 90

174

281

0

50

100

150

200

250

300

02 03 04 05

Crude Charge (MB/D)Crude Charge (MB/D)

Hess Net Income ($MM)Hess Net Income ($MM) Distributions & Note Repayments ($MM)(Net of Taxes Paid)

Distributions & Note Repayments ($MM)(Net of Taxes Paid)

0

98

Port Reading RefineryPort Reading Refinery

65 MB/D FCC

Major gasoline manufacturer in NY Harbor

Capable of running 100% low sulfur resid

Strong income generator

65 MB/D FCC

Major gasoline manufacturer in NY Harbor

Capable of running 100% low sulfur resid

Strong income generator

17

27

60

100

0

20

40

60

80

100

02 03 04 05

17

27

60

100

0

20

40

60

80

100

02 03 04 05

Net Income ($MM)Net Income ($MM)

53 54 52

61

0

10

20

30

40

50

60

70

02 03 04 05

53 54 52

61

0

10

20

30

40

50

60

70

02 03 04 05

Charge Rate (MB/D)Charge Rate (MB/D)

(last 9 months)

99

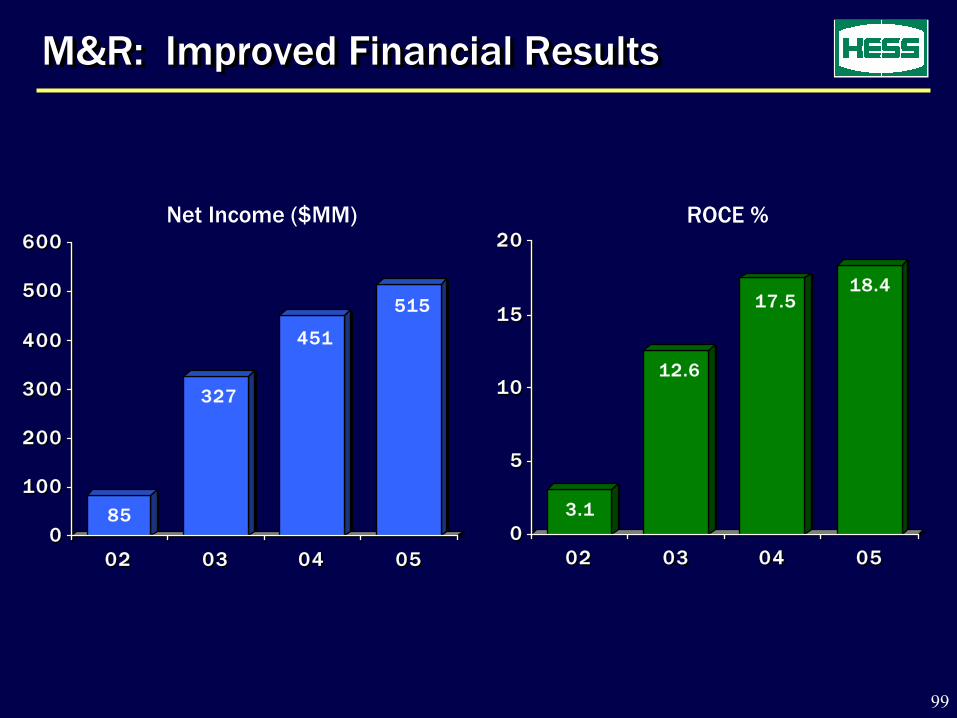

M&R: Improved Financial ResultsM&R: Improved Financial Results

85

327

451

515

0

100

200

300

400

500

600

02 03 04 05

85

327

451

515

0

100

200

300

400

500

600

02 03 04 05

3.1

12.6

17.518.4

0

5

10

15

20

02 03 04 05

3.1

12.6

17.518.4

0

5

10

15

20

02 03 04 05

Net Income ($MM) ROCE %

100

0.00

0.50

1.00

1.50

2.00

2.50

HES VLO BP XOM MRO COP TSO RDS SUN CVX MUR0.00

0.50

1.00

1.50

2.00

2.50

HES VLO BP XOM MRO COP TSO RDS SUN CVX MUR

Competitive ResultsCompetitive Results

0%

10%

20%

30%

XOM SUN MRO COP HES VLO TSO RDS CVX BP MUR0%

10%

20%

30%

XOM SUN MRO COP HES VLO TSO RDS CVX BP MUR

Source: Company filings

U.S. M&R Net Income / Oil BBL Sold2002 – 2005 Average

U.S. M&R Net Income / Oil BBL Sold2002 – 2005 Average

U.S. M&R Return on Capital Employed2002 – 2005 Average

U.S. M&R Return on Capital Employed2002 – 2005 Average

$

0

101

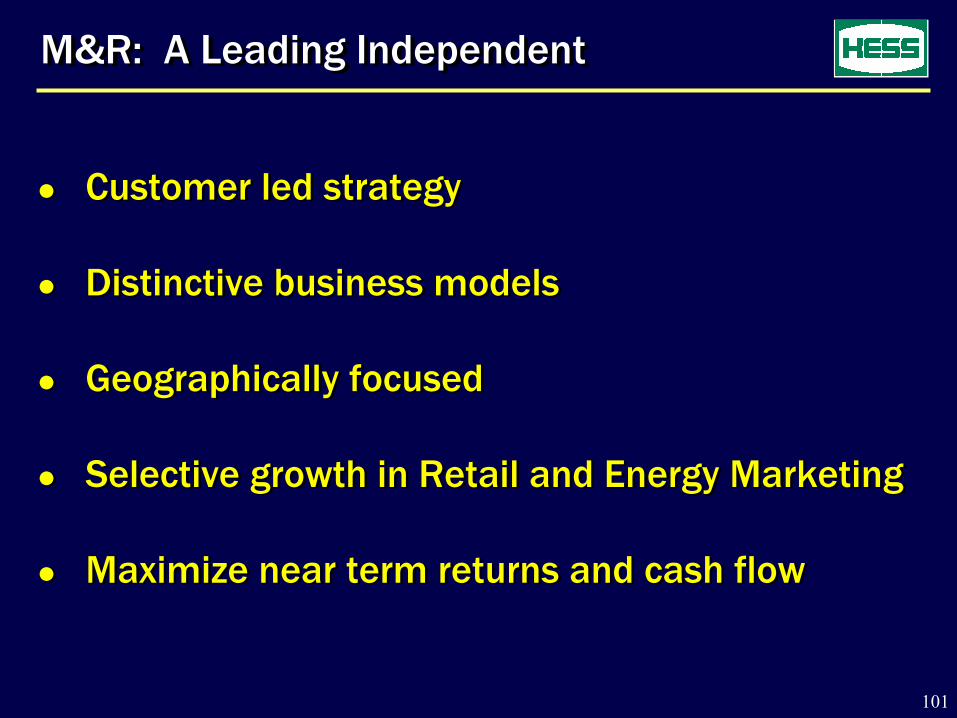

M&R: A Leading IndependentM&R: A Leading Independent

Customer led strategy

Distinctive business models

Geographically focused

Selective growth in Retail and Energy Marketing

Maximize near term returns and cash flow

Customer led strategy

Distinctive business models

Geographically focused

Selective growth in Retail and Energy Marketing

Maximize near term returns and cash flow

JOHN RIELLYCHIEF FINANCIAL OFFICER

103

Financial StrategyFinancial Strategy

Ensure capital availability to fund growth

• Cash flow from operations

• Balance sheet

• Liquidity

Deliver first quartile financial performance

• Return on capital employed

• Total shareholder returns

104

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

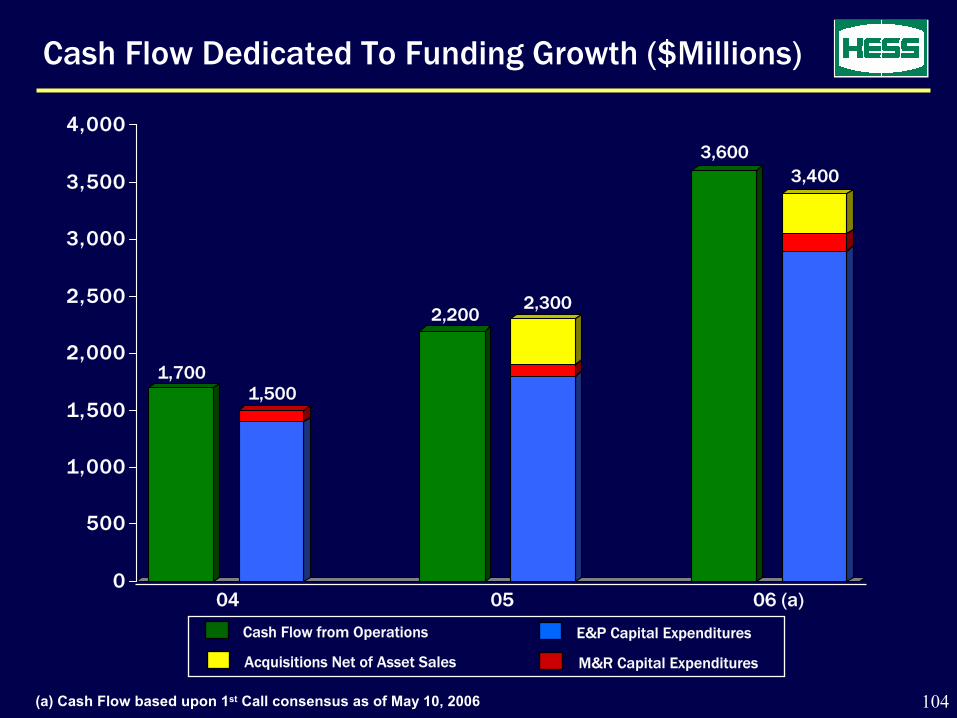

Cash Flow Dedicated To Funding Growth ($Millions)

(a) Cash Flow based upon 1st Call consensus as of May 10, 2006

1,7001,500

2,2002,300

3,6003,400

04 05 06 (a)

Cash Flow from Operations E&P Capital Expenditures

M&R Capital ExpendituresAcquisitions Net of Asset Sales

105

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

(a) Based upon 1st Call CPS as of May 10, 2006. Consensus WTI 2007 / 2008; $57.40 / $54.10 respectively

Cash Flow Available To Fund Growth ($Millions)

3,6003,400

3,600 3,700

Cash Flow from Operations E&P Capital Expenditures

M&R Capital ExpendituresAcquisitions Net of Asset Sales

06 (a) 07 (a) 08 (a)

$50.00 WTI

$50.00 WTI

$57.40 WTI

$54.10 WTI

106

3.8

5.6

3.8

6.3

3.8

8.5

3.7

10.5

3.7

12.3

0

2

4

6

8

10

12

14

16

00

Improving Balance Sheet ($ Billions)

04 05 06(a) 07(a) 08(a)

DebtDebtEquity Debt to CapitalDebt to Capital

45%45%

2020

1010

55

1515

3030

2525

4040

3535

(a) Based upon 1st Call earnings consensus as of May 10, 2006.

$$

107

Strong Financial Liquidity

New $3 billion revolving credit facility

• Five year term, with three one year options

Debt maturities of $251MM over 5 years

• Represents 7% of total debt

26 26 28

142

29

0

50

100

150

06 07 08 09 10

26 26 28

142

29

0

50

100

150

06 07 08 09 10

$M

M$

MM

$$

108

9 %

12 % 12 %

14 % 14 %

2 1%

19 %

0%

5%

10%

15%

20%

25%

Improving ROCE

(b) Based upon 1st Call estimate as of May 10, 2006 (b) Based upon 1st Call estimate as of May 10, 2006 (a) Peer Group per Proxy(a) Peer Group per Proxy

Source: Bloomberg using a consistent basis with HessSource: Bloomberg using a consistent basis with Hess

0303 0404 0505 06 (b)06 (b)

HESS PEERS (a)

109

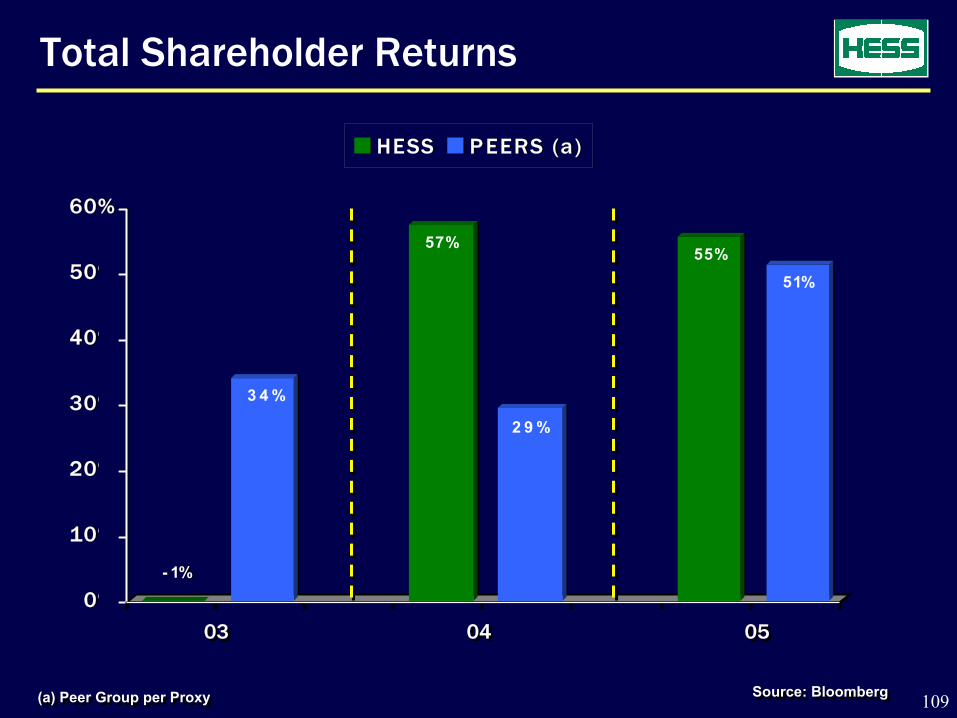

Total Shareholder Returns

- 1%

3 4 %

57%

2 9 %

55%

51%

0%

10%

20%

30%

40%

50%

60%

HESS P EERS (a)

- 1%

3 4 %

57%

2 9 %

55%

51%

0%

10%

20%

30%

40%

50%

60%

HESS P EERS (a)

0303

Source: BloombergSource: Bloomberg(a) Peer Group per Proxy(a) Peer Group per Proxy

0404 0505

110

Financial Summary

Strong cash flow from operations

Declining debt-to-capital ratio

Substantial liquidity

Improving financial and shareholder returns

JOHN HESSCHAIRMAN OF THE BOARD CHIEF EXECUTIVE OFFICER

JOHN HESSCHAIRMAN OF THE BOARD CHIEF EXECUTIVE OFFICER

112

SummarySummary

● Strategy in place

● Portfolio reshaped

● Delivering performance

● Exciting investment opportunities

● Sustainable growth

● Skilled management team

● Strategy in place

● Portfolio reshaped

● Delivering performance

● Exciting investment opportunities

● Sustainable growth

● Skilled management team

113

Forward-Looking Statements and Other InformationForward-Looking Statements and Other Information

This presentation contains projections and other forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These projections and statements reflect the company’s current views with respect to future events and financial performance. No assurances can be given, however, that these events will occur or that these projections will be achieved, and actual results could differ materially from those projected as a result of certain risk factors. A discussion of these risk factors is included in the company’s periodic reports filed with the Securities and Exchange Commission.

The SEC permits oil and gas companies, in their filings with the SEC, to disclose only proved reserves that a company has demonstrated by actual production or conclusive formation tests to be economically and legally producible under existing economic and operating conditions. We use certain terms in this presentation relating to reserves other than proved, such as unproved resources, that the SEC’s guidelines prohibit registrants from including in filings with the SEC. Investors are urged to consider closely the disclosure in Hess’ Form 10-K, File No. 1-1204, available from Hess Corporation, 1185 Avenue of the Americas, New York, New York 10036 c/o Corporate Secretary and on our website at www.hess.com. You can also obtain this form from the SEC on the EDGAR system.

This presentation contains certain non-GAAP financial measures. A reconciliation of the differences between these non-GAAP financial measures and the most directly comparable GAAP financial measures can be found in this presentation on our website at www.hess.com.

This presentation contains projections and other forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These projections and statements reflect the company’s current views with respect to future events and financial performance. No assurances can be given, however, that these events will occur or that these projections will be achieved, and actual results could differ materially from those projected as a result of certain risk factors. A discussion of these risk factors is included in the company’s periodic reports filed with the Securities and Exchange Commission.

The SEC permits oil and gas companies, in their filings with the SEC, to disclose only proved reserves that a company has demonstrated by actual production or conclusive formation tests to be economically and legally producible under existing economic and operating conditions. We use certain terms in this presentation relating to reserves other than proved, such as unproved resources, that the SEC’s guidelines prohibit registrants from including in filings with the SEC. Investors are urged to consider closely the disclosure in Hess’ Form 10-K, File No. 1-1204, available from Hess Corporation, 1185 Avenue of the Americas, New York, New York 10036 c/o Corporate Secretary and on our website at www.hess.com. You can also obtain this form from the SEC on the EDGAR system.

This presentation contains certain non-GAAP financial measures. A reconciliation of the differences between these non-GAAP financial measures and the most directly comparable GAAP financial measures can be found in this presentation on our website at www.hess.com.

![2008 UBS Global Oil and Gas Conference[1]library.corporate-ir.net/library/10/101/101801/items/295700/Hess...Bakken Jambi Merang Seminole ROZ 2009 Pangkah Oil Shenzi 2008 ... position](https://img.pdfslide.us/doc/110x75/5acbb3057f8b9a875a8bb3b7/2008-ubs-global-oil-and-gas-conference1-jambi-merang-seminole-roz-2009-pangkah.jpg)