Embed Size (px)

Citation preview

Research & Forecast Report

4Q 2013Jakarta | Office

Jakarta Property Market Report

Research & Forecast Report

4th Quarter 2014

Accelerating success.

2 Research & Forecast Report | 4Q 2014 | Contents | Colliers International

Contents

Office Sector 3

Apartment Sector 13

Expatriate Housing Sector 23

Retail Sector 23

Industrial Estate Sector 32

3 Research & Forecast Report | 4Q 2014 | Office | Colliers International

Office SectorThe slowing economy and the election has brought occupancy rates down modestly by 1% YoY to 95.4%. In response to the sluggish market, several premium and grade A office buildings lowered their overly optimistic asking base rents by 10 to 20%. This restrained the growth of average base rents in the CBD. Nevertheless, the asking base rents for US dollar denominated buildings grew by 6.9% YoY to USD36.84.

Apartment SectorOnly 51% or 10,701 units of the previously projected supply for the whole 2014 of 20,899 units came onto the market in 2014. As a result, the remaining 49% (or 10,188 units) will be completed this year for a total potential supply in 2015 of 38,562 units representing 25% of the total existing supply. Take-up rates of projects under development dropped moderately this year to 72.1%.

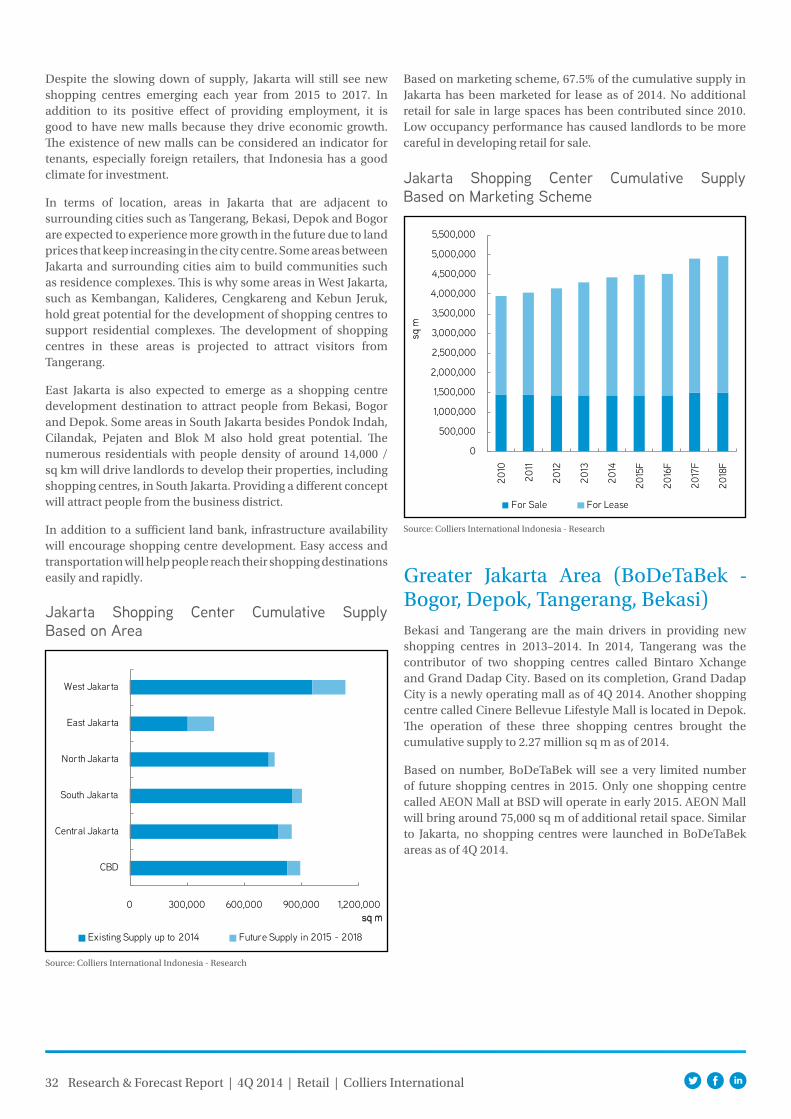

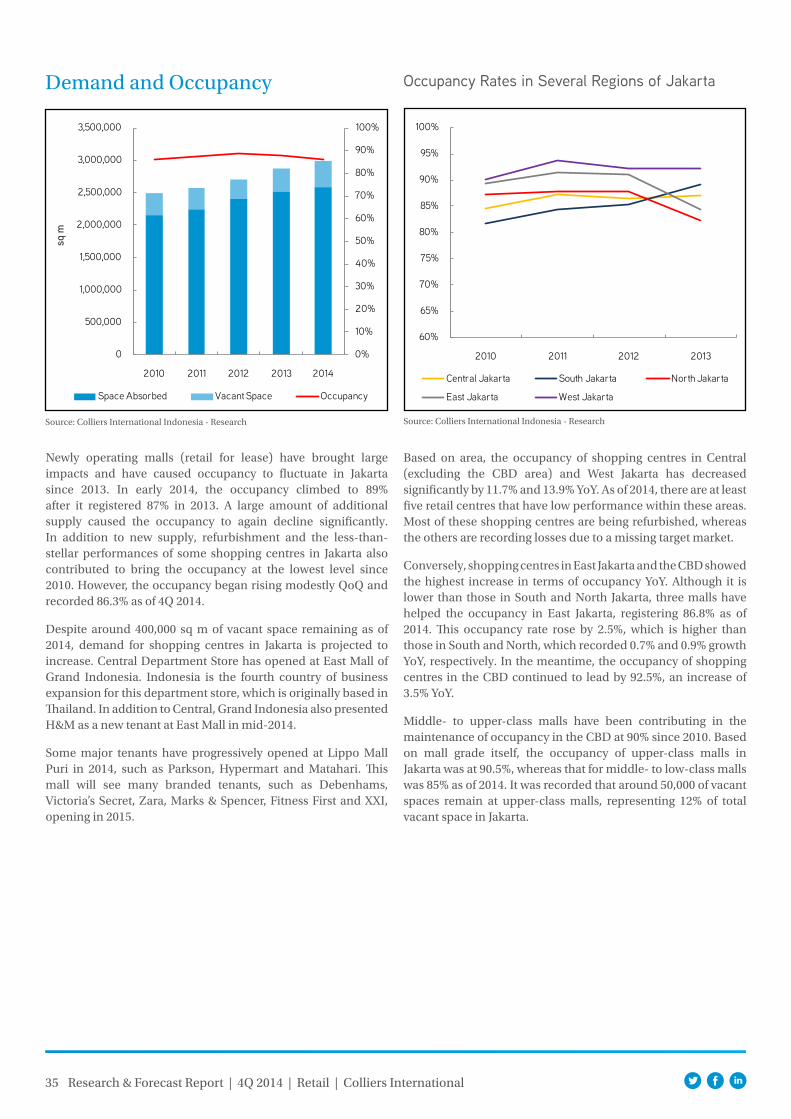

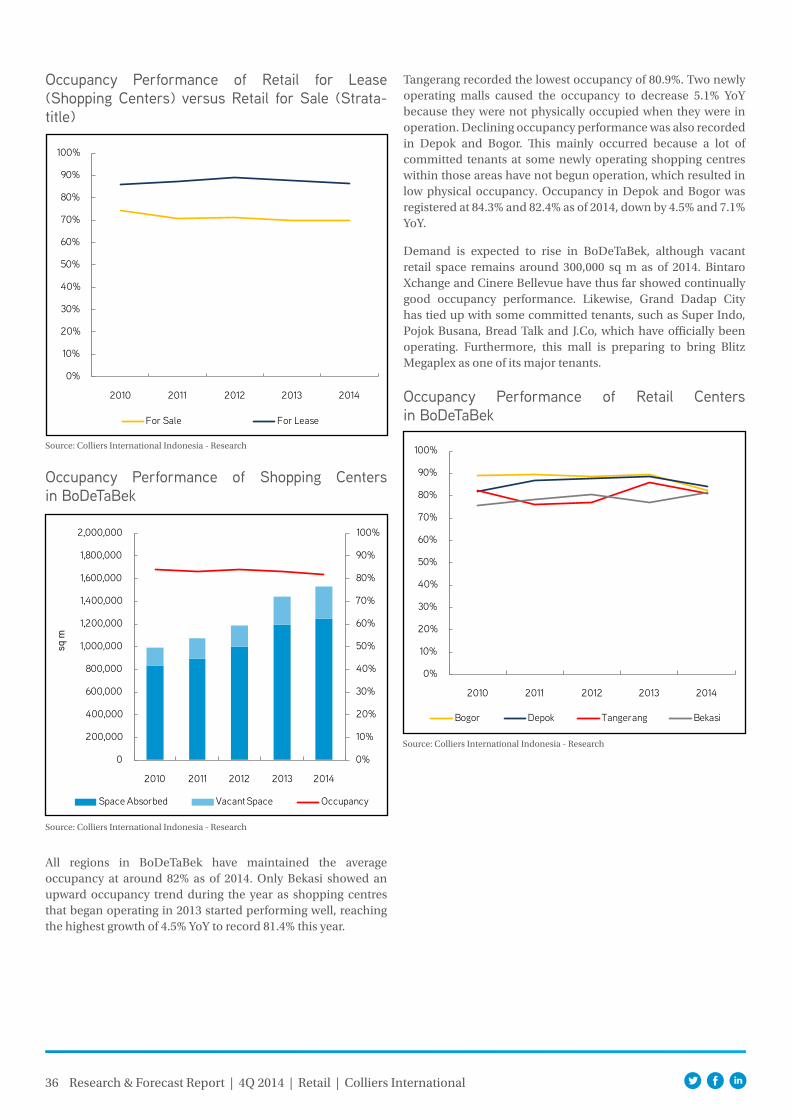

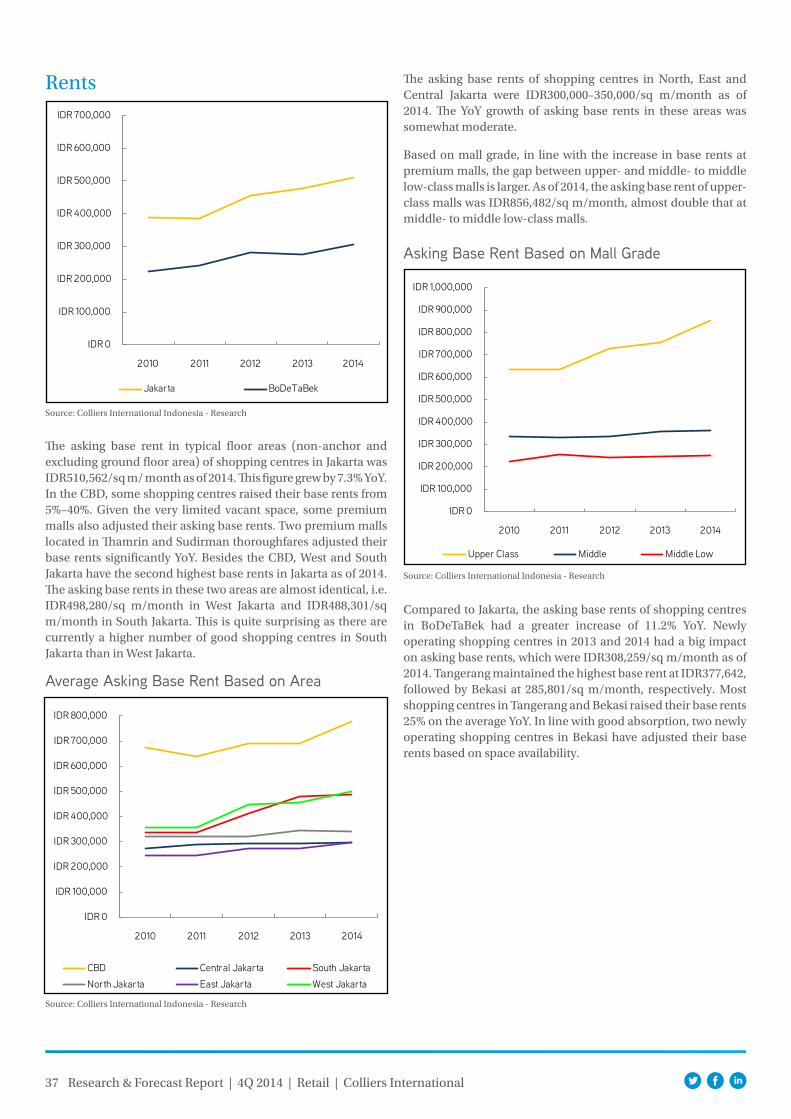

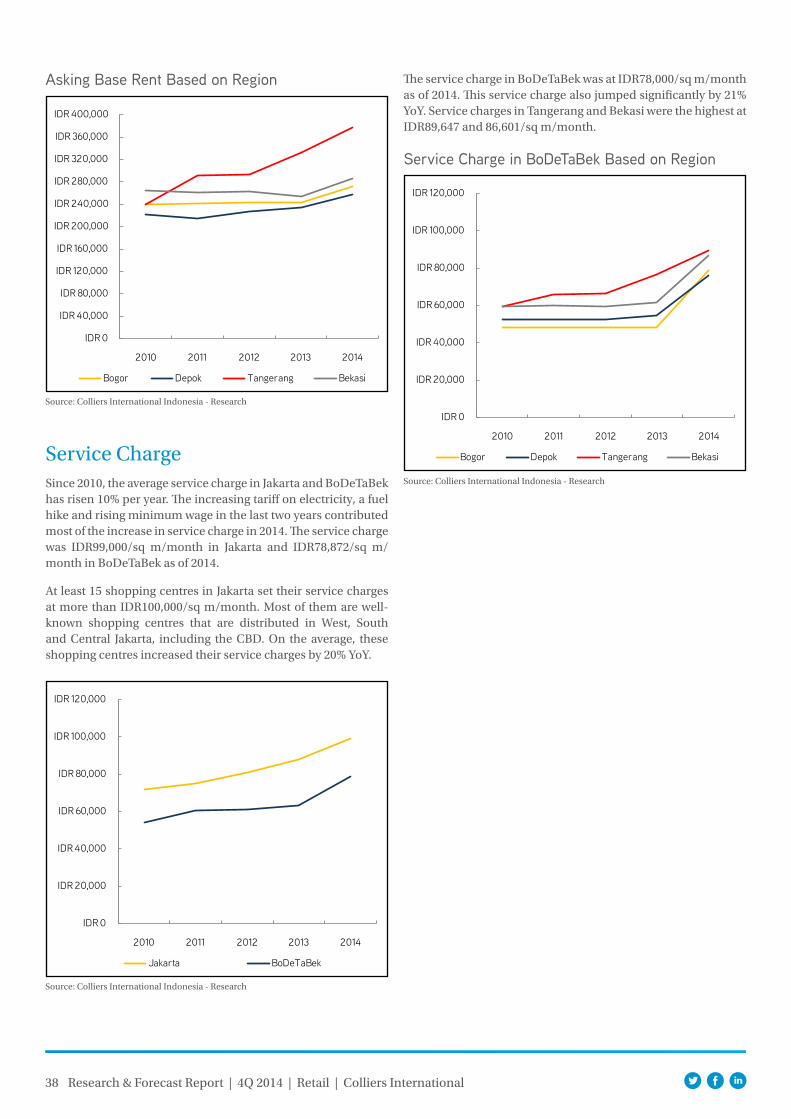

Retail SectorThere are a limited number of new retail properties completed in 2014 in DKI Jakarta bringing cumulative supply to 4.44 million sq m for a 3.2% increase YoY. The YoY occupancy was down modestly and was recorded at 86.3% at end of 2014 because the physical occupancy in contrast with the leased spaces of newly operating shopping center was still relatively low. Given this situation, the asking base rent only grew by 7.3% YoY to IDR510,562/sq m/month.

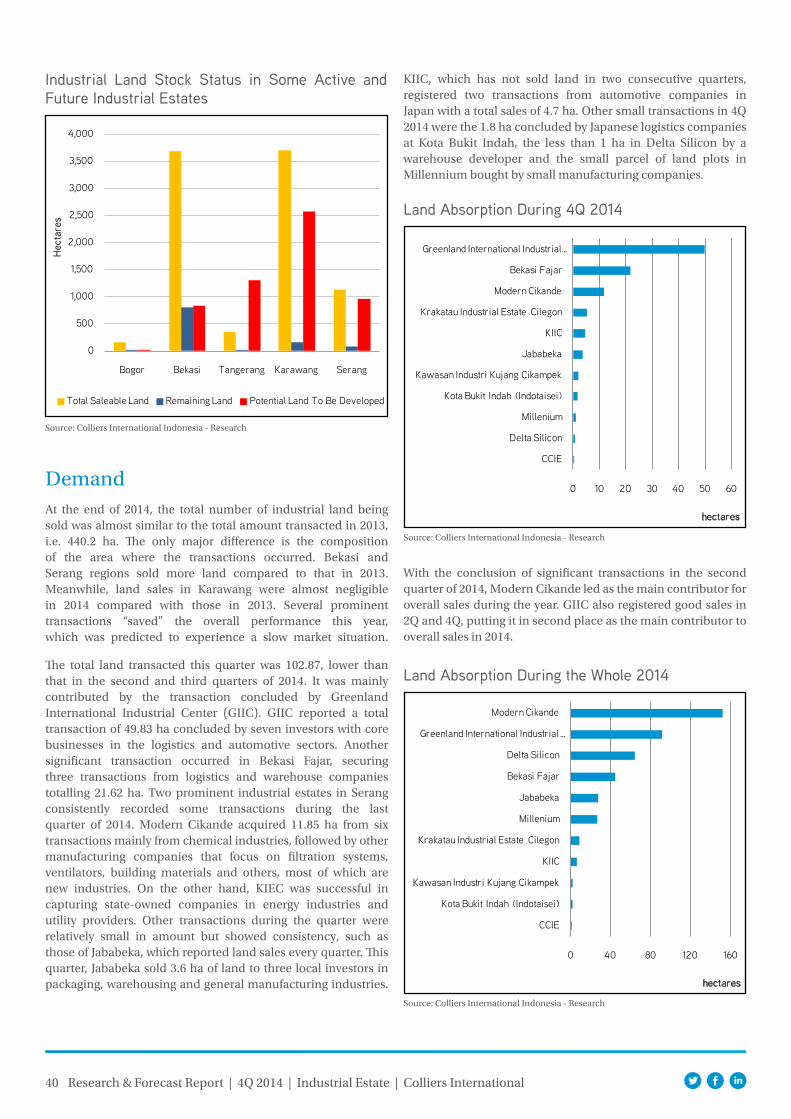

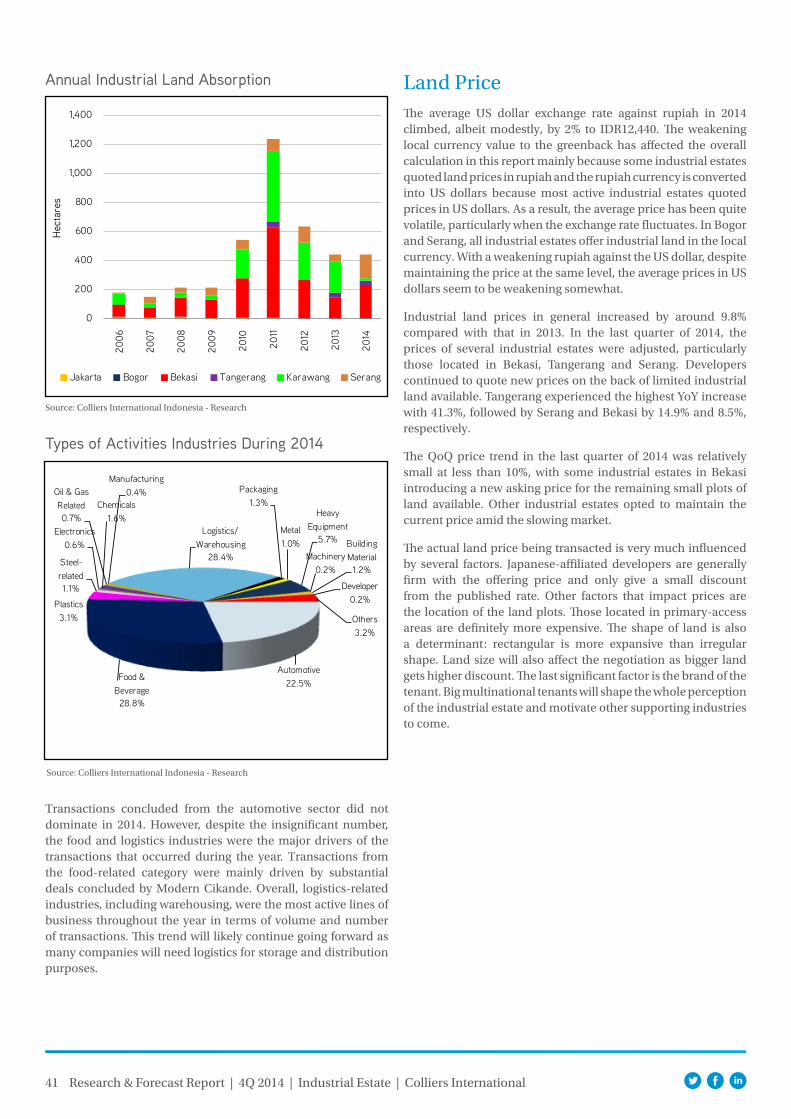

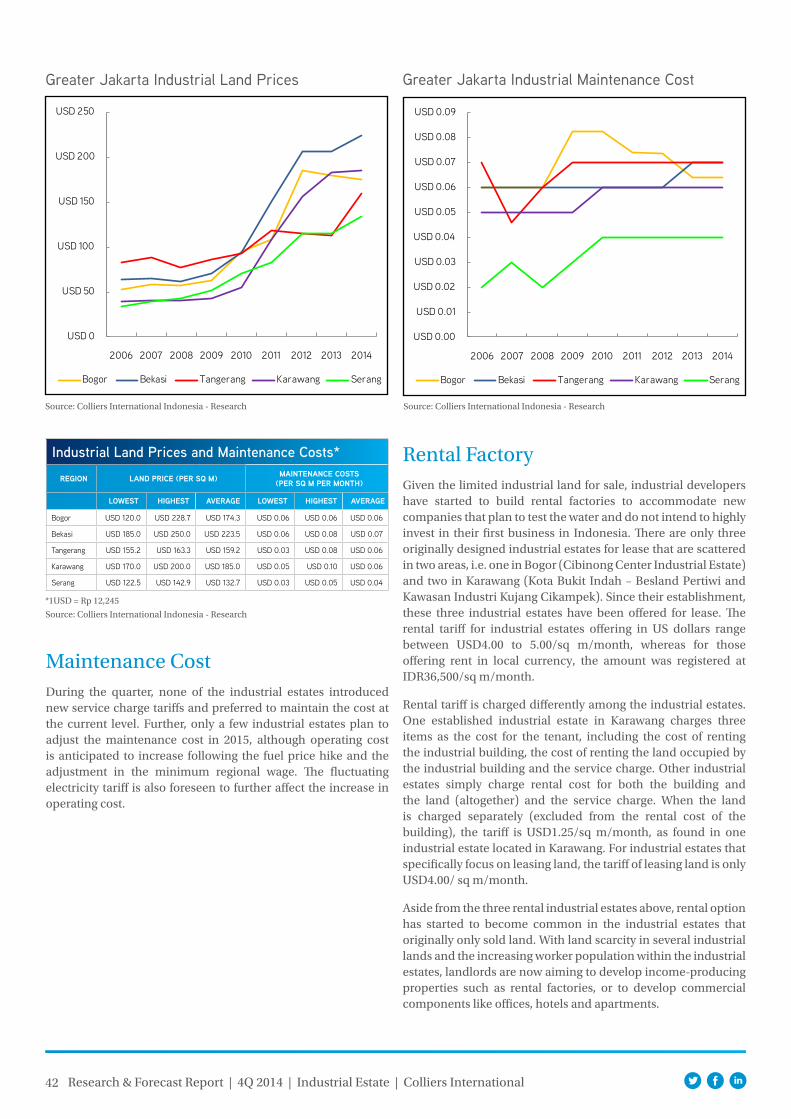

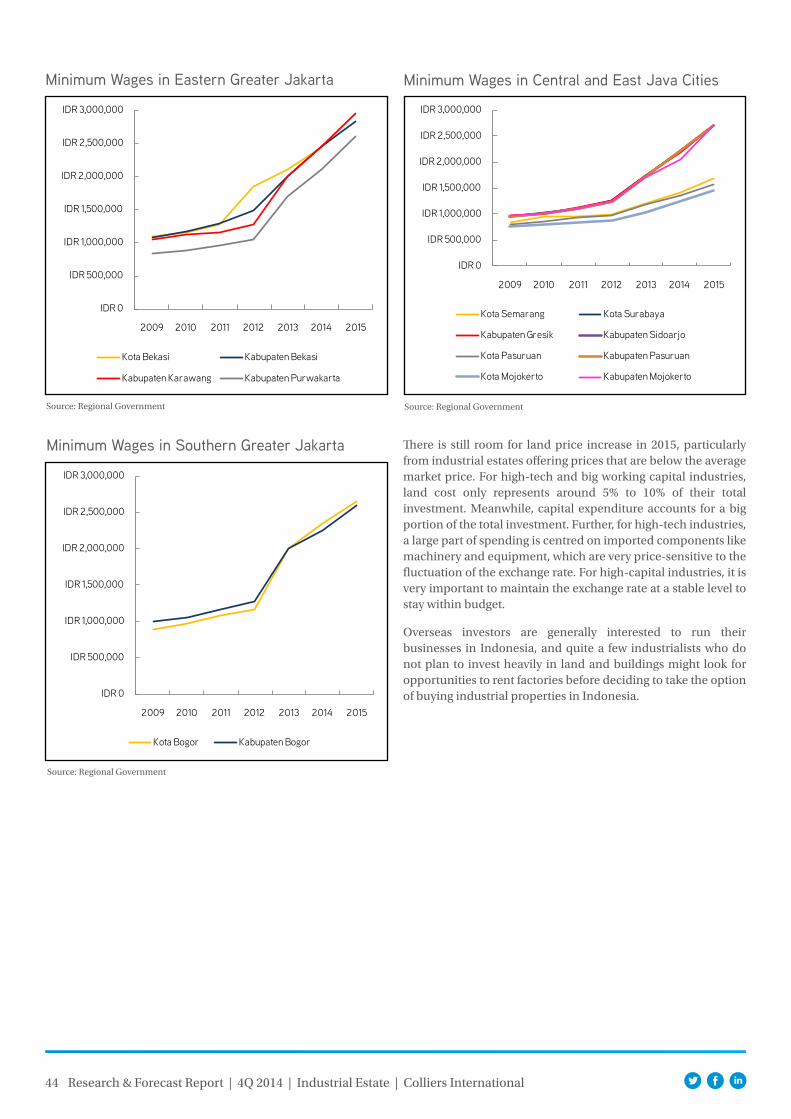

Industrial Estate SectorAlthough the downturn in the economy and political uncertainty characterized 2014, total industrial land sales during the year reached 421 ha which was almost equal to total sales in 2013. Another surprising fact is that land prices continued to increase, albeit moderately, by 9.8% YoY, mainly driven by adjustments occurring in several estates located in Bekasi, Serang and Tangerang.

Highlight

Colliers International

is a leader in global real estate services, defined by our spirit of enterprise. Through a culture of service excellence and collaboration, we integrate the resources of real estate specialists worldwide to accelerate the success of our partners. We represent property investors, developers and occupiers in local and global markets. Our expertise spans all property sectors–office, industrial, retail, residential, rural & agribusiness, healthcare & retirement living, hotels & leisure.

By Ferry SalantoAssociate Director | [email protected]

4

OFFICE SECTORLeased Office

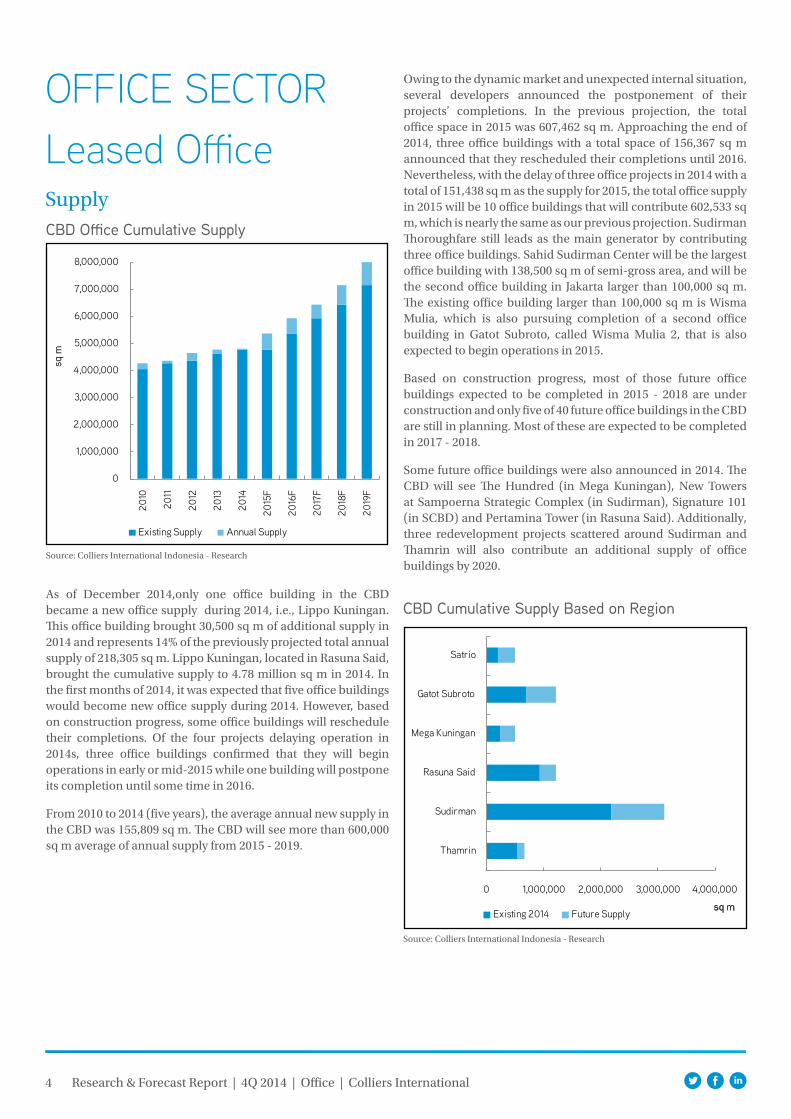

CBD Office Cumulative Supply

Source: Colliers International Indonesia - Research

Supply

As of December 2014,only one office building in the CBD became a new office supply during 2014, i.e., Lippo Kuningan. This office building brought 30,500 sq m of additional supply in 2014 and represents 14% of the previously projected total annual supply of 218,305 sq m. Lippo Kuningan, located in Rasuna Said, brought the cumulative supply to 4.78 million sq m in 2014. In the first months of 2014, it was expected that five office buildings would become new office supply during 2014. However, based on construction progress, some office buildings will reschedule their completions. Of the four projects delaying operation in 2014s, three office buildings confirmed that they will begin operations in early or mid-2015 while one building will postpone its completion until some time in 2016.

From 2010 to 2014 (five years), the average annual new supply in the CBD was 155,809 sq m. The CBD will see more than 600,000 sq m average of annual supply from 2015 - 2019.

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

2010

2011

2012

2013

2014

2015

F

2016

F

2017

F

2018

F

2019

F

sq m

Existing Supply Annual Supply

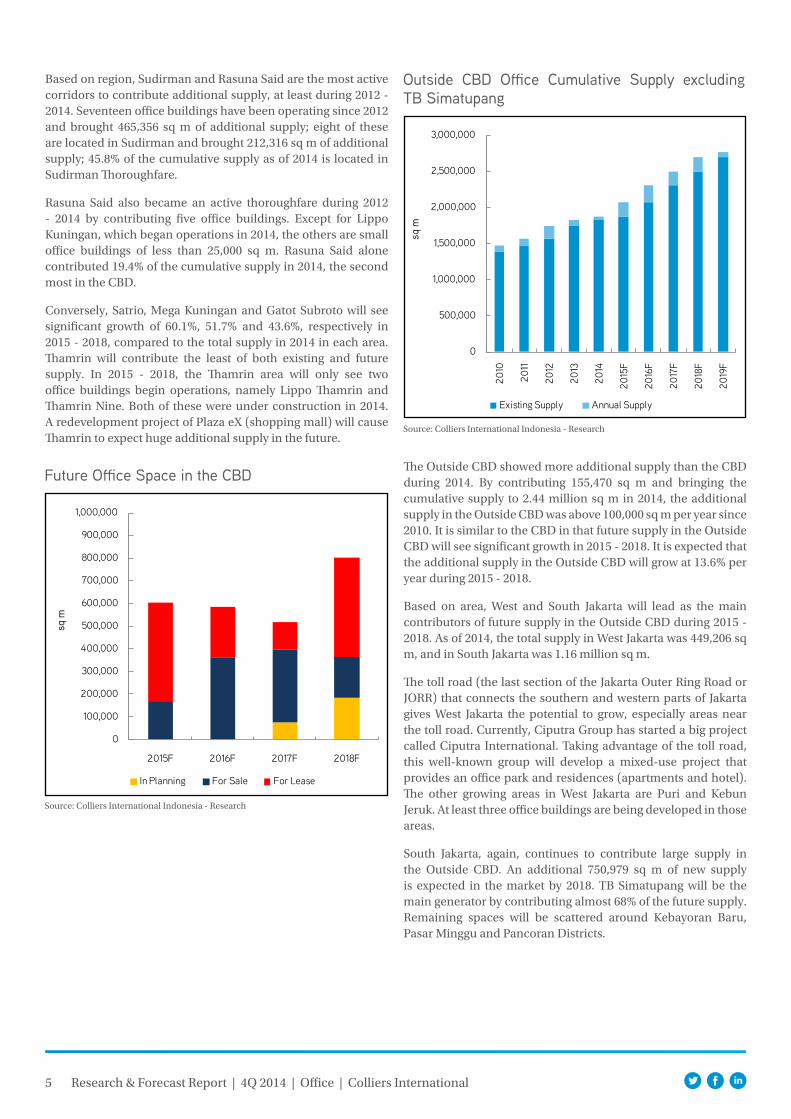

CBD Cumulative Supply Based on Region

Source: Colliers International Indonesia - Research

Owing to the dynamic market and unexpected internal situation, several developers announced the postponement of their projects’ completions. In the previous projection, the total office space in 2015 was 607,462 sq m. Approaching the end of 2014, three office buildings with a total space of 156,367 sq m announced that they rescheduled their completions until 2016. Nevertheless, with the delay of three office projects in 2014 with a total of 151,438 sq m as the supply for 2015, the total office supply in 2015 will be 10 office buildings that will contribute 602,533 sq m, which is nearly the same as our previous projection. Sudirman Thoroughfare still leads as the main generator by contributing three office buildings. Sahid Sudirman Center will be the largest office building with 138,500 sq m of semi-gross area, and will be the second office building in Jakarta larger than 100,000 sq m. The existing office building larger than 100,000 sq m is Wisma Mulia, which is also pursuing completion of a second office building in Gatot Subroto, called Wisma Mulia 2, that is also expected to begin operations in 2015.

Based on construction progress, most of those future office buildings expected to be completed in 2015 - 2018 are under construction and only five of 40 future office buildings in the CBD are still in planning. Most of these are expected to be completed in 2017 - 2018.

Some future office buildings were also announced in 2014. The CBD will see The Hundred (in Mega Kuningan), New Towers at Sampoerna Strategic Complex (in Sudirman), Signature 101 (in SCBD) and Pertamina Tower (in Rasuna Said). Additionally, three redevelopment projects scattered around Sudirman and Thamrin will also contribute an additional supply of office buildings by 2020.

0 1,000,000 2,000,000 3,000,000 4,000,000

Thamrin

Sudirman

Rasuna Said

Mega Kuningan

Gatot Subroto

Satrio

sq mExisting 2014 Future Supply

Research & Forecast Report | 4Q 2014 | Office | Colliers International

5

Based on region, Sudirman and Rasuna Said are the most active corridors to contribute additional supply, at least during 2012 - 2014. Seventeen office buildings have been operating since 2012 and brought 465,356 sq m of additional supply; eight of these are located in Sudirman and brought 212,316 sq m of additional supply; 45.8% of the cumulative supply as of 2014 is located in Sudirman Thoroughfare.

Rasuna Said also became an active thoroughfare during 2012 - 2014 by contributing five office buildings. Except for Lippo Kuningan, which began operations in 2014, the others are small office buildings of less than 25,000 sq m. Rasuna Said alone contributed 19.4% of the cumulative supply in 2014, the second most in the CBD.

Conversely, Satrio, Mega Kuningan and Gatot Subroto will see significant growth of 60.1%, 51.7% and 43.6%, respectively in 2015 - 2018, compared to the total supply in 2014 in each area. Thamrin will contribute the least of both existing and future supply. In 2015 - 2018, the Thamrin area will only see two office buildings begin operations, namely Lippo Thamrin and Thamrin Nine. Both of these were under construction in 2014. A redevelopment project of Plaza eX (shopping mall) will cause Thamrin to expect huge additional supply in the future.

Future Office Space in the CBD

Source: Colliers International Indonesia - Research

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

1,000,000

2015F 2016F 2017F 2018F

sq m

In Planning For Sale For Lease

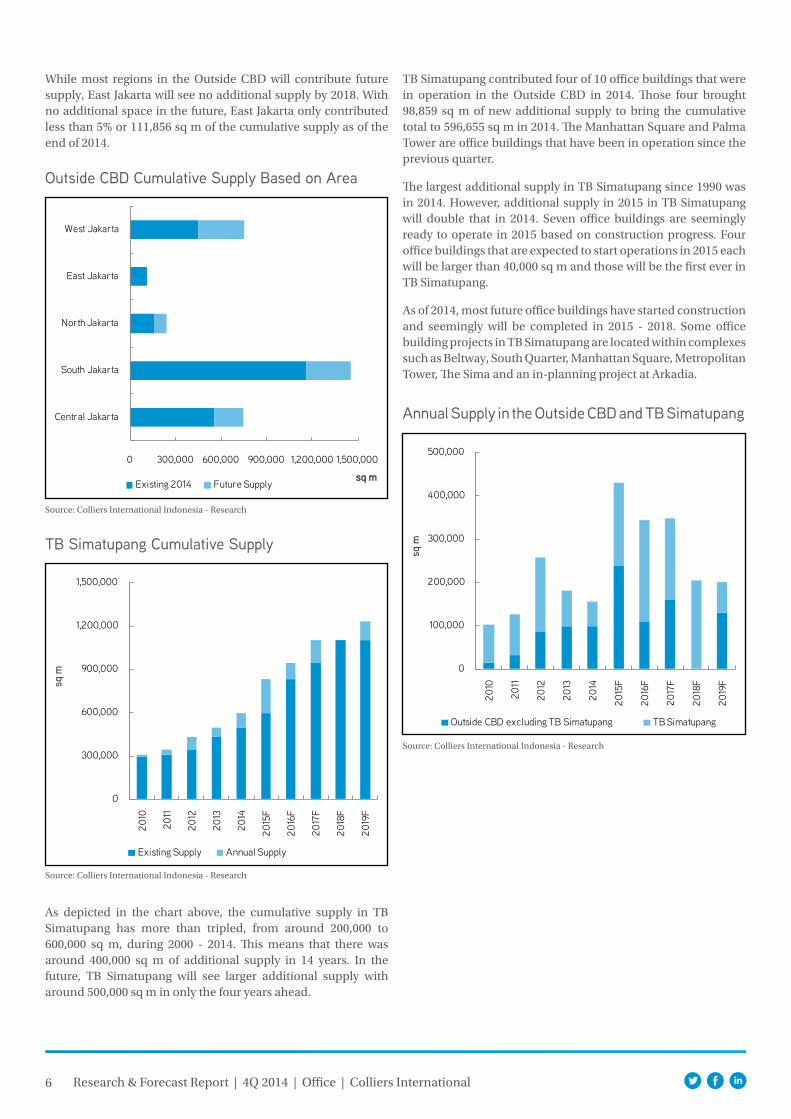

Outside CBD Office Cumulative Supply excluding TB Simatupang

Source: Colliers International Indonesia - Research

The Outside CBD showed more additional supply than the CBD during 2014. By contributing 155,470 sq m and bringing the cumulative supply to 2.44 million sq m in 2014, the additional supply in the Outside CBD was above 100,000 sq m per year since 2010. It is similar to the CBD in that future supply in the Outside CBD will see significant growth in 2015 - 2018. It is expected that the additional supply in the Outside CBD will grow at 13.6% per year during 2015 - 2018.

Based on area, West and South Jakarta will lead as the main contributors of future supply in the Outside CBD during 2015 - 2018. As of 2014, the total supply in West Jakarta was 449,206 sq m, and in South Jakarta was 1.16 million sq m.

The toll road (the last section of the Jakarta Outer Ring Road or JORR) that connects the southern and western parts of Jakarta gives West Jakarta the potential to grow, especially areas near the toll road. Currently, Ciputra Group has started a big project called Ciputra International. Taking advantage of the toll road, this well-known group will develop a mixed-use project that provides an office park and residences (apartments and hotel). The other growing areas in West Jakarta are Puri and Kebun Jeruk. At least three office buildings are being developed in those areas.

South Jakarta, again, continues to contribute large supply in the Outside CBD. An additional 750,979 sq m of new supply is expected in the market by 2018. TB Simatupang will be the main generator by contributing almost 68% of the future supply. Remaining spaces will be scattered around Kebayoran Baru, Pasar Minggu and Pancoran Districts.

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

2010

2011

2012

2013

2014

2015

F

2016

F

2017

F

2018

F

2019

F

sq m

Existing Supply Annual Supply

Research & Forecast Report | 4Q 2014 | Office | Colliers International

6

Outside CBD Cumulative Supply Based on Area

Source: Colliers International Indonesia - Research

0 300,000 600,000 900,000 1,200,000 1,500,000

Central Jakarta

South Jakarta

North Jakarta

East Jakarta

West Jakarta

sq mExisting 2014 Future Supply

TB Simatupang Cumulative Supply

Source: Colliers International Indonesia - Research

0

300,000

600,000

900,000

1,200,000

1,500,000

2010

2011

2012

2013

2014

2015

F

2016

F

2017

F

2018

F

2019

F

sq m

Existing Supply Annual Supply

As depicted in the chart above, the cumulative supply in TB Simatupang has more than tripled, from around 200,000 to 600,000 sq m, during 2000 - 2014. This means that there was around 400,000 sq m of additional supply in 14 years. In the future, TB Simatupang will see larger additional supply with around 500,000 sq m in only the four years ahead.

While most regions in the Outside CBD will contribute future supply, East Jakarta will see no additional supply by 2018. With no additional space in the future, East Jakarta only contributed less than 5% or 111,856 sq m of the cumulative supply as of the end of 2014.

TB Simatupang contributed four of 10 office buildings that were in operation in the Outside CBD in 2014. Those four brought 98,859 sq m of new additional supply to bring the cumulative total to 596,655 sq m in 2014. The Manhattan Square and Palma Tower are office buildings that have been in operation since the previous quarter.

The largest additional supply in TB Simatupang since 1990 was in 2014. However, additional supply in 2015 in TB Simatupang will double that in 2014. Seven office buildings are seemingly ready to operate in 2015 based on construction progress. Four office buildings that are expected to start operations in 2015 each will be larger than 40,000 sq m and those will be the first ever in TB Simatupang.

As of 2014, most future office buildings have started construction and seemingly will be completed in 2015 - 2018. Some office building projects in TB Simatupang are located within complexes such as Beltway, South Quarter, Manhattan Square, Metropolitan Tower, The Sima and an in-planning project at Arkadia.

Annual Supply in the Outside CBD and TB Simatupang

Source: Colliers International Indonesia - Research

0

100,000

200,000

300,000

400,000

500,000

2010

2011

2012

2013

2014

2015

F

2016

F

2017

F

2018

F

2019

F

sq m

Outside CBD excluding TB Simatupang TB Simatupang

Research & Forecast Report | 4Q 2014 | Office | Colliers International

7 Research & Forecast Report | 4Q 2014 | Office | Colliers International

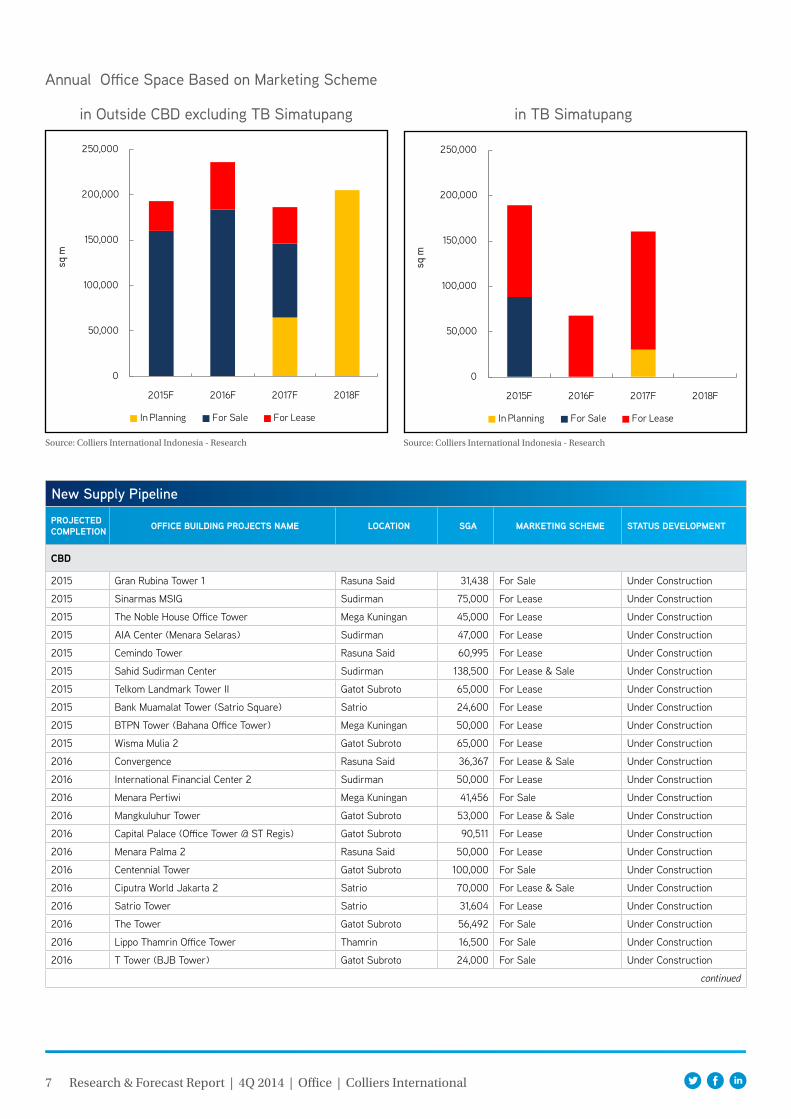

Annual Office Space Based on Marketing Scheme

in Outside CBD excluding TB Simatupang in TB Simatupang

Source: Colliers International Indonesia - Research Source: Colliers International Indonesia - Research

0

50,000

100,000

150,000

200,000

250,000

2015F 2016F 2017F 2018F

sq m

In Planning For Sale For Lease

0

50,000

100,000

150,000

200,000

250,000

2015F 2016F 2017F 2018F

sq m

In Planning For Sale For Lease

New Supply Pipeline

projected completion oFFice Building projectS name location Sga marketing Scheme StatuS development

cBd

2015 Gran Rubina Tower 1 Rasuna Said 31,438 For Sale Under Construction

2015 Sinarmas MSIG Sudirman 75,000 For Lease Under Construction

2015 The Noble House Office Tower Mega Kuningan 45,000 For Lease Under Construction

2015 AIA Center (Menara Selaras) Sudirman 47,000 For Lease Under Construction

2015 Cemindo Tower Rasuna Said 60,995 For Lease Under Construction

2015 Sahid Sudirman Center Sudirman 138,500 For Lease & Sale Under Construction

2015 Telkom Landmark Tower II Gatot Subroto 65,000 For Lease Under Construction

2015 Bank Muamalat Tower (Satrio Square) Satrio 24,600 For Lease Under Construction

2015 BTPN Tower (Bahana Office Tower) Mega Kuningan 50,000 For Lease Under Construction

2015 Wisma Mulia 2 Gatot Subroto 65,000 For Lease Under Construction

2016 Convergence Rasuna Said 36,367 For Lease & Sale Under Construction

2016 International Financial Center 2 Sudirman 50,000 For Lease Under Construction

2016 Menara Pertiwi Mega Kuningan 41,456 For Sale Under Construction

2016 Mangkuluhur Tower Gatot Subroto 53,000 For Lease & Sale Under Construction

2016 Capital Palace (Office Tower @ ST Regis) Gatot Subroto 90,511 For Lease Under Construction

2016 Menara Palma 2 Rasuna Said 50,000 For Lease Under Construction

2016 Centennial Tower Gatot Subroto 100,000 For Sale Under Construction

2016 Ciputra World Jakarta 2 Satrio 70,000 For Lease & Sale Under Construction

2016 Satrio Tower Satrio 31,604 For Lease Under Construction

2016 The Tower Gatot Subroto 56,492 For Sale Under Construction

2016 Lippo Thamrin Office Tower Thamrin 16,500 For Sale Under Construction

2016 T Tower (BJB Tower) Gatot Subroto 24,000 For Sale Under Construction

continued

8 Research & Forecast Report | 4Q 2014 | Office | Colliers International

New Supply Pipeline

projected completion oFFice Building projectS name location Sga marketing Scheme StatuS development

continuation

2017 Prosperity Tower @ Distict 8 Sudirman 71,545 For Sale Under Construction

2017 Gran Rubina Tower 2 Rasuna Said 32,000 For Sale Under Construction

2017 Sequis Life Tower 2 Sudirman 80,000 For Lease Under Construction

2017 Treasury Tower @ District 8 Sudirman 139,000 For Sale Under Construction

2017 Gayanti City Gatot Subroto 25,000 For Lease In Planning

2017 Sopo Del Tower A Mega Kuningan 80,000 For Lease & Sale Under Construction

2017 Sopo Del Tower B Mega Kuningan 40,000 For Lease Under Construction

2018 Sudirman 7.8 (ex Nugra Santana) Sudirman 52,000 For Sale In Planning

2018 SSI Tower (Graha Surya Intenusa) Rasuna Said 100,000 For Lease Under Construction

2018 Mangkuluhur Tower II Gatot Subroto 50,000 For Lease In Planning

2018 Tower Two at The City Center Sudirman 39,204 For Lease Under Construction

2018 World Trade Center III Sudirman 70,000 For Lease Under Construction

2018 Icon Tower Sudirman 72,500 For Lease Under Construction

2018 Tower 2 @ Ciputra World Jakarta 1 Satrio 70,000 For Lease & Sale Under Construction

2018 Astra Tower Sudirman 80,000 For Lease In Planning

2018 Thamrin Nine Thamrin 97,500 For Lease Under Construction

2018 Chitaland Gatot Subroto 100,000 For Lease In Planning

2019 The Hundred Mega Kuningan 35,000 For Lease In Planning

2019 SCBD Lot.10 (PCPD Tower) Sudirman 96,000 For Lease Under Construction

2019 World Capital Tower Mega Kuningan 72,000 For Sale Under Construction

2019 Gran Rubina Tower 2 Rasuna Said 32,000 For Sale In Planning

2019 Tower Three at The City Center Sudirman 34,000 For Lease In Planning

2019 Tower 1 at Sampoerna Strategic Square Sudirman 43,000 For Sale In Planning

2019 Tower 2 at Sampoerna Strategic Square Sudirman 118,000 For Lease In Planning

2019 Redevelopment at Sequis Center Sudirman 100,000 For Lease In Planning

2019 Redevelopment eX Thamrin 150,000 For Lease In Planning

2019 Pertamina Tower Rasuna Said 306,000 For Lease In Planning

outSide cBd eXcluding tB Simatupang

2015 Menara Sentraya Blok M 52,072 For Sale Under Construction

2015 ST Moritz Office Tower Puri Indah 19,500 For Sale Under Construction

2015 The Suites Pantai Indah Kapuk 13,200 For Sale Under Construction

2015 MNC Tower II Kebon Sirih 20,000 For Lease Under Construction

2015 Soho Capital Slipi 36,000 For Sale Under Construction

2015 Altira Sunter 40,000 For Sale Under Construction

2015 Maxima Tower Kelapa Gading 8,000 For Lease Under Construction

2015 Nariba Office Suites Mampang 4,200 For Lease Under Construction

2016 Puri Indah Financial Tower Puri Indah 38,500 For Sale In Planning

2016 Gallery West Kebun Jeruk 29,000 For Sale Under Construction

2016 Sky 18 Tower Pasar Minggu 27,500 For Sale Under Construction

2016 Soho Pancoran Pancoran 30,000 For Sale Under Construction

2016 Jakarta Box Tower Kebon Sirih 36,000 For Lease Under Construction

2016 Lippo Tower Holland Village Cempaka Putih 27,000 For Sale In Planning

2016 One Tower Kemayoran 21,400 For Sale In Planning

2016 BKP Office Tower Sunter 16,000 For Lease In Planning

2016 Tamansari Parama Wahid Hasyim 10,800 For Sale In Planning

continued

9 Research & Forecast Report | 4Q 2014 | Office | Colliers International

Source: Colliers International Indonesia - Research

Source: Colliers International Indonesia - Research

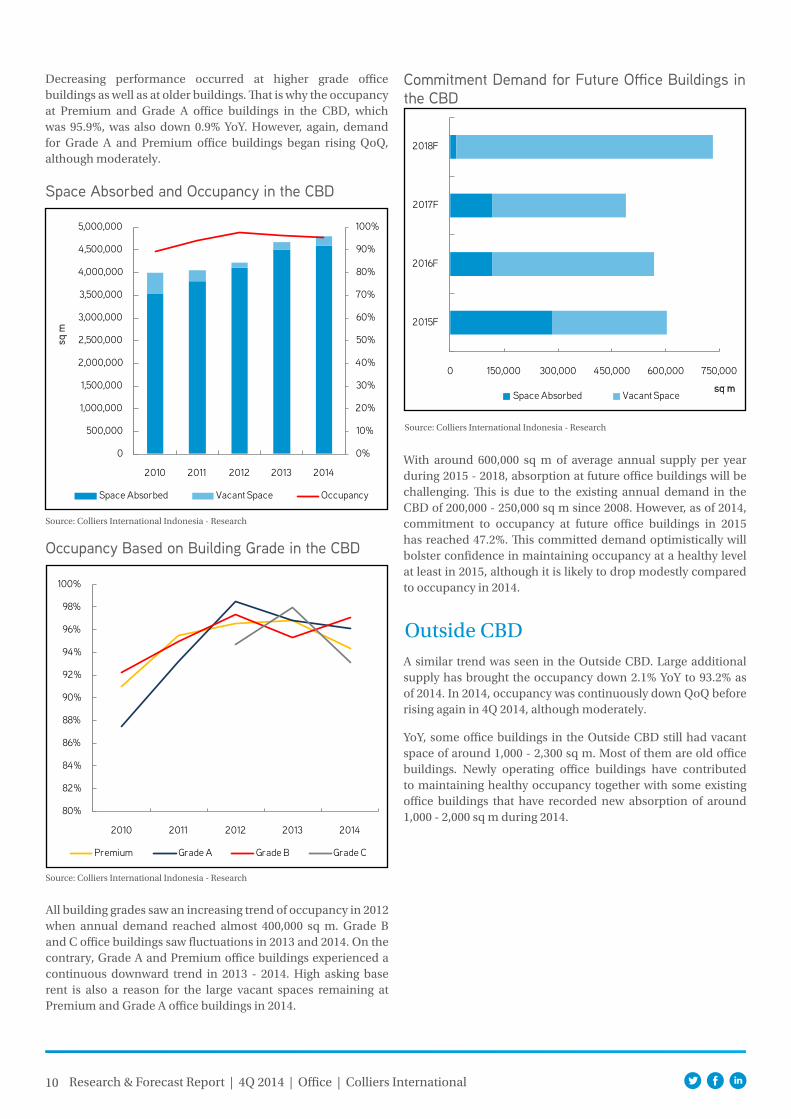

CBD2013 YoY 2014 QoQ 3Q 2014

96.5% 95.7% 95.4%

Demand and Occupancy Despite being down more than 1% YoY, occupancy saw a moderate increase QoQ. The election and the slowing economy have had a big impact on office demand in the CBD, especially from the end of 2013 to mid-2014. Some potential tenants preferred to wait and see and hold their expansion plans. Fortunately, the election ran smoothly and office demand began rising, albeit modestly.

During 2014, some office buildings experienced declining performance QoQ and there was more than 2,000 sq m of vacant space remaining. In a certain case, we noted that declining performance of an office building was caused by relocating tenants due to a change in ownership. Two examples of relocating large spaces of tenants in 2014 were recorded at office buildings in Gatot Subroto and Sudirman. Another office building in Sudirman also will relocate their tenants due to the landlord demolishing and redeveloping the existing office building.

CBD

Since it was at 97.2% in 2012, the highest on record in the CBD, the occupancy continued slumping to 95.4% in 2014. YoY, the occupancy was down 1.1%.

projected completion oFFice Building projectS name location Sga marketing Scheme StatuS development

continuation

outSide cBd eXcluding tB Simatupang

2016 BKP Office Tower Sunter 16,000 For Lease In Planning

2016 Tamansari Parama Wahid Hasyim 10,800 For Sale In Planning

2017 L'Office Pasar Minggu 41,597 For Sale Under Construction

2017 Ciputra Business District Kemayoran Tower 1 Kemayoran 40,000 For Sale In Planning

2017 Ciputra Business District Kemayoran Tower 2 Kemayoran 40,000 For Lease In Planning

2017 Ciputra International Puri 1 Phase 1 Puri 15,000 For Lease In Planning

2017 Ciputra International Puri 2 Phase 1 Puri 20,000 For Lease In Planning

2017 Ciputra International Puri 3 Phase 1 Puri 30,000 For Lease In Planning

2018 Kota Kasablanka Office Tower 2 Casablanca 90,000 For Lease In Planning

2018 Ciputra International Puri Phase 2 Puri 15,000 For Lease In Planning

2018 Ciputra International Puri 1 Phase 3 Puri 15,000 For Lease In Planning

2018 Ciputra Internatinal Puri 2 Phase 3 Puri 15,000 For Lease In Planning

2018 Summarecon Tower Slipi 70,000 For Lease In Planning

tB Simatupang

2015 Graha MRA 13,000 For Lease Under Construction

2015 Plaza Oleos 39,778 For Lease & Sale Under Construction

2015 18 Office Park (Cityland Tower) 40,000 For Sale Under Construction

2015 AD Premier 18,900 For Lease Under Construction

2015 Metropolitan Tower 44,000 For Lease & Sale Under Construction

2015 South Quarter Tower 1 40,778 For Sale Under Construction

2015 South Quarter Tower 2 40,778 For Lease Under Construction

2016 South Quarter Tower 3 40,778 For Lease Under Construction

2016 Zuria 6,584 For Lease Under Construction

2016 Cibis Tower 60,800 For Lease Under Construction

2017 Beltway Office Park Tower 4 30,839 For Lease Under Construction

2017 The Sima 60,000 For Lease Under Construction

2017 The Manhattan Square Tower 2 39,375 For Lease & Sale In Planning

2017 Arkadia Tower G 30,000 For Lease In Planning

10 Research & Forecast Report | 4Q 2014 | Office | Colliers International

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

5,000,000

2010 2011 2012 2013 2014

sq m

Space Absorbed Vacant Space Occupancy

Decreasing performance occurred at higher grade office buildings as well as at older buildings. That is why the occupancy at Premium and Grade A office buildings in the CBD, which was 95.9%, was also down 0.9% YoY. However, again, demand for Grade A and Premium office buildings began rising QoQ, although moderately.

Space Absorbed and Occupancy in the CBD

Source: Colliers International Indonesia - Research

Occupancy Based on Building Grade in the CBD

Source: Colliers International Indonesia - Research

80%

82%

84%

86%

88%

90%

92%

94%

96%

98%

100%

2010 2011 2012 2013 2014

Premium Grade A Grade B Grade C

All building grades saw an increasing trend of occupancy in 2012 when annual demand reached almost 400,000 sq m. Grade B and C office buildings saw fluctuations in 2013 and 2014. On the contrary, Grade A and Premium office buildings experienced a continuous downward trend in 2013 - 2014. High asking base rent is also a reason for the large vacant spaces remaining at Premium and Grade A office buildings in 2014.

Commitment Demand for Future Office Buildings in the CBD

Source: Colliers International Indonesia - Research

With around 600,000 sq m of average annual supply per year during 2015 - 2018, absorption at future office buildings will be challenging. This is due to the existing annual demand in the CBD of 200,000 - 250,000 sq m since 2008. However, as of 2014, commitment to occupancy at future office buildings in 2015 has reached 47.2%. This committed demand optimistically will bolster confidence in maintaining occupancy at a healthy level at least in 2015, although it is likely to drop modestly compared to occupancy in 2014.

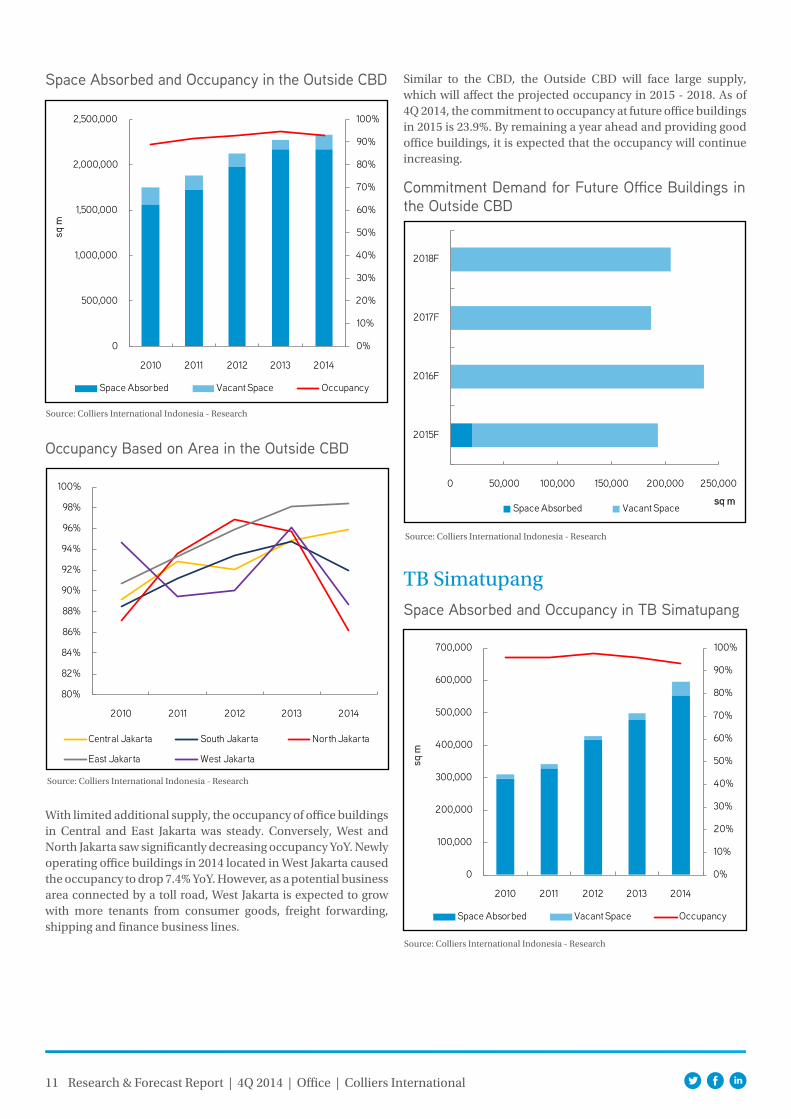

Outside CBDA similar trend was seen in the Outside CBD. Large additional supply has brought the occupancy down 2.1% YoY to 93.2% as of 2014. In 2014, occupancy was continuously down QoQ before rising again in 4Q 2014, although moderately.

YoY, some office buildings in the Outside CBD still had vacant space of around 1,000 - 2,300 sq m. Most of them are old office buildings. Newly operating office buildings have contributed to maintaining healthy occupancy together with some existing office buildings that have recorded new absorption of around 1,000 - 2,000 sq m during 2014.

0 150,000 300,000 450,000 600,000 750,000

2015F

2016F

2017F

2018F

sq mSpace Absorbed Vacant Space

11 Research & Forecast Report | 4Q 2014 | Office | Colliers International

0 50,000 100,000 150,000 200,000 250,000

2015F

2016F

2017F

2018F

sq mSpace Absorbed Vacant Space

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

2010 2011 2012 2013 2014

sq m

Space Absorbed Vacant Space Occupancy

Occupancy Based on Area in the Outside CBD

Source: Colliers International Indonesia - Research

80%

82%

84%

86%

88%

90%

92%

94%

96%

98%

100%

2010 2011 2012 2013 2014

Central Jakarta South Jakarta North Jakarta

East Jakarta West Jakarta

With limited additional supply, the occupancy of office buildings in Central and East Jakarta was steady. Conversely, West and North Jakarta saw significantly decreasing occupancy YoY. Newly operating office buildings in 2014 located in West Jakarta caused the occupancy to drop 7.4% YoY. However, as a potential business area connected by a toll road, West Jakarta is expected to grow with more tenants from consumer goods, freight forwarding, shipping and finance business lines.

Commitment Demand for Future Office Buildings in the Outside CBD

Source: Colliers International Indonesia - Research

TB SimatupangSpace Absorbed and Occupancy in TB Simatupang

Source: Colliers International Indonesia - Research

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

2010 2011 2012 2013 2014

sq m

Space Absorbed Vacant Space Occupancy

Space Absorbed and Occupancy in the Outside CBD

Source: Colliers International Indonesia - Research

Similar to the CBD, the Outside CBD will face large supply, which will affect the projected occupancy in 2015 - 2018. As of 4Q 2014, the commitment to occupancy at future office buildings in 2015 is 23.9%. By remaining a year ahead and providing good office buildings, it is expected that the occupancy will continue increasing.

12 Research & Forecast Report | 4Q 2014 | Office | Colliers International

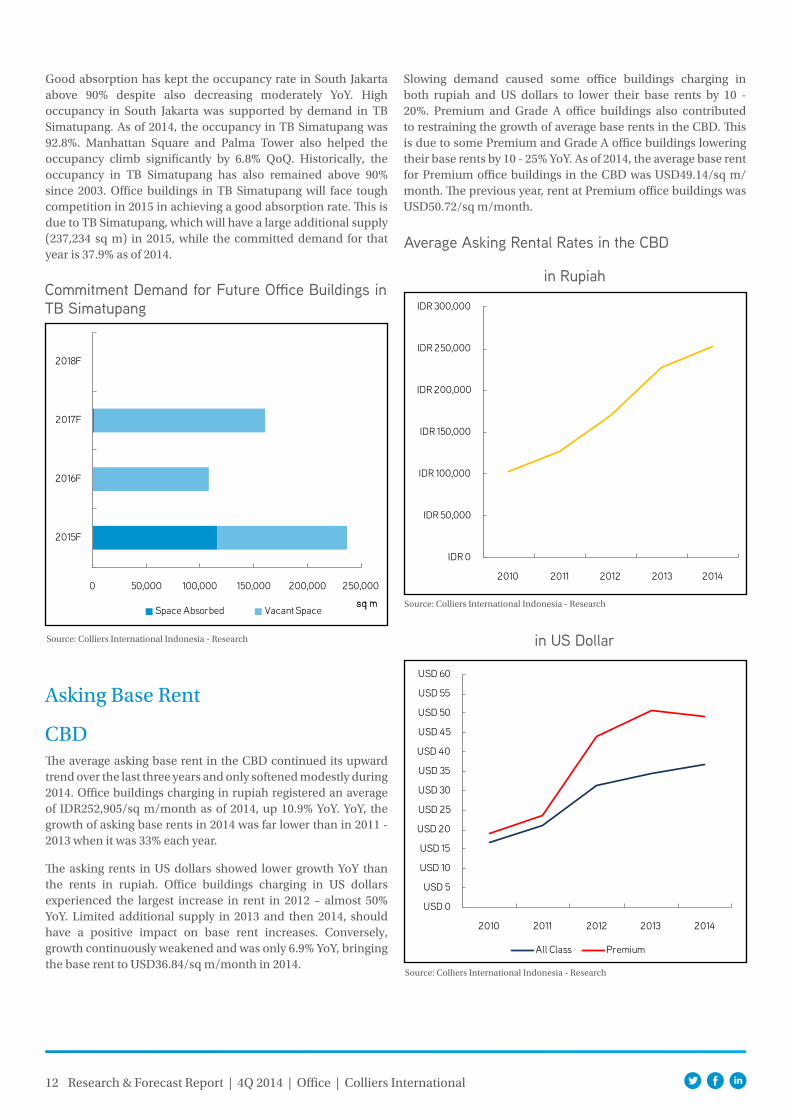

Good absorption has kept the occupancy rate in South Jakarta above 90% despite also decreasing moderately YoY. High occupancy in South Jakarta was supported by demand in TB Simatupang. As of 2014, the occupancy in TB Simatupang was 92.8%. Manhattan Square and Palma Tower also helped the occupancy climb significantly by 6.8% QoQ. Historically, the occupancy in TB Simatupang has also remained above 90% since 2003. Office buildings in TB Simatupang will face tough competition in 2015 in achieving a good absorption rate. This is due to TB Simatupang, which will have a large additional supply (237,234 sq m) in 2015, while the committed demand for that year is 37.9% as of 2014.

Commitment Demand for Future Office Buildings in TB Simatupang

Source: Colliers International Indonesia - Research

Asking Base Rent

CBDThe average asking base rent in the CBD continued its upward trend over the last three years and only softened modestly during 2014. Office buildings charging in rupiah registered an average of IDR252,905/sq m/month as of 2014, up 10.9% YoY. YoY, the growth of asking base rents in 2014 was far lower than in 2011 - 2013 when it was 33% each year.

The asking rents in US dollars showed lower growth YoY than the rents in rupiah. Office buildings charging in US dollars experienced the largest increase in rent in 2012 – almost 50% YoY. Limited additional supply in 2013 and then 2014, should have a positive impact on base rent increases. Conversely, growth continuously weakened and was only 6.9% YoY, bringing the base rent to USD36.84/sq m/month in 2014.

Slowing demand caused some office buildings charging in both rupiah and US dollars to lower their base rents by 10 - 20%. Premium and Grade A office buildings also contributed to restraining the growth of average base rents in the CBD. This is due to some Premium and Grade A office buildings lowering their base rents by 10 - 25% YoY. As of 2014, the average base rent for Premium office buildings in the CBD was USD49.14/sq m/month. The previous year, rent at Premium office buildings was USD50.72/sq m/month.

Average Asking Rental Rates in the CBD

in Rupiah

IDR 0

IDR 50,000

IDR 100,000

IDR 150,000

IDR 200,000

IDR 250,000

IDR 300,000

2010 2011 2012 2013 2014

in US Dollar

Source: Colliers International Indonesia - Research

USD 0

USD 5

USD 10

USD 15

USD 20

USD 25

USD 30

USD 35

USD 40

USD 45

USD 50

USD 55

USD 60

2010 2011 2012 2013 2014

All Class Premium

Source: Colliers International Indonesia - Research

0 50,000 100,000 150,000 200,000 250,000

2015F

2016F

2017F

2018F

sq mSpace Absorbed Vacant Space

13 Research & Forecast Report | 4Q 2014 | Office | Colliers International

Asking Base Rent Based on Grade

in Rupiah

in US Dollar

Source: Colliers International Indonesia - Research

Source: Colliers International Indonesia - Research

IDR 0

IDR 50,000

IDR 100,000

IDR 150,000

IDR 200,000

IDR 250,000

IDR 300,000

IDR 350,000

IDR 400,000

IDR 450,000

IDR 500,000

IDR 550,000

IDR 600,000

Grade A Grade B Grade C

USD 0.00

USD 5.00

USD 10.00

USD 15.00

USD 20.00

USD 25.00

USD 30.00

USD 35.00

USD 40.00

USD 45.00

USD 50.00

USD 55.00

USD 60.00

USD 65.00

USD 70.00

USD 75.00

Premium Grade A Grade B Grade C

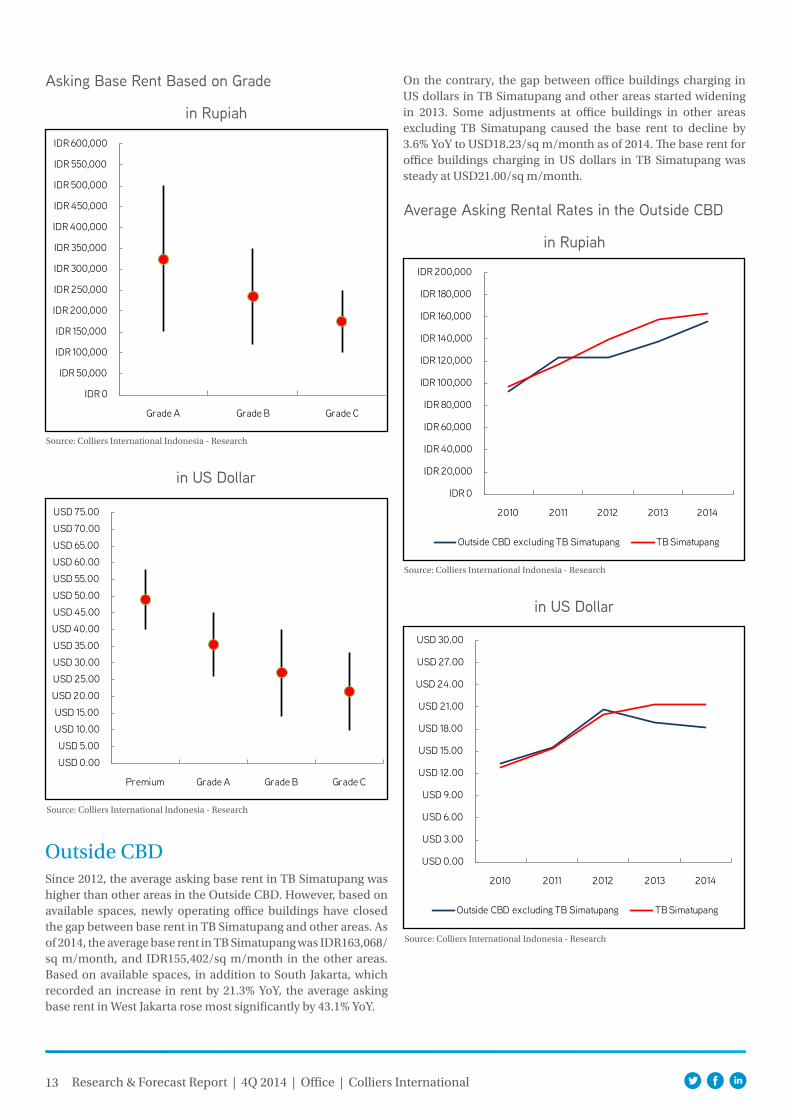

Outside CBDSince 2012, the average asking base rent in TB Simatupang was higher than other areas in the Outside CBD. However, based on available spaces, newly operating office buildings have closed the gap between base rent in TB Simatupang and other areas. As of 2014, the average base rent in TB Simatupang was IDR163,068/sq m/month, and IDR155,402/sq m/month in the other areas. Based on available spaces, in addition to South Jakarta, which recorded an increase in rent by 21.3% YoY, the average asking base rent in West Jakarta rose most significantly by 43.1% YoY.

On the contrary, the gap between office buildings charging in US dollars in TB Simatupang and other areas started widening in 2013. Some adjustments at office buildings in other areas excluding TB Simatupang caused the base rent to decline by 3.6% YoY to USD18.23/sq m/month as of 2014. The base rent for office buildings charging in US dollars in TB Simatupang was steady at USD21.00/sq m/month.

Average Asking Rental Rates in the Outside CBD

in Rupiah

in US Dollar

Source: Colliers International Indonesia - Research

Source: Colliers International Indonesia - Research

IDR 0

IDR 20,000

IDR 40,000

IDR 60,000

IDR 80,000

IDR 100,000

IDR 120,000

IDR 140,000

IDR 160,000

IDR 180,000

IDR 200,000

2010 2011 2012 2013 2014

Outside CBD excluding TB Simatupang TB Simatupang

USD 0.00

USD 3.00

USD 6.00

USD 9.00

USD 12.00

USD 15.00

USD 18.00

USD 21.00

USD 24.00

USD 27.00

USD 30.00

2010 2011 2012 2013 2014

Outside CBD excluding TB Simatupang TB Simatupang

14 Research & Forecast Report | 4Q 2014 | Office | Colliers International

0 100,000 200,000 300,000 400,000

2015F

2016F

2017F

sq m

Space Absorbed Vacant Space

Service Charge

Service Charges of Office Buildings in Jakarta

Source: Colliers International Indonesia - Research

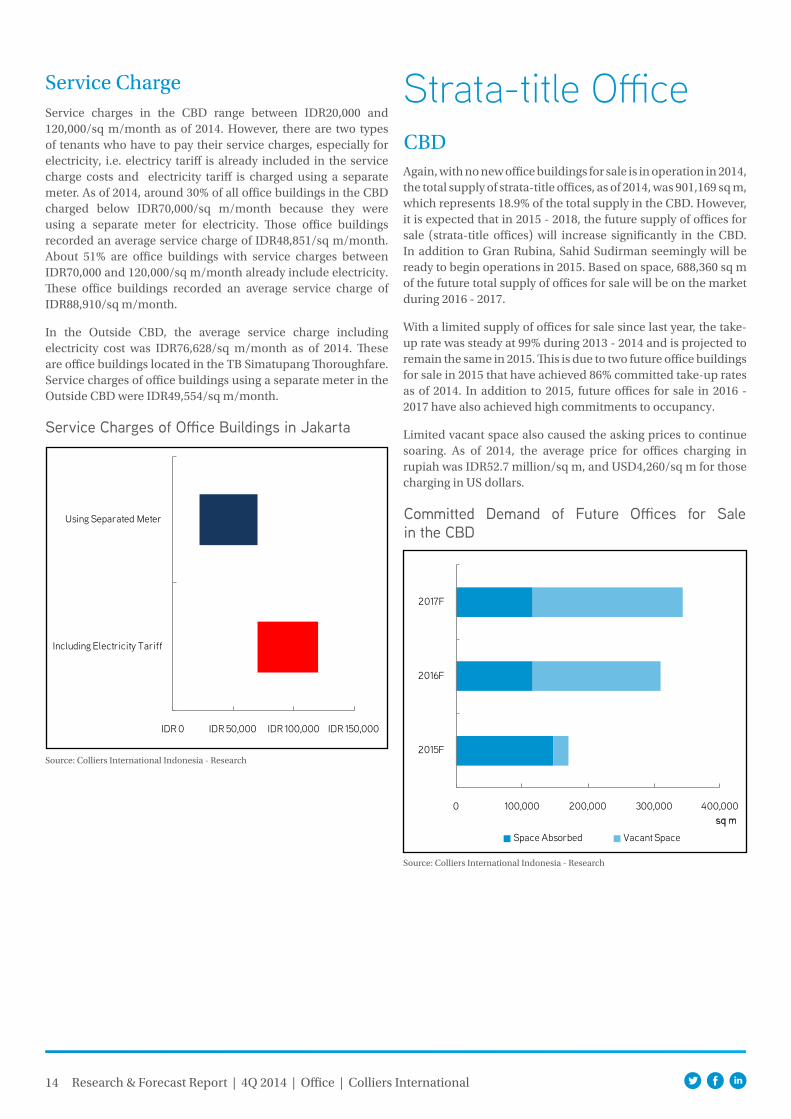

Service charges in the CBD range between IDR20,000 and 120,000/sq m/month as of 2014. However, there are two types of tenants who have to pay their service charges, especially for electricity, i.e. electricy tariff is already included in the service charge costs and electricity tariff is charged using a separate meter. As of 2014, around 30% of all office buildings in the CBD charged below IDR70,000/sq m/month because they were using a separate meter for electricity. Those office buildings recorded an average service charge of IDR48,851/sq m/month. About 51% are office buildings with service charges between IDR70,000 and 120,000/sq m/month already include electricity. These office buildings recorded an average service charge of IDR88,910/sq m/month.

In the Outside CBD, the average service charge including electricity cost was IDR76,628/sq m/month as of 2014. These are office buildings located in the TB Simatupang Thoroughfare. Service charges of office buildings using a separate meter in the Outside CBD were IDR49,554/sq m/month.

IDR 0 IDR 50,000 IDR 100,000 IDR 150,000

Including Electricity Tariff

Using Separated Meter

Strata-title Office

Committed Demand of Future Offices for Sale in the CBD

Source: Colliers International Indonesia - Research

Again, with no new office buildings for sale is in operation in 2014, the total supply of strata-title offices, as of 2014, was 901,169 sq m, which represents 18.9% of the total supply in the CBD. However, it is expected that in 2015 - 2018, the future supply of offices for sale (strata-title offices) will increase significantly in the CBD. In addition to Gran Rubina, Sahid Sudirman seemingly will be ready to begin operations in 2015. Based on space, 688,360 sq m of the future total supply of offices for sale will be on the market during 2016 - 2017.

With a limited supply of offices for sale since last year, the take-up rate was steady at 99% during 2013 - 2014 and is projected to remain the same in 2015. This is due to two future office buildings for sale in 2015 that have achieved 86% committed take-up rates as of 2014. In addition to 2015, future offices for sale in 2016 - 2017 have also achieved high commitments to occupancy.

Limited vacant space also caused the asking prices to continue soaring. As of 2014, the average price for offices charging in rupiah was IDR52.7 million/sq m, and USD4,260/sq m for those charging in US dollars.

CBD

15 Research & Forecast Report | 4Q 2014 | Office | Colliers International

0 50,000 100,000 150,000 200,000250,000300,000350,000

2015F

2016F

2017F

sq m

Space Absorbed Vacant Space

During 2014, the Outside CBD area provided more strata-title offices for sale than the CBD. Three office buildings for sale were in operation in 2014, namely Green Kosmo Mansion, The Manhattan Square and GP Plaza. GP Plaza is the latest office building that began operation since 2014 and is located in Slipi, West Jakarta. This office building provides small office spaces for sale, which are integrated into an apartment development.

With the influx of new additional strata-title office buildings, the take-up rate of offices for sale in the Outside CBD remained high and was 93.6% in 2014. It is expected that a large future supply will come in 2015 - 2016 in the Outside CBD and will have an effect on the projected take-up rate. However, by achieving 74 and 64% of pre-committed absorption in 2014 and 2015, respectively, the projected take-up rate is expected to continue to rise in 2015.

TB Simatupang has become the greatest contributor of demand for strata-title offices in the Outside CBD. As of 2014, almost 70% of 161,377 sq m of total future offices for sale in TB Simatupang in 2014 - 2015 has been absorbed.

Committed Demand for Future Offices for Sale in the Outside CBD

Source: Colliers International Indonesia - Research

Outside CBD

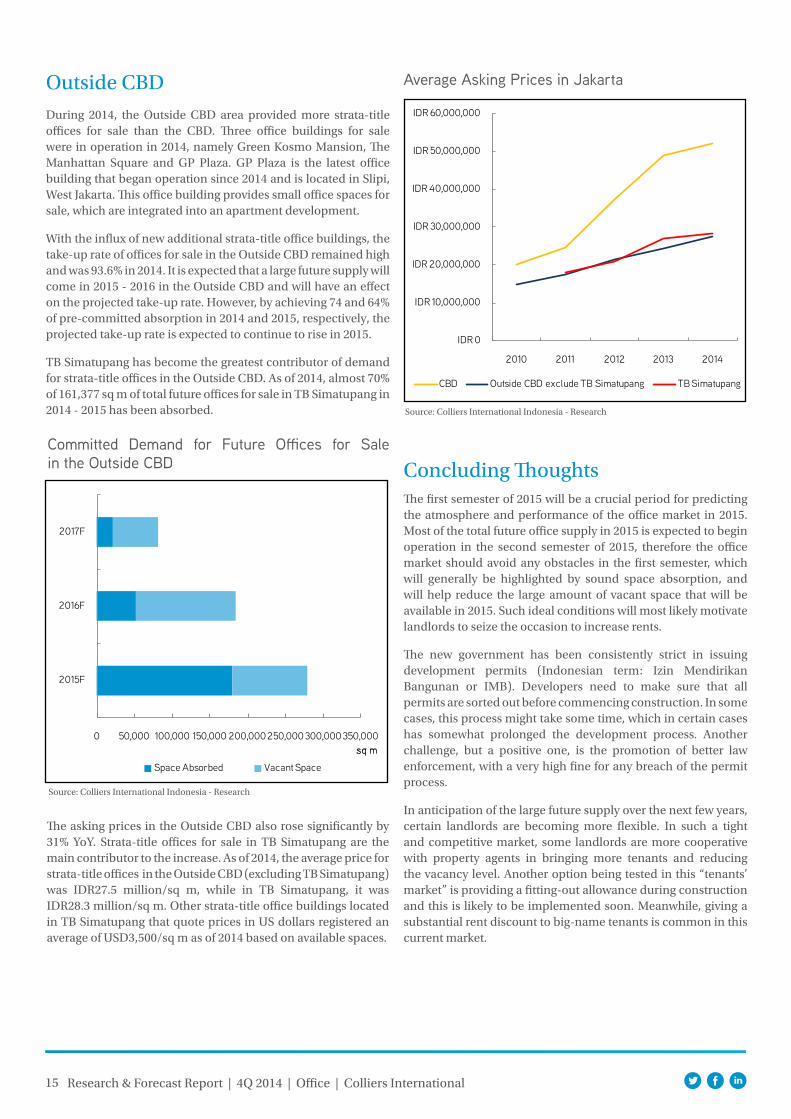

The asking prices in the Outside CBD also rose significantly by 31% YoY. Strata-title offices for sale in TB Simatupang are the main contributor to the increase. As of 2014, the average price for strata-title offices in the Outside CBD (excluding TB Simatupang) was IDR27.5 million/sq m, while in TB Simatupang, it was IDR28.3 million/sq m. Other strata-title office buildings located in TB Simatupang that quote prices in US dollars registered an average of USD3,500/sq m as of 2014 based on available spaces.

Average Asking Prices in Jakarta

Source: Colliers International Indonesia - Research

IDR 0

IDR 10,000,000

IDR 20,000,000

IDR 30,000,000

IDR 40,000,000

IDR 50,000,000

IDR 60,000,000

2010 2011 2012 2013 2014

CBD Outside CBD exclude TB Simatupang TB Simatupang

Concluding ThoughtsThe first semester of 2015 will be a crucial period for predicting the atmosphere and performance of the office market in 2015. Most of the total future office supply in 2015 is expected to begin operation in the second semester of 2015, therefore the office market should avoid any obstacles in the first semester, which will generally be highlighted by sound space absorption, and will help reduce the large amount of vacant space that will be available in 2015. Such ideal conditions will most likely motivate landlords to seize the occasion to increase rents.

The new government has been consistently strict in issuing development permits (Indonesian term: Izin Mendirikan Bangunan or IMB). Developers need to make sure that all permits are sorted out before commencing construction. In some cases, this process might take some time, which in certain cases has somewhat prolonged the development process. Another challenge, but a positive one, is the promotion of better law enforcement, with a very high fine for any breach of the permit process.

In anticipation of the large future supply over the next few years, certain landlords are becoming more flexible. In such a tight and competitive market, some landlords are more cooperative with property agents in bringing more tenants and reducing the vacancy level. Another option being tested in this “tenants’ market” is providing a fitting-out allowance during construction and this is likely to be implemented soon. Meanwhile, giving a substantial rent discount to big-name tenants is common in this current market.

16 Research & Forecast Report | 4Q 2014 | Apartment | Colliers International

Apartment SectorApartment for Strata-title

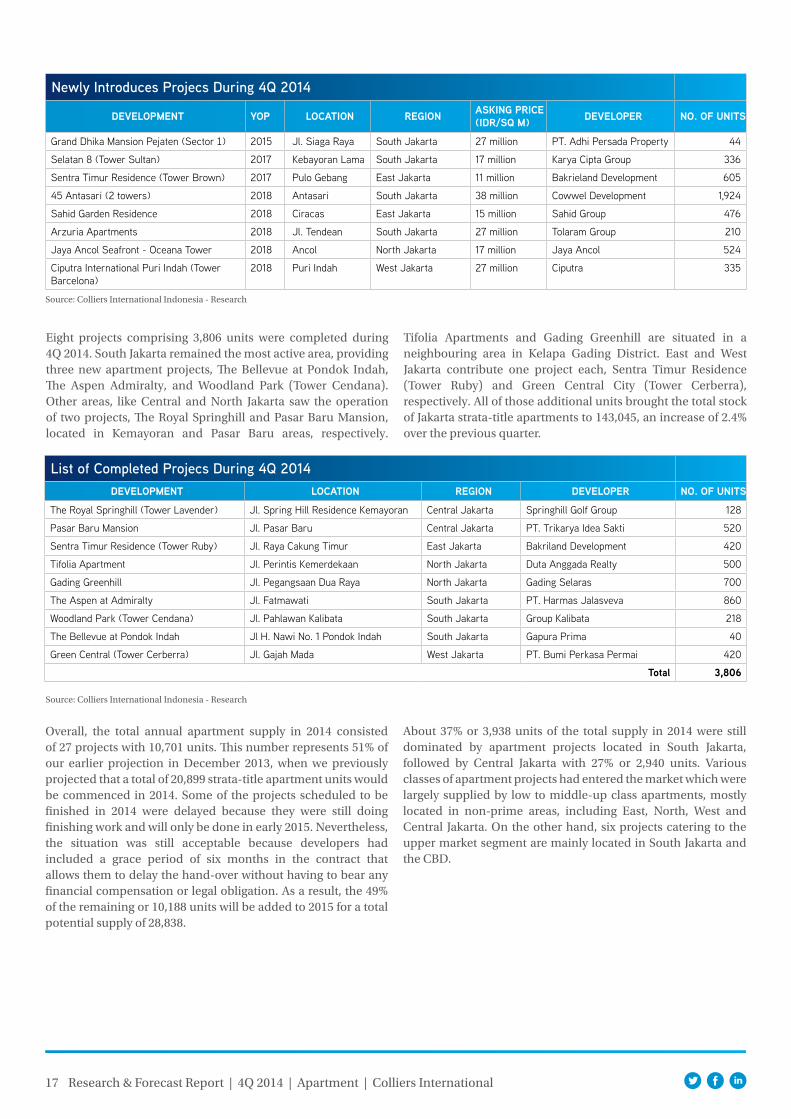

SupplyEntering the last quarter of 2014, the Jakarta apartment market remained upbeat, evidenced by the number of units launched this quarter that outstripped the number of units launched in the last three consecutive quarters. A large number of developers generally had a positive perception of apartment market performance during the post-election period. They continued to introduce new projects targeting various market segments. Between October and December, eight new strata-title apartment projects were introduced in Jakarta, bringing a total of 4,454 units to the market. The volume of newly launched/introduced apartments almost tripled from 1,319 in 3Q 2014 to 4,454 units this quarter. Some of these were the extensions (additional towers) of operating projects such as Sentra Timur Residence (Tower Brown) and Ciputra International Puri Indah (Tower Barcelona). The other six are brand new developments like Grand Dhika Mansion Pejaten (Sector I), 45 Antasari, Selatan 8 (Tower Sultan), Sahid Garden Residence, Arzuria Apartments and Jaya Ancol Seafront (Tower Oceana).

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

1Q 2013

2Q 2013

3Q 2013

4Q 2013

1Q 2014

2Q 2014

3Q 2014

4Q 2014

units

Source: Colliers International Indonesia - Research

Newly Introduce Apartment Units in Every Quarter of 2013 - 2014

17 Research & Forecast Report | 4Q 2014 | Apartment | Colliers International

Source: Colliers International Indonesia - Research

Newly Introduces Projecs During 4Q 2014

development Yop location region aSking price (idr/SQ m) developer no. oF unitS

Grand Dhika Mansion Pejaten (Sector 1) 2015 Jl. Siaga Raya South Jakarta 27 million PT. Adhi Persada Property 44

Selatan 8 (Tower Sultan) 2017 Kebayoran Lama South Jakarta 17 million Karya Cipta Group 336

Sentra Timur Residence (Tower Brown) 2017 Pulo Gebang East Jakarta 11 million Bakrieland Development 605

45 Antasari (2 towers) 2018 Antasari South Jakarta 38 million Cowwel Development 1,924

Sahid Garden Residence 2018 Ciracas East Jakarta 15 million Sahid Group 476

Arzuria Apartments 2018 Jl. Tendean South Jakarta 27 million Tolaram Group 210

Jaya Ancol Seafront - Oceana Tower 2018 Ancol North Jakarta 17 million Jaya Ancol 524

Ciputra International Puri Indah (Tower Barcelona)

2018 Puri Indah West Jakarta 27 million Ciputra 335

Eight projects comprising 3,806 units were completed during 4Q 2014. South Jakarta remained the most active area, providing three new apartment projects, The Bellevue at Pondok Indah, The Aspen Admiralty, and Woodland Park (Tower Cendana). Other areas, like Central and North Jakarta saw the operation of two projects, The Royal Springhill and Pasar Baru Mansion, located in Kemayoran and Pasar Baru areas, respectively.

Tifolia Apartments and Gading Greenhill are situated in a neighbouring area in Kelapa Gading District. East and West Jakarta contribute one project each, Sentra Timur Residence (Tower Ruby) and Green Central City (Tower Cerberra), respectively. All of those additional units brought the total stock of Jakarta strata-title apartments to 143,045, an increase of 2.4% over the previous quarter.

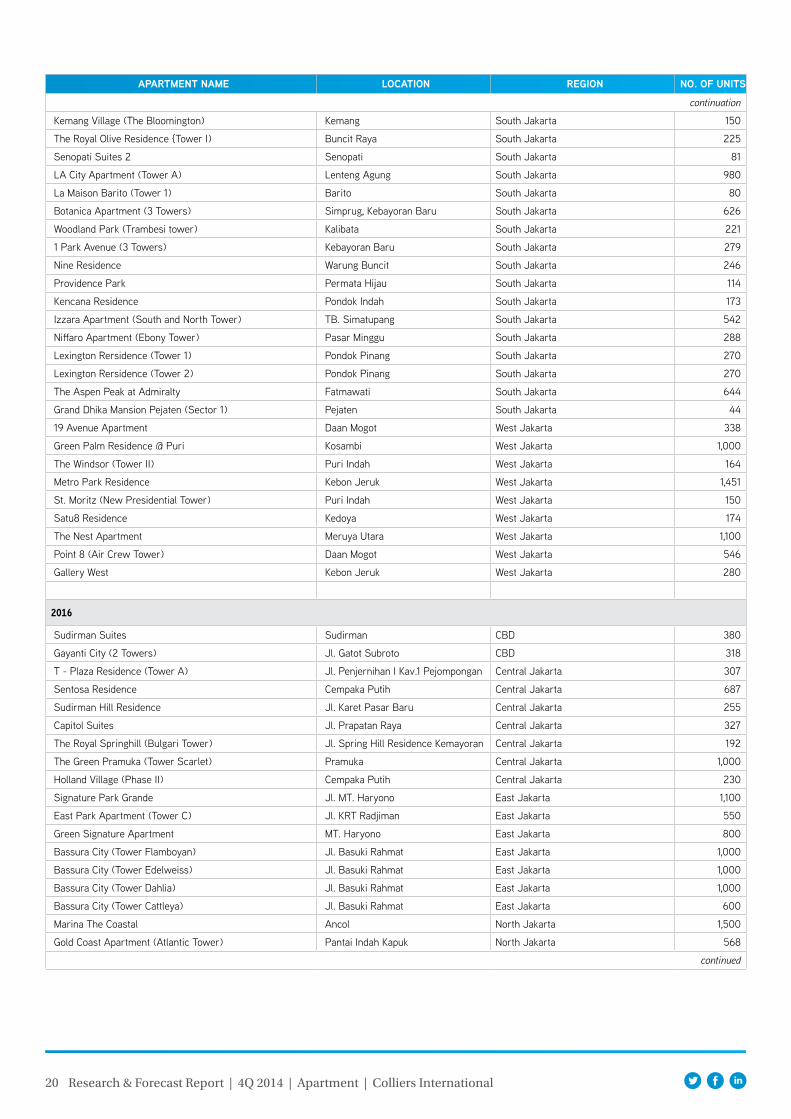

Overall, the total annual apartment supply in 2014 consisted of 27 projects with 10,701 units. This number represents 51% of our earlier projection in December 2013, when we previously projected that a total of 20,899 strata-title apartment units would be commenced in 2014. Some of the projects scheduled to be finished in 2014 were delayed because they were still doing finishing work and will only be done in early 2015. Nevertheless, the situation was still acceptable because developers had included a grace period of six months in the contract that allows them to delay the hand-over without having to bear any financial compensation or legal obligation. As a result, the 49% of the remaining or 10,188 units will be added to 2015 for a total potential supply of 28,838.

About 37% or 3,938 units of the total supply in 2014 were still dominated by apartment projects located in South Jakarta, followed by Central Jakarta with 27% or 2,940 units. Various classes of apartment projects had entered the market which were largely supplied by low to middle-up class apartments, mostly located in non-prime areas, including East, North, West and Central Jakarta. On the other hand, six projects catering to the upper market segment are mainly located in South Jakarta and the CBD.

Source: Colliers International Indonesia - Research

List of Completed Projecs During 4Q 2014development location region developer no. oF unitS

The Royal Springhill (Tower Lavender) Jl. Spring Hill Residence Kemayoran Central Jakarta Springhill Golf Group 128

Pasar Baru Mansion Jl. Pasar Baru Central Jakarta PT. Trikarya Idea Sakti 520

Sentra Timur Residence (Tower Ruby) Jl. Raya Cakung Timur East Jakarta Bakriland Development 420

Tifolia Apartment Jl. Perintis Kemerdekaan North Jakarta Duta Anggada Realty 500

Gading Greenhill Jl. Pegangsaan Dua Raya North Jakarta Gading Selaras 700

The Aspen at Admiralty Jl. Fatmawati South Jakarta PT. Harmas Jalasveva 860

Woodland Park (Tower Cendana) Jl. Pahlawan Kalibata South Jakarta Group Kalibata 218

The Bellevue at Pondok Indah Jl H. Nawi No. 1 Pondok Indah South Jakarta Gapura Prima 40

Green Central (Tower Cerberra) Jl. Gajah Mada West Jakarta PT. Bumi Perkasa Permai 420

total 3,806

18

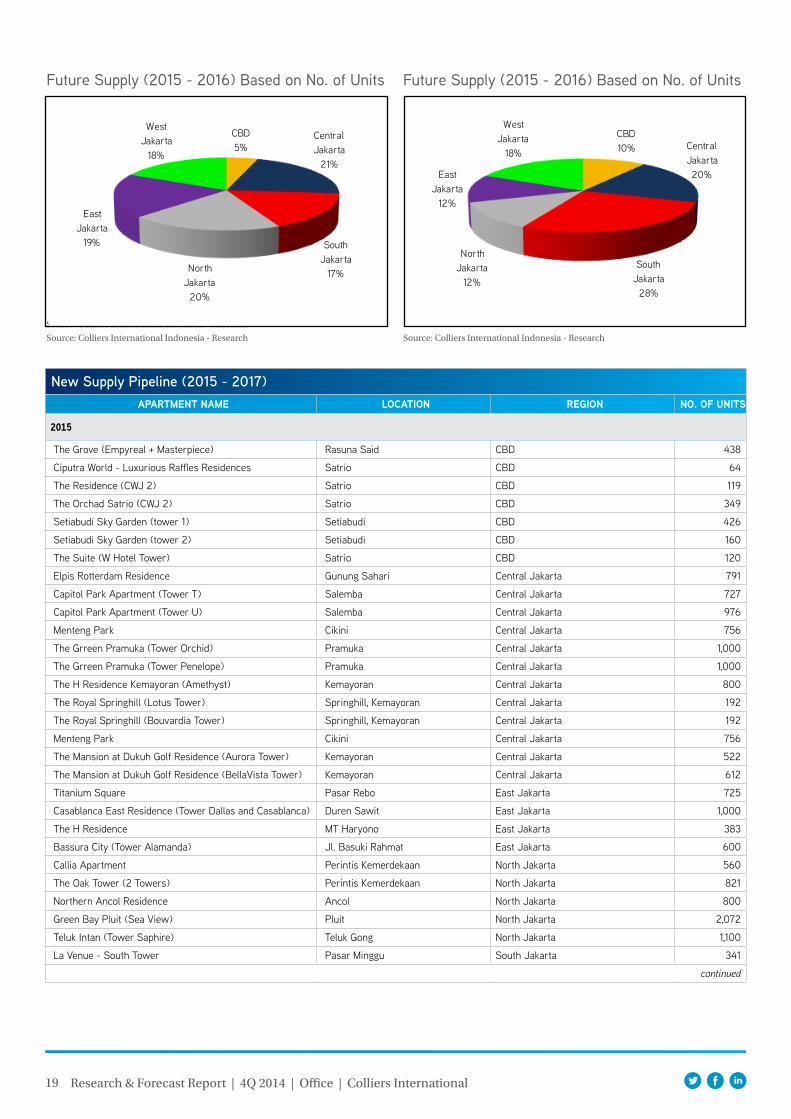

Analysis of Apartment Market in 2015 - 2016We anticipate further supply growth from 2015 to 2016 with an additional 47,269 units (of which 22% are scheduled to be on the market in 2016). Most future apartments will be concentrated in the areas outside of the CBD, such as Central Jakarta (the areas that are not part of the CBD like Kemayoran, Salemba or Cempaka Putih), East Jakarta, and North Jakarta. The largest amount of supply will come from Central Jakarta, targeted at young families and workers, taking advantage

of the proximity to the downtown and commercial area, where there are malls, business district and offices. Benefitting from the strategic location and easy access to public transport, the leasing market has the potential to be robust. Being a very active market location, South Jakarta continues to witness plenty of apartment projects in the pipeline for the next two years with a total of 25 projects consisting of 7,462 units.

Source: Colliers International Indonesia - Research

List of All New Apartment Projects in 2014development location region developer no. oF unitS

Ambassade Residence Tower A Jl. Puri Denpasar CBD PT Duta Regency 234

MyHome Apartment at Ciputra World Jl. Prof Dr Satrio CBD PT Ciputra Property Tbk 136

Verde Apartment (Tower East) Jl. HR. Rasuna Said CBD Farpoint Realty 114

Pasar Baru Mansion Jl. Pasar Baru Central Jakarta PT Trikarya Idea Sakti 520

The Green Pramuka (Tower Chrysant) Jl. Jenderal Ahmad Yani Central Jakarta PT Duta Paramindo 1,000

The Green Pramuka (Tower Bougenville) Jl. Jenderal Ahmad Yani Central Jakarta PT Duta Paramindo 1,000

The Royal Springhill (Tower Lavender) Jl. Spring Hill Residence Kemayoran Central Jakarta Springhill Golf Group 128

Sentra Timur Residence (Tower Ruby) Jl. Raya Cakung Timur East Jakarta Bakrieland Development 420

Sentra Timur Residence (Tower Orange) Jl. Pulo Gebang East Jakarta Bakrieland Development 390

The Hive @ Tamansari Jl. DI Panjaitan East Jakarta Wika Realty 422

Sherwood Residence (Tower Wellington) Kelapa Gading North Jakarta Summarecon 100

Sherwood Residence (Tower Regent) Kelapa Gading North Jakarta Summarecon 100

Tifolia Apartment Jl. Perintis Kemerdekaan North Jakarta Duta Anggada Realty 500

Gading Greenhill Jl. Pegangsaan Dua Raya North Jakarta Gading Selaras 700

Kemang Village (Tower The Intercon) Jl. P Antasari South Jakarta Lippo Karawaci 400

Kemang Village (Tower The Infinity) Jl. P Antasari South Jakarta Lippo Karawaci 175

The East at Essence Dharmawangsa Jl. Dharmawangsa X South Jakarta PT Prakarsa Semesta Alam 244

The Aspen at Admiralty Jl. Fatmawati South Jakarta PT Harmas Jalasveva 860

Woodland Park (Tower Cendana) Jl. Pahlawan Kalibata South Jakarta PT Pardika Wisthi Sarana 218

Pakubuwono Terrace (Tower North) Jl. Kebayoran Lama South Jakarta PT Selaras Mitra Sejati 750

Pakubuwono Terrace (Tower South) Jl. Kebayoran Lama South Jakarta PT Selaras Mitra Sejati 720

The Pakubuwono Signature Jl. Teuku Nyak Syarief South Jakarta PT Mandiri Eka Abadi 188

Woodland Park (Tower Matoa) Jl. Pahlawan Kalibata South Jakarta PT Pardika Wisthi Sarana 221

The Bellevue at Pondok Indah Jl H. Nawi No. 1 South Jakarta Gapura Prima 40

Green Central City (Tower Cerberra) Jl. Gajah Mada West Jakarta PT Bumi Perkasa Permai 420

The Windsor (Tower I) Jl. Puri Indah West Jakarta PT Antilope Madju Puri Indah 176

Sky Terrace Lagoon Jl. Tampak Siring, Kalideres West Jakarta Fajar Surya Perkasa 525

19

New Supply Pipeline (2015 - 2017)apartment name location region no. oF unitS

2015

The Grove (Empyreal + Masterpiece) Rasuna Said CBD 438

Ciputra World - Luxurious Raffles Residences Satrio CBD 64

The Residence (CWJ 2) Satrio CBD 119

The Orchad Satrio (CWJ 2) Satrio CBD 349

Setiabudi Sky Garden (tower 1) Setiabudi CBD 426

Setiabudi Sky Garden (tower 2) Setiabudi CBD 160

The Suite (W Hotel Tower) Satrio CBD 120

Elpis Rotterdam Residence Gunung Sahari Central Jakarta 791

Capitol Park Apartment (Tower T) Salemba Central Jakarta 727

Capitol Park Apartment (Tower U) Salemba Central Jakarta 976

Menteng Park Cikini Central Jakarta 756

The Grreen Pramuka (Tower Orchid) Pramuka Central Jakarta 1,000

The Grreen Pramuka (Tower Penelope) Pramuka Central Jakarta 1,000

The H Residence Kemayoran (Amethyst) Kemayoran Central Jakarta 800

The Royal Springhill (Lotus Tower) Springhill, Kemayoran Central Jakarta 192

The Royal Springhill (Bouvardia Tower) Springhill, Kemayoran Central Jakarta 192

Menteng Park Cikini Central Jakarta 756

The Mansion at Dukuh Golf Residence (Aurora Tower) Kemayoran Central Jakarta 522

The Mansion at Dukuh Golf Residence (BellaVista Tower) Kemayoran Central Jakarta 612

Titanium Square Pasar Rebo East Jakarta 725

Casablanca East Residence (Tower Dallas and Casablanca) Duren Sawit East Jakarta 1,000

The H Residence MT Haryono East Jakarta 383

Bassura City (Tower Alamanda) Jl. Basuki Rahmat East Jakarta 600

Callia Apartment Perintis Kemerdekaan North Jakarta 560

The Oak Tower (2 Towers) Perintis Kemerdekaan North Jakarta 821

Northern Ancol Residence Ancol North Jakarta 800

Green Bay Pluit (Sea View) Pluit North Jakarta 2,072

Teluk Intan (Tower Saphire) Teluk Gong North Jakarta 1,100

La Venue - South Tower Pasar Minggu South Jakarta 341

continued

Research & Forecast Report | 4Q 2014 | Office | Colliers International

Source: Colliers International Indonesia - Research

Future Supply (2015 - 2016) Based on No. of Units

CBD5%

Central Jakarta

21%

South Jakarta

17%North Jakarta

20%

East Jakarta

19%

West Jakarta

18%

Future Supply (2015 - 2016) Based on No. of Units

CBD10% Central

Jakarta20%

South Jakarta

28%

North Jakarta

12%

East Jakarta

12%

West Jakarta

18%

Source: Colliers International Indonesia - Research Source: Colliers International Indonesia - Research

20 Research & Forecast Report | 4Q 2014 | Apartment | Colliers International

apartment name location region no. oF unitS

continuation

Kemang Village (The Bloomington) Kemang South Jakarta 150

The Royal Olive Residence {Tower I) Buncit Raya South Jakarta 225

Senopati Suites 2 Senopati South Jakarta 81

LA City Apartment (Tower A) Lenteng Agung South Jakarta 980

La Maison Barito (Tower 1) Barito South Jakarta 80

Botanica Apartment (3 Towers) Simprug, Kebayoran Baru South Jakarta 626

Woodland Park (Trambesi tower) Kalibata South Jakarta 221

1 Park Avenue (3 Towers) Kebayoran Baru South Jakarta 279

Nine Residence Warung Buncit South Jakarta 246

Providence Park Permata Hijau South Jakarta 114

Kencana Residence Pondok Indah South Jakarta 173

Izzara Apartment (South and North Tower) TB. Simatupang South Jakarta 542

Niffaro Apartment (Ebony Tower) Pasar Minggu South Jakarta 288

Lexington Rersidence (Tower 1) Pondok Pinang South Jakarta 270

Lexington Rersidence (Tower 2) Pondok Pinang South Jakarta 270

The Aspen Peak at Admiralty Fatmawati South Jakarta 644

Grand Dhika Mansion Pejaten (Sector 1) Pejaten South Jakarta 44

19 Avenue Apartment Daan Mogot West Jakarta 338

Green Palm Residence @ Puri Kosambi West Jakarta 1,000

The Windsor (Tower II) Puri Indah West Jakarta 164

Metro Park Residence Kebon Jeruk West Jakarta 1,451

St. Moritz (New Presidential Tower) Puri Indah West Jakarta 150

Satu8 Residence Kedoya West Jakarta 174

The Nest Apartment Meruya Utara West Jakarta 1,100

Point 8 (Air Crew Tower) Daan Mogot West Jakarta 546

Gallery West Kebon Jeruk West Jakarta 280

2016

Sudirman Suites Sudirman CBD 380

Gayanti City (2 Towers) Jl. Gatot Subroto CBD 318

T - Plaza Residence (Tower A) Jl. Penjernihan I Kav.1 Pejompongan Central Jakarta 307

Sentosa Residence Cempaka Putih Central Jakarta 687

Sudirman Hill Residence Jl. Karet Pasar Baru Central Jakarta 255

Capitol Suites Jl. Prapatan Raya Central Jakarta 327

The Royal Springhill (Bulgari Tower) Jl. Spring Hill Residence Kemayoran Central Jakarta 192

The Green Pramuka (Tower Scarlet) Pramuka Central Jakarta 1,000

Holland Village (Phase II) Cempaka Putih Central Jakarta 230

Signature Park Grande Jl. MT. Haryono East Jakarta 1,100

East Park Apartment (Tower C) Jl. KRT Radjiman East Jakarta 550

Green Signature Apartment MT. Haryono East Jakarta 800

Bassura City (Tower Flamboyan) Jl. Basuki Rahmat East Jakarta 1,000

Bassura City (Tower Edelweiss) Jl. Basuki Rahmat East Jakarta 1,000

Bassura City (Tower Dahlia) Jl. Basuki Rahmat East Jakarta 1,000

Bassura City (Tower Cattleya) Jl. Basuki Rahmat East Jakarta 600

Marina The Coastal Ancol North Jakarta 1,500

Gold Coast Apartment (Atlantic Tower) Pantai Indah Kapuk North Jakarta 568

continued

21 Research & Forecast Report | 4Q 2014 | Apartment | Colliers International

apartment name location region no. oF unitS

continuation

Pluit Seaview (Tower Maldives) Pluit North Jakarta 940

Pluit Seaview (Tower Belize) Pluit North Jakarta 300

La Venue - North Tower Jl. Pasar Minggu South Jakarta 253

Senopati Suites 3 Jl. Senopati South Jakarta 54

Pakubuwono Terrace Grand Tower Kebayoran Lama South Jakarta 435

Apartment Pejaten Park Residence Jl. Warung Buncit Raya No.21 South Jakarta 560

Four Winds Jl. Permata Hijau Raya No.1 South Jakarta 122

Bellevue Place MT Haryono, Tebet South Jakarta 208

Kebayoran Icon Jl. Ciledug Raya South Jakarta 256

Belmont Residence (TowerAthena) Jl. Meruya Ilir West Jakarta 165

Puri Mansion Apartment (Tower A) Puri Mansion West Jakarta 900

Madison Park Tanjung Duren West Jakarta 1,200

Veranda Jl. Pesanggrahan Raya, Kembangan West Jakarta 174

St Moritz (The New Ambassador Suite Tower) Jl. Puri Indah Kembangan West Jakarta 200

Belmont Residence (Tower Montblanc) Meruya Ilir West Jakarta 350

Gianetti Apartment Kemanggisan West Jakarta 500

Source: Colliers International Indonesia - Research

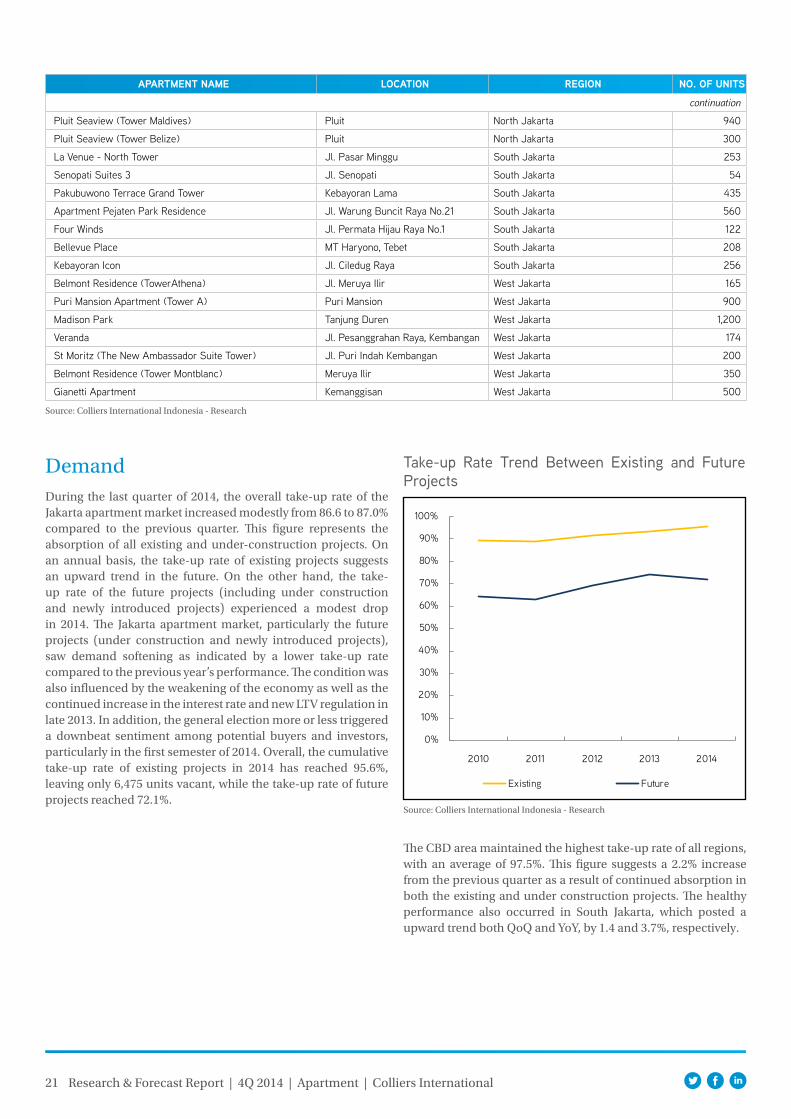

DemandDuring the last quarter of 2014, the overall take-up rate of the Jakarta apartment market increased modestly from 86.6 to 87.0% compared to the previous quarter. This figure represents the absorption of all existing and under-construction projects. On an annual basis, the take-up rate of existing projects suggests an upward trend in the future. On the other hand, the take-up rate of the future projects (including under construction and newly introduced projects) experienced a modest drop in 2014. The Jakarta apartment market, particularly the future projects (under construction and newly introduced projects), saw demand softening as indicated by a lower take-up rate compared to the previous year’s performance. The condition was also influenced by the weakening of the economy as well as the continued increase in the interest rate and new LTV regulation in late 2013. In addition, the general election more or less triggered a downbeat sentiment among potential buyers and investors, particularly in the first semester of 2014. Overall, the cumulative take-up rate of existing projects in 2014 has reached 95.6%, leaving only 6,475 units vacant, while the take-up rate of future projects reached 72.1%.

Take-up Rate Trend Between Existing and Future Projects

Source: Colliers International Indonesia - Research

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013 2014

Existing Future

The CBD area maintained the highest take-up rate of all regions, with an average of 97.5%. This figure suggests a 2.2% increase from the previous quarter as a result of continued absorption in both the existing and under construction projects. The healthy performance also occurred in South Jakarta, which posted a upward trend both QoQ and YoY, by 1.4 and 3.7%, respectively.

22

High demand for apartments in the CBD and South Jakarta area was driven mostly by investors who are quite optimistic about business prospects in the coming years. This, in turn, will potentially lead to the creation of more leasing demand, especially from the expatriate market. Moreover, the growth of the TB Simatupang area in South Jakarta, as a prominent business location for many multinational companies, has become a pull factor attracting investors to buy apartment units, which contributed to the sound performance of apartment projects located in the surrounding area.

In contrast to the CBD and South Jakarta area, the non-prime areas, including Central, West, East and North Jakarta, experienced sluggish performance due to the abundance of newly introduced apartment projects that exceeded the consistent absorption. This became the main factor affecting the downswing of the take-up rate to 83.4% over the reviewed quarter. The massive number of units from mid-low to lower apartment projects created a more competitive market and curbed potential growth of the take-up rate in the non-prime areas. On another front, apartment projects that provide a better concept, good building quality and design, and which are adjacent to public facilities and developed by reputable developers, are expected to generate sales in the upcoming quarters.

Research & Forecast Report | 4Q 2014 | Apartment | Colliers International

Source: Colliers International Indonesia - Research

Average Take-up Rate Performance in Different Locations

area 4Q 2013 3Q 2014 4Q 2014change

QoQ YoY

CBD 97.10% 95.30% 97.50% 2.20% 0.40%

South Jakarta 88.90% 91.20% 92.60% 1.40% 3.70%

Non-prime area 83.10% 83.60% 83.40% -0.20% 0.30%

Together with 26.2% of the population aged below 15, Indonesia has a huge pool of productive workers to draw upon over the long term.

Some attractive payment methods are still being used in order to attract more buyers during this challenging period, especially after the implementation of the new LTV regulation last year. Some of those methods are nil down payment without interest rate, balloon payment or longer period of instalments that have been acknowledged as attractive options for buyers to whom access to a bank mortgage is limited. Moreover, several promotional programmes offering various incentives, including direct electronic prizes, air conditioners or kitchen sets, which will be installed in the apartment, and city car.

Bank Indonesia, the Central Bank, decided to increase the benchmark interest rate by 25 bps to 7.75% in November 2014, in response to the new government’s fuel subsidy reform policy. For the short term, it is expected that the slowing down of demand is likely to continue, particularly in the primary market. However, assuming that economic conditions improve and the political situation is stable in the upcoming years, apartment sales are envisaged to gradually improve in the long term. Hence, the overall take-up rate is anticipated to stabilise within a short period before gradually increasing. Overall, strong interest from both end-users and investors has driven demand for new and off-plan apartments over the past few years. Apartments in the inner city close to train stations, shopping centres, universities and business hubs are the property of choice for these buyers. The Indonesian property market is primarily a domestic play driven by the strength of the local economy, particularly because foreigners are not allowed to buy apartments in this country. Based on the latest data from the office of Statistics Bureau (BPS), almost 70% of Indonesia’s population is in the working age group of 15 to 64 years. Among the working population, the majority (42.3%) are between the ages of 25 and 54. People in this group are vital to the economy due to their strong earning and purchasing power.

Asking PriceOverall, this quarter still witnessed a climb in asking prices. Between October and December 2014, prices grew by an average of 3.1% QoQ or 16.9% YoY, putting the average asking price at around IDR27.7 million/sq m. In the reviewed quarter, asking prices in the Jakarta apartment market continued to grow positively albeit at a slower pace compared to the last two consecutive quarters.

Source: Colliers International Indonesia - Research

Comparison of Average Growth Asking Prices of Jakarta Apartment

1Q 2014 vs 2Q 2014 2Q 2014 vs 3Q 2014 3Q 2014 vs 4Q 20144.70% 5.70% 3.10%

4Q 2011 vs 4Q 2012 4Q 2012 vs 4Q 2013 4Q 2013 vs 4Q 201411.90% 21.10% 16.90%

Average Asking Price of Strata-title Apartment in Jakarta

Source: Colliers International Indonesia - Research

IDR 0

IDR 5,000,000

IDR 10,000,000

IDR 15,000,000

IDR 20,000,000

IDR 25,000,000

IDR 30,000,000

4Q 2

011

1Q 2

012

2Q 2

012

3Q 2

012

4Q 2

012

1Q 2

013

2Q 2

013

3Q 2

013

4Q 2

013

1Q 2

014

2Q 2

014

3Q 2

014

4Q 2

014

23 Research & Forecast Report | 4Q 2014 | Apartment | Colliers International

In line with the demand, the growth of apartment prices in Jakarta experienced sluggish performance over the reviewed quarter. The slowdown in the economy, which is accompanied by the rise in interest rates has led to lower sales performance, thus putting a drag on the price increases, which in many cases are driven by a developer’s decision. In addition, a bountiful new development in the strata-title market has triggered more market competition, which could lead to downward pressure on price. However, the continued progress of construction activity and strong absorption in particular projects located in premium as well as strategic areas, became the determining factors of the price to increase.

Overall, in terms of price growth, South Jakarta still has the highest growth (YoY) among all areas. The accelerating price that occurred in South Jakarta was largely driven by robust demand, particularly at those on-going projects located in prime locations and surrounding the TB Simatupang area. For instance, one middle-class project that has not been launched yet, achieved exceptionally high demand, with 50 - 60% absorption within four months. Further, one upper-class project in a premium area, Pondok Indah, achieved an 85% take-up rate within six to seven months. On the other hand, price adjustments at apartment projects in the CBD were driven by the continued progress of construction and sales performance during this reviewed quarter. Several middle- to upper-class apartment projects located in good areas, like Ciputra International and The Windsor in Puri Indah area, as well as Kensington Residence in the Kelapa Gading area, introduced higher prices compared to other projects while the massive development projects maintained their current asking prices in order to attract buyers amid the strong competition, especially in the middle- to low-class apartment segment.

Source: Colliers International Indonesia - Research

Average Asking Price in Different Locations (in IDR)

area 4Q 2013 3Q 2014 4Q 2014change

QoQ YoYCBD 36,174,524 41,759,611 43,472,842 4% 20%

South Jakarta 25,854,554 31,241,685 32,033,471 3% 24%

Non-Prime Area 18,298,766 20,320,645 20,764,022 2% 13%

Apartment For Lease

SupplyThis quarter saw additional supply from the serviced apartments, Ascott Kuningan, which comprises 185 fully furnished 1- to 3-bedroom units. The Ascott Kuningan is strategically located in Mega Kuningan and is part of the mixed-use development, Ciputra World Jakarta I. This development will benefit from its prime location in the business area and embassy district where there is a sizeable expatriate community. With the completion of this development, the cumulative supply of serviced apartments at the end of 2014 rose gently by 3.9% QoQ to 4,954 units. The non-serviced apartments (apartments purely for lease) remained steady, with a total of 3,565 units.

Overall, as of 4Q 2014, the cumulative supply of apartments for lease in Jakarta was recorded at 8,519, with 44.2% of the total stock in the CBD. We expect to see an additional 640 serviced apartment units enter the market during 2015 - 2016. However, this number can change, particularly because serviced apartments called Pejaten Park has not released the official information regarding the operator and number of units. Based on information in the marketing, there will be serviced apartments in the second tower of Pejaten Park Residence (Tower Catalonia), on Levels 2 to 6.

Source: Colliers International Indonesia - Research

Future Serviced Apartment Pipeline in 2015 - 2016

name oF development Year oF operation location region developer no. oF

unitS

TBS Linera Apartment Service 2015 Cilandak Barat South Jakarta Constructa Builder 110

Fraser Place Setiabudi Sky Garden (Tower III) 2015 Karbela Selatan CBD Jakarta Setiabudi International 150

Oakwood at District 8 Senopati 2016 Senopati South Jakarta Oakwood 180

Serviced Apartment at Pejaten Park Residence 2016 Warung Buncit South Jakarta Bahama Group N/A

Fraser Suites at Ciputra World Jakarta II 2016 Satrio CBD Frasers Hospitality 200

24 Research & Forecast Report | 4Q 2014 | Apartment | Colliers International

Average Rental RatesThe rental rates for serviced apartments in Jakarta experienced a slight increase over the reviewed quarter. The trigger for this quarter increase is due to the commencement of Ascott Kuningan Serviced Apartment located at Jalan Dr. Satrio, which quotes a rental tariff way above the average market rate and thus impacted to the overall rental rates. On the other hand, the average rental rate of non-serviced apartment remained stable. However, since the majority of non-serviced apartment are offered in US dollars while the remainder are offered in local currency, the overall rental rates in US dollars (after converting from IDR to USD with the current exchange rate) somewhat dropped due to the strengthening US dollar against the rupiah during this quarter.

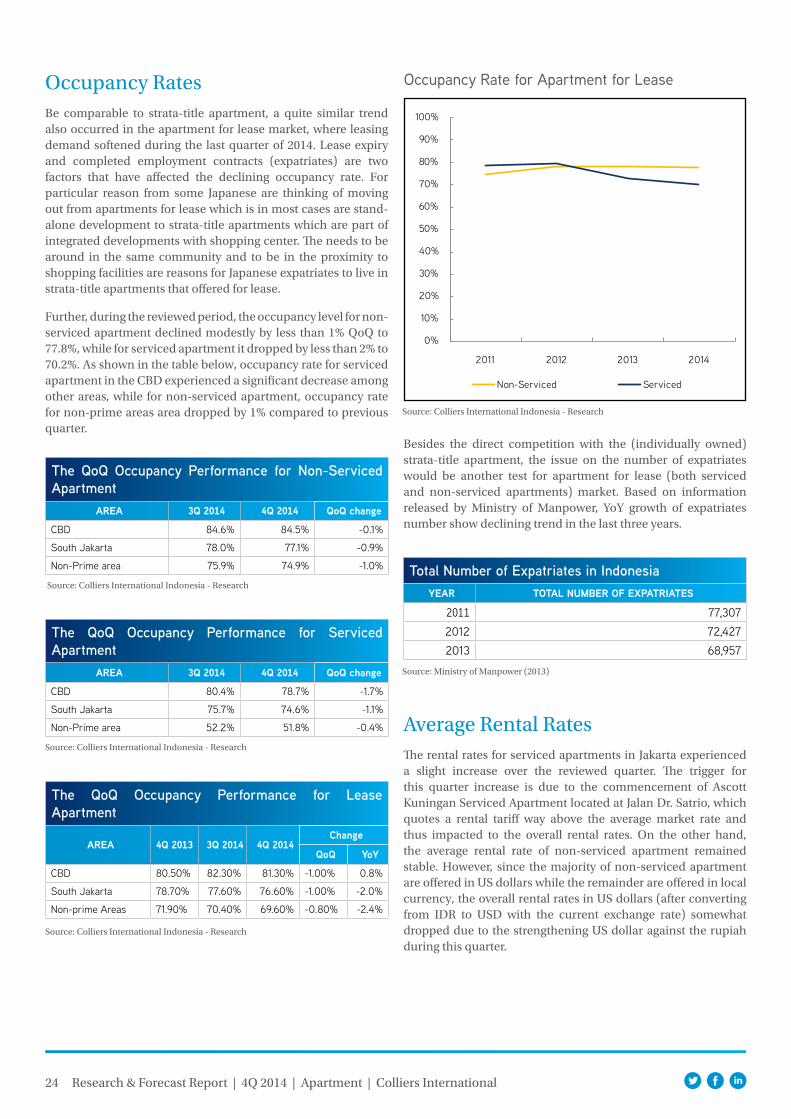

Occupancy RatesBe comparable to strata-title apartment, a quite similar trend also occurred in the apartment for lease market, where leasing demand softened during the last quarter of 2014. Lease expiry and completed employment contracts (expatriates) are two factors that have affected the declining occupancy rate. For particular reason from some Japanese are thinking of moving out from apartments for lease which is in most cases are stand-alone development to strata-title apartments which are part of integrated developments with shopping center. The needs to be around in the same community and to be in the proximity to shopping facilities are reasons for Japanese expatriates to live in strata-title apartments that offered for lease.

Further, during the reviewed period, the occupancy level for non-serviced apartment declined modestly by less than 1% QoQ to 77.8%, while for serviced apartment it dropped by less than 2% to 70.2%. As shown in the table below, occupancy rate for serviced apartment in the CBD experienced a significant decrease among other areas, while for non-serviced apartment, occupancy rate for non-prime areas area dropped by 1% compared to previous quarter.

Source: Colliers International Indonesia - Research

The QoQ Occupancy Performance for Non-Serviced Apartment

area 3Q 2014 4Q 2014 QoQ change

CBD 84.6% 84.5% -0.1%

South Jakarta 78.0% 77.1% -0.9%

Non-Prime area 75.9% 74.9% -1.0%

Occupancy Rate for Apartment for Lease

Source: Colliers International Indonesia - Research

The QoQ Occupancy Performance for Serviced Apartment

area 3Q 2014 4Q 2014 QoQ change

CBD 80.4% 78.7% -1.7%

South Jakarta 75.7% 74.6% -1.1%

Non-Prime area 52.2% 51.8% -0.4%

Source: Colliers International Indonesia - Research

Source: Colliers International Indonesia - Research

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011 2012 2013 2014

Non-Serviced Serviced

Besides the direct competition with the (individually owned) strata-title apartment, the issue on the number of expatriates would be another test for apartment for lease (both serviced and non-serviced apartments) market. Based on information released by Ministry of Manpower, YoY growth of expatriates number show declining trend in the last three years.

Total Number of Expatriates in IndonesiaYear total numBer oF eXpatriateS

2011 77,307 2012 72,427 2013 68,957

Source: Ministry of Manpower (2013)

The QoQ Occupancy Performance for Lease Apartment

area 4Q 2013 3Q 2014 4Q 2014change

QoQ YoY

CBD 80.50% 82.30% 81.30% -1.00% 0.8%

South Jakarta 78.70% 77.60% 76.60% -1.00% -2.0%

Non-prime Areas 71.90% 70.40% 69.60% -0.80% -2.4%

25 Research & Forecast Report | 4Q 2014 | Apartment | Colliers International

OutlookOverall, the 2014 performance was under the level of accomplishment in 2013. In term of total units of newly introduced projects, the total apartment supply in 2014 was only 12,164 units, dropped by 45% compared to 2013’s figure of 21,935 units. Moreover, the overall lackluster absorption was mainly due to the tight competition among under-construction projects.

The competition among the under-construction apartment and the limitation in financing due to LTV regulation has pushed developers to become more creative like providing flexible financing terms and marketing gimmick which alleviate the burden of consumers.

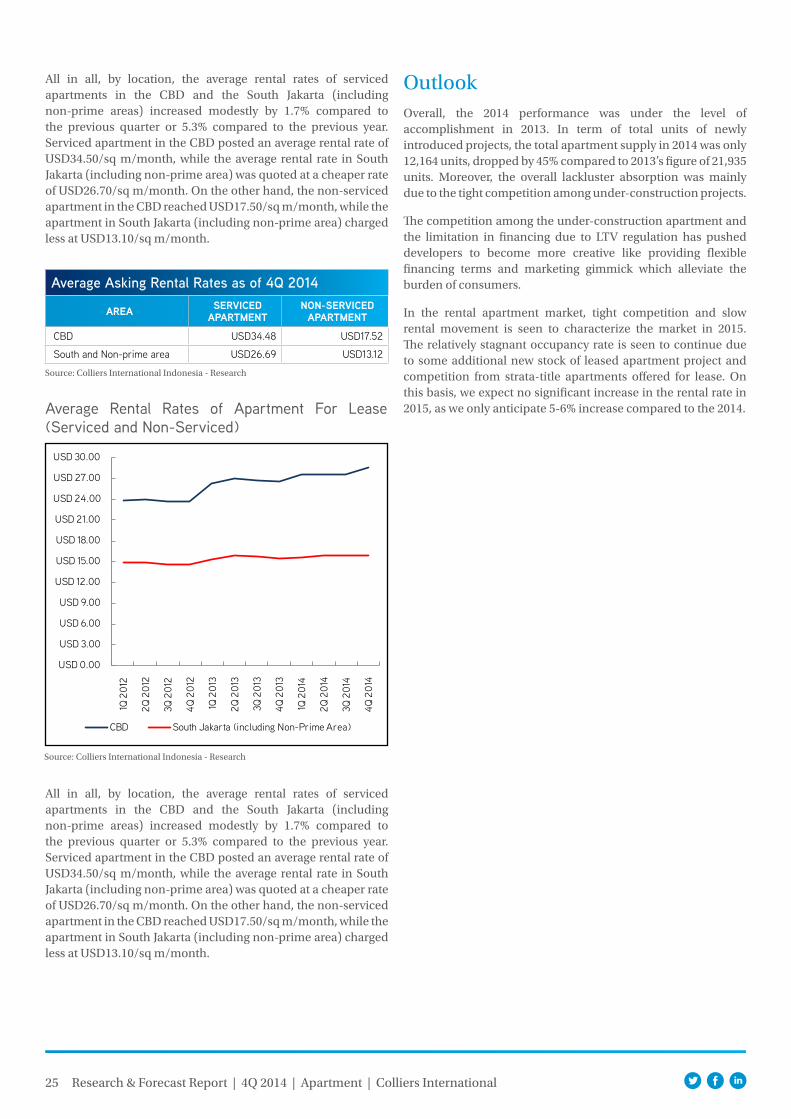

In the rental apartment market, tight competition and slow rental movement is seen to characterize the market in 2015. The relatively stagnant occupancy rate is seen to continue due to some additional new stock of leased apartment project and competition from strata-title apartments offered for lease. On this basis, we expect no significant increase in the rental rate in 2015, as we only anticipate 5-6% increase compared to the 2014.

All in all, by location, the average rental rates of serviced apartments in the CBD and the South Jakarta (including non-prime areas) increased modestly by 1.7% compared to the previous quarter or 5.3% compared to the previous year. Serviced apartment in the CBD posted an average rental rate of USD34.50/sq m/month, while the average rental rate in South Jakarta (including non-prime area) was quoted at a cheaper rate of USD26.70/sq m/month. On the other hand, the non-serviced apartment in the CBD reached USD17.50/sq m/month, while the apartment in South Jakarta (including non-prime area) charged less at USD13.10/sq m/month.

Average Rental Rates of Apartment For Lease (Serviced and Non-Serviced)

Source: Colliers International Indonesia - Research

Average Asking Rental Rates as of 4Q 2014

area Serviced apartment

non-Serviced apartment

CBD USD34.48 USD17.52

South and Non-prime area USD26.69 USD13.12

Source: Colliers International Indonesia - Research

USD 0.00

USD 3.00

USD 6.00

USD 9.00

USD 12.00

USD 15.00

USD 18.00

USD 21.00

USD 24.00

USD 27.00

USD 30.00

1Q 2

012

2Q 2

012

3Q 2

012

4Q 2

012

1Q 2

013

2Q 2

013

3Q 2

013

4Q 2

013

1Q 2

014

2Q 2

014

3Q 2

014

4Q 2

014

CBD South Jakarta (including Non-Prime Area)

All in all, by location, the average rental rates of serviced apartments in the CBD and the South Jakarta (including non-prime areas) increased modestly by 1.7% compared to the previous quarter or 5.3% compared to the previous year. Serviced apartment in the CBD posted an average rental rate of USD34.50/sq m/month, while the average rental rate in South Jakarta (including non-prime area) was quoted at a cheaper rate of USD26.70/sq m/month. On the other hand, the non-serviced apartment in the CBD reached USD17.50/sq m/month, while the apartment in South Jakarta (including non-prime area) charged less at USD13.10/sq m/month.

26

Expatriate Housing SectorExpatriate HousingDuring 2H 2014, two locations in Cilandak and Kemand saw the completion of five new expat-standard, 3- to 4-bedroom, 400 to 450 sq m houses with 500 sq m of land. The supply of expat housing stock is still lagging behind the demand. The stock situation of expat housing mostly remained as it was in 1H 2014. As the favourite expat location remains South Jakarta, the growth of new housing stock is always limited compared to the need for houses. Land stock is also limited, particularly the most sought after locations like Kebayoran Baru, Pondok Indah, Kemang, Cipete and Kuningan, and even Menteng in the Central Jakarta area. Furthermore, land is selling for very high prices, making the investment in low-rise residences yield a low return. South Jakarta area is still irreplaceable as the home of expatriates from European and American countries as it provides almost all of the facilities such as international school, entertainment spots, shopping destinations, golf courses and other points of interest.

For the sake of security and comfort, gated compounds are always interesting, particularly for non-corporate expatriates. Quite a few corporations are considering not housing all of their expat employees in one compound. Nowadays, it is common to see gated communities inhabited by expats from different companies. Although the interest in such integrated housing compounds is quite strong, gated housing compounds are not widely available in expatriate locations.

Due to limited supply, expatriate-standard housing in expatriate locations, such as in South Jakarta is considered premium property, and therefore landlords owning many housing units tend to have a “take-it or leave-it” attitude when negotiating with tenants. Individual landlords having only a few houses are generally quite flexible in terms of rent negotiations as they rely heavily on the income from the property. Currently, the minimum rent for a house for expatriates is USD3,000 / month / unit, for a 3-bedroom house in Cipete and the maximum is USD15,000 / month / unit for a 4- to 5-bedroom house in the Kebayoran, Menteng and Pondok Indah areas.

The expatriate housing market reached a plateau in early 2014, highlighted by modest inquiries for housing accommodation. Nevertheless, landlords who have a great number of houses were still confident in maintaining the rental rate at the high level due to their success in 2013. On the other hand, individual landlords are more willing to negotiate the rental rate. These landlords are more concerned when their houses are vacant for periods of more than three months. Negotiating rent with certain individual landlords is relatively pleasant as they will lower the rental rates between 10 and 15%.

Research & Forecast Report | 4Q 2014 | Expatriate Housing | Colliers International

27

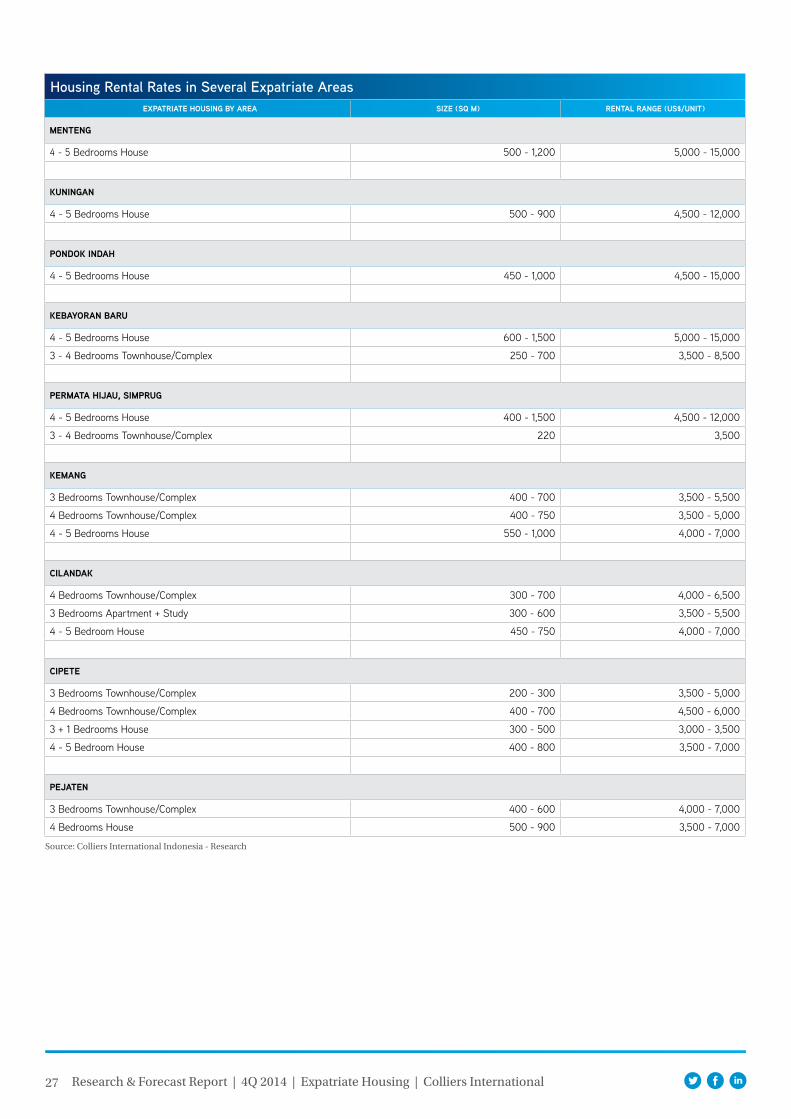

Housing Rental Rates in Several Expatriate AreaseXpatriate houSing BY area Size (SQ m) rental range (uS$/unit)

menteng

4 - 5 Bedrooms House 500 - 1,200 5,000 - 15,000

kuningan

4 - 5 Bedrooms House 500 - 900 4,500 - 12,000

pondok indah

4 - 5 Bedrooms House 450 - 1,000 4,500 - 15,000

keBaYoran Baru

4 - 5 Bedrooms House 600 - 1,500 5,000 - 15,000

3 - 4 Bedrooms Townhouse/Complex 250 - 700 3,500 - 8,500

permata hijau, Simprug

4 - 5 Bedrooms House 400 - 1,500 4,500 - 12,000

3 - 4 Bedrooms Townhouse/Complex 220 3,500

kemang

3 Bedrooms Townhouse/Complex 400 - 700 3,500 - 5,500

4 Bedrooms Townhouse/Complex 400 - 750 3,500 - 5,000

4 - 5 Bedrooms House 550 - 1,000 4,000 - 7,000

cilandak

4 Bedrooms Townhouse/Complex 300 - 700 4,000 - 6,500

3 Bedrooms Apartment + Study 300 - 600 3,500 - 5,500

4 - 5 Bedroom House 450 - 750 4,000 - 7,000

cipete

3 Bedrooms Townhouse/Complex 200 - 300 3,500 - 5,000

4 Bedrooms Townhouse/Complex 400 - 700 4,500 - 6,000

3 + 1 Bedrooms House 300 - 500 3,000 - 3,500

4 - 5 Bedroom House 400 - 800 3,500 - 7,000

pejaten

3 Bedrooms Townhouse/Complex 400 - 600 4,000 - 7,000

4 Bedrooms House 500 - 900 3,500 - 7,000

Source: Colliers International Indonesia - Research

Research & Forecast Report | 4Q 2014 | Expatriate Housing | Colliers International

28

DemandThere was no significant change in the absorption level of expatriate housing during 2H 2014 compared to the previous semester. Currently, the Immigration Office is quite bold in implementing regulations, for example, they will not allow expatriates more than fifty years old to work in Indonesia in compliance with the maximum working age.