Embed Size (px)

Citation preview

JAKARTA REAL ESTATE RESEARCH & FORECAST REPORT

www.colliers.co.id

1Q 2012 I PROPERTY MARKET REPORT

Property Sector OverviewOFFICE SECTORBase rental rates in the CBD for this quarter continue to improve. Average asking base rental rates for all classes of office buildings were recorded at Rp134,099/sq m/month (5% change Q-o-Q) for Rupiah denominated buildings and US$23.26/sq m/month (10% change Q-o-Q) for US Dollar denominated buildings. The primary reason that landlords are asking for higher rents is the fact that it is currently very tough to find good quality office space. Accordingly, occupancy levels have also climbed modestly to 94.5.% this quarter.

APARTMENT SECTORNew apartment projects were launched, providing 4,273 units and brought the overall apartment units in Jakarta to 101,776, a 4.31% Q-o-Q increase. The average price for the Jakarta area edged higher by 5.2% Q-o-Q to Rp13.62 million/sq m due to the influx of new apartment projects with price above the average market price. The average price in the CBD moved by 2.3% Q-o-Q to Rp18.53 million/sq m.

RETAIL SECTORA total of 247,456 sq m of the retail space to be completed along 2012 has been 81% committed. Of the space has already been absorbed by some major tenants. Further 59% of the 129,200 sq m of retail space to be completed in 2013 has been committed. Similarly, in the cities surrounding Jakarta, of total retail space of around 93,000 sq m projected to be completed in 2012, around 86% has been taken up. Despite small changes in average asking rental rates and occupancy rates in this quarter, we believe that the retail market rental rates will strengthen this year as retail space inventory grows moderately.

INDUSTRIAL ESTATE SECTORMeanwhile sales of industrial land in 1Q 2012 are recorded at 193 hectares. With limited industrial land to sell, land price increase as much as 10% in this quarter alone . We still expect total sales for the rest of 2011 will be brisk eventhough the land availability will be the general obstacle for industrial market to grow throughout the year of 2012. Bekasi and Karawang areas recorded the most significant increase from US$150.33/sq m to US$164.75/sq m and US$108.22/sq m to US$116.98/sq m Q-o-Q, respectively.

Office SectorSupply

JAKARTA OFFICE SUPPLY

Colliers International Indonesia - Research

01,000,0002,000,0003,000,0004,000,0005,000,0006,000,0007,000,0008,000,0009,000,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

1Q 2

012

2012

F

2013

F

2014

F

sq m

Existing Supply Annual Supply

JAKARTA SUPPLYTwo new buildings were completed during 1Q 2012 while one building was taken out from our database. New buildings during the quarter include Multivision Tower, located in Jalan Rasuna Said and Menara Satu in Kelapa Gading, East Jakarta. These two supplied an additional office stock of 40,770 sq m. Meanwhile, an office building in the Barito area, South Jakarta was demolished and will be replaced by a new apartment tower. All in all, the total office space in Jakarta is now 6.27 million sq m with 70% of it located in the CBD area.

Office completions during 2012 in Jakarta will be quite significant. Several buildings have shown rapid construction progress towards completion. The office supply grew by only 3% annually over the last ten years while the office supply from 2012 - 2014 will grow by 8.7% annually. This shows a greater amount of office supply, however most of the future buildings have confirmed high commitment levels even before their completion.

CBD

EXISTING SUPPLYLast year the office supply only grew by less than 100,000 sq m (the lowest growth in the last five years). In this quarter, the operation of Multivision Tower brought the cumulative supply of CBD offices to 4.38 million sq m. Colliers International Indonesia has reviewed the grading of existing office buildings and implemented a fairer methodology in categorising office gradings. Location and building quality criteria are the most significant factors. A CBD location of course has more weight than locations outside of the CBD while building quality includes several factors like the design of the building (architecture), lifts, mechanical & electrical, structure and green

building compliance. Other factors taken into account are building size, floor plate size, age, management and maintenance, facilities and tenant profile. Thus, based on the methodology, around 45% of the buildings in the CBD are of Premium and Grade A categories. The trend this year is towards strata-title office buildings this year with around 51% of the total annual supply being marketed as office space for sale. This is a repetition of 2005 and 2010 when the number of annual strata-title sales was greater than the number of offices for lease. To date, of the total office space in the CBD, 15% is office space for sale representing 637,232 million sq m.

P. 2 | COLLIERS INTERNATIONAL

JAKARTA | 1Q 2012 | OFFICE

CBD ANNUAL OFFICE SUPPLY BASED ON MARKETING SCHEME

Colliers International Indonesia - Research

0

50,000

100,000

150,000

200,000

250,000

300,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

1Q 2

012

2012

F

2013

F

2014

F

sq m

For Lease For Strata-title

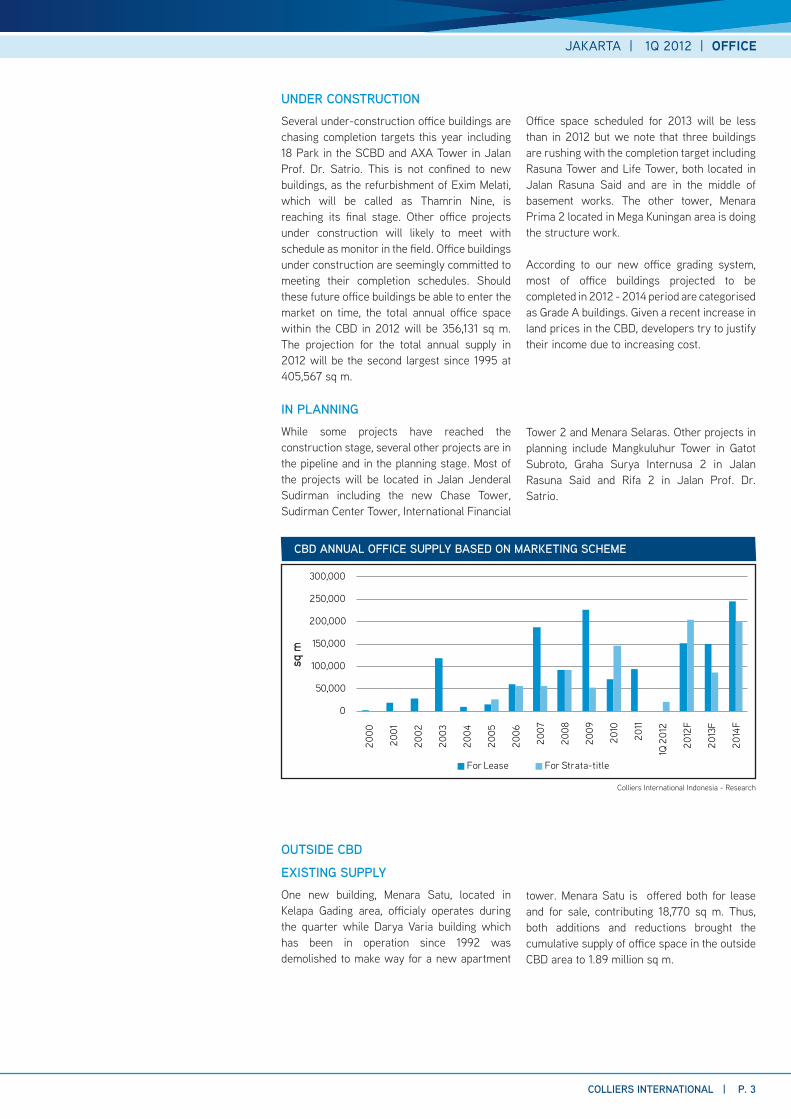

UNDER CONSTRUCTIONSeveral under-construction office buildings are chasing completion targets this year including 18 Park in the SCBD and AXA Tower in Jalan Prof. Dr. Satrio. This is not confined to new buildings, as the refurbishment of Exim Melati, which will be called as Thamrin Nine, is reaching its final stage. Other office projects under construction will likely to meet with schedule as monitor in the field. Office buildings under construction are seemingly committed to meeting their completion schedules. Should these future office buildings be able to enter the market on time, the total annual office space within the CBD in 2012 will be 356,131 sq m. The projection for the total annual supply in 2012 will be the second largest since 1995 at 405,567 sq m.

Office space scheduled for 2013 will be less than in 2012 but we note that three buildings are rushing with the completion target including Rasuna Tower and Life Tower, both located in Jalan Rasuna Said and are in the middle of basement works. The other tower, Menara Prima 2 located in Mega Kuningan area is doing the structure work. According to our new office grading system, most of office buildings projected to be completed in 2012 - 2014 period are categorised as Grade A buildings. Given a recent increase in land prices in the CBD, developers try to justify their income due to increasing cost.

IN PLANNINGWhile some projects have reached the construction stage, several other projects are in the pipeline and in the planning stage. Most of the projects will be located in Jalan Jenderal Sudirman including the new Chase Tower, Sudirman Center Tower, International Financial

Tower 2 and Menara Selaras. Other projects in planning include Mangkuluhur Tower in Gatot Subroto, Graha Surya Internusa 2 in Jalan Rasuna Said and Rifa 2 in Jalan Prof. Dr. Satrio.

OUTSIDE CBD

EXISTING SUPPLYOne new building, Menara Satu, located in Kelapa Gading area, officialy operates during the quarter while Darya Varia building which has been in operation since 1992 was demolished to make way for a new apartment

tower. Menara Satu is offered both for lease and for sale, contributing 18,770 sq m. Thus, both additions and reductions brought the cumulative supply of office space in the outside CBD area to 1.89 million sq m.

COLLIERS INTERNATIONAL | P. 3

JAKARTA | 1Q 2012 | OFFICE

OUTSIDE CBD ANNUAL OFFICE SUPPLY BASED ON MARKETING SCHEME

Colliers International Indonesia - Research

0

50,000

100,000

150,000

200,000

250,000

300,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

1Q 2

012

2012

F

2013

F

2014

F

sq m

For Lease For Strata-title

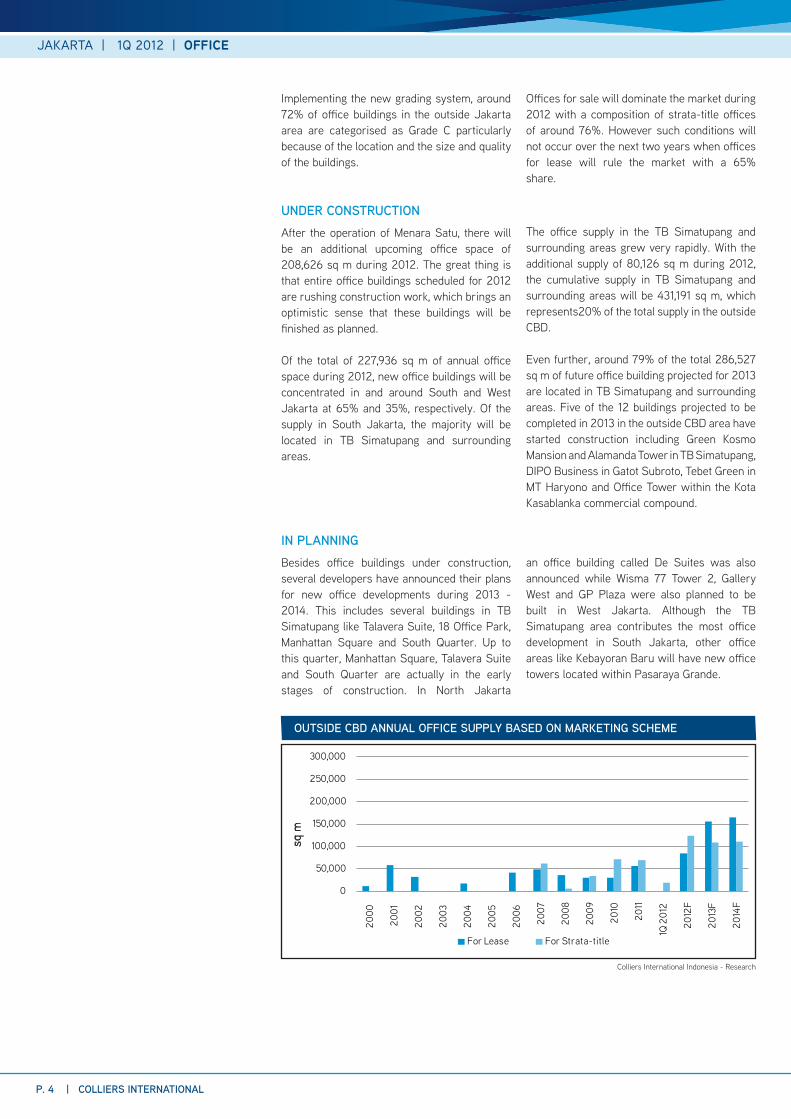

UNDER CONSTRUCTIONAfter the operation of Menara Satu, there will be an additional upcoming office space of 208,626 sq m during 2012. The great thing is that entire office buildings scheduled for 2012 are rushing construction work, which brings an optimistic sense that these buildings will be finished as planned. Of the total of 227,936 sq m of annual office space during 2012, new office buildings will be concentrated in and around South and West Jakarta at 65% and 35%, respectively. Of the supply in South Jakarta, the majority will be located in TB Simatupang and surrounding areas.

The office supply in the TB Simatupang and surrounding areas grew very rapidly. With the additional supply of 80,126 sq m during 2012, the cumulative supply in TB Simatupang and surrounding areas will be 431,191 sq m, which represents20% of the total supply in the outside CBD.

Even further, around 79% of the total 286,527 sq m of future office building projected for 2013 are located in TB Simatupang and surrounding areas. Five of the 12 buildings projected to be completed in 2013 in the outside CBD area have started construction including Green Kosmo Mansion and Alamanda Tower in TB Simatupang, DIPO Business in Gatot Subroto, Tebet Green in MT Haryono and Office Tower within the Kota Kasablanka commercial compound.

IN PLANNINGBesides office buildings under construction, several developers have announced their plans for new office developments during 2013 - 2014. This includes several buildings in TB Simatupang like Talavera Suite, 18 Office Park, Manhattan Square and South Quarter. Up to this quarter, Manhattan Square, Talavera Suite and South Quarter are actually in the early stages of construction. In North Jakarta

an office building called De Suites was also announced while Wisma 77 Tower 2, Gallery West and GP Plaza were also planned to be built in West Jakarta. Although the TB Simatupang area contributes the most office development in South Jakarta, other office areas like Kebayoran Baru will have new office towers located within Pasaraya Grande.

Implementing the new grading system, around 72% of office buildings in the outside Jakarta area are categorised as Grade C particularly because of the location and the size and quality of the buildings.

Offices for sale will dominate the market during 2012 with a composition of strata-title offices of around 76%. However such conditions will not occur over the next two years when offices for lease will rule the market with a 65% share.

P. 4 | COLLIERS INTERNATIONAL

JAKARTA | 1Q 2012 | OFFICE

FUTURE OFFICE BUILDINGS

PROJECTED COMPLETION

TIMEBUILDING NAME LOCATION SGA

(SQ M) MARKETING SCHEME STATUS*

CBD AREA

2Q 2012 18 PARK SCBD 23,136 For Lease Under Construction

2Q 2012 AXA Tower Satrio 60,995 For Lease and For Strata-title Under Construction

2Q 2012 Thamrin Nine (Exim Melati) MH Thamrin 8,000 For Lease Under Construction

3Q 2012 World Trade Center 2 Sudirman 57,000 For Lease Under Construction

4Q 2012 Office 8 SCBD 48,000 For Strata-title Under Construction

4Q 2012 Tower One at The City Center KH Mas Mansyur 84,000 For Lease and For Strata-title Under Construction

4Q 2012 Perkantoran Setiabudi Setiabudi 11,000 For Lease and For Strata-title Under Construction

4Q 2012 DBS Tower at Ciputra World 1 Jakarta Satrio 64,000 For Lease and For Strata-title Under Construction

1Q 2013 Menara Prima 2 Mega Kuningan 40,000 For Lease Under Construction

4Q 2013 Chase Tower Sudirman 57,406 For Strata-title Under Construction

4Q 2013 Life Tower HR Rasuna Said 30,500 For Lease Under Construction

4Q 2013 Rasuna Tower HR Rasuna Said 80,000 For Lease Under Construction

4Q 2013 Rifa 2 Satrio 30,000 For Strata-title In Planning

1Q 2014 Menara Selaras Sudirman 36,596 For Lease In Planning

1Q 2014 The City Center (phase 2) KH Mas Mansyur 34,000 For Strata-title In Planning

1Q 2014 The City Center (phase 3) KH Mas Mansyur 40,000 For Lease In Planning

2Q 2014 International Financial Center 2 Sudirman 40,000 For Lease In Planning

4Q 2014 Sudirman Center Tower Sudirman 126,600 For Strata-title In Planning

4Q 2014 Menara Palma 2 HR Rasuna Said 50,000 For Lease In Planning

4Q 2014 Menara Pertiwi Mega Kuningan 40,000 For Strata-title In Planning

4Q 2014 Graha Surya Internusa 2 HR Rasuna Said 40,000 For Lease In Planning

4Q 2014 Mangkuluhur Tower B Gatot Subroto 39,356 For Lease In Planning

OUTSIDE CBD AREA

2Q 2012 Wisma Pondok Indah 3 Sultan Iskandar Muda 36,106 For Lease Under Construction

2Q 2012 Grand Soho Slipi S. Parman 52,000 For Strata-title Under Construction

2Q 2012 Sovereign Plaza TB Simatupang 16,020 For Lease and For Strata-title Under Construction

3Q 2012 Chitatex Tower Tb Simatupang 28,000 For Lease Under Construction

4Q 2012 Blue Green Office Boutique Meruya 20,000 For Lease Under Construction

4Q 2012 Eighty8 Kasablanka 56,500 For Strata-title Under Construction

1Q 2013 De Suites Pantai Indah Kapuk 8,000 For Strata-title In Planning

2Q 2013 Alamanda Tower TB Simatupang 33,000 For Lease and For Strata-title Under Construction

2Q 2013 Gallery West Kebon Jeruk 22,800 For Strata-title In Planning

4Q 2013 Green Kosmo Mansion (GKM) Tower TB Simatupang 23,000 For Strata-title Under Construction

4Q 2013 Talavera Suite TB Simatupang 16,250 For Lease In Planning

4Q 2013 Graha Elnusa 2 TB Simatupang 40,000 For Lease In Planning

4Q 2013 18 Office Park (Cityland Tower) TB Simatupang 36,627 For Lease In Planning

4Q 2013 Tebet Green MT Haryono 8,750 For Lease In Planning

4Q 2013 Signum Tower TB Simatupang 58,500 For Lease In Planning

4Q 2013 DIPO Business Park Gatot Subroto 19,600 For Strata-title Under Construction

continued

COLLIERS INTERNATIONAL | P. 5

JAKARTA | 1Q 2012 | OFFICE

continuation

1Q 2014 The Manhattan Square TB Simatupang 37,699 For Strata-title In Planning

2Q 2014 Wisma 77 Tower 2 S. Parman 24,200 For Strata-title In Planning

2Q 2014 Graha Kirana 2 Yos Sudarso 25,000 For Lease In Planning

4Q 2014 GP Plaza Gatot Subroto 12,204 For Strata-title In Planning

4Q 2014 Beltway Office Park Tower B TB Simatupang 10,500 For Lease In Planning

4Q 2014 Beltway Office Park Tower D TB Simatupang 49,675 For Lease In Planning

4Q 2014 South Quarter TB Simatupang 40,000 For Lease In Planning

4Q 2014 Office Tower at Pasaraya Grande Sultan Iskandaryah 40,000 For Lease and For Strata-title In Planning

4Q 2014 La Venue Pasar Minggu 37,168 For Strata-title In Planning

Colliers International Indonesia - Research

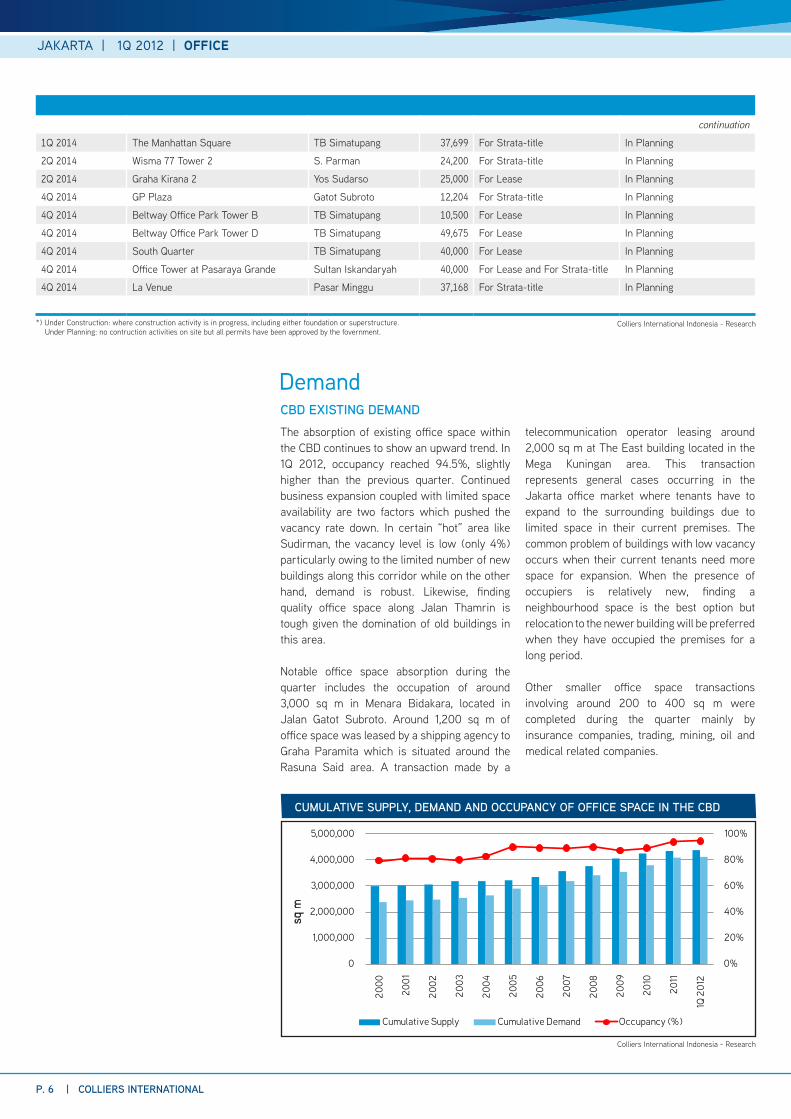

DemandCBD EXISTING DEMANDThe absorption of existing office space within the CBD continues to show an upward trend. In 1Q 2012, occupancy reached 94.5%, slightly higher than the previous quarter. Continued business expansion coupled with limited space availability are two factors which pushed the vacancy rate down. In certain “hot” area like Sudirman, the vacancy level is low (only 4%) particularly owing to the limited number of new buildings along this corridor while on the other hand, demand is robust. Likewise, finding quality office space along Jalan Thamrin is tough given the domination of old buildings in this area. Notable office space absorption during the quarter includes the occupation of around 3,000 sq m in Menara Bidakara, located in Jalan Gatot Subroto. Around 1,200 sq m of office space was leased by a shipping agency to Graha Paramita which is situated around the Rasuna Said area. A transaction made by a

telecommunication operator leasing around 2,000 sq m at The East building located in the Mega Kuningan area. This transaction represents general cases occurring in the Jakarta office market where tenants have to expand to the surrounding buildings due to limited space in their current premises. The common problem of buildings with low vacancy occurs when their current tenants need more space for expansion. When the presence of occupiers is relatively new, finding a neighbourhood space is the best option but relocation to the newer building will be preferred when they have occupied the premises for a long period. Other smaller office space transactions involving around 200 to 400 sq m were completed during the quarter mainly by insurance companies, trading, mining, oil and medical related companies.

CUMULATIVE SUPPLY, DEMAND AND OCCUPANCY OF OFFICE SPACE IN THE CBD

Colliers International Indonesia - Research

0%

20%

40%

60%

80%

100%

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

1Q 2

012

sq m

Cumulative Supply Cumulative Demand Occupancy (%)

*) Under Construction: where construction activity is in progress, including either foundation or superstructure. Under Planning: no contruction activities on site but all permits have been approved by the fovernment.

P. 6 | COLLIERS INTERNATIONAL

JAKARTA | 1Q 2012 | OFFICE

CUMULATIVE SUPPLY, DEMAND AND OCCUPANCY OF OFFICE SPACE IN THE OUTSIDE CBD

Colliers International Indonesia - Research

OUTSIDE CBD EXISTING DEMANDThe influx of Menara Satu has less impact on the overall occupancy rate because Menara Satu begins operation with high occupancy.

The occupancy level as of 1Q 2012 reached 92%, a modest rise over the previous quarter.

PRE-COMMITMENT DEMANDDespite huge supply projections, the office market during 2012 is predicted to perform well as new buildings projected to operate this year has secured a high commitment level of 77%. With three quarters remaining in this year, the office market is quite confident of maintaining a high occupancy level. The majority of offices for lease have secured occupancy of more than 60% and even buildings like WTC 2 and AXA Tower have recorded very high pre-commitment levels before the buildings are in operation. On the strata-title front, sales rates of under-construction buildings projected to operate in 2012 have generally reached 82% with only a building having low absorption rates (mainly due to location considerations). The only empty building is a small office building located around the Rasuna Said area but this is mainly because the owner is selling the building as an en-bloc investment. However, the other four buildings have registered very high sales rates of above 90%.

Similarly, four buildings projected to operate this year have announced their major tenants with an average pre-commitment occupancy of 80%. Three new buildings are located in the Pondok Indah and TB Simatupang areas where they get big tenants like oil and gas, mining, bank and technology product companies. For buildings planned to operate in 2013, only Alamanda Tower has reported of having pre-commitment agreement with their tenants.

Strata-title buildings in the outside CBD area include partial space in Sovereign Plaza, Grand SOHO Slipi and partial space in Menara Satu. Except for the Grand SOHO with a relatively low pre-commitment level, other two buildings have been sold out. Thus far, of the total 126,527 sq m of strata-title space projected to be completed in 2013, around 18% have been reported sold.

0%

20%

40%

60%

80%

100%

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

1Q 2

012

sq m

Cumulative Supply Cumulative Demand Occupancy (%)

COLLIERS INTERNATIONAL | P. 7

JAKARTA | 1Q 2012 | OFFICE

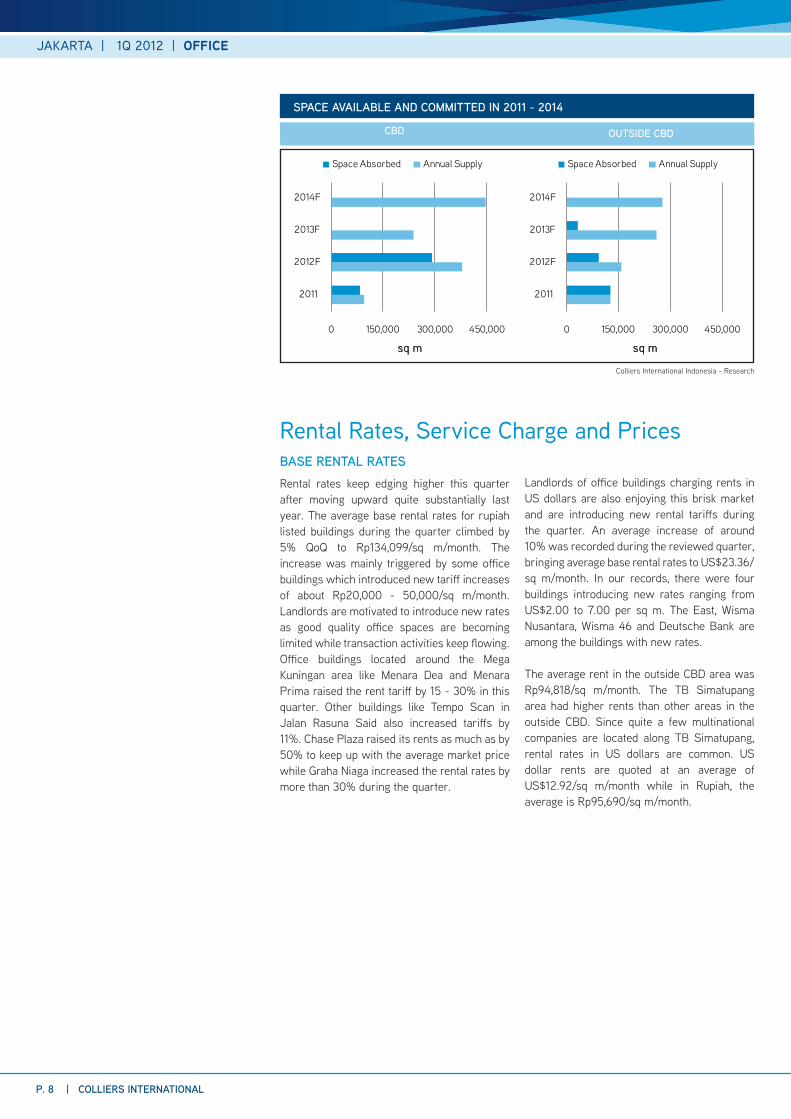

WITHIN CBD AREA

SPACE AVAILABLE AND COMMITTED IN 2011 - 2014

Colliers International Indonesia - Research

CBD OUTSIDE CBD

0 150,000 300,000 450,000

2011

2012F

2013F

2014F

sq m

Space Absorbed Annual Supply

0 150,000 300,000 450,000

2011

2012F

2013F

2014F

sq m

Space Absorbed Annual Supply

BASE RENTAL RATESRental rates keep edging higher this quarter after moving upward quite substantially last year. The average base rental rates for rupiah listed buildings during the quarter climbed by 5% QoQ to Rp134,099/sq m/month. The increase was mainly triggered by some office buildings which introduced new tariff increases of about Rp20,000 - 50,000/sq m/month. Landlords are motivated to introduce new rates as good quality office spaces are becoming limited while transaction activities keep flowing. Office buildings located around the Mega Kuningan area like Menara Dea and Menara Prima raised the rent tariff by 15 - 30% in this quarter. Other buildings like Tempo Scan in Jalan Rasuna Said also increased tariffs by 11%. Chase Plaza raised its rents as much as by 50% to keep up with the average market price while Graha Niaga increased the rental rates by more than 30% during the quarter.

Landlords of office buildings charging rents in US dollars are also enjoying this brisk market and are introducing new rental tariffs during the quarter. An average increase of around 10% was recorded during the reviewed quarter, bringing average base rental rates to US$23.36/ sq m/month. In our records, there were four buildings introducing new rates ranging from US$2.00 to 7.00 per sq m. The East, Wisma Nusantara, Wisma 46 and Deutsche Bank are among the buildings with new rates. The average rent in the outside CBD area was Rp94,818/sq m/month. The TB Simatupang area had higher rents than other areas in the outside CBD. Since quite a few multinational companies are located along TB Simatupang, rental rates in US dollars are common. US dollar rents are quoted at an average of US$12.92/sq m/month while in Rupiah, the average is Rp95,690/sq m/month.

Rental Rates, Service Charge and Prices

P. 8 | COLLIERS INTERNATIONAL

JAKARTA | 1Q 2012 | OFFICE

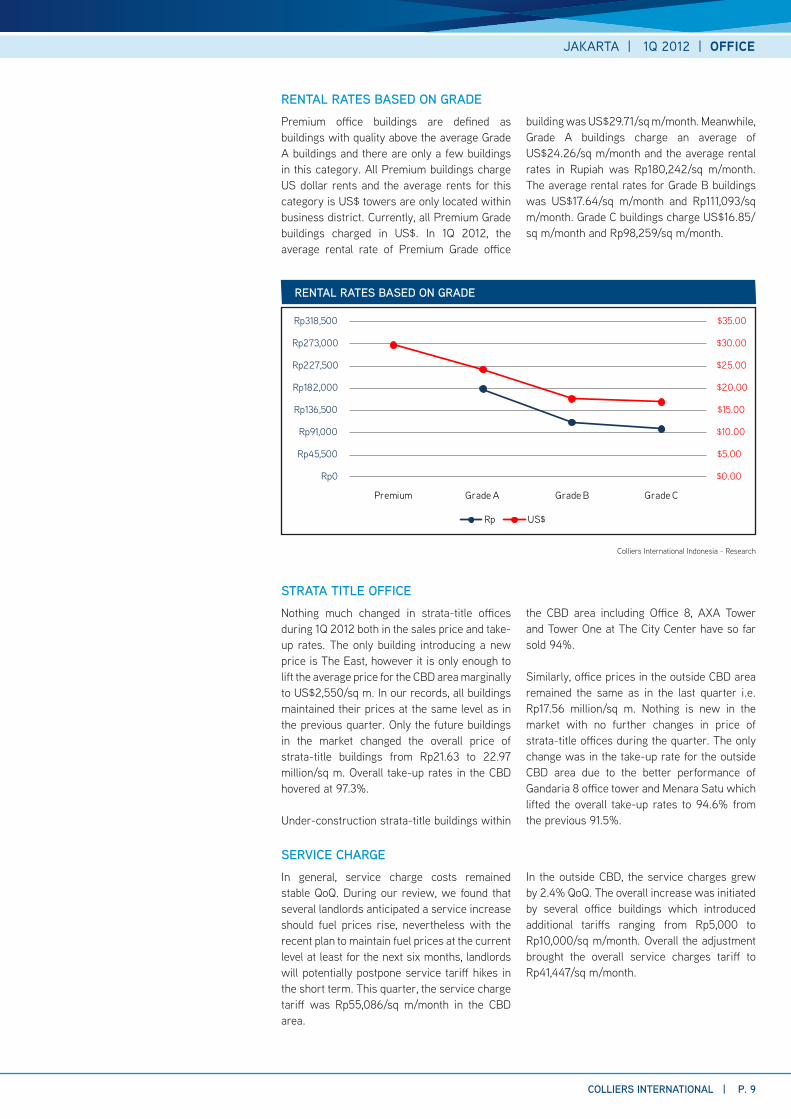

RENTAL RATES BASED ON GRADEPremium office buildings are defined as buildings with quality above the average Grade A buildings and there are only a few buildings in this category. All Premium buildings charge US dollar rents and the average rents for this category is US$ towers are only located within business district. Currently, all Premium Grade buildings charged in US$. In 1Q 2012, the average rental rate of Premium Grade office

building was US$29.71/sq m/month. Meanwhile, Grade A buildings charge an average of US$24.26/sq m/month and the average rental rates in Rupiah was Rp180,242/sq m/month. The average rental rates for Grade B buildings was US$17.64/sq m/month and Rp111,093/sq m/month. Grade C buildings charge US$16.85/sq m/month and Rp98,259/sq m/month.

STRATA TITLE OFFICENothing much changed in strata-title offices during 1Q 2012 both in the sales price and take-up rates. The only building introducing a new price is The East, however it is only enough to lift the average price for the CBD area marginally to US$2,550/sq m. In our records, all buildings maintained their prices at the same level as in the previous quarter. Only the future buildings in the market changed the overall price of strata-title buildings from Rp21.63 to 22.97 million/sq m. Overall take-up rates in the CBD hovered at 97.3%. Under-construction strata-title buildings within

the CBD area including Office 8, AXA Tower and Tower One at The City Center have so far sold 94%.

Similarly, office prices in the outside CBD area remained the same as in the last quarter i.e. Rp17.56 million/sq m. Nothing is new in the market with no further changes in price of strata-title offices during the quarter. The only change was in the take-up rate for the outside CBD area due to the better performance of Gandaria 8 office tower and Menara Satu which lifted the overall take-up rates to 94.6% from the previous 91.5%.

SERVICE CHARGEIn general, service charge costs remained stable QoQ. During our review, we found that several landlords anticipated a service increase should fuel prices rise, nevertheless with the recent plan to maintain fuel prices at the current level at least for the next six months, landlords will potentially postpone service tariff hikes in the short term. This quarter, the service charge tariff was Rp55,086/sq m/month in the CBD area.

In the outside CBD, the service charges grew by 2.4% QoQ. The overall increase was initiated by several office buildings which introduced additional tariffs ranging from Rp5,000 to Rp10,000/sq m/month. Overall the adjustment brought the overall service charges tariff to Rp41,447/sq m/month.

RENTAL RATES BASED ON GRADE

Colliers International Indonesia - Research

$0.00

$5.00

$10.00

$15.00

$20.00

$25.00

$30.00

$35.00

Rp0

Rp45,500

Rp91,000

Rp136,500

Rp182,000

Rp227,500

Rp273,000

Rp318,500

Premium Grade A Grade B Grade C

Rp US$

COLLIERS INTERNATIONAL | P. 9

JAKARTA | 1Q 2012 | OFFICE

Land price increases in the main commercial area will be unavoidable. The CBD area of Jakarta has recorded substantial increases in land prices particularly because of the scarcity of land, the plans for the MRT that will potentially lift the commercial value of the land and the limited number of willing sellers. Most are unmotivated sellers who offer their land at a very high price because they do not really wish to sell. Having said that, developers are pushed to build high-quality buildings to achieve high price and/or high rent to justify the land costs they have incurred. The good news is that the Jakarta government is considering an increase in the plot ratio to justify the commercial value of the land mainly in certain area within the neighbourhood of the MRT station. Thus, in the future, prime commercial areas like Jalan Sudirman and Jalan Thamrin will be adorned with skyscrapers.

Rents will continue to soar during 2012. The

under-construction buildings projected to operate this year have secured high commitment levels meaning that the remaining vacant space will be limited. With great optimism over the outlook for the Indonesian economy, business expansion is expected to be rosy and demand for business location buoyant. This combination will bolster landlords’ position and accordingly will lead occupancy tariffs to increase.

The positive side of land scarcity in the CBD is that it allows other parts of Jakarta to grow as commercial areas. Indeed, the profile of the prestigious CBD is still needed for multinational companies or high profile local companies but there are other growing business entities which do not require high profile locations, particularly the non-service industries, consumer goods, data centres, etc. We have noted some plans for developing office buildings outside of the main commercial areas like the CBD or TB Simatupang area.

Outlook

P. 10 | COLLIERS INTERNATIONAL

JAKARTA | 1Q 2012 | OFFICE

Apartment Sector

Apartment Strata-title

Colliers International Indonesia - Research

The year 2012 began with 4,273 new completed units at five apartment projects. The addition brought the cumulative total of strata-title apartments to 101,776. In other words, the total supply during the quarter contributed as much as 4.31% of the total apartment supply in Jakarta. These 4,273 units or 16.37% of the total projected 26,098 units which will be

completed this year are scattered in the CBD, South, East, and West Jakarta. Furthermore, of the total supply coming this quarter, around 44.2% are considered middle- to low- and 38.2% are considered low-class developments (categorised as rusunami – low-class multi-family housing), while the remaining 17.5% are middle- to upper-class.

The early part of 2012 began with great optimism among developers as they launched several new projects, taking advantage of the growing property market and economy. Apart from the completed projects mentioned above, there were six apartment projects entering the ground-breaking stage during 1Q 2012 including The H Residence; Woodland Park Residence; The Hive Tamansari; Ciputra World 2 Jakarta; Setiabudi Sky Garden and Senopati Penthouse. Meanwhile, quite a few new projects ranging from the middle to upper classes scattered in five municipalities in Jakarta made early bird offers to potential buyers. These include new projects from reputable developers such as:

Metro Park Residence (Agung Podomoro Group) and Aeropolis Residence (Intiland) both located in West Jakarta; The Heritage (Wika Realty) located in Central Jakarta; and Botanica Apartment (Pikko Group) located in South Jakarta. Other than that, the new line of developers includes The Aspen Residence (Harmas Jalesveva), L’avenue Apartment (PT. Bintang Rajawali Perkasa), and The Royal Olive Residence (PT. AD Realty) located in South Jakarta; followed by Sudirman Terrace (PT. Tristar Gemilang Abadi) located in the CBD; and T - Plaza Residence (PT. Prima Kencana) located in Central Jakarta.

Supply

LIST OF COMPLETED NEW PROJECTS IN 1Q 2012

DEVELOPMENT LOCATION REGION #UNITSEast Park Apartment (Tower B) KRT Radjiman East Jakarta 550

Green Palace Apartment (Tower L) Kalibata South Jakarta 630

Green Palace Apartment (Tower M) Kalibata South Jakarta 630

Green Palace Apartment (Tower N) Kalibata South Jakarta 630

Central Park Residence Tower Adeline S. Parman West Jakarta 350

Puri Park View (Tower A) Pesanggrahan, Meruya Utara West Jakarta 1,083

Thamrin Executive Residence MH Thamrin CBD 400

0

10

20

30

40

50

60

CBD Central Jakarta South Jakarta North Jakarta East Jakarta West Jakarta

Num

ber o

f Pro

ject

s

Colliers International Indonesia - Research

APARTMENT DISTRIBUTION IN SEVERAL REGIONS OF JAKARTA

COLLIERS INTERNATIONAL | P. 11

JAKARTA | 1Q 2012 | APARTMENT

Colliers International Indonesia - Research

P. 12 | COLLIERS INTERNATIONAL

JAKARTA | 1Q 2012 | APARTMENT

LIST OF UNDER CONSTRUCTION OF STRATA-TITLE APARTMENT

APARTMENT NAME LOCATION REGION DEVELOPER NAME #UNITS2012

Regatta Rio de Janeiro Pantai Mutiara North Jakarta Badan Kerjasama Mutiara Buana (JO PT Intiland

Development & PT Global Ekabuana)

110

Green Palace (5 Towers) Kalibata South Jakarta Agung Podomoro Group 3,150

Belmont Residence (Tower Everest) Kebon Jeruk West Jakarta Gapura Prima 553

Ambassade Residence (Tower A) Kuningan CBD PT Duta Regency 400

Senopati Suites Senopati South Jakarta PT Mahkota Asia Graha 103

Denpasar Residence (Tower Kintamani and Ubud) Satrio CBD Agung Podomoro Group 1,100

The Grove Rasuna Said CBD PT Bakrieland Development 416

Residence 8 at Senopati (2 Towers) Senopati South Jakarta Agung Sedayu Group 400

The Wave Rasuna Said CBD PT Bakrieland Development 1,900

Pancoran Riverside Pengadegan Timur South Jakarta PT Graha Rayhan Tri Putra (Riyadh Group) 1,900

Luxurious Raffles Residences at Ciputra World Jakarta 1 Satrio CBD PT Ciputra Property Tbk 88

St Moritz (The Presidential Suite Tower, The

Ambassador Suite Tower & The Royal Suite Tower)

Puri Indah West Jakarta PT Lippo Karawaci Tbk 484

Sentra Timur Residence (phase 2) Cakung East Jakarta PT Bakrieland Development 1,143

Menteng Square Matraman East Jakarta PT Bahama Development 1,500

Cervino Village Kasablanka South Jakarta Pakkodian 518

Puri Park View (2 Towers) Meruya Utara West Jakarta PT Pelaksana Jaya Mulia & PT Alam Jaya

Perkasa

2,000

The Grove Suite Rasuna Said CBD PT Bakrieland Development 151

The Royal Springhill (Tower Marygold & Magnolia) Kemayoran Central Jakarta Springhill Golf Group 384

The East at Essence Darmawangsa Kebayoran South Jakarta PT Prakarsa Semesta Alam 244

Myhome Apartment at Ciputra World Jakarta 1 Satrio CBD PT Ciputra Property Tbk 136

Gading Nias Residence block Grand Emerald Kelapa Gading North Jakarta Agung Podomoro Group 747

One Park Residence Gandaria South Jakarta PT Intiland Development 379

Tamansari Semanggi Gatot Subroto CBD PT Wika Realty 1,400

Verde Condominium Rasuna Said CBD PT Farpoint Realty Indonesia 257

The H Tower Rasuna Said CBD PT Hutama Karya Realtindo 9

Season City (Tower C) Grogol West Jakarta Agung Podomoro Group 714

2013Belmont Residence (Tower Montblanc) Kebon Jeruk West Jakarta Gapura Prima 350

Westmark Tanjung Duren West Jakarta Cowell Development 550

Kebagusan City (Tower B) S Parman West Jakarta Gapura Prima 588

GP Plaza Gatot Subroto CBD Gapura Prima 320

Pasar Baru Mansion (2 Towers) Pasar Baru Central Jakarta PT Trikarya Idea Sakti 520

Kemang Village (The Tiffany & The Infinity) Kemang South Jakarta PT Lippo Karawaci Tbk 415

Residence at Dharmawangsa Dharmawangsa South Jakarta PT Bina Puri Lestari 89

Sentra Timur Residence (Stage 2) Cakung East Jakarta PT Bakrieland Development 1,000

Green Bay Pluit Pluit North Jakarta Agung Podomoro Group 3,200

Green Lake Sunter Sunter North Jakarta Agung Podomoro Group 2,400

d’Green Pramuka (Tower Faggio & Pino) Rawasari Central Jakarta PT Duta Paramindo 2,900

The Windsor (2 Towers) Puri Indah West Jakarta PT Antilope Madju Puri Indah 340

Pakubuwono Terrace (Tower I) Ciledug South Jakarta PT Selaras Mitra Sejati 750

The H Residence Cawang East Jakarta PT Hutama Karya Realtindo 505

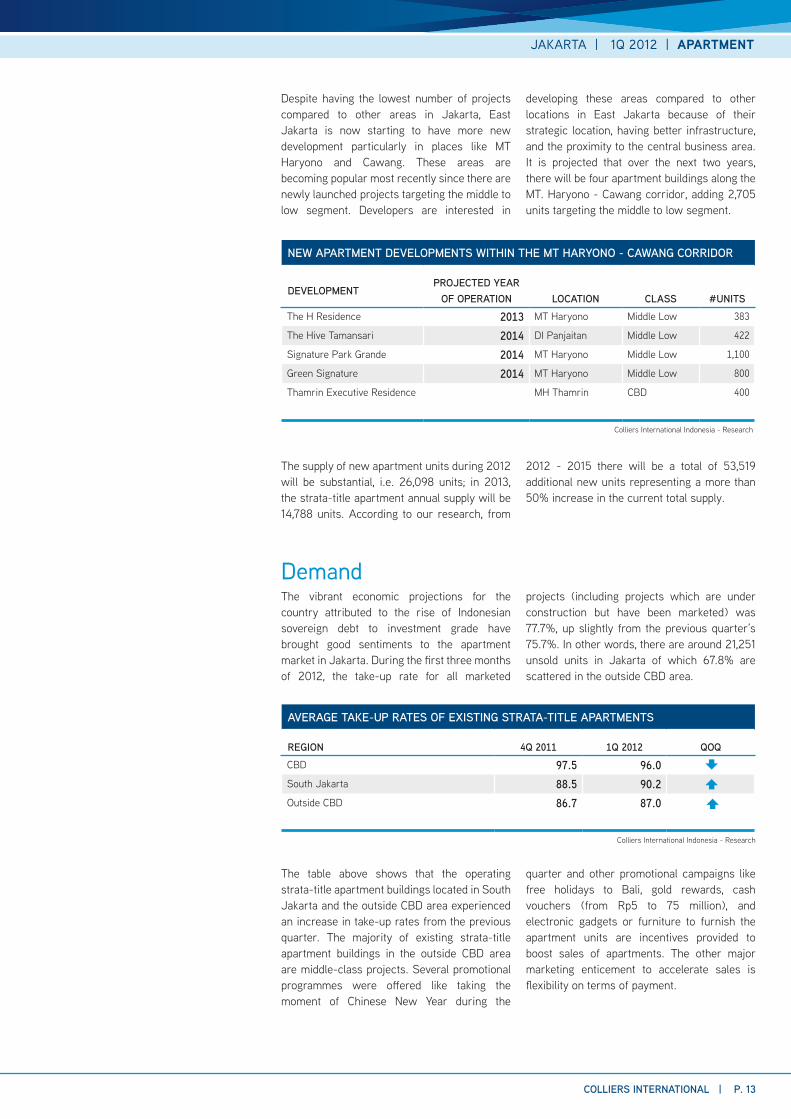

Despite having the lowest number of projects compared to other areas in Jakarta, East Jakarta is now starting to have more new development particularly in places like MT Haryono and Cawang. These areas are becoming popular most recently since there are newly launched projects targeting the middle to low segment. Developers are interested in

developing these areas compared to other locations in East Jakarta because of their strategic location, having better infrastructure, and the proximity to the central business area. It is projected that over the next two years, there will be four apartment buildings along the MT. Haryono - Cawang corridor, adding 2,705 units targeting the middle to low segment.

Colliers International Indonesia - Research

The supply of new apartment units during 2012 will be substantial, i.e. 26,098 units; in 2013, the strata-title apartment annual supply will be 14,788 units. According to our research, from

2012 - 2015 there will be a total of 53,519 additional new units representing a more than 50% increase in the current total supply.

DemandThe vibrant economic projections for the country attributed to the rise of Indonesian sovereign debt to investment grade have brought good sentiments to the apartment market in Jakarta. During the first three months of 2012, the take-up rate for all marketed

projects (including projects which are under construction but have been marketed) was 77.7%, up slightly from the previous quarter’s 75.7%. In other words, there are around 21,251 unsold units in Jakarta of which 67.8% are scattered in the outside CBD area.

Colliers International Indonesia - Research

AVERAGE TAKE-UP RATES OF EXISTING STRATA-TITLE APARTMENTS

REGION 4Q 2011 1Q 2012 QOQCBD 97.5 96.0South Jakarta 88.5 90.2Outside CBD 86.7 87.0

NEW APARTMENT DEVELOPMENTS WITHIN THE MT HARYONO - CAWANG CORRIDOR

DEVELOPMENTPROJECTED YEAR

OF OPERATION LOCATION CLASS #UNITSThe H Residence 2013 MT Haryono Middle Low 383

The Hive Tamansari 2014 DI Panjaitan Middle Low 422

Signature Park Grande 2014 MT Haryono Middle Low 1,100

Green Signature 2014 MT Haryono Middle Low 800

Thamrin Executive Residence MH Thamrin CBD 400

The table above shows that the operating strata-title apartment buildings located in South Jakarta and the outside CBD area experienced an increase in take-up rates from the previous quarter. The majority of existing strata-title apartment buildings in the outside CBD area are middle-class projects. Several promotional programmes were offered like taking the moment of Chinese New Year during the

quarter and other promotional campaigns like free holidays to Bali, gold rewards, cash vouchers (from Rp5 to 75 million), and electronic gadgets or furniture to furnish the apartment units are incentives provided to boost sales of apartments. The other major marketing enticement to accelerate sales is flexibility on terms of payment.

COLLIERS INTERNATIONAL | P. 13

JAKARTA | 1Q 2012 | APARTMENT

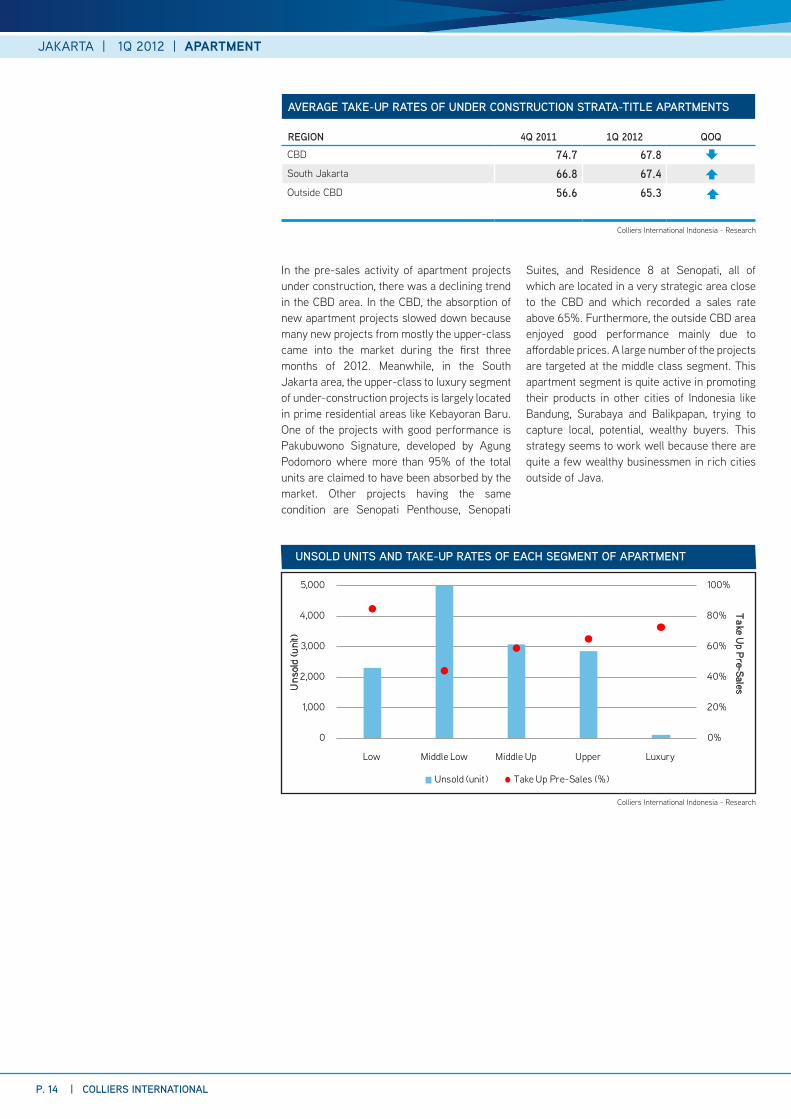

AVERAGE TAKE-UP RATES OF UNDER CONSTRUCTION STRATA-TITLE APARTMENTS

REGION 4Q 2011 1Q 2012 QOQCBD 74.7 67.8South Jakarta 66.8 67.4Outside CBD 56.6 65.3

In the pre-sales activity of apartment projects under construction, there was a declining trend in the CBD area. In the CBD, the absorption of new apartment projects slowed down because many new projects from mostly the upper-class came into the market during the first three months of 2012. Meanwhile, in the South Jakarta area, the upper-class to luxury segment of under-construction projects is largely located in prime residential areas like Kebayoran Baru. One of the projects with good performance is Pakubuwono Signature, developed by Agung Podomoro where more than 95% of the total units are claimed to have been absorbed by the market. Other projects having the same condition are Senopati Penthouse, Senopati

Suites, and Residence 8 at Senopati, all of which are located in a very strategic area close to the CBD and which recorded a sales rate above 65%. Furthermore, the outside CBD area enjoyed good performance mainly due to affordable prices. A large number of the projects are targeted at the middle class segment. This apartment segment is quite active in promoting their products in other cities of Indonesia like Bandung, Surabaya and Balikpapan, trying to capture local, potential, wealthy buyers. This strategy seems to work well because there are quite a few wealthy businessmen in rich cities outside of Java.

Colliers International Indonesia - Research

UNSOLD UNITS AND TAKE-UP RATES OF EACH SEGMENT OF APARTMENT

Colliers International Indonesia - Research

0%

20%

40%

60%

80%

100%

0

1,000

2,000

3,000

4,000

5,000

Low Middle Low Middle Up Upper Luxury

Uns

old

(uni

t)

Unsold (unit) Take Up Pre-Sales (%)

Take

Up P

re-Sales

P. 14 | COLLIERS INTERNATIONAL

JAKARTA | 1Q 2012 | APARTMENT

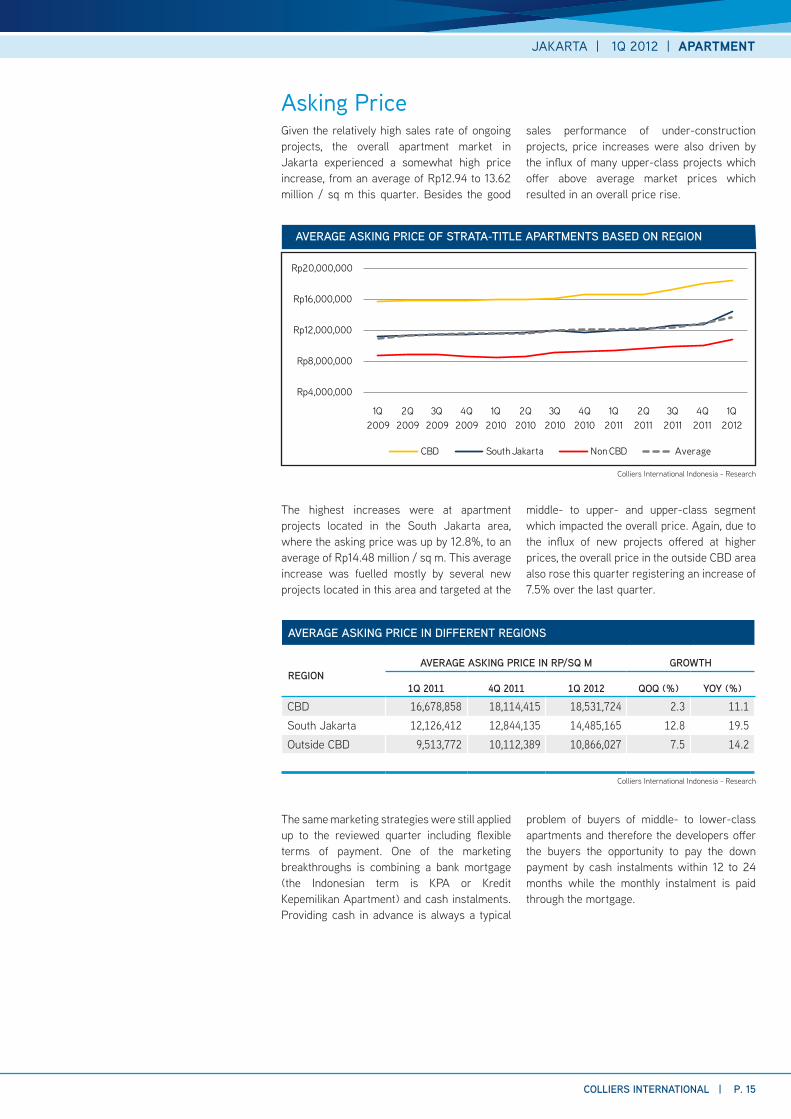

Given the relatively high sales rate of ongoing projects, the overall apartment market in Jakarta experienced a somewhat high price increase, from an average of Rp12.94 to 13.62 million / sq m this quarter. Besides the good

sales performance of under-construction projects, price increases were also driven by the influx of many upper-class projects which offer above average market prices which resulted in an overall price rise.

Asking Price

AVERAGE ASKING PRICE OF STRATA-TITLE APARTMENTS BASED ON REGION

Colliers International Indonesia - Research

AVERAGE ASKING PRICE IN DIFFERENT REGIONS

REGIONAVERAGE ASKING PRICE IN RP/SQ M GROWTH

1Q 2011 4Q 2011 1Q 2012 QOQ (%) YOY (%)

CBD 16,678,858 18,114,415 18,531,724 2.3 11.1South Jakarta 12,126,412 12,844,135 14,485,165 12.8 19.5Outside CBD 9,513,772 10,112,389 10,866,027 7.5 14.2

The same marketing strategies were still applied up to the reviewed quarter including flexible terms of payment. One of the marketing breakthroughs is combining a bank mortgage (the Indonesian term is KPA or Kredit Kepemilikan Apartment) and cash instalments. Providing cash in advance is always a typical

problem of buyers of middle- to lower-class apartments and therefore the developers offer the buyers the opportunity to pay the down payment by cash instalments within 12 to 24 months while the monthly instalment is paid through the mortgage.

The highest increases were at apartment projects located in the South Jakarta area, where the asking price was up by 12.8%, to an average of Rp14.48 million / sq m. This average increase was fuelled mostly by several new projects located in this area and targeted at the

middle- to upper- and upper-class segment which impacted the overall price. Again, due to the influx of new projects offered at higher prices, the overall price in the outside CBD area also rose this quarter registering an increase of 7.5% over the last quarter.

Colliers International Indonesia - Research

Rp4,000,000

Rp8,000,000

Rp12,000,000

Rp16,000,000

Rp20,000,000

1Q 2009

2Q 2009

3Q 2009

4Q 2009

1Q 2010

2Q 2010

3Q 2010

4Q 2010

1Q 2011

2Q 2011

3Q 2011

4Q 2011

1Q 2012

CBD South Jakarta Non CBD Average

COLLIERS INTERNATIONAL | P. 15

JAKARTA | 1Q 2012 | APARTMENT

Basically there are three payment methods of buying apartments, mortgages (KPA), cash instalments and hard cash. From our survey it was found that cash instalments is the most frequent method used (55 to 70% of buyers, ranging from the lower to upper segments). Most buyers opt for this because they have the capability to pay cash instalments and it offers simplicity, flexibility, and privacy (because they do not want to reveal their income). It is interesting to note that payment through a bank mortgage is not widely chosen even for lower-class apartment projects. These units (the

Indonesian term is “rusunami”) were originally government-subsidised projects for the low to middle income levels, however the fact is that buyers of these apartments preferred to pay using cash instalments. This indicates that the target buyers have deviated because the fact is that buyers are not middle income occupiers but are investors. For buyers of middle to upper class apartments they may pay cash installment or hard cash because buyers are mainly those with strong financial capability and they do no want to endure the hassle of dealing with bank procedures.

COMPOSITION OF PAYMENT METHODS FOR BUYING APARTMENT UNITS

Colliers International Indonesia - Research

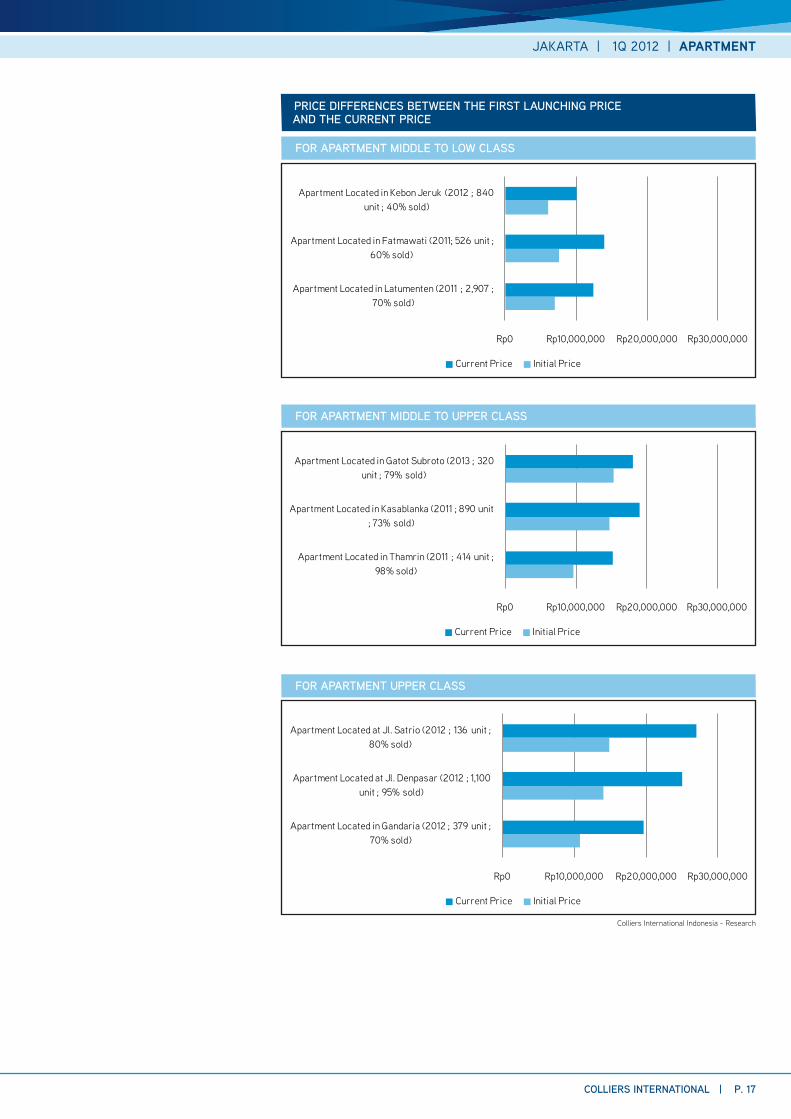

The graphs follow give an overview of new apartment sales and price performance from middle to upper class. We take some samples of operating and under-construction apartment projects to show the price differences between

the first launching price and the current price. This has been a common practice among developers where prices are always reviewed in accordance with the sales performance.

COMPARISON OF KPA AND CASH INSTALLMENT PAYMENT PERIOD

KPA (MORTGAGES) CASH INSTALLMENTPayment Tenure Maximum of up to 15 years (depending on

the age of applicant)Generally 1 - 3 years

Requirements ID card, income statement and BI (Bank

Central) checking account

ID card and marriage certificate

(if applicable)

Typical Buyers Employees Traders and Businessmen

Colliers International Indonesia - Research

0%

20%

40%

60%

80%

100%

KPA Hardcash Installment (12 - 36x)

Low (Rusunami) Middle Upper

P. 16 | COLLIERS INTERNATIONAL

JAKARTA | 1Q 2012 | APARTMENT

PRICE DIFFERENCES BETWEEN THE FIRST LAUNCHING PRICE AND THE CURRENT PRICE

FOR APARTMENT MIDDLE TO LOW CLASS

FOR APARTMENT MIDDLE TO UPPER CLASS

FOR APARTMENT UPPER CLASS

Colliers International Indonesia - Research

Rp0 Rp10,000,000 Rp20,000,000 Rp30,000,000

Apartment Located in Latumenten (2011 ; 2,907 ; 70% sold)

Apartment Located in Fatmawati (2011; 526 unit ; 60% sold)

Apartment Located in Kebon Jeruk (2012 ; 840 unit ; 40% sold)

Current Price Initial Price

Rp0 Rp10,000,000 Rp20,000,000 Rp30,000,000

Apartment Located in Thamrin (2011 ; 414 unit ; 98% sold)

Apartment Located in Kasablanka (2011 ; 890 unit ; 73% sold)

Apartment Located in Gatot Subroto (2013 ; 320 unit ; 79% sold)

Current Price Initial Price

Rp0 Rp10,000,000 Rp20,000,000 Rp30,000,000

Apartment Located in Gandaria (2012 ; 379 unit ; 70% sold)

Apartment Located at Jl. Denpasar (2012 ; 1,100 unit ; 95% sold)

Apartment Located at Jl. Satrio (2012 ; 136 unit ; 80% sold)

Current Price Initial Price

COLLIERS INTERNATIONAL | P. 17

JAKARTA | 1Q 2012 | APARTMENT

Apartment For Lease (Serviced and Non-serviced)

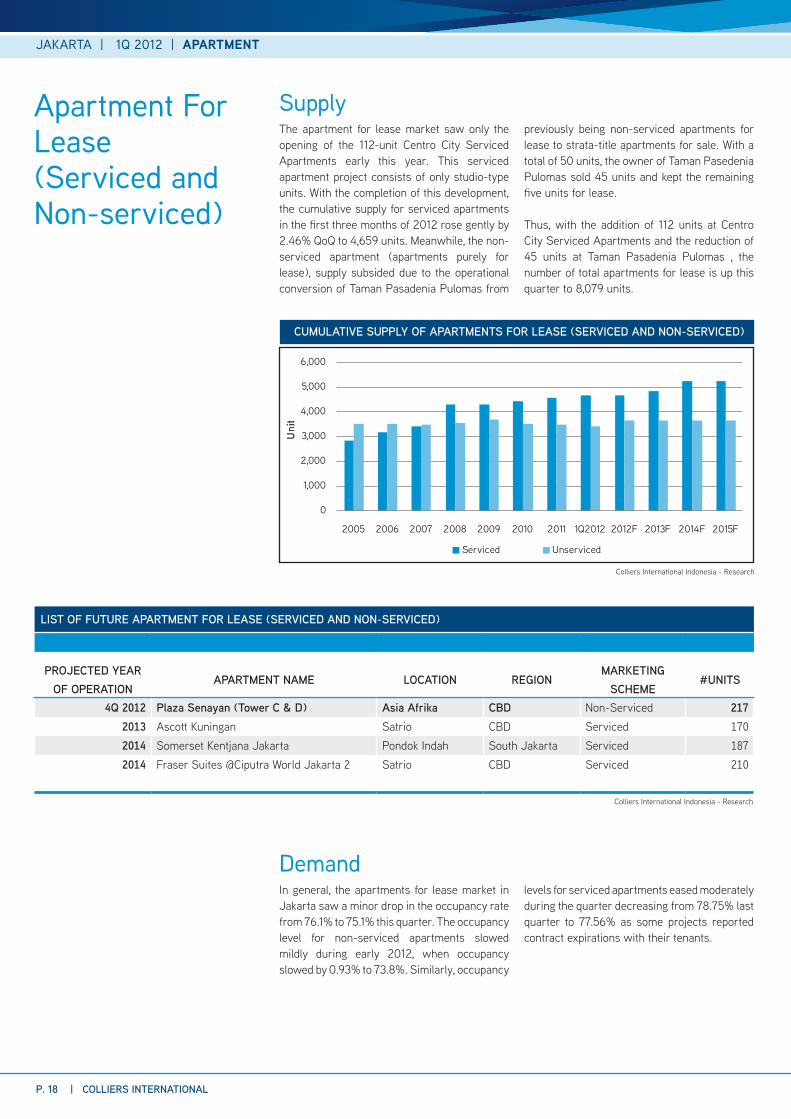

The apartment for lease market saw only the opening of the 112-unit Centro City Serviced Apartments early this year. This serviced apartment project consists of only studio-type units. With the completion of this development, the cumulative supply for serviced apartments in the first three months of 2012 rose gently by 2.46% QoQ to 4,659 units. Meanwhile, the non-serviced apartment (apartments purely for lease), supply subsided due to the operational conversion of Taman Pasadenia Pulomas from

previously being non-serviced apartments for lease to strata-title apartments for sale. With a total of 50 units, the owner of Taman Pasedenia Pulomas sold 45 units and kept the remaining five units for lease.

Thus, with the addition of 112 units at Centro City Serviced Apartments and the reduction of 45 units at Taman Pasadenia Pulomas , the number of total apartments for lease is up this quarter to 8,079 units.

Colliers International Indonesia - Research

In general, the apartments for lease market in Jakarta saw a minor drop in the occupancy rate from 76.1% to 75.1% this quarter. The occupancy level for non-serviced apartments slowed mildly during early 2012, when occupancy slowed by 0.93% to 73.8%. Similarly, occupancy

levels for serviced apartments eased moderately during the quarter decreasing from 78.75% last quarter to 77.56% as some projects reported contract expirations with their tenants.

Supply

LIST OF FUTURE APARTMENT FOR LEASE (SERVICED AND NON-SERVICED)

PROJECTED YEAR OF OPERATION

APARTMENT NAME LOCATION REGIONMARKETING

SCHEME#UNITS

4Q 2012 Plaza Senayan (Tower C & D) Asia Afrika CBD Non-Serviced 2172013 Ascott Kuningan Satrio CBD Serviced 1702014 Somerset Kentjana Jakarta Pondok Indah South Jakarta Serviced 1872014 Fraser Suites @Ciputra World Jakarta 2 Satrio CBD Serviced 210

Demand

CUMULATIVE SUPPLY OF APARTMENTS FOR LEASE (SERVICED AND NON-SERVICED)

Colliers International Indonesia - Research

0

1,000

2,000

3,000

4,000

5,000

6,000

2005 2006 2007 2008 2009 2010 2011 1Q2012 2012F 2013F 2014F 2015F

Uni

t

Serviced Unserviced

P. 18 | COLLIERS INTERNATIONAL

JAKARTA | 1Q 2012 | APARTMENT

Geographically, apartments located in the CBD area captured the highest occupancy level compared to other areas although the occupancy level showed a minor drop QoQ to 84.4%. Compared to the occupancy performance in the outside CBD area that was only 66.5%, the CBD area is still the best location for renting apartments. In general, apartments for lease,

either serviced or non-serviced, are occupied by expatriates who are looking for proximity either to the workplace or an international school. Therefore, the performance of apartments for lease in South Jakarta is much better despite having a minor drop in occupancy (76.2%) this quarter.

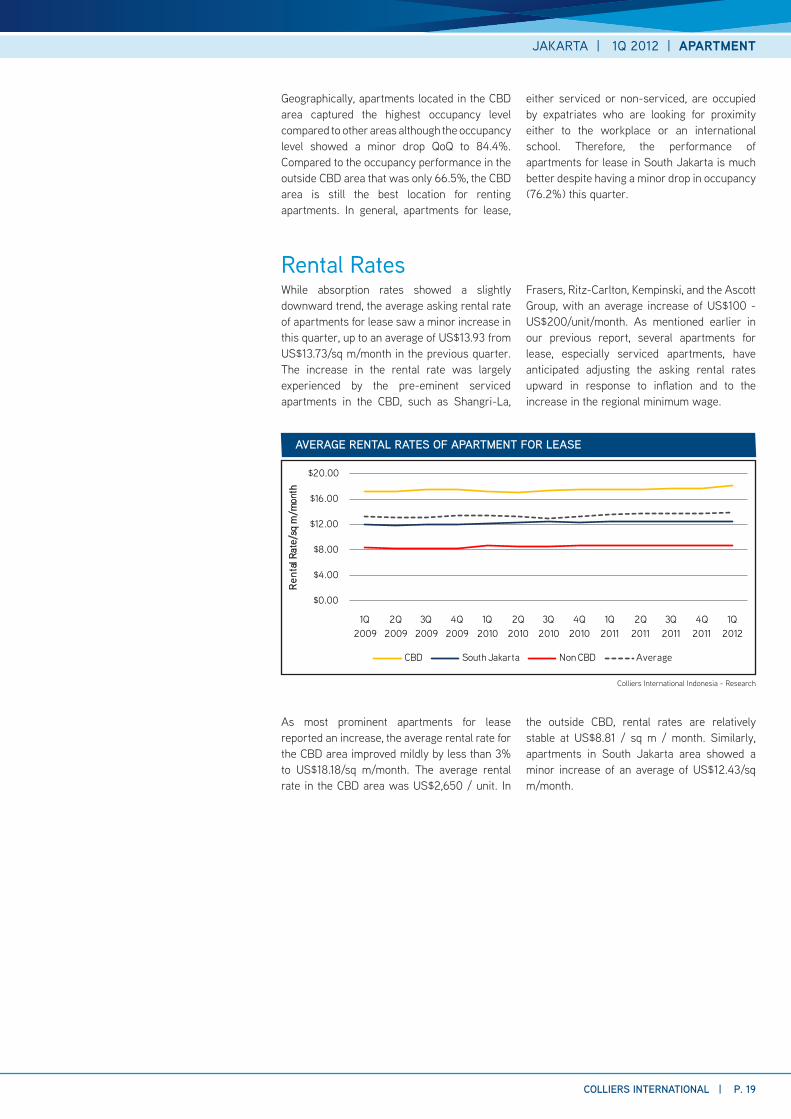

While absorption rates showed a slightly downward trend, the average asking rental rate of apartments for lease saw a minor increase in this quarter, up to an average of US$13.93 from US$13.73/sq m/month in the previous quarter. The increase in the rental rate was largely experienced by the pre-eminent serviced apartments in the CBD, such as Shangri-La,

Frasers, Ritz-Carlton, Kempinski, and the Ascott Group, with an average increase of US$100 - US$200/unit/month. As mentioned earlier in our previous report, several apartments for lease, especially serviced apartments, have anticipated adjusting the asking rental rates upward in response to inflation and to the increase in the regional minimum wage.

Rental Rates

AVERAGE RENTAL RATES OF APARTMENT FOR LEASE

Colliers International Indonesia - Research

As most prominent apartments for lease reported an increase, the average rental rate for the CBD area improved mildly by less than 3% to US$18.18/sq m/month. The average rental rate in the CBD area was US$2,650 / unit. In

the outside CBD, rental rates are relatively stable at US$8.81 / sq m / month. Similarly, apartments in South Jakarta area showed a minor increase of an average of US$12.43/sq m/month.

$0.00

$4.00

$8.00

$12.00

$16.00

$20.00

1Q 2009

2Q 2009

3Q 2009

4Q 2009

1Q 2010

2Q 2010

3Q 2010

4Q 2010

1Q 2011

2Q 2011

3Q 2011

4Q 2011

1Q 2012

Ren

tal R

ate/

sq m

/mon

th

CBD South Jakarta Non CBD Average

COLLIERS INTERNATIONAL | P. 19

JAKARTA | 1Q 2012 | APARTMENT

The prospects for the apartment market will remain favourable as long as underlying local market conditions and business confidence continue to be rosy. We do not expect too much land reform concerning the foreign ownership of Indonesian property but as long as the conducive business atmosphere can be maintained there is plenty of room for the apartment market to grow, particularly benefiting from the potential spending of wealthy Indonesians from the other rich provinces of Indonesia. As we predicted earlier, apartment prices will surge ahead this year and this has already

proven to be the case in the early part of 2012 when the average apartment price went up albeit moderately. Price increases will not only be a result of the new and under-construction projects with above average market prices; they will also be impacted by the continued adjustments made by pre-selling apartment projects (i.e. apartments under construction but which have already been marketed). New projects in the CBD area will surely experience the most increases as land prices soar and in anticipation of the fuel price hike which will be implemented in six months, increasing construction costs which will be a significant factor in adjusting apartment prices.

Outlook

P. 20 | COLLIERS INTERNATIONAL

JAKARTA | 1Q 2012 | APARTMENT

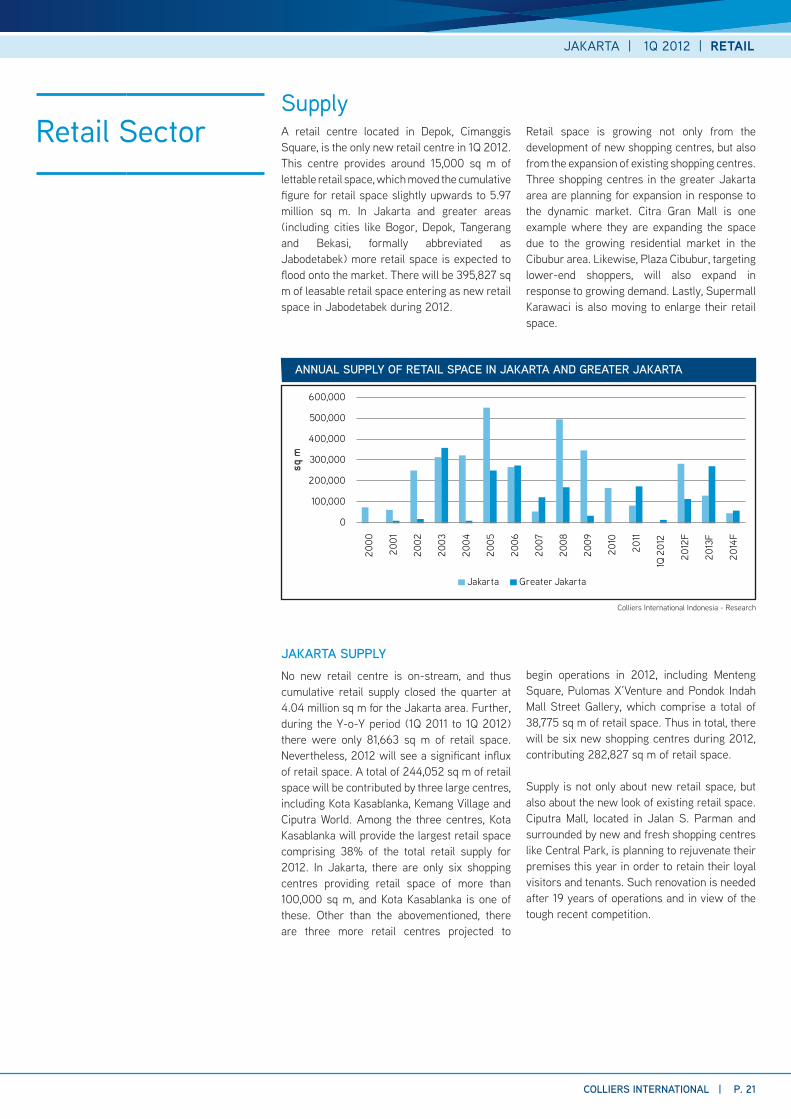

Retail Sector A retail centre located in Depok, Cimanggis Square, is the only new retail centre in 1Q 2012. This centre provides around 15,000 sq m of lettable retail space, which moved the cumulative figure for retail space slightly upwards to 5.97 million sq m. In Jakarta and greater areas (including cities like Bogor, Depok, Tangerang and Bekasi, formally abbreviated as Jabodetabek) more retail space is expected to flood onto the market. There will be 395,827 sq m of leasable retail space entering as new retail space in Jabodetabek during 2012.

Retail space is growing not only from the development of new shopping centres, but also from the expansion of existing shopping centres. Three shopping centres in the greater Jakarta area are planning for expansion in response to the dynamic market. Citra Gran Mall is one example where they are expanding the space due to the growing residential market in the Cibubur area. Likewise, Plaza Cibubur, targeting lower-end shoppers, will also expand in response to growing demand. Lastly, Supermall Karawaci is also moving to enlarge their retail space.

Supply

ANNUAL SUPPLY OF RETAIL SPACE IN JAKARTA AND GREATER JAKARTA

Colliers International Indonesia - Research

JAKARTA SUPPLYNo new retail centre is on-stream, and thus cumulative retail supply closed the quarter at 4.04 million sq m for the Jakarta area. Further, during the Y-o-Y period (1Q 2011 to 1Q 2012) there were only 81,663 sq m of retail space. Nevertheless, 2012 will see a significant influx of retail space. A total of 244,052 sq m of retail space will be contributed by three large centres, including Kota Kasablanka, Kemang Village and Ciputra World. Among the three centres, Kota Kasablanka will provide the largest retail space comprising 38% of the total retail supply for 2012. In Jakarta, there are only six shopping centres providing retail space of more than 100,000 sq m, and Kota Kasablanka is one of these. Other than the abovementioned, there are three more retail centres projected to

begin operations in 2012, including Menteng Square, Pulomas X’Venture and Pondok Indah Mall Street Gallery, which comprise a total of 38,775 sq m of retail space. Thus in total, there will be six new shopping centres during 2012, contributing 282,827 sq m of retail space. Supply is not only about new retail space, but also about the new look of existing retail space. Ciputra Mall, located in Jalan S. Parman and surrounded by new and fresh shopping centres like Central Park, is planning to rejuvenate their premises this year in order to retain their loyal visitors and tenants. Such renovation is needed after 19 years of operations and in view of the tough recent competition.

0

100,000

200,000

300,000

400,000

500,000

600,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

1Q 2

012

2012

F

2013

F

2014

F

sq m

Jakarta Greater Jakarta

COLLIERS INTERNATIONAL | P. 21

JAKARTA | 1Q 2012 | RETAIL

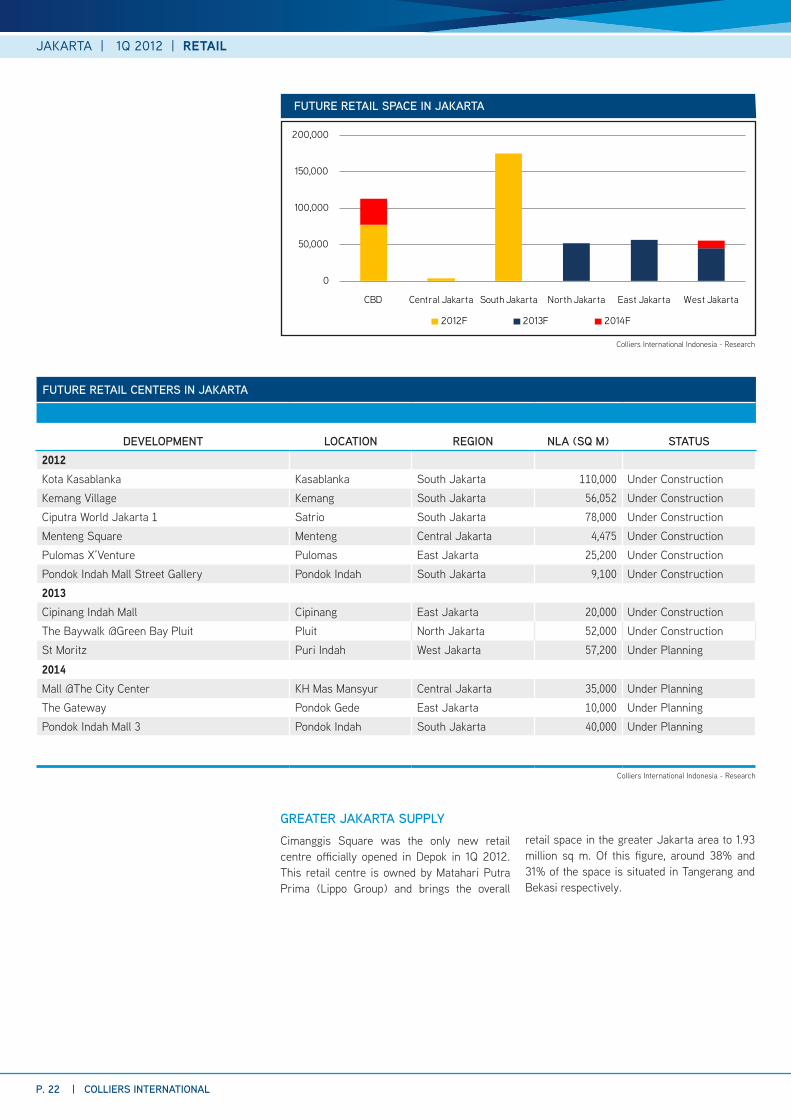

FUTURE RETAIL CENTERS IN JAKARTA

DEVELOPMENT LOCATION REGION NLA (SQ M) STATUS2012Kota Kasablanka Kasablanka South Jakarta 110,000 Under ConstructionKemang Village Kemang South Jakarta 56,052 Under ConstructionCiputra World Jakarta 1 Satrio South Jakarta 78,000 Under ConstructionMenteng Square Menteng Central Jakarta 4,475 Under ConstructionPulomas X’Venture Pulomas East Jakarta 25,200 Under ConstructionPondok Indah Mall Street Gallery Pondok Indah South Jakarta 9,100 Under Construction2013Cipinang Indah Mall Cipinang East Jakarta 20,000 Under ConstructionThe Baywalk @Green Bay Pluit Pluit North Jakarta 52,000 Under ConstructionSt Moritz Puri Indah West Jakarta 57,200 Under Planning

2014Mall @The City Center KH Mas Mansyur Central Jakarta 35,000 Under PlanningThe Gateway Pondok Gede East Jakarta 10,000 Under PlanningPondok Indah Mall 3 Pondok Indah South Jakarta 40,000 Under Planning

Colliers International Indonesia - Research

FUTURE RETAIL SPACE IN JAKARTA

Colliers International Indonesia - Research

0

50,000

100,000

150,000

200,000

CBD Central Jakarta South Jakarta North Jakarta East Jakarta West Jakarta

2012F 2013F 2014F

GREATER JAKARTA SUPPLYCimanggis Square was the only new retail centre officially opened in Depok in 1Q 2012. This retail centre is owned by Matahari Putra Prima (Lippo Group) and brings the overall

retail space in the greater Jakarta area to 1.93 million sq m. Of this figure, around 38% and 31% of the space is situated in Tangerang and Bekasi respectively.

P. 22 | COLLIERS INTERNATIONAL

JAKARTA | 1Q 2012 | RETAIL

RETAIL SPACE DISTRIBUTION IN GREATER JAKARTA

Colliers International Indonesia - Research

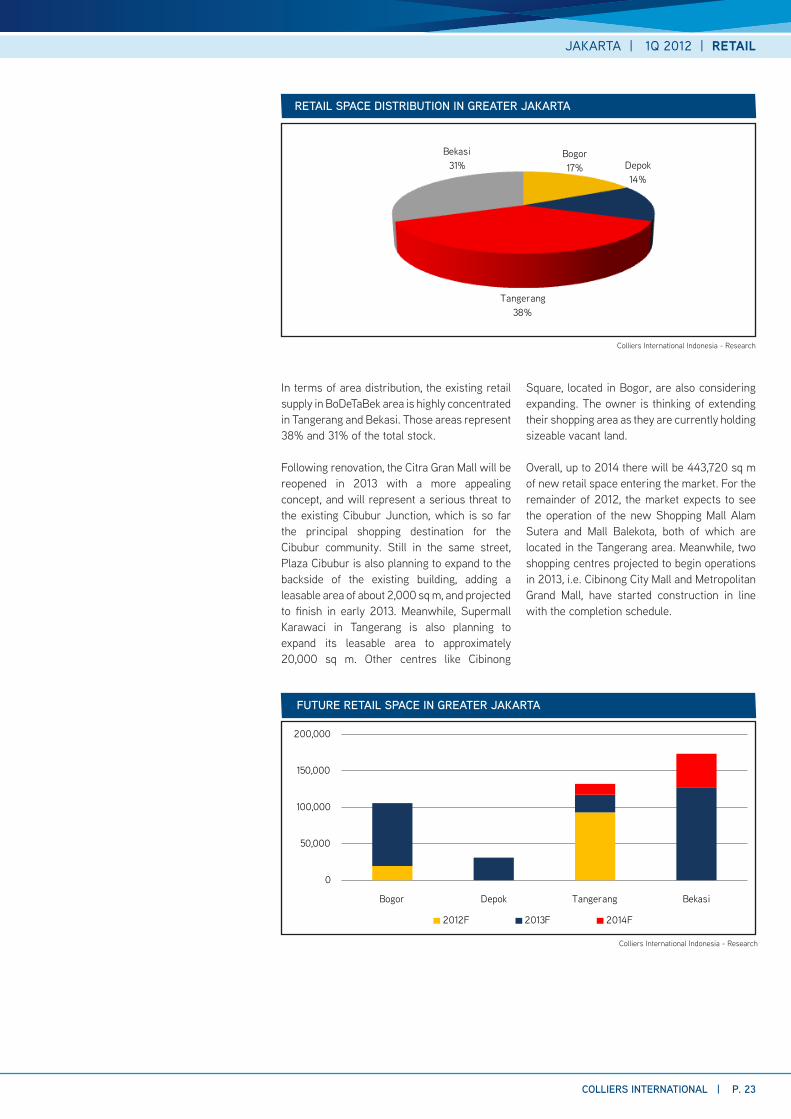

In terms of area distribution, the existing retail supply in BoDeTaBek area is highly concentrated in Tangerang and Bekasi. Those areas represent 38% and 31% of the total stock. Following renovation, the Citra Gran Mall will be reopened in 2013 with a more appealing concept, and will represent a serious threat to the existing Cibubur Junction, which is so far the principal shopping destination for the Cibubur community. Still in the same street, Plaza Cibubur is also planning to expand to the backside of the existing building, adding a leasable area of about 2,000 sq m, and projected to finish in early 2013. Meanwhile, Supermall Karawaci in Tangerang is also planning to expand its leasable area to approximately 20,000 sq m. Other centres like Cibinong

Square, located in Bogor, are also considering expanding. The owner is thinking of extending their shopping area as they are currently holding sizeable vacant land. Overall, up to 2014 there will be 443,720 sq m of new retail space entering the market. For the remainder of 2012, the market expects to see the operation of the new Shopping Mall Alam Sutera and Mall Balekota, both of which are located in the Tangerang area. Meanwhile, two shopping centres projected to begin operations in 2013, i.e. Cibinong City Mall and Metropolitan Grand Mall, have started construction in line with the completion schedule.

Bogor17% Depok

14%

Tangerang38%

Bekasi31%

FUTURE RETAIL SPACE IN GREATER JAKARTA

Colliers International Indonesia - Research

0

50,000

100,000

150,000

200,000

Bogor Depok Tangerang Bekasi

2012F 2013F 2014F

COLLIERS INTERNATIONAL | P. 23

JAKARTA | 1Q 2012 | RETAIL

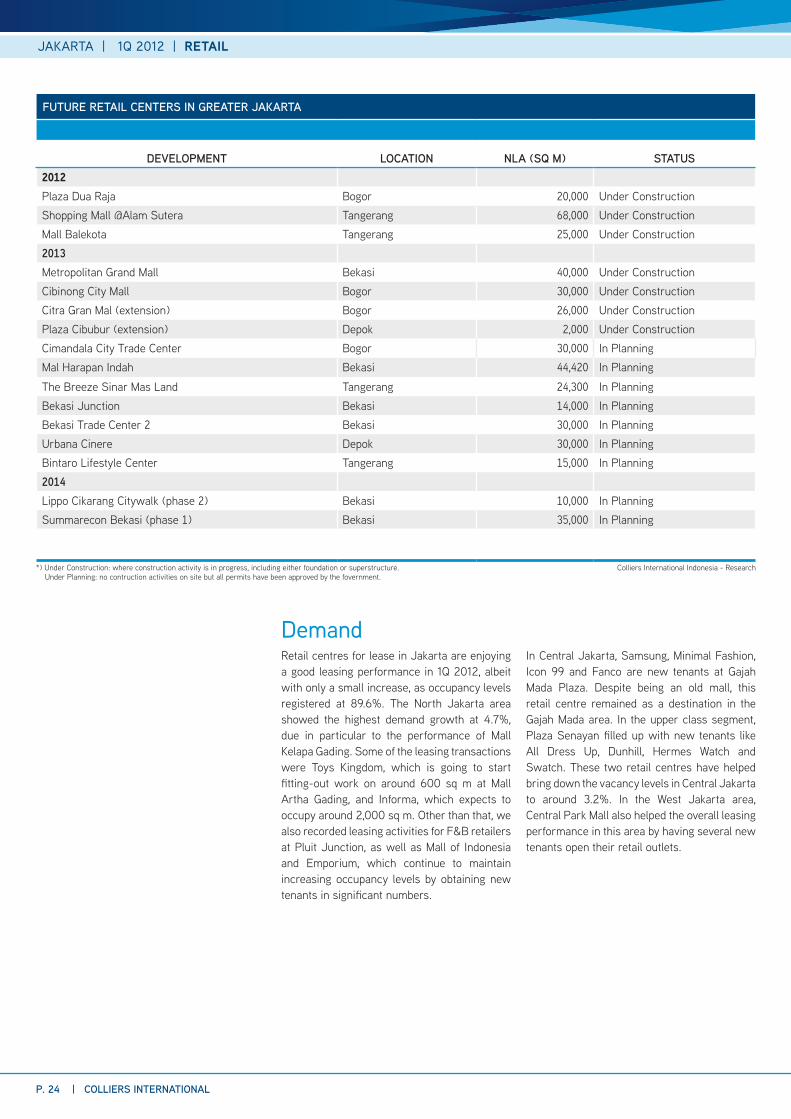

FUTURE RETAIL CENTERS IN GREATER JAKARTA

DEVELOPMENT LOCATION NLA (SQ M) STATUS2012Plaza Dua Raja Bogor 20,000 Under ConstructionShopping Mall @Alam Sutera Tangerang 68,000 Under ConstructionMall Balekota Tangerang 25,000 Under Construction2013Metropolitan Grand Mall Bekasi 40,000 Under ConstructionCibinong City Mall Bogor 30,000 Under ConstructionCitra Gran Mal (extension) Bogor 26,000 Under ConstructionPlaza Cibubur (extension) Depok 2,000 Under ConstructionCimandala City Trade Center Bogor 30,000 In PlanningMal Harapan Indah Bekasi 44,420 In Planning

The Breeze Sinar Mas Land Tangerang 24,300 In PlanningBekasi Junction Bekasi 14,000 In PlanningBekasi Trade Center 2 Bekasi 30,000 In PlanningUrbana Cinere Depok 30,000 In PlanningBintaro Lifestyle Center Tangerang 15,000 In Planning2014Lippo Cikarang Citywalk (phase 2) Bekasi 10,000 In PlanningSummarecon Bekasi (phase 1) Bekasi 35,000 In Planning

Colliers International Indonesia - Research

Demand Retail centres for lease in Jakarta are enjoying a good leasing performance in 1Q 2012, albeit with only a small increase, as occupancy levels registered at 89.6%. The North Jakarta area showed the highest demand growth at 4.7%, due in particular to the performance of Mall Kelapa Gading. Some of the leasing transactions were Toys Kingdom, which is going to start fitting-out work on around 600 sq m at Mall Artha Gading, and Informa, which expects to occupy around 2,000 sq m. Other than that, we also recorded leasing activities for F&B retailers at Pluit Junction, as well as Mall of Indonesia and Emporium, which continue to maintain increasing occupancy levels by obtaining new tenants in significant numbers.

In Central Jakarta, Samsung, Minimal Fashion, Icon 99 and Fanco are new tenants at Gajah Mada Plaza. Despite being an old mall, this retail centre remained as a destination in the Gajah Mada area. In the upper class segment, Plaza Senayan filled up with new tenants like All Dress Up, Dunhill, Hermes Watch and Swatch. These two retail centres have helped bring down the vacancy levels in Central Jakarta to around 3.2%. In the West Jakarta area, Central Park Mall also helped the overall leasing performance in this area by having several new tenants open their retail outlets.

*) Under Construction: where construction activity is in progress, including either foundation or superstructure. Under Planning: no contruction activities on site but all permits have been approved by the fovernment.

P. 24 | COLLIERS INTERNATIONAL

JAKARTA | 1Q 2012 | RETAIL

In East Jakarta, Kramat Jati Indah is still being renovated, but a number of tenants are preparing to return to a better concept in the mall. XXI cinema will be occupying this shopping centre, and it will be the first XXI in East Jakarta.

In South Jakarta, food and beverages (F&B) retailers are quite actively expanding their outlets in several retail centres, along with other mini-anchors, to complement tenancy mainly in the newly operating malls.

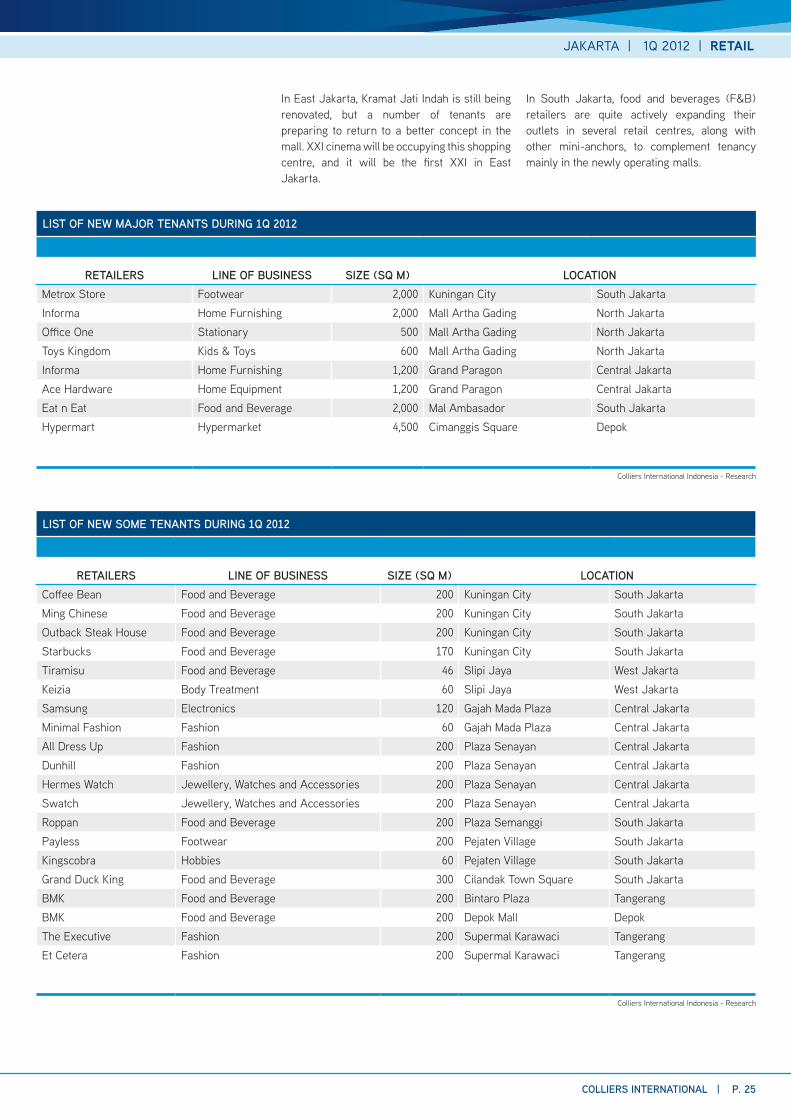

LIST OF NEW MAJOR TENANTS DURING 1Q 2012

RETAILERS LINE OF BUSINESS SIZE (SQ M) LOCATIONMetrox Store Footwear 2,000 Kuningan City South JakartaInforma Home Furnishing 2,000 Mall Artha Gading North JakartaOffice One Stationary 500 Mall Artha Gading North JakartaToys Kingdom Kids & Toys 600 Mall Artha Gading North JakartaInforma Home Furnishing 1,200 Grand Paragon Central JakartaAce Hardware Home Equipment 1,200 Grand Paragon Central JakartaEat n Eat Food and Beverage 2,000 Mal Ambasador South JakartaHypermart Hypermarket 4,500 Cimanggis Square Depok

Colliers International Indonesia - Research

LIST OF NEW SOME TENANTS DURING 1Q 2012

RETAILERS LINE OF BUSINESS SIZE (SQ M) LOCATIONCoffee Bean Food and Beverage 200 Kuningan City South JakartaMing Chinese Food and Beverage 200 Kuningan City South JakartaOutback Steak House Food and Beverage 200 Kuningan City South JakartaStarbucks Food and Beverage 170 Kuningan City South JakartaTiramisu Food and Beverage 46 Slipi Jaya West JakartaKeizia Body Treatment 60 Slipi Jaya West JakartaSamsung Electronics 120 Gajah Mada Plaza Central JakartaMinimal Fashion Fashion 60 Gajah Mada Plaza Central JakartaAll Dress Up Fashion 200 Plaza Senayan Central JakartaDunhill Fashion 200 Plaza Senayan Central JakartaHermes Watch Jewellery, Watches and Accessories 200 Plaza Senayan Central JakartaSwatch Jewellery, Watches and Accessories 200 Plaza Senayan Central JakartaRoppan Food and Beverage 200 Plaza Semanggi South JakartaPayless Footwear 200 Pejaten Village South JakartaKingscobra Hobbies 60 Pejaten Village South JakartaGrand Duck King Food and Beverage 300 Cilandak Town Square South JakartaBMK Food and Beverage 200 Bintaro Plaza TangerangBMK Food and Beverage 200 Depok Mall DepokThe Executive Fashion 200 Supermal Karawaci TangerangEt Cetera Fashion 200 Supermal Karawaci Tangerang

Colliers International Indonesia - Research

COLLIERS INTERNATIONAL | P. 25

JAKARTA | 1Q 2012 | RETAIL

By contrast, there were also several termination cases during the reviewed quarter. The first case occurred in Pasaraya Grande, where they are now trying to deliver a new concept to accommodate and attract more visitors. This brings consequences for underperforming tenants who may pull out from their premises in order for the mall to become more competitive in the retail business. Similarly, this also happened to old shopping centres like Ratu Plaza, where the new owner demanded a better performance for the mall and introduced a fresher concept to entice new prospective tenants and to lure more visitors. Consequently, a number of tenants could leave their premises. The expansion of convenience stores has impacted those F&B retailers which leased food court area in a retail centre located around Pasar Baru. Such F&B retailers are seeing

fierce competition from convenience stores and decided to close down in order to save themselves from greater loss. This was not exclusive to local brands, as an international prominent burger restaurant has had to close their store in Pondok Indah Mall following their previous closure at Gandaria. Overall occupancy rates in greater Jakarta area rose modestly by 2% compared to the previous quarter, which registered at 86.3%. The strong performance of new retail centres such as Summarecon Mal Serpong 2, Tangerang City, Living World, Metropolitan Mall, Supermal Karawaci, Depok Mall, Teraskota and Margo City has helped contribute to the overall performance. Even the newly operating Cimanggis Square operates with two major tenants (of their own group) i.e. Hypermart and Matahari Department Store.

VACANCY OF RETAIL SPACE IN JAKARTA AND GREATER JAKARTA

Colliers International Indonesia - Research

0%

5%

10%

15%

20%

25%

30%

35%

40%

2005 2006 2007 2008 2009 2010 2011 1Q 2012

Central Jakarta South Jakarta North Jakarta

East Jakarta West Jakarta Greater Jakarta

Up to the first quarter of 2012, the pre-committed occupancy of future retail centres in Jakarta reached 80%, a reasonable increase of 3% compared to the previous quarter. Hypermart opens at Kemang Village, marking their soft launch in a mall located in the expatriate area of South Jakarta. Leaving around 10% of vacant space, Kemang Village is projected to begin operations in around 2Q or 3Q 2012.

In the greater Jakarta area, Mall Balekota witnessed significant commitment from various tenants. Planning to open this year, this retail centre located around Tangerang Government Center has secured about a 50% leasing commitment from major tenants such as Hypermart, Matahari Department Store, Gramedia, Ace Hardware, Toys Kingdom, Electronic Solution, Informa, Gold’s Gym and XXI, while some food and beverages retailers comprise Burger King, Dominos Pizza and Starbucks.

DEMAND FOR FUTURE RETAIL CENTRES

P. 26 | COLLIERS INTERNATIONAL

JAKARTA | 1Q 2012 | RETAIL

PRE-COMMITMENT LEVEL DURING 2011 - 2013

Colliers International Indonesia - Research

JAKARTA AREA BODETABEK AREA

0 100,000 200,000 300,000 400,000

2011

2012F

2013F

sq m

Space Absorbed Annual Supply

0 100,000 200,000 300,000 400,000

2011

2012F

2013F

sq m

Space Absorbed Annual Supply

LIST OF NEW COMMITTED TENANTS IN THE OPERATING SHOPPING CENTRES

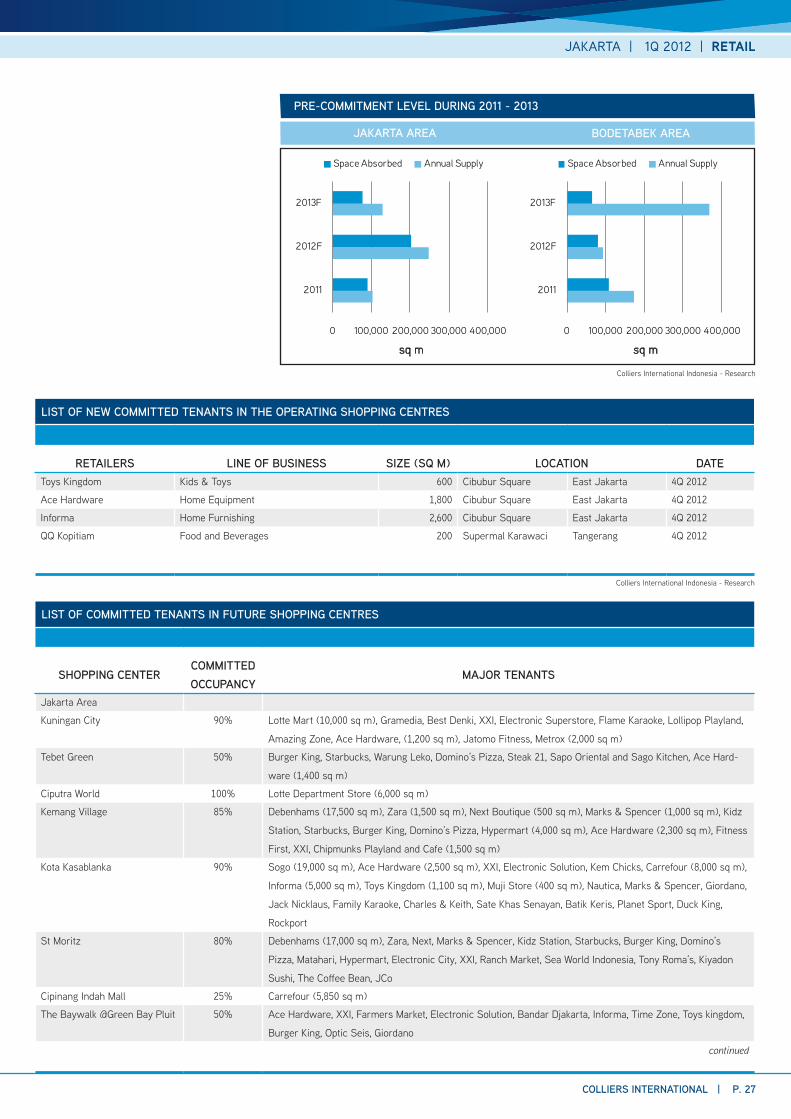

RETAILERS LINE OF BUSINESS SIZE (SQ M) LOCATION DATEToys Kingdom Kids & Toys 600 Cibubur Square East Jakarta 4Q 2012

Ace Hardware Home Equipment 1,800 Cibubur Square East Jakarta 4Q 2012

Informa Home Furnishing 2,600 Cibubur Square East Jakarta 4Q 2012

QQ Kopitiam Food and Beverages 200 Supermal Karawaci Tangerang 4Q 2012

LIST OF COMMITTED TENANTS IN FUTURE SHOPPING CENTRES

SHOPPING CENTERCOMMITTED OCCUPANCY

MAJOR TENANTS

Jakarta Area

Kuningan City 90% Lotte Mart (10,000 sq m), Gramedia, Best Denki, XXI, Electronic Superstore, Flame Karaoke, Lollipop Playland,

Amazing Zone, Ace Hardware, (1,200 sq m), Jatomo Fitness, Metrox (2,000 sq m)

Tebet Green 50% Burger King, Starbucks, Warung Leko, Domino’s Pizza, Steak 21, Sapo Oriental and Sago Kitchen, Ace Hard-

ware (1,400 sq m)

Ciputra World 100% Lotte Department Store (6,000 sq m)

Kemang Village 85% Debenhams (17,500 sq m), Zara (1,500 sq m), Next Boutique (500 sq m), Marks & Spencer (1,000 sq m), Kidz

Station, Starbucks, Burger King, Domino’s Pizza, Hypermart (4,000 sq m), Ace Hardware (2,300 sq m), Fitness

First, XXI, Chipmunks Playland and Cafe (1,500 sq m)

Kota Kasablanka 90% Sogo (19,000 sq m), Ace Hardware (2,500 sq m), XXI, Electronic Solution, Kem Chicks, Carrefour (8,000 sq m),

Informa (5,000 sq m), Toys Kingdom (1,100 sq m), Muji Store (400 sq m), Nautica, Marks & Spencer, Giordano,

Jack Nicklaus, Family Karaoke, Charles & Keith, Sate Khas Senayan, Batik Keris, Planet Sport, Duck King,

Rockport

St Moritz 80% Debenhams (17,000 sq m), Zara, Next, Marks & Spencer, Kidz Station, Starbucks, Burger King, Domino’s

Pizza, Matahari, Hypermart, Electronic City, XXI, Ranch Market, Sea World Indonesia, Tony Roma’s, Kiyadon

Sushi, The Coffee Bean, JCo

Cipinang Indah Mall 25% Carrefour (5,850 sq m)

The Baywalk @Green Bay Pluit 50% Ace Hardware, XXI, Farmers Market, Electronic Solution, Bandar Djakarta, Informa, Time Zone, Toys kingdom,

Burger King, Optic Seis, Giordano

continued

Colliers International Indonesia - Research

COLLIERS INTERNATIONAL | P. 27

JAKARTA | 1Q 2012 | RETAIL

continuation

Greater Jakarta Area

Living World Alam Sutera 85% Han Gang Korean Food, Sushimise, Steak 21, Canton Boy, Sate Khas Senayan, Ajisen Ramen, Kopitiam,

Informa (30,000 sq m), Ace Hardware (15,000 sq m), Toys Kingdom, XXI, Gramedia, (1,200 sq m), Kampoeng

Nelayan, Breadtalk, Hero

Summarecon Mall Serpong 2 95% Eat and Eat (1,500 sq m), Centro Department Store (10,000 sq m), Best Denki, Do It Best Pongs Home Center

(3,000 sq m), Takigawa, Dante, Secret Recipe

Shopping Mall @Alam Sutera 90% Sogo Department Store (10,000 sq m), The Food Hall (3,000 sq m), Funworld, Mango Farm, Gramedia (1,200

sq m), XXI, Chipmunks Playland & Cafe (2,100 sq m), Electronic Solution, Home Solution, Giant (5,000 sq m),

Guardian

Grand Metropolitan 70% Centro, Farmers Market, Toys Kingdom, Funworld Sate Khas Senayan, Optik Melawai

CitraGran Mall 75% Matahari (10,000 sq m), Hypermart (6,000 sq m), Gramedia (1,200 sq m), Starbucks, Bengawan Solo

Mall Balekota 75% Hypermart (7,300 sq m), Electronic Solution (4,500 sq m), Ace Hardware (1,000 sq m), Gramedia, Informa,

XXI, Matahari (7,000 sq m), Toys Kingdom (2,000 sq m), Amazone (900 sq m)

Colliers International Indonesia - Research

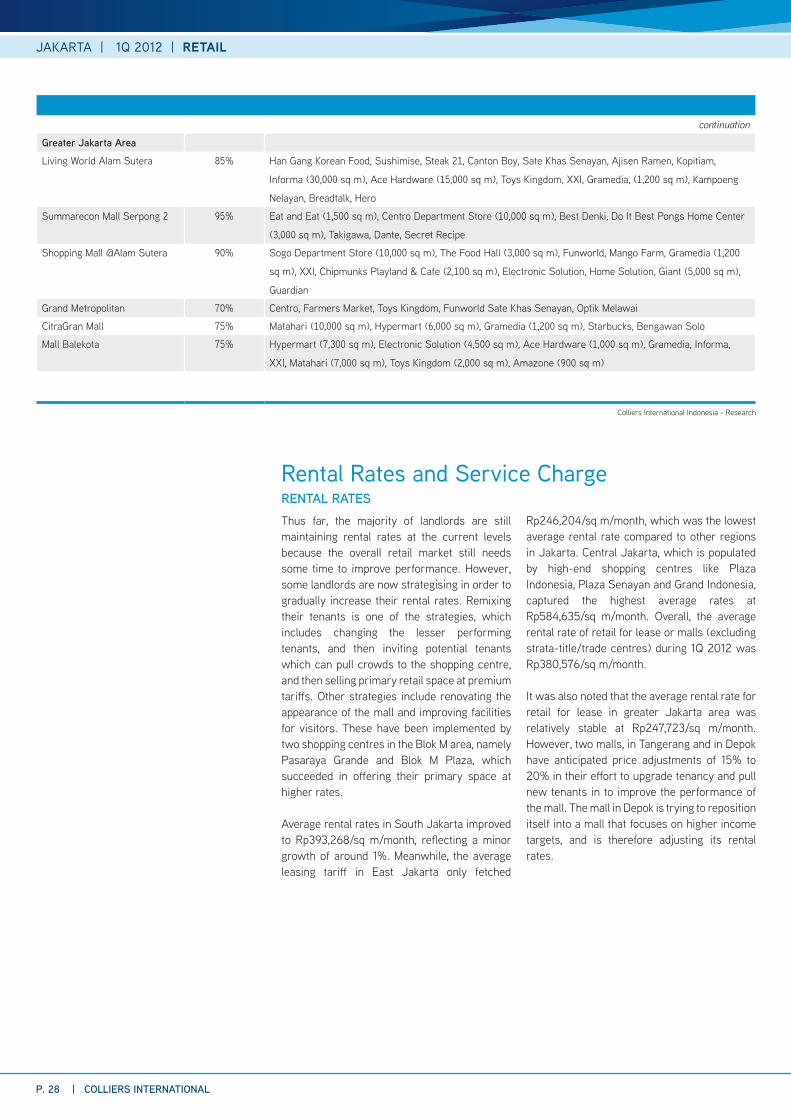

Rental Rates and Service Charge RENTAL RATESThus far, the majority of landlords are still maintaining rental rates at the current levels because the overall retail market still needs some time to improve performance. However, some landlords are now strategising in order to gradually increase their rental rates. Remixing their tenants is one of the strategies, which includes changing the lesser performing tenants, and then inviting potential tenants which can pull crowds to the shopping centre, and then selling primary retail space at premium tariffs. Other strategies include renovating the appearance of the mall and improving facilities for visitors. These have been implemented by two shopping centres in the Blok M area, namely Pasaraya Grande and Blok M Plaza, which succeeded in offering their primary space at higher rates.

Average rental rates in South Jakarta improved to Rp393,268/sq m/month, reflecting a minor growth of around 1%. Meanwhile, the average leasing tariff in East Jakarta only fetched

Rp246,204/sq m/month, which was the lowest average rental rate compared to other regions in Jakarta. Central Jakarta, which is populated by high-end shopping centres like Plaza Indonesia, Plaza Senayan and Grand Indonesia, captured the highest average rates at Rp584,635/sq m/month. Overall, the average rental rate of retail for lease or malls (excluding strata-title/trade centres) during 1Q 2012 was Rp380,576/sq m/month.

It was also noted that the average rental rate for retail for lease in greater Jakarta area was relatively stable at Rp247,723/sq m/month. However, two malls, in Tangerang and in Depok have anticipated price adjustments of 15% to 20% in their effort to upgrade tenancy and pull new tenants in to improve the performance of the mall. The mall in Depok is trying to reposition itself into a mall that focuses on higher income targets, and is therefore adjusting its rental rates.

P. 28 | COLLIERS INTERNATIONAL

JAKARTA | 1Q 2012 | RETAIL

AVERAGE ASKING RENTAL RATES OF DIFFERENT CLASS SHOPPING CENTRES IN JAKARTA AND GREATER JAKARTA

Colliers International Indonesia - Research

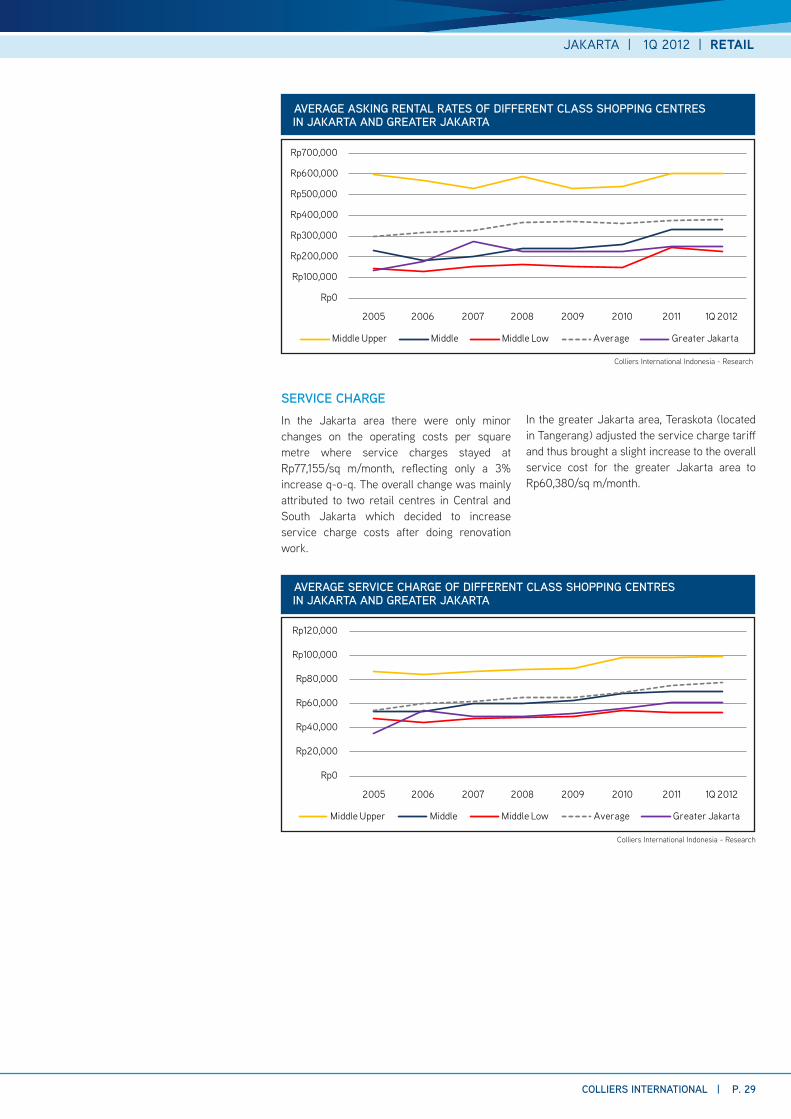

SERVICE CHARGEIn the Jakarta area there were only minor changes on the operating costs per square metre where service charges stayed at Rp77,155/sq m/month, reflecting only a 3% increase q-o-q. The overall change was mainly attributed to two retail centres in Central and South Jakarta which decided to increase service charge costs after doing renovation work.

In the greater Jakarta area, Teraskota (located in Tangerang) adjusted the service charge tariff and thus brought a slight increase to the overall service cost for the greater Jakarta area to Rp60,380/sq m/month.

Rp0

Rp100,000

Rp200,000

Rp300,000

Rp400,000

Rp500,000

Rp600,000

Rp700,000

2005 2006 2007 2008 2009 2010 2011 1Q 2012

Middle Upper Middle Middle Low Average Greater Jakarta

AVERAGE SERVICE CHARGE OF DIFFERENT CLASS SHOPPING CENTRES IN JAKARTA AND GREATER JAKARTA

Colliers International Indonesia - Research

Rp0

Rp20,000

Rp40,000

Rp60,000

Rp80,000

Rp100,000

Rp120,000

2005 2006 2007 2008 2009 2010 2011 1Q 2012

Middle Upper Middle Middle Low Average Greater Jakarta

COLLIERS INTERNATIONAL | P. 29

JAKARTA | 1Q 2012 | RETAIL

2012 will be a brisk period for retail business, highlighted by retailers’ business expansion and landlords’ efforts to deliver under-construction projects on time due to pre-commitment agreements with tenants. In fact, several macro indicators suggest that the economy has a positive outlook. Further, domestic consumption and lifestyle shifts will be increasing, and these will be the key drivers for retail business growth. On the retailers’ side, several lines of business have reported enjoying surging profits from growing consumption. For example, Hero is a robust prospect as it acquired franchising licenses from Swedish home furnishing stores brand IKEA which will start in 2014. The attempt to bring in this well-known brand is aimed at growing middle and upper-middle customers which have been pampered by home furnishing retailers like Ace Hardware. Likewise, a subsidiary of South Korean retailer Lotte Group, Lotteria Co Ltd, will open more Lotteria

fast food franchises in addition to their three retail outlets. This retailer will serve meals featuring organic food and expects to become one of the top three fast food restaurants in Indonesia by 2020. For some time now, branded products have benefitted from the improving standard of living of the middle class. Such a phenomenon continues to encourage more foreign retailers to expand their operations to Indonesia, as they endeavour to capitalise on the growth momentum. Thus, both retailers and consumers will propel the country’s retail markets. More business expansion by operating retailers, combined with the expanding business of overseas retailers will lead to lower levels of vacant retail space, and accordingly occupancy costs will head upwards. Given the solid performance of the retail business, vacancy levels are projected to fall further to less than 10% over the next two years in Jakarta.

Outlook

P. 30 | COLLIERS INTERNATIONAL

JAKARTA | 1Q 2012 | RETAIL

Supply Over the last two years, the major challenge facing the industrial market has been sourcing industrial land ready for development. Over the same time period, the fear of limited industrial land stock has been identified, as several industrial estates failed to anticipate a vibrant industrial market in which absorption rates exceeded the rate at which new industrial land was introduced. For some industrial estates, it can be quite frustrating to lose transaction opportunities due to limited stock of industrial land.

This quarter, the industrial market failed again to see the development of any new industrial land. All of the expansion activities currently underway require a few more months before they will be ready to operate. For example, Bekasi Fajar is developing a total of 300 hectares, but they require around one year to clear the land and build infrastructure before the site is ready for operation. Meanwhile, within the same area, MM2100 cannot sell the remaining land. In fact, the company needs to acquire more land to substitute for the green area. Another industrial estate in Bekasi is still actively selling despite its limited land stock. In

certain cases, buyers are willing to pay in advance before the land is ready in order to take advantage of the current price. The condition of limited supply also occurred in Karawang, where two industrial estates are now running out of stock to sell. One industrial estate in Karawang reported that the main obstacle to its own expansion is the contour of the land, which requires major work and investment. In our view, limited new industrial land stock will be completed in 2012. In short, the general problem facing most industrial estates is delivery time, as they are now rushing to counterbalance the increasing demand for land.

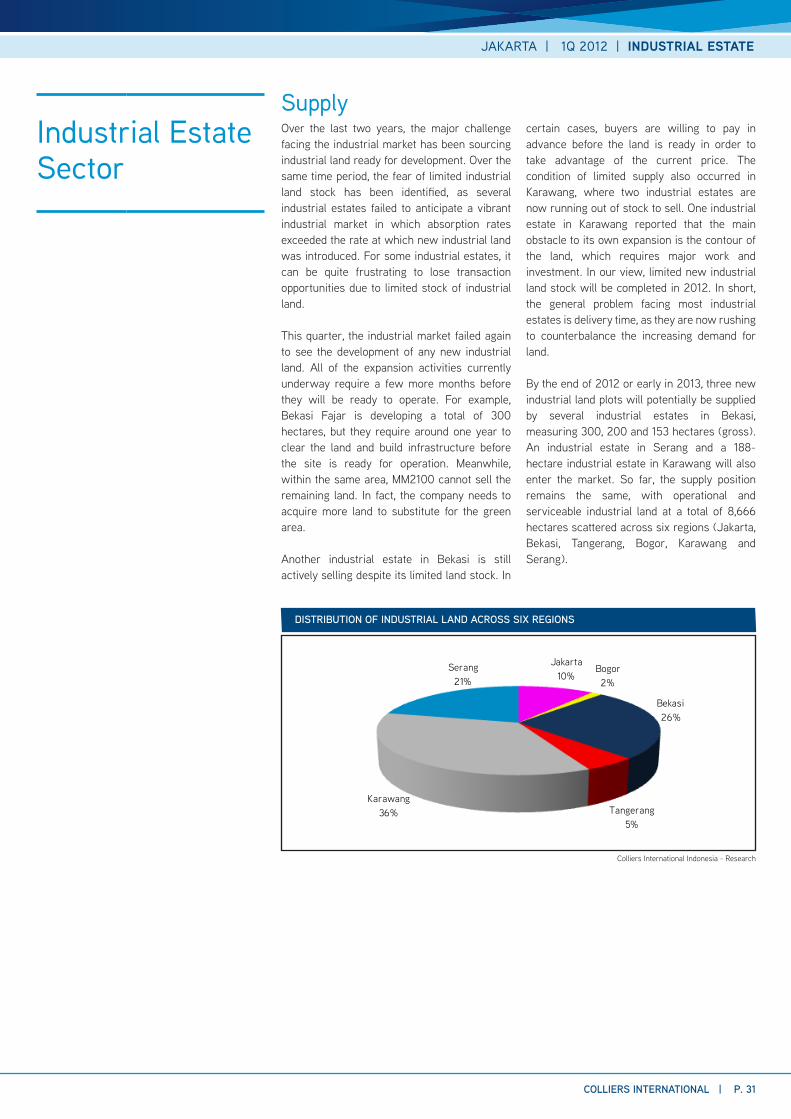

By the end of 2012 or early in 2013, three new industrial land plots will potentially be supplied by several industrial estates in Bekasi, measuring 300, 200 and 153 hectares (gross). An industrial estate in Serang and a 188-hectare industrial estate in Karawang will also enter the market. So far, the supply position remains the same, with operational and serviceable industrial land at a total of 8,666 hectares scattered across six regions (Jakarta, Bekasi, Tangerang, Bogor, Karawang and Serang).

Industrial Estate Sector

DISTRIBUTION OF INDUSTRIAL LAND ACROSS SIX REGIONS

Colliers International Indonesia - Research

Jakarta10%

Bogor2%

Bekasi26%

Tangerang5%

Karawang36%

Serang21%

COLLIERS INTERNATIONAL | P. 31

JAKARTA | 1Q 2012 | INDUSTRIAL ESTATE

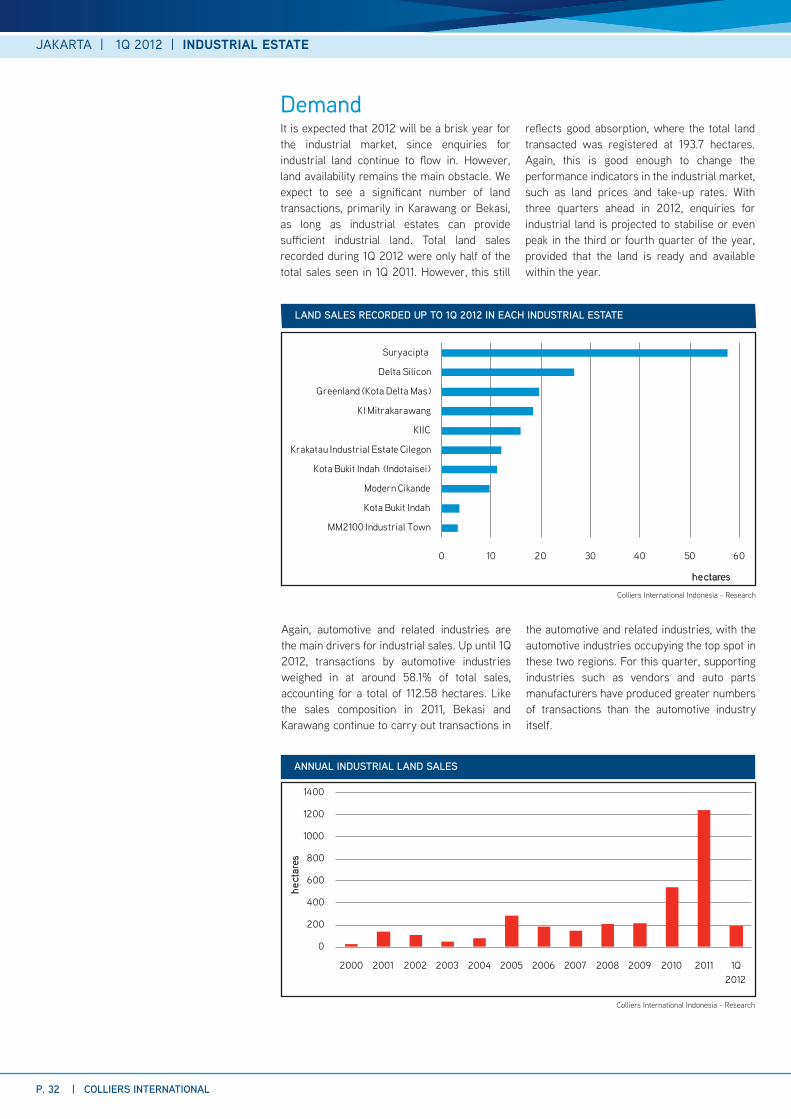

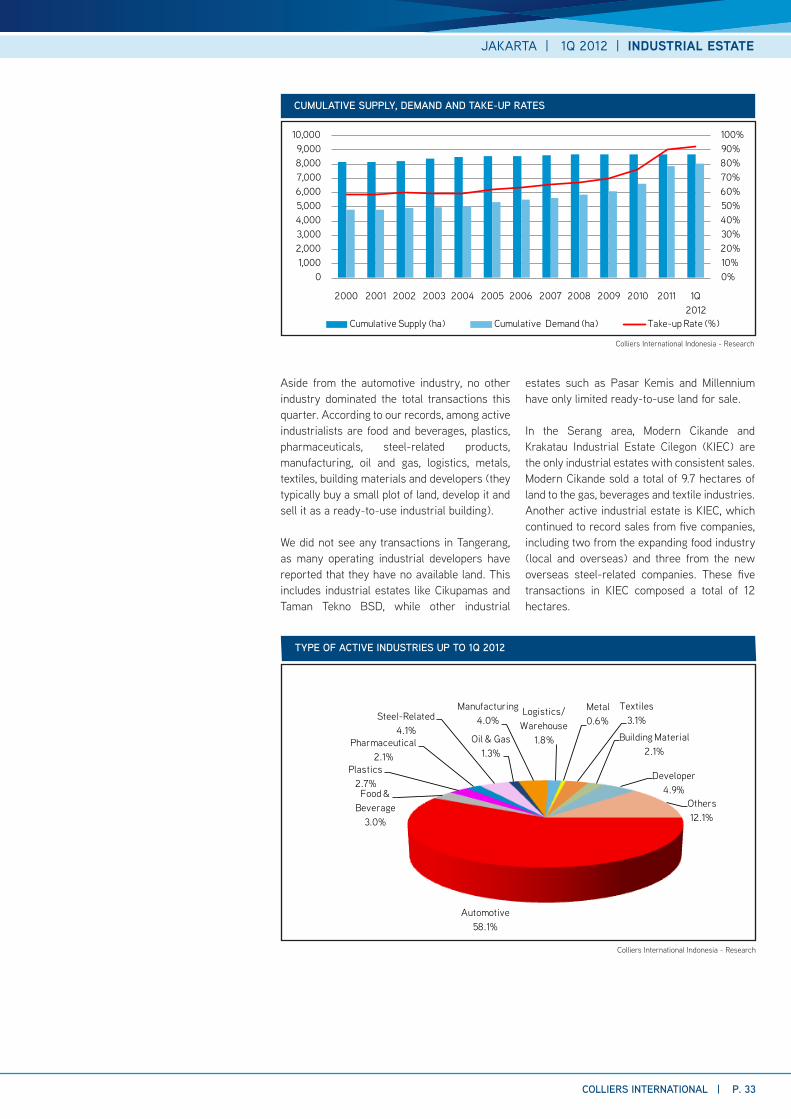

It is expected that 2012 will be a brisk year for the industrial market, since enquiries for industrial land continue to flow in. However, land availability remains the main obstacle. We expect to see a significant number of land transactions, primarily in Karawang or Bekasi, as long as industrial estates can provide sufficient industrial land. Total land sales recorded during 1Q 2012 were only half of the total sales seen in 1Q 2011. However, this still

reflects good absorption, where the total land transacted was registered at 193.7 hectares. Again, this is good enough to change the performance indicators in the industrial market, such as land prices and take-up rates. With three quarters ahead in 2012, enquiries for industrial land is projected to stabilise or even peak in the third or fourth quarter of the year, provided that the land is ready and available within the year.

Demand

Colliers International Indonesia - Research

LAND SALES RECORDED UP TO 1Q 2012 IN EACH INDUSTRIAL ESTATE

0 10 20 30 40 50 60

MM2100 Industrial Town

Kota Bukit Indah

Modern Cikande

Kota Bukit Indah (Indotaisei)

Krakatau Industrial Estate Cilegon

KIIC

KI Mitrakarawang

Greenland (Kota Delta Mas)

Delta Silicon

Suryacipta

hectares

Again, automotive and related industries are the main drivers for industrial sales. Up until 1Q 2012, transactions by automotive industries weighed in at around 58.1% of total sales, accounting for a total of 112.58 hectares. Like the sales composition in 2011, Bekasi and Karawang continue to carry out transactions in