Embed Size (px)

Citation preview

© 2016 Fox Rothschild

IVC 3rd Annual High-Tech Seminar: Expanding Your Business into the US MarketLoren D. Danzis, Esq. February 9, 2016

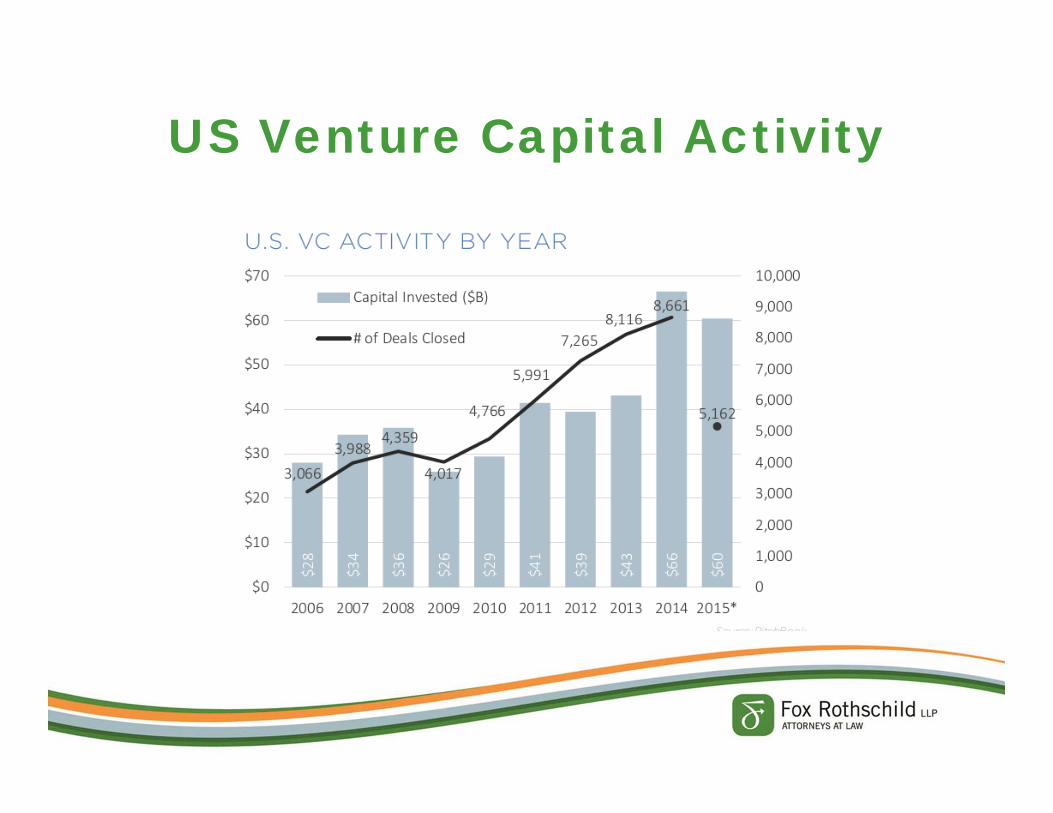

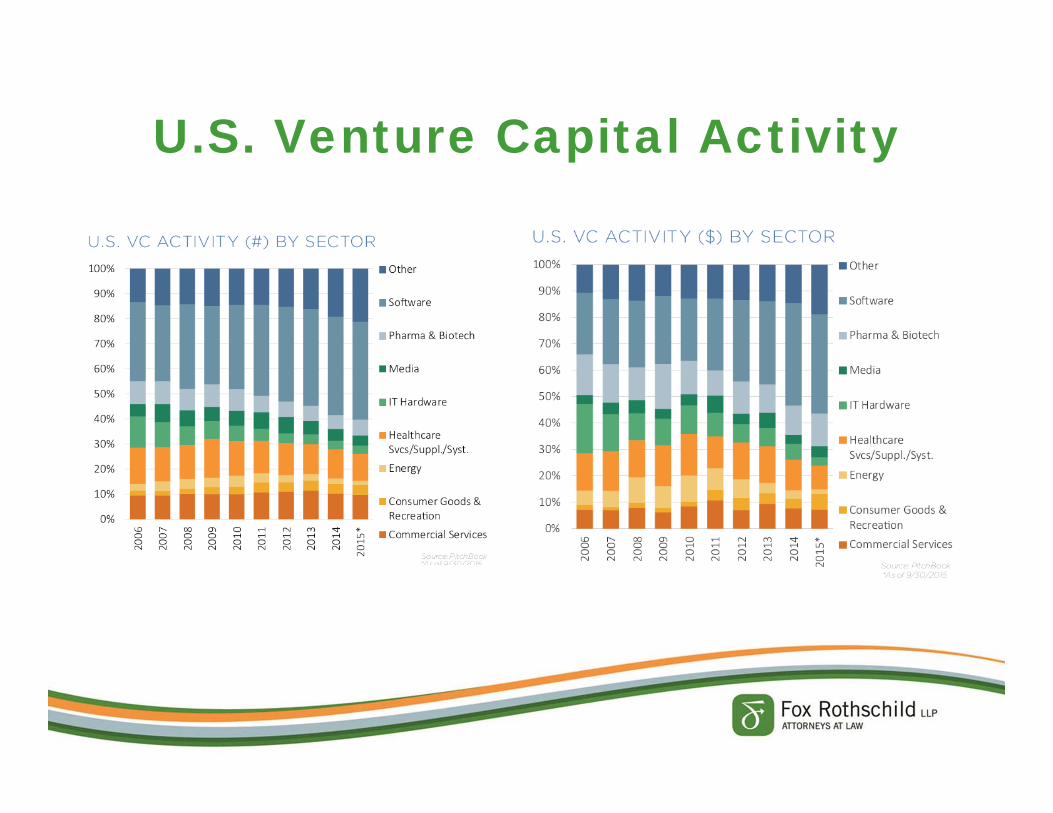

US Venture Capital Activity

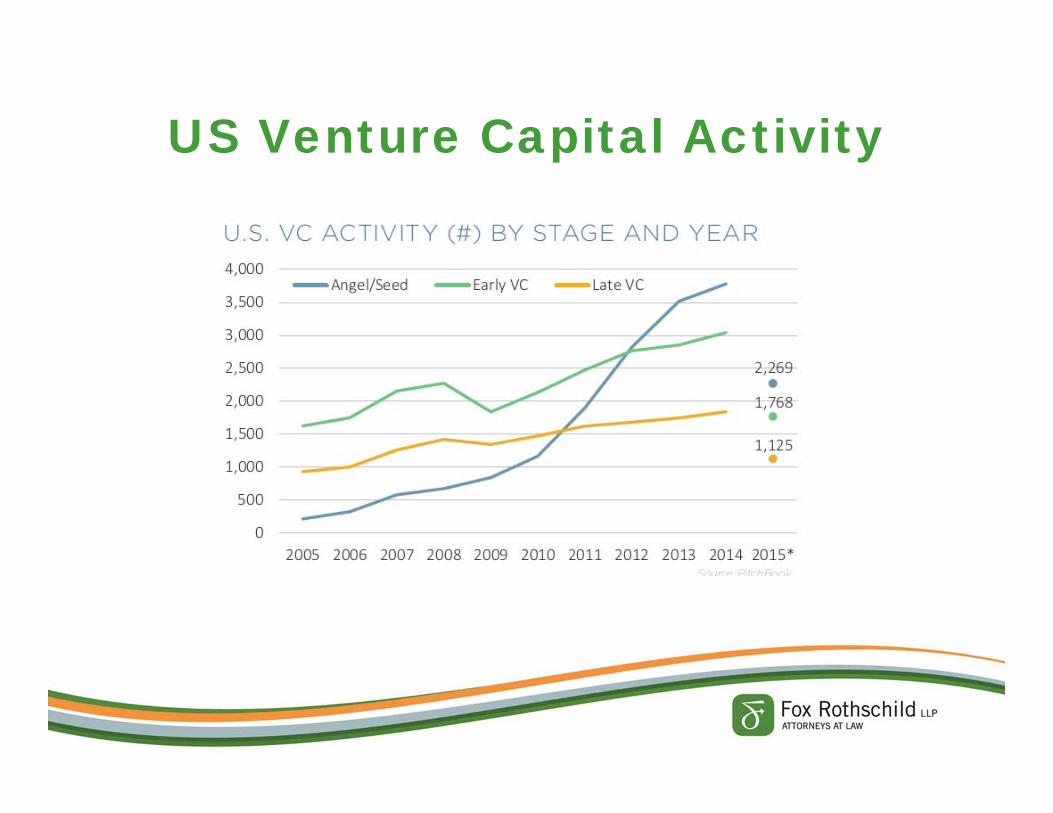

US Venture Capital Activity

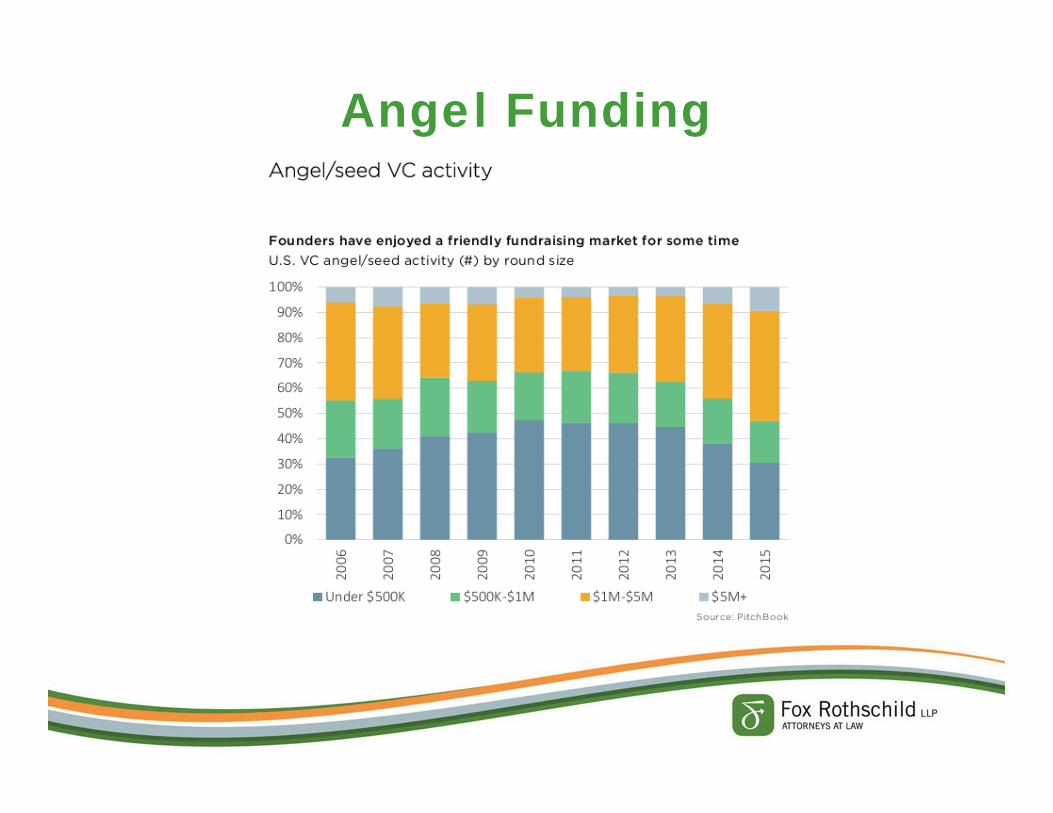

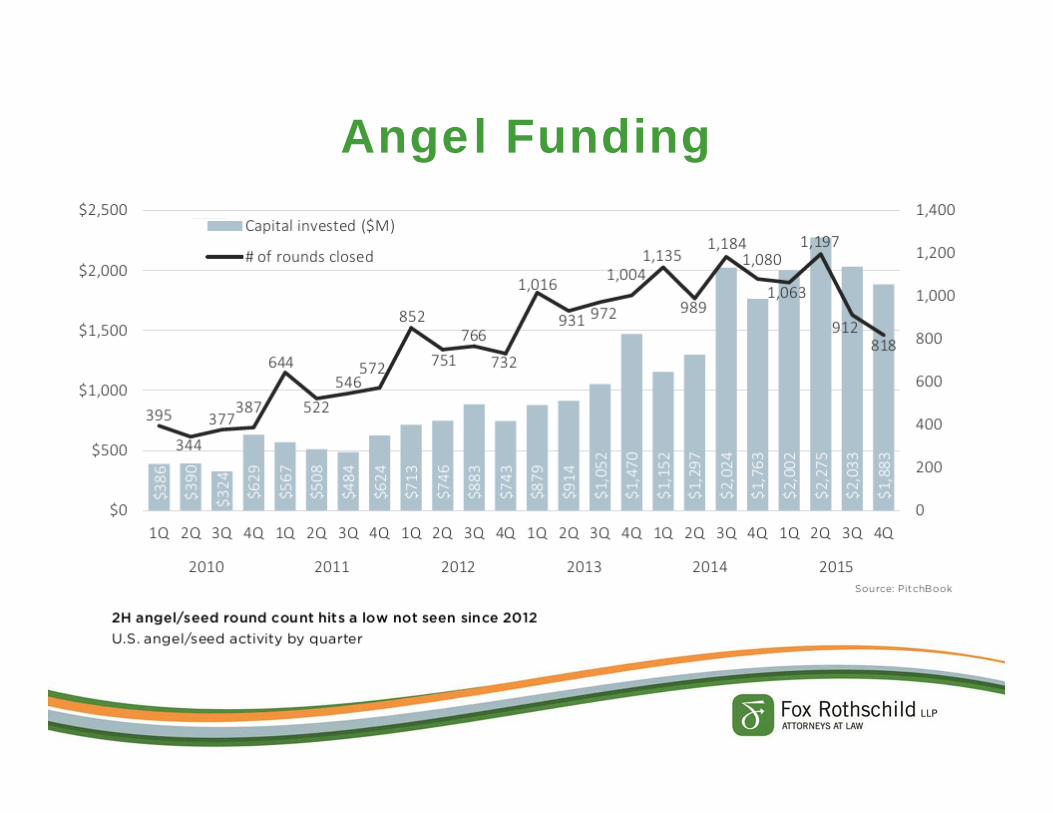

Angel Funding

Angel Funding

U.S. Venture Capital Activity

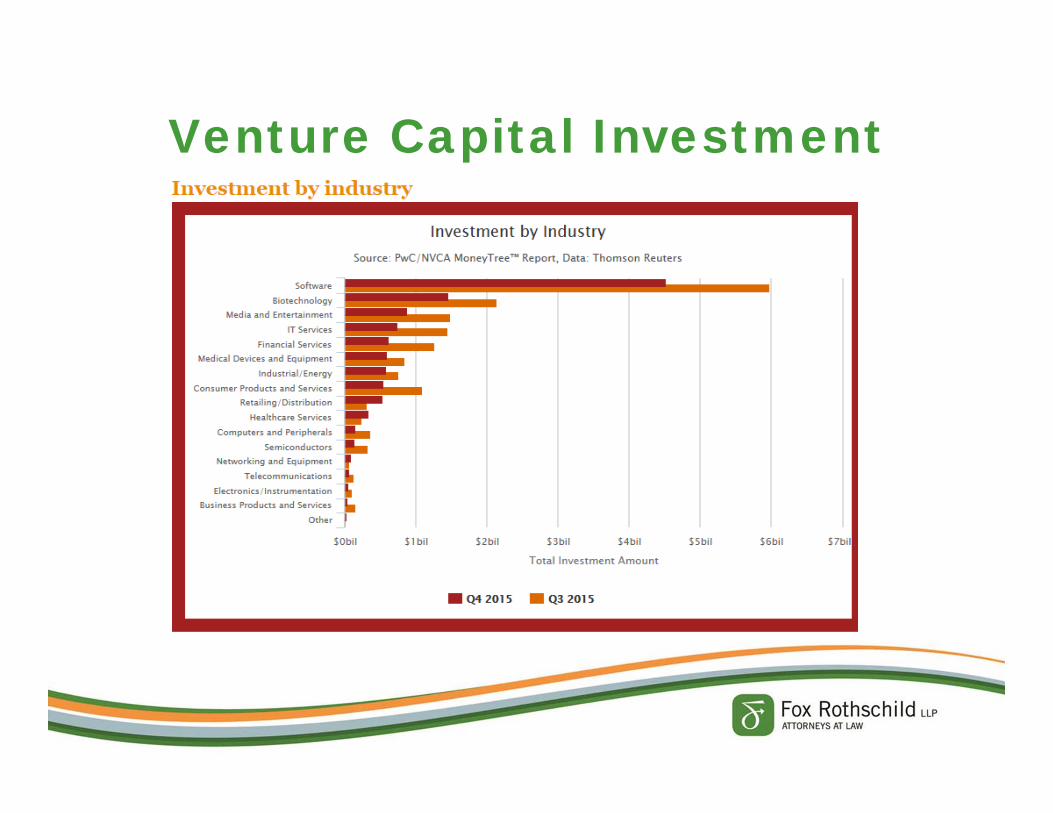

Venture Capital Investment

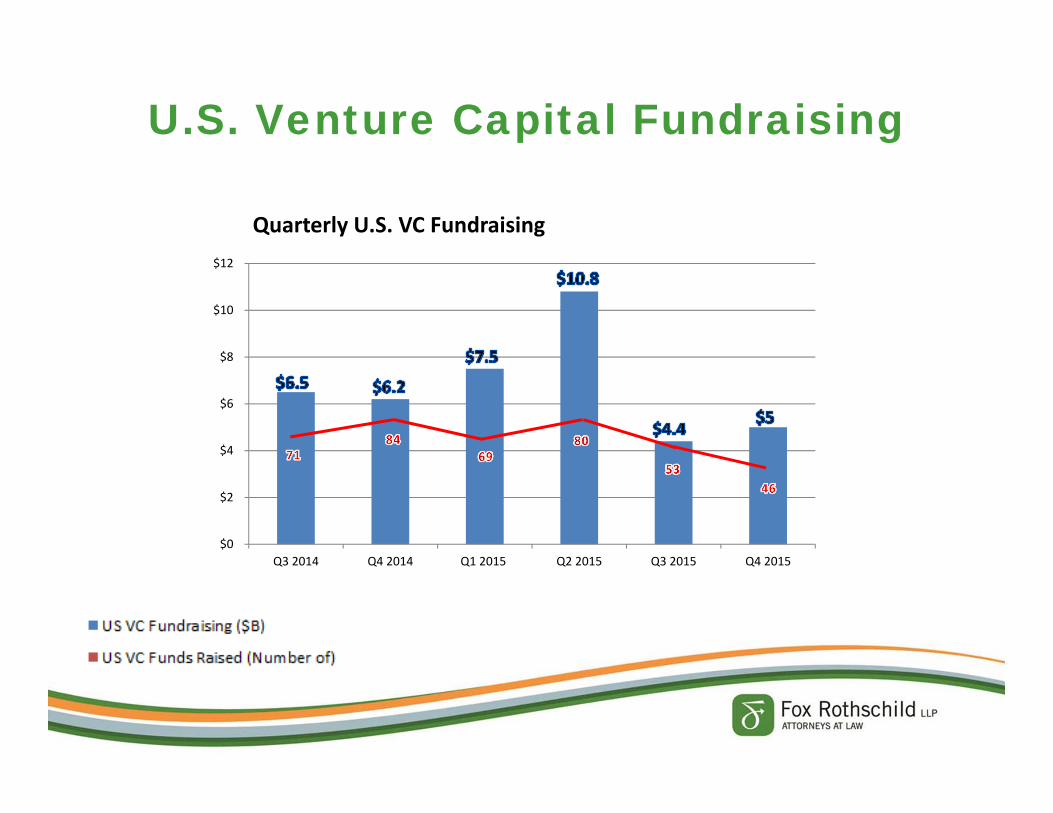

U.S. Venture Capital Fundraising

$0

$2

$4

$6

$8

$10

$12

Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015 Q4 2015

Quarterly U.S. VC Fundraising

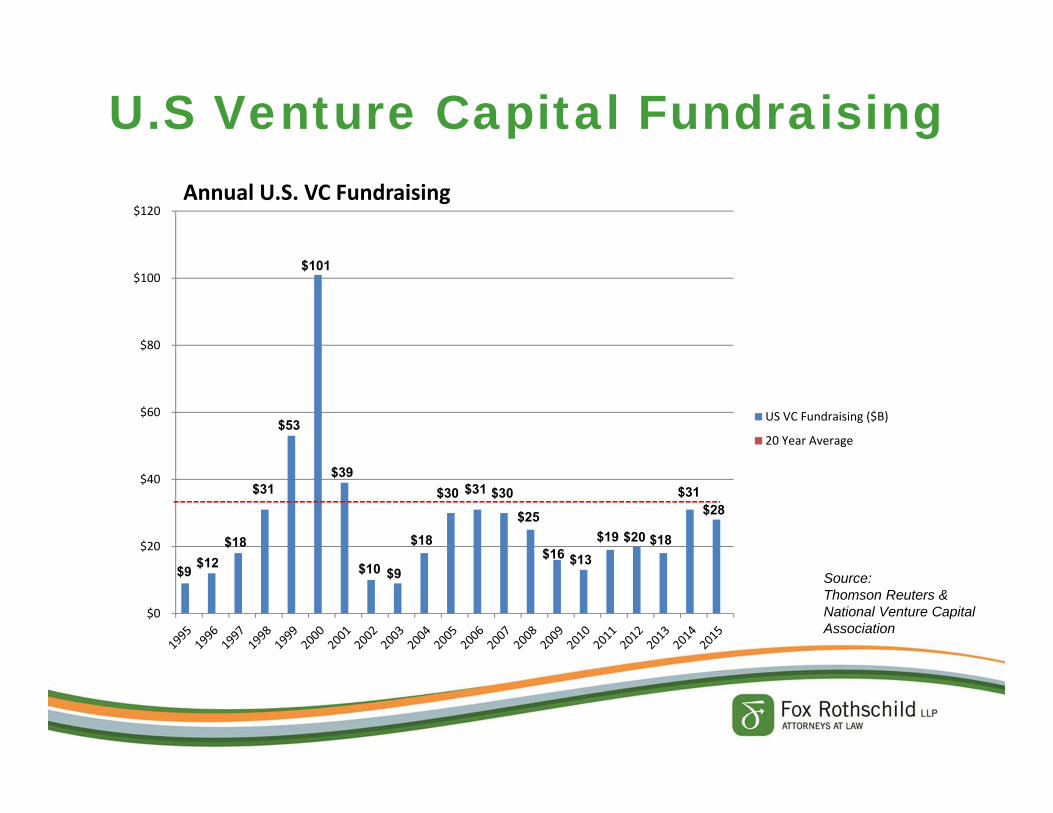

U.S Venture Capital Fundraising

$0

$20

$40

$60

$80

$100

$120

US VC Fundraising ($B)

20 Year Average

Annual U.S. VC Fundraising

$9 $12$18

$31

$53

$101

$39

$10 $9

$18

$30 $31 $30

$25

$16 $13$19 $20 $18

$31$28

Source: Thomson Reuters & National Venture Capital Association

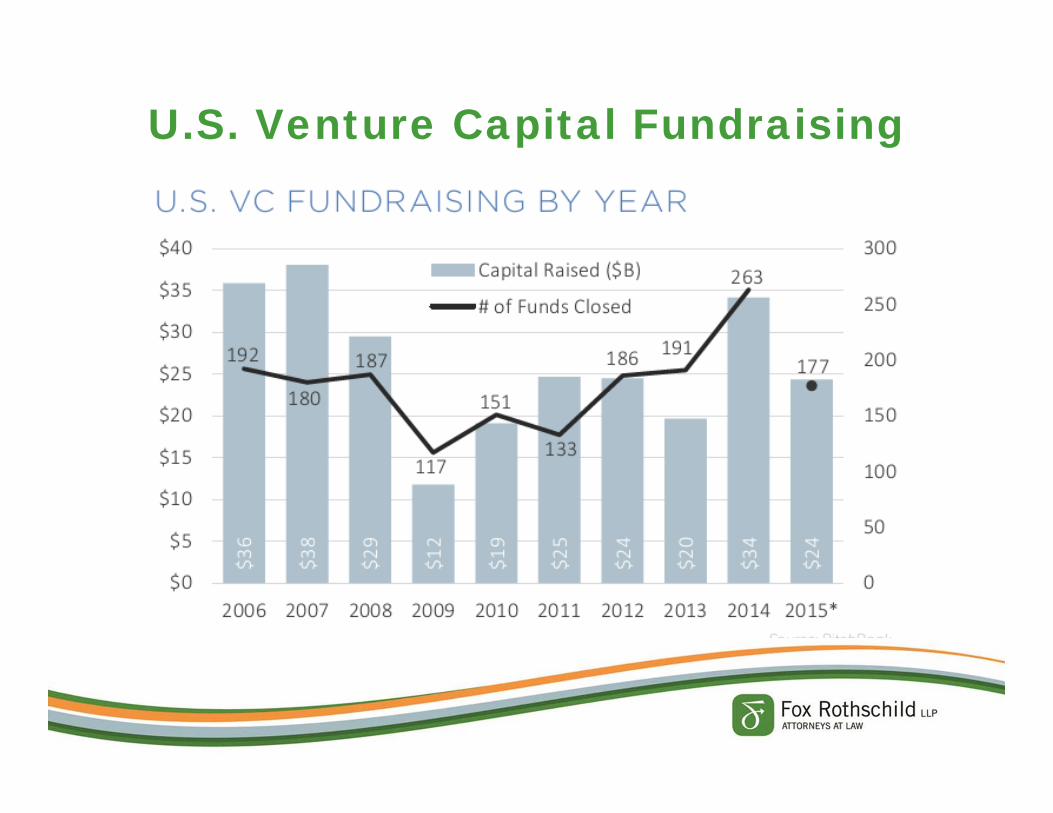

U.S. Venture Capital Fundraising

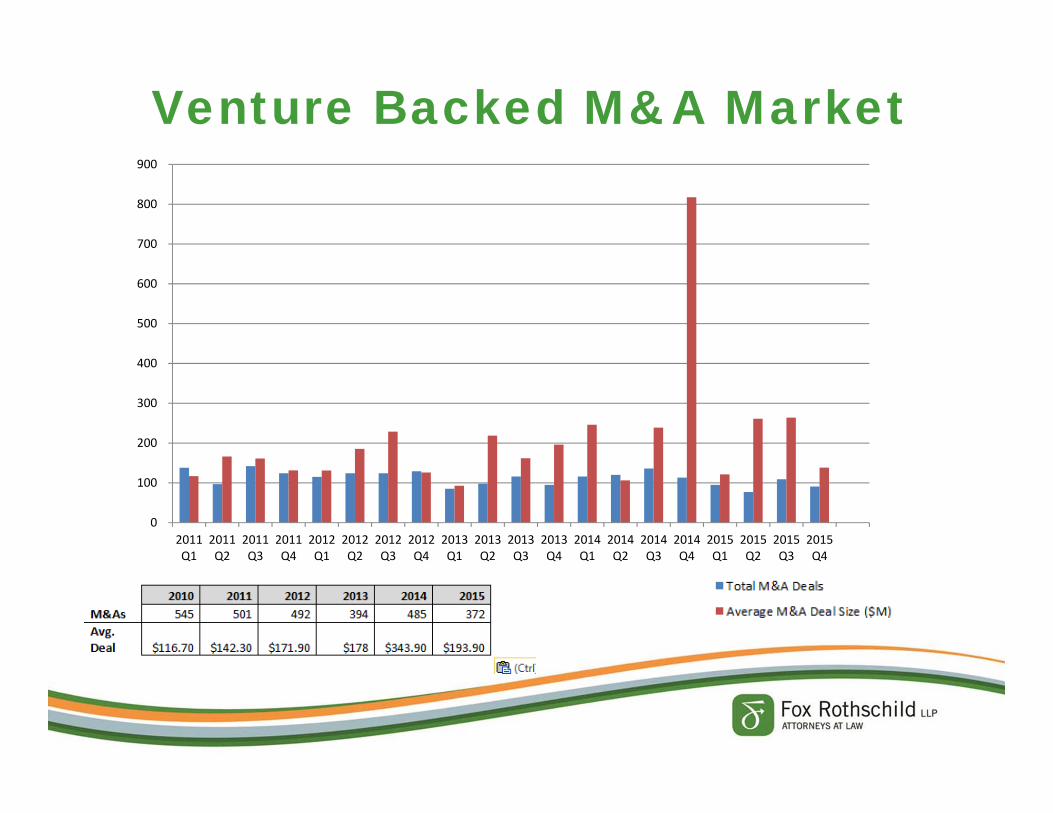

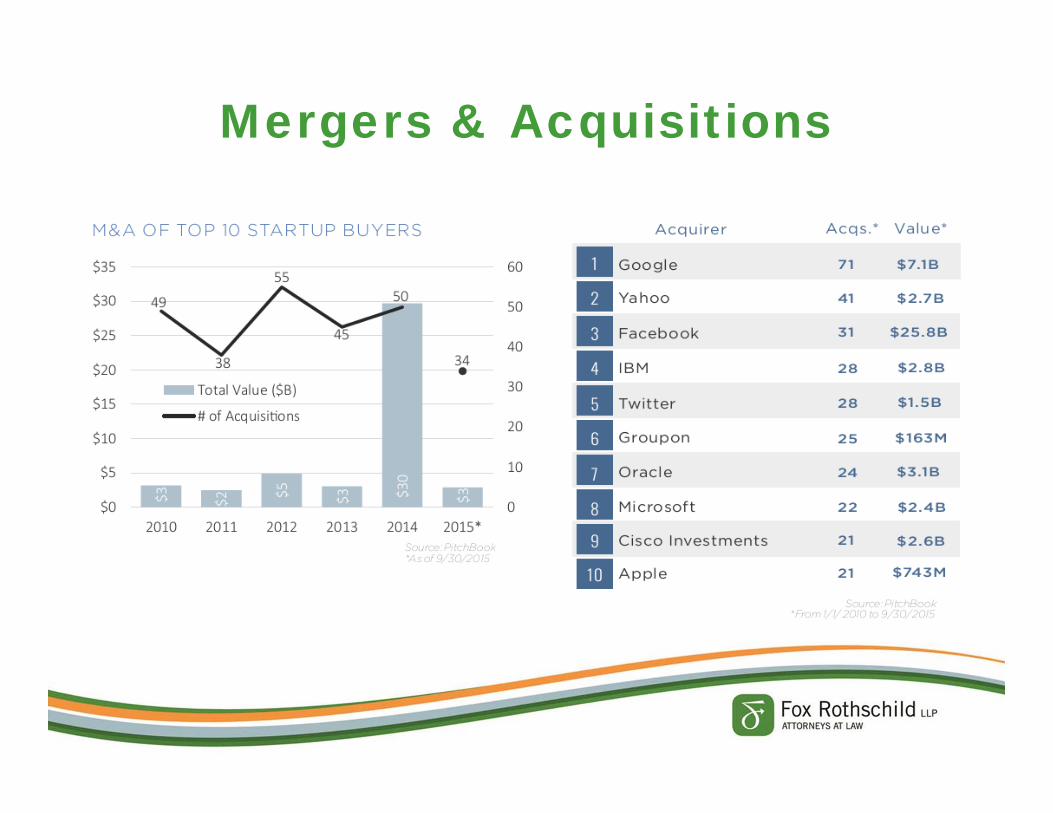

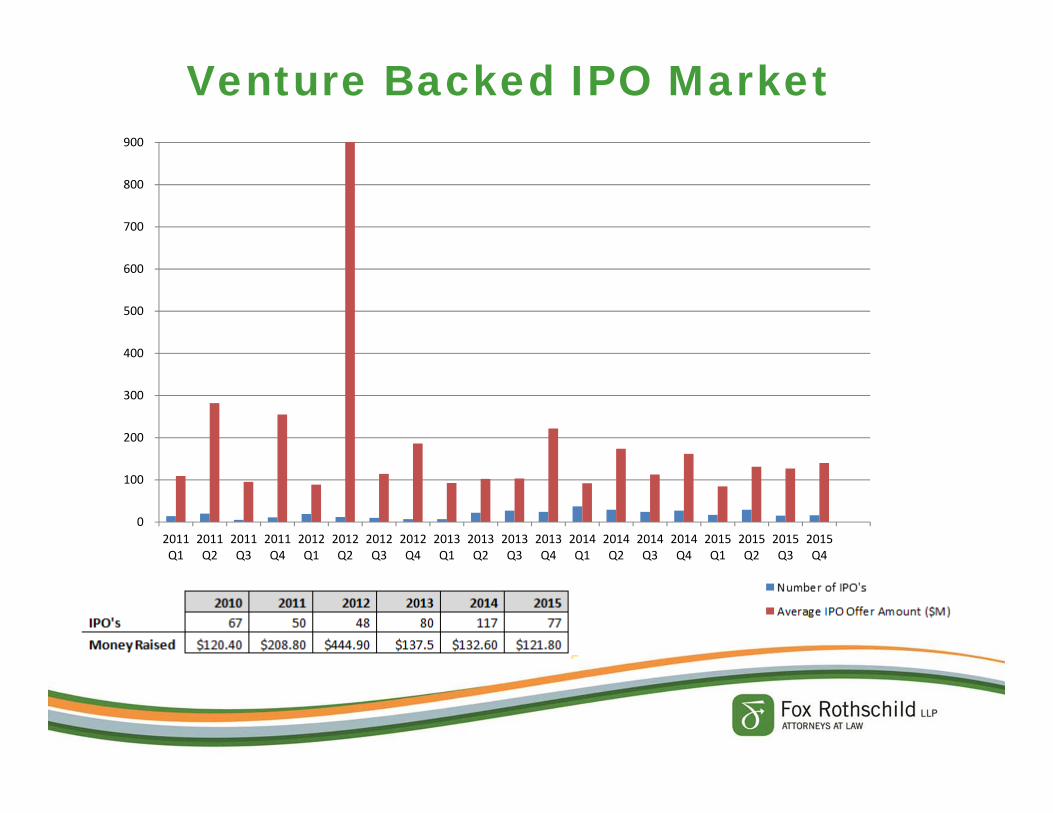

Venture Backed M&A Market

0

100

200

300

400

500

600

700

800

900

2011Q1

2011Q2

2011Q3

2011Q4

2012Q1

2012Q2

2012Q3

2012Q4

2013Q1

2013Q2

2013Q3

2013Q4

2014Q1

2014Q2

2014Q3

2014Q4

2015Q1

2015Q2

2015Q3

2015Q4

Mergers & Acquisitions

Venture Backed IPO Market

0

100

200

300

400

500

600

700

800

900

2011Q1

2011Q2

2011Q3

2011Q4

2012Q1

2012Q2

2012Q3

2012Q4

2013Q1

2013Q2

2013Q3

2013Q4

2014Q1

2014Q2

2014Q3

2014Q4

2015Q1

2015Q2

2015Q3

2015Q4

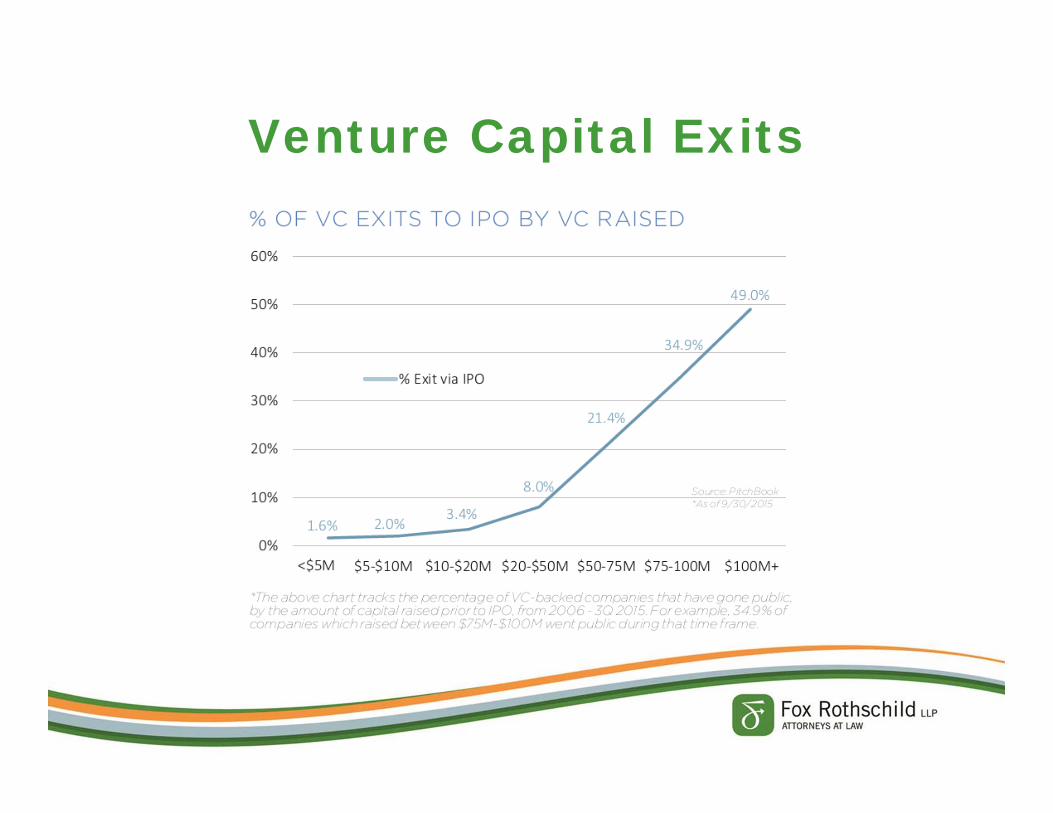

Venture Capital Exits

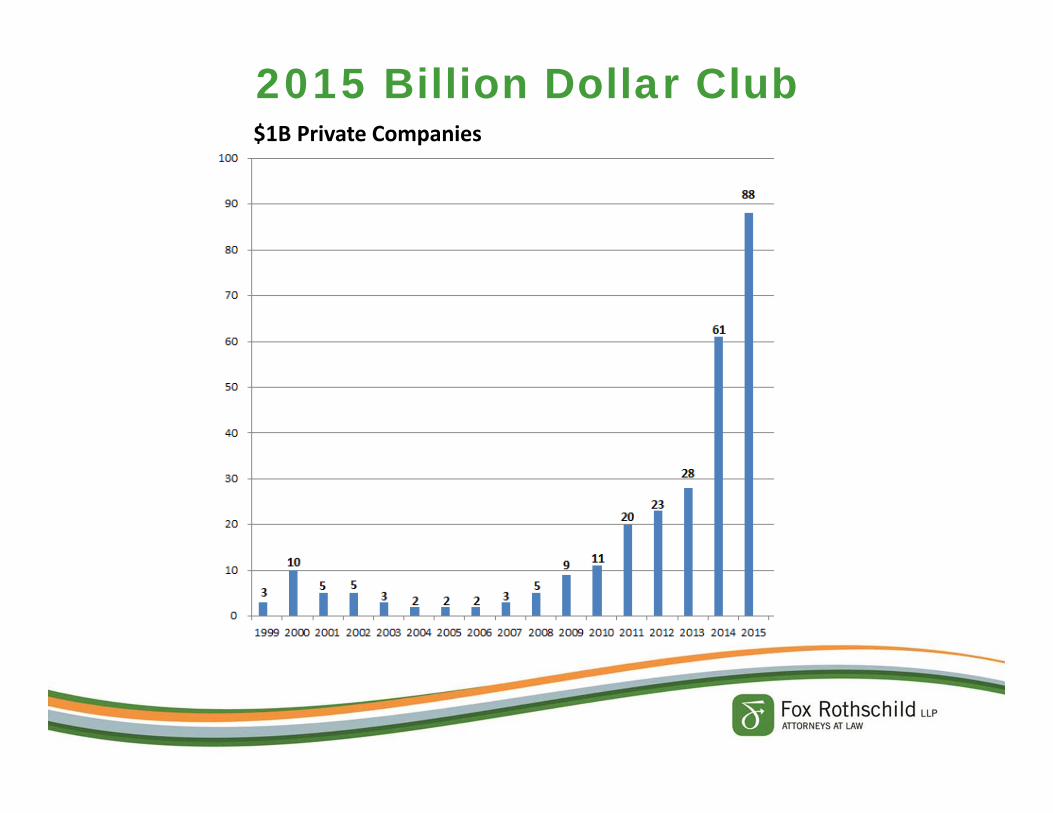

2015 Billion Dollar Club

10

5 53 2 2 2 3

59 11

2023

28

61

88

$1B Private Companies

Selection Bias in VC

Source: Greenspring Associates Fall Investor Meeting

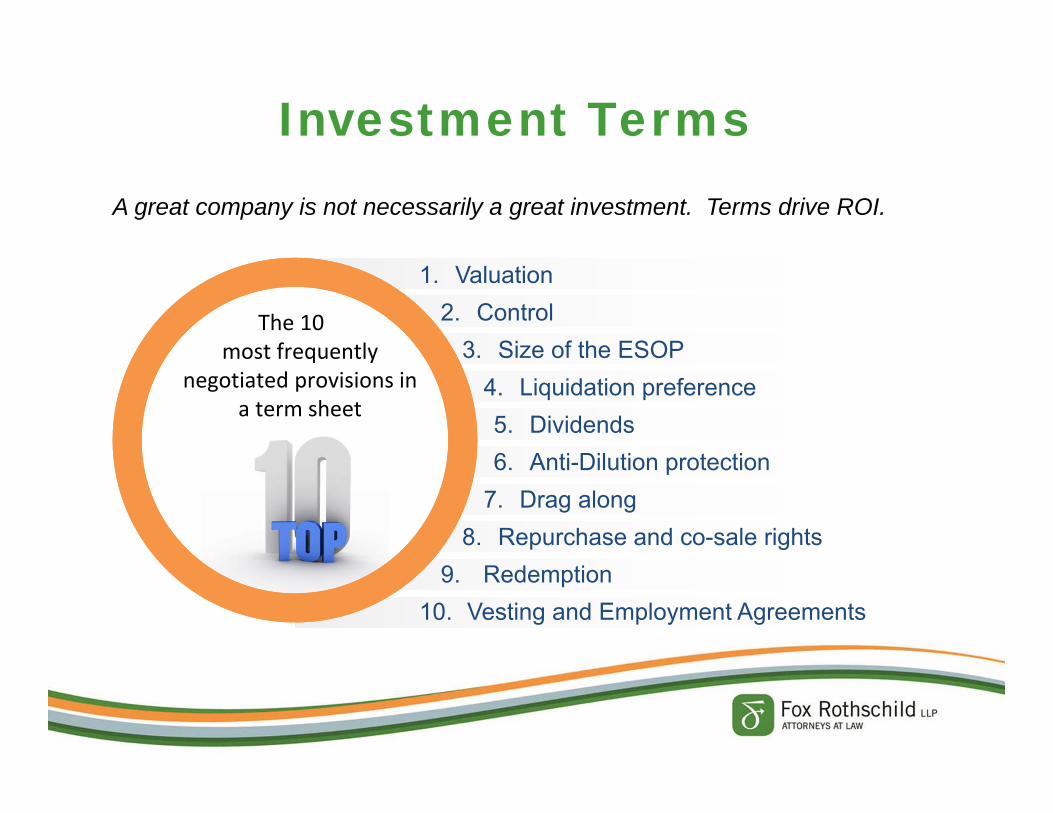

Investment Terms

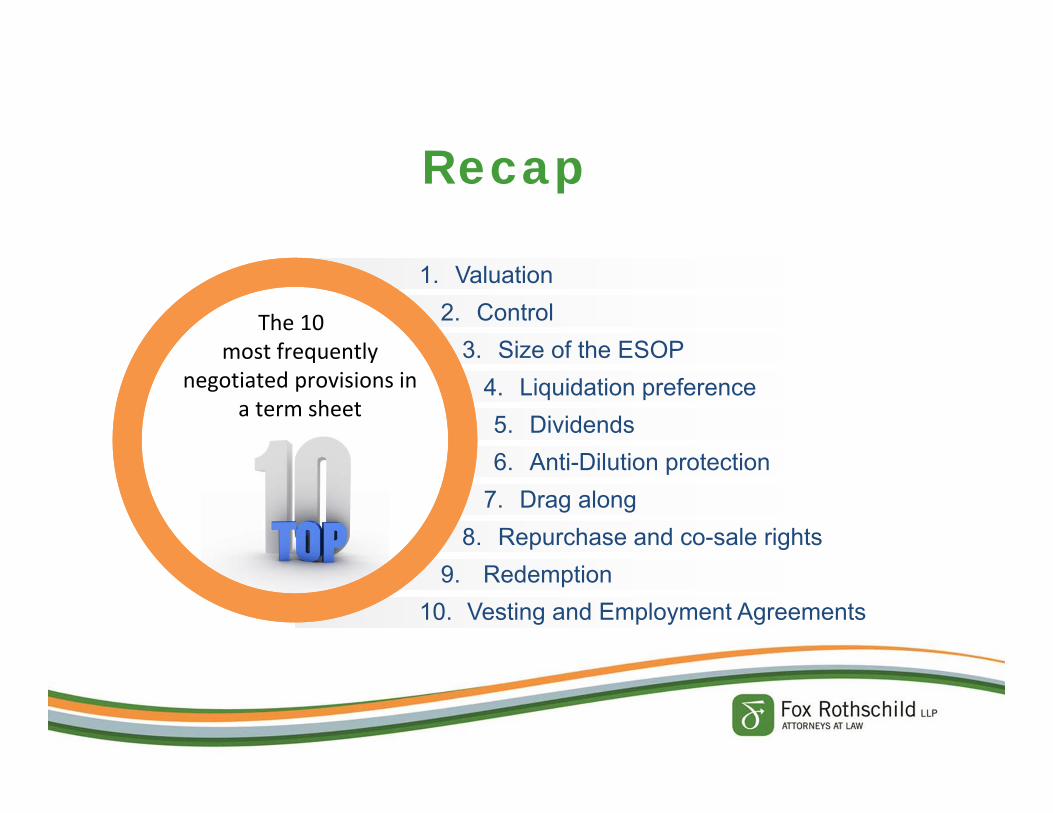

The 10most frequently

negotiated provisions in a term sheet

1. Valuation2. Control

3. Size of the ESOP4. Liquidation preference5. Dividends6. Anti-Dilution protection

7. Drag along8. Repurchase and co-sale rights

9. Redemption10. Vesting and Employment Agreements

A great company is not necessarily a great investment. Terms drive ROI.

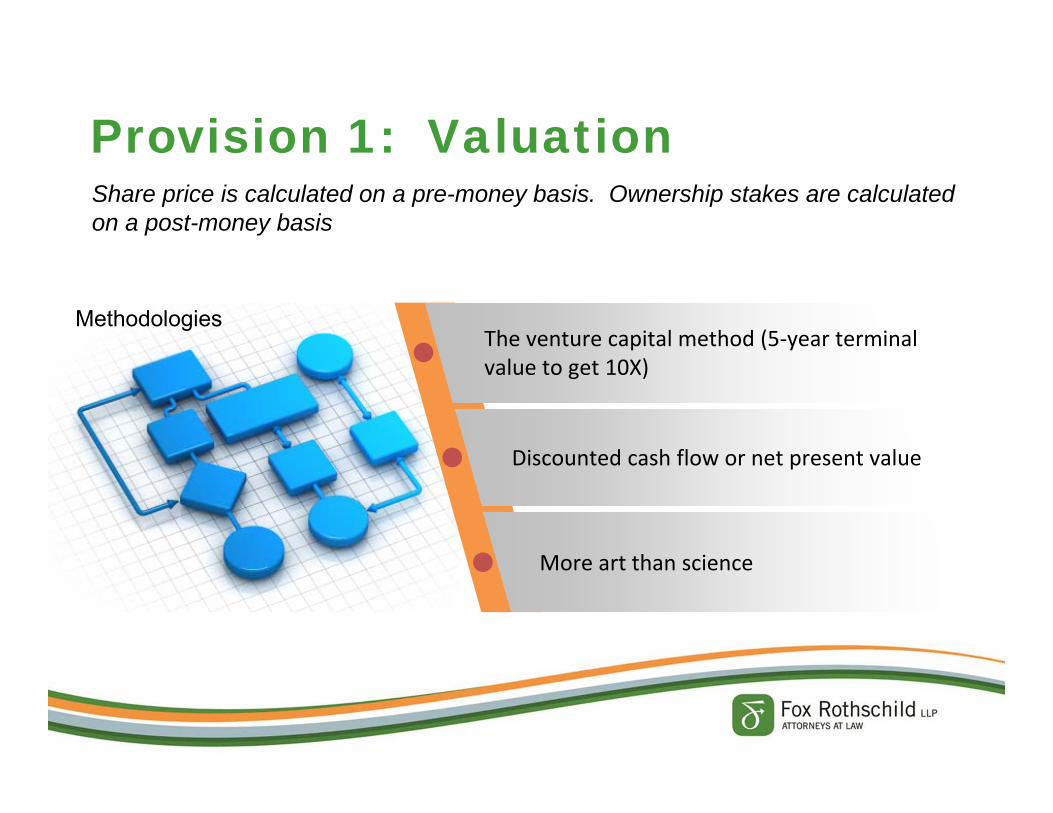

Provision 1: Valuation

MethodologiesThe venture capital method (5‐year terminal value to get 10X)

Discounted cash flow or net present value

More art than science

Share price is calculated on a pre-money basis. Ownership stakes are calculated on a post-money basis

Existing shareholders tend to

focus on the pre-money valuation

Existing shareholders tend to

focus on the pre-money valuation

New investors care about how

post-money valuation…

New investors care about how

post-money valuation…

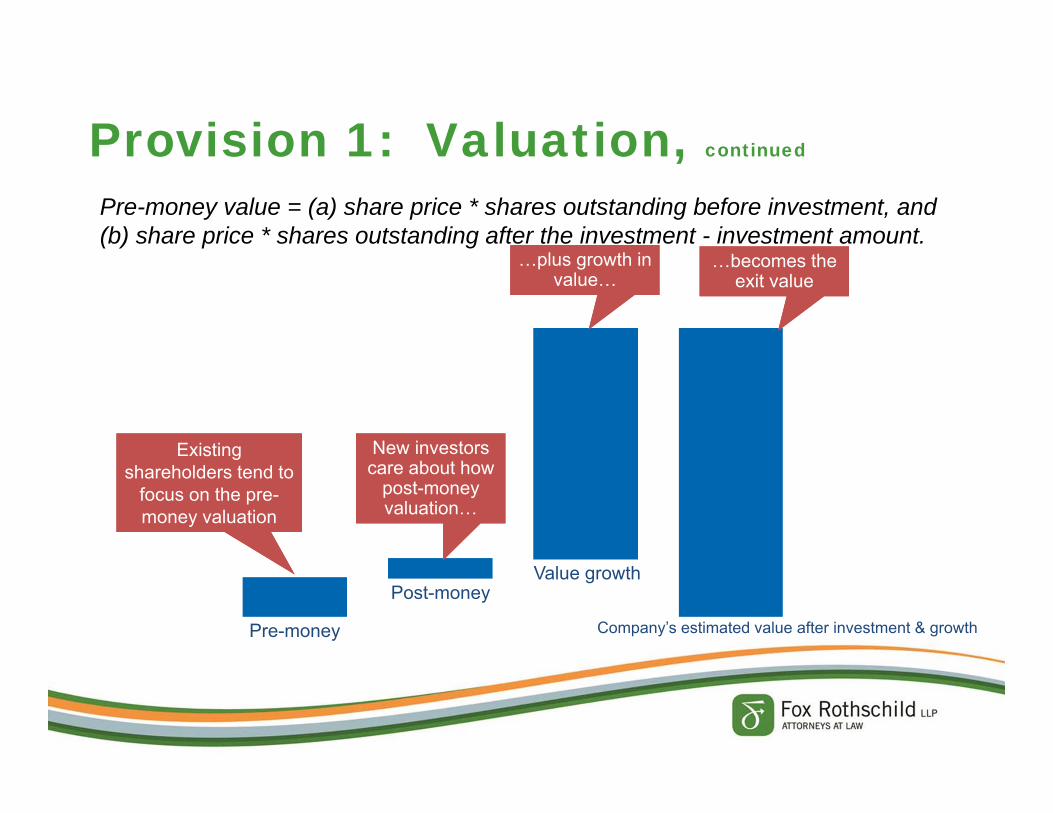

Provision 1: Valuation, continued

Pre-money value = (a) share price * shares outstanding before investment, and (b) share price * shares outstanding after the investment - investment amount.

Pre-money

Post-moneyValue growth

Company’s estimated value after investment & growth

…plus growth in value…

…plus growth in value…

…becomes the exit value

…becomes the exit value

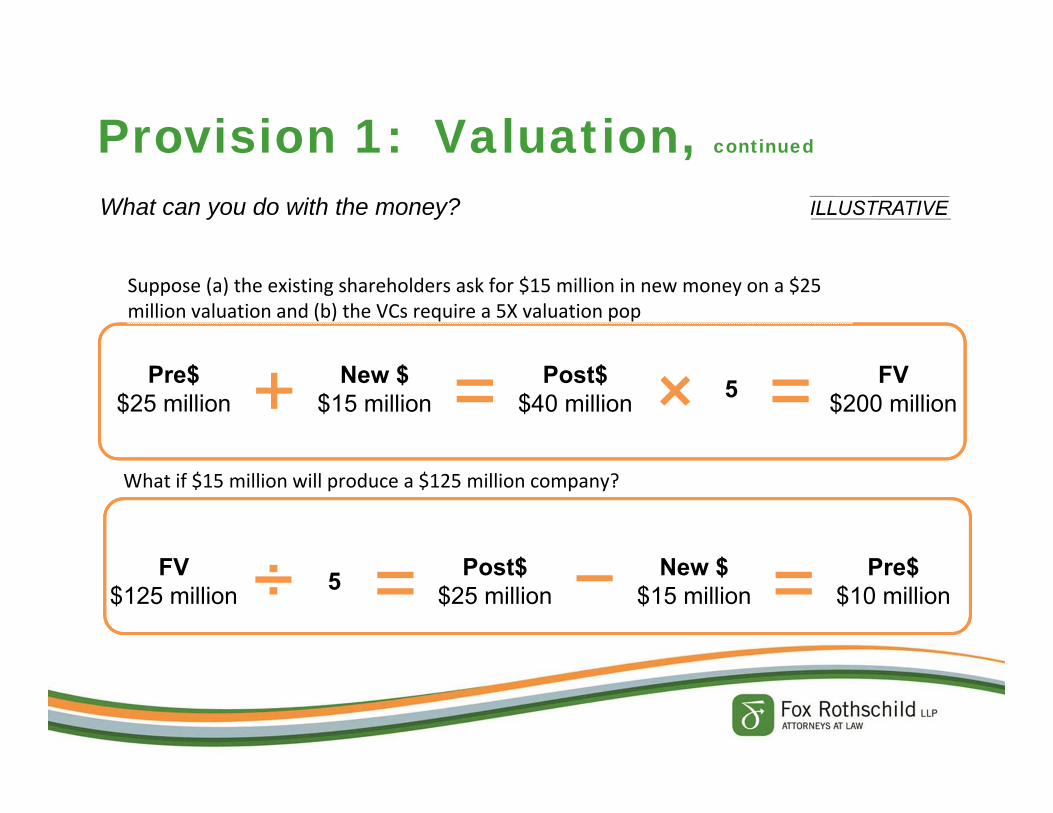

Provision 1: Valuation, continued

What can you do with the money?

Pre$ $25 million

New $ $15 million

Post$ $40 million 5 FV

$200 million

Suppose (a) the existing shareholders ask for $15 million in new money on a $25 million valuation and (b) the VCs require a 5X valuation pop

FV$125 million

New $ $15 million

Post$ $25 million5 Pre$

$10 million

What if $15 million will produce a $125 million company?

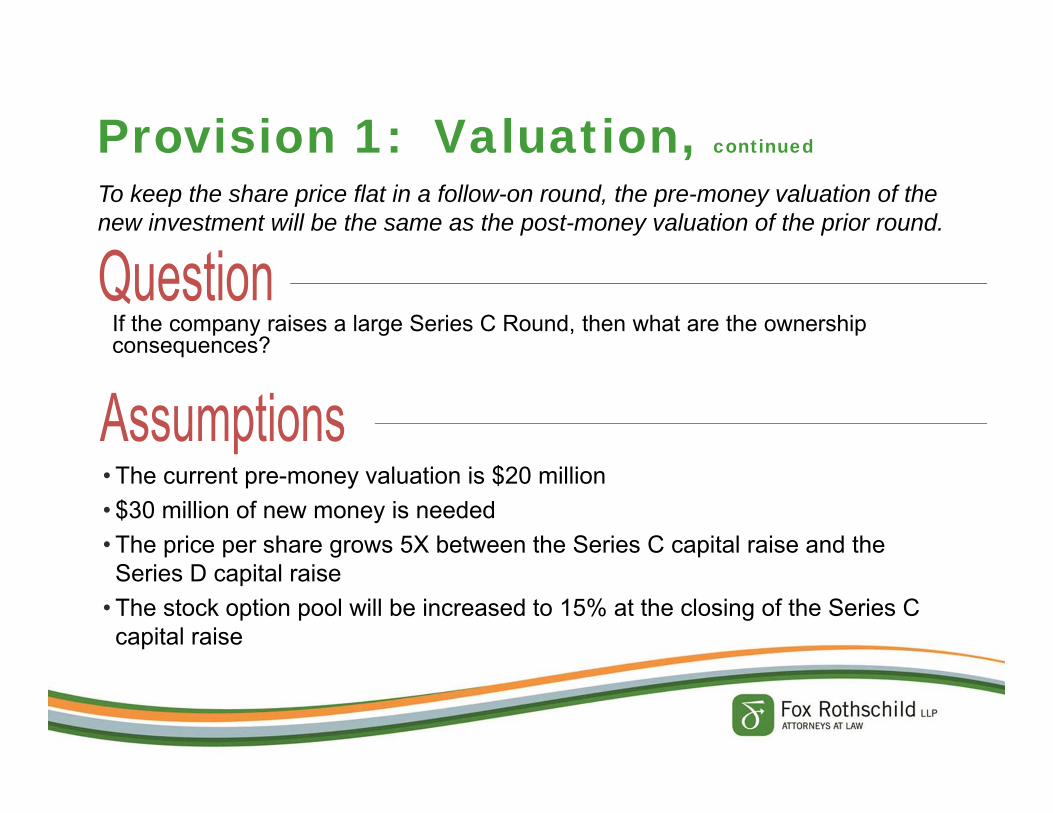

If the company raises a large Series C Round, then what are the ownership consequences?

Provision 1: Valuation, continued

To keep the share price flat in a follow-on round, the pre-money valuation of the new investment will be the same as the post-money valuation of the prior round.

• The current pre-money valuation is $20 million• $30 million of new money is needed• The price per share grows 5X between the Series C capital raise and the Series D capital raise

• The stock option pool will be increased to 15% at the closing of the Series C capital raise

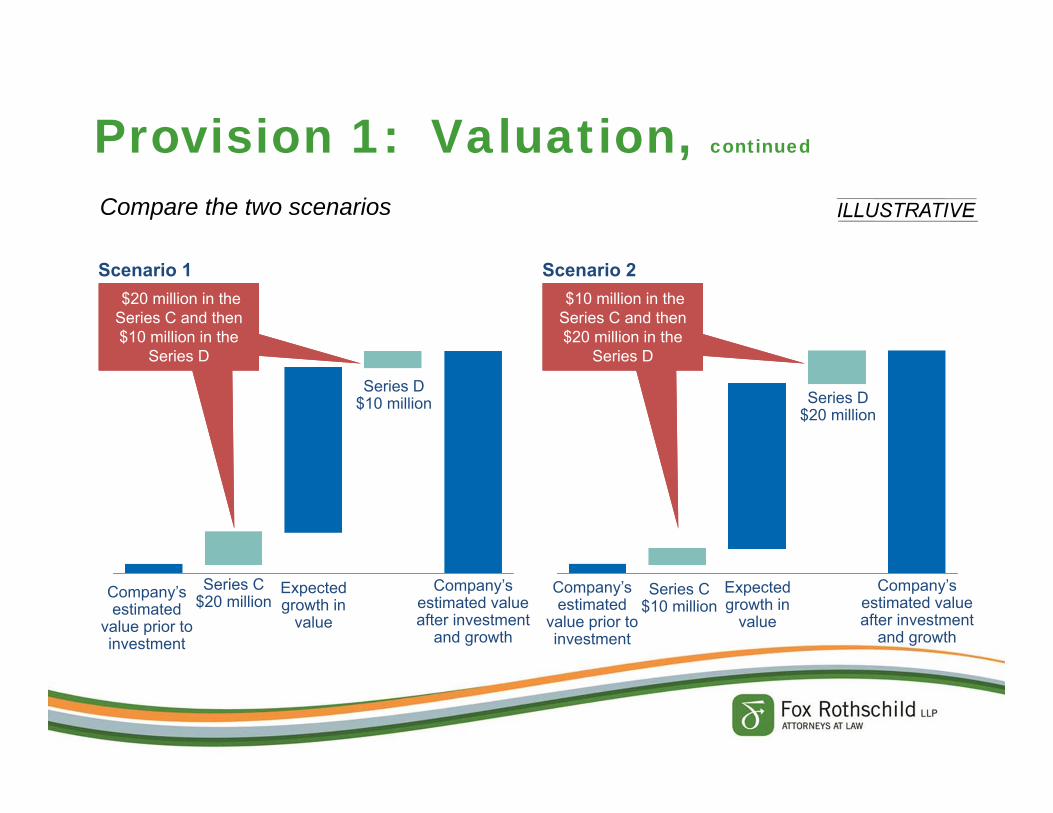

Provision 1: Valuation, continued

Compare the two scenarios

Company’s estimated

value prior to investment

Expected growth in

value

Company’s estimated value after investment

and growth

Scenario 1

Series C$20 million

Series D$10 million

$20 million in the Series C and then $10 million in the

Series D

$20 million in the Series C and then $10 million in the

Series D

$20 million in the Series C and then $10 million in the

Series D

$20 million in the Series C and then $10 million in the

Series D

Company’s estimated

value prior to investment

Expected growth in

value

Company’s estimated value after investment

and growth

Scenario 2

Series C$10 million

Series D$20 million

$20 million in the Series C and then $10 million in the

Series D

$10 million in the Series C and then $20 million in the

Series D

$20 million in the Series C and then $10 million in the

Series D

$10 million in the Series C and then $20 million in the

Series D

Provision 1: Valuation, continued

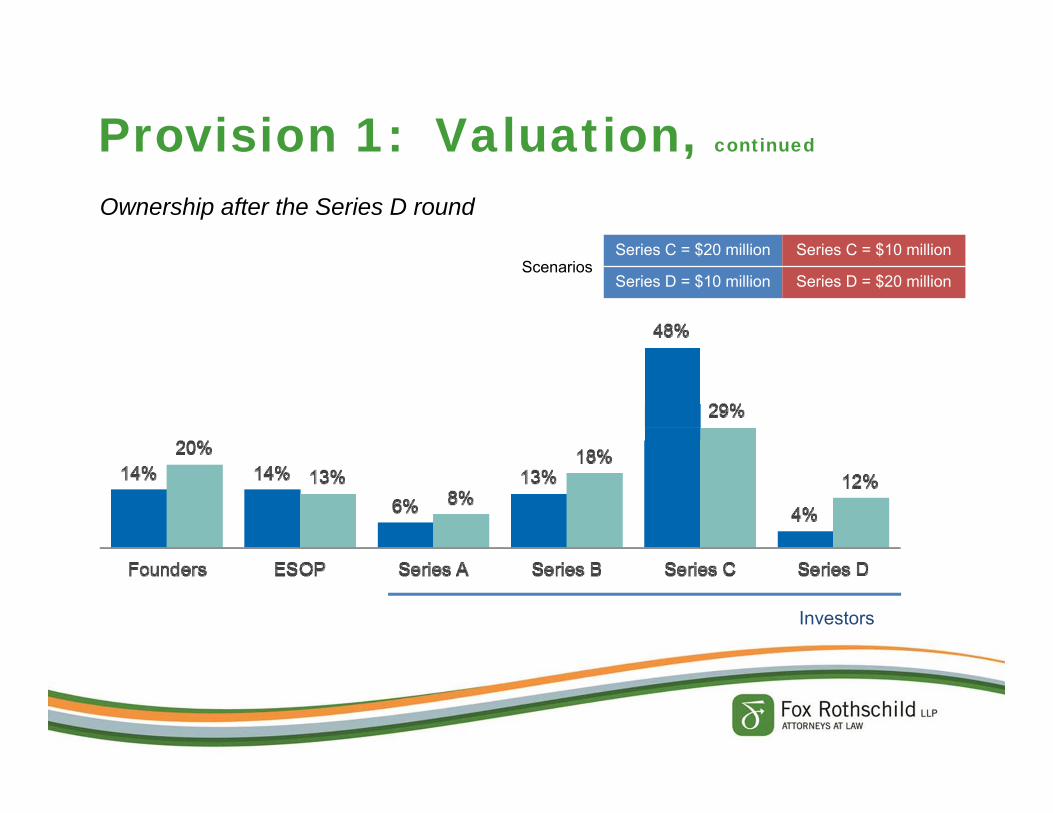

Ownership after the Series D round

Investors

ScenariosSeries C = $20 million Series C = $10 million

Series D = $10 million Series D = $20 million

Provision 1: Valuation, continued

"No, thank you, I don't want your money now. I want it next year."

Lessons• Raise the money needed, grow value, then raise the rest• Capital efficiency preserves ownership

Other Considerations

• If the money is available, then take it• Essential employees may get "trued up"

through option grants. Early investors and nonessential employees get diluted

Provision 2: Control

… Board control important?

… Board control not enough?

Board control

Provision 2: Control, continued

Shareholder veto

Do all preferred vote as 1 class, or is there a separate vote of each series?

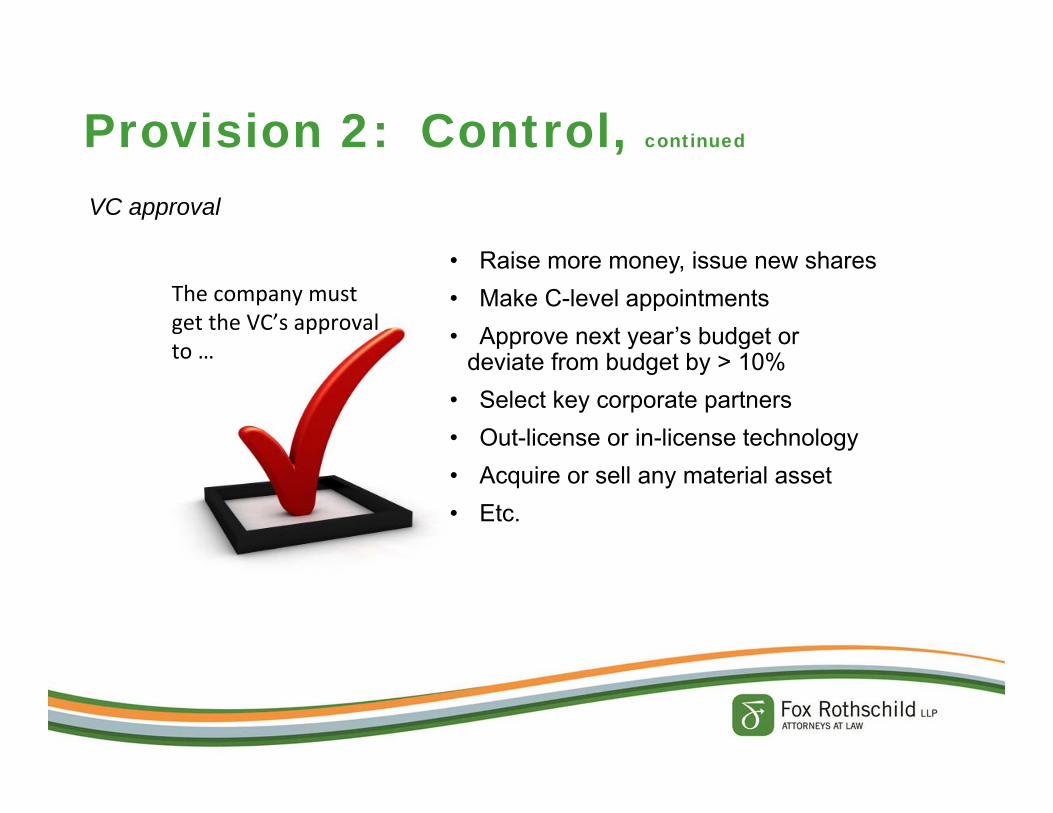

Provision 2: Control, continued

VC approval

The company must get the VC’s approval to …

• Raise more money, issue new shares• Make C-level appointments• Approve next year’s budget or

deviate from budget by > 10%• Select key corporate partners• Out-license or in-license technology• Acquire or sell any material asset• Etc.

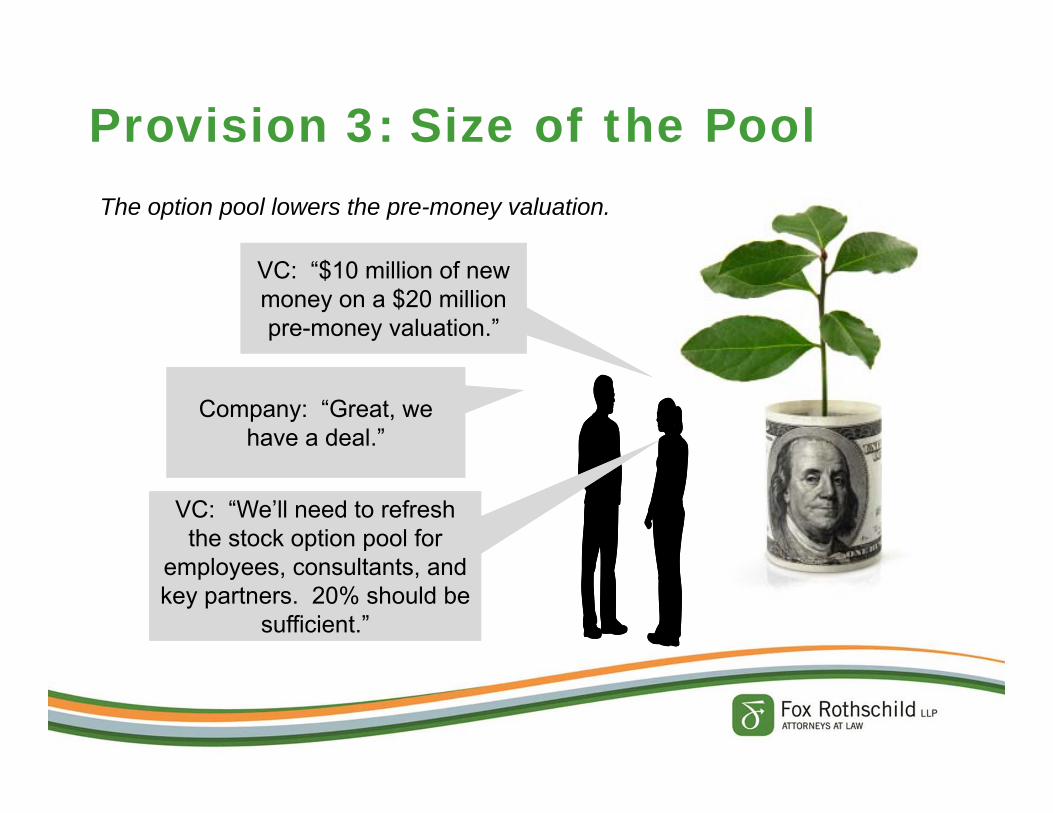

Provision 3: Size of the PoolThe option pool lowers the pre-money valuation.

VC: “$10 million of new money on a $20 million pre-money valuation.”

VC: “$10 million of new money on a $20 million pre-money valuation.”

Company: “Great, we have a deal.”

Company: “Great, we have a deal.”

VC: “We’ll need to refresh the stock option pool for

employees, consultants, and key partners. 20% should be

sufficient.”

VC: “We’ll need to refresh the stock option pool for

employees, consultants, and key partners. 20% should be

sufficient.”

Provision 4: Liquidation PreferencesA liquidation preference is the amount investor will receive prior to pro rata distribution

A 1X liquidation preference means that, upon a sale of the company, the investor gets back its initial investment

Provision 4: Liquidation Preferences, continued

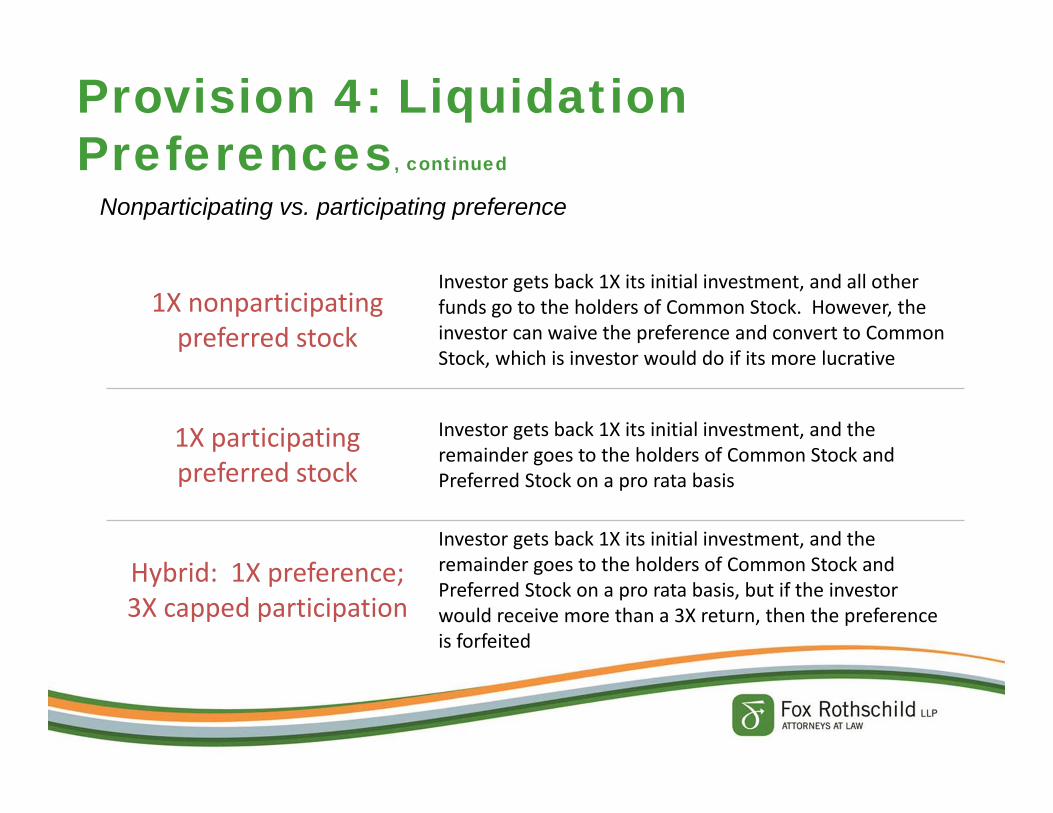

Nonparticipating vs. participating preference

1X nonparticipating preferred stock

Investor gets back 1X its initial investment, and all other funds go to the holders of Common Stock. However, the investor can waive the preference and convert to Common Stock, which is investor would do if its more lucrative

1X participating preferred stock

Investor gets back 1X its initial investment, and the remainder goes to the holders of Common Stock and Preferred Stock on a pro rata basis

Hybrid: 1X preference; 3X capped participation

Investor gets back 1X its initial investment, and the remainder goes to the holders of Common Stock and Preferred Stock on a pro rata basis, but if the investor would receive more than a 3X return, then the preference is forfeited

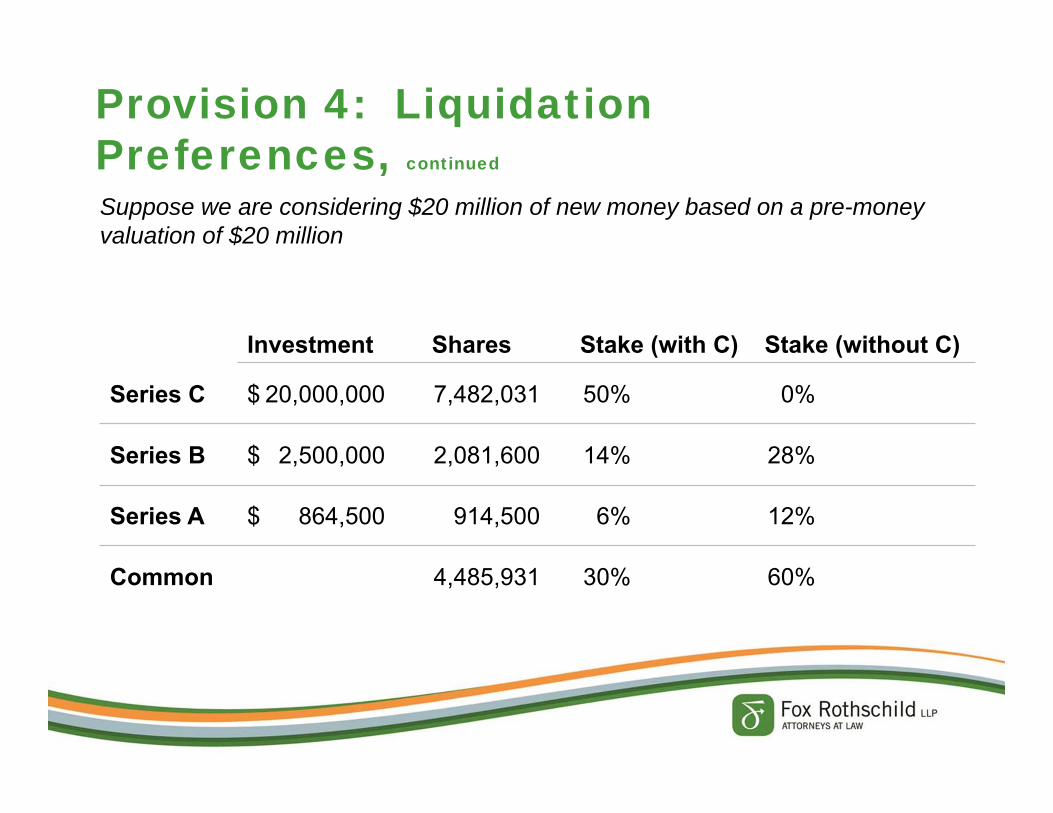

Investment Shares Stake (with C) Stake (without C)

Series C $ 20,000,000 7,482,031 50% 0%

Series B $ 2,500,000 2,081,600 14% 28%

Series A $ 864,500 914,500 6% 12%

Common 4,485,931 30% 60%

Provision 4: Liquidation Preferences, continued

Suppose we are considering $20 million of new money based on a pre-money valuation of $20 million

1X non-participating¹

1Xparticipating

1X preference;3X cap ROI

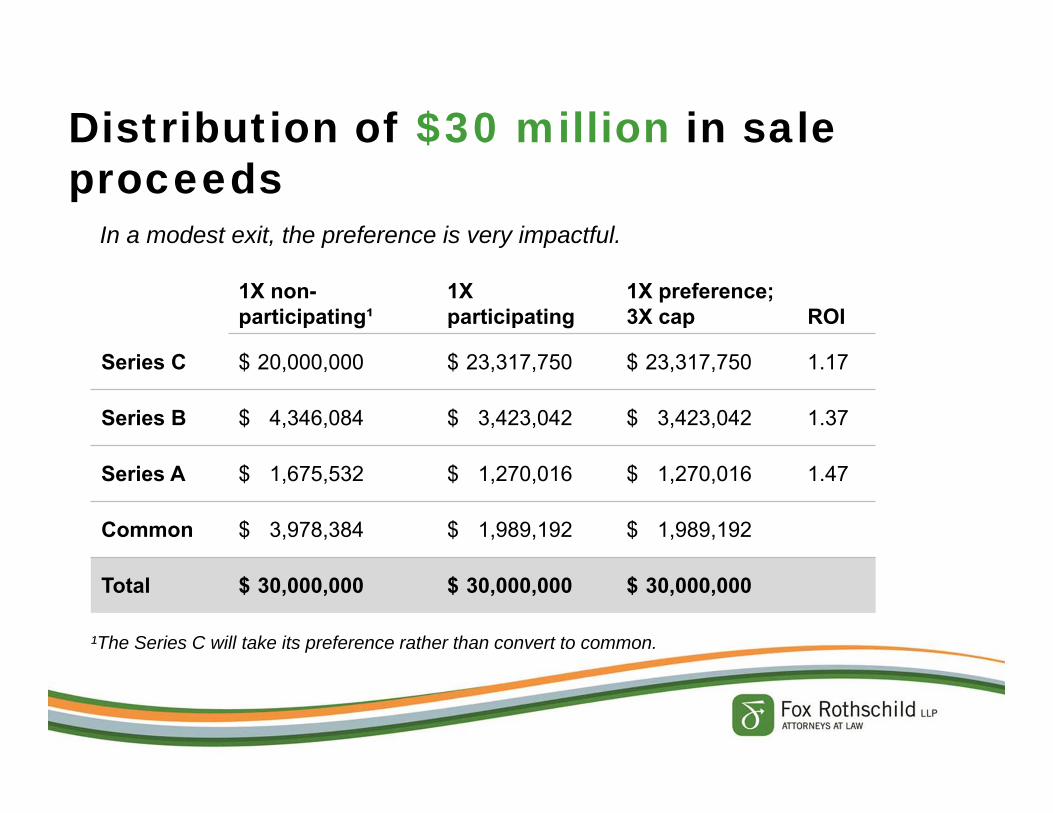

Series C $ 20,000,000 $ 23,317,750 $ 23,317,750 1.17

Series B $ 4,346,084 $ 3,423,042 $ 3,423,042 1.37

Series A $ 1,675,532 $ 1,270,016 $ 1,270,016 1.47

Common $ 3,978,384 $ 1,989,192 $ 1,989,192

Total $ 30,000,000 $ 30,000,000 $ 30,000,000

Distribution of $30 million in sale proceeds

In a modest exit, the preference is very impactful.

¹The Series C will take its preference rather than convert to common.

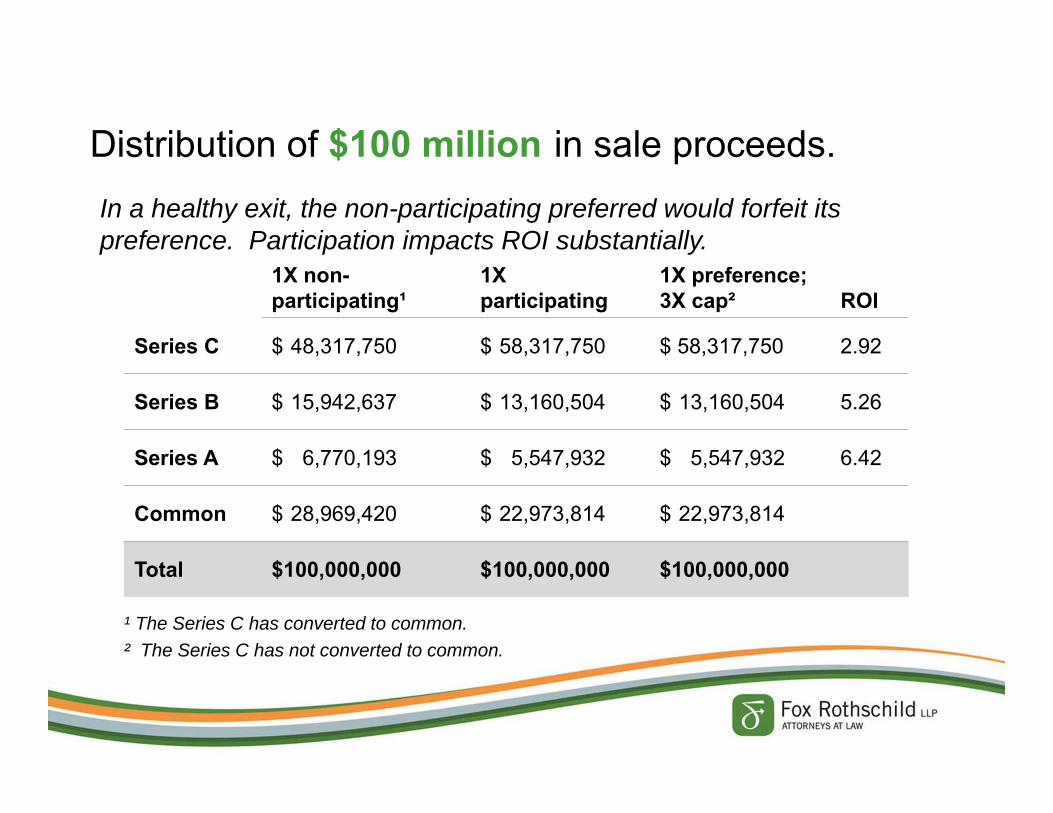

Distribution of $100 million in sale proceeds.In a healthy exit, the non-participating preferred would forfeit its preference. Participation impacts ROI substantially.

1X non-participating¹

1Xparticipating

1X preference;3X cap² ROI

Series C $ 48,317,750 $ 58,317,750 $ 58,317,750 2.92

Series B $ 15,942,637 $ 13,160,504 $ 13,160,504 5.26

Series A $ 6,770,193 $ 5,547,932 $ 5,547,932 6.42

Common $ 28,969,420 $ 22,973,814 $ 22,973,814

Total $100,000,000 $100,000,000 $100,000,000

¹ The Series C has converted to common.² The Series C has not converted to common.

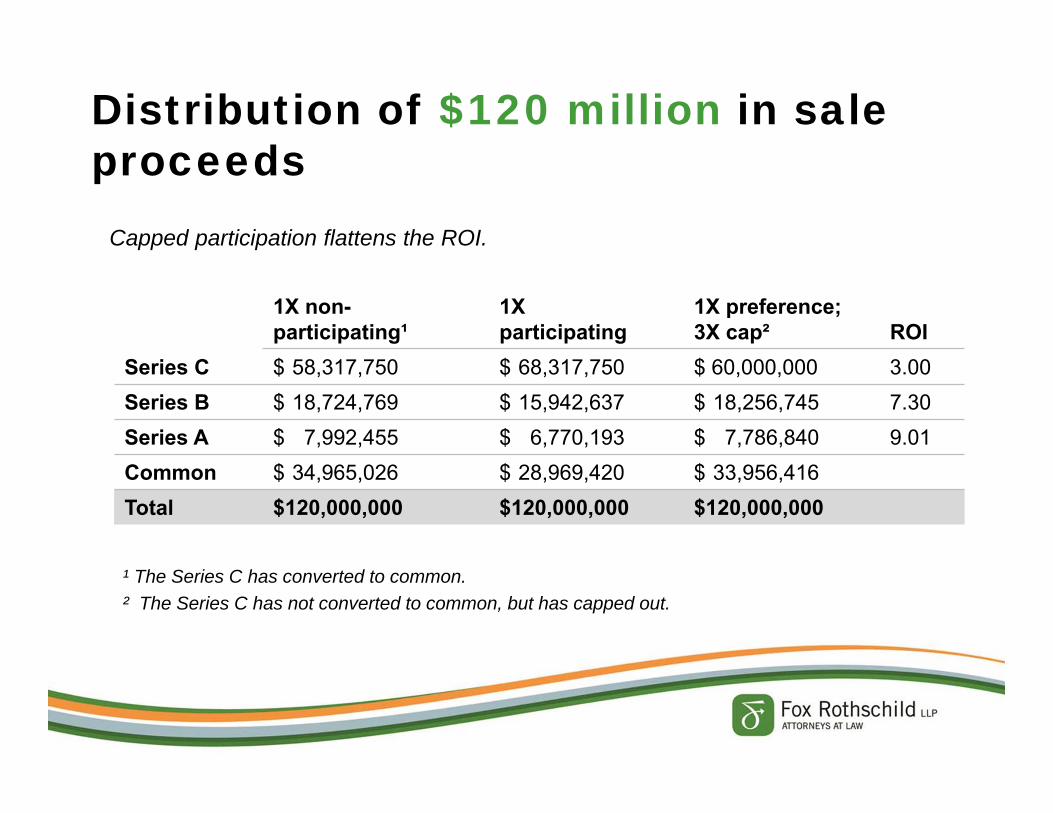

Distribution of $120 million in sale proceeds

Capped participation flattens the ROI.

1X non-participating¹

1Xparticipating

1X preference;3X cap² ROI

Series C $ 58,317,750 $ 68,317,750 $ 60,000,000 3.00Series B $ 18,724,769 $ 15,942,637 $ 18,256,745 7.30Series A $ 7,992,455 $ 6,770,193 $ 7,786,840 9.01Common $ 34,965,026 $ 28,969,420 $ 33,956,416Total $120,000,000 $120,000,000 $120,000,000

¹ The Series C has converted to common.² The Series C has not converted to common, but has capped out.

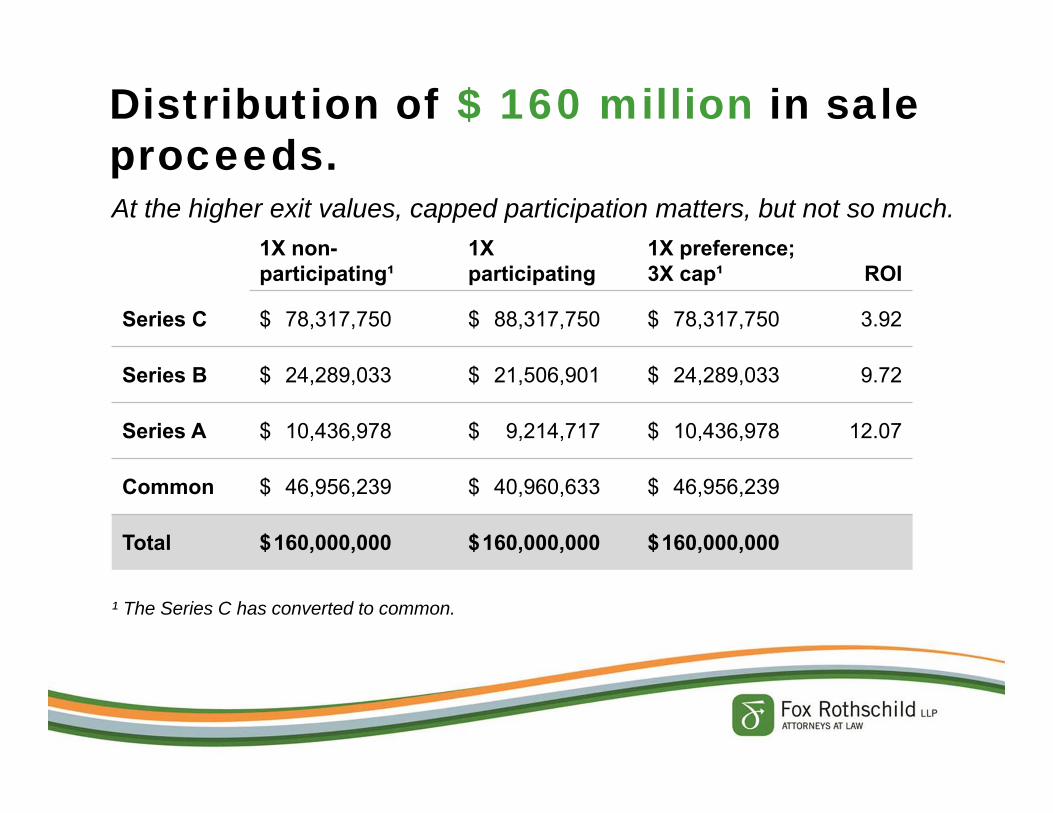

Distribution of $ 160 million in sale proceeds.At the higher exit values, capped participation matters, but not so much.

1X non-participating¹

1Xparticipating

1X preference;3X cap¹ ROI

Series C $ 78,317,750 $ 88,317,750 $ 78,317,750 3.92

Series B $ 24,289,033 $ 21,506,901 $ 24,289,033 9.72

Series A $ 10,436,978 $ 9,214,717 $ 10,436,978 12.07

Common $ 46,956,239 $ 40,960,633 $ 46,956,239

Total $160,000,000 $160,000,000 $160,000,000

¹ The Series C has converted to common.

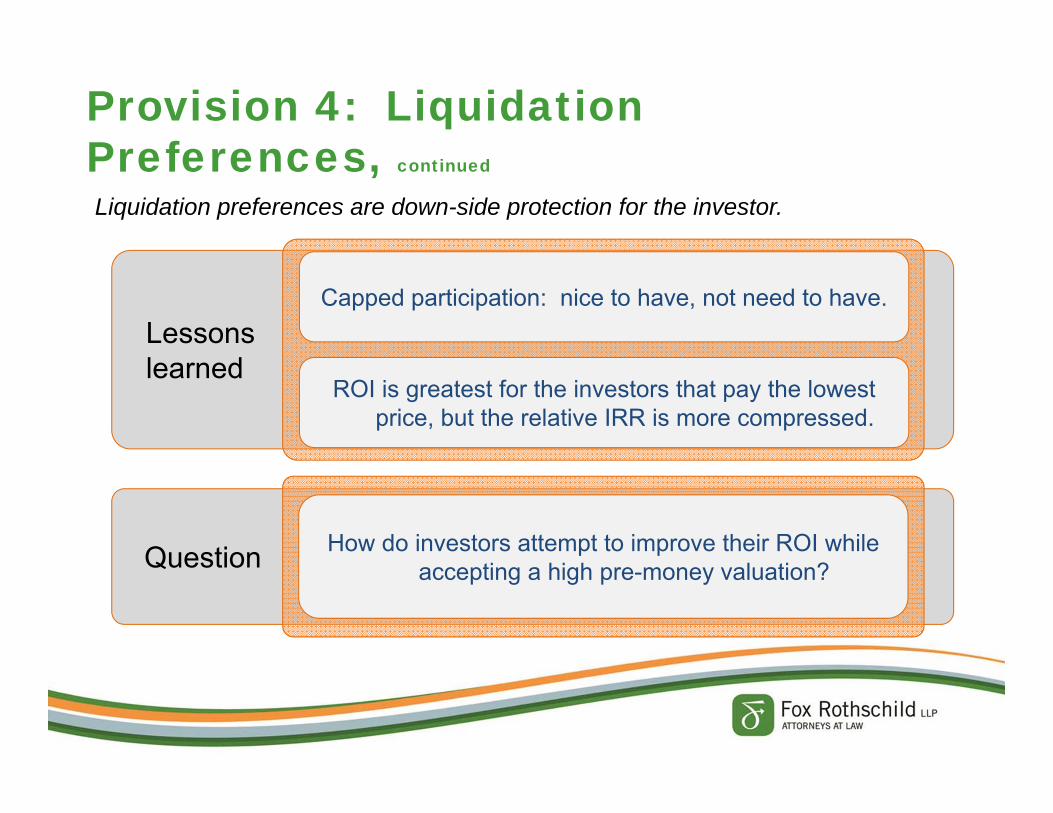

Provision 4: Liquidation Preferences, continued

Liquidation preferences are down-side protection for the investor.

Lessonslearned

Capped participation: nice to have, not need to have.

ROI is greatest for the investors that pay the lowest price, but the relative IRR is more compressed.

Question How do investors attempt to improve their ROI while accepting a high pre-money valuation?

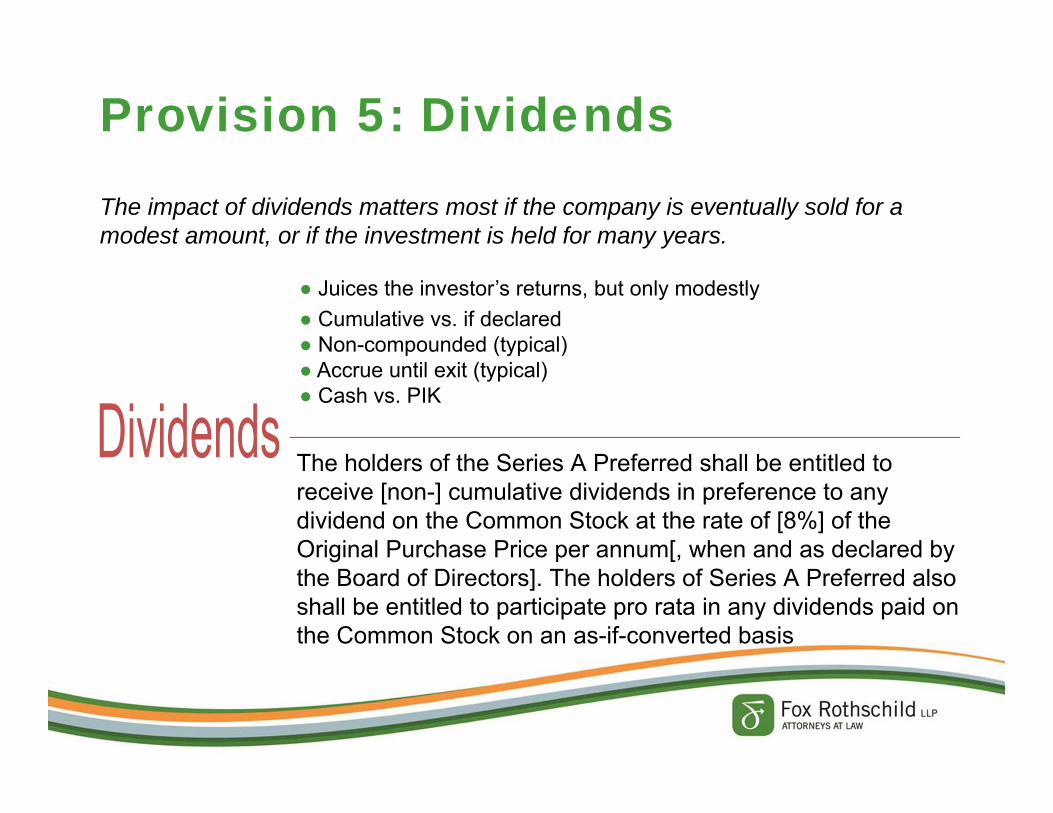

● Juices the investor’s returns, but only modestly● Cumulative vs. if declared● Non-compounded (typical)● Accrue until exit (typical)● Cash vs. PIK

Provision 5: Dividends

The impact of dividends matters most if the company is eventually sold for a modest amount, or if the investment is held for many years.

The holders of the Series A Preferred shall be entitled to receive [non-] cumulative dividends in preference to any dividend on the Common Stock at the rate of [8%] of the Original Purchase Price per annum[, when and as declared by the Board of Directors]. The holders of Series A Preferred also shall be entitled to participate pro rata in any dividends paid on the Common Stock on an as-if-converted basis

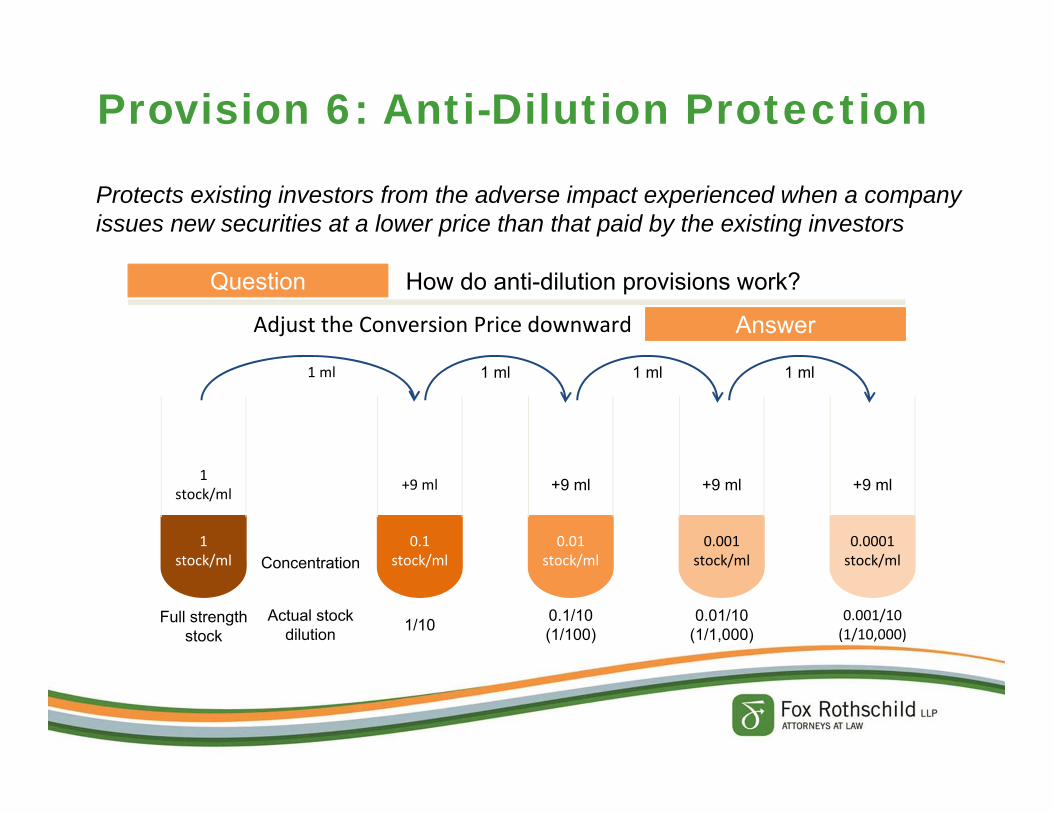

Provision 6: Anti-Dilution Protection

Protects existing investors from the adverse impact experienced when a company issues new securities at a lower price than that paid by the existing investors

Question

Answer

How do anti-dilution provisions work?

Adjust the Conversion Price downward

1 stock/ml

0.1 stock/ml

0.01 stock/ml

0.001 stock/ml

0.0001 stock/ml

1 stock/ml +9 ml +9 ml +9 ml +9 ml

Full strength stock

1/10 0.1/10 (1/100)

0.01/10 (1/1,000)

0.001/10 (1/10,000)

1 ml 1 ml 1 ml 1 ml

Concentration

Actual stock dilution

Provision 6: Anti-Dilution Protection, continued

Weighted average anti-dilution protection is more friendly to entrepreneur than full ratchet anti-dilution protection.

What are the common types of anti-dilution protection?

• Ratchet• Weighted average

What are the common types of anti-dilution protection?

• Ratchet• Weighted average

What kind of “issuance” can trigger anti-dilution protection?

What kind of “issuance” can trigger anti-dilution protection?

Provision 6: Anti-Dilution Protection, continued

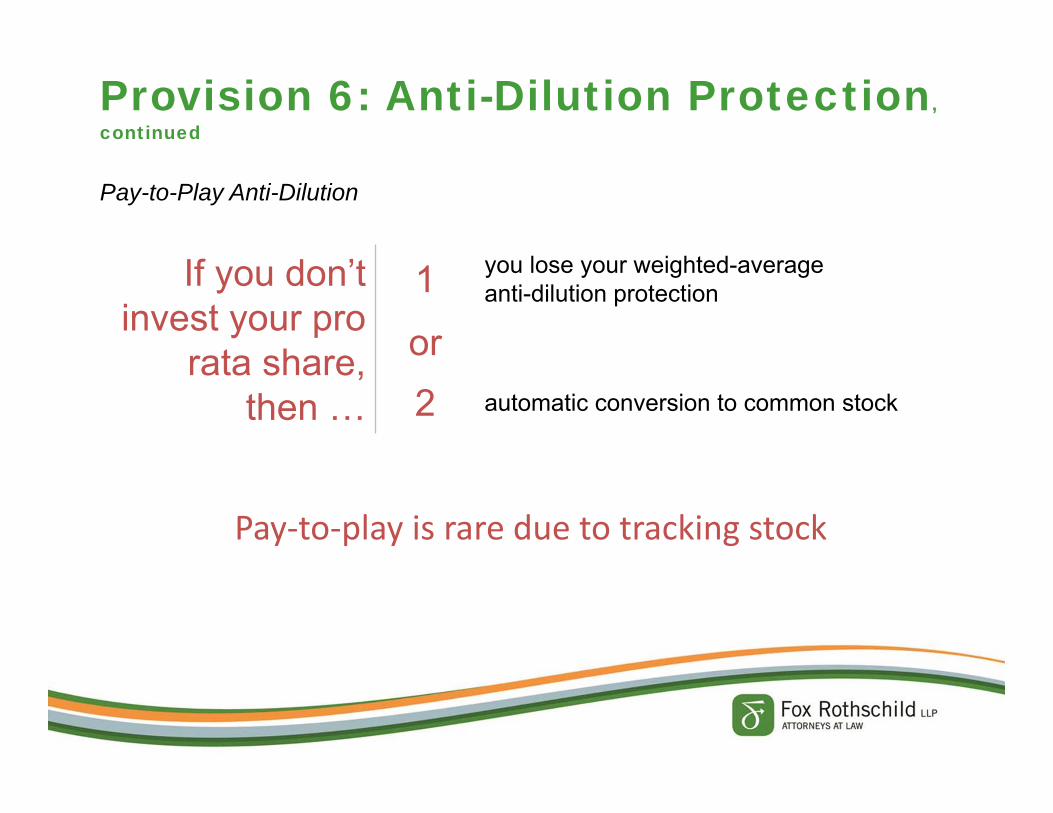

Pay-to-Play Anti-Dilution

If you don’t invest your pro

rata share, then …

1 you lose your weighted-average anti-dilution protection

or2 automatic conversion to common stock

Pay‐to‐play is rare due to tracking stock

Provision 7: Drag AlongDrag along has become standard.

• The new investor can require existing stockholders to vote in favor of a merger or sale of assets, or otherwise to sell their stock to a third party

• Rationale: (1) added security that a negotiated M&A event can be closed; (2) avoid/minimize dissenters rights, which interferes with tax‐free transactions

• Is it necessary?

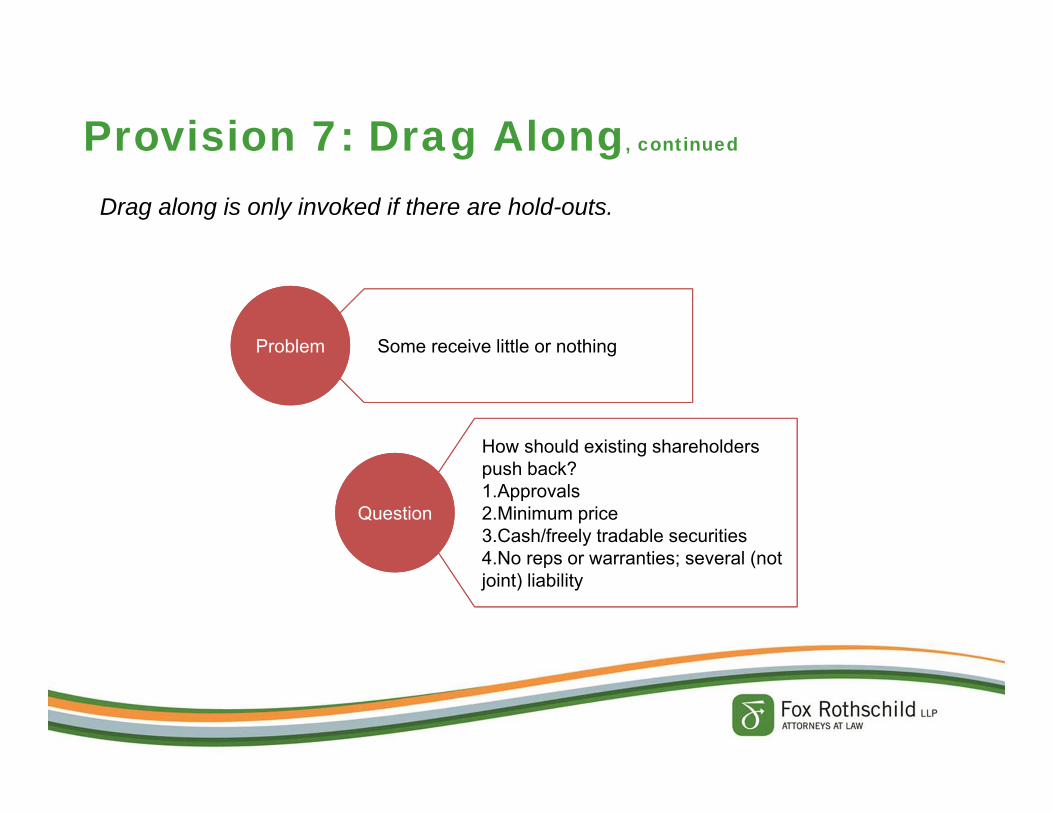

Provision 7: Drag Along, continued

Drag along is only invoked if there are hold-outs.

ProblemProblem Some receive little or nothing

QuestionQuestion

How should existing shareholders push back?1.Approvals2.Minimum price3.Cash/freely tradable securities4.No reps or warranties; several (not joint) liability

Provision 8: Repurchase and Co-Sale RightsRepurchase and co-sale right limit the incentive and ability of the founders to dispose of a significant portion of their holdings.

RoFR A repurchase right, exercisable by the company or the investor

Co-Sale The right to tag along with a founder or junior preferred stockholder who is selling

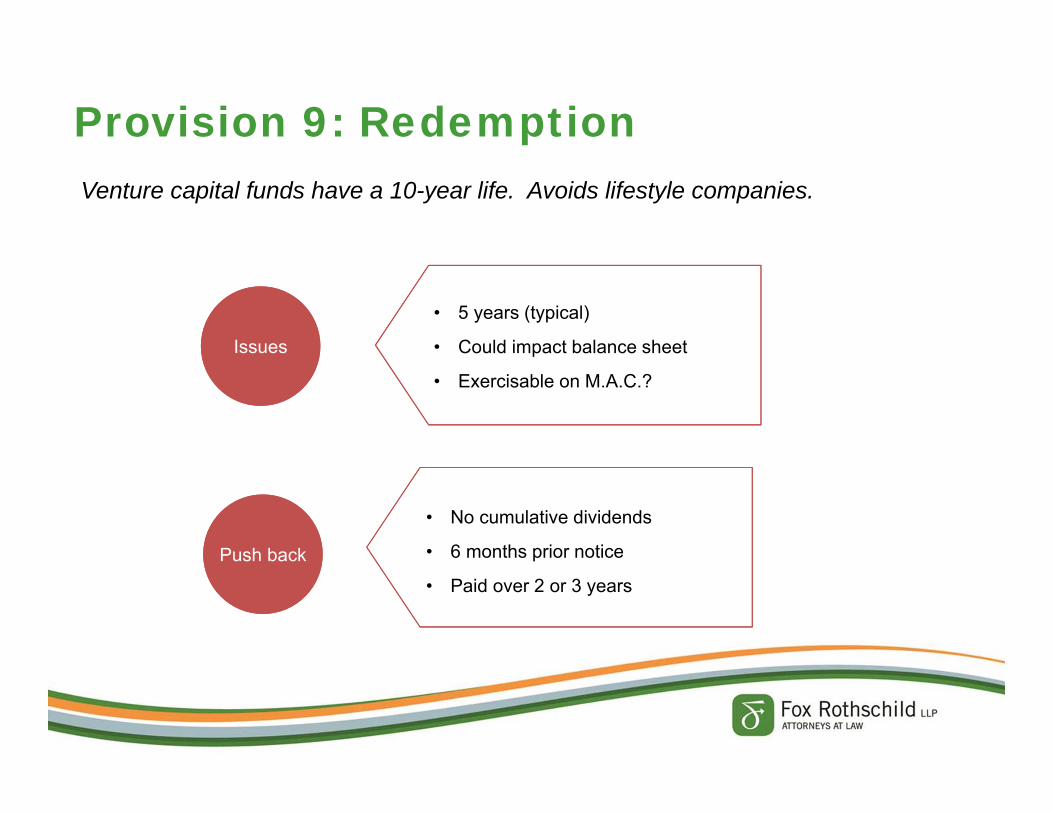

Provision 9: RedemptionVenture capital funds have a 10-year life. Avoids lifestyle companies.

Push backPush back

• No cumulative dividends

• 6 months prior notice

• Paid over 2 or 3 years

IssuesIssues

• 5 years (typical)

• Could impact balance sheet

• Exercisable on M.A.C.?

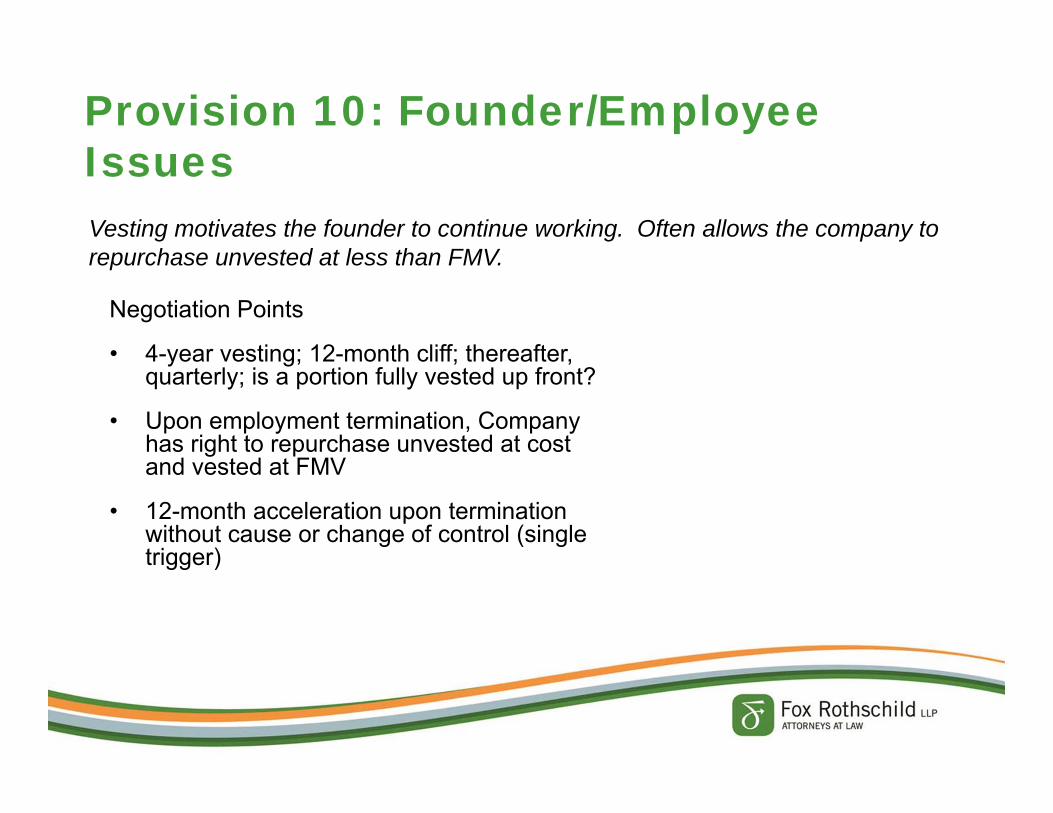

Provision 10: Founder/Employee Issues

Negotiation Points

• 4-year vesting; 12-month cliff; thereafter, quarterly; is a portion fully vested up front?

• Upon employment termination, Company has right to repurchase unvested at cost and vested at FMV

• 12-month acceleration upon termination without cause or change of control (single trigger)

Vesting motivates the founder to continue working. Often allows the company to repurchase unvested at less than FMV.

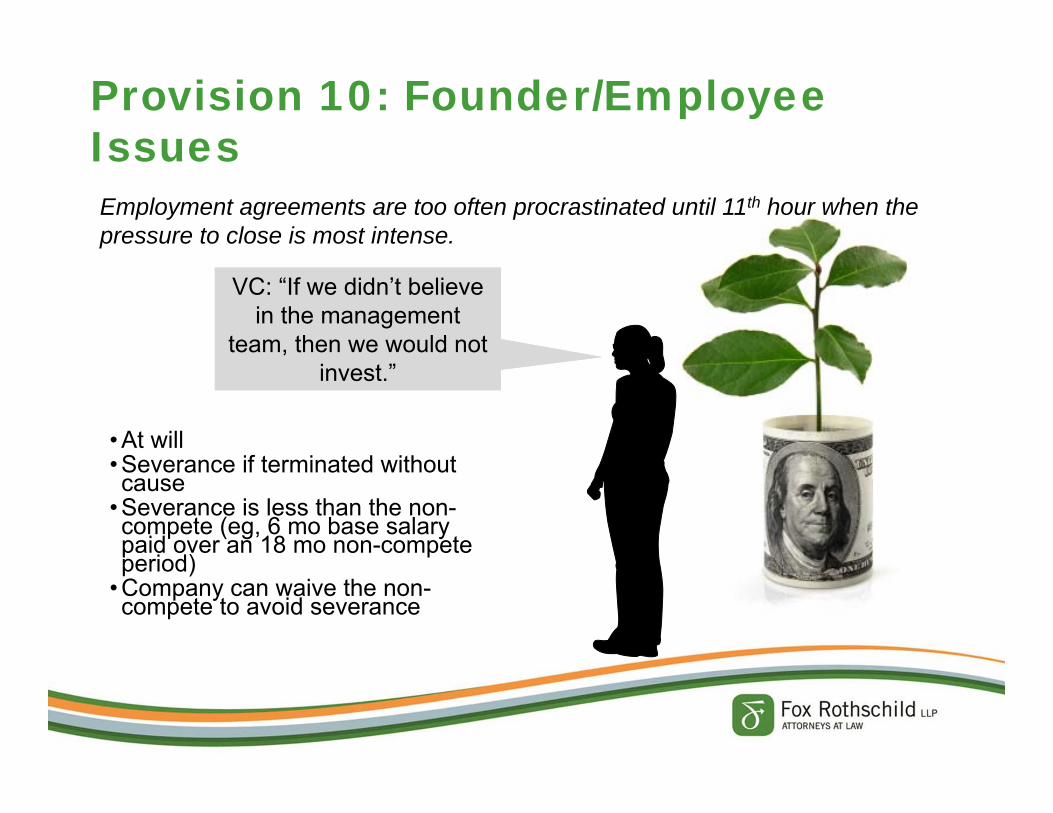

VC: “If we didn’t believe in the management

team, then we would not invest.”

VC: “If we didn’t believe in the management

team, then we would not invest.”

Provision 10: Founder/Employee Issues

• At will• Severance if terminated without cause

• Severance is less than the non-compete (eg, 6 mo base salary paid over an 18 mo non-compete period)

• Company can waive the non-compete to avoid severance

Employment agreements are too often procrastinated until 11th hour when the pressure to close is most intense.

Recap

The 10most frequently

negotiated provisions in a term sheet

1. Valuation2. Control

3. Size of the ESOP4. Liquidation preference5. Dividends6. Anti-Dilution protection

7. Drag along8. Repurchase and co-sale rights

9. Redemption10. Vesting and Employment Agreements

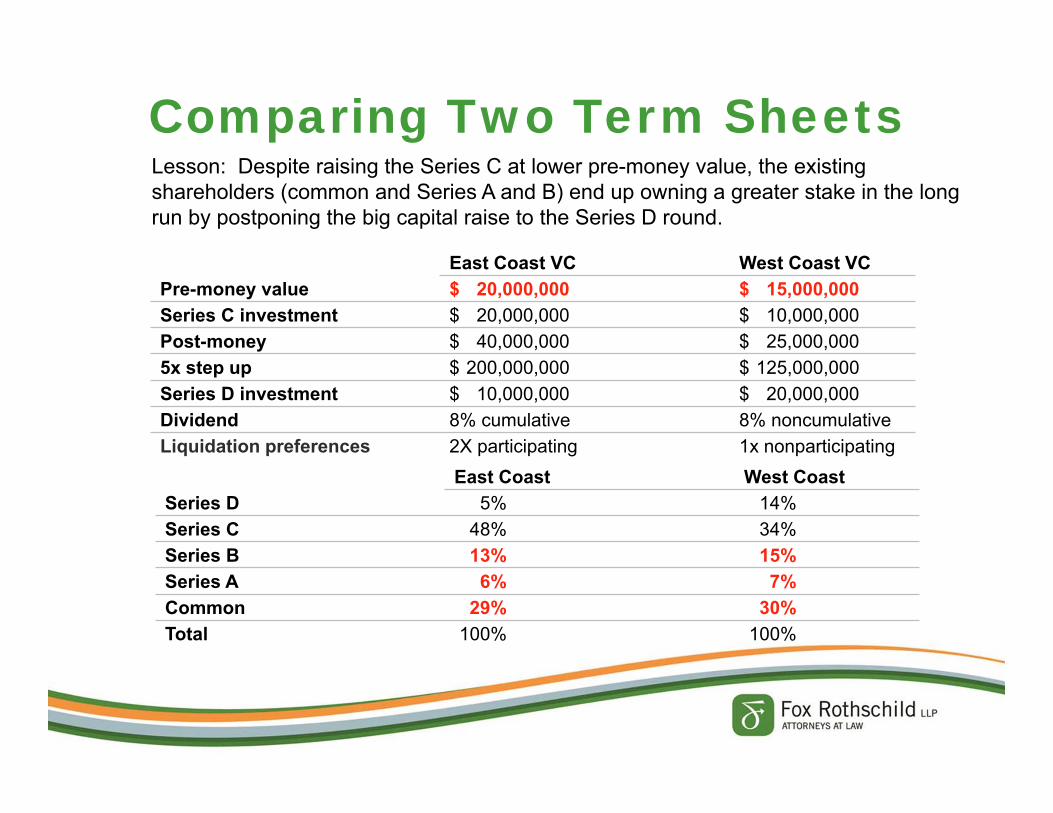

Comparing Two Term Sheets

East Coast VC West Coast VCPre-money value $ 20,000,000 $ 15,000,000Series C investment $ 20,000,000 $ 10,000,000Post-money $ 40,000,000 $ 25,000,0005x step up $ 200,000,000 $ 125,000,000Series D investment $ 10,000,000 $ 20,000,000Dividend 8% cumulative 8% noncumulativeLiquidation preferences 2X participating 1x nonparticipating

East Coast West CoastSeries D 5% 14%Series C 48% 34%Series B 13% 15%Series A 6% 7%Common 29% 30%Total 100% 100%

Lesson: Despite raising the Series C at lower pre-money value, the existing shareholders (common and Series A and B) end up owning a greater stake in the long run by postponing the big capital raise to the Series D round.

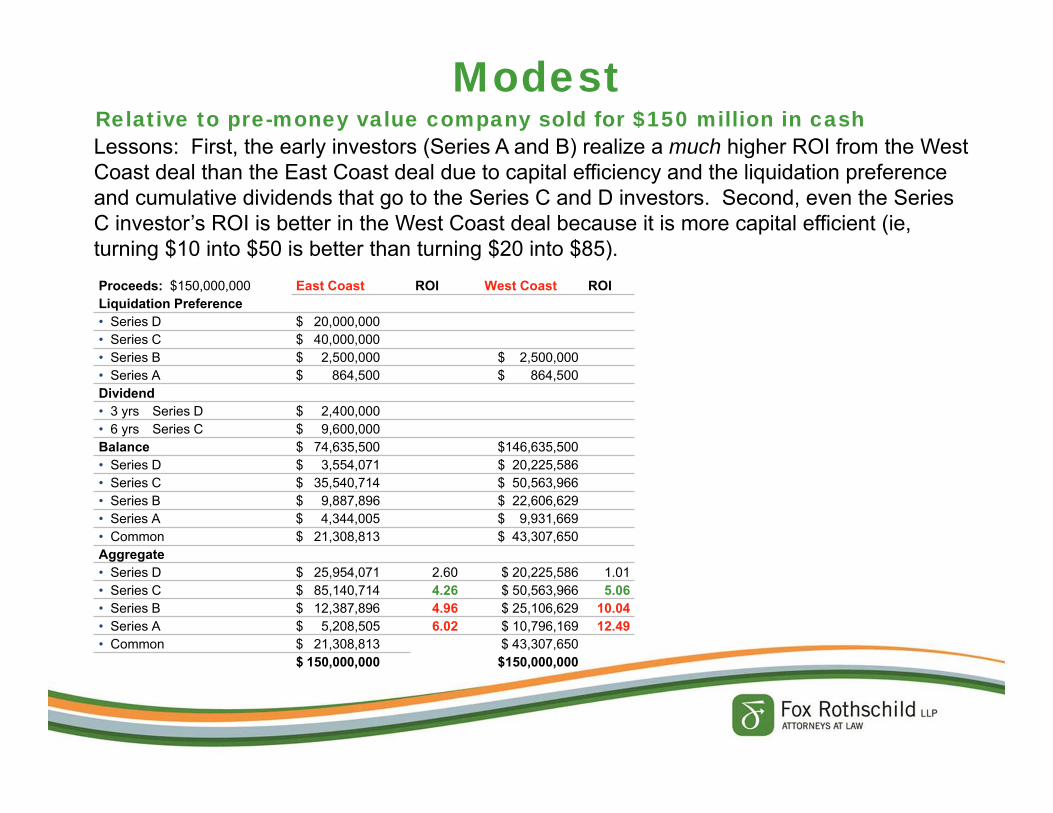

Proceeds: $150,000,000 East Coast ROI West Coast ROILiquidation Preference• Series D $ 20,000,000• Series C $ 40,000,000• Series B $ 2,500,000 $ 2,500,000• Series A $ 864,500 $ 864,500Dividend• 3 yrs Series D $ 2,400,000• 6 yrs Series C $ 9,600,000Balance $ 74,635,500 $146,635,500 • Series D $ 3,554,071 $ 20,225,586 • Series C $ 35,540,714 $ 50,563,966 • Series B $ 9,887,896 $ 22,606,629 • Series A $ 4,344,005 $ 9,931,669 • Common $ 21,308,813 $ 43,307,650 Aggregate• Series D $ 25,954,071 2.60 $ 20,225,586 1.01• Series C $ 85,140,714 4.26 $ 50,563,966 5.06• Series B $ 12,387,896 4.96 $ 25,106,629 10.04• Series A $ 5,208,505 6.02 $ 10,796,169 12.49• Common $ 21,308,813 $ 43,307,650

$ 150,000,000 $150,000,000

ModestLessons: First, the early investors (Series A and B) realize a much higher ROI from the West Coast deal than the East Coast deal due to capital efficiency and the liquidation preference and cumulative dividends that go to the Series C and D investors. Second, even the Series C investor’s ROI is better in the West Coast deal because it is more capital efficient (ie, turning $10 into $50 is better than turning $20 into $85).

Relative to pre-money value company sold for $150 million in cash

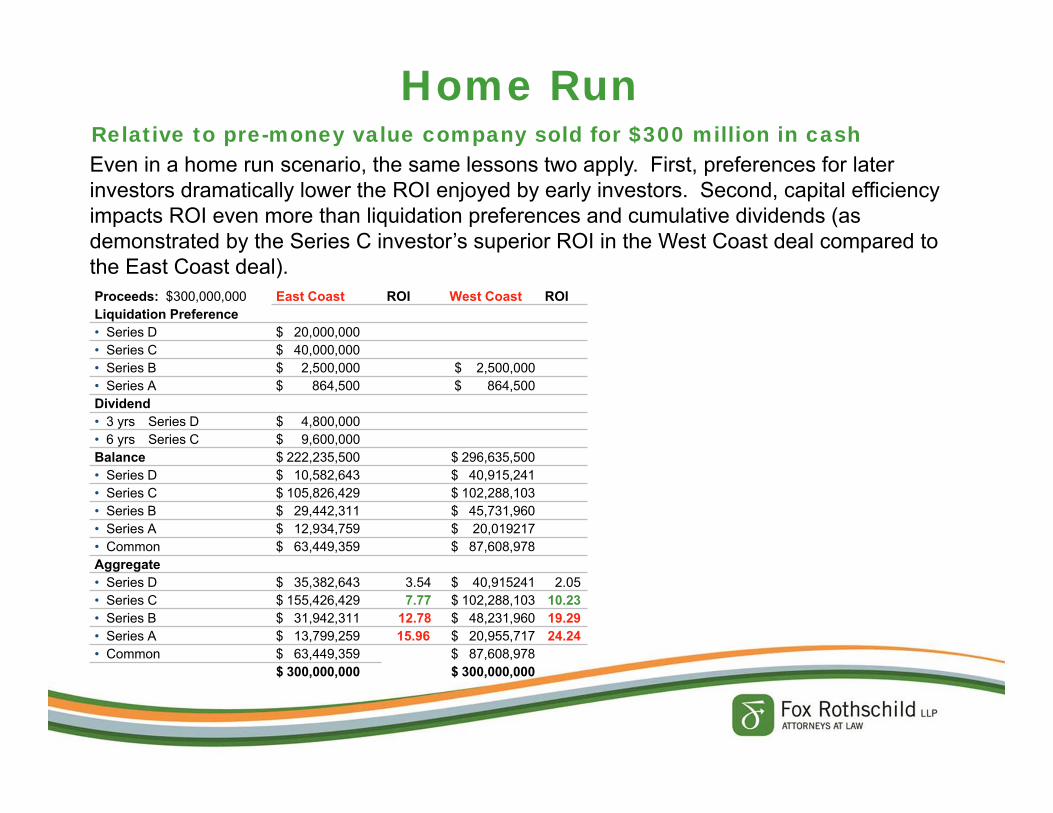

Proceeds: $300,000,000 East Coast ROI West Coast ROILiquidation Preference• Series D $ 20,000,000• Series C $ 40,000,000• Series B $ 2,500,000 $ 2,500,000• Series A $ 864,500 $ 864,500Dividend• 3 yrs Series D $ 4,800,000• 6 yrs Series C $ 9,600,000Balance $ 222,235,500 $ 296,635,500• Series D $ 10,582,643 $ 40,915,241• Series C $ 105,826,429 $ 102,288,103• Series B $ 29,442,311 $ 45,731,960• Series A $ 12,934,759 $ 20,019217• Common $ 63,449,359 $ 87,608,978Aggregate• Series D $ 35,382,643 3.54 $ 40,915241 2.05• Series C $ 155,426,429 7.77 $ 102,288,103 10.23• Series B $ 31,942,311 12.78 $ 48,231,960 19.29• Series A $ 13,799,259 15.96 $ 20,955,717 24.24• Common $ 63,449,359 $ 87,608,978

$ 300,000,000 $ 300,000,000

Home RunEven in a home run scenario, the same lessons two apply. First, preferences for later investors dramatically lower the ROI enjoyed by early investors. Second, capital efficiency impacts ROI even more than liquidation preferences and cumulative dividends (as demonstrated by the Series C investor’s superior ROI in the West Coast deal compared to the East Coast deal).

Relative to pre-money value company sold for $300 million in cash

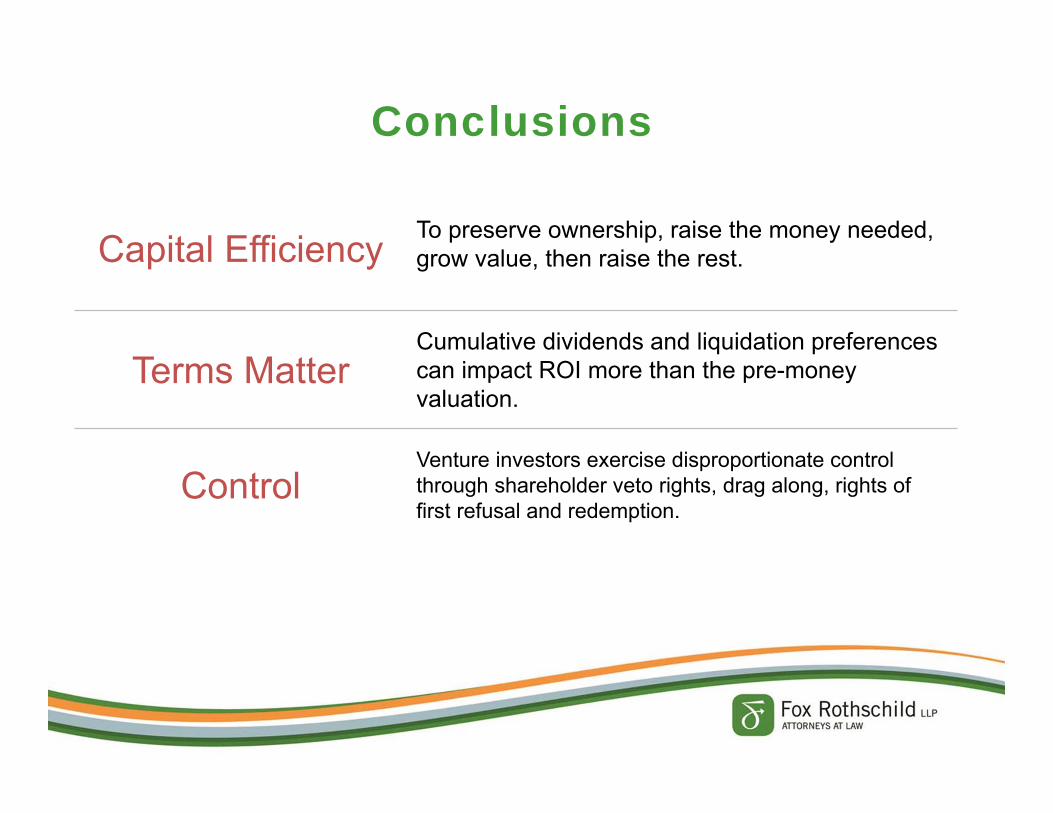

Conclusions

Capital Efficiency To preserve ownership, raise the money needed, grow value, then raise the rest.

Terms MatterCumulative dividends and liquidation preferences can impact ROI more than the pre-money valuation.

ControlVenture investors exercise disproportionate control through shareholder veto rights, drag along, rights of first refusal and redemption.