Embed Size (px)

Citation preview

Investor Presentation

March 2014

www.bice.cl

2

Presenters

♦ Alberto Schilling – Chief Executive Officer (47, married (23), 3 children)

♦ Mr. Schilling has served in various positions at BICE prior to becoming CEO, including, Credit Analyst and Account Executive

(Corporations), Vice President of Structured Finance, Director of Investment Banking (BICE Chileconsult Asesorías

Financieras S.A) and Head of Corporate Banking. Between 1995 and 1997 worked in NM Rothschild & Sons Ltd. in London.

♦ Mr. Schilling is currently on the boards or executive committees of BICE Inversiones Administradora General de Fondos S.A.,

Securitizadora BICE S.A., BICE Inversiones Corredores de Bolsa S.A., BICE Corredores de Seguros Ltda., BICE Factoring

S.A., BICE Chileconsult Asesorías Financieras S.A., BICE Asset Management, BICE Carteras S.A.

♦ Aside from his involvement in BICE, he is a member of the boards of Corporación Chileno-Alemana de Beneficencia

(Chilean-German non-profit organization), Clínica Alemana SpA (3 Clinics in Chile), and Chairman of Hogares Alemanes and

Hogares Alemanes Osorno (3 elderly homes). Has been a board member of Club Deportivo Manquehue (Sport Club) and

Cámara Chileno-Alemana de Comercio (Chilean-German Chamber of Commerce).

♦ Mr. Schilling holds a degree in Business Administration from Universidad de Chile; he attended the Advanced Management

Program at Harvard Business School in 2008.

♦ Rodrigo Álvarez – Chief Financial Officer (51, married (28), 4 children)

♦ Mr. Alvarez has been the CFO at BICE for 10 years, prior to which held various positions including at Bancard S.A. and

Citibank in Chile, where he held the positions of FX Trader, FX Professional Head, FX Unit Head and Research Head, and

eventually Country Treasurer and Head of the Sales and Trading Business from 1998 to 2004.

♦ Mr. Alvarez is a Board member of BICE Vida Compañía de Seguros S.A., where he sits on the Financial Investment

Committee and the Real Estate Investment Committee. He is also a member of the executive committee of BICE

Chileconsult Asesorías Financieras S.A. and a former member of the Boards of Securitizadora BICE S.A. and BICE

Inversiones Corredores de Bolsa S.A.

♦ Aside from his involvement in BICE, he is a member of the board of OPTE, a non-profit organization with the purpose of

improving the education of children in a vulnerable social situation.

♦ Mr. Alvarez holds a degree in Civil Industrial Engineering from the Catholic University of Chile and a Master of Science

Degree in Engineering. He attended the Financial Management Program at Stanford University in 1995 and the Advanced

Management Program at Harvard Business School in 2010.

Section 1

Investor Highlights

www.bice.cl

4

Investment Highlights

Strong bank in the Emerging Markets’ highest rated country

Strong, consistent asset quality

Conservative risk policies resulting in stability

throughout economic cycles

Experienced management team

Solid brand recognition and a key part of

Chile’s prestigious Matte Group

Section 2

Chilean Macroeconomic Highlights

www.bice.cl

6

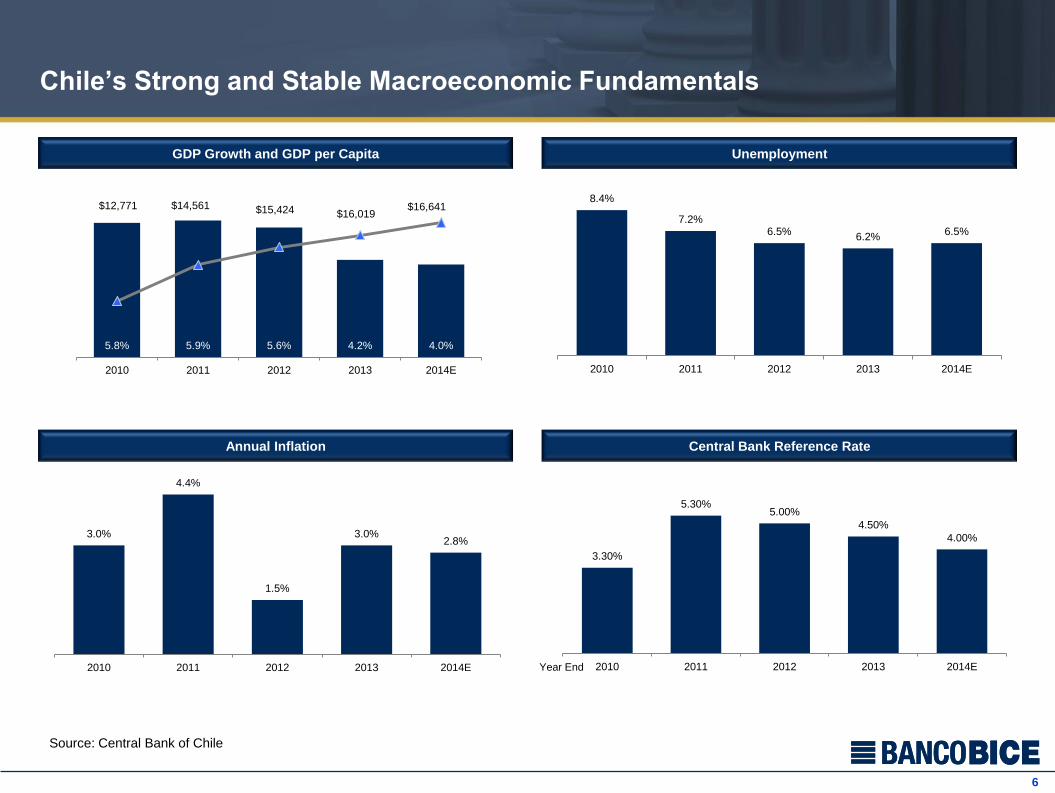

Chile’s Strong and Stable Macroeconomic Fundamentals

GDP Growth and GDP per Capita Unemployment

Annual Inflation Central Bank Reference Rate

8.4%

7.2% 6.5%

6.2% 6.5%

2010 2011 2012 2013 2014E

3.30%

5.30% 5.00%

4.50%

4.00%

2010 2011 2012 2013 2014E

Source: Central Bank of Chile

3.0%

4.4%

1.5%

3.0% 2.8%

2010 2011 2012 2013 2014E Year End

5.8% 5.9% 5.6% 4.2% 4.0%

$12,771 $14,561 $15,424 $16,019 $16,641

$10,000

$12,000

$14,000

$16,000

$18,000

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

2010 2011 2012 2013 2014E

7

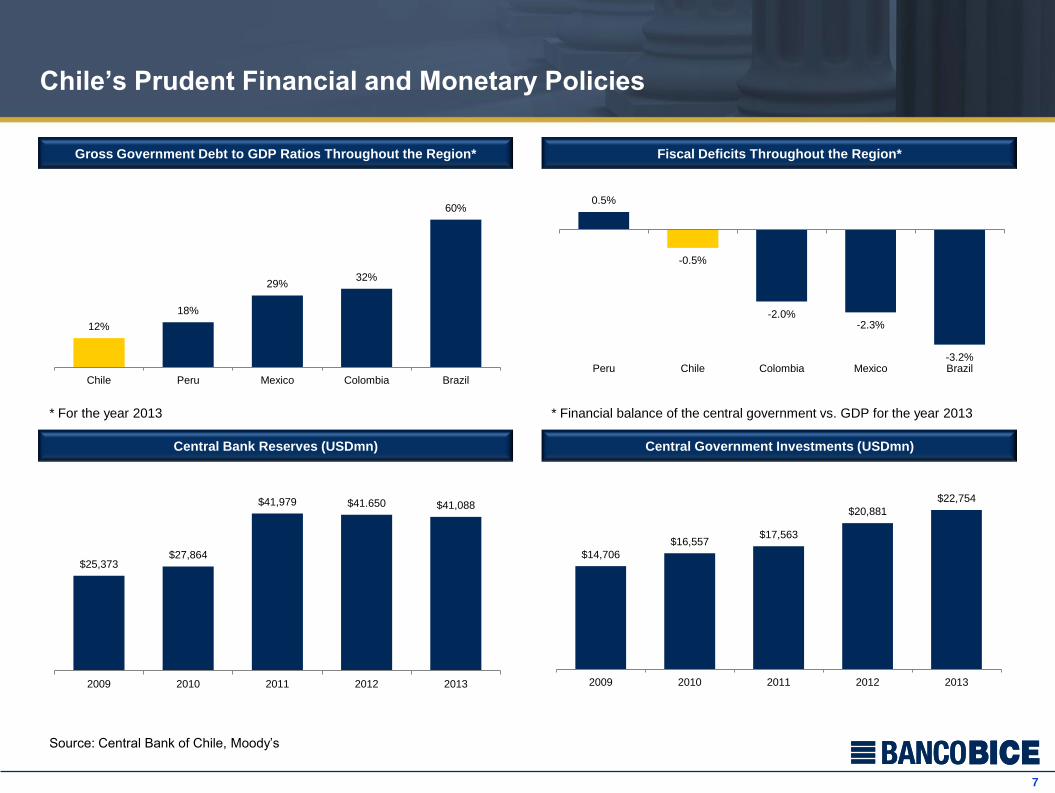

Chile’s Prudent Financial and Monetary Policies

Gross Government Debt to GDP Ratios Throughout the Region* Fiscal Deficits Throughout the Region*

Central Bank Reserves (USDmn) Central Government Investments (USDmn)

Source: Central Bank of Chile, Moody’s

$25,373 $27,864

$41,979 $41.650 $41,088

2009 2010 2011 2012 2013

12%

18%

29% 32%

60%

Chile Peru Mexico Colombia Brazil

0.5%

-0.5%

-2.0% -2.3%

-3.2% Peru Chile Colombia Mexico Brazil

* Financial balance of the central government vs. GDP for the year 2013

$14,706

$16,557 $17,563

$20,881

$22,754

2009 2010 2011 2012 2013

* For the year 2013

8

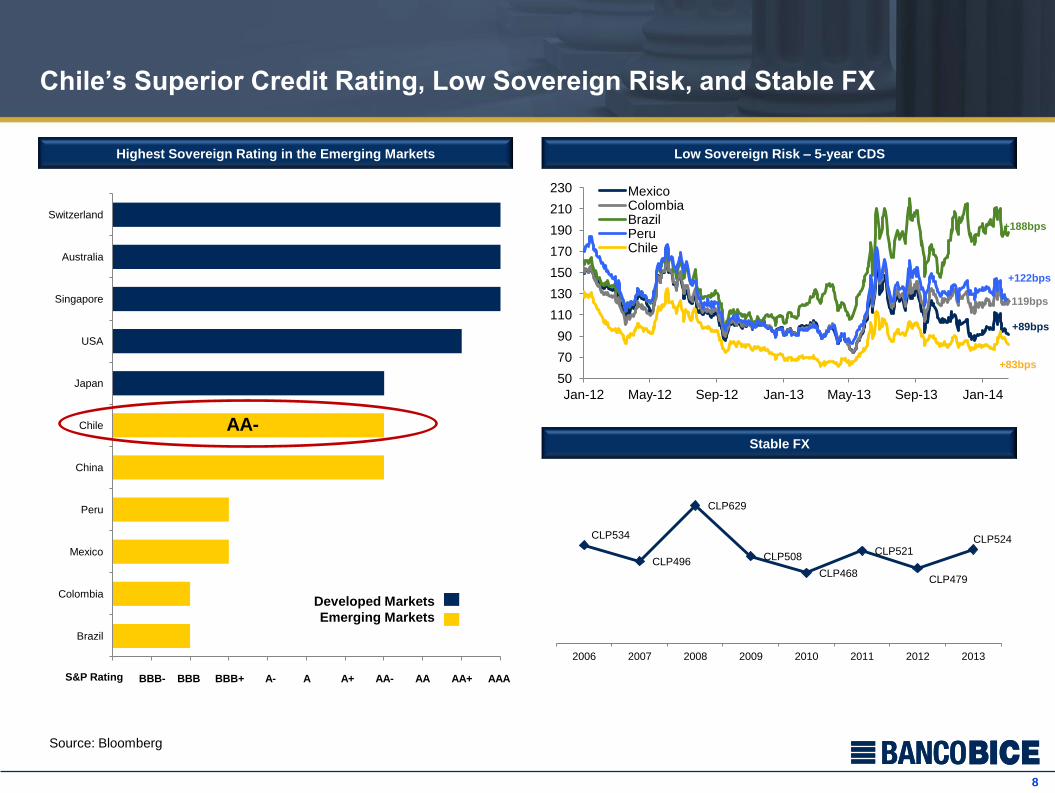

Chile’s Superior Credit Rating, Low Sovereign Risk, and Stable FX

Highest Sovereign Rating in the Emerging Markets Low Sovereign Risk – 5-year CDS

BBB- BBB BBB+ A- A A+ AA- AA AA+ AAA

Source: Bloomberg

50

70

90

110

130

150

170

190

210

230

Jan-12 May-12 Sep-12 Jan-13 May-13 Sep-13 Jan-14

Mexico Colombia Brazil Peru Chile

Brazil

Colombia

Mexico

Peru

China

Chile

Japan

USA

Singapore

Australia

Switzerland

Developed Markets

Emerging Markets

+188bps

+83bps

+89bps

+119bps

+122bps

Stable FX

CLP534

CLP496

CLP629

CLP508

CLP468

CLP521

CLP479

CLP524

2006 2007 2008 2009 2010 2011 2012 2013

AA-

S&P Rating

9

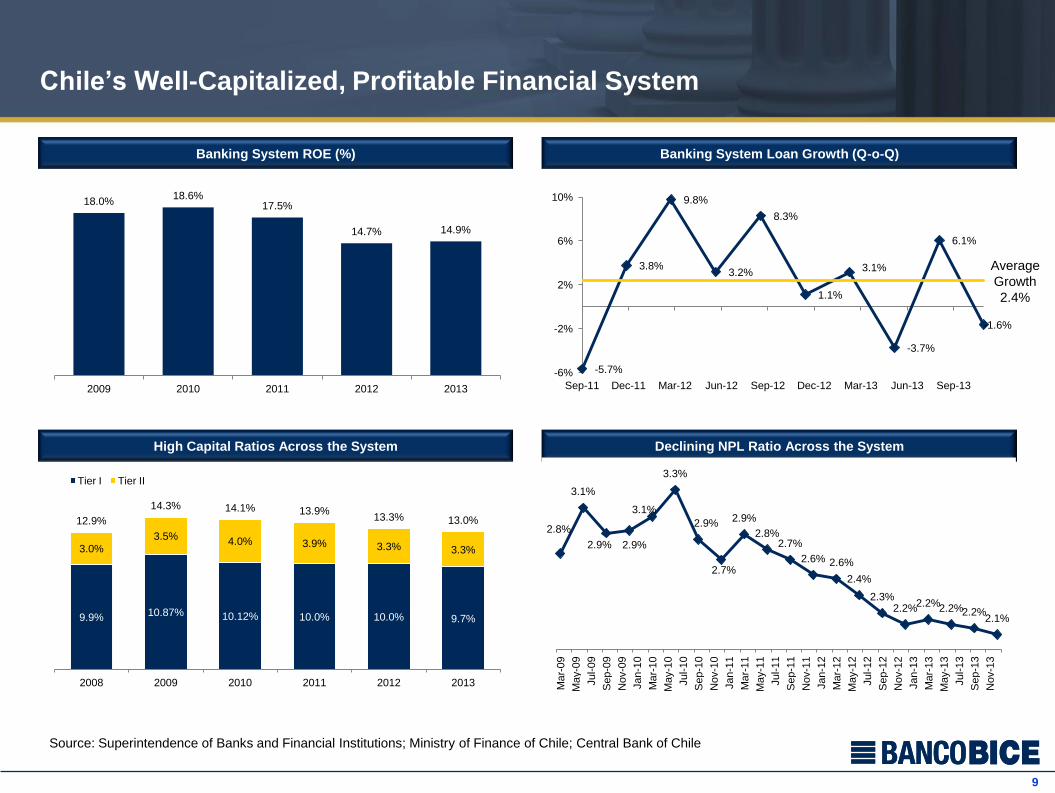

Chile’s Well-Capitalized, Profitable Financial System

Banking System ROE (%) Banking System Loan Growth (Q-o-Q)

High Capital Ratios Across the System Declining NPL Ratio Across the System

Source: Superintendence of Banks and Financial Institutions; Ministry of Finance of Chile; Central Bank of Chile

-5.7%

3.8%

9.8%

3.2%

8.3%

1.1%

3.1%

-3.7%

6.1%

-1.6%

-6%

-2%

2%

6%

10%

Sep-11 Dec-11 Mar-12 Jun-12 Sep-12 Dec-12 Mar-13 Jun-13 Sep-13

Average

Growth

2.4%

9.9% 10.87% 10.12% 10.0% 10.0% 9.7%

3.0% 3.5%

4.0% 3.9% 3.3% 3.3%

12.9%

14.3% 14.1% 13.9% 13.3% 13.0%

2008 2009 2010 2011 2012 2013

Tier I Tier II

2.8%

3.1%

2.9% 2.9%

3.1%

3.3%

2.9%

2.7%

2.9%

2.8% 2.7%

2.6% 2.6%

2.4%

2.3% 2.2%

2.2% 2.2% 2.2%

2.1%

Mar-

09

May-0

9

Jul-09

Sep-0

9

Nov-0

9

Jan-1

0

Mar-

10

May-1

0

Jul-10

Sep-1

0

Nov-1

0

Jan-1

1

Mar-

11

May-1

1

Jul-11

Sep-1

1

Nov-1

1

Jan-1

2

Mar-

12

May-1

2

Jul-12

Sep-1

2

Nov-1

2

Jan-1

3

Mar-

13

May-1

3

Jul-13

Sep-1

3

Nov-1

3

18.0% 18.6%

17.5%

14.7% 14.9%

2009 2010 2011 2012 2013

Section 3

Banco BICE Overview

www.bice.cl

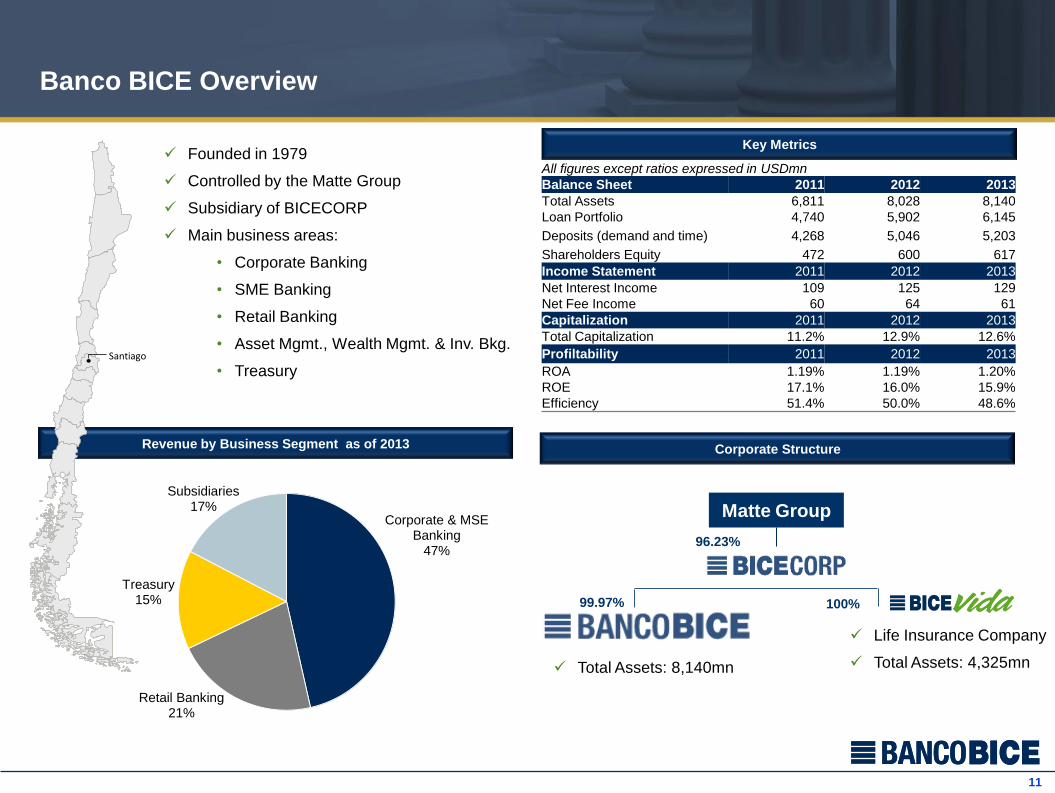

11

Corporate & MSE Banking

47%

Retail Banking 21%

Treasury 15%

Subsidiaries 17%

Banco BICE Overview

All figures except ratios expressed in USDmn

Balance Sheet 2011 2012 2013

Total Assets 6,811 8,028 8,140

Loan Portfolio 4,740 5,902 6,145

Deposits (demand and time) 4,268 5,046 5,203

Shareholders Equity 472 600 617

Income Statement 2011 2012 2013

Net Interest Income 109 125 129

Net Fee Income 60 64 61

Capitalization 2011 2012 2013

Total Capitalization 11.2% 12.9% 12.6%

Profiltability 2011 2012 2013

ROA 1.19% 1.19% 1.20%

ROE 17.1% 16.0% 15.9%

Efficiency 51.4% 50.0% 48.6%

99.97% 100%

Matte Group

96.23%

Corporate Structure

Key Metrics Founded in 1979

Controlled by the Matte Group

Subsidiary of BICECORP

Main business areas:

• Corporate Banking

• SME Banking

• Retail Banking

• Asset Mgmt., Wealth Mgmt. & Inv. Bkg.

• Treasury

Revenue by Business Segment as of 2013

Santiago

Life Insurance Company

Total Assets: 4,325mn

Total Assets: 8,140mn

12

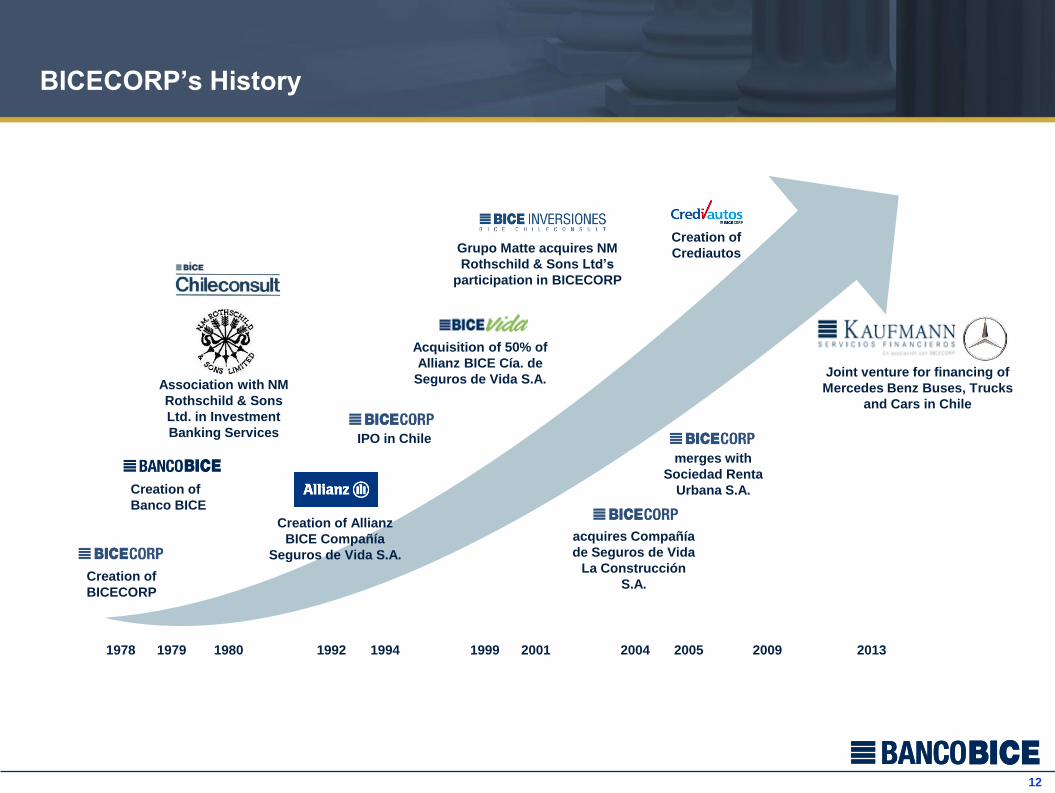

BICECORP’s History

1979

Creation of

Banco BICE

1992

Creation of Allianz

BICE Compañía

Seguros de Vida S.A.

IPO in Chile

2005

acquires Compañía

de Seguros de Vida

La Construcción

S.A.

1980

Association with NM

Rothschild & Sons

Ltd. in Investment

Banking Services

2001

Acquisition of 50% of

Allianz BICE Cía. de

Seguros de Vida S.A.

2004

Grupo Matte acquires NM

Rothschild & Sons Ltd’s

participation in BICECORP

1994

Creation of

BICECORP

1978

merges with

Sociedad Renta

Urbana S.A.

2013

Joint venture for financing of

Mercedes Benz Buses, Trucks

and Cars in Chile

2009

Creation of

Crediautos

1999

13

Key position in Chile’s Prestigious Matte Group

■ The Matte Group is among the most prestigious names in the Chilean economy, with a range of businesses in the Forestry, Energy, Telecom, Ports,

Building Materials and Financial Services sectors, among other investments.

Sector Financial Services Forestry Telecom Energy Other Investments

Description One of the most

important financial

holding companies

in Chile

Diversified pulp,

paper, and other

forestry products

Leading Chilean

Telecom company

2nd largest electricity

generator in Chile

Energy, Forestry, Conglomerate

~11% ownership

USD17.1bn Mkt. Cap

Container Port Terminals

~71% ownership

USD0.2bn Mkt. Cap

Building materials

Joint venture with Saint Gobain

~46% ownership

USD0.3bn Mkt. Cap

Processor of Molybdenum

~10% ownership

USD1.9bn Mkt. Cap

Sales

2012

LTM

USD1.2bn

USD1.3bn

USD5.0bn

USD5.0bn

USD3.0bn

USD3.1bn

USD1.4bn

USD1.7bn

EBITDA

2012

LTM

(Net Income)

USD0.2bn

USD0.2bn

USD1.0bn

USD1.0bn

USD1.1bn

USD1.0bn

USD0.3bn

USD0.4bn

Market Cap

(current) USD1.4bn USD5.3bn USD2.7bn USD4.0bn

Ownership

of the Group ~96% ~55%

~18%

(controlled through a

shareholder agreement)

~49%

14

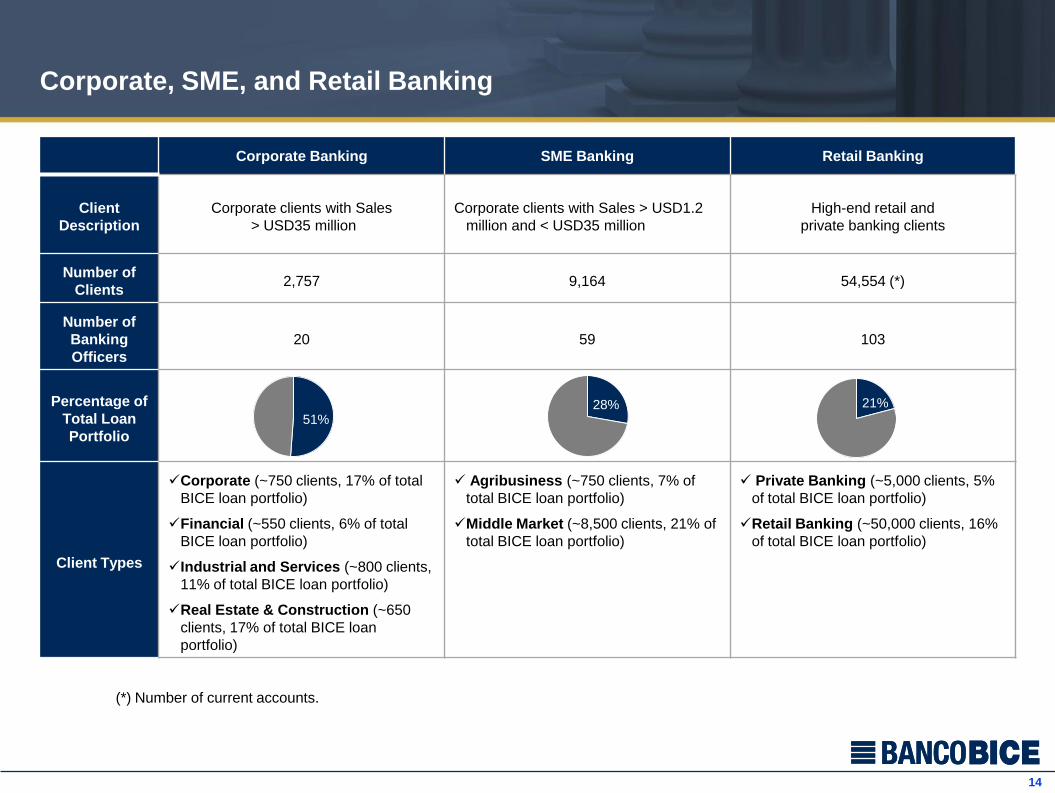

Corporate, SME, and Retail Banking

Corporate Banking SME Banking Retail Banking

Client

Description

Corporate clients with Sales

> USD35 million

Corporate clients with Sales > USD1.2

million and < USD35 million

High-end retail and

private banking clients

Number of

Clients 2,757 9,164 54,554 (*)

Number of

Banking

Officers

20 59 103

Percentage of

Total Loan

Portfolio

Client Types

Corporate (~750 clients, 17% of total

BICE loan portfolio)

Financial (~550 clients, 6% of total

BICE loan portfolio)

Industrial and Services (~800 clients,

11% of total BICE loan portfolio)

Real Estate & Construction (~650

clients, 17% of total BICE loan

portfolio)

Agribusiness (~750 clients, 7% of

total BICE loan portfolio)

Middle Market (~8,500 clients, 21% of

total BICE loan portfolio)

Private Banking (~5,000 clients, 5%

of total BICE loan portfolio)

Retail Banking (~50,000 clients, 16%

of total BICE loan portfolio)

51% 28% 21%

(*) Number of current accounts.

15

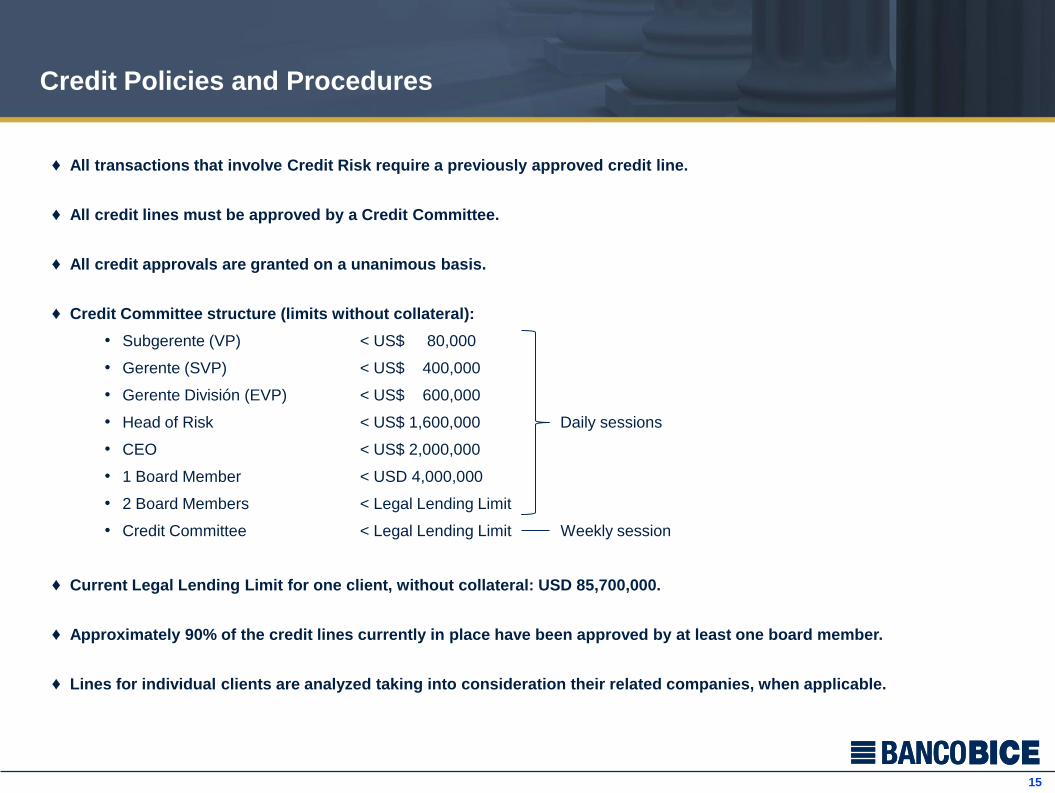

Credit Policies and Procedures

♦ All transactions that involve Credit Risk require a previously approved credit line.

♦ All credit lines must be approved by a Credit Committee.

♦ All credit approvals are granted on a unanimous basis.

♦ Credit Committee structure (limits without collateral):

• Subgerente (VP) < US$ 80,000

• Gerente (SVP) < US$ 400,000

• Gerente División (EVP) < US$ 600,000

• Head of Risk < US$ 1,600,000 Daily sessions

• CEO < US$ 2,000,000

• 1 Board Member < USD 4,000,000

• 2 Board Members < Legal Lending Limit

• Credit Committee < Legal Lending Limit Weekly session

♦ Current Legal Lending Limit for one client, without collateral: USD 85,700,000.

♦ Approximately 90% of the credit lines currently in place have been approved by at least one board member.

♦ Lines for individual clients are analyzed taking into consideration their related companies, when applicable.

16

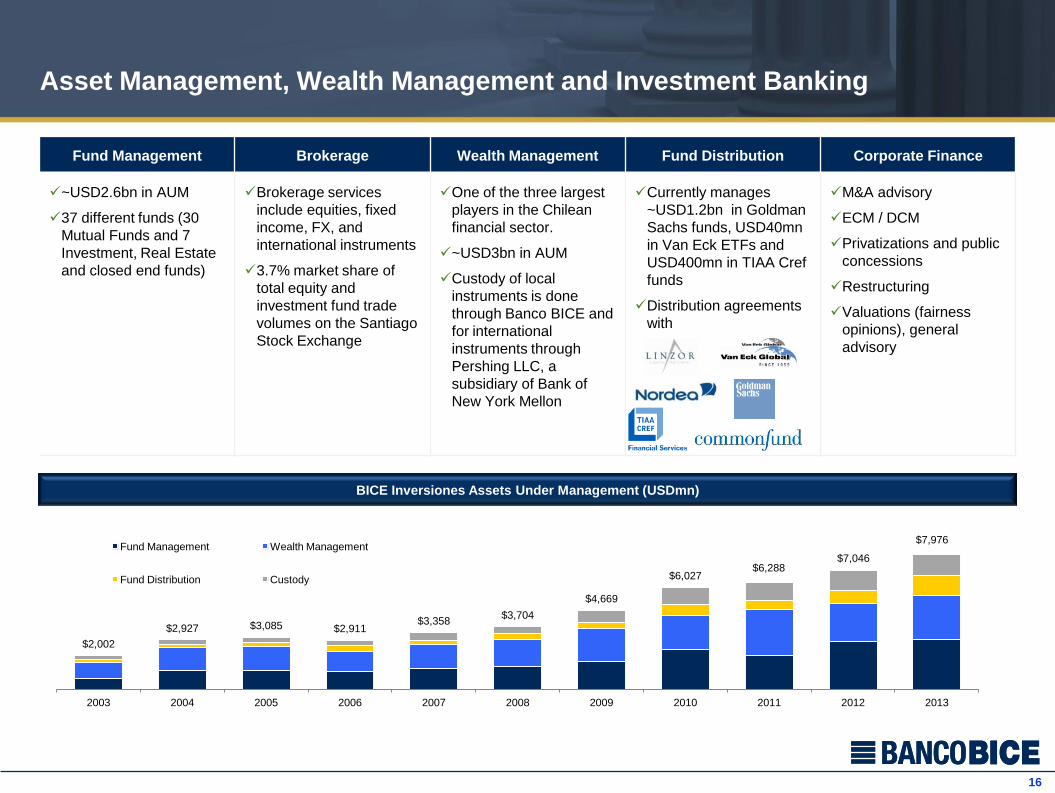

Fund Management Brokerage Wealth Management Fund Distribution Corporate Finance

~USD2.6bn in AUM

37 different funds (30

Mutual Funds and 7

Investment, Real Estate

and closed end funds)

Brokerage services

include equities, fixed

income, FX, and

international instruments

3.7% market share of

total equity and

investment fund trade

volumes on the Santiago

Stock Exchange

One of the three largest

players in the Chilean

financial sector.

~USD3bn in AUM

Custody of local

instruments is done

through Banco BICE and

for international

instruments through

Pershing LLC, a

subsidiary of Bank of

New York Mellon

Currently manages

~USD1.2bn in Goldman

Sachs funds, USD40mn

in Van Eck ETFs and

USD400mn in TIAA Cref

funds

Distribution agreements

with

M&A advisory

ECM / DCM

Privatizations and public

concessions

Restructuring

Valuations (fairness

opinions), general

advisory

Asset Management, Wealth Management and Investment Banking

BICE Inversiones Assets Under Management (USDmn)

$2,002

$2,927 $3,085 $2,911 $3,358

$3,704

$4,669

$6,027 $6,288

$7,046

$7,976

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Fund Management Wealth Management

Fund Distribution Custody

17

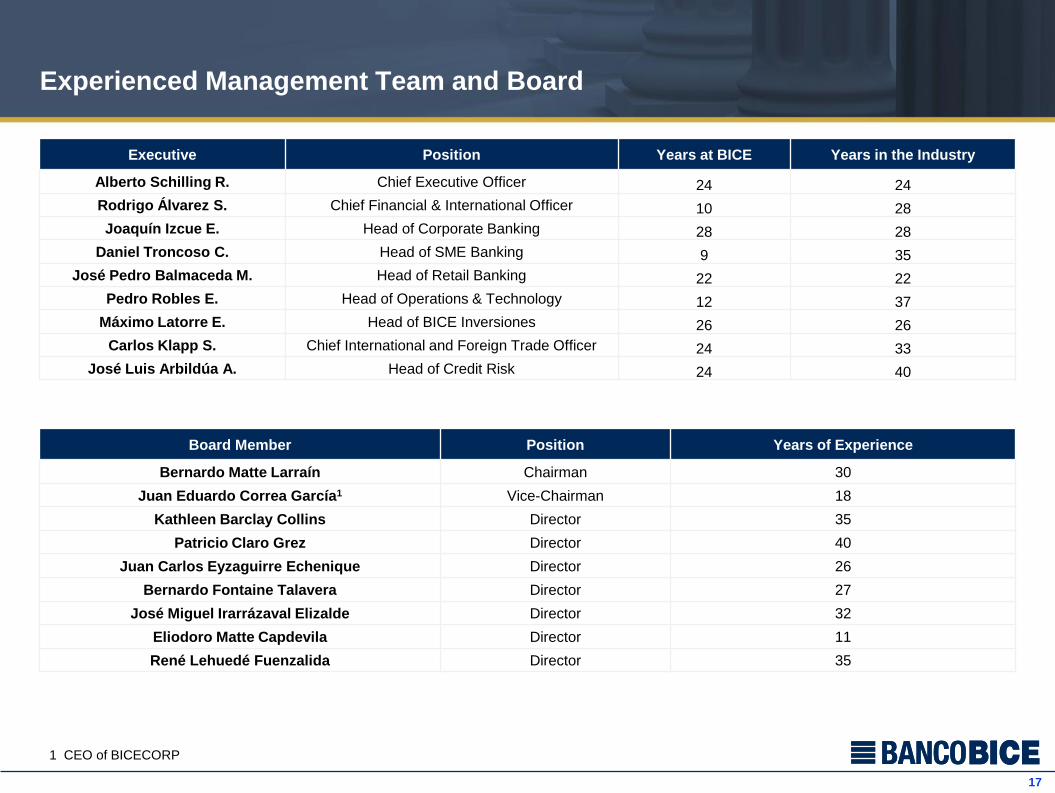

Experienced Management Team and Board

Board Member Position Years of Experience

Bernardo Matte Larraín Chairman 30

Juan Eduardo Correa García1 Vice-Chairman 18

Kathleen Barclay Collins Director 35

Patricio Claro Grez Director 40

Juan Carlos Eyzaguirre Echenique Director 26

Bernardo Fontaine Talavera Director 27

José Miguel Irarrázaval Elizalde Director 32

Eliodoro Matte Capdevila Director 11

René Lehuedé Fuenzalida Director 35

Executive Position Years at BICE Years in the Industry

Alberto Schilling R. Chief Executive Officer 24 24

Rodrigo Álvarez S. Chief Financial & International Officer 10 28

Joaquín Izcue E. Head of Corporate Banking 28 28

Daniel Troncoso C. Head of SME Banking 9 35

José Pedro Balmaceda M. Head of Retail Banking 22 22

Pedro Robles E. Head of Operations & Technology 12 37

Máximo Latorre E. Head of BICE Inversiones 26 26

Carlos Klapp S. Chief International and Foreign Trade Officer 24 33

José Luis Arbildúa A. Head of Credit Risk 24 40

1 CEO of BICECORP

Section 4

Financial Highlights

www.bice.cl

19

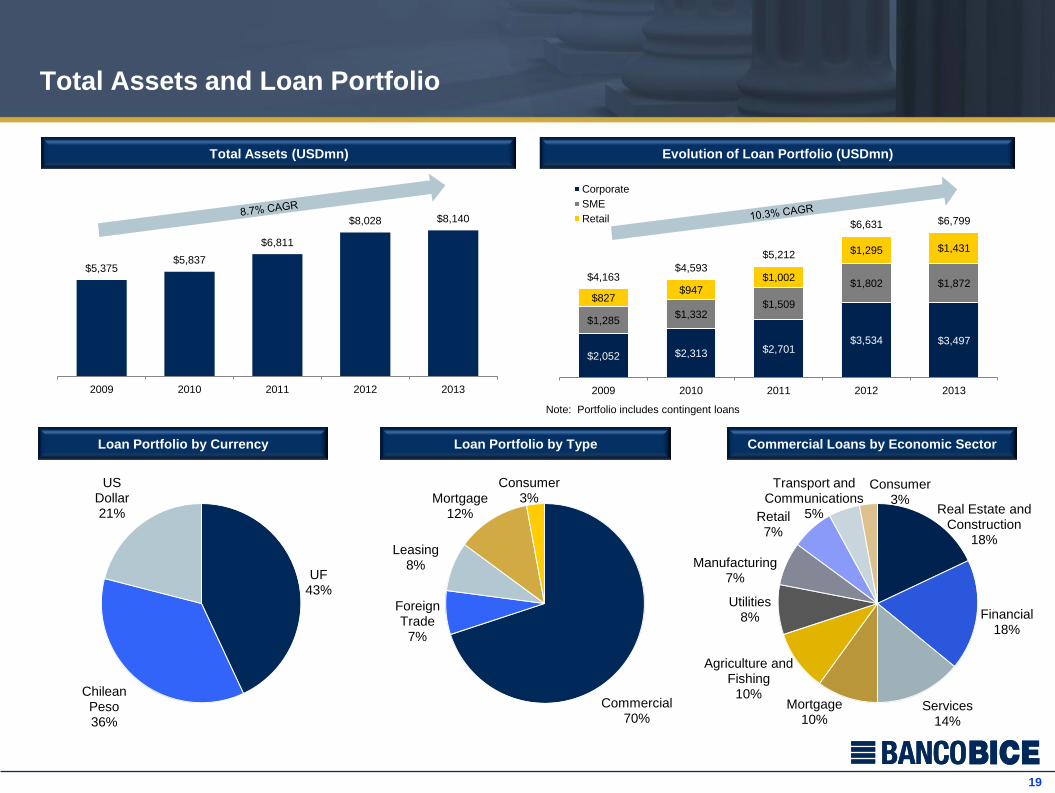

Total Assets and Loan Portfolio

Total Assets (USDmn) Evolution of Loan Portfolio (USDmn)

Real Estate and Construction

18%

Financial 18%

Services 14%

Mortgage 10%

Agriculture and Fishing

10%

Utilities 8%

Manufacturing 7%

Retail 7%

Transport and Communications

5%

Consumer 3%

Loan Portfolio by Currency Loan Portfolio by Type Commercial Loans by Economic Sector

Commercial 70%

Foreign Trade

7%

Leasing 8%

Mortgage 12%

Consumer 3%

UF 43%

Chilean Peso 36%

US Dollar 21%

$5,375 $5,837

$6,811

$8,028 $8,140

2009 2010 2011 2012 2013

$2,052 $2,313 $2,701 $3,534 $3,497

$1,285 $1,332

$1,509

$1,802 $1,872

$827 $947

$1,002

$1,295 $1,431

$4,163 $4,593

$5,212

$6,631 $6,799

2009 2010 2011 2012 2013

Corporate

SME

Retail

Note: Portfolio includes contingent loans

20

Asset Quality

Past Due Loans / Total Loans Provisions / Total Loans

Write-Offs / Total Loans Provisions / Past Due Loans

1.13%

0.76%

0.34% 0.27%

0.28%

0.0%

0.4%

0.8%

1.2%

2009 2010 2011 2012 2013

2.04% 2.16%

1.44% 1.43%

1.49%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

2009 2010 2011 2012 2013

0.12%

0.40%

0.23%

0.10%

0.06%

0.0%

0.1%

0.2%

0.3%

0.4%

0.5%

2009 2010 2011 2012 2013

1.8x

2.9x

5.6x

7.0x

6.9x

x

2x

4x

6x

8x

2009 2010 2011 2012 2013

21

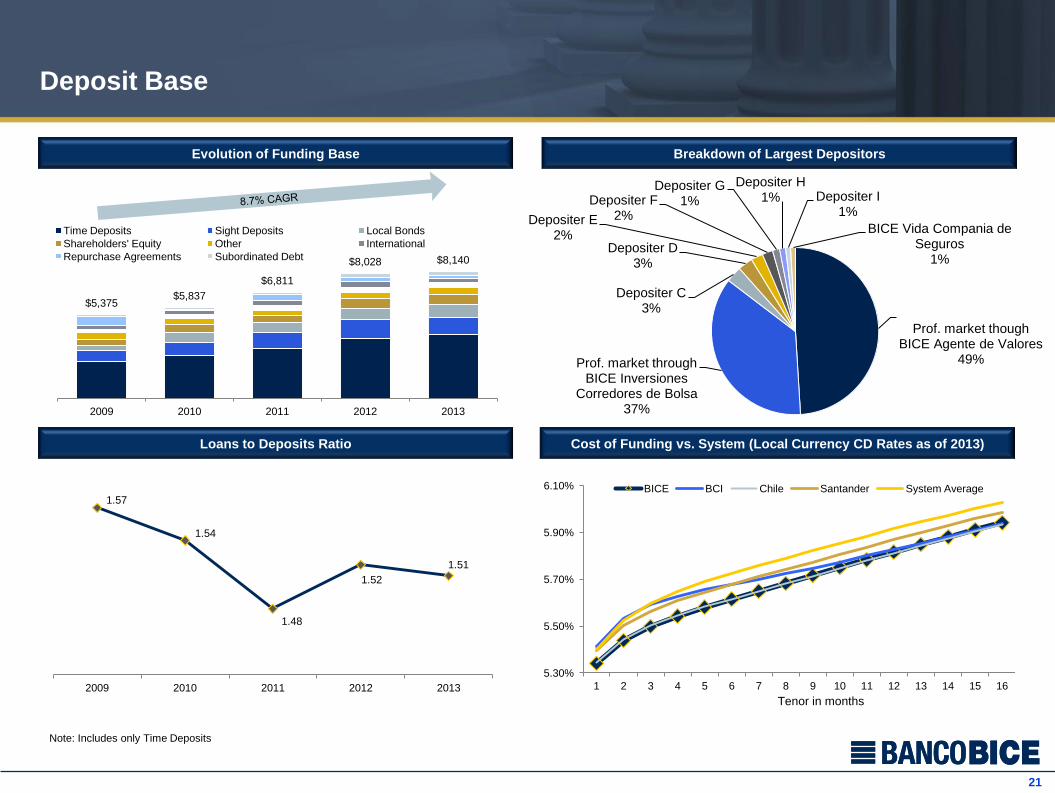

5.30%

5.50%

5.70%

5.90%

6.10%

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

BICE BCI Chile Santander System Average

$5,375 $5,837

$6,811

$8,028 $8,140

2009 2010 2011 2012 2013

Time Deposits Sight Deposits Local Bonds

Shareholders' Equity Other International

Repurchase Agreements Subordinated Debt

Deposit Base

Evolution of Funding Base Breakdown of Largest Depositors

Loans to Deposits Ratio Cost of Funding vs. System (Local Currency CD Rates as of 2013)

Prof. market though BICE Agente de Valores

49% Prof. market through BICE Inversiones

Corredores de Bolsa 37%

Depositer C 3%

Depositer D 3%

Depositer E 2%

Depositer F 2%

Depositer G 1%

Depositer H 1% Depositer I

1%

BICE Vida Compania de Seguros

1%

Tenor in months

Note: Includes only Time Deposits

1.57

1.54

1.48

1.52

1.51

2009 2010 2011 2012 2013

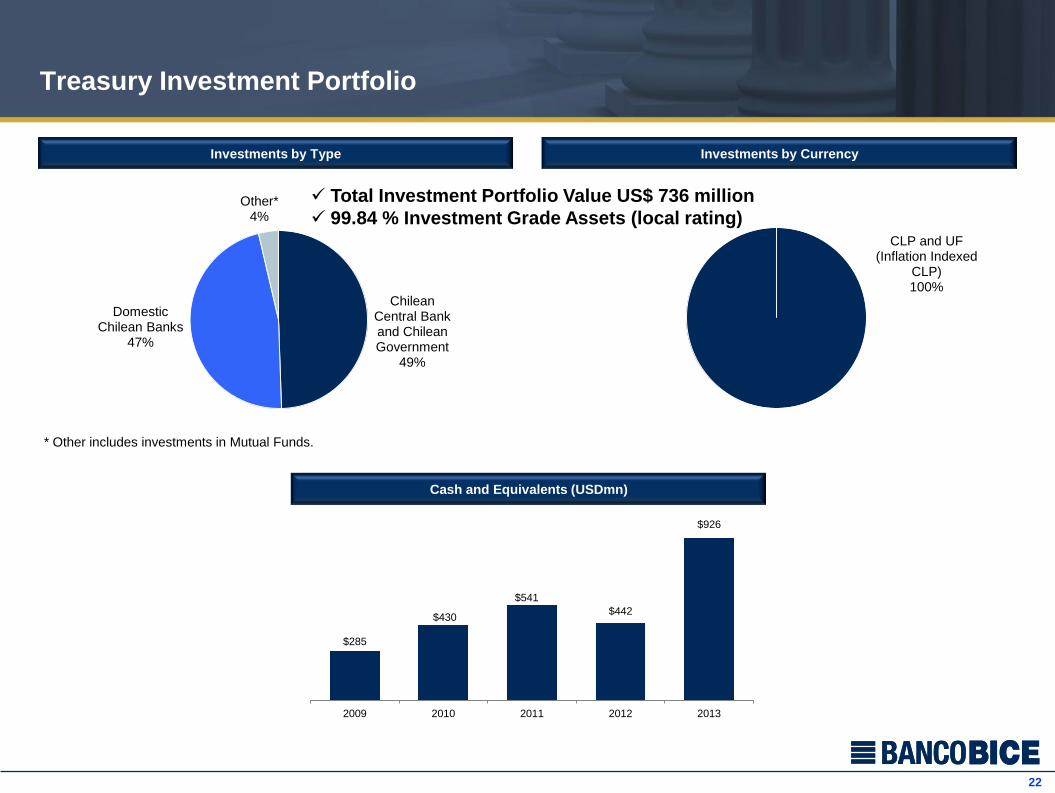

22

$285

$430

$541

$442

$926

2009 2010 2011 2012 2013

Treasury Investment Portfolio

Investments by Type Investments by Currency

Total Investment Portfolio Value US$ 736 million

99.84 % Investment Grade Assets (local rating)

Chilean Central Bank and Chilean Government

49%

Domestic Chilean Banks

47%

Other* 4%

* Other includes investments in Mutual Funds.

Cash and Equivalents (USDmn)

CLP and UF (Inflation Indexed

CLP) 100%

23

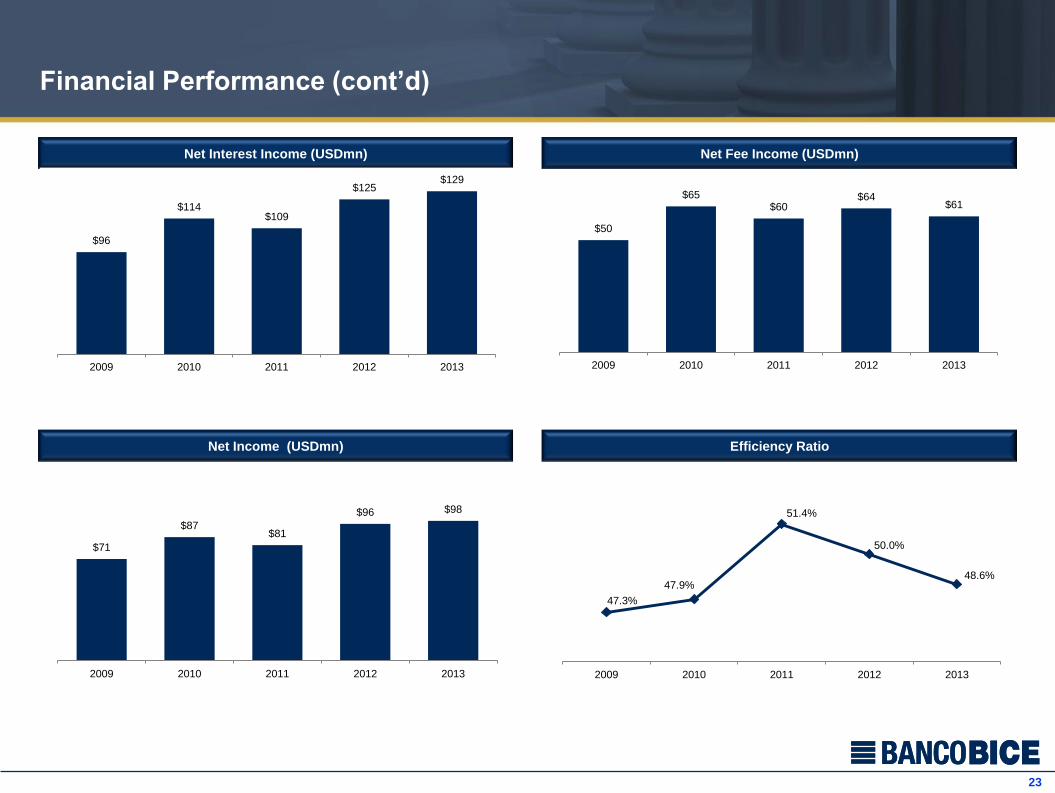

Financial Performance (cont’d)

Net Interest Income (USDmn) Net Fee Income (USDmn)

Net Income (USDmn) Efficiency Ratio

47.3%

47.9%

51.4%

50.0%

48.6%

2009 2010 2011 2012 2013

$50

$65 $60

$64 $61

2009 2010 2011 2012 2013

$96

$114 $109

$125 $129

2009 2010 2011 2012 2013

$71

$87 $81

$96 $98

2009 2010 2011 2012 2013

24

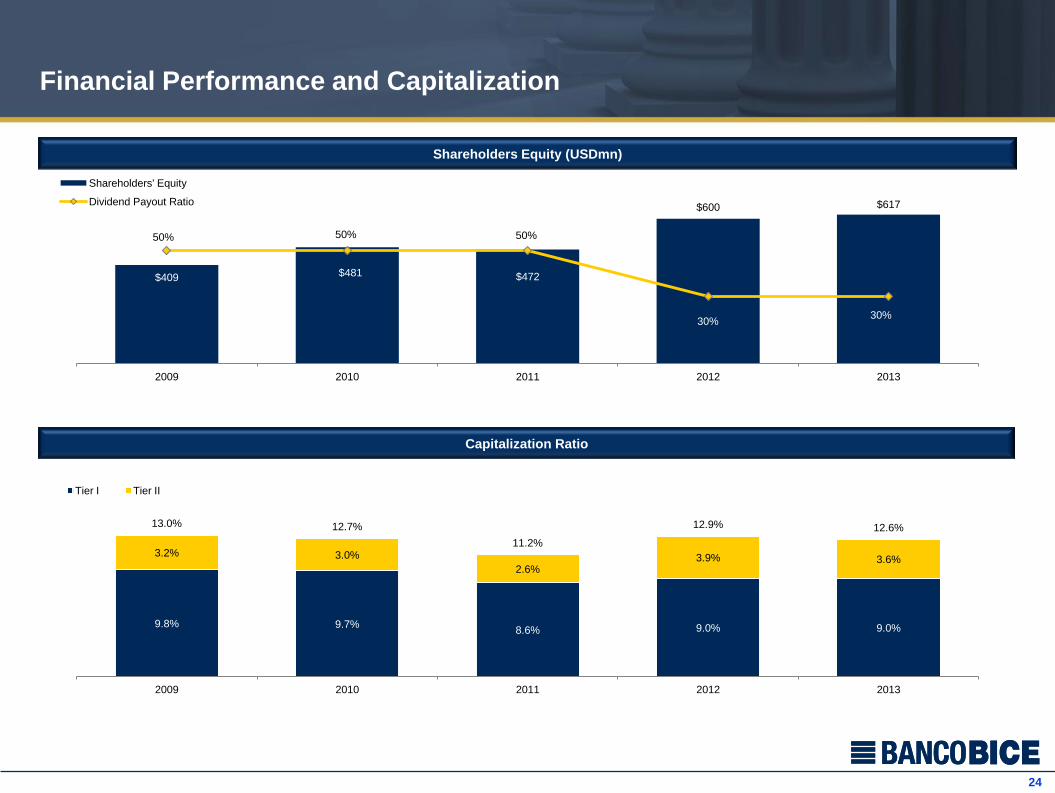

Financial Performance and Capitalization

Shareholders Equity (USDmn)

Capitalization Ratio

$409 $481 $472

$600 $617

50% 50% 50%

30% 30%

0%

25%

50%

75%

0

100

200

300

400

500

600

700

2009 2010 2011 2012 2013

Shareholders' Equity

Dividend Payout Ratio

9.8% 9.7% 8.6% 9.0% 9.0%

3.2% 3.0%

2.6% 3.9% 3.6%

13.0% 12.7%

11.2%

12.9% 12.6%

2009 2010 2011 2012 2013

Tier I Tier II

25

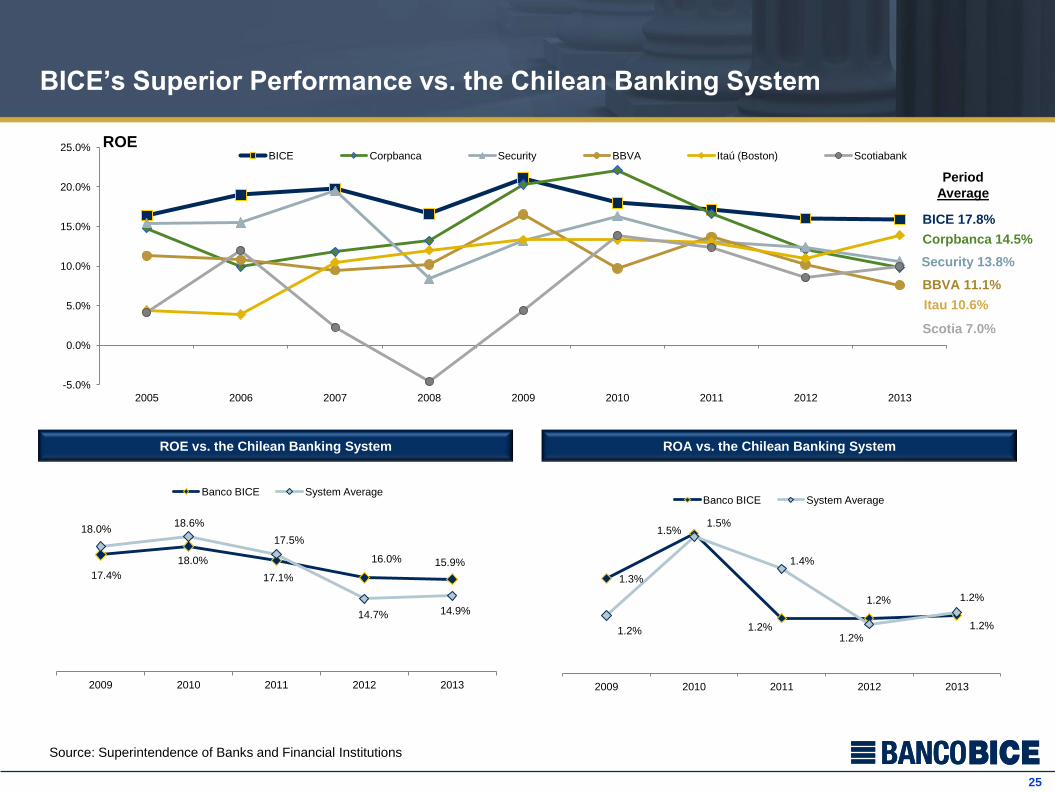

BICE’s Superior Performance vs. the Chilean Banking System

ROE vs. the Chilean Banking System ROA vs. the Chilean Banking System

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

2005 2006 2007 2008 2009 2010 2011 2012 2013

BICE Corpbanca Security BBVA Itaú (Boston) Scotiabank

Source: Superintendence of Banks and Financial Institutions

BICE 17.8%

Itau 10.6%

Security 13.8%

BBVA 11.1%

Scotia 7.0%

Corpbanca 14.5%

Period

Average

17.4%

18.0%

17.1%

16.0% 15.9%

18.0% 18.6%

17.5%

14.7% 14.9%

2009 2010 2011 2012 2013

Banco BICE System Average

ROE

1.3%

1.5%

1.2%

1.2%

1.2% 1.2%

1.5%

1.4%

1.2%

1.2%

2009 2010 2011 2012 2013

Banco BICE System Average

Thank You

www.bice.cl