Embed Size (px)

Citation preview

INVESTOR PRESENTATIONF e br u a r y 2 0 1 8

R-City Ghatkopar, Mumbai

Disclaimer

2

This presentation and the following discussion may contain “forward looking statements” by Inox Leisure Limited (“ILL” or “theCompany”) that are not historical in nature. These forward looking statements, which may include statements relating to future stateof affairs, results of operations, financial condition, business prospects, plans and objectives, are based on the current beliefs,assumptions, expectations, estimates, and projections of the management of ILL about the business, industry and markets in which ILLoperates.

These statements are not guarantees of future performance, and are subject to known and unknown risks, uncertainties, and otherfactors, some of which are beyond ILL’s control and difficult to predict, that could cause actual results, performance or achievementsto differ materially from those in the forward looking statements.

Such statements are not, and should not be construed, as a representation as to future performance or achievements of ILL. Inparticular, such statements should not be regarded as a projection of future performance of ILL. It should be noted that the actualperformance or achievements of ILL may vary significantly from such statements.

Due to rounding-off, figures presented throughout this document may not add up precisely to the totals provided and percentagesmay not precisely reflect the rounded-off figures.

All financial figures, upto and including FY15 are as per IGAAP and for FY16 and thereafter are as per IND-AS. Revenues for FY13 toFY15 are shown net of entertainment tax, to be consistent with the revenues under IND-AS for FY16 and FY17

3

D I S C U S S I O N S U M M A R Y

I N D U S T R Y O V E R V I E W

C O M P A N Y O V E R V I E W

C O M P E T I T I V E A D V A N T A G E & O U T L O O K

A N N E X U R E

Atria, Worli, Mumbai

4

INDUSTRY OVERVIEW

CR2, Nariman Point, Mumbai

Strong Fundamentals & Huge Growth Potential

5

125

95 80

60 57 40

26 25 16 12 10 8

US France Spain UK Germany South Korea Japan Taiwan China Thailand Brazil India

H o w e v e r , I n d i a ’ s S c r e e n D e n s i t y i s O n e o f t h e L o w e s t

Screens / Million population

Source: CRISIL Report, http://uis.unesco.org/en/news/cinema-data-release (2015)

2,178 1,930

1,364

208 197 176 171 169 156 146

China India US France Mexico UK Japan S. Korea Germany Russia

2 n d H i g h e s t N u m b e r O f T h e a t r e F o o t f a l l s i n t h e W o r l d

Footfalls in Million2,000

791686

581

300 298 269 255 226 185

-4 00

100

600

1,10 0

1,60 0

2,10 0

India US China Japan France UK S. Korea Spain Germany Italy

H i g h e s t N u m b e r o f F i l m P r o d u c e d i n t h e W o r l d

Steady Performance and Resilience

6

85.1 93.4 93.5 101.4 99.8 106.6 111.8 117.9 124.2 131.2

112.4125.3 126.4

138.1 142.4155.0

166.0178.2

191.6206.6

0

50

100

150

200

250

2012 2013 2014 2015 2016 2017E 2018E 2019E 2020E 2021E

Domestic Theatrical Overseas Theatrical Home Video Cable & Satellite Rights Ancilliary Revenue Streams

In Rs. Billion

CAGR 6.1%

CAGR 7.7%

I n d i a n F i l m I n d u s t r y D i s p l a y s S t e a d y P e r f o r m a n c e T r e n d s

D o m e s t i c T h e a t r i c a l s C o n s t i t u t e s 7 0 % O f T o t a l F i l m I n d u s t r y

Source: FICCI-KPMG 2017 Report

70%

8%

1%

11%

11%

Domestic Theatrical

Overseas Theatrical

Home Video

Cable & Satellite Rights

Ancillary Revenue Streams

2016

Multiplexes Witnessing Rapid Growth

7

FACTORS DRIVING GROWTH IN

MULTIPLEXES:

Strong demographics, rising disposable

incomes and discretionary spends.

Superior location, destination and

parking facilities.

Multiple screens in one location offer a

wider variety of content to the patrons.

Different screen sizes provide

programming flexibility. This results in

higher occupancy ratios.

State of art equipment (high quality

video and audio), superior interiors,

ambience and service.

Source: CRISIL Report, FICCI-KPMG Report 2017, Industry Sources, Internal Estimates

M u l t i p l e x e s c u r r e n t l y a c c o u n t f o r ~ 3 0 % m a r k e t s h a r e o f t h e s c r e e n s ,

h o w e v e r t h e y a c c o u n t f o r m o r e t h a n 4 5 % o f b o x o f f i c e

c o l l e c t i o n s

Number of Screens

9,3

08

9,1

21

8,6

85

8,4

51

8,0

02

6,0

00

6,0

00

6,0

00

1,0

75

1,2

25

1,3

50

1,5

00

1,6

30

2,1

34

2,2

25

2,5

13

-

1,00 0

2,00 0

3,00 0

4,00 0

5,00 0

6,00 0

7,00 0

8,00 0

9,00 0

10,0 00

2010 2011 2012 2013 2014 2015 2016 Feb18

Single Screens Multiplexes

Increasing Number Of INR 1bn + Movies

8

1,000 1,598

2,065 2,101 2,638 3,014

3,446 3,359

5,200 4,500

5,300

6,500

3 Idiots(2009)

Dabaang(2010)

Bodyguard(2011)

Ek Tha Tiger(2012)

Dabaang 2(2012)

ChennaiExpress(2013)

Dhoom 3(2013)

Kick(2014)

P.K(2014)

BajrangiBhaijaan(2015)

Dangal(2016)

Bahubali 2 -The

Conclusion(2017)

1 2

5

9 6 7

5 8 7

1

2 1

1

- 3

- --

-

-- 1

1

2 2

2008 2009 2010 2011 2012 2013 2014 2015 2016 Jan-17 to Feb-18

INR 1Bn to 1.99Bn INR 2Bn to 2.99 Bn INR 3Bn and above

Wider Screen Releases

Higher Number Of INR 1 Bn + Movies

INCREASING NUMBER OF

MOVIES ARE GENERATING MORE

THAN RS 1 BN IN NET BOX OFFICE

COLLECTIONS DRIVEN BY WIDER

SCREEN RELEASES AND

FACILITATED BY DIGITISATION OF

CONTENT DELIVERY

Source: Industry

I n d i a ’ s C o n s u m p t i o n S t o r y

9

Target Audience (Middle & Affluent Class) is estimated to grow from 268 million in 2015 to 614 million in 2025

As much as 70% of household income will be spent on discretionary spending in 2025

Source: Mckinsey - Tracking the growth of Indias Middle Class - 2017

6148 39 30

3952 61 70

1995 2005 2015 2025

Necessities Discretionary

%Share of Average Annual Household Consumption

%Share of Population by Income Bracket

9380

54

3522

618

41

43

36

1 25

22

42

0

10

20

30

40

50

60

70

80

90

100

1985 1995 2005 2015 2025

Lower Class Lower Middle Class Middle & Affluent Class

755 928

1,107 1,278

1,429

-

200

400

600

800

1,00 0

1,20 0

1,40 0

1,60 0

1985 1995 2005 2015 2025

Population of India (Million)

Based on Annual Household Income• Lower Class: < Rs.90,000• Lower Middle Class: Rs.90,000 to Rs.199,999• Middle & Affluent Class: > Rs.200,000

10

Company Overview

Atria, Worli, Mumbai

Track Record of Aggressive Expansion

11

8 12 25 35 5176 91

119

239 257 279310

372420

468 488

2 3 6 9 1422 26 32

63 68 72 7996

107118 122

-50

-30

-10

10

30

50

70

90

110

130

0

100

200

300

400

500

600FY

03

FY04

FY05

FY06

FY0

7

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY1

7

Feb

-18

Screens Properties

Note: Includes Acquisition of 89 Cinemas in FY07, Fame in FY11 and Satyam in FY15

ON AN AVERAGE ADDITION OF 3 SCREENS EVERY MONTH SINCE INCEPTION

PAN India Presence

12

ONE OF THE LARGEST MULTIPLEX CHAIN OPERATOR IN INDIA

* Includes 8 management properties with 29 screens and 7,370 seats

KERALA |1 Property | 6 Screens

19States

60Cities

122Properties

488Screens

121,281Seats

JHARKHAND | 1 Property | 4 Screens

WEST BENGAL | 14 Properties | 55 Screens

ODISHA | 1 Property | 3 Screens

CHHATTISGARH | 2 Properties | 8 Screens

TELANGANA | 2 Properties | 11 Screens

ANDHRA PRADESH | 7 Properties | 28 ScreensKARNATAKA |10 Properties | 40 Screens

GOA | 4 Properties | 14 Screens

MAHARASHTRA | 27 Properties | 118 Screens

GUJARAT | 16 Properties | 67 Screens

MADHYA PRADESH | 4 Properties | 16 Screens

RAJASTHAN | 13 Properties | 43 Screens

HARYANA | 5 Properties | 16 Screens

TAMIL NADU | 3 Properties | 14 Screens

UTTAR PRADESH | 6 Properties | 24 Screens

DELHI | 4 Properties | 13 Screens

PUNJAB | 1 Property | 6 Screens

Assam | 1 Property | 2 Screens

13

Introducing the ‘THEATRE OF DREAMS’…

INOX INSIGNIA at Atria Mall, Worli Mumbai

• Theatres with opulent recliners

• Personalized ticketing and butler-on-call

• Gourmet Menu curated by Celebrity Chef Vicky Ratnani

• Staff Uniforms crafted by Arjun Khanna

• Live food counter serving gourmet delights

• A new level of luxury paired with bespoke interiors

• Laser projection with Dolby Atmos Sound and 3D

powered by Volfoni systems

14

Introducing the all new 7 STAR

METRO INOX MUMBAI’S GREATEST LOVE STORY…

• 6 Screens, 1271 seats

• Mumbai’s first kids theatre - KIDDLES

• Cafe UNWIND

• Advanced 4K Projection

• Augmented Reality

• Dolby Atmos

• Volfoni 3D

15

Atria, Worli, Mumbai

16

GVK One, Hyderabad

17

CR2, Nariman Point, Mumbai

18

Mantri Square, Bangalore

19

Quest, Kolkata

20

INSIGNIA – LUXURY MOVIE

WATCHING EXPERIENCE

R-City Ghatkopar, Mumbai

21

Atria, Worli, Mumbai

22

R-City, Ghatkopar, Mumbai

23

Mantri Square, Bangalore

24

Amanora, Pune

25

VR Surat, Surat

26

Bund Garden, Pune

R e v e n u e f r o m O p e r a t i o n s

27All figures in INR Crs., unless specified

298.0

325.9

280 .0

285 .0

290 .0

295 .0

300 .0

305 .0

310 .0

315 .0

320 .0

325 .0

330 .0

Q3FY17 Q3FY18

9%

10%

932.2

1,024.5

880 .0

900 .0

920 .0

940 .0

960 .0

980 .0

1,00 0.0

1,02 0.0

1,04 0.0

9MFY17 9MFY18

663.2 762.8

895.4

1,160.6 1,220.7

FY13 FY14 FY15 FY16 FY17

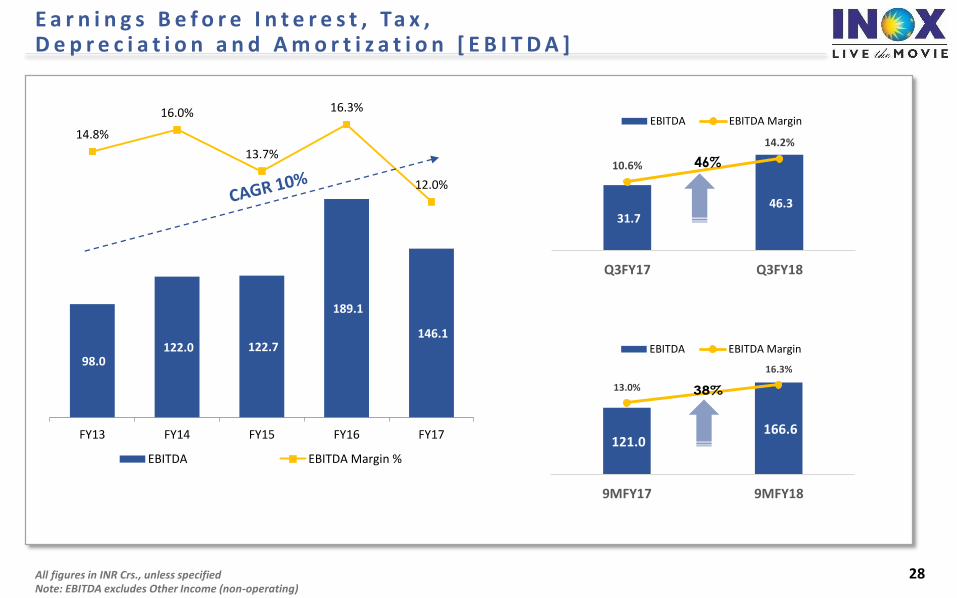

E a r n i n g s B e f o r e I n t e r e s t , Ta x ,D e p r e c i a t i o n a n d A m o r t i z a t i o n [ E B I T D A ]

28All figures in INR Crs., unless specified

98.0 122.0 122.7

189.1

146.1

14.8%

16.0%

13.7%

16.3%

12.0%

0.0 %

2.0 %

4.0 %

6.0 %

8.0 %

10. 0%

12. 0%

14. 0%

16. 0%

18. 0%

FY13 FY14 FY15 FY16 FY17

EBITDA EBITDA Margin %

31.7 46.3

10.6%

14.2%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

Q3FY17 Q3FY18

EBITDA EBITDA Margin

46%

121.0 166.6

13.0%

16.3%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

-

20.0

40.0

60.0

80.0

100 .0

120 .0

140 .0

160 .0

180 .0

9MFY17 9MFY18

EBITDA EBITDA Margin

38%

Note: EBITDA excludes Other Income (non-operating)

P r o f i t a f t e r t a x [ PAT ]

29All figures in INR Crs., unless specified

18.5

36.9

20.0

81.0

30.6

2.8%

4.8%

2.2%

7.0%

2.5%

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

FY13 FY14 FY15 FY16 FY17

PAT PAT Margin %

3.8

13.2 1.3%

4.0%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

Q3FY17 Q3FY18

PAT PAT Margin

251%

88%

30.3

56.9

3.2%

5.6%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

-

10.0

20.0

30.0

40.0

50.0

60.0

9MFY17 9MFY18

PAT PAT Margin

R e v e n u e s - S e g m e n t B r e a k u p

30All figures in INR Crs., unless specified

456.7 490.5 551.6 712.8 748.1

141.8 162.3

191.0

265.6 284.1

32.4 49.5

81.5

91.0 96.2

32.3 60.4

71.2

91.1 92.3

-

200 .0

400 .0

600 .0

800 .0

1,00 0.0

1,20 0.0

1,40 0.0

FY13 FY14 FY15 FY16 FY17

NBOC F & B Advertising Others

895.4

1160.61220.7

663.2

762.8176.4 187.9

67.673.1

30.240.323.724.6298.0

325.9

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

Q3FY17 Q3FY18

3.9%

33.3%

8.2%

6.5%

569.4 612.7

218.4228.4

75.3105.769.177.7932.2

1024.5

0.0

200.0

400.0

600.0

800.0

1000.0

1200.0

9MFY17 9MFY18

12.4%

40.4%

4.6%

7.6%

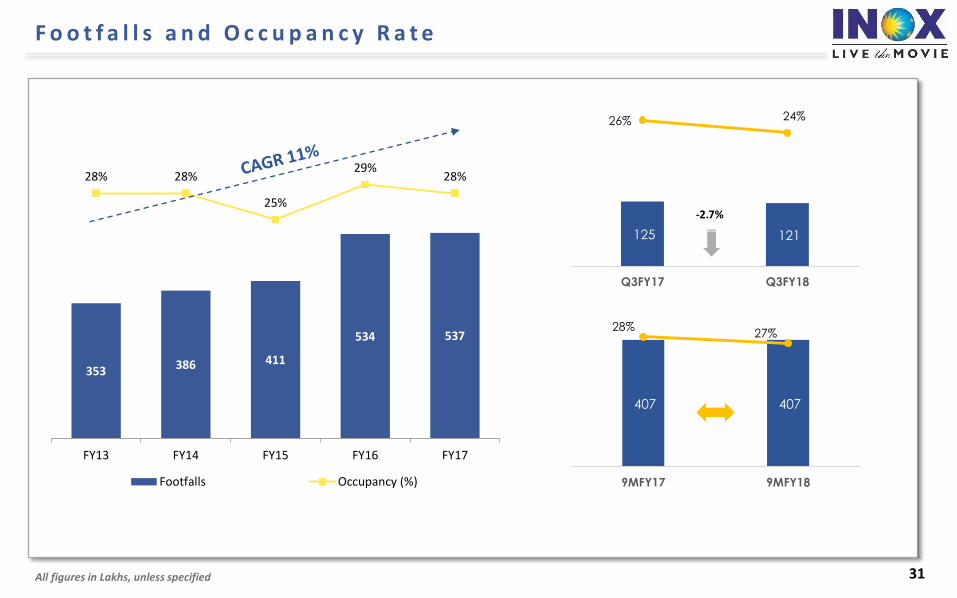

F o o t f a l l s a n d O c c u p a n c y R a t e

31

353 386 411

534 537

28% 28%

25%

29%28%

0%

5%

10%

15%

20%

25%

30%

35%

FY13 FY14 FY15 FY16 FY17

Footfalls Occupancy (%)

All figures in Lakhs, unless specified

125 121

26% 24%

3%

8%

13%

18%

23%

28%

-

50

100

150

200

250

300

Q3FY17 Q3FY18

-2.7%

407 407

28%27%

3%

8%

13%

18%

23%

28%

33%

-

50

100

150

200

250

300

350

400

450

500

9MFY17 9MFY18

A v e r a g e T i c k e t P r i c e [ AT P ]

32

160156

164

170

178

FY13 FY14 FY15 FY16 FY17

All figures in INR, unless specified

182

199

170

175

180

185

190

195

200

205

Q3FY17 Q3FY18

9.6%

179

193

170

175

180

185

190

195

9MFY17 9MFY18

7.3%

S p e n d P e r H e a d [ S P H ]

33

47 4955 58 62

FY13 FY14 FY15 FY16 FY17

All figures in INR, unless specified

63 70

-

10

20

30

40

50

60

70

80

90

100

Q3FY17 Q3FY18

63 66

-

10

20

30

40

50

60

70

80

90

100

9MFY17 9MFY18

10.5%

5.5%

F & B a n d S P H C o n t r i b u t i o n

34

70.0%71.3%

74.1% 75.0% 76.0%

33 35

41 44

47

-

5

10

15

20

25

30

35

40

45

60. 0%

62. 0%

64. 0%

66. 0%

68. 0%

70. 0%

72. 0%

74. 0%

76. 0%

78. 0%

FY13 FY14 FY15 FY16 FY17

F & B Contribution (%) SPH Contribution (Rs.)

76.1% 75.8%

48 53

60.0%

62.0%

64.0%

66.0%

68.0%

70.0%

72.0%

74.0%

76.0%

78.0%

Q3FY17 Q3FY18

-

10

20

30

40

50

F&B Net Contribution(%) SPH Contribution (Rs.)

10.1%

75.8% 76.0%

48 50

60.0%

62.0%

64.0%

66.0%

68.0%

70.0%

72.0%

74.0%

76.0%

78.0%

9MFY17 9MFY18

-

10

20

30

40

50

F&B Net Contribution(%) SPH Contribution (Rs.)

5.7%

A d v e r t i s e m e n t I n c o m e p e r s c r e e n

35

13.8

18.5

25.1 24.6 22.4

FY13 FY14 FY15 FY16 FY17

All figures in INR Lakhs, unless specified

30.2

40.3

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

Q3FY17 Q3FY18

33.3%

75.3

105.7

-

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

100.0

9MFY17 9MFY18

40.4%

e

O t h e r O p e r a t i n g I n c o m e P e r S c r e e n

36

13.7

22.5 21.9 24.6

22.7

FY13 FY14 FY15 FY16 FY17

All figures in INR Lakhs, unless specified

23.7 24.6

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

Q3FY17 Q3FY18

3.9%

69.1 77.7

-

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

100.0

9MFY17 9MFY18

12.4%

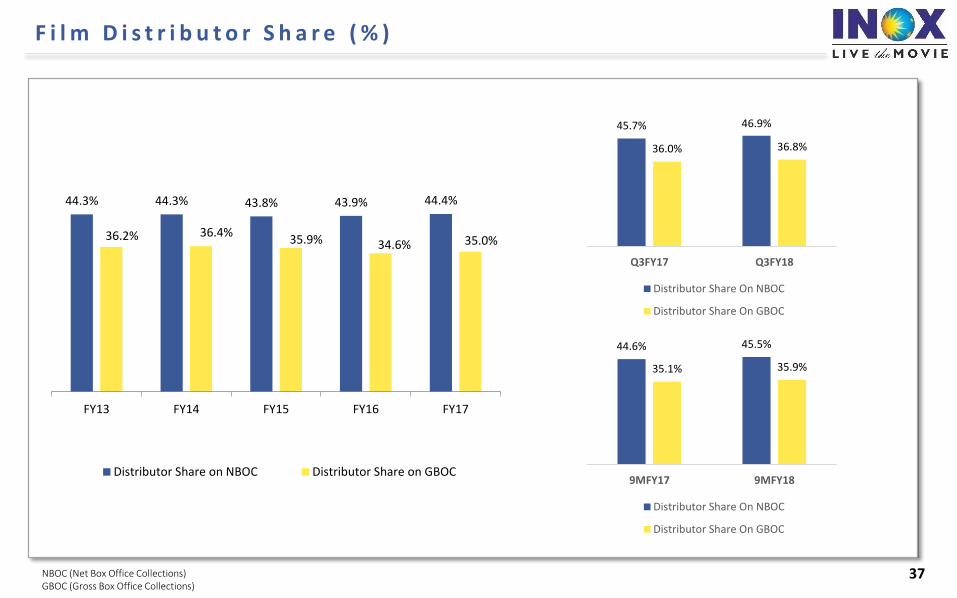

F i l m D i s t r i b u t o r S h a r e ( % )

37

44.3% 44.3% 43.8% 43.9% 44.4%

36.2% 36.4%35.9% 34.6% 35.0%

0.0 %

5.0 %

10. 0%

15. 0%

20. 0%

25. 0%

30. 0%

35. 0%

40. 0%

45. 0%

50. 0%

FY13 FY14 FY15 FY16 FY17

Distributor Share on NBOC Distributor Share on GBOC

NBOC (Net Box Office Collections) GBOC (Gross Box Office Collections)

45.7% 46.9%

36.0% 36.8%

0.0 %

5.0 %

10. 0%

15. 0%

20. 0%

25. 0%

30. 0%

35. 0%

40. 0%

45. 0%

50. 0%

Q3FY17 Q3FY18

Distributor Share On NBOC

Distributor Share On GBOC

44.6% 45.5%

35.1% 35.9%

0.0 %

5.0 %

10. 0%

15. 0%

20. 0%

25. 0%

30. 0%

35. 0%

40. 0%

45. 0%

50. 0%

9MFY17 9MFY18

Distributor Share On NBOC

Distributor Share On GBOC

O t h e r O v e r h e a d s P e r O p e r a t i n g S c r e e n

38

18.1 18.5 20.3 20.1 21.2

39.3 40.2 41.3 44.0 45.6

35.4 39.2 40.8 45.5 42.9

39.8 40.4 43.447.5 52.7

FY13 FY14 FY15 FY16 FY17

Employee Benefits Lease Rental & Hire Charges

CAM, Power & Fuel, R&M Other Overheads

157.0138.3

145.8132.5

162.5

All figures in INR Lakhs, unless specified

16.1 16.4

34.2 35.1

32.6 33.3

39.9 34.8

122.7 119.7

(10.0)

10.0

30.0

50.0

70.0

90.0

110.0

130.0

9MFY17 9MFY18

-12.6%

2.3%

2.7%

1.9%

5.1 5.6

11.3 11.6

10.2 10.0

13.5 11.8

40.1 39.0

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

Q3FY17 Q3FY18

-12.5%

-2.5%

2.9%

9.6%

39

Compet i t ive Advantage• R e c o g n i s e d A n d T r u s t e d C o r p o r a t e G r o u p

• W e l l D i v e r s i f i e d P r e s e n c e A c r o s s I n d i a

• S t r o n g N e w S c r e e n s P i p e l i n e

• S t r o n g B r a n d P a r t n e r s h i p s

• U n d e r - l e v e r a g e d B a l a n c e S h e e t W i t h F u r t h e r S c o p e F o r D i l u t i o n

• S t a t e O f T h e A r t T e c h n o l o g y , U n m a t c h e d S e r v i c e A n d A m b i e n c e

R-City, Ghatkopar, Mumbai

Substantially exited wind

farming business by selling

246 MW out of 269 MW of

operational capacity

L i s t e d C o m p a n i e s O t h e r K e y C o m p a n i e s

INOX LeisureLimited

Largest producer of (by volume)

Chloromethanes, refrigerants

and Polytetrafluoroethylene in

India.

Pioneer of carbon credits in

India

INOX Air Products Private Limited

50:50 joint venture with Air

Products Inc., USA

Largest producer of industrial

gases in India

40 plants spread throughout

the country

One of the largest multiplex

chains in India

In the business of setting up,

operating and managing a

national chain of multiplexes

under the brand name ‘INOX’

Present in 60 cities with 122

multiplexes and 488 screens

Gujarat FluorochemicalsLimited

Largest producer of cryogenic

liquid storage and transport

tanks in India

Offers comprehensive

solutions in cryogenic storage,

vaporization and distribution

engineering

Has operations in India, USA,

Canada, Netherlands and

Brazil

INOX India PrivateLimited

INOX RenewablesLimited

Fully integrated player in the

wind energy market

State-of-the-art manufacturing

plants near Ahmedabad

(Gujarat), Una (Himachal

Pradesh) and Barwani (Madhya

Pradesh). Our Madhya Pradesh

facility is one of the largest in

Asia

Ability to provide end-to-end

turnkey solutions for wind farms

INOX Wind Limited

R e c o g n i s e d & Tr u s t e d C o r p o r a t e G r o u p

40

• 90 Year track record of consistent business growth• USD $3 Billion Inox Group diversified across 7 different businesses

• 10,000+ employees at 150+ business units across India• Distribution network spread over 50+ countries

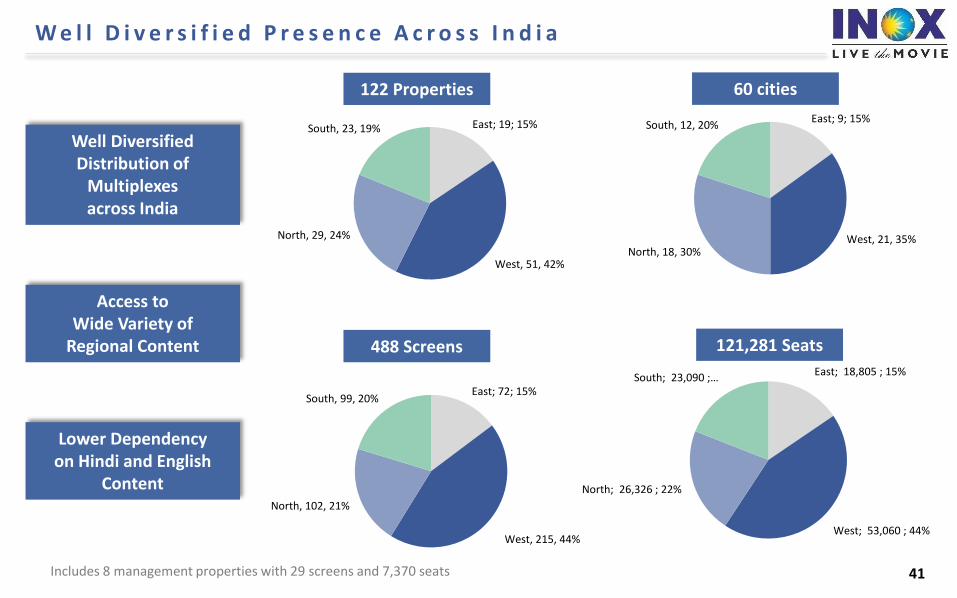

W e l l D i v e r s i f i e d P r e s e n c e A c r o s s I n d i a

41

East; 19; 15%

West, 51, 42%

North, 29, 24%

South, 23, 19%East; 9; 15%

West, 21, 35%North, 18, 30%

South, 12, 20%

East; 72; 15%

West, 215, 44%

North, 102, 21%

South, 99, 20%

East; 18,805 ; 15%

West; 53,060 ; 44%

North; 26,326 ; 22%

South; 23,090 ; …

Well DiversifiedDistribution of

Multiplexesacross India

Access toWide Variety of

Regional Content

Lower Dependencyon Hindi and English

Content

Includes 8 management properties with 29 screens and 7,370 seats

122 Properties 60 cities

488 Screens 121,281 Seats

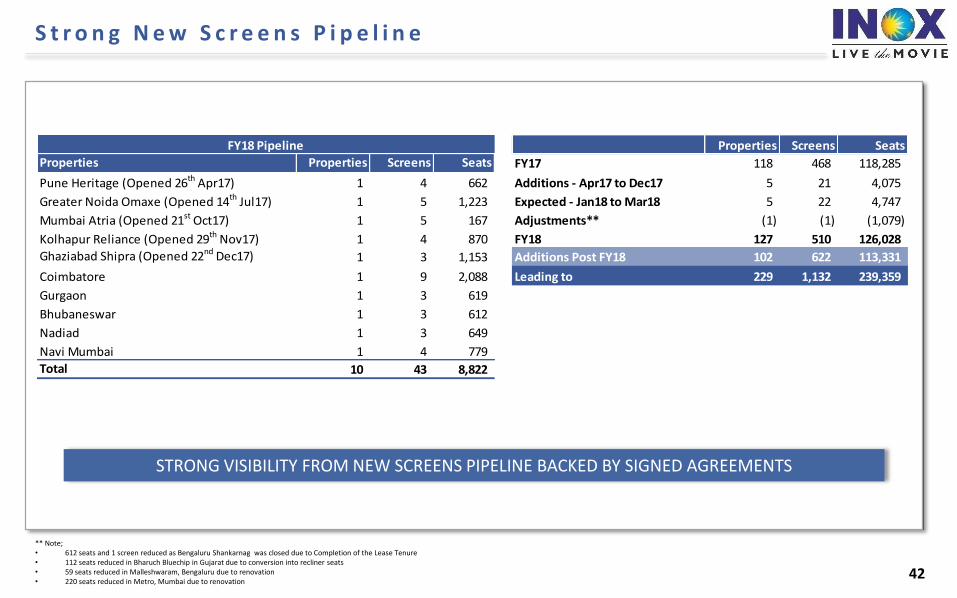

S t r o n g N e w S c r e e n s P i p e l i n e

42

Properties Screens Seats

Properties Properties Screens Seats FY17 118 468 118,285

Pune Heritage (Opened 26th Apr17) 1 4 662 Additions - Apr17 to Dec17 5 21 4,075

Greater Noida Omaxe (Opened 14th Jul17) 1 5 1,223 Expected - Jan18 to Mar18 5 22 4,747

Mumbai Atria (Opened 21st Oct17) 1 5 167 Adjustments** (1) (1) (1,079)

Kolhapur Reliance (Opened 29th Nov17) 1 4 870 FY18 127 510 126,028

Ghaziabad Shipra (Opened 22nd Dec17) 1 3 1,153 Additions Post FY18 102 622 113,331

Coimbatore 1 9 2,088 Leading to 229 1,132 239,359

Gurgaon 1 3 619

Bhubaneswar 1 3 612

Nadiad 1 3 649

Navi Mumbai 1 4 779

Total 10 43 8,822

FY18 Pipeline

** Note;• 612 seats and 1 screen reduced as Bengaluru Shankarnag was closed due to Completion of the Lease Tenure• 112 seats reduced in Bharuch Bluechip in Gujarat due to conversion into recliner seats• 59 seats reduced in Malleshwaram, Bengaluru due to renovation• 220 seats reduced in Metro, Mumbai due to renovation

STRONG VISIBILITY FROM NEW SCREENS PIPELINE BACKED BY SIGNED AGREEMENTS

Automobiles Ecommerce & TelecomBFSIMedia FMCG Consumer Durables Others

S t r o n g B r a n d P a r t n e r s h i p s

S t r o n g B a l a n c e S h e e t

44

Potential To Grow Aggressively Without Any

Stress On Balance Sheet

Net D/E:

Treasury Stock in Inox Benefit Trust

Promoters Stake

Low Leverage

• Calculated on Trailing 12 Months Basis• ROE: PAT/Avg. Equity, ROCE: EBIT/Avg. Capital Employed (Capital Employed = Equity + Total Debt)

* Share price As of 14th Feb 2018

Particulars (INR Crs.) Mar-17 Sep-17

Share Capital 96.2 96.2

Other Equity 489.0 533.5

Interest in Inox Benefit Trust, at cost (32.7) (32.7)

Total Shareholder funds 552.5 597.0

Non-Controlling Interest 0.01 0.01

Total Equity 552.5 597.0

Total Debt 317.0 307.0

Other Non-Current Liabilities 96.0 93.3

Total Sources of Funds 965.5 997.4

Fixed Assets 765.3 771.9

Other Non-Current Assets 273.5 277.7

Current Assets 81.8 101.8

Cash & Cash Equivalents 23.5 85.8

Less: Current Liabilities 178.5 239.9 Net Current Assets (73.3) (52.2)

Total Assets 965.5 997.4

Key Balance sheet Ratios Mar-17 Sep-17

Net Debt : Equity 0.53 0.37

Return on Equity (ROE) 5.7% 8.3%

Return on Capital Employed (ROCE) 7.3% 10.5%

48.7%

Real Estate on Balance Sheet

INR 350 Crs.

134 INR Crs.*

0.4x

S t a t e o f t h e A r t Te c h n o l o g y, U n m a t c h e d S e r v i c e & A m b i e n c e

45

ILL is the first multiplex chain to implement SAP HANA with all integrated functions

Focus on ensuring transparency with regulatory agencies and distributors through daily performance analysis reports

The Network Operations Centre (NOC) in Mumbai enables continuous monitoring, control and reporting of information on all digital

systems across the country. Advertisers can track their advertisement screening at various multiplexes on real-time basis leading to

improved transparency and higher advertising revenues for ILL

ILL have signed the single largest deal with IMAX in India to provide truly encaptivating and completely immersive viewing experience

ILL has pioneered Laser projection across the country including India’s first Laserplex

ILL operates high quality DCI Compliant 2K & 4K Digital Projection Systems across all the screens in India

High-definition picture quality, strong 3D capabilities and high frame rate (HFR) (can go up to 60 fps)

ILL has been one of the early adopters of Dolby ATMOS sound technology. Excellent acoustic systems and distortion free sound

Focus on providing world class ambience.

ILL with its in-app F&B ordering and Qbuster service, is able to considerably reduce its queue size and transaction time

Emphasis on safety, comfort and convenience

Focus On Strong Technology, Unmatched Service And Ambience

Focus On Technology

Focus on high quality video and audio:

Focus on service and ambience:

Content Pipeline – January 2018

46

1921

Release Date: 12th January 2018Cast: Zareen Khan, Karan KundraDirector: VikramBhattBanner: Reliance Entertainment, Motion Picture Capital

Thaana SerndhaKootam (Tamil)

Release Date:12th January 2018Cast: Surya, KeerthySureshDirector: VighneshShivanBanner: Studio Green

Padmaavat

Release Date: 25th January 2018Cast: DeepikaPadukone, RanveerSinghDirector: Sanjay LeelaBhansaliBanner: BhansaliProductions

Kaalakaandi

Release Date: 12th January 2018Cast: Saif Ali Khan, Vijay RaazDirector: AkshatVermaBanner: CinestaanFilm Company Pvt.Ltd., Flying Unicorn Entertainment

Mukkabaaz

Release Date: 12th January 2018Cast: Vineet Kumar Singh, Zoya HussainDirector: AnuragKashyapBanner: Eros InternationalPhantom FilmsColour Yellow Productions

The Post

Release Date:12th January 2018Cast: Meryl Streep, Tom Hanks, Sarah PaulsonDirector: Steven SpielbergBanner: Amblin Entertainment, DreamWorks, Participant Media

47

Content Pipeline – February 2018

Aiyaary

Release Date: 9th February 2018Cast: Siddharth Malhotra, Manoj BajpayeeDirector: Neeraj PandeyBanner: Reliance Entertainment,Plan C Studios,Friday Filmworks,Jayantilal Gada

Maze Runner : The Death Cure (3D Imax)

Release Date:2nd February 2018Cast: Dylan O Brian, Kaya Skodelario, Thomas BrodieDirector: Wes BallBanner: Gotham Group, Temple Hill Entertainment,TSG Entertainment

Hichki

Release Date: 23th February 2018Cast: Rani MukherjeeDirector: Siddharth P. MalhotraBanner: Yash Raj Films

Black Panther (3D Imax)

Release Date:16th February 2018Cast: Chadwick Boseman, Michael B Jordon, Lupita NyongDirector: Ryan CooglerBanner: Marvel Studios

Padman

Release Date: 9th February 2018Cast: Akshay Kumar, Sonam Kapoor, Radhika ApteDirector: R BalkiBanner: MrsFunnybones Movies

Sonu Ke Titu Ki Sweety

Release Date:23rd February 2018Cast: Karthik Aaryan, Nusrat Bharucha, Sunny Singh NajjarDirector: Luv RanjanBanner: T-Series, Luv Films

48

Content Pipeline – March 2018

Drive

Release Date: 2nd March 2018Cast: Sushant Singh Rajput, Jacquline FernandesDirector: Tarun MansukhaniBanner: Dharma Productions, Fox Star Studios

Raid

Release Date: 16th March 2018Cast: Ajay Devgan, Illiana D CruzDirector: Rajkumar GuptaBanner: T-Series Super Cassettes Industries Ltd.,Panorama Studios

Pacific Rim : Uprising

Release Date:23th March 2018Cast: Scott Eastwood, John BogeyaDirector: Steven S DenightBanner: Legendary Pictures, UpperRoom Entertainment Limited, DDY

Baaghi 2

Release Date:30th March 2018Cast: Tiger Shroff, Disha PataniDirector: Ahmed KhanBanner: NadiadwalaGrandson Entertainment, Fox Star Studios

Pari

Release Date: 2nd March 2018Cast: Anushka Sharma, Paambarta ChatterjeeDirector: Prosit RoyBanner: Clean Slate Films, KriArj Entertainment,KYTA Productions

Parmanu - The Story Of Pokhran

Release Date: 2nd Mar 2018Cast: John Abraham, Boman Irani, Diana PentyDirector: Abhishek SharmaBanner: KriArj Entertainment, J A Entertainment, KYTA Productions, Zee Studios

49

Content Pipeline – April 2018

October

Release Date: 13th April 2018Cast: Varun Dhawan, Banita SandhuDirector: Shoojit SircarBanner: Rising Sun Films, Sony Pictures Networks Productions,KriArj Entertainment

Rampage

Release Date: 20th April 2018Cast: Jeffrey Dean Morgan, Dwayne Johnson, Jake LacyDirector: Brad PeytonBanner: New Line Cinema, Twisted Media, Wrigley Pictures

2.0

Release Date:14th April 2018Cast: Rajinikanth, Akshay Kumar, Amy JacksonDirector: S ShankarBanner: LycaProductions

Avengers: Infinity War

Release Date:27th April 2018Cast: Karen Gillan, Pom Klementieff, Tessa ThompsonDirector: Anthony Russo, Joe RussoBanner: Marvel Studios

Manikarnika – The Queen Of Jhansi

Release Date:27th April 2018Cast: Kangana Ranaut, Suresh OberoiDirector: KrishBanner: Zee Studios,Kairos Kontent Studios

Bharat Ane Nenu(Telugu)

Release Date: 27th April 2018Cast: Mahesh Babu,Kiara Advani. Director: Koratala SivaBanner: DVV Danayya

50

Annexure

CR2 Nariman Point, Mumbai

Per Screen Economics

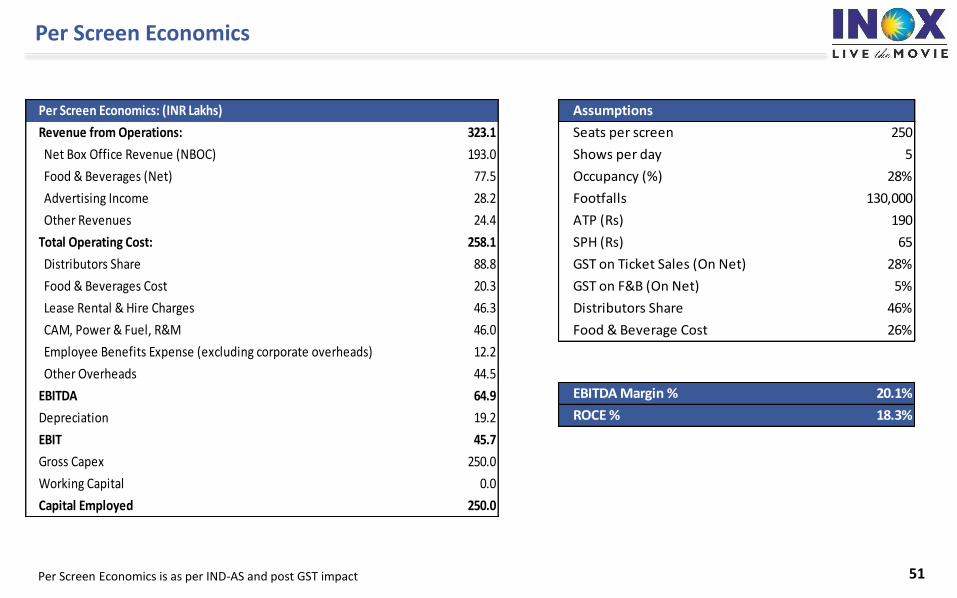

51Per Screen Economics is as per IND-AS and post GST impact

Per Screen Economics: (INR Lakhs)

Revenue from Operations: 323.1

Net Box Office Revenue (NBOC) 193.0

Food & Beverages (Net) 77.5

Advertising Income 28.2

Other Revenues 24.4

Total Operating Cost: 258.1

Distributors Share 88.8

Food & Beverages Cost 20.3

Lease Rental & Hire Charges 46.3

CAM, Power & Fuel, R&M 46.0

Employee Benefits Expense (excluding corporate overheads) 12.2

Other Overheads 44.5

EBITDA 64.9

Depreciation 19.2

EBIT 45.7

Gross Capex 250.0

Working Capital 0.0

Capital Employed 250.0

Assumptions

Seats per screen 250

Shows per day 5

Occupancy (%) 28%

Footfalls 130,000

ATP (Rs) 190

SPH (Rs) 65

GST on Ticket Sales (On Net) 28%

GST on F&B (On Net) 5%

Distributors Share 46%

Food & Beverage Cost 26%

EBITDA Margin % 20.1%

ROCE % 18.3%

Shareholding Structure

52

Source: BSE

Public/Others, 11.23%

INOX Benefit Trust, 4.51%

DII, 17.69%

FII, 17.87%

Promoter & Promoter

Group, 48.70%

% Shareholding as of 9th Feb’18

Source: Company Source: Company

Key Institutional Investors – 9th Feb'18 % Holding

DSP Blackrock MF 7.0%

Reliance MF 4.0%

Aditya Birla Sunlife 3.1%

Kuwait Investment Authority Fund 3.0%

Morgan Stanley 2.8%

Goldman Sachs India Ltd. 2.6%

RAMS Equities Portfolio Fund 1.8%

Sundaram MF 1.5%

ICICI Prudential MF 1.1%

AADI Financial Advisors LLP 1.0%

Source: BSE

Market Data As on 14th Feb 2018

Market Capitalisation (INR Crs.) 2,981

Price (INR) 309.1

No. of Shares Outstanding (Crs.) 9.6

Face Value (INR) 10.0

52 week High/Low (INR) 326/213.300

50

100

150

200

250

300

350

Ap

r-1

3

Jul-

13

Oct

-13

Jan

-14

Ap

r-1

4

Jul-

14

Oct

-14

Jan

-15

Ap

r-1

5

Jul-

15

Oct

-15

Jan

-16

Ap

r-1

6

Jul-

16

Oct

-16

Jan

-17

Ap

r-1

7

Jul-

17

Oct

-17

Jan

-18

INR

Share Price Performance

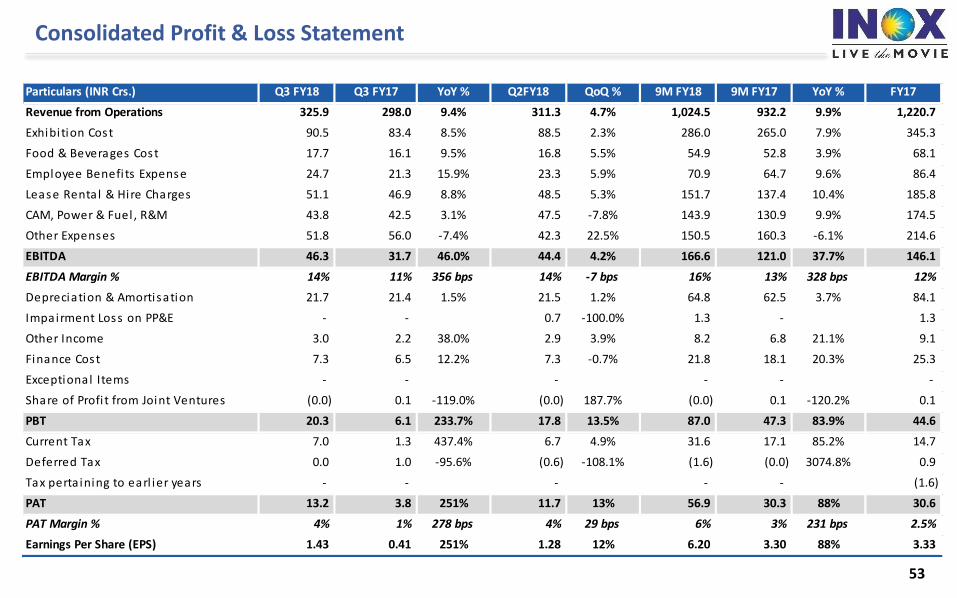

Consolidated Profit & Loss Statement

53

Particulars (INR Crs.) Q3 FY18 Q3 FY17 YoY % Q2FY18 QoQ % 9M FY18 9M FY17 YoY % FY17

Revenue from Operations 325.9 298.0 9.4% 311.3 4.7% 1,024.5 932.2 9.9% 1,220.7

Exhibi tion Cost 90.5 83.4 8.5% 88.5 2.3% 286.0 265.0 7.9% 345.3

Food & Beverages Cost 17.7 16.1 9.5% 16.8 5.5% 54.9 52.8 3.9% 68.1

Employee Benefi ts Expense 24.7 21.3 15.9% 23.3 5.9% 70.9 64.7 9.6% 86.4

Lease Rental & Hire Charges 51.1 46.9 8.8% 48.5 5.3% 151.7 137.4 10.4% 185.8

CAM, Power & Fuel , R&M 43.8 42.5 3.1% 47.5 -7.8% 143.9 130.9 9.9% 174.5

Other Expenses 51.8 56.0 -7.4% 42.3 22.5% 150.5 160.3 -6.1% 214.6

EBITDA 46.3 31.7 46.0% 44.4 4.2% 166.6 121.0 37.7% 146.1

EBITDA Margin % 14% 11% 356 bps 14% -7 bps 16% 13% 328 bps 12%

Depreciation & Amortisation 21.7 21.4 1.5% 21.5 1.2% 64.8 62.5 3.7% 84.1

Impairment Loss on PP&E - - 0.7 -100.0% 1.3 - 1.3

Other Income 3.0 2.2 38.0% 2.9 3.9% 8.2 6.8 21.1% 9.1

Finance Cost 7.3 6.5 12.2% 7.3 -0.7% 21.8 18.1 20.3% 25.3

Exceptional Items - - - - - -

Share of Profi t from Joint Ventures (0.0) 0.1 -119.0% (0.0) 187.7% (0.0) 0.1 -120.2% 0.1

PBT 20.3 6.1 233.7% 17.8 13.5% 87.0 47.3 83.9% 44.6

Current Tax 7.0 1.3 437.4% 6.7 4.9% 31.6 17.1 85.2% 14.7

Deferred Tax 0.0 1.0 -95.6% (0.6) -108.1% (1.6) (0.0) 3074.8% 0.9

Tax perta ining to earl ier years - - - - - (1.6)

PAT 13.2 3.8 251% 11.7 13% 56.9 30.3 88% 30.6

PAT Margin % 4% 1% 278 bps 4% 29 bps 6% 3% 231 bps 2.5%

Earnings Per Share (EPS) 1.43 0.41 251% 1.28 12% 6.20 3.30 88% 3.33

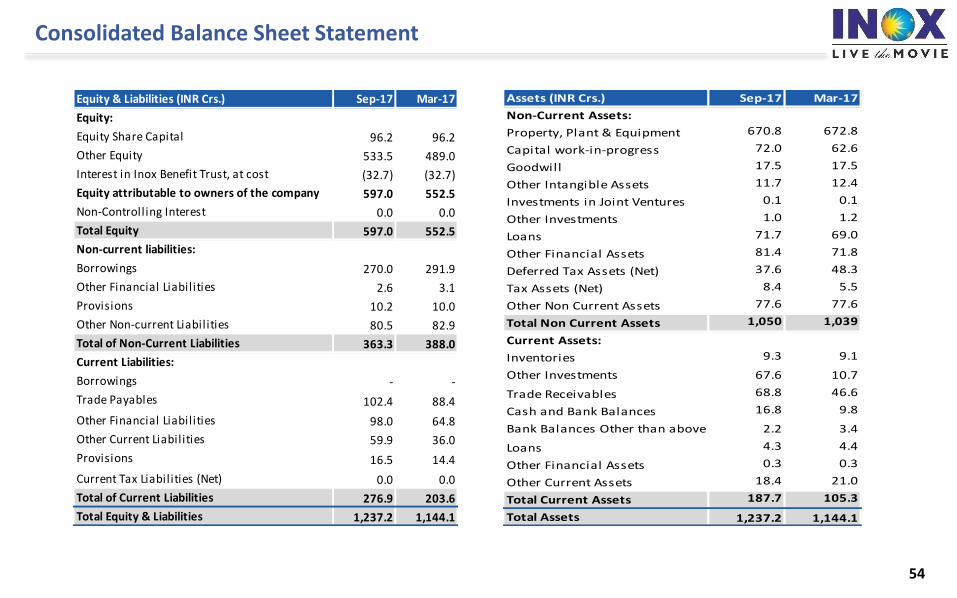

Consolidated Balance Sheet Statement

54

Assets (INR Crs.) Sep-17 Mar-17

Non-Current Assets:

Property, Plant & Equipment 670.8 672.8

Capital work-in-progress 72.0 62.6

Goodwill 17.5 17.5

Other Intangible Assets 11.7 12.4

Investments in Joint Ventures 0.1 0.1

Other Investments 1.0 1.2

Loans 71.7 69.0

Other Financial Assets 81.4 71.8

Deferred Tax Assets (Net) 37.6 48.3

Tax Assets (Net) 8.4 5.5

Other Non Current Assets 77.6 77.6

Total Non Current Assets 1,050 1,039

Current Assets:

Inventories 9.3 9.1

Other Investments 67.6 10.7

Trade Receivables 68.8 46.6

Cash and Bank Balances 16.8 9.8

Bank Balances Other than above 2.2 3.4

Loans 4.3 4.4

Other Financial Assets 0.3 0.3

Other Current Assets 18.4 21.0

Total Current Assets 187.7 105.3

Total Assets 1,237.2 1,144.1

Equity & Liabilities (INR Crs.) Sep-17 Mar-17

Equity:

Equity Share Capital 96.2 96.2

Other Equity 533.5 489.0

Interest in Inox Benefit Trust, at cost (32.7) (32.7)

Equity attributable to owners of the company 597.0 552.5

Non-Controlling Interest 0.0 0.0

Total Equity 597.0 552.5

Non-current liabilities:

Borrowings 270.0 291.9

Other Financial Liabilities 2.6 3.1

Provisions 10.2 10.0

Other Non-current Liabilities 80.5 82.9

Total of Non-Current Liabilities 363.3 388.0

Current Liabilities:

Borrowings - -

Trade Payables 102.4 88.4

Other Financial Liabilities 98.0 64.8

Other Current Liabilities 59.9 36.0

Provisions 16.5 14.4

Current Tax Liabilities (Net) 0.0 0.0

Total of Current Liabilities 276.9 203.6

Total Equity & Liabilities 1,237.2 1,144.1

Thank YouBalesh Talapady GM – Business AnalysisINOX Leisure Ltd.Contact+91-22-4062 6927Email: [email protected]

55

Atria, Worli, Mumbai