Embed Size (px)

Citation preview

1

Vitaliy N. Katsenelson, CFADirector of Research / Portfolio Manager

Investment Management Associates, Inc.

2

3

We are used to thinking about secular (longer than 5 years) markets in binary terms:

OR

4

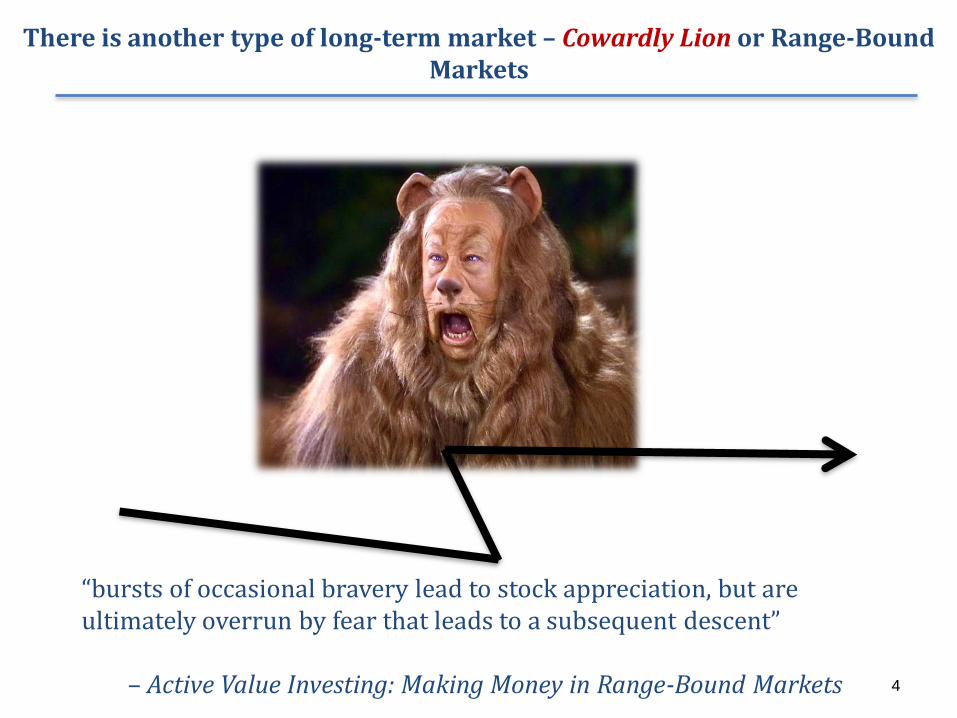

There is another type of long-term market – Cowardly Lion or Range-Bound Markets

or

“bursts of occasional bravery lead to stock appreciation, but are ultimately overrun by fear that leads to a subsequent descent”

– Active Value Investing: Making Money in Range-Bound Markets

5

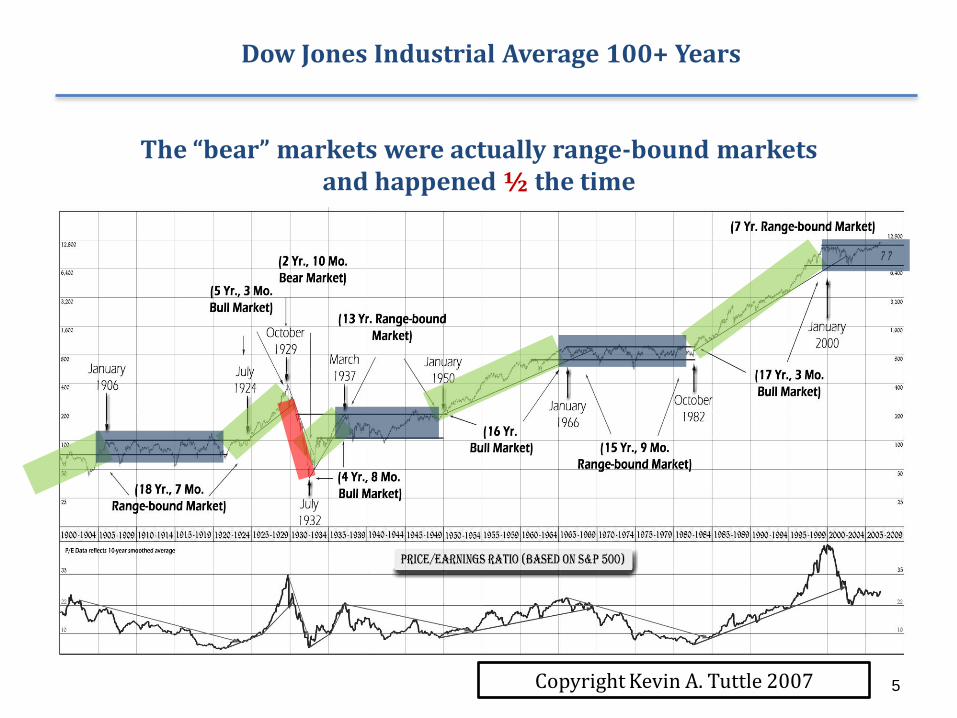

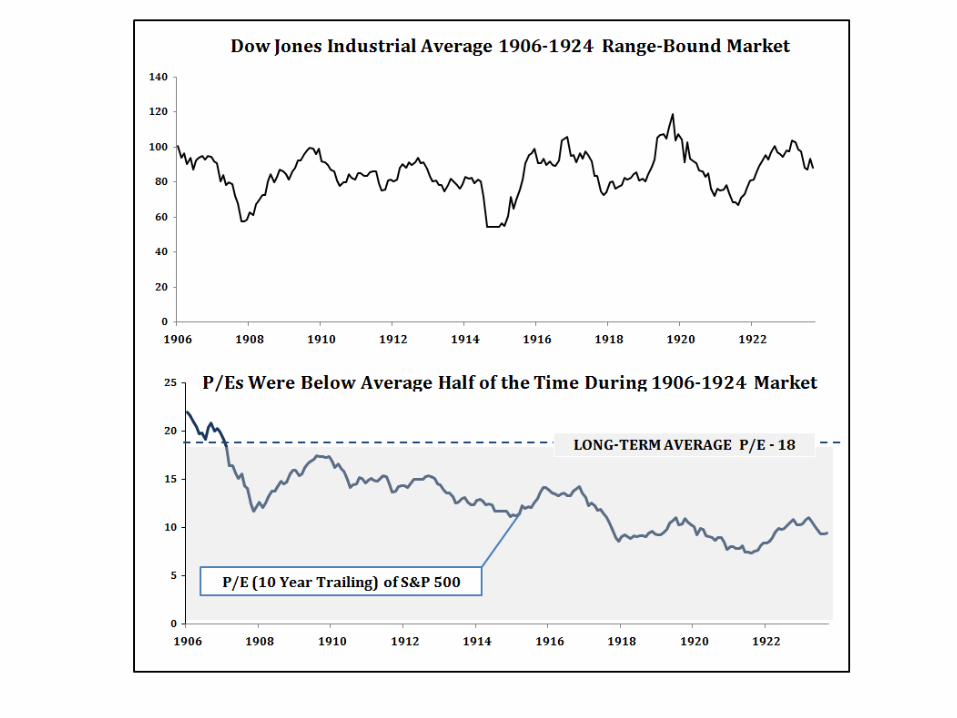

Dow Jones Industrial Average 100+ Years

The “bear” markets were actually range-bound markets and happened ½ the time

Copyright Kevin A. Tuttle 2007

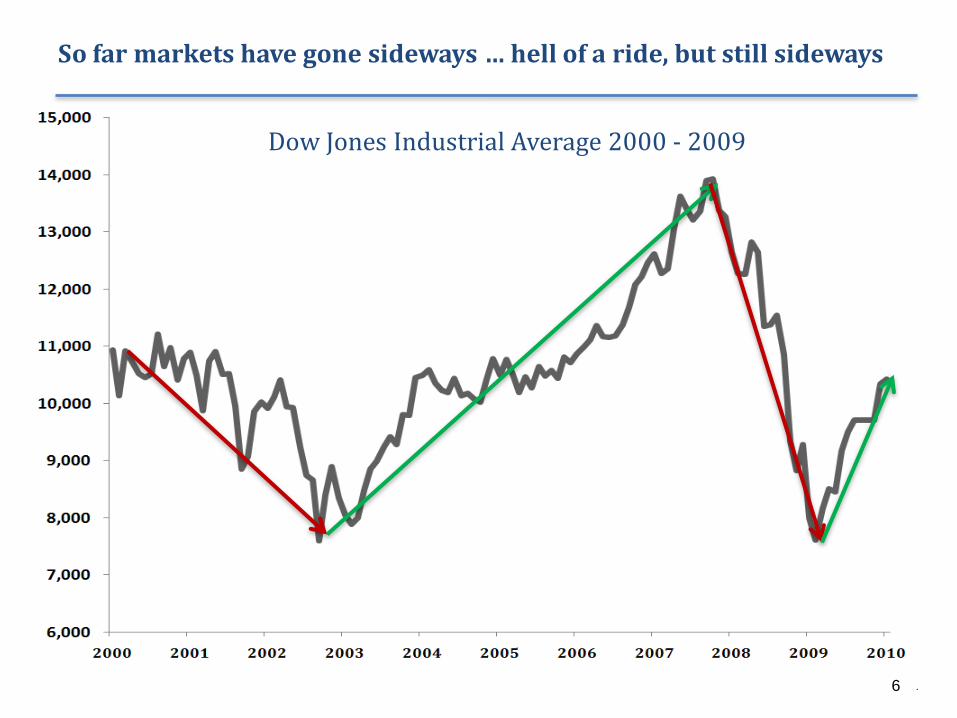

Dow Jones Industrial Average 2000 - 2009

So far markets have gone sideways … hell of a ride, but still sideways

6

7

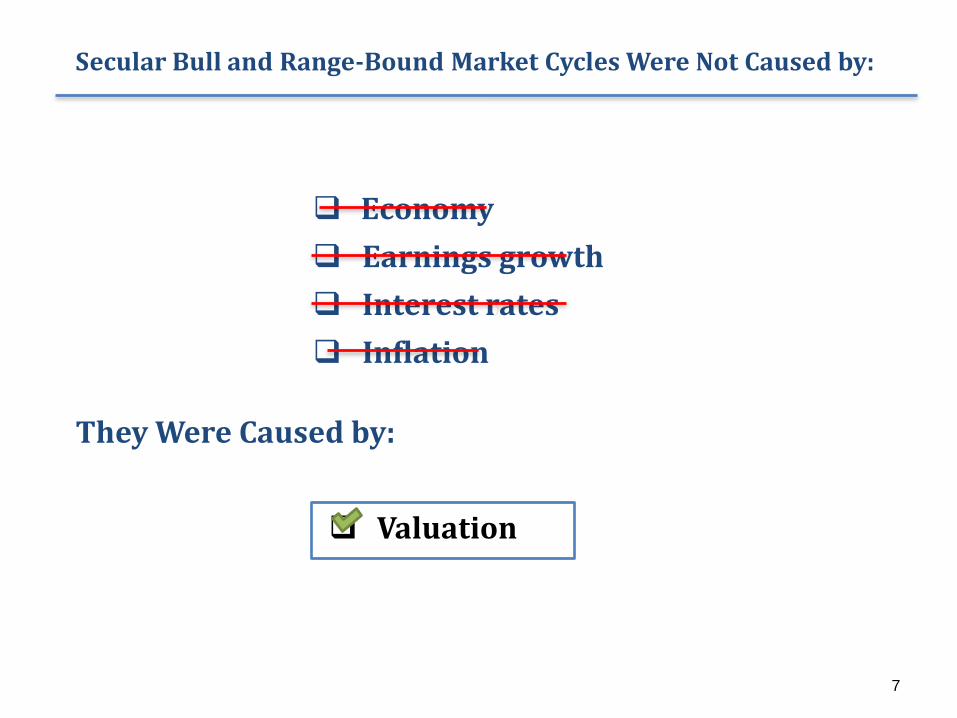

Secular Bull and Range-Bound Market Cycles Were Not Caused by:

or

Economy

Earnings growth

Interest rates

Inflation

Valuation

They Were Caused by:

8

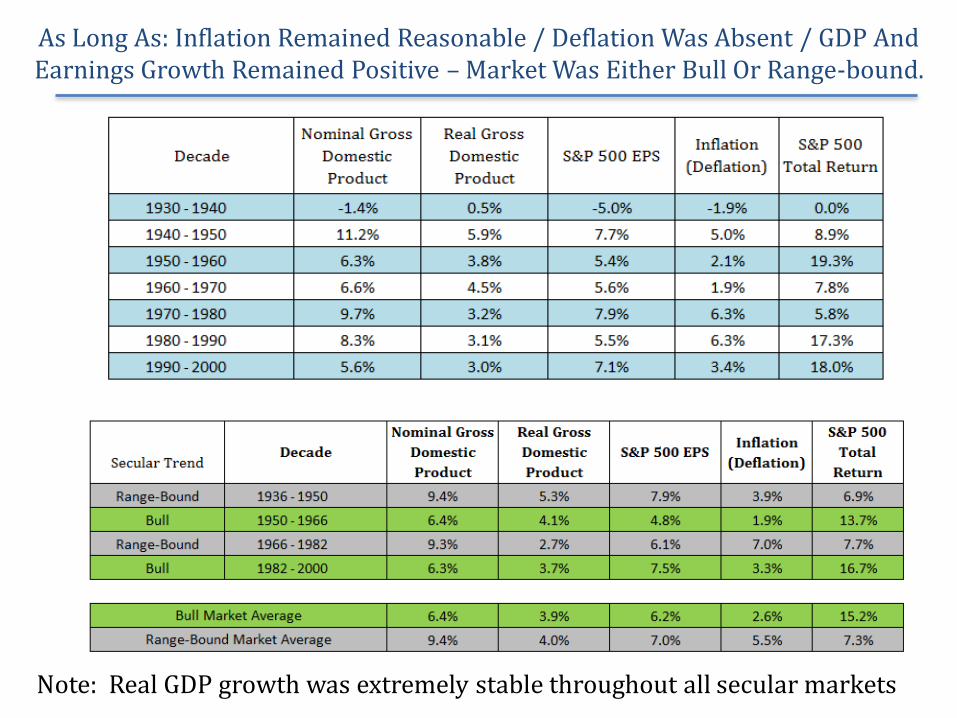

As Long As: Inflation Remained Reasonable / Deflation Was Absent / GDP And Earnings Growth Remained Positive – Market Was Either Bull Or Range-bound.

Note: Real GDP growth was extremely stable throughout all secular markets

9

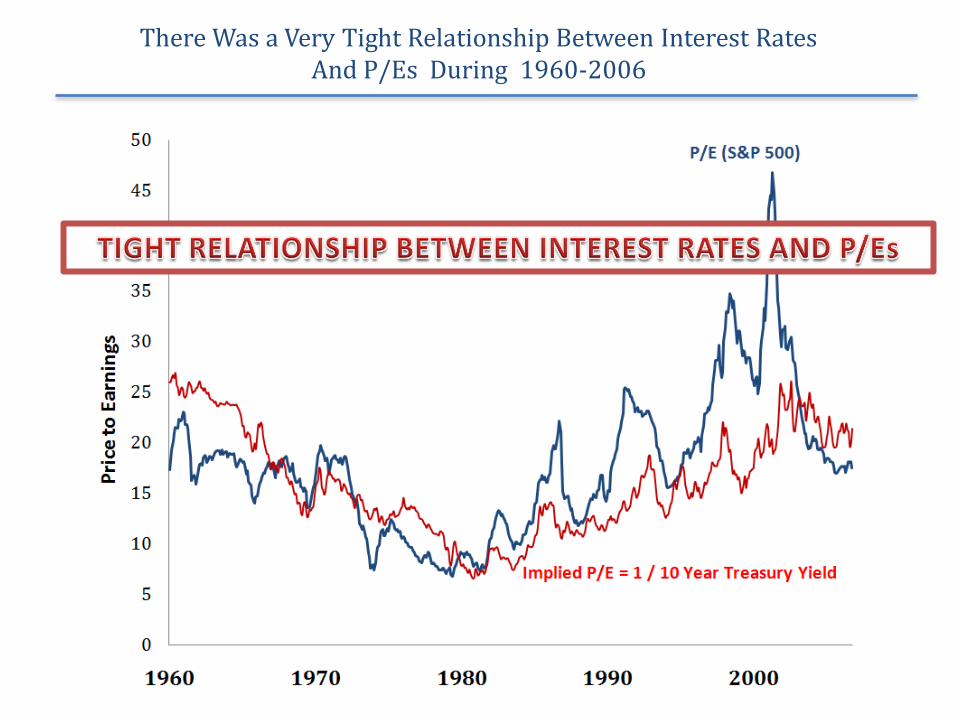

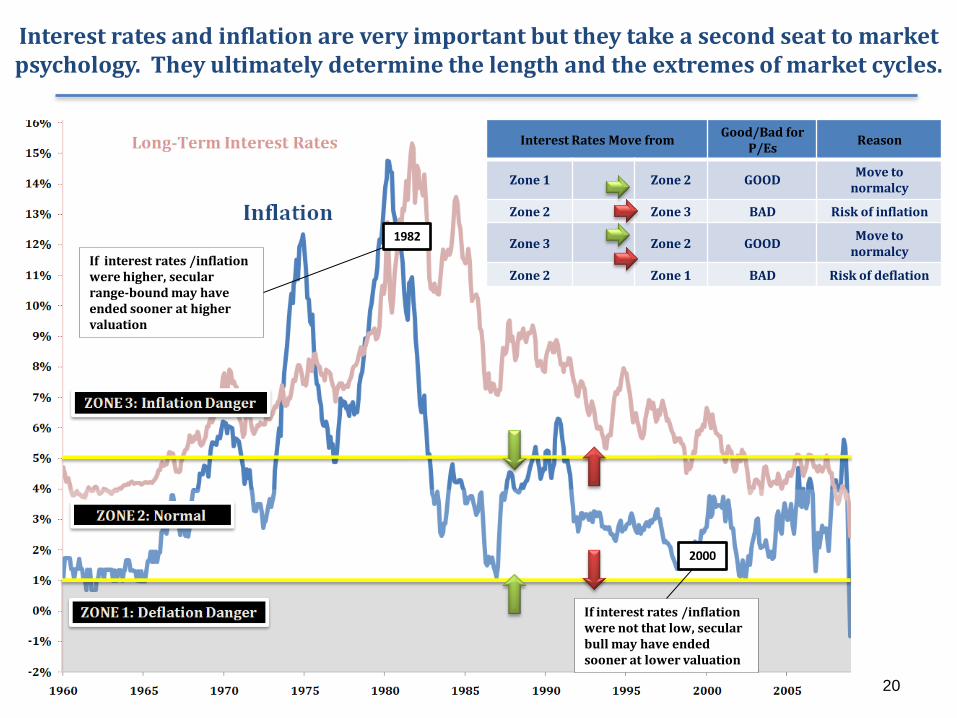

There Was a Very Tight Relationship Between Interest Rates And P/Es During 1960-2006

10

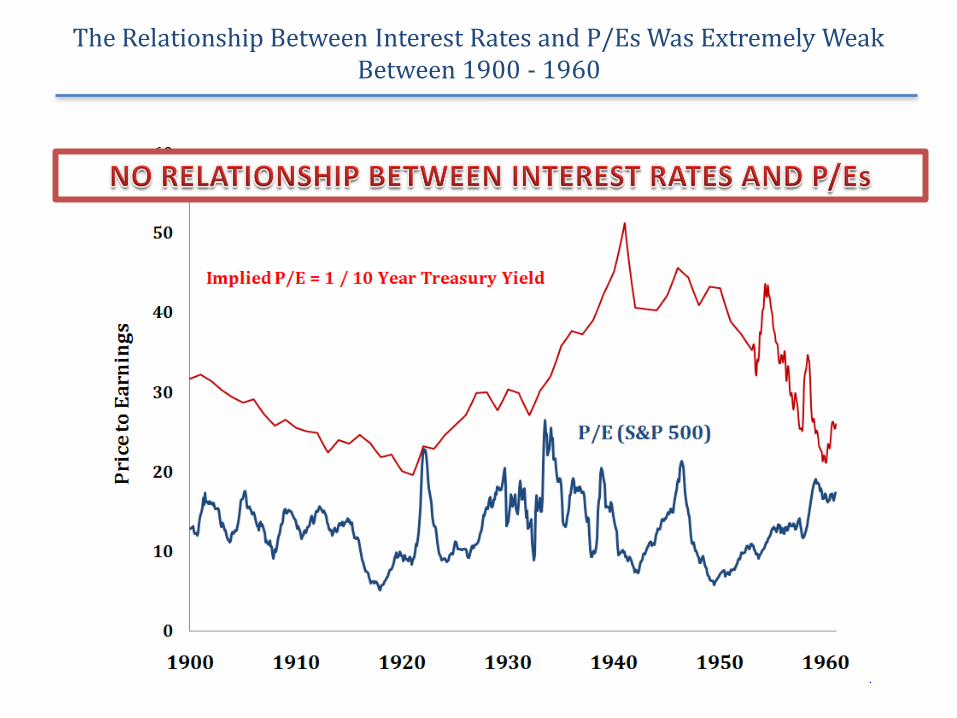

The Relationship Between Interest Rates and P/Es Was Extremely Weak Between 1900 - 1960

Earnings Growth+

∆ P/E

11

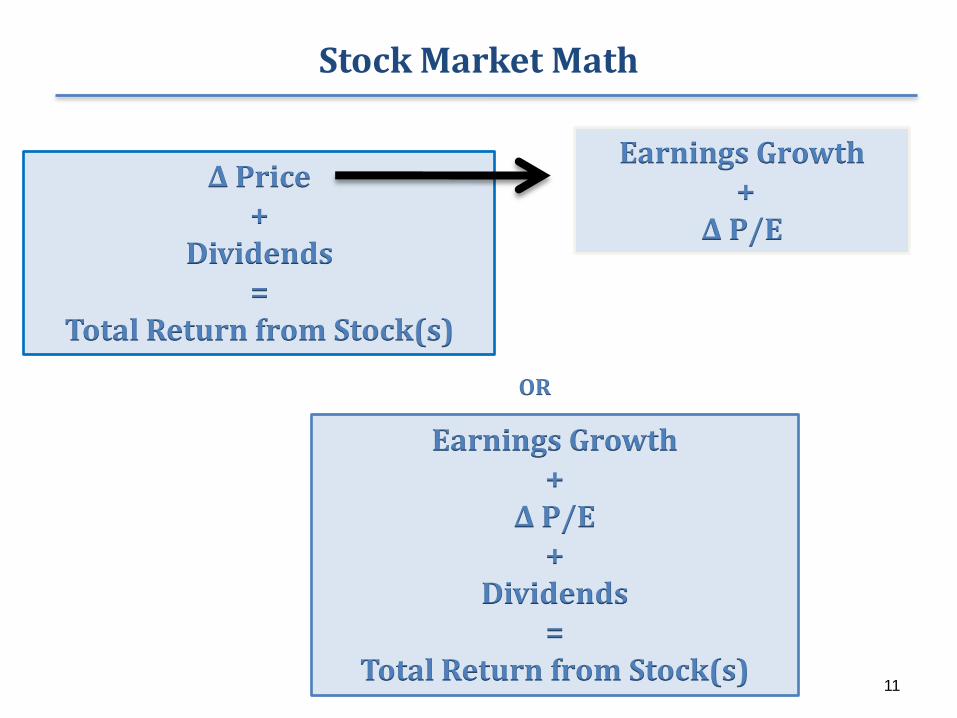

Stock Market Math

∆ Price+

Dividends=

Total Return from Stock(s)

Earnings Growth+

∆ P/E+

Dividends=

Total Return from Stock(s)

OR

12

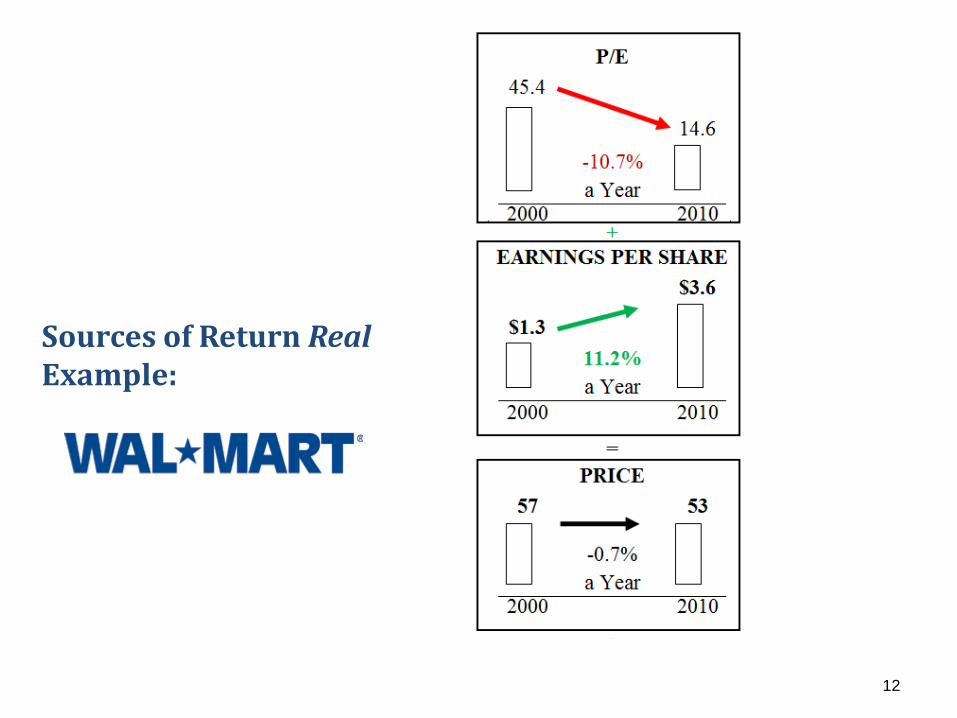

Sources of Return RealExample:

13

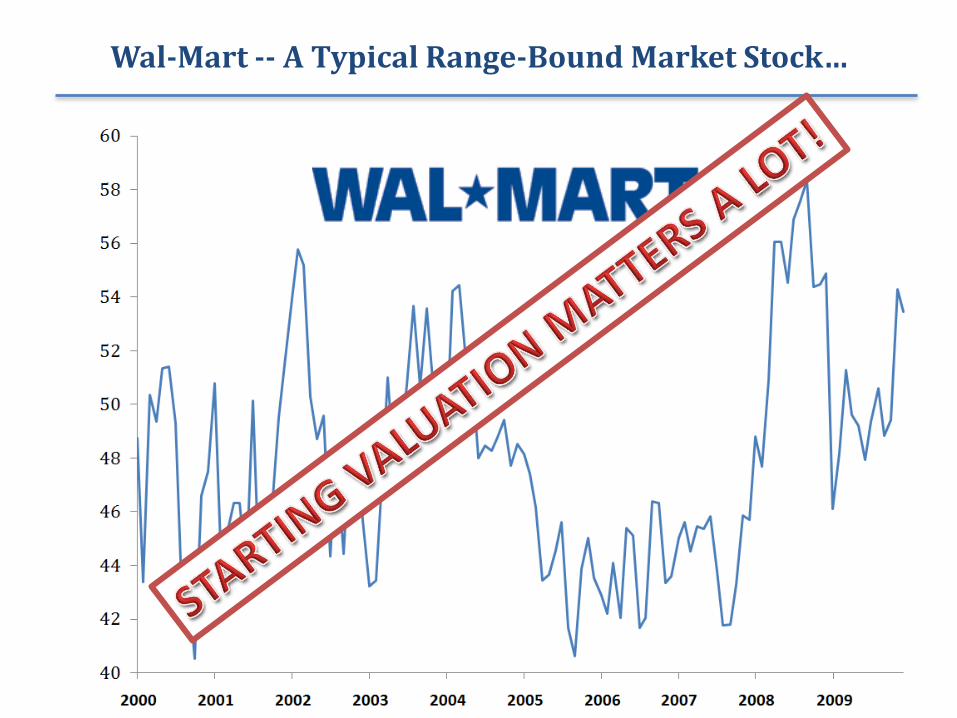

Wal-Mart -- A Typical Range-Bound Market Stock…

2001 - 2009

14

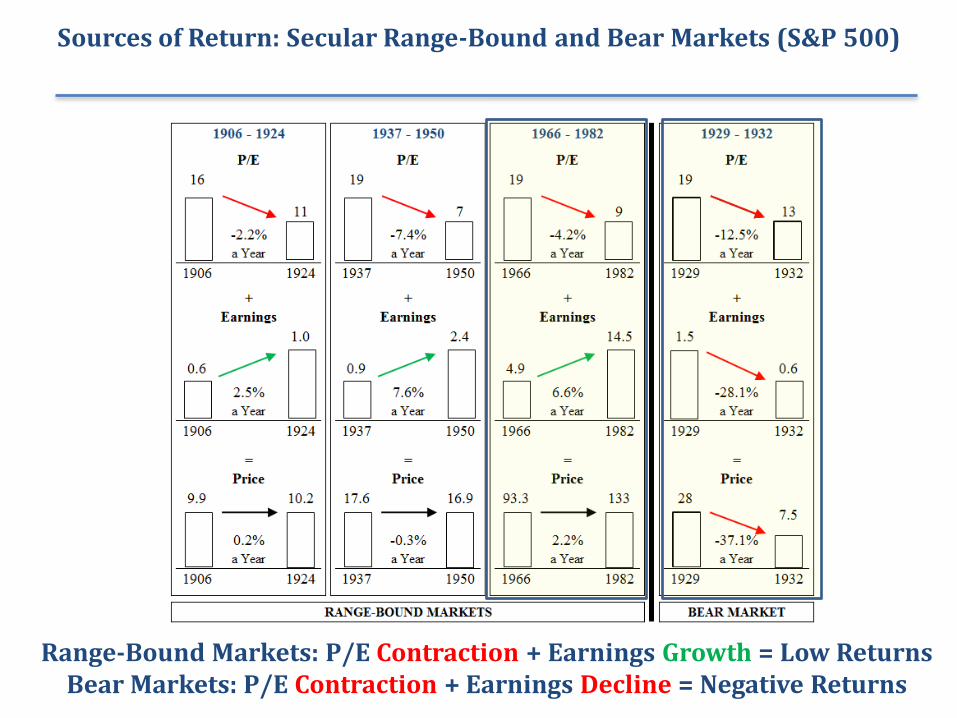

Sources of Return: Secular Range-Bound and Bear Markets (S&P 500)

Range-Bound Markets: P/E Contraction + Earnings Growth = Low ReturnsBear Markets: P/E Contraction + Earnings Decline = Negative Returns

15

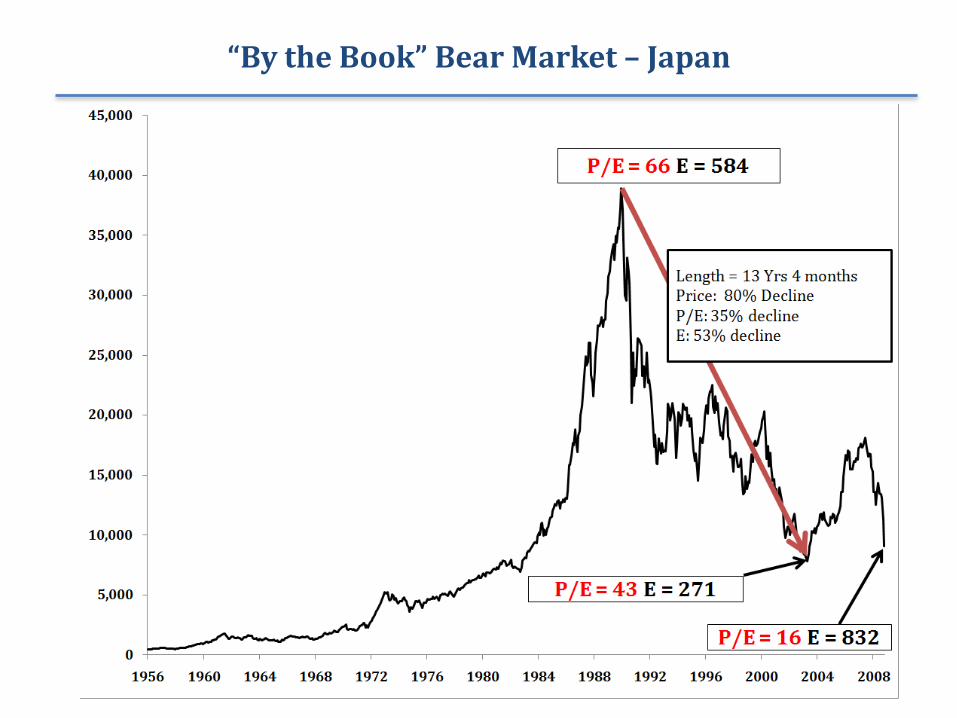

“By the Book” Bear Market – Japan

16

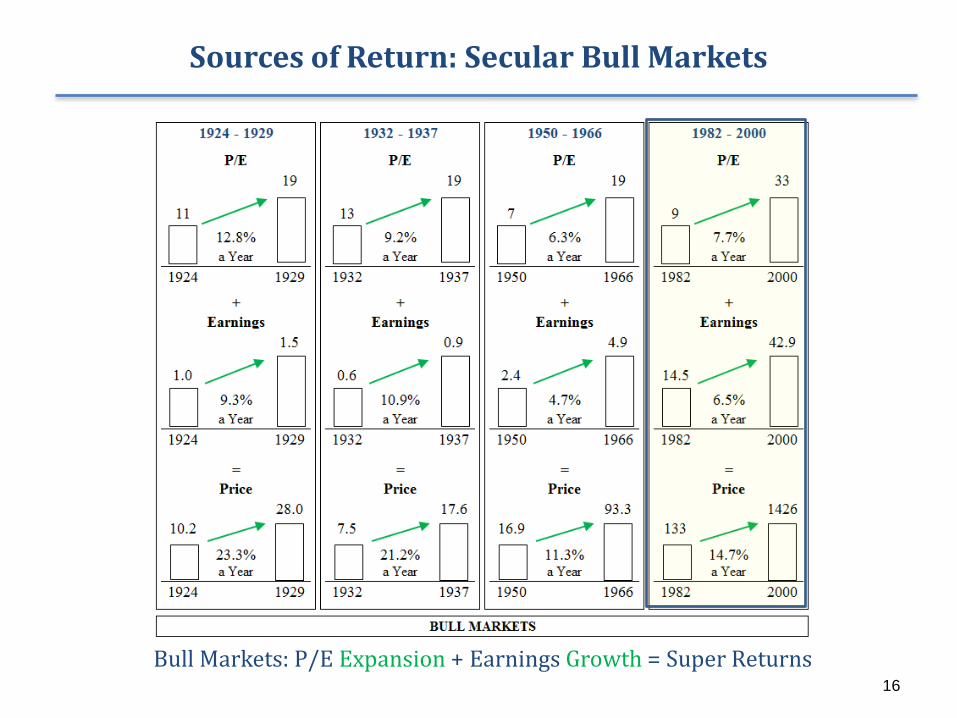

Sources of Return: Secular Bull Markets

Bull Markets: P/E Expansion + Earnings Growth = Super Returns

17

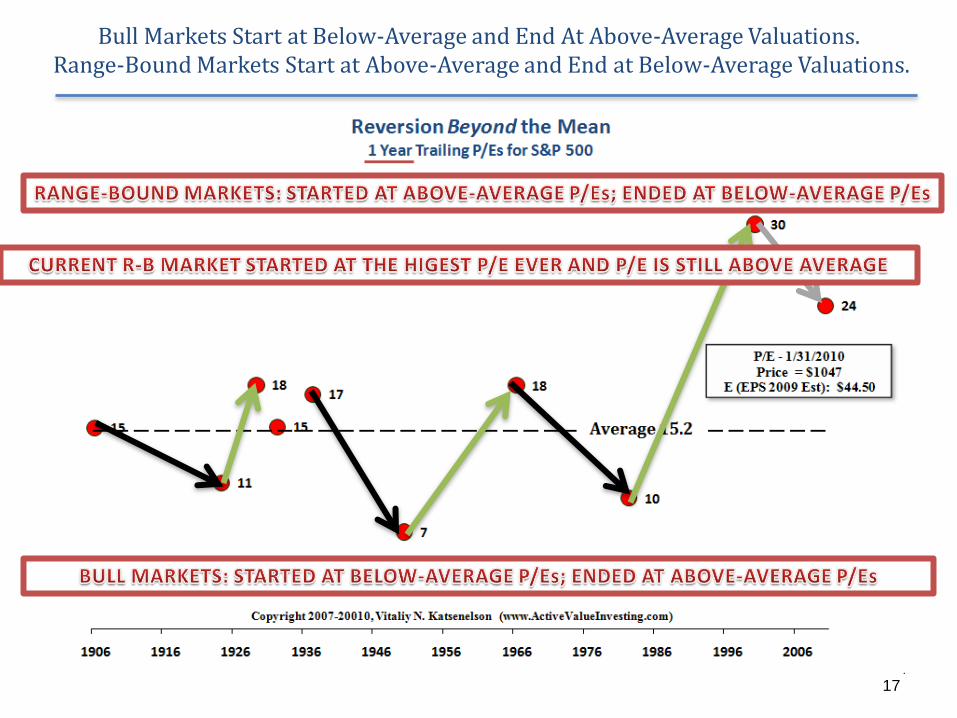

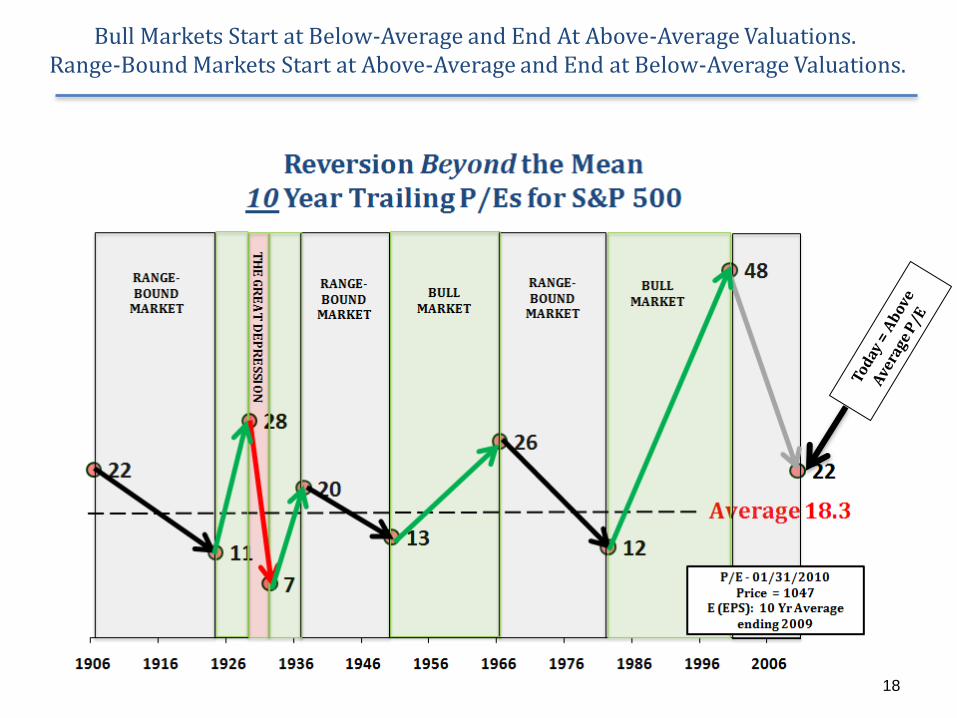

Bull Markets Start at Below-Average and End At Above-Average Valuations. Range-Bound Markets Start at Above-Average and End at Below-Average Valuations.

18

Bull Markets Start at Below-Average and End At Above-Average Valuations. Range-Bound Markets Start at Above-Average and End at Below-Average Valuations.

19

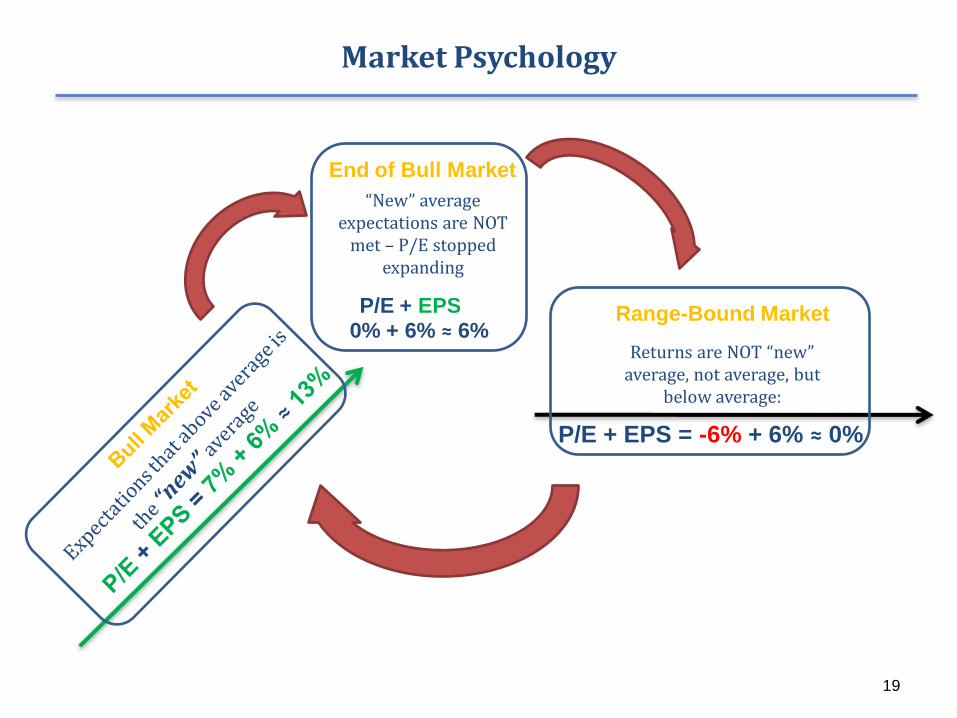

Market Psychology

19

P/E + EPS = 0% + 6% ≈ 6%

“New” average expectations are NOT

met – P/E stopped expanding

End of Bull Market

P/E + EPS = -6% + 6% ≈ 0%

Returns are NOT “new” average, not average, but

below average:

Range-Bound Market

Interest Rates Move fromGood/Bad for

P/EsReason

Zone 1 Zone 2 GOODMove to

normalcy

Zone 2 Zone 3 BAD Risk of inflation

Zone 3 Zone 2 GOODMove to

normalcy

Zone 2 Zone 1 BAD Risk of deflation

20

Interest rates and inflation are very important but they take a second seat to market psychology. They ultimately determine the length and the extremes of market cycles.

If interest rates /inflation were higher, secular range-bound may have ended sooner at higher valuation

If interest rates /inflation were not that low, secular bull may have ended sooner at lower valuation

1982

2000

21

Still in the Range-Bound /Sideways/ Market?

Valuations are still high (above average).

Valuations need to stay below average for a while (see next slide).

Real earnings growth will be lower in the future due to higher future taxes, higher interest rates (caused by government borrowing), consumer deleveraging – range-bound market may last longer than we expect.

High inflation will shorten range-bound market duration, but final P/E will be lower as well.

If nominal earnings growth doesn’t materialize in the future (3,5,10 years), earnings decline – we are set for a secular bear market

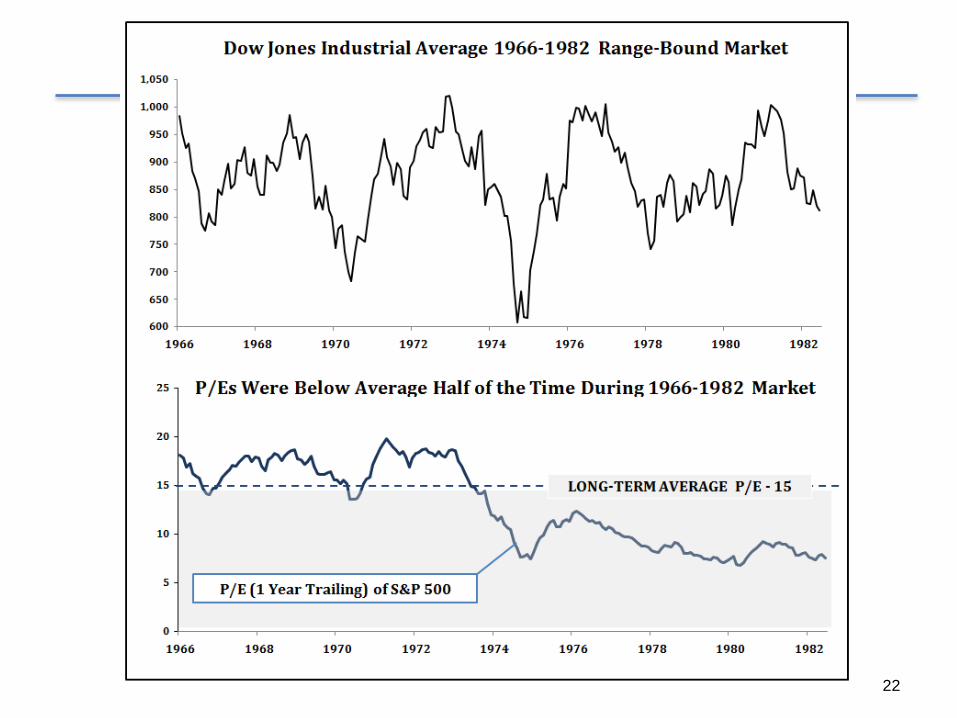

22

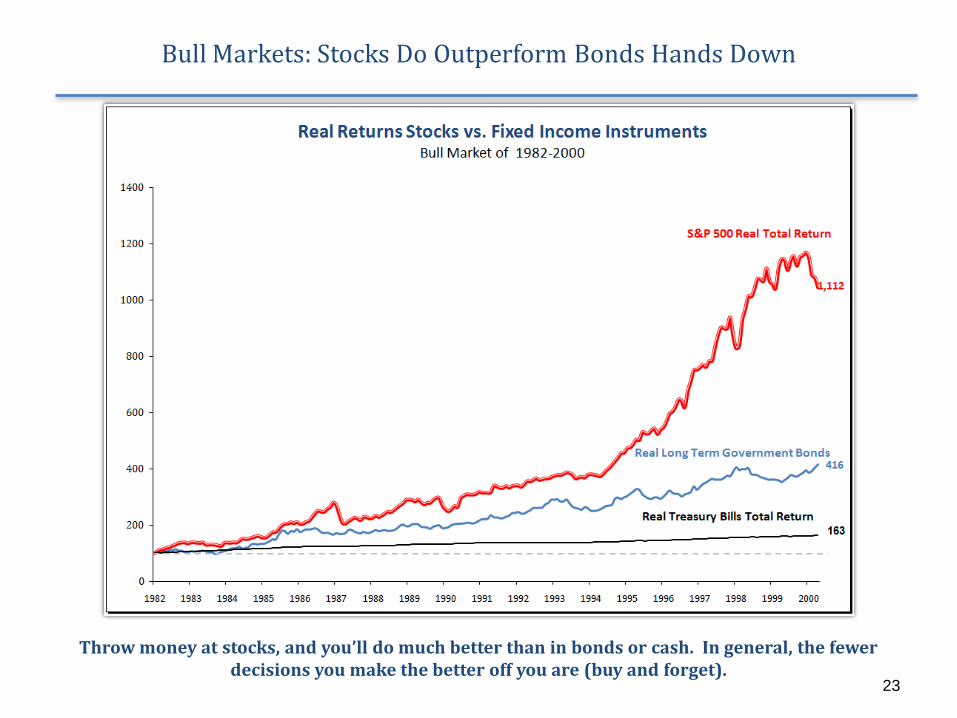

23

Bull Markets: Stocks Do Outperform Bonds Hands Down

Throw money at stocks, and you’ll do much better than in bonds or cash. In general, the fewer decisions you make the better off you are (buy and forget).

24

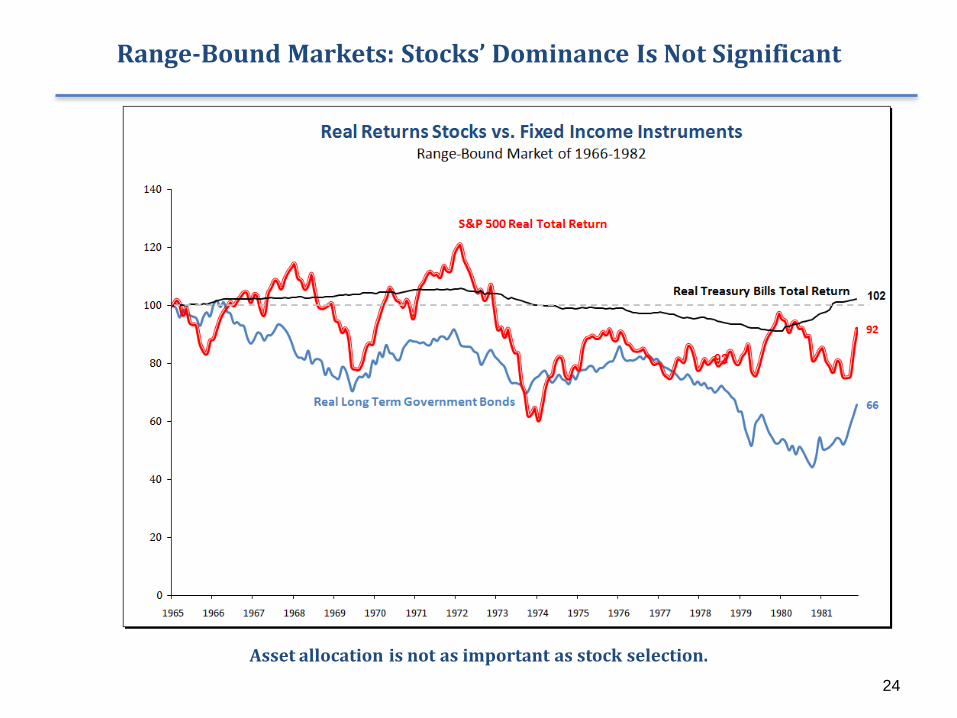

Range-Bound Markets: Stocks’ Dominance Is Not Significant

Asset allocation is not as important as stock selection.

25

Conclusion: Stock Selection Matters A Lot!

26

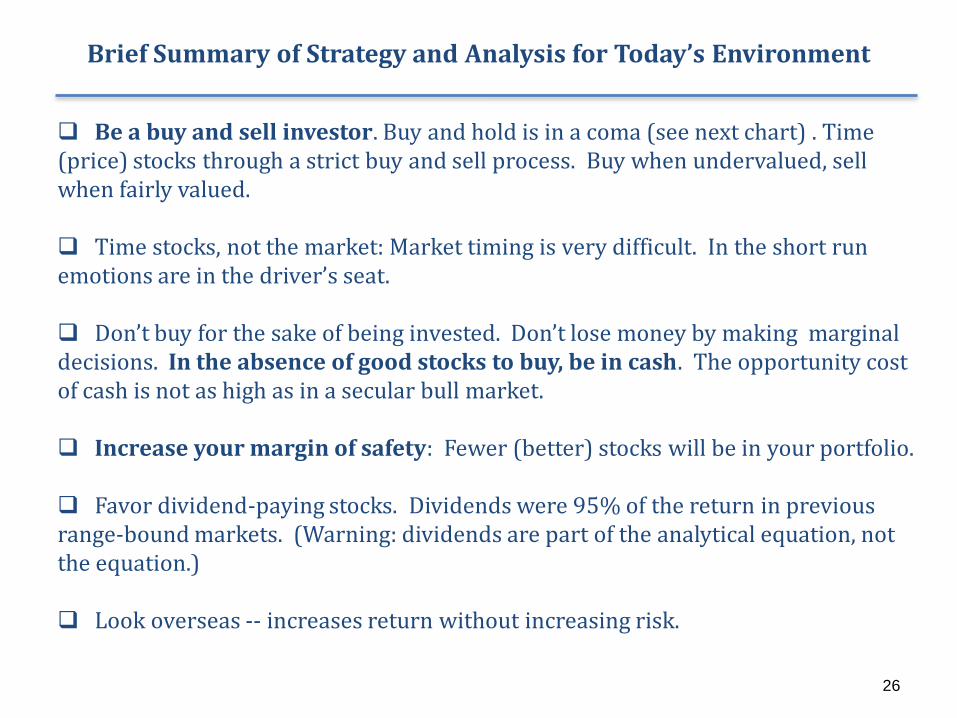

Brief Summary of Strategy and Analysis for Today’s Environment

Be a buy and sell investor. Buy and hold is in a coma (see next chart) . Time (price) stocks through a strict buy and sell process. Buy when undervalued, sell when fairly valued.

Time stocks, not the market: Market timing is very difficult. In the short run emotions are in the driver’s seat.

Don’t buy for the sake of being invested. Don’t lose money by making marginal decisions. In the absence of good stocks to buy, be in cash. The opportunity cost of cash is not as high as in a secular bull market.

Increase your margin of safety: Fewer (better) stocks will be in your portfolio.

Favor dividend-paying stocks. Dividends were 95% of the return in previous range-bound markets. (Warning: dividends are part of the analytical equation, not the equation.)

Look overseas -- increases return without increasing risk.

27

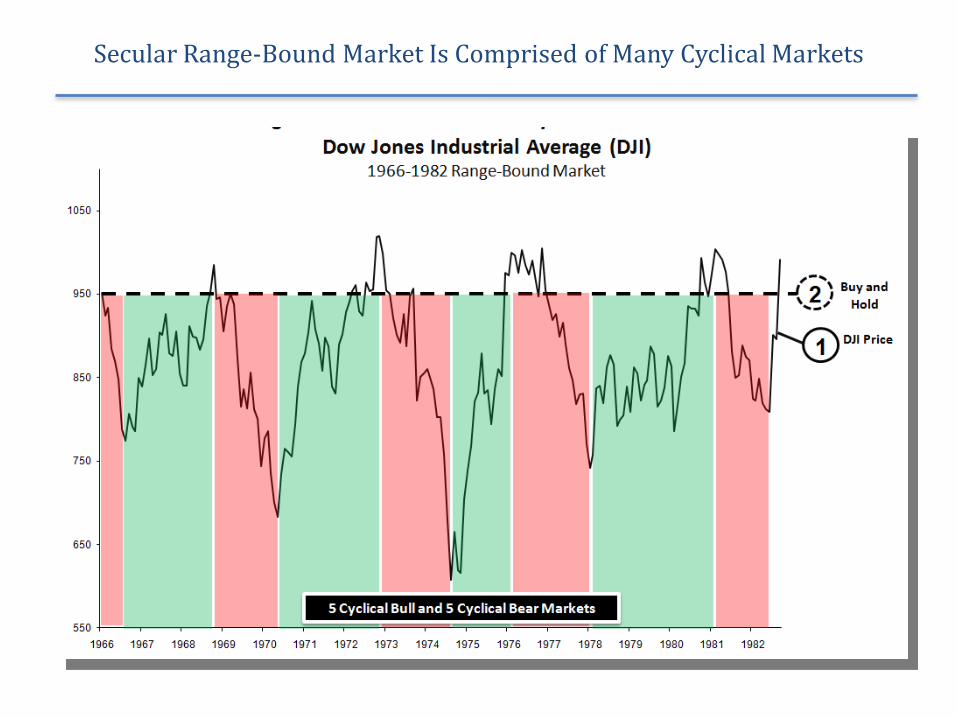

Secular Range-Bound Market Is Comprised of Many Cyclical Markets

28

Thank You!

To signup for complimentary articles via email visit

www.ContrarianEdge.com

More information about the book and for PDF of this presentation visit

www.ActiveValueInvesting.com

Investment Management Associates Inc.7979 E. Tufts Ave, Suit 820, Denver, Co 80237

303.796.8333 / www.imausa.com

29

30

On the surface, the vital signs of our economy are improving:

• Employment is declining at a slower rate

• GDP’s stopped declining and started growing

But what you see on the surface is very deceiving. Here is how we view our economy:

• Like a marathon runner who runs too hard and hurts himself. But now he has another race to run. So he’s injected with some serious, industrial-quality steroids, and away he goes. He’s up and running, so he must be ok. What we don’t see is what is behind this athlete’s terrific performance – the steroids.

Value investment approach needs to be

adjusted for this very different economy

31

Serious steroid intake comes at a cost:

• It exaggerates true performance.

• Steroids are addictive; once we get used to their effects it is hard to give them up.

• The longer we take them the less effective they are.

• They damage the athlete’s body.

32

Our economy suffered severe injuries last year and now there is a giant IV hooked up to the veins of the economy, through which billions of dollars are constantly being pumped.

The stimulus is everywhere:

Auto industry

To help the auto industry taxpayers were subsidizing the price of autos and thus were creating artificial demand.

GMAC is to receive a third government bailout. So far taxpayers have pumped $13.5 billion into GMAC.

The housing market

On one side there is a buyer (used to be just first-time buyer, now it is any buyer) tax credit.

Interest rates are kept artificially low by the Fed’s quantitative easing, fancy econ-speak for the Federal Reserve buying long-term bonds.

Fannie and Freddie -- (now) defunct, government-controlled, they are the mortgage market of our economy, accounting for the bulk of new mortgages originated today.

33

Banking Sector

Banks are the conduits through which the government pumps stimulus into the economy. The aforementioned government involvement in the housing market helps them generate enormous fees.

Profitability is boosted (at the expense of savers) by almost zero short-term interest rates, again thanks to the friendly Fed. They earn a healthy interest-rate spread.

34

Infrastructure projects - giant, multi-hundred-billion-dollar infrastructure projects that are coming on line as you read this.

Unemployment benefits - government also extended unemployment benefits several times last year, spending billions in the process, and it's likely to continue doing this well into 2010.

Now let’s look at the side effects

• Our economy’s true, unsteroided, unstimulated performance is a lot lower than the one we observe.

Government can spend money at a high rate for longer than one would rationally expect. Stimuli are finite, come with heavy price tags, financed with higher future taxes and rising government debt, thus higher future interest rates.

35

Steroids and stimulus are both addictive and have consequences

Once we’re used to them it’s hard to give them up, as the short-term consequences bring pain. The $8,000 tax credit started as a temporary measure. The program was extended and supersized by providing the tax credit to anyone with the patriotic ambition to buy a house.

The longer we stimulate the economy the less effective stimuli become. Japan has been on a zero-interest-rate policy since the 1990s. Now it is a prisoner of zero interest rates, as its economy is geared that way. Now, even a small increase in interest rates (say, from 1% to 2%) would be devastating for Japan’s economy.

Not a viable long-term solution. Japan has been on the stimulus bandwagon since 1990 and has nothing to show for it except government debt-to-GDP tripling.

Stimulus just rewinds future sales to an earlier date, at the taxpayer’s expense. After Cash for Clunkers ran its course, demand for autos fell into the abyss. The same will be the fate of industries exposed to infrastructure projects.

36

Consequences

Postpone our problems into the future. Results in higher debt and higher taxes.

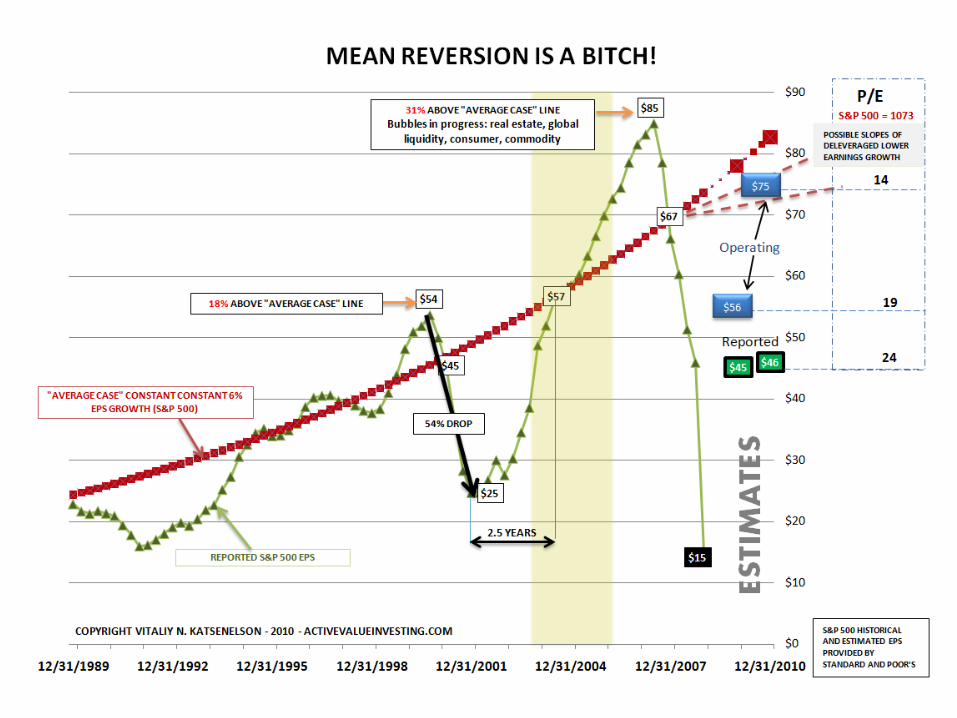

Stimuli cause bubbles. The fix for the 2002 recession involved interest rates staying at extremely low levels for a long time, and resulted in the housing/liquidity bubbles we’re paying for today. The present stimuli will leave us with even more serious damage, somewhere down the line.

Stimulus creates an appearance of stability and growth, but a lot of it is teetering on a very weak foundation of government intervention.

The hopes that we’ll painlessly transition from government steroiding back to an economy running on its own are overoptimistic; there is just too much stimulus in the economy for that to happen. The detox process from the massive consumption of steroids will not be smooth and painless.

37

Process adjustments for this economy

38

Defensive posture in stock selection. The portfolio is positioned for subdued economic recovery. We ask ourselves a question: what is the company’s true earning power after stimulus runs its course?

Earning power of our stocks should remain intact in the absence of recovery or post-stimulus.

Economic recovery should benefit our stocks. However, if the pace of recovery is off the charts our stocks will lag (junky) cyclical stocks. We’d rather make less money than lose money. In other words, we’d rather give up a low-probability / high-return opportunity than lose money.

Cyclical stocks are priced as if in the go-go days of 2002-2007 global growth, which was predicated on several bubbles colliding, and will come back after $3.5 trillion in global stimulus is out of the system post-2010. Though governments will try, Act II of the 2002-2007 bubble will be hard to pull off (at least not this soon – the wounds are too fresh).

Stock selection, stock selection, stock selection. It is paramount to distinguish between what is real and what is not.

Do not buy marginal stocks for the sake of diversification. Investment success will not only depend on what stocks you own but also on the ones you don’t. We won’t subject the portfolio to unattractive risk/reward scenarios for the sake of diversification.

39

Err on the side of quality

• Pricing power. We don’t know when or if we’ll have inflation, but in case of inflation we want to own companies with pricing power.

• Strong balance sheets. We are assuming that interest rates will rise in the future (with or without inflation). We want low debt levels or the ability to pay off debt in a few years from very stable cash flows.

• Quality stocks should outperform low-quality stocks in a low-growth or deflationary environment. According to GMO, quality stocks have outperformed low-quality stocks in Japan during its multi-decade debacle. (Our explanation for this: Deflation causes risk premiums to skyrocket, high quality is rewarded.)

The US is not Japan, but economic growth rate will likely be lower over the next decade than in the past (deleveraging is a lengthy process).

40

41

Thank You!

To signup for complimentary articles via email visit

www.ContrarianEdge.com

More information about the book and for PDF of this presentation visit

www.ActiveValueInvesting.com

Investment Management Associates Inc.7979 E. Tufts Ave, Suit 820, Denver, Co 80237

303.796.8333 / www.imausa.com

![[CONTINUED FROM FRONT FLAP] $39.95 USA | $47.95 CAN€¦ · —VITALIY KATSENELSON Director of Research at Investment Management Associates, Inc., and author of Active Value Investing:](https://img.pdfslide.us/doc/110x75/5b0d8e0d7f8b9ab7658c93c0/continued-from-front-flap-3995-usa-4795-can-vitaliy-katsenelson-director.jpg)