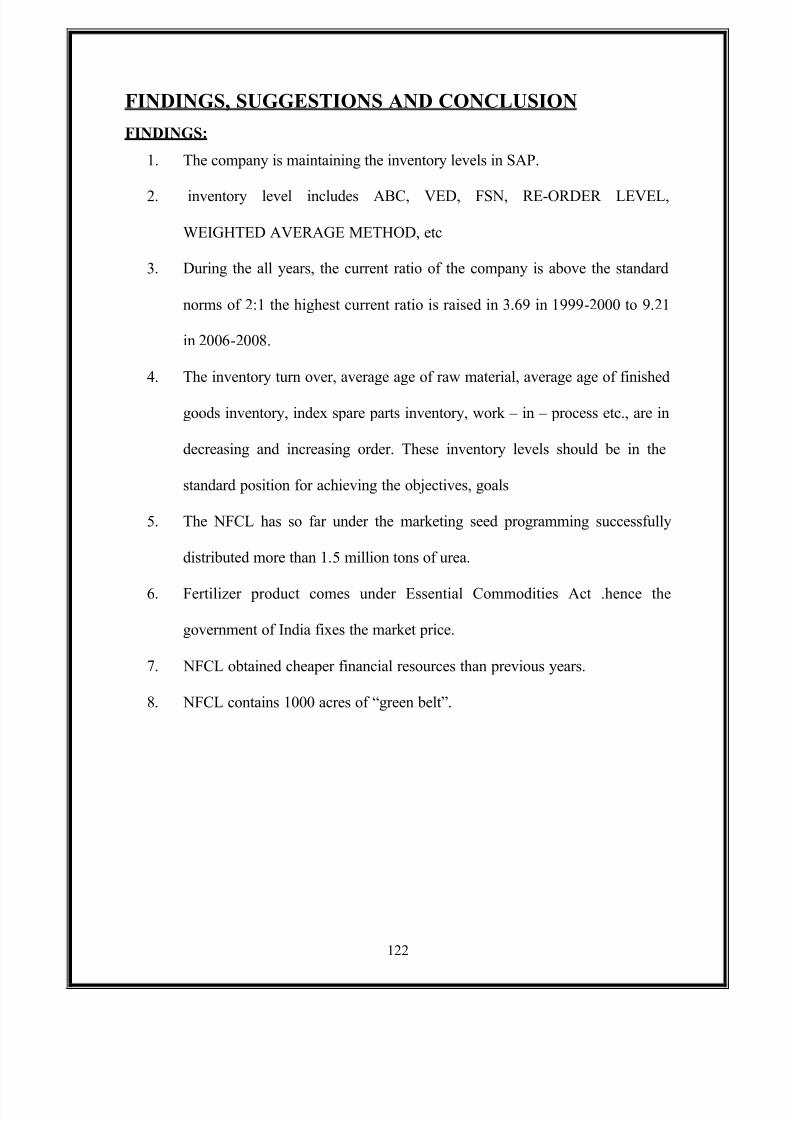

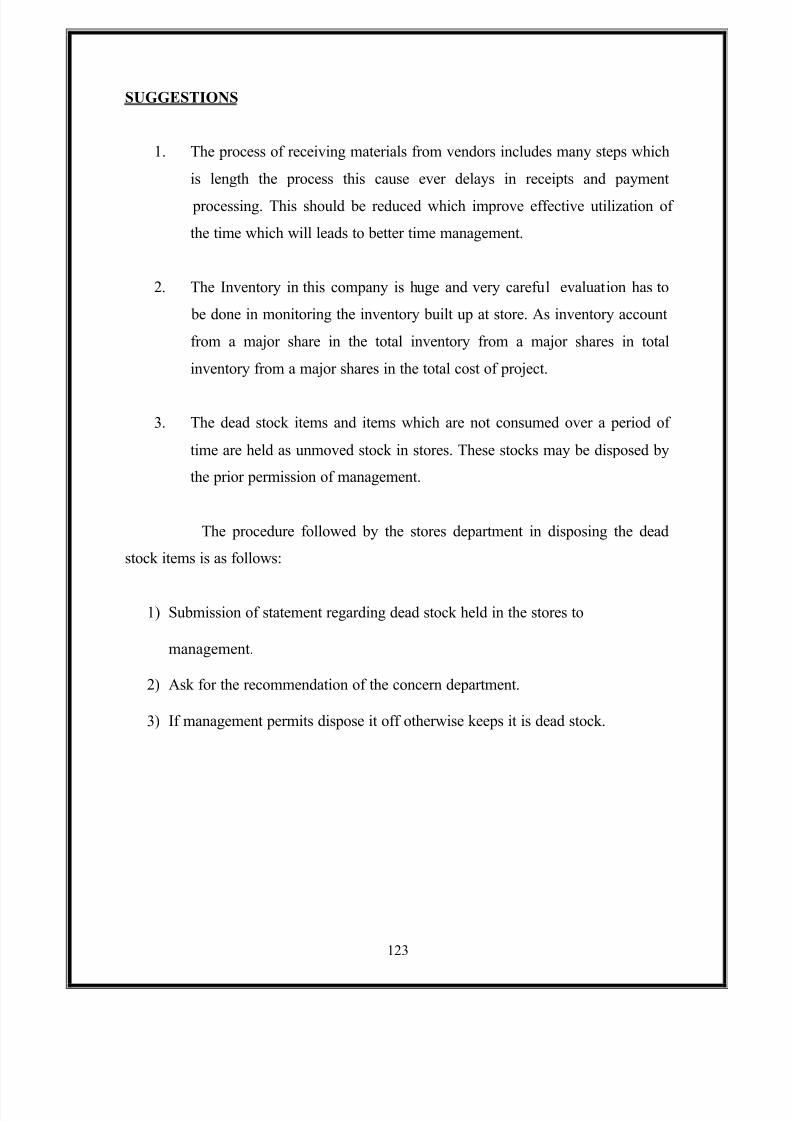

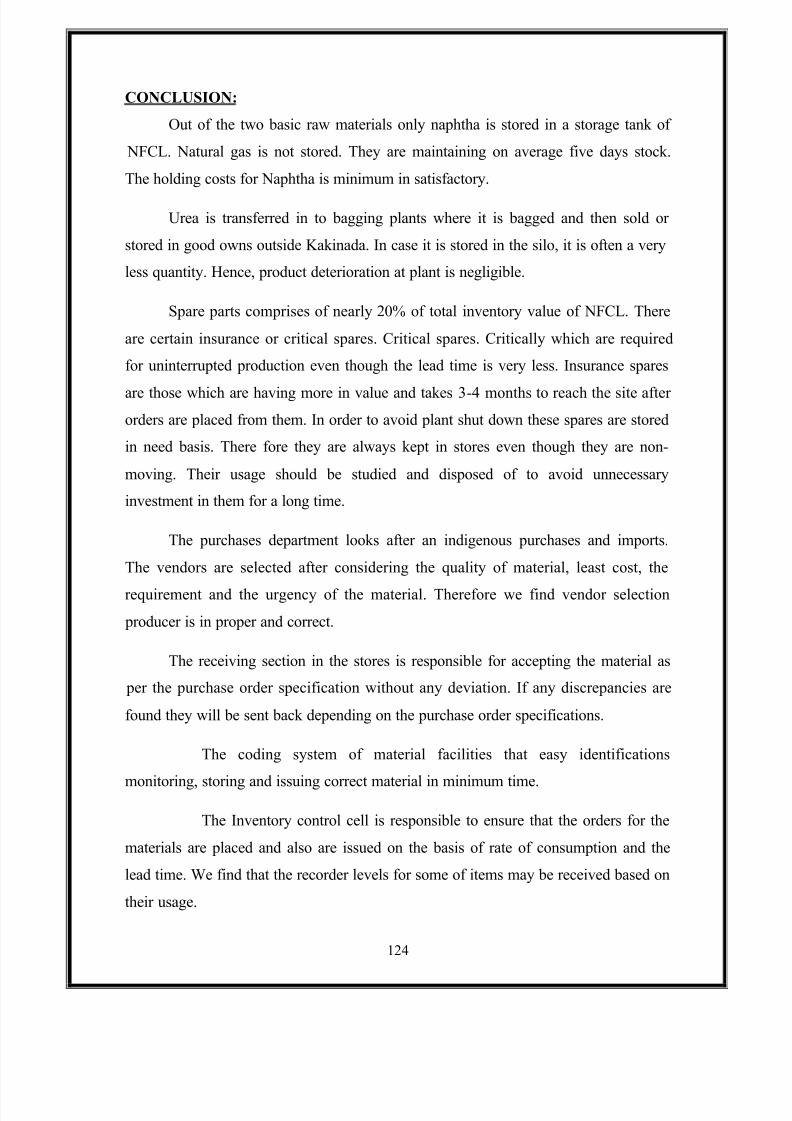

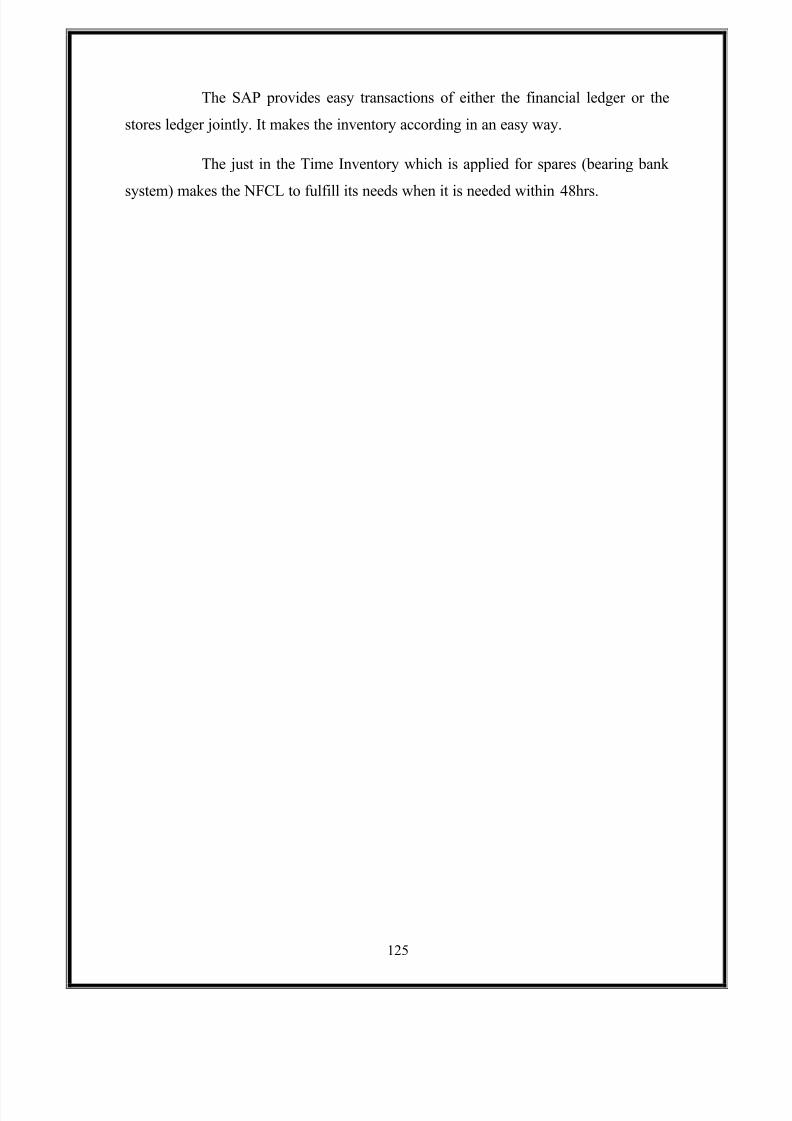

Embed Size (px)

Citation preview

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 1/126

1

A STUDY ON

INVENTORY MANAGEMENT

WITH REFERENCE TO

NAGARJUNA FERTILIZERS AND CHEMICALS LTD

KAKINADA

A project report submitted to the Department of Management Studies, jntuk,

Kakinada, in partial Fulfillment for the award of the degree of

MASTER OF BUSINESS ADMINISTRATION

Submitted by

G PRABHAKAR REDDY

NALANDA INSTITUTE OF TECHNOLOGY

SATTENAPALLI(KANTEPUDI)

2009 - 2011

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 2/126

2

ACKNOWLEDGMENT

I take this opportunity to express my gratitude to

SRI.S.KRISHNA MURTHY,DGM(PLANT HPD),

Mr. P.S.N. MURTHY, D.G.M (FINANCE),

for giving me the privilege to undergo project work on

³A STUDY on Inventory management in NFCL.´

I would like to express my sincere thanks to

Smt Y.RAMADEVI ,HEAD TRAINING &DEVELOPMENT,

of NFCL, who guided me throughout tenure of this project, work

in innumerable ways.

In the presentation of this report I recall with a sincere

gratitude to each of those who have been a source of immense help

and inspiration during the process of my project work. I feel grateful

to my family members and friends for their kind co-operation.

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 3/126

3

DECLARATION

I hereby declare that this project entitled

³INVENTORY MANAGEMENT´ with reference to

³NAGARJUNA FERTILIZERS AND CHEMICALS LTD,

KAKINADA´ is the original work done by me and submitted

to JNTUK, KAKINADA in partial fulfillment of the

requirement for the award of the degree of

MASTER OF BUSINESS ADMINISTRATION and this

has not been submitted to any other university or publication

any time.

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 4/126

4

CONTENTS

CHAPTER-I

INTRODUCTION

SCOPE OF THE STUDY

SIGNIFICANCE OF THE STUDY

OBJECTIVES

METHODOLOGY

LIMITATIONS

CHAPTER-II

INDUSTRY PROFILE

CHAPTER-III

COMPANY PROFILE

CHAPTER-IV

THEORETICAL FRAMEWORK

CHAPTER-V

ANALSIS &INTERPRETATIONS

CHAPTER-VI

FINDINGS

SUGGESTIONS

CONCLUSION

BIBLOGRAPHY

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 5/126

5

INTRODUCTION

Finance is regarded as ́ THE LIFE BLOOD OF BUSINESS

ENTERPRISEµ. Finance function has become so important that it has given

birth to financial management as a separate subject. So, this subject is

acquiring universal applicability. Financial Management is that managerial

activity which is concerned with the planning and controlling of the firm·s

financial resources. As a separate activity or discipline is of recent origin it

was a branch of economics till 1890. Still today it has no unique knowledge

of its own, and it draws heavily on economy for its theoretical co ncepts.

The subject of financial management is of immense interest to both

academicians and practicing managers. It is of great interest to

academicians because the subject is still developing, and there are still

certain areas where controversies exist for which no unanimous solutions

have been reached as yet. Practicing Managers are interested in this subject

because among the most crucial decisions of the firm are those which relate

to finance and an understanding of the theory of financial managemen t

provides them with conceptual and analytical insights .

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 6/126

6

Scope of Finance Management:

Firms create manufacturing capacities for production for goods; some

provide services to customers. They sell their goods or services to earn

profits. They raise funds to acquire manufacturing and other facilities.

Thus, the three most important activities of a business firm are:

Production

Marketing

Finance

A firm secures whatever capital it needs and employees it (finance

activity) in activities that generate returns on invested capital (production

and marketing activities). A business firm thus is an entity that engages in

activities to perform the functions of finance, production and marketing.

The raising of capital funds and using them for generating returns to the

supplies of funds is called the finance function of the firm.

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 7/126

7

FUNCTIONS OF FINANCIAL MANAGEMENT

Two significant contribution to the development of

modern theory of financial management are:

Theory of Portfolio Management developed by Harry Markowitz in

1950, which deals with portfolio selection with risky investment. This

theory uses statistical concepts to quantify the risk -return

characteristics of holding a group/portfolio of securities, investment

or assets.

The theory of Leverage and Valuation of Fire developed by Modigliani

and Miller in 1958. They have shown by introducing analytical

approach as to how the financial decision making in any firm be

oriented towards maximization of the value of the firm and the

maximization of the shareholders wealth.

Type of Financial Actions:

1. The Financial Management of trading or manufacturing firms

2. Financial Management of Financial Institutions.

3. Financial activities relating to investment activities.

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 8/126

8

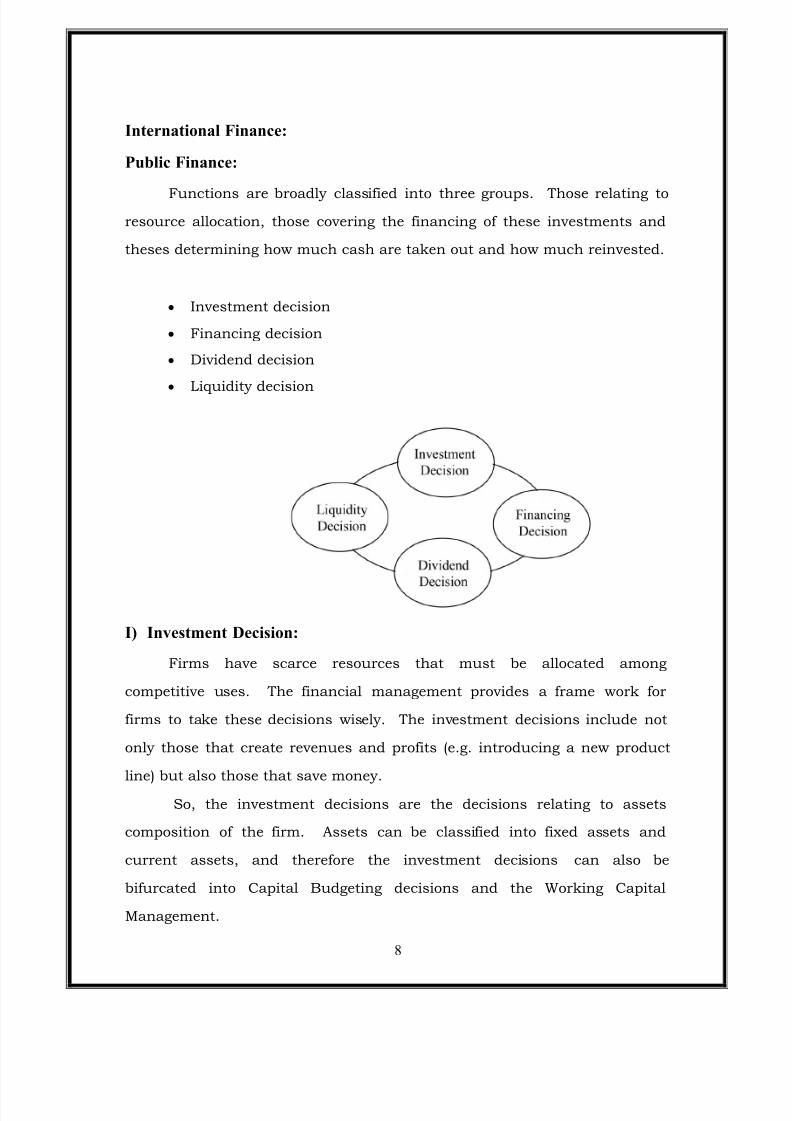

International Finance:

Public Finance:

Functions are broadly classified into three groups. Those relating to

resource allocation, those covering the financing of these investments and

theses determining how much cash are taken out and how much reinvested.

y Investment decision

y Financing decision

y Dividend decision

y

Liquidity decision

I) Investment Decision:

Firms have scarce resources that must be allocated among

competitive uses. The financial management provides a frame work for

firms to take these decisions wisely. The investment decisions include not

only those that create revenues and profits (e.g. introducing a new product

line) but also those that save money.So, the investment decisions are the decisions relating to assets

composition of the firm. Assets can be classified into fixed assets and

current assets, and therefore the investment decisions can also be

bifurcated into Capital Budgeting decisions and the Working Capital

Management.

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 9/126

9

The Capital Budgeting decisions are more crucial for any firm. A

finance manager may be asked to decide about.

1. Which asset should be purchased out of different alternative options;

2. To buy an asset or to get it on lease;

3. To produce a part of the final product or to procure it from some other

supplier;

4. To by or not an other firm as a running concern;

5. Proposal of merger of other group firms to avail the synergies o f

consolidation.

Working Capital Management, on the other hand, deals with the

Management of current assets of the firm. Though the current assets do not

contribute directly to the earnings, yet their existence is necessitated for the

proper, efficient and optimum utilization of fixed assets. There are dangers

of both the excessive working capital as well as the shortage of working

capital. A finance manager has to ensure sufficient and adequate working

capital to the firm.

II) Financing Decisions:

As firms make decisions concerning where to invest these resources,

they have also to decide two they should raise resources. There are two

main sources of finance for nay firm, the shareholders funds and the

borrowed funds. The borrowed funds are always repayable and require

payment of a committed cost in the form of interest on a periodic basis. The

borrowed funds are relatively cheaper but always entail risk.

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 10/126

10

The risk is known as the financial risk i.e., the risk of insolvency due to non -

payment of interest or non-repayment of capital amount. The shareholders

fund is the main source of funds to any firm.

This may comprise of the equity share capital, preference share capital and

the accumulated profits. Firms usually adopt a policy of employing both the

borrowed funds as well as the shareholders funds to finance their activities.

The employment of these sources in combination is also known as financial

management.

III) Dividend Decisions:

Another major area of the decision marking by a finance manager is

known as the Dividend decisions which deal with the appropriation of after

tax profits. These profits are available to be distributed among the

shareholders or can be retained by the firm for reinvestment with in the

firm. The profits which are not distributed are impliedly retained in the

firm. Al firms whether small or big, have to decide how much of the profits

should be reinvested back in the business and how much should be taken

out in form of dividends i.e., return on capital. On one hand, paying out

more to the owners may help satisfying their expectations; on the other

hand, doing so has other implications as a business that reinvests less will

tend to grow slower.

Reinvestment opportunities available to the firm,

The opportunity rate of the shareholders .

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 11/126

11

IV) Liquidity Decisions:

Current assets management that affects a firm·s

liquidity is yet another important finance function, in addition to the

management of long-term assets. Current assets should be managed

efficiently for safeguarding the firm against the dangers of illiquidity

and insolvency. Investment in current assets a ffects the firm·s

profitability, liquidity and risk.

The Identification of the relevant groups:

The various groups which may have stakes in the financial decisions

making of a firm and therefore required to be3 considered while taking

financial decisions are:

The shareholders

The debt investors,

The employees,

The customer and the suppliers,

The public,

The Government, and

The Management

Objective of the Financial Decision Making

The following two are often considered as the objectives of the

financial management.

The maximization of the profits of the firm, and

The maximization of the shareholders wealth

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 12/126

12

Maximization of the Profits of the firm:

For any business firm, the maximization of the profits is often

considered as the implied objective and therefore it is natural to retain the

maximization of profit as the goal of the financial also.

The profit maximization as the objective of financial management has

a built in favour for its choice. The profit is regarded as yard stick for the

economic efficiency of any form. If all business firm of the society are

working towards profit maximization then the economic resources of the

society as a whole would have been most efficiently, economically and

profitably used. The profit maximization by one firm and if targeted by all,

will ensure the maximization of the welfare of the society. So, the profit

maximization as objective of financial management will result inefficient

allocation of resources not only from the point of view of the firm but also for

the society as such.

It ignores the risk.

The profit maximization concentrates on the profitability only and

ignores the financing aspect of that decision and the risk associated

with that financing.

It ignores the timings of costs and returns and thereby ignores the

time value of money

The profit maximization as an objective is ague and ambiguous.

The profit maximization may widen the gap between the perception of

the management and that of the shareholders.

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 13/126

13

The profit maximization borrows the concept of profit from the field of

accounting and thus tends to concentrate on the immediate effect of a

financial decisions as reflected in the increase in the profit of that year

or in near future.

Maximization of Shareholder Wealth:

This objective is generally expressed in term of maximization of the

value of a share of a firm. It is necessary to know and determine as to how

the maximization of shareholders wealth is to be measured.

The measure of wealth which is used in financial management is the

concept of economic value. The economic value is defined as the present

value of the future cash flows generated by a decision, discounted as

appropriate rate of discount which reflects the degree of associated risk.

This measure of economic value is based on cash flows rather than profit.

The economic value concept is objective in its approach and also takes into

account the timing of cash flows and the level of risk through the

discounting process .

Profit Maximization Versus Wealth Maximization:

The objective of profit maximization measures the performance of a

firm by a looking at its total profit. The objective of maximization of the

shareholders wealth is operational and objective in its approa ch. A firm that

wishes to maximize the profits may opt to pay no dividend and to reinvest

the retained earnings, whereas a firm that wishes to maximize the

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 14/126

14

shareholders wealth may pay regular dividends .

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 15/126

15

THE CHANGING ROLE OF FINANCIAL MANAGEMENT:

Many changes in the contemporary world, financial management has

undergone significant changes over the years. The financial management

has a very limited role in business enterprise. Finance Manger is responsible

only for maintaining financial records, preparing reports of the company·s

status, performance and arranging funds recorded by company so that it

would meet its obligations in time.

Financial Manager as a matter of act was regarded as specializes

officers in the company concerned only with administer ing sources of funds,

he has called upon only when the company experimental the problem

relates the financial managers to locate the suitable sources for funds and

additional funds. The emphasis on decision making has continued in recent

years.

First there was been increased belief the cost of capital producer the

required accurate measurement of the cost of capital.

Secondly, capital has been in short supplies the old interest in the

ways of raising funds.

Thirdly, there was has been a continued managerial activity that has

led to revealed interests in takeovers.

Fourthly, accelerated progress in transportation and communication

has brought the countries of the world close together.

They in turn have stimulated interest in the international finance.

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 16/126

16

IMPORTANCE OF FINANCIAL MANGEMENT:

Finance Management is of greater importance on the present

corporate world. It is a science of money, which permits the authorizes to go

further.

SIGNIFICANCE OF FINANCIAL MANAGEMENT CAN BESUMMARISED AS:

It assists in the assessment of financial needs of industry large or

small and indicates the internal and external resources for meeting them. It

assesses the efficiency and effectiveness of the financial institution in

mobilizing individual or corporate science. It also prescribes various means

for such mobilization of savings into desirable investment channels.

It assists the management while investing the funds in profitable

projects by analyzing the viability of that project through capital budgeting

techniques. It permits the management to safeguard against the interest of

shareholders by properly utilizing the funds procured from different sources

and it also regulates and controls the funds to get maximize use.

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 17/126

17

SCOPE OF THE STUDY:-

The scope of my study is confined to one of the key areas of finance i.e.

inventory management. The study concentrates on the methods and techniques

followed by NAGARJUNA FERTILIZERS AND CHEMICALS LTD for its

inventory management and its relative merits and demerits.

The study appraises the company¶s success in meeting the requirements of the

company and the country by helping the farmers to raise agriculture output to

meet the requirement of the country¶s growing population for food grains.

PURPOSE OF THE STUDY:-

To study about the inventory management at NAGARJUNA

FERTILIZERS AND CHEMICALS LTD and to have an idea about the

utilization of the inventory and little more about the storage procedure that are

practically implemented in organization. Inventory plays a vital role in every

manufacturing organization to have an uninterrupted production process by

maintaining an optimum level of raw materials available at all time.

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 18/126

18

OBJECTIVES OF THE STUDY:-

The study titled ³INVENTORY MANAGEMENT´- A case study of

Nagarjuna fertilizers and chemicals ltd., has been carried out with the following

objectives.

To find whether the NFCL ensures a continuous supply of materials to

facilitate uninterrupted production.

To study the inventory management policies, techniques and their

effectiveness.

To give suggestions to increase inventory turnover.

To make an appropriate investment in inventories and keep it at an optimum

level.

To study the efficiency with which the firm is utilizing its inventory management

skills in generating more sales

To study the extent to which the firm has used its inventory management skills and

maximize the wealth of the organization.

This study is made to know whether the inventory is properly managed or not.

To review the structure, original growth and performance of NFCL during the study

period.

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 19/126

19

METHODOLOGY OF THE STUDY

The required for this study would be collected through two sources i.e.,

1. Primary Data:

The primary data comprises information obtained by the candidate during

discussions with Heads of Departments and from the meeting with officials and staff.

2. Secondary Data:

The secondary data has been collected from information through Annual

Reports, Public Report, journals relating to fertilizers industry , Bulleting and other

Printed Materials supplied by the Company.

In the present study 1/4

th

of the total information of time is from primary data

and the rest is from the secondary data.

Both primary and secondary data were used in conducting this project

which is as follows:

METHODS

PRIMARY DATA SECONDARY DATA

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 20/126

20

LIMITATIONS:-

The below mentioned are the constraints under which my study has been

carried out

The study is limited to NFCL, Kakinada; it does not relate to any other

company of Nagarjuna Group or other firm¶s of Fertilizer Industry.

The smaller time frame for understanding this study is also a significant

limitation.

The ratios are calculated on the basis of past data; these are not future

indicators.

The scope of study is limited to the last five years balance sheets.

The analysis is made basing only on the Annual Reports of NFCL.

Most of the information has been kept confidential and as such is not passed on

as a part of the policy of the company.

Since the number and size of inventory is very large, all the raw materials

could not be included in the analysis.

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 21/126

21

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 22/126

22

INDUSTRY PROFILE

India has been predominantly considered as an agricultural dependent

economy. Agriculture plays a very dominant role as more than one-fourth of our GDP

come from this sector. Nearly 70% of population depends on the agriculture for their

lively-hood. The basic need for an agricultural dependant economy is fertilizers and

urea is one of the main fertilizers. India is the second largest manufacturing country

in the world.

All fertilizers consist if three main ingredients.

Nitrogen²(N) -- which promotes general plant growth

Phosphorous²(P) -- which promotes flowering

Potassium ± (K) ± which promotes strong roots.

The ingredients are mixed in various combinations because plants have different

needs.

The combinations are indicated by a three number code:

The first number is the percent of nitrogen (N)

The second number is the percent of phosphorus (P)

The third number is the percent of potassium (K)

About Fertilizer:

Fertilizer is simply, plant food. Just like the human body needs vitamins and

minerals, plants need nutrients in order to grow. Plants need large amounts of three

nutrients ± nitrogen, phosphorus, and potassium. These are commonly referred to as

macronutrients. Fertilizer makers take those three nutrients from nature and put them

into soluble forms that plants can easily use.

There are a number of other nutrients plants need in small amounts. These are

referred to as the minor nutrients, or micronutrients. These many nutrients are

typically produced separately, but end up being mixed together in varying amou nts to

match the needs of a particular crop. The analysis found on each bag or bulk

shipment of fertilizer tells the farmer or consumer the amount of nutrients being

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 23/126

23

supplied. States have a system of laws and regulations that ensure the fertilizer is

properly labeled and delivers the amount for nutrients stated on the bag.

Our world would be vastly different without commercial fertilizers. Following

the World War II, new technologies allowed for the rapid expansion of fertilizer

production. Coupled with growing food demand and the development of higher -

yielding crop varieties, fertilizer helped fuel the Green Revolution. Today, the

abundance of food we enjoy is just one way fertilizers help enrich the world around

us.

While fertilizers provide many important benefits that are necessary for our

way of life, the improper use of fertilizers can harm our environment. We¶ve used the

most recent developments in science to study our products and make sure safety

comes first.

FERTILIZER:

Fuel for growing plants just like humans and animals, plants need adequate

water, sufficient food, and protection from diseases and pests to be healthy.

Commercially produced fertilizers give growing plants the nutrients they crave in the

form they can most readily absorb and use: nitrogen (N), available phosphate (P) and

soluble potash (K), Elements needed in smaller amounts, or micronutrients, include

iron (Fe); zinc (Zn), copper (Cu) and boron (B).

Each crop year, certain amounts of these nutrients are depleted and must be

returned to the soil to maintain fertility and ensure continued, healthy future crops.

Scientists project that the earth¶s soil contains less than 20 percent of the organic plant

nutrients needed to meet our current food production needs. Therefore, through the

scientific application of manufactured fertilizers, farmers are meeting the challenge of

the future, today.

Another component of plant DNA is phosphate, which helps plants to usewater efficiently. It also helps to promote root growth and improves the quality of

grain and accelerates its ripening. And potassium, commonly called potash, is

important because it is necessary for photosynthesis, which is the production,

transportat ion and accumulation of sugars in the plant. Potash makes plants hardy and

helps them to withstand the stress of drought and fight off disease.

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 24/126

24

Fertilizer Types:

Because every crop is different and the soils and weather conditions crops are

grown in vary dramatically around the world, commercial fertilizers, which are

manufactured from natural sources, come in many formulations.

Combining air with hydrogen using natural gas as the feedstock makes

ammonia, the building block for nitrogen fertilizers. Ammoniated phosphates, which

include mono ammonium phosphate (MAP) and diammonium phosphate (DAP), are

made by reacting ammonia with phosphoric acid. Muriate of potash, also called

potassium chloride, is made from mine ores that have been processed to remove

naturally occurring salts.

Ammonium nitrate is a solid fertilizer containing approximately 34 percent

nitrogen that is water soluble and used in various fertilizer solutions. Aqua ammonia

is another nitrogen-based fertilizer made by combining ammonia with water. It

contains up to 25 percent nitrogen and is either app lied directly to the soil or is used to

manufacture phosphate fertilizers.

Nitrogen solutions are water solutions of ammonia, ammonium nitrate and,

sometimes, urea, a solid fertilizer containing approximately 45 percent nitrogen, and

other soluble compounds of nitrogen. Nitrogen solutions are used in ammoniating

super phosphate, the manufacture of complete fertilizer and for direct injection into

the soil. They vary in composition and nitrogen content and are sometimes applied

under pressure.

NITROGEN (N):

Nitrogen is a part of all plant proteins and is a component of DNA and RNA ±

the ³blueprints´ for genetic characteristics. It is necessary for plant growth andchlorophyll production. Nitrogen is the building b lock for many fertilizers. Where

does N come from? Nitrogen is present in vast quantities in the air, making up about

78 percent of the atmosphere. Nitrogen from the air is combined with natural gas in a

complex chemical process to make ammonia.

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 25/126

25

PHOSPHOURUS/PHOSPHATE (P):

Phosphorus as a nutrient is sometimes most valuable to plants when put near

the seed for early plant health and root growth. Plant root uptake is dependent on an

adequate supply of soil P. Phosphorus is relatively insoluble in water. The water in

most soils must replace all of the P in the soil water 2 to 3 times each day to meet the

crop¶s demand for P. Phosphorus compounds help in directing where energy will be

used. Phosphorus compounds are needed in plant photosynthesis to ³repackage´ and

transfer energy. Phosphate is also a component of DNA, so it is one of the building

blocks of genes and chromosomes. Phosphorus is involved in seed germination and

helps plants to use water efficiently. Where does P come from? Phosphorus occurs in

natural geological deposits. Deposits can be found in the U.S. and other parts of the

world.

Potassium/Potash (K):

Potassium protects plants against stresses. Potassium protects plants from cold

winter temperatures and helps them to resist invasion by pests such as weeds and

insects. Potassium stops wilting, helps roots stay in one place and assists in

transferring food. Potassium is a regulator. It activates plant enzymes and ensures the

plant uses water efficiently. Potassium is also responsible for making sure the food

you buy is fresh. Where does K come from? The element potassium is seventh in

order of abundance in the Earth¶s crust.

Through long-term natural processes K filters into the oceans and seas. Over

time, these bodies of water evaporate, leaving behind mineral deposits. Although

some of these deposits are covered with several thousands of feet of earth, it is mined

as potash or potassium chloride. Potash ore may be used without complex chemical

conversion; just some processing is necessary to remove impurities such as commonsalt.

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 26/126

26

INDUSTRY PROFILE FOR NFCL:

AMMONIA PROCESS The feed stock natural gas is disulphurised by conversion of stable organic sulphur

compounds into Hydrogen Sulphide in presence of Nickel Molybdenum catalyst

followed by adsorption of Hydrogen Sulphide on Zinc Oxide bed. The desulphurised

natural gas is mixed with super heated steam to give steam to Carbon ratio of 3.3:1,

preheated and fed to the catalyst tubes in Primary Reformer. The Primary Reformer

is a side-fired furnace with radiant burners. The natural gas, which is predominantly

methane, undergoes following reactions producing Hydrogen and Carbon Oxides:

CH4 + H2O ------------- 3 H2+ CO - heat

CO + H2O ------------- CO2 + H2 + heat

The process gas from the tubes is gathered by a collector system and sent to the

Secondary Reformer.

The Secondary Reformer is a refractory lined vessel containing Nickel catalyst. Air

from atmosphere comes in contact with the process gas from Primary Reformer.

Combustion of some part of Hydrogen and Met hane occurs consuming the total

oxygen in the air and the temperature rises to about 1300 deg. C. This supplies the

heat needed for completion of the endothermic reaction in the catalyst bed. Nitrogen

needed for ammonia synthesis gets introduced in to the system in the Secondary

Reformer through the process air. The gas leaving Secondary Reformer contains

residual Methane of 0.6%. The exit gas from Secondary Reformer is cooled to about

380 deg. C in the Waste Heat Boiler where high -pressure steam is generated.

The carbon monoxide formed in the reforming step is converted to CO 2 by water gas

shift reaction in two stages, namely, high temperature shift conversion and low

temperature shift conversion. The HT shift reaction takes place in presence of iron

oxide chromium oxide catalyst and LT shift reaction takes place in presence of

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 27/126

27

copper oxide zinc oxide catalyst. The shift conversion reaction being exothermic,

steam is produced by heat recovery.

The reaction-taking place in the shift conversion can be represen ted as:

CO + H2O --------- CO2 + H2 + heat

The process gas leaving the CO conversion step contains in addition to Hydrogen

and Nitrogen, large quantity of CO 2 and small quantities of CO, Argon and Methane.

The CO2 present in the process gas is removed in the CO 2 removal section using

Giammarco Vetrocoke process.

Here, CO2 absorbed in potassium Carbonate solution is regenerated by reducing the

pressure and addition of heat in two stage regenerators.

The regenerated solution is pumped back to the absorber. Thus, the system

operates in closed circulation. The CO 2 gas stripped from the solution in the

regenerators is cooled and sent to Urea plant.

The process gas exit absorber now contains only traces of CO and CO 2. Since

carbon oxides act as poison to the ammonia synthesis catalyst, the residual carbon

oxides present in the process gas are converted into methane in a methanator

reactor containing nickel catalyst. This step is the reverse of reforming reaction and

consumes a small amount of hydrogen.

The methanator exit gas after cooling and removal of condensate is the synthesis

gas with some inert. This gas is compressed from 24 Kg/Cm 2g to 134 Kg/Cm2g in a

centrifugal syn gas compressor. Also, there is a recirculation stage in the

compressor where the recycle of unconverted gas along with the compressed make

up gas are further compressed to about 142 Kg/Cm2g. This gas after pre-heating is

admitted to ammonia synthesis converter containing promoted iron catalyst, where

Hydrogen and Nitrogen combine to form ammonia with evolution of heat. The

ammonia synthesis reaction is:

N2 + 3 H2 ------------- 2 NH3 + heat

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 28/126

28

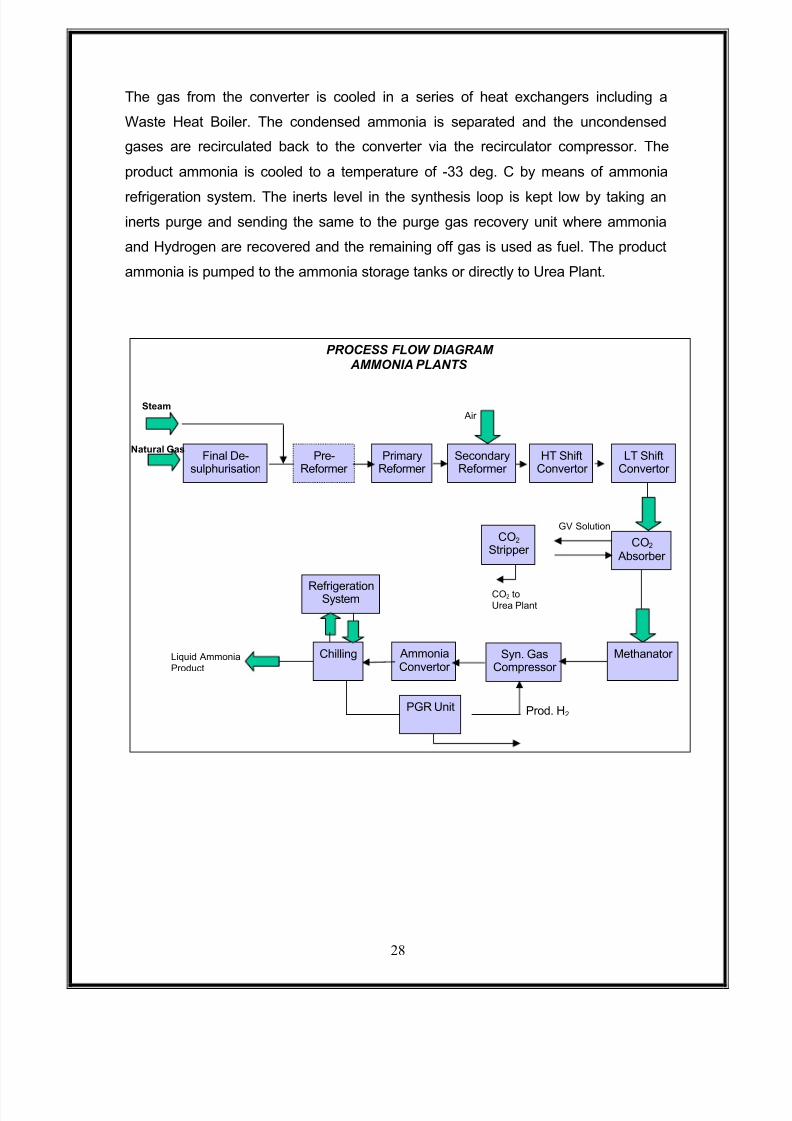

The gas from the converter is cooled in a series of heat exchangers including a

Waste Heat Boiler. The condensed ammonia is separated and the uncondensed

gases are recirculated back to the converter via the recirculator compressor. The

product ammonia is cooled to a temperature of -33 deg. C by means of ammonia

refrigeration system. The inerts level in the synthesis loop is kept low by taking an

inerts purge and sending the same to the purge gas recovery unit where ammonia

and Hydrogen are recovered and the remaining off gas is used as fuel. The product

ammonia is pumped to the ammonia storage tanks or directly to Urea Plant.

PROCESS FLOW DIAGRAM AMMONIA PLANTS

Steam

Final De-sulphurisation

Pre-Reformer

PrimaryReformer

SecondaryReformer

HT ShiftConvertor

LT ShiftConvertor

RefrigerationSystem

CO2 Stripper

CO2 Absorber

Chilling AmmoniaConvertor

Syn. GasCompressor

Methanator

PGR Unit

GV Solution

CO2 to

Urea Plant

Prod. H2

Liquid Ammonia

Product

Air

Natural Gas

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 29/126

29

U REA PLANT The production of Urea requires ammonia and CO 2 as the inputs, both of which are

available from Ammonia plant. The CO 2 from ammonia plant is compressed to about

160 Kg/CM2

and sent to the Urea Reactor. Liquid Ammonia is pumped using high -

pressure reactor feed pump and along with recycle carbamate enters into Urea

Reactor. Urea Reactor operates at about 156 Kg/CM2 and 188 deg. C. Following

reactions take place in the Urea Reactor:

2 NH3 + CO2 -------- NH2COONH4 (Ammonium Carbamate) +

heat

NH2COONH4 ----- CO (NH2)2 + H2O ± heat (Urea)

The product stream from the Urea Reactor contains in addition to Urea, large

quantity of unconverted ammonia, CO2 and water. The ammonium carbamate in the

product stream is recovered in three stages viz., high pressure stage, medium

pressure stage and low pressure stage by decomposing the carbamate into

ammonia and CO2, separating the gases from the liquid product stream and

recondensing the gases back to carbamate solution which is recycled back to the

Urea Synthesis Reactor. In this process, the product stream becomes richer and

richer in the urea content. In the high -pressure section, separation of Ammonia and

CO2 in the falling film of liquid in the tubes is stripped by ammonia vapour. Medium

pressure steam supplies the required heat. As the Urea Reactor operates with

excess ammonia, the excess ammonia is recovered in ammonia condenser. The

product stream leaving the low-pressure section contains 70% Urea. This is further

concentrated in the vacuum concentrators to get 99.8% Urea melt. This molten Urea

is pumped to the top of urea prilling tower and fed into a prilling bucket. The prilling

tower of 22-M diameter and 75 M free fall height operates under natural draft. The

Urea Prills from the bottom of the prilling tower are transported through mechanized

belt conveyor system into urea storage silo or directly to urea bagging plant. The

bagged urea is dispatched by rail wagons/road trucks.

Tail Gas as Fuel

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 30/126

30

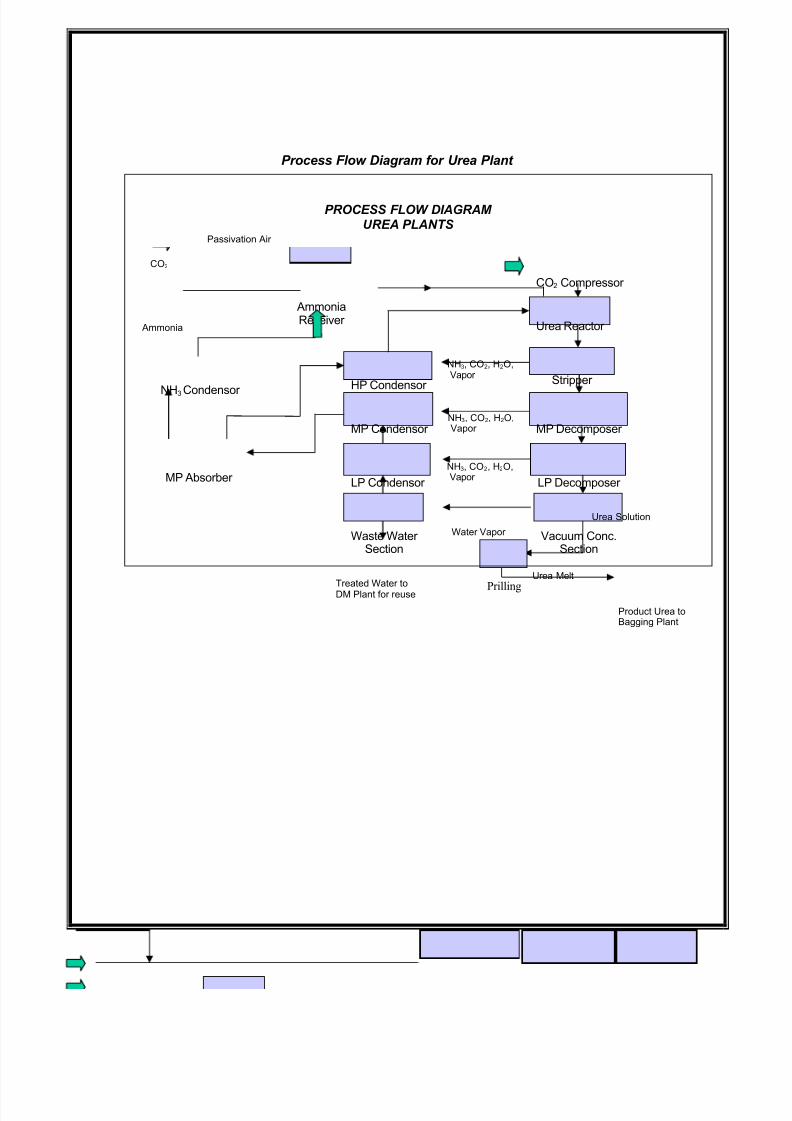

Process Flow Diagram for U rea Plant

PROCESS FLOW DIAGRAM U REA PLANTS

AmmoniaReceiver

NH3 Condensor

MP Absorber

CO2 Compressor

CO2

HP Condensor

MP Condensor

LP Condensor

Waste Water Section

Vacuum Conc.Section

LP Decomposer

MP Decomposer

Stripper

Urea Reactor Ammonia

Treated Water toDM Plant for reuse

Urea Melt

Water Vapor

NH3, CO2, H2O,Vapor

NH3, CO2, H2O,Vapor

NH3, CO2, H2O,Vapor

Passivation Air

Urea Solution

Prilling

Product Urea toBagging Plant

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 31/126

31

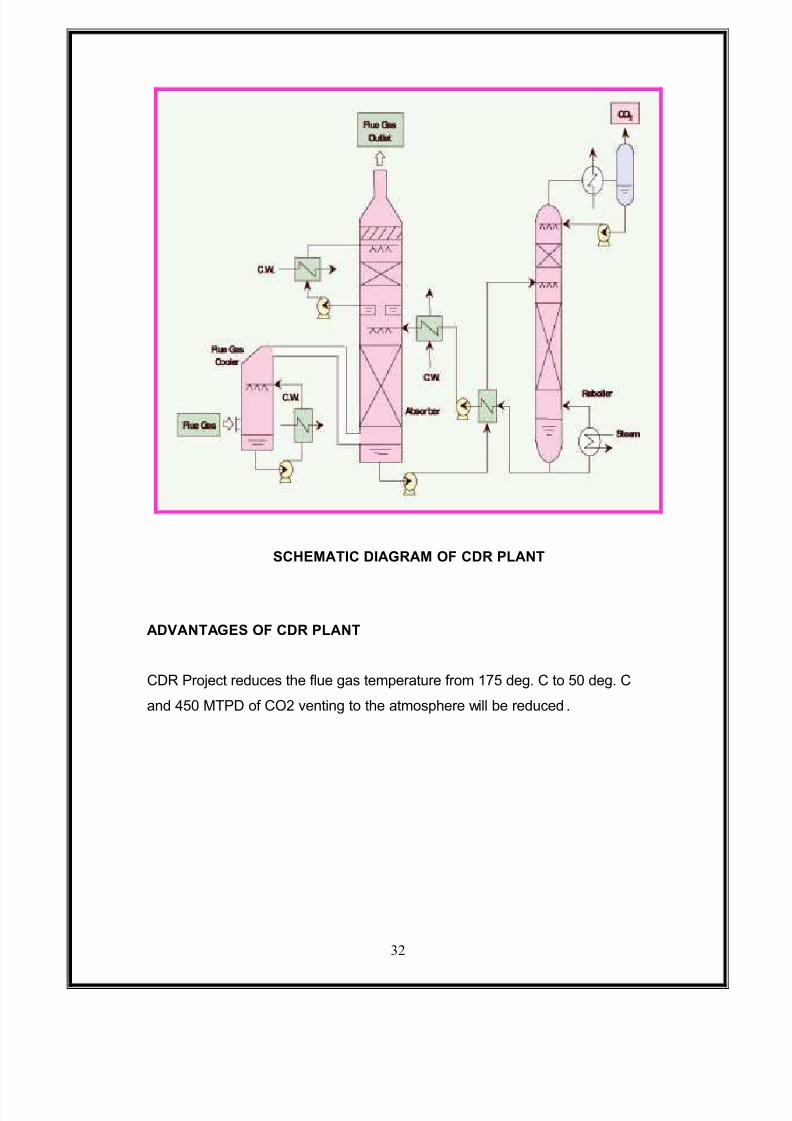

PROCESS DESCRIPTION OF

CARBON-DI-OXIDE RECOVERY (CDR) PLANT

Technology Supplier: Mitsubishi Heavy Industries (MHI), Japan.

CO2 Absorbent: KS-1 Solution, Proprietary Supply from MHI, Japan.

The Flue Gas from Primary Reformer enters the Flue Gas Quencher, where it is

cooled to 40°C. The Flue Gas is compressed to a pressure of 1.113 Ksca and enters

the CO2 Absorber. The CO2 in Flue Gas is absorbed by KS-1 Solvent, which is

distributed from top through packed bed system. Subsequent to contact with KS-1

Solution the Flue Gas is further washed with DM Water in the top section of CO2

Absorber. The Flue Gas after removal of CO 2 is sent out to atmosphere through a

stack provided at CO2 Absorber top. The CO2 rich solution at 55°C is pumped to the

Lean / Rich Heat Exchanger. The Lean Solution is recycled back to CO 2 Absorber.

The rich solution stream is heated up to 114 °C and sent to CO 2 Regenerator,

wherein CO2 is stripped off from rich solution by providing necessary heat to Reboiler

using Low Pressure Steam. The CO 2 thus liberated is washed with DM water at the

top of CO2 Regenerator, cooled to ambient temperature in an overhead condenser

and sent to Urea Plants.

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 32/126

32

SCHEMATIC DIAGRAM OF CDR PLANT

ADVANTAGES OF CDR PLANT

CDR Project reduces the flue gas temperature from 175 deg. C to 50 deg. C

and 450 MTPD of CO2 venting to the atmosphere will be reduced .

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 33/126

33

FOOD FOR THE GROWING WORLD

Industry at a glance:

Since 1883 the industry has worked to promote the advances in the

development and application of fertilizers that have helped to feed a hungry world.

The revolutionary concept of plant nutrition was born from the discovery of the

biological role of chemical elements in plant nutrition and the need to feed a growing

population concentrated away from the farm in the rising industrial centers of the

world.

Because of modern fertilizers, world food production since 1960 has more than

doubled, keeping pace with the population explosion. Today, the fertilizer industry is

poised to help produce the food that will be needed to feed the world¶s projected 9

billion people in 2025.

The fertilizer industry is essentially concerned with the provision of three

major plant nutrients ± nitrogen (N), phosphorous (P) and potassium (K) ± in plant

available form. Each nutrient is responsible for different aspects of plant growth and

health.

Fertilizers:

Regulated for quality and safety like other manufactured goods, fertilizers are

regulated for quality and safety at the federal and state levels. Every state in the

country, plus Puerto Rico, has its own fertilizer regulatory program, usually

administered by the state department of agriculture.

State Regulation:

State regulation is concerned with consumer protection, labeling, the protection

of human health and the environment, and the proper handling and application of

fertilizers. Fertilizers are regulated at the state level because soil conditions vary

dramatically from state to state across the country. For example, the rocky, thin soils

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 34/126

34

of New England are vastly different from the deep, rich black soils of the Midwest

Corn Belt. A different level of fertilizer nutrients in the soil, different crops (potatoes

versus corn, for instance) and different weather and cropping patterns require state-

specific regulation.

Where Science and safety come first the modern commercial fertilizer industry

was founded on the revolutionary scientific discovery in the last part of the 18th

century that chemical elements play a direct role in plant nutrition. This initial

concept was supported by direct scientific experiment and opened the way for

industrial-scale manufacturing of fertilizers of all types in the 19th

century, beginning

with superphosphate in 1843. This was followed by ammonium Sulphate, sodium

nitrate and, finally, in the first two decades of the 20th

century, the manufacturing of

synthetic nitrogen fertilizers directly from atmospheric nitrogen.

Assessing Fertilizer Safety:

Fertilizer research and development historically have been focused on

maximizing economic crop yields from given rates of nutrient application. Since the

advent of the modern environmental movement in the 1960s, research has also been

concerned with minimizing potentially adverse human health and environmental

effects from fertilizer manufacture and application.

As part of its continuing commitment to safety, in 1996, the Fertilizer Institute

initiated a comprehensive safety assessment project to determine the risks, if any, of

metals in fertilizer. Small amounts of metals are found in phosphate and potash

fertilizers due to their presence in the mined ore bodies. In addition to phosphate and

potash products, some micronutrient fertilizers, which come from both mined ores and

recycled wastes, also contain metals.

Fertilizers Enrich our World:

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 35/126

35

Improvements in agricultural efficiency through research and technology

increase food output while protecting the environment and enriching our world in

numerous ways.

Fertilizers feed the growing world. As the world¶s population continues to

climb toward an estimated 8.5 billion in 2040, experts estimate that food production

must increase more than two percent annually to even maintain current diets.

Commercial fertilizers will be the key in the fight to feed the growing world.

Fertilizers protect the environment. The efficient use of fertilizer also helps to

conserve the natural environment. With fertilizers and modern high yield farming

practices, more food is produced per acre each year, so land may be conserved.

Fertilizers, used properly, help to prevent the widespread loss of habitat that results

from wasteful ³slash and burn´ low-yield farming, which is a major global

environmental threat.

Fertilizers at work in industry:

Aside from their benefits to agriculture, fertilizer components are central to

such industrial process as semiconductor chip making, resin manufacture, cattle feed

production, metal finishing, the manufacture of detergents, fiberglass insulation and

more, even rocket fuel.

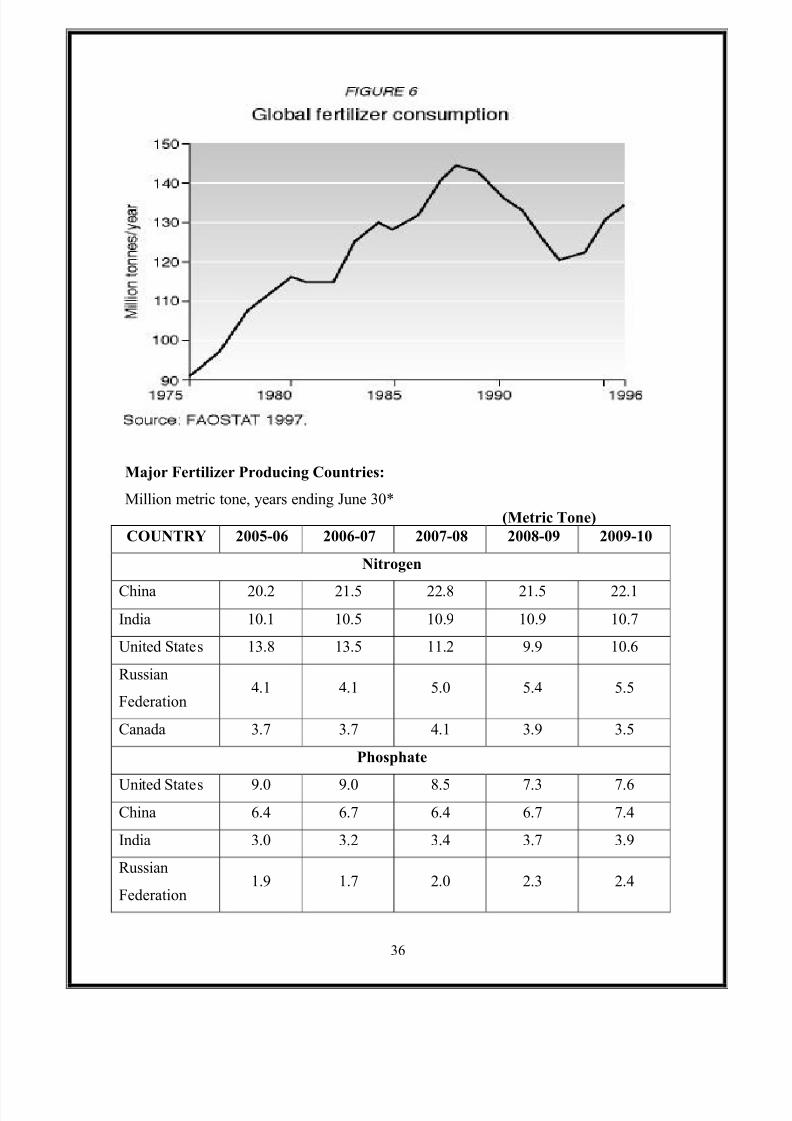

Global Fertilizer Consumption

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 36/126

36

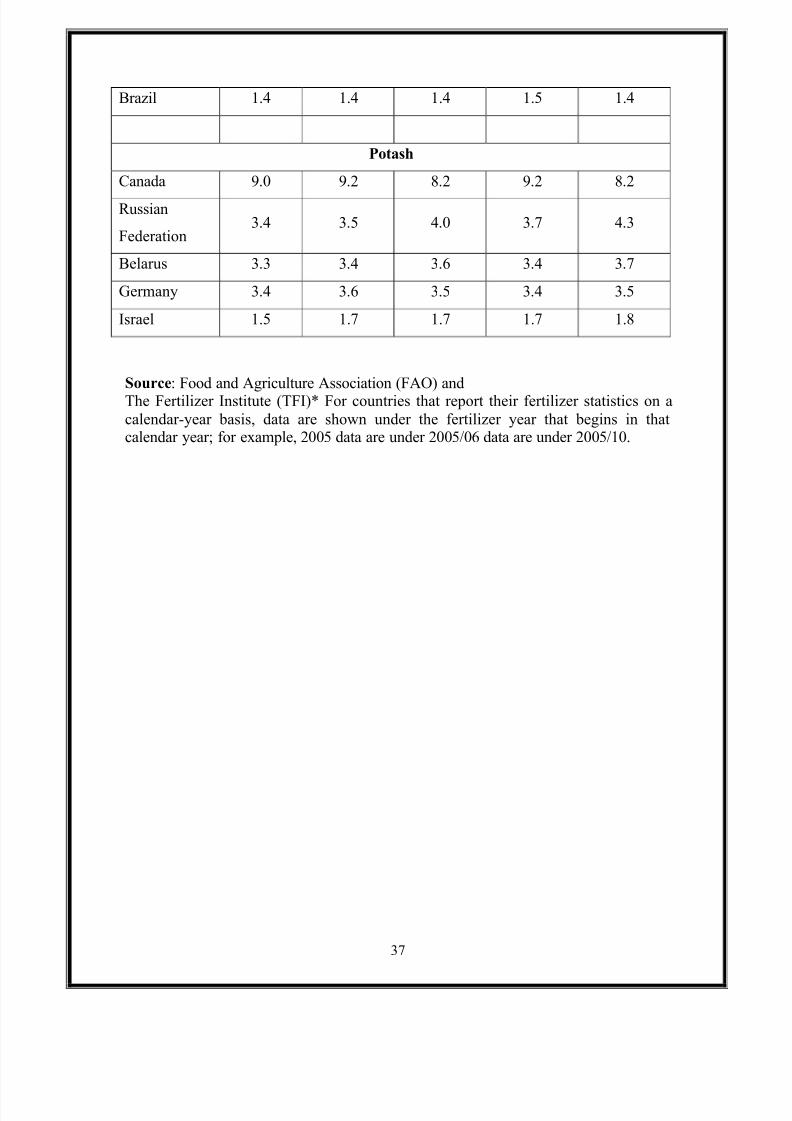

Major Fertilizer Producing Countries:

Million metric tone, years ending June 30*

(Metric Tone)

COUNTRY 2005-06 2006-07 2007-08 2008-09 2009-10

Nitrogen

China 20.2 21.5 22.8 21.5 22.1

India 10.1 10.5 10.9 10.9 10.7

United States 13.8 13.5 11.2 9.9 10.6

Russian

Federation4.1 4.1 5.0 5.4 5.5

Canada 3.7 3.7 4.1 3.9 3.5

Phosphate

United States 9.0 9.0 8.5 7.3 7.6

China 6.4 6.7 6.4 6.7 7.4

India 3.0 3.2 3.4 3.7 3.9

Russian

Federation1.9 1.7 2.0 2.3 2.4

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 37/126

37

Brazil 1.4 1.4 1.4 1.5 1.4

Potash

Canada 9.0 9.2 8.2 9.2 8.2

Russian

Federation3.4 3.5 4.0 3.7 4.3

Belarus 3.3 3.4 3.6 3.4 3.7

Germany 3.4 3.6 3.5 3.4 3.5

Israel 1.5 1.7 1.7 1.7 1.8

Source: Food and Agriculture Association (FAO) andThe Fertilizer Institute (TFI)* For countries that report their fertilizer statistics on a

calendar-year basis, data are shown under the fertilizer year that begins in thatcalendar year; for example, 2005 data are under 2005/06 data are under 2005/10.

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 38/126

38

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 39/126

39

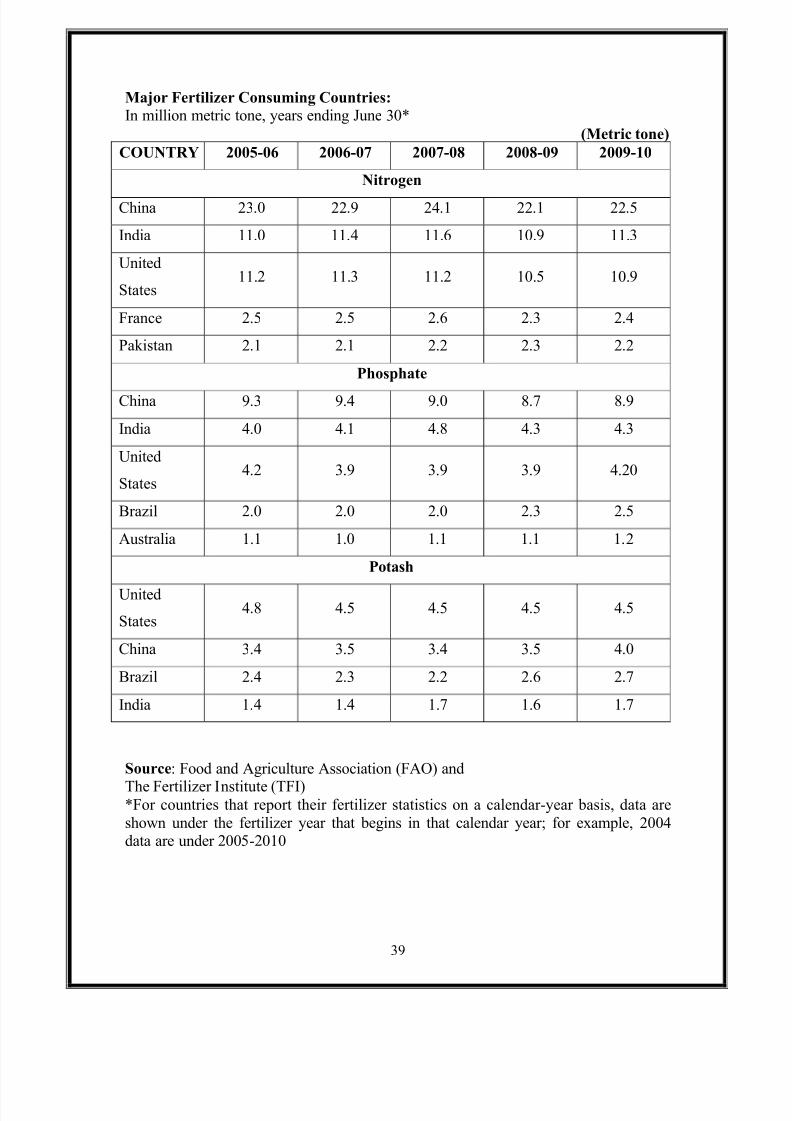

Major Fertilizer Consuming Countries:

In million metric tone, years ending June 30*

(Metric tone)

COUNTRY 2005-06 2006-07 2007-08 2008-09 2009-10

Nitrogen

China 23.0 22.9 24.1 22.1 22.5

India 11.0 11.4 11.6 10.9 11.3

United

States11.2 11.3 11.2 10.5 10.9

France 2.5 2.5 2.6 2.3 2.4

Pakistan 2.1 2.1 2.2 2.3 2.2

Phosphate

China 9.3 9.4 9.0 8.7 8.9

India 4.0 4.1 4.8 4.3 4.3

United

States4.2 3.9 3.9 3.9 4.20

Brazil 2.0 2.0 2.0 2.3 2.5

Australia 1.1 1.0 1.1 1.1 1.2

Potash

United

States4.8 4.5 4.5 4.5 4.5

China 3.4 3.5 3.4 3.5 4.0

Brazil 2.4 2.3 2.2 2.6 2.7

India 1.4 1.4 1.7 1.6 1.7

Source: Food and Agriculture Association (FAO) and

The Fertilizer Institute (TFI)*For countries that report their fertilizer statistics on a calendar-year basis, data are

shown under the fertilizer year that begins in that calendar year; for example, 2004 data are under 2005-2010

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 40/126

40

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 41/126

41

COMPANY PROFILE

THE NAGARJUNA GROUP

Our founder Sri K.V.K. Raju (28.11.1928 ² 16.06.1993) laid the

foundation of the Nagarjuna Group in 1974 with an investment of Rs. 50

millions. He was a visionary and a professional technocrat entrepreneur

who realized the importance of Core Sectors to an economy like ours. He

has guided the group with his philosophy

SERVING SOCIETY THROUGH INDUSTRY

Nagarjuna Fertilizers and Chemicals Limited (NFCL) is the first gas

based fertilizer factory in South India. The plant is based on the latest

fertilizer technology from M/s. Snamprogetti, Italy for Urea process with an

installed capacity of 1500 Mt/day for each unit. The ammonia process is

based on technology from M/s. Haldor Topsoe, Denmark with an installed

capacity of 900 MT/day per each unit.

The feed stock for unit ² I is natural gas and feed stock for Unit ² II is

NG/Naphtha. The current consumption of natural gas is 2.15 million

standard cubic meters per day and 500 MT of Naphtha per day. The naturalgas is being received through pipe lines from Tatipaka situated 92 Kms away

from the factory and is marketed by M/s Gas Authority of India Limited.

Naphtha is being supplied by M/s HPCL. The water requirement of 6.0

Million Gallons/day is received from Samalkot Summer Reservoir thro ugh

two pipeline.

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 42/126

42

Finance:

The total cost of the existing complex is Rs. 2156 crores (Rs. 1186

crores for Unit-I and Rs. 970 crores for Unit ² II). This consists

of loan of Rs. 1,162 crores (Rs. 515 crores for Unit-I and Rs. 647 crores for

Unit ² II) sanctioned by IDBI, IFCI, ICICI, UTI, LIC, GIC and also Banks.

The foreign exchange component of Rs. 781.07 cores was met by the Indian

Financial Institutions like IDBI, IFCI & ICICI and also by Italian Buyers

credit.

LIVING IN HARMONY WITH NATURE ± NFCL¶S

CONTRIBUTION TO ECOLOGY

Environmental protection is an avowed corporate philosophy and the

plant is built on the principle of zero-effluent discharge and is totally eco-

friendly. NFCL·s aim is to maintain ecological harmony, which is NATURE·S

INVALUABLE AND BEAUTIFUL GIFT TO MANKIND.

Man can live in harmony with the environment only when mankind is

guided by respect for the Mother Earth and all living things. Nagarjuna

Fertilizers and Chemicals Limited believe that Industry should exist in

harmony with nature. In pursuance of the corporate vision, and as a

humble contribution to the Mother Nature, the complete ecological system

in and around the factory has been changed by establishing a K.V.K.RAJU

SUNDARAVANAMU in an area of 747 acres surrounding the Complex.

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 43/126

43

The entire area has been covered with 4,50,000 plants consisting of 170

species, transforming a once highly saline marshy area devoid of any

vegetation into a lush green arboreal park. The establishment of 1 KM wide

KVK Sundaravanam is an integral part of overall natural ecological system

consisting of eleven water bodies for fish, habitat for animal life and

sanctuary for both indigenous as well as migratory birds with the factory

nestled in the most natural and idyllic surroundings cre ated with

dedication.

An integrated Environmental Management Plan (EMP) has been

incorporated in the basic design itself to ensure strict adherence to

International Standards. The investment on pollution control equipment in

the Plant is close to Rs. 110 crores of capital investment

and recurring expenditure of Rs. 6 crores being spent annually for operating

and maintaining the equipment.

MAIN FEATURES OF ECO-SYSTEM:

A forestation:

740 acres of area has been planted with 4.5 lakh saplings of 170

species. Weak areas have been planted with selected species based on

criteria like tolerance to salinity, availability from local sources and their

ability survive with least maintenance. A full -fledged nursery with mist

chamber and sprinkler irrigation system has been developed for supply of

plants to a forestation programmed .

Animal Enclosures:

A deer park with spotted deer has been set up in an area of six

hectares with chain-link fence on all sides. Separate enclosures for birds,

rabbits and certain other animals are made available. Some of these

animals like jungle cat, fox, jackals, mongooses, squirrels, bats, snakes, and

turtles are also being let out freely in this eco-system as a part of our animal

conservation programme.

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 44/126

44

Use of Treated Effluent:

The total treated effluent generated from the factory is being utilized

through a network of over 17 KM of PVC pipeline for sustenance of the eco-

system to show the purity levels of the effluents and the technological

efficiency of the plant equipment.

Awareness Programme:

As a part of NFCL·s sincere endeavor to bring awareness about the

benefits of cleaner environment on the general standards of life,

company has started ´GREENING THE ROADSµ of Kakinada in Phases. As

a part of this programme, flowering trees were planted on either side of the 4

km length of roads from Bhanugudi Junction to Nagamallithota and from

Nagamallithota to NFCL. This programme is being extended to further areas

in phases.

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 45/126

45

VALUES STATEMENT OF NFCL

COMMITMENT

We the Associates of NFCL are committed to continuously evokingcustomer delight through constant review and monitoring and delivering

proactive value added solutions. We are also committed to strive for

satisfaction of all stakeholders in a balanced manner through sustainable

growth and profitability

Excellence:

We shall continuously strive for Excellence in all dimensions of the

Company through teamwork, creativity and other means.

Ethics:

We shall strive for wholesome business relationships by adhering to

the principles of trusteeship, fair play and transparency in all our dealings

that we shall practice a work cultural, which is performance driven and

conducive to in proving discipline, accountability and depth of character,

team spirit and honesty in all our personal and professional relationships.

We shall build a learning organization where creativity, innovation,

entrepreneurship and knowledge sharing are encouraged and fostered

actively

Concern:

We consciously recognize that the development of associates is

inextricably linked to the sustainable growth and profitability of the

organization. Therefore, mutual care and concern between the associates

and the organization shall be our abiding value.

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 46/126

46

NFCL¶S VISION STATEMENT

SERVING SOCIETY THROUGH INDUSTRY

´For close to two decades, we at NFCL have predominantly been in the

business of manufacturing and marketing Urea, a segment of the plant

Nutrition business space. Given our cumulated experience and strengths in

understanding the farmer, the agriculture, various initiatives taken in the

past, the exposure of Indian agriculture to global economy and therefore the

need for Indian farmers to be globally competitive, have realized the need to

provide innovative and comprehensive Plant Nutrition Solutions.

´The leadership we refer to in our Vision Statement is in terms of

providing innovative and creative solutions.µ

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 47/126

47

NFCL¶S MISSION STATEMENT

We shall:

- Pioneer transformation in the approach to plant nutrition

- Deliver holistic plant nutrition solutions to the farmers

- Be the most preferred organization to be associated with

Pioneer transformation in the approach to plant nutrition we shall

develop crop, site and stage specific wholesome plant nutrition solutions.

NFCL shall focus on all necessary initiatives towards this ² be it

manufacturing technology, regulatory, logistics and using a mix of several

sciences and skills. The most preferred organization to be associated with in

the process of providing these solutions , NFCL shall delight all the

stakeholders ² employees, investors, suppliers, customers and society at

large. The stakeholders would prefer to be associated with us not only for

the higher value we offer, but also shall cherish their relationship with us

due to the way we deal with them ² with full commitment, responsibility and

accountability.

EMPLOYEE FOCUS:

NFCL·s aim to have the most satisfied employee base by the turn of

the century through its commitment to Personal and professional

development of the individual.

y Rewarding teamwork, innovation and quality behavior

y

Through job satisfactiony Creating and sustaining a close-knit family culture wherein every

individual experience a sense of belonging .

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 48/126

48

Marketing:

NFCL is operating in Andhra Pradesh, Orissa, West Bengal,

Maharastra, Karnataka, Pondicherry (Yanam territory). A professional team,

with a wide range of products, that include Urea, traded fertilizers (DAP,

MOP, Complex fertilizers), Micro-nutrients, Pesticides, Organic fertilizers

and Bio-Pesticides, has taken NFCL very close to the farmers and made

NAGARJUNA a household name among the farming community

Keeping pace with the changes in agricultural practices NFCL has

developed organic-fertilizers and bio-pesticides with support from NARDI. A

new concept in fertilizers i.e., Customized Fertilizer Granules (CFGs) has

been developed and the product is in trials.

NFCL·s Development activities focus on imparting training to farmers

and dealers on the latest package of practices in various crop sand

technology transfer. Training programs are carried out both on campus at

KVK, Kakinada and off-campus at villages and towns. A Well-equipped and

trained development tem organizes the programs using audio -visual vans,

jeeps, slide projectors and literature on products and crops, etc. State

Governments, Agriculture Universities and the farming community as awhole have acknowledged the effectiveness of development programs being

carried out by NFCL.

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 49/126

49

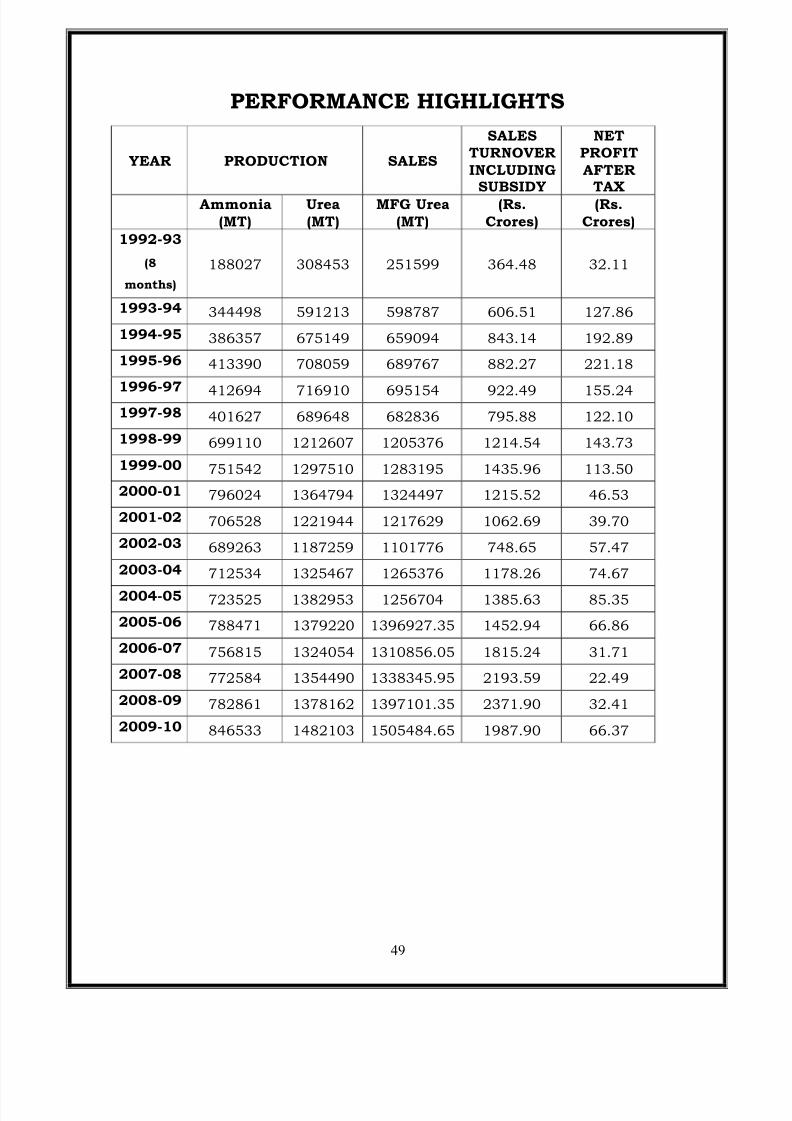

PERFORMANCE HIGHLIGHTS

YEAR PRODUCTION SALES

SALES

TURNOVER

INCLUDINGSUBSIDY

NET

PROFIT

AFTERTAX

Ammonia

(MT)

Urea

(MT)

MFG Urea

(MT)

(Rs.

Crores)

(Rs.

Crores)

1992-93

(8

months)

188027 308453 251599 364.48 32.11

1993-94 344498 591213 598787 606.51 127.86

1994-95 386357 675149 659094 843.14 192.89

1995-96 413390 708059 689767 882.27 221.18

1996-97 412694 716910 695154 922.49 155.241997-98 401627 689648 682836 795.88 122.10

1998-99 699110 1212607 1205376 1214.54 143.73

1999-00 751542 1297510 1283195 1435.96 113.50

2000-01 796024 1364794 1324497 1215.52 46.53

2001-02 706528 1221944 1217629 1062.69 39.70

2002-03 689263 1187259 1101776 748.65 57.47

2003-04 712534 1325467 1265376 1178.26 74.67

2004-05 723525 1382953 1256704 1385.63 85.35

2005-06 788471 1379220 1396927.35 1452.94 66.86

2006-07 756815 1324054 1310856.05 1815.24 31.71

2007-08 772584 1354490 1338345.95 2193.59 22.49

2008-09 782861 1378162 1397101.35 2371.90 32.41

2009-10 846533 1482103 1505484.65 1987.90 66.37

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 50/126

50

CUSTOMER FOCUS:

In recognition that business is based on quality and integrity, NFCL·s

aim to have the most satisfied customer base by enhancing farmer

productivity through forward integration on the one hand, and through

catering to industrial needs on the other. Unto this end, NFCL shall:

y Produce high quality products that give value for money

y Offer, both products and services

y Innovate to satisfy the real needs of customers

y Engage in fair, open and ethical practices.

SHAREHOLDER FOCUSNFCL aim to keep its shareholders satisfied by:

y Delivering the best long-term return on investment amongst all

companies in the Indian agri-business industry.

y Continuous growth and excellence in business performance.

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 51/126

51

AWARDS AND HONOURS

´EPICµ Award for Anti-Pollution measures taken by the Industry by

Environment Public interest Committee, Kakinada in 1993.

Good Housekeeping Award for 1994 by National Safety Council, A.P.

Chapter.

Best Industrial Canteen Award for 1994 by National Safety Council, A.P.

Chapter.

Indian Chemical Manufacturer·s Association (ICMA) Award for

´Environmental Control Strategies and Safety in Chemical Plantsµ for

the year 1994.

Award of Merit for 1994-95 by National Safety Council, U.S.A. for

completing 2 Million Accident Freeman Hours.

ISO 9002 Certification from Bureau Verities Quality International (BVQI),

Netherlands, in 1995.

Golden Peacock National Quality Award by Institute of Directors, New

Delhi, India for 1995.

British Safety Council·s National Safety Award for the five consecutive

years, 1994, 1995, 1996, 1997 & 1998 and also for the year 2000.

´Rajiv Gandhi Parti Bhoomi Mitraµ Award for 1994-96 by Wasteland

Development Board, Government of India.

National Safety Award for 1996 by National Safety Council, U.S.A.

Award for Innovative and Purposeful Programme for Social Progress for

the year 1996 by Indian Chemical Manufacturer·s Association (ICMA),

Mumbai.

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 52/126

52

Merit Award for 1997 and 1998 by Royal Society for the Prevention of

Accident (RSPA)

´Best Workersµ Welfare (including Family Planning) effort by an Industri al

or Commercial Unit in the Stateµ for the year 1997-98 by Andhra

Pradesh Chambers of Commerce & Industry (FAPCCI)

Golden Peacock National Award for environmental Management by World

Environment Foundation for the year 1998

Paryavarana Parirakshak Award by Rotary International at

Visakhapatnam for the year 1998

VANAMITRA ² 1999 from Govt., of A.P. for Developing and Maintaining

Greenbelt.

Achieved 84% in OH & S ² Audit conducted by British Safety Council,

U.K. in January 2000.

Best School Industry Linkage Award 2000 by NCERT ² an Autonomous

Organization of Government of India ² December 2000.

Best Environmental Management Plan ² 2000-01 in Vizag Zone by

Andhra Pradesh Pollution Control Board, Visakhapatnam.

National Safety award for 2000-01 from British Safety Council, U.K.

Best Environmental Improvement Effort by Industries located in the

State in 2000-2001 from Federation of A.P. Chamber of Commerce and

Industry, Andhra Pradesh.

Bronze Award for Occupational Safety for the year 2001 by Royal Society

for the Prevention of Accident (ROSPA), UK.

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 53/126

53

Commendation Trophy jointly given by National Safety Council, A.P.

Chapter & Director of Factories, A.P. for Implementing OHSAS 18001 in

March 2001.

¶ Environmental Protection Award· in Nitrogenous Fertilizer plants

category for the year 2001-02 from Fertilizer Association of India, New

Delhi.

´Perfect Recordµ in Occupational Safety/Health Award Programme for

operating two million employee hours without occupational injury or

illness for the period from 10.10.01 to 1 3.11.02 from National Safety

Council (NSC) of USA.

Commendation prize under the process stream category for its energy

conversation initiatives by Andhra Pradesh productivity council,

Hyderabad in 2007.

National award for ´Water efficient unit 2007µ by confederation of Indian

industry Hyderabad in 2007.

Certificate of Appreciation for implementing the process safety

management system (PSMS) by national safety council, A.P. Chapter,

Hyderabad in 2008.

NFCL bagged two awards from the Fertilizer Association of India (FAI),

New Delhi for the year 2008. It won the prestigious FAI Environmental

Protection Award in the nitrogenous fertilizer plants category and award

for the best article in ¶ Production and Technology·.

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 54/126

54

NFCL has bagged ICC AWARD for Excellence in Management of

Health/Safety/Environment from Indian Chemical Council, Mumbai for

the year 2008.

NFCL bagged two awards from the Fertilizer Association of India (FAI),

New Delhi for the year 2009. It won the prestigious FAI Environmental

Protection Award in the nitrogenous fertilizer plants category and stood

as joint winner for excellence in Safety Award.

NFCL has bagged Green Leaf 2nd runner-up award in the Global

Competition for Excellence and Innovation in Safety, Health and

Environment held by International Fertilizer Industry Association (IFA)

in 2009.

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 55/126

55

OTHER GROUP COMPANY / INSTITUTION

y Nagarjuna Investors Services Limited

y Nagarjuna Agric hem Limited

y Nagarjuna Palma India Limited

y

Nagarjuna Agricultural Research & Development Institute

y KVK Raju International Leadership Academy

y Nagarjuna power Corporation Limited

y Nagarjuna Haifa India Limited

y Nagarjuna Oil Corporation Limited

y Bijam Biosciences Limited

y Nagarjuna Foundation

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 56/126

56

FUTURE PLANS OF THE COMPANY

1) To improve the capacity utilization and energy efficiency through

technology up gradation.

2) Switching over to 100% natural gas as raw material instead of

Naphtha in Ammonia plant II

3) To continue to improve environmental performance under the

framework of ISO 14000 ² EMS.

4) To achieve British Safety convenience sword of honor in safety

management.

5) To enhance the standards in the present quality management system

(ISO 9002) by adopting the ISO 9001-2000 revision.

6) To enhance the standard in the present quality management system

(ISO 9002) by adopting the ISO 9001-2000 revision.

7) To widen the scope and offer technical services to various external

agencies including overs as a excitement .

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 57/126

57

Diversification:

Nagarjuna Group is on the threshold of major growth phase. Nagarjuna·s

aim is not just to meet the challenges of change, but to be the leaders in

all the businesses that we are in namely, Agri Inputs/Outputs, Energy

Sector and Refinery. Nagarjuna Group will thus have significant presence

in the core sectors of the economy, which will have a multiplier effect on

the industrial and socio-economic development of the country.

Nagarjuna Fertilizers and Chemicals Limited (NFCL) has sought the Center·spermission to expand the existing production capacity of urea from 12 lakh

metric tones per annum to 17 lakh tones per annum, reports Business

Standard.

NFCL is also undertaking several activities for the development of the

surrounding villages by providing free medical, educational and drinking

water facilities besides supporting the mental ly-retarded children.

The Kakinada facility of Nagarjuna Fertilizers and Chemicals Limited

(NFCL), has achieved a record Urea production of 113.1%, producing a total

of 13.79 lakh Metric Tonne of Urea during 2005-06. The Plant has repeated

this phenomenal feat, producing Urea more than its capacity, for the

consecutive second year. NFCL produces Urea in two units. While the Unit

one Produced 7,03,645 Metric Tonne, unit two also surpassed its capacity

by producing 6,75,571 Metric Tonne making this phenomenal feat repeated

during 2005-06 too. Total capacity of the plant is 11,94,600 Metric Tonne.

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 58/126

58

The Plant also has achieved this record production at a very

optimal utilization of energy of 5.662 MKcal/MT of Urea against

Internal target of 5.67 McCall/MT, which is already much lower than

the standard Fertilizer Industry Coordination Committee·s (FICC)

norm of 5.712 MKcal/MT. NFCL has one more reason to celebrate that

full production of Urea i.e., 13.79 lakh Metric Tonne has been

dispatched to the farmers.

Along with the production, NFCL has also done well in sales and

distribution wings. It·s products, which include Mahazinc, Zinc Sulphate,

zeta specialty fertilizers besides Urea have been sold out during 2005 -06.

NFCL WINS GAS CONSERVATION AWARD FROM GAIL:

Fertilizer facility of Nagarjuna Fertilizers and Chemicals Limited in

Kakinada has been selected for the ¶Award for Excellence in Natural Gas

Conservation· in the ¶ Fertilizers Sector· category for it·s outstanding

contribution to natural gas conservation in the country during 2004 -05.

This annual award has been instituted by Gas Authority of India

Limited (GAIL) as recognition of the excellent work done by the o rganizations

in Gas Conservation. GAIL has been conducting a nation -wide Natural Gas

Conservation Programme, meant to spread the word of conservation of this

precious natural resource. All the natural gas using industries like power,

fertilizer, steel, sponge iron, transport, glass, ceramic and petrochemicals

would be considered for this award.

This is the 4th achievement of NFCL for it·s excellence in different

departments during 2005. these include; 5 star rating in O.H & S Audit

from British Safety Council, UK. Commendation Award in ´Leadership and

Excellence Awards in Safety, Health & Environment (SHE) 2004µ, by

Confederation of Indian Industry,

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 59/126

59

Southern Region, Chennai. Re-certification for ISO 9001:2000 by

Bureau Verities Quality International (BVAI) for quality management

systems. And NFCL also received Environment Protection Award from

Fertilizers Association of India.

NFCL wins the prestigious Environment Protection Award from the

Fertilizer Association of India

Nagarjuna Fertilizers and Chemicals Limited (NFCL) the flagship

company of the Nagarjuna Group has won the prestigious FAI (Fertilizer

Association of India) Environment Protection Award in the Nitrogenous

fertilizer plants category for the year 2004-05. NFCL had

won the same award for 2001-02 also. Going much beyond the statutory

requirements of law for environment protection, NFCL has implemented a

comprehensive protection plan in its plant at Kakinada. NFCL has been

widely acknowledged for its Commitment to the betterment of Environment

and this award further adds to the long list of recognition.

NFCL has also won two more awards from FAI. A video film titled

´The Sugarcaneµ produced by NFCL was adjudged Runner-up in the Annual

Video Film Competition by FAI for the yea r 2004-05. The video film has

been developed with the objective to transfer technology and to enhance the

yield of sugarcane farmers in Andhra Pradesh. For NFCL, this is the second

consecutive year of winning in this category. An article titled ´From

Products to Solutions ² Exploring Opportunitiesµ published in the

September 2005 issue of the Indian Journal of Fertilizers was awarded the

Second prize in the category of Shriram Award for Best article in Marketing.

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 60/126

60

Bureau Verities Quality International (BVQI) awards re-

certification of ISO 9001:2000 for Nagarjuna Fertilizers and

Chemicals Limited.

Nagarjuna Fertilizers and Chemicals Limited (NFCL) have been re -

certified of ISO 9001:2000 by Bureau Verities Quality International (BVQI),

for its Quality Management Systems. The Flagship Company of the

Nagarjuna Group has already been an ISO 9001:2000 organization since

1995. This re-certification, which is valid up to February 2008, is only an

extension of recognition for company·s excellent quality management

systems.

BVQI team has done the re-certification audit during February at NFCL

plant Kakinada. After conducting audit in Plant Operations and Area

Marketing Offices BVQI sent a certificate to NFCL in which it mentioned

´Quality Management System of the Nagarjuna Fertilizers and Chemicals

Limited has been audited and found to be in accordance with the

requirements of the standards ISO 9001:2000µ.

BVQI is today the most widely recognized certification body in the

world, offering solutions in the key strategic fields of companies operations:

Quality, Health and Safety, Environment and Social Responsibility. It is

recognized by more than 30 national and international accreditation bodies

across the world to deliver ISO 9001 certification.

Nagarjuna Fertilizers and Chemicals Limited Awarded the

prestigious 5 star Rating by the British Safety Council, U.K

:Nagarjuna Fertilizers and Chemicals Limited (NFCL), the flagship

company of the Nagarjuna Group has been awarded the hi ghly coveted 5

star rating by the British Safety Council, U.K. After a detailed Health and

Safety Management System Audit conducted during the month of January

2005, the British Safety Council has awarded an ¶ Excellent· rating (Score of

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 61/126

61

92.39%) to NFCL·s manufacturing facility at Kakinada. The audit covered

eight areas of NFCL·s management systems leading to best practices, Fire

Control Systems, Measurement and Control Systems, Workplace

implementation, Verification, Best practice and Continuous improveme nt.

The British Safety Council (BSC) is one of the world·s

leading occupational health, safety and environmental organizations. BSC·s

Five Star Health and Safety Management System Audit is a benchmark for

best practices. It provides a detailed examina tion of the organization·s

current practices, and gives a comprehensive report and plan for

implementing, monitoring and achieving continuous improvement.

It is based on the Business excellence Model and goes beyond HS(G)65 and

OHSAS 18001 to measure how far an organization has gone towards

achieving best practice.

Information Technology & Communications Department,

Government of Andhra Pradesh signs MoU with IKisan Limited

To provide Agriculture related information and services through

Rajiv Internet Village Centers / (RSDPs/Rural eSeva Centers)

In its efforts towards Grameen Vikas aimed at alleviating rural poverty

and ensuring agricultural development, the Information Technology &

Communications Department, Government of Andhra Pradesh today signed

a MoU with Ikisan Limited to provide agricultural related information and

services to the vast farming community of the state through Rajiv Internet

Village Centers (RSDPs/Rural eSeva Centres).

The Information Technology and Communications Department has

already set up 1200 kiosks spreading across the state under the Rural

Service Delivery Point Project (RSDP) in rural areas to serve as centers of e -

commerce and information dissemination. Ikisan Limited has partnered

with the Information Technology & Communications Department to provide

agriculture information software and services in these kiosks. The modules

5/7/2018 Inventary Mgnt - slidepdf.com

http://slidepdf.com/reader/full/inventary-mgnt 62/126

62

will be in Telugu and voice enabled addressing the needs of rural population