Embed Size (px)

Citation preview

International Seaways, Inc.

1

International Seaways, Inc.Third Quarter 2017

Earnings Presentation

November 9, 2017

International Seaways, Inc.2

Disclaimer

Forward-Looking StatementsDuring the course of this presentation, the Company (International Seaways, Inc. (INSW)) may make forward-looking statements or provide forward-looking information. All statements other than statements of historical facts should be considered forward-looking statements. Some of these statements include words such as ‘‘outlook,’’ ‘‘believe,’’ ‘‘expect,’’ ‘‘potential,’’ ‘‘continue,’’ ‘‘may,’’ ‘‘will,’’ ‘‘should,’’ ‘‘could,’’ ‘‘seek,’’ ‘‘predict,’’ ‘‘intend,’’ ‘‘plan,’’ ‘‘estimate,’’ ‘‘anticipate,’’ ‘‘target,’’ ‘‘project,’’ ‘‘forecast,’’ ‘‘shall,’’ ‘‘contemplate’’ or the negative version of those words or other comparable words. Although they reflect INSW’s current expectations, these statements are not guarantees of future performance, but involve a number of risks, uncertainties, and assumptions which are difficult to predict. Some of the factors that may cause actual outcomes and results to differ materially from those expressed in, or implied by, the forward-looking statements include, but are not necessarily limited to, general economic conditions, competitive pressures, the nature of the Company’s services and their price movements, and the ability to retain key employees. The Company does not undertake to update any forward-looking statements as a result of future developments, new information or otherwise.

Non-GAAP Financial MeasuresIncluded in this presentation are certain non-GAAP financial measures, including Time Charter Equivalent (“TCE”) revenue, EBITDA, Adjusted EBITDA, and total leverage ratios, designed to complement the financial information presented in accordance with generally accepted accounting principles in the United States of America because management believes such measures are useful to investors. TCE revenues, which represents shipping revenues less voyage expenses, is a measure to compare revenue generated from a voyage charter to revenue generated from a time charter. EBITDA represents net (loss)/income before interest expense, income taxes and depreciation and amortization expense. Adjusted EBITDA consists of EBITDA adjusted for the impact of certain items that we do not consider indicative of our ongoing operating performance. Total leverage ratios are calculated as total debt divided by Adjusted EBITDA. We present non-GAAP measures when we believe that the additional information is useful and meaningful to investors. Non-GAAP financial measures do not have any standardized meaning and are therefore unlikely to be comparable to similar measures presented by other companies. The presentation of non-GAAP financial measures is not intended to be a substitute for, and should not be considered in isolation from, the financial measures reported in accordance with GAAP. See Appendix for a reconciliation of certain non-GAAP measures to the comparable GAAP measures.

This presentation also contains estimates and other information concerning our industry that are based on industry publications, surveys and forecasts. This information involves a number of assumptions and limitations, and we have not independently verified the accuracy or completeness of the information.

Additional Information You should read the Company’s Quarterly Report on Form 10-Q for the quarter ended September 30, 2017, and the other documents the Company has filed with the SEC for additional information regarding the Company, its operations and the risks and uncertainties it faces. You may obtain these documents for free by visiting EDGAR on the SEC Web site at www.sec.gov, or from the Company’s website at www.intlseas.com.

Business Review – Lois K. Zabrocky, President & CEO

International Seaways, Inc.4

Third Quarter 2017 Highlights & Recent Accomplishments

Seaways Investing at the Bottom of the Cycle

o Invested $169 million in modern vessels

o Acquired Seaways Hatteras and Seaways Montauk - two Suezmax

newbuildings - which delivered to us in July

o Acquired Seaways Raffles - a 2010-built VLCC - which delivered to us

in November

Divesting Select Older Assets

o Sold Overseas Petromar, a 2001-built MR, in August

o Entered into agreements to sell a 2004-built and a 2002-built MR,

expected to close in Q4 2017 and Q1 2018, respectively

Repurchased Shares

o Acted on our authorized two-year $30 million share buyback program

o Repurchased 160,000 shares during the quarter

o Executed at average share price of $19.86/share, total $3.2 million

Strong Base of Contracted Cash Flows

o Previously announced 5 year FSO contracts commenced during Q3

o FSO debt completely repaid in July

o Expected to generate in excess of $180 million of EBITDA for Seaways

over the five year period

Solid Performance in a Weak Market

o 2017 Q3 results:

o Net loss of $21.8 million, or $0.75 per share

o TCE revenues of $56.5 million

o Adjusted EBITDA of $15.8 million

o Cash flow positive after debt service and capex due to low

breakevens

International Seaways, Inc.

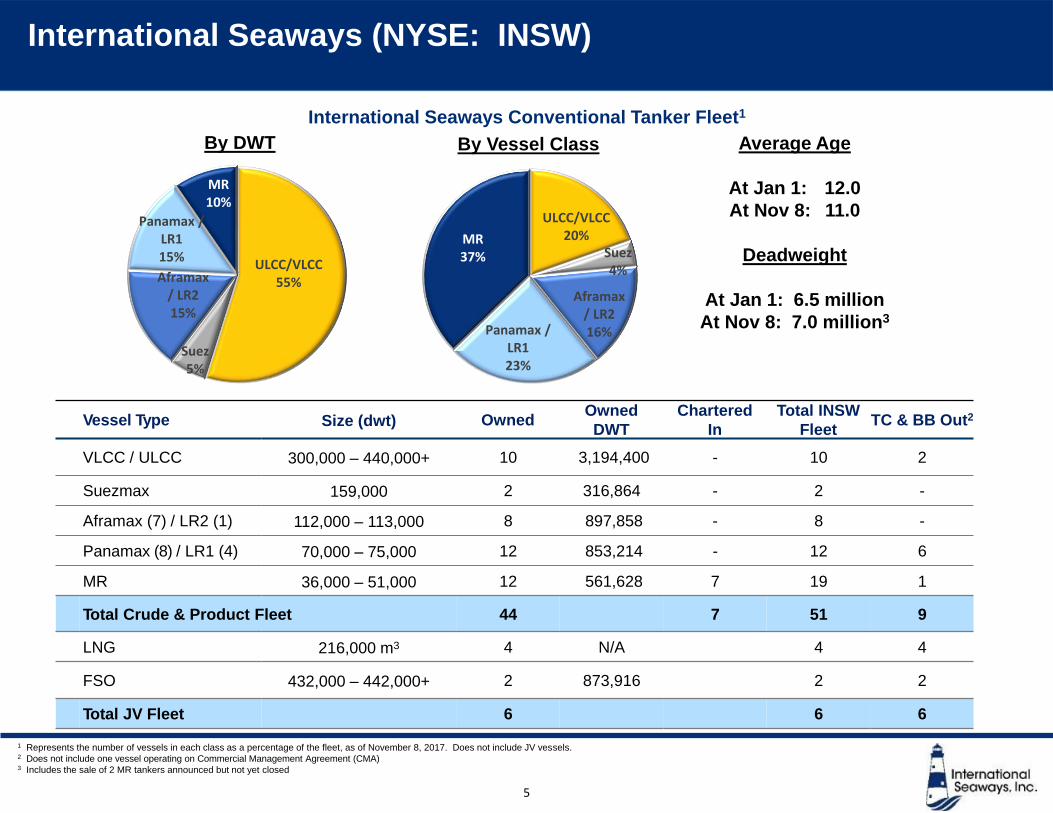

International Seaways (NYSE: INSW)

Vessel Type Size (dwt) OwnedOwned

DWT

Chartered

In

Total INSW

FleetTC & BB Out2

VLCC / ULCC 300,000 – 440,000+ 10 3,194,400 - 10 2

Suezmax 159,000 2 316,864 - 2 -

Aframax (7) / LR2 (1) 112,000 – 113,000 8 897,858 - 8 -

Panamax (8) / LR1 (4) 70,000 – 75,000 12 853,214 - 12 6

MR 36,000 – 51,000 12 561,628 7 19 1

Total Crude & Product Fleet 44 7 51 9

LNG 216,000 m3 4 N/A 4 4

FSO 432,000 – 442,000+ 2 873,916 2 2

Total JV Fleet 6 6 6

5

International Seaways Conventional Tanker Fleet1

ULCC/VLCC20%

Suez4%

Aframax / LR216%Panamax /

LR123%

MR37%

By Vessel Class

ULCC/VLCC55%

Suez5%

Aframax / LR215%

Panamax / LR115%

MR10%

By DWT Average Age

At Jan 1: 12.0

At Nov 8: 11.0

Deadweight

At Jan 1: 6.5 million

At Nov 8: 7.0 million3

1 Represents the number of vessels in each class as a percentage of the fleet, as of November 8, 2017. Does not include JV vessels.2 Does not include one vessel operating on Commercial Management Agreement (CMA)3 Includes the sale of 2 MR tankers announced but not yet closed

International Seaways, Inc.

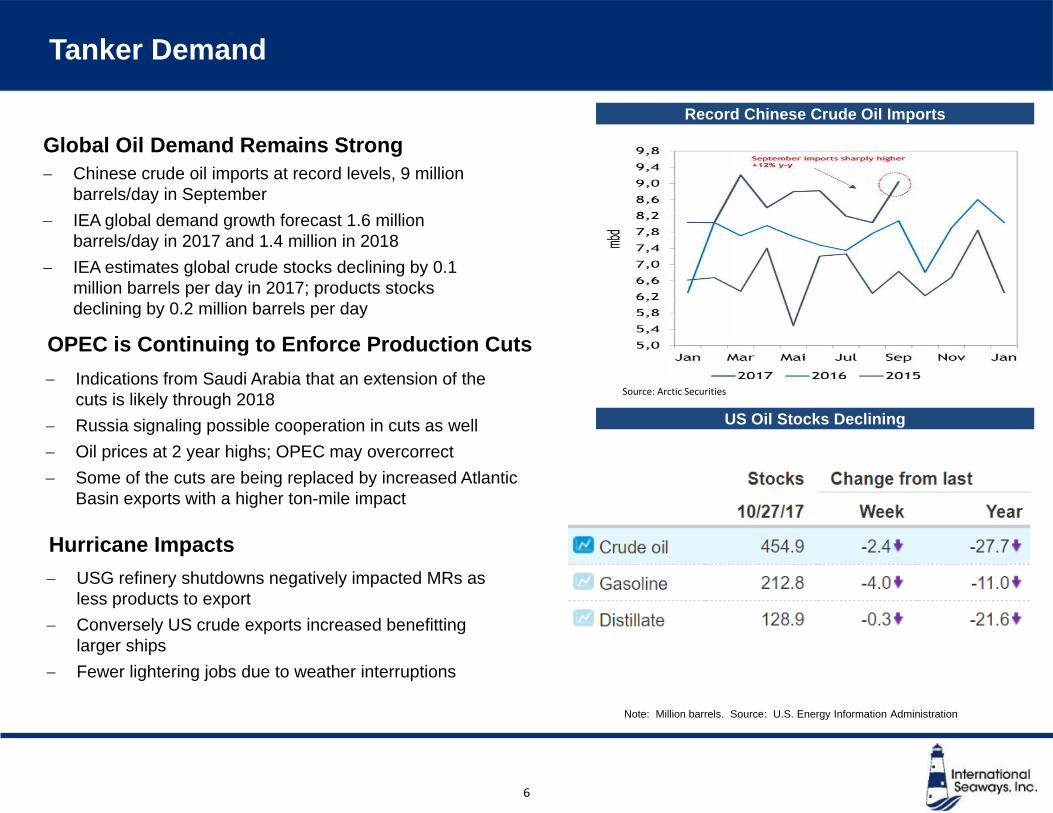

Tanker Demand

Source: Arctic Securities

OPEC is Continuing to Enforce Production Cuts

Indications from Saudi Arabia that an extension of the

cuts is likely through 2018

Russia signaling possible cooperation in cuts as well

Oil prices at 2 year highs; OPEC may overcorrect

Some of the cuts are being replaced by increased Atlantic

Basin exports with a higher ton-mile impact

Global Oil Demand Remains Strong

Chinese crude oil imports at record levels, 9 million

barrels/day in September

IEA global demand growth forecast 1.6 million

barrels/day in 2017 and 1.4 million in 2018

IEA estimates global crude stocks declining by 0.1

million barrels per day in 2017; products stocks

declining by 0.2 million barrels per day

Hurricane Impacts

USG refinery shutdowns negatively impacted MRs as

less products to export

Conversely US crude exports increased benefitting

larger ships

Fewer lightering jobs due to weather interruptions

Record Chinese Crude Oil Imports

6

Note: Million barrels. Source: U.S. Energy Information Administration

US Oil Stocks Declining

International Seaways, Inc.

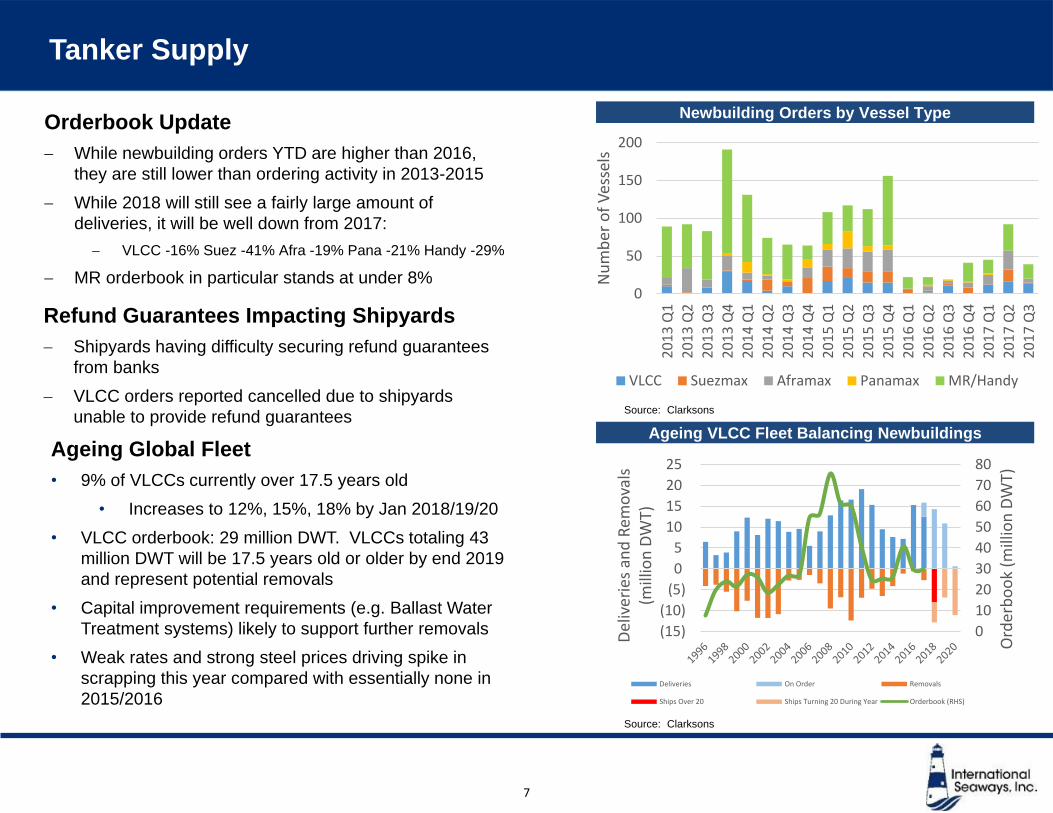

Newbuilding Orders by Vessel Type

Tanker Supply

Orderbook Update

While newbuilding orders YTD are higher than 2016,

they are still lower than ordering activity in 2013-2015

While 2018 will still see a fairly large amount of

deliveries, it will be well down from 2017:

VLCC -16% Suez -41% Afra -19% Pana -21% Handy -29%

MR orderbook in particular stands at under 8%

Refund Guarantees Impacting Shipyards

Shipyards having difficulty securing refund guarantees

from banks

VLCC orders reported cancelled due to shipyards

unable to provide refund guarantees

7

Source: Clarksons

Ageing VLCC Fleet Balancing Newbuildings

Source: Clarksons

0

10

20

30

40

50

60

70

80

(15)

(10)

(5)

0

5

10

15

20

25

Ord

erb

oo

k (m

illio

n D

WT)

Del

iver

ies

and

Rem

ova

ls

(mill

ion

DW

T)

Deliveries On Order Removals

Ships Over 20 Ships Turning 20 During Year Orderbook (RHS)

0

50

100

150

200

20

13

Q1

20

13

Q2

20

13

Q3

20

13

Q4

20

14

Q1

20

14

Q2

20

14

Q3

20

14

Q4

20

15

Q1

20

15

Q2

20

15

Q3

20

15

Q4

20

16

Q1

20

16

Q2

20

16

Q3

20

16

Q4

20

17

Q1

20

17

Q2

20

17

Q3

Nu

mb

er o

f V

esse

ls

VLCC Suezmax Aframax Panamax MR/Handy

Ageing Global Fleet

• 9% of VLCCs currently over 17.5 years old

• Increases to 12%, 15%, 18% by Jan 2018/19/20

• VLCC orderbook: 29 million DWT. VLCCs totaling 43

million DWT will be 17.5 years old or older by end 2019

and represent potential removals

• Capital improvement requirements (e.g. Ballast Water

Treatment systems) likely to support further removals

• Weak rates and strong steel prices driving spike in

scrapping this year compared with essentially none in

2015/2016

Financial Review – Jeffrey D. Pribor, SVP & CFO

International Seaways, Inc.

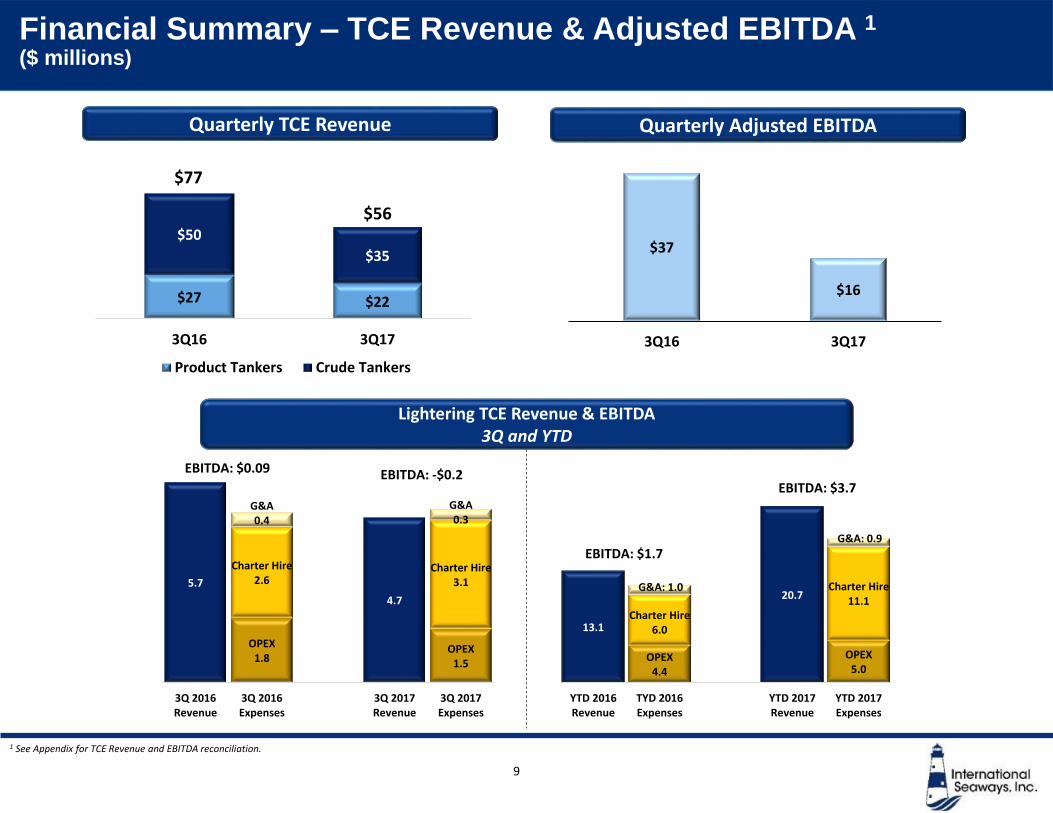

Financial Summary – TCE Revenue & Adjusted EBITDA 1($ millions)

Quarterly Adjusted EBITDA

9

Lightering TCE Revenue & EBITDA3Q and YTD

5.7

OPEX 1.8

4.7

OPEX 1.5

Charter Hire2.6

Charter Hire3.1

G&A0.4

G&A0.3

3Q 2016Revenue

3Q 2016Expenses

3Q 2017Revenue

3Q 2017Expenses

EBITDA: $0.09 EBITDA: -$0.2

Quarterly TCE Revenue

$27 $22

$50

$35

3Q16 3Q17

Product Tankers Crude Tankers

$77

$56

$37

$16

3Q16 3Q17

1 See Appendix for TCE Revenue and EBITDA reconciliation.

13.1

OPEX4.4

20.7

OPEX5.0

Charter Hire6.0

Charter Hire11.1

G&A: 1.0

G&A: 0.9

YTD 2016Revenue

TYD 2016Expenses

YTD 2017Revenue

YTD 2017Expenses

EBITDA: $1.7

EBITDA: $3.7

International Seaways, Inc.

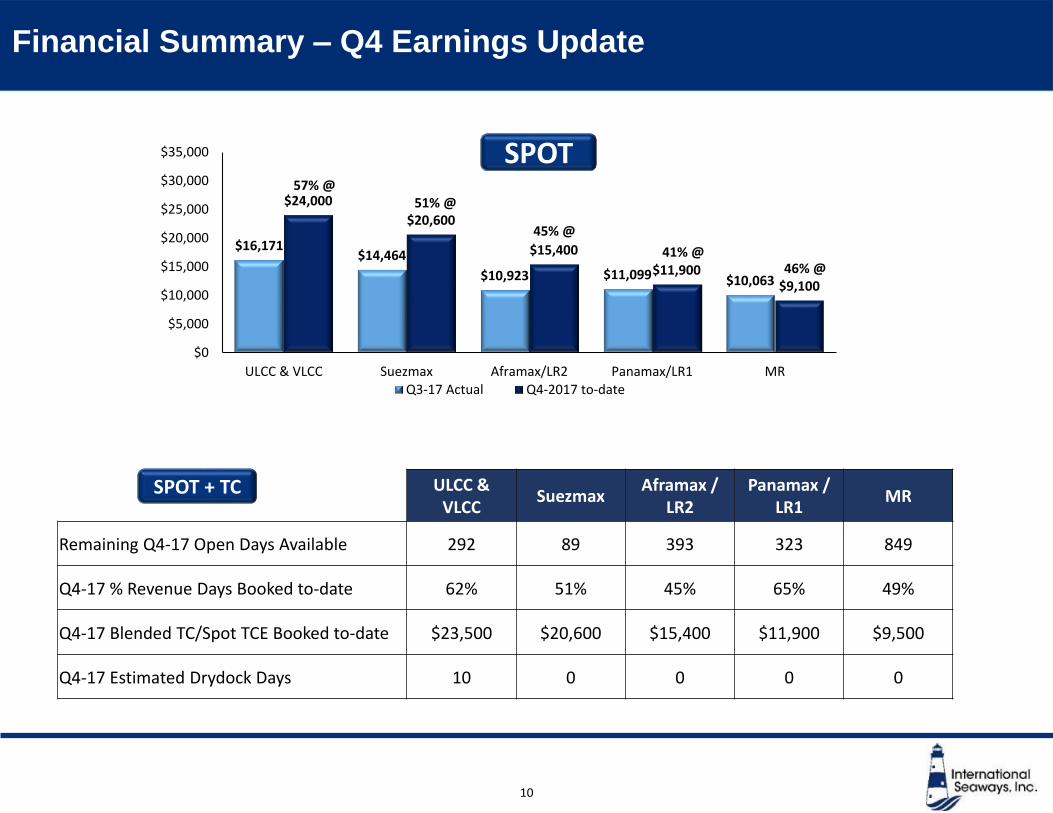

Financial Summary – Q4 Earnings Update

$16,171$14,464

$10,923 $11,099 $10,063

$24,000

$20,600

$15,400

$11,900$9,100

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

ULCC & VLCC Suezmax Aframax/LR2 Panamax/LR1 MRQ3-17 Actual Q4-2017 to-date

ULCC & VLCC

SuezmaxAframax /

LR2Panamax /

LR1MR

Remaining Q4-17 Open Days Available 292 89 393 323 849

Q4-17 % Revenue Days Booked to-date 62% 51% 45% 65% 49%

Q4-17 Blended TC/Spot TCE Booked to-date $23,500 $20,600 $15,400 $11,900 $9,500

Q4-17 Estimated Drydock Days 10 0 0 0 0

10

57% @

45% @

41% @46% @

SPOT

SPOT + TC

51% @

International Seaways, Inc.

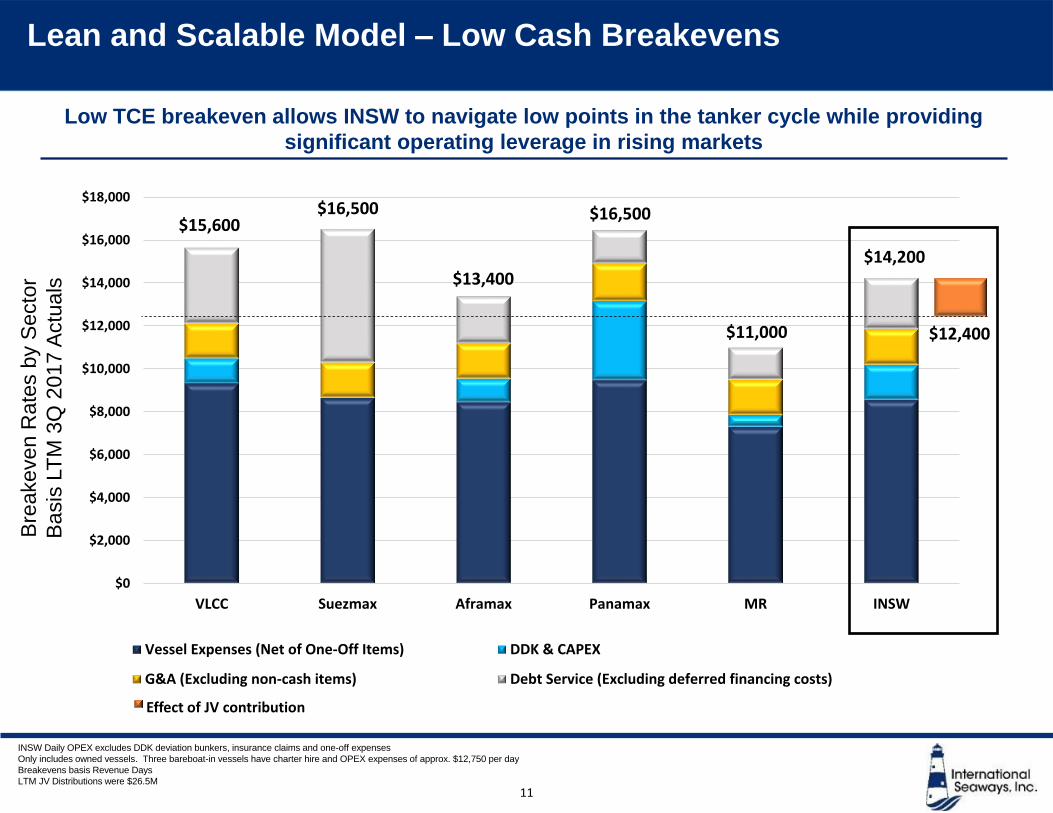

Lean and Scalable Model – Low Cash Breakevens

11

INSW Daily OPEX excludes DDK deviation bunkers, insurance claims and one-off expenses

Only includes owned vessels. Three bareboat-in vessels have charter hire and OPEX expenses of approx. $12,750 per day

Breakevens basis Revenue Days

LTM JV Distributions were $26.5M

Low TCE breakeven allows INSW to navigate low points in the tanker cycle while providing

significant operating leverage in rising markets

Bre

ake

ve

n R

ate

s b

y S

ecto

r

Ba

sis

LT

M 3

Q 2

01

7 A

ctu

als

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

$18,000

VLCC Suezmax Aframax Panamax MR INSW

Vessel Expenses (Net of One-Off Items) DDK & CAPEX

G&A (Excluding non-cash items) Debt Service (Excluding deferred financing costs)

$15,600

$13,400

$16,500

$11,000

$14,200

$16,500

$12,400

Effect of JV contribution

International Seaways, Inc.

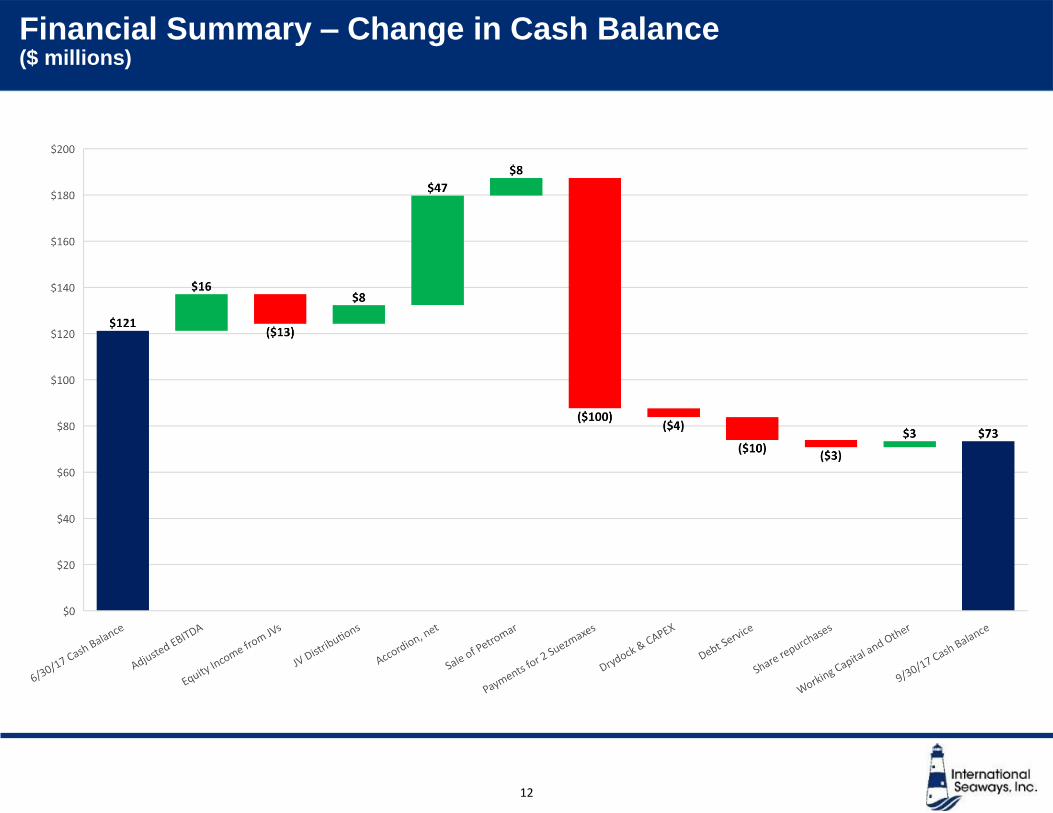

Financial Summary – Change in Cash Balance ($ millions)

12

International Seaways, Inc.

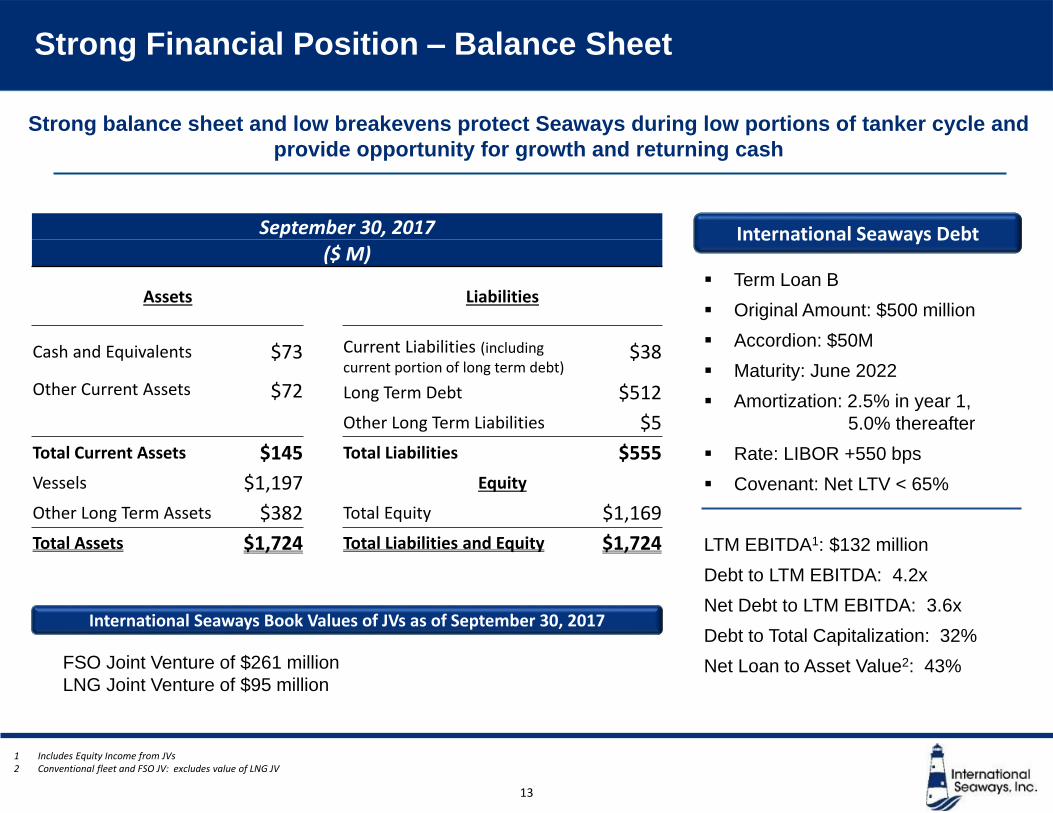

Strong Financial Position – Balance Sheet

13

Strong balance sheet and low breakevens protect Seaways during low portions of tanker cycle and

provide opportunity for growth and returning cash

▪ Term Loan B

▪ Original Amount: $500 million

▪ Accordion: $50M

▪ Maturity: June 2022

▪ Amortization: 2.5% in year 1,

5.0% thereafter

▪ Rate: LIBOR +550 bps

▪ Covenant: Net LTV < 65%

LTM EBITDA1: $132 million

Debt to LTM EBITDA: 4.2x

Net Debt to LTM EBITDA: 3.6x

Debt to Total Capitalization: 32%

Net Loan to Asset Value2: 43%

International Seaways Debt

1 Includes Equity Income from JVs2 Conventional fleet and FSO JV: excludes value of LNG JV

FSO Joint Venture of $261 million

LNG Joint Venture of $95 million

International Seaways Book Values of JVs as of September 30, 2017

September 30, 2017($ M)

Assets Liabilities

Cash and Equivalents $73 Current Liabilities (including current portion of long term debt)

$38

Other Current Assets $72 Long Term Debt $512

Other Long Term Liabilities $5

Total Current Assets $145 Total Liabilities $555

Vessels $1,197 Equity

Other Long Term Assets $382 Total Equity $1,169

Total Assets $1,724 Total Liabilities and Equity $1,724

Summary – Lois K. Zabrocky, President & CEO

International Seaways, Inc.

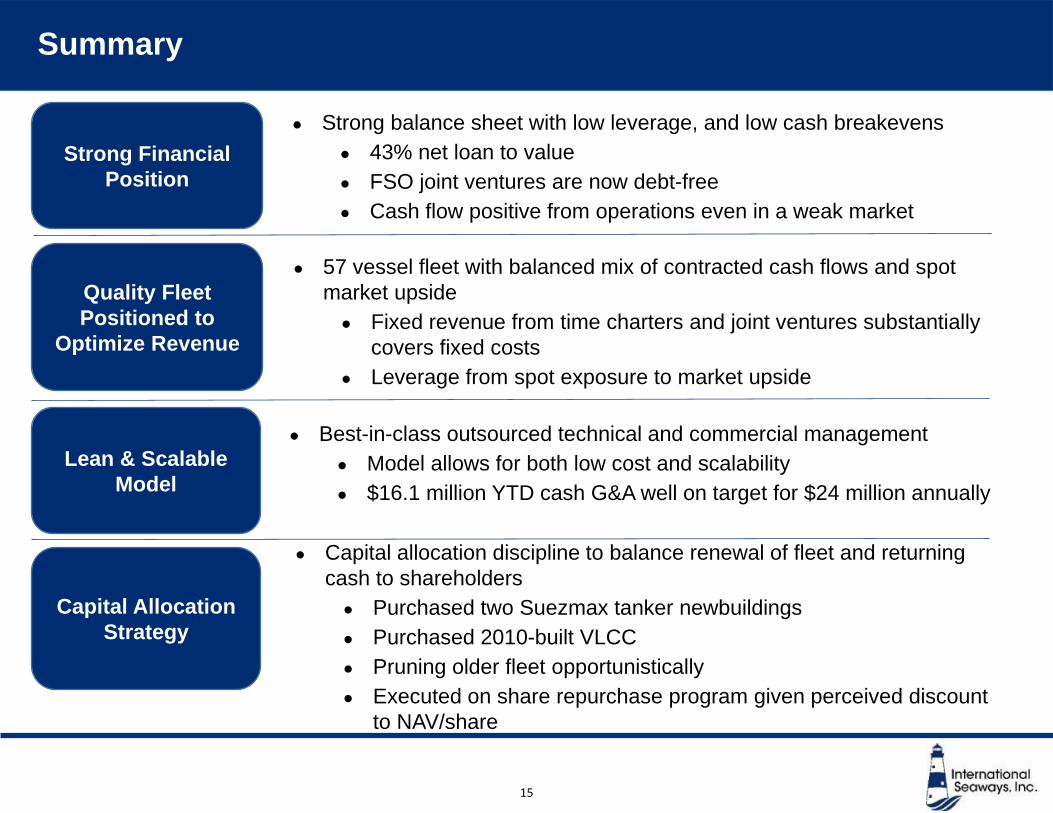

Summary

15

Quality Fleet

Positioned to

Optimize Revenue

● 57 vessel fleet with balanced mix of contracted cash flows and spot

market upside

● Fixed revenue from time charters and joint ventures substantially

covers fixed costs

● Leverage from spot exposure to market upside

Lean & Scalable

Model

● Best-in-class outsourced technical and commercial management

● Model allows for both low cost and scalability

● $16.1 million YTD cash G&A well on target for $24 million annually

Capital Allocation

Strategy

● Capital allocation discipline to balance renewal of fleet and returning

cash to shareholders

● Purchased two Suezmax tanker newbuildings

● Purchased 2010-built VLCC

● Pruning older fleet opportunistically

● Executed on share repurchase program given perceived discount

to NAV/share

Strong Financial

Position

● Strong balance sheet with low leverage, and low cash breakevens

● 43% net loan to value

● FSO joint ventures are now debt-free

● Cash flow positive from operations even in a weak market

Appendix

International Seaways, Inc.

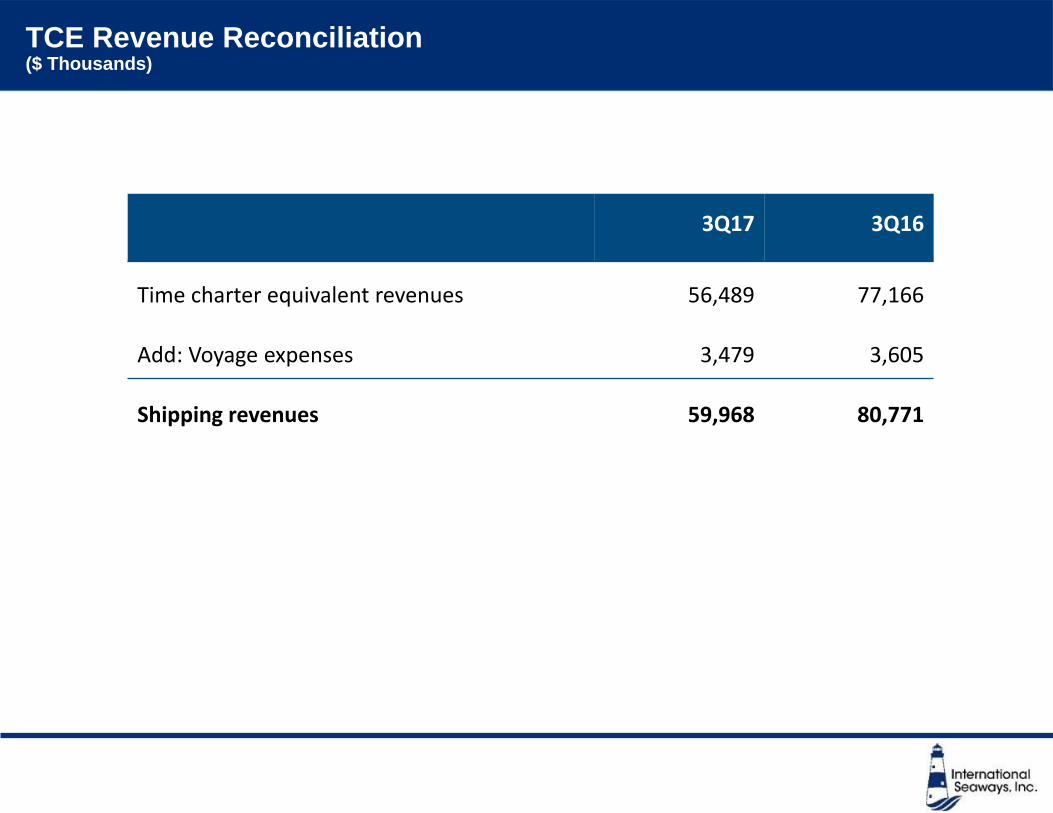

TCE Revenue Reconciliation($ Thousands)

3Q17 3Q16

Time charter equivalent revenues 56,489 77,166

Add: Voyage expenses 3,479 3,605

Shipping revenues 59,968 80,771

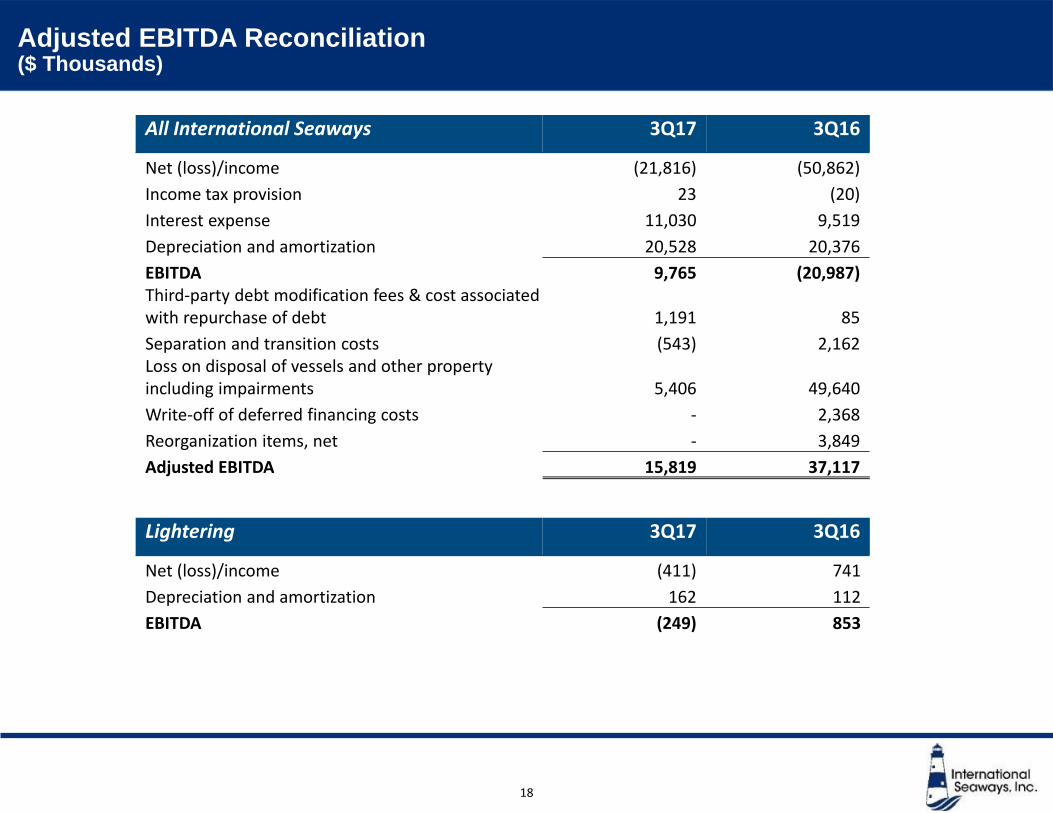

International Seaways, Inc.18

All International Seaways 3Q17 3Q16

Net (loss)/income (21,816) (50,862)

Income tax provision 23 (20)

Interest expense 11,030 9,519

Depreciation and amortization 20,528 20,376

EBITDA 9,765 (20,987)Third-party debt modification fees & cost associated with repurchase of debt 1,191 85

Separation and transition costs (543) 2,162Loss on disposal of vessels and other property including impairments 5,406 49,640

Write-off of deferred financing costs - 2,368

Reorganization items, net - 3,849

Adjusted EBITDA 15,819 37,117

Adjusted EBITDA Reconciliation($ Thousands)

Lightering 3Q17 3Q16

Net (loss)/income (411) 741

Depreciation and amortization 162 112

EBITDA (249) 853