Embed Size (px)

Citation preview

Dollarization in MexicoJingwen Fu Xintong Hou & Mengye Zhu

Introduction of Dollarization in Mexico

Foreign Exchange Regime of Mexico – A Historical Perspective

Pros and Cons—On-going debate on dollarization in Mexico& other Latin America countries

Dollarization in Mexico

Introduction What is dollarization?

Currency Substitution: The use of a foreign currency in transactions in place of the domestic currency

Dollarization is the degree to which real and financial transactions are performed in dollars relative to those realized in domestic currency

Measure: The proportion of dollars to domestic currency circulating at any point in time.

Full dollarization vs Partially

Official vs unofficial (Mexico)

Why is dollarization emerged?

Domestic residents have strong incentives to

diversify the composition of their currency holdings.

Individuals and firms engaged in international exchange have

similar transaction and portfolio incentives

Border transactions is particularly important in the Mexican case

Tourism

There is a greater incentive to diversify the portfolio of liquid money

assets under floating rates

Depreciation pressure on Peso

trillema

Introduction

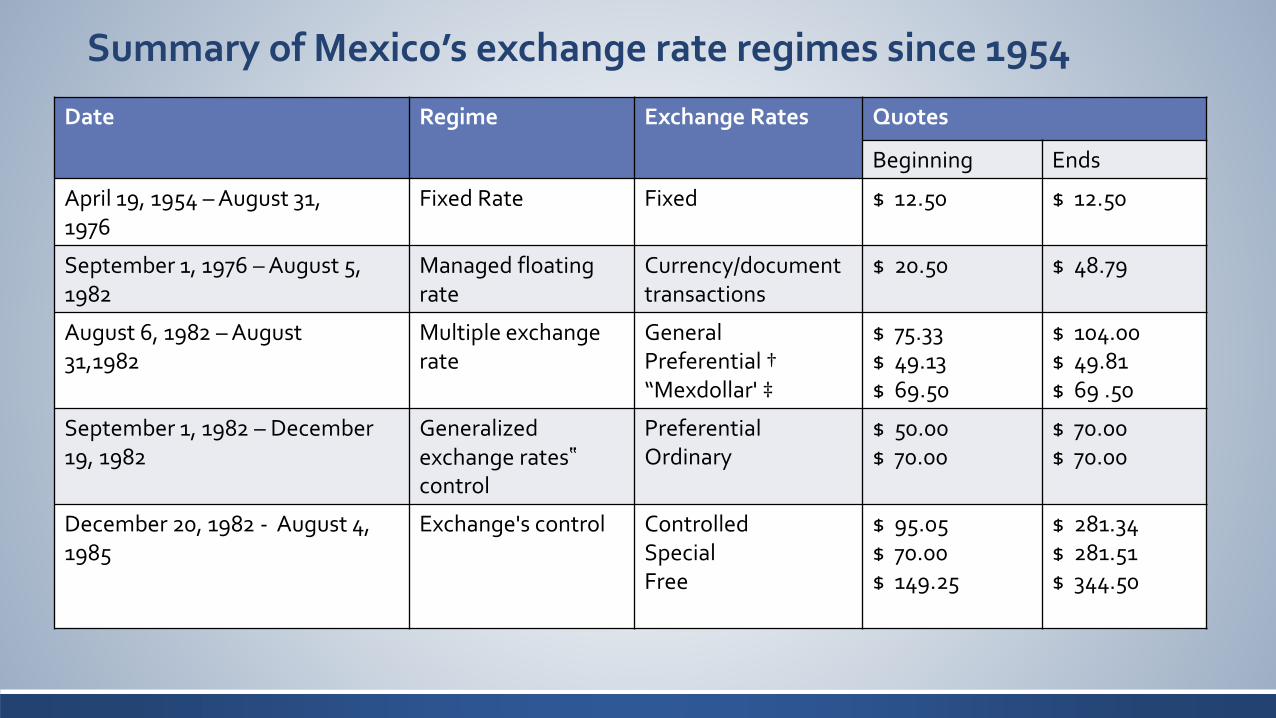

Summary of Mexico’s exchange rate regimes since 1954

Date Regime Exchange Rates Quotes

Beginning Ends

April 19, 1954 – August 31, 1976

Fixed Rate Fixed $ 12.50 $ 12.50

September 1, 1976 – August 5, 1982

Managed floating rate

Currency/document transactions

$ 20.50 $ 48.79

August 6, 1982 – August 31,1982

Multiple exchange rate

General Preferential † “Mexdollar' ‡

$ 75.33$ 49.13$ 69.50

$ 104.00$ 49.81$ 69 .50

September 1, 1982 – December 19, 1982

Generalized exchange rates‟control

Preferential Ordinary

$ 50.00 $ 70.00

$ 70.00 $ 70.00

December 20, 1982 - August 4, 1985

Exchange's control Controlled SpecialFree

$ 95.05 $ 70.00$ 149.25

$ 281.34 $ 281.51$ 344.50

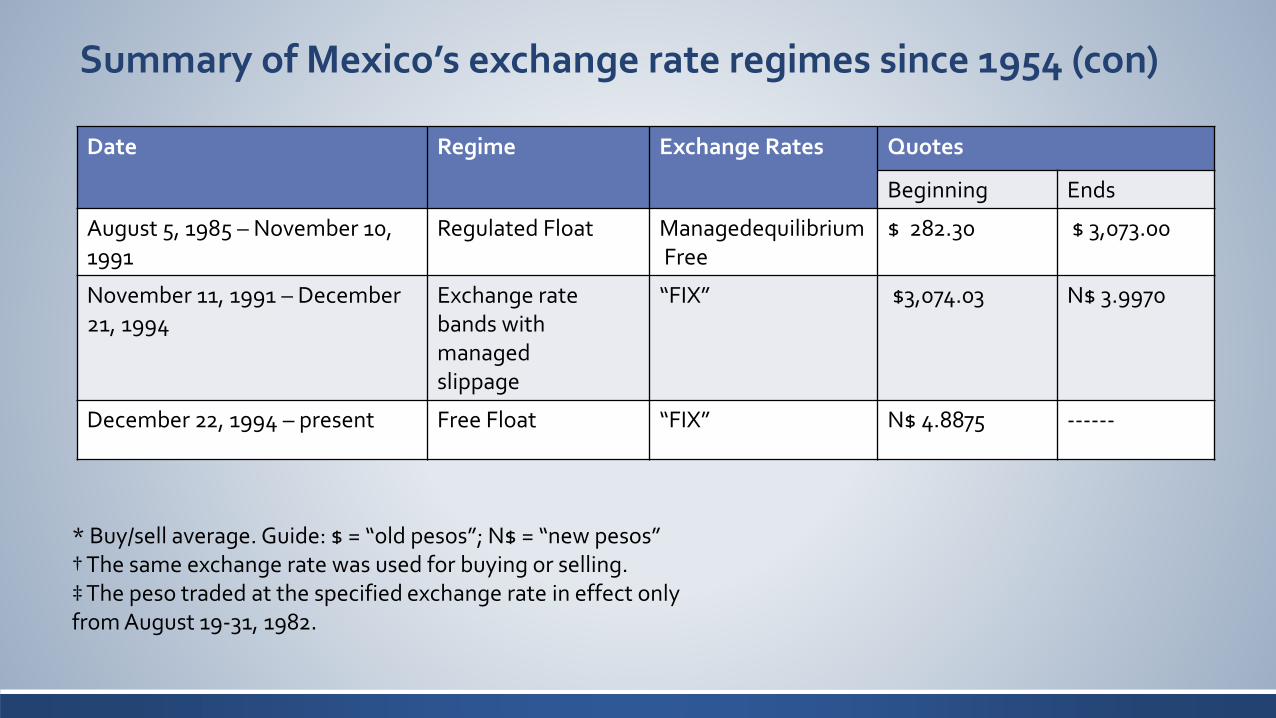

Summary of Mexico’s exchange rate regimes since 1954 (con)

Date Regime Exchange Rates Quotes

Beginning Ends

August 5, 1985 – November 10, 1991

Regulated Float ManagedequilibriumFree

$ 282.30 $ 3,073.00

November 11, 1991 – December 21, 1994

Exchange rate bands with managed slippage

“FIX” $3,074.03 N$ 3.9970

December 22, 1994 – present Free Float “FIX” N$ 4.8875 ------

* Buy/sell average. Guide: $ = “old pesos”; N$ = “new pesos” † The same exchange rate was used for buying or selling. ‡ The peso traded at the specified exchange rate in effect only from August 19-31, 1982.

I. Fixed rate regime (April 19, 1954 – August 31, 1976)

For several years prior to 1954, the Mexican peso was relatively stable against the US dollar at around 8.65 pesos per USD.

In 1954, however, certain unfavorable conditions occurred in Mexico.

In order to correct these imbalances, on April 19, 1954, the peso was devalued and fixed at 12.50 against the dollar.

II. Managed floating rate regime (September 1, 1976 – August 5, 1982)

A fixed peso/dollar exchange rate of 12.50 was maintained until September 1976

In view of the imbalances in both the current account and the capital account, on September 1, 1976, the fixed exchange rate regime was replaced by a managed floating rate regime.

During the managed floating rate regime there were in practice two exchange rates: one for currency transactions and another one for transactions with documents. Although buy/sell quotes for each exchange rate were often different, the average buy/sell quote usually coincided.

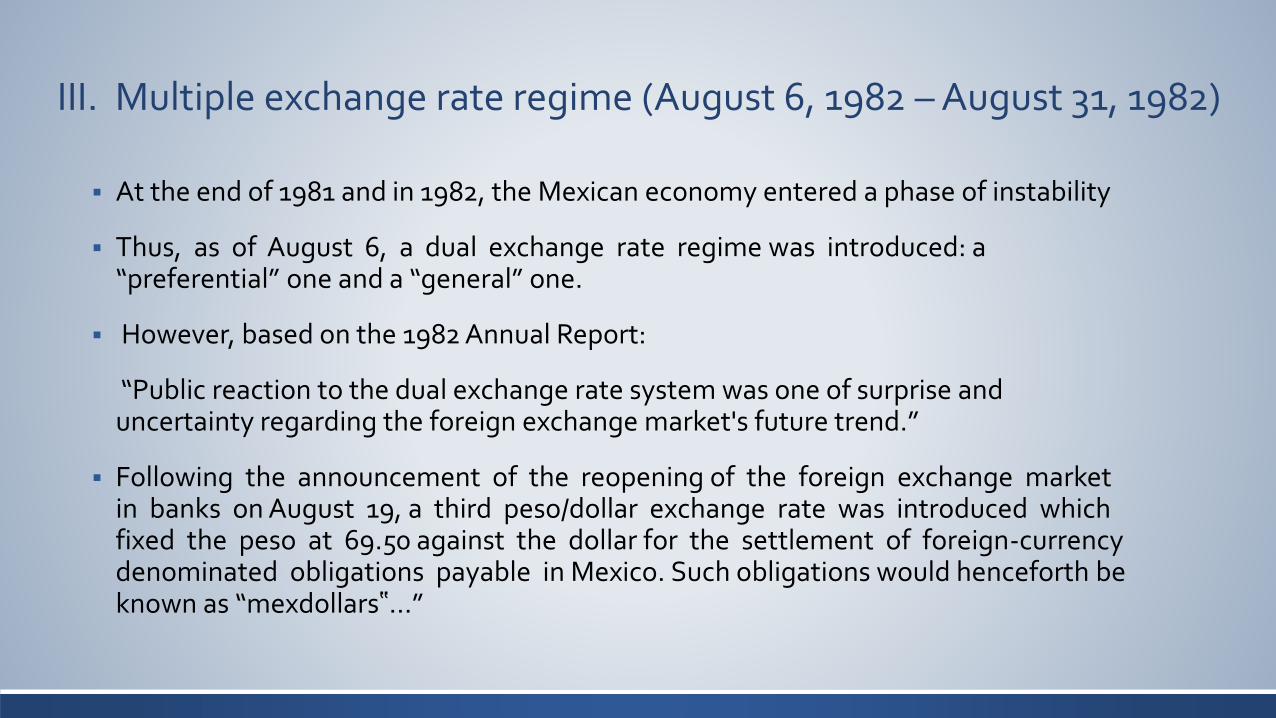

III. Multiple exchange rate regime (August 6, 1982 – August 31, 1982)

At the end of 1981 and in 1982, the Mexican economy entered a phase of instability

Thus, as of August 6, a dual exchange rate regime was introduced: a “preferential” one and a “general” one.

However, based on the 1982 Annual Report:

“Public reaction to the dual exchange rate system was one of surprise and uncertainty regarding the foreign exchange market's future trend.”

Following the announcement of the reopening of the foreign exchange market in banks on August 19, a third peso/dollar exchange rate was introduced which fixed the peso at 69.50 against the dollar for the settlement of foreign-currency denominated obligations payable in Mexico. Such obligations would henceforth be known as “mexdollars‟…”

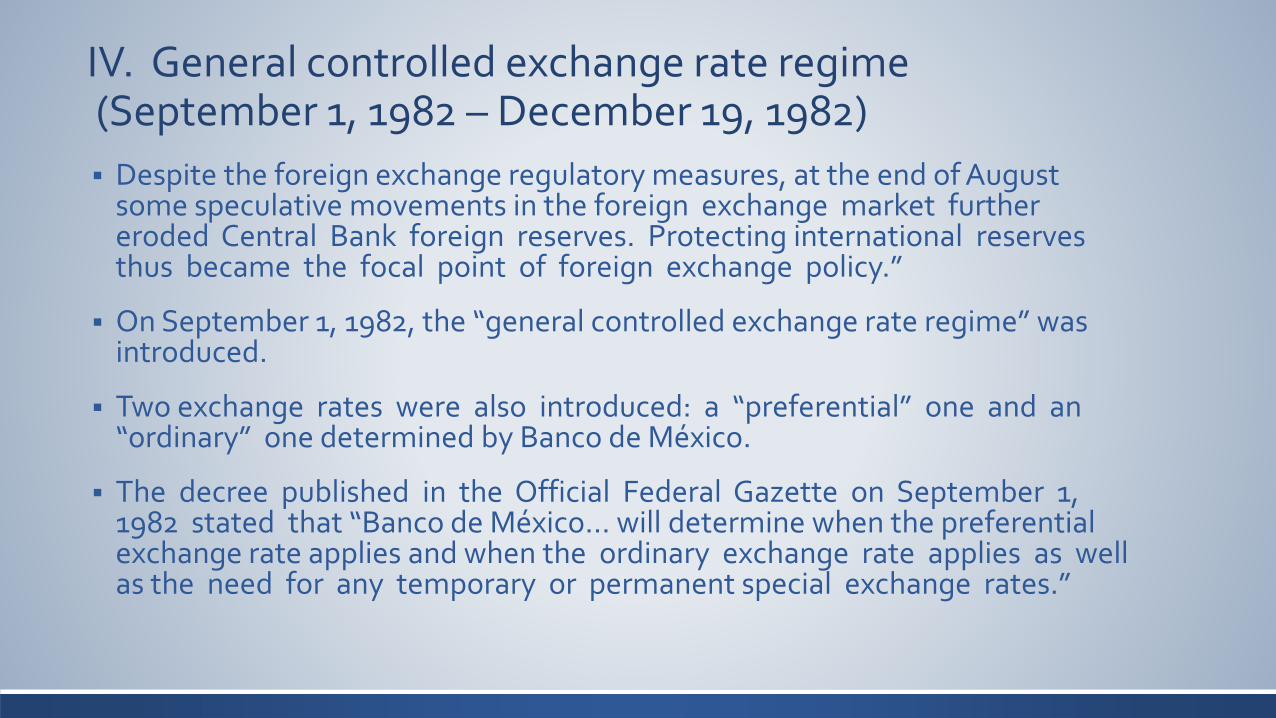

IV. General controlled exchange rate regime(September 1, 1982 – December 19, 1982)

Despite the foreign exchange regulatory measures, at the end of August some speculative movements in the foreign exchange market further eroded Central Bank foreign reserves. Protecting international reserves thus became the focal point of foreign exchange policy.”

On September 1, 1982, the “general controlled exchange rate regime” was introduced.

Two exchange rates were also introduced: a “preferential” one and an “ordinary” one determined by Banco de México.

The decree published in the Official Federal Gazette on September 1, 1982 stated that “Banco de México… will determine when the preferential exchange rate applies and when the ordinary exchange rate applies as well as the need for any temporary or permanent special exchange rates.”

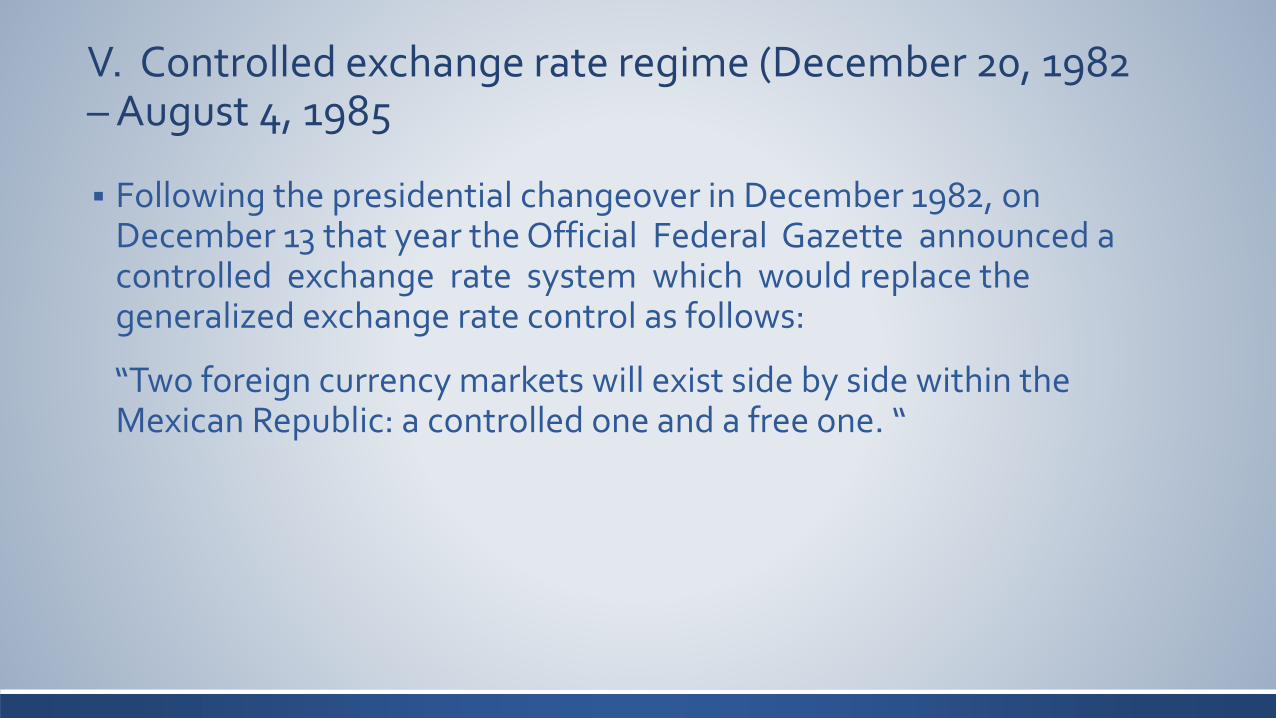

V. Controlled exchange rate regime (December 20, 1982 – August 4, 1985

Following the presidential changeover in December 1982, on December 13 that year the Official Federal Gazette announced a controlled exchange rate system which would replace the generalized exchange rate control as follows:

“Two foreign currency markets will exist side by side within the Mexican Republic: a controlled one and a free one. “

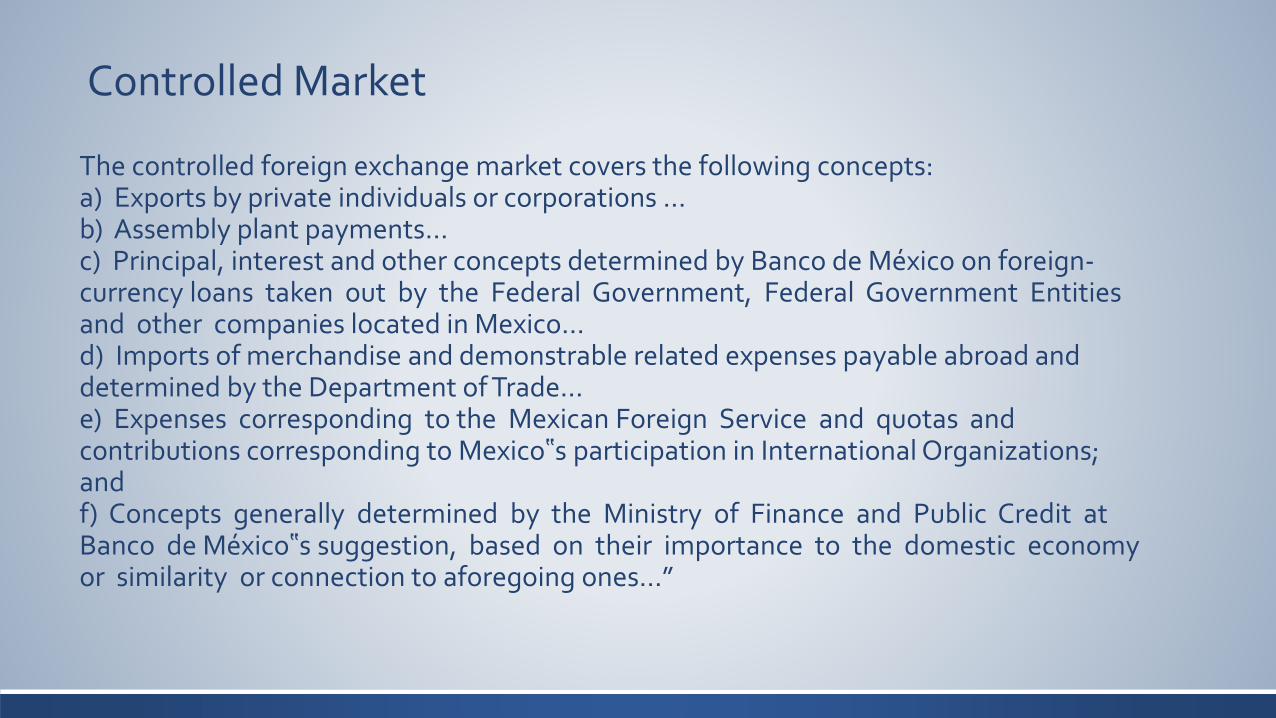

The controlled foreign exchange market covers the following concepts: a) Exports by private individuals or corporations … b) Assembly plant payments… c) Principal, interest and other concepts determined by Banco de México on foreign-currency loans taken out by the Federal Government, Federal Government Entities and other companies located in Mexico… d) Imports of merchandise and demonstrable related expenses payable abroad and determined by the Department of Trade… e) Expenses corresponding to the Mexican Foreign Service and quotas and contributions corresponding to Mexico‟s participation in International Organizations; and f) Concepts generally determined by the Ministry of Finance and Public Credit at Banco de México‟s suggestion, based on their importance to the domestic economy or similarity or connection to aforegoing ones…”

Controlled Market

The free market covers foreign currency transactions not subject to the controlled market.

Free market transactions, including the buying and selling, possession and transfer of foreign currency, are not subject to restrictions.

Exchange rates agreed on by the contracting parties will apply to foreign currency buy/sell transactions covered by the free market.

Free Market

VI. Regulated floating rate regime (August 5, 1985 –November 10, 1991)

Towards the end of 1985, it was considered that foreign exchange policy at the time did not take account of the prevailing and expected trend in monetary aggregates or their impact on international reserves, as the exchange rate moved evenly in accordance with a daily slippage and not in accordance with prevailing conditions. Therefore it was announced that:

“…as of August 5, a regulated floating system will be introduced to replace the even slippage in effect since December 1982. Under the new system the controlled exchange rate will be modified on a daily basis by not necessarily even amounts and not abruptly”

VII. Exchange rate band with managed slippage regime (November 11, 1991 – December 21, 1994)

In order to “provide exporters and assembly plants with a stimulus” as of November 11, 1991, exchange rates were no longer managed and the free and controlled exchange rates were unified. The new system consisted of letting the exchange rate float within a band which widened on a daily basis. The floor of the band was set at 3,051.20 pesos against the dollar while the ceiling was adjusted upwards by 20 cents daily (including Saturdays and Sundays) from 3,086.40 pesos. On October 21, 1992, the ceiling’s slippage was increased to 40 cents daily.

VIII. Free floating regime (December 22, 1994 – present)

In 1994, several events occurred in Mexico which caused market instability and resulted in a speculative attack on Banco de Mexico‟s international reserves at the end of that year, making the exchange rate band regime unsustainable.

Thus, on the evening of December 19, 1994, the Foreign Exchange Commission reached an agreement to replace the previous exchange rate regime with a floating rate regime.

Under the floating rate regime, which has remained in effect ever since, the exchange rate is determined by the free market without the intervention of the authorities.

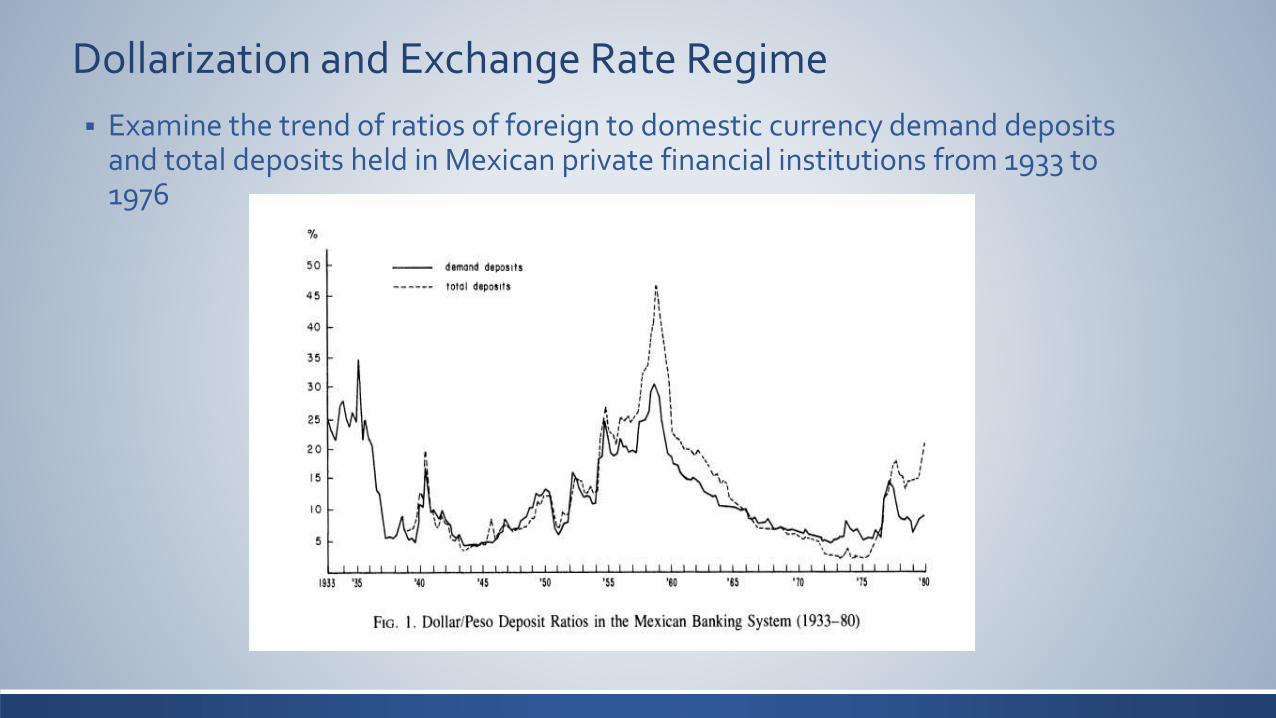

Dollarization and Exchange Rate Regime

Examine the trend of ratios of foreign to domestic currency demand deposits and total deposits held in Mexican private financial institutions from 1933 to 1976

Dollarization and Exchange Rate Regime

During the first fixed exchange rate period (from November 1933 until March 1938) the demand deposit ratio fell consistently.

In March of 1938, President Cardenas nationalized the oil industry and the peso was allowed to float again for thirty- one months. A new process of dollarization began with the floating of the peso.

The dollar/peso deposit ratio reached its highest point in September 1940, and declined substantially following the establishment of a fixed peso/dollar exchange rate .

Dollarization and Exchange Rate Regime

A new period of floating exchange rates lasting only eleven months took place between July 1948 and June 1949; the dollarization coefficient increased from 7.5 to 11.5 percent during the float.

The new parity established in 1949 (8.65 pesos to a dollar) lasted until 1954 when the peso was devalued approximately 45 percent. The exchange rate was then maintained at 12.5 pesos to a dollar until September 1976 when authorities decided to float the peso once more.

The dollarization coefficients climbed once more with the 1976 devaluation

Then while the checking deposit peso/dollar ratio declined after the third quarter of 1977, the total deposit ratio has remained at substantially higher levels.

Dollarization and Exchange Rate Regime

The largest jumps of the dollarization ratio (after 1937) occurred in 1940, 1952, 1954, 1957-58, and 1976. Of these dates, 1940, 1952, 1958, and 1976 correspond to the last year of the incumbent administration. Of these dates, 1940, 1952, 1958, and 1976 correspond to the last year of the incumbent administration, while a devaluation also occurred in 1954 and 1976.

Conclusion: Both devaluation expectations and perceptions of possible "economic regime" changes (or increased political risk) associated with the renewal of the administration must play an important role in explaining the historical record of Mexican dollarization.

Pros and Cons of Full Dollarization

Benefit

1. In the short run is the decline of inflation rates and inflation expectations. Full dollarization eliminates the risk of depreciation of the domestic currency, a contributing factor to the acceleration of inflation.

2. Enhancement of economic policy credibility. The high cost of reversing full dollarization could restore confidence in policymakers’ long-term commitment to price stabilization and fiscal discipline. This gain in policy credibility reinforces the reduction in inflation fears.

3. Reduction of the cost of borrowing. Use of the US dollar eliminates the devaluation risk and should reduce interest rates.

Benefit and Cos t of Full DollarizationCost

Countries are likely to be reluctant to abandon their own currencies, symbols of their nationhood, particularly in favor of those of other nations. As a practical matter, political resistance is nearly certain, and likely to be strong.

From an economic point of view, the right to issue a country's currency provides its government with seigniorage revenues, which show up as central bank profits and are transferred to the government. They would be lost to dollarizing countries and gained by the United States unless it agreed to share them.

A dollarizing country would relinquish any possibility of having an autonomous monetary and exchange rate policy, including the use of central bank credit to provide liquidity support to its banking system in emergencies.

Panama-Full Dollarization

Panama was the first fully dollarized economy in Latin America.

After the country gained independence from Colombia in 1904, the US dollar became the legal tender for transactions and the domestic currency.

Panama’s decision to adopt full dollarization responded to political and historical reasons rather than economic ones.

1. Stability of output and prices

an average stable growth rate of 4.4%, exceeding the average growth rates of Central American countries.

average inflation rate remained very low (1.1%) and stable (0.4% of volatility)

2. Promotion of fiscal discipline

Foreign debt began to decline in 1996 thanks to an external bond exchange and a debt reduction operation.

Benefits

Cost

Increasing vulnerability to external and internal shocks

In the 1960s, political conflicts over the Canal Zone resulted in the massive withdrawal of domestic deposits, offset by an increase in domestic lending.

The increase in international oil prices in 1973 and 1978 caused increases in domestic prices, resulting in high inflation rates.

A major crisis came in 1987 and 1989, as a result of political tensions between the governments of Panama and the United States. Banks borrowed abroad and reduced their liquid assets to compensate for the loss in domestic resources, but also reduced lending.

Real GDP decreased 15.6% in 1988 and 0.4% in1989, accompanied by large-scale capital flight.

The effect of the financial crises in 1997-1998 was more pronounced in Panama’s dollarized economy because of the increase in interest rates. In 2001, Panama’s GDP grew 0.3%, the lowest growth rate in the decade

Ecuador’s recent experience with full dollarization

In January 2000, President Jamil Mahuad called for full dollarization to avoid the collapse of the banking system.

Ecuador started enjoying the expected benefits of full dollarization even before the US dollar was officially adopted on September 9, 2000

enhanced credibility

release of frozen bank deposits

Lower inflation

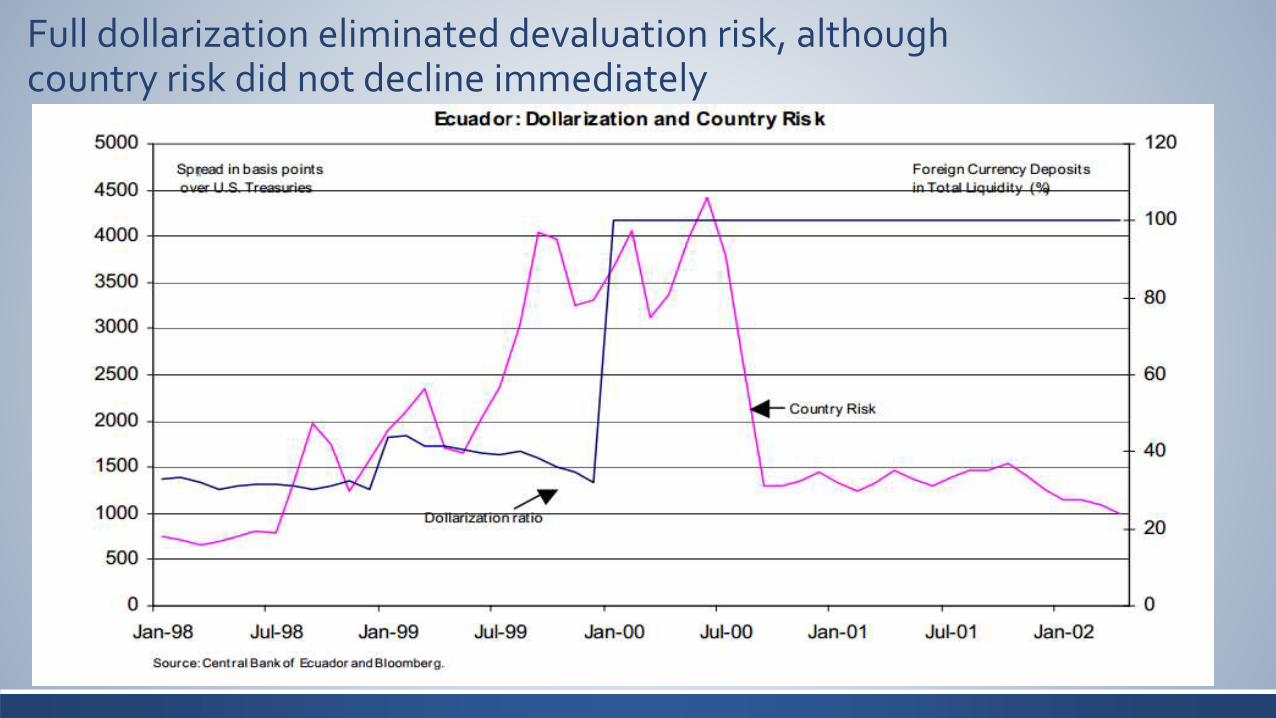

Full dollarization eliminated devaluation risk, although country risk did not decline immediately

Critics

Ecuador is still vulnerable to external shocks due to its dependency on revenues from oil and external financing. Full dollarization imposes an additional cost to this vulnerability: the lack of flexibility of economic policies to respond to real, financial and political shocks.

An additional challenge to the dollarization process is the circulation of counterfeit currency.

Political consensus will be the greatest challenge for structural reform in Ecuador.

Full dollarization has helped Ecuador reduce inflation and enhance policy credibility and has supported economic stability in the short run. In the long term, however, further benefits for economic growth and development will depend on structural and institutional reforms.

Experience from above Countries

Full dollarization can help countries achieve lower inflation, economic stability and growth.

Full dollarization enhances policy credibility and encourages foreign investment. It promotes fiscal discipline, a competitive financial system and economic integration with international markets.

However, countries implementing full dollarization must establish structural programs and institutional reforms to ensure that short-term stability develops into long-term economic growth.

Deliverables

What products or services will your project deliver?

Include client requirements

Success Factors

Identify elements that are key to the success of the project, such as:

Satisfied clients or stakeholders

Met project objectives

Completed within budget

Delivered on time

Implementation

Tasks/activities

Procedures

Tools/technology

Project change control process

DYA: define your acronyms!

Resources

People

Resource 1Resource 2Resource 3Resource 4

Notes

Equipment

Resource 1Resource 2Resource 3Resource 4

Notes

Locations

Resource 1Resource 2Resource 3Resource 4

Notes

Outside Services

Resource 1Resource 2Resource 3Resource 4

Notes

Manufacturing

Resource 1Resource 2Resource 3Resource 4

Notes

Sales

Resource 1Resource 2Resource 3Resource 4

Notes

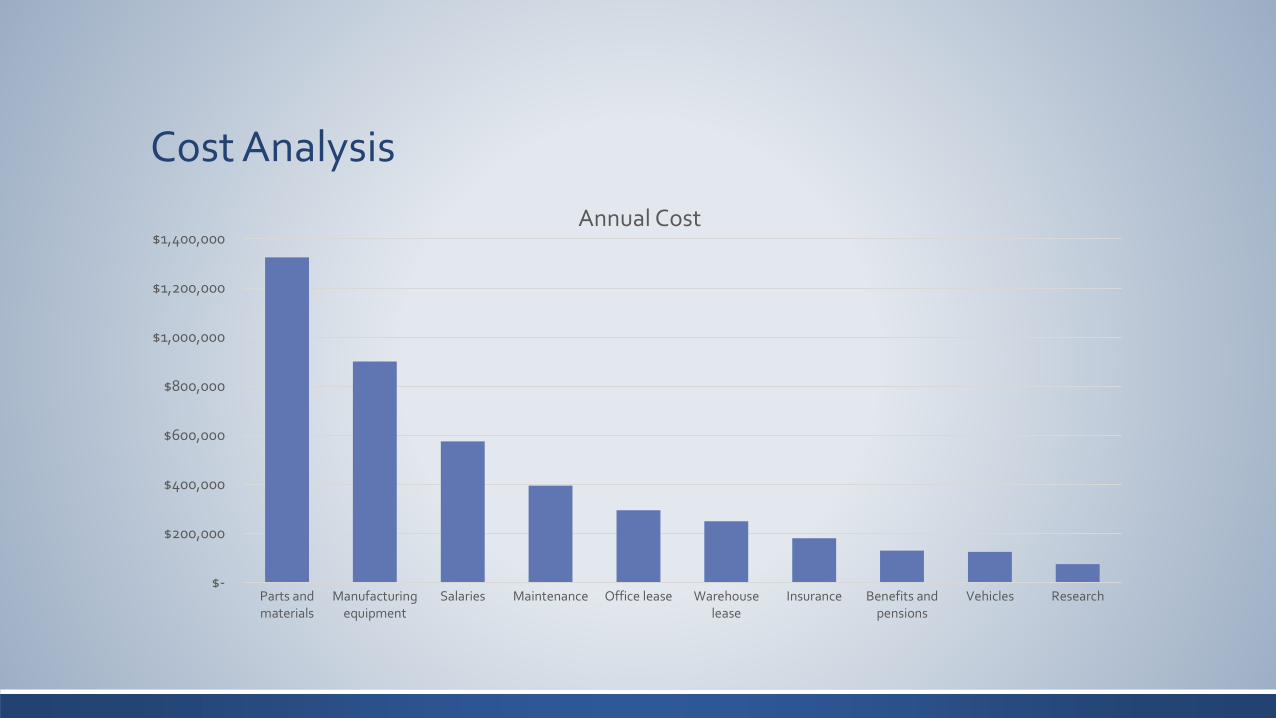

Cost Analysis

$-

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

$1,400,000

Parts andmaterials

Manufacturingequipment

Salaries Maintenance Office lease Warehouselease

Insurance Benefits andpensions

Vehicles Research

Annual Cost

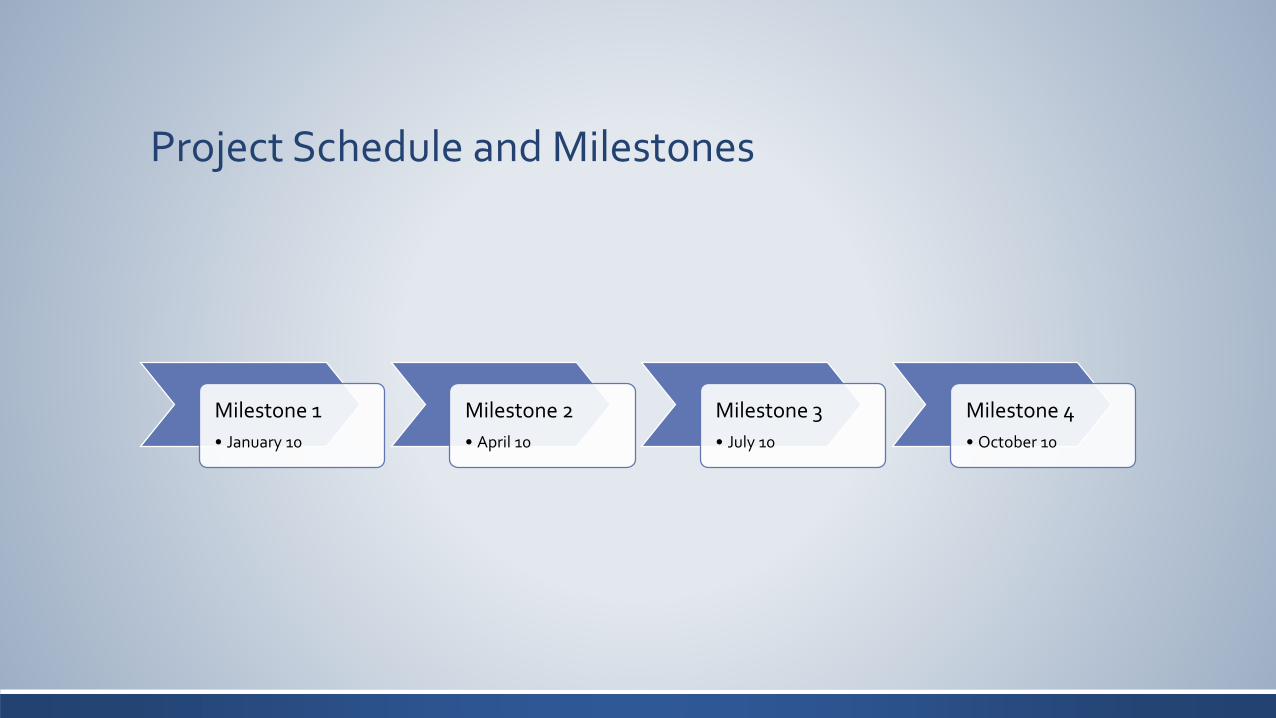

Project Schedule and Milestones

Milestone 1

• January 10

Milestone 2

• April 10

Milestone 3

• July 10

Milestone 4

• October 10

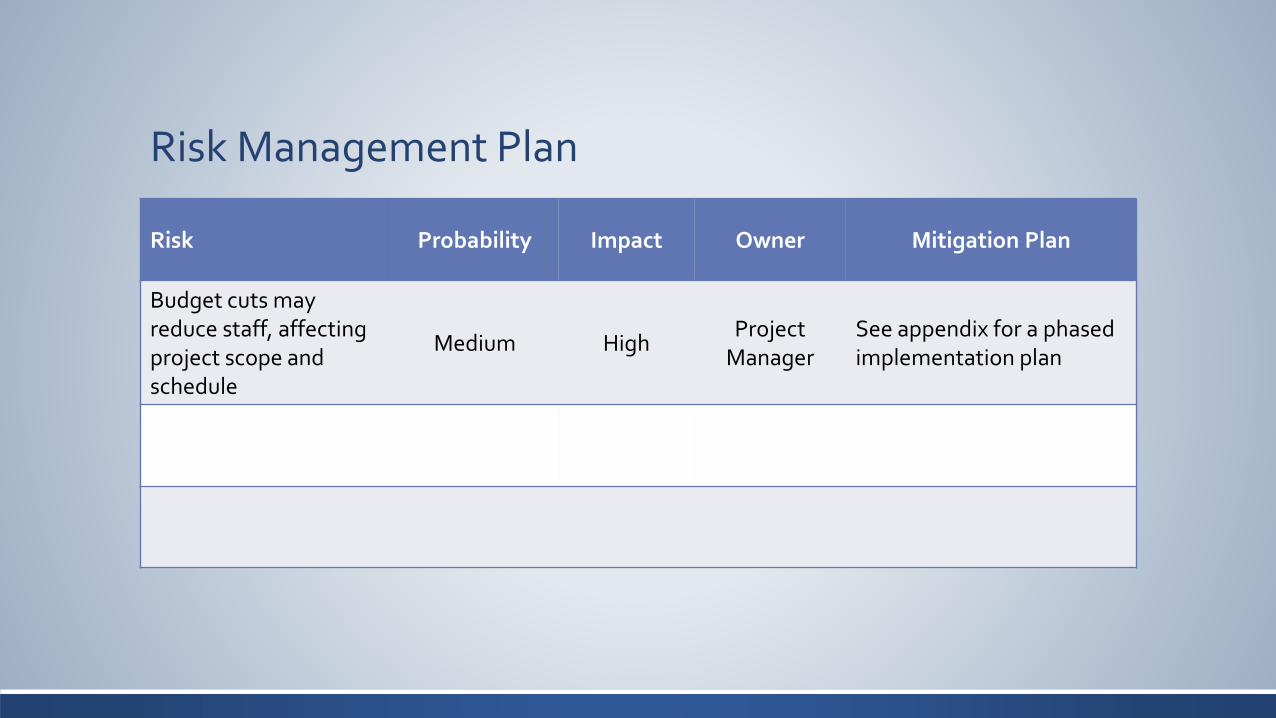

Risk Management Plan

Risk Probability Impact Owner Mitigation Plan

Budget cuts may reduce staff, affecting project scope and schedule

Medium HighProject

ManagerSee appendix for a phased implementation plan

Quality Management and Performance Measures

Define quality management plans

How will you monitor and control costs?

How will you monitor and control schedule?

Appendix

Reference supplementary materials and resources