Embed Size (px)

Citation preview

3Q 2019

International CSRC Investment Holdings Co.

INVESTOR'S CONFERENCE

Disclaimer

The forward-looking statements contained in this presentation are subject to risks

and uncertainties and actual results may differ materially from those expressed or

implied in these forward-looking statements.

International CSRC Investment Holdings Co. makes no representation or warranty

as to the accuracy or completeness of these forward-looking statements and nor

does International CSRC Investment Holdings Co. undertake any obligation to

update any forward-looking statements, whether as a result of new information or

future events.

Carbon B lack Segment

Biotech Segment

3Q 2019 Operat ing Resu l ts

01

02

03

CSRC Group Business Overview

AMERICAEUROPE/MEA ASIA

Manufacturing Sites

Technology Centers

Licensee Manufacturing Site

Offices

Sunray, TX

Ponca City, OK

Houston, TX

Barberton, OH

Phenix City, AL

Brussels, Belgium

Kemya, Saudi Arabia

New Delhi, India

Liaoning, Mainland China

Anhui, Mainland China

Chongqing, Mainland ChinaTaipei, Taiwan

Kaohsiung, Taiwan

E-ONE MOLI

E-ONE MOLI

E-ONE MOLI

Gujarat, India

Expansion Site

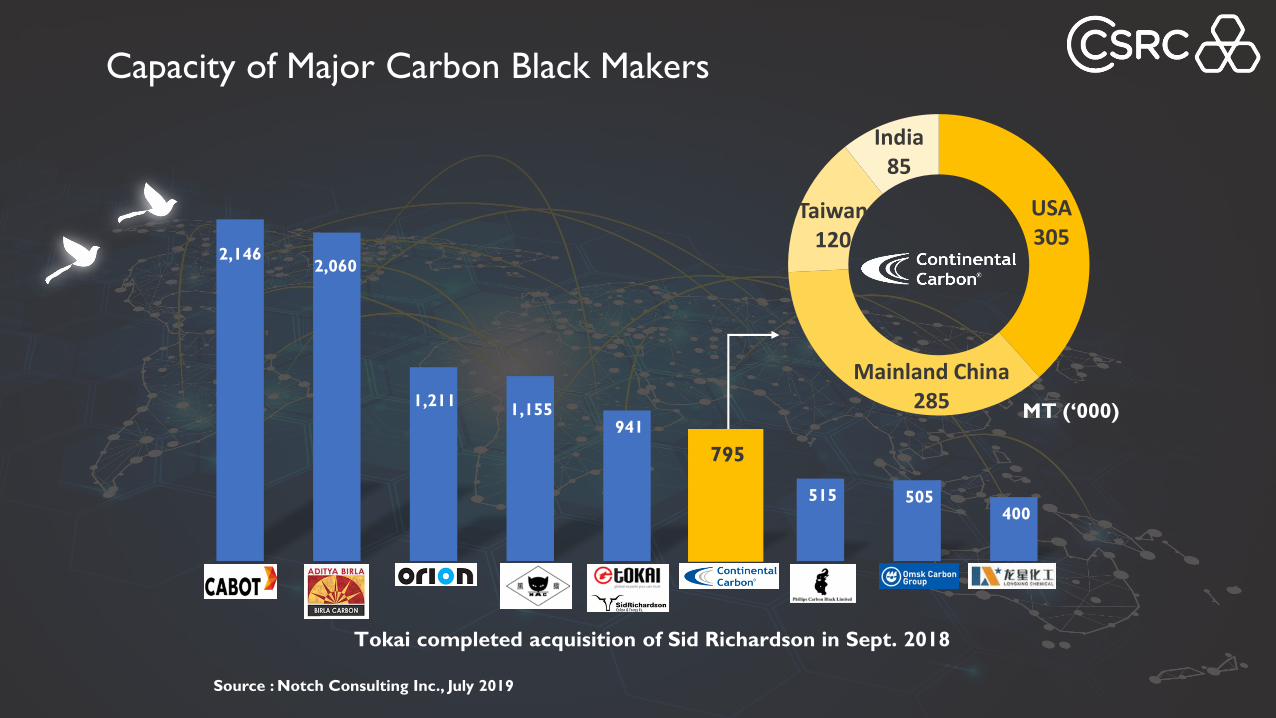

Carbon Black Segment

O1

2,1462,060

1,211 1,155

941

795

515 505 400

Cabot Birla Orion Black Cat Tokai & Sid

Richardson

CSRC PCBL OMSK Longxing

Source : Notch Consulting Inc., July 2019

Tokai completed acquisition of Sid Richardson in Sept. 2018

Capacity of Major Carbon Black Makers

795

USA305

Mainland China285

Taiwan120

India85

MT (‘000)

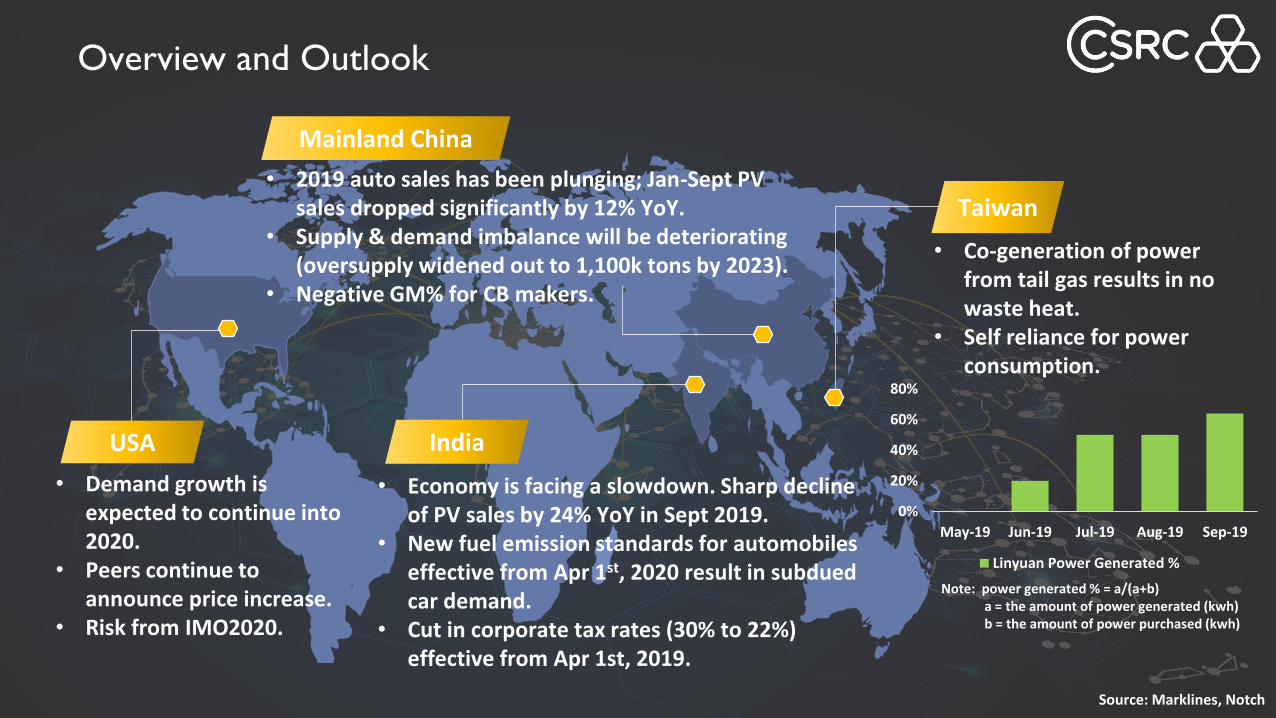

• Demand growth is expected to continue into 2020.

• Peers continue to announce price increase.

• Risk from IMO2020.

• 2019 auto sales has been plunging; Jan-Sept PV sales dropped significantly by 12% YoY.

• Supply & demand imbalance will be deteriorating(oversupply widened out to 1,100k tons by 2023).

• Negative GM% for CB makers.

• Economy is facing a slowdown. Sharp decline of PV sales by 24% YoY in Sept 2019.

• New fuel emission standards for automobiles effective from Apr 1st, 2020 result in subdued car demand.

• Cut in corporate tax rates (30% to 22%) effective from Apr 1st, 2019.

• Co-generation of power from tail gas results in no waste heat.

• Self reliance for power consumption.

Overview and Outlook

0%

20%

40%

60%

80%

May-19 Jun-19 Jul-19 Aug-19 Sep-19

Linyuan Power Generated %

Note: power generated % = a/(a+b)a = the amount of power generated (kwh)b = the amount of power purchased (kwh)

USA India

Mainland China

Taiwan

Source: Marklines, Notch

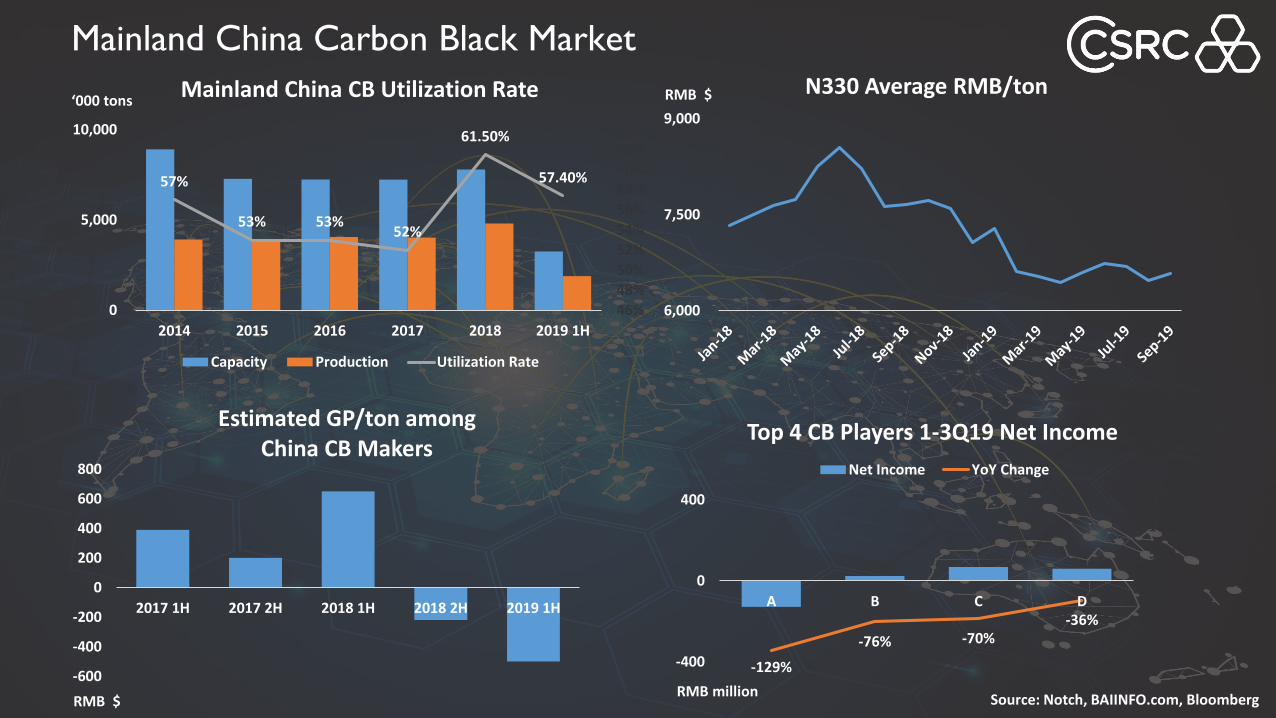

Mainland China Carbon Black Market

57%

53% 53%52%

61.50%

57.40%

46%

48%

50%

52%

54%

56%

58%

60%

62%

64%

0

5,000

10,000

2014 2015 2016 2017 2018 2019 1H

Mainland China CB Utilization Rate

Capacity Production Utilization Rate

-600

-400

-200

0

200

400

600

800

2017 1H 2017 2H 2018 1H 2018 2H 2019 1H

Estimated GP/ton among China CB Makers

6,000

7,500

9,000

N330 Average RMB/ton

-129%

-76% -70%-36%

-150%

-100%

-50%

0%

50%

100%

150%

-400

0

400

A B C D

Top 4 CB Players 1-3Q19 Net Income

Net Income YoY Change

Source: Notch, BAIINFO.com, BloombergRMB million

‘000 tons

RMB $

RMB $

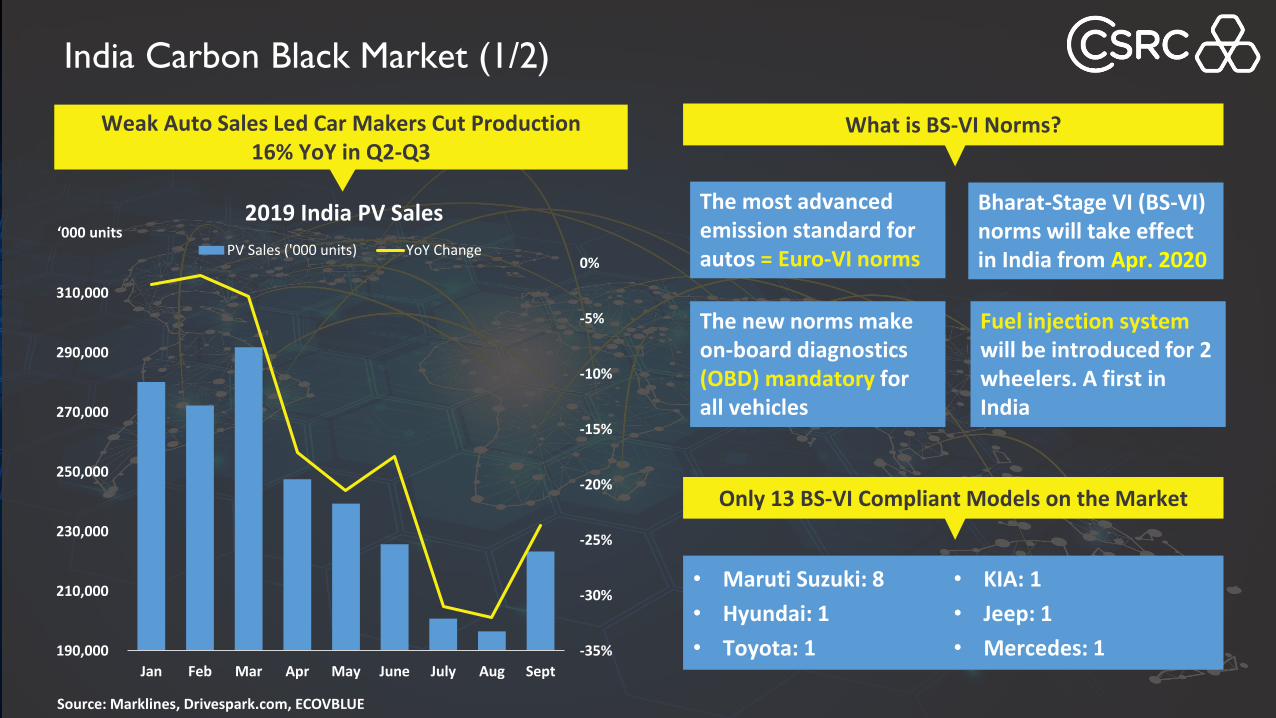

India Carbon Black Market (1/2)

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

190,000

210,000

230,000

250,000

270,000

290,000

310,000

Jan Feb Mar Apr May June July Aug Sept

2019 India PV Sales

PV Sales ('000 units) YoY Change

Source: Marklines, Drivespark.com, ECOVBLUE

Weak Auto Sales Led Car Makers Cut Production 16% YoY in Q2-Q3

‘000 units

What is BS-VI Norms?

• Maruti Suzuki: 8

• Hyundai: 1

• Toyota: 1

• KIA: 1

• Jeep: 1

• Mercedes: 1

Bharat-Stage VI (BS-VI) norms will take effect in India from Apr. 2020

The most advanced emission standard for autos = Euro-VI norms

Only 13 BS-VI Compliant Models on the Market

The new norms make on-board diagnostics (OBD) mandatory for all vehicles

Fuel injection system will be introduced for 2 wheelers. A first in India

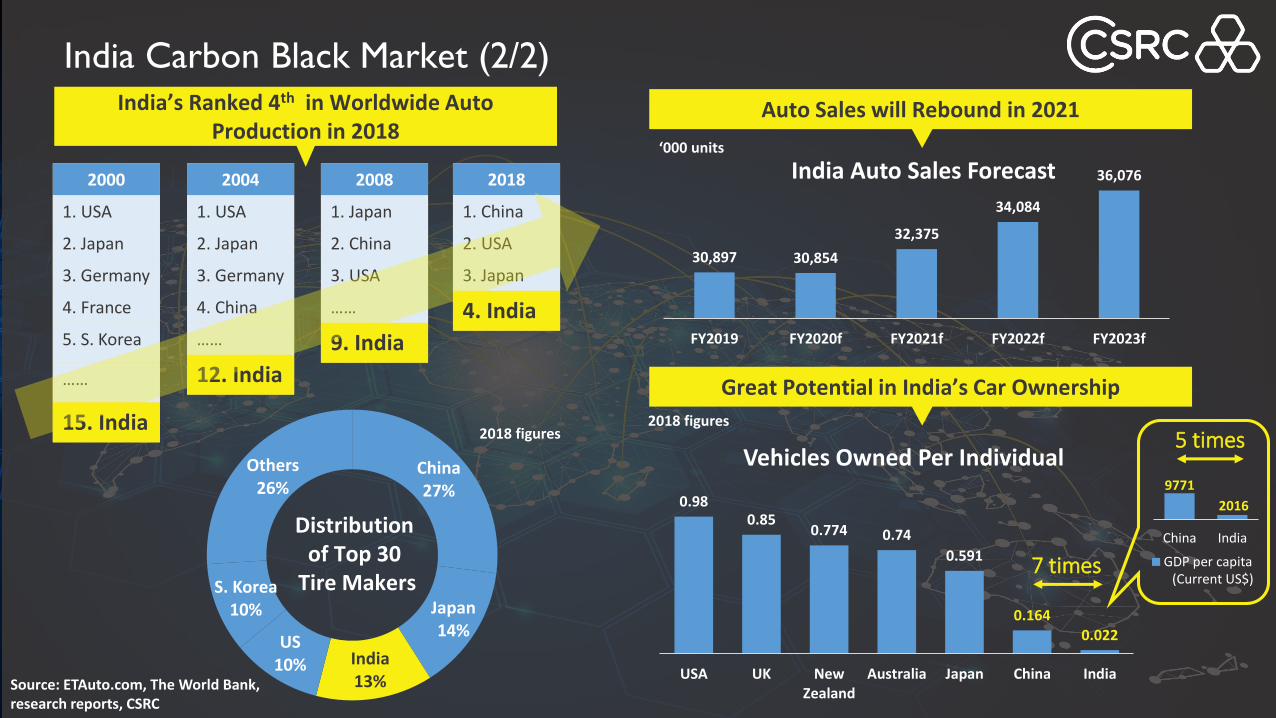

0.980.85

0.774 0.74

0.591

0.1640.022

USA UK NewZealand

Australia Japan China India

Vehicles Owned Per Individual

7 times

9771

2016500

10500

20500

China India

GDP per capita(Current US$)

5 times2018 figures

India Carbon Black Market (2/2)

Source: ETAuto.com, The World Bank,research reports, CSRC

India’s Ranked 4th in Worldwide Auto Production in 2018

2000

1. USA

2. Japan

3. Germany

4. France

5. S. Korea

……

15. India

2004

1. USA

2. Japan

3. Germany

4. China

……

12. India

2008

1. Japan

2. China

3. USA

……

9. India

2018

1. China

2. USA

3. Japan

4. India

30,897 30,854

32,375

34,084

36,076

FY2019 FY2020f FY2021f FY2022f FY2023f

India Auto Sales Forecast‘000 units

Auto Sales will Rebound in 2021

China27%

Japan14%

India13%

US10%

S. Korea10%

Others26%

Distribution of Top 30

Tire Makers

Great Potential in India’s Car Ownership

2018 figures

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5

2005 2010 2015 2020 2025

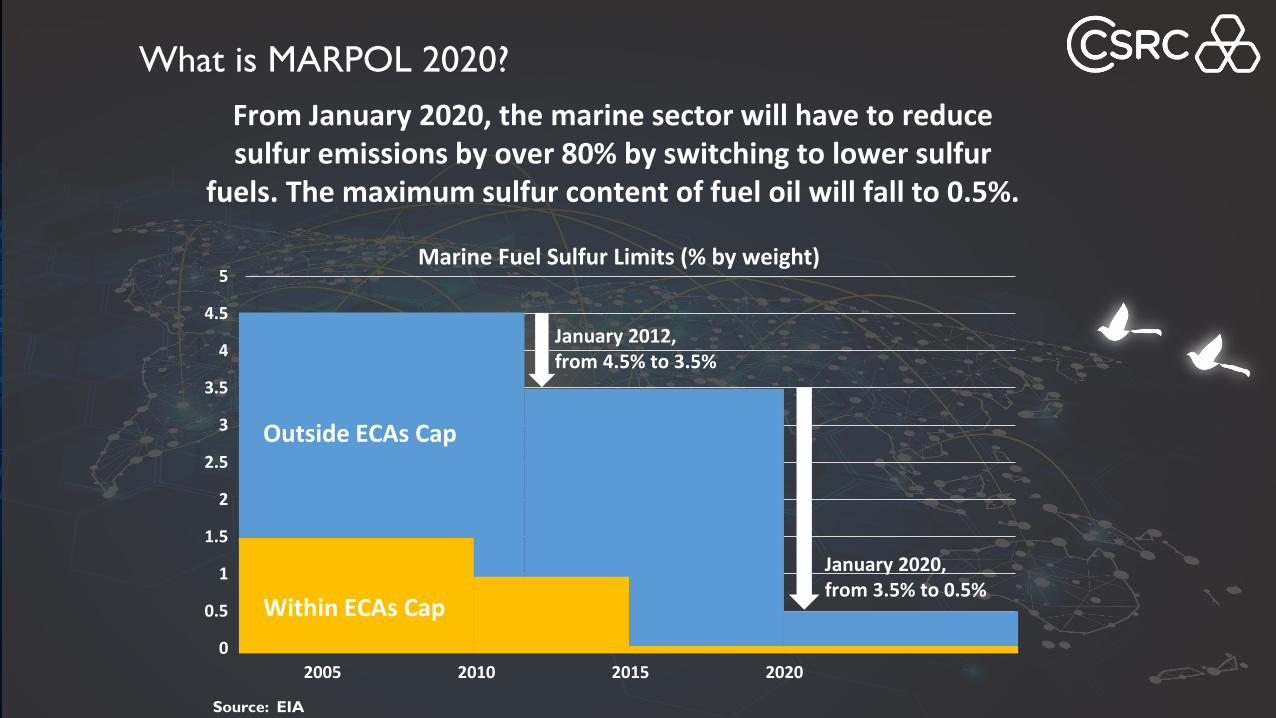

Marine Fuel Sulfur Limits (% by weight)

What is MARPOL 2020?

Outside ECAs Cap

Within ECAs Cap

January 2012, from 4.5% to 3.5%

January 2020, from 3.5% to 0.5%

From January 2020, the marine sector will have to reduce sulfur emissions by over 80% by switching to lower sulfur

fuels. The maximum sulfur content of fuel oil will fall to 0.5%.

Source: EIA

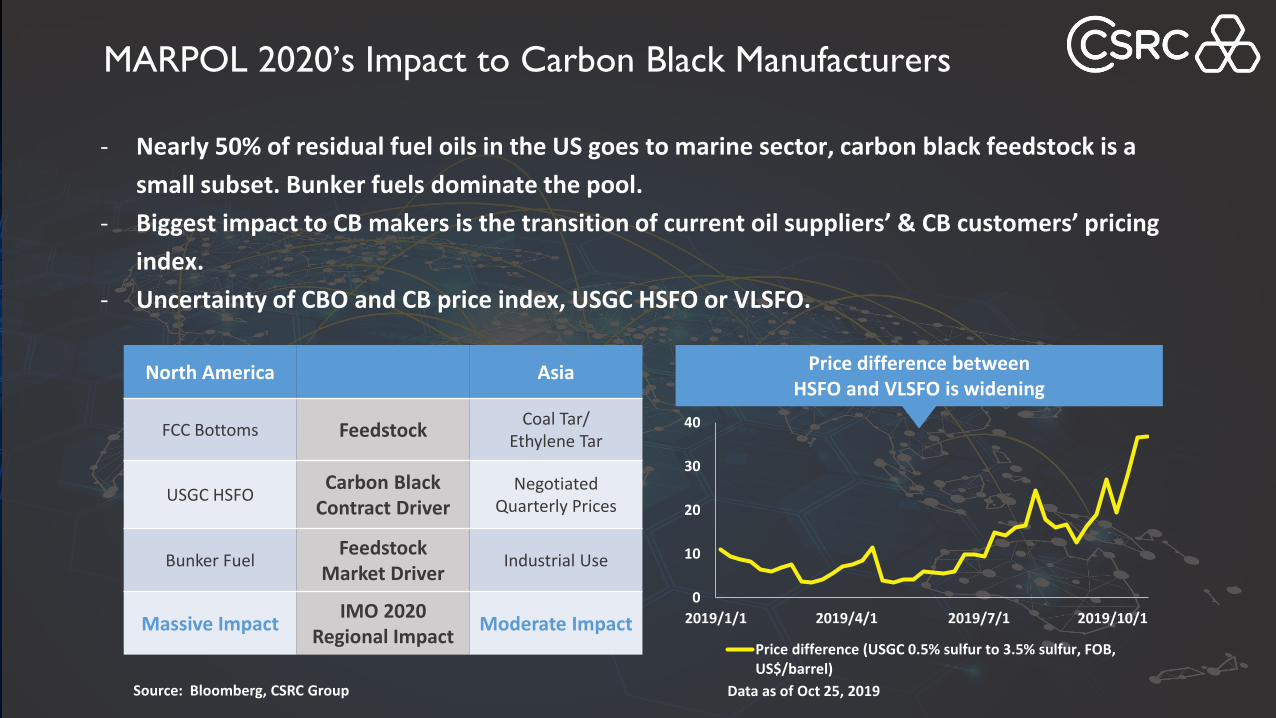

MARPOL 2020’s Impact to Carbon Black Manufacturers

- Nearly 50% of residual fuel oils in the US goes to marine sector, carbon black feedstock is a

small subset. Bunker fuels dominate the pool.

- Biggest impact to CB makers is the transition of current oil suppliers’ & CB customers’ pricing

index.

- Uncertainty of CBO and CB price index, USGC HSFO or VLSFO.

North America Asia

FCC Bottoms FeedstockCoal Tar/

Ethylene Tar

USGC HSFOCarbon Black

Contract DriverNegotiated

Quarterly Prices

Bunker FuelFeedstock

Market DriverIndustrial Use

Massive ImpactIMO 2020

Regional ImpactModerate Impact

Source: Bloomberg, CSRC Group

0

10

20

30

40

2019/1/1 2019/4/1 2019/7/1 2019/10/1

Price difference (USGC 0.5% sulfur to 3.5% sulfur, FOB,US$/barrel)

Data as of Oct 25, 2019

Price difference between HSFO and VLSFO is widening

- R&D Centers built in Taiwan & India to strengthen capabilities.

- Moving up the value chain in rubber and non-rubber grades to

develop a stronger product portfolio.

- Continue to grow market share and expand operations to new

geographies.

Growth Strategies

Strong Focus on Research and Development

Innovation towards Tire Black

CONTINEX LH SERIES

Environmental Friendly

Carbon Black for

Truck & Passenger Car Tires

Made for Green Tire, Enhancing Fuel Economy

- Greater Dispersibility & Processability

- Reducing Rolling Resistance of Tires

- Increasing Wear Resistance of Tires

- Improving Heat Build-Up of Tires

金鉅獎

年度創新獎

Heat Build-Up

Rolling Resistance

Wear Resistance

Innovation towards Non-Tire Black

SATIN BLACK SERIES

Providing better appearance, higher reinforcement,

and greater pigmentation

- Handle Grips

- Rubber Tubes

- Shoe Soles

- Car Door Seals

- Conveyor Belts

- Color Masterbatch

- Cables and Wires

- Automotive Interiors

- PE & PVC Pipes

- Plastic Moulded Goods

PlasticsRubber

Summer Camp at Shanwei Elementary School, Taiwan 2019

Donation of Environmental Comic Books , Taiwan 2019

Commitment to Sustainability (1/2)

Cement Academy, Mainland China 2019

International Day of Yoga, India 2019

Commitment to Sustainability (2/2)

TCSA

企業永續報告

金獎

CSR Awards TCIA Award

TCSA

台灣永續企業

績優獎

EcoVadis

企業社會責任

銀牌獎

TCIA

循環經濟

成果獎

Biotech Segment

O2

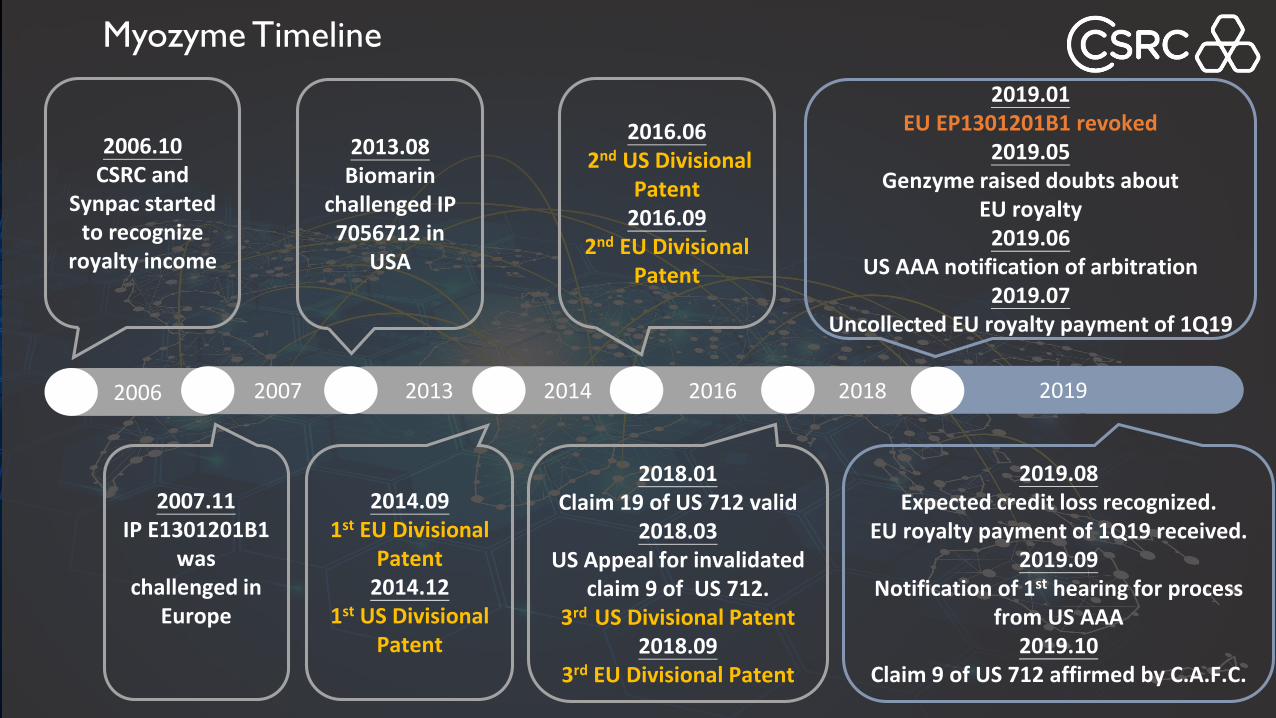

Myozyme Timeline

2007 2013

2007.11IP E1301201B1

was challenged in

Europe

2013.08Biomarin

challenged IP 7056712 in

USA

2014

2014.091st EU Divisional

Patent 2014.12

1st US Divisional Patent

2016

2016.062nd US Divisional

Patent 2016.09

2nd EU Divisional Patent

2018

2018.01Claim 19 of US 712 valid

2018.03US Appeal for invalidated

claim 9 of US 712.3rd US Divisional Patent

2018.093rd EU Divisional Patent

2019

2019.08Expected credit loss recognized.

EU royalty payment of 1Q19 received.2019.09

Notification of 1st hearing for process from US AAA

2019.10Claim 9 of US 712 affirmed by C.A.F.C.

2019.01EU EP1301201B1 revoked

2019.05Genzyme raised doubts about

EU royalty 2019.06

US AAA notification of arbitration2019.07

Uncollected EU royalty payment of 1Q19

2006

2006.10CSRC and

Synpac started to recognize

royalty income

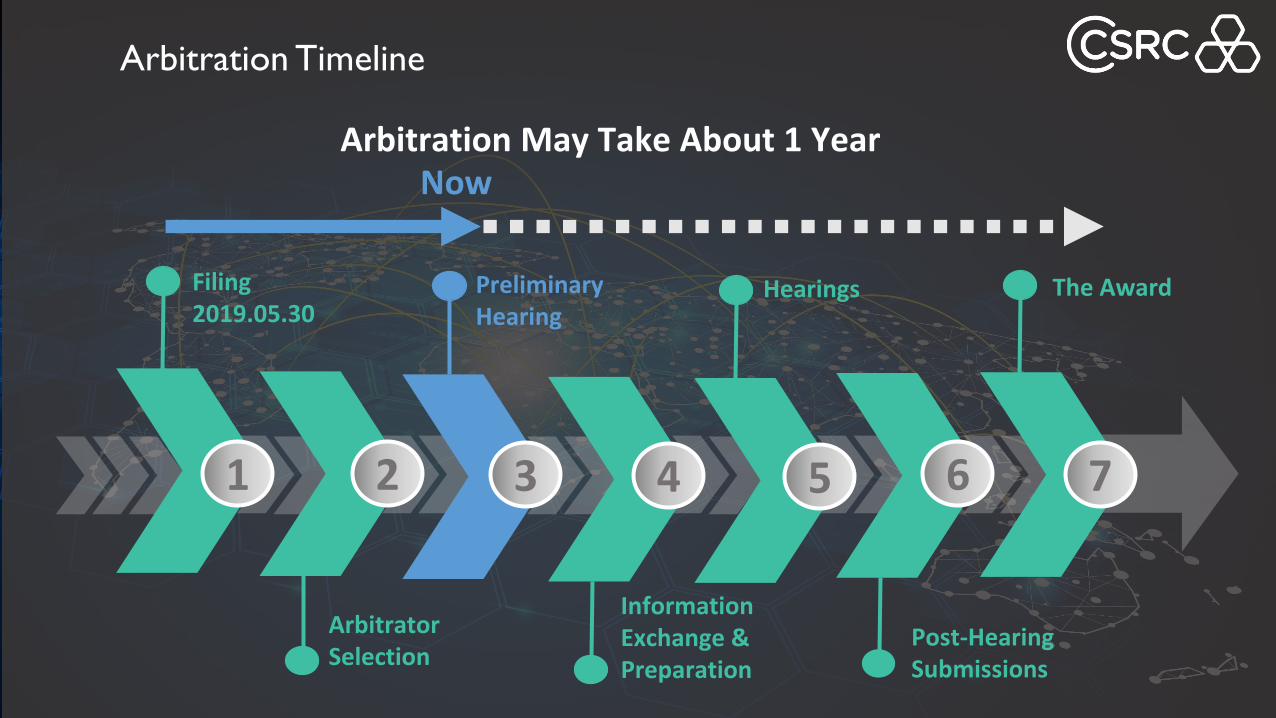

Arbitration Timeline

1 2 3 4 5 6 7

Filing2019.05.30

Arbitrator Selection

Preliminary Hearing

Information Exchange & Preparation

Hearings

Post-Hearing Submissions

The Award

NowArbitration May Take About 1 Year

3Q 2019 Operating Results

O3

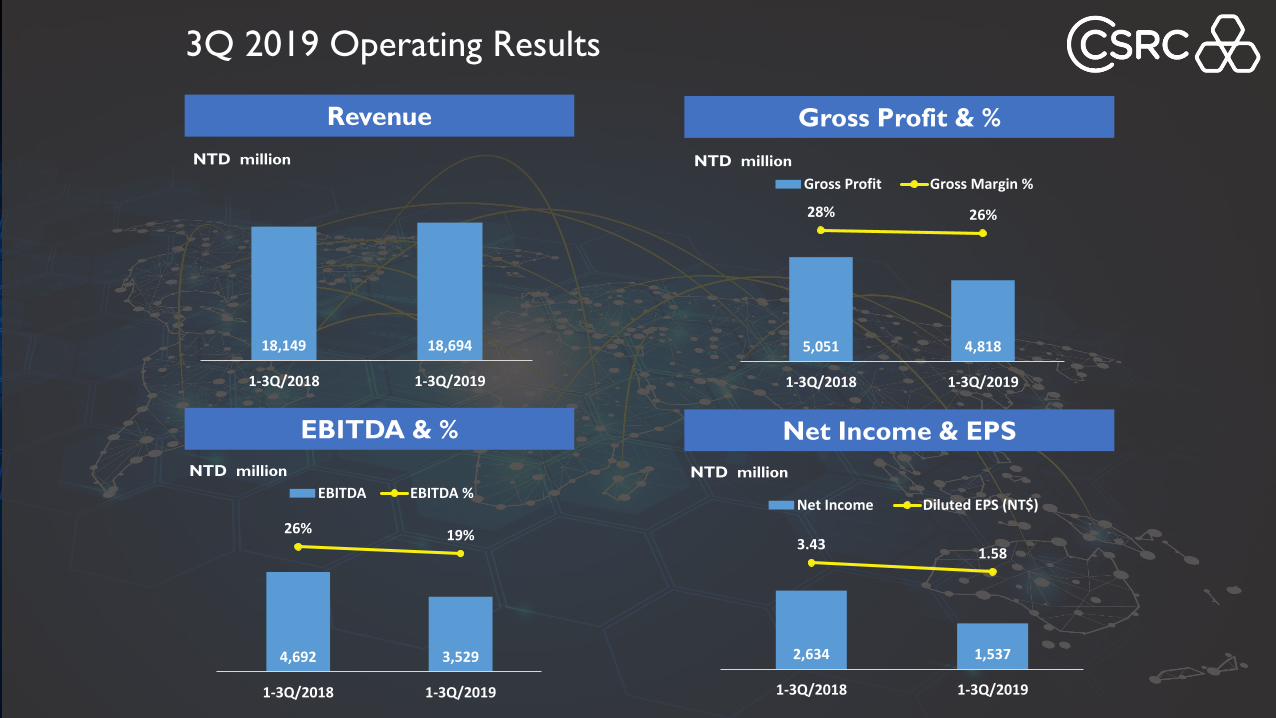

3Q 2019 Operating Results

Revenue Gross Profit & %

EBITDA & % Net Income & EPS

NTD million

NTD million

18,149 18,694

1-3Q/2018 1-3Q/2019

5,051 4,818

28% 26%

1-3Q/2018 1-3Q/2019

Gross Profit Gross Margin %

4,692 3,529

26% 19%

1-3Q/2018 1-3Q/2019

EBITDA EBITDA %

2,634 1,537

3.431.58

1-3Q/2018 1-3Q/2019

Net Income Diluted EPS (NT$)

NTD million

NTD million

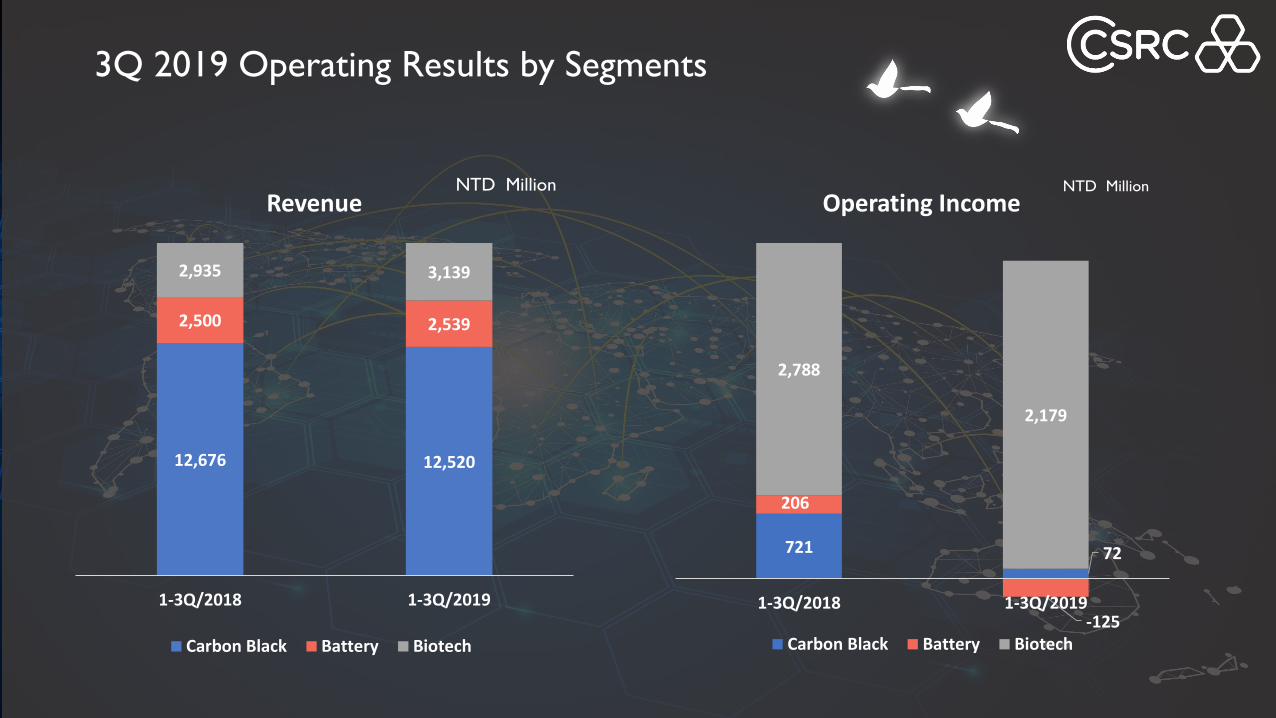

12,676 12,520

2,500 2,539

2,935 3,139

1-3Q/2018 1-3Q/2019

Revenue

Carbon Black Battery Biotech

3Q 2019 Operating Results by Segments

721 72

206

-125

2,788

2,179

1-3Q/2018 1-3Q/2019

Operating Income

Carbon Black Battery Biotech

NTD Million NTD Million

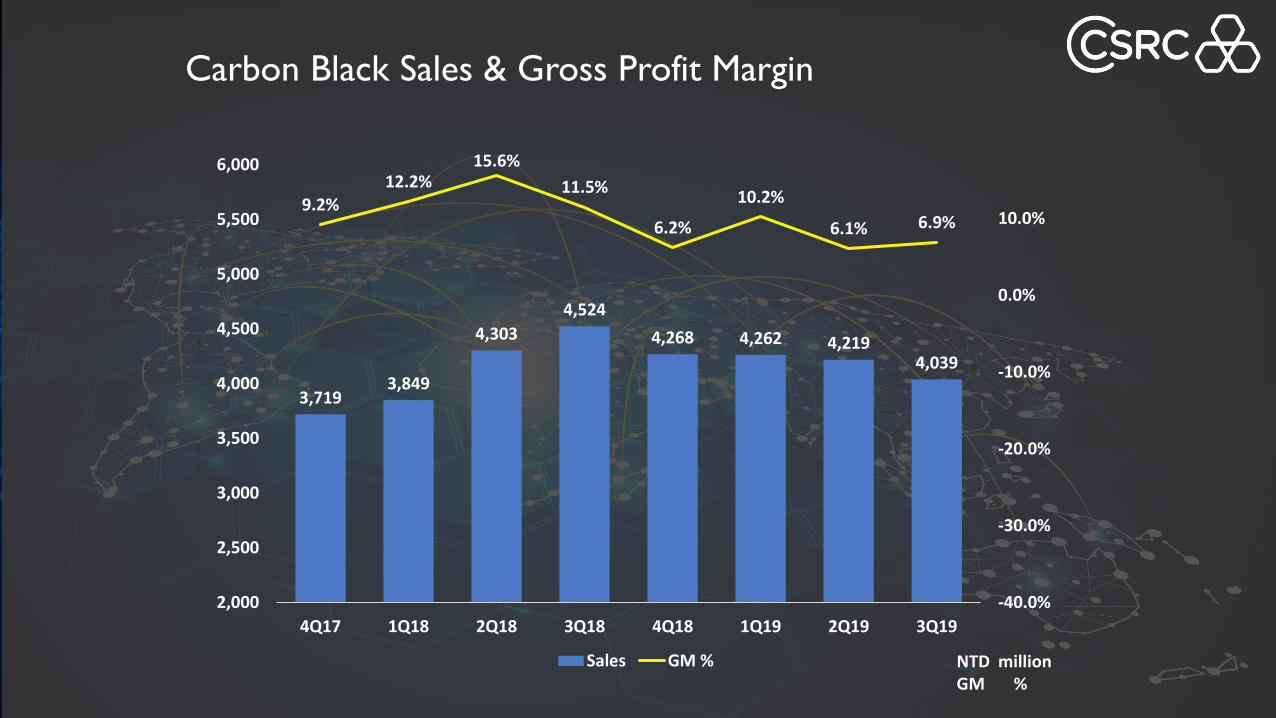

Carbon Black Sales & Gross Profit Margin

NTD millionGM %

3,7193,849

4,303

4,524

4,268 4,262 4,2194,039

9.2%12.2%

15.6%

11.5%

6.2%

10.2%

6.1% 6.9%

-40.0%

-30.0%

-20.0%

-10.0%

0.0%

10.0%

2,000

2,500

3,000

3,500

4,000

4,500

5,000

5,500

6,000

4Q17 1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19

Sales GM %

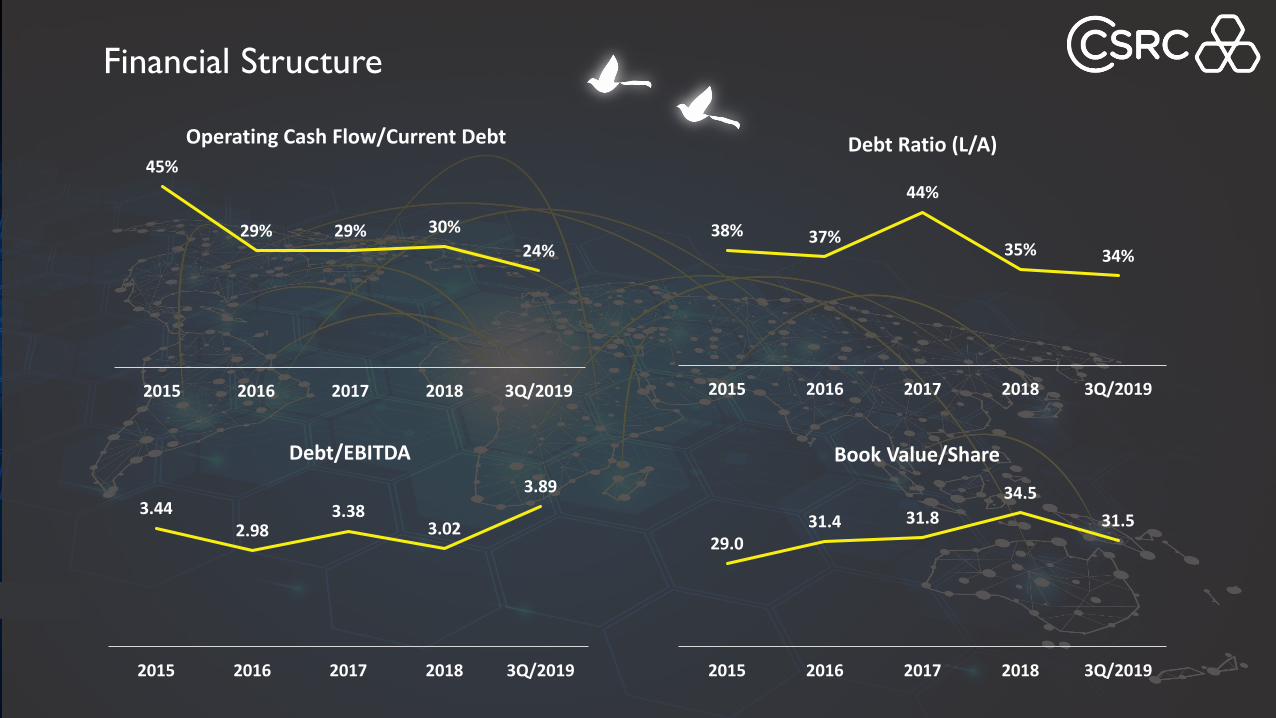

Financial Structure

45%

29% 29% 30%

24%

2015 2016 2017 2018 3Q/2019

Operating Cash Flow/Current Debt

3.44 2.98

3.38 3.02

3.89

2015 2016 2017 2018 3Q/2019

Debt/EBITDA

38% 37%

44%

35% 34%

2015 2016 2017 2018 3Q/2019

Debt Ratio (L/A)

29.0 31.4 31.8

34.5

31.5

2015 2016 2017 2018 3Q/2019

Book Value/Share