Embed Size (px)

Citation preview

Plenary Session IASB@AFRAC 2007

Monday, 26 November 2007 1

®

International Accounting Standards

Board

Technical UpdateTechnical UpdateIASB Progress & PlansIASB Progress & Plans

IASB IASB RoadshowRoadshow –– Vienna 26 November 2007Vienna 26 November 2007Philippe DANJOU Member of Philippe DANJOU Member of IASBIASB

The views expressed in this presentation are those of the presenThe views expressed in this presentation are those of the presenters, ters, not necessarily those of the IASBnot necessarily those of the IASB

Agenda for Agenda for todaytoday

Part I : IASB Part I : IASB –– WhyWhy ? ? WhatWhat isis itit ? ? WhichWhichimpact ?impact ?Part II Part II –– TechnicalTechnical plan and plan and recentrecent textstexts

Plenary Session IASB@AFRAC 2007

Monday, 26 November 2007 2

The The towertower of Babelof Babel

PART I PART I -- IASBIASB

Structures and Structures and processesprocessesInfluence Influence todaytodayConvergence, adoption, etc.Convergence, adoption, etc.

Plenary Session IASB@AFRAC 2007

Monday, 26 November 2007 3

HistoryHistory19731973 International Accounting Standards International Accounting Standards

Committee (IASC) founded by 10 Committee (IASC) founded by 10 national accountancy organisations. national accountancy organisations.

19811981 All members of IFAC became All members of IFAC became members of IASC.members of IASC.

19991999 100+ countries. Structure reviewed.100+ countries. Structure reviewed.20012001 International Accounting Standards International Accounting Standards

Board (IASB) began operations.Board (IASB) began operations.20042004 Constitutional reviewConstitutional review20052005 EU adoptionEU adoption20072007 US lifts reconciliationUS lifts reconciliation

IASB’sIASB’s missionmission

IASBIASB… is committed to developing, in the … is committed to developing, in the public interest, a single set of high public interest, a single set of high quality, global accounting standards quality, global accounting standards that require transparent and that require transparent and comparable information in financial comparable information in financial statements … statements …

Plenary Session IASB@AFRAC 2007

Monday, 26 November 2007 4

Working groups

ARG, GPG…

Standards Advisory Council

IASC Foundation

(22 Trustees)

StructureStructure

(14) International Accounting

Standards Board

Staff

(12+) IFRIC

The standard setting operation

IFRS

IFRIC

International regulators

Members of the Board Members of the Board

Tatsumi YamadaTatsumi YamadaGilbert Gilbert GélardGélardPhilippe DanjouPhilippe DanjouRobert GarnettRobert GarnettJohn SmithJohn SmithJan Jan EngströmEngström

Warren McGregorWarren McGregorxx

WeiWei--Guo ZhangGuo ZhangStephen CooperStephen Cooper

James LeisenringJames LeisenringMary BarthMary BarthThomas Jones, Vice ChairmanThomas Jones, Vice Chairman

Sir David Tweedie, Chairman Sir David Tweedie, Chairman

Plenary Session IASB@AFRAC 2007

Monday, 26 November 2007 5

IASB CompositionIASB Composition

131333United StatesUnited States33United KingdomUnited Kingdom11SwedenSweden

131311South AfricaSouth Africa22OtherOther11JapanJapan22AcademicAcademic11Analyst/UserAnalyst/User22FranceFrance33PreparerPreparer11ChinaChina55AuditorAuditor11Australia / NZAustralia / NZ

Elements ofElements of due processdue process

Research

StandardSetter/ EFRAG

DiscussionPaper

Exposure Draft

Others

Comment analysis

9-15 months 9-15 months

Comment analysis

EffectiveDate

12-18 months

FeedbackstatementsRoundtables

>01/01/2009>01/01/2009

Standard

2 years Postimplementation

review

Plenary Session IASB@AFRAC 2007

Monday, 26 November 2007 6

Tracking the processTracking the process

WebsiteWebsitewww.iasb.orgwww.iasb.org

Meetings:Meetings:Observer notes Observer notes Web cast of IASB meetingWeb cast of IASB meetingDecision summaries / UpdateDecision summaries / Update

12

INFLUENCE OF ACCOUNTING INFLUENCE OF ACCOUNTING STANDARDS IN THE WORLD (2007)STANDARDS IN THE WORLD (2007)

MarketMarket capitalizationscapitalizations by by accountingaccounting normnorm

0

10

20

30

40

50

60

trillion $

IFRS in force:Euronext,DeutscheBorse, LSE…IFRS convergent

US GAAP

Total world 58trn

31% 26% 43%

100%

1815 25

58

44% of the world’s Fortune 500 Companiesreport under IFRS and 18% are injurisdictions that converge to IFRS

Source : Azieres Conseil

Plenary Session IASB@AFRAC 2007

Monday, 26 November 2007 7

Adoption or Convergence Adoption or Convergence

IFRS

USA2007 FPIs

JAPAN2011

AUSNZ, SA2005-2007

CANADA2011

ADOPTION,CONVERGENCE,EQUIVALENCE...ACCELERATION OF MOMENTUM

CHINAEnd 2009

KOREAFrom 2009-2011

INDIAFrom 2011

EU2005-2007

BRAZILFrom 2010

CHILEFrom 2009

Plenary Session IASB@AFRAC 2007

Monday, 26 November 2007 8

SECSEC-- RoadmapRoadmapWashington, D.C., Washington, D.C., April 21, 2005April 21, 2005 —— SEC Chairman William Donaldson and SEC Chairman William Donaldson and EU Internal Market Commissioner Charles EU Internal Market Commissioner Charles McCreevyMcCreevy met today to discuss met today to discuss a range of topics of mutual interest between the Commission and a range of topics of mutual interest between the Commission and the the European Union, including the importance of compatible approacheEuropean Union, including the importance of compatible approaches to s to furthering investor protection, and expanding the use of highfurthering investor protection, and expanding the use of high--quality quality global accounting standards. global accounting standards. Chairman Donaldson reaffirmed his support for the convergenChairman Donaldson reaffirmed his support for the convergence program ce program being undertaken jointly by the International Accounting Standarbeing undertaken jointly by the International Accounting Standards Board ds Board (IASB) and the U.S. Financial Accounting Standards Board (FASB).(IASB) and the U.S. Financial Accounting Standards Board (FASB).

Washington, D.C., Washington, D.C., Feb. 8, 2006Feb. 8, 2006 —— On the occasion of the visit of EU On the occasion of the visit of EU Internal Markets Commissioner Charlie Internal Markets Commissioner Charlie McCreevyMcCreevy to Washington DC, SEC to Washington DC, SEC Chairman Christopher Cox and Commissioner Chairman Christopher Cox and Commissioner McCreevyMcCreevy took stock of took stock of progress on and affirmed their commitment to eliminating the neeprogress on and affirmed their commitment to eliminating the need for d for reconciliation between International Financial Reporting Standarreconciliation between International Financial Reporting Standards (IFRS) ds (IFRS) and US Generally Accepted Accounting Principles (GAAP).and US Generally Accepted Accounting Principles (GAAP).

SECSEC-- RoadmapRoadmapWashington, D.C., Washington, D.C., July 3, 2007July 3, 2007 -- The Securities and The Securities and Exchange Commission has published for public Exchange Commission has published for public comment a proposal to eliminate the current comment a proposal to eliminate the current requirement that foreign private issuers filing their requirement that foreign private issuers filing their financial statements using International Financial financial statements using International Financial Reporting Standards (IFRS) Reporting Standards (IFRS) as published by the as published by the International Accounting Standards Board (IASB) International Accounting Standards Board (IASB) also file a reconciliation of those financial also file a reconciliation of those financial statements to U.S. Generally Accepted Accounting statements to U.S. Generally Accepted Accounting Principles (U.S. GAAP). The Commission voted Principles (U.S. GAAP). The Commission voted unanimously on June 20, 2007, to issue the proposal unanimously on June 20, 2007, to issue the proposal for public comment.for public comment.

Plenary Session IASB@AFRAC 2007

Monday, 26 November 2007 9

Washington, D.C., Washington, D.C., November 15, 2007November 15, 2007 -- …the …the Commission today approved…financial statements from Commission today approved…financial statements from foreign private issuers in the U.S. will be foreign private issuers in the U.S. will be accepted accepted without reconciliationwithout reconciliation to U.S. Generally Accepted to U.S. Generally Accepted Accounting Principles Accounting Principles only if they are prepared using only if they are prepared using International Financial Reporting Standards (IFRS) as International Financial Reporting Standards (IFRS) as issued by the International Accounting Standards issued by the International Accounting Standards BoardBoard...apply to financial statements covering years ...apply to financial statements covering years ended after Nov. 15, 2007…the SEC will convene two ended after Nov. 15, 2007…the SEC will convene two roundtables, on December 13 and December 17, to collect roundtables, on December 13 and December 17, to collect more feedback from the public on the issue of giving U.S. more feedback from the public on the issue of giving U.S. domestic issuers the same option that foreign issuers domestic issuers the same option that foreign issuers have in our markets to use either IFRS or U.S. GAAP. have in our markets to use either IFRS or U.S. GAAP. http://www.sec.gov/news/press/2007/2007http://www.sec.gov/news/press/2007/2007--235.htm235.htm

SECSEC-- RoadmapRoadmap

FASB/IASB AgreementFASB/IASB Agreement

Remove differencesRemove differencesAlign AgendasAlign AgendasInterpretationInterpretation

Plenary Session IASB@AFRAC 2007

Monday, 26 November 2007 10

RoadmapRoadmap1.1. Align conceptual frameworkAlign conceptual framework

2.2. Short termShort term-- remove major differences remove major differences

3.3. Medium termMedium term-- new joint standards where significant new joint standards where significant improvement requiredimprovement required

Plenary Session IASB@AFRAC 2007

Monday, 26 November 2007 11

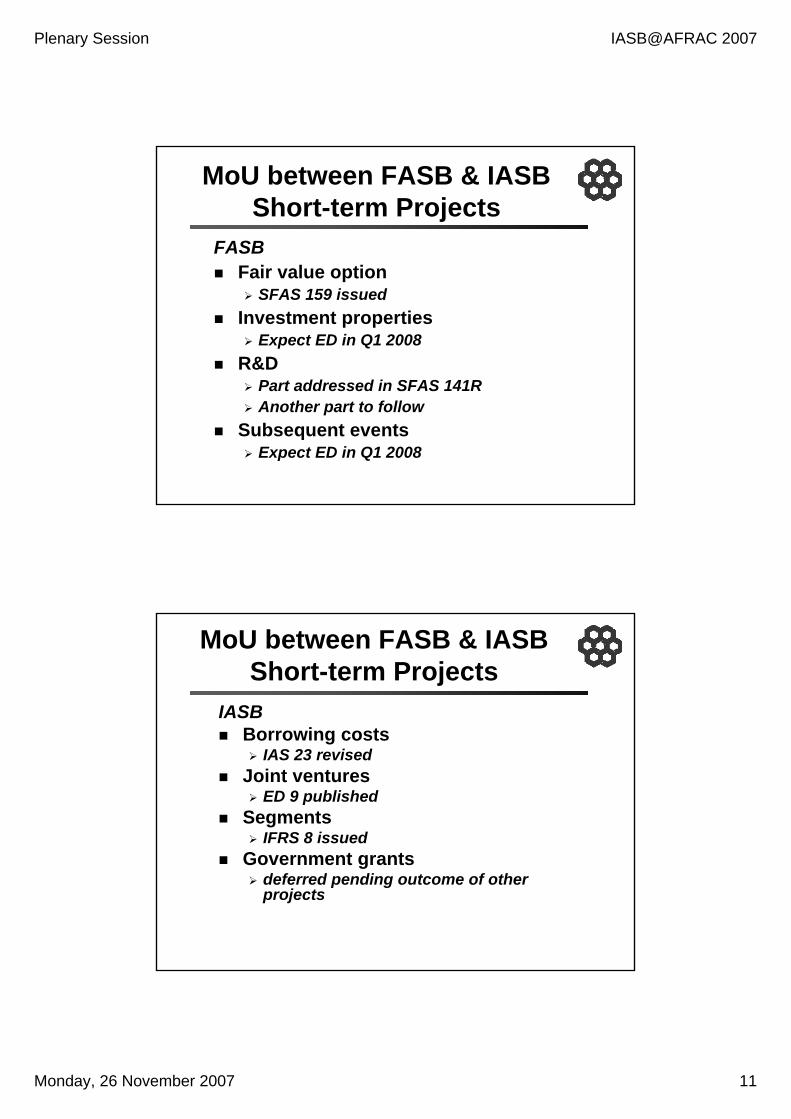

MoUMoU between FASB & IASBbetween FASB & IASBShortShort--term Projectsterm Projects

FASBFASBFair value optionFair value option

SFAS 159 issuedSFAS 159 issuedInvestment propertiesInvestment properties

Expect ED in Q1 2008Expect ED in Q1 2008R&DR&D

Part addressed in SFAS 141RPart addressed in SFAS 141RAnother part to followAnother part to follow

Subsequent eventsSubsequent eventsExpect ED in Q1 2008Expect ED in Q1 2008

MoUMoU between FASB & IASBbetween FASB & IASBShortShort--term Projectsterm Projects

IASBIASBBorrowing costsBorrowing costs

IAS 23 revisedIAS 23 revisedJoint ventures Joint ventures

ED 9 publishedED 9 publishedSegments Segments

IFRS 8 issuedIFRS 8 issuedGovernment grants Government grants

deferred pending outcome of other deferred pending outcome of other projectsprojects

Plenary Session IASB@AFRAC 2007

Monday, 26 November 2007 12

MoUMoU between FASB & IASBbetween FASB & IASBShortShort--term Projectsterm Projects

JointJointImpairment Impairment

agenda decision by end of 2007agenda decision by end of 2007Income taxes Income taxes

expect ED in Q1 2008expect ED in Q1 2008

MoU MoU –– MilestonesMilestones

MilestoneMilestone——Due process documentDue process documenton all topics to be issued on all topics to be issued Work doneWork done——IAS 1 revised, Q3 2007 IAS 1 revised, Q3 2007 ExpectExpect——PVD & DP in Q1 2008PVD & DP in Q1 2008

Financial Statement Financial Statement PresentationPresentation

MilestoneMilestone——Converged Converged guidanceguidance to to be issuedbe issuedWork doneWork done——SFAS 157 and DP SFAS 157 and DP Fair Fair Value MeasurementsValue Measurements issuedissued

Fair Value Measurement Fair Value Measurement guidanceguidance

AchievedAchieved——SFAS 141, IFRS 3 and SFAS 141, IFRS 3 and IAS 27 revised and SFAS 160 issuedIAS 27 revised and SFAS 160 issued

Business CombinationsBusiness Combinations

2008 Milestone2008 MilestoneProjectProject

Plenary Session IASB@AFRAC 2007

Monday, 26 November 2007 13

MoU MoU –– MilestonesMilestones

MilestoneMilestone——Due process documentDue process documentto be issued to be issued Work doneWork done——SFAS 158 issuedSFAS 158 issuedExpectExpect——DP in Q1 2008DP in Q1 2008

PostPost--employment Benefitsemployment Benefits

MilestoneMilestone——Due process documentDue process documentto be issuedto be issuedExpectExpect——PVD & DP in Q4 2007PVD & DP in Q4 2007

Liabilities and EquityLiabilities and Equity

MilestoneMilestone——Due process documentDue process documentfor comprehensive standard to be for comprehensive standard to be issued issued ExpectExpect——PVD & DP in H1 2008PVD & DP in H1 2008

Revenue RecognitionRevenue Recognition

2008 Milestone2008 MilestoneProjectProject

MoU MoU –– MilestonesMilestones

MilestoneMilestone——Implement work to Implement work to complete development of converged complete development of converged standards standards ExpectExpect——ITC & DP in H1 2008ITC & DP in H1 2008

Consolidations and Consolidations and SPEsSPEs

MilestoneMilestone——Due process documentDue process document to to be issued be issued ExpectExpect——PVD & DP in Q1 2008PVD & DP in Q1 2008

Financial InstrumentsFinancial Instruments

MilestoneMilestone——Due process documentDue process document to to be issued on results of staff research be issued on results of staff research ExpectExpect——staff research report in Q4 staff research report in Q4 20072007

DerecognitionDerecognition

2008 Milestone2008 MilestoneProjectProject

Plenary Session IASB@AFRAC 2007

Monday, 26 November 2007 14

MoU MoU –– MilestonesMilestones

MilestoneMilestone——Consider results of Consider results of research and research and decide on scope and decide on scope and timing of potential agenda projectstiming of potential agenda projectsCommitmentCommitment——both Boards to both Boards to consider agenda proposal in Q4 2007consider agenda proposal in Q4 2007

Intangible AssetsIntangible Assets

AchievedAchieved——scope of the project scope of the project determined and placed on the Active determined and placed on the Active Agenda of both BoardsAgenda of both Boards

LeasesLeases

2008 Milestone2008 MilestoneProjectProject

Outcome of RoadmapOutcome of Roadmap

Not identical statements in short termNot identical statements in short termReconciliation to US GAAP removedReconciliation to US GAAP removedClose alignmentClose alignmentComparable trendsComparable trendsContinued coContinued co--operation operation same resultssame results

Plenary Session IASB@AFRAC 2007

Monday, 26 November 2007 15

PART IIPART II

TECH PLANTECH PLANPROJECTSPROJECTS

Plenary Session IASB@AFRAC 2007

Monday, 26 November 2007 16

Remaining Research Remaining Research AgendaAgenda

Extractive industriesExtractive industriesJoint venturesJoint venturesMD&AMD&AHyperinflationHyperinflationInvestment entitiesInvestment entities

Agenda Decision in December 2007Agenda Decision in December 2007

Plenary Session IASB@AFRAC 2007

Monday, 26 November 2007 17

Conceptual FrameworkConceptual FrameworkOverviewOverview

Foundation for all standardsFoundation for all standardsCurrent versionsCurrent versions nneed an overhauleed an overhaul

Refine, update, complete, convergeRefine, update, complete, convergeBeing done in phasesBeing done in phasesPlan to finalise in phasesPlan to finalise in phasesJoint project with FASBJoint project with FASB

Conceptual FrameworkConceptual FrameworkWork planWork plan

Q4 2007Q4 2007

H2 2008H2 2008TBDTBDQ4 2007Q4 2007TBDTBDTBDTBDTBDTBDTBDTBD

EDED

DPDPDPDPDPDPDPDPDPDPDPDPTBDTBD

A: Objective and qualitative A: Objective and qualitative characteristicscharacteristics

B: Elements and recognitionB: Elements and recognitionC: MeasurementC: MeasurementD: Reporting entityD: Reporting entityE: Presentation and disclosureE: Presentation and disclosureF: Purpose and statusF: Purpose and statusG: NotG: Not--forfor--profit entitiesprofit entitiesH: Remaining issuesH: Remaining issues

Timing Timing estimateestimate

Next step / Next step / current statuscurrent status

PhasesPhases

Plenary Session IASB@AFRAC 2007

Monday, 26 November 2007 18

Phase A: Objective of general Phase A: Objective of general purpose external financial reportingpurpose external financial reporting

to provide information about the reporting to provide information about the reporting entity that is useful to present & potential entity that is useful to present & potential investors, lenders and other creditors in investors, lenders and other creditors in making the decisions that they make in their making the decisions that they make in their capacity as capital providers to the reporting capacity as capital providers to the reporting entityentity

NotesNotesScopeScope——wider than financial statementswider than financial statementsAudienceAudience——capital providerscapital providersPurposePurpose——information for capital providers’ information for capital providers’ decisions (includes stewardship)decisions (includes stewardship)

Phase A Phase A Qualitative CharacteristicsQualitative Characteristics

‘‘Necessary’ QCsNecessary’ QCsRelevanceRelevanceFaithful representationFaithful representation

‘‘Enhancing’ QCsEnhancing’ QCsVerifiabilityVerifiabilityComparabilityComparabilityUnderstandabilityUnderstandabilityTimeliness Timeliness

Pervasive constraintsPervasive constraintsMaterialityMaterialityCost versus benefitsCost versus benefits

Plenary Session IASB@AFRAC 2007

Monday, 26 November 2007 19

Phase BPhase BElements and RecognitionElements and Recognition

Definition of elements:Definition of elements:AssetAssetLiabilityLiabilityLiabilities/equityLiabilities/equityIncomeIncome

ExpenseExpenseOthers (eg cash Others (eg cash flow, flow, comprehensive comprehensive income)income)

Recognition and derecognitionRecognition and derecognitionUnit of accountUnit of account

Phase CPhase CMeasurementMeasurement

Divided into 3 milestones:I. Define and describe potential

measurement basesII. Evaluate measurement bases using

criteria that includes the qualitative characteristics

III. Derive conceptual conclusions from Milestones I and II and address practical implications

Plenary Session IASB@AFRAC 2007

Monday, 26 November 2007 20

Phase CPhase C——Milestone I Milestone I Measurement Basis CandidatesMeasurement Basis Candidates

Past Past ----Entry priceEntry priceModified entry Modified entry amountamountExit priceExit price

Present Present ----Entry priceEntry priceExit priceExit priceEquilibrium priceEquilibrium priceValue in useValue in use

Future Future ----Entry priceEntry priceExit priceExit price

Phase DPhase DThe Reporting EntityThe Reporting Entity

The current frameworks do not include The current frameworks do not include a reporting entity concepta reporting entity conceptWhat is an individual reporting entity?What is an individual reporting entity?What is a group reporting entity?What is a group reporting entity?Should parentShould parent--only financial only financial statements be required?statements be required?

Plenary Session IASB@AFRAC 2007

Monday, 26 November 2007 21

ProjectsProjectsIASB/FASB IASB/FASB MoUMoU

H1 2009H1 2009EDEDFair value measurement Fair value measurement guidanceguidance

Q1 2008Q1 2008Phase B: DPPhase B: DPFinancial statement Financial statement presentationpresentation

Q1 2008Q1 2008DPDPConsolidationConsolidationCurrentCurrentH2 2008H2 2008

ED 9 ED 9 IFRSIFRS

Joint arrangementsJoint arrangements

Q1 2008Q1 2008DPDPRevenue recognitionRevenue recognitionH2 2008H2 2008DPDPLeasesLeases

Next step/Timing Next step/Timing estimateestimate

Next step / Next step / current statuscurrent status

ProjectProject

ProjectsProjectsIASB/FASB IASB/FASB MoUMoU

Q1 2008Q1 2008Phase A: DPPhase A: DPPostPost--employment employment benefitsbenefits

Q1 2008Q1 2008EDEDIncome taxesIncome taxes

Timing estimateTiming estimateNext step / Next step / current statuscurrent status

ProjectProject

Plenary Session IASB@AFRAC 2007

Monday, 26 November 2007 22

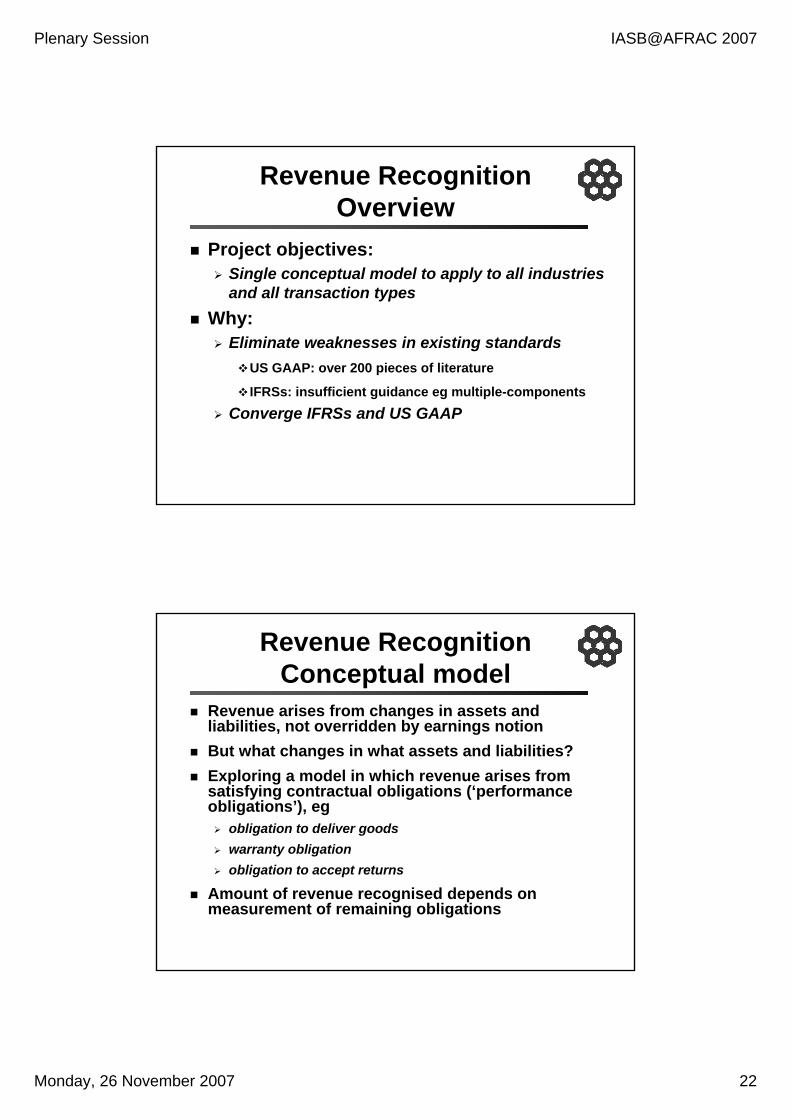

Revenue RecognitionRevenue RecognitionOverviewOverview

Project objectives:Project objectives:Single conceptual model to apply to all industries Single conceptual model to apply to all industries and all transaction types and all transaction types

Why:Why:Eliminate weaknesses in existing standardsEliminate weaknesses in existing standards

US GAAP: over 200 pieces of literatureUS GAAP: over 200 pieces of literature

IFRSs: insufficient guidance IFRSs: insufficient guidance egeg multiplemultiple--componentscomponentsConverge IFRSs and US GAAPConverge IFRSs and US GAAP

Revenue RecognitionRevenue RecognitionConceptual modelConceptual model

Revenue arises from changes in assets and Revenue arises from changes in assets and liabilities, not overridden by earnings notionliabilities, not overridden by earnings notionBut what changes in what assets and liabilities?But what changes in what assets and liabilities?Exploring a model in which revenue arises from Exploring a model in which revenue arises from satisfying contractual obligations (‘performance satisfying contractual obligations (‘performance obligations’), obligations’), egeg

obligation to deliver goodsobligation to deliver goodswarranty obligationwarranty obligationobligation to accept returnsobligation to accept returns

Amount of revenue recognised depends on Amount of revenue recognised depends on measurement of remaining obligationsmeasurement of remaining obligations

Plenary Session IASB@AFRAC 2007

Monday, 26 November 2007 23

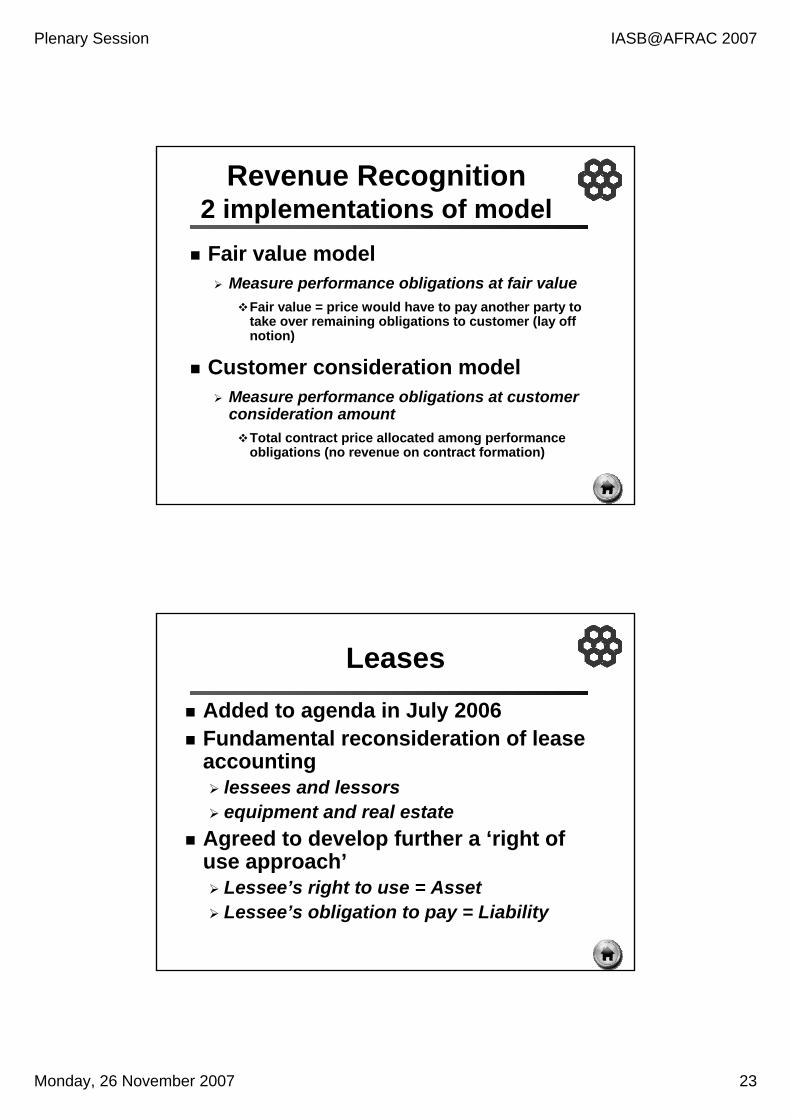

Revenue RecognitionRevenue Recognition2 implementations of model2 implementations of modelFair value modelFair value model

Measure performance obligations at fair valueMeasure performance obligations at fair valueFair value = price would have to pay another party to Fair value = price would have to pay another party to take over remaining obligations to customer (lay off take over remaining obligations to customer (lay off notion)notion)

Customer consideration modelCustomer consideration modelMeasure performance obligations at customer Measure performance obligations at customer consideration amountconsideration amount

Total contract price allocated among performance Total contract price allocated among performance obligations (no revenue on contract formation)obligations (no revenue on contract formation)

LeasesLeasesAdded to agenda in July 2006Added to agenda in July 2006Fundamental reconsideration of lease Fundamental reconsideration of lease accountingaccounting

lessees and lessorslessees and lessorsequipment and real estateequipment and real estate

Agreed to develop further a ‘right of Agreed to develop further a ‘right of use approach’use approach’

Lessee’s right to use = AssetLessee’s right to use = AssetLessee’s obligation to pay = LiabilityLessee’s obligation to pay = Liability

Plenary Session IASB@AFRAC 2007

Monday, 26 November 2007 24

Financial Statement PresentationFinancial Statement PresentationPhase A: DecisionsPhase A: Decisions

A complete set of financial statements A complete set of financial statements consists of: consists of:

Statement of financial position Statement of financial position Statement of comprehensive incomeStatement of comprehensive incomeStatement of cash flowsStatement of cash flowsStatement of changes in equityStatement of changes in equity

Permits comprehensive income to be Permits comprehensive income to be presented in either one or two statementspresented in either one or two statementsAll shown with equal prominenceAll shown with equal prominenceA minimum of two annual periods of A minimum of two annual periods of complete financial statementscomplete financial statements

Financial Statement PresentationFinancial Statement PresentationPhase B: Working PrinciplesPhase B: Working Principles

Portray cohesive financial picturePortray cohesive financial pictureConsistent categorisation between statementsConsistent categorisation between statements

Separate financing from business activitiesSeparate financing from business activitiesHelp users understand Help users understand

Measurement attributes Measurement attributes Measurement uncertaintiesMeasurement uncertaintiesCauses of changes in recognised amountsCauses of changes in recognised amounts

Plenary Session IASB@AFRAC 2007

Monday, 26 November 2007 25

Financial Statement PresentationFinancial Statement PresentationPhase B: Working PrinciplesPhase B: Working Principles

Help users assessHelp users assessAbility to generate future cash flowsAbility to generate future cash flowsAbility to meet its obligations, its ability Ability to meet its obligations, its ability to pay dividends, and its need for to pay dividends, and its need for external financingexternal financing

Help users Help users differentiate cash differentiate cash transactions and accrualstransactions and accruals

Tentative Views: Tentative Views: Working FormatWorking Format

FinancingFinancingFinancing asset cash flowsFinancing asset cash flowsFinancing liability cash flowsFinancing liability cash flows

FinancingFinancingFinancing incomeFinancing incomeFinancing expensesFinancing expenses

FinancingFinancingFinancing assetsFinancing assetsFinancing liabilitiesFinancing liabilities

EquityEquityEquityEquity

Statement of Changes in Statement of Changes in EquityEquity

Income taxesIncome taxesIncome taxesIncome taxesIncome taxesIncome taxes

Discontinued operationsDiscontinued operationsDiscontinued operationsDiscontinued operationsDiscontinued operationsDiscontinued operations

BusinessBusinessOperating cash flowsOperating cash flowsInvesting cash flowsInvesting cash flows

BusinessBusinessOperating incomeOperating incomeInvesting incomeInvesting income

BusinessBusinessOperating assets and Operating assets and

liabilitiesliabilitiesInvesting assets and Investing assets and

liabilitiesliabilities

Statement of Statement of Cash FlowsCash Flows

Statement of Statement of Comprehensive IncomeComprehensive Income

Statement of Statement of Financial PositionFinancial Position

Plenary Session IASB@AFRAC 2007

Monday, 26 November 2007 26

Financial Statement PresentationFinancial Statement PresentationPhase B: Remaining TopicsPhase B: Remaining Topics

Defining totals and subtotalsDefining totals and subtotalsDP will include alternative statements DP will include alternative statements of comprehensive incomeof comprehensive incomeRecycling?Recycling?Direct or indirect cash flow?Direct or indirect cash flow?Tax allocations or one tax line?Tax allocations or one tax line?

Project onProject onFair Value MeasurementsFair Value Measurements

Project objectivesProject objectivesClarify the fair value measurement Clarify the fair value measurement objectiveobjectiveDevelop a single source of guidance for all Develop a single source of guidance for all fair value measurementsfair value measurementsEliminate dispersed and inconsistent fair Eliminate dispersed and inconsistent fair value measurement guidance from IFRSsvalue measurement guidance from IFRSs

Plenary Session IASB@AFRAC 2007

Monday, 26 November 2007 27

Project on Project on Fair Value MeasurementsFair Value Measurements

This projectThis projectdeals only with measuring fair value when deals only with measuring fair value when fair value is required by another standardfair value is required by another standardwill will notnot result in the recognition of result in the recognition of additional items at fair valueadditional items at fair valuewill will notnot reconsider previous decisions by reconsider previous decisions by the IASB or its predecessor to require fair the IASB or its predecessor to require fair value in current IFRSsvalue in current IFRSs

Project on Project on Fair Value MeasurementsFair Value Measurements

Next stepsNext stepsAnalyse comment letters on DPAnalyse comment letters on DPRoundRound--table meetings (timing?)table meetings (timing?)ReRe--deliberate:deliberate:

Definition of fair value and related guidanceDefinition of fair value and related guidanceAssess whether each use of ‘fair value’ in IFRSs Assess whether each use of ‘fair value’ in IFRSs has the same measurement objective as the has the same measurement objective as the revised definitionrevised definitionDevelop an exposure draftDevelop an exposure draft

Convergence discussion if different viewsConvergence discussion if different viewsConsolidate/replace existing FVM guidanceConsolidate/replace existing FVM guidance

Plenary Session IASB@AFRAC 2007

Monday, 26 November 2007 28

Joint ArrangementsJoint Arrangements

ED 9 issued September 2007ED 9 issued September 2007Remove option for proportionate Remove option for proportionate consolidationconsolidationClarify definitionClarify definitionMore extensive guidanceMore extensive guidance

ConsolidationsConsolidations

Concept of control as the basis for Concept of control as the basis for consolidationconsolidationDeveloping a single approach to all Developing a single approach to all entities, including SPEsentities, including SPEsIASB and FASB working separately IASB and FASB working separately but projects must be combined laterbut projects must be combined later

Plenary Session IASB@AFRAC 2007

Monday, 26 November 2007 29

Income TaxesIncome TaxesShortShort--term term convergenceconvergenceCurrent IFRS and US GAAPCurrent IFRS and US GAAP

basically same underlying standard with different basically same underlying standard with different exceptions to fundamental principleexceptions to fundamental principle

ProposalProposal——IFRS and US GAAP same IFRS and US GAAP same fundamental principle with same exceptionsfundamental principle with same exceptions

goodwillgoodwillforeign subsidiaries and joint venturesforeign subsidiaries and joint ventures

Tax uncertaintiesTax uncertaintiesFIN 48 FIN 48 vsvs IAS 37 approachIAS 37 approach

PostPost--employment Benefitsemployment BenefitsPhase 1: by 2010Phase 1: by 2010

Definition of defined benefit and Definition of defined benefit and defined contribution arrangements and defined contribution arrangements and accounting for cash balance plans accounting for cash balance plans Smoothing and deferral mechanisms Smoothing and deferral mechanisms Treatment of settlements and Treatment of settlements and curtailments curtailments PresentationPresentationDP expected Q1 2008DP expected Q1 2008

Plenary Session IASB@AFRAC 2007

Monday, 26 November 2007 30

PostPost--employment Benefitsemployment BenefitsPhase 2Phase 2

Comprehensive review of postComprehensive review of post--employment benefitsemployment benefitsInternational convergenceInternational convergence

Major Projects Major Projects continuedcontinuedFinancial InstrumentsFinancial Instruments

Q1 2008Q1 2008IFRSIFRSPuttablePuttable instrumentsinstruments

Q1 2008Q1 2008DPDPReplacing existing Replacing existing standardsstandards

EDED

RRRR

DPDP

Next stepsNext steps

Q4 2007Q4 2007DerecognitionDerecognition

Q3 2007Q3 2007Exposures qualifying for Exposures qualifying for hedginghedging

ShortShort--term projects term projects outside outside MoUMoU

Q4 2007Q4 2007Liabilities and equityLiabilities and equity

Timing Timing estimateestimate

LongerLonger--term projects term projects in IASB/FASB in IASB/FASB MoUMoU

Plenary Session IASB@AFRAC 2007

Monday, 26 November 2007 31

Financial InstrumentsFinancial InstrumentsReplace existing standardsReplace existing standards

DP document will discuss:DP document will discuss:longlong--term objectivesterm objectivesways to achieve longways to achieve long--term objectivesterm objectives

AimAimprinciple based standardprinciple based standardfew exceptionsfew exceptions

This will reduce complexityThis will reduce complexity

Financial InstrumentsFinancial InstrumentsLiabilities and EquityLiabilities and Equity

Modified joint projectModified joint projectIASB to publish a DP including the IASB to publish a DP including the FASB’s preliminary views documentFASB’s preliminary views documentFASB 3 distinct modelsFASB 3 distinct models

OwnershipOwnership--settlementsettlementOwnershipOwnershipReassessed Expected OutcomesReassessed Expected Outcomes

Plenary Session IASB@AFRAC 2007

Monday, 26 November 2007 32

Financial InstrumentsFinancial InstrumentsDerecognitionDerecognition

Initial focusInitial focus——financial assets at fair valuefinancial assets at fair valueFI are divisible into individual rights & obligationsFI are divisible into individual rights & obligationsFA have complicated derecognition issuesFA have complicated derecognition issuesFA at FV separates derecognition from revenueFA at FV separates derecognition from revenue

We consideredWe consideredChanges to asset definitionChanges to asset definitionOther factors, such as balance sheet displayOther factors, such as balance sheet display

Currently testing whether Currently testing whether derecognitionderecognitionprinciples for financial assets can be principles for financial assets can be extended to other assets and liabilitiesextended to other assets and liabilities

Financial InstrumentsFinancial InstrumentsPuttable instrumentsPuttable instruments

Exposure draft published in 2006Exposure draft published in 200687 comment letters analysed and 87 comment letters analysed and discusseddiscussedReRe--deliberations have led to:deliberations have led to:

Final amendment to be released Q1 2008 Final amendment to be released Q1 2008 using principles of subordination and using principles of subordination and participation to identify equity instrumentsparticipation to identify equity instrumentsSeparately, research other instruments Separately, research other instruments with similar issues as raised in the with similar issues as raised in the comment letterscomment letters

Plenary Session IASB@AFRAC 2007

Monday, 26 November 2007 33

Exposures Qualifying for Exposures Qualifying for Hedge AccountingHedge Accounting

Specify the risks that qualify for Specify the risks that qualify for designation as a hedged risk (proposed designation as a hedged risk (proposed IAS39.80Z)IAS39.80Z)Provide additional guidance on what Provide additional guidance on what can be designated as a hedged portion can be designated as a hedged portion in a hedging relationship (proposed in a hedging relationship (proposed IAS39.AG99BA/BB/E)IAS39.AG99BA/BB/E)

Identification Of Identification Of ‘Other Portions’ Of Cash Flows‘Other Portions’ Of Cash Flows

Part of time period to maturityPart of time period to maturityProportion or percentageProportion or percentageOneOne--sided risksided riskContractually specified & independent Contractually specified & independent RiskRisk--free interest ratefree interest rateQuoted interbank rateQuoted interbank rate

Plenary Session IASB@AFRAC 2007

Monday, 26 November 2007 34

Active Agenda ProjectsActive Agenda ProjectsOutside IASB/FASB Outside IASB/FASB MoUMoU

variousvariousvariousvariousAmendments to Amendments to IASsIASs 24 24 & 33 and & 33 and IFRSsIFRSs 1 & 21 & 2

YTBDYTBDIFRSIFRSLiabilitiesLiabilities

CurrentCurrent20092009

DPDPEDED

Insurance contractsInsurance contracts

CurrentCurrentH2 2008H2 2008

EDEDIFRSIFRS

IFRS for IFRS for SMEsSMEs

Q4 2007Q4 2007Q2 2008Q2 2008

EDEDIFRSIFRS

Annual improvementsAnnual improvements

Timing estimateTiming estimateNext step / Next step / current statuscurrent status

ProjectProject

LiabilitiesLiabilities

Scope Scope Apply to all liabilities not within scope of Apply to all liabilities not within scope of another standardanother standard

Except executory contracts, unless onerousExcept executory contracts, unless onerous

Eliminate ‘contingent’ liabilitiesEliminate ‘contingent’ liabilitiesCurrently describes two different ideasCurrently describes two different ideas

Unrecognised present obligationUnrecognised present obligationPossible obligation (business risks)Possible obligation (business risks)

Plenary Session IASB@AFRAC 2007

Monday, 26 November 2007 35

LiabilitiesLiabilities

Present obligations Present obligations areare liabilitiesliabilitiesNonNon--recognition inconsistent with Framework and recognition inconsistent with Framework and other standardsother standards

Business risks Business risks are notare not liabilitiesliabilitiesRecognition inconsistent with FrameworkRecognition inconsistent with Framework

Recognise liabilities that can be measured Recognise liabilities that can be measured reliablyreliably

Uncertainty about outflow affects measurement Uncertainty about outflow affects measurement not recognitionnot recognitionUse expected value to measure all liabilitiesUse expected value to measure all liabilities

LiabilitiesLiabilitiesKey issues from roundKey issues from round--tablestables

Distinguish liabilities from business Distinguish liabilities from business risksrisksExistence of a present obligationExistence of a present obligationReflecting uncertainty in measurementReflecting uncertainty in measurementBuilding blocks of an expected valueBuilding blocks of an expected valueLawsuitsLawsuitsDisclosure of business risksDisclosure of business risks

Plenary Session IASB@AFRAC 2007

Monday, 26 November 2007 36

Insurance ContractsInsurance Contracts

Preliminary views documentPreliminary views documentBuilding a new universal prospective Building a new universal prospective modelmodel3 basic building blocks3 basic building blocks

Estimates of future cash flowsEstimates of future cash flowsTime value of moneyTime value of moneyA margin for riskA margin for risk

ChallengesChallenges

MarginsMarginsPolicyholder behaviour and future Policyholder behaviour and future premiumspremiumsPolicyholder participationPolicyholder participationReporting changes in insurance Reporting changes in insurance liabilities (reporting performance)liabilities (reporting performance)

Plenary Session IASB@AFRAC 2007

Monday, 26 November 2007 37

IFRS for IFRS for SMEsSMEs

IASB’sIASB’s approachapproach::Based on full IFRSs, which are developed for Based on full IFRSs, which are developed for public capital marketspublic capital marketsModifications based on user needs and costModifications based on user needs and cost--benefitbenefitEnables investors, lenders, others to compare Enables investors, lenders, others to compare SMEs’ financial performance, financial SMEs’ financial performance, financial condition, and cash flowscondition, and cash flows

WhichWhich EntitiesEntities

IASB’sIASB’s view: view: IFRS for SMEs is appropriate for the IFRS for SMEs is appropriate for the general purpose financial statements of general purpose financial statements of an entity with no public accountability:an entity with no public accountability:

not publicly traded; and not publicly traded; and not a financial institutionnot a financial institution

Jurisdiction decides which entities will useJurisdiction decides which entities will useJurisdiction could add a size testJurisdiction could add a size test

Plenary Session IASB@AFRAC 2007

Monday, 26 November 2007 38

Finding an AnswerFinding an Answer

SME must try to find answers in the IFRS for SME must try to find answers in the IFRS for SMEs:SMEs:

by analogy, and by analogy, and

by using pervasive principles in first section of IFRS by using pervasive principles in first section of IFRS for for SMEsSMEs

MayMay look to full IFRSs if answer cannot be found look to full IFRSs if answer cannot be found in IFRS for in IFRS for SMEsSMEsBut, But, no mandatory fallbackno mandatory fallback to full to full IFRSsIFRSs

Types of simplifications Types of simplifications ~ user needs & cost~ user needs & cost--benefitbenefit

1. Some topics in IFRSs not included if irrelevant to SME1. Some topics in IFRSs not included if irrelevant to SME

2. Where IFRS has options, include only simpler option2. Where IFRS has options, include only simpler option

3. Recognition and measurement simplifications3. Recognition and measurement simplifications

4. Reduced disclosures <400 (full IFRS >3,000)4. Reduced disclosures <400 (full IFRS >3,000)

5. Simplified drafting5. Simplified drafting

Plenary Session IASB@AFRAC 2007

Monday, 26 November 2007 39

Annual ImprovementsAnnual ImprovementsFor nonFor non--urgent, minor amendmentsurgent, minor amendmentsPurposePurpose——practical expedientpractical expedient

resolve inconsistencies between standardsresolve inconsistencies between standardsclarify unclear wordingclarify unclear wording

ProcessProcessAnnual EDAnnual ED90 day exposure90 day exposure12 month effective date12 month effective date

BenefitsBenefitsImproved use of IASB timeImproved use of IASB timeLess burdensome for constituentsLess burdensome for constituents

Some IssuesSome Issues

IFRSsIFRSs::IFRSsIFRSs as adopted by …as adopted by …

Possibly we would need to strengthen IAS1 Possibly we would need to strengthen IAS1 requirementsrequirements

Consistent application?Consistent application?Combined role of IFRIC, Audit Firms, RegulatorsCombined role of IFRIC, Audit Firms, Regulators

US GAAP:US GAAP:Level of detail?Level of detail?Specialized industry standards?Specialized industry standards?

Plenary Session IASB@AFRAC 2007

Monday, 26 November 2007 40

We are only one pieceWe are only one pieceof the puzzleof the puzzle

Auditing

EnforcementAccounting Standards

Corporategovernance

Preparers Users

AFTER 2007:AFTER 2007:

ConvergenceConvergenceImprovementsImprovementsSimplificationSimplification

One world standardOne world standard

Plenary Session IASB@AFRAC 2007

Monday, 26 November 2007 41

Questions?Questions?Comments?Comments?

EXPRESSIONS OF INDIVIDUAL VIEWS BY MEMBERS OF THE IASB AND ITS STAFF ARE ENCOURAGED. THE VIEWS EXPRESSED IN THIS PRESENTATION ARE THOSE OF Mr DANJOU. OFFICIAL POSITIONS OF THE IASB ON ACCOUNTING MATTERS ARE DETERMINED ONLY AFTER EXTENSIVE DUE PROCESS AND DELIBERATION.