Embed Size (px)

Citation preview

Insert Text Here

Interim results presentation

6 months ended 31 July 2017

26 September 2017

2

Forward-looking statements

This presentation contains certain forward-looking statements with respect to the financial condition, results of operations, and businesses of Card Factory plc. These statements and forecasts involve risk, uncertainty and assumptions because they relate to events and depend upon circumstances that will occur in the future. There are a number of factors that could cause actual results or developments to differ materially from those expressed or implied by these forward-looking statements. These forward-looking statements are made only as at the date of this presentation. Nothing in this presentation should be construed as a profit forecast. Except as required by law, Card Factory plc has no obligation to update the forward-looking statements or to correct any inaccuracies therein.

The financial information in this presentation does not contain sufficient detail to allow a full understanding of the results Card Factory plc. For more detailed information, please see the interim results announcement for the six months ended 31 July 2017 which can be found on www.cardfactoryinvestors.com.

3

Agenda

• Introduction Geoff Cooper (Chairman)

• Financial review Kris Lee (CFO)

• Business update Karen Hubbard (CEO)

• Questions

4

Introduction

Geoff CooperChairman

5

Financial review

Kris LeeChief Financial Officer

6

Financial highlights

H1 FY18 H1 FY17Year-on-year

change

Revenue £179.6m £169.2m +6.1%

Card Factory LFLs +3.1% +0.2%

EBITDA £32.8m £34.2m -4.0%

Margin 18.3% 20.2% -1.9ppts

Operating profit £27.7m £29.0m -4.6%

Margin 15.4% 17.1% -1.7ppts

Profit before tax £26.3m £27.6m -4.8%

Effective tax rate 19.7% 20.4% -0.7ppts

Basic EPS 6.19p 6.45p -4.0%

Interim dividend 2.9p 2.8p +3.6%

Special dividend 15.0p/£51.2m 15.0p/£51.1m

Total dividends since IPO 72.3p/£246.5m 48.1p/£163.8m

Net debt £146.0m £121.7m

Leverage 1.50x 1.26x

Note

All figures shown on an underlying basis

7

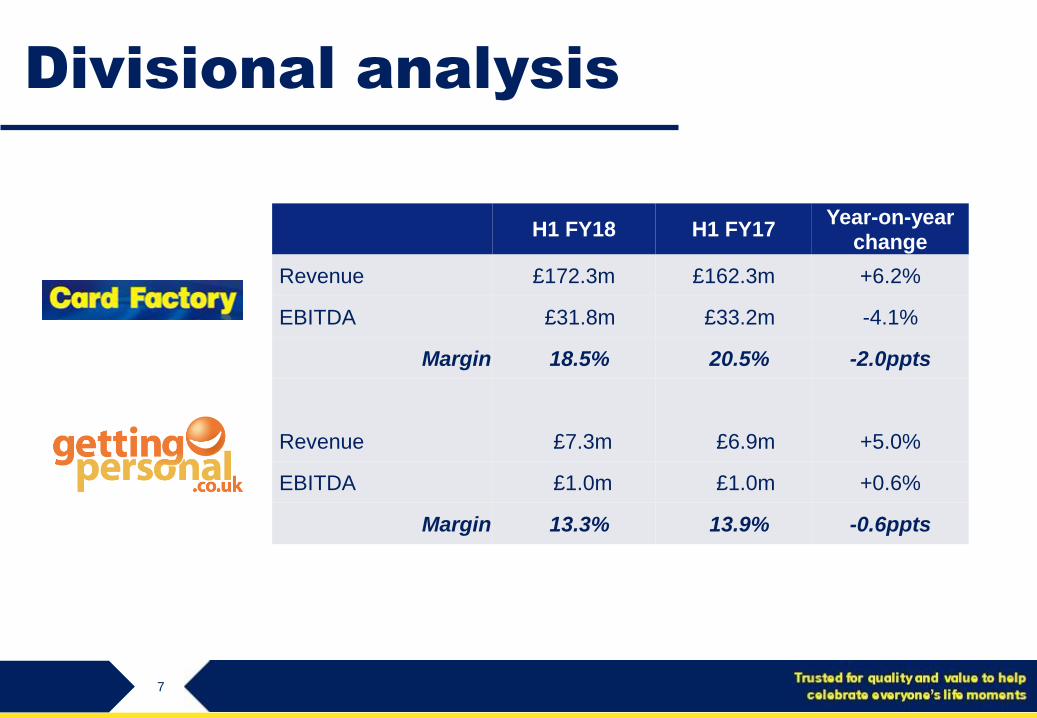

Divisional analysis

H1 FY18 H1 FY17Year-on-year

change

Revenue £172.3m £162.3m +6.2%

EBITDA £31.8m £33.2m -4.1%

Margin 18.5% 20.5% -2.0ppts

Revenue £7.3m £6.9m +5.0%

EBITDA £1.0m £1.0m +0.6%

Margin 13.3% 13.9% -0.6ppts

8

Revenue and like-for-like sales

Strong store like-for-like sales performance

FY18 H1

Highest like-for-like sales performance in 4

years

Non-card investment in ranges showing

strong performance

149.4 161.4 169.2 179.6

203.9 220.2 229.0

FY15 FY16 FY17 FY18

£’m

H2

H1

Card Factory* FY15 FY16 FY17 FY18

LFL H1 +2.6% +2.7% -0.1% +3.0%

LFL FY +1.8% +2.8% +0.4%

* relate to stores only

9

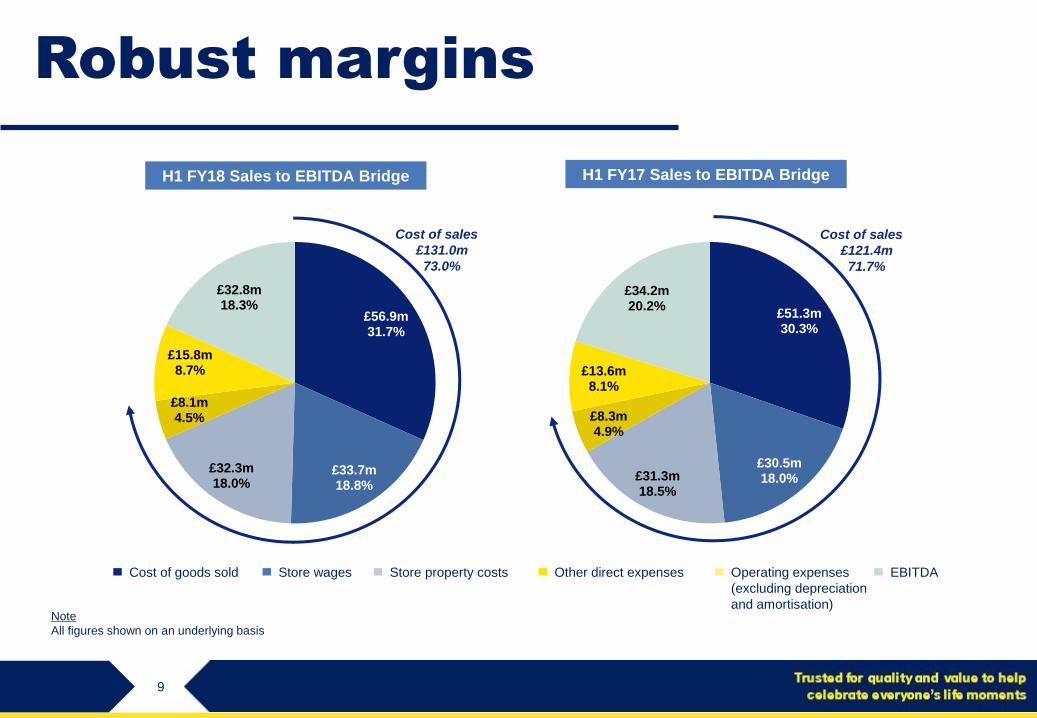

£51.3m30.3%

£30.5m18.0%£31.3m

18.5%

£8.3m4.9%

£13.6m8.1%

£34.2m20.2%

Robust margins

H1 FY17 Sales to EBITDA Bridge

£56.9m31.7%

£33.7m18.8%

£32.3m18.0%

£8.1m4.5%

£15.8m8.7%

£32.8m18.3%

H1 FY18 Sales to EBITDA Bridge

Cost of sales

£131.0m

73.0%

Cost of sales

£121.4m

71.7%

Note

All figures shown on an underlying basis

Cost of goods sold Store property costsStore wages Other direct expenses EBITDAOperating expenses

(excluding depreciation

and amortisation)

10

Margin headwinds & mitigation

H1 2018

• Gross impact to EBITDA margin of c230bps attributable to FX and NLW headwinds

• Business efficiencies mitigation, offset by product mix and a small element of investment, giving net impact of c190bps

FY 2018

• Gross impact to EBITDA margin of c320bps attributable to FX and NLW headwinds

• Expected business efficiencies mitigation, offset by product mix and a small element of investment, giving an expected net margin impact for the year of c200bps

• Previously advised gross impact to EBITDA margin of c300bps, c150bps post mitigation

FY 2019

• Continued pressure from FX and NLW, with focus on business efficiencies and mitigation

11

Highly cash generative

H1 FY18

£’m

H1 FY17

£’m

Cash inflow from operating activities 27.6 * 37.9

Corporation tax (8.8) (8.8)

Net cash inflow from operating activities 18.8 29.1

Cash outflow from investing activities

Capital expenditure (see over) (6.6) (5.6)

Net cash outflow from investing activities (6.6) (5.6)

Net cash inflow before financing activities 12.2 23.5

Cash generation impacted by working capital

* reduction in operating cash flow versus H1 FY17 principally reflects £5.2m FX impact and an increase in stock, in part due to the impact of foreign exchange on unit costs, and in part due to planned build-up of stocks on popular lines

12

Capex

Low, predictable and well controlled

• Total capex includes:

• Recurring annual capex

• Refurbishments and roll-out

• c£8-9m pa

• One-off strategic projects

• EPOS

• Investment of £4.8m this year

• Improved stock control

• Better analysis of performing lines

• Medium term view

• Annual capex of c£12m in medium term

with some additional investment in EPOS in

the short term

H1 FY18

£’m

H1 FY17

£’m

One-off strategic projects

Digital print - 1.0

LED conversions 0.6 0.4

EPOS 2.1 0.8

Online packaging 0.2 -

Sub-total 2.9 2.2

Recurring capex

New stores 2.2 2.3

Existing stores 0.1 0.3

Relocations 0.2 0.2

Other capex 1.2 0.6

Sub-total 3.7 3.4

Total capex 6.6 5.6

13

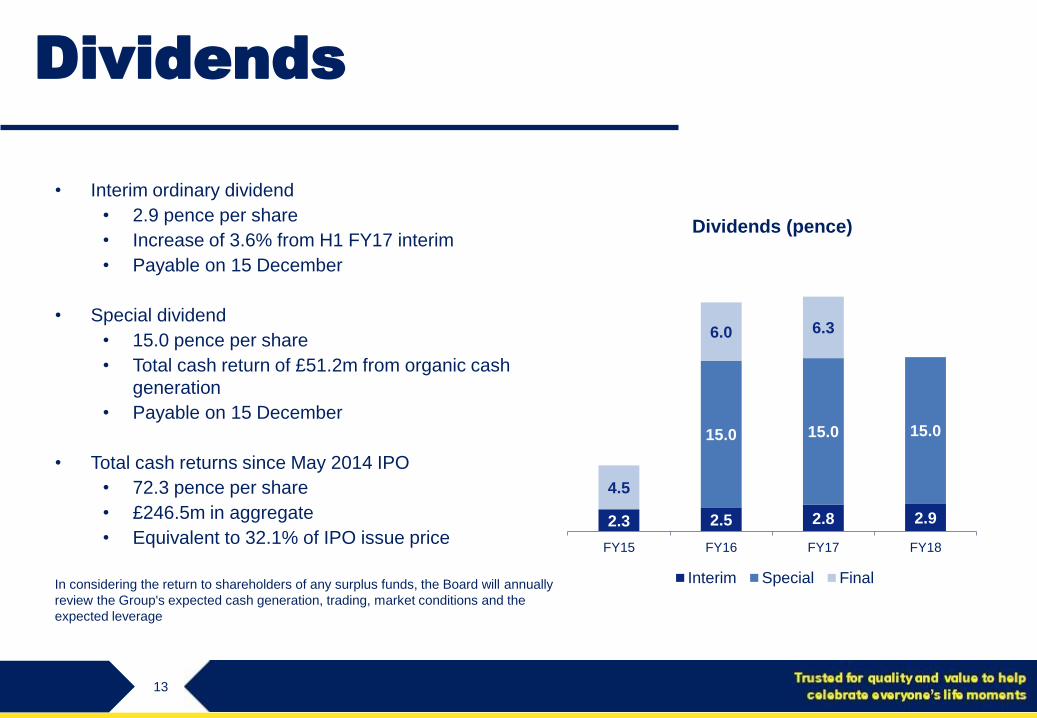

Dividends

• Interim ordinary dividend

• 2.9 pence per share

• Increase of 3.6% from H1 FY17 interim

• Payable on 15 December

• Special dividend

• 15.0 pence per share

• Total cash return of £51.2m from organic cash

generation

• Payable on 15 December

• Total cash returns since May 2014 IPO

• 72.3 pence per share

• £246.5m in aggregate

• Equivalent to 32.1% of IPO issue price

In considering the return to shareholders of any surplus funds, the Board will annually

review the Group's expected cash generation, trading, market conditions and the

expected leverage

2.3 2.5 2.8 2.9

15.0 15.0 15.0

4.5

6.0 6.3

FY15 FY16 FY17 FY18

Dividends (pence)

Interim Special Final

14

Financial performance

Summary

Strong profit margins- Margin headwinds, mainly living

wage, FX and maintaining price points

- Cost control culture

- Business efficiencies

Strong revenue growth- Good average spend increases

- Outperforming footfall trends

- New store roll out

- Online development

Surplus cash returns- Leverage of 1.50x LTM EBITDA

- Special dividend of 15p (£51.2m)

- £246.5m returned since IPO

- Timing and amount of future

returns to be reviewed

Highly cash generative- Strong underlying operating cashflow

- Low, predictable and well controlled

capex

15

Insert Text Here

Business update

Karen Hubbard

Chief Executive Officer

16

H1 FY18 four pillar performance

Like-for-like

sales growth

Store LFL: 3.0%

cardfactory.co.uk: 29.8%

New stores

30 net new UK store

openings

895 UK stores

1 ROI trial store

Business

efficiencies

EBITDA margin: 18.3%

Further mitigation in H2

Online

development

Sales growth:

Getting Personal: 5.0 %

cardfactory.co.uk: 29.8%

17

Like-for-like sales growth

OpportunitiesInitiative

Card

Non-

card

Customer

offer

• Improved quality / range

• New & modern designs

• Increase in non-card sales

• New ranges on trend

• Redesigns in key categories

• Improved availability

• Space to growing

categories

• Customer service &

standards

• Significant redesigns and new formats

• Continue to develop wider card ranges that

appeal to our customers

• Strong sales in non-card ranges

• Build on the success of non-card ranges, with

ongoing redesigns and on trend ranges

• Store availability and space optimisation a key

focus on the back of EPOS data

• Improved customer services through better

layouts and new EPOS system

18

New store roll out

OpportunitiesInitiative

• 50 net new stores

• Opportunity with retail

parks

• Assess viability of

Card Factory to

trade in ROI

• Profitable and cost

effectiveRetail

Estate

Republic

of Ireland

New

Stores

• Continue to open 50 net new stores with

appropriate stores for that customer base

• Continue to assess ROI performance and

identify opportunity to open new space

• Continue to drive cost effective property,

whilst at the same time improving the

customer proposition

19

Card Factory continues to work in

multiple locations

Price sensitive

shopping precinct

Catford

Mid-tier demographic

retail park

Longbridge

Affluent market

town high street

Wokingham

20

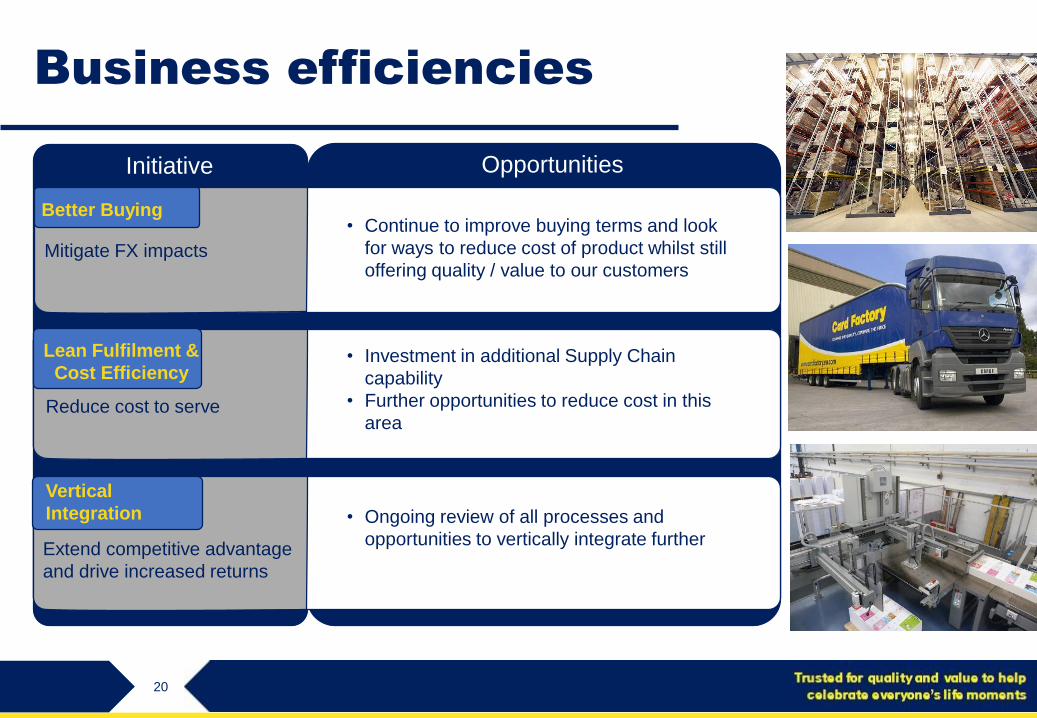

Business efficiencies

Opportunities Initiative

Mitigate FX impacts

Extend competitive advantage

and drive increased returns

Vertical

Integration

Reduce cost to serve

Lean Fulfilment &

Cost Efficiency

Better Buying• Continue to improve buying terms and look

for ways to reduce cost of product whilst still

offering quality / value to our customers

• Investment in additional Supply Chain

capability

• Further opportunities to reduce cost in this

area

• Ongoing review of all processes and

opportunities to vertically integrate further

21

Online development

Reminder: Two distinct brands & propositions

• Card Factory - a multi-channel business

• Quality & value

• Card Factory ranges personalised online

• Bulk purchases and a selected range

from store

• Unique and personalised gifts online

• Focus on the “personal” and fun

• Product innovation

• Gifts the primary purchase, cards

secondary

22

cardfactory.co.uk

Progress StatusInitiative OpportunitiesInitiative

Customer Experience

Product

Acquire Customers• Further innovative and cost effective ways to

drive awareness of the Card Factory online

proposition

• Development of ranges in line with quality /

value with a focus on seasonal & occasion

based ranges

• Significant development of platform and

customer experience

23

Getting Personal

StatusOpportunitiesInitiative

Customer Experience

Product

Acquire Customers

• Further development of customer acquisition

required across all channels

• Continue to innovate with personal &

personalised ranges which are differentiated

and meet the needs of the Getting Personal

customer

• Ongoing focus required on improved

customer experience

24

Enabling projects

OpportunitiesInitiative

Reduce retail vacancies &

turnover of managers

Improve simplicity in stores,

reduce cost to serve

Productivity

EPOS &

Contactless

EPOS and contactless in

all stores by Christmas

• Roll out across all of the estate to reduce

turnover and offer staff development

• Productivity programme commenced to

remove task from store and reduce cost to

serve

• Convert existing EPOS stores across to the

new platform

25

Building team to drive growth

Jo Bennett

Studio Director

Ian Dyson

Chief Technology Officer

Steve Lilley

Retail Stores Director

Craig Miles

Supply Chain Development Director

26

Forward View

• Strong sales performance

• Ongoing cost headwinds

• A retailer fit for the future

• The right team in place

• Encouraging start to H2

27

Trusted for quality and value to help

celebrate everyone’s life moments

28

Insert Text Here

Questions