Embed Size (px)

Citation preview

Interim ReportPeriod: 01-01-2007 to 30-09-2007

TABLE OF CONTENTS

At a glance – Group key figures 3

Letter by the Management Board 4

Group Management Report 6

Increasing volume of world trade is driving the growth market forfaiting 6

Development of the forfaiting volume 7

Expansion of the network ensures sustained earnings development 8

Net assets, financial position and result of operations 9

Performance of the DF Deutsche Forfait share 11

The risks of future development 11

Outlook 12

Consolidated Balance Sheet – Assets 14

Consolidated Balance Sheet – Equity and Liabilities 15

Consolidated Income Statement – Q3 comparison 16

Consolidated Income Statement – period comparison 17

Consolidated Cash flow Statement 18

Development of consolidated equity 19

Corporate Notes 20

DF Deutsche Fortfait AG

Kattenbug 18 – 24

50667 Köln

Phone +49 (0) 221 97376–0

Fax +49 (0) 221 97376–76

E-Mail [email protected]

Internet www.dfag.de

3 Interim Statement DF Deutsche Forfait AG

Period: 01-01-2007 to 30-09-2007

AT A GLANCE

Group key figures

2007 2006 Change

in EUR million (unless otherwise noted) Q1 Q2 Q3 Jan. - Sept. Jan. - Sept. Jan. - Sept.

Forfaiting volume 229.66 230.30 273.26 733.22 772.12 -5%

Gross result including financial results 2.88 3.63 4.98 11.50 8.19 40%

Forfaiting margin including financial results 1.3% 1.6% 1.8% 1.6% 1.1% 48%

Administrative costs 1.21 1.84 2.52 5.58 3.53 58%

Earnings before income taxes 1.70 1.84 2.44 5.98 4.75 26%

Consolidated profit 1.02 1.16 1.56 3.75 2.85 32%

Earnings per share in EUR 0.20 0.21 0.23 0.64 0.57 12%

Jan. - Sept. 2006 Jan. - Sept. 2007 Jan. - Sept. 2006 Jan. - Sept. 2007 Jan. - Sept. 2006 Jan. - Sept. 2007

12

10

8

6

4

2

00

100

Gross result inc. financial results (in EUR million)

Forfaiting volume (in EUR million)

Consolidated profit(in EUR million)

200

300

400

500

600

700

800 772.12733.22

8.19 2.85

3.7511.50

0.5

2.5

2.0

3.0

3.5

4.0

1.5

1.0

0

Dear Shareholders,

The positive effects of the IPO of DF Deutsche Forfait AG, completed in May 2007, showed initial results in

the third quarter of the current financial year. As a result of the increase in the company’s equity capital and

the related increase in credit lines, the reporting period saw a notable increase in the gross result including

financial results, which is decisive for the economic performance of the Group. At EUR 4.98 million, the gross

result including financial results was well above the comparative figures for the previous quarters. Consolidated

profits rose from EUR 1.02 million in the first quarter and EUR 1.16 million in the second quarter to EUR 1.56

million in the reporting period. This development confirmed our expectations of being able to make use of

the additional resources to increase profits in the current financial year.

The international network is being further expanded to ensure a lasting increase in earning power. As already

announced, the DF Group will shortly be opening an office in Pakistan. From the company’s point of view, the

market in Pakistan offers interesting business potential in the field of forfaiting despite the current political

crisis. A slightly positive contribution margin is expected as early as the coming year.

On 26 November, the DF Group announced the takeover of the forfaiting activities of Aon Forfaiting Limited.

Through the related establishment of an office in London, DF Deutsche Forfait has taken a decisive step

towards further expansion of its business and of its market position. The takeover did not involve any

financial consideration on the part of the DF Group. The company has succeeded in engaging the services of

two very experienced forfaiting brokers for the London office; these are from Aon Forfaiting Limited and have

4 Interim Statement DF Deutsche Forfait AG

Period: 01-01-2007 to 30-09-2007

LETTER BY THE MANAGEMENT BOARD

Ulrich Wippermann

MarinaAttawar

JochenFranke

long-established contacts in particular to British corporate clients. This will give the DF Group outstanding

access to the British corporate market, which offers major potential for the forfaiting business, given the high

number of export-oriented companies.

In addition, the cooperation also agreed with Aon, the world’s largest insurance broker, means that the DF

Group can make use of Aon’s global sales network for the acquisition of business, and has its own office in

London, the leading location for the international forfaiting market. Against this background, the

Management assumes that the London office will generate a forfaiting volume of at least EUR 100 million as

early as from the coming financial year 2008, thus laying the basis for sustained increases in earnings in

subsequent years.

Sincerely,

Your Management Board

5 Interim Statement DF Deutsche Forfait AG

Period: 01-01-2007 to 30-09-2007

LETTER BY THE MANAGEMENT BOARD

Ulrich WippermannMarina Attawar Jochen Franke

The increase in the equity capital base by EUR 13.50

million, less costs, to EUR 21,57 million, resulting

from the IPO in May of this year, creates the basis

for continued growth of the DF Group. As expected,

the increased room for manoeuvre had a positive

effect on the development of income, in particular

in the forfaiting business, already in the third

quarter.

The gross result including financial results rose

continuously during the course of the year from EUR

2.88 million in the first three months to EUR 3.63

million in the second quarter and reached a level of

EUR 4.98 million in the period from July to

September 2007. Parallel to this, consolidated

profits also increased noticeably in the third quarter;

at EUR 1.56 million in the reporting period, they

were around 53% higher than results for the first

quarter and 34% above profits in the second

quarter.

Overall, the DF Group achieved a gross result

including financial results of EUR 11.50 million in the

first nine months of 2007, a considerable increase

compared with the same period of the previous year

(EUR 8.19 million). The 40% increase was the result

of an improvement in the forfaiting margin includ-

ing financial result to 1.6% following 1.1% in the

first nine months of 2006 against a slight reduction

in the forfaiting volume of 5% to EUR 733.22 million.

Consolidated profits for the first nine months also

grew strongly by 32% to EUR 3.75 million (previous

year: EUR 2.85 million).

Increasing volume of world trade is

driving the growth market forfaiting

In international trade, exporters frequently offer to

supply their customers with a period for payment

meaning that the delivery remains a receivable in

the exporters’ balance sheet. Within the scope of

forfaiting, these receivables are purchased on a non-

recourse basis. For the exporter, this instrument of

forfaiting offers the advantage of increased liquidity,

an improved balance sheet structure as well as a

reduction in the risks associated with the receivable.

On the other hand, this investment form is very

interesting for many investors because the receiv-

ables are a real economic asset with a relatively high

margin compared with the risk. Times of advancing

globalisation and continuous growth in world trade

are accompanied by an increase in the importance

of forfaiting.

As a forfaiting company, the DF Group is involved in

world-wide financing of trade with emerging

markets and developing countries. In addition to its

forfaiting business, the company also offers its

clients the possibility of assuming risks through

purchase commitments. With purchase commit-

ments – in contrast to forfaiting – exclusively the

country and counterparty risk is assumed. The

onward sale or outplacement of the receivables is a

central component of the DF Group’s business

model. Purchase commitments issued are hedged

and outplaced by way of bank guarantees, mutual

6 Interim Statement DF Deutsche Forfait AG

Period: 01-01-2007 to 30-09-2007

GROUP MANAGEMENT REPORT

liability agreements with third parties or credit insur-

ance benefiting the DF Group. Receivables that can-

not be sold are added to the DF Group’s portfolio.

The margins from forfaiting transactions are based

on the one hand on the underlying country and coun-

terparty risks, on the other hand on the complexity

of a transaction or of its documentation require-

ments. The most important income constituent is the

discount retained when purchasing the receivables.

In addition, the DF Group generates income from

commitment fees as well as from other commission.

The discount is calculated from money and capital

market interest rates with matched maturities (e.g.

one-year LIBOR) and a risk margin which is directly

dependent on the risk of the individual transaction.

When selling the receivables, expenses correspond-

ing to the forms of income are incurred.

Given the varying structure of the individual forfait-

ing transactions and the different estimates of market

players regarding the risks associated with a receiv-

able, there is no uniform market price but rather a

market price range. The DF Group takes advantage

of this situation when executing its transactions to

maximise income.

Development of the forfaiting volume

In the reporting period there was an increased focus

on structured, high-margin business which ensured

a noticeable increase in the gross result including

financial results. In contrast, the first nine months of

the previous year mainly involved standard transac-

tions with a comparatively simple structure. This re-

sulted in a high forfaiting volume with lower margins

compared to the current year. The gross result includ-

ing financial results increased by 40% compared with

the first nine months of 2006 whilst the forfaiting

volume fell slightly by 5% to EUR 733.22 million.

The additional resources from the IPO as well as the

ongoing high demand for forfaiting solutions have

led to a considerable expansion of the forfaiting

volume in the third quarter of 2007 compared with

the first two quarters of this year. Measured against

the nominal value of the receivables underlying the

transactions, the volume rose from EUR 229.66

million in the first quarter and EUR 230.30 million in

the second quarter to EUR 273.26 million in the

period from July to September 2007. The forfaiting

volume for the current year is spread over the

following countries:

7 Interim Statement DF Deutsche Forfait AG

Period: 01-01-2007 to 30-09-2007

GROUP MANAGEMENT REPORT

Breakdown of the forfaiting volume by region

in the period 01-01 to 30-09-2007

5%

15%

21%16%

23%

11%UAE

Brazil

Serbia-Montenegro

Other

Mexico

Iran

UK

9%

EUR 733.3 millionforfaiting volume

As to the breakdown of the forfaiting volume, the

trends of the first six months of 2007 are con-

tinuing. As expected, Mexico accounted for the

highest share at 23%; over the whole of 2006,

Mexico was the second most important debtor

country behind Iran. As was already recognisable in

the first half of 2007, Iran’s share fell to 21%. New,

significant debtor countries are the United Arab

Emirates (UAE) with a share of 11% and Serbia-

Montenegro with 5%. The volume of transactions

with Great Britain and Brazil, which had already

made significant contributions in the previous year,

increased to 16% and 9% respectively over the

course of 2007.

The risk assessment of countries and debtors

changes regularly over the course of time resulting

in an adjustment of margins. The DF Group has

established an optimisation process which continu-

ously adjusts the forfaiting volume to the current

market situation. This leads to a constant variation

in the breakdown of the forfaiting volume by coun-

try and ensures the business success of the DF Group.

DF Deutsche Forfait has specialised in transactions

with risks above all from the so-called emerging

markets and from developing countries. The current

crisis in the financial markets has resulted in an

increase in the level of margins and a corresponding

rise in the number of countries in the line of focus

of the DF Group. On the one hand, high risks offer

high margins; nevertheless, they also impair the

ability to place a receivable. This is where the

extensive experience of the DF Team in the

structuring of the receivables acquired comes into

play with the aim of optimising the risk for onward

sale.

Expansion of the network ensures

sustained earnings development

With its subsidiaries in Miami and Prague, represen-

tative offices in Helsinki and Paris as well as cooper-

ation partners in Dubai, Cairo and London, the DF

Group already has a strong presence in important

target markets with direct access to clients. The DF

Group uses this international network to generate

its business directly in local markets.

The expansion of the international network is of

central importance for the strategic development of

the DF Group. Two new offices will shortly be

opened in London and Pakistan, and a cooperation

agreement for the forfaiting business has been

reached with Aon, the world’s largest insurance

broker. Above all the new office in London and the

cooperation with Aon are two very significant steps

in expanding the market position of the DF Group.

The planned office in Pakistan, to be opened by the

DF Group together with a partner, is currently in the

process of being set up. The director spent several

months at DF Group’s head office in Cologne as part

of his job familiarisation and will start business in

Lahore by the turn of the year. Despite the current

political unrest, the DF Group sees very promising

8 Interim Statement DF Deutsche Forfait AG

Period: 01-01-2007 to 30-09-2007

GROUP MANAGEMENT REPORT

business potential in Pakistan and is expecting a

slightly positive contribution margin as early as in

2008.

A further office will be opened in London on 30

November 2007. This will give the company impor-

tant access to the British corporate market which is

very attractive for forfaiting business due to the

numerous export-oriented companies. The strength-

ening of the presence in London is the result of the

takeover of the forfaiting business of the previous

competitor Aon Forfaiting Limited. The transaction

did not involve a purchasing price. The office will be

headed by two very experienced forfaiting brokers

who have thus far worked for Aon Forfaiting

Limited and who have excellent contacts to

potential clients in the British market.

In addition, an intensive cooperation has been

agreed on with the parent company, Aon Trade

Credit, concerning the generation and financing of

forfaiting transactions, as a result of which the DF

Group will gain additional access to clients via Aon’s

global sales network.

The presence in London, the world’s leading

location in the international forfaiting market, will

create an excellent basis for future growth of the

company. The Management assumes that the

London office will generate a forfaiting volume of at

least EUR 100 million in the coming year and that

the volume will increase considerably in the ensuing

years.

Net assets, financial position and

result of operations

The DF Group is an earnings-driven company and

strives to maximise net profit and thereby its return

on equity. Profits from the forfaiting business come

from the gross result and financial results. Interest

income and interest expense of the DF group relate

directly to the forfaiting business. Interest expenses

are incurred during the receivables’ refinancing

period, between the payout for the purchase and

the incoming payment for the sale or repayment of

the respective receivable. The corresponding income

figure is the discount income when acquiring the

receivable, which is included in the gross result.

Compared to the first nine months of the previous

year, a much higher proportion of income was gen-

erated by structured, high-margin transactions. The

gross result including financial results increased by

40% to EUR 11.50 million. This improvement was

primarily due to a significant increase in the forfait-

ing margin including financial results – from 1.1% to

1.6% – while the total forfaiting volume decreased

slightly by 5%. The increase in the gross result includ-

ing financial results during the third quarter – 73%

compared to the first and 37% compared to the

second quarter – was mainly due to the availability

of additional resources from the DF Group’s IPO.

Credit insurance is frequently used to structure

business transactions. Receivables are hedged by

9 Interim Statement DF Deutsche Forfait AG

Period: 01-01-2007 to 30-09-2007

GROUP MANAGEMENT REPORT

credit insurance – usually with a deductible – which

substantially reduces the risk of the component

covered by credit insurance. Due to the risk improve-

ment, discount expense is reduced when selling the

receivable and discount results improve correspon-

dingly. Discount results (discount earnings less

discount expenses) have improved by EUR 2.54

million to EUR 14.05 million compared to the

previous year, contributing considerably to the

increase in profits. At the same time, credit

insurance premiums rose by EUR 1.62 million to EUR

3.03 million.

The positive development of the gross result

including financial results with an increase of EUR

3.31 million more than compensated for the rise in

administrative costs by EUR 2.05 million compared

to the previous year. The total administrative costs

for the first nine months of 2007 were EUR 5.58

million, of which EUR 0.60 million were bonuses,

which are variable expenses. This increase was

mainly due to additional costs related to the

company’s IPO. Consolidated net profit increased by

32% to EUR 3.75 million compared to the previous

year. Thus, the DF Group has achieved 78% of the

budgeted profit of EUR 4.80 million for the 2007

fiscal year.

Due to a change in the mix of the forfaiting volume

with a considerably higher proportion of structured

transactions, the average refinancing period has

been extended which has led to an increase in total

assets. The outplacement of business transactions

remains at the previous year’s level from a risk point

of view. As at the reporting date of 30 September,

accounts receivables increased by EUR 102.03

million to EUR 134.88 million compared to 31

December 2006. Irrevocable confirmation for the

purchase of receivables in the amount of EUR 56.00

million had been received from a buyer by the end

of the quarter, which means the risk was transferred

to the buyer. Furthermore, the DF Group also held

guarantees for receivables in the amount of EUR

62.27 million, which mainly consisted of EUR 40.87

million in credit insurance and EUR 18.15 million in

cash deposits. The increase in accounts receivables

as well as liquid funds by EUR 14.10 million to

EUR 22.31 million contributed to the increase in

total assets by EUR 116.31 million compared to the

end of the year, to a total of EUR 159.18 million.

On the equity and liabilities side, liabilities increased

by EUR 103.96 million to EUR 135.77 million, and

equity rose by EUR 12.14 million to EUR 23.07

million. As experienced in the past, accounts receiv-

ables and therefore total assets will decrease consid-

erably by the end of the year, due to the seasonal

nature of the business.

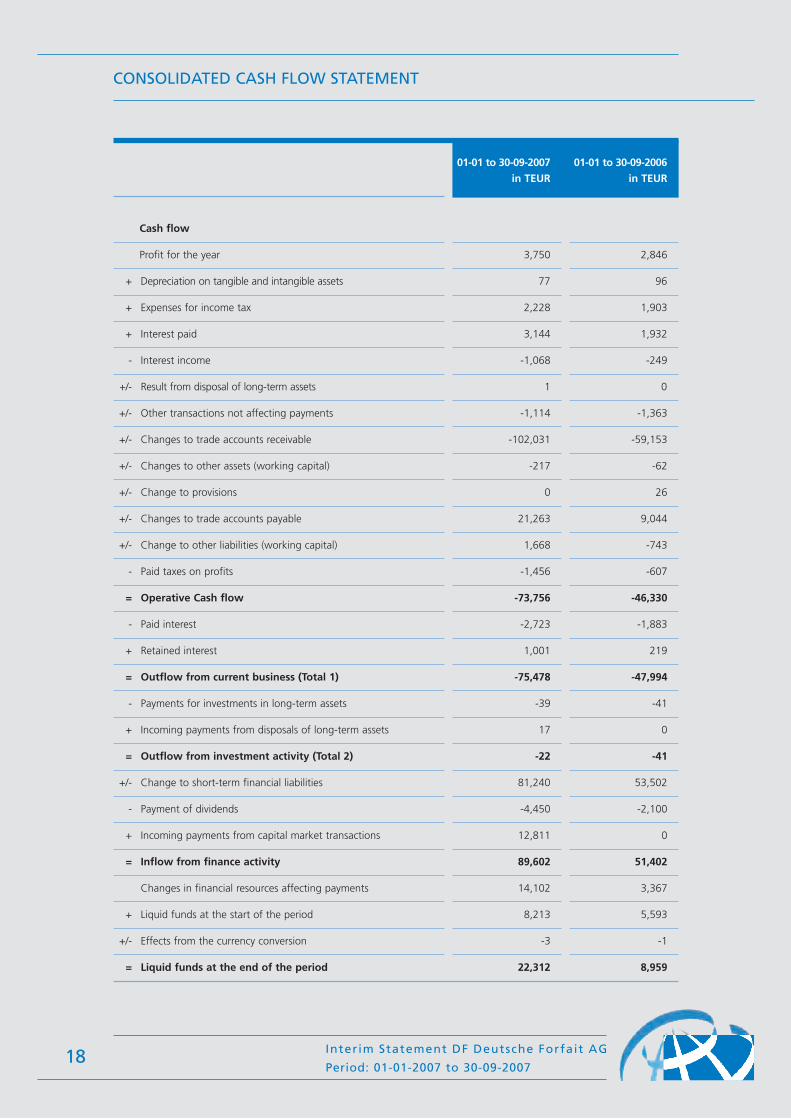

The increase in accounts receivables also impacted

the cash flow from operations during the reporting

period, which was clearly negative at EUR -73.76

million. This was mainly compensated by cash from

financing activities in the amount of EUR 89.60

million. Cash flow will improve again significantly by

the end of 2007 as a result of the disposal of receiv-

ables. Nothing currently stands in the way of the

planned dividend payment for the fiscal year 2007.

10 Interim Statement DF Deutsche Forfait AG

Period: 01-01-2007 to 30-09-2007

GROUP MANAGEMENT REPORT

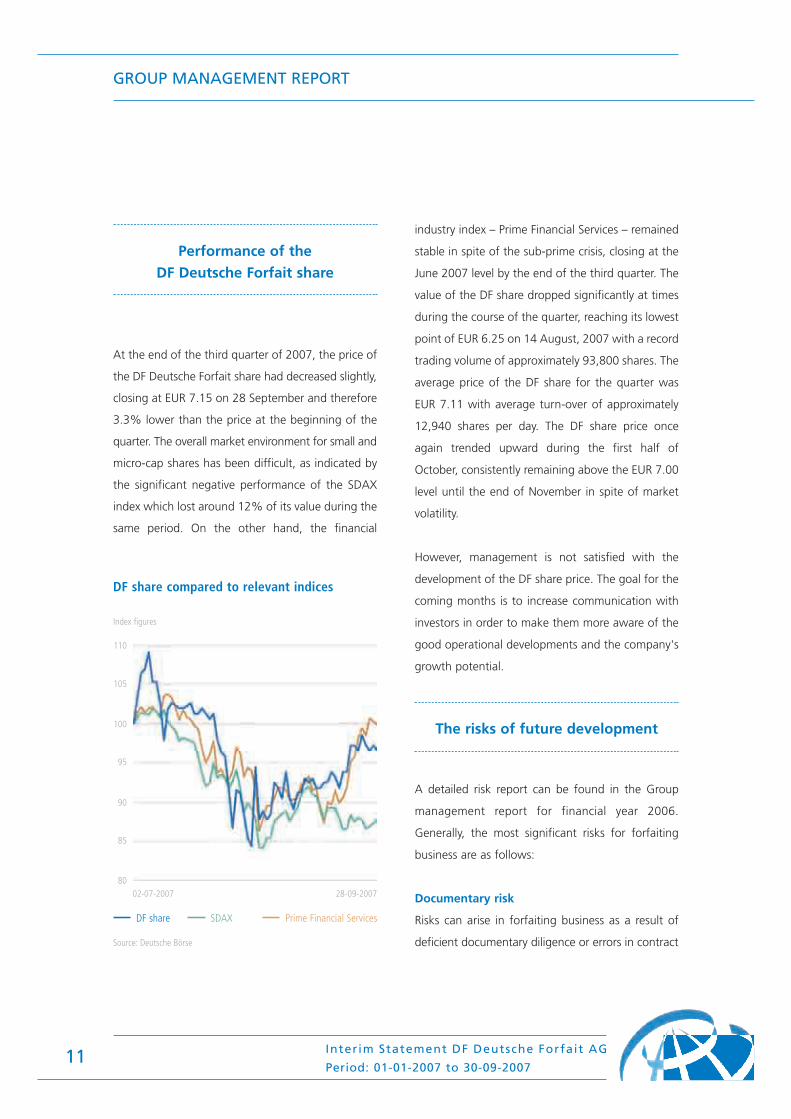

Performance of the

DF Deutsche Forfait share

At the end of the third quarter of 2007, the price of

the DF Deutsche Forfait share had decreased slightly,

closing at EUR 7.15 on 28 September and therefore

3.3% lower than the price at the beginning of the

quarter. The overall market environment for small and

micro-cap shares has been difficult, as indicated by

the significant negative performance of the SDAX

index which lost around 12% of its value during the

same period. On the other hand, the financial

industry index – Prime Financial Services – remained

stable in spite of the sub-prime crisis, closing at the

June 2007 level by the end of the third quarter. The

value of the DF share dropped significantly at times

during the course of the quarter, reaching its lowest

point of EUR 6.25 on 14 August, 2007 with a record

trading volume of approximately 93,800 shares. The

average price of the DF share for the quarter was

EUR 7.11 with average turn-over of approximately

12,940 shares per day. The DF share price once

again trended upward during the first half of

October, consistently remaining above the EUR 7.00

level until the end of November in spite of market

volatility.

However, management is not satisfied with the

development of the DF share price. The goal for the

coming months is to increase communication with

investors in order to make them more aware of the

good operational developments and the company's

growth potential.

The risks of future development

A detailed risk report can be found in the Group

management report for financial year 2006.

Generally, the most significant risks for forfaiting

business are as follows:

Documentary risk

Risks can arise in forfaiting business as a result of

deficient documentary diligence or errors in contract

11 Interim Statement DF Deutsche Forfait AG

Period: 01-01-2007 to 30-09-2007

GROUP MANAGEMENT REPORT

100

110

105

Index figures

95

90

85

80

Source: Deutsche Börse

02-07-2007 28-09-2007

DF share SDAX Prime Financial Services

DF share compared to relevant indices

preparation, particularly as the seller is generally

responsible for the legal validity of receivables when

reselling them (moral hazard). This risk is countered

by a well trained and well-manned contract settle-

ment team.

Country and counterparty risk

In a national crisis, debtors can be prevented from

paying their due receivables. Cash cannot be trans-

ferred on account of political restrictions (transfer

risk) or cannot be converted into a different curren-

cy (convertibility risk). Counterparty risk refers to the

risk that a debtor could default on a receivable on

account of, for example, insolvency; the provider of

collateral (e.g. a bank or credit insurance) can also

default. The undertaking of country and counter-

party risks is regulated in detail by a limit system. As

a trading house, the DF Group reduces this risk by

selling the receivables quickly. When a transaction is

sold, the risks are transferred to the buyer. Sufficient

risk provisions have been made for the country and

counterparty risks.

In terms of income, the biggest risks lie in a global

economic crisis which would cause a decline in the

international exchange of goods, particularly within

the emerging markets. Export to emerging markets

is at a high level this year and there are no indica-

tions of a notable decline. Another material risk is a

global crisis in the finance markets that would

extend to the forfaiting market, which belongs to

the trade finance market segment. The current

financial crisis has so far led to an increase in mar-

gins. This rise in margins is positive for the DF Group

as it results in a higher number of transactions with

the minimum margin required for the business model

of the company. Negative consequences would only

arise in case of a global liquidity crisis in the banking

sector leading to a reduction of the demand for trade

receivables. Currently this demand is at continuing

high levels partly due to the direct reference to the

flow of goods from exporters to importers.

Outlook

The forfaiting market continues to remain stable.

The IMF (International Monetary Fund) is predicting

that the growth rate for world trade will increase

from 7.1% in 2007 to 7.4% in 2008. According to

estimates by the WTO (World Trade Organisation),

emerging markets in particular are benefiting from

globalisation. Due to the sub-prime crisis, margins

on the forfaiting market have increased significantly

over the course of the last few months. As a result,

more and more transactions have the minimum

margin required for the DF Group business model.

On the sales side, both the forfaiting market and

the credit insurance market remain strong. Bank

refinancing costs have increased as a result of the

financial crisis. The cost of bank placements has

increased accordingly, but this effect was more than

compensated by the general increase in margins on

the forfaiting market.

The IPO created the foundation for future growth of

the DF Group. Extending the refinancing capacities

12 Interim Statement DF Deutsche Forfait AG

Period: 01-01-2007 to 30-09-2007

GROUP MANAGEMENT REPORT

and increasing some internal limits has considerably

expanded the range of options open to the DF

Group. The management board expects another

increase in the lines of credit over the course of the

coming months. Based on generally positive market

indicators, the management board is very confident

that the consolidated net profit of EUR 4.8 million

budgeted for the 2007 fiscal year can be achieved,

even if market conditions deteriorate, and that share-

holders will receive an attractive dividend for the

fiscal year.

The DF Group is in a good position to take advan-

tage of growth opportunities in the market in order

to expand its business. The management board

believes that the new office in London and the

cooperation agreement with Aon will make a

significant contribution towards the implementation

of the growth strategy fuelled by the IPO. The

London office will commence operations by the

beginning of next year. A positive profit contribution

is expected for 2008, with a rising trend over the

coming years. Despite of the current difficult politi-

cal situation, the management board also expects a

positive profit contribution for the DF Group from

Pakistan.

Cologne, November 2007

The Management Board

13 Interim Statement DF Deutsche Forfait AG

Period: 01-01-2007 to 30-09-2007

GROUP MANAGEMENT REPORT

14 Interim Statement DF Deutsche Forfait AG

Period: 01-01-2007 to 30-09-2007

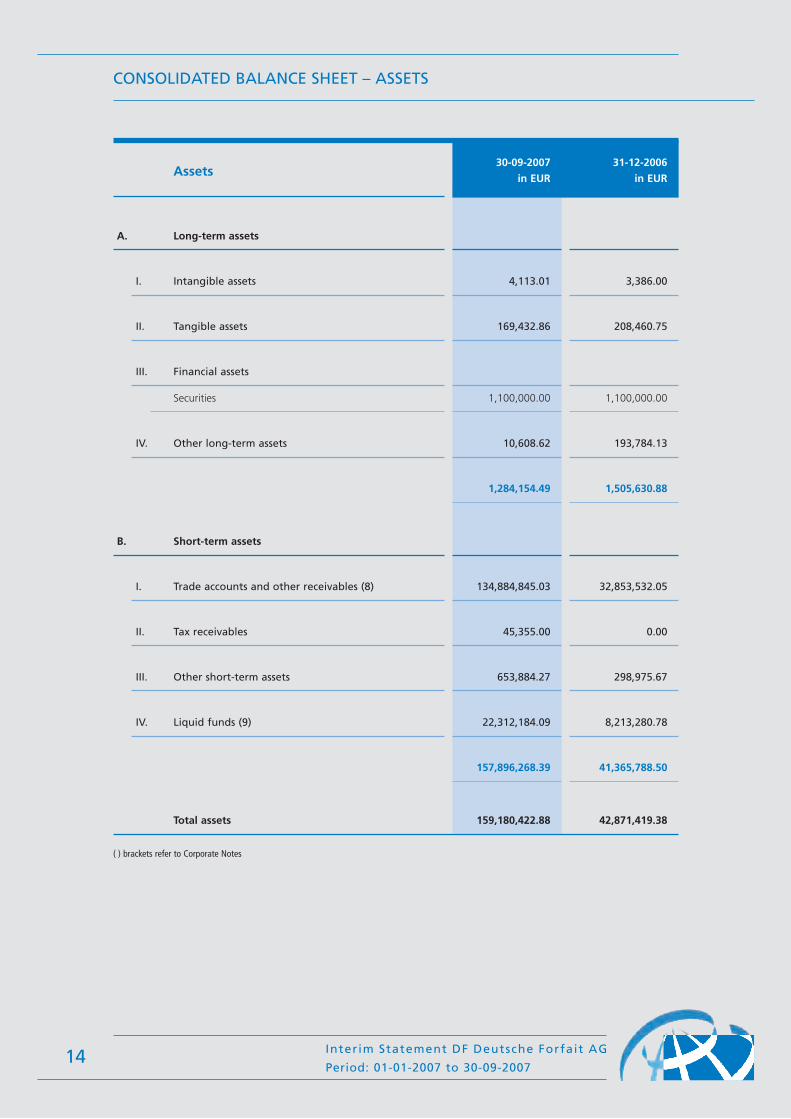

CONSOLIDATED BALANCE SHEET – ASSETS

A. Long-term assets

30-09-2007 31-12-2006

in EUR in EURAssets

Total assets 159,180,422.88 42,871,419.38

I. Intangible assets 4,113.01 3,386.00

II. Tangible assets 169,432.86 208,460.75

III. Financial assets

Securities 1,100,000.00 1,100,000.00

1,284,154.49 1,505,630.88

IV. Other long-term assets 10,608.62 193,784.13

B. Short-term assets

I. Trade accounts and other receivables (8) 134,884,845.03 32,853,532.05

III. Other short-term assets 653,884.27 298,975.67

II. Tax receivables 45,355.00 0.00

IV. Liquid funds (9) 22,312,184.09 8,213,280.78

157,896,268.39 41,365,788.50

( ) brackets refer to Corporate Notes

15 Interim Statement DF Deutsche Forfait AG

Period: 01-01-2007 to 30-09-2007

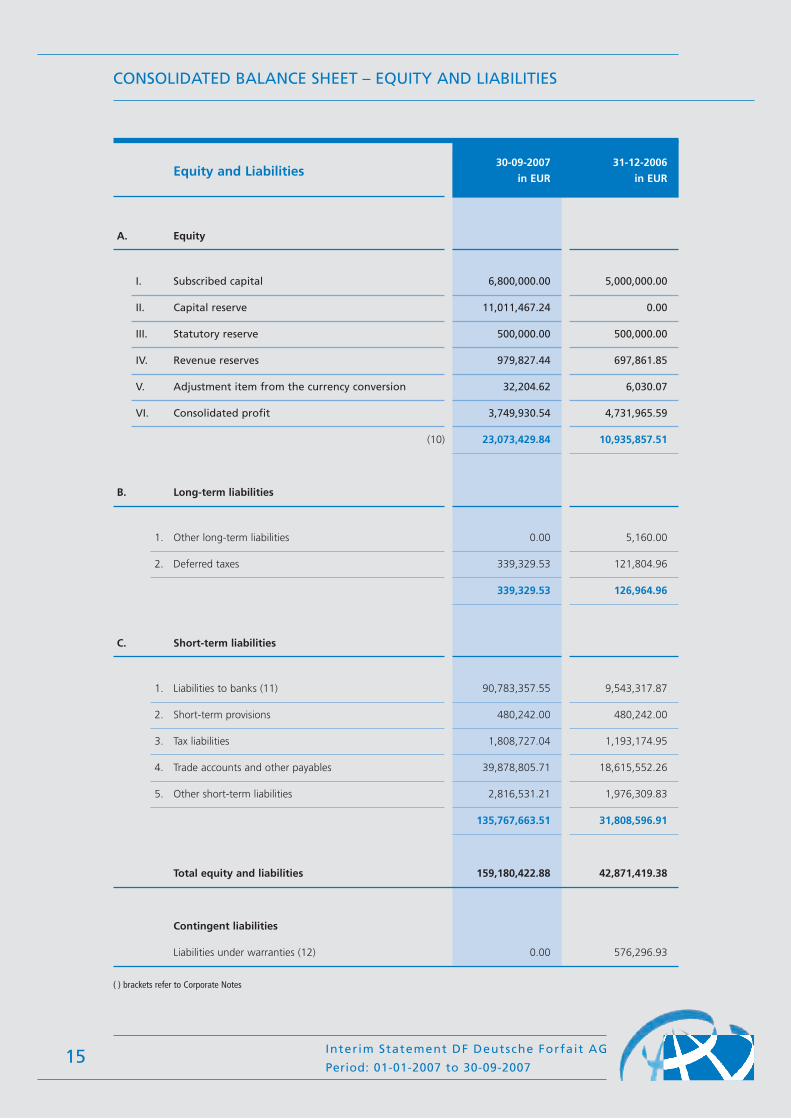

CONSOLIDATED BALANCE SHEET – EQUITY AND LIABILITIES

A. Equity

30-09-2007 31-12-2006

in EUR in EUREquity and Liabilities

Total equity and liabilities 159,180,422.88 42,871,419.38

I. Subscribed capital 6,800,000.00 5,000,000.00

II. Capital reserve 11,011,467.24 0.00

III. Statutory reserve 500,000.00 500,000.00

(10) 23,073,429.84 10,935,857.51

IV. Revenue reserves 979,827.44 697,861.85

V. Adjustment item from the currency conversion 32,204.62 6,030.07

VI. Consolidated profit 3,749,930.54 4,731,965.59

B. Long-term liabilities

339,329.53 126,964.96

1. Other long-term liabilities 0.00 5,160.00

2. Deferred taxes 339,329.53 121,804.96

C. Short-term liabilities

135,767,663.51 31,808,596.91

1. Liabilities to banks (11) 90,783,357.55 9,543,317.87

Contingent liabilities

Liabilities under warranties (12) 0.00 576,296.93

2. Short-term provisions 480,242.00 480,242.00

3. Tax liabilities 1,808,727.04 1,193,174.95

4. Trade accounts and other payables 39,878,805.71 18,615,552.26

5. Other short-term liabilities 2,816,531.21 1,976,309.83

( ) brackets refer to Corporate Notes

16 Interim Statement DF Deutsche Forfait AG

Period: 01-01-2007 to 30-09-2007

CONSOLIDATED INCOME STATEMENT – Q3 COMPARISON

5. Personnel expenses

a) Wages and salaries 861,495.71 584,416.70

b) Social security contributions and expenditure for pensions

and social welfare 171,687.60 114,564.64

11. Income tax

a) Income and earnings tax 836,481.97 660,664.85

b) Deferred taxes 44,290.94 -432.46

6. Depreciation on tangible and intangible assets 25,364.08 32,276.71

01-07 to 30-09-2007 01-07 to 30-09-2006

in EUR in EUR

20,353,925.15 16,378,716.19

4. Other operating income -14,494.60 26,771.64

7. Other operating expenditure 1,465,833.58 476,155.34

8. Interest income 204,293.52 19,105.60

9. Interest paid 790,227.61 867,588.36

Average number of shares 6,800,000 5,000,000

Earnings per share 0.23 0.19

10. Profit before income tax 2,443,590.21 1,634,050.84

12. Consolidated profit 1,562,817.30 973,818.45

3. Gross result 5,568,399.87 3,663,175.35

1. Typical forfaiting income

a) Discounts earned 9,363,946.95 13,435,091.34

b) Commission income 2,849,822.24 1,506,835.53

c) Income from additional interest charged 5,122,012.89 130,336.64

d) Exchange profits 3,018,143.07 1,306,452.68

e) Income from the reduction of value adjustments

on receivables and from the writing back of provisions

for forfaiting and purchase commitments 0.00 0.00

14,785,525.28 12,715,540.84

2. Typical forfaiting expenditure

a) Discounts paid 4,187,264.97 9,513,527.93

b) Commissions paid 1,822,164.83 1,298,307.12

c) Interest paid 4,598,837.19 8,249.42

d) Exchange losses 3,131,955.43 1,322,985.90

e) Credit insurance premiums 895,302.86 422,470.47

f) Depreciation and value adjustments on receivables

as well as additions to provisions for forfaiting

and purchase commitments 150,000.00 150,000.00

17 Interim Statement DF Deutsche Forfait AG

Period: 01-01-2007 to 30-09-2007

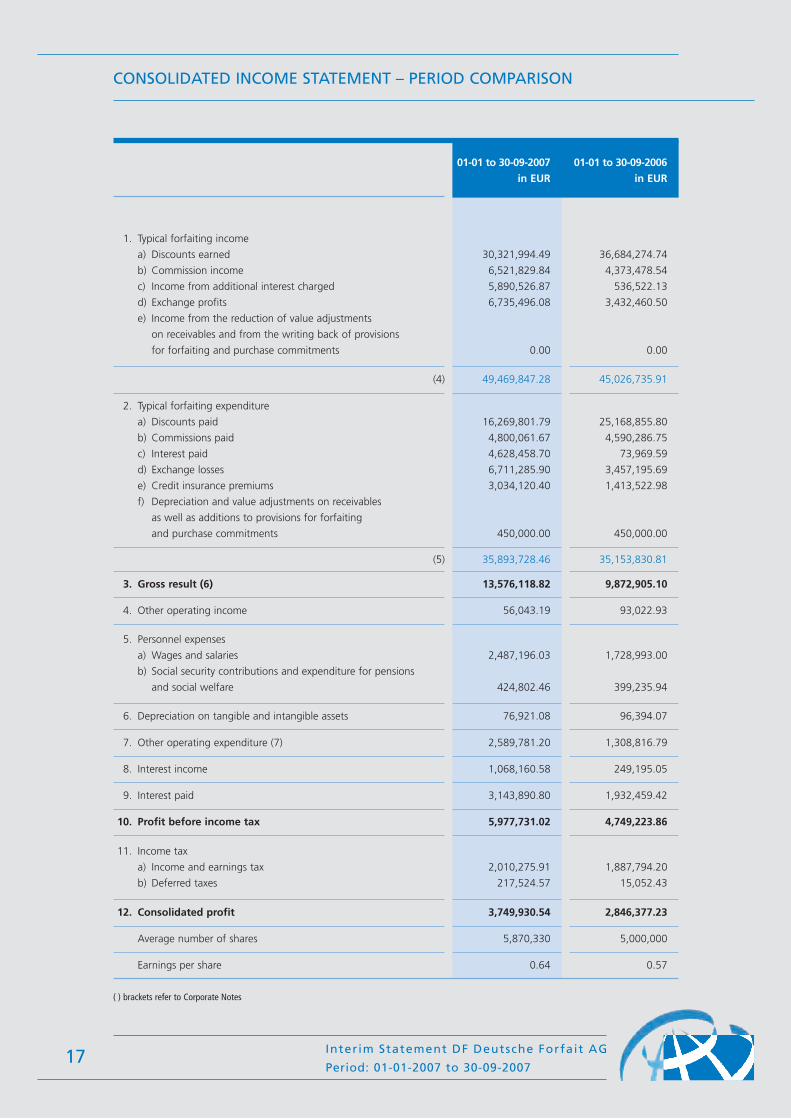

CONSOLIDATED INCOME STATEMENT – PERIOD COMPARISON

5. Personnel expenses

a) Wages and salaries 2,487,196.03 1,728,993.00

b) Social security contributions and expenditure for pensions

and social welfare 424,802.46 399,235.94

11. Income tax

a) Income and earnings tax 2,010,275.91 1,887,794.20

b) Deferred taxes 217,524.57 15,052.43

6. Depreciation on tangible and intangible assets 76,921.08 96,394.07

01-01 to 30-09-2007 01-01 to 30-09-2006

in EUR in EUR

(4) 49,469,847.28 45,026,735.91

4. Other operating income 56,043.19 93,022.93

7. Other operating expenditure (7) 2,589,781.20 1,308,816.79

8. Interest income 1,068,160.58 249,195.05

9. Interest paid 3,143,890.80 1,932,459.42

Average number of shares 5,870,330 5,000,000

Earnings per share 0.64 0.57

10. Profit before income tax 5,977,731.02 4,749,223.86

12. Consolidated profit 3,749,930.54 2,846,377.23

3. Gross result (6) 13,576,118.82 9,872,905.10

1. Typical forfaiting income

a) Discounts earned 30,321,994.49 36,684,274.74

b) Commission income 6,521,829.84 4,373,478.54

c) Income from additional interest charged 5,890,526.87 536,522.13

d) Exchange profits 6,735,496.08 3,432,460.50

e) Income from the reduction of value adjustments

on receivables and from the writing back of provisions

for forfaiting and purchase commitments 0.00 0.00

(5) 35,893,728.46 35,153,830.81

2. Typical forfaiting expenditure

a) Discounts paid 16,269,801.79 25,168,855.80

b) Commissions paid 4,800,061.67 4,590,286.75

c) Interest paid 4,628,458.70 73,969.59

d) Exchange losses 6,711,285.90 3,457,195.69

e) Credit insurance premiums 3,034,120.40 1,413,522.98

f) Depreciation and value adjustments on receivables

as well as additions to provisions for forfaiting

and purchase commitments 450,000.00 450,000.00

( ) brackets refer to Corporate Notes

18 Interim Statement DF Deutsche Forfait AG

Period: 01-01-2007 to 30-09-2007

CONSOLIDATED CASH FLOW STATEMENT

01-01 to 30-09-2007 01-01 to 30-09-2006

in TEUR in TEUR

Cash flow

Profit for the year 3,750 2,846

+ Depreciation on tangible and intangible assets 77 96

+ Expenses for income tax 2,228 1,903

+ Interest paid 3,144 1,932

- Interest income -1,068 -249

+/- Result from disposal of long-term assets 1 0

+/- Other transactions not affecting payments -1,114 -1,363

+/- Changes to trade accounts receivable -102,031 -59,153

+/- Changes to other assets (working capital) -217 -62

+/- Change to provisions 0 26

+/- Changes to trade accounts payable 21,263 9,044

+/- Change to other liabilities (working capital) 1,668 -743

- Paid taxes on profits -1,456 -607

= Operative Cash flow -73,756 -46,330

- Paid interest -2,723 -1,883

+ Retained interest 1,001 219

= Outflow from current business (Total 1) -75,478 -47,994

- Payments for investments in long-term assets -39 -41

+ Incoming payments from disposals of long-term assets 17 0

= Outflow from investment activity (Total 2) -22 -41

+/- Change to short-term financial liabilities 81,240 53,502

- Payment of dividends -4,450 -2,100

+ Incoming payments from capital market transactions 12,811 0

= Inflow from finance activity 89,602 51,402

Changes in financial resources affecting payments 14,102 3,367

+ Liquid funds at the start of the period 8,213 5,593

+/- Effects from the currency conversion -3 -1

= Liquid funds at the end of the period 22,312 8,959

19 Interim Statement DF Deutsche Forfait AG

Period: 01-01-2007 to 30-09-2007

DEVELOPMENT OF CONSOLIDATED EQUITY

Difference Subscribed Capital Statutory Revenue from currency

capital reserve reserve reserves conversion Totalin EUR

Balance 01-01-2006 5,000,000.00 – 177,033.00 3,120,828.85 6,744.58 8,304,606.43

Profit appropriation 322,967.00 (322,967.00)

Consolidated profit 2,846,377.23 2,846,377.23

Currency conversion (2,363.79) (2,363.79)

Dividend payment (2,100,000.00) (2,100,000.00)

Allocation to the reserves – – –

Balance 30-09-2006 5,000,000.00 – 500,000.00 3,544,239.08 4,380.79 9,048,619.87

Difference Subscribed Capital Statutory Revenue from currency

capital reserve reserve reserves conversion Totalin EUR

Balance 01-01-2007 5,000,000.00 – 500,000.00 5,429,827.44 6,030.07 10,935,857.51

Profit appropriation – –

Consolidated profit 3,749,930.54 3,749,930.54

Currency conversion 26,174.55 26,174.55

Dividend payment (4,450,000.00) (4,450,000.00)

Capital increase 1,800,000.00 11,011,467.24 12,811,467.24

Allocation to the reserves – – –

Balance 30-09-2007 6,800,000.00 11,011,467.24 500,000.00 4,729,757.98 32,204.62 23,073,429.84

Development of consolidated equity in the period 01-01-2006 to 30-09-2006

Development of consolidated equity in the period 01-01-2007 to 30-09-2007

(1) Basic principles

The shortened consolidated interim financial statements were prepared on a reduced scale compared to the

consolidated financial statements as at 31 December 2006, in accordance with the rules of IAS 34. The interim

financial statements as at 30 September 2007 use the same financial reporting and valuation methods as the

consolidated annual financial statements for the financial year 2006. The interim financial statements were subjected

to an audit inspection and ensure a fair view of the assets, financial and profit situation from the point of view of the

management. The group currency is demonstrated in euros. All amounts are stated in thousands of euros (EUR ‘000),

unless otherwise stated.

The legal form of DF Deutsche Forfait AG is that of a stock corporation. The company's registered office is in

Cologne, Germany, according to its Articles of Association. The company's address is Kattenbug 18-24, 50667

Cologne, Germany. It is listed under the number HRB 32949 at Cologne Local Court. DF Deutsche Forfait AG is a

forfaiting company and, as such, a finance company within the meaning of §1, section 3 of the German Banking

Act (KWG).

The shortened consolidated profit and loss account has been prepared using the total cost method. Pursuant to IFRS 7

("Financial Instruments: Disclosures"), income and expenses are grouped according to type and the total of the main

types of income and expenditure are stated so as to take account of the special features of a forfaiting company. The

shortened consolidated balance sheet corresponds to the classification rules of IAS 1.

(2) Consolidated companies

As at 31 December 2006, the subsidiaries DF Deutsche Forfait s.r.o., Prague/Czech Republic, and DF Deutsche Forfait

Americas, Inc., Miami/USA are still included in the consolidated interim financial statements.

(3) Currency conversion

The financial statements prepared in foreign currency of the included group companies are converted on the basis of

the concept of functional currency (IAS 21, "The Effects of Changes in Foreign Exchange Rates") according to the

modified closing rate method.

The functional currency of the subsidiaries is basically identical to the company's respective national currency.

Therefore, in the consolidated interim financial statements, the expenditure and income arising from the financial

statements of subsidiaries which are prepared in foreign currency are converted at the annual average rate, while

assets and liabilities are converted at the closing rate.

The exchange rates used as a basis for converting currency to euros are as follows:

20 Interim Statement DF Deutsche Forfait AG

Period: 01-01-2007 to 30-09-2007

CORPORATE NOTES

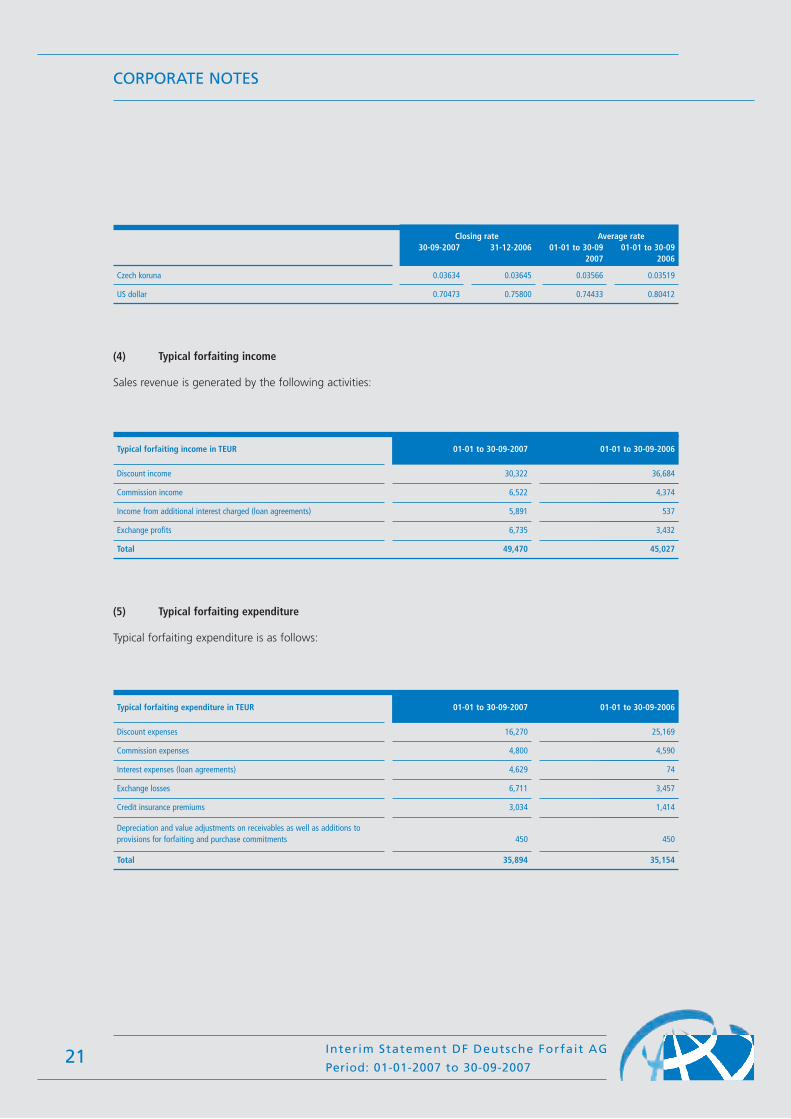

(4) Typical forfaiting income

Sales revenue is generated by the following activities:

21 Interim Statement DF Deutsche Forfait AG

Period: 01-01-2007 to 30-09-2007

CORPORATE NOTES

Closing rate Average rate30-09-2007 31-12-2006 01-01 to 30-09 01-01 to 30-09

2007 2006

Czech koruna 0.03634 0.03645 0.03566 0.03519

US dollar 0.70473 0.75800 0.74433 0.80412

Discount income 30,322 36,684

Typical forfaiting income in TEUR 01-01 to 30-09-2007 01-01 to 30-09-2006

Commission income 6,522 4,374

Income from additional interest charged (loan agreements) 5,891 537

Exchange profits 6,735 3,432

Total 49,470 45,027

Discount expenses 16,270 25,169

Typical forfaiting expenditure in TEUR 01-01 to 30-09-2007 01-01 to 30-09-2006

Commission expenses 4,800 4,590

Interest expenses (loan agreements) 4,629 74

Exchange losses 6,711 3,457

Credit insurance premiums 3,034 1,414

Depreciation and value adjustments on receivables as well as additions to provisions for forfaiting and purchase commitments 450 450

Total 35,894 35,154

(5) Typical forfaiting expenditure

Typical forfaiting expenditure is as follows:

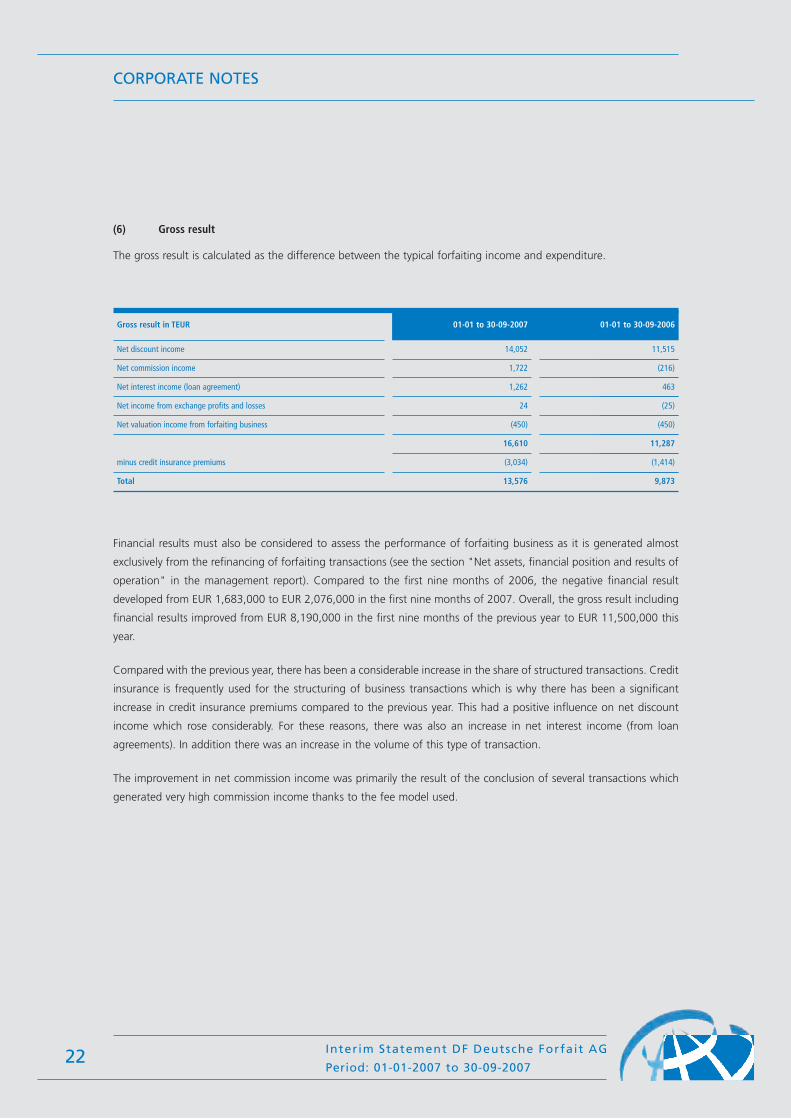

(6) Gross result

The gross result is calculated as the difference between the typical forfaiting income and expenditure.

22 Interim Statement DF Deutsche Forfait AG

Period: 01-01-2007 to 30-09-2007

CORPORATE NOTES

Net discount income 14,052 11,515

Gross result in TEUR 01-01 to 30-09-2007 01-01 to 30-09-2006

Net commission income 1,722 (216)

Net interest income (loan agreement) 1,262 463

Net income from exchange profits and losses 24 (25)

Net valuation income from forfaiting business (450) (450)

minus credit insurance premiums (3,034) (1,414)

Total 13,576 9,873

16,610 11,287

Financial results must also be considered to assess the performance of forfaiting business as it is generated almost

exclusively from the refinancing of forfaiting transactions (see the section "Net assets, financial position and results of

operation" in the management report). Compared to the first nine months of 2006, the negative financial result

developed from EUR 1,683,000 to EUR 2,076,000 in the first nine months of 2007. Overall, the gross result including

financial results improved from EUR 8,190,000 in the first nine months of the previous year to EUR 11,500,000 this

year.

Compared with the previous year, there has been a considerable increase in the share of structured transactions. Credit

insurance is frequently used for the structuring of business transactions which is why there has been a significant

increase in credit insurance premiums compared to the previous year. This had a positive influence on net discount

income which rose considerably. For these reasons, there was also an increase in net interest income (from loan

agreements). In addition there was an increase in the volume of this type of transaction.

The improvement in net commission income was primarily the result of the conclusion of several transactions which

generated very high commission income thanks to the fee model used.

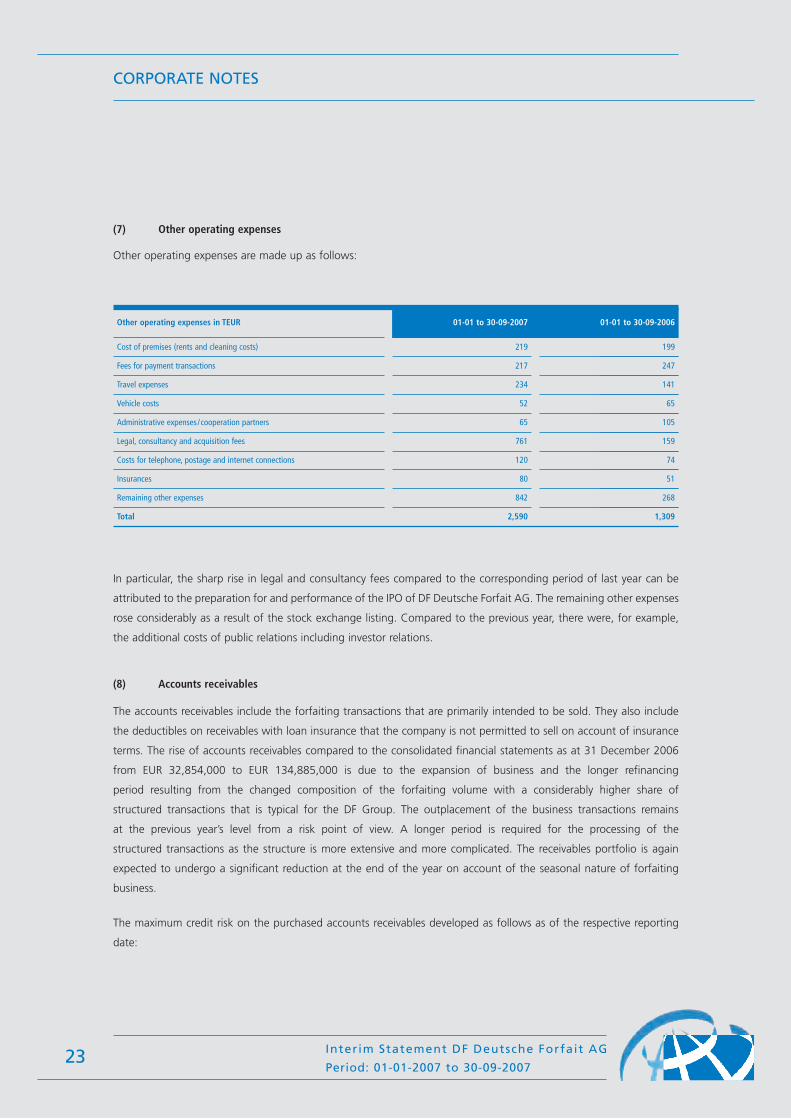

(7) Other operating expenses

Other operating expenses are made up as follows:

23 Interim Statement DF Deutsche Forfait AG

Period: 01-01-2007 to 30-09-2007

CORPORATE NOTES

In particular, the sharp rise in legal and consultancy fees compared to the corresponding period of last year can be

attributed to the preparation for and performance of the IPO of DF Deutsche Forfait AG. The remaining other expenses

rose considerably as a result of the stock exchange listing. Compared to the previous year, there were, for example,

the additional costs of public relations including investor relations.

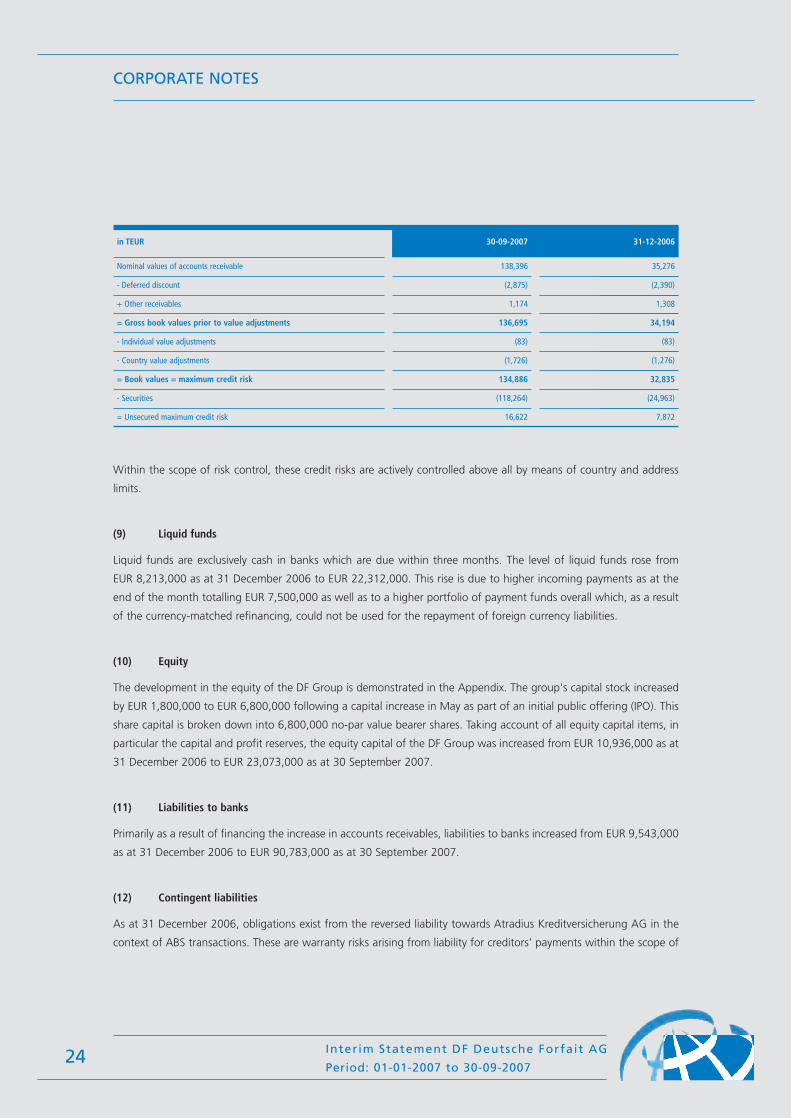

(8) Accounts receivables

The accounts receivables include the forfaiting transactions that are primarily intended to be sold. They also include

the deductibles on receivables with loan insurance that the company is not permitted to sell on account of insurance

terms. The rise of accounts receivables compared to the consolidated financial statements as at 31 December 2006

from EUR 32,854,000 to EUR 134,885,000 is due to the expansion of business and the longer refinancing

period resulting from the changed composition of the forfaiting volume with a considerably higher share of

structured transactions that is typical for the DF Group. The outplacement of the business transactions remains

at the previous year’s level from a risk point of view. A longer period is required for the processing of the

structured transactions as the structure is more extensive and more complicated. The receivables portfolio is again

expected to undergo a significant reduction at the end of the year on account of the seasonal nature of forfaiting

business.

The maximum credit risk on the purchased accounts receivables developed as follows as of the respective reporting

date:

Cost of premises (rents and cleaning costs) 219 199

Other operating expenses in TEUR 01-01 to 30-09-2007 01-01 to 30-09-2006

Fees for payment transactions 217 247

Travel expenses 234 141

Vehicle costs 52 65

Administrative expenses/cooperation partners 65 105

Legal, consultancy and acquisition fees 761 159

Costs for telephone, postage and internet connections 120 74

Insurances 80 51

Remaining other expenses 842 268

Total 2,590 1,309

Within the scope of risk control, these credit risks are actively controlled above all by means of country and address

limits.

(9) Liquid funds

Liquid funds are exclusively cash in banks which are due within three months. The level of liquid funds rose from

EUR 8,213,000 as at 31 December 2006 to EUR 22,312,000. This rise is due to higher incoming payments as at the

end of the month totalling EUR 7,500,000 as well as to a higher portfolio of payment funds overall which, as a result

of the currency-matched refinancing, could not be used for the repayment of foreign currency liabilities.

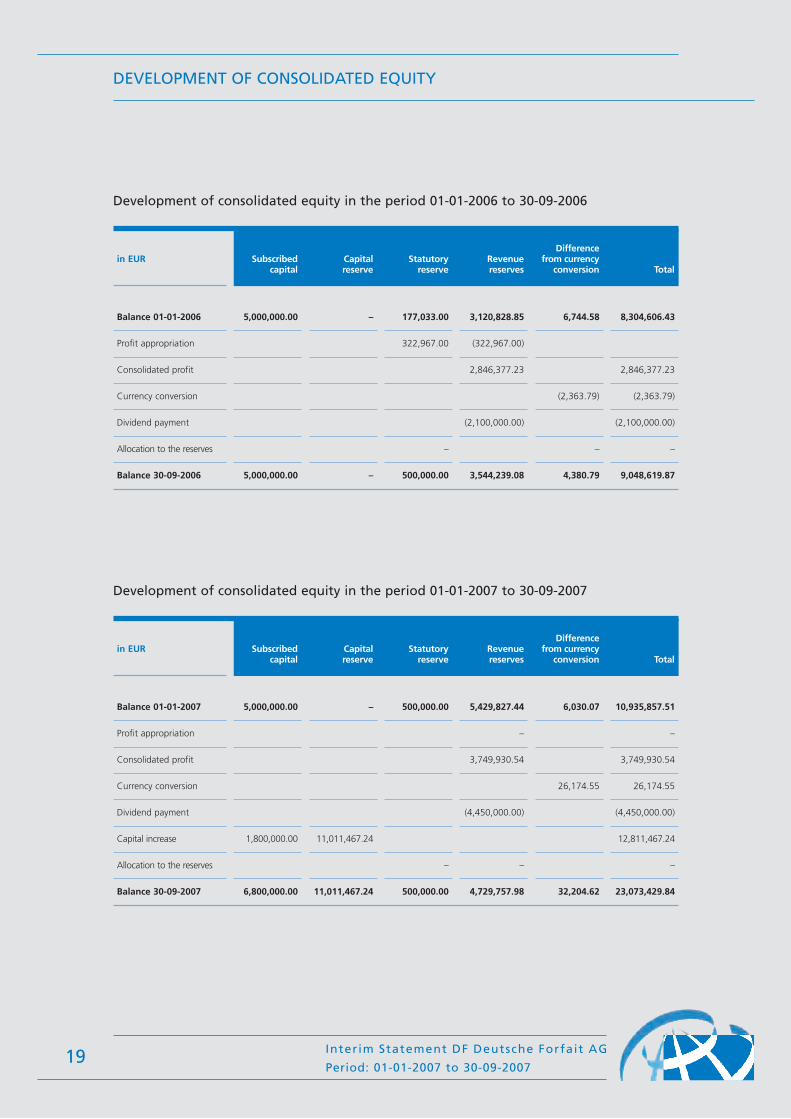

(10) Equity

The development in the equity of the DF Group is demonstrated in the Appendix. The group's capital stock increased

by EUR 1,800,000 to EUR 6,800,000 following a capital increase in May as part of an initial public offering (IPO). This

share capital is broken down into 6,800,000 no-par value bearer shares. Taking account of all equity capital items, in

particular the capital and profit reserves, the equity capital of the DF Group was increased from EUR 10,936,000 as at

31 December 2006 to EUR 23,073,000 as at 30 September 2007.

(11) Liabilities to banks

Primarily as a result of financing the increase in accounts receivables, liabilities to banks increased from EUR 9,543,000

as at 31 December 2006 to EUR 90,783,000 as at 30 September 2007.

(12) Contingent liabilities

As at 31 December 2006, obligations exist from the reversed liability towards Atradius Kreditversicherung AG in the

context of ABS transactions. These are warranty risks arising from liability for creditors' payments within the scope of

24 Interim Statement DF Deutsche Forfait AG

Period: 01-01-2007 to 30-09-2007

CORPORATE NOTES

Nominal values of accounts receivable 138,396 35,276

in TEUR 30-09-2007 31-12-2006

- Deferred discount (2,875) (2,390)

+ Other receivables 1,174 1,308

= Gross book values prior to value adjustments 136,695 34,194

- Individual value adjustments (83) (83)

- Country value adjustments (1,726) (1,276)

= Book values = maximum credit risk 134,886 32,835

- Securities (118,264) (24,963)

= Unsecured maximum credit risk 16,622 7,872

the agreed "first loss" rule: The last remaining reversed liability has expired as a result of the proper payment of the

receivable in May of this year. As a result, there are no longer any such contingent liabilities:

25 Interim Statement DF Deutsche Forfait AG

Period: 01-01-2007 to 30-09-2007

CORPORATE NOTES

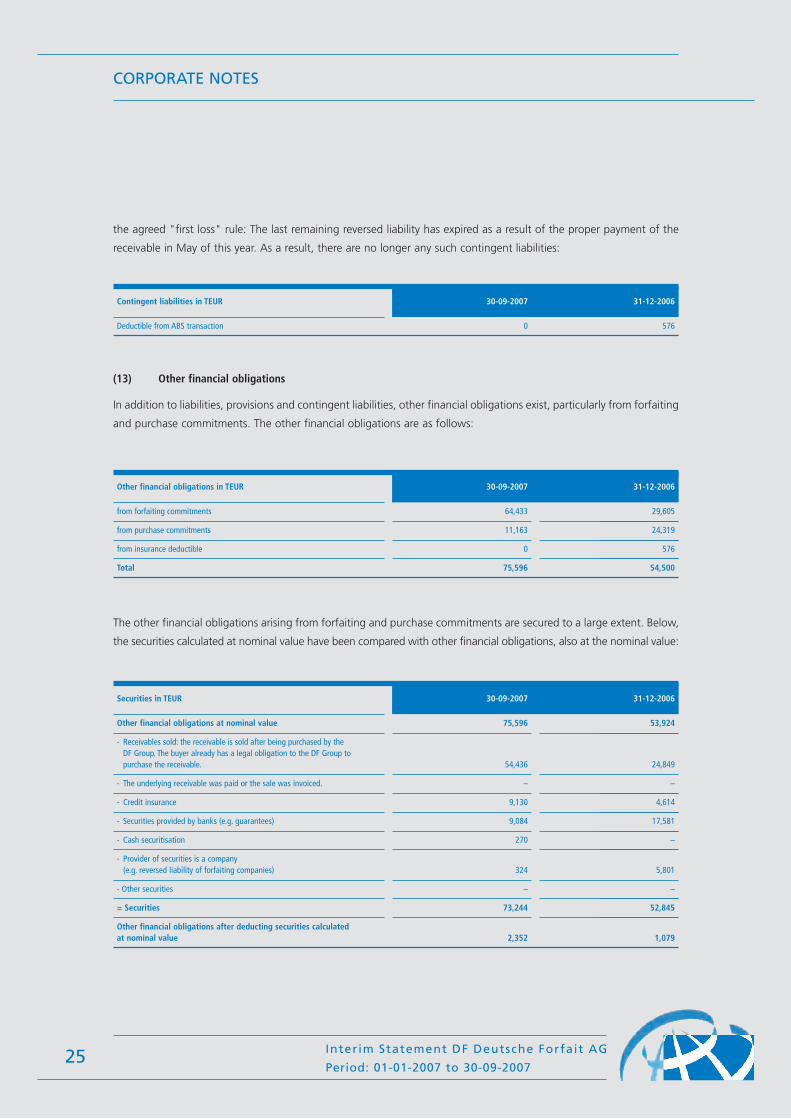

from forfaiting commitments 64,433 29,605

from purchase commitments 11,163 24,319

from insurance deductible 0 576

Total 75,596 54,500

Other financial obligations at nominal value 75,596 53,924

Securities in TEUR 30-09-2007 31-12-2006

- Receivables sold: the receivable is sold after being purchased by the DF Group. The buyer already has a legal obligation to the DF Group to purchase the receivable. 54,436 24,849

- The underlying receivable was paid or the sale was invoiced. – –

- Credit insurance 9,130 4,614

- Securities provided by banks (e.g. guarantees) 9,084 17,581

- Cash securitisation 270 –

- Provider of securities is a company (e.g. reversed liability of forfaiting companies) 324 5,801

Other financial obligations after deducting securities calculated at nominal value 2,352 1,079

- Other securities – –

= Securities 73,244 52,845

(13) Other financial obligations

In addition to liabilities, provisions and contingent liabilities, other financial obligations exist, particularly from forfaiting

and purchase commitments. The other financial obligations are as follows:

Other financial obligations in TEUR 30-09-2007 31-12-2006

Deductible from ABS transaction 0 576

Contingent liabilities in TEUR 30-09-2007 31-12-2006

The other financial obligations arising from forfaiting and purchase commitments are secured to a large extent. Below,

the securities calculated at nominal value have been compared with other financial obligations, also at the nominal value:

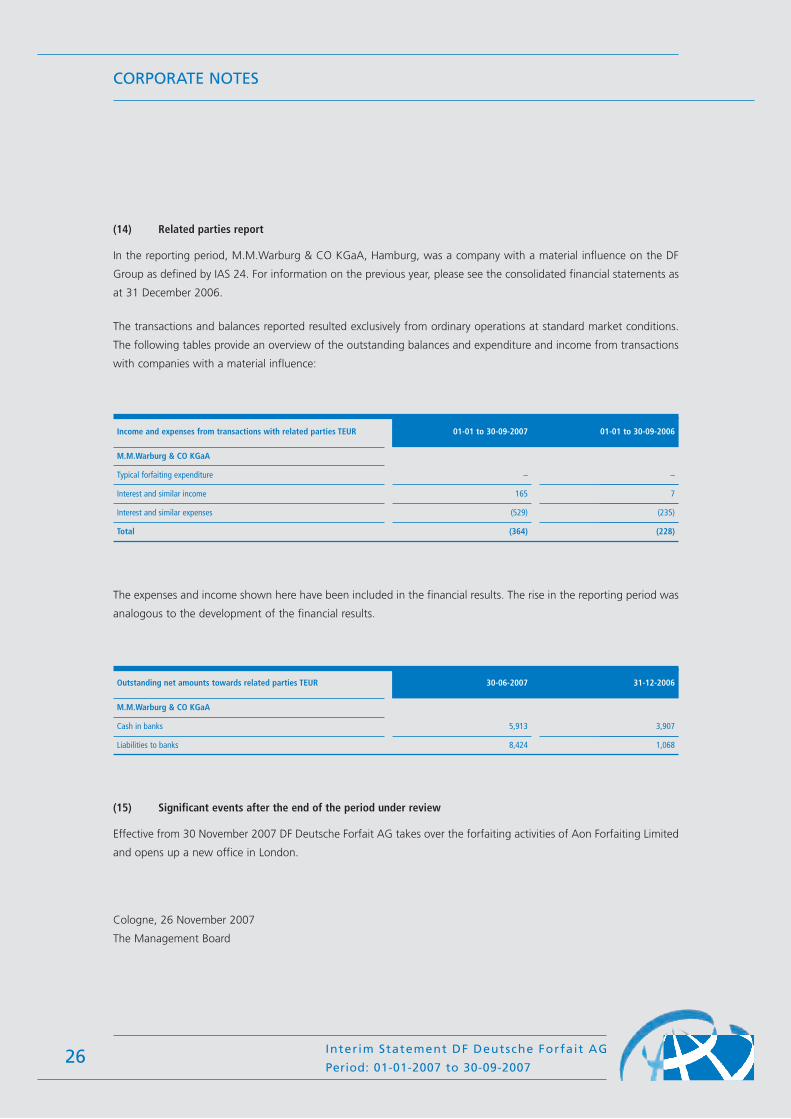

(14) Related parties report

In the reporting period, M.M.Warburg & CO KGaA, Hamburg, was a company with a material influence on the DF

Group as defined by IAS 24. For information on the previous year, please see the consolidated financial statements as

at 31 December 2006.

The transactions and balances reported resulted exclusively from ordinary operations at standard market conditions.

The following tables provide an overview of the outstanding balances and expenditure and income from transactions

with companies with a material influence:

26 Interim Statement DF Deutsche Forfait AG

Period: 01-01-2007 to 30-09-2007

CORPORATE NOTES

M.M.Warburg & CO KGaA

Typical forfaiting expenditure – –

Interest and similar income 165 7

Interest and similar expenses (529) (235)

Total (364) (228)

Income and expenses from transactions with related parties TEUR 01-01 to 30-09-2007 01-01 to 30-09-2006

M.M.Warburg & CO KGaA

Cash in banks 5,913 3,907

Liabilities to banks 8,424 1,068

Outstanding net amounts towards related parties TEUR 30-06-2007 31-12-2006

The expenses and income shown here have been included in the financial results. The rise in the reporting period was

analogous to the development of the financial results.

(15) Significant events after the end of the period under review

Effective from 30 November 2007 DF Deutsche Forfait AG takes over the forfaiting activities of Aon Forfaiting Limited

and opens up a new office in London.

Cologne, 26 November 2007

The Management Board

Review engagement report

We have completed a review of the condensed interim consolidated financial statements – consisting of the

condensed balance sheet, condensed profit and loss statement, condensed statement of changes in financial

position, and condensed statement of changes in shareholders’ equity as well as selected notes to the financial

statements – and the interim group management report of DF Deutsche Forfait Aktiengesellschaft, Cologne, for

the period from January 1, 2007 to September 30, 2007. Preparing the condensed interim consolidated finan-

cial statements according to IFRS principles for interim reporting as they apply to the EU, and the interim group

management report according to the WpHG (Securities Trade Act) regulations as they apply to group interim

management reports is the responsibility of the company’s legal representatives. Our responsibility is to issue an

opinion on the condensed interim consolidated financial statements and the group interim management report

based on the review engagement completed by us.

We completed our review of the condensed interim consolidated financial statements and the group interim

management report based on German principles for financial reporting review engagements established by the

IDW (“Institut der Wirtschaftsprüfer”, German institute of auditors). According to these principles, a review

engagement must be planned and carried out so that, based on a critical appraisal, we can be reasonably

certain that the condensed interim consolidated financial statements comply with the IFRS principles for interim

reporting as they apply to the EU in all material respects and that the interim group management report

complies with the WpHG (Securities Trade Act) regulations as they apply to group interim management reports

in all material respects. A review engagement is mainly limited to interviews with company employees and an

analytical evaluation, which means it does not result in the same level of certainty attained by an audit. Since

we were not engaged to complete an audit, we are not issuing an audit opinion.

During our review engagement, we did not become aware of any information that would indicate that the

condensed interim consolidated financial statements do not comply with the IFRS principles for interim

reporting as they apply to the EU in all material respects or that the interim group management report does not

comply with the WpHG (Securities Trade Act) regulations as they apply to group interim management reports

in all material respects.

Hamburg, November 27, 2007

BDO Deutsche Warentreuhand Aktiengesellschaft Audit Firm

von Thermann ppa. Briese

Wirtschaftsprüfer Wirtschaftsprüfer

27 Interim Statement DF Deutsche Forfait AG

Period: 01-01-2007 to 30-09-2007

CORPORATE NOTES

www.dfag.de