Embed Size (px)

Citation preview

Deutsche Asset & Wealth Management

May 15, 2015

Sales Prospectus and Management Regulations

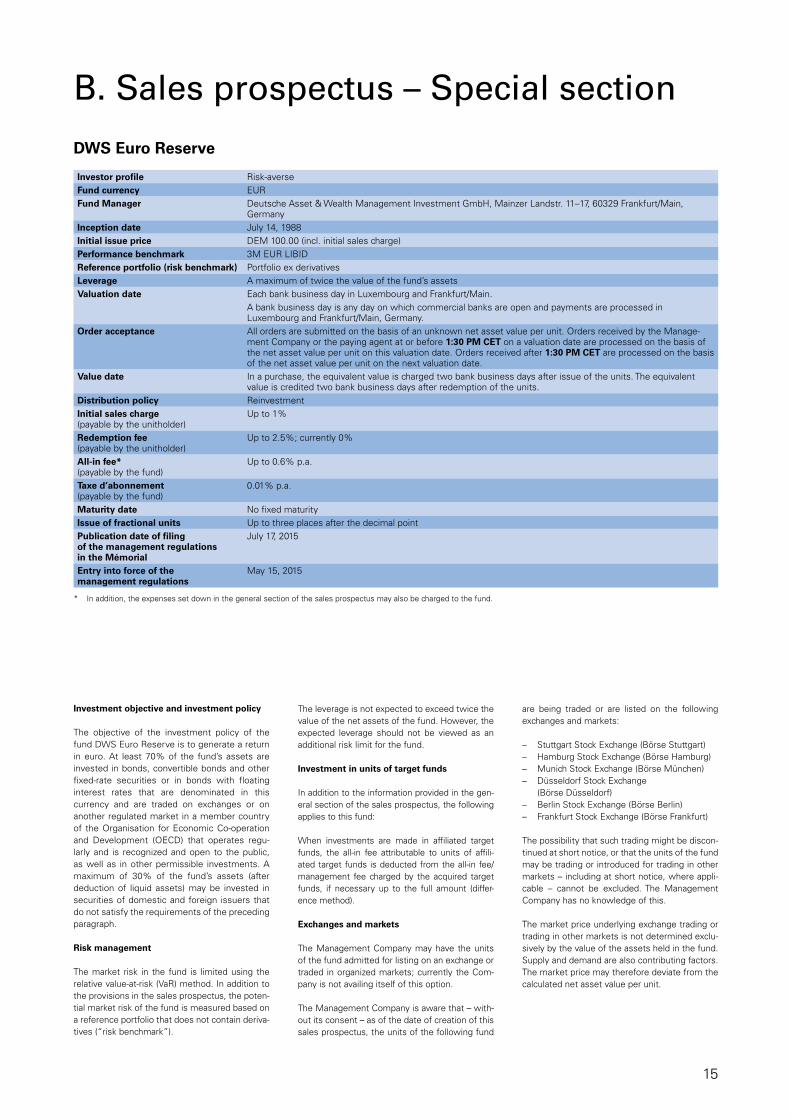

DWS Euro Reserve

Deutsche Asset & Wealth Management Investment S.A.

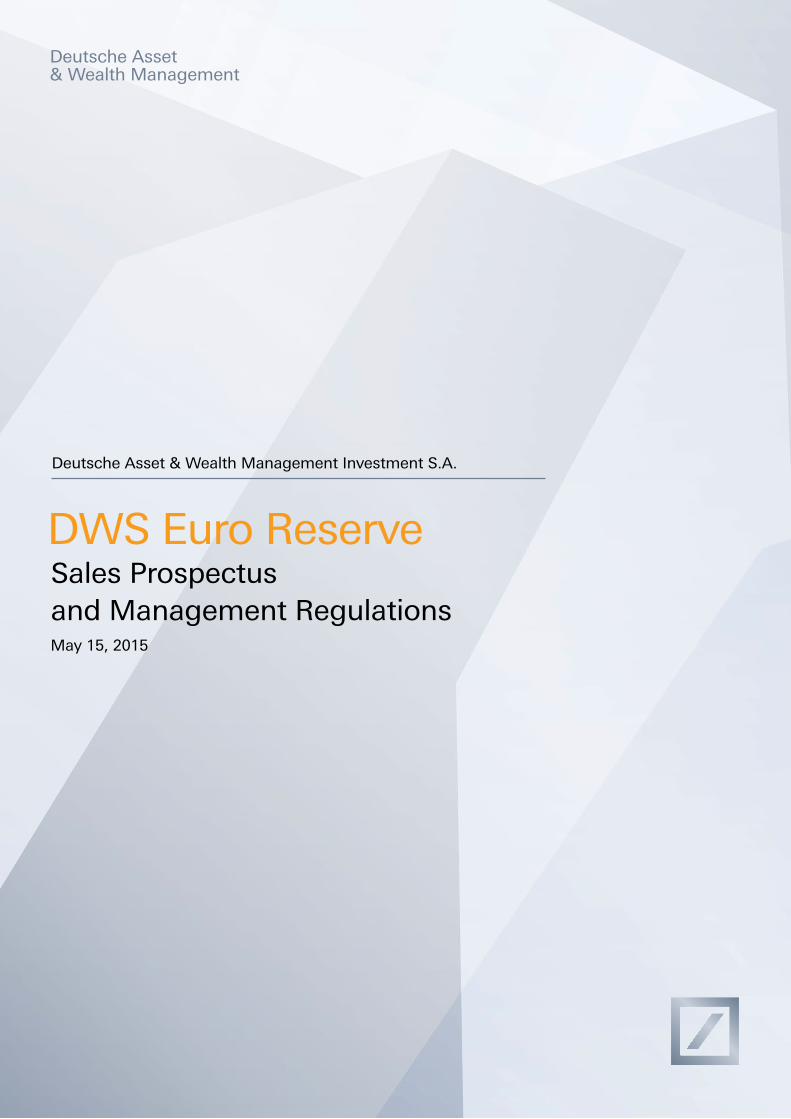

Deutsche Asset & Wealth Management Investment S.A. currently manages the following investment funds in the legal form of a fonds commun de placement (FCP) in accordance with the Law of December 17, 2010 (as of May 15, 2015):

AL DWS GlobalAktiv+

ARERO – Der WeltfondsBreisgau-FondsBethmann Absolute Flex InternationalBethmann Vermögensverwaltung AusgewogenBethmann Vermögensverwaltung ErtragBethmann Vermögensverwaltung WachstumDB Advisors Emerging Markets Equities – PassiveDB Advisors Invest*DB Advisors Strategy Fund*DB Fixed Coupon Fund 2018DB Fixed Coupon Fund 2018 IIDB OpportunityDB Portfolio*db PrivatMandat Fit*Deutsche Bank*Deutsche Bank Zins & Dividende – OffensivDeutsche European Real Estate Securities Master FundDeutsche Floating Rate NotesDWS BestSelect BranchenDWS Concept ARTS ConservativeDWS Concept ARTS DynamicDWS Concept ARTS BalancedDWS Dividende Direkt 2017DWS Dividende Emerging Markets Direkt 2015DWS Dividende Garant 2016DWS Emerging Corporate Bond Master FundDWS Emerging Markets Bonds (Short)DWS Emerging Markets Corporates 2015DWS Emerging Sovereign Bond Fund AUDDWS Emerging Sovereign Bond Fund USDDWS Emerging Sovereign Bond Fund USD (AUD)DWS EtoileDWS Euro ReserveDWS Euro-Bonds (Long)DWS Euro-Bonds (Medium)DWS EurorentaDWS Garant 80 FPIDWS Global*DWS Global Equity Focus FundDWS Global Protect 80 IIDWS Global Utility Bond Master FundDWS G-SIFIs Hybrid Bond Fund

DWS Global ValueDWS Gold plusDWS IndiaDWS Megatrend Performance 2016DWS Multi OpportunitiesDWS OsteuropaDWS Performance Rainbow 2015DWS Rendite*DWS Rendite Garant 2015DWS Rendite Garant 2015 IIDWS Rendite OptimaDWS Rendite Optima Four SeasonsDWS Renten Direkt 2017DWS Renten Direkt Select 2016DWS RussiaDWS Top BalanceDWS Top DynamicDWS Top Portfolio BalanceDWS Top Portfolio DefensivDWS TürkeiDWS (US Dollar) ReserveDWS Vermögensbildungsfonds I (Lux)DWS Vermögensmandat*DWS Vola StrategyDWS Vorsorge*DWS World Funds*DWS Zeitwert ProtectFI ALPHA*GIS High Conviction Equity (USD)Global Emerging Markets Balance PortfolioMulti OpportunitiesMulti Opportunities IIIMulti Style – MarsOona SolutionsPAM International Fund Selection Portfolio*Postbank DynamikPostbank StrategiePWM Mandat – DWS*SFC Global MarketsSüdwestbank Vermögensmandat*Vermögensfondsmandat flexibel (80% teilgeschützt)Zurich*Zurich Vorsorge Dachfonds II

as well as 26 investment companies in the legal form of a Société d’Investissement à Capital Variable (SICAV) pursuant to the Law of December 17, 2010, and another 17 specialized investment funds pursuant to the Law of February 13, 2007, in the form of a SICAV-SIF or a FCP-SIF.

* Umbrella FCP

1

Contents

Legal structure:

FCP according to Part I of the Law of December 17, 2010, on Undertakings for Collective Investment.

General information

The legally dependent investment fund described in this sales prospectus is a Luxembourg invest-ment fund (fonds commun de placement) organized under Part I of the Luxembourg law on Undertakings for Collective Investment of December 17, 2010 (“Law of 2010”), and in compli-ance with the provisions of Directive 2009/65/EC of the European Parliament and of the Council of July 13, 2009, which replaces Directive 85/611/EEC (UCITS), as well as the provisions of the Grand- Ducal Regulation of February 8, 2008, relating to certain definitions of the Law of Decem-ber 20, 2002, on Undertakings for Collective Investment, as amended1 (“Grand-Ducal Regu-lation of February 8, 2008”) and implementing Directive 2007/16/EC2 (“Directive 2007/16/EC”) in Luxembourg law.

With regard to the provisions contained in Direc-tive 2007/16/EC and in the Grand-Ducal Regula-tion of February 8, 2008, the guidelines of the Committee of European Securities Regulators (CESR) set out in the document “CESR’s guide-lines concerning eligible assets for investment by UCITS" as amended, provide a set of additional explanations that are to be observed in relation to the financial instruments that are applicable for UCITS falling under Directive 2009/65/EC, as amended.3

It is prohibited to provide any information or to make any representations other than those con-tained in the sales prospectus and in the man-agement regulations. Deutsche Asset & Wealth Management Investment S.A. shall not be liable

if such divergent information or representations are supplied.

1 Replaced by the Law of 2010.2 Commission Directive 2007/16/EC of March 19, 2007,

implementing Council Directive 85/611/EEC on the coordination of laws, regulations and administra-tive provisions relating to undertakings for collective investment in transferable securities (UCITS) as regards the clarification of certain definitions (“Direc-tive 2007/16/EC”).

3 See CSSF circular 08-339 in the currently applicable ver-sion: CESR’s guidelines concerning eligible assets for investment by UCITS – March 2007, ref.: CESR/07-044; CESR’s guidelines concerning eligible assets for investment by UCITS – The classification of hedge fund indices as financial indices – July 2007, ref.: CESR/07-434.

A. Sales prospectus – General section 2

B. Sales prospectus – Special section 15

C. Management regulations 17

DWS Euro Reserve

2

A. Sales prospectus – General section

Management Company, Central Administration Agent, Transfer Agent,

Registrar and Main Distributor

Deutsche Asset & Wealth Management Investment S.A.2, Boulevard Konrad Adenauer1115 Luxembourg, Luxembourg

Management and Administration

Supervisory Board

Holger Naumann ChairmanDeutsche Asset & Wealth ManagementInvestment GmbH, Frankfurt/Main, Germany

Dr. Asoka WöhrmannDeutsche Asset & Wealth Management Investment GmbH, Frankfurt/Main, Germany

Dr. Matthias LiermannDeutsche Asset & Wealth Management Investment GmbH, Frankfurt/Main, Germany

Marzio HugDeutsche Bank AG, London branch, United Kingdom

Dr. Boris Nikolaj LiedtkeDeutsche Bank Luxembourg S.A., Luxembourg

Nathalie BauschDeutsche Bank Luxembourg S.A., Luxembourg

Reinhard BelletDeutsche Bank AG, Frankfurt/Main, Germany

Fund Manager

Deutsche Asset & Wealth Management Investment GmbHMainzer Landstr. 11-1760329 Frankfurt/Main, Germany

Management Board

Manfred Bauer Chairman Deutsche Asset & Wealth Management Investment S.A., Luxembourg

Ralf Rauch Deutsche Asset & Wealth Management Investment GmbH, Frankfurt/Main, Germany

Martin SchönefeldDeutsche Asset & Wealth Management Investment S.A., Luxembourg

Barbara SchotsDeutsche Asset & Wealth ManagementInvestment S.A., Luxembourg

Depositary

State Street Bank Luxembourg S.C.A.49, Avenue J. F. Kennedy1855 Luxembourg, Luxembourg

Auditor

KPMG Luxembourg Société Coopérative39, Avenue J. F. Kennedy1855 Luxembourg, Luxembourg

3

Sales, Information and Paying Agents

LuxembourgDeutsche Bank Luxembourg S.A.2, Boulevard Konrad Adenauer1115 Luxembourg, Luxembourg

GermanyDeutsche Bank AGTaunusanlage 1260325 Frankfurt/Main, Germanyand its branches

Deutsche Bank Privat- und Geschäftskunden AGTheodor-Heuss-Allee 7260486 Frankfurt/Main, Germanyand its branches

BelgiumDeutsche Bank NV/S.A.13–15, Avenue Marnix1000 Brussels, Belgium

FranceSociété Générale29, Boulevard Haussmann75009 Paris, France

SpainDeutsche Bank S.A.E.Ronda General Mitre 72–7408017 Barcelona, Spain

SwitzerlandDeutsche Bank (Suisse) S.A.3, place des Bergues1211 Geneva, Switzerland

Deutsche Bank (Schweiz) AGHardstrasse 2018005 Zurich, Switzerland

Deutsche Bank (Svizzera) S.A.Via Ferruccio Pelli 16901 Lugano, Switzerland

PortugalDeutsche Bank (Portugal) S.A.Rua Castilho, n. 201250-069 Lisbon, Portugal

AustriaDeutsche Bank Österreich AGStock-im-Eisen-Platz 31010 Vienna, Austria

4

General regulations

Attached to this sales prospectus are the man-agement regulations for the fund. The sales prospectus and management regulations form a unit, providing information on and explanations of one and the same subject, and therefore supple-ment one another.

The sales prospectus, the key investor infor-mation document and the management regu-lations, as well as the annual and semiannual reports, are available free of charge from the Management Company and the paying agents. Other important information will be communi-cated to unitholders in a suitable form by the Management Company. The Management Com-pany will use an additional publication to inform investors of the point after which it will only be possible to view notices to unitholders on the Internet at www.dws.lu. Where provided for in a distribution country, notices shall nonetheless be published in a newspaper and/or in another publication medium as directed by law. Where provided for by Luxembourg law, notices will continue to be published in at least one Luxem-bourg daily newspaper and, if necessary, in the Mémorial.

Management Company

The fund is managed by Deutsche Asset & Wealth Management Investment S.A., Luxembourg (the “Management Company”), which fulfills the requirements of chapter 15 of the Law of 2010, and thus the provisions of Directive 2009/65/EC of the European Parliament and of the Council of July 13, 2009, governing management companies.

The Management Company was established on April 15, 1987, with subsequent publication in the Mémorial C taking place on May 4, 1987. Its sub-scribed and paid-in capital is EUR 30,677,400. The management of the investment fund includes, but is not limited to, those tasks specified in Appendix II of the Law of 2010.

The Management Company may, in compliance with the regulations of the Luxembourg Law of 2010, and regulation 10-04 of the Commission de Surveillance du Secteur Financier and related circulars if applicable, delegate one or more tasks to third parties under its supervision and control.

(i) Investment management

The Management Company, under its respon-sibility and control and at its own expense, has entered into a fund management agreement for the fund with Deutsche Asset & Wealth Manage-ment Investment GmbH, Frankfurt/Main, Ger-many. Deutsche Asset & Wealth Management Investment GmbH is an investment company under German law. The contract may be termi-nated by either of the parties on three months’ notice.

In this respect, fund management shall encom-pass the day-to-day implementation of the invest-ment policy and direct investment decisions. The designated fund manager may delegate fund management services in whole or in part, under its supervision, control and responsibility, and at its own expense.

(ii) Administration, registrar and transfer agent

The first responsibility of the Management Com-pany, Deutsche Asset & Wealth Management Investment S.A., is to perform central administra-tion functions, in particular fund bookkeeping and net asset value calculation. In addition, Deutsche Asset & Wealth Management Investment S.A. is responsible for the remaining administrative tasks. These include, among other things, the retrospec-tive monitoring of investment limits and restrictions as well as the functions of domiciliary agent and registrar and transfer agent.

With regard to the function as registrar and trans-fer agent, Deutsche Asset & Wealth Management Investment S.A. has entered into a sub-transfer agent agreement with State Street Bank GmbH in Munich, Germany. Within the scope of this agreement, State Street Bank GmbH in particular assumes the duties of managing the global certifi-cate, which is deposited with Clearstream Banking AG in Frankfurt/Main, Germany.

(iii) Distribution

Deutsche Asset & Wealth Management Invest-ment S.A. acts as the main distributor.

Special notice

The Management Company draws investors’ attention to the fact that any investor can only assert his investor rights in their entirety directly against the fund if the investor subscribed the fund units himself and in his own name. In cases where an investor invested in a fund via an inter-mediary, who invested in his own name but for the account of the investor, the investor may not be able to directly assert all his investors’ rights directly against the fund. Investors are advised to find out about their rights.

Depositary

The Depositary is State Street Bank Luxembourg S.C.A. The Depositary holds the assets of the fund and discharges all other obligations imposed on the Depositary pursuant to Luxembourg law.

General risk warnings

Investing in the units involves risks. These can encompass or involve equity or bond market risks, interest rate, credit, default, liquidity and counter-party risks as well as exchange rate, volatility, or political risks. Any of these risks may also occur in conjunction with other risks. Some of these risks are addressed briefly below. Potential investors should possess experience of investing in instru-ments that are employed within the scope of the proposed investment policy. Investors should also have a clear picture of the risks involved in invest-ing in the units and should not make a decision to invest until they have fully consulted their legal, tax and financial advisors, auditors or other advisors about (i) the suitability of investing in the units, taking into account their personal financial and tax situation and other circumstances, (ii) the informa-tion contained in this sales prospectus, and (iii) the fund’s investment policy.

It must be noted that investments made by a fund also contain risks in addition to the

opportunities for price increases. The fund’s units are securities, the value of which is determined by the price fluctuations of the assets contained in the fund. Accordingly, the value of the units may rise or fall in com-parison with the purchase price.

No assurance can therefore be given that the investment objectives will be achieved.

Market risk

The price or market performance of financial products depends, in particular, on the perfor-mance of the capital markets, which in turn are affected by the overall economic situation and the general economic and political framework in individual countries. Irrational factors such as sentiment, opinions and rumors have an effect on general price performance, particularly on an exchange.

Credit risk

The credit quality (ability and willingness to pay) of the issuer of a security or money market instrument held directly or indirectly by the fund may subsequently decline. This usually leads to price drops in the individual security in excess of the usual market fluctuations.

Country or transfer risk

A country risk exists when a foreign borrower, despite ability to pay, cannot make payments at all, or not on time, because of the inability or unwillingness of its country of domicile to execute transfers. This means that, for exam-ple, payments to which the fund is entitled may not occur, or be in a currency that is no longer convertible due to restrictions on currency exchange.

Settlement risk

Especially when investing in unlisted securities, there is a risk that settlement via a transfer sys-tem is not executed as expected because a pay-ment or delivery did not take place in time or as agreed.

Legal and tax risk

The legal and tax treatment of funds may change in ways that cannot be predicted or influenced. In the case of a correction with tax consequences that are essentially unfavorable for the investor, changes to the fund’s taxation bases for preced-ing fiscal years made because these bases are found to be incorrect can result in the investor having to bear the tax burden resulting from the correction for preceding fiscal years, even though he may not have held an investment in the invest-ment fund at the time. Conversely, the investor may fail to benefit from an essentially favorable correction for the current or preceding fiscal years during which he held an investment in the investment fund if the units are redeemed or sold before the correction takes place.

In addition, a correction of tax data can result in a situation where taxable income or tax benefits are actually assessed for tax in a different assess-ment period to the applicable one and that this has a negative effect for the individual investor.

5

Currency risk

To the extent the fund invests in assets denomi-nated in currencies other than the fund currency, the fund will receive income, repayments and proceeds from such investments in the respec-tive currency. If the value of these currencies falls in relation to the fund currency, the value of the fund’s assets is reduced.

Custody risk

The custody risk describes the risk resulting from the basic possibility that, in the event of insolvency, violation of due diligence or improper conduct on the part of the Depositary or any sub-depositary, the fund may, in whole or in part and to its detriment, be deprived of access to the investments held in custody.

Company-specific risk

The price performance of the securities and money market instruments held directly or indi-rectly by the fund is also dependent on compa-ny-specific factors, for example on the business situation of the issuer. If the company-specific factors deteriorate, the market value of the indi-vidual security may significantly and persistently decline, even if the market is performing strongly in general.

Concentration risk

Additional risks may arise from a concentration of investments in particular assets or markets. The fund then becomes particularly heavily dependent on the performance of these assets or markets.

Risk of changes in interest rates

Investors should be aware that investing in units may involve interest rate risks. These risks may occur in the event of interest rate fluctuations in the denomination currency of the securities or the fund.

Political risk/Regulatory risk

The fund may invest abroad. This involves the risk of detrimental international political develop-ments, changes in government policy, taxation and other changes in the legal status.

Inflation risk

All assets are subject to a risk of devaluation through inflation.

Key individual risk

The exceptionally positive performance of certain funds during a particular period is also attributable to the abilities of the individuals acting on behalf of such funds, and therefore to the correct decisions made by their respective fund management. Fund management personnel can change, however. New decision-makers might not be as successful.

Change in the investment policy

The risk associated with the fund may change in terms of content due to a change in the invest-ment policy within the range of investments permitted for the fund.

Changes to the management regulations; liquidation or merger

In the management regulations for the fund, the Management Company reserves the right to change the management regulations. In addi-tion, the Management Company may, in accor-dance with the provisions of the management regulations, liquidate the fund entirely or merge it with another fund. For the investor, this entails the risk that the holding period planned by the investor will not be realized.

Credit risk

Investors should be absolutely clear that an investment of this type may involve credit risks. Bonds or debt instruments involve a credit risk with regard to the issuers, for which the issu-er’s credit rating can be used as a benchmark. Bonds or debt instruments floated by issuers with a lower rating are generally viewed as secu-rities with a higher credit risk and greater risk of default on the part of the issuer than those instruments that are floated by issuers with a better rating. If an issuer of bonds or debt instru-ments runs into financial or economic difficul-ties, this can affect the value of the bonds or debt instruments (this value could drop to zero) and the payments made on the basis of these bonds or debt instruments (these payments could drop to zero).

Risk of default

In addition to the general trends on capital markets, the particular performance of each individual issuer also affects the price of an investment. The risk of a decline in the assets of issuers, for example, cannot be eliminated even by the most careful selection of the securities.

Risks connected to derivatives transactions

Buying and selling options, as well as the conclu-sion of futures contracts or swaps, involves the following risks:

– Price changes in the underlying can cause a decrease in the value of the option or futures contract, and even result in a total loss. This can have a negative effect on the value of the fund’s assets. Changes in the value of the asset underlying a swap or total return swap can also result in losses for the fund’s assets.

– Any necessary back-to-back transactions (closing of position) incur costs, which can reduce the value of the fund’s assets.

– The leverage effect of options may alter the value of the fund’s assets more strongly than the direct purchase of underlyings would.

– The purchase of options entails the risk that the options are not exercised because the prices of the underlying assets do not change as expected, meaning that the fund loses the option premium it paid. If options are sold, there is the risk that the fund may be obliged to buy assets at a price that is higher than the current market price, or obliged to deliver assets at a price which is lower than the current market price. In that case, the fund will incur a loss amounting

to the price difference minus the option pre-mium collected.

– Futures contracts also entail the risk that the fund assets may make losses due to market prices not having developed as expected at maturity.

Risk connected to the acquisition of units of investment funds

When investing in units of target funds, it must be taken into consideration that the fund managers of the individual target funds act independently of one another and that therefore multiple target funds may follow investment strategies which are identical or contrary to one another. This can result in a cumulative effect of existing risks, and any opportunities might be offset.

Liquidity risk

Liquidity risks arise when a particular security is difficult to dispose of. In principle, acquisitions for the fund shall only consist of securities that can be sold again at any time. Nevertheless, it may be difficult to sell particular securities at the desired time during certain phases or in partic-ular exchange segments. There is also the risk that securities traded in a rather narrow market segment will be subject to considerable price volatility.

Counterparty risk

When the fund conducts over-the-counter (OTC) transactions, it may be exposed to risks relat-ing to the credit standing of its counterparties and to their ability to fulfill the conditions of the contracts it enters into with them. The fund may consequently enter into futures transactions, options transactions and swap transactions or use other derivative techniques, such as total return swaps, that will subject the fund to the risk of a counterparty not fulfilling its obligations under a particular contract.

In the event that the counterparty becomes bank-rupt or insolvent, the fund may suffer significant losses due to a delay in liquidating positions, including the loss in value of the investments while the fund pursues its rights. Likewise, it is possible that the use of the agreed techniques may be halted, for example due to bankruptcy, ille-gality or changes to the law in comparison with the laws that applied at the time the agreements were concluded.

Funds can also enter into transactions in OTC and interdealer markets, for example. Typically, participants in these markets are not subject to the same financial supervision as participants in regulated markets. A fund that invests in swaps, total return swaps, derivatives, synthetic instruments or other OTC transactions in these markets bears the counterparty credit risk and is also subject to risk of default by the counter-party. These risks can differ significantly from those for transactions in regulated markets, as the latter are safeguarded by means of guaran-tees, daily mark-to-market valuation, daily set-tlement and corresponding segregation, as well as minimum capital requirements. Transactions concluded directly between two counterparties do not generally benefit from this protection.

6

The fund is also subject to the risk that the counterparty will not execute the transaction as agreed due to a disagreement regarding the terms of contract (regardless of whether or not this is in good faith) or due to a credit or liquidity problem. This can lead to losses for the respective fund. This counterparty risk increases for contracts with a longer maturity period, as events may preclude agreement, or if the fund has oriented its transactions to a single counter-party or to a small group of counterparties.

In the event of default by the counterparty, the fund may be subject to adverse market move-ments while replacement transactions are being carried out. The fund can conclude a transaction with any counterparty. It can also conclude an unlimited number of transactions with one coun-terparty. The fact that the fund can conduct trans-actions with any counterparty, the lack of mean-ingful and independent evaluation of the financial characteristics of the counterparty as well as the lack of a regulated market for the conclusion of agreements may increase the loss exposure of the fund.

Risks in connection with the use of securities lending transactions and repurchase agreements

If the counterparty of a securities lending trans-action or repurchase agreement defaults, the fund may suffer a loss due to the fact that the income from the sale of the collateral held by the fund in connection with the securities lend-ing transaction or repurchase agreement is less than the securities lent or sold. In addition, the fund may suffer losses due to bankruptcy or due to similar proceedings against the counterparty of the securities lending transaction or repur-chase agreement or due to any other type of non-fulfillment of the return of the securities, e.g. loss of interest or loss of the respective security as well as default and enforcement costs in relation to the securities lending trans-action or repurchase agreement. It is assumed that the use of a purchase with a repurchase option or of a reverse repurchase agreement and securities lending agreement does not have any substantial influence on the performance of the fund. However, the use of such instruments can have a significant effect, either positive or negative, on the net asset value of the fund.

Investment policy

The fund’s assets shall be invested in compliance with the principle of risk-spreading and within the general investment policy guidelines specified in the special section of the sales prospectus and in accordance with the investment options and restrictions of article 4 of the management reg-ulations.

Performance benchmark

The fund can use a financial index as a perfor-mance benchmark for comparing performance, however it will not try to reproduce the compo-sition of such an index. If a performance index is used for the fund, further information can be found in the special section of the sales prospec-tus. When a financial index is used as part of the fund’s investment strategy, the fund’s investment policy will reflect this approach (see also the

“Use of financial indices” section of this sales prospectus).

Techniques for efficient portfolio management

In accordance with CSSF circular 13/559, tech-niques for efficient portfolio management may be used for the fund. These also include any form of derivatives transactions as well as securities lend-ing transactions and repurchase agreements.

Use of derivatives

The fund may – provided an appropriate risk man-agement system is in place – invest in any type of derivative that is derived from assets that may be purchased for the fund or from financial indices, interest rates, exchange rates or currencies. In particular, this includes options, financial futures contracts and swaps, as well as combinations thereof. Their use need not be limited to hedging the fund’s assets; they may also be part of the investment strategy.

Trading in derivatives is conducted within the con-fines of the investment limits and provides for the efficient management of the fund’s assets, while also regulating investment maturities and risks.

Swaps

The Management Company may conduct the fol-lowing swap transactions for the account of the fund within the scope of the investment princi-ples:

– interest rate swaps, – currency swaps, – equity swaps, – total return swaps or – credit default swaps.

Swap transactions are exchange contracts in which the parties swap the assets or risks under-lying the respective transaction.

Total return swaps

If the fund exercises the opportunity to use total return swaps or other derivatives of the same nature to substantially implement the investment strategy, information on the underlying strategy or the counterparty, for example, is to be found in the special section of the sales prospectus.

Swaptions

Swaptions are options on swaps. A swaption is the right, but not the obligation, to conduct a swap transaction, the terms of which are precisely specified, at a certain point in time or within a certain period.

Credit default swaps

Credit default swaps are credit derivatives that enable the transfer of a volume of potential credit defaults to other parties. As compensation for accepting the credit default risk, the seller of the risk (the protection buyer) pays a premium to its counterparty.

In all other aspects, the information for swaps applies accordingly.

Securitized financial instruments

The Management Company may also acquire the financial instruments described above if they are securitized. Transactions pertaining to finan-cial instruments may also constitute elements of securities (e.g. warrant-linked bonds). The state-ments on opportunities and risks apply accordingly to such securitized financial instruments, but with the condition that the risk of loss in the case of securitized instruments is limited to the value of the security.

OTC derivatives transactions

The Management Company may conduct both derivatives transactions admitted for trading on an exchange or included in another organized market and over-the-counter (OTC) transactions. It shall include a process for accurate and inde-pendent assessment of the value of OTC deriva-tive instruments.

Securities lending transactions and repurchase agreements

The fund is permitted to lend securities from its assets to a counterparty for a specified period and in return for appropriate market compensa-tion. The fund ensures that all securities trans-ferred within the framework of a securities lend-ing transaction can be transferred back at any time and that all securities lending agreements entered into can be terminated at any time.

a) Securities lending transactions

Unless further restricted by the investment policies of the fund as described in the spe-cial section below, the fund is permitted to conclude securities lending transactions. The respective restrictions are to be found in the currently applicable version of CSSF circu-lar 08/356.

Those transactions may be entered into for one or more of the following aims: (i) reduc-tion of risk, (ii) reduction of cost and (iii) genera-tion of additional capital or income with a level of risk which is consistent with the risk pro-file of the Fund and with the risk diversification rules applicable to it. Those transactions may be carried out for 100% of the assets of the fund provided (i) that their volume is always kept at an appropriate level or that it is possi-ble to demand the return of the securities lent in a manner that enables the fund to meet its redemption obligations at all times and (ii) that these transactions do not jeopardize the man-agement of the fund’s assets in accordance with its investment policy. The risks associated with these transactions shall be controlled within the framework of the risk management process of the Management Company.

The fund may only enter into securities lend-ing transactions provided that it complies with the following rules:

(i) The fund may only lend securities through a standardized system organized by a rec-ognized clearing institution or through a first class financial institution subject to prudent supervision rules which are recognized by the CSSF as equivalent to

7

those laid down in Community law and specializing in this type of transaction.

(ii) The borrower must be subject to prudent supervision rules considered by the CSSF as equivalent to those prescribed by Community law.

(iii) The counterparty risk vis-à-vis a single counterparty (which, for the avoidance of doubt, may be reduced by the use of collateral) arising from one or more securities lending transaction(s) may not exceed 10% of the assets of the fund when the counterparty is a financial insti-tution falling within article 41 (1) (f) of the Law of 2010, or 5% of its assets in all other cases.

The Management Company shall disclose the global valuation of the securities lent in the annual and semiannual reports.

Securities lending may also be conducted synthetically (“synthetic securities lend-ing”). In a synthetic securities loan, a secu-rity contained in the fund is sold to a coun-terparty at the current market price. The sale is, however, subject to the condition that the fund simultaneously receives from the coun-terparty a securitized unleveraged option giving the fund the right to demand deliv-ery at a later date of securities of the same kind, quality and quantity as the sold secu-rities. The price of the option (the “option price”) is equal to the current market price received from the sale of the securities less (a) the securities lending fee, (b) the income (e.g., dividends, interest payments, corpo-rate actions) from the securities that can be demanded back upon exercise of the option and (c) the exercise price associated with the option. The option will be exercised at the exercise price during the term of the option. If the security underlying the syn-thetic securities lending is to be sold during the term of the option in order to imple-ment the investment strategy, such a sale may also be executed by selling the option at the then prevailing market price less the exercise price.

Securities lending transactions may also be entered into with respect to individual unit classes, taking into account their respective specific characteristics and/or investor pro-files, with any right to income and collateral under such securities lending transactions arising at the level of the relevant unit class.

b) Repurchase agreements

Unless otherwise provided for in the spe-cial section below, the fund may (i) enter into repurchase agreement transactions which consist of the purchase and sale of securities with a clause reserving the seller the right or the obligation to repurchase from the buyer the securities sold at a price and term spec-ified by the two parties in their contractual arrangement and (ii) enter into reverse repur-chase agreement transactions, which con-sist of a forward transaction at the maturity of which the seller (counterparty) has the obli-gation to repurchase the securities sold and

the fund the obligation to return the securi-ties received under the transaction (collec-tively, the “repurchase agreements”).

The fund can act either as buyer or seller in repurchase agreement transactions or a series of continuing repurchase agreement transactions. Its involvement in such trans-actions is, however, subject to the following rules:

(i) The fund is only permitted to buy or sell securities as part of a repurchase agree-ment provided the counterparty to this transaction is subject to prudential super-vision rules considered by CSSF as equiv-alent to those laid down in Community law.

(ii) The counterparty risk vis-à-vis a single counterparty (which, for the avoidance of doubt, may be reduced by the use of collateral) arising from one or more repur-chase agreements may not exceed 10% of the assets of the fund when the coun-terparty is a financial institution falling within article 41 (1) (f) of the Law of 2010, or 5% of its assets in all other cases.

(iii) During the term of a repurchase agree-ment in which the fund acts as buyer, the fund is only permitted to sell the securi-ties which are the subject of the contract after the counterparty has exercised its right to repurchase these securities or after the deadline for the repurchase has expired, unless the fund has other means of coverage.

(iv) The securities purchased by the fund as part of a repurchase agreement must meet the investment policy and invest-ment restrictions of the fund and must be limited to:

– short-term bank certificates or money market instruments as defined in Directive 2007/16/EC of March 19, 2007;

– bonds issued or guaranteed by a member state of the OECD or by their local authorities or by suprana-tional institutions and authorities at EU, regional or international level;

– units of a UCI investing in money mar-ket instruments, calculating a daily net asset value and which have a rat-ing of AAA or its equivalent;

– bonds issued by non-governmental issuers offering an adequate liquid-ity; and

– equities listed or traded on a regulated market of a member state of the Euro-pean Union or on a stock exchange of a member state of the OECD, provided that these equities are included in a major index.

The Management Company shall disclose the total amount of the open repurchase agreement transactions on the date of

reference of its annual and semiannual reports.

Repurchase agreement transactions may also be entered into with respect to indi-vidual unit classes, taking into account their respective specific characteristics and/or investor profiles, with any right to income and collateral under such repur-chase agreement transactions arising at the level of the relevant unit class.

Collateral management for transactions with OTC derivatives and techniques for efficient portfolio management

For transactions with OTC derivatives and for reverse repurchase agreement transactions, the fund may receive collateral to reduce the counter-party risk. Within the scope of its securities lending transactions, the fund must receive collateral, the value of which, during the duration of the agree-ment, must be equal to at least 90% of the global valuation of the securities lent (taking into account interest, dividends, other eventual rights and any agreed discounts or minimum transfer amounts).

As a guarantee for the obligations, the fund can accept all collateral that corresponds to the regula-tions of CSSF circulars 08/356, 11/512 and 13/559.

I. In the case of securities lending, such collat-eral must be received prior to or simultane-ously with the transfer of the securities lent. When the securities are lent through inter-mediaries, the transfer of the securities lent may be effected prior to receipt of the col-lateral, if the relevant intermediary ensures proper completion of the transaction. Said intermediary may provide collateral in lieu of the borrower.

II. Collateral for securities lending transactions, reverse repurchase agreement transac-tions and transactions with OTC derivatives (except currency forward transactions) must, be provided in one of the following forms:

– liquid assets such as cash, short-term bank deposits, money market instru-ments as defined in Directive 2007/16/EC of March 19, 2007, letters of credit and guarantees at first demand issued by a first class credit institution not affiliated to the counterparty, or bonds issued or guaranteed by a member state of the OECD or by their local authorities or by supranational insti-tutions and bodies of a community, regional or world-wide scope;

– units of a UCI investing in money market instruments, calculating a daily net asset value and which have a rating of AAA or its equivalent;

– units issued by a UCITS investing mainly in bonds/equities mentioned in the fol-lowing two indents;

– bonds issued or guaranteed by first class issuers offering an adequate liquidity; or

– equities admitted to or traded on a reg-ulated market of a member state of the

8

European Union or on a stock exchange of a member state of the OECD, pro-vided that these equities are included in a major index.

III. The collateral given under any form other than cash or units of a UCI/UCITS shall be issued by an entity not affiliated to the coun-terparty.

IV. When the collateral given in the form of cash exposes the fund to a credit risk vis-à-vis the trustee of this collateral, such exposure shall be subject to the 20% limitation as laid down in article 43 (1) of the Law of 2010. More-over such cash collateral shall not be held in safekeeping by the counterparty unless it is legally protected from the consequences of default of the latter.

V. The collateral given in a form other than cash shall not be held in safekeeping by the counterparty, except if it is adequately segre-gated from the latter’s own assets.

VI. If collateral fulfills a series of criteria such as standards for liquidity, valuation, credit standing of the issuer, correlation and diversification, it can be offset against the gross commitment of the counterparty. If collateral is offset, its value can be reduced by a percentage (a “discount” or “hair-cut”) depending on its price volatility. This discount is intended to compensate for short-term fluctuations in the value of the commitment and the collateral. Discounts are generally not applied to cash collateral.

The criterion of adequate diversification in relation to issuer concentration is deemed fulfilled if the fund, as part of efficient port-folio management or for transactions with OTC derivatives, receives from the counter-party a collateral basket whereby the total value of the open positions with respect to a particular issuer does not exceed 20% of the net asset value. When the fund has different counterparties, the different collateral bas-kets should be aggregated to calculate the 20% limit for the total value of open posi-tions with respect to a single issuer.

VII. For assets that it accepts as collateral, the Management Company follows a strategy for valuing the discounts (“haircut strat-egy”). The discounts applied to the collateral are based either on:

a) the credit worthiness of the counter-party,

b) the liquidity of the collateral,

c) the price volatility of the collateral,

d) the credit standing of the issuer, and/or

e) the country or market in which the collat-eral is traded.

For collateral furnished in the context of OTC derivatives transactions, a discount of at least 2% is generally applied, e.g. for short-term government bonds with excel-lent credit quality. The value of such col-

lateral must therefore exceed the value of the secured receivable by at least 2% and thereby reach a degree of overcollateraliza-tion of at least 102%. A correspondingly higher discount of currently up to 33% (and therefore a higher degree of overcollateral-ization of 133%) is set for securities with longer maturities or for securities of issuers with lower ratings. Overcollateralization in the context of OTC derivative transactions is generally within the following range:

OTC derivatives transactionsOvercollateralization 102% to 133%

In the context of securities lending trans-actions, when the issuer has an excellent credit standing and the credit quality of the collateral is excellent, the collateral may occasionally be recognized in full, whereas higher discounts may be applied for equities and other securities with a lower credit qual-ity, taking into account the credit standing of the counterparty. Overcollateralization in the context of securities lending transactions generally takes place according to the fol-lowing gradation:

Securities lending transactionsDegree of overcollateralization for government bonds with excellent credit quality 103% to 105%

Degree of overcollateralization for low investment grade government bonds 103% to 115%

Degree of overcollateralization for corporate bonds with excellent credit quality 105%

Degree of overcollateralization for low investment grade corporate bonds 107% to 115%

Degree of overcollateralization for blue chips and mid caps 105%

VIII. The discounts used are checked for their adequacy at regular intervals, at least yearly, and adjusted accordingly if necessary.

IX. The fund (or its delegates) shall conduct a valuation of the collateral received on a daily basis. In case the value of the collateral already granted appears to be insufficient in comparison with the amount to be covered, the counterparty shall provide additional col-lateral at very short notice. If appropriate, safety margins shall apply in order to take into consideration exchange risks or market risks inherent to the assets accepted as collateral.

X. The fund shall ensure that it is able to claim its rights on the collateral in case of the occurrence of an event requiring the exe-cution thereof, meaning that the collateral shall be available at all times, either directly or through the intermediary of a first class financial institution or a wholly-owned sub-sidiary of this institution, in such a manner that the fund is able to appropriate or realize the assets given as collateral, without delay, if the counterparty does not comply with its obligation to return the securities lent.

XI. During the term of the agreement, the collat-eral cannot be sold or given as a security or

pledged, except if the fund has other means of coverage.

XII. A fund receiving collateral for at least 30% of its assets should examine the associated risk within the framework of regular stress tests that should be carried out under normal and exceptional liquidity conditions so that the consequences of changes to the market value and the liquidity risk attached to the collateral can be assessed. The strategy for liquidity stress tests should contain provisions for the following aspects:

a) concept for analyzing the stress test sce-nario, including calibration, certification and sensitivity analysis;

b) empirical approach for estimating con-sequences, including the back-testing of liquidity risk assessments;

c) reporting frequency and reporting limits/loss tolerance threshold(s);

d) measures for stemming losses, including haircut strategy and gap risk protection.

Use of financial indices

Where specified in the special section of this sales prospectus, the objective of the investment policy may be to replicate a certain index or a leveraged index. This is subject to the condition that

– the composition of the index is sufficiently diversified;

– the index represents an adequate benchmark for the market to which it refers;

– the index is published in an appropriate man-ner.

If an index is replicated, the frequency of the adjustment of the index composition depends on the index to be replicated. As a rule, the adjust-ment takes place on a half-yearly, quarterly or monthly basis. The replication and adjustment of the composition of the index can lead to costs that may reduce the value of the fund’s net assets.

Risk management

The fund shall include a risk management pro-cess that enables the Management Company to monitor and measure at any time the risk of the positions and their contribution to the overall risk profile of the portfolio.

The Management Company monitors the fund in compliance with the requirements of regula-tion 10-04 of the Commission de Surveillance du Secteur Financier (“CSSF”) and the Direc-tives issued from time to time by the Luxem-bourg or European authorities, in particular the CSSFF circular 11-512 of May 30, 2011, and the “Guidelines on Risk Measurement and the Cal-culation of Global Exposure and Counterparty Risk for UCITS” from the Committee of Euro-pean Securities Regulators (CESR/10-788) and CSSF circular 13-559 of February 18, 2013. The Management Company ensures for the fund that the total risk related to derivative financial instruments in accordance with article 42 (3)

9

of the Law of 2010, does not exceed 100% of the fund’s net assets and that the market risk of the fund does not exceed the market risk of the reference portfolio, which does not contain derivatives, by more than 200% (in the case of a relative VaR approach) or by more than 20% (in the case of an absolute VaR approach).

The risk management approach applied to the fund is detailed in the special section of the sales prospectus for the fund.

The Management Company generally strives to ensure that the level of investment of the fund is not increased by more than twice the value of the fund’s assets by the use of derivatives (hereinaf-ter “leverage effect”), unless otherwise specified in the special section of the sales prospectus. The leverage effect is calculated using the sum of the notional approach (absolute (notional) amount of each derivative divided by the current net value of the portfolio). When calculating the leverage effect, the portfolio’s derivatives are taken into account. Collateral is not currently reinvested and is thus not taken into account.

However, this leverage effect fluctuates depend-ing on market conditions and/or changes to posi-tions (including to protect the fund against unfa-vorable market movements). For this reason, the targeted ratio could be exceeded at some point in spite of constant monitoring by the Management Company. The expected leverage should not be viewed as an additional risk limit for the fund.

In addition, the option to borrow 10% of its net assets is available for the fund, provided that this borrowing is temporary and the borrowing pro-ceeds are not used for investment purposes.

An overall increased commitment can thus sig-nificantly increase both the opportunities and the risks associated with an investment (see in par-ticular the risk warnings in the “Risks connected to derivative transactions” section).

Potential conflicts of interest

Within the scope of and in compliance with the applicable procedures and measures for conflict management, the Management Com-pany, Management Company Managing Board Members and Supervisory Board Members, the management, the fund manager, the designated sales agents and persons authorized to carry out the distribution, the Depositary, if applicable the investment advisor, the administrator, the unitholders, as well as all subsidiaries, affiliated companies, representatives or agents of the aforementioned entities and persons (“Associ-ated Persons”):

1. conduct among themselves, or on behalf of the fund, financial and banking transactions or other transactions such as derivative transac-tions, securities lending transactions or secu-rities repurchase transactions or enter into the corresponding contracts, including those that are directed at investments in securities by the fund or at investments by an Associ-ated Person in a company or undertaking, such investment being a constituent part of the fund’s assets, or be involved in such con-tracts or transactions;

2. for their own accounts or for the accounts of third parties, invest in units, securities or assets of the same type as the components of the fund and trade in them;

3. in their own names or in the names of third parties, participate in the purchase or sale of securities or other assets in or from the fund via the Management Company or jointly with the Management Company or the Depositary or a subsidiary, an affiliated company, repre-sentative or agent of such.

Assets of the fund in the form of liquid assets or securities may be deposited with an Associated Person in accordance with the legal provisions governing the Depositary. Liquid assets of the fund may be invested in certificates of deposit issued by an Associated Person or in bank depos-its offered by an Associated Person. Banking or comparable transactions may also be conducted with or through an Associated Person. Companies in the Deutsche Bank Group and/or employees, representatives, affiliated companies or subsid-iaries of companies in the Deutsche Bank Group (“DB Group Members”) may be counterparties in the Management Company’s derivatives trans-actions or derivatives contracts (“Counterparty”). Furthermore, in some cases a counterparty may be required to evaluate such derivatives transac-tions or derivatives contracts. Such evaluations may constitute the basis for calculating the value of particular assets of the fund. The Management Company is aware that DB Group Members may possibly be involved in a conflict of interest if they act as counterparty and/or provide such informa-tion. The evaluation will be adjusted and carried out in a manner that is verifiable. However, the Management Company believes that such con-flicts can be handled appropriately and assumes that the counterparty possesses the aptitude and competence to perform such evaluations.

In accordance with the respective terms agreed, DB Group Members may act as Managing Board Members or Supervisory Board Members, sales agents and sub-agents, depositaries, fund manag-ers or investment advisors, and may offer to pro-vide financial and banking transactions to the Man-agement Company. The Management Company is aware that conflicts of interest may arise due to the functions that DB Group Members perform in relation to the Management Company. In respect of such eventualities, each DB Group Member has undertaken to endeavor, to a reasonable extent, to resolve such conflicts of interest equitably (with regard to the Members’ respective duties and responsibilities), and to ensure that the interests of the Management Company and of the unithold-ers are not adversely affected. The Management Company is of the view that DB Group Members possess the required aptitude and competence to perform such duties.

The Management Company believes that the interests of the Management Company might conflict with those of the entities mentioned above. The Management Company has taken reasonable steps to avoid conflicts of interest. In the event of unavoidable conflicts of interest, the Management Company will endeavor to resolve such conflicts in favor of the fund.

For the fund, transactions involving the fund assets may be conducted with or between Asso-

ciated Persons, provided that such transactions are in the best interests of the investors.

Combating money laundering

The transfer agent may demand such proof of identity as it deems necessary in order to comply with the laws applicable in Luxembourg for com-bating money laundering. If there is doubt regard-ing the identity of the investor or if the transfer agent does not have sufficient details to establish the identity, the transfer agent may demand fur-ther information and/or documentation in order to be able to unequivocally establish the identity of the investor. If the investor refuses or fails to sub-mit the requested information and/or documen-tation, the transfer agent may refuse or delay the transfer to the Company’s register of unitholders of the investor’s data. The information submitted to the transfer agent is obtained solely to comply with the laws for combating money laundering.

The transfer agent is, in addition, obligated to examine the origin of money collected from a financial institution unless the financial institution in question is subject to a mandatory proof-of-identity procedure that is the equivalent of the proof-of-identity procedure provided for under Luxembourg law. The processing of subscription applications can be suspended until such a time as the transfer agent has properly established the origin of the money.

Initial or subsequent subscription applications for units can also be made indirectly, i.e., via the sales agents. In this case, the transfer agent may dispense with the aforementioned required proof of identity under the following circumstances or under the circumstances deemed to be sufficient in accordance with the money laundering laws applicable in Luxembourg:

– if a subscription application is being pro-cessed via a sales agent that is under the supervision of the responsible authorities whose regulations provide for a proof-of-identity procedure for customers that is equivalent to the proof-of-identity procedure provided for under Luxembourg law for com-bating money laundering, and the sales agent is subject to these regulations;

– if a subscription application is being pro-cessed via a sales agent whose parent company is under the supervision of the responsible authorities whose regulations provide for a proof of identity procedure for customers that is equivalent to the proof of identity procedure in accordance with Lux-embourg law and serves to combat money laundering, and if the corporate policy or the law applicable to the parent company also imposes the equivalent obligations on its subsidiaries or branches.

In the case of countries that have ratified the rec-ommendations of the Financial Action Task Force (FATF), it is assumed that the respective respon-sible supervisory authorities in these countries have imposed regulations for implementing proof-of-identity procedures for customers on physical persons or legal entities operating in the financial sector and that these regulations are the equiva-lent of the proof-of-identity procedure required in accordance with Luxembourg law.

10

The sales agents can provide a nominee service to investors that acquire units through them. Investors may decide at their own discretion whether or not to take up this service, which involves the nominee holding the units in its name for and on behalf of investors; the latter are entitled to demand direct ownership of the units at any time. Notwithstanding the preceding provi-sions, the investors are free to make investments directly with the Management Company without taking up the nominee service.

Data protection

The personal data of investors provided in the application forms, as well as the other informa-tion collected within the scope of the business relationship with the Management Company are recorded, stored, compared, transmitted and otherwise processed and used (“processed”) by the Management Company, and/or other entities of Deutsche Asset & Wealth Management, the Depositary and the financial intermediaries of the investors. The data is used for the purposes of account management, examination of mon-ey-laundering activities, determination of taxes pursuant to EU Directive 2003/48/EC on the tax-ation of interest payments and for the develop-ment of business relationships.

For these purposes, the data may also be for-warded to businesses appointed by the Manage-ment Company in order to support the activities of the Management Company (for example, client communication agents and paying agents).

Legal status of investors

The money invested in the fund is invested by the Management Company in its own name for the collective account of the investors (the “unithold-ers”) in securities, money market instruments and other permissible assets, based on the principle of risk-spreading. The money invested in a fund and the assets purchased with the money constitute the fund’s assets, which are kept separate from the Management Company’s own assets.

Unitholders as joint owners have an interest in the fund’s assets in proportion to the number of units they hold. Their rights are represented by bearer units and securitized in the form of global certificates. All fund units have the same rights.

Bearer units represented by global certificates

The Management Company may resolve to issue bearer units that are represented by one or sev-eral global certificates.

These global certificates are issued in the name of the Management Company and deposited with the clearing agents. The transferability of the bearer units represented by a global certificate is subject to the respectively applicable laws, and to the regulations and procedures of the clear-ing agent undertaking the transfer. Investors receive the bearer units represented by a global certificate when they are posted to the securities accounts of their financial intermediaries, which in turn are held directly or indirectly with the clearing agents. Such bearer units represented by a global certificate are transferable according to and in compliance with the provisions con-

tained in this sales prospectus, the regulations that apply on the respective exchange and/or the regulations of the respective clearing agent. Unitholders that do not participate in such a sys-tem can transfer bearer units represented by a global certificate only via a financial intermediary participating in the settlement system of the cor-responding clearing agent.

Payments of distributions for bearer units repre-sented by global certificates take place by way of credits to the accounts at the relevant clear-ing agent of the financial intermediaries of the unitholders.

The law of July 28, 2014, relating to the freezing of bearer shares and units (the “Law of 2014”) constituted a new legal provision in relation to bearer shares and units (the “units”). The Law of 2014 stipulates the mandatory filing and registration of the units placed with the nomi-nated Depositary by Luxembourg public limited companies and partnerships limited by shares, as well as investment funds (“fonds commun de placement”). The Depositary appointed under the terms of this law was Deutsche Bank Luxembourg S.A., 2, Boulevard Konrad Adenauer, 1115 Luxembourg, Luxembourg.

If the units have not been filed and registered by February 18, 2016, the Law of 2014 requires the units to be deleted. The deletion of these units will lead to a capital reduction. The correspond-ing amount will be placed with the “Caisse de Consignation” until a person who can establish legal ownership demands reimbursement.

This also relates to actual units of the fund in cir-culation bearing the name “DM Reserve”.

Calculation of the NAV per unit

In order to calculate the net asset value per unit, the value of the assets belonging to the fund less its liabilities is calculated on each bank business day in Luxembourg and Frankfurt/Main (valuation date) and the result is divided by the number of units outstanding. A bank business day is any day (excluding Saturdays and Sundays) on which commercial banks are open and payments are processed in Luxembourg and Frankfurt/Main, Germany.

Particulars on the calculation of the NAV per unit and on asset valuation are provided in the man-agement regulations.

At this time, the Management Company and the Depositary will refrain from calculating the NAV per unit on public holidays that are bank busi-ness days in a country that is significant for the valuation date, as well as on December 24 and December 31 of each year. Any calculation of the net asset value per unit that deviates from this specification will be published in appropri-ate newspapers, as well as on the Internet at www.dws.lu.

Issue of units

Fund units are issued on each valuation date at their net asset value per unit plus the initial sales charge payable by the purchaser for the benefit of the Management Company. The initial sales charge may be retained in whole or in part by interme-

diaries as remuneration for sales services. Where units are issued in countries where stamp duties or other charges apply, the issue price increases accordingly.

Fund units may also be issued as fractional units, with up to three places after the decimal point. Unit fractions are rounded up or down to the near-est thousandth. Such rounding may be to the ben-efit of either the respective unitholder or the fund.

Newly subscribed units are only issued to the investor upon receipt of payment by the Deposi-tary or the approved correspondent banks. From a bookkeeping standpoint, however, the corre-sponding units are already taken into account in the calculation of the net asset value on the value date following the corresponding securities settlement, and can be canceled until receipt of payment. Insofar as an investor’s units must be canceled due to failure to pay or delayed payment of these units, it is possible for the fund to incur a loss in value.

The Management Company is authorized to issue new units continuously. Nevertheless, the Management Company reserves the right to suspend or permanently discontinue the issue of units. In this instance, payments already made will be reimbursed immediately. Unitholders will be informed immediately of the suspension and resumption of the issue of units.

Units can be purchased from the Management Company and via the paying agents. If the Man-agement Company no longer issues new units, it is only possible to purchase units from existing holders.

An example of calculating the issue price is pre-sented below:

Net assets EUR 1,000,000.00÷ Number of units

outstanding on the reference date 10.000,00

Net asset value per unit EUR 100.00+ Initial sales charge

(e.g., 5%) EUR 5.00Issue price EUR 105.00

Redemption of units

Fund units are redeemed on each valuation date at their net asset value less the redemption fee payable by the unitholder. A redemption fee is not charged at this time. Where units are redeemed in countries where stamp duties or other charges apply, the redemption price decreases accordingly.

In the event of large-scale applications for redemp-tion, the Management Company reserves the right, with the prior consent of the Depositary, to redeem units at the applicable NAV only after it has sold the corresponding assets promptly, yet always acting in the best interests of the unitholders.

Units can be returned to the Management Com-pany and to the sales and paying agents. Any other payments to unitholders are also made through these offices.

An example of calculating the redemption price is presented below:

11

Net assets EUR 1,000,000.00÷ Number of units outstanding on the reference date 10.000,00Net asset value per unit EUR 100.00- Redemption fee (e.g., 2.5%) EUR 2,50Redemption price EUR 97.50

The Management Company may, at its sole discre-tion, restrict or prohibit the ownership of units of the fund by unauthorized persons (“Unauthorized Persons”). Unauthorized persons are private indi-viduals, partnerships or corporations that are not authorized, at the sole discretion of the Manage-ment Company, to subscribe or hold units of the fund or, where applicable, of a particular sub-fund or of a particular unit class (i) if, in the opinion of the Management Company, such a unitholding might be detrimental to the fund, (ii) if this might result in the violation of laws or regulations appli-cable within or outside of Luxembourg, (iii) if this might result in the fund suffering adverse tax, legal or financial consequences that it otherwise would not have faced, or (iv) if the aforementioned per-sons or companies do not meet the prerequisites set for investors as regards the acquisition of the units.

The Management Company may require investors to provide any information or documents that it deems necessary in order to be able to determine whether the beneficial owner of the units is (i) an unauthorized person, (ii) a U.S. person or (iii) a per-son that holds units but does not meet the neces-sary prerequisites.

If the Management Company receives knowl-edge at any time that units are being held ben-eficially by persons identified under (i), (ii) and (iii) above (irrespective of whether they are sole or joint owners) and if the relevant person does not respond appropriately to a request by the Management Company to sell its units and to provide proof of such sale to the Management Company within 30 calendar days following issuance by the Management Company of such a request, the Management Company may, at its own discretion, forcibly redeem the units at the redemption price. Such forced redemption takes place, in accordance with the terms and conditions applicable for the units, immediately following the close of business on the date indi-cated by the Management Company in its corre-sponding notice to the Unauthorized Person, and such investors are no longer considered owners of these units.

Market timing and short-term trading

The Management Company prohibits all practices connected with market timing and short-term trading and reserves the right to refuse orders if it suspects that such practices are being applied. In such cases, the Management Company will take all measures necessary to protect the other inves-tors in the fund.

Late trading

Late trading occurs when an order is accepted after the close of the relevant acceptance deadlines on the respective valuation date, but is executed at that same day’s price based on the net asset value.

The practice of late trading is not permitted as it violates the conditions of the sales prospectus of the fund, under which the price at which an order placed after the order acceptance limit is executed is based on the next valid net asset value per unit.

Publication of the issue and redemption prices

The current issue and redemption prices and all other information for unitholders may be requested at any time at the registered office of the Management Company and from the paying agents. In addition, the issue and redemption prices are published in every country of distri-bution through appropriate media (such as the Internet, electronic information systems, news-papers, etc.). Neither the Management Company nor the paying agents shall be liable for any errors or omissions with respect to the publication of prices.

Costs and services received

The fund shall pay the Management Company an all-in fee on the net assets of the fund based on the NAV per unit calculated on the valuation date. The amount of the all-in fee is defined in the respective special section of the sales pro-spectus. This all-in fee shall in particular serve as compensation for investment management, fund management, the distribution of the fund and the services of the Depositary. The all-in fee shall generally be withdrawn from the fund at the end of each month. Aside from the all-in fee, the fol-lowing costs may be charged to the fund:

– all of the taxes charged to the assets of the fund and to the fund itself (especially the taxe d’abonnement), as well as any taxes that may arise in connection with administrative and custodial costs;

– any costs that may arise in connection with the acquisition and disposal of assets;

– extraordinary costs (e.g., court costs) that may be incurred in order to protect the inter-ests of unitholders of the fund; the Manage-ment Company shall decide in each individual case whether or not to assume such costs and will report these separately in the annual report;

– costs for informing the fund investors by means of a durable medium, with the excep-tion of costs for informing the investors in the case of a fund merger and in the case of measures related to accounting errors in determining the NAV or when contravening investment limits.

In addition, a performance-based fee may be payable, the amount of which is also specified in the respective special section of the sales pro-spectus.

Investment in units of target funds

Investments in target funds may lead to dupli-cate costs, as fees are incurred at the level of the respective fund as well as at the level of a target fund. In conjunction with the acquisition of target fund units, the following types of fees are to be borne, directly or indirectly, by the fund’s investors:

– the management fee/all-in fee of the target fund;

– the performance-based fees of the target fund;

– the initial sales charges and redemption fees of the target fund;

– reimbursements of expenses of the target fund;

– other costs.

The initial sales charges and redemption fees that have been charged to the fund in the reporting period for the acquisition and redemption of units in target funds shall be disclosed in the annual and semiannual reports. Furthermore, the annual and semiannual reports will disclose the remuneration charged to the fund by another company as the management fee/all-in fee for the target fund units held in the fund.

If the fund’s assets are invested in units of a tar-get fund that is managed directly or indirectly by the same Management Company or by another company that is affiliated with the Management Company by virtue of joint management or con-trol, or by material direct or indirect shareholding, the Management Company or the other company will not charge to the fund’s assets any initial sales charges or redemption fees for the acquisition or redemption of units of this other fund.

The share of the management fee or all-in fee to be attributed to the units of affiliated fixed assets (duplicate costs or difference method) is indicated in the special section of the sales prospectus.

Income arising from the use of securities lending transactions and repurchase agreements shall in principle – less direct and indirect operational costs – flow into the fund’s assets. The Manage-ment Company shall be entitled to charge a fee for initiating, preparing and implementing such agreements. The Management Company shall receive a flat fee for initiating, preparing and implementing securities lending transactions (including synthetic securities lending trans-actions) and securities repurchase agreement transactions for the account of the fund amount-ing to up to 40% of the income from these transactions. The Management Company shall bear the costs which arise in connection with preparing and implementing such transactions, including any fees payable to third parties (e.g., the transaction costs payable to the Depositary as well as the costs for using special information systems to ensure best execution).

With regard to trading activity for the investment fund, the Management Company is entitled to make use of valuable benefits that are offered by brokers and traders and that are used by the Man-agement Company to make investment decisions in the interests of the unitholders. These services include direct services offered by brokers and traders themselves, such as research and financial analyses, and indirect services such as market and price information systems.

The specified costs are listed in the annual reports.

The Management Company usually passes on some of its management fee to intermediaries.

12

This is paid as remuneration for sales services performed on an agency basis. This may con-stitute a substantial amount. The annual report contains additional information on this. The Man-agement Company does not receive any reim-bursement of the fees and expense reimburse-ments payable to the Depositary and third parties out of the fund’s assets. Valuable benefits offered by brokers and traders, which the Company uses in the interests of investors, shall not be affected (see the sections entitled “Buy and sell orders for securities and financial instruments” and “Com-mission sharing”).

In addition to the aforementioned costs, the investor may incur additional costs that are con-nected to the tasks and services of local sales agents, paying agents or similar agents. These costs shall not be borne by the fund’s assets, but directly by the investor.

Repayment to certain investors of management fees collected

The Management Company may, at its discretion, agree with individual investors the partial repay-ment to them of the management fees collected. This can be a consideration especially in the case of institutional investors which invest large amounts directly for the long term. The “Institutional Sales” division at Deutsche Asset & Wealth Management Investment S.A. is responsible for these matters.

Total expense ratio

The total expense ratio (TER) is defined as the proportion of the fund’s expenditures to the aver-age assets of the fund, excluding accrued trans-action costs. The effective TER is calculated annu-ally and published in the annual report.

Buy and sell orders for securities and financial instruments

The Management Company generally submits buy and sell orders for securities and financial instruments directly to brokers and traders for the account of the fund’s assets. It concludes agree-ments with these brokers and traders under customary market conditions that comply with first-rate execution standards. When selecting the broker or trader, the Management Company takes into account all relevant factors, such as the credit rating of the broker or trader and the quality of the market information, the analyses, as well as the execution capacities provided.

Moreover, the Management Company currently accepts and concludes agreements in which it can take advantage of and utilize valuable benefits offered by brokers and traders. The Management Company has the right to retain these services, which include services provided by brokers and traders directly (for more information, see the provi-sion in the management regulations – special sec-tion – dealing with the reimbursement of the fees and expenses). These direct services include par-ticular advice regarding the advisability of trading an asset or its valuation, analyses and consultation services, economic and political analyses, portfo-lio analyses (including valuation and performance measurement), market analyses as well as indirect services, such as market and price information sys-tems, information services, computer hardware and software or any other options for gathering