Embed Size (px)

Citation preview

Industry Perspectives Panel Discussion

IEAGHG International CCS Summer School 18th – 23rd July 2011

Champaign, Illinois, USA Locally hosted by STEP and MGSC

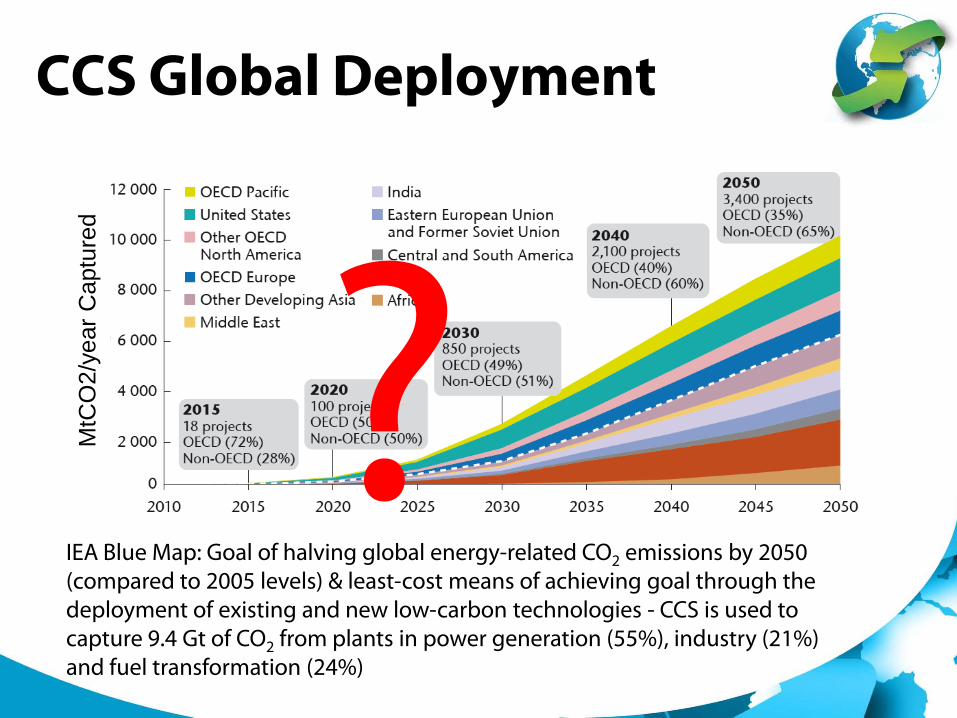

CCS Global Deployment M

tCO

2/ye

ar C

aptu

red

IEA Blue Map: Goal of halving global energy-related CO2 emissions by 2050 (compared to 2005 levels) & least-cost means of achieving goal through the deployment of existing and new low-carbon technologies - CCS is used to capture 9.4 Gt of CO2 from plants in power generation (55%), industry (21%) and fuel transformation (24%)

Philip Sharman Alstom

© ALSTOM 2011. All rights reserved. Information contained in this document is indicative only. No representation or warranty is given or should be relied on that it is complete or correct or will apply to any particular project. This will depend on the technical and commercial circumstances. It is provided without liability and is subject to change without notice. Reproduction, use or disclosure to third parties, without express written authority, is strictly prohibited.

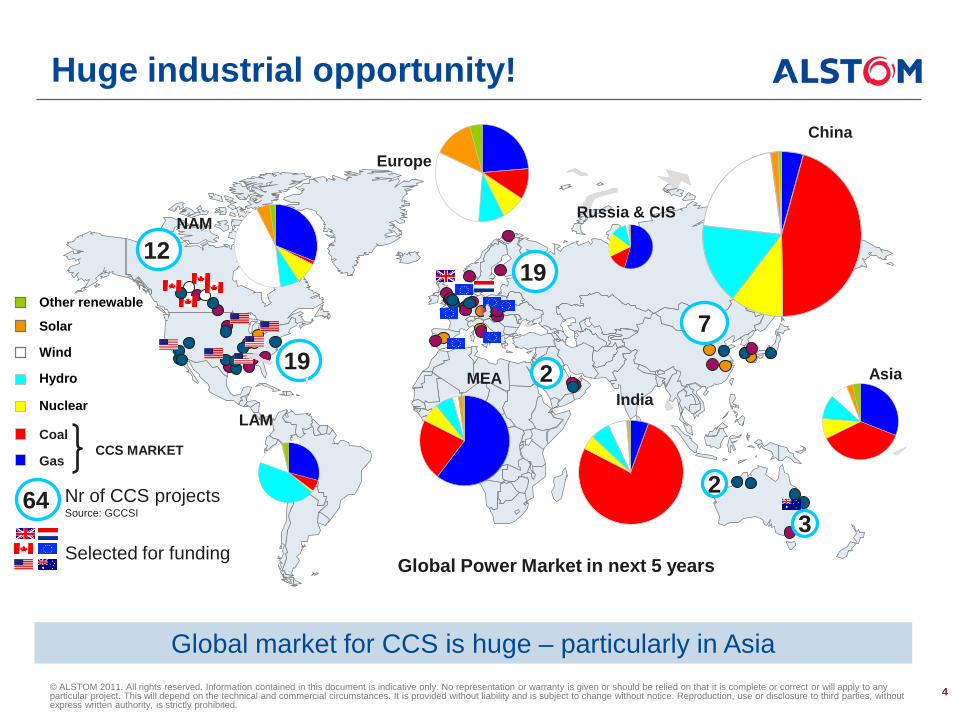

Global market for CCS is huge – particularly in Asia

Selected for funding

12

19

19

2

7

2

3

Asia

China

India

Russia & CIS

Europe

MEA

NAM

LAM

Global Power Market in next 5 years

64 Nr of CCS projects Source: GCCSI

Wind

Hydro

Nuclear

Coal

Gas

Solar

Other renewable

Huge industrial opportunity!

CCS MARKET

4

© ALSTOM 2011. All rights reserved. Information contained in this document is indicative only. No representation or warranty is given or should be relied on that it is complete or correct or will apply to any particular project. This will depend on the technical and commercial circumstances. It is provided without liability and is subject to change without notice. Reproduction, use or disclosure to third parties, without express written authority, is strictly prohibited.

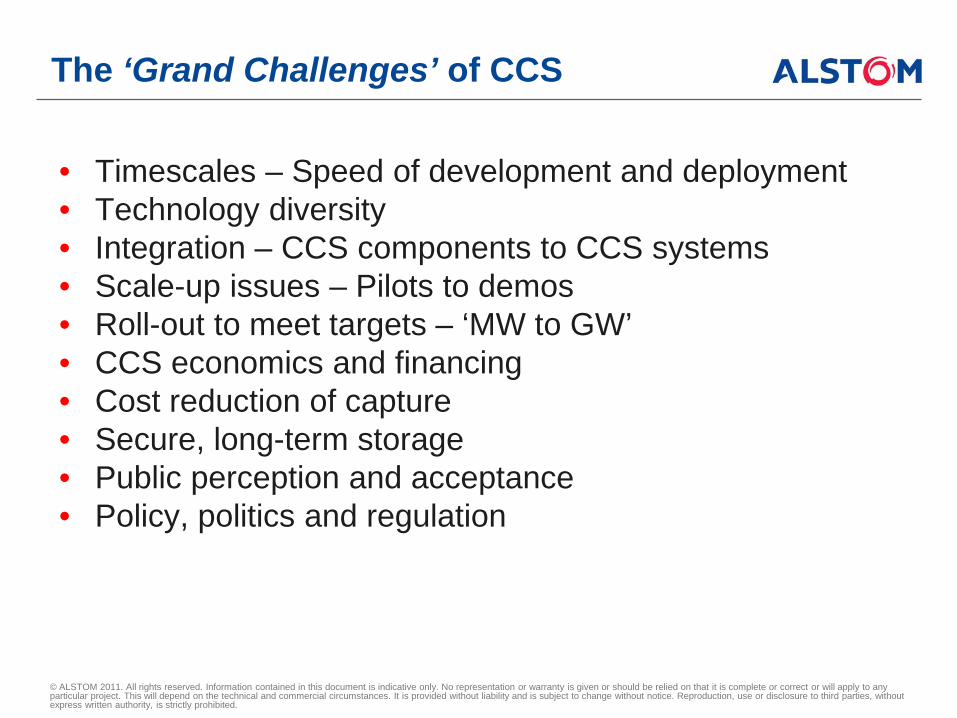

The ‘Grand Challenges’ of CCS

• Timescales – Speed of development and deployment • Technology diversity • Integration – CCS components to CCS systems • Scale-up issues – Pilots to demos • Roll-out to meet targets – ‘MW to GW’ • CCS economics and financing • Cost reduction of capture • Secure, long-term storage • Public perception and acceptance • Policy, politics and regulation

© ALSTOM 2011. All rights reserved. Information contained in this document is indicative only. No representation or warranty is given or should be relied on that it is complete or correct or will apply to any particular project. This will depend on the technical and commercial circumstances. It is provided without liability and is subject to change without notice. Reproduction, use or disclosure to third parties, without express written authority, is strictly prohibited.

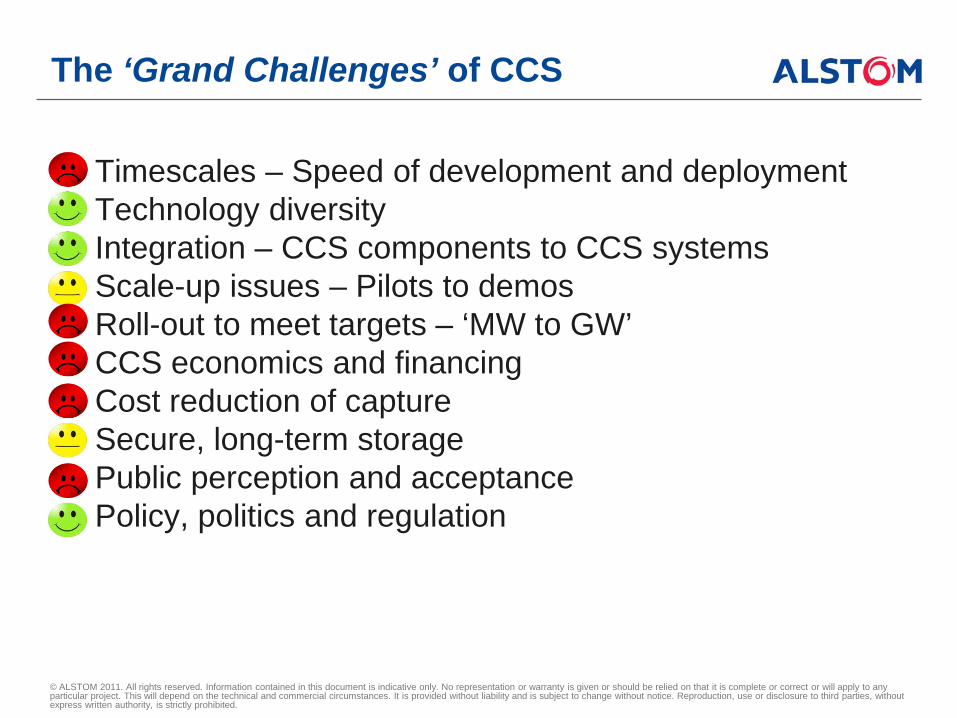

The ‘Grand Challenges’ of CCS

• Timescales – Speed of development and deployment • Technology diversity • Integration – CCS components to CCS systems • Scale-up issues – Pilots to demos • Roll-out to meet targets – ‘MW to GW’ • CCS economics and financing • Cost reduction of capture • Secure, long-term storage • Public perception and acceptance • Policy, politics and regulation

© ALSTOM 2011. All rights reserved. Information contained in this document is indicative only. No representation or warranty is given or should be relied on that it is complete or correct or will apply to any particular project. This will depend on the technical and commercial circumstances. It is provided without liability and is subject to change without notice. Reproduction, use or disclosure to third parties, without express written authority, is strictly prohibited.

The ‘Grand Challenges’ of CCS

• Timescales – Speed of development and deployment • Technology diversity • Integration – CCS components to CCS systems • Scale-up issues – Pilots to demos • Roll-out to meet targets – ‘MW to GW’ • CCS economics and financing • Cost reduction of capture • Secure, long-term storage • Public perception and acceptance • Policy, politics and regulation

Tony Booer Schlumberger Carbon Services

Sch

lum

berg

er Pu

blic

IEAGHG Summer School, Champaign, IL. July 17–22, 2011

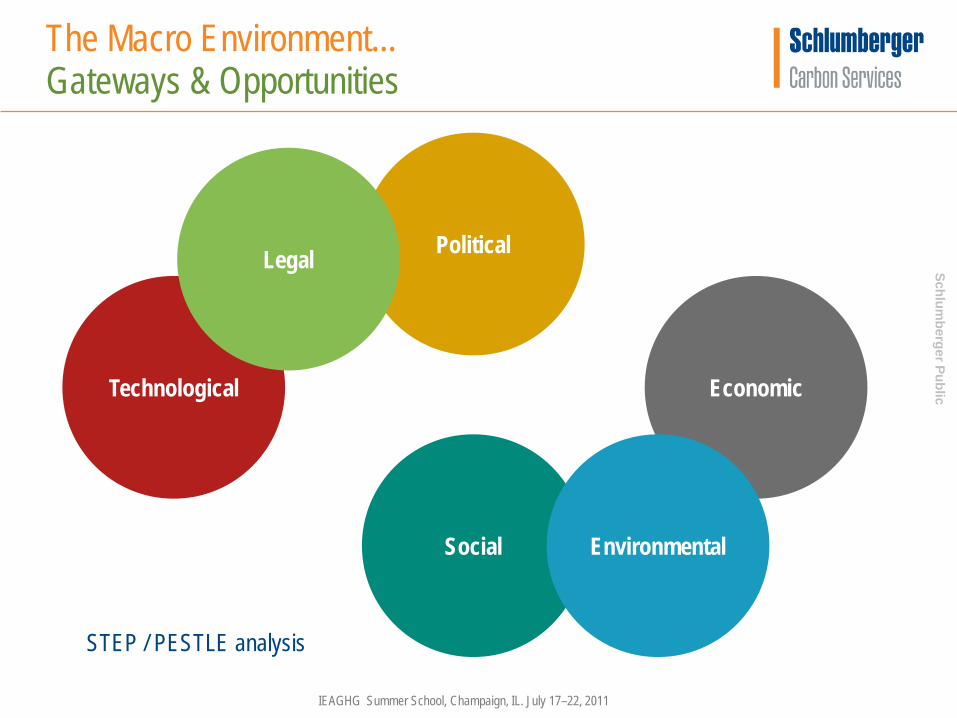

Technological

Political

Social

Economic

STEP / PESTLE analysis

The Macro Environment... Obstacles and Barriers

Legal

Environmental

The Macro Environment... Gateways & Opportunities

Sch

lum

berg

er Pu

blic

IEAGHG Summer School, Champaign, IL. July 17–22, 2011

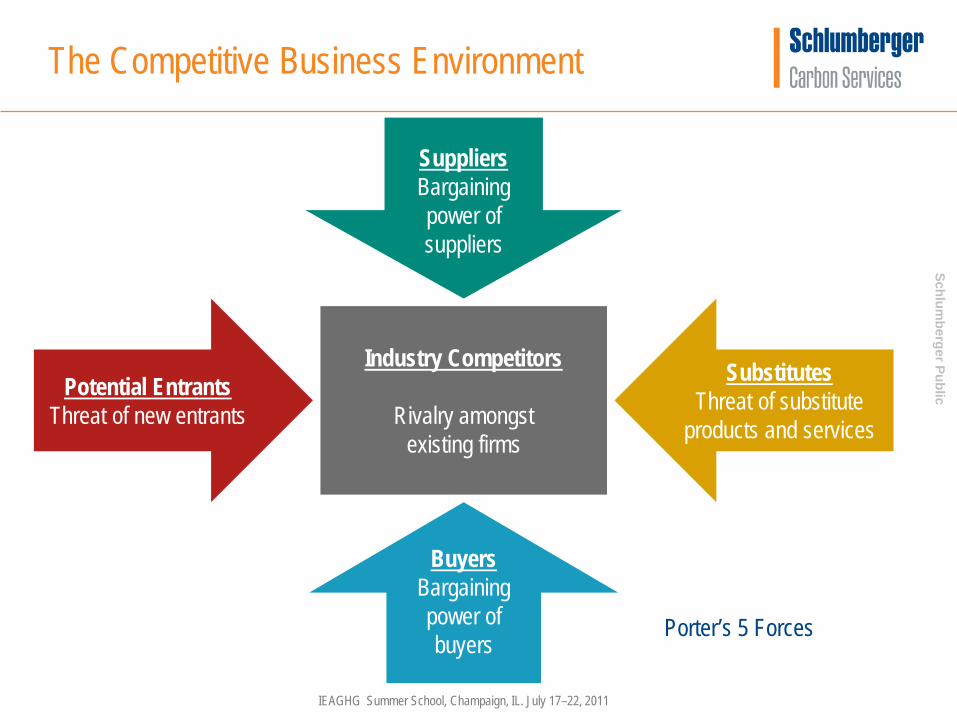

The Competitive Business Environment

Porter’s 5 Forces

Potential Entrants Threat of new entrants

Substitutes Threat of substitute

products and services

Suppliers Bargaining power of suppliers

Buyers Bargaining power of buyers

Industry Competitors

Rivalry amongst existing firms

Sch

lum

berg

er Pu

blic

IEAGHG Summer School, Champaign, IL. July 17–22, 2011

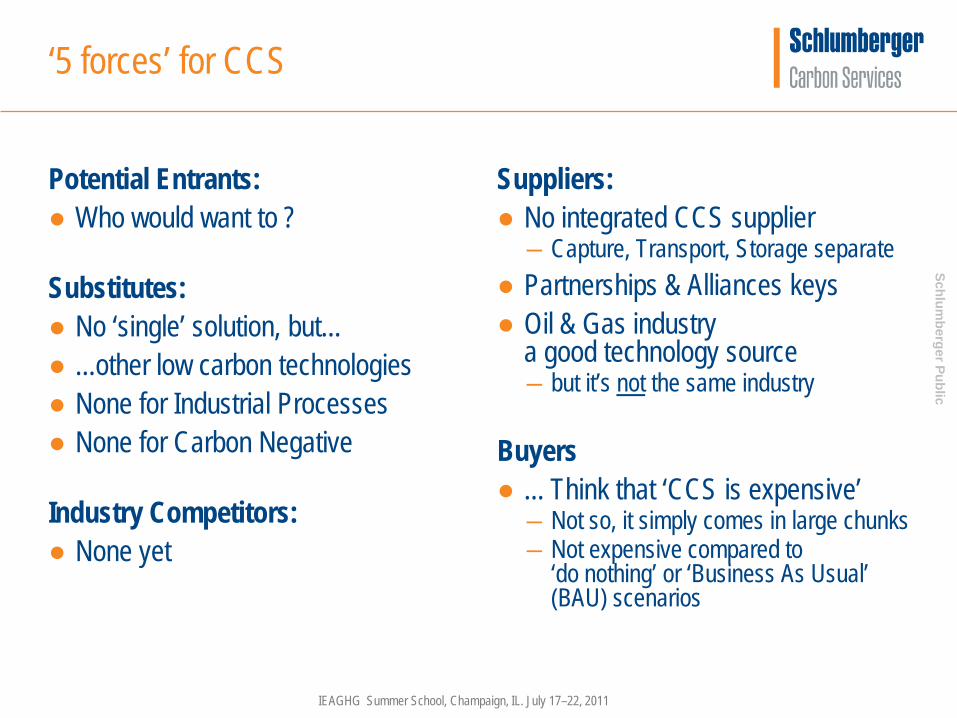

‘5 forces’ for CCS

Potential Entrants: ● Who would want to ? Substitutes: ● No ‘single’ solution, but... ● ...other low carbon technologies ● None for Industrial Processes ● None for Carbon Negative Industry Competitors: ● None yet

Suppliers: ● No integrated CCS supplier

― Capture, Transport, Storage separate ● Partnerships & Alliances keys ● Oil & Gas industry

a good technology source ― but it’s not the same industry

Buyers ● ... Think that ‘CCS is expensive’

― Not so, it simply comes in large chunks ― Not expensive compared to

‘do nothing’ or ‘Business As Usual’ (BAU) scenarios

Sch

lum

berg

er Pu

blic

IEAGHG Summer School, Champaign, IL. July 17–22, 2011

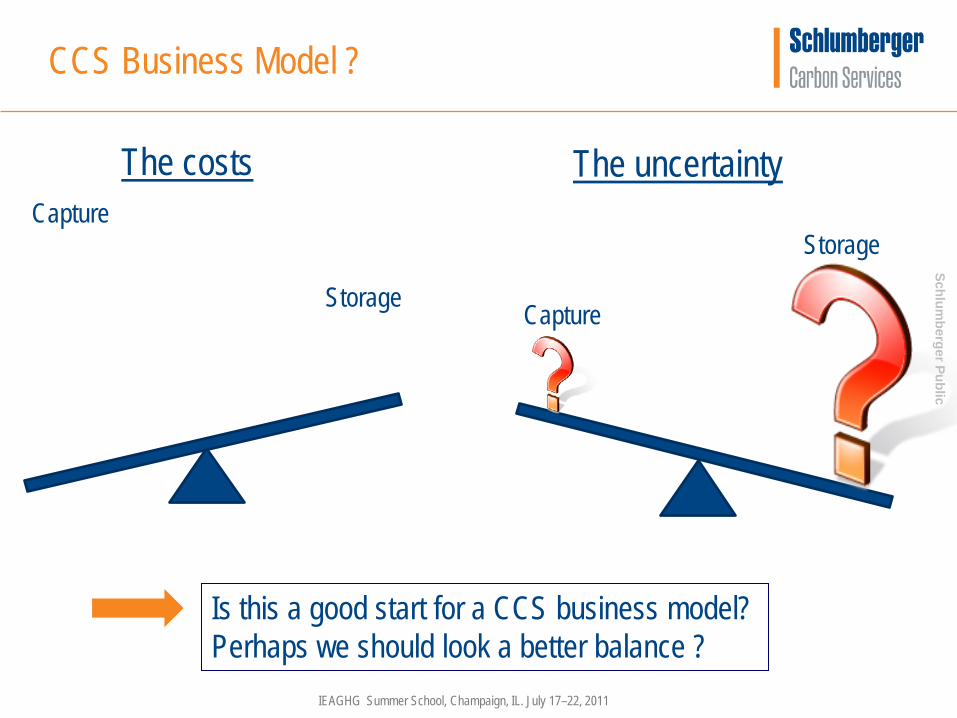

CCS Business Model ?

The costs The uncertainty Capture

Storage Capture

Storage

Is this a good start for a CCS business model? Perhaps we should look a better balance ?

Sch

lum

berg

er Pu

blic

IEAGHG Summer School, Champaign, IL. July 17–22, 2011

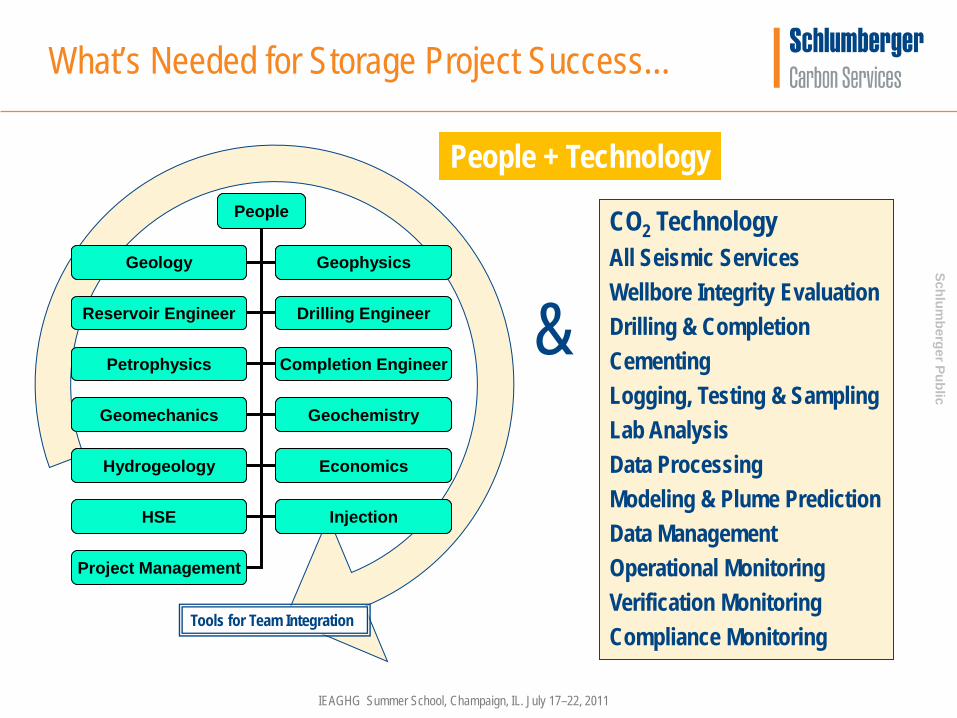

CO2 Technology All Seismic Services Wellbore Integrity Evaluation Drilling & Completion Cementing Logging, Testing & Sampling Lab Analysis Data Processing Modeling & Plume Prediction Data Management Operational Monitoring Verification Monitoring Compliance Monitoring

What’s Needed for Storage Project Success…

People + Technology

&

People

Geology Geophysics

Reservoir Engineer Drilling Engineer

Petrophysics Completion Engineer

Geomechanics Geochemistry

Hydrogeology Economics

HSE Injection

Project Management

People

Geology Geophysics

Reservoir Engineer Drilling Engineer

Petrophysics Completion Engineer

Geomechanics Geochemistry

Hydrogeology Economics

HSE Injection

Project Management

Tools for Team Integration

Sch

lum

berg

er Pu

blic

IEAGHG Summer School, Champaign, IL. July 17–22, 2011

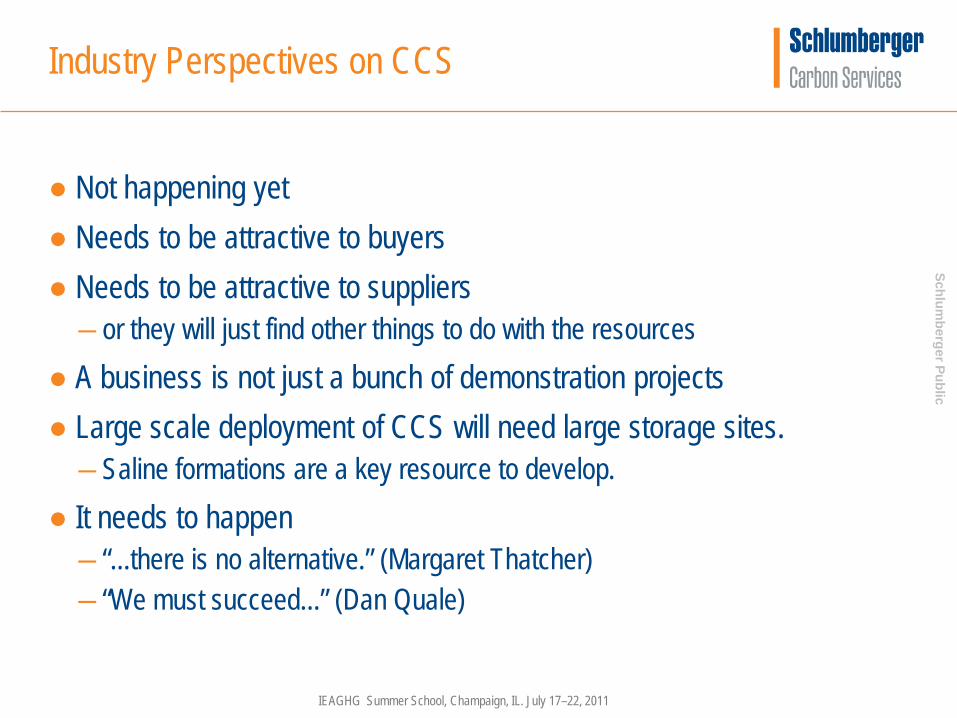

Industry Perspectives on CCS

● Not happening yet ● Needs to be attractive to buyers ● Needs to be attractive to suppliers ―or they will just find other things to do with the resources

● A business is not just a bunch of demonstration projects ● Large scale deployment of CCS will need large storage sites. ―Saline formations are a key resource to develop.

● It needs to happen ― “...there is no alternative.” (Margaret Thatcher) ― “We must succeed...” (Dan Quale)

Kevin McCauley Babcock & Wilcox

Shared Learnings and Continued Momentum

Eric Drosin Director of Communications

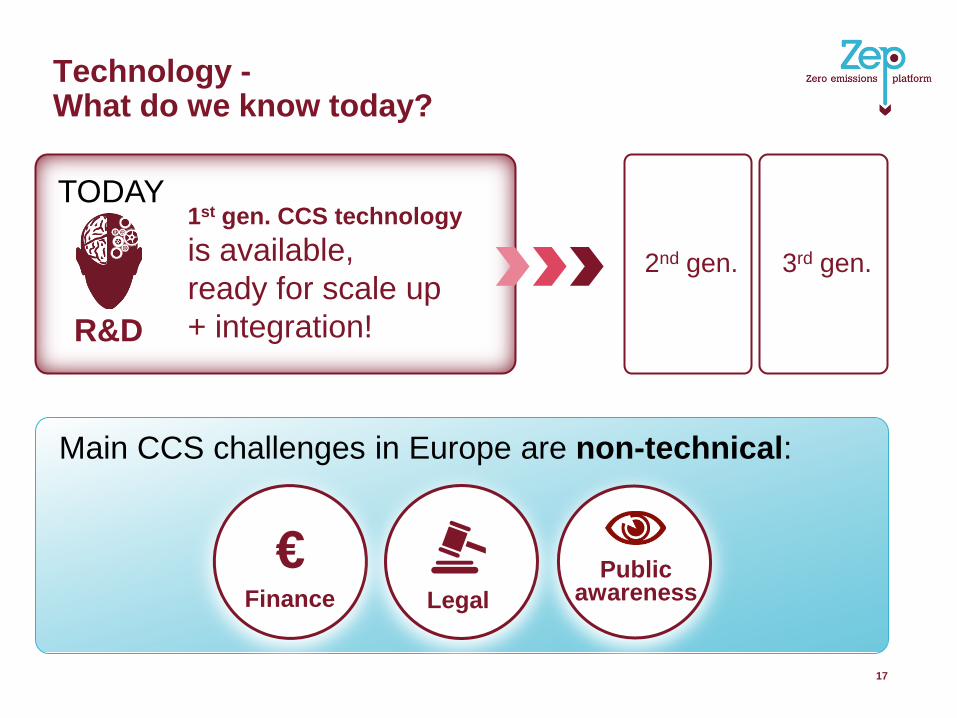

Technology - What do we know today?

17

Finance

€ Legal

Public awareness

Main CCS challenges in Europe are non-technical:

R&D

TODAY 1st gen. CCS technology

is available, ready for scale up + integration!

2nd gen. 3rd gen.

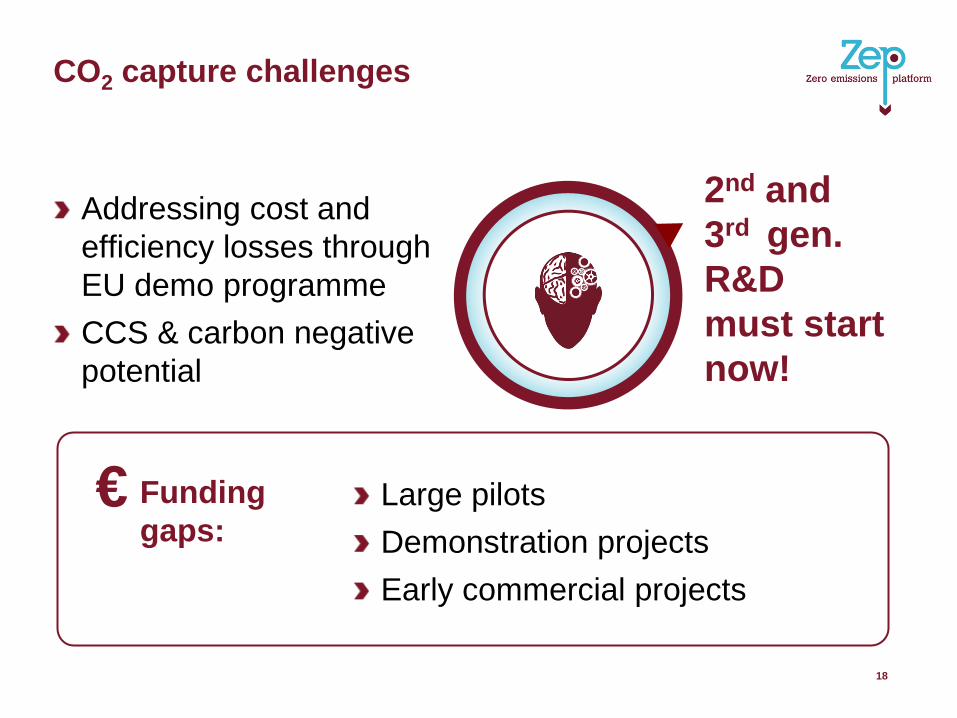

CO2 capture challenges

Addressing cost and efficiency losses through EU demo programme

CCS & carbon negative potential

2nd and 3rd gen. R&D must start now!

€ Funding gaps:

Large pilots

Demonstration projects

Early commercial projects

18

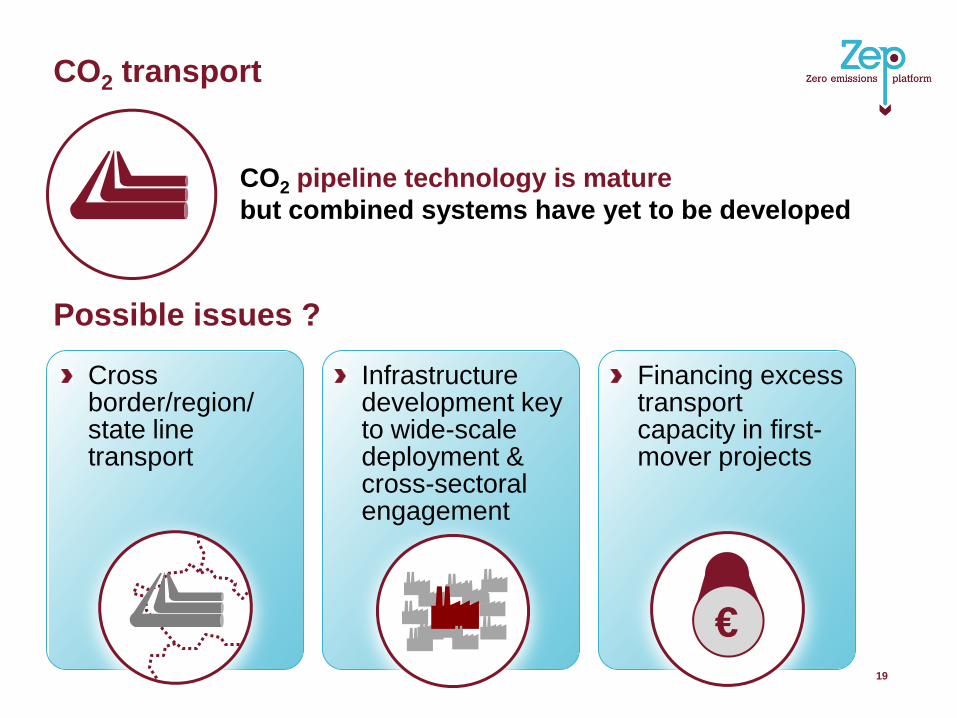

CO2 transport

CO2 pipeline technology is mature but combined systems have yet to be developed

19

Possible issues ?

€

Cross border/region/ state line transport

Infrastructure development key to wide-scale deployment & cross-sectoral engagement

Financing excess transport capacity in first-mover projects

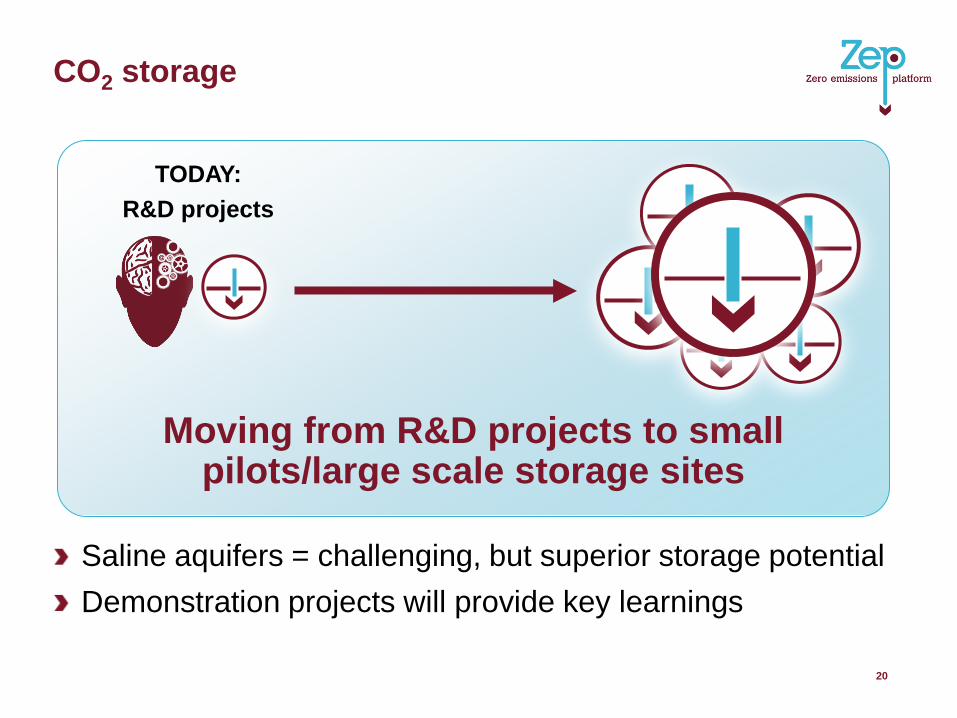

CO2 storage

Saline aquifers = challenging, but superior storage potential

Demonstration projects will provide key learnings

TODAY: R&D projects

Moving from R&D projects to small pilots/large scale storage sites

20

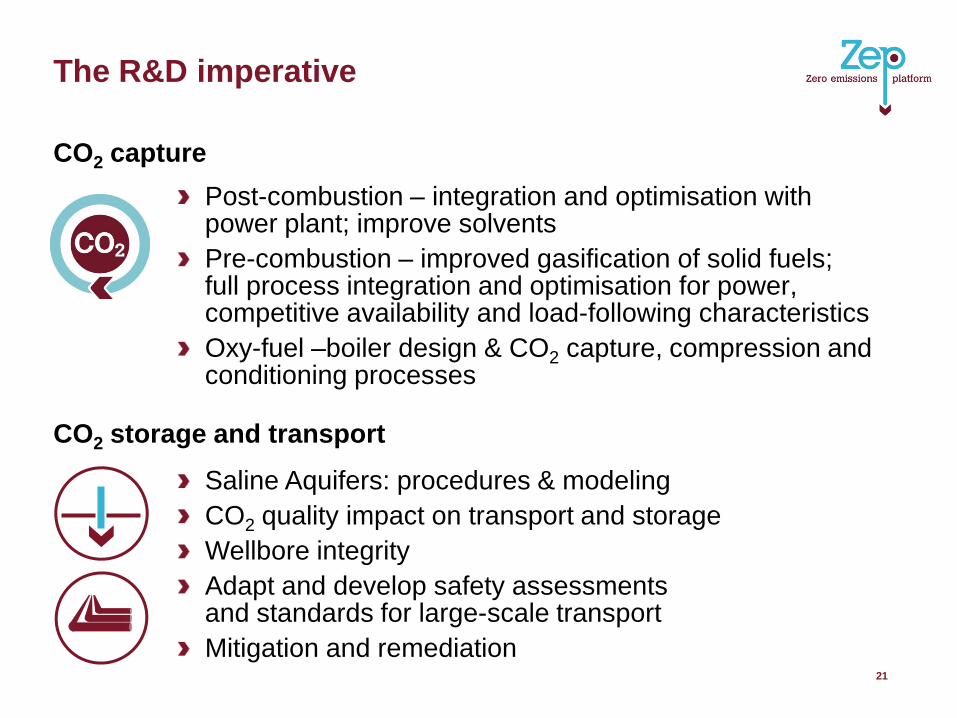

The R&D imperative

Post-combustion – integration and optimisation with power plant; improve solvents Pre-combustion – improved gasification of solid fuels; full process integration and optimisation for power, competitive availability and load-following characteristics Oxy-fuel –boiler design & CO2 capture, compression and conditioning processes

CO2 capture

21

Saline Aquifers: procedures & modeling CO2 quality impact on transport and storage Wellbore integrity Adapt and develop safety assessments and standards for large-scale transport Mitigation and remediation

CO2 storage and transport

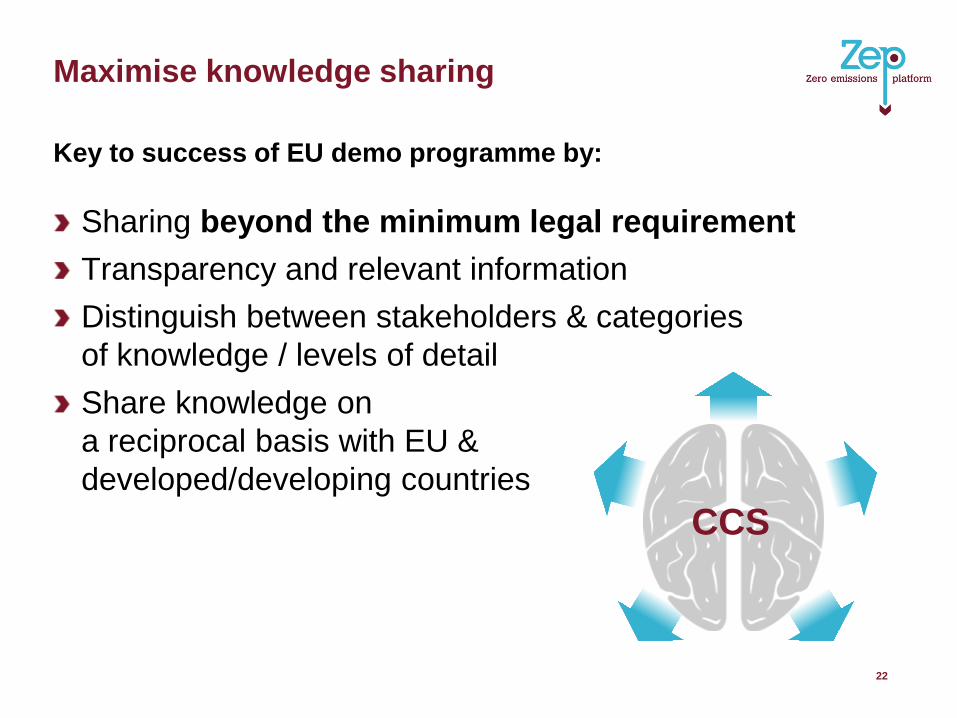

Maximise knowledge sharing

Sharing beyond the minimum legal requirement

Transparency and relevant information

Distinguish between stakeholders & categories of knowledge / levels of detail

Share knowledge on a reciprocal basis with EU & developed/developing countries

Key to success of EU demo programme by:

22

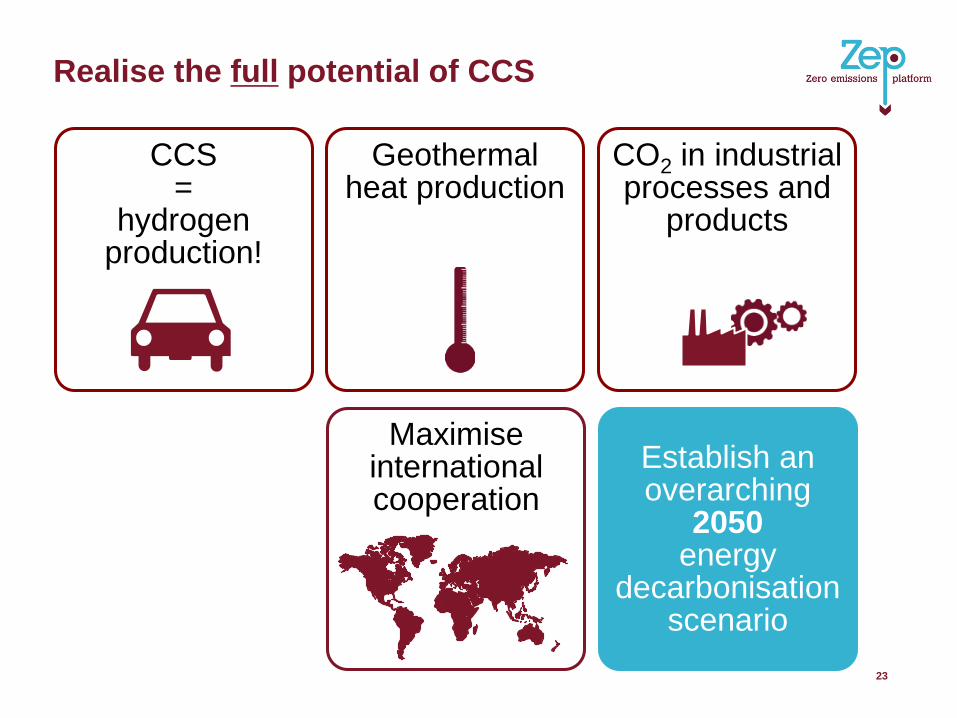

CCS

Realise the full potential of CCS

23

CO2 in industrial processes and

products

Geothermal heat production

Establish an overarching

2050 energy

decarbonisation scenario

Maximise international cooperation

CCS =

hydrogen production!

Time to throw your questions at the experts!