Embed Size (px)

Citation preview

© 2011 Deloitte Haskins & Sells

1GOODS AND SERVICE

TAX (GST)ONE COUNTRY – ONE TAX

THE NEW INDIRECT TAX FOR THE COUNTRY

Private Circulations onlywww.gkca.in

GST – One County, One Tax

© 2011 Deloitte Haskins & Sells

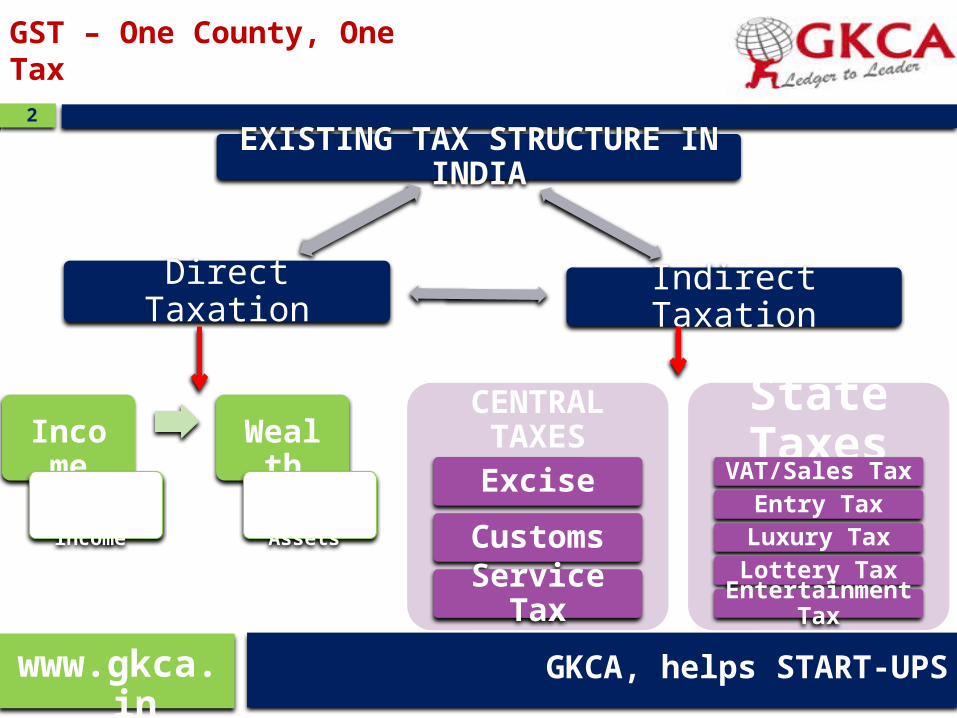

2EXISTING TAX STRUCTURE

IN INDIA

Indirect TaxationDirect Taxation

Income Tax• Means

Tax on income

Wealth Tax• Means

Tax on Assets

CENTRAL TAXESExcise

CustomsService

Tax

State TaxesVAT/Sales TaxEntry Tax

Luxury TaxLottery Tax

Entertainment Tax

www.gkca.in GKCA, helps START-UPS

GST – One County, One Tax

© 2011 Deloitte Haskins & Sells

3

The major changes in taxation are;DIRECT TAXATION

1) Wealth tax has been removed w.e.f 1st April 2014 onwards2) Income tax untouched

INDIRECT TAXATION1) All the Central and state acts have been clubbed together and a new law called GST formed w.e.f 1st April 2016 onwards

However, Income Tax (Direct Tax) and Customs (Indirect Tax) are untouched

www.gkca.in GKCA advises to Forbes Top corporates

GST – One County, One Tax

© 2011 Deloitte Haskins & Sells

4Concept of GST GST is one indirect tax for the whole nation, which will make India one unified common market. GST is a single tax on the supply of GOODS and SERVICES, right from the manufacturer to the

consumer. Any Credits of input taxes paid at each stage will be available in the subsequent stage of value addition,

which makes GST essentially a tax only on value addition at each stage. The final consumer will thus bear only the GST charged by the last dealer in the supply chain, with set-off benefits at all the previous stages.

Broad Constitute of GST

GSTIntra-State

CGST SGSTInter-State

IGST

www.gkca.in GKCA is part of panel discussion of GST

GST – One County, One Tax

© 2011 Deloitte Haskins & Sells

5GST – Internationally; Approximately, 160 countries have adopted so far, FRANCE was the first country to adopt it 1954. Hungary (27%), Gambia(40%) adopted the highest rates whereas Malaysia(6%) is the least. India proposed GST rate of 15 to 18%, technically 18%.

S. NO REGION NO. OF COUNTRIES

TAX RATE (RANGE)

1 ASEAN-(Thailand & Philippines) 7 7 – 12%2 Asia- (Iran & Tajikistan) 19 5-20%3 Europe- (Jersey & Hungary) 53 5-27% 4 Oceania- (Niue & New Zealand) 7 5-15%

Africa- (Nigeria & Gambia) 44 5-40% 6 South America- (Brazil & Uruguay) 11 10-22% 7 Caribbean, Central& North America -

(Canada & Barbados)19 5-17.5%

www.gkca.in GKCA is one of the leading consulting firms in India

GST – One County, One Tax

© 2011 Deloitte Haskins & Sells

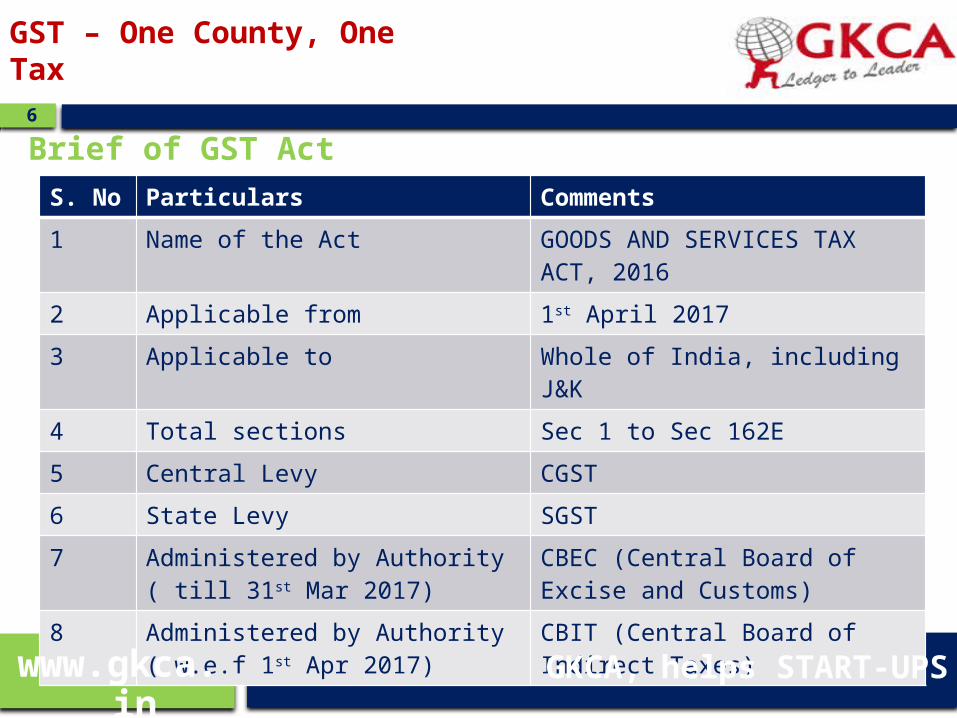

6Brief of GST Act

S. No Particulars Comments1 Name of the Act GOODS AND SERVICES TAX

ACT, 20162 Applicable from 1st April 20173 Applicable to Whole of India, including J&K4 Total sections Sec 1 to Sec 162E5 Central Levy CGST6 State Levy SGST7 Administered by Authority ( till

31st Mar 2017)CBEC (Central Board of Excise and Customs)

8 Administered by Authority ( w.e.f 1st Apr 2017)

CBIT (Central Board of Indirect Taxes)

www.gkca.in GKCA, helps START-UPS

GST – One County, One Tax

© 2011 Deloitte Haskins & Sells

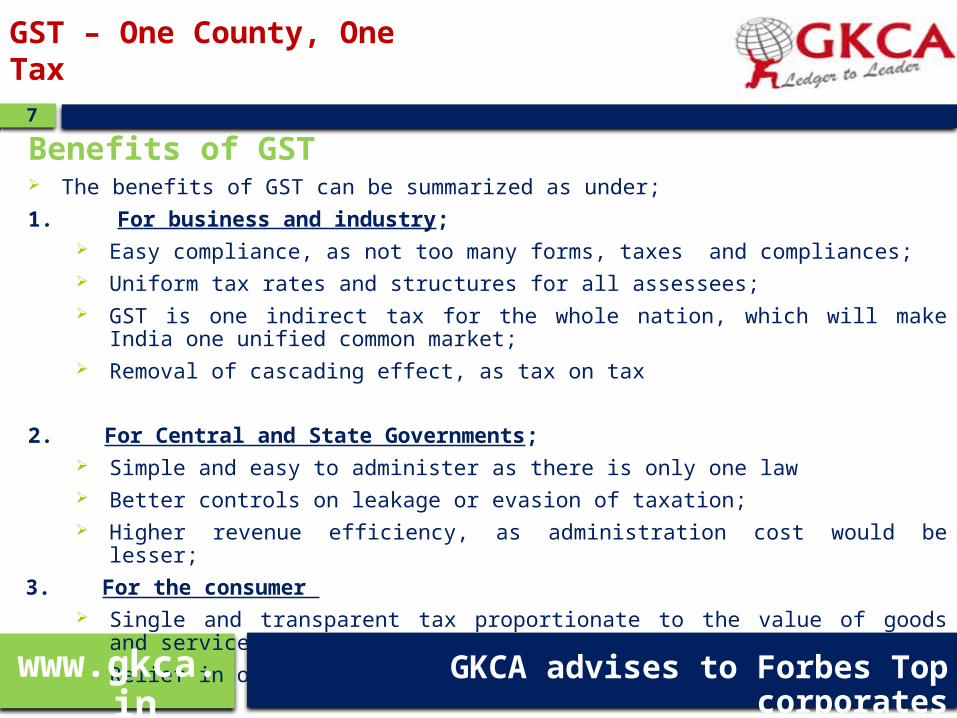

7Benefits of GST The benefits of GST can be summarized as under;1. For business and industry;

Easy compliance, as not too many forms, taxes and compliances; Uniform tax rates and structures for all assessees; GST is one indirect tax for the whole nation, which will make India one unified common market; Removal of cascading effect, as tax on tax

2. For Central and State Governments; Simple and easy to administer as there is only one law Better controls on leakage or evasion of taxation; Higher revenue efficiency, as administration cost would be lesser;

3. For the consumer Single and transparent tax proportionate to the value of goods and services; Relief in overall tax burden;

www.gkca.in GKCA advises to Forbes Top corporates

GST – One County, One Tax

© 2011 Deloitte Haskins & Sells

8

inCGS

T

•Central Excise duty•Additional excise duty•Service tax•Counter-Veiling duty•Special Addition duty•Surcharge & Cess

inSGS

T

•VAT/Sales Tax/CST•Entertainment tax•Luxury tax•Lottery tax•Entry tax•Stamp duty•Taxes on vehicle

Following taxes have been submerged in GST (Dual mode)

www.gkca.in GKCA is part of panel discussion of GST

GST – One County, One Tax

© 2011 Deloitte Haskins & Sells

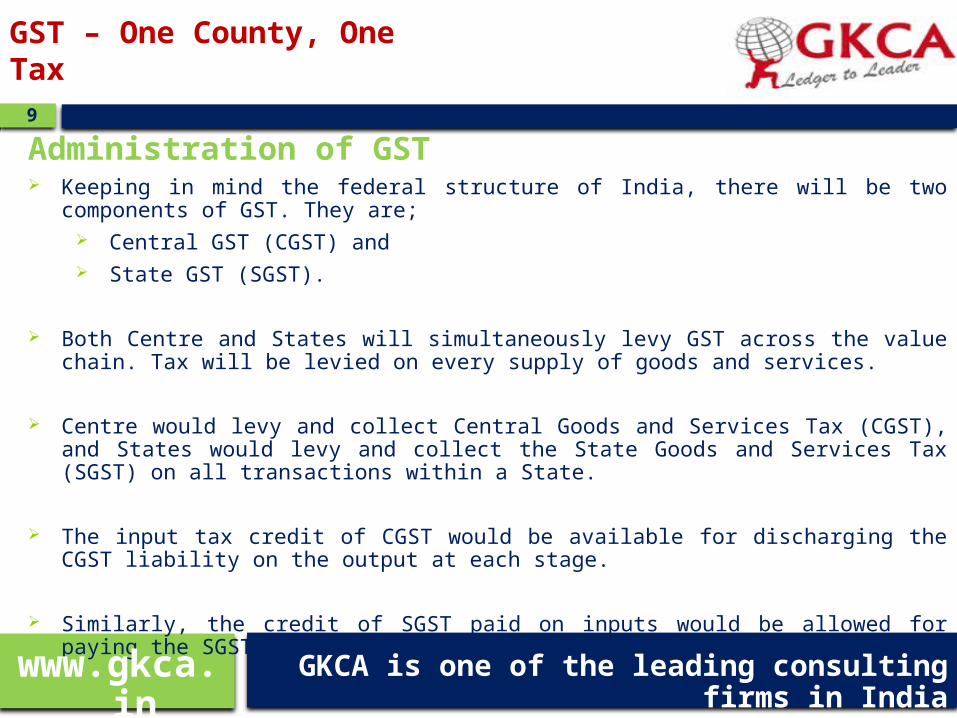

9Administration of GST Keeping in mind the federal structure of India, there will be two components of GST. They are;

Central GST (CGST) and State GST (SGST).

Both Centre and States will simultaneously levy GST across the value chain. Tax will be levied on every supply of goods and services.

Centre would levy and collect Central Goods and Services Tax (CGST), and States would levy and collect the State Goods and Services Tax (SGST) on all transactions within a State.

The input tax credit of CGST would be available for discharging the CGST liability on the output at each stage.

Similarly, the credit of SGST paid on inputs would be allowed for paying the SGST on output.

www.gkca.in GKCA is one of the leading consulting firms in India

GST – One County, One Tax

© 2011 Deloitte Haskins & Sells

10Cross utilisation of credit Cross utilization of credit of CGST between goods and services would be allowed.

Similarly, the facility of cross utilization of credit will be available in case of SGST.

However, the cross utilization of CGST and SGST would not be allowed except in the case of inter-State supply of goods and services under the IGST model.

Taxation of inter state transaction of goods and services In case of inter-State transactions, the Centre would levy and collect the Integrated Goods and Services

Tax (IGST) on all inter-State supplies of goods and services under Article 269A (1) of the Constitution.

The IGST would roughly be equal to CGST plus SGST.

The inter-State seller would pay IGST on the sale of his goods to the Central Government after adjusting credit of IGST, CGST and SGST on his purchases.

www.gkca.in GKCA, helps START-UPS

GST – One County, One Tax

© 2011 Deloitte Haskins & Sells

11Taxation of imports under GST

The Additional Duty of Excise or CVD and the Special Additional Duty or SAD presently being levied on imports will be subsumed under GST.

As per explanation to clause (1) of article 269A of the Constitution, IGST will be levied on all imports into the territory of India.

Unlike in the present regime, the States where imported goods are consumed will now gain their share from this IGST paid on imported goods.

The exporting State will transfer to the Centre the credit of SGST used in payment of IGST.

www.gkca.in GKCA advises to Forbes Top corporates

GST – One County, One Tax

© 2011 Deloitte Haskins & Sells

12Registration under GSTEXISTING DEALERS: Existing VAT/Central excise/Service Tax payers will not have to apply afresh for registration under

GST.

NEW DEALERS: Single application to be filed online for registration under GST.

The registration number will be PAN based and will serve the purpose for Centre and State.

Each dealer to be given unique ID GSTIN.

Deemed approval within three days.

Post registration verification in risk based cases only.

www.gkca.in GKCA is part of panel discussion of GST

GST – One County, One Tax

© 2011 Deloitte Haskins & Sells

13

www.gkca.in GKCA is one of the leading consulting firms in India

GKCA (P) LTD#123/30, 1st Floor, W.O.C Road

Magadi Road Tollgate CircleBangalore – 560044

P: 080 4201 2207M+91 99862 34100Web: www.gkca.in

Email: [email protected]

GST – One County, One Tax