Embed Size (px)

Citation preview

India Strategy & Top Ideas

All eyes on Fed Rate hikes and Chinese policy actions

R Sreesankar [email protected]

+91-22-66322214

Click to edit Master title style LilladherPrabhudas September 2015

Prabhudas Lilladher Pvt. Ltd. and/or its associates (the 'Firm') does and/or seeks to do business with companies covered in its research reports. As a result investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of the report. Investors should consider this report as only a single factor in making their investment decision.

Please refer to important disclosures and disclaimers at the end of the report.

LilladherPrabhudas Contents

9/9/2015 2

Page No.

Large Caps

HDFC Bank 24

Infosys 26

State Bank of India 28

ICICI Bank 30

Larsen & Toubro 32

Maruti Suzuki 35

Tata Motors 37

Indian Oil Corporation 39

IndusInd Bank 41

Mid-Caps

Glenmark Pharmaceuticals 44

Cummins India 46

Motherson Sumi Systems 48

Aurobindo Pharma 50

MindTree 52

Persistent Systems 55

Jubilant Life Sciences 57

Sadbhav Engineering 59

JK Lakshmi Cement 61

Rallis India 63

Va Tech Wabag 65

Page No.

Domestic beginning to see bright spots, global negative outlook 3-4

Global Growth – US to lead the Growth 5

South West Monsoon-Below the LPA 6

Low oil prices lead to CAD under control 7

Tax collections up 8

Traction in plan expenditure 9

Inflation continues to move down 10

Markets

Equity markets under pressure across the globe 11

IT and Healthcare sectors leads the way 12

Small and Midcaps underperform 13

Global Currencies – A painful month 14

FII outflows in second half of August 15

Global Agri commodities - Sugar and wheat weaken further 16

Global Industrial Commodities continues to decline 17

Equity markets weak across the board 18

Indian Market – Valuation and Strategy 19

Nifty Valuations: Historic Trends 20

Nifty Valuation 21

Top Pick Summary 22

(Prices as on September 08, 2015)

LilladherPrabhudas Domestic beginning to see bright spots, global

negative outlook • Metal index the worst hit : The CNX Metal index has turned out the worst performance having lost over 45% in the last twelve months,

reflecting the 16 year low in steel prices. The outlook for the global commodities continue to remain negative despite the large losses and underperformance of the sector.

• Infrastructure, outlay higher and Orders for new projects on the rise: The allocation for the road sector has been higher, though we would have been happy with a speedier implementation on awarding of road projects from the government side to speed up the government spending as well as the economic recovery. In the first four months alone, 2700km worth Rs350bn has been awarded.

• Politics, All eyes on Bihar elections: From GST and land bills, the attention has now shifted to Bihar elections expected in less than 60 days. The outcome though will not affect the number game at the centre, a strong performance by the ruling BJP led coalition will help them increase their numbers in the upper house of the parliament and send a strong a signal to the Indian equity markets.

• Interest rates, will it be a RBI reduction or by market forces? The repo rates under the Liquidity Adjustment Factor (LAF) was reduced by 25bps from 7.50% to 7.25% in the bi-monthly monetary policy on June 2, 2015. Since then we have seen the inflation rates correcting sharply and the WPI based inflation has remained negative, while the CPI too has corrected to 3.8%, much below the RBIS comfort zone of 6%. The banks have reduced the deposit rates and we strongly believe further reductions in interest rates may happen through transition.

• IT and Pharma Sector, expected to do well, while FMCG may face headwinds: We had maintained our neutral stance on the IT sector ahead of the 2QFY16 results, while the sector outlook of the street was negative. With Infosys reporting results better than expected and with a guidance beating the street expectations, the IT sector have seen an improved demand and the sector has seen a sharp out performance over the last two months. In case of the FMCG companies, while the lower commodity prices have helped see an expansion in margins, the slowing growth in the rural sector is resulting in demand headwinds. Should the monsoon remain below normal, the expected pick up in demand in rural areas may not materialize leading to an underperformance.

• Falling CAD, have we seen the best of it: The steady decline seen in merchandise exports since July 2014 have seen a reversal in July 2015. The exports, which were at a monthly run rate of US$22bn and have improved to over US$23bn in July 2015. Given the slower global growth and relative out performance of the Indian Rupee, the headwinds for exports are likely to continue. The CAD has crossed the US$12bn for the first time in the last eight months.

9/9/2015 3

LilladherPrabhudas Contd…

• Correction in Private sector banks overdone? The privates sector banks space has seen a sharp correction in the last fortnight alone. Axis Bank, ICICI Bank and Yes bank have seen the maximum corrections. Axis Bank has corrected from 2.5x FY17 ABV to 1.9x, ICICI to 1.5x from 2.1x FY17ABV and Yes Bank to 1.6x from 2.2x FY17ABV. We believe that the correction has been steep and the fundamentals do not warrant a steep correction of that nature. Though the pace of the economic recovery is slower than anticipated, we expect to see lower NPA additions and hence lower credit costs and higher profits. Hence, we continue to recommend an overweight position in the financials. While the broader calls remain the above, within the financials we continue to remain heavily leaned towards the private sector banks. The 1QFY16 performance of the private sector banks was in line with expectations, the shocks and the volatility of the PSU banks makes us continue to believe that the PSU banks are at best trading bets. Our preferred picks continue to be HDFC Bank, ICICI Bank, IndusInd Bank and State Bank of India among the PSU banks.

• PCs and CVs preferred over two wheelers: The outlook for automobiles especially for passenger cars and commercial vehicles looks good till the festival season in October 2015. Our top picks in the sector continues to be Maruti Suzuki and Tata Motors and we have added Motherson Sumi Systems to the top picks following the massive underperformance seen in the last three months. Tata Motors have been an under performer in the last one year and the negatives in terms of transition and JLRs China operations is overdone in the price.

• Indian Oil Corporation, a big beneficiary of falling oil prices: The benign crude oil prices benefit the down stream companies much better than the upstream companies and within the downstream companies, (i) IOC is cheaper in terms of valuation, (ii) the Rs100bn OFS overhang is over as they are done with the sale and (iii) unlike HPCL and BPCL which are pure marketing margin stories, IOC will also benefit from a surge in petrochemical margins.

• Global Commodities and Agricultural commodities continue to be under pressure: The global commodities and the agricultural commodities continue to remain under pressure, more complicated by the recent weakness in the Chinese Renminbi as well.

• Market trading range revised downwards: The equity market is trading at a one year forward multiple of 16.4x, still at a marginal premium to the 10 year average. This is mainly on account of downward revision of FY16 earnings. We have revised our estimate for the market trading range to 7500-8200 in the near term.

• Our preferred picks continue to be HDFC Bank, SBI, IndusInd and ICICI bank among the financials, L&T and Sadbhav Engineering among Engineering & Capital Goods and Infosys,, MindTree and Persistent among IT, JK Lakshmi Cement among Basic materials and Tata Motors, Motherson Sumi Sytems and Maruti Suzuki among Automobiles with Glenmark, Jubilant Life and Aurobindo Pharma among Pharmaceuticals.

9/9/2015 4

LilladherPrabhudas Global Growth – US to lead the Growth

• US expected to lead the Global growth: US economy is expected to drive global growth in both 2015 and 2016. US economy shrug off the global economic anxiety in the second quarter with a 2.3% growth. The rebound in growth after a sluggish first quarter was supported by consumer spending, government outlays and exports. The world growth for CY2015 is expected at 2.4%.

• US Non farm pay roll and un employment levels to a new low: The non farm payroll additions were at 173,000 in August 2015 thereby keeping the un employment levels to a new low of 5.1%. Energy sector continues to see increased lay offs, as job cuts in energy sector surged, reflecting the low oil prices. The payroll additions have also dropped below the 12 month average of 245,000.

• Crude oil Prices, at five year lows: The Brent crude oil prices have further corrected to a new low at US$42.69 to a barrel on 24th August 2015. Since then, though crude prices recovered, it is still hovering below the lows achieved in July 2015.

• Global Volatility and Indian Volatility higher: The CBOE VIX volatility index, a measure of the cost of equity portfolio protection has have seen higher volatility and trades at 27.80, with the Indian VIX at 24.56 at relatively higher levels indicating higher volatility. Both these have shot up post August 20, 2015.

• Tough time for emerging Markets: As capital flows back to the USA in expectations of higher interest rates, some emerging markets, especially those with the twin deficits of government and external deficit will particularly be vulnerable with renewed pressures on their currency. The “ fragile five” in this category are Brazil, India, Indonesia, Turkey and South Africa. Of this according to us, India is relatively stable as the government and the central bank are following a different management. In addition to the countries with fiscal and CADs, countries with weak institutions, exposure to low commodity prices and high political risk could also be vulnerable. This could include Russia, Venezuela and Columbia. We have seen a severe pain in all these markets ranging from depreciating currencies to economic turmoil, with India being the sole exception so far.

• Fed Rate hike, will it happen now? It is anticipated that we will see a monetary tightening cycle for the first time since 2004. With un employment levels at 5.1% at a new low, price pressures will rise as a tight labor market forces wage inflation. It is expected that the sooner Fed raises rates, there will be more room to take action during the next downturn. However, it needs to be wait and seen with Japan and China in the middle of a monetary easing programme, how a divergent policy will work, especially when if it contributes to a strengthening Dollar.

9/9/2015 5

LilladherPrabhudas South West Monsoon-Below the LPA

Source: IMD

• The country as a whole witnessed 640.7mm rainfall from 01 June 2015 till 02 September 2015. As against the Long Period Average (LPA) of 728.3mm, the rainfall was short to the extent of 12% on the lower side from LPA.

• After a good rainfall during June and second half of July, the country has witnessed a deficient rainfall till now with some parts of North-West and East & North-East region witnessing heavy rainfall while South Peninsula & major parts of Central India witnessing deficient rainfall.

• As of September 2, 2015, 2 subdivisions have witnessed excess monsoon and 17 subdivisions have witnessed normal rain while 17 subdivisions have had below normal/deficient rainfall till now. There is no subdivision where rainfall is scanty (i.e.-66% to -99%) or no rain.

• The lower rainfall is reflected in the water storage levels across the country. Water storage at 91 major reservoirs has dipped to 87% of the storage of corresponding period last year and 88% of storage of average of last 10 years.

• As per the data released by the government, as of August 28, 2015, total kharif sowing is completed in 967.8 lakh hectares (which is ~84% of average seasonal Kharif sowing) which is higher by ~1% y-o-y. Except cotton and jute (which are lower by 8% and 4% y-o-y resp) all other Kharif crop have seen year on year higher sowing till now.

Cumulative Seasonal Rainfall Map as on September 02, 2015

9/9/2015 6

LilladherPrabhudas Low oil prices lead to CAD under control

9/9/2015 7

• The CAD has been under control, thanks to the low oil prices. Over the last five months, the ,trade deficit have been hovering around

US$10bn a month. While the low oil prices continue to be a boon, the challenge is going to be managing an increase in non oil non gold

imports once the domestic economy recovers. CAD in July 2015 has shot up above US$12bn.

External debt break-up between ST and LT

Source: RBI, PL Research * Data revised on exchange rate fluctuation

Trade Deficit

Source: RBI, PL Research

US $ Mn Sep'14 Oct'14 Nov'14 Dec'14 Jan'15 Feb’15 Mar’15 Apr’15 May’15 Jun’15 Jul’15 YTD YTD YoY

Exports 28,903 26,094 25,961 25,398 23,883 21,545 23,951 22,055 22,347 22,289 23,137 89,828 105,905

Imports 43,151 39,452 42,822 34,833 32,206 28,392 35,745 33,047 32,753 33,117 35,950 134,866 153,264

- Oil 14,497 12,365 11,716 9,942 8,248 6,101 7,413 7,443 8,539 8,676 9,487 34,145 55,360

- Gold 3,752 4,170 5,610 1,340 1,550 1,980 4,980 3,131 2,420 1,967 2,965 10,483 9,268

- Non Oil Non Gold 24,902 22,916 25,496 23,551 22,408 20,311 23,351 25,604 21,794 22,473 23,498 90,239 88,636

Trade Deficit (14,247) (13,357) (16,861) (9,435) (8,323) (6,847) (11,794) (10,992) (10,406) (10,827) (12,812) (45,038) (47,359)

3.6 2.8 4.7 4.4 17.7 19.5 28.1 45.8 43.3 52.4 64.9 78.2 96.6 91.5 87.8 86.2 85.5 84.7

97.7 96.0 100.2 108.2 116.3 119.6

144.3 178.6 181.2

208.5 241.0

267.6 312.8 354.8 362.3 369.7 376.4 391.1

0

100

200

300

400

500

2000

-01

20

01

-02

20

02

-03

20

03

-04

20

04

-05

2005

-06

20

06

-07

2007

-08

20

08

-09

2009

-10

20

10

-11

2011

-12

20

12

-13

20

13

-14

Jun

-14

Sep

-14

Dec

-14

Mar

-15

(US$

bn

)

Short Term Debt Long Term Debt

LilladherPrabhudas Tax collections up

Source: Controller General of Accounts – Ministry of Finance, PL Research

Trends in Government’s Fiscal Deficit • Non tax revenues were up , mainly on account of income from auction of telecom licenses.

• Excise duties are up due to increase in excise on petroleum products earlier in the year. On a higher base, there is a strong month on month increase in Excise duties.

• The service tax has been hiked w.e.f. July 1, 2015 and we expect this to reflect from July 2015 onwards in increased revenues.

Source: Controller General of Accounts – Ministry of Finance, PL Research

Trends in Tax Receipts

9/9/2015 8

(Rs bn) Upto

Jul'14

Upto

Jul'15 YoY %

Budget

Est

% to total

Budget Est.Shortfall

Revenue Receipts 1,756 2,090 19% 11,416 18% (9,326)

Tax Revenue (Net) 1,469 1,539 5% 9,198 17% (7,660)

Non-Tax Revenue 288 551 92% 2,217 25% (1,666)

Non-Debt Capital Receipts 34 69 104% 803 9% (734)

Recovery of Loans 33 35 8% 108 33% (72)

Other Receipts 1 34 NA 695 5% (661)

Total Receipts 1,790 2,159 21% 12,218 18% (10,060)

Non-Plan Expenditure 3,719 4,431 19% 13,122 34% (8,691)

On Revenue Account 3,380 4,087 21% 12,060 34% (7,973)

(i) of which Interest Payments 1,186 1,276 8% 4,561 28% (3,285)

On Capital Account 338 344 2% 1,062 32% (718)

(i) of which Loans disbursed 99 99 0% 10 89

Plan Expenditure 1,320 1,578 20% 4,653 34% (3,074)

On Revenue Account 1,040 1,062 2% 3,300 32% (2,238)

On Capital Account 280 516 84% 1,353 38% (836)

(i) of which Loans disbursed 76 104 36% 231 (127)

Total Expenditure 5,039 6,010 19% 17,775 34% (11,765)

Fiscal Deficit 3,249 3,851 19% 5,556 69% (1,705)

Revenue Deficit 2,664 3,060 15% 3,945 78% (885)

Primary Deficit 2,063 2,575 25% 995 259% 1,580

Tax Revenue (in Rs.Bn) Upto

Jul'14

Upto

Jul'15 YoY %

Budget

Est

% to total

Budget Est. Shortfall

Corporate Tax 625 663 6% 4,706 14% (4,043)

Income Tax 649 620 -5% 3,274 19% (2,654)

Customs 539 664 23% 2,083 32% (1,419)

Union Excise Duties 323 580 80% 2,298 25% (1,718)

Service Tax 416 485 17% 2,098 23% (1,612)

Other Tax 37 39 5% 36 108% 3

Gross Tax Revenue 2,589 3,051 18% 14,495 21% (11,444)

Surcharges 12 16 27% 57 27% (41)

Assignment to states 1,108 1,497 35% 5,240 29% (3,743)

Net Tax Revenue 1,469 1,539 5% 9,198 17% (7,660)

LilladherPrabhudas Traction in plan expenditure

9/9/2015 9

• The plan expenditure has seen a substantial increase in the first four months of FY16 with both the ministry of Surface transport and Highways as well as Ministry of urban transport seeing the increased spend.

• The current low oil prices have resulted in the lower outgo of planned subsidies in the petroleum sector.

Source: Controller General of Accounts – Ministry of Finance, PL Research

In Rs Bn Upto

Jul'14

Upto

Jul'15 YoY %

Budget

Est

% to total

Budget Est.

Non-Plan Expenditure 3,719 4,431 19% 12,199 36%

-Dept. of Fertil izers 207 353 70% 730 48%

-Dept. of Food & PDS 483 539 12% 1250 43%

-Dept. of Petroleum & Gas 250 92 -63% 301 31%

Plan Expenditure 1,320 1,578 20% 12,199 13%

-Min. of Road Transport & Highway 78 272 249% 429 63%

-Min. of Rural Development 271 350 29% 733 48%

-Min. of Urban Development 25 54 113% 161 33%

-Min. of Agriculture 80 67 -16% 218 31%

-Min. of Railways 100 113 12% 400 28%

-Min. of Drinking Water & Sanitation 27 51 87% 62 81%

-Min. of Health & Family Welfare 69 101 45% 267 38%

-Min. of Human Resource 184 173 -6% 549 32%

Plan Expenditure and Non-plan expenditure

LilladherPrabhudas Inflation continues to move down

• Both the retail and the wholesale inflation saw a decrease in July 2015. The whole sale inflation still continues to be in the negative territory , both m-o-m as well as y-o-y leading to the real rates remaining positive.

• 10yr G-Sec Yield is trading at 7.80%, and has been in a range of 7.74% to 7.89% in the last one month.

• The June 2015 IIP data continue to be disappointing at 3.8%, though it was marginally better than the 2.7% achieved in May 2015.

Source: Bloomberg, PL Research

Source: Bloomberg, PL Research

CPI Inflation

GDP Growth YoY (Quarterly)

Source: Bloomberg, PL Research

10yr. G-Sec Yield & Liquidity

9/9/2015 10

-

2.0

4.0

6.0

8.0

10.0 (2,500)

(2,000)

(1,500)

(1,000)

(500)

-

500

1,000

1,500

Aug

-10

Dec

-10

Apr

-11

Aug

-11

Dec

-11

Apr

-12

Aug

-12

De

c-1

2

Apr

-13

Aug

-13

Dec

-13

Apr

-14

Aug

-14

Dec

-14

Apr

-15

Aug

-15

Liquidity (Rs bn) 10yr. G-Sec Yied (%) (RHS)

0

2

4

6

8

10

12

Sep

-05

Dec

-05

Mar

-06

Jun

-06

Se

p-0

6D

ec-0

6M

ar-0

7Ju

n-0

7Se

p-0

7D

ec-0

7M

ar-

08

Jun

-08

Sep

-08

De

c-0

8M

ar-0

9Ju

n-0

9Se

p-0

9D

ec-0

9M

ar-

10

Jun

-10

Sep

-10

De

c-1

0M

ar-1

1Ju

n-1

1S

ep

-11

Dec

-11

Mar

-12

Jun

-12

Sep

-12

Dec

-12

Mar

-13

Jun

-13

Sep

-13

Dec

-13

Mar

-14

Jun

-14

Sep

-14

Dec

-14

Ma

r-1

5Ju

n-1

5

(%)

8.6

7.98.2 8.5 8.3

6.87.4

7.0

5.6

4.6

3.3

4.3

5.2 5.4 5.34.9 5.0

5.4

3.8

3.0

4.0

5.0

6.0

7.0

8.0

9.0

Jan

-14

Feb

-14

Mar

-14

Apr

-14

May

-14

Jun-

14

Jul-

14

Aug

-14

Se

p-1

4

Oct

-14

Nov

-14

Dec

-14

Jan

-15

Feb

-15

Mar

-15

Apr

-15

May

-15

Jun-

15

Jul-

15

Consumer Price Index (CPI)

LilladherPrabhudas Equity markets under pressure across the globe

• MoM: The Equity markets across the board have come under pressure due to increased risk aversion with money moving out of EMs. Hong Kong was one of the biggest losers along with China, Germany and Japan.

• YoY and YTD: On a y-o-y basis, China, Japan and Russia are the only markets on the positive side, with China the biggest gainer. While on a YTD basis, Russia, Japan and Germany are on the positive side, with Russia the biggest gainer though Russian Ruble declined 82% during the period.

Source: Bloomberg, PL Research

Source: Bloomberg, PL Research

Month-on-Month

Year-on-Year

Source: Bloomberg, PL Research

Calendar Year-to-date

9/9/2015 11

1.6

(4.6)

(7.1) (7.1) (7.3) (7.8)(9.0) (9.2)

(10.7)(10.9)(12.2)(12.8)

(14.2)(16.0)(14.0)(12.0)(10.0)

(8.0)(6.0)(4.0)(2.0)

-2.0 4.0

Ru

ssia

S.Ko

rea

USA

S&P

Bra

zil

Indo

nesi

a

FTSE

Indi

a

Au

stra

lia

Japa

n

Ger

man

y

Chin

a

Hon

g Ko

ng

(%)

21.1

0.0

(8.3)(5.3) (7.1)

(15.3)

(7.4) (6.9) (6.3)

4.9 2.5

(2.3)

(11.3)(20.0)

(15.0)

(10.0)

(5.0)

-

5.0

10.0

15.0

20.0

25.0

Ru

ssia

S.Ko

rea

USA

S&P

Bra

zil

Indo

nesi

a

FTSE

Indi

a

Au

stra

lia

Japa

n

Ger

man

y

Chin

a

Hon

g Ko

ng

(%)

16.7

(6.6) (4.3) (2.6)

(24.9)

(15.3)(11.5)

(5.7)(10.4)

16.4

4.4

38.1

(17.3)(30.0)

(20.0)

(10.0)

-

10.0

20.0

30.0

40.0

50.0

Ru

ssia

S.Ko

rea

USA

S&P

Bra

zil

Indo

nesi

a

FTSE

Indi

a

Au

stra

lia

Japa

n

Ger

man

y

Chin

a

Hon

g Ko

ng

(%)

LilladherPrabhudas IT and Healthcare sectors leads the way

• MoM: Despite the carnage that we had seen in the last month, both IT and Healtcare sector have given positive returns. Healthcare sector has been the star performer of the last one month and have out performed in the last one month. Strong performance from Infosys and Cognizant has been one of the reasons for the relative out performance. Low crude oil prices led to a strong performance from the downstream oil marketing companies, while metals, realty and up stream oil companies disappoint with steel prices reaching a 16 year low.

• YTD and YoY: On a YTD and YoY basis, Capital goods, Health care, IT and FMCG continue to have a strong performance, while Metals and Realty continue to languish.

Source: Bloomberg, PL Research

Source: Bloomberg, PL Research

Month-on-Month

Year-on-Year

Source: Bloomberg, PL Research

Calendar Year-to-date

9/9/2015 12

3.4 2.2

(4.7) (5.5)

(9.6) (10.3)(12.2)

(13.9) (14.0) (15.1) (16.4)(20.0)

(15.0)

(10.0)

(5.0)

-

5.0

(%)

29.9

7.4 11.2 5.7

(31.1)

(2.3)

(24.7)

1.4 1.0

(15.7)

(43.3)(50.0)(40.0)(30.0)(20.0)(10.0)

-10.0 20.0 30.0 40.0

(%)

20.6

6.1 10.7

0.1

(19.1)

(7.4)(12.6) (12.9)

1.0

(15.7)

(33.3)(40.0)

(30.0)

(20.0)

(10.0)

-

10.0

20.0

30.0

(%)

LilladherPrabhudas Small and Midcaps underperform

• MoM: After periods of strong out performance, Small caps and Mid caps have underperformed in the last one month.

• YoY: The Mid cap index continue to out perform over the last six months and twelve months, while the small cap index has out performed over the last twelve months, while it has underperformed the large caps over the six month period.

Source: Bloomberg, PL Research

Source: Bloomberg, PL Research

Month-on-Month

Year-on-Year

Source: Bloomberg, PL Research

Calendar Year-to-date

9/9/2015 13

(7.3)

(8.6) (8.6)(9.1)(10.0)

(9.0)

(8.0)

(7.0)

(6.0)

(5.0)

(4.0)

(3.0)

(2.0)

(1.0)

-

BSEMDCAP Index BSE500 Index BSE100 Index BSESMCAP Index

(%)

14.9

(0.4)

(3.5)

4.7

(5.0)

-

5.0

10.0

15.0

20.0

BSEMDCAP Index BSE500 Index BSE100 Index BSESMCAP Index

(%)

3.6

(3.9)

(5.4)

(2.7)

(6.0)

(5.0)

(4.0)

(3.0)

(2.0)

(1.0)

-

1.0

2.0

3.0

4.0

5.0

BSEMDCAP Index BSE500 Index BSE100 Index BSESMCAP Index

(%)

LilladherPrabhudas Global Currencies – A painful month

• MoM: Emerging market currencies continued to be under pressure with both Brazil and Malaysia being the worst hit with losses of over 9%, followed by South Africa, Indonesia, Turkey and Russia at around 5% each.

• CYTD and YoY: On a CYTD basis, Brazil is the worst performer(41.5%) followed by Turkey(26.1%) and Malaysia (21.1%). On a y-o-y basis, Russia(82.2%), Brazil (67.6%), Turkey(36.5%), Malaysia(33.0%) and South Africa (25.7%) were the biggest losers.

Source: Bloomberg, PL Research

Source: Bloomberg, PL Research

Month-on-Month

Year-on-Year

Source: Bloomberg, PL Research

Calendar Year-to-date

9/9/2015 14

3.7 2.8

1.9

(0.1)(0.8)

(2.0)(2.2)(2.3)(2.4)(2.4)(2.8)(3.5)(4.9)

(5.6)(5.9)(5.9)

(9.0)(9.8)(12.0)

(10.0)

(8.0)

(6.0)

(4.0)

(2.0)

-

2.0

4.0

6.0

(%)

14.1

(0.6)

1.8 2.5

(14.1)(9.0)(8.9)

(4.5)(2.4)

7.3

(2.8)(5.1)

(14.4)(10.5)

(26.1)

(16.1)

(41.5)

(21.0)

(50.0)

(40.0)

(30.0)

(20.0)

(10.0)

-

10.0

20.0

(%)

24.9

(15.0)

7.1

(5.7)

(21.8)(16.6)(11.9)(7.2)(3.5)

14.7

(8.7)(9.6)(20.5)

(82.2)

(36.5)(25.7)

(67.6)

(33.0)

(100.0)

(80.0)

(60.0)

(40.0)

(20.0)

-

20.0

40.0

(%)

LilladherPrabhudas FII outflows in second half of August

• FIIs were net sellers in August 2015 to the extent of Rs172.09bn(US$2.64bn) , while the DIIs were net buyers to the extent of Rs162.48bn(US$2.50bn). The domestic inflows continue to remain encouraging with strong positive flows with the CYTD flows at Rs438.72bn(US$6.75bn) as against an outflow of Rs303.2bn(US$5bn) in CY2014.

9/9/2015 15

(200.00)(150.00)(100.00)

(50.00)-

50.00 100.00 150.00 200.00 250.00

Jan

-13

Feb

-13

Mar

-13

Ap

r-1

3M

ay-1

3Ju

n-1

3Ju

l-13

Au

g-1

3Se

p-1

3O

ct-1

3N

ov-

13

Dec

-13

Jan

-14

Feb

-14

Ma

r-1

4A

pr-1

4M

ay-1

4Ju

n-1

4Ju

l-14

Aug

-14

Sep

-14

Oct

-14

Nov

-14

Dec

-14

Jan

-15

Feb

-15

Mar

-15

Apr

-15

Ma

y-1

5Ju

n-1

5Ju

l-15

Aug

-15

DII Net Cash Market FII Net Cash Market

CY13 - Total FII buying Rs1,112.77bn against DII net

selling at Rs-734.64bn

CY14FII Rs970.68bnDII Rs-303.21bn

CY15FII Rs438.72bnDII Rs264.10bn

LilladherPrabhudas Global Agri commodities - Sugar and wheat

weaken further • Wheat, sugar, corn, palm oil and soya all continue to have a

weak performance in the last one month. Only rice recovered 2.4% following the 4.8% recovery seen in July 2015. On a 12 month performance, all these commodities continue to remain under pressure with sugar and wheat being the largest losers at 42.7% and 21.2% respectively.

• Sugar continues to be under severe pressure as the Brazilian currency gets hammered, and with Brazil being the largest exporter of sugar is taking the brunt of it.

• Despite the expected effects of El Nino leading to shortages in agricultural commodities, the agricultural commodities continue to remain under pressure.

Source: Bloomberg, PL Research

Source: Bloomberg, PL Research *Price in US$

Performance of Global Agricultural Commodities

Year-on-Year Performance

Source: Bloomberg, PL Research *Price in US$

Month-on-Month Performance

9/9/2015 16

50

60

70

80

90

100

110

120

130

Sep

-14

Oct

-14

No

v-1

4

Dec

-14

Jan

-15

Feb

-15

Mar

-15

Apr

-15

May

-15

Jun

-15

Jul-

15

Aug

-15

Sep

-15

Rice Wheat Corn Soya Plam Oil Sugar

2.4

(1.5)

(2.8)

(5.7)(6.6)

(8.4)(10.0)

(8.0)

(6.0)

(4.0)

(2.0)

-

2.0

4.0

Rice Sugar Corn Wheat Soya Palm Oil

(%)

(8.9)

(42.7)

(7.5)

(21.2)

(15.3)

(4.4)

(45.0)

(40.0)

(35.0)

(30.0)

(25.0)

(20.0)

(15.0)

(10.0)

(5.0)

-

Rice Sugar Corn Wheat Soya Palm Oil

(%)

LilladherPrabhudas Global Industrial Commodities continues to

decline • The global commodities continue to remain under

pressure during the last one month. The performance of both the BSE Metal index as well as the NSE Metal index reflect this trend. While crude was up 1.3% in the last one month, Nickel was the biggest loser at 10.5%. On a YoY basis, all the global commodities, Thermal Coal, Lead, Aluminum, inc, Copper, Nickel and Brent Crude, all have lost over 20% with Brent having lost over 51.1% during the period.

Source: Bloomberg, PL Research *Price in US$

Source: Bloomberg, PL Research *Price in US$

Month-on-Month

Year-on-Year

Source: Bloomberg, PL Research *Price in US$

Calendar Year-to-date

9/9/2015 17

1.3 0.3

(0.2) (0.6)(1.6)

(7.0)

(10.5)(12.0)

(10.0)

(8.0)

(6.0)

(4.0)

(2.0)

-

2.0

Brent crude

Lead Aluminium Thermal Coal

Copper Zinc Nickel

(%)

(51.1)

(23.9) (24.4) (25.4) (26.4) (24.8)

(46.7)

(60.0)

(50.0)

(40.0)

(30.0)

(20.0)

(10.0)

-

Brent

crude

Lead Aluminium Thermal

Coal

Copper Zinc Nickel

(%)

(11.1)(7.8)

(13.5)

(2.0)

(19.3)(17.6)

(34.7)(40.0)

(35.0)

(30.0)

(25.0)

(20.0)

(15.0)

(10.0)

(5.0)

-

Brent

crude

Lead Aluminium Thermal

Coal

Copper Zinc Nickel

(%)

LilladherPrabhudas Equity markets weak across the board

Sources : Bloomberg

• Following the weather induced contraction in the first quarter of CY2015, the US economy grew at 2.3% in the second quarter of 2015 supported by strong spending in consumer spending, government outlays and exports. The strong Dollar and the increasing retrenchment in energy sector created headwinds which could challenge the growth forecasts of 2.4%. The non farm payroll increased by 173,000 jobs in August 2015 after seeing an average monthly gain of 247,000 in the previous 12 months, keeping the un employment levels at a new low of 5.1%. The pay roll addition for June and July were revised upwards to 245,000 each from 231,000 and 215,000 respectively.

• The Eurozone has continued to benefit from the low commodity prices. The momentum was expected to ebb in the second half, however the same has already started taking effect. The Euro zone grew by 0.3% in 2QCY15 with Germany growing by 0.4% and France reporting zero growth. The benefits from a weak oil price, weak euro, easy monetary policies and a more prudent fiscal policy is being offset by the weak investment demand in Germany and France.

• The Chinese government in early August adjusted the exchange rate in a way that allowed the Renminbi to depreciate against the Dollar, This devaluation pushed down commodity prices as well as emerging market currencies which was already under pressure ahead of a possible US Fed rate increase.

• Nifty after touching a high of 8,996 had corrected, but with the strong FII selling that we have witnessed in the second half of August of Rs172.09bn, the market has been correcting sharply. We believe that till the time the FII selling subsides, the market direction continues to look negative, though the Nifty at 7,688 looks attractive at 16.3X September 16 earnings, closer to the ten year average.

World Equity Indices:

9/9/2015 18

Index Country Value YTD (%) 1 Week (%) 1 Mth (%) 3 Mth (%)

Dow Jones USA 16,493 (7.46) (0.21) (5.07) (7.16)

S&P 500 USA 1,969 (4.35) (0.14) (5.21) (5.32)

Nasdaq USA 4,812 1.60 0.74 (4.59) (4.03)

FTSE 100 LONDON 6,146 (6.40) 1.45 (8.52) (9.00)

DAX GERMANY 10,271 4.75 2.55 (10.61) (6.63)

CAC 40 FRANCE 4,598 7.62 1.26 (10.80) (5.19)

Nikkei JAPAN 18,403 5.45 1.70 (11.20) (8.43)

TSX CANADA 13,631 (6.85) (1.65) (4.70) (8.01)

MICEX RUSSIA 1,714 22.74 0.95 1.40 3.02

JSE SA 44,107 0.31 2.62 (5.01) (2.84)

SGX SA 7,688 (7.18) (1.25) (10.23) (4.17)

TING TURKEY 88,474 (16.65) (1.99) (8.00) (7.19)

IBOV BRAZIL 46,762 (6.49) 0.29 (3.74) (11.46)

Jakarta Comp INDONESIA 4,332 (17.13) (1.58) (9.19) (11.60)

PSEI Phillipine PHILIPPINES 6,938 (4.05) (1.91) (7.90) (5.27)

SE THAI 50 THAILAND 898 (10.33) 0.98 (4.04) (8.53)

Euro Stoxx EUROZONE 3,234 2.78 1.41 (11.10) (6.45)

IBEX 35 SPAIN 9,866 (4.02) (1.27) (11.74) (9.80)

Hang Seng HONG KONG 21,780 (7.73) 2.80 (11.29) (19.30)

AS30 AUSTRALIA 5,218 (3.16) 1.93 (4.65) (4.77)

Shanghai CHINA 3,242 0.24 1.14 (13.40) (36.59)

Taiwan TAIWAN 8,232 (11.55) 2.45 (2.49) (10.44)

Kospi KOREA 1,921 0.28 0.30 (4.44) (6.93)

CNX Nifty INDIA 7,688 (7.18) (1.25) (10.23) (4.17)

BSE Sensex INDIA 25,318 (7.93) (1.47) (10.34) (4.39)

KLCI MALAYSIA 1,601 (9.11) 0.67 (4.86) (7.42)

NZX 50 NEWZEALAND 5,668 1.79 1.39 (3.42) (3.32)

MEXBOL MEXICO 43,084 (0.14) 0.40 (3.96) (3.22)

LilladherPrabhudas Indian Market – Valuation and Strategy

• NIFTY earnings estimates for FY16 revised downwards: With the global recovery taking more time than expected and with the domestic activity being subdued, we have seen the FY16 EPS estimate getting revised downwards to Rs436.9 from the earlier estimates of Rs448.3 and the FY17 estimates to Rs.524.1 from 541.0. There definitely seems to be an improvement in the confidence levels in IT companies, as Infosys have come outwit h a strong set of numbers for 1QFY16 and their guidance was also positive. However the global commodity prices continues to remain under pressure with the Renminbis devaluation not helping their cause. With the strong preference for risk aversion, the Emerging markets have been under pressure and India is not exempted from the rout though we continue to strongly believe that India is on a relatively on a better positioning. Reflecting the sentiments, we are revising our near term trading range for the market to 7500-8200 levels. NIFTY at 7688 is trading at 17.6 FY16E and at 14.7 FY17E estimated free-float earnings. The last ten-year average for NIFTY’s one-year forward PE is at 16.0x, implying the NIFTY at 16.4x (12 month forward multiple for Sep 16 EPS of Rs470.5) is continuing to trade at a marginal premium to its last 10-years average of one-year forward multiple of 16.0x. We have already seen a 12% reduction in EPS estimates for FY16 since April 2015.

• The earnings growth is expected to be led by sectors namely financials, Automobiles, Oil& Gas, FMCG, Pharma and IT. Going forward, we expect the slippages to be lower than what we saw in FY15 and hence the provisioning is expected to be lower leading to higher net earnings, Automobiles, with good performance from both the PCs and the CVs though the Motorcycles continue to see headwinds, The benign crude oil prices helping the earnings growth of the downstream oil companies and FMCGs though the demand becomes an issue for FMCGs . Good export potential keeps the pharma sector in limelight with optimistic demand environment and a weak currency keeps IT in demand.

• The chart on Page 20 indicates MSCI India’s premium to MSCI Asia (excluding Japan) over the last ten years. The average of the last 10-year’s premium was at 28% and the current premium is at 37%. The out performance of the Indian market has been behind this and the recent relative strength of the currency and the out performance have resulted in the market becoming expensive Vs peers. Despite the same, the relative strength of the economy among the EMs is expected be beneficial. We continue to believe that the superior economic fundamentals and political and policy scenario will keep the Indian markets at a premium to peers in the region for the near term.

• The South west monsoon has been below normal so far by 12% till 02 September 2015. With the southern peninsula receiving a large deficit of 22% in rainfall, the demand levels and the rural income impact these areas are going to be crucial for the FMCG companies. Though the rains have seen an improvement from the initial large deficiencies, in most of the sub divisions, the rainfall have been below normal. The effect of the crop losses in the rural consumption is not yet clear, yet it is expected that this could slow down the rural consumption which is something which needs to watched out for the FMCG companies in particular.

• The near term trading range for the Nifty seems to be between 7500-8200 levels, given the current weakness. Given the headwinds that we are seeing in emerging markets and in currencies, we are revising our 12 month Nifty target down to 8800-9000 levels. The commentaries on future outlook remains robust and we believe that this makes us more bullish on the sector. We continue to remain overweight in Financial services, while remaining neutral in IT, Automobiles, FMCG, Healthcare and Engineering &Capital Goods.

9/9/2015 19

LilladherPrabhudas Nifty Valuations: Historic Trends

Source: Bloomberg, PL Research

Nifty 1-year forward P/E

Source: Bloomberg, PL Research

MSCI India Premium to MSCI Asia (Ex‐Japan)

9/9/2015 20

37%37%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

Se

p-0

5

Dec

-05

Mar

-06

Jun-

06

Se

p-0

6

Dec

-06

Mar

-07

Jun-

07

Se

p-0

7

Dec

-07

Mar

-08

Jun-

08

Se

p-0

8

Dec

-08

Mar

-09

Jun-

09

Se

p-0

9

De

c-0

9

Mar

-10

Jun-

10

Se

p-1

0

De

c-1

0

Mar

-11

Jun-

11

Sep-

11

De

c-1

1

Mar

-12

Jun-

12

Sep-

12

De

c-1

2

Mar

-13

Jun-

13

Sep-

13

De

c-1

3

Mar

-14

Jun-

14

Sep-

14

De

c-1

4

Mar

-15

Jun-

15

Se

p-1

5

10 year Avg.

28%

16.4

-

5.0

10.0

15.0

20.0

25.0

30.0

Sep

-05

Dec

-05

Mar

-06

Jun-

06

Sep

-06

De

c-0

6

Mar

-07

Jun-

07

Sep

-07

Dec

-07

Mar

-08

Jun-

08

Sep

-08

De

c-0

8

Mar

-09

Jun-

09

Sep

-09

Dec

-09

Mar

-10

Jun-

10

Sep

-10

De

c-1

0

Mar

-11

Jun-

11

Sep

-11

Dec

-11

Mar

-12

Jun-

12

Sep

-12

De

c-1

2

Mar

-13

Jun-

13

Sep

-13

De

c-1

3

Mar

-14

Jun-

14

Sep

-14

De

c-1

4

Mar

-15

Jun-

15

Sep

-15

10 year Avg.

16.0x

LilladherPrabhudas Nifty Valuation

9/9/2015 21

Note: Telecom Nos. are Bloomberg Consensus / Sector Weightages are updated as on September 08, 2015

Weight-

age (%)FY14 FY15 FY16E FY17E

Weight-

age (%)FY14 FY15 FY16E FY17E

Banking & Fin. 30.3% Cement 2.9%

PER (x) 20.8 18.5 15.6 13.0 PER (x) 25.7 28.8 28.8 21.9

PAT Growth (%) 2.4 12.6 18.3 20.0 PAT Growth (%) (15.5) (10.5) (0.2) 31.4

Technology 17.3% Telecom 2.4%

PER (x) 24.5 22.0 19.3 17.0 PER (x) 40.7 23.1 20.0 19.3

PAT Growth (%) 28.6 11.2 13.9 13.8 PAT Growth (%) 44.2 76.7 15.1 3.9

FMCG 10.1% Media 0.7%

PER (x) 38.3 35.6 31.4 27.3 PER (x) 39.0 35.6 33.6 26.5

PAT Growth (%) 13.4 7.7 13.1 15.3 PAT Growth (%) 24.0 9.6 5.8 26.8

Auto 9.0% Nifty as on Sep 08 7,688

PER (x) 17.8 16.5 15.1 11.9

PAT Growth (%) 22.0 8.4 9.2 26.4 EPS (Rs) - Free Float 354.9 373.5 436.9 524.1

Growth (%) 4.8 5.2 17.0 20.0

Pharma 8.4% PER (x) 21.7 20.6 17.6 14.7

PER (x) 37.9 40.2 35.0 29.5

PAT Growth (%) 38.5 (5.7) 14.7 18.6 EPS (Rs) - Free Float

Nifty Cons. 354.9 373.5 451.7 548.8

Oil & Gas 8.2% Var. (PLe v/s Cons.) (%) - - (3.3) (4.5)

PER (x) 8.5 11.0 9.4 8.3

PAT Growth (%) 10.6 (22.5) 16.5 14.3 Sensex as on Sep 08 25,318

Eng. & Power 7.5% EPS (Rs) - Free Float 1,184.9 1,238.0 1,347.8 1,628.6

PER (x) 15.9 17.8 14.8 12.7 Growth (%) 11.5 4.5 8.9 20.8

PAT Growth (%) (17.4) (10.5) 20.0 16.8 PER (x) 21.4 20.5 18.8 15.5

Metals 3.2%

PER (x) 9.6 60.2 12.2 9.4 Sensex Cons. 1,184.9 1,238.0 1,373.8 1,670.2

PAT Growth (%) 7.2 (84.1) 392.5 30.5 Var. (PLe v/s Cons.) (%) - - (1.9) (2.5)

LilladherPrabhudas Top Pick Summary

9/9/2015 22

2016E 2017E 2016E 2017E 2016E 2017E 2016E 2017E 2016E 2017E 2016E 2017E

Large Cap

HDFC Bank 1,004 1,200 19.5% 2,516.6 20.8 21.8 20.1 24.2 18.7 20.0 1.9 2.0 20.1 16.2 3.7 3.2

Infosys 1,059 1,340 26.6% 2,422.5 13.6 14.6 8.8 17.7 23.1 24.2 23.1 24.2 18.1 15.3 4.0 3.5

State Bank of India 228 350 53.3% 1,704.8 11.7 11.7 16.3 19.7 11.3 12.3 0.7 0.7 11.2 9.3 1.6 1.4

ICICI Bank 261 390 49.5% 1,512.2 17.1 18.8 14.6 15.6 15.0 15.5 1.8 1.8 11.8 10.2 2.1 1.8

Larsen & Toubro 1,565 2,000 27.8% 1,454.3 15.0 20.0 31.7 25.4 14.2 16.0 5.7 6.3 25.0 20.0 3.2 2.9

Maruti Suzuki 4,139 4,712 13.8% 1,250.4 15.7 19.2 42.5 34.6 20.5 23.1 20.6 23.1 23.6 17.6 4.5 3.7

Tata Motors 331 518 56.5% 1,065.1 4.8 16.3 (12.8) 26.7 21.8 21.3 12.6 13.5 7.6 6.0 1.4 1.2

Indian Oil Corporation 392 548 39.7% 952.6 (9.4) 5.4 155.7 2.0 17.2 15.7 10.9 10.6 7.6 7.4 1.2 1.1

IndusInd Bank 840 1,050 24.9% 456.7 25.3 25.1 19.8 25.7 15.9 15.4 1.8 1.9 20.9 16.6 2.9 2.5

Mid Caps

Glenmark Pharmaceuticals 1,006 1,186 17.9% 272.9 25.8 37.4 130.0 89.8 27.2 33.8 15.5 23.7 25.0 13.2 5.3 3.8

Cummins India 1,055 1,285 21.8% 292.6 16.6 18.3 21.7 29.8 27.4 30.3 27.3 30.0 34.1 26.3 8.8 7.3

Motherson Sumi Systems 281 400 42.1% 248.1 15.7 20.2 (9.2) 58.4 35.7 43.1 21.3 29.3 27.9 17.6 8.9 6.6

Aurobindo Pharma 727 761 4.8% 212.2 15.5 14.7 (38.7) 24.8 34.1 32.6 21.3 22.9 21.2 17.0 6.4 4.9

MindTree 1,319 1,500 13.7% 110.4 24.3 18.7 13.9 14.8 26.9 24.8 26.5 24.5 18.1 15.7 4.4 3.5

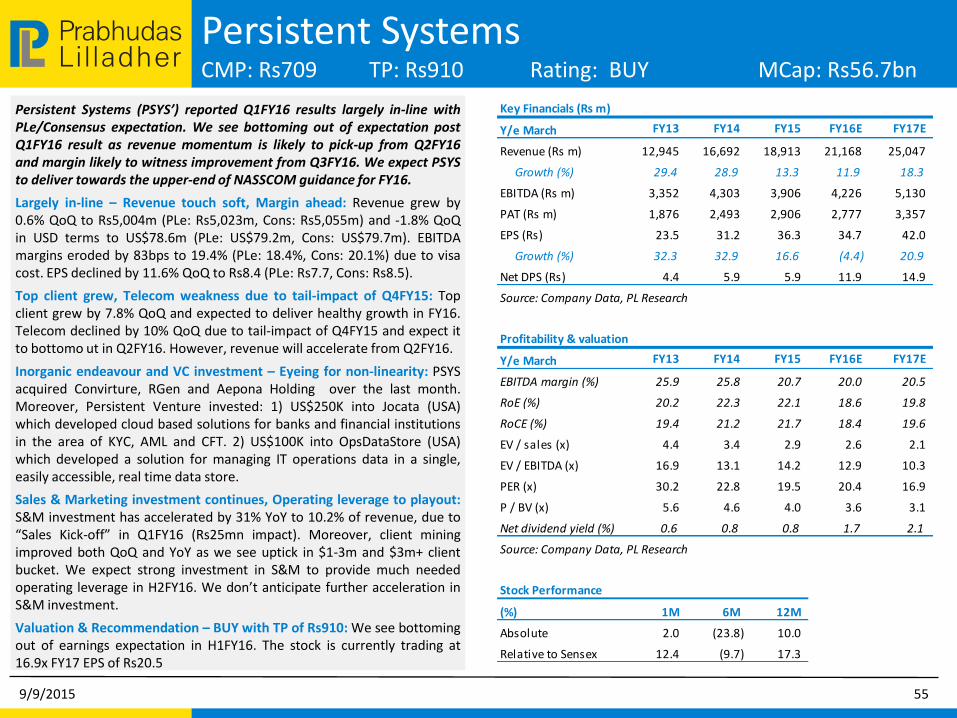

Persistent Systems 709 910 28.4% 56.7 11.9 18.3 (4.4) 20.9 18.6 19.8 18.4 19.6 20.4 16.9 3.6 3.1

Jubilant Life Sciences 306 578 89.1% 48.7 13.3 12.4 NA 39.0 19.6 21.9 12.2 14.6 9.0 6.5 1.6 1.3

Sadbhav Engineering 284 380 34.0% 48.1 18.0 26.4 24.1 43.0 9.9 12.8 8.8 11.0 34.0 23.8 3.2 2.9

JK Lakshmi Cement 360 450 25.0% 42.4 21.8 22.1 (86.5) 825.4 1.5 13.1 4.3 8.9 209.1 22.6 3.1 2.8

Rallis India 207 270 30.3% 40.3 11.6 14.9 19.3 22.3 21.5 22.8 27.7 30.6 21.5 17.6 4.3 3.7

Va Tech Wabag 666 1,000 50.2% 36.2 12.5 12.5 28.4 23.6 14.7 16.1 11.7 12.4 25.6 20.7 3.6 3.1

* For Banks P/ABV

RoE (%)Upside

Mcap

(Rs bn)

RoCE (%)CMP (Rs.) TP (Rs)

Revenue Growth (%) Earnings Growth (%) PER (x) P/BV (x)*

LilladherPrabhudas

LARGE CAP

9/9/2015 23

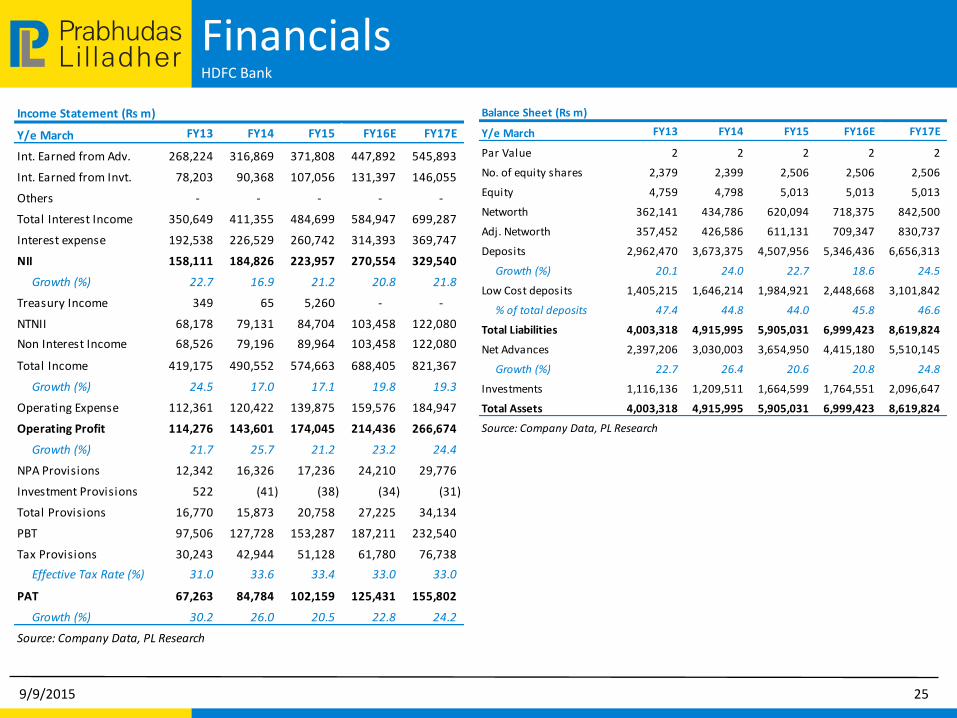

LilladherPrabhudas HDFC Bank

CMP: Rs1,004 TP: Rs1,200 Rating: BUY MCap: Rs2,516.6bn

Revenue growth remains impressive: HDFCB delivered ~25% YoY growth in core revenues led by strong growth in NII and robust core fees/FX income/recovery from written‐off accounts. Core other income grew 28% YoY and HDFCB had treasury gains of Rs1.26bn during the quarter which boosted overall other income growth to 33% YoY. NII growth was led by healthy loan growth and better retail mix. Margins, however, compressed by 10bps QoQ as CASA mix declined 440bps QoQ to 39.6% led by sharp surge in time deposits. HDFCB opened 87 branches during the quarter & increased its branch network to 4,101.

Loan growth remains healthy; retail mix increases by 173bps QoQ: Overall loan growth stood at ~22% YoY (4.5% QoQ) led by healthy growth in retail portfolio ‐ particularly personal loans, home loan and business banking segments, all of which reported double‐digit sequential growth. Wholesale loan book reported muted 1% QoQ growth. The mix of retail loans has, thus, increased by 173bps QoQ to ~49%. HDFCB indicated healthy loan growth prospects on underlying improvement in product segments where it has gained market share and as it benefits from increasing footprint.

Asset quality broadly stable; outlook remains positive: GNPLs increased by 6% QoQ as bank reported a slippage rate of 1.4% (annualized), largely belonging to agriculture & SME segment. Coverage ratio declined by 207bps QoQ, while outstanding restructured assets stood at 0.1% of total loans. HDFCB made floating provisions of Rs650m, taking the total quantum of such provisions to Rs15.9bn. We maintain our earnings estimates and ‘BUY’ rating with a PT of Rs1,200.

9/9/2015 24

Key Financials (Rs m)

Y/e March FY13 FY14 FY15 FY16E FY17E

Net interest income 158,111 184,826 223,957 270,554 329,540

Growth (%) 22.7 16.9 21.2 20.8 21.8

Operating profit 114,276 143,601 174,045 214,436 266,674

PAT 67,263 84,784 102,159 125,431 155,802

EPS (Rs) 28.5 35.5 41.7 50.0 62.2

Growth (%) 28.7 24.7 17.4 20.1 24.2

Net DPS (Rs) 5.5 6.8 8.0 9.0 10.5

Source: Company Data, PL Research

Profitability & valuation

Y/e March FY13 FY14 FY15 FY16E FY17E

NIM (%) 4.6 4.4 4.3 4.4 4.4

RoAE (%) 20.3 21.3 19.4 18.7 20.0

RoAA (%) 1.8 1.9 1.9 1.9 2.0

P / BV (x) 6.6 5.5 4.1 3.5 3.0

P / ABV (x) 6.8 5.9 4.3 3.7 3.2

PE (x) 35.3 28.3 24.1 20.1 16.2

Net dividend yield (%) 0.5 0.7 0.8 0.9 1.0

Source: Company Data, PL Research

Stock Performance

(%) 1M 6M 12M

Absolute (8.1) (7.5) 16.1

Relative to Sensex 2.2 6.6 23.4

LilladherPrabhudas Financials

HDFC Bank

9/9/2015 25

Income Statement (Rs m)

Y/e March FY13 FY14 FY15 FY16E FY17E

Int. Earned from Adv. 268,224 316,869 371,808 447,892 545,893

Int. Earned from Invt. 78,203 90,368 107,056 131,397 146,055

Others - - - - -

Total Interest Income 350,649 411,355 484,699 584,947 699,287

Interest expense 192,538 226,529 260,742 314,393 369,747

NII 158,111 184,826 223,957 270,554 329,540

Growth (%) 22.7 16.9 21.2 20.8 21.8

Treasury Income 349 65 5,260 - -

NTNII 68,178 79,131 84,704 103,458 122,080

Non Interest Income 68,526 79,196 89,964 103,458 122,080

Total Income 419,175 490,552 574,663 688,405 821,367

Growth (%) 24.5 17.0 17.1 19.8 19.3

Operating Expense 112,361 120,422 139,875 159,576 184,947

Operating Profit 114,276 143,601 174,045 214,436 266,674

Growth (%) 21.7 25.7 21.2 23.2 24.4

NPA Provisions 12,342 16,326 17,236 24,210 29,776

Investment Provisions 522 (41) (38) (34) (31)

Total Provisions 16,770 15,873 20,758 27,225 34,134

PBT 97,506 127,728 153,287 187,211 232,540

Tax Provisions 30,243 42,944 51,128 61,780 76,738

Effective Tax Rate (%) 31.0 33.6 33.4 33.0 33.0

PAT 67,263 84,784 102,159 125,431 155,802

Growth (%) 30.2 26.0 20.5 22.8 24.2

Source: Company Data, PL Research

Balance Sheet (Rs m)

Y/e March FY13 FY14 FY15 FY16E FY17E

Par Value 2 2 2 2 2

No. of equity shares 2,379 2,399 2,506 2,506 2,506

Equity 4,759 4,798 5,013 5,013 5,013

Networth 362,141 434,786 620,094 718,375 842,500

Adj. Networth 357,452 426,586 611,131 709,347 830,737

Deposits 2,962,470 3,673,375 4,507,956 5,346,436 6,656,313

Growth (%) 20.1 24.0 22.7 18.6 24.5

Low Cost deposits 1,405,215 1,646,214 1,984,921 2,448,668 3,101,842

% of total deposits 47.4 44.8 44.0 45.8 46.6

Total Liabilities 4,003,318 4,915,995 5,905,031 6,999,423 8,619,824

Net Advances 2,397,206 3,030,003 3,654,950 4,415,180 5,510,145

Growth (%) 22.7 26.4 20.6 20.8 24.8

Investments 1,116,136 1,209,511 1,664,599 1,764,551 2,096,647

Total Assets 4,003,318 4,915,995 5,905,031 6,999,423 8,619,824

Source: Company Data, PL Research

LilladherPrabhudas Infosys

CMP: Rs1,059 TP: Rs1,340 Rating: BUY MCap: Rs2,422.5bn

Infosys’ Q1FY16 performance was ahead of expectation on all counts with upward revision of FY16 revenue guidance and Aspiration 2020 reiterated. Infosys’ initiatives over the last one year are showing signs of early success. Management remains confident of achieving industry leading growth by FY17. Full benefits of the management efforts will be visible in H2FY16 and that will drive multiple expansion. However, volatility in demand environment and macro challenges could yield negative surprises.

Strong beat to expectation in 1QFY16: Revenue grew by 4.5% (4.4%@cc) QoQ, ahead of the most bullish expectation (Cons./PLe: +3%/2.6%). Q1FY16 performance (both in terms of volume and USD revenue growth) was the strongest Q1 since Q1FY11. We see the quarter performance as an early sign of success of new initiatives like 1) Focus on Top 15 clients from CEO office, 2) Centralized team for large deal RFPs, 3) Investment in automation, platform, & solution, 4) Offering solution using “DT”.

Concern on margin – Strong growth could resolve: EBITDA margin have likely bottomed out in Q1FY16. We expect Infosys to achieve its stated objective of improving EBIT margin to 30% by 2020 and retaining EBIT margin at 25% (-/+1%) in the near term driven by: 1) Investments in automation, solution, & platforms. 2) Focus on increasing Rev/Emp, 3) Improving client mining, 4) Improvement in Utilization which is lower than peers like TCS.

Upward revision of guidance – Alienate sceptics: FY16 USD revenue guidance has been revised upward to 7.2-9.2% YoY (from 6.2-8.2%). We expect momentum to accelerate as Infosys enters the strongest quarter putting low-double digit growth at sight. Management indicated seasonality impact on H2FY16 to be possibly lower than usual.

Valuation & Recommendation – Retain ‘BUY’, revise TP to Rs1,340: We expect initiatives translating into improved growth momentum in FY16. The stock is currently trading at 15.3x FY17E EPS of Rs69.

9/9/2015 26

Key Financials (Rs m)

Y/e March FY13 FY14 FY15 FY16E FY17E

Revenue (Rs m) 403,520 501,330 533,190 605,695 693,964

Growth (%) 19.6 24.2 6.4 13.6 14.6

EBITDA (Rs m) 115,580 134,150 149,000 164,173 186,656

PAT (Rs m) 94,210 106,480 123,290 134,172 157,957

EPS (Rs) 41.2 46.5 53.9 58.6 69.0

Growth (%) (71.7) 13.0 15.8 8.8 17.7

Net DPS (Rs) 10.5 15.7 22.2 30.0 34.9

Source: Company Data, PL Research

Profitability & valuation

Y/e March FY13 FY14 FY15 FY16E FY17E

EBITDA margin (%) 28.6 26.8 27.9 27.1 26.9

RoE (%) 25.7 24.4 24.1 23.1 24.2

RoCE (%) 25.6 24.3 24.0 23.1 24.2

EV / sales (x) 5.5 4.3 4.0 3.4 2.9

EV / EBITDA (x) 19.1 16.1 14.2 12.7 10.9

PER (x) 25.7 22.8 19.6 18.1 15.3

P / BV (x) 6.1 5.1 4.4 4.0 3.5

Net dividend yield (%) 1.0 1.5 2.1 2.8 3.3

Source: Company Data, PL Research

Stock Performance

(%) 1M 6M 12M

Absolute (3.4) (5.8) 12.0

Relative to Sensex 7.0 8.2 19.3

LilladherPrabhudas Financials

Infosys

9/9/2015 27

Income Statement (Rs m)

Y/e March FY13 FY14 FY15 FY16E FY17E

Net Revenue 403,520 501,330 533,190 605,695 693,964

Direct Expenses 241,510 307,670 318,150 367,054 422,507

% of Net Sales 59.9 61.4 59.7 60.6 60.9

Employee Cost - - - - -

% of Net Sales 0.0 0.0 0.0 0.0 0.0

SG&A Expenses 46,430 59,510 66,040 74,468 84,802

% of Net Sales 11.5 11.9 12.4 12.3 12.2

Other Expenses - - - - -

% of Net Sales 0.0 0.0 0.0 0.0 0.0

EBITDA 115,580 134,150 149,000 164,173 186,656

Margin (%) 28.6 26.8 27.9 27.1 26.9

Depreciation 11,290 13,740 10,680 12,621 13,152

PBIT 104,290 120,410 138,320 151,551 173,504

Interest Expenses - - - - -

PBT 127,880 147,100 172,590 183,797 213,455

Total tax 33,670 40,620 49,290 49,625 55,498

Effective Tax rate (%) 26.3 27.6 28.6 27.0 26.0

PAT 94,210 106,480 123,290 134,172 157,957

Extraordinary Gain/(Loss) - - - - -

Adjusted PAT 94,210 106,480 123,290 134,172 157,957

Source: Company Data, PL Research

Balance Sheet (Rs m)

Y/e March FY13 FY14 FY15 FY16E FY17E

Share Capital 11,440 11,440 11,440 11,440 11,440

Reserves & Surplus 355,630 432,960 508,130 573,760 651,752

Shareholder's Fund 397,970 475,300 547,630 613,260 691,252

Preference Share Capital - - - - -

Total Debt - - - - -

Other Liabilities(net) 1,490 3,230 460 460 460

Deferred Tax Liability 1,190 640 1,600 1,600 1,600

Total Liabilities 400,650 479,170 549,690 615,320 693,312

Gross Block 106,760 134,120 155,470 180,303 208,756

Less: Depreciation 42,080 55,250 64,220 76,841 89,993

Net Block 64,680 78,870 91,250 103,462 118,763

Capital Work in Progress - - - - -

Cash & Cash Equivalent 235,710 292,210 313,420 346,173 393,628

Total Current Assets 335,740 397,480 462,210 505,686 577,808

Total Current Liabilities 62,860 91,380 113,830 103,888 113,320

Net Current Assets 272,880 306,100 348,380 401,798 464,488

Other Assets 45,700 61,490 100,310 100,310 100,310

Total Assets 400,650 479,170 549,690 615,320 693,312

Source: Company Data, PL Research

LilladherPrabhudas State Bank of India

CMP: Rs228 TP: 350 Rating: BUY MCap: Rs1,727.7bn

SBIN has been reporting declining trend in slippages for few quarters.

Margins have been under pressure as cost of deposits remain sticky while

lending yield declined due to recent cut in base rate. However, we expect

trends to improve as deposit portfolio re-prices gradually. SBIN is well

capitalized and has a very strong liability franchise which the bank will

be able to leverage as credit growth revives, meanwhile push into retail

will remain the focus area in FY16.

Other income drives revenue growth; NII disappoints: During Q1FY16,

SBIN reported 20% YoY growth in other income, led by strong treasury

gains (Rs8.7 bn), modest growth in fee income and higher recoveries from

written‐off account (Rs4.3 bn). NII growth has lagged loan book as lending

yields remain under pressure following recent cuts in base rate while

deposit cost remains sticky and will take longer to reprice. SBIN guided for

13‐14% loan growth during FY16 and suggested for early signs of revival in

project lending.

Slippages broadly stable; SME/Mid‐corporate remains the vulnerable

segments: Asset quality remained stable as fresh slippages stood at

Rs73.1bn (26% YoY decline; 2.3% annualized), while SBIN refinanced assets

worth Rs64.8bn consisting of five accounts (metal, port and power

accounts). Management explained that fears of deficient monsoon has

resulted in higher slippages in agriculture while within SME segment it is

mostly the small‐ticket loans (<Rs100mn) where the NPL formation rate

remains higher else the bank is seeing some signs of recovery.

Margins recovery to be gradual; retain ‘BUY’: SBIN has been flushed with

deposits as time deposits grew 18% YoY which the bank has parked into

low-yielding investments. We expect margin recovery to be slow and

gradual and will be a function of credit growth and deposit maturity

profile. We estimate RoA to improve gradually and maintain ‘BUY’ with PT

of Rs350 based on Mar-17 ABV.

9/9/2015 28

Key Financials (Rs m)

Y/e March FY13 FY14 FY15 FY16E FY17E

Net interest income 443,313 492,822 550,156 614,782 686,973

Growth (%) 2.4 11.2 11.6 11.7 11.7

Operating profit 310,817 321,092 389,139 431,360 497,134

PAT 141,050 108,912 131,020 153,336 184,800

EPS (Rs) 20.8 15.2 17.5 20.4 24.4

Growth (%) 16.1 -26.9 15.3 16.3 19.7

Net DPS (Rs) 4.1 1.5 3.5 3.7 3.8

Source: Company Data, PL Research

Profitability & valuation

Y/e March FY13 FY14 FY15 FY16E FY17E

NIM (%) 3.2 3.0 3.0 2.9 2.9

RoAE (%) 15.4 10.0 10.6 11.3 12.3

RoAA (%) 1.0 0.6 0.7 0.7 0.7

P / BV (x) 1.6 1.4 1.3 1.2 1.1

P / ABV (x) 2.2 2.2 1.8 1.6 1.4

PE (x) 11.0 15.0 13.0 11.2 9.3

Net dividend yield (%) 1.8 0.7 1.5 1.6 1.6

Source: Company Data, PL Research

Stock Performance

(%) 1M 6M 12M

Absolute (18.8) (22.3) (11.0)

Relative to Sensex (8.5) (8.2) (3.7)

LilladherPrabhudas Financials

State Bank of India

9/9/2015 29

Income Statement (Rs m)

Y/e March FY13 FY14 FY15 FY16E FY17E

Int. Earned from Adv. 905,371 1,024,841 1,123,439 1,224,266 1,381,199

Int. Earned from Invt. 272,006 319,419 370,878 435,161 492,361

Others - - - - -

Total Interest Income 1,196,571 1,363,508 1,523,971 1,684,434 1,900,440

Interest expense 753,258 870,686 973,814 1,069,652 1,213,467

NII 443,313 492,822 550,156 614,782 686,973

Growth (%) 2.4 11.2 11.6 11.7 11.7

Treasury Income 10,981 20,767 36,182 57,890 92,625

NTNII 149,367 164,762 189,577 192,702 194,053

Non Interest Income 160,348 185,529 225,759 250,592 286,678

Total Income 1,356,919 1,549,037 1,749,730 1,935,027 2,187,118

Growth (%) 12.3 14.2 13.0 10.6 13.0

Operating Expense 292,844 357,259 386,776 434,015 476,517

Operating Profit 310,817 321,092 389,139 431,360 497,134

Growth (%) (1.6) 3.3 21.2 10.8 15.2

NPA Provisions 106,570 144,785 187,129 193,015 204,041

Investment Provisions (9,670) 5,633 (5,904) (3,542) 2,125

Total Provisions 111,308 159,354 195,995 202,500 221,313

PBT 199,509 161,739 193,144 228,860 275,821

Tax Provisions 58,459 52,827 62,124 75,524 91,021

Effective Tax Rate (%) 29.3 32.7 32.2 33.0 33.0

PAT 141,050 108,912 131,020 153,336 184,800

Growth (%) 20.5 (22.8) 20.3 17.0 20.5

Source: Company Data, PL Research

Balance Sheet (Rs m)

Y/e March FY13 FY14 FY15 FY16E FY17E

Par Value 1 1 1 1 1

No. of equity shares 6,840 7,466 7,466 7,566 7,566

Equity 6,840 7,466 7,466 7,566 7,566

Networth 988,837 1,182,822 1,284,383 1,428,088 1,576,953

Adj. Networth 769,272 871,862 1,036,006 1,187,192 1,338,481

Deposits 12,027,396 13,944,085 15,767,933 17,865,068 20,759,209

Growth (%) 15.2 15.9 13.1 13.3 16.2

Low Cost deposits 5,390,634 5,984,004 6,764,443 7,896,360 9,196,330

% of total deposits 44.8 42.9 42.9 44.2 44.3

Total Liabilities 15,662,609 17,922,346 20,480,799 23,175,405 26,870,108

Net Advances 10,456,165 12,098,287 13,000,264 14,573,296 16,817,584

Growth (%) 20.5 15.7 7.5 12.1 15.4

Investments 3,509,273 3,983,082 4,950,274 5,927,348 6,986,616

Total Assets 15,662,609 17,922,346 20,428,632 28,198,553 32,812,368

Source: Company Data, PL Research

LilladherPrabhudas ICICI Bank

CMP: Rs261 TP: Rs390 Rating: BUY MCap: Rs1,512.2bn

ICICI Bank (ICICIBC) has been reporting relatively stable operating performance even as macro-environment remains challenging. Declining trend in NPL formation, granular residual restructured book, coupled with positive management guidance and reasonable valuations makes us retain our ‘BUY’ rating with TP of Rs390 based on Mar-17 ABV.

NII growth on track; other income sluggish on lower treasury gains: ICICIBC in Q1FY16 reported 14% YoY growth in NII led by 22bps YoY & 11bps QoQ margin improvement to 3.6% mainly on strong growth in Retail & SME. Other income growth of ~5% was low mainly on lower treasury gains, while core fee income saw marginal uptick which is being mainly contributed by retail segment. Management has guided for double‐digit fee growth in FY16, led by retail fees.

Asset quality remains stable partly on lower slippages and partly from higher write‐offs: In Q1FY16, Fresh slippages of Rs16.7bn were lower than Rs32.6bn in Q4FY15. The bank has up-fronted some of its restructuring and hence, restructured Rs19.6bn in Q1FY16. Management guided NIL pipeline on restructured or 5:25 scheme. Guidance on credit cost is at 90‐95bps of loans for FY16 (currently at 97bps) as management re‐affirmed stressed accretion to be lower in FY16 than FY15 mainly on lower restructuring, lower lumpy relapses in restructured book and lower rate of slippages from loan book.

Advances book tilt remains towards retail: Advances has grown by 15% YoY in Q1FY16 with strong growth of 25% in retail with contribution from all segments, especially housing & un‐secured. Management has guided for 18‐20% loan growth with 25% growth in retail for FY16 and stable margins of at ~3.5%. ICICIBC is trading at ~25% discount to AXSB valuations and we believe discount would narrow on improving asset quality trends, high growth towards retail and re‐gaining market share in CASA enabling ICICIBC to improve its ROE profile in line with peers.

9/9/2015 30

Key Financials (Rs m)

Y/e March FY13 FY14 FY15 FY16E FY17E

Net interest income 138,664 164,756 190,396 223,026 264,898

Growth (%) 29.2 18.8 15.6 17.1 18.8

Operating profit 131,992 165,946 197,199 222,238 259,538

PAT 83,255 98,105 111,753 128,327 148,307

EPS (Rs) 14.4 17.0 19.3 22.1 25.6

Growth (%) 28.7 17.7 13.6 14.6 15.6

Net DPS (Rs) 4.0 4.5 5.0 6.4 7.0

Source: Company Data, PL Research

Profitability & valuation

Y/e March FY13 FY14 FY15 FY16E FY17E

NIM (%) 2.9 3.1 3.2 3.3 3.3

RoAE (%) 13.1 14.0 14.5 15.0 15.5

RoAA (%) 1.6 1.7 1.8 1.8 1.8

P / BV (x) 2.3 2.1 1.9 1.7 1.5

P / ABV (x) 2.9 2.6 2.4 2.1 1.8

PE (x) 18.1 15.3 13.5 11.8 10.2

Net dividend yield (%) 1.5 1.7 1.9 2.5 2.7

Source: Company Data, PL Research

Stock Performance

(%) 1M 6M 12M

Absolute (15.9) (25.0) (16.8)

Relative to Sensex (5.6) (11.0) (9.5)

LilladherPrabhudas Financials

ICICI Bank

9/9/2015 31

Income Statement (Rs m)

Y/e March FY13 FY14 FY15 FY16E FY17E

Int. Earned from Adv. 273,411 314,279 356,311 411,043 501,728

Int. Earned from Invt. 110,093 115,571 119,446 138,578 160,370

Others - - - - -

Total Interest Income 400,756 441,782 490,911 563,143 678,025

Interest expense 262,092 277,026 300,515 340,117 413,127

NII 138,664 164,756 190,396 223,026 264,898

Growth (%) 29.2 18.8 15.6 17.1 18.8

Treasury Income 4,364 7,654 15,485 - -

NTNII 79,093 96,625 106,277 141,487 162,851

Non Interest Income 83,457 104,279 121,761 141,487 162,851

Total Income 484,213 546,060 612,673 704,630 840,876

Growth (%) 18.0 12.8 12.2 15.0 19.3

Operating Expense 90,129 103,089 114,958 142,275 168,211

Operating Profit 131,992 165,946 197,199 222,238 259,538

Growth (%) 27.1 25.7 18.8 12.7 16.8

NPA Provisions 13,948 22,523 31,410 36,019 43,517

Investment Provisions 1,262 711 2,980 - -

Total Provisions 18,025 26,264 38,996 38,913 47,671

PBT 113,967 139,682 158,203 183,325 211,867

Tax Provisions 30,712 41,577 46,450 54,997 63,560

Effective Tax Rate (%) 26.9 29.8 29.4 30.0 30.0

PAT 83,255 98,105 111,753 128,327 148,307

Growth (%) 28.8 17.8 13.9 14.8 15.6

Source: Company Data, PL Research

Balance Sheet (Rs m)

Y/e March FY13 FY14 FY15 FY16E FY17E

Par Value 2 2 2 2 2

No. of equity shares 5,768 5,775 5,798 5,798 5,798

Equity 11,536 11,550 11,597 11,597 11,597

Networth 667,015 732,068 804,219 903,327 1,007,253

Adj. Networth 644,708 699,087 741,663 846,208 948,912

Deposits 2,926,135 3,319,137 3,615,627 4,324,290 5,279,958

Growth (%) 14.5 13.4 8.9 19.6 22.1

Low Cost deposits 1,225,762 1,423,784 1,643,799 1,881,066 2,296,782

% of total deposits 41.9 42.9 45.5 43.5 43.5

Total Liabilities 5,367,946 5,946,416 6,461,293 7,684,060 9,254,940

Net Advances 2,902,494 3,387,026 3,875,221 4,599,887 5,639,461

Growth (%) 14.4 16.7 14.4 18.7 22.6

Investments 1,713,936 1,770,218 1,865,800 2,114,876 2,464,954

Total Assets 5,367,946 5,946,416 6,461,293 7,684,060 9,254,940

Source: Company Data, PL Research

LilladherPrabhudas Larsen & Toubro

CMP: Rs1,565 TP: Rs2,000 Rating: BUY MCap: Rs1,454.3bn

Strong Guidance: L&T maintained its guidance of 15% sales growth, 15%

order inflow growth and 100bps improvement in margin (excl. services).

While order flow for the quarter was down 21% YoY to Rs263bn, L&T

remains confident of achieving 15% growth in inflow for FY16, given strong

pipeline of orders. The current prospect pipeline is Rs5trn (v/s Rs6.3trn at

the start of Q1FY16 and Rs5trn at the start of Q1FY15). Out of prospect

pipeline of Rs5trn, Rs2.4trn is from Infrastructure, Rs1.3trn from Power,

Rs250bn from Metal & Material handling, Rs450bn from Hydrocarbon and

Rs650bn from various other sectors. Order book stood at Rs2.3trn, up 22%

YoY. L&T believes the revenue growth could be back-ended as large order

flow will start contributing meaningfully from H2FY16: The consolidated

working capital as percentage of sales for at end of FY15 stood at ~ 25%,

down from 26% Sales in Q3FY15, an improvement of 100 bps

Worst behind for Hydrocarbon business: L&T had recently carved out

hydrocarbon business into subsidiary. Sales in hydrocarbon business

increased 41% YoY to Rs22bn and L&T posted an EBITDA of Rs0.9bn for

Q1FY16 (v/s loss of Rs8.9bn). Orders booked in FY15 (International and

Domestic) are contributing to revenue growth. L&T is in the process of

closing three legacy projects by end of FY16; the company expects the

close out cost in these projects to be compensated by pending claims

against the projects. L&T has a fixed cost of US$50m in Hydrocarbon

business, the company expects under recovery of ~US$25m to lead to

EBITDA break-even and loss at PAT level in Hydrocarbon businesses.

Outlook and Valuation: : The stock is trading at core PE of 17.2x FY17E

earnings. We have revised our earnings downward by ~5% for FY16E &

FY17E respectively to factor in weak performance in Q1FY16. L&T

continues to be the best play in the Indian infrastructure space, given its

strong business model, diverse skill sets, strong execution capabilities and

relatively healthy/large balance sheet.

9/9/2015 32

Key Financials (Rs m)

Y/e March FY13 FY14 FY15 FY16E FY17E

Revenue (Rs m) 744,980 851,284 920,046 1,058,053 1,269,663

Growth (%) 15.8 14.3 8.1 15.0 20.0

EBITDA (Rs m) 98,592 107,543 113,356 136,944 165,710

PAT (Rs m) 49,578 43,135 44,077 58,060 72,831

EPS (Rs) 80.6 46.5 47.4 62.5 78.4

Growth (%) 6.7 (42.2) 1.9 31.7 25.4

Net DPS (Rs) 18.1 14.3 13.6 16.1 20.2

Source: Company Data, PL Research

Profitability & valuation

Y/e March FY13 FY14 FY15 FY16E FY17E

EBITDA margin (%) 13.2 12.6 12.3 12.9 13.1

RoE (%) 15.7 15.6 13.3 14.2 16.0

RoCE (%) 7.8 5.9 5.0 5.7 6.3

EV / sales (x) 2.0 2.7 2.6 2.3 2.0

EV / EBITDA (x) 15.2 21.1 20.8 17.7 15.2

PER (x)* 13.8 23.8 23.4 17.8 14.2

P / BV (x) 2.8 3.8 3.6 3.2 2.9

Net dividend yield (%) 1.2 0.9 0.9 1.0 1.3

Source: Company Data, PL Research * Core PE

Stock Performance

(%) 1M 6M 12M

Absolute (14.7) (14.3) (4.0)

Relative to Sensex (4.3) (0.3) 3.3

LilladherPrabhudas SOTP

9/9/2015 33

Fair Value (Rs) Basis

L&T Core business 1,574 23x FY17E EPS Ex dividends

L&T Hydrocarbon business 7 10x FY17E EPS

L&T IDPL 139 1.5x P/B and ‐1x for Hyderabad metro

L&T InfoTech 161 12x FY17E EPS

L&T Finance Holding 79 83% stake; 20% Hold co discount on current market cap

L&T's equity investment in BTG 4 1.5x equity investment

Other businesses 65 1.5x book value

Target price 2,000

LilladherPrabhudas Financials

Larsen & Toubro

9/9/2015 34

Income Statement (Rs m)

Y/e March FY13 FY14 FY15 FY16E FY17E

Net Revenue 744,980 851,284 920,046 1,058,053 1,269,663

Direct Expenses 584,652 663,842 727,468 829,211 998,271

% of Net Sales 78.5 78.0 79.1 78.4 78.6

Employee Cost 62,242 80,276 79,222 91,898 105,682

% of Net Sales 8.4 9.4 8.6 8.7 8.3

SG&A Expenses (506) (378) - - -

% of Net Sales (0.1) (0.0) 0.0 0.0 0.0

Other Expenses - - - - -

% of Net Sales 0.0 0.0 0.0 0.0 0.0

EBITDA 98,592 107,543 113,356 136,944 165,710

Margin (%) 13.2 12.6 12.3 12.9 13.1

Depreciation 16,371 14,458 26,225 27,536 28,913

PBIT 82,221 93,085 87,131 109,407 136,797

Interest Expenses 20,950 31,414 28,507 30,788 33,867

PBT 75,598 74,892 72,172 89,555 113,733

Total tax 23,985 26,076 22,836 29,553 38,669

Effective Tax rate (%) 31.7 34.8 31.6 33.0 34.0

PAT 52,057 49,020 47,648 58,060 72,831

Extraordinary Gain/(Loss) 2,479 5,885 3,572 - -

Adjusted PAT 49,578 43,135 44,077 58,060 72,831

Source: Company Data, PL Research

Balance Sheet (Rs m)

Y/e March FY13 FY14 FY15 FY16E FY17E

Share Capital 1,231 1,854 1,859 1,859 1,859

Reserves & Surplus 337,366 375,262 407,232 450,457 505,672

Shareholder's Fund 338,597 377,116 409,091 452,280 502,337

Preference Share Capital - - - - -

Total Debt 573,409 862,988 955,700 1,037,667 1,119,928

Other Liabilities(net) - - - - -

Deferred Tax Liability 3,779 6,179 5,396 5,396 5,396

Total Liabilities 915,785 1,246,283 1,370,186 1,495,342 1,627,661

Gross Block 356,028 401,773 437,842 474,345 504,345

Less: Depreciation - - - - -

Net Block 356,028 401,773 437,842 474,345 504,345

Capital Work in Progress 40,175 42,626 42,626 42,626 42,626

Cash & Cash Equivalent 123,390 122,055 153,683 169,021 150,132

Total Current Assets 924,034 1,150,574 1,335,860 1,446,919 1,668,049

Total Current Liabilities 515,266 453,944 571,655 594,060 712,872

Net Current Assets 408,768 696,630 764,205 852,859 955,176

Other Assets 23,140 24,166 29,392 29,392 29,392

Total Assets 915,785 1,246,283 1,370,186 1,495,343 1,627,660

Source: Company Data, PL Research

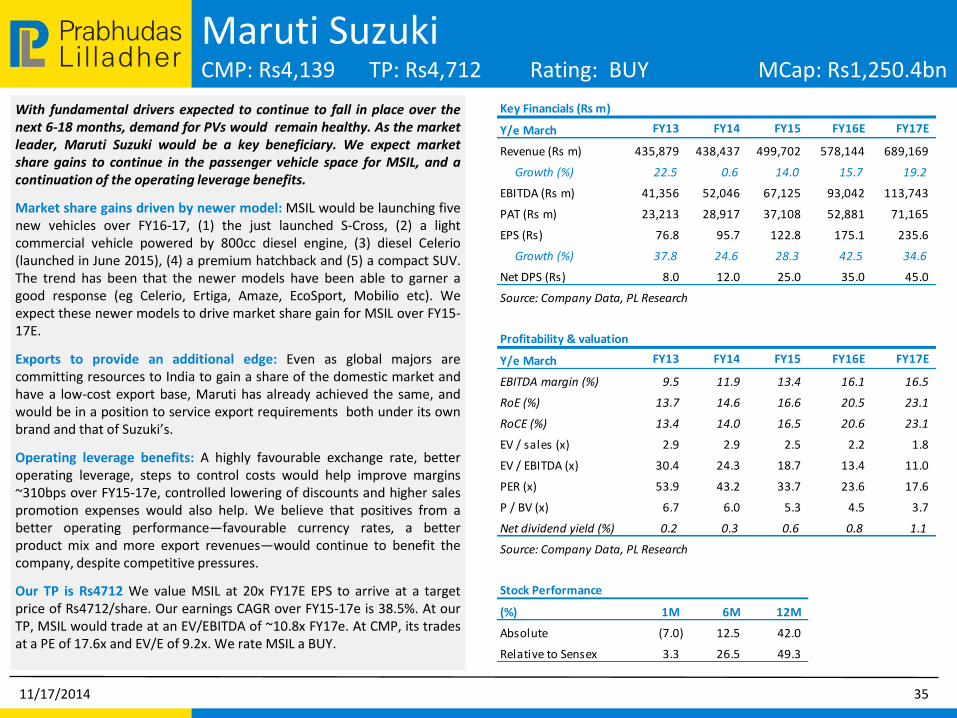

LilladherPrabhudas Maruti Suzuki

CMP: Rs4,139 TP: Rs4,712 Rating: BUY MCap: Rs1,250.4bn

With fundamental drivers expected to continue to fall in place over the next 6-18 months, demand for PVs would remain healthy. As the market leader, Maruti Suzuki would be a key beneficiary. We expect market share gains to continue in the passenger vehicle space for MSIL, and a continuation of the operating leverage benefits.

Market share gains driven by newer model: MSIL would be launching five new vehicles over FY16-17, (1) the just launched S-Cross, (2) a light commercial vehicle powered by 800cc diesel engine, (3) diesel Celerio (launched in June 2015), (4) a premium hatchback and (5) a compact SUV. The trend has been that the newer models have been able to garner a good response (eg Celerio, Ertiga, Amaze, EcoSport, Mobilio etc). We expect these newer models to drive market share gain for MSIL over FY15-17E.

Exports to provide an additional edge: Even as global majors are committing resources to India to gain a share of the domestic market and have a low-cost export base, Maruti has already achieved the same, and would be in a position to service export requirements both under its own brand and that of Suzuki’s.

Operating leverage benefits: A highly favourable exchange rate, better operating leverage, steps to control costs would help improve margins ~310bps over FY15-17e, controlled lowering of discounts and higher sales promotion expenses would also help. We believe that positives from a better operating performance—favourable currency rates, a better product mix and more export revenues—would continue to benefit the company, despite competitive pressures.

Our TP is Rs4712 We value MSIL at 20x FY17E EPS to arrive at a target price of Rs4712/share. Our earnings CAGR over FY15-17e is 38.5%. At our TP, MSIL would trade at an EV/EBITDA of ~10.8x FY17e. At CMP, its trades at a PE of 17.6x and EV/E of 9.2x. We rate MSIL a BUY.

11/17/2014 35

Key Financials (Rs m)

Y/e March FY13 FY14 FY15 FY16E FY17E

Revenue (Rs m) 435,879 438,437 499,702 578,144 689,169

Growth (%) 22.5 0.6 14.0 15.7 19.2

EBITDA (Rs m) 41,356 52,046 67,125 93,042 113,743

PAT (Rs m) 23,213 28,917 37,108 52,881 71,165

EPS (Rs) 76.8 95.7 122.8 175.1 235.6

Growth (%) 37.8 24.6 28.3 42.5 34.6

Net DPS (Rs) 8.0 12.0 25.0 35.0 45.0

Source: Company Data, PL Research

Profitability & valuation

Y/e March FY13 FY14 FY15 FY16E FY17E

EBITDA margin (%) 9.5 11.9 13.4 16.1 16.5

RoE (%) 13.7 14.6 16.6 20.5 23.1

RoCE (%) 13.4 14.0 16.5 20.6 23.1

EV / sales (x) 2.9 2.9 2.5 2.2 1.8

EV / EBITDA (x) 30.4 24.3 18.7 13.4 11.0

PER (x) 53.9 43.2 33.7 23.6 17.6

P / BV (x) 6.7 6.0 5.3 4.5 3.7

Net dividend yield (%) 0.2 0.3 0.6 0.8 1.1

Source: Company Data, PL Research

Stock Performance

(%) 1M 6M 12M

Absolute (7.0) 12.5 42.0

Relative to Sensex 3.3 26.5 49.3

LilladherPrabhudas Financials

Maruti Suzuki

11/17/2014 36

Income Statement (Rs m)

Y/e March FY13 FY14 FY15 FY16E FY17E

Net Revenue 435,879 438,437 499,702 578,144 689,169

Direct Expenses 325,590 313,488 350,080 390,825 466,912

% of Net Sales 74.7 71.5 70.1 67.6 67.7

Employee Cost 10,696 13,681 16,066 19,118 22,368

% of Net Sales 2.5 3.1 3.2 3.3 3.2

SG&A Expenses 33,700 34,360 37,948 42,205 48,242

% of Net Sales 7.7 7.8 7.6 7.3 7.0

Other Expenses 24,538 24,861 28,483 32,954 37,904

% of Net Sales 5.6 5.7 5.7 5.7 5.5

EBITDA 41,356 52,046 67,125 93,042 113,743

Margin (%) 9.5 11.9 13.4 16.1 16.5

Depreciation 18,612 20,844 24,703 27,752 29,601

PBIT 22,744 31,202 42,422 65,290 84,142

Interest Expenses 1,460 1,416 2,060 1,142 1,072

PBT 28,978 36,585 48,677 72,439 93,638

Total tax 5,988 8,755 11,570 19,559 22,473

Effective Tax rate (%) 20.7 23.9 23.8 27.0 24.0

PAT 23,920 27,830 37,108 52,881 71,165

Extraordinary Gain/(Loss) - - - - -

Adjusted PAT 23,213 28,917 37,108 52,881 71,165

Source: Company Data, PL Research

Balance Sheet (Rs m)

Y/e March FY13 FY14 FY15 FY16E FY17E

Share Capital 1,510 1,510 1,510 1,510 1,510

Reserves & Surplus 184,279 208,270 235,532 277,840 335,411

Shareholder's Fund 185,789 209,780 237,043 279,350 336,922

Preference Share Capital - - - - -

Total Debt 13,892 18,239 1,802 2,802 2,752

Other Liabilities(net) - - - - -

Deferred Tax Liability 4,087 5,866 4,810 4,810 4,810

Total Liabilities 203,768 233,885 243,655 286,962 344,484