Embed Size (px)

Citation preview

Real estate May 13, 2014

Oberoi Realty

Bloomberg: OBER IN Reuters: OEBO.BO

BUY

Institutional Equities

India Research

RESULT REVIEW

Recommendation

CMP: Rs203

Target Price: Rs296

Previous Target Price: Rs285

Upside (%) 46%

Stock Information Market Cap. (Rs bn / US$ mn) 67/1,114

52-week High/Low (Rs) 284/153

3m ADV (Rs mn /US$ mn) 37/0.6

Beta 0.9

Sensex/ Nifty 23,551/7,014

Share outstanding (mn) 328

Stock Performance (%) 1M 3M 12M YTD

Absolute (10.1) 9.7 (15.2) (13.3)

Rel. to Sensex (13.5) (4.7) (27.6) (22.1)

Performance

Source: Bloomberg

Earnings Revision

(%) FY14E FY15E

Revenue - 4.1

EBITDA - 1.3

PAT 11.0 5.7

Source: Company

Analysts Contact Parikshit Kandpal

022 6184 4311

150 170 190 210 230 250 270

15,000 17,000 19,000 21,000 23,000 25,000

Ap

r-1

3

Jun

-13

Jul-

13

Au

g-1

3

Sep

-13

No

v-1

3

Dec

-13

Jan

-14

Mar

-14

Ap

r-1

4

Sensex (LHS) Oberoi (RHS)

Multiple triggers Oberoi Realty Ltd. (ORL) 4QFY14 Revenue, EBIDTA and Profit was 23%,

30.9% and 15% ahead of our estimate - pickup in unit sales in Exquisite &

Priviera projects resulted in this outperformance. With ~7mn sqft of new

launches planned for FY15E (Mulund ~3.2mn sqft, Borivali ~3.2mn, Worli –

~0.6mn sqft), ORL has multiple triggers panned out for re-rating. We

maintain our BUY on ORL’s with increased NAV of Rs296/share.

Sales recovery positively impact 4QFY14 performance

ORL 4QFY14 Consolidated Net revenue, EBIDTA & PAT de-grew (27.4%),

(29.5%) & (47%) YoY respectively, ahead of our estimates by 23.0%, 30.9% &

15.0% respectively. EBIDTA margin expanded by 421bps YoY to 56.9% on

account of higher margins in Priviera & Exquisite. The customer advances

remains stable at Rs6,402.6mn. Balance sheet remains strong.

New launches of ~7mn sqft during FY15E ORL has finalized Ritz Carlton as Worli Hotel operator and will be launching

the project during 1HFY15E. Besides this ORL is planning to launch Mulund

& Borivali projects during 2HFY15E, with affordable luxury theme. The ticket

size for Borivali shall be Rs20mn/unit whilst for Mulund Rs30mn/unit. These

new launches shall provide much needed visibility on pre-sales and launch

success remain key re-rating trigger.

Best placed v/s Western peers ORL stands out as a leader in our competitive business mapping of the

Western developers. High land bank quality, superior brand recall and

relatively healthy access to finance are the key contributing factors. We

expect ORL to capture incremental market share outside home location and

deliver above industry average growth.

Maintain BUY: NAV increased to Rs296/share We have incorporated ORL’s Borivali project valuation and debt into our

estimates. We have cut our FY15E & FY16E EPS estimates by 11% & 5.7%

owing to debt finance of Rs8bn for Borivali project. We maintain BUY stance

with a increased SOTP-based target price of Rs296/share (previous target

Rs285/share). We believe that the near-term catalysts are: (i) Mulund & Worli

launch; (ii) successful foray outside Mumbai & (iii) new land acquisitions.

Key risks: (i) Unaffordability may lead to a 8-10% real estate price

correction; (ii) Delays in new land acquisitions remains key de-rating trigger.

Key Financial - Consolidated

Y/E Mar (Rs mn) FY12 FY13 FY14 FY15E FY16E

Operating income 8,247 10,476 7,985 17,177 28,428

EBITDA 4,835 6,121 4,348 10,296 16,428

Net profit 4,633 5,049 3,111 6,475 10,724

EPS (Rs) 14.1 15.4 9.2 19.7 32.7

RoCE (%) 17.3 17.3 10.8 19.8 26.0

P/E (x) 14.4 13.2 22.1 10.3 6.2

Source: Company, Karvy Institutional Research

2

May 13, 2014

Real Estate

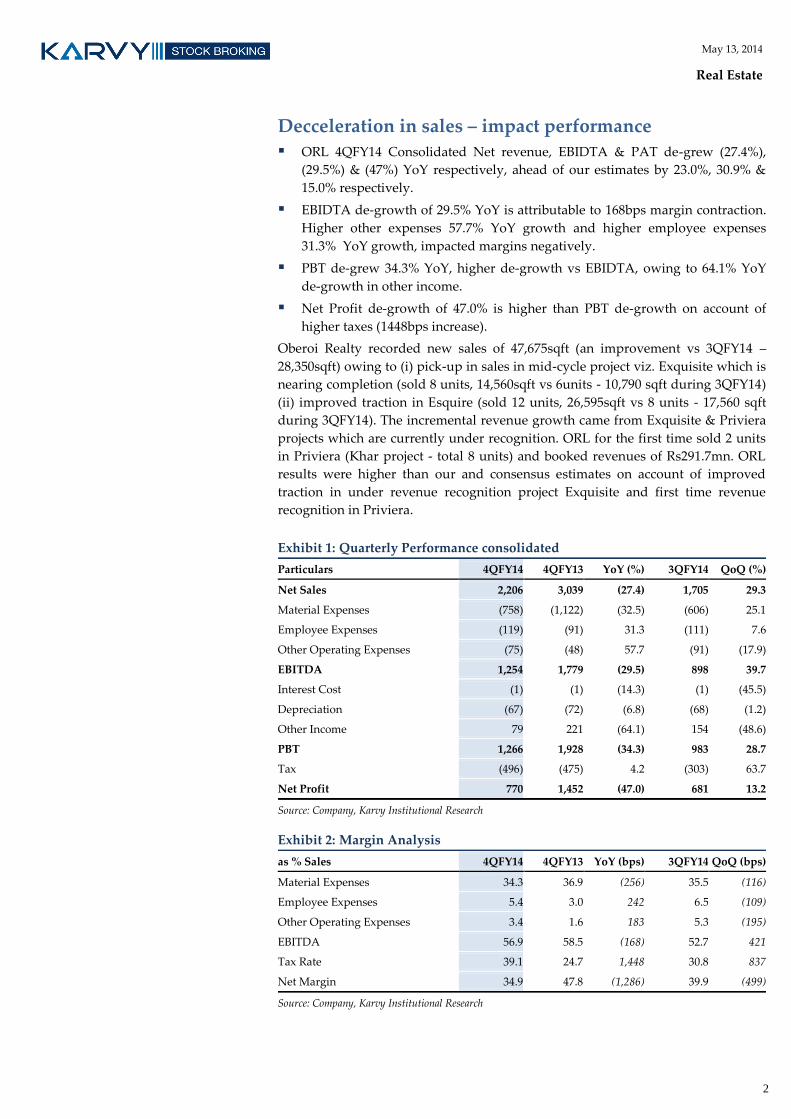

Decceleration in sales – impact performance

ORL 4QFY14 Consolidated Net revenue, EBIDTA & PAT de-grew (27.4%),

(29.5%) & (47%) YoY respectively, ahead of our estimates by 23.0%, 30.9% &

15.0% respectively.

EBIDTA de-growth of 29.5% YoY is attributable to 168bps margin contraction.

Higher other expenses 57.7% YoY growth and higher employee expenses

31.3% YoY growth, impacted margins negatively.

PBT de-grew 34.3% YoY, higher de-growth vs EBIDTA, owing to 64.1% YoY

de-growth in other income.

Net Profit de-growth of 47.0% is higher than PBT de-growth on account of

higher taxes (1448bps increase).

Oberoi Realty recorded new sales of 47,675sqft (an improvement vs 3QFY14 –

28,350sqft) owing to (i) pick-up in sales in mid-cycle project viz. Exquisite which is

nearing completion (sold 8 units, 14,560sqft vs 6units - 10,790 sqft during 3QFY14)

(ii) improved traction in Esquire (sold 12 units, 26,595sqft vs 8 units - 17,560 sqft

during 3QFY14). The incremental revenue growth came from Exquisite & Priviera

projects which are currently under recognition. ORL for the first time sold 2 units

in Priviera (Khar project - total 8 units) and booked revenues of Rs291.7mn. ORL

results were higher than our and consensus estimates on account of improved

traction in under revenue recognition project Exquisite and first time revenue

recognition in Priviera.

Exhibit 1: Quarterly Performance consolidated

Particulars 4QFY14 4QFY13 YoY (%) 3QFY14 QoQ (%)

Net Sales 2,206 3,039 (27.4) 1,705 29.3

Material Expenses (758) (1,122) (32.5) (606) 25.1

Employee Expenses (119) (91) 31.3 (111) 7.6

Other Operating Expenses (75) (48) 57.7 (91) (17.9)

EBITDA 1,254 1,779 (29.5) 898 39.7

Interest Cost (1) (1) (14.3) (1) (45.5)

Depreciation (67) (72) (6.8) (68) (1.2)

Other Income 79 221 (64.1) 154 (48.6)

PBT 1,266 1,928 (34.3) 983 28.7

Tax (496) (475) 4.2 (303) 63.7

Net Profit 770 1,452 (47.0) 681 13.2

Source: Company, Karvy Institutional Research

Exhibit 2: Margin Analysis

as % Sales 4QFY14 4QFY13 YoY (bps) 3QFY14 QoQ (bps)

Material Expenses 34.3 36.9 (256) 35.5 (116)

Employee Expenses 5.4 3.0 242 6.5 (109)

Other Operating Expenses 3.4 1.6 183 5.3 (195)

EBITDA 56.9 58.5 (168) 52.7 421

Tax Rate 39.1 24.7 1,448 30.8 837

Net Margin 34.9 47.8 (1,286) 39.9 (499)

Source: Company, Karvy Institutional Research

3

May 13, 2014

Real Estate

Sales momentum – marginal recovery

ORL has recorded improvement in pre-sales volume with new sales at 47,675sqft

vs 28,350sqft during 3QFY14. The management sounded upbeat on change in

sentiment post elections contingent on (i) stable Government & (ii) economic

recovery. As of now ORL is holding on to prices and focusing on completing

Exquisite (200 units in inventory, pending cost Rs500mn, current quarterly sales

runrate 9 units). The projects is expected to be delivered by Dec-13 and may see

buying recovery post completion. Esquire will see increased momentum from

1QFY15E as all approvals are in place now. Oasis Worli may get launched during

1HFY15E whilst Mulund & Borivali projects may get launched end FY15E.

Exhibit 3: 4QFY14 – new sales

Pre-sales - mnsf 1QFY12 2QFY12 3QFY12 4QFY12 1QFY13 2QFY13 3QFY13 4QFY13 1QFY14 2QFY14 3QFY14 4QFY14

Oberoi Esquire 0.17 0.13 0.07 0.07 0.06 0.07 0.05 0.05 0.03 0.02 0.02 0.03

Oberoi Exquisite 0.01 0.02 0.01 0.03 0.03 0.03 0.04 0.04 0.02 0.02 0.01 0.01

Oberoi Splendor

Grande 0.03 0.03 0.03 0.04 0.02 0.02 0.02 0.01 - - - 0.00

Oberoi Splendor 0.00 0.00 0.01 0.02 0.01 0.01 0.01 0.02 - - - -

Oberoi Oasis - 0.11 - -

Oberoi Priviera

0.00

Total 0.21 0.18 0.12 0.17 0.12 0.13 0.12 0.12 0.05 0.15 0.03 0.05

Pre-Sales - Rs mn

Oberoi Esquire 1,973 1,486 852 1,036 927 1,100 784 780 411 433 349 435

Oberoi Exquisite 211 276 229 442 495 488 781 740 478 385 226 352

Oberoi Splendor

Grande 368 413 403 651 374 345 311 202 36 - - 42

Oberoi Splendor 67 65 297 456 190 287 199 505 - 3,179 - -

Oberoi Oasis - - -

Oberoi Priviera

292

Total 2,619 2,239 1,780 2,585 1,986 2,220 2,074 2,227 925 3,997 575 1,122

Source: Company, Karvy Institutional Research

Oberoi Esquire will hit revenue recognition during 2HFY15E whilst Worli project

shall hit P&L during FY15E. ORL has done 23 units pre-sales in Worli project and

recorded 12 units as of 4QFY14.

Exhibit 4: Cumulative sales trend

Project Area (msf)

Area sold as

of 4QFY14

(mnsf)

Sales Value

(Rs mn)

Average

realisation

(Rs/sqft)

PoCM (%)

Balance

Revenues to be

recognised (Rs

mn)

Cash to be

received (Rs

mn)

Oberoi Esquire 1.5 1.0 13,287 13,246 <20% 13,287 8,287

Oberoi Exquisite 1.5 1.0 14,149 13,431 88% 933 560

Oberoi Splendor Grande 0.3 0.3 4,187 14,599 100% - 7

Oberoi Splendor 1.3 1.3 15,714 12,304 100% - 111

Oberoi Oasis 1.8 0.1 3,491 27,704 <20% 3,179 2,408

Oberoi Priviera* 0.0 0.0 292 62,064 38% 0 0

Total 6.4 3.7 51,120 13,902 17,399 11,373

Source: Company, Karvy Institutional Research; *: On Carpet area & carpet price.

4

May 13, 2014

Real Estate

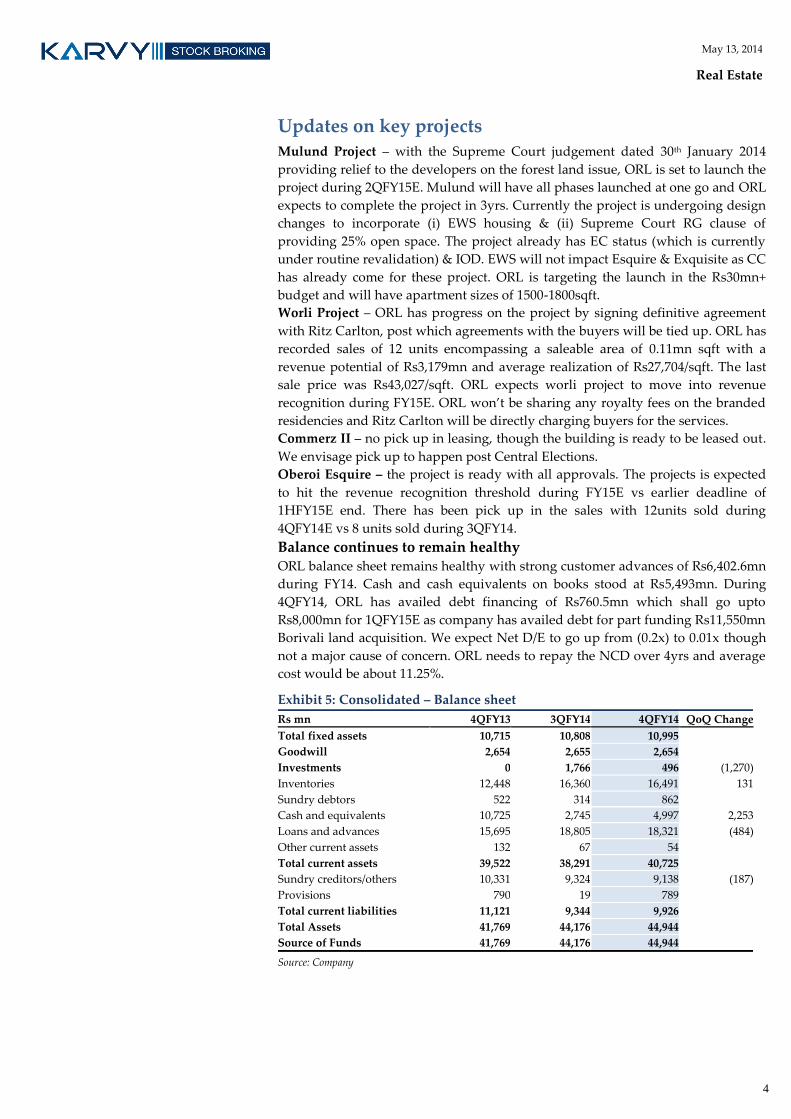

Updates on key projects Mulund Project – with the Supreme Court judgement dated 30th January 2014

providing relief to the developers on the forest land issue, ORL is set to launch the

project during 2QFY15E. Mulund will have all phases launched at one go and ORL

expects to complete the project in 3yrs. Currently the project is undergoing design

changes to incorporate (i) EWS housing & (ii) Supreme Court RG clause of

providing 25% open space. The project already has EC status (which is currently

under routine revalidation) & IOD. EWS will not impact Esquire & Exquisite as CC

has already come for these project. ORL is targeting the launch in the Rs30mn+

budget and will have apartment sizes of 1500-1800sqft.

Worli Project – ORL has progress on the project by signing definitive agreement

with Ritz Carlton, post which agreements with the buyers will be tied up. ORL has

recorded sales of 12 units encompassing a saleable area of 0.11mn sqft with a

revenue potential of Rs3,179mn and average realization of Rs27,704/sqft. The last

sale price was Rs43,027/sqft. ORL expects worli project to move into revenue

recognition during FY15E. ORL won’t be sharing any royalty fees on the branded

residencies and Ritz Carlton will be directly charging buyers for the services.

Commerz II – no pick up in leasing, though the building is ready to be leased out.

We envisage pick up to happen post Central Elections.

Oberoi Esquire – the project is ready with all approvals. The projects is expected

to hit the revenue recognition threshold during FY15E vs earlier deadline of

1HFY15E end. There has been pick up in the sales with 12units sold during

4QFY14E vs 8 units sold during 3QFY14.

Balance continues to remain healthy ORL balance sheet remains healthy with strong customer advances of Rs6,402.6mn

during FY14. Cash and cash equivalents on books stood at Rs5,493mn. During

4QFY14, ORL has availed debt financing of Rs760.5mn which shall go upto

Rs8,000mn for 1QFY15E as company has availed debt for part funding Rs11,550mn

Borivali land acquisition. We expect Net D/E to go up from (0.2x) to 0.01x though

not a major cause of concern. ORL needs to repay the NCD over 4yrs and average

cost would be about 11.25%.

Exhibit 5: Consolidated – Balance sheet

Rs mn 4QFY13 3QFY14 4QFY14 QoQ Change

Total fixed assets 10,715 10,808 10,995

Goodwill 2,654 2,655 2,654

Investments 0 1,766 496 (1,270)

Inventories 12,448 16,360 16,491 131

Sundry debtors 522 314 862

Cash and equivalents 10,725 2,745 4,997 2,253

Loans and advances 15,695 18,805 18,321 (484)

Other current assets 132 67 54

Total current assets 39,522 38,291 40,725

Sundry creditors/others 10,331 9,324 9,138 (187)

Provisions 790 19 789

Total current liabilities 11,121 9,344 9,926

Total Assets 41,769 44,176 44,944

Source of Funds 41,769 44,176 44,944

Source: Company

5

May 13, 2014

Real Estate

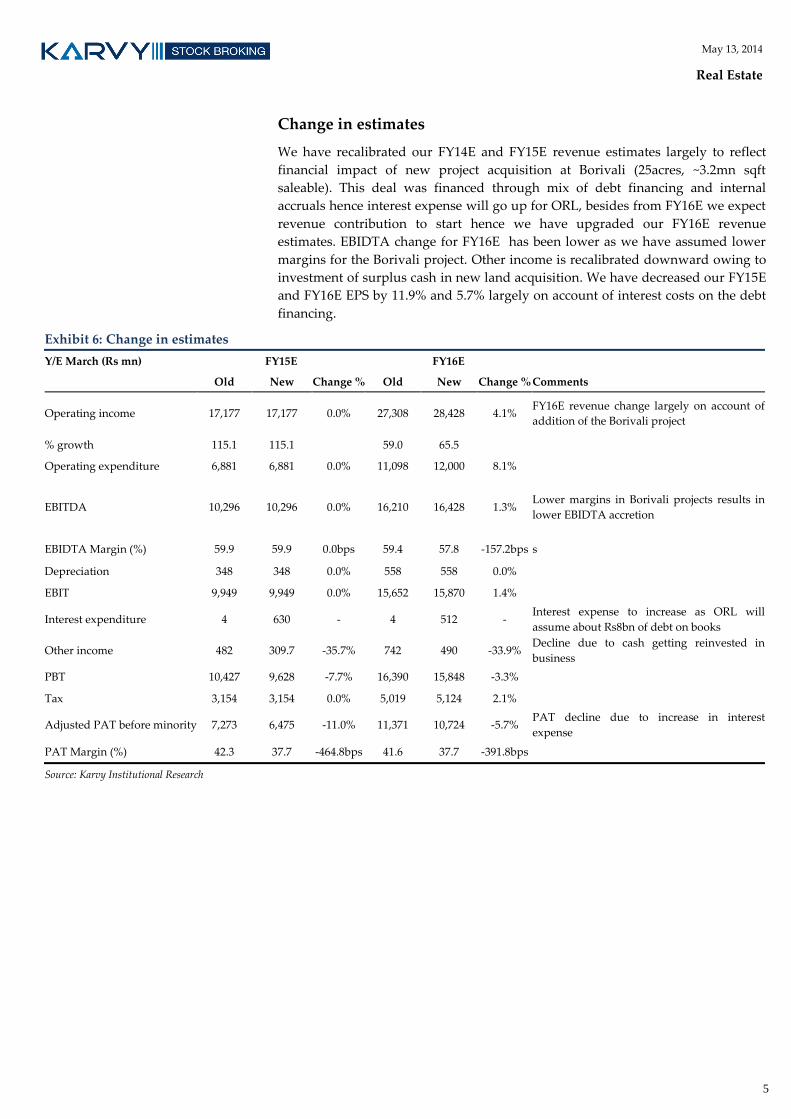

Change in estimates

We have recalibrated our FY14E and FY15E revenue estimates largely to reflect

financial impact of new project acquisition at Borivali (25acres, ~3.2mn sqft

saleable). This deal was financed through mix of debt financing and internal

accruals hence interest expense will go up for ORL, besides from FY16E we expect

revenue contribution to start hence we have upgraded our FY16E revenue

estimates. EBIDTA change for FY16E has been lower as we have assumed lower

margins for the Borivali project. Other income is recalibrated downward owing to

investment of surplus cash in new land acquisition. We have decreased our FY15E

and FY16E EPS by 11.9% and 5.7% largely on account of interest costs on the debt

financing.

Exhibit 6: Change in estimates

Y/E March (Rs mn) FY15E FY16E

Old New Change % Old New Change % Comments

Operating income 17,177 17,177 0.0% 27,308 28,428 4.1% FY16E revenue change largely on account of

addition of the Borivali project

% growth 115.1 115.1

59.0 65.5

Operating expenditure 6,881 6,881 0.0% 11,098 12,000 8.1%

EBITDA 10,296 10,296 0.0% 16,210 16,428 1.3% Lower margins in Borivali projects results in

lower EBIDTA accretion

EBIDTA Margin (%) 59.9 59.9 0.0bps 59.4 57.8 -157.2bps s

Depreciation 348 348 0.0% 558 558 0.0%

EBIT 9,949 9,949 0.0% 15,652 15,870 1.4%

Interest expenditure 4 630 - 4 512 - Interest expense to increase as ORL will

assume about Rs8bn of debt on books

Other income 482 309.7 -35.7% 742 490 -33.9% Decline due to cash getting reinvested in

business

PBT 10,427 9,628 -7.7% 16,390 15,848 -3.3%

Tax 3,154 3,154 0.0% 5,019 5,124 2.1%

Adjusted PAT before minority 7,273 6,475 -11.0% 11,371 10,724 -5.7% PAT decline due to increase in interest

expense

PAT Margin (%) 42.3 37.7 -464.8bps 41.6 37.7 -391.8bps

Source: Karvy Institutional Research

6

May 13, 2014

Real Estate

Investment Rationale

Strong balance sheet lends scope for locational diversification

outside home location

Regional to Top 8 cities aspiration is driving domestic realty players to diversify

outside their core regions. Whilst we believe that pan India theme has its own

challenges we expect ORL’s competitive position to change in markets outside its

core. NCR now contributes 15% to Sobha’s sales volume and we expect similar

numbers to pan out for Oberoi on back of strong brand recall replication in other

markets. Moreover, a debt free balance sheet augurs well for any acquisition

opportunity in newer markets though ORL remains focused on JDA (Joint

development agreement) model of diversification.

Exhibit 7: Strategy to move out of home markets

Mumbai Pune NCR Bangalore Chennai Hyderabad Overall Comments

DLF

Broad based presence across markets, strong

competitive positioning, though Mumbai exit

remains key dampener

Oberoi

Diversification outside Mumbai remains key re-

rating trigger; we see strong change in competitive

positioning over next 2-3yrs with NCR, Bangalore

markets as new additions. We estimate new

markets to contribute 10-15% to volumes

Sobha

Successful NCR foray sets tone for a stronger

growth outside home turf Bangalore. We rate

Sobha as a mid-quartile

Prestige

Middling in most regions. Competitive positioning

in Bangalore remains strong, Chennai

consolidating

Puravankara

Middling on most locations. Bangalore & Chennai

remain dominant regions. Looking to diversify

outside the home markets

Godrej

We rate Godrej as a mid-quartile for diversification

outside Mumbai. Launches have met with strong

success. Brand leveraging will help further

consolidation in the competitive positioning

Kolte

Middling on most locations. Kolte is a dominant

Pune player with emerging presence in Bangalore

where it is looking to further consolidate and

improve market share, whilst in Mumbai the

company is looking towards its first launch.

Source: Karvy Institutional Research; Note: Strong; Relatively Strong; Average; Relatively Weak Weak

Gaining market share in newer location offers an option value and should a

developer exercise this option successfully the growth can be ahead of industry. It

remains as a long term option to be exercised and a potential re-rating trigger for

ORL.

7

May 13, 2014

Real Estate

Dominant Western markets positioning

ORL is best placed amongst the Western peers on account of its superior land bank

quality, access to finance, healthy balance sheet and high potential for successful

foray in newer markets. The micro factors are well supported by strong execution,

quality construction & management bandwidth. We highlight our finding in

exhibit 8 to arrive at overall competitive positioning.

Exhibit 8: Overall competitive positioning of real estate developers

Macro

Competitive

- 30% weight

Business

Competitive -

25% weight

Land bank

& Pricing -

20% weight

Balance

Sheet

positioning -

25% weight

Overall Comments

Oberoi

Top quartile with no debt, higher return ratios and strong

cash-flows

Godrej

A top quartile on macro competitive whilst mid-quartile on

all other parameter. High leverage is the key overhang. We

rate it a mid-quartile

HDIL

Middling in all parameter

Hiranandani

Raheja

Middling in all parameter

Sunteck

Overall a Mid -quartile on back of low leverage, high return

ratios

Wadhwa

Middling in all parameter

Kolte Patil

A Mid -quartile on all parameters

Source: Karvy Institutional Research; Note: Strong; Relatively Strong; Average; Relatively Weak Weak

On overall competitive positioning, we find that the top real estate players

include Oberoi, Godrej, Hirandandani & Sunteck in Western markets. ORL with

the right mix of branding, execution capability, balance sheet strength and

underlying business fundamentals remains best poised amongst the peers.

Notwithstanding their scores differ on these factors we see limited differentiation

on an overall basis.

8

May 13, 2014

Real Estate

Valuation – NAV increased to Rs296/share

SOTP Valuation We have adopted DCF methodology to arrive at ORL’s NAV/share. We have

introduced the Borivali (~3.2mn sqft project into our SOTP). We value the

residential real estate business at Rs161/share (vs Rs123/share earlier), hotels at

Rs21/share, commercial annuity assets at Rs90/share, social infrastructure at

Rs10/share, other assets at Rs15/share and net debt (Rs1) (vs Rs27/share earlier) to

arrive at total SOTP valuation of Rs296/share for the Company (vs Rs285/share

earlier). We don’t ascribe any NAV discount to ORL as we have only valued the

projects which have visibility over the next 5years. For land bank beyond 5 years

we ascribe 1x P/BV for invested equity.

Exhibit 9: Sum of the Parts

Rs mn Rs/share Comments

Gross NAV Residential 52,887 161 NAV based on the methodology discussed below

Gross NAV Hotels 6,961 21 8x FY15E EV/EBIDTA

Gross NAV Commercial 29,599 90 NAV based on the methodology discussed

Social Infra 3,134 10 discounting at 12% cap rate viz. school, hospital etc

Other Assets 4,911 15 investments in other projects at 1x P/BV,viz. Sangam city, Juhu hotel etc

Less: Net Debt 258 (1) Increase in debt to Rs8bn has resulted in ORL being a Net debt company

NAV 97,235 296

Source: Karvy Institutional Research

Real estate development – NAV calculation methodology

We have divided ORL’s entire land bank into residential projects (based on the

information given by the company)

We have arrived at the sale price/sq ft. and the anticipated sales volumes for

each project based on our discussions with industry experts

We have deducted the cost of construction based on our assumed cost

estimates which have been arrived at after discussions with industry experts

We have further deducted marketing and other costs which have been

assumed at 5% of the sales revenue

We have then deducted income tax based on the tax applicable for the project

The resultant cash inflows at the project level have been discounted based on

WACC of 14% (cost of equity 14% based on beta of 1x & debt/equity ratio of

0x). All the project level NAVs have then been summed up to arrive at the

NAV of the company

For commercial office we have discounted rentals using 14% WACC for the

forecasted period and terminal value using the cap rate of 11%

Social infrastructure created by ORL viz. School, Hospital etc has been

discounted using cap rate of 12%

Other assets have been valued at 1x P/BV of invested equity

From the NAV, we have deducted the net debt as of FY15E to arrive at the

final valuation of the company.

Location Gross NAV

(Rs mn)

Rs/

Share

Residential

Goregaon 13,716 42

JVLR 6,943 21

Worli - Residential 8,132 25

Mulund 11,421 35

Borivali 12,675 39

Total Residential 52,887 161

Hotels

Westin Hotel 4,085 12

Worli Hotel 2,876 9

Total Hotel 6,961 21

Commercial

Commerz-All Phases 20,712 63

Oberoi Mall 6,274 19

Worli Commercial 2,613 8

Total Commercial 29,599 90

Grand Total 89,448 273

Source: Karvy Institutional Research

9

May 13, 2014

Real Estate

Key valuation assumptions

In exhibit 10 we highlight our sales and cost inflation forecasts. We expect

property price appreciation in line with WPI inflation i.e. 5%. We forecast other

costs including marketing, SGA and employees’ costs at 5% of sales.

Exhibit 10: Base case assumptions

Discount rate 14%

Annual rate of inflation-sales price 5%

Annual rate of inflation-cost of construction 5%

Other costs – marketing, SGA, employee cost (as % of sales) 5%

Tax rate (%) 33%

Source: Karvy Institutional Research

In the exhibit 11 we highlight our sale price and construction cost forecasts. Our

pricing assumptions are moderate and at a 0-10% premium to the current

prevailing prices on account of ORL 15-20% brand premium vs peers.

Exhibit 11: Base property price and construction cost assumptions

Location Prices Cost

Rs/sq ft Rs/sq ft

Goregaon 14,000 5,500

Worli 35,000 7,500

Mulund 11,500 4,000

Borivali 12,000 5,000

JVLR 13,500 5,000

Source: Karvy Institutional Research

10

May 13, 2014

Real Estate

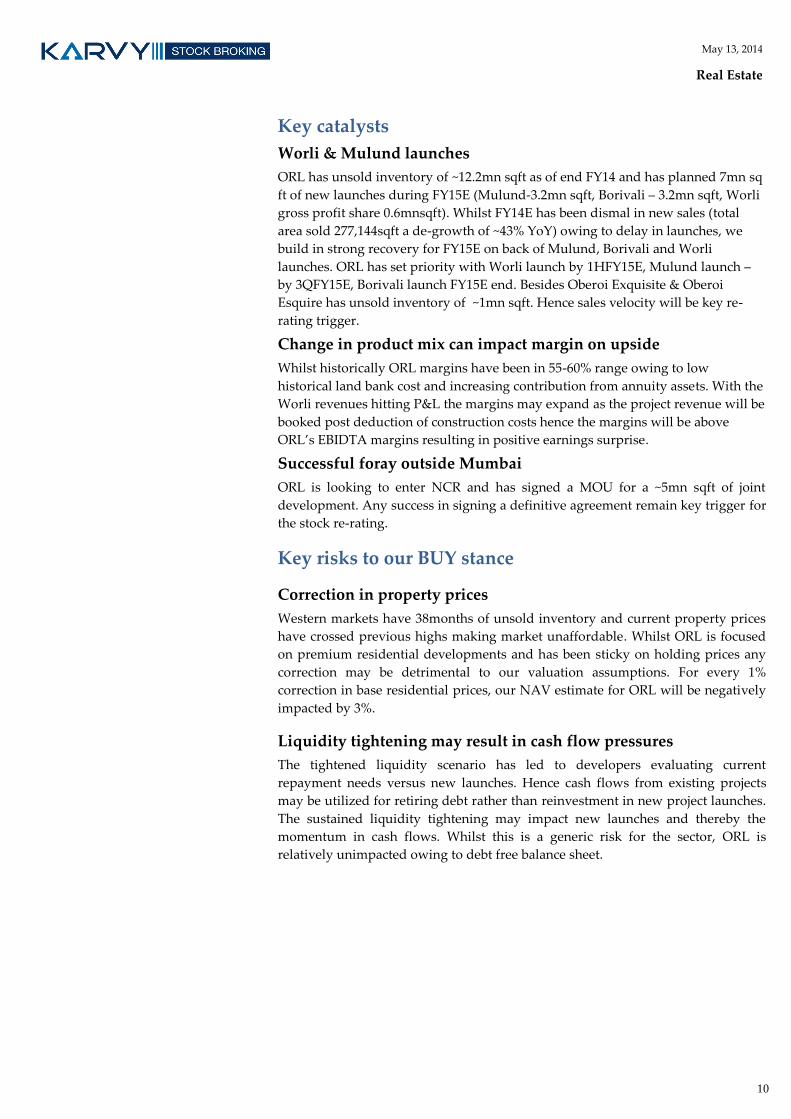

Key catalysts

Worli & Mulund launches

ORL has unsold inventory of ~12.2mn sqft as of end FY14 and has planned 7mn sq

ft of new launches during FY15E (Mulund-3.2mn sqft, Borivali – 3.2mn sqft, Worli

gross profit share 0.6mnsqft). Whilst FY14E has been dismal in new sales (total

area sold 277,144sqft a de-growth of ~43% YoY) owing to delay in launches, we

build in strong recovery for FY15E on back of Mulund, Borivali and Worli

launches. ORL has set priority with Worli launch by 1HFY15E, Mulund launch –

by 3QFY15E, Borivali launch FY15E end. Besides Oberoi Exquisite & Oberoi

Esquire has unsold inventory of ~1mn sqft. Hence sales velocity will be key re-

rating trigger.

Change in product mix can impact margin on upside

Whilst historically ORL margins have been in 55-60% range owing to low

historical land bank cost and increasing contribution from annuity assets. With the

Worli revenues hitting P&L the margins may expand as the project revenue will be

booked post deduction of construction costs hence the margins will be above

ORL’s EBIDTA margins resulting in positive earnings surprise.

Successful foray outside Mumbai

ORL is looking to enter NCR and has signed a MOU for a ~5mn sqft of joint

development. Any success in signing a definitive agreement remain key trigger for

the stock re-rating.

Key risks to our BUY stance

Correction in property prices

Western markets have 38months of unsold inventory and current property prices

have crossed previous highs making market unaffordable. Whilst ORL is focused

on premium residential developments and has been sticky on holding prices any

correction may be detrimental to our valuation assumptions. For every 1%

correction in base residential prices, our NAV estimate for ORL will be negatively

impacted by 3%.

Liquidity tightening may result in cash flow pressures

The tightened liquidity scenario has led to developers evaluating current

repayment needs versus new launches. Hence cash flows from existing projects

may be utilized for retiring debt rather than reinvestment in new project launches.

The sustained liquidity tightening may impact new launches and thereby the

momentum in cash flows. Whilst this is a generic risk for the sector, ORL is

relatively unimpacted owing to debt free balance sheet.

11

May 13, 2014

Real Estate

Financials - Consolidated

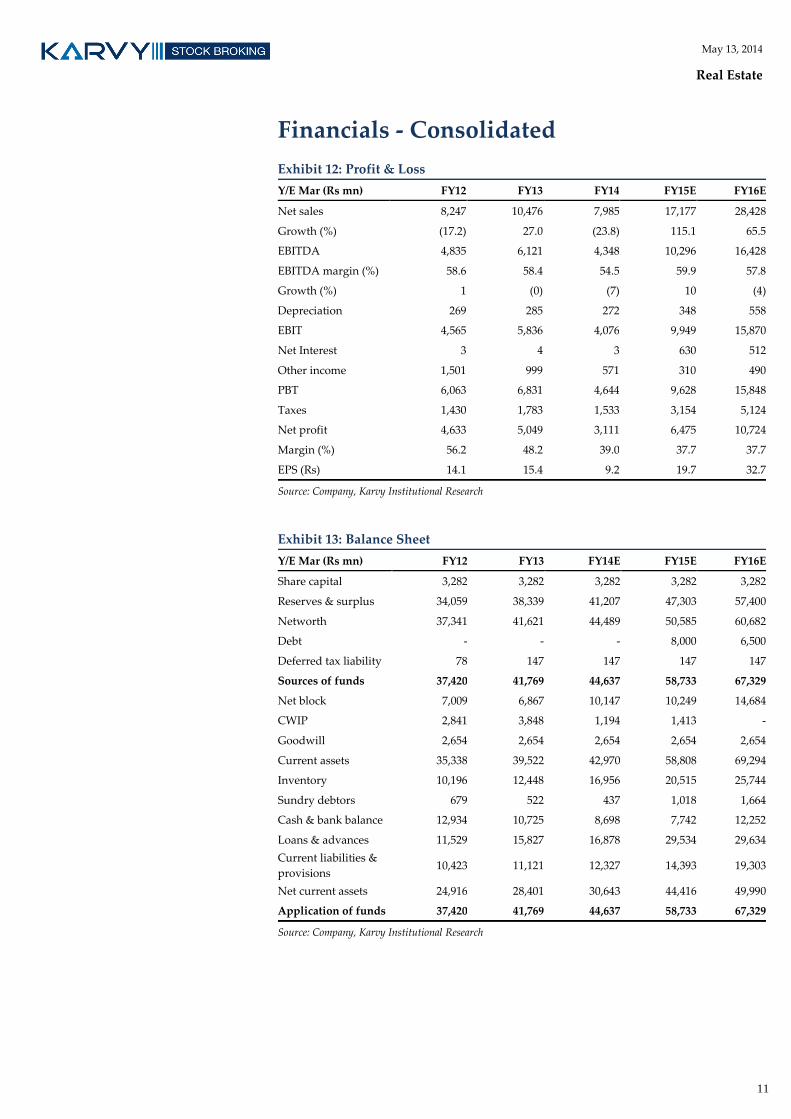

Exhibit 12: Profit & Loss

Y/E Mar (Rs mn) FY12 FY13 FY14 FY15E FY16E

Net sales 8,247 10,476 7,985 17,177 28,428

Growth (%) (17.2) 27.0 (23.8) 115.1 65.5

EBITDA 4,835 6,121 4,348 10,296 16,428

EBITDA margin (%) 58.6 58.4 54.5 59.9 57.8

Growth (%) 1 (0) (7) 10 (4)

Depreciation 269 285 272 348 558

EBIT 4,565 5,836 4,076 9,949 15,870

Net Interest 3 4 3 630 512

Other income 1,501 999 571 310 490

PBT 6,063 6,831 4,644 9,628 15,848

Taxes 1,430 1,783 1,533 3,154 5,124

Net profit 4,633 5,049 3,111 6,475 10,724

Margin (%) 56.2 48.2 39.0 37.7 37.7

EPS (Rs) 14.1 15.4 9.2 19.7 32.7

Source: Company, Karvy Institutional Research

Exhibit 13: Balance Sheet

Y/E Mar (Rs mn) FY12 FY13 FY14E FY15E FY16E

Share capital 3,282 3,282 3,282 3,282 3,282

Reserves & surplus 34,059 38,339 41,207 47,303 57,400

Networth 37,341 41,621 44,489 50,585 60,682

Debt - - - 8,000 6,500

Deferred tax liability 78 147 147 147 147

Sources of funds 37,420 41,769 44,637 58,733 67,329

Net block 7,009 6,867 10,147 10,249 14,684

CWIP 2,841 3,848 1,194 1,413 -

Goodwill 2,654 2,654 2,654 2,654 2,654

Current assets 35,338 39,522 42,970 58,808 69,294

Inventory 10,196 12,448 16,956 20,515 25,744

Sundry debtors 679 522 437 1,018 1,664

Cash & bank balance 12,934 10,725 8,698 7,742 12,252

Loans & advances 11,529 15,827 16,878 29,534 29,634

Current liabilities &

provisions 10,423 11,121 12,327 14,393 19,303

Net current assets 24,916 28,401 30,643 44,416 49,990

Application of funds 37,420 41,769 44,637 58,733 67,329

Source: Company, Karvy Institutional Research

12

May 13, 2014

Real Estate

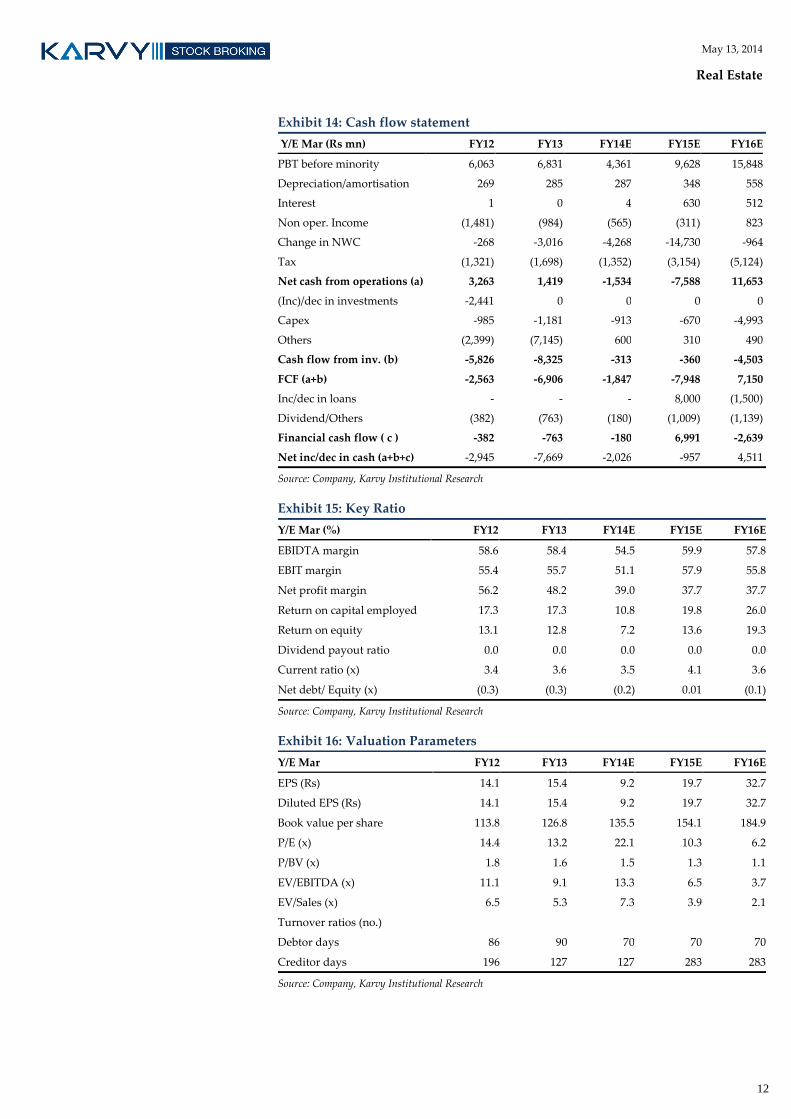

Exhibit 14: Cash flow statement

Y/E Mar (Rs mn) FY12 FY13 FY14E FY15E FY16E

PBT before minority 6,063 6,831 4,361 9,628 15,848

Depreciation/amortisation 269 285 287 348 558

Interest 1 0 4 630 512

Non oper. Income (1,481) (984) (565) (311) 823

Change in NWC -268 -3,016 -4,268 -14,730 -964

Tax (1,321) (1,698) (1,352) (3,154) (5,124)

Net cash from operations (a) 3,263 1,419 -1,534 -7,588 11,653

(Inc)/dec in investments -2,441 0 0 0 0

Capex -985 -1,181 -913 -670 -4,993

Others (2,399) (7,145) 600 310 490

Cash flow from inv. (b) -5,826 -8,325 -313 -360 -4,503

FCF (a+b) -2,563 -6,906 -1,847 -7,948 7,150

Inc/dec in loans - - - 8,000 (1,500)

Dividend/Others (382) (763) (180) (1,009) (1,139)

Financial cash flow ( c ) -382 -763 -180 6,991 -2,639

Net inc/dec in cash (a+b+c) -2,945 -7,669 -2,026 -957 4,511

Source: Company, Karvy Institutional Research

Exhibit 15: Key Ratio

Y/E Mar (%) FY12 FY13 FY14E FY15E FY16E

EBIDTA margin 58.6 58.4 54.5 59.9 57.8

EBIT margin 55.4 55.7 51.1 57.9 55.8

Net profit margin 56.2 48.2 39.0 37.7 37.7

Return on capital employed 17.3 17.3 10.8 19.8 26.0

Return on equity 13.1 12.8 7.2 13.6 19.3

Dividend payout ratio 0.0 0.0 0.0 0.0 0.0

Current ratio (x) 3.4 3.6 3.5 4.1 3.6

Net debt/ Equity (x) (0.3) (0.3) (0.2) 0.01 (0.1)

Source: Company, Karvy Institutional Research

Exhibit 16: Valuation Parameters

Y/E Mar FY12 FY13 FY14E FY15E FY16E

EPS (Rs) 14.1 15.4 9.2 19.7 32.7

Diluted EPS (Rs) 14.1 15.4 9.2 19.7 32.7

Book value per share 113.8 126.8 135.5 154.1 184.9

P/E (x) 14.4 13.2 22.1 10.3 6.2

P/BV (x) 1.8 1.6 1.5 1.3 1.1

EV/EBITDA (x) 11.1 9.1 13.3 6.5 3.7

EV/Sales (x) 6.5 5.3 7.3 3.9 2.1

Turnover ratios (no.)

Debtor days 86 90 70 70 70

Creditor days 196 127 127 283 283

Source: Company, Karvy Institutional Research

Institutional Equities Team Rahul Sharma

Head – Institutional Equities /

Research / Pharma +91‐22 61844310 [email protected]

Gurdarshan Singh Kharbanda Head ‐ Sales‐Trading +91‐22 61844368/69 [email protected]

INSTITUTIONAL RESEARCH

Analysts Industry / Sector Desk Phone Email ID

Hatim Broachwala, CFA Banking +91‐22 61844329 [email protected]

Maruti Kadam Research Associate +91‐22 61844322 [email protected]

Mitul Shah Automobiles/Auto Ancillary +91‐22 61844312 [email protected]

Parikshit Kandpal Infra / Real Estate / Strategy/Consumer +91‐22 61844311 [email protected]

Rahul Singh Textile/MidCap +91‐40‐44857911 [email protected]

Rajesh Kumar Ravi Cement/ Logistics/ Paints +91‐22 61844313 [email protected]

Rupesh Sankhe Power/Capital Goods +91‐22 61844315 [email protected]

Varun Chakri Research Associate +91 22 61844326 [email protected]

Vinesh Vala Research Associate +91 22 61844325 [email protected]

INSTITUTIONAL SALES

Celine Dsouza Sales +91 22 61844341 [email protected]

Edelbert Dcosta Sales +91 22 61844344 [email protected]

INSTITUTIONAL SALES TRADING & DEALING

Bhavesh Gandhi Institutional Sales/Trading +91‐22 61844361 [email protected]

Prashant Oza Institutional Sales/Trading +91‐22 61844370 /71 [email protected]

Pratik Sanghvi Institutional Dealing +91‐22 61844366 /67 [email protected]

For further enquiries please contact:

Tel: +91‐22‐6184 4300

Disclosures Appendix

Analyst certification

The following analyst(s), who is (are) primarily responsible for this report, certify (ies) that the views expressed

herein accurately reflect his (their) personal view(s) about the subject security (ies) and issuer(s) and that no part of

his (their) compensation was, is or will be directly or indirectly related to the specific recommendation(s) or views

contained in this research report.

Disclaimer

The information and views presented in this report are prepared by Karvy Stock Broking Limited. The information

contained herein is based on our analysis and upon sources that we consider reliable. We, however, do not vouch for

the accuracy or the completeness thereof. This material is for personal information and we are not responsible for any

loss incurred based upon it. The investments discussed or recommended in this report may not be suitable for all

investors. Investors must make their own investment decisions based on their specific investment objectives and

financial position and using such independent advice, as they believe necessary. While acting upon any information

or analysis mentioned in this report, investors may please note that neither Karvy nor Karvy Stock Broking nor any

person connected with any associate companies of Karvy accepts any liability arising from the use of this information

and views mentioned in this document.

The author, directors and other employees of Karvy and its affiliates may hold long or short positions in the above

mentioned companies from time to time. Every employee of Karvy and its associate companies are required to

disclose their individual stock holdings and details of trades, if any, that they undertake. The team rendering

corporate analysis and investment recommendations are restricted in purchasing/selling of shares or other securities

till such a time this recommendation has either been displayed or has been forwarded to clients of Karvy. All

employees are further restricted to place orders only through Karvy Stock Broking Ltd. This report is intended for a

restricted audience and we are not soliciting any action based on it. Neither the information nor any opinion

expressed herein constitutes an offer or an invitation to make an offer, to buy or sell any securities, or any options,

futures nor other derivatives related to such securities.

Karvy Stock Broking Limited Institutional Equities

Office No. 702, 7th Floor, Hallmark Business Plaza, Opp.‐Gurunanak Hospital, Mumbai 400 051 Regd Off : 46, Road No 4, Street No 1, Banjara Hills, Hyderabad – 500 034.

Karvy Stock Broking Research is also available on: Bloomberg ‐ KRVY <GO>, Thomson Publisher & Reuters.

Stock Ratings Absolute ReturnsBuy : > 15%Hold : 5‐15%Sell : < 5%