Embed Size (px)

Citation preview

1

DELOITTE TAX LLP 600 Renaissance Center, Suite 900 Detroit, MI 48243-1595 Telephone: 313-396-3000

Tax Service Providers for the Debtors and Debtors in Possession

IN THE UNITED STATES BANKRUPTCY COURT EASTERN DISTRICT OF MICHIGAN

SOUTHERN DIVISION

In re: ) Chapter 11 ) COLLINS & AIKMAN CORPORATION, et al.1 ) Case No. 05-55927 (SWR) ) (Jointly Administered) Debtors. ) ) (Tax Identification #13-3489233) ) ) Honorable Steven W. Rhodes

THIS SUMMARY SHEET APPLIES TO:

X All Debtors Collins & Aikman Interiors Inc

Collins & Aikman Corporation Dura Convertible Systems Inc

Collins & Aikman Products Co. Comet Acoustics Inc

1 The Debtors in the jointly administered cases include: Collins & Aikman Corporation; Amco Convertible Fabrics, Inc., Case No. 05-55949; Becker Group, LLC (d/b/a/ Collins & Aikman Premier Mold), Case No. 05-55977; Brut Plastics, Inc., Case No. 05-55957; Collins & Aikman (Gibraltar) Limited, Case No. 05-55989; Collins & Aikman Accessory Mats, Inc. (f/k/a the Akro Corporation), Case No. 05-55952; Collins & Aikman Asset Services, Inc., Case No. 05-55959; Collins & Aikman Automotive (Argentina), Inc. (f/k/a Textron Automotive (Argentina), Inc.), Case No. 05-55965; Collins & Aikman Automotive (Asia), Inc. (f/k/a Textron Automotive (Asia), Inc.), Case No. 05-55991; Collins & Aikman Automotive Exteriors, Inc. (f/k/a Textron Automotive Exteriors, Inc.), Case No. 05-55958; Collins & Aikman Automotive Interiors, Inc. (f/k/a Textron Automotive Interiors, Inc.), Case No. 05-55956; Collins & Aikman Automotive International, Inc., Case No. 05-55980; Collins & Aikman Automotive International Services, Inc. (f/k/a Textron Automotive International Services, Inc.), Case No. 05-55985; Collins & Aikman Automotive Mats, LLC, Case No. 05-55969; Collins & Aikman Automotive Overseas Investment, Inc. (f/k/a Textron Automotive Overseas Investment, Inc.), Case No. 05-55978; Collins & Aikman Automotive Services, LLC, Case No. 05-55981; Collins & Aikman Canada Domestic Holding Company, Case No. 05-55930; Collins & Aikman Carpet & Acoustics (MI), Inc., Case No. 05-55982; Collins & Aikman Carpet & Acoustics (TN), Inc., Case No. 05-55984; Collins & Aikman Development Company, Case No. 05-55943; Collins & Aikman Europe, Inc., Case No. 05-55971; Collins & Aikman Fabrics, Inc. (d/b/a Joan Automotive Industries, Inc.), Case No. 05-55963; Collins & Aikman Intellimold, Inc. (d/b/a M&C Advanced Processes, Inc.), Case No. 05-55976; Collins & Aikman Interiors, Inc., Case No. 05-55970; Collins & Aikman International Corporation, Case No. 05-55951; Collins & Aikman Plastics, Inc., Case No. 05-55960; Collins & Aikman Products Co., Case No. 05-55932; Collins & Aikman Properties, Inc., Case No. 05-55964; Comet Acoustics, Inc., Case No. 05-55972; CW Management Corporation, Case No. 05-55979; Dura Convertible Systems, Inc., Case No. 05-55942; Gamble Development Company, Case No. 05-55974; JPS Automotive, Inc. (d/b/a PACJ, Inc.), Case No. 05-55935; New Baltimore Holdings, LLC, Case No. 05-55992; Owosso Thermal Forming, LLC, Case No. 05-55946; Southwest Laminates, Inc. (d/b/a Southwest Fabric Laminators Inc.), Case No. 05-55948; Wickes Asset Management, Inc., Case No. 05-55962; and Wickes Manufacturing Company, Case No. 05-55968.

2

Gamble Development Company JPS Automotive, Inc

Collins & Aikman Properties, Inc. Collins & Aikman Accessory Mats, Inc.

Wickes Manufacturing Company Collins & Aikman Canada Domestic Holding Company

Wickes Asset Management, Inc. Collins & Aikman Carpet & Acoustics (MI), Inc.

Collins & Aikman Asset Services, Inc. Collins & Aikman Carpet & Acoustics (TN), Inc.

Carcorp, Inc. Collins & Aikman Plastics, Inc.

Waterstone Insurance, Inc. Collins & Aikman Automotive Services, LLC

Collins & Aikman Development Company CW Management Corporation

Collins & Aikman International Corporation SAF Services Corporation

Southwest Laminates, Inc. Hopkins Services, Inc

Collins & Aikman Fabrics, Inc. Collins & Aikman Europe, Inc

Collins & Aikman Automotive Exteriors Inc. Collins & Aikman Automotive International, Inc.

Synova Plastics, LLC Collins & Aikman Automotive Interiors, Inc.

Amco Convertible Fabrics, Inc. Synova Carpets LLC

ACAP LLC Becker Group LLC

Collins & Aikman (Gibraltar) Limited Collins & Aikman Automotive Mats LLC

Collins & Aikman Automotive (Asia), Inc. Collins & Aikman Automotive Overseas Investment, Inc.

Collins & Aikman Intellimold, Inc. Owosso Thermal Forming, LLC

Collins & Aikman – MOBIS, LLC Brut Plastics, Inc.

Engineered Plastic Products, Inc. Collins & Aikman Automotive (Argentina) Inc.

Collins & Aikman International Services, Inc. New Baltimore Holdings, LLC

3

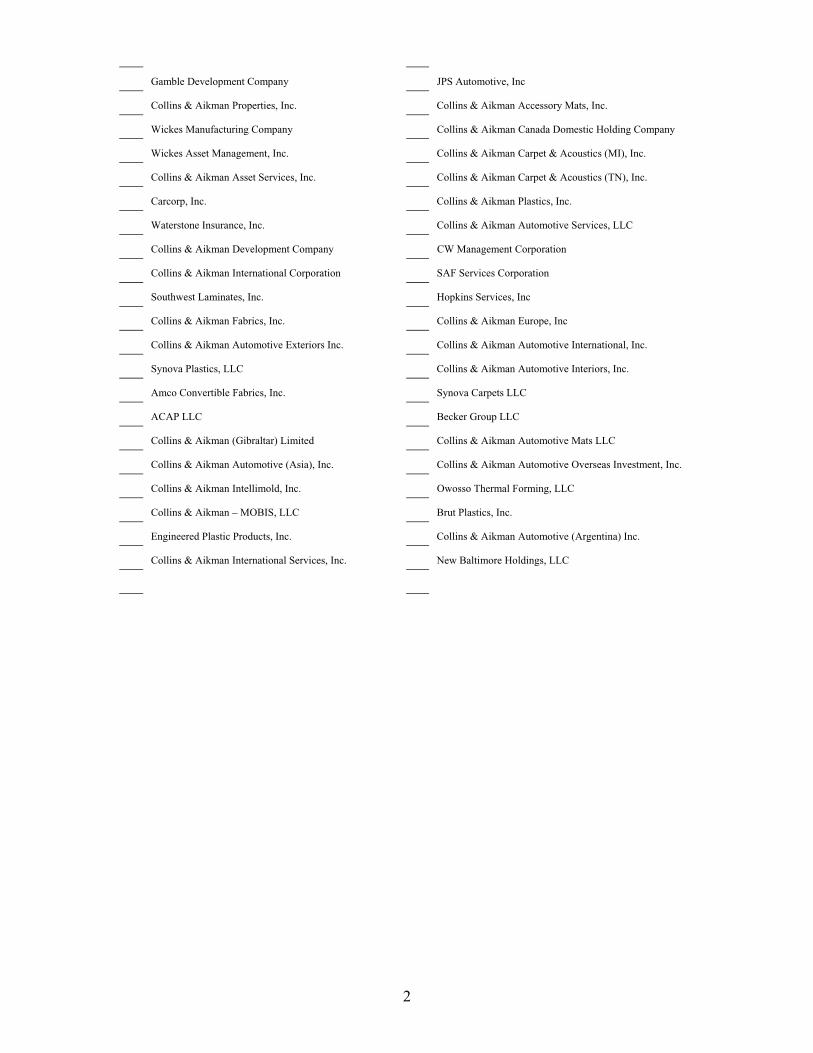

SUMMARY SHEET PURSUANT TO THE UNITED STATES TRUSTEE GUIDELINES FOR REVIEWING APPLICATIONS FOR COMPENSATION

AND REIMBURSEMENT OF EXPENSES FILED UNDER 11 U.S.C. § 330

Name of Applicant: DELOITTE TAX LLP

Date of Retention: Nunc Pro Tunc to September 1, 2005

Date of Entry of Order Authorizing Employment November 10, 2005

Period for Which Compensation and Reimbursement is Sought: September 1, 2006 through and including

December 31, 2006

Amount of Compensation Sought As Actual, Necessary and Reasonable: $391681

Amount of Expense Reimbursement Sought as Actual, Necessary, and Reasonable: $3,840

This is: A Fourth Interim Fee Application

Blended Applicable Hourly Rate of Professionals And Paraprofessionals $239.85

- 1 -

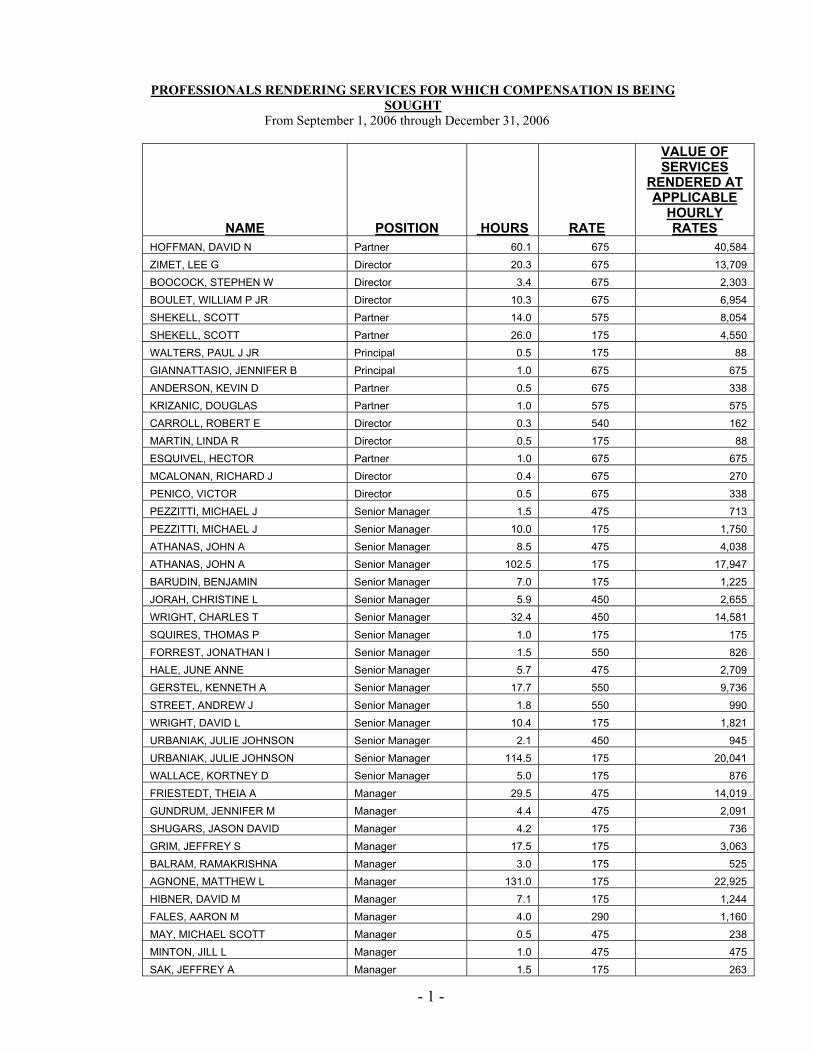

PROFESSIONALS RENDERING SERVICES FOR WHICH COMPENSATION IS BEING SOUGHT

From September 1, 2006 through December 31, 2006

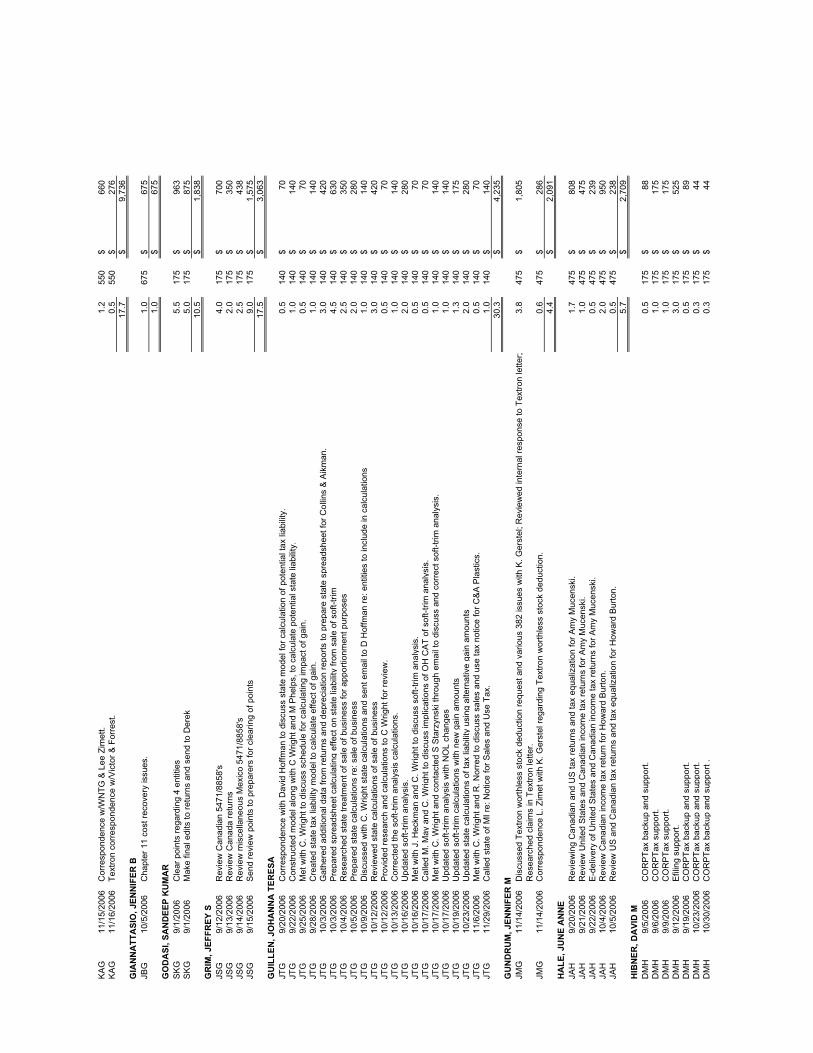

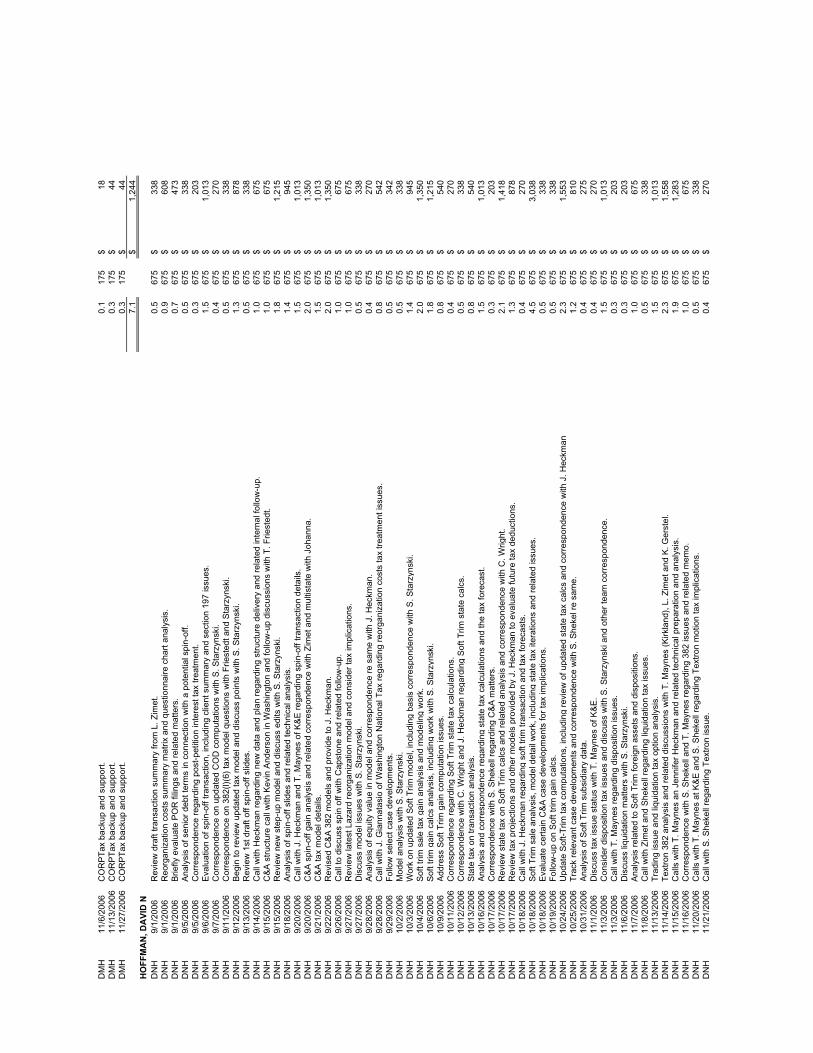

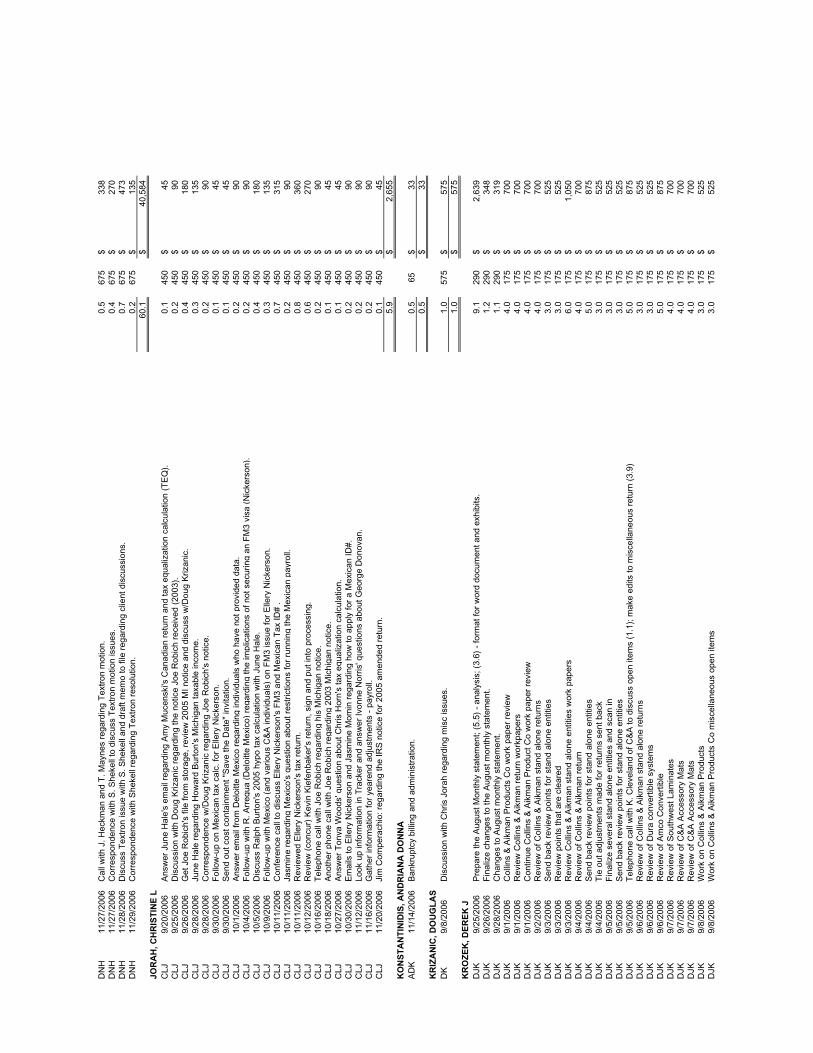

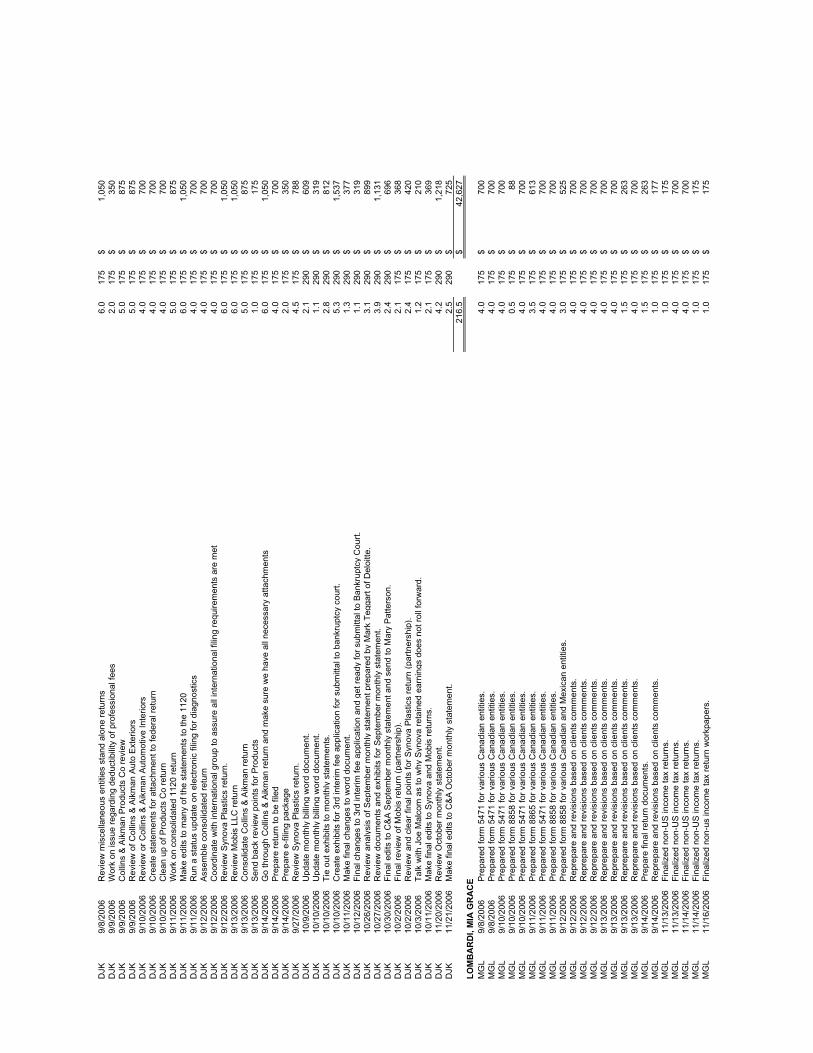

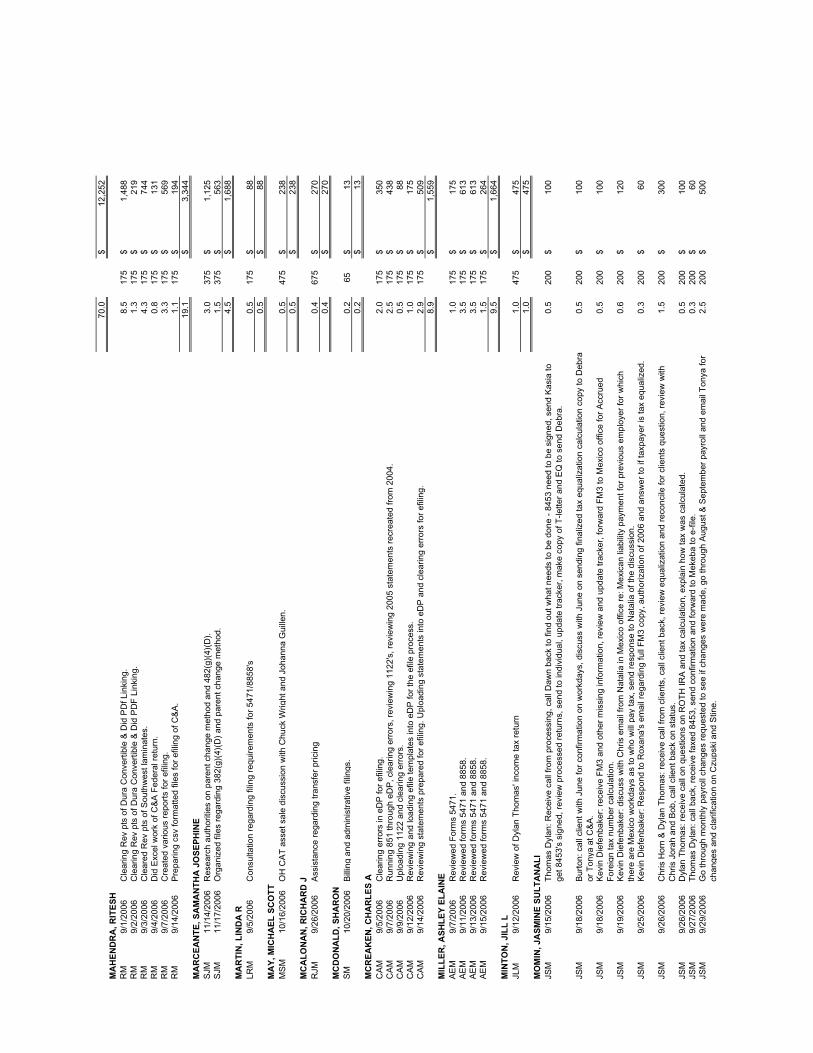

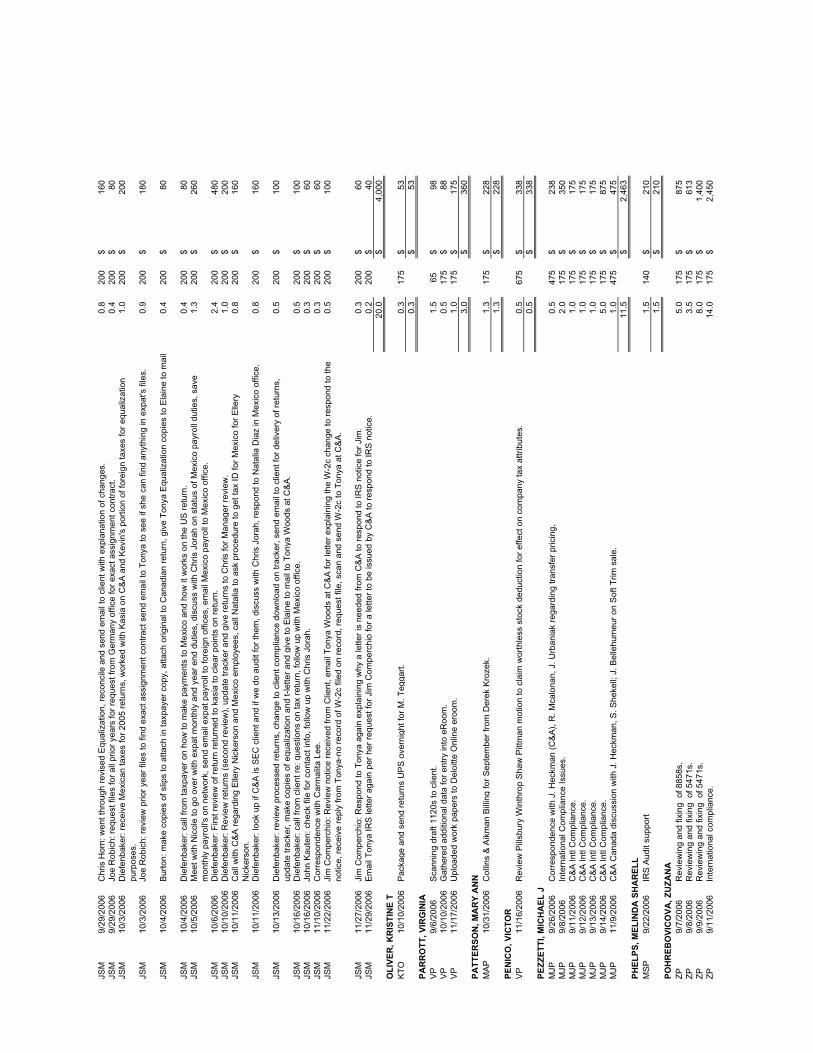

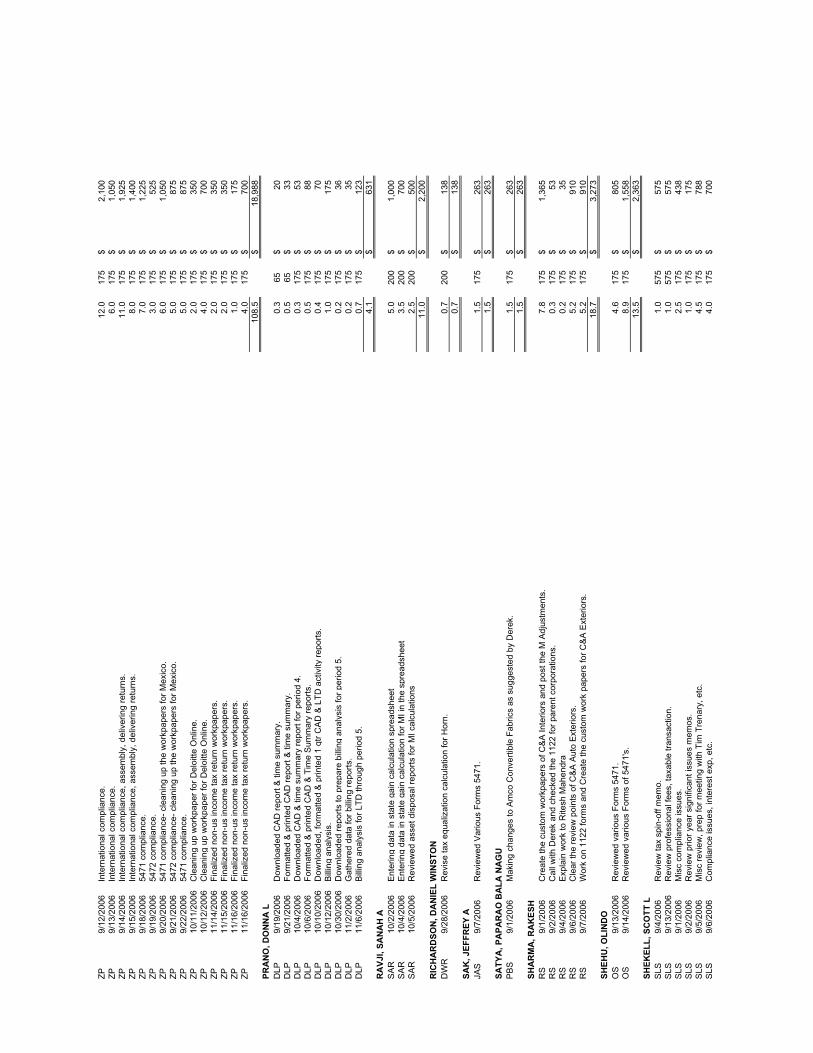

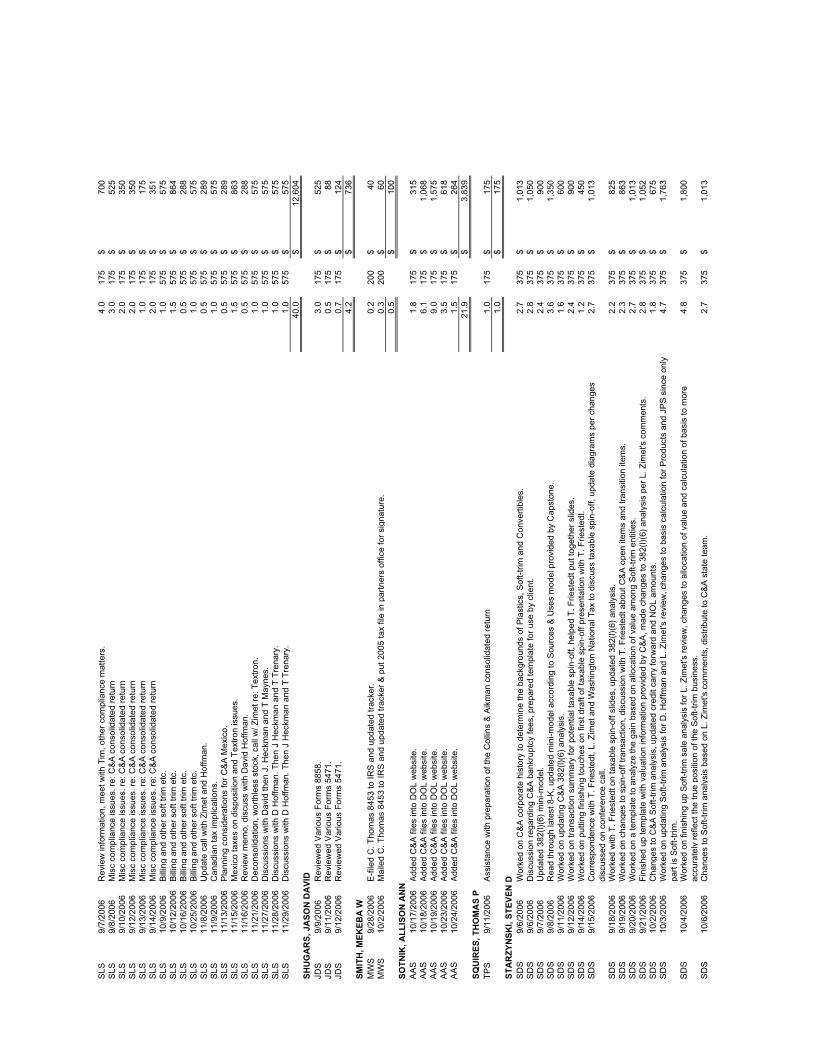

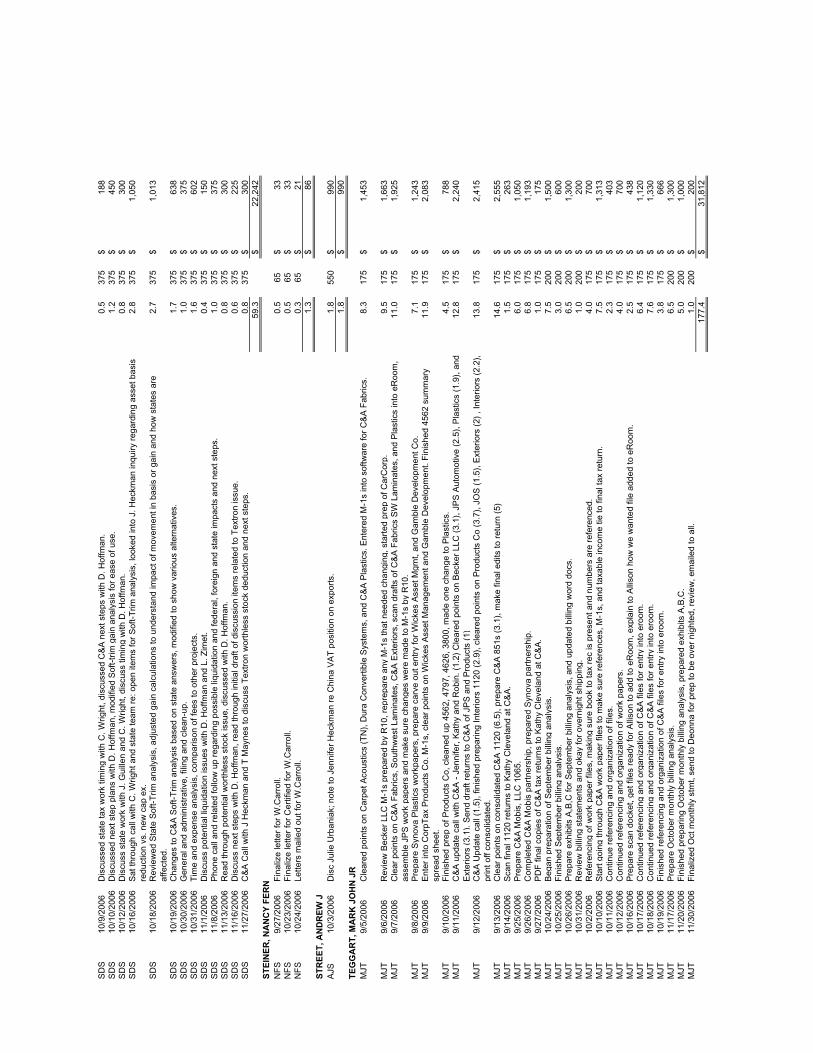

NAME POSITION HOURS RATE

VALUE OF SERVICES

RENDERED AT APPLICABLE

HOURLY RATES

HOFFMAN, DAVID N Partner 60.1 675 40,584

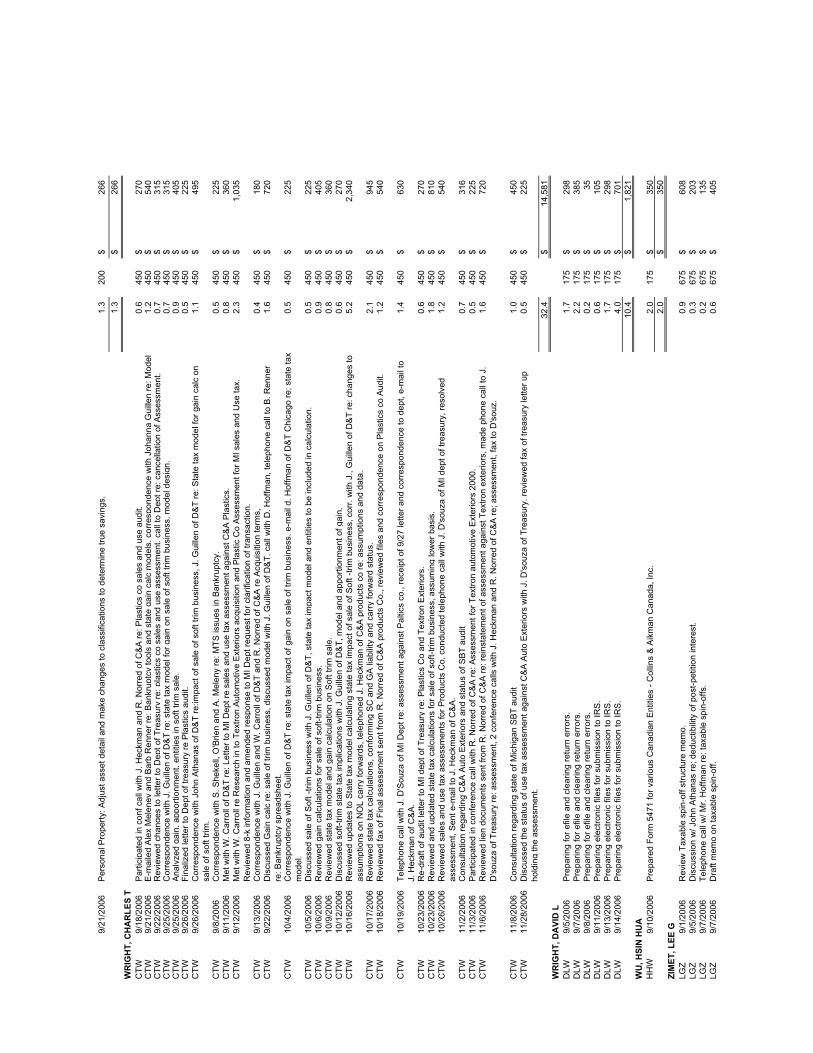

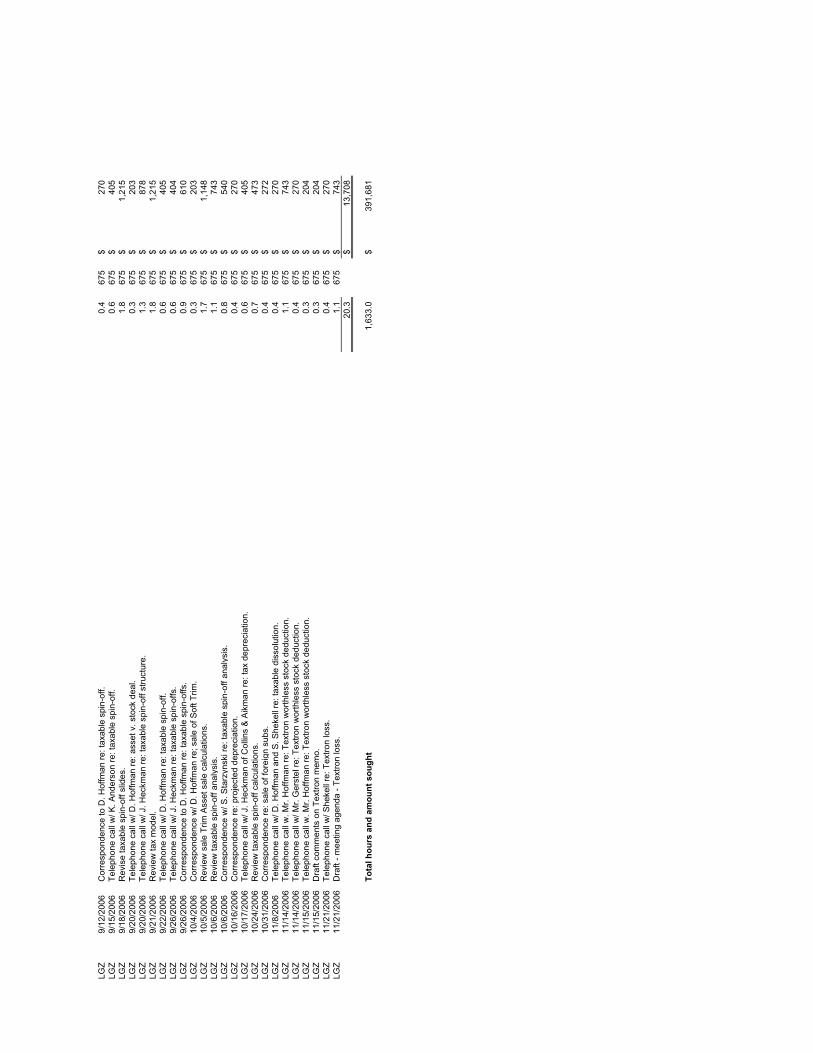

ZIMET, LEE G Director 20.3 675 13,709

BOOCOCK, STEPHEN W Director 3.4 675 2,303

BOULET, WILLIAM P JR Director 10.3 675 6,954

SHEKELL, SCOTT Partner 14.0 575 8,054

SHEKELL, SCOTT Partner 26.0 175 4,550

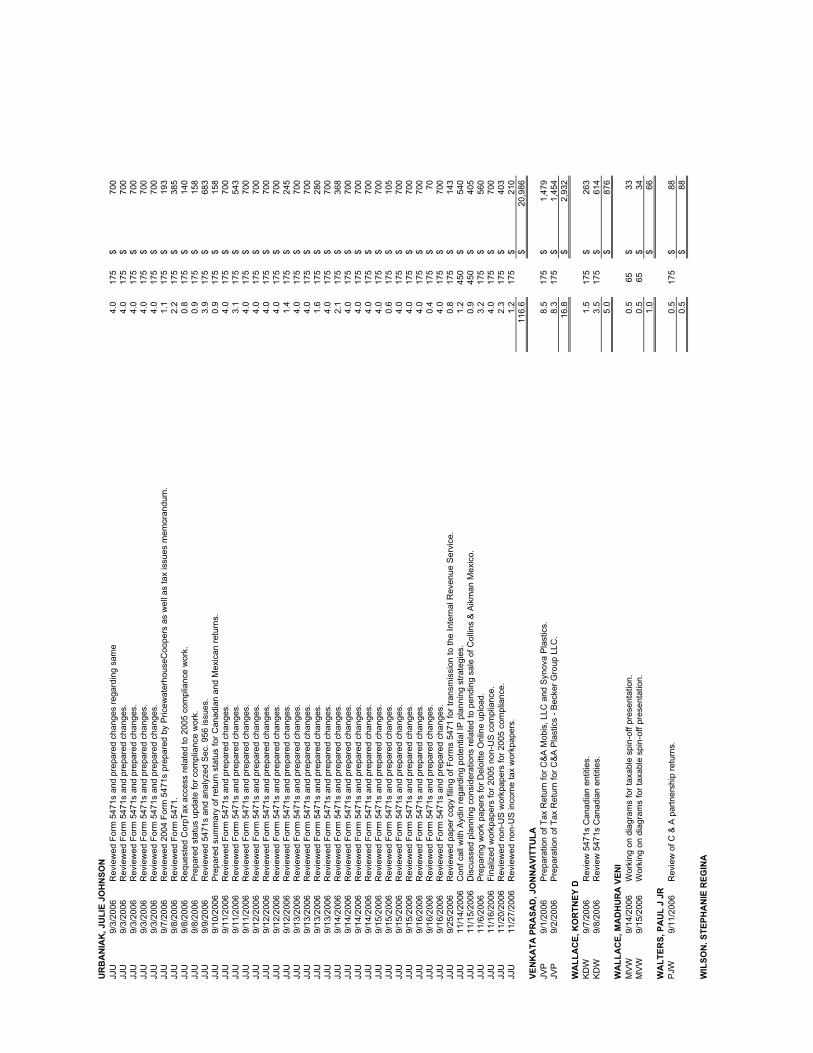

WALTERS, PAUL J JR Principal 0.5 175 88

GIANNATTASIO, JENNIFER B Principal 1.0 675 675

ANDERSON, KEVIN D Partner 0.5 675 338

KRIZANIC, DOUGLAS Partner 1.0 575 575

CARROLL, ROBERT E Director 0.3 540 162

MARTIN, LINDA R Director 0.5 175 88

ESQUIVEL, HECTOR Partner 1.0 675 675

MCALONAN, RICHARD J Director 0.4 675 270

PENICO, VICTOR Director 0.5 675 338

PEZZITTI, MICHAEL J Senior Manager 1.5 475 713

PEZZITTI, MICHAEL J Senior Manager 10.0 175 1,750

ATHANAS, JOHN A Senior Manager 8.5 475 4,038

ATHANAS, JOHN A Senior Manager 102.5 175 17,947

BARUDIN, BENJAMIN Senior Manager 7.0 175 1,225

JORAH, CHRISTINE L Senior Manager 5.9 450 2,655

WRIGHT, CHARLES T Senior Manager 32.4 450 14,581

SQUIRES, THOMAS P Senior Manager 1.0 175 175

FORREST, JONATHAN I Senior Manager 1.5 550 826

HALE, JUNE ANNE Senior Manager 5.7 475 2,709

GERSTEL, KENNETH A Senior Manager 17.7 550 9,736

STREET, ANDREW J Senior Manager 1.8 550 990

WRIGHT, DAVID L Senior Manager 10.4 175 1,821

URBANIAK, JULIE JOHNSON Senior Manager 2.1 450 945

URBANIAK, JULIE JOHNSON Senior Manager 114.5 175 20,041

WALLACE, KORTNEY D Senior Manager 5.0 175 876

FRIESTEDT, THEIA A Manager 29.5 475 14,019

GUNDRUM, JENNIFER M Manager 4.4 475 2,091

SHUGARS, JASON DAVID Manager 4.2 175 736

GRIM, JEFFREY S Manager 17.5 175 3,063

BALRAM, RAMAKRISHNA Manager 3.0 175 525

AGNONE, MATTHEW L Manager 131.0 175 22,925

HIBNER, DAVID M Manager 7.1 175 1,244

FALES, AARON M Manager 4.0 290 1,160

MAY, MICHAEL SCOTT Manager 0.5 475 238

MINTON, JILL L Manager 1.0 475 475

SAK, JEFFREY A Manager 1.5 175 263

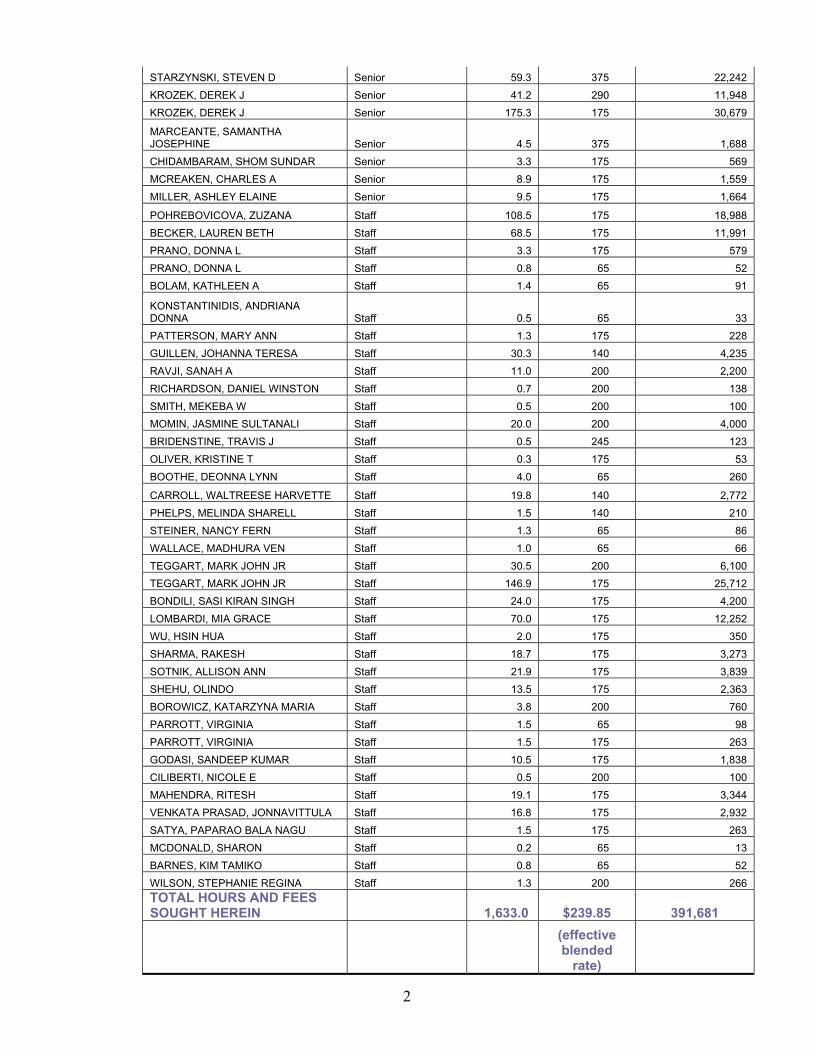

2

STARZYNSKI, STEVEN D Senior 59.3 375 22,242

KROZEK, DEREK J Senior 41.2 290 11,948

KROZEK, DEREK J Senior 175.3 175 30,679

MARCEANTE, SAMANTHA JOSEPHINE Senior 4.5 375 1,688

CHIDAMBARAM, SHOM SUNDAR Senior 3.3 175 569

MCREAKEN, CHARLES A Senior 8.9 175 1,559

MILLER, ASHLEY ELAINE Senior 9.5 175 1,664

POHREBOVICOVA, ZUZANA Staff 108.5 175 18,988

BECKER, LAUREN BETH Staff 68.5 175 11,991

PRANO, DONNA L Staff 3.3 175 579

PRANO, DONNA L Staff 0.8 65 52

BOLAM, KATHLEEN A Staff 1.4 65 91

KONSTANTINIDIS, ANDRIANA DONNA Staff 0.5 65 33

PATTERSON, MARY ANN Staff 1.3 175 228

GUILLEN, JOHANNA TERESA Staff 30.3 140 4,235

RAVJI, SANAH A Staff 11.0 200 2,200

RICHARDSON, DANIEL WINSTON Staff 0.7 200 138

SMITH, MEKEBA W Staff 0.5 200 100

MOMIN, JASMINE SULTANALI Staff 20.0 200 4,000

BRIDENSTINE, TRAVIS J Staff 0.5 245 123

OLIVER, KRISTINE T Staff 0.3 175 53

BOOTHE, DEONNA LYNN Staff 4.0 65 260

CARROLL, WALTREESE HARVETTE Staff 19.8 140 2,772

PHELPS, MELINDA SHARELL Staff 1.5 140 210

STEINER, NANCY FERN Staff 1.3 65 86

WALLACE, MADHURA VEN Staff 1.0 65 66

TEGGART, MARK JOHN JR Staff 30.5 200 6,100

TEGGART, MARK JOHN JR Staff 146.9 175 25,712

BONDILI, SASI KIRAN SINGH Staff 24.0 175 4,200

LOMBARDI, MIA GRACE Staff 70.0 175 12,252

WU, HSIN HUA Staff 2.0 175 350

SHARMA, RAKESH Staff 18.7 175 3,273

SOTNIK, ALLISON ANN Staff 21.9 175 3,839

SHEHU, OLINDO Staff 13.5 175 2,363

BOROWICZ, KATARZYNA MARIA Staff 3.8 200 760

PARROTT, VIRGINIA Staff 1.5 65 98

PARROTT, VIRGINIA Staff 1.5 175 263

GODASI, SANDEEP KUMAR Staff 10.5 175 1,838

CILIBERTI, NICOLE E Staff 0.5 200 100

MAHENDRA, RITESH Staff 19.1 175 3,344

VENKATA PRASAD, JONNAVITTULA Staff 16.8 175 2,932

SATYA, PAPARAO BALA NAGU Staff 1.5 175 263

MCDONALD, SHARON Staff 0.2 65 13

BARNES, KIM TAMIKO Staff 0.8 65 52

WILSON, STEPHANIE REGINA Staff 1.3 200 266 TOTAL HOURS AND FEES SOUGHT HEREIN 1,633.0 $239.85

391,681

(effective blended

rate)

3

DELOITTE TAX LLP 600 Renaissance Center, Suite 900 Detroit, MI 48243-1595 Telephone: 313-396-3000

Tax Service Providers for the Debtors and Debtors in Possession

IN THE UNITED STATES BANKRUPTCY COURT EASTERN DISTRICT OF MICHIGAN

SOUTHERN DIVISION

In re: ) Chapter 11 ) COLLINS & AIKMAN CORPORATION, et al.2 ) Case No. 05-55927 (SWR) ) (Jointly Administered) Debtors. ) ) (Tax Identification #13-3489233) ) Honorable Steven W. Rhodes

THIS STATEMENT APPLIES TO:

X All Debtors Collins & Aikman Interiors Inc

2 The Debtors in the jointly administered cases include: Collins & Aikman Corporation; Amco Convertible Fabrics, Inc., Case No. 05-55949; Becker Group, LLC (d/b/a/ Collins & Aikman Premier Mold), Case No. 05-55977; Brut Plastics, Inc., Case No. 05-55957; Collins & Aikman (Gibraltar) Limited, Case No. 05-55989; Collins & Aikman Accessory Mats, Inc. (f/k/a the Akro Corporation), Case No. 05-55952; Collins & Aikman Asset Services, Inc., Case No. 05-55959; Collins & Aikman Automotive (Argentina), Inc. (f/k/a Textron Automotive (Argentina), Inc.), Case No. 05-55965; Collins & Aikman Automotive (Asia), Inc. (f/k/a Textron Automotive (Asia), Inc.), Case No. 05-55991; Collins & Aikman Automotive Exteriors, Inc. (f/k/a Textron Automotive Exteriors, Inc.), Case No. 05-55958; Collins & Aikman Automotive Interiors, Inc. (f/k/a Textron Automotive Interiors, Inc.), Case No. 05-55956; Collins & Aikman Automotive International, Inc., Case No. 05-55980; Collins & Aikman Automotive International Services, Inc. (f/k/a Textron Automotive International Services, Inc.), Case No. 05-55985; Collins & Aikman Automotive Mats, LLC, Case No. 05-55969; Collins & Aikman Automotive Overseas Investment, Inc. (f/k/a Textron Automotive Overseas Investment, Inc.), Case No. 05-55978; Collins & Aikman Automotive Services, LLC, Case No. 05-55981; Collins & Aikman Canada Domestic Holding Company, Case No. 05-55930; Collins & Aikman Carpet & Acoustics (MI), Inc., Case No. 05-55982; Collins & Aikman Carpet & Acoustics (TN), Inc., Case No. 05-55984; Collins & Aikman Development Company, Case No. 05-55943; Collins & Aikman Europe, Inc., Case No. 05-55971; Collins & Aikman Fabrics, Inc. (d/b/a Joan Automotive Industries, Inc.), Case No. 05-55963; Collins & Aikman Intellimold, Inc. (d/b/a M&C Advanced Processes, Inc.), Case No. 05-55976; Collins & Aikman Interiors, Inc., Case No. 05-55970; Collins & Aikman International Corporation, Case No. 05-55951; Collins & Aikman Plastics, Inc., Case No. 05-55960; Collins & Aikman Products Co., Case No. 05-55932; Collins & Aikman Properties, Inc., Case No. 05-55964; Comet Acoustics, Inc., Case No. 05-55972; CW Management Corporation, Case No. 05-55979; Dura Convertible Systems, Inc., Case No. 05-55942; Gamble Development Company, Case No. 05-55974; JPS Automotive, Inc. (d/b/a PACJ, Inc.), Case No. 05-55935; New Baltimore Holdings, LLC, Case No. 05-55992; Owosso Thermal Forming, LLC, Case No. 05-55946; Southwest Laminates, Inc. (d/b/a Southwest Fabric Laminators Inc.), Case No. 05-55948; Wickes Asset Management, Inc., Case No. 05-55962; and Wickes Manufacturing Company, Case No. 05-55968.

4

Collins & Aikman Corporation Dura Convertible Systems Inc

Collins & Aikman Products Co. Comet Acoustics Inc

Gamble Development Company JPS Automotive, Inc

Collins & Aikman Properties, Inc. Collins & Aikman Accessory Mats, Inc.

Wickes Manufacturing Company Collins & Aikman Canada Domestic Holding Company

Wickes Asset Management, Inc. Collins & Aikman Carpet & Acoustics (MI), Inc.

Collins & Aikman Asset Services, Inc. Collins & Aikman Carpet & Acoustics (TN), Inc.

Carcorp, Inc. Collins & Aikman Plastics, Inc.

Waterstone Insurance, Inc. Collins & Aikman Automotive Services, LLC

Collins & Aikman Development Company CW Management Corporation

Collins & Aikman International Corporation SAF Services Corporation

Southwest Laminates, Inc. Hopkins Services, Inc

Collins & Aikman Fabrics, Inc. Collins & Aikman Europe, Inc

Collins & Aikman Automotive Exteriors Inc. Collins & Aikman Automotive International, Inc.

Synova Plastics, LLC Collins & Aikman Automotive Interiors, Inc.

Amco Convertible Fabrics, Inc. Synova Carpets LLC

ACAP LLC Becker Group LLC

Collins & Aikman (Gibraltar) Limited Collins & Aikman Automotive Mats LLC

Collins & Aikman Automotive (Asia), Inc. Collins & Aikman Automotive Overseas Investment, Inc.

Collins & Aikman Intellimold, Inc. Owosso Thermal Forming, LLC

Collins & Aikman – MOBIS, LLC Brut Plastics, Inc.

Engineered Plastic Products, Inc. Collins & Aikman Automotive (Argentina) Inc.

Collins & Aikman International Services, Inc. New Baltimore Holdings, LLC

FOURTH INTERIM FEE APPLICATION OF DELOITTE TAX LLP AS TAX SERVICE PROVIDERS FOR THE DEBTORS FOR ALLOWANCE

OF INTERIM COMPENSATION FOR SERVICES RENDERED AND EXPENSES INCURRED

FROM SEPTEMBER 1, 2006 THROUGH DECEMBER 31, 2006

Deloitte Tax LLP (“Deloitte Tax”), tax service providers for Collins &

Aikman Corporation (“Collins & Aikman”) and certain of its affiliates, as debtors

and debtors in possession (collectively, the “Debtors”), pursuant to sections

330(a) and 331 of title 11 of the United States Code (the “Bankruptcy Code”) and

Rule 2016 of the Federal Rules of Bankruptcy Procedure (the “Bankruptcy

Rules”), Rules 2016-1 and 9014-1 of the Local Rules for the United States

5

Bankruptcy Court, Eastern District of Michigan, the Retention Order (as defined

below) and the Administrative Order (as defined below) files this application (the

“Fourth Interim Fee Application”) for, and hereby applies for entry of an order,

substantially in the form of Exhibit F, allowing it interim allowance of,

compensation for professional services performed by Deloitte Tax for the period

from September 1, 2006 through December 31, 2006 (the “Compensation

Period”) and for reimbursement of expenses associated therewith. Deloitte Tax

respectfully represents:

JURISDICTION

1. This Court has jurisdiction to consider this Fourth Interim

Application pursuant to 28 U.S.C. §§ 157 and 1334. Consideration of this Fourth

Interim Application is a core proceeding pursuant to 28 U.S.C. § 157(b)(2).

Venue of this case is proper in this district pursuant to 28 U.S.C. §§ 1408 and

1409, respectively. The statutory predicate for the relief requested herein is

sections 330 and 331 of the Bankruptcy Code.

GENERAL BACKGROUND

2. On September 1, 2005 (the "Petition Date"), each of the Debtors

filed a petition with this Court under Chapter 11 of the Bankruptcy Code. The

Debtors are operating their businesses and managing their property as debtors in

possession pursuant to sections 1107(a) and 1108 of the Bankruptcy Code. No

request for the appointment of a trustee or examiner has been made in these

Chapter 11 cases.

6

THE RETENTION OF DELOITTE TAX LLP

3. On November 10, 2005 the Court entered an Order Approving the

Employment of Deloitte Tax LLP as Tax Service Providers Nunc Pro Tunc to

September 1, 2005 (the “Retention Order”), pursuant to a retention application

submitted by the Debtors (the “Retention Application”). A copy of the Retention

Order is attached hereto as Exhibit A. Pursuant to the Retention Order, Deloitte

Tax was authorized to perform and to be compensated by the Debtors, subject to

application to this Court as set forth therein, for various tax services, including

expatriate tax services, contingent fee strategic review services and other

bankruptcy-related tax consulting services, and, inter alia, tax advisory services

for the Debtors related to debt discharge issues arising in connection with this

case. The Retention Order also authorized Deloitte Tax’s reimbursement for

actual and necessary expenses incurred, subject to application to this Court as set

forth therein.

SUMMARY OF PROFESSIONAL COMPENSATION AND REIMBURSEMENT OF EXPENSES REQUESTED

4. Except as is clarified herein, Deloitte Tax has striven to prepare the

Fourth Interim Fee Application in accordance with applicable guidelines for fees

and disbursements of professionals in the Eastern District of Michigan bankruptcy

cases, adopted by the Court (the “Local Guidelines”), or United States Trustee

guidelines for reviewing applications for compensation and reimbursement of

expenses filed under 11 U.S.C. § 330 (the “UST Guidelines”), and with the

interim compensation Administrative Order Establishing Procedures for Monthly

Compensation and Reimbursement of Expenses of Professionals and Official

7

Committee Members [Docket No. 290] (the “Administrative Order,” and together

with the Local Guidelines and the UST Guidelines, the “Guidelines”).

5. Deloitte Tax seeks allowance of interim compensation for the tax

services (the “Tax Services”) rendered to the Debtors during the Compensation

Period in the amount of $391,681 as is more fully described below. Deloitte Tax

is also seeking allowance of interim reimbursement of expenses incurred in

connection with the Tax Services rendered to the Debtors during the

Compensation Period in the amount of $3,840, and reserves the right to seek

trailing expenses, including, without limitation, for December 2006, if any, in a

future interim fee application.

6. The compensation for fees being sought in this Fourth Interim Fee

Application is thus only for 1,633.00 hours of the Tax Services at a $239.85

blended hourly rate in the total amount of $391,681for the Compensation Period

and, as noted above, reflects time incurred in connection with Chapter 11

administration matters.

7. Deloitte Tax has received no promises regarding compensation in

these Chapter 11 cases other than in accordance with the Bankruptcy Code and as

set forth in the Retention Application. In respect of the services to be provided by

Deloitte Tax to the Debtors in these Chapter 11 cases, Deloitte Tax has no

agreement with any nonaffiliated entity to share any revenues from such services.

8. Deloitte Tax’s fees in these cases are billed in accordance with the

existing compensation arrangements set forth in the engagement letter(s) between

the Debtors and Deloitte Tax in effect during the Compensation Period. The rates

Deloitte Tax charges for the services rendered by professionals in these Chapter

11 cases are consistent with the rates Deloitte Tax charges for professional

8

services rendered in comparable non-bankruptcy-related matters. Such fees are

reasonable based on the customary compensation charged by comparably skilled

practitioners in comparable non-bankruptcy cases in a competitive professional

services market.

9. Pursuant to the Guidelines, supplied herewith is a schedule setting

forth all professionals and paraprofessionals who have performed services in these

Chapter 11 cases during the Compensation Period for which interim

compensation is being sought, each such individual’s position with Deloitte Tax

the hourly rate charged by Deloitte Tax, for services performed by each such

individual, and the aggregate number of hours expended by each such individual.

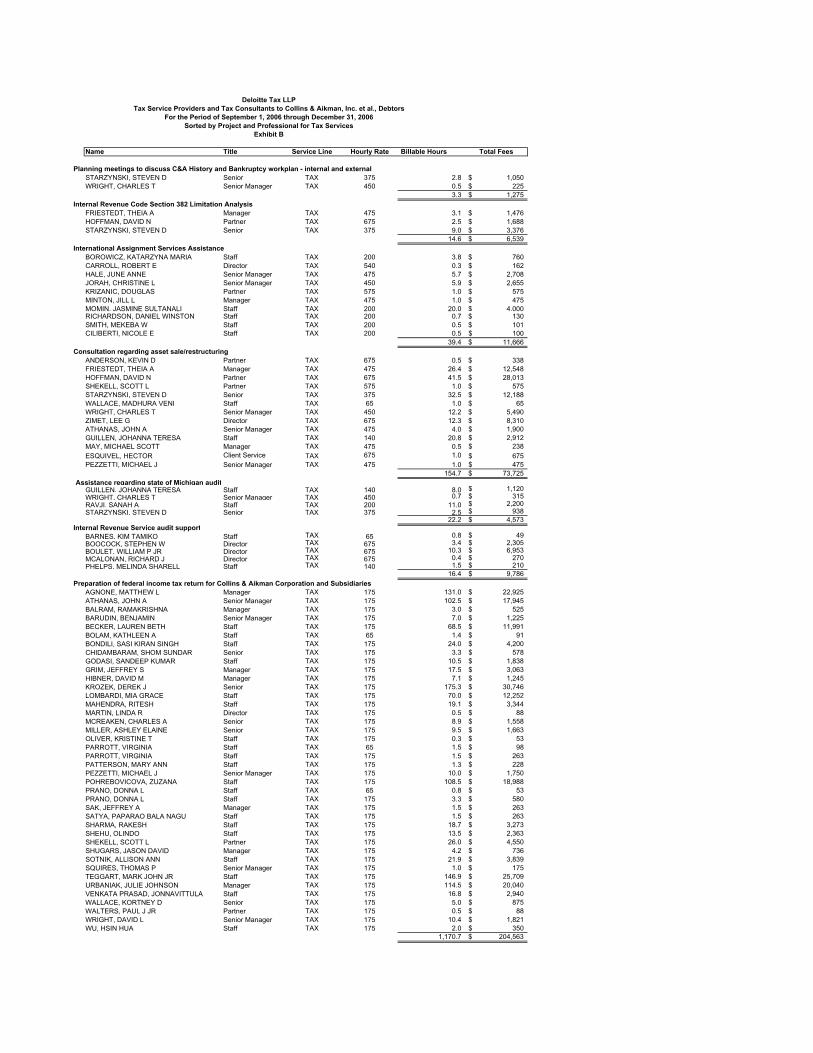

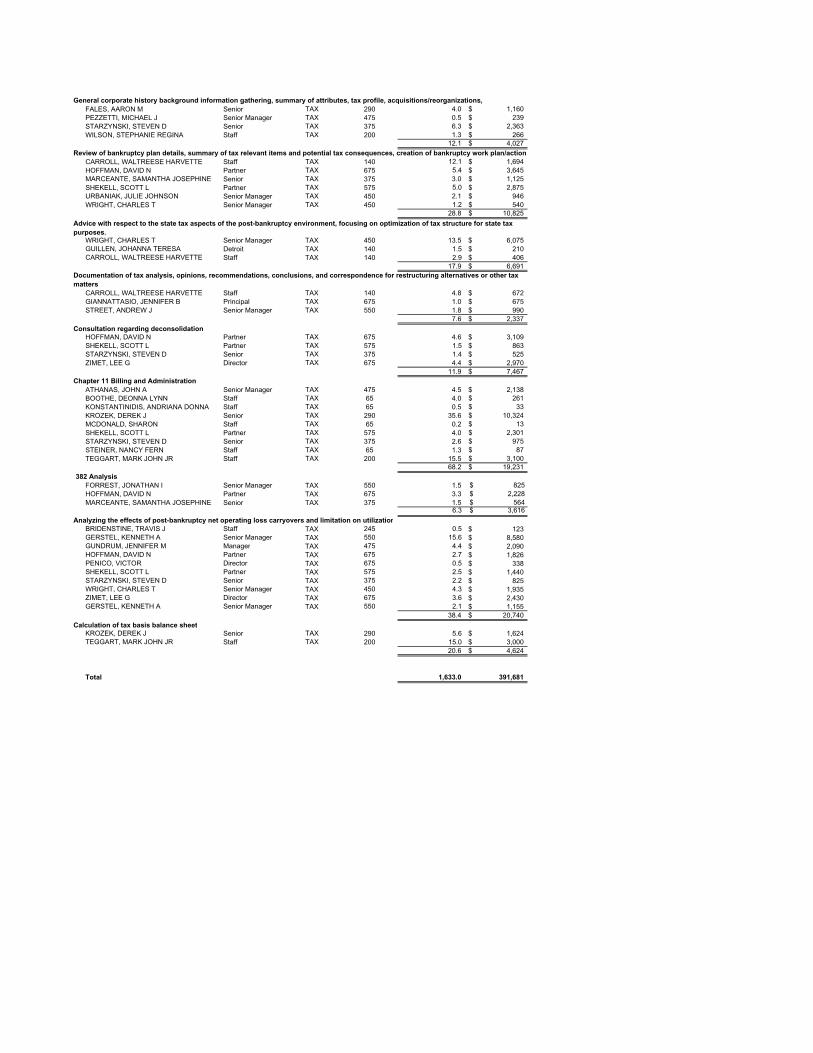

10. Pursuant to the Guidelines, annexed hereto as Exhibit B is a

summary statement of the number of hours of services rendered by each

professional and the hourly rate of each by project categories for the services

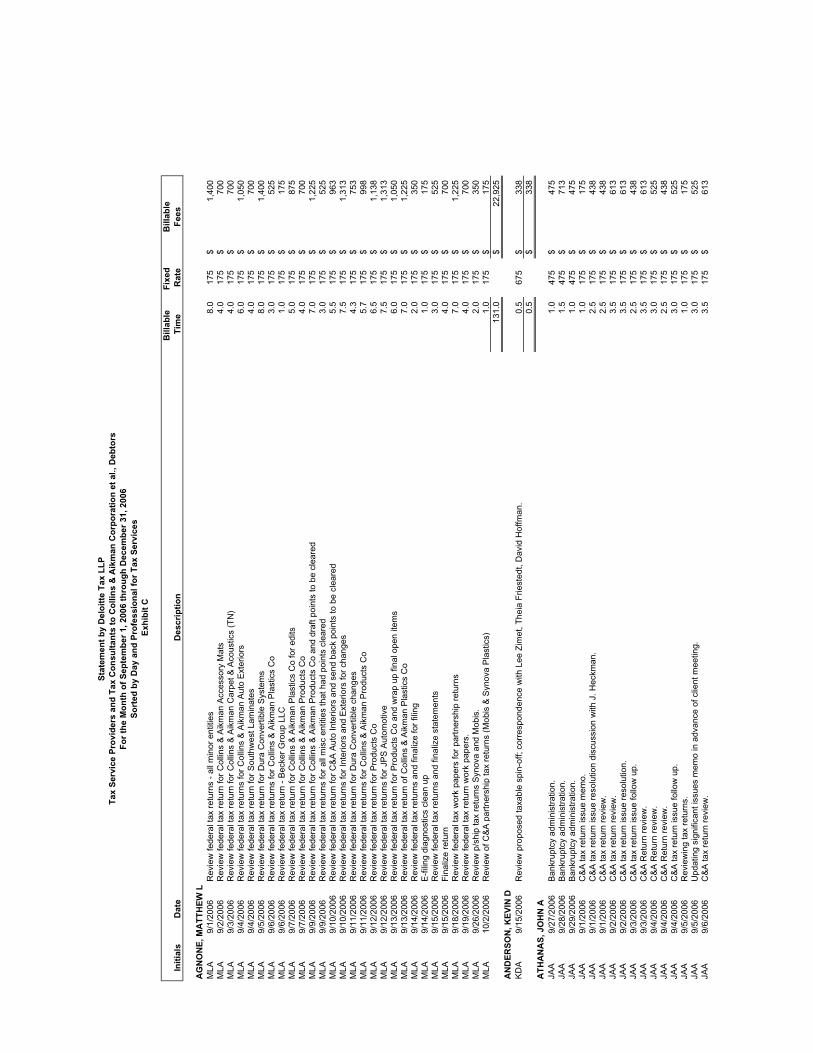

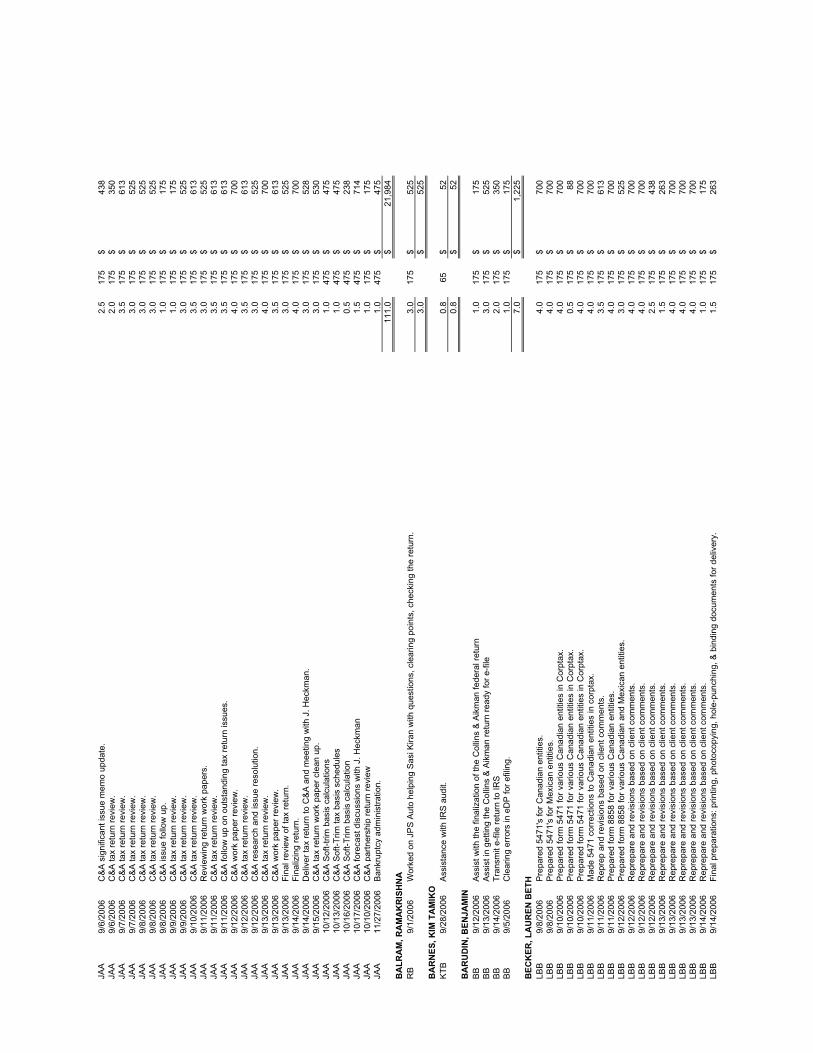

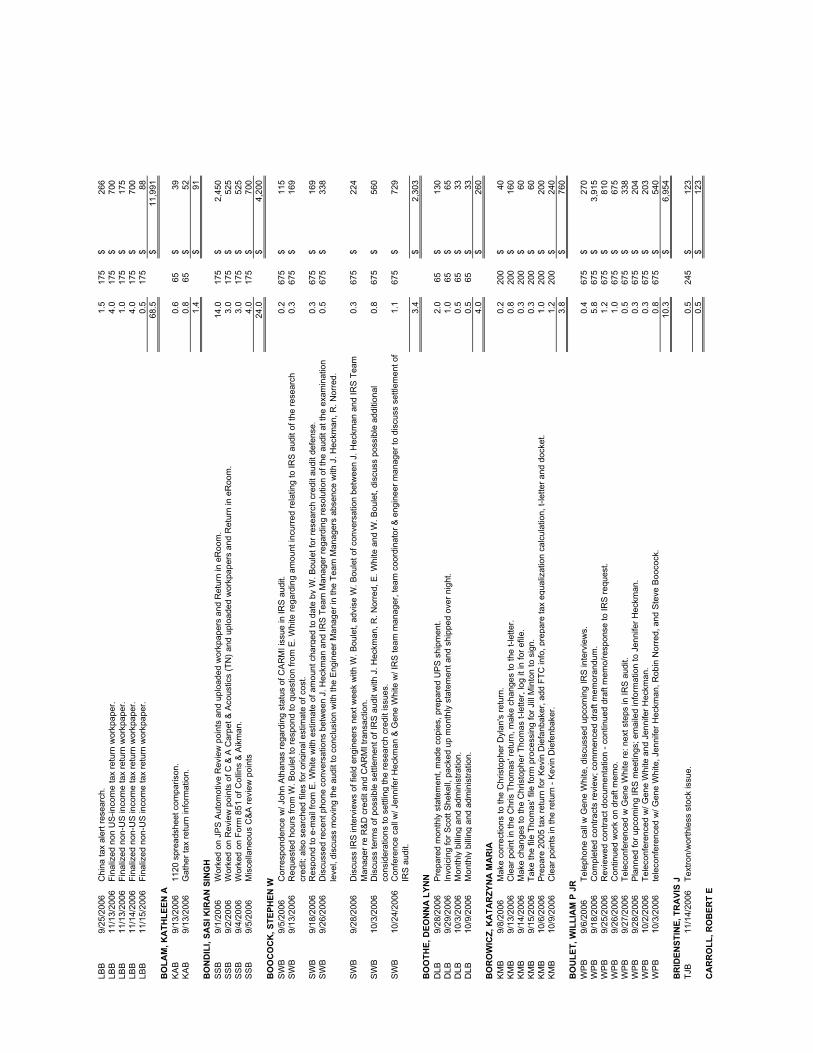

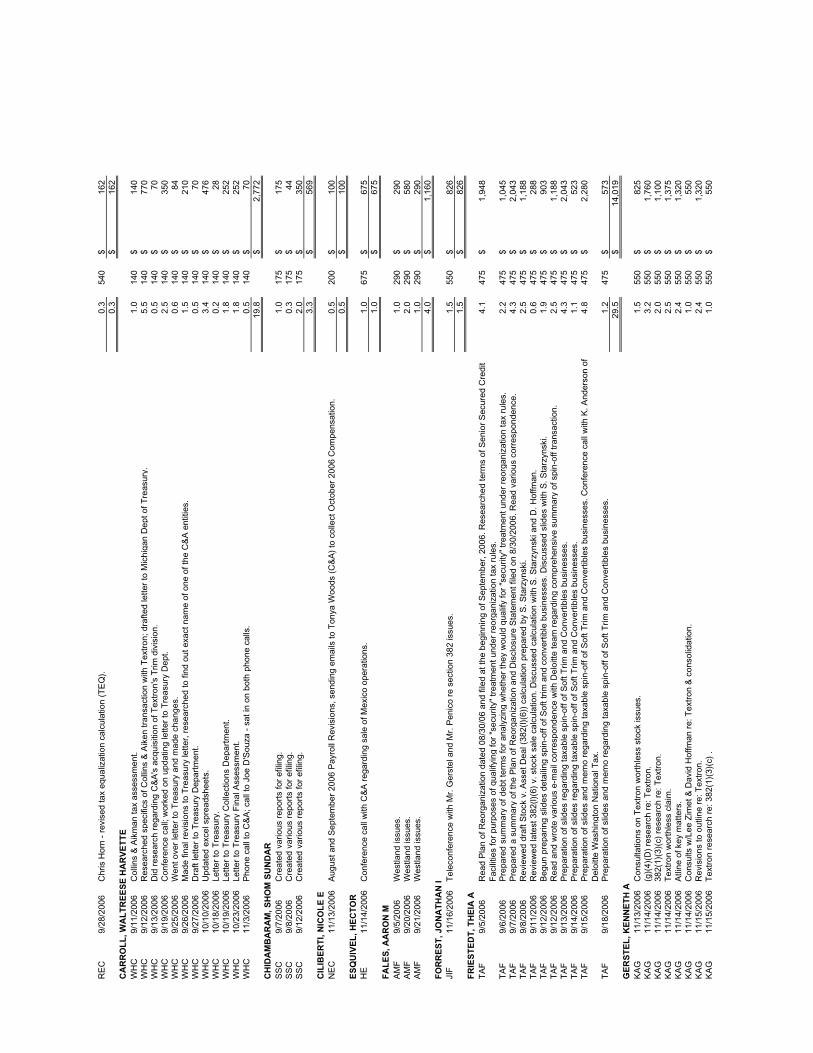

performed by Deloitte Tax during the Compensation Period. Exhibit C is an

itemized time record, in chronological order, of each specific service for which an

award of compensation is sought. This is in the form of a spreadsheet reflecting

detailed descriptions of services rendered and time thereby expended (in

increments on one-tenth of an hour) sorted by each professional providing the

services by day. Exhibit D contains the biographical statements of the

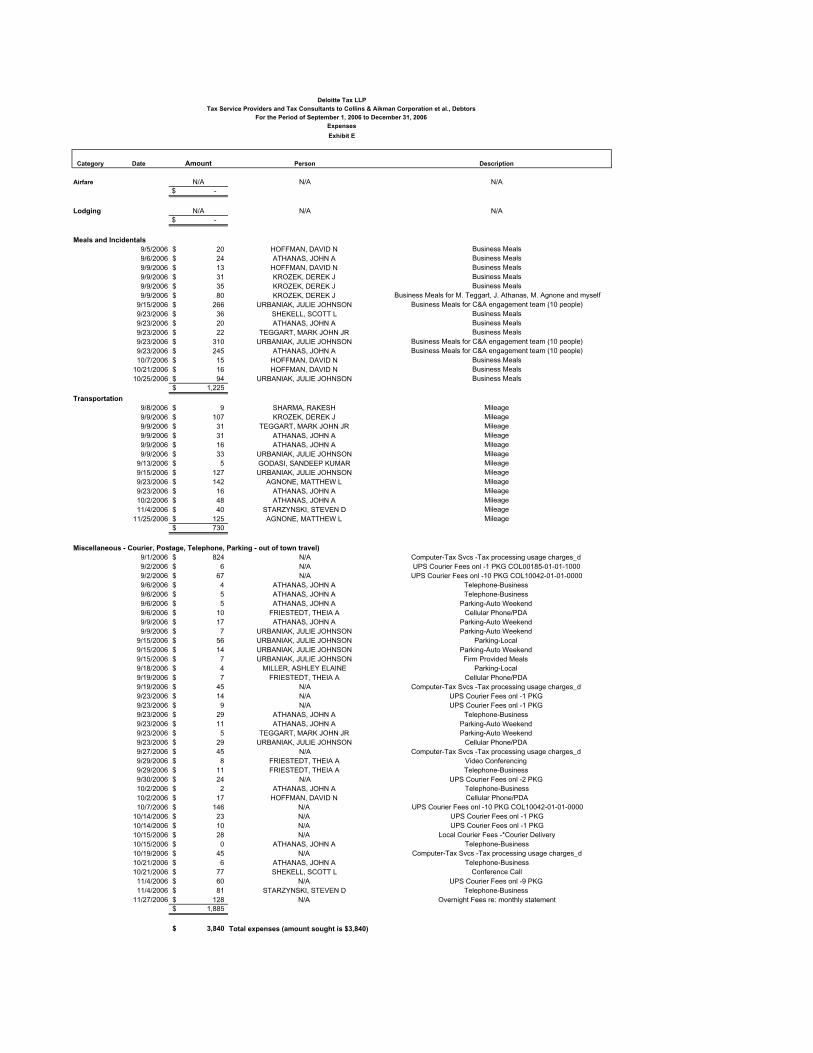

engagement partners for the Tax Services rendered. Exhibit E is an itemized

statement of expenses reflecting the actual and necessary expenses incurred by

Deloitte Tax in the provision of services to the Debtor for which expenses

reimbursement is sought.

11. As noted above, the daily contemporaneous activity descriptions of

each of the Deloitte Tax professionals and paraprofessionals providing services to

9

the Debtors for the Fourth Interim Fee Application pertaining to the

Compensation Period is reflected on Exhibit C hereto.

12. Deloitte Tax has attempted to include in this Fourth Interim Fee

Application all time relating to the Compensation Period. Delays in processing

such time and receiving invoices for certain expenses, however, do occur.

Accordingly, Deloitte Tax reserves the right to request compensation and

reimbursement for fees and trailing expenses, if any, incurred during the period

September 1, 2006 through and including December 31, 2006, but not reflected in

this Fourth Interim Fee Application, in future fee applications.

REASONABLE AND NECESSARY SERVICES RENDERED BY DELOITTE TAX (CATEGORIZED BY SUBJECT MATTER)

13. In addition to the detail supplied in Exhibit C, the description of

services of Exhibit B further summarizes the Tax Services rendered by Deloitte

Tax during the Compensation Period (including for Chapter 11 administration),

and highlights the benefits conferred upon the Debtors and their estates and

creditors as a result of Deloitte Tax’s services. The specific professional services

that Deloitte Tax rendered during the Compensation Period are listed at Exhibit B

which is a summary of the hours billed by subject matter during the

Compensation Period and include these categories: (1) general corporate history,

(2) Internal Revenue Code (“IRS”) Section 382 limitation analysis, (3)

international assignments services consulting, (4) loan staff arrangement state and

local tax consulting, (5) IRS audit support, (6) internal and external planning

meetings, (7) calculation of tax basis balance sheet, (8) assistance regarding state

of Michigan audit, (9) consultation regarding Section 9100 relief regarding IRS

audit, (10) Consolidated Return issues, (11) specialized tax issues, (12)

10

consultation regarding sale of European subsidiaries, (13) advice with respect to

the state tax aspects of the post-bankruptcy environment, focusing on

optimization of tax structure for state tax purposes, (14) consultation regarding

asset sale, (15) review of bankruptcy plan details, summary of tax relevant items

and potential tax consequences and assistance with determination of the state tax

consequences, (16) Value Added Tax (VAT) registration consultation, (17)

preparation of federal income tax return for Collins & Aikman Corporation and

subsidiaries, and (18) Chapter 11 administration[DK1], including, but not limited to,

billing and tracking time in anticipation of fee application preparation

computation of stock basis.

ALLOWANCE OF COMPENSATION

14. Section 331 of the Bankruptcy Code allows a bankruptcy court to

authorize interim compensation for “[a] trustee, an examiner, a debtor’s attorney,

or any professional person employed under section 327 or 1103 of this title … not

more than once every 120 days after an order for relief in a case under this title

[.]” Instruction for Section 331 disbursements is “provided under section 330 of

this title.”

15. Section 330 of the Bankruptcy Code authorizes the bankruptcy

court to award a trustee, an examiner or a professional employed pursuant to 11

U.S.C. § 327, reasonable compensation for its services and reimbursement of its

expenses. Specifically, Section 330 of the Bankruptcy Code provides as follows:

(a)(1) After notice to the parties in interest and to the United States Trustee and a

Hearing, and subject to sections 326, 328, and 329, the court may award to a trustee, an examiner, ombudsman, a professional person employed under section 327 or 1103 –

11

(A) reasonable compensation for actual, necessary services rendered bythe trustee, examiner, professional person, or attorney and by any paraprofessional person employed by such person; and

(B) reimbursement for actual, necessary expenses.

11 U.S.C. § 330(a)(1).

16. Section 330(a)(3) of the Bankruptcy Code provides that in

determining the amount of reasonable compensation to be awarded, the court

should consider the nature, extent and value of the services rendered to the estate,

taking into account all relevant factors, including:

(A) the time spent on such services;

(B) the rates charged for such services;

(C) whether the services were necessary to the administration of, or beneficial at the time, at which the service was rendered toward the completion of, a case under this title;

(D) whether the services were performed within a reasonable amount of time commensurate with the complexity, importance, and nature of the problem, issue, or task addressed; and . . .

(F) whether the compensation is reasonable, based on the customary compensation charged by comparably skilled practitioners in cases other than cases under this title.

11 U.S.C. § 330(a)(3)(A)-(E).

17. As analyzed below, Deloitte Tax respectfully submits that the

elements governing awards of compensation justify the allowance requested.

(1) THE TIME AND LABOR REQUIRED

18. During the Compensation Period, 1,633.0 recorded hours have

been expended by the relevant professionals or other personnel in providing the

hourly-rate Tax Services. Exhibit C hereto details the time and labor expended by

12

these professionals or other personnel on behalf of the Debtors and identifies the

hours that are being billed.

(2) THE RATES CHARGED FOR SUCH SERVICES

19. During the Compensation Period, Deloitte Tax’s applicable hourly

billing rates or those of Deloitte Tax personnel involved ranged from $175.00 to

$675.00 per hour for partners, principals and directors, $175.00 to $550.00 per

hour for senior managers, $175.00 to $475.00 per hour for managers, $175.00 to

$375.00 per hour for seniors, $175.00 to $240.00 per hour for staff, and $65.00 to

$175.00 per hour for administrative personnel. Based on the recorded billable

hours expended by Deloitte Tax’s professionals, the average hourly billing rate

for such professional services was approximately $239.85 including

paraprofessionals.

20. The applicable amounts charged to the Debtors for the particular

services rendered are consistent with the approximate rates charged other clients

of Deloitte Tax for comparable services in similar situations.

(3) THE NECESSITY OF THE SERVICES AND BENEFIT TO THE ESTATE

26. As detailed above, services provided to the Debtors were necessary

for the Debtors’ business operations and conferred substantial benefit on the

Debtors’ estates. Chapter 11 administration services were a prerequisite to

continuing to provide post-petition services to the Debtors.

(4) CUSTOMARY COMPENSATION

27. Deloitte Tax relies on the Court’s experience and knowledge with

respect to the compensation awards in similar cases. Given that frame of

13

reference, Deloitte Tax submits that, in light of the circumstances of the case and

the substantial benefits derived from Deloitte Tax’s assistance, compensation in

the amount requested is fair and reasonable.

(5) WHETHER SERVICES WERE PERFORMED IN A REASONABLE AMOUNT OF TIME

28. Deloitte Tax believes that Tax Services were performed in a

reasonable amount of time, given the complexity of the issues and the scope of

services involved and that the time expended on various tasks was necessary and

appropriate.

(6) WHETHER COMPENSATION IS REASONABLE

29. The Tax Services that have been rendered in an efficient manner

by professionals with extensive experience in providing services within the scope

of the Retention Order.

30. Deloitte Tax further believes that the compensation sought for the

Tax Services rendered in connection with these Chapter 11 cases is reasonable

and commensurate with those rates charged by comparable professional services

firms.

31. As set forth in more detail above, Deloitte Tax’s time has been

appropriately spent in this case. Based upon Deloitte Tax’s blended hourly rate of

$239.85 for professionals (including paraprofessionals), Deloitte Tax submits that

its applicable rates are indeed comparable to those prevailing in the relevant

professional services market. Therefore, taking into consideration the time and

labor spent, the nature and extent of the professional services rendered and the

nature of these proceedings, Deloitte Tax believes the allowance asked for is

reasonable.

14

32. In sum, based on the factors to be considered under sections 330

and 331 of the Bankruptcy Code, the allowance in full of Deloitte Tax’s

compensation herein is justified.

DISBURSEMENTS

33. For this Compensation Period, in connection with its provision of

the Tax Services, Deloitte Tax is seeking in this Fourth Interim Fee Application

reimbursement for its reasonable and necessary expenses incurred on behalf of the

Debtors during September 1 through December 31, 2006 in the aggregate amount

of $3,840.

34. In summary, by this Fourth Interim Fee Application, Deloitte Tax

requests allowance and payment of any outstanding amounts of fees and expenses

in the total amount of $395,521, consisting of $391,681 for the actual, reasonable,

and necessary professional services rendered by Deloitte Tax on behalf of the

Debtors (representing 100% of fees for services rendered) and $3,840 for actual

and necessary expenses (representing 100% of the expenses incurred by Deloitte

Tax). Application of a 20% holdback to the actual amount to be paid by the

Debtors at this time upon the Court’s approval of this Fourth Interim Fee

Application would result in a payment of $317,186 for the tax services at this

time.

WHEREFORE, Deloitte Tax respectfully requests entry of an order,

substantially in the form attached hereto as Exhibit F (a) allowing an

administrative expense claim for Deloitte Tax for compensation and

reimbursement for its fees and expenses incurred during the Compensation

15

Period, (b) authorizing and directing payment of such amounts, and (c) granting

such other and further relief as is just and proper.

Dated: February 11, 2007 Detroit, Michigan

Respectfully submitted, DELOITTE TAX LLP

/s/ Scott Shekell Scott Shekell, Partner

600 Renaissance Center, Suite 900 Detroit, MI 48243-1595 Telephone: 313-396-3297 Facsimile: 313-392-7794

Tax Service Providers for the Debtors

K&E 11632799.2

IN THE UNITED STATES BANKRUPTCY COURT EASTERN DISTRICT OF MICHIGAN

SOUTHERN DIVISION

In re: ) Chapter 11 ) COLLINS & AIKMAN CORPORATION, et al.1 ) Case No. 05-55927 (SWR) ) (Jointly Administered) Debtors. ) ) (Tax Identification #13-3489233) ) ) Honorable Steven W. Rhodes

NOTICE AND OPPORTUNITY TO RESPOND TO THE FOURTH INTERIM FEE APPLICATION OF DELOITTE TAX LLP AS TAX SERVICE PROVIDERS FOR

THE DEBTORS FOR ALLOWANCE OF INTERIM COMPENSATION FORSERVICES RENDERED AND EXPENSES INCURRED FROM

SEPTEMBER 1, 2006 THROUGH DECEMBER 31, 2006

PLEASE TAKE NOTICE THAT Deloitte Tax LLP have filed their Fourth Interim Fee

Application of Deloitte Tax LLP as Tax Service Providers for the Debtors for Allowance of Interim

Compensation for Services Rendered and Expenses Incurred from September 31, 2006 through

December 31, 2006 (the “Application”) pursuant to the Administrative Order Establishing

Procedures for Monthly Compensation and Reimbursement of Expenses for Professionals and

1 The Debtors in the jointly administered cases include: Collins & Aikman Corporation; Amco Convertible Fabrics, Inc., Case No. 05-55949; Becker Group, LLC (d/b/a/ Collins & Aikman Premier Mold), Case No. 05-55977; Brut Plastics, Inc., Case No. 05-55957; Collins & Aikman (Gibraltar) Limited, Case No. 05-55989; Collins & Aikman Accessory Mats, Inc. (f/k/a the Akro Corporation), Case No. 05-55952; Collins & Aikman Asset Services, Inc., Case No. 05-55959; Collins & Aikman Automotive (Argentina), Inc. (f/k/a Textron Automotive (Argentina), Inc.), Case No. 05-55965; Collins & Aikman Automotive (Asia), Inc. (f/k/a Textron Automotive (Asia), Inc.), Case No. 05-55991; Collins & Aikman Automotive Exteriors, Inc. (f/k/a Textron Automotive Exteriors, Inc.), Case No. 05-55958; Collins & Aikman Automotive Interiors, Inc. (f/k/a Textron Automotive Interiors, Inc.), Case No. 05-55956; Collins & Aikman Automotive International, Inc., Case No. 05-55980; Collins & Aikman Automotive International Services, Inc. (f/k/a Textron Automotive International Services, Inc.), Case No. 05-55985; Collins & Aikman Automotive Mats, LLC, Case No. 05-55969; Collins & Aikman Automotive Overseas Investment, Inc. (f/k/a Textron Automotive Overseas Investment, Inc.), Case No. 05-55978; Collins & Aikman Automotive Services, LLC, Case No. 05-55981; Collins & Aikman Canada Domestic Holding Company, Case No. 05-55930; Collins & Aikman Carpet & Acoustics (MI), Inc., Case No. 05-55982; Collins & Aikman Carpet & Acoustics (TN), Inc., Case No. 05-55984; Collins & Aikman Development Company, Case No. 05-55943; Collins & Aikman Europe, Inc., Case No. 05-55971; Collins & Aikman Fabrics, Inc. (d/b/a Joan Automotive Industries, Inc.), Case No. 05-55963; Collins & Aikman Intellimold, Inc. (d/b/a M&C Advanced Processes, Inc.), Case No. 05-55976; Collins & Aikman Interiors, Inc., Case No. 05-55970; Collins & Aikman International Corporation, Case No. 05-55951; Collins & Aikman Plastics, Inc., Case No. 05-55960; Collins & Aikman Products Co., Case No. 05-55932; Collins & Aikman Properties, Inc., Case No. 05-55964; Comet Acoustics, Inc., Case No. 05-55972; CW Management Corporation, Case No. 05-55979; Dura Convertible Systems, Inc., Case No. 05-55942; Gamble Development Company, Case No. 05-55974; JPS Automotive, Inc. (d/b/a PACJ, Inc.), Case No. 05-55935; New Baltimore Holdings, LLC, Case No. 05-55992; Owosso Thermal Forming, LLC, Case No. 05-55946; Southwest Laminates, Inc. (d/b/a Southwest Fabric Laminators Inc.), Case No. 05-55948; Wickes Asset Management, Inc., Case No. 05-55962; and Wickes Manufacturing Company, Case No. 05-55968.

2 K&E 11632799.2

Official Committee Members dated June 9, 2005 [Docket No. 290] (the “Compensation Procedures

Order”).

PLEASE TAKE FURTHER NOTICE THAT your rights may be affected. You may wish

to review the Application and discuss it with your attorney, if you have one in these cases. (If

you do not have an attorney, you may wish to consult one.)

PLEASE TAKE FURTHER NOTICE THAT in accordance with the Compensation

Procedures Order, if you wish to object to the Court granting the relief sought in the Application, or

if you want the Court to otherwise consider your views on the Application, no later than

March 12, 2007 at 4:00 p.m. prevailing Eastern Time, or such shorter time as the Court may

hereafter order and of which you may receive subsequent notice (the “Objection Deadline”),

you or your attorney must file with the Court a written response, explaining your position at:2

United States Bankruptcy Court 211 West Fort Street, Suite 2100

Detroit, Michigan 48226

PLEASE TAKE FURTHER NOTICE THAT if you mail your response to the Court for

filing, you must mail it early enough so the Court will receive it on or before the

Objection Deadline.

PLEASE TAKE FURTHER NOTICE THAT you must also serve the documents so that they

are received on or before the Objection Deadline, in accordance with the Compensation Procedures

Order, including to:

2 Response or answer must comply with Rule 8(b), (c) and (e) of the Federal Rules of Civil Procedure.

3 K&E 11632799.2

Scott Shekell Deloitte Tax LLP

600 Renaissance Center, Suite 900 Detroit, Michigan 48243-1595

PLEASE TAKE FURTHER NOTICE THAT if no responses to the Application are timely

filed and served, the Court may grant the Application and enter the order without a hearing as set

forth in Rule 2016-3 of the Local Rules for the United States Bankruptcy Court for the

Eastern District of Michigan.

K&E 11632799.2

Dated: February 15, 2007 KIRKLAND & ELLIS LLP

/s/ Marc J. Carmel Richard M. Cieri (NY RC 6062)

Citigroup Center 153 East 53rd Street New York, New York 10022 Telephone: (212) 446-4800 Facsimile: (212) 446-4900

-and-

David L. Eaton (IL 3122303) Ray C. Schrock (IL 6257005) Marc J. Carmel (IL 6272032) 200 East Randolph Drive Chicago, Illinois 60601 Telephone: (312) 861-2000 Facsimile: (312) 861-2200

-and-

CARSON FISCHER, P.L.C.

Joseph M. Fischer (P13452) 4111 West Andover Road West - Second Floor Bloomfield Hills, Michigan 48302 Telephone: (248) 644-4840 Facsimile: (248) 644-1832

Co-Counsel for the Debtors

K&E 11632799.2

CERTIFICATE OF SERVICE

I, Marc Carmel, an attorney, certify that no later than the 16th day of February, 2007, I caused to be served, by e-mail and by first class mail, in the manner and to the parties set forth on the attached service lists, a true and correct copy of the foregoing Fourth Interim Fee Application of Deloitte Tax LLP as Tax Service Providers for the Debtors for Allowance of Interim Compensation for Services Rendered and Expenses Incurred from September 1, 2006 through December 31, 2006.

Dated: February 15, 2007 /s/ Marc J. Carmel Marc J. Carmel

Served via Electronic Mail

CREDITOR NAME CREDITOR NOTICE NAME EMAIL

A Freeman [email protected]

Acord Inc John Livingston [email protected]

Adrian City Hall John Fabor [email protected]

Alice B Eaton [email protected]

Athens City Tax Collector Mike Keith [email protected]

Basell USA Inc Scott Salerni [email protected]

Brendan G Best [email protected]

Bryan Clay [email protected]

Champaign County Collector Barb Neal [email protected]

Chris Kocinski [email protected]

City Of Eunice The Mayor at City Hall [email protected]

City Of Evart Roger Elkins City Manager [email protected]

City Of Kitchener Finance Dept Pauline Houston [email protected]

City Of Lowell Lowell Regional Wastewater [email protected]

City Of Marshall Maurice S Evans City Manager [email protected]

City Of Muskegon Derrick Smith [email protected]

City Of Port Huron Treasurer's Office [email protected]

City Of Rialto City Treasurer [email protected]

City Of Rochester Hills Kurt A Dawson City Assesor Treasurer [email protected]

City Of Salisbury Business License Div [email protected]

City Of Westland [email protected]

City Of Woonsocket Ri Pretreatment Division [email protected]

City Treasurer Tracy Horvarter [email protected]

City Treasurer [email protected]

DaimlerChrysler [email protected]

DaimlerChrysler [email protected]

Daniella Saltz [email protected]

Danielle Kemp [email protected]

David H Freedman [email protected]

David Heller [email protected]

David Youngman [email protected]

Dow Chemical Company Kathleen Maxwell [email protected]

DuPont Bruce Tobiansky [email protected]

Earle I Erman [email protected]

Erin M Casey [email protected]

Frank Gorman [email protected]

Gail Perry [email protected]

Ge Capital [email protected]

GE Polymerland Val Venable [email protected]

George E Schulman [email protected]

Gold Lange & Majoros PC Stuart A Gold & Donna J Lehl

Hal Novikoff [email protected]

Heather Sullivan [email protected]

James A Plemmons [email protected]

Jim Clough [email protected]

Joe LaFleur [email protected]

Joe Saad [email protected]

John A Harris [email protected]

John Green [email protected]

John J Dawson [email protected]

John S Sawyer [email protected]

Josef Athanas [email protected]

Joseph Delehant Esq [email protected]

Joseph M Fischer Esq [email protected]

K Crumbo [email protected]

K Schultz [email protected]

Kim Stagg [email protected]

Kimberly Davis Rodriguez [email protected]

Leigh Walzer [email protected]

Levine Fricke Inc [email protected]

M Crosby [email protected]

Macomb Intermediate School [email protected]

Marc J Carmel [email protected]

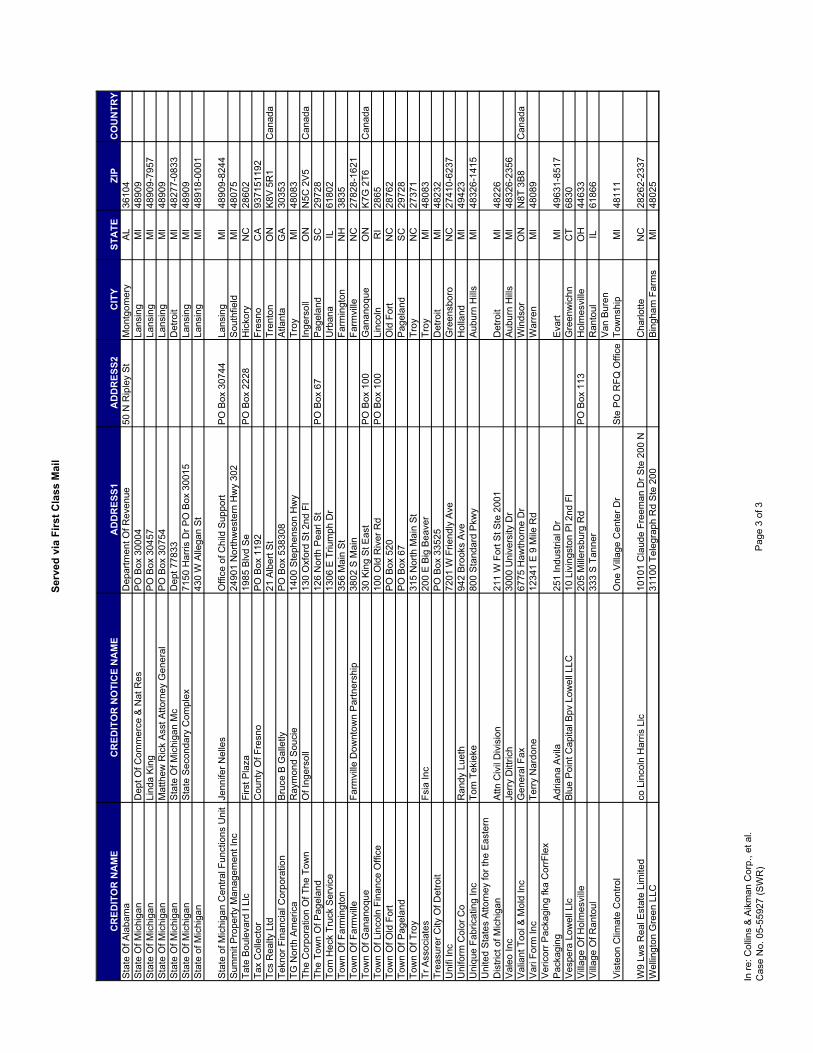

In re: Collins & Aikman Corp., et al.

Case No. 05-55927 (SWR) Page 1 of 2

Served via Electronic Mail

CREDITOR NAME CREDITOR NOTICE NAME EMAIL

Mark Fischer [email protected]

Michael R Paslay [email protected]

Michael Stamer [email protected]

Michigan Department Of Treasury [email protected]

Mike O'Rourke [email protected]

Mike Paslay [email protected]

Ministry Of Finance Corp Tax Branch [email protected]

Missouri Dept Of Revenue 15663507 [email protected]

Municipalite Du Village De Lacolle [email protected]

Nick Shah [email protected]

Nina Rosete [email protected]

Paul Hoffman [email protected]

Pension Benefit Guaranty Corporation Sara Eagle & Gail Perry [email protected]

Pension Benefit Guaranty Corporation Sara Eagle & Gail Perry [email protected]

Peter Schmidt [email protected]

Peter V Pantaleo [email protected]

Phh Canada Inc [email protected]

Philip Dublin [email protected]

Phoenix Contracting Company Tricia Sommers [email protected]

R Aurand [email protected]

R J Sidman [email protected]

Ralph E McDowell [email protected]

Ray C Schrock [email protected]

Rick Feinstein [email protected]

Ricoh Canada Inc [email protected]

Robert J Diehl Jr [email protected]

Robert Weiss [email protected]

Ronald A Leggett Collector Of Revenue [email protected]

Ronald R Rose [email protected]

Sarah Eagle [email protected]

Sean P Corcoran [email protected]

Sheryl Toby [email protected]

Stark County Treasurer PA Powers [email protected]

State Of Michigan

Michigan Dept Of Environmental Quality

Environmental Assistance Div [email protected]

State Of Michigan

Michigan Dept Of Treasury Collection Div

Office of Financial Mgmt

Cashiers Office [email protected]

State Of Michigan Michigan Unemployment Insurance Agency [email protected]

Stephen E Spence US Trustee [email protected]

Stephen S LaPlante [email protected]

T Pryce [email protected]

Tax Administrator Jim Cambio [email protected]

Thomas Radom [email protected]

Treasurer Of State Joseph T. Deters [email protected]

Tricia Sherick [email protected]

Tyco Capital Inc [email protected]

United Rentals Of Canada Inc [email protected]

Ville De Farnham Service de la Tresorerie [email protected]

Voridian Canada Company [email protected]

William C Andrews [email protected]

William G Diehl [email protected]

William J Byrne [email protected]

In re: Collins & Aikman Corp., et al.

Case No. 05-55927 (SWR) Page 2 of 2

Serv

ed

via

Fir

st

Cla

ss M

ail

CR

ED

ITO

R N

AM

EC

RE

DIT

OR

NO

TIC

E N

AM

EA

DD

RE

SS

1A

DD

RE

SS

2C

ITY

ST

AT

EZ

IPC

OU

NT

RY

Ad

va

nce

d C

om

po

site

s I

nc

Ro

b M

org

an

10

62

S 4

th A

ve

Sid

ne

yO

H4

53

65

-89

77

Am

erica

n G

en

era

l F

ina

nce

50

5 S

Ne

il S

tC

ha

mp

aig

nIL

61

82

0-2

50

0

Asso

c R

ece

iva

ble

s F

un

din

g I

nc

PO

Bo

x 1

62

53

Gre

en

vill

eS

C2

96

06

Ath

en

s C

ity T

ax C

olle

cto

rM

ike

Ke

ith

PO

Bo

x 8

49

Ath

en

sT

N3

73

71

-08

49

Ba

sf

Co

rpo

ratio

nC

ha

rlie

Bu

rrill

16

09

Bid

dle

Ave

Wya

nd

ott

eM

I4

81

92

Ba

ye

r M

ate

ria

l S

cie

nce

sL

ind

a V

esci

10

0 B

aye

r R

d B

ldg

16

Pitts

bu

rgh

PA

15

20

5-9

70

7

BN

Y M

idw

est

Tru

st

Co

mp

an

yM

ary

Ca

llah

an

2 N

ort

h L

aS

alle

St

Ste

10

20

Ch

ica

go

IL6

06

02

BN

Y M

idw

est

Tru

st

Co

mp

an

yR

oxa

ne

Ellw

alle

ge

r2

No

rth

La

Sa

lle S

t S

te 1

02

0C

hic

ag

oIL

60

60

2

Bro

wn

Co

rpo

ratio

nM

ark

Fe

rde

rbe

r4

01

S S

tee

le S

teIo

nia

MI

48

84

6

Ca

na

da

Cu

sto

ms &

Re

v A

ge

ncy

Att

n R

ece

ive

r G

en

era

l1

5 N

otr

e A

ve

Su

db

ury

ON

P3

A 5

C2

Ca

na

da

Ca

na

da

Cu

sto

ms &

Re

v A

ge

ncy

Inte

rna

tio

na

l T

ax S

erv

ice

22

04

Wa

lkle

y R

dO

tta

wa

ON

K1

A 1

B1

Ca

na

da

Ch

art

er

To

wn

sh

ip O

f P

lym

ou

thP

O B

ox 8

04

0P

lym

ou

thM

I4

81

70

-43

94

City O

f A

lbe

ma

rle

Utilit

ies D

ep

art

me

nt

14

4 N

Se

co

nd

St

PO

Bo

x 1

90

Alb

em

arle

NC

28

00

2-0

19

0

City O

f B

arb

ert

on

Inco

me

Ta

x D

ivis

ion

10

4 3

rd S

t N

WB

arb

ert

on

OH

44

20

3

City O

f B

att

le C

ree

kIn

co

me

Ta

x D

ivis

ion

10

N D

ivis

ion

St

Su

ite

11

4 4

90

14

PO

Bo

x 1

71

7B

att

le C

ree

kM

I4

90

14

City O

f C

an

ton

Ca

nto

n I

nco

me

Ta

x D

ep

tP

O B

ox 9

95

1C

an

ton

OH

44

71

1-9

95

1

City O

f D

ove

rW

aste

wa

ter

La

bro

rato

ry4

84

Mid

dle

Rd

Do

ve

rN

H3

82

0

City O

f D

ove

rP

O B

ox 8

18

Do

ve

rN

H0

38

20

-08

18

City O

f E

va

rt R

ecre

atio

n D

ep

t2

00

So

uth

Ma

in S

tE

va

rtM

I4

96

31

City O

f F

ulle

rto

n3

03

W C

om

mo

nw

ea

lth

Ave

Fu

llert

on

CA

92

63

2

City O

f H

avre

De

Gra

ce

Ma

ry E

llen

Hin

ckle

71

1 P

en

nin

gto

n A

ve

Ha

vre

De

Gra

ce

MD

21

07

8

City O

f L

on

gvie

wW

ate

r U

tilit

ies

PO

Bo

x 1

95

2L

on

gvie

wT

X7

56

06

City O

f L

os A

ng

ele

sD

ep

t O

f B

uild

ing

An

d S

afe

ty2

01

N F

igu

ero

a S

t N

o 7

86

File

54

56

3L

os A

ng

ele

sC

A9

00

12

City O

f P

ho

en

ixC

ity A

tto

rne

ys O

ffic

e2

00

W W

ash

ing

ton

St

13

th F

lP

ho

en

ixA

Z8

50

03

City O

f R

oxb

oro

Ta

x D

ep

art

me

nt

PO

Bo

x 1

28

Ro

xb

oro

NC

27

57

3

City O

f S

t Jo

se

ph

Wa

ter

De

pa

rtm

en

t7

00

BR

d S

tS

t Jo

se

ph

MI

49

08

5-1

35

5

City O

f S

terlin

g H

eig

hts

Ja

me

s P

Bu

lhin

ge

r C

ity T

rea

su

rer

40

55

5 U

tica

Rd

PO

Bo

x 8

09

9S

terlin

g H

eig

hts

MI

48

31

1-8

00

9

City O

f W

illia

msto

n1

61

E G

ran

d R

ive

rW

illia

msto

nM

I4

88

95

City T

rea

su

rer

Po

rt H

uro

n P

olic

e D

ep

art

me

nt

10

0 M

cm

orr

an

Po

rt H

uro

nM

I4

80

60

Co

lbo

nd

In

cD

on

Bro

wn

Sa

nd

Hill

Rd

PO

Bo

x 1

05

7E

nka

NC

28

78

2

Co

llecto

r O

f R

eve

nu

eB

arb

ara

J W

alk

er

20

1 N

Se

co

nd

St

St

Ch

arle

sM

O6

33

01

Co

llin

s &

Aik

ma

n C

orp

Sta

cy F

ox

25

0 S

tep

he

nso

n H

wy

Tro

yM

I4

80

83

Da

yto

n B

ag

& B

urla

p C

oJe

ff R

utt

er

32

2 D

avis

Ave

Da

yto

nO

H4

54

03

-29

10

Du

Po

nt

Su

sa

n F

He

rrD

uP

on

t L

eg

al D

71

56

10

07

N M

ark

et

St

Wilm

ing

ton

DE

19

89

8

En

erf

lex S

olu

tio

ns L

LC

To

dd

McC

allu

m1

51

5 E

qu

ity D

r 2

00

Tro

yM

I4

80

84

-80

84

ER

Wa

gn

er

Ma

nu

factu

rin

gG

ary

To

rke

46

11

No

rth

32

nd

St

Milw

au

ke

eW

I5

32

09

-60

23

Exxo

n C

he

mic

als

La

w D

ep

t1

35

01

Ka

ty F

wy

Ho

usto

nT

X7

70

79

-13

05

Fis

he

r A

uto

mo

tive

Syste

ms F

ish

er

Am

erica

In

cW

illia

m S

tie

fel

10

84

Do

ris R

dA

ub

urn

Hill

sM

I4

83

26

-26

13

Fre

ud

en

be

rg N

ok I

nc

47

69

0 E

An

ch

or

Ct

Ply

mo

uth

MI

48

17

0

Ga

De

pt

Of

Re

ve

nu

eD

ire

cto

r's O

ffic

e f

or

Ta

xp

aye

r S

erv

ice

s D

ivis

ion

PO

Bo

x 1

05

49

9A

tla

nta

GA

30

34

8-5

49

9

Ga

sto

n C

ou

nty

PO

Bo

x 8

90

69

1C

ha

rlo

tte

NC

28

28

9-0

69

1

Ge

Ca

pita

lP

O B

ox 7

40

43

4A

tla

nta

GA

30

37

4

Ge

Ca

pita

lP

O B

ox 6

40

38

7P

itts

bu

rgh

PA

15

26

4-0

38

7

Ge

Ca

pita

lP

O B

ox 6

42

44

4P

itts

bu

rgh

PA

15

26

4

Ge

Ca

pita

l C

om

m S

erv

Astr

o D

ye

PO

Bo

x 6

05

00

Ch

arlo

tte

NC

28

26

0

Ha

rfo

rd C

ou

nty

Re

ve

nu

e2

20

So

uth

Ma

in S

tB

el A

irM

D2

10

14

In r

e:

Co

llin

s &

Aik

ma

n C

orp

., e

t a

l.

Ca

se

No

. 0

5-5

59

27

(S

WR

)P

ag

e 1

of

3

Serv

ed

via

Fir

st

Cla

ss M

ail

CR

ED

ITO

R N

AM

EC

RE

DIT

OR

NO

TIC

E N

AM

EA

DD

RE

SS

1A

DD

RE

SS

2C

ITY

ST

AT

EZ

IPC

OU

NT

RY

Hig

hw

oo

ds F

ors

yth

Lp

co

Hig

hw

oo

ds P

rop

ert

ies L

lcA

ttn

Le

ase

Ad

min

istr

atio

n

33

22

We

st

En

d

Ave

Ste

60

0N

ash

vill

eT

N3

72

03

Hig

hw

oo

ds F

ors

yth

Lp

co

Hig

hw

oo

ds P

rop

ert

ies L

lcA

ttn

Le

ase

Ad

min

istr

atio

n

31

00

Sm

oke

tre

e C

t

Ste

60

0R

ale

igh

NC

27

60

4

Hn

k M

ich

iga

n P

rop

ert

ies

co

Ru

do

lph

lib

be

Pro

pe

rtie

s7

25

5 C

rossle

igh

Co

urt

Ste

10

8T

ole

do

OH

43

61

7

Ind

ian

a D

ep

art

me

nt

Of

Re

ve

nu

e1

00

N S

en

ate

Ave

Ind

ian

ap

olis

IN4

62

04

-22

53

Ind

ian

a D

ep

t O

f R

eve

nu

eP

O B

ox 7

21

8In

dia

na

po

lisIN

46

20

7-7

21

8

Ind

ustr

ial D

eve

lop

me

nt

Bo

ard

of

the

City o

f M

on

tgo

me

ryP

O B

ox 4

66

0M

on

tgo

me

ryA

L3

61

03

-46

60

Ind

ustr

ial L

ea

sin

g C

om

pa

ny

PO

Bo

x 1

80

3G

ran

d R

ap

ids

MI

49

50

1

Ind

ustr

ial T

ruck S

ale

s &

Svc

PO

Bo

x 1

80

7D

urh

am

NC

27

70

2-1

80

7

Inm

et

Div

isio

n o

f M

ultim

atic

35

We

st

Milm

ot

St

Ric

hm

on

d H

illO

NL

4B

1L

7C

an

ad

a

Inte

rna

l R

eve

nu

e S

erv

ice

SB

SE

In

so

lve

ncy U

nit

Bo

x 3

30

50

0 S

top

15

De

tro

itM

I4

82

32

Inte

rte

x W

orld

Re

so

urc

es T

rin

tex C

orp

Bill

We

eks

50

0 W

ed

ow

ee

St

Bo

wd

on

G

A3

01

08

-15

41

Invis

ta6

01

S L

A S

alle

St

Ste

31

0C

hic

ag

oIL

60

60

5-1

72

5

ISP

Ela

sto

me

rT

im G

orm

an

PO

Bo

x 4

34

6H

ou

sto

nT

X7

72

10

Ja

ne

svill

e P

rod

ucts

La

ura

Ke

lly2

70

0 P

att

ers

on

Ave

Gra

nd

Ra

pid

sM

I4

95

46

Ke

ith

Mill

iga

n3

74

5 C

Us H

wy 8

0 W

Ph

en

ixA

L3

68

70

La

ke

Erie

Pro

du

cts

Lili

a R

om

an

32

1 F

oste

r A

ve

Wo

od

Da

leIL

60

19

1

Le

ar

Co

rp2

15

57

Te

leg

rap

h R

dS

ou

thfie

ldM

I4

80

34

Ma

np

ow

er

C G

arla

nd

Wa

ller

30

80

0 N

ort

hw

este

rn H

wy

Fa

rmin

gto

n H

ills

MI

48

33

4

Me

rid

ian

Ma

gn

esiu

m2

00

1 I

nd

ustr

ial D

rE

ato

n R

ap

ids

MI

48

82

7

Me

rid

ian

Pa

rk2

70

7 M

erid

ian

Dr

Gre

en

vill

eN

C2

78

34

Min

istr

e D

u R

eve

nu

Du

Qu

eb

ec

38

00

Ma

rly

Ste

Fo

yQ

CG

1X

4A

5C

an

ad

a

Mu

nic

ipa

lity O

f P

ort

Ho

pe

PO

Bo

x 1

17

Po

rt H

op

eO

NL

1A

3V

9C

an

ad

a

No

rth

Lo

op

Pa

rtn

ers

Ltd

co

Be

er

We

lls R

ea

l E

sta

teP

O B

ox 3

44

9L

on

gvie

wT

X7

56

06

Off

ice

of

Fin

an

ce

of

Lo

s A

ng

ele

sB

an

kru

ptc

y A

ud

ito

r3

70

0 W

ilsh

ire

Ste

31

0L

os A

ng

ele

sC

A9

00

10

Pe

nsio

n B

en

efit

Gu

ara

nty

Co

rpo

ratio

nS

ara

Ea

gle

& G

ail

Pe

rry

12

00

K S

t N

W

Off

ice

of

the

Ch

ief

Co

un

se

lW

ash

ing

ton

DC

20

00

5-4

02

6

Pin

e R

ive

r P

lastics I

nc

Ba

rb K

rzyw

iecki

11

11

Fre

d W

Mo

ore

Hw

yS

t C

lair

MI

48

07

9-4

96

7

Po

lyO

ne

Co

rpW

oo

dy B

an

33

58

7 W

alk

er

Rd

Avo

n L

ake

OH

44

01

2

Pre

stig

e P

rop

ert

y T

ax S

pe

cia

l1

02

5 K

ing

St

Ea

st

Ca

mb

rid

ge

ON

N3

H 3

P5

Ca

na

da

Prin

ce

ton

Pro

pe

rtie

s6

78

Prin

ce

ton

Blv

dL

ow

ell

MA

18

51

Pro

gre

ssiv

e M

ou

lde

d P

rod

ucts

Da

n T

hiffa

ult

90

24

Ke

ele

St

Co

nco

rd

ON

L4

K 2

N2

Ca

na

da

Qrs

14

Pa

yin

g A

ge

nt

Ch

urc

h S

t S

tatio

nP

O B

ox 6

52

9N

ew

Yo

rkN

Y1

02

49

Qrs

14

Pa

yin

g A

ge

nt

Inc

50

Ro

cke

felle

r L

ob

by 2

Ne

w Y

ork

NY

10

02

0-1

60

5

Ra

ilro

ad

Drive

Lp

10

0 V

esp

er

Exe

cu

tive

Pk

Tyn

gsb

oro

MA

01

87

9-2

71

0

Re

ce

ive

r G

en

era

l F

or

Ca

na

da

Ca

na

da

Cu

sto

ms &

Re

v A

ge

ncy T

ech

no

log

y C

tr8

75

He

ron

Rd

Ott

aw

aO

NK

1A

1B

1C

an

ad

a

Re

ce

ive

r G

en

era

l F

or

Ca

na

da

Ind

ustr

y C

an

ad

a A

ls F

ina

ncia

lP

osta

l S

tatio

n D

Bo

x 2

33

0O

tta

wa

ON

K1

P 6

K1

Ca

na

da

Re

ce

ive

r G

en

era

l fo

r C

an

ad

a7

00

Le

igh

Ca

pre

ol

Do

rva

lQ

CH

4Y

1G

7C

an

ad

a

Re

ce

ive

r G

en

era

l F

or

Ca

na

da

11

Sta

tio

n S

tB

elle

vill

eO

NK

8N

2S

3C

an

ad

a

Re

ve

nu

e C

an

ad

a2

75

Po

pe

Rd

Ste

10

2S

um

me

rsid

eP

EC

1N

5Z

7C

an

ad

a

Re

ve

nu

e C

an

ad

aO

tta

wa

Te

ch

no

log

y C

en

tre

8

75

He

ron

Rd

Ott

aw

aO

NK

1A

9Z

9C

an

ad

a

Riv

erf

ron

t P

lastic P

rod

ucts

In

cG

eo

rge

Ta

bry

78

0 H

illsd

ale

St

Wya

nd

ott

eM

I4

81

92

-71

20

Se

cu

ritie

s a

nd

Exch

an

ge

Co

mm

issio

nM

idw

est

Re

gio

na

l O

ffic

e1

75

W J

ackso

n B

lvd

Ste

90

0C

hic

ag

oIL

60

60

4

Se

lect

Ind

ustr

ies C

orp

Ch

ristin

e B

row

n2

40

De

tric

k S

tD

ayto

nO

H4

54

04

-16

99

So

uth

Ca

rolin

a D

ep

t O

f R

eve

nu

eS

ale

s &

Use

Ta

x D

ivis

ion

PO

Bo

x 1

25

Co

lum

bia

SC

29

20

20

10

1

So

uth

co

Lo

rra

ine

Zin

ar

21

0 N

Brin

ton

La

ke

Rd

Co

nco

rdvill

eP

A1

93

31

-93

31

Sta

nd

ard

Fe

de

ral B

an

kD

an

iel W

ats

on

26

00

We

st

Big

Be

ave

r R

dT

roy

MI

48

08

4

In r

e:

Co

llin

s &

Aik

ma

n C

orp

., e

t a

l.

Ca

se

No

. 0

5-5

59

27

(S

WR

)P

ag

e 2

of

3

Serv

ed

via

Fir

st

Cla

ss M

ail

CR

ED

ITO

R N

AM

EC

RE

DIT

OR

NO

TIC

E N

AM

EA

DD

RE

SS

1A

DD

RE

SS

2C

ITY

ST

AT

EZ

IPC

OU

NT

RY

Sta

te O

f A

lab

am

aD

ep

art

me

nt

Of

Re

ve

nu

e5

0 N

Rip

ley S

tM

on

tgo

me

ryA

L3

61

04

Sta

te O

f M

ich

iga

nD

ep

t O

f C

om

me

rce

& N

at

Re

sP

O B

ox 3

00

04

La

nsin

gM

I4

89

09

Sta

te O

f M

ich

iga

nL

ind

a K

ing

PO

Bo

x 3

04

57

La

nsin

gM

I4

89

09

-79

57

Sta

te O

f M

ich

iga

nM

att

he

w R

ick A

sst

Att

orn

ey G

en

era

lP

O B

ox 3

07

54

La

nsin

gM

I4

89

09

Sta

te O

f M

ich

iga

nS

tate

Of

Mic

hig

an

Mc

De

pt

77

83

3D

etr

oit

MI

48

27

7-0

83

3

Sta

te O

f M

ich

iga

nS

tate

Se

co

nd

ary

Co

mp

lex

71

50

Ha

rris

Dr

PO

Bo

x 3

00

15

La

nsin

gM

I4

89

09

Sta

te o

f M

ich

iga

n4

30

W A

lleg

an

St

La

nsin

g

MI

48

91

8-0

00

1

Sta

te o

f M

ich

iga

n C

en

tra

l F

un

ctio

ns U

nit

Je

nn

ife

r N

elle

sO

ffic

e o

f C

hild

Su

pp

ort

PO

Bo

x 3

07

44

La

nsin

gM

I4

89

09

-82

44

Su

mm

it P

rop

ert

y M

an

ag

em

en

t In

c2

49

01

No

rth

we

ste

rn H

wy 3

02

So

uth

fie

ldM

I4

80

75

Ta

te B

ou

leva

rd I

Llc

First

Pla

za

19

85

Blv

d S

eP

O B

ox 2

22

8H

icko

ryN

C2

86

02

Ta

x C

olle

cto

rC

ou

nty

Of

Fre

sn

oP

O B

ox 1

19

2F

resn

oC

A9

37

15

11

92

Tcs R

ea

lty L

td2

1 A

lbe

rt S

tT

ren

ton

ON

K8

V 5

R1

Ca

na

da

Te

kn

or

Fin

an

cia

l C

orp

ora

tio

nB

ruce

B G

alle

tly

PO

Bo

x 5

38

30

8A

tla

nta

GA

30

35

3

TG

No

rth

Am

erica

Ra

ym

on

d S

ou

cie

14

00

Ste

ph

en

so

n H

wy

Tro

yM

I4

80

83

Th

e C

orp

ora

tio

n O

f T

he

To

wn

Of

Ing

ers

oll

13

0 O

xfo

rd S

t 2

nd

Fl

Ing

ers

oll

ON

N5

C 2

V5

Ca

na

da

Th

e T

ow

n O

f P

ag

ela

nd

12

6 N

ort

h P

ea

rl S

tP

O B

ox 6

7P

ag

ela

nd

SC

29

72

8

To

m H

eck T

ruck S

erv

ice

13

06

E T

riu

mp

h D

rU

rba

na

IL6

18

02

To

wn

Of

Fa

rmin

gto

n3

56

Ma

in S

tF

arm

ing

ton

NH

38

35

To

wn

Of

Fa

rmvill

eF

arm

vill

e D

ow

nto

wn

Pa

rtn

ers

hip

38

02

S M

ain

Fa

rmvill

eN

C2

78

28

-16

21

To

wn

Of

Ga

na

no

qu

e3

0 K

ing

St

Ea

st

PO

Bo

x 1

00

Ga

na

no

qu

eO

NK

7G

2T

6C

an

ad

a

To

wn

Of

Lin

co

ln F

ina

nce

Off

ice

10

0 O

ld R

ive

r R

dP

O B

ox 1

00

Lin

co

lnR

I2

86

5

To

wn

Of

Old

Fo

rtP

O B

ox 5

20

Old

Fo

rtN

C2

87

62

To

wn

Of

Pa

ge

lan

dP

O B

ox 6

7P

ag

ela

nd

SC

29

72

8

To

wn

Of

Tro

y3

15

No

rth

Ma

in S

tT

roy

NC

27

37

1

Tr

Asso

cia

tes

Fsia

In

c2

00

E B

ig B

ea

ve

rT

roy

MI

48

08

3

Tre

asu

rer

City O

f D

etr

oit

PO

Bo

x 3

35

25

De

tro

itM

I4

82

32

Un

ifi In

c7

20

1 W

Frie

nd

ly A

ve

Gre

en

sb

oro

NC

27

41

0-6

23

7

Un

ifo

rm C

olo

r C

oR

an

dy L

ue

th

94

2 B

roo

ks A

ve

Ho

llan

dM

I4

94

23

Un

iqu

e F

ab

rica

tin

g I

nc

To

m T

ekie

ke

80

0 S

tan

da

rd P

kw

yA

ub

urn

Hill

sM

I4

83

26

-14

15

Un

ite

d S

tate

s A

tto

rne

y f

or

the

Ea

ste

rn

Dis

tric

t o

f M

ich

iga

nA

ttn

Civ

il D

ivis

ion

21

1 W

Fo

rt S

t S