Embed Size (px)

Citation preview

August, 2004

IN THE SUPREME COURT

OF THE STATE OF OREGON

WALSH CONSTRUCTION CO.,

Appellant,

v.

MUTUAL OF ENUMCLAW,

Appellee.

SC No. S51104

CA No. A117368

TC No. 0104-03398

BRIEF ON THE MERITS OF AMICUS CURIAE

AMERICAN SUBCONTRACTORS ASSOCIATION

James C. Chaney 91191 THE CHANEY FIRM, LLC 777 High Street, Suite 280 Eugene, Oregon 97401 Telephone: (541) 683-3800 Attorney for Appellant Walsh Construction Co.

Christopher A. Rycewicz 86275 RYCEWICZ & CHENOWITH, LLP 601 S.W. Second Avenue, Suite 1940 Portland, Oregon 97204 Telephone: (503) 221-7958 Attorney for American Subcontractors Association, Inc.

Thomas M. Christ 83406 COSGRAVE VERGEER & KESTER LLP805 S.W. Broadway, 8th Floor Portland, Oregon 97205 Telephone: (503) 323-9000 Attorney for Respondent Mutual of Enumclaw

William H. Walters 82481 D. Gary Christensen 88180 MILLER NASH, LLP 3400 US Bancorp Tower 111 SW Fifth Avenue Portland, Oregon 97204-3699 Telephone: (503) 224-5858 Attorneys for Oregon-Columbia Chapter of Associated Oregon Industries, Pacific Northwest Regional Council of Carpenters, Oregon Building Industry Association, Columbia Corridor Association, Hoffman Construction Company, and Senator Frank Morse

i

TABLE OF CONTENTS

Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

I. Material Facts “Undisputed” by Walsh Construction on Summary Judgment . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

II. What it Means “To Indemnify” Under O.R.S. § 30.140 . . . . . . . . . . . . . . . . . . . . .

A. Distinctions Without a Difference . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

B. Oregon Law Avoids Moral Hazards That Cause Accidents and Construction Defects . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

C. Insurance Procured in Violation of Law and Public Policy Must Be Void . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

III. Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . .1

. . .2

. . .4

. . .8

. .11

. .14

. .18

Appendix

A. Workplace Fatalities Labor Statistics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

B. Standard Form for Commercial General Liability Insurance: CG 00 01 07 98 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

C. The Additional Insured Book, Chapter 1 “Executive Summary” . . . . . . . . . .

D. ASA’s Subcontractors’ Chart of State Anti-Indemnity Laws . . . . . . . . . . . . .

. . .App-1

. . .App-3

. .App-17

. .App-28

TABLE OF AUTHORITIES

Cases

Acceptance Insurance Company v. Syufy Enterprises 81 Cal.Rptr.2d 557 (Cal. App. 1999) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

American Country Ins. Co. v. Cline, 722 N.E.2d 755 (Ill.App. 1 Dist. 1999) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Barton-Malow v. Grunau, 835 So.2d 1164 (Fla.App.2nd Dist 2002) . . . . .

Babineaux v. McBroom Rig Building, 806 F.2d 1282 (5th Cir. 1987) . . . . .

. . . . . . . . . . . .6

. . . . . . . . 8, 17

. . . . . . . . . . 10

. . . . . . . . . . . 9

ii

Buckeye Union Ins. v. Zavarella Bros., 699 N.E.2d 127 (Ohio 8th App. 1997) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Charter Oak Fire Insurance Co. v. Color Converting Industries Co., 45F.3d 1170 (7th Cir. 1995) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Chevron v. Bragg Crane & Rigging, 180 Cal.App.3d 639, 225 Cal. Rptr. 742 (1986) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Chrysler Corp. v. Merrell & Garaguso, Inc., 796 A.2d 648 (Del. 2002). . .

Davis v. Comm. Edison Co., 336 N.E.2d 881 (Ill. Supr. 1975) . . . . . . . . . .

Fitzgerald v. Neal, 113 Or. 103, 231 P. 645 (1924) . . . . . . . . . . . . . . . . . .

Gardner v. First Escrow Corp., 71 Or.App. 715, 696 P.2d 1172 (1985) . .

Gerow v. Rohm & Haas Company, 308 F.3d 721 (2002) . . . . . . . . . . . . . .

Greer v. City of Philadelphia, 795 A.2d 376, 381-382 (Pa. 2002) . . . . . . .

Hall v. Life Insurance Company of North America, 317 F.3d 773, 775 (7th

Cir. 2003) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Harrell v. Travelers Indemnity Co., 279 Or. 199, 567 P.2d 1013 (1978) . .

Jacobs Constructors v. NPS Energy, 264 F.3d 365 (3d Cir. 2001) . . . . . . .

Jankele v. Texas Co., 54 P.2d 425 (Utah 1936) . . . . . . . . . . . . . . . . . . . . . .

Lamb v. Armco, Inc., 518 N.E.2d 53 (Ohio App. 1986) . . . . . . . . . . . . . . .

Mortenson v. National Union Fire Insurance Co. of Pittsburgh, Pa., 249 F.3d 667 (7th Cir. 2001) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

National Union Fire Insurance Co. v. Nationwide Insurance, 82 Cal.Rptr.2d 16 (Cal.App. 4 Dist. 1999) . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Pardee Construction v. Insurance Company of the West, 92 Cal. Rptr. 2d 443 (2000) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Pickhover v. Smith’s Management Corp., 771 P.2d 664 (Utah App. 1989) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Stickovich v. Cleveland, 757 N.E.2d 50 (Ohio 8th App. 2001) . . . . . . . . . .

Snyder v. Nelson, 278 Or. 409, 564 P.2d 681 (1977) . . . . . . . . . . . . . . . . .

. . . . . . . . .9-10

. . . . . . . . . . 12

. . . . . . . . . . . 6

. . . .6, 7, 16-17

. . . . . . . . 7, 14

. . . . . . . . . . 15

. . . . . . . . . . 15

. . . . . . . . . . 12

. . . . . . . . . . . 8

. . . . . . . . . . 12

. . . . . . . . . . 15

. . . . . . . . . . 16

. . . . . . . . .7, 14

. . . . . . . . .7, 14

. . . . . . . . . . .12

. . . 1, 7, 11, 14

. . . . . . . 2, 4, 5

. . . . . . . 14 n.2

. . . . . . . . . . .10

. . . . . . . . . . 15

iii

Structure Tone v. Component Assembly Sys., 713 N.Y.S.2d 161 (A.D. 1 Dept. 2000) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Tishman Const. Corp. v. CNA Insurance, 652 N.Y.S.2d 742 (A.D. 1 Dept. 1997) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

W.M. Schlosser Co., Inc. v. Maryland Drywall Co., 673 A.2d 647 (D.C.App. 1996) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . 6

. . . . . . . . . . .11

. . . . . . . . 6, 16

Statutes

15 U.S.C. § 1012(b) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Fla. Stat. § 725.06 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

La. Rev. Stat § 9:2780(G) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Mont. Rev. Code Title 28, Ch. 2, Part 21 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Missouri Rev. Stat. § 434-100(2)(8) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

N.M. Stat. § 56-7-1 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

O.R.S. § 30.140 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1-5,

O.R.S. § 701.105 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

O.R.S. § 737.007 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

O.R.S. § 737.225 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

O.R.S. § 737.255 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

O.R.S. § 737.526 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Subcontractors’ Chart of State Anti-Indemnity Laws . . . . . . . . . . . . . . . . . . . . .

. . . . . .13

. . . . . .10

. . . . . . . 9

. . . . . . .9

. . . . . . 10

. . . . . . .9

14-15, 18

. . . . . .17

. . . . . .13

. . . . . . 13

. . . . . .13

. . . . . . 13

. .App-28

Texts, Treatises or Other Authorities

CG 00 01 07 98 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

English, Kenneth G., Government Complicity and a Government

Contractor’s Liability in Qui Tam and Tort Cases, 33 Public Contract Law Journal 649 (American Bar Association 2004) . . . . . . . . . . . . . . . . . .

. . . . . 4, App-4

. . . . . . . 11-13

iv

Gibson, Ligeros & Malecki, The Additional Insured Book, Chapter 1, “Executive Summary” (IRMI 2000). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Kaplow, Louis, An Economic Analysis of Legal Transitions, 99 Harv.L.Rev. 509 (1986) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Mehta, Additional Insured Status In Construction Contracts And Moral

Hazard, 3 Conn.Ins.L.J. 169 (1996) . . . . . . . . . . . . . . . . . . . . . . . . . . . . .5,

Posner, Richard A., Economic Analysis of Law, Little, Brown & Company (1986) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Seidenfeld, An Apology for the Administrative Law in The Contracting

State, 28 Fla.St.U.L.Rev. 215 (2000) . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . 5, App-17

. . . . . . . . . . 12

7, 9, 11, 13-14

. . . . . . . . . . 12

. . . . . . . . . . .11

1

INTRODUCTION

Amicus Curiae American Subcontractors Association, Inc. (“ASA”), urges this

Court to do two things. First, to affirm the decision of the Court of Appeals that plaintiff-

appellant, Walsh Construction Co. (“Walsh Construction”), failed to adduce evidence on

motions for summary judgment raising a genuine dispute about the extent, if any, of its

subcontractor’s negligence, as required by O.R.S. § 30.140(2). Second, to reject the

argument of defendant-respondent, Mutual of Enumclaw (“Mutual of Enumclaw”), that

the use of alternate policy forms to those employed in this case would have permitted

Walsh Construction to have coverage as an “additional insured” against its own

negligence, thereby circumventing Oregon’s public policy as expressed in O.R.S. §

30.140, Oregon’s anti-indemnity statute. See Response to Petition for Review at 3 (“The

Court of Appeals decision in this case applies only to blanket-style endorsements”).

Oregon’s anti-indemnity statute is designed to reduce the number of injuries to

construction workers, and also to reduce the number of construction defects plaguing the

construction industry, by forcing those who lead and supervise construction projects to

pay for the consequences of their own negligence using their own insurance and assets,

rather than using the assets and insurance of their subcontractors by way of “hold

harmless” clauses and “additional insured” contract requirements. See, e.g., National

Union Fire Insurance Co. v. Nationwide Insurance, 82 Cal.Rptr.2d 16, 22 (Cal.App. 4

Dist. 1999) (limited construction of an additional insured endorsement “furthers

California’s interest in preventing construction-related accidents”).

Oregon’s public policy on indemnification in construction contracts is a gravely

important matter: the construction industry accounted for twenty percent (20%) of

workplace fatalities in the United States in 2001 and 2002, according to the U.S. Bureau

2

of Labor Statistics, although it employed only five percent (5%) of the workforce in

either of those years. See Appendix at 1-3. Construction is not only plagued by worker

injury lawsuits such as that underlying the instant matter, but also by construction defect

lawsuits. These are the very issues addressed by Oregon’s anti-indemnity statute,

because lawsuits for worker injuries and construction defects are the primary subjects of

obligations to hold harmless and procure insurance in construction contracts.

This case, for instance, involves an injury to the employee of Ron Rust Drywall, a

subcontractor to Walsh Construction. For a construction defect example, see, e.g.,

Pardee Construction v. Insurance Company of the West, 92 Cal. Rptr. 2d 443, 454-456

(2000) (ruling that certain “additional insured” coverage forms include completed

operations coverage for the additional insured, while others do not, depending on their

language).

Oregon’s anti-indemnity statute is worded, and intended, to address the moral

hazards that arise when the leaders of a construction project can make claims on policies

that do not name them as named insureds, undermining the safety of construction

workers, as well as the quality of life for every citizen of Oregon who lives or works in a

building. This Court’s unambiguous ruling to effectuate the intent of the statute, and to

prohibit the enforcement of insurance procured in direct violation of Oregon law and

public policy, is vital to protect Oregon’s workers and other citizens.

I. MATERIAL FACTS “UNDISPUTED”

BY WALSH CONSTRUCTION ON SUMMARY JUDGMENT

The court of appeals did not “seemingly ignore” ORS § 30.140(2), as contended

in the Brief on the Merits of Amici Curiae Oregon-Coumbia Chapter of Associated

General Contractors, et al., at page 7. Quite to the contrary, the court of appeals directly

3

held that it was “undisputed” that subsection (2) of Oregon’s anti-indemnity statute did

not apply to this case. In other words, paraphrasing subsection (2), no evidence was

proffered by Walsh Construction to show “the extent that the … bodily injury [to an

employee of Walsh Construction’s subcontractor, Ron Rust Drywall, on December 8,

1998] … arises out of the fault of [Mutual of Enumclaw’s named insured, Ron Rust

Drywall],” even though the extent of Ron Rust’s negligence was a material fact on

motions for summary judgment. Any suggestion that the lower courts failed to afford

Walsh Construction with an opportunity to litigate the extent of the negligence of Ron

Rust Drywall is, therefore, unjustified. As noted in the Brief on the Merits of Amici

Curiae Oregon-Columbia Chapter of Associated General Contractors, et al., at 3,

“Walsh’s position did not include an alternative argument based on the relative fault of

itself and Rust, Enumclaw’s insured.” That’s precisely why the court of appeals

specifically found that the non-application of the exception for indemnity based on the

negligence of the indemnitor, as provided by ORS § 30.140(2), was “undisputed.”

ASA urges this Court to clarify that the court of appeals did not hold “that a

commonplace contract requirement is entirely void,” as Walsh Construction apparently

has convinced the legislative sponsor of ORS § 30.140, Senator Frank Morse. See

sentence beginning “Walsh, however, says …,” in the Senator’s letter dated February 12,

2004, attached to the February 2004 Brief of Amici Curiae Oregon-Columbia Chapter of

Associated General Contractors et al., at APP-7 thereof. As the Senator pointed out in

his letter, “ORS 30.140 is clear that contractual provisions are void only ‘to the extent’

that they in fact require one to bear another’s liability.” But, contrary to the Senator’s

contention, the court of appeals cannot be fairly said to have “called into question the

validity of risk-allocation clauses … regardless of who bears the liability,” because the

4

extent of Ron Rust Drywall’s negligence was never made the subject of a factual dispute

by Walsh Construction on motions for summary judgment. The point, that Walsh

Construction failed to adduce evidence raising a factual dispute, seems to have been lost

on learned observers like the Senator, and their lawyers, perhaps because the court of

appeals dealt with the issue so briefly, in a single sentence, where it wrote that the

inapplicability of ORS 30.140(2) was “undisputed.” ASA therefore urges the Court to

further elucidate the point, for sake of clarity, in laymen’s terms.

II. WHAT IT MEANS “TO INDEMNIFY” UNDER O.R.S. § 30.140

“Hold harmless” terms and “additional insured” requirements in construction

subcontracts each provide an alternate route to the same general liability insurance

coverage purchased by a named insured subcontractor. The standard form for

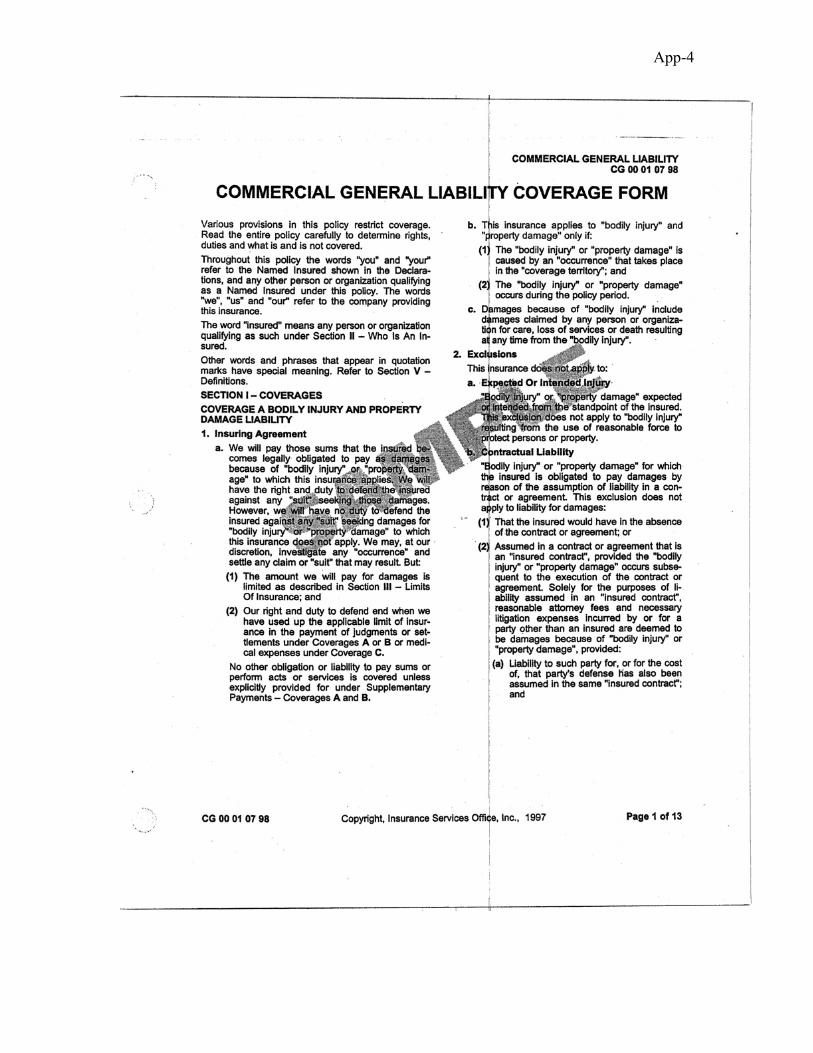

commercial general liability policies published by Insurance Services Office, Inc., (ISO),1

the CG 00 01 form (07/98 edition) (copy attached at App-4), for example, includes

coverage for the named insured’s obligations contained in contracts “pertaining to [the

named insured’s] business,” to defend and hold others harmless against “tort liability.”

See App-4 at Section I, ¶ 2.b.(2)(a) (exception to exclusion of assumed liabilities), and

App-14 at Section V, ¶ 9.f. (defining “insured contract”).

Other standard forms (notably the CG 20 10 forms discussed in Pardee

Construction, 92 Cal.Rptr2d at 454-456) exist for the purpose of adding “additional

insureds” to the same insurance policies, providing yet another means for a contracting

1 “ISO is a nonprofit trade association that provides rating, statistical, and actuarial policy forms and related drafting services to approximately 3,000 nationwide property or casualty insurers. Policy forms developed by ISO are approved by its constituent insurance carriers and then submitted to state agencies for review. Most carriers use the basic ISO forms, at least as the starting point for their general liability policies.” Pardee Construction, 92 Cal. Rptr. 2d at 456 n.15 (internal quotes omitted).

5

party to ensure coverage under a general liability insurance policy procured by someone

else. In fact:

Indemnitees sometimes require additional insured status in an attempt to circumvent statutes prohibiting the transfer of sole fault in indemnity provisions. This goal may be achieved with additional insured status if the endorsement used to provide additional insured status does not exclude the additional insured’s sole fault (most do not) and if the contract is drafted carefully (with the insurance requirements stated separately from the defense and indemnification provisions).

Malecki, Ligeros and Gibson, The Additional Insured Book, International Risk

Management Institute (2000) at 3, App-21, under “Coverage Scope” (an earlier edition of

this book was cited in Pardee Construction, 92 Cal. Rptr.2d at 456, along with other

IRMI publications); see also Mehta, Additional Insured Status & Moral Hazard, 3

Conn.Ins.L.J. 169, 183 (“Most courts have held that despite statutes prohibiting broad

form indemnity, where a party has been named an additional insured, this party is entitled

to receive indemnification from the indemnitor’s insurer”).

Thus, “hold harmless” terms and “additional insured” requirements are

indistinguishable in their purpose, which is to put the general liability insurance of the

contract obligor, or else the other assets of the contract obligor, at risk when a third-party

lawsuit is filed against the contract obligee. Webster’s Ninth New Collegiate Dictionary

defines “insurance” as “coverage by contract whereby one party undertakes to indemnify

or guarantee another against loss by a specified contingency or peril [emphasis

supplied].” Merriam-Webster, Inc., 1985; compare ORS § 30.140 (“to indemnify”).

Additionally, the remedy for breach of a requirement to purchase insurance and

name another as an “additional insured,” and for breach of an “additional insured”

endorsement by an insurance company, and for breach of a “hold harmless” requirement,

6

is the same: indemnity and defense. See, e.g., Chrysler Corp. v. Merrell & Garaguso,

Inc., 796 A.2d 648 (Del. 2002) (Chrysler’s claim that “under the terms of the contract

between Chrysler and Merrell, Merrell was required to indemnify and defend Chrysler

from all claims arising under the construction contract” was based on both “hold

harmless” terms (ruled void) and “additional insured” requirements in the contract;

remanded “to determine such rights as Chrysler may be able to assert under the Penn

National policy” purchased by Merrell); compare Chevron v. Bragg Crane & Rigging,

180 Cal.App.3d 639, 225 Cal. Rptr. 742 (1986) (prime contractor, Bragg, force to

indemnify project owner, Chevron, against Chevron’s own negligence based on breach of

“additional insured” requirement to the extent of Bragg’s deductible, because the

contractual insurance requirements did not mention a deductible); compare also W.M.

Schlosser Co., Inc. v. Maryland Drywall Co., 673 A.2d 647 (D.C.App. 1996) (“hold

harmless” indemnity for general contractor against $3,000,000 judgment in favor of

drywall subcontractor’s employee who fell three-stories through a door-sized opening in

the floor rendering him a quadriplegic) and Structure Tone v. Component Assembly Sys.,

713 N.Y.S.2d 161 (A.D. 1 Dept. 2000) (carpentry subcontractor’s general liability carrier

required “to indemnify” general contractor, who was named as an “additional insured,”

against a lawsuit by an employee of carpentry subcontractor’s sub-subcontractor) and

Acceptance Insurance Company v. Syufy Enterprises 81 Cal.Rptr.2d 557 (Cal. App.

1999) (declaratory judgment action by carrier against additional insured to determine “the

parties’ rights and obligations in the defense and indemnification of [the injured

subcontractor’s employee]’s claim”).

Contract terms that require one party to hold another harmless, and contract terms

that require one party to purchase a general liability insurance policy and name the other

7

party as an “additional insured” on that policy, both shift not only the same kinds of

losses, but also records of loss experience, to the general liability insurance purchased by

the indemnifying party (the “named insured”) who must pay the future insurance

premiums. See Mehta, Additional Insured Status In Construction Contracts And Moral

Hazard, 3 Conn.Ins.L.J. 169, 187 (1996); see also the sentence accompanying n.1, above.

As a consequence, both loss-shifting mechanisms have the same public policy

implications, i.e., they both create a “moral hazard” which undermines both worker safety

and quality in building construction. See, e.g., National Union Fire Insurance Co. v.

Nationwide Insurance, 82 Cal.Rptr.2d 16, 22 (Cal.App. 4 Dist. 1999) (limited

construction of an additional insured endorsement “furthers California’s interest in

preventing construction-related accidents”), and Lamb v. Armco, Inc., 518 N.E.2d 53, 55-

56 (Ohio App. 1986) (purpose of anti-indemnity legislation “is to require employers to

provide employees with a safe place to work [original emphasis]”), and Davis v. Comm.

Edison Co., 336 N.E.2d 881, 884 (Ill. Supr. 1975) (“Having arranged the avoidance of

the burdens of liability, they no longer have the same motivations to lessen the extent of

the danger... to the prejudice of the worker's safety and interest”), and Jankele v. Texas

Co., 54 P.2d 425, 427 (Utah 1936) (“contracts exempting persons from liability for

negligence induce a want of care…. It has therefore been declared to be good doctrine

that no person may contract against his own negligence” (internal quotes omitted));

compare Chrysler, 796 A.2d at 652 (acknowledging “the force of the policy argument

limiting enforcement of the insurance savings provision [of Delaware’s anti-indemnity

law], but finding “equally strong policy considerations supporting the opposite view”

after a worker has been injured, based on court’s assumption that putting additional

insurance policies at risk substantially increases the odds of full compensation).

8

Oregon’s anti-indemnity statute uses broad language in the service of important

public policy goals to reduce construction defect litigation, and to improve worker safety,

by ensuring that those responsible for selection of subcontractors to perform work, and

for supervising and inspecting that work, are responsible for the financial consequences

of their own negligence. The law still permits an additional insured, or indemnitee under

a hold harmless clause, to be covered for liability that is “imputed” or “vicarious,” i.e.,

due to the negligence of the named insured or indemnitee under a hold harmless clause,

as well as for liability arising in strict liability. See, e.g., American Country Ins. Co. v.

Cline, 722 N.E.2d 755, 763 (Ill.App. 1 Dist. 1999) (“additional insured” coverage form

which limited coverage to “liability specifically resulting from the conduct of the Named

Insured which may be imputed to the Additional Insured,” and which excluded “liability

arising out of the claimed negligence of the Additional Insured,” would cover vicarious

and strict liability only and was not void as “illusory”) and compare Greer v. City of

Philadelphia, 795 A.2d 376, 381-382 (Pa. 2002) (hold harmless terms covering

indemnitees’ liability and attorneys fees “only to the extent caused in whole or in part by

negligent acts or omissions of the Subcontractor, the Subcontractor’s Sub-Subcontractors,

anyone directly or indirectly employed by them or anyone for whose acts they may be

liable,” held to provide “a meaningful benefit” including, but not limited to, attorneys

fees, unlike Pennsylvania contribution statute).

A. DISTINCTIONS WITHOUT A DIFFERENCE

It is true that “hold harmless” terms are generally subject to judicial limits that do

not apply to insurance policies, because unlike insurance policies which are construed in

favor of coverage, “hold harmless” terms are construed against coverage. In addition, 36

state legislatures have enacted “anti-indemnity” statutes extending protections to

9

construction subcontractors, which widely vary in their terms and effectiveness and

which are generally held to distinguish “hold harmless” terms from requirements to

purchase insurance. See App-28-App-30, see also Mehta, 3 Conn.L.J. at 182-183 (“Most

courts have held that despite statutes prohibiting broad form indemnity, where a party has

been named an additional insured, this party is entitled to receive indemnification from

the indemnitor’s insurer”). These distinctions, however, do not address the economic

reality that a claim for breach of a contractual requirement to purchase insurance, or a

claim against the insurance company (where the requirement was complied with), or a

claim for breach of a hold harmless clause, all lead to the same remedy. Since insurance

is a contract for indemnity, the remedy for breach is indemnity, and vice versa. See cases

discussed above at 5-6.

Statutory anti-indemnity language varies widely from state to state, making any

distinction between “hold harmless” terms and “additional insured” requirements with

regard to anti-indemnity legislation arguably more defensible in some jurisdictions than

others. It is worthy of note that Louisiana has barred the use of both broad “hold

harmless” and “additional insured” coverages in connection with oil drilling contracts for

decades, apparently without shutting down the oil drilling industry in that state. See

Babineaux v. McBroom Rig Building, 806 F.2d 1282 (5th Cir. 1987) (applying Louisiana

Oilfield Indemnity Act, La.Rev.Stat. § 9:2780(G)). Oregon also appears to have started a

trend to apply anti-indemnity limits to “additional insured” requirements in construction

contracts, recently followed by legislatures in Montana (Montana Revised Code Title 28,

Chapter 2, Part 21 (HB 482 (2003))) and New Mexico (N.M. Stat. §56-7-1 (SB 280

(2003)). Ohio courts have interpreted that state’s anti-indemnity law both ways, as either

extending, or not extending, to “additional insured” requirements. Compare Buckeye

10

Union Ins. v. Zavarella Bros., 699 N.E.2d 127 (Ohio 8th App. 1997) (additional insured

barred) and Stickovich v. Cleveland, 757 N.E.2d 50, 61 (Ohio 8th App. 2001) (additional

insured permitted).

Walsh Construction argued before the appeals court that insurance can be legally

distinguished from indemnification because indemnity is never subject to dollar limits,

while insurance is always subject to dollar limits. However, indemnity often is subject to

dollar limits. Current and former versions of Florida law, for example, bar, and have

barred, the use of unlimited indemnity terms in construction contracts without dollar

limits. See Fla. Stat. § 725.06. (A law passed in 2000 briefly removed the previous

statute’s requirement to use a dollar limit, however, the dollar limit requirement was

reinstated a short time later. See, e.g., Barton-Malow v. Grunau, 835 So.2d 1164

(Fla.App.2nd Dist. 2002)). Another example is provided by Missouri law, which puts

limits on hold harmless terms in any construction contracts which also include insurance

requirements, by limiting the hold harmless obligations to the limits of the required

insurance. Mo. Rev. Stat. § 434-100(2)(8).

Further, Walsh Construction’s argument leads to absurd results. If indemnity

terms could not have dollar limits, then the mere artifice of a dollar limit would serve to

undermine both statutory and judicial restrictions on the use of indemnity terms in

construction contracts throughout the country: anti-indemnity laws, after all, apply to

indemnity obligations. According to Walsh Construction, none of those laws (see App-

28-App-30 for a list) can apply to a hold harmless clause containing a dollar limit, since a

contract clause with a dollar limit cannot be an “indemnity clause.” Presumably not even

judicial rules of construction of indemnity clauses would apply, so long as a dollar limit

is included.

11

Finally, neither Walsh nor amicus has cited legislative history suggesting that

Oregon’s legislature intended to use the term appearing in the anti-indemnity statute, “to

indemnify,” to mean anything other than what it means in ordinary usage. See, e.g.,

Tishman Const. Corp. v. CNA Insurance, 652 N.Y.S.2d 742 (A.D. 1 Dept. 1997)

(majority and dissenting opinions discussing whether insurance carrier, CNA, “must

indemnify Tishman [an additional insured] to the extent of the policy limits [emphasis

supplied]”).

B. OREGON LAW AVOIDS MORAL HAZARDS

THAT CAUSE ACCIDENTS AND CONSTRUCTION DEFECTS

Insurance companies assign loss experience to the “named insured” on an affected

insurance policy, not to “hold harmless” or “additional insured” indemnitees who also

have claims paid by the policy. See Mehta, Additional Insured Status In Construction

Contracts And Moral Hazard, 3 Conn.Ins.L.J. at 187 (1996) (“In the ordinary insurance

relationship, the insured is also deterred from engaging in risky activity by the notion that

an accident or occurrence will result in the insurer raising its premiums,” however, “the

additional insured is insulated against this prospect by the fact that it is not responsible

for premium payments to the insurer and is unaffected by the raising of premiums”),

quoted in Nat. Union Fire Ins. Co. v. Nationwide Ins., 82 Cal.Rptr.2d 16, 22 (Cal. App. 4

Dist. 1999) (limited construction of additional insured policy endorsement “furthers

California’s interest in preventing construction-related accidents.”). The result is a

“moral hazard” problem, where “a party to a transaction can engage in behavior that

changes the risks to the other party associated with the transaction.” Seidenfeld, An

Apology for the Administrative Law in The Contracting State, 28 Fla.St.U.L.Rev. 215,

225 n.44 (2000), quoted in English, Kenneth G., Government Complicity and a

12

Government Contractor’s Liability in Qui Tam and Tort Cases, 33 Public Contract Law

Journal 649, 658 (American Bar Association 2004).

“[T]he moral hazard of insurance [is] the chance that the existence of insurance

will increase the likelihood of the insured event.” Hall v. Life Insurance Company of

North America, 317 F.3d 773, 775 (7th Cir. 2003); see also Charter Oak Fire Insurance

Co. v. Color Converting Industries Co., 45 F.3d 1170, 1174 (7th Cir. 1995) (“moral

hazard” arises when insurance companies “insure against risks that the insured controls.

Such insurance would give the insured an incentive to increase risk, since he would have

shifted the cost of the increased risk to the insurance company”), see also Kaplow, Louis,

An Economic Analysis of Legal Transitions, 99 Harv.L.Rev. 509, 537 (1986). Acute

moral hazards justify many public policy limits on the use of insurance, such as the

“familiar example [of] taking out a life insurance policy on another person’s life without

his consent,” or “the rule that forbids insuring against criminal fines.” Mortenson v.

National Union Fire Insurance Co. of Pittsburgh, Pa., 249 F.3d 667, 671 (7th Cir. 2001).

The “moral hazard” of insurance is a common tool of economic analysis that has been

analogized to many issues not directly related to insurance, such as: (i) bankruptcy (“One

can buy and consume all sorts of nice things on debt and then default. The problem (a

particularly serious form of the general moral hazard problem of insurance) could be

solved only by distinguishing between voluntary and involuntary defaults and limiting

the privilege to the latter.” Posner, Richard A., Economic Analysis of Law, Little, Brown

& Company (1986) at 376-377); (ii) contractual attorneys fees provisions (“An

opportunity to litigate on the adversary’s dime, without any need to prevail in order to

collect, creates a moral hazard ….” Gerow v. Rohm & Haas Company, 308 F.3d 721,

725-6 (2002)); and (iii) the scienter element of qui tam litigation (see English, 33 Public

13

Contract Law Journal at 658). “Moral hazard” has also been applied to international

monetary policy (see, e.g., http://www.morganstanley.com/GEFdata/digests/20000724-

mon.html#anchor0), banking policy (see, e.g., http://www.gametheory.net/

News/Items/002.html), and even topics like the designated hitter rule in Major League

Baseball, and whether skiers should wear helmets (see generally http://www.

gametheory.net/cgi-bin/viewnewsdate.pl).

In the context of insurance, the moral hazard problem is ordinarily alleviated by

“monitoring” of the named insured by the insurance carrier. See Mehta, 3 Conn.L.J. at

185-6. Insurance carriers can provide affirmative incentives to their named insureds to

reduce the risk of loss, and they can also monitor the loss experience of their named

insureds and adjust premiums accordingly. Mehta, 3 Conn.L.J. at 186-187. In fact,

insurance carriers share loss experience information with each other through “rating

organizations” (see O.R.S. §§ 737.007, .225, .255, .526), which are explicitly exempted

from federal anti-trust laws by the McCarran-Ferguson Act of 1945 (15 U.S.C. §§ 1011-

1015). See 15 U.S.C. § 1012(b). The ability to share loss experience information solves

the moral hazard problem for most common forms of insurance, but an “additional

insured” is “not responsible for direct premium payments to the insurer,” and “is

unaffected by the raising of premiums.” Mehta, 3 Conn. L.J. at 186-187. “[W]hile the

primary insured, by way of its direct contractual relationship with the insurer, has a

continuing motivation to exercise high standards of care, the additional insured has no

such motivation once the contract has been executed. Without this continuing

14

motivation, the additional insured’s standard of care will expose third parties to the

increased likelihood of harm.” 2 Mehta, 3 Conn.L.J. at 187.

Thus, narrow construction of additional insured coverage “further’s California’s

interest in preventing construction-related accidents.” National Union Fire Insurance

Co. v. Nationwide Insurance, 82 Cal.Rptr.2d 16, 22 (Cal.App. 4 Dist. 1999). See also

Lamb v. Armco, Inc., 518 N.E.2d 53, 55-56 (Ohio App. 1986) (purpose of anti-indemnity

legislation “is to require employers to provide employees with a safe place to work

[original emphasis]”), and Davis v. Comm. Edison Co., 336 N.E.2d 881, 884 (Ill. Supr.

1975) (“Having arranged the avoidance of the burdens of liability, they no longer have

the same motivations to lessen the extent of the danger ... to the prejudice of the worker's

safety and interest”), and Jankele v. Texas Co., 54 P.2d 425, 427 (Utah 1936) (“contracts

exempting persons from liability for negligence induce a want of care …. It has therefore

been declared to be good doctrine that no person may contract against his own

negligence.”);

Oregon’s anti-indemnity statute, by extending not only to the parties to a

construction contract but also to their sureties and insurers, implicitly recognizes that

“The same moral hazard public policy argument which disfavors broad form indemnities

also disfavors additional insured arrangements.” Mehta, 3 Conn.Ins.L.J. at 181.

C. INSURANCE PROCURED IN VIOLATION

OF LAW AND PUBLIC POLICY MUST BE VOID

In its Response to Petition for Review, Mutual of Enumclaw downplayed the

grave public policy concerns addressed by Oregon’s anti-indemnity law and suggested

2 The contrary conclusion of the Utah Court of Appeals in Pickhover v. Smith’s Management Corp., 771 P.2d 664 (Utah App. 1989), quoted on page 7 of Walsh Construction’s Brief on the Merits, that “a contractual entitlement to insurance provided by another does not encourage the beneficiary of that agreement to act any more irresponsibly than the insurance policy itself would,” is incorrect, because it fails to account for either the moral hazard problem of insurance, or the solution of monitoring.

15

that, by using forms other than “blanket forms” to add additional insureds to a

construction subcontractor’s general liability policy, different results could have still been

obtained by Walsh Construction and its insurer, Zurich. See Response to Petition for

Review at 2-4. Such a construction of the statute would render it prospectively

ineffective, because it would allow the statute to be easily circumvented by those willing

to bully their subcontractors into compliance with illegal insurance requirements.

Statutes enacted for the benefit of the public should be liberally construed to

effectuate the purpose for which they were enacted. Fitzgerald v. Neal, 113 Or. 103, 110,

231 P. 645, 648 (1924) cited in Gardner v. First Escrow Corp., 72 Or.App. 715, 696 P.2d

1172, 1179 (1985). O.R.S. § 30.140 is such a statute, designed to prevent harm to

workers during construction, and to protect inhabitants of the built environment from

construction defects after the work is completed.

Insurance coverage has been held void where an insured acts purposefully to

cause injuries and damage. In Snyder v. Nelson, 278 Or. 409, 451-416, 564 P.2d 681,

684-685 (1977), this Court remanded a claim for automobile insurance coverage to the

trial court to determine a “legitimate question of fact as to whether [the insured] intended

the injuries and damage,” because public policy prohibits insurance coverage for damage

that the insured causes on purpose. The drafting of contractual requirements for

“additional insured” coverage that is not limited to the extent of the negligence of the

named insured is quite deliberate, and does not involve merely a reckless conduct as in

Harrell v. Travelers Indemnity Company, 279 Or. 199, 567 P.2d 1013 (1978) (punitive

damages, awarded against an insured for an automobile collision caused by the insured’s

“reckless driving after drinking,” were a permissible subject of insurance coverage). It

follows that where a contract requires insurance for the negligent acts of an “additional

16

insured,” and the contract was drafted and signed intentionally, then the coverage

procured to satisfy the illegal contractual requirement must be void.

Mutual of Enumclaw’s position, which would permit coverage for the negligence

of the “additional insured” by means of different forms, is arguably supported by policy

arguments discussed by the Delaware Supreme Court in its Chrysler opinion. Although

the Delaware Supreme Court acknowledged “the force of the policy argument limiting

enforcement of the insurance savings provision [of Delaware’s anti-indemnity law],” it

nonetheless found that “equally strong policy considerations supporting the opposite view

[that ‘additional insured’ coverage should be permitted],” because, by multiplying the

number of insurance policies at risk, the odds of full compensation for victims are, the

court assumed, substantially increased. Chrysler, 796 A.2d at 652.

Naturally, the Delaware Supreme Court’s reasoning is based on statutory

language quite different from the statute in question here. But its reasoning is also

flawed, because it is based on the premise that dollar compensation is full compensation

for an injury, and because it fails to consider other transactional costs. The Delaware

Court’s logic presupposes that, for example, the victim Robertson, in the W.M. Schlosser

case was just as well off as a quadriplegic but $3,000,000 richer, as he would have been

had the general contractor discovered and remedied the unsafe condition before the

accident, preventing its occurrence. Or that the families of the victims in Jacobs

Constructors v. NPS Energy, 264 F.3d 365 (3d Cir. 2001), were just as well off with

millions of dollars, but without their loved ones who perished while working as

construction laborers, as they would have been had the Pennzoil plant, to which the

laborers were constructing an addition, never exploded into flames. Surely such extreme,

materialistic assumptions are incorrect. Life and health are valued more highly than

17

money in any society of proper perspective and good morals, as well as by any sane

individual. It is preferable to not be a victim in the first place, than to be a well-

compensated victim.

Moreover, the Delaware Court failed to consider ancillary costs to society, which

is burdened with a larger population of quadriplegics and orphaned children than in a

world with fewer accidents. Nor did that court consider the costs imposed on a county

depending on property tax revenue from a development of defective homes, or from a

defective office building. Nor did the court consider the time of judges and juries who

must weigh the appropriate levels of compensation for each victim.

Even more fundamental to its reasoning, the Delaware Court’s analysis assumes

that general contracting firms will not have adequate insurance in some significant

number of cases. Such an assumption is grossly flawed. For one thing, general

contractors are required to have $500,000 in general liability coverage just to be licensed

in Oregon. O.R.S. § 701.105(a). Additionally, construction contracts ordinarily contain

insurance requirements of their own, as in this case. See American Country Ins. Co. v.

Cline, 722 N.E.2d 755, 761-762 (court assumed that “businesses in the construction

industry carry coverage for liability arising out their own work,” and that an additional

insured general contractor “would have its own general liability coverage”); see also the

February 23, 2004, letter from the Executive Director for the Oregon-Columbia Chapter

of the Associated General Contractors of America, attached to the February 2004 Brief of

Amici Curiae Oregon-Columbia Chapter of the Associated General Contractors of

America, et al., at APP-10 thereof: (“In order to do business in today’s market, general

contractors and subcontractors through contractual requirements must carry significantly

more insurance than is required by law”).

18

Here, the Oregon legislature has recognized, and moved to correct, by

amendment, the loophole that had permitted a construction contractor’s “insurer” to

indemnify losses that the contractor could not be required to indemnify directly. This

Court should not fashion yet another loophole that would encourage contractors

throughout Oregon to withhold work from subcontractors who will not comply with

illegal contract requirements. To the contrary, the Court should make clear, as this

controversy is bound to arise again, that no coverage for an “additional insured” that is

provided pursuant to a construction contract will be permitted in Oregon except “to the

extent that the death or bodily injury to persons or damage to property arises out of the

fault of the indemnitor, or the fault of the indemnitor's agents, representatives or

subcontractors." O.R.S. § 30.140(2). Parties seeking coverage as “additional insureds”

should be prepared to adduce some evidence proving “the extent … of … fault” of the

named insured, or else they should be prepared to lose their case on motions for summary

judgment, as Walsh Construction did in this case.

Contractors should compete for general liability insurance coverage based on their

records for negligence and loss, not on their ability to enforce illegal contractual

insurance requirements through bullying tactics. Insurance procured pursuant to illegal

and void contractual requirements must also be void, or else the law’s purpose will be

utterly frustrated.

III. CONCLUSION

This Court should affirm the decision of the Court of Appeals, clarifying that it

was incumbent upon Walsh Construction, as the trial court plaintiff, to proffer evidence

on summary judgment motions showing the extent of the negligence of the named

insured of the trial court defendant, Mutual of Enumclaw. This Court should also

19

expressly reject the contentions of Mutual of Enumclaw that insurance procured in

violation of the law and public policy of Oregon may be enforced depending on the

policy form that is used.

Respectfully submitted, AMERICAN SUBCONTRACTORS ASSOCIATION, INC., by and through its counsel,

___________________________________Christopher A. Rycewicz 86275 RYCEWICZ & CHENOWETH 601 S.W. Second Avenue, Suite 1940 Portland, Oregon 97204 Telephone: (503) 221-7958

Brian W. Cubbage, Construction Law & Contracts Counsel, AMERICAN SUBCONTRACTORS ASSOCIATION, INC., assisted the preparation of this brief

App-1

APPENDIX

A. Workplace Fatalities Labor Statistics

Excerpts from a report by the U.S. Department of Labor, Bureau of Labor Statistics

(“BLS), at http://www.bls.gov/iif/oshwc/cfoi/cfch0001.pdf (July 1, 2004), show U.S.

workplace fatalities for 2001 and 2002, as well as workplace fatalities for the

construction industry in 2002:

App-2

Another report available at http://data.bls.gov/cgi-bin/surveymost?cf shows fatalities in

the construction industry for both 2001 and 2002:

Census of Fatal Occupational Injuries

Series Id: CFU00M20081

Case Type: Fatalities by detailed private industry

Category: Total

Industry: Construction

Year Annual

2001 1226(n)

2002 1121(p)

n : Excludes Sept. 11th terrorist attacks

p : preliminary

The reports show that the construction industry accounted for 1121 out of 5524

workplace fatalities in 2002, or 20.3%, and 1226 out of 5915 workplace fatalities in

2001, or 20.7%.

App-3

BLS reports on its “Industry at a Glance” Web page for the construction industry

(http://www.bls.gov/iag/construction.htm) that “construction employs about 5.2 percent

of all workers,” and its Quarterly Census of Employment and Wages, available at

http://data.bls.gov/cgi-bin/dsrv?en, confirms that the construction industry employed

6,716,000 out of 128,233,919 in 2002 (or 5.2%) and 6,683,000 out of 129,635,800 in

2001 (or 5.2%):

Quarterly Census of Employment and Wages

Series Id: ENUUS00010010

State: U.S. TOTAL

Area: U.S. TOTAL

Industry: Total, all industries

Owner: Total Covered

Size: All establishment sizes

Type: All Employees

Year Annual

2001 129635800

2002 128233919

Series Id: ENUUS0001051012

State: U.S. TOTAL

Area: U.S. TOTAL

Industry: Construction

Owner: Private

Size: All establishment sizes

Type: All Employees

Year Annual

2001 6773512

2002 6683553

B. Standard Form for Commercial General Liability Insurance: CG 00 01 07 98

The following form for Commercial General Liability Insurance is published by the

Insurance Services Office, Inc. (“ISO”). ISO’s activities are described in Pardee

Construction, 92 Cal. Rptr. 2d at 456 n.15 (internal quotes omitted).

App-4

App-5

App-6

App-7

App-8

App-9

App-10

App-11

App-12

App-13

App-14

App-15

App-16

![[J-92A-E-2019][M.O. - Donohue, J.] IN THE SUPREME COURT OF ... · [j-92a-e-2019][m.o. - donohue, j.] in the supreme court of pennsylvania western district richard thomas walsh, executor](https://img.pdfslide.us/doc/110x75/5f8e071b72c1067c865bf472/j-92a-e-2019mo-donohue-j-in-the-supreme-court-of-j-92a-e-2019mo.jpg)