Embed Size (px)

Citation preview

For Private Circulation Only

Private & Confidential

IMPRESS-Portfolio

Private & Confidential

28th Feb 2018

IMPRESS-Portfolio

nvestments in

ulticap

ortfolio of

ising

nterprises with

ound corporate track record

ustainable business model

For Private Circulation Only

Private & Confidential

IMPRESS-Portfolio Objective & Investment Philosophy

Focus on Return Optimization by investing in multicap

portfolio of rising enterprises with sound corporate track

record and sustainable business model keeping balance

between value and growth strategy.

Objective

Value investing is the art of buying stocks which trade at a significant discount to their

intrinsic value. Portfolio Manager achieve this by looking for companies on cheap valuation metrics,

typically low multiples of their profits or assets, for reasons which are not justified over the longer term .

Growth investing is a style of investment strategy focused on capital appreciation. Portfolio

Manager invest in companies that exhibit signs of above-average growth, even if the share price

appears expensive in terms of metrics such as price-to-earnings or price-to-book ratios.

For Private Circulation Only

Private & Confidential

IMPRESS-Portfolio Why Multicap Strategy

The table shows outperformance of the Mid Cap and Small Cap Index over the Sensex Index during the Bull Period.

Outperformance of the Mid Cap and small caps happens because of better earnings growth in the bull phase.

The P/E for Mid cap and Small Caps also expands as earnings growth is superior v/s Sensex earnings growth.

Identifying the business within attractive valuation compare to their growth is key factor for outperformance.

Returns delivered from Mid Cap and Small Cap do outperform the Large Cap, however one should keep in mind the risk associated with it as we see the higher volatility in it. Therefore we emphasis on stringent stock selection strategy and create a diversified Multicap portfolio to create alpha over the benchmark.

Today’s Small Cap

Small Cap

are tomorrows Mid cap

Mid Cap

Which may eventually

become Large Cap

Large Cap

Apr-03 Dec-07 CAGR Volatility

Sensex 2960 20287 51.0% 22.0%

BSE Mid Cap 952 9789 64.6% 25.0%

BSE Small Cap 893 13348 78.4% 31.6%

Dec-07 Dec-11 CAGR Volatility

Sensex 20287 15455 -6.6% 31.2%

BSE Mid Cap 9789 5135 -14.9% 40.5%

BSE Small Cap 13348 5550 -19.7% 45.4%

Dec-11 Dec-17 CAGR Volatility

Sensex 15455 34057 14.1% 9.0%

BSE Mid Cap 5135 17822 23.0% 12.0%

BSE Small Cap 5550 19231 23.0% 13.5%

Bull Period

Bear Period

Current Bull period

For Private Circulation Only

Private & Confidential

IMPRESS-Portfolio

Business Model either in 1) Improving Market Share 2) Leadership 3) Niche Business Model

Rising Enterprises 1) Stable and Improving Margins 2) Improving ROE and ROCE

Sustainability 1) Visibility of Earnings over next 2-3 years 2) Predictable business model

Sound Corporate Track Record 1) Management back ground 2) Accounting & Corporate policies

Sector opportunity 1) Sector potential to grow 2) Cyclical / Non

Cyclical 3) Favoring Policies

Diversification 1) Sectorally well diversified portfolio of 15-20

stocks across Market Capitalization

Exposure 1) Single Stock exposure < 10% 2) Single Sector exposure < 30%

Stock Selection

Allocation

Investment Process

For Private Circulation Only

Private & Confidential

IMPRESS-Portfolio Top Holdings & Market Cap Allocation

5

The current model client portfolio comprise of 20 stocks. Portfolio is well diversified across market capitalization. We have shown top 3 stocks based on current weightage in each of the market capitalization.

Most of the stocks are given more or less equal and sizable weightage in portfolio

Data as on 28th Feb 2018

Large Cap, 28%

Mid Cap, 49%

Small Cap, 22%

Cash, 1%

Market Cap AllocationSr No Large Cap % Holdings

1 Bharat Forge Ltd. 5.7%

2 Bajaj Finance Ltd. 5.3%

3 Larsen & Toubro Ltd. 4.8%

Sr No Mid Cap % Holdings

1 Finolex Cables Ltd. 6.1%

2 Minda Industries Ltd. 5.9%

3 Aarti Industries Ltd. 5.8%

Sr No Small Cap % Holdings

1 Deepak Nitrite Ltd. 7.6%

2 Ratnamani Metals & Tubes Ltd. 5.7%

3 SH Kelkar & Co Ltd. 5.1%

For Private Circulation Only

Private & Confidential

IMPRESS-Portfolio Diversified Sector

The current portfolio participates

in most of the sectors which are

going to be in fore front of the

growth in the economy.

With positive real interest rates

which is helping to stimulate the

financial savings will in turn provide

stimulus to consumption led

economy.

Most of the company selected

belongs to the sectors which are

also being boosted by the

government reforms such as of

Power, Housing, Clean and Green

India, Digital India, Infrastructure.

etc.

0.0% 5.0% 10.0% 15.0% 20.0%

Chemicals

Financials

Auto & Ancillary

Capital Goods

Consumer Durables

Metal Product

Infrastructure

Plastic Product

Shipping

Power

Textiles

Oil & Gas

Agri Chemical

Sector Allocation

For Private Circulation Only

Private & Confidential

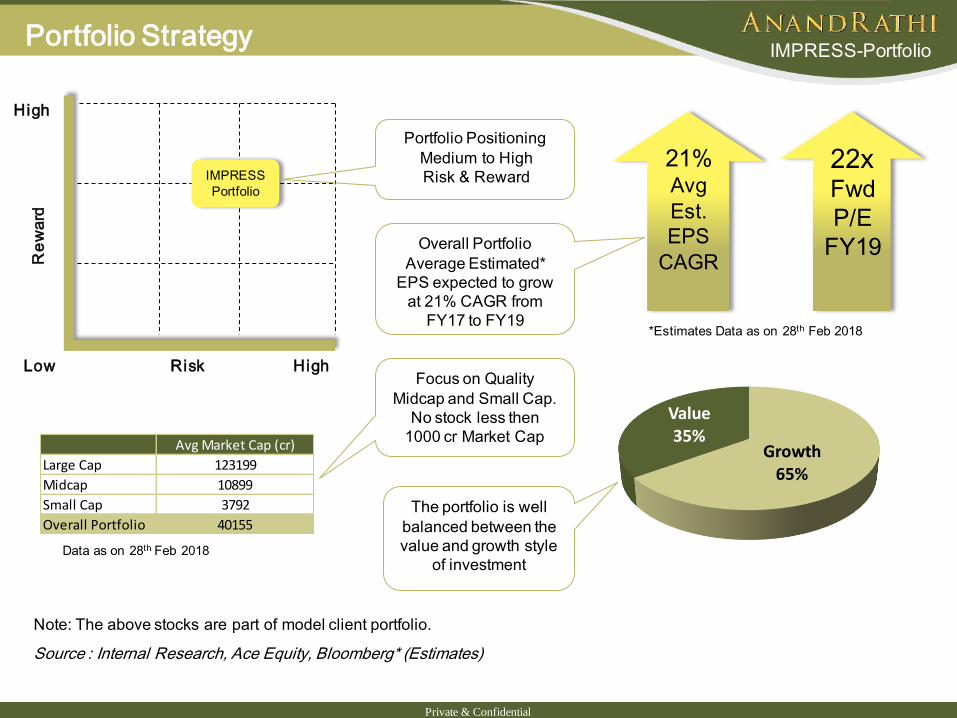

IMPRESS-Portfolio Portfolio Strategy

7 Source : Internal Research, Ace Equity, Bloomberg* (Estimates)

21% Avg

Est.

EPS

CAGR

Growth65%

Value35%

Note: The above stocks are part of model client portfolio.

22x Fwd

P/E

FY19

Risk

Re

wa

rd

Low High

High

IMPRESS

Portfolio

Portfolio Positioning

Medium to High

Risk & Reward

Overall Portfolio

Average Estimated*

EPS expected to grow

at 21% CAGR from

FY17 to FY19

Focus on Quality

Midcap and Small Cap.

No stock less then

1000 cr Market Cap

The portfolio is well

balanced between the

value and growth style

of investment Data as on 28th Feb 2018

*Estimates Data as on 28th Feb 2018

Avg Market Cap (cr)

Large Cap 123199

Midcap 10899

Small Cap 3792

Overall Portfolio 40155

For Private Circulation Only

Private & Confidential

IMPRESS-Portfolio Portfolio Performance

8 Note: Performance is net of all expenses of the initial client based on Flat Fee Model.

Disclaimer: Past Performance is not necessarily indicative of likely future performance

2.5%

7.7%

15.2%14.0%

1.2%

6.5%

10.9% 11.20%

0%

4%

8%

12%

16%

20%

3 Month 6 Month 9 Month Since Inception (31st May 2017)

Absolute Performance as on 28th Feb 2018

IMPRESS Portfolio NIFTY 500

For Private Circulation Only

Private & Confidential

IMPRESS-Portfolio Supreme Industries Ltd.

Supreme Industries Limited (SI), founded in 1942 is India's leading polymers and resins processing company offering wide range of plastic products. The company operates in various product categories viz. Plastic Piping System, Cross Laminated Films & Products, Protective Packaging Products, Industrial Molded Components, Molded Furniture, Storage & Material Handling Products, Performance Packaging Films & Composite LPG Cylinders.

Supreme Industries has 25 technologically advanced manufacturing facilities located at various places spread across the country and a distribution network of over 2,800 channel partners.

The company currently has a diversified product portfolio with established brand equity along with significant market share in each of its business verticals.

The company has also 29.99% stake in Supreme Petrochem Ltd which is into manufacturing of Polystyrene, Expanded Polystyrene (normal and cup grade), Extruded Polystyrene Insulation Boards, Compounds of Polyolefins products.

Going ahead, the company intends to increase its contribution from value added products to around 40% or more of its total revenues through focusing on technological innovations and designs. The value added products generally has margins of more than 17% for the company which should help increase margins for the company.

The company plans to incur capex of around 400 to 450 crore in FY-18 on setting up greenfield plants in South India, North-East India and Rajasthan while augmenting its capacities at existing facilities in the country. The company has planned to fund this expenditure with internal accruals. The management has also provided revenue guidance for the next financial year at between Rs.5,200 to Rs.5,500 crore.

Outlook: The company’s primary driver is increased volumes through wider and deeper penetration across the country supported by addition of timely manufacturing capacities. The company plans to achieve 7 lakh ton per year installed capacity by FY-21. Currently the company is undergoing expansion of its plastic piping, protective packaging and furniture units.

Key Holdings

For Private Circulation Only

Private & Confidential

IMPRESS-Portfolio COCHIN SHIPYARD

Cochin Shipyard (CSL), a public sector enterprise, is one of the most stable companies in the Indian shipbuilding and ship repair sector. The company caters to the clients engaged in the defence sector in India along with clients engaged in the commercial sector worldwide. In addition to

shipbuilding, ship repair, CSL also offers marine engineering training. The company’s Indian clients

include the Indian Navy, the Indian Coast Guard, SCI, ONGC, DGLL, DCI, etc, while foreign clients include NPCC, the Clipper Group, Vroon and Sigba AS

Over the years, CSL has emerged as a premier player in the Indian shipbuilding segment with expertise in design, engineering and project implementation. CSL is also a market leader with a market share of ~39% and has undertaken repairs of most complex ships of the country. As on FY17, shipbuilding constitutes 74% of the topline while ship repair comprises the remaining 26%.

Even during turbulent times in the global shipbuilding history, it has delivered topline, bottom line growth of 11.1%, 18.7% CAGR, respectively, in FY07-17. CSL has a strong balance sheet with debt of Rs 123 crore and cash of Rs 1,600 crore.

CSL is consciously improving its business mix by increasing the share of ship-repairs orders (2x profitable than shipbuilding business) in its order book. Better business mix coupled with strong bidding pipeline of over ~Rs 11,900 crore augur well for the company. Currently, CSL has a healthy order book of RS 2,856 crore plus L1 status of Rs 5400 crore. It is also likely to receive order for phase III of IAC, which is likely to be ~Rs 10,900 crore. We believe these orders give strong revenue visibility to CSL till FY23.

Outlook: CSL’s has strong order book and bidding pipeline, core competency in both shipbuilding & ship repair (specially defence), debt-free status, best-in-class working capital cycle, reliability in execution and being a natural beneficiary of large & critical government projects. Hence Buying for long term

10

For Private Circulation Only

Private & Confidential

IMPRESS-Portfolio

SH KELKAR & CO

SH Kelkar Limited (SHK), incorporated in 1922 as a manufacturer of industrial perfumes is currently India’s largest Fragrance & Flavor company aiming to be a significant domestic and international player. The company’s businesses are primarily spread across three segments Fragrances & Aroma Ingredients, Flavours, and Services of which Fragrance business is the primary contributor to revenues .

SHK is the fourth largest company with a market share of 12% in Indian fragrance & flavour

industry and is the only Indian company having a market share of more than 1% in the

segment. The other larger competitors are five MNC companies having a combined market share of ~60% within them.

Over the years, it has developed a library of 680 flavors categorized under the natural, nature-identical or artificial head sand available in liquid, drymix, emulsion and encapsulated forms. SHK’s R&D team synthesized 128 new molecules in FY16. It has also patented its first molecule listed in U.S. during the year .

Going ahead the company aims to Focus on retaining current domestic market leadership and enhancing market share in fragrance industry in India and emerging markets, introduce new products, strengthen innovation platform to enhance products portfolio, expand presence in the branded small pack portfolio

The Indian F&F industry is expected to continue to grow at a round10% CAGR upto 2020 along with consolidation of market share towards larger players from smaller ones.

Outlook: We believe SHK presents a unique opportunity for investors to take part in this growing segment in medium to long term. The company is currently operating at a 45% utilization levels and is expected to witness improvement in profitability margins going ahead as utilization levels improve. It is also to be noted that every 15% increase in utilizations could increase its revenues by around 100%. Hence Buying for Long Term

11

For Private Circulation Only

Private & Confidential

IMPRESS-Portfolio Founder & Promoter (Anand Rathi Group)

One of the leading financial and investment experts in India and South-east Asia, Mr. Anand Rathi on

acquiring a Chartered Accountancy qualification had a long, successful and illustrious career of over 40 years as a core member of the legendary late Mr. Aditya Birla’s business group. He was actively involved

in all strategic initiatives, being instrumental in shaping the group’s cement business, and spearheaded its

foray into diverse businesses in manufacturing and services.

In 1999 as the President of BSE, he was the driving force behind the expansion of BOLT, the BSE Online Trading System. He also set up the Trade Guarantee Fund and played a vital role in setting up the Central

Depository Services (CDS).

A respected member of the ICAI, he is popular among chartered accountants and finance professionals as

also public life in general because of his active philanthropy and Corporate Social Responsibility (CSR) initiatives. These include training and career opportunities to bright young professionals.

Anand Rathi Founder & Chairman

Pradeep Gupta Co Founder &

Vice Chairman

Mr. Gupta brings with him long experience of setting up and running a variety of business enterprises. His

first exposure was in the family-owned textiles business, however is passion for financial markets led to his

starting Navratan Capital & Securities Pvt. Ltd, later merged with Anand Rathi Financial Services.

At AnandRathi, he has played a pivotal role in laying the foundation of the Institutional Broking and

Investment Services arms of the group. His ground-breaking spirit has helped the firm to rapidly expanding

its footprint and emerge as a leading capital market player in the country.

He has been instrumental in leading the group to bag prestigious accolades and often appears in the media,

sharing his views and insights on macro-economic aspects.

He is also an active member of the Rotary Club of Bombay.

For Private Circulation Only

Private & Confidential

IMPRESS-Portfolio Fund Management Team

Mayur Shah - Fund Manager

More than 12 years of rich experience in Investment advisory, Product Development

and Portfolio Management

Working with Anand Rathi since 2007 across Portfolio Management and Private

Client Group Equity Advisory

Started Career with “Kotak Securities Ltd” in 2005 as an Investment Advisor

subsequently got into developing Equity products and running the same

Qualified MBA (Finance) from Mumbai University and Certified Financial Planner

Vinod Vaya

More than 12 years of rich experience in Investment advisory, Portfolio Management

and research

Worked in past with Standard Chartered Securities, Religare Securities, Enam

Securities.

PGDBM from Mumbai

For Private Circulation Only

Private & Confidential

IMPRESS-Portfolio Product Features

Minimum investment

Portfolio:

Themes offered

Type of instruments

Benchmark

Fund Manager

Rs. 25 lakhs.

15-20 STOCKS, diversified across sectors.

Multicap – Spread between Small, Mid and Large Cap

Multicap Portfolio - Balanced between Value and Growth

Most of the companies have adequate analyst coverage.

Most of the stocks will be part of core portfolio.

Equity & Equity Related Instruments, Fixed Income

Instruments, Cash & Cash Equivalent

NIFTY 500

Mayur Shah

Benefits

• Dedicated Web Login for client to monitor portfolio.

• A relationship manager to cater to investment needs

• Constant monitoring of the portfolio

• Audited statement at year end for tax filing purpose.

Support

Back office customer service desk to address client queries.

Name : Vinod Vaya

Tel : 022 – 4001 3947

Email ID : [email protected]

Product Support

Name : Archana Bhor

Tel : 022 – 4001 3878

E-MAIL : [email protected]

Back Office Support

For Private Circulation Only

Private & Confidential

IMPRESS-Portfolio

PMS registered under : Anand Rathi Advisors Ltd.

PMS Registration Number : INP00000282.

Custodian : IL&FS Securities Services Ltd.

OFFICIAL ADDRESS : 4 th Floor , Silver Metropolis, Jaicoach Compound Opposite Bimbisar Nagar,

Goregaon(East), Mumbai - 400 063. India

BOARD LINES : +91 22 4001 3700

All Investment are subject to Market Risk.

Please read the risk factors before investing in the same.

Past Performance is not necessarily indicative of likely future performance

Specific Disclaimer

Registration Details

Disclaimer & Registration Details

For Private Circulation Only

Private & Confidential

IMPRESS-Portfolio

Private & Confidential

Disclaimer:-This report has been issued by Anand Rathi Advisors Limited (ARAL), which is regulated by SEBI. The information herein was obtained from various sources; we do not guarantee its accuracy or completeness. Neither the information nor any opinion expressed constitutes an offer, or an invitation to make an offer, to buy or sell any securities or any options, futures or other derivatives related to such securities ("related investments"). ARAL and its affiliates may trade for their own accounts as market maker / jobber and/or arbitrageur in any securities of this issuer(s) or in related investments, and may be on the opposite side of public orders. ARAL, its affiliates, directors, officers, and employees may have a long or short position in any securities of this issuer(s) or in related investments. ARAL or its affiliates may from time to time perform investment banking or other services for, or solicit investment banking or other business from, any entity mentioned in this report. This research report is prepared for private circulation. It does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. Investors should seek financial advice regarding the appropriateness of investing in any securities or investment strategies discussed or recommended in this report and should understand that statements regarding future prospects may not be realized. Investors should note that income from such securities, if any, may fluctuate and that each security's price or value may rise or fall. Past performance is not necessarily a guide to future performance. Foreign currency rates of exchange may adversely affect the value, price or income of any security or related investment mentioned in this report.