Embed Size (px)

Citation preview

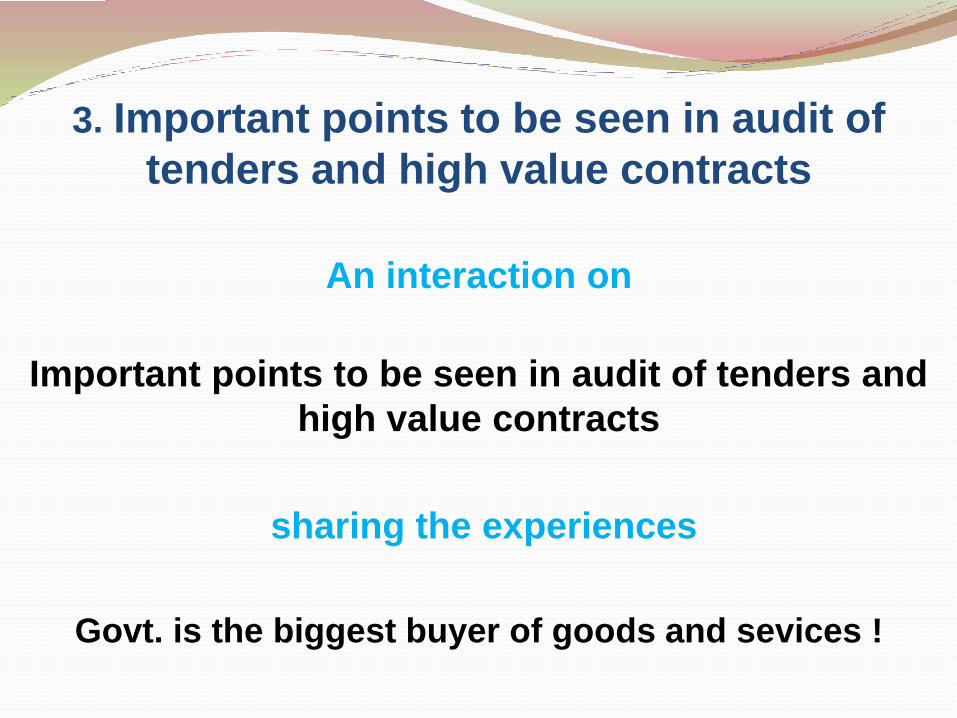

3. Important points to be seen in audit of

tenders and high value contracts

An interaction on

Important points to be seen in audit of tenders and

high value contracts

sharing the experiences

Govt. is the biggest buyer of goods and sevices !

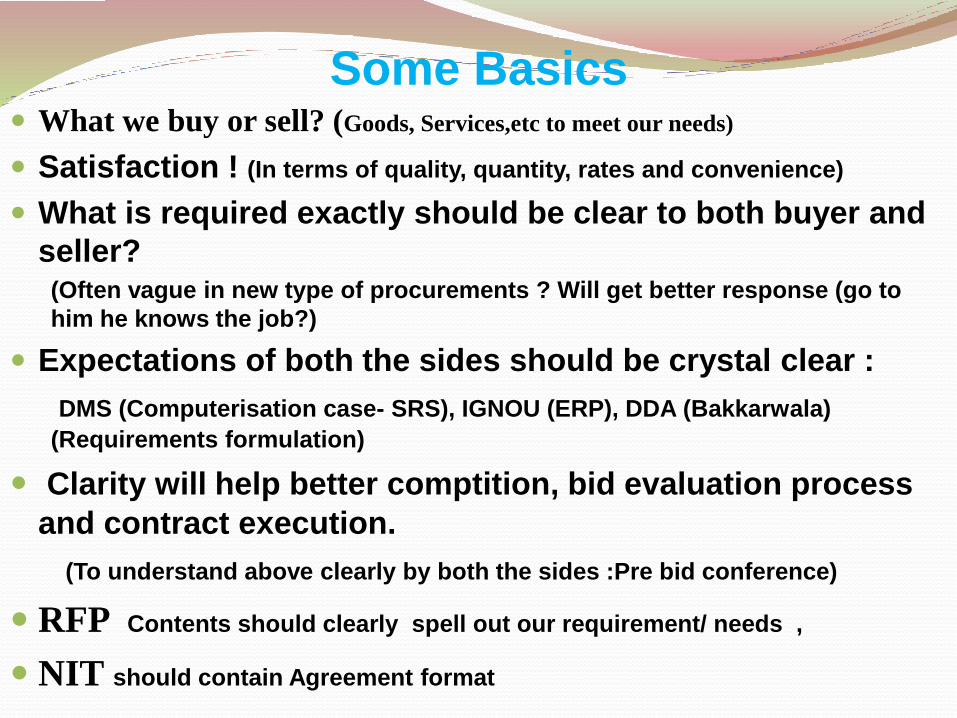

Some Basics What we buy or sell? (Goods, Services,etc to meet our needs)

Satisfaction ! (In terms of quality, quantity, rates and convenience)

What is required exactly should be clear to both buyer and

seller? (Often vague in new type of procurements ? Will get better response (go to

him he knows the job?)

Expectations of both the sides should be crystal clear :

DMS (Computerisation case- SRS), IGNOU (ERP), DDA (Bakkarwala)

(Requirements formulation)

Clarity will help better comptition, bid evaluation process

and contract execution.

(To understand above clearly by both the sides :Pre bid conference)

RFP Contents should clearly spell out our requirement/ needs ,

NIT should contain Agreement format

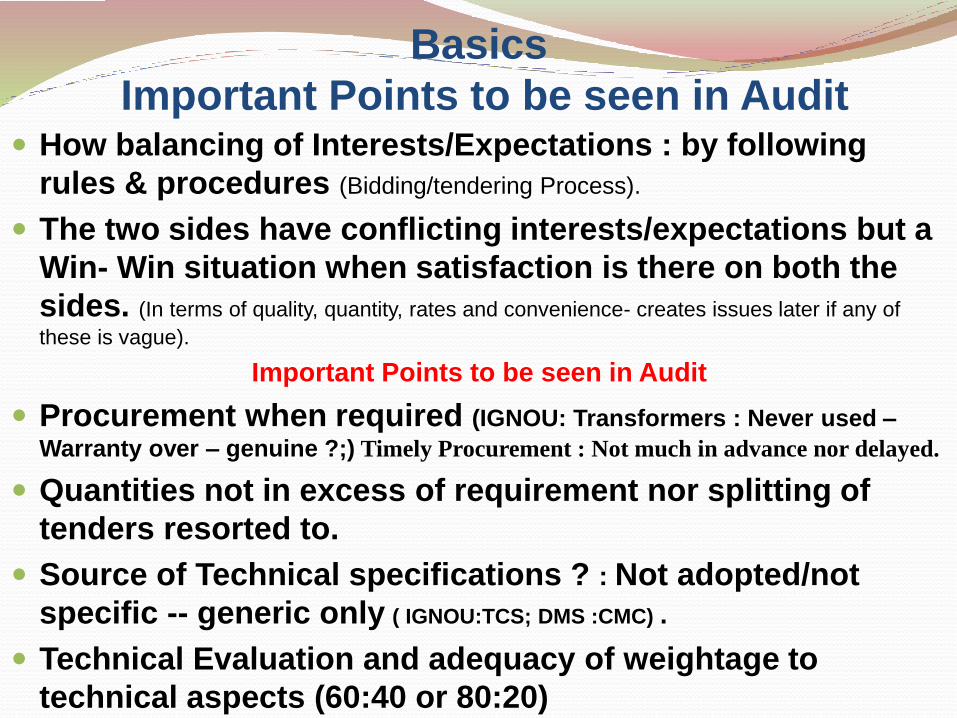

Basics

Important Points to be seen in Audit How balancing of Interests/Expectations : by following

rules & procedures (Bidding/tendering Process).

The two sides have conflicting interests/expectations but a

Win- Win situation when satisfaction is there on both the

sides. (In terms of quality, quantity, rates and convenience- creates issues later if any of

these is vague).

Important Points to be seen in Audit

Procurement when required (IGNOU: Transformers : Never used –

Warranty over – genuine ?;) Timely Procurement : Not much in advance nor delayed.

Quantities not in excess of requirement nor splitting of

tenders resorted to.

Source of Technical specifications ? : Not adopted/not

specific -- generic only ( IGNOU:TCS; DMS :CMC) .

Technical Evaluation and adequacy of weightage to

technical aspects (60:40 or 80:20)

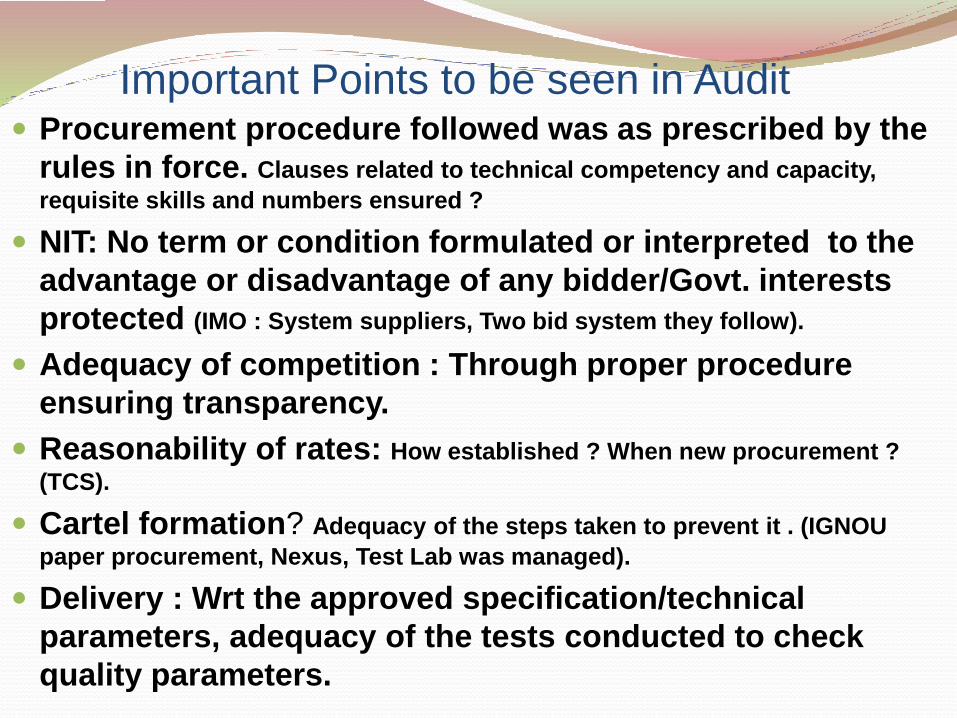

Important Points to be seen in Audit Procurement procedure followed was as prescribed by the

rules in force. Clauses related to technical competency and capacity,

requisite skills and numbers ensured ?

NIT: No term or condition formulated or interpreted to the

advantage or disadvantage of any bidder/Govt. interests

protected (IMO : System suppliers, Two bid system they follow).

Adequacy of competition : Through proper procedure

ensuring transparency.

Reasonability of rates: How established ? When new procurement ?

(TCS).

Cartel formation? Adequacy of the steps taken to prevent it . (IGNOU

paper procurement, Nexus, Test Lab was managed).

Delivery : Wrt the approved specification/technical

parameters, adequacy of the tests conducted to check

quality parameters.

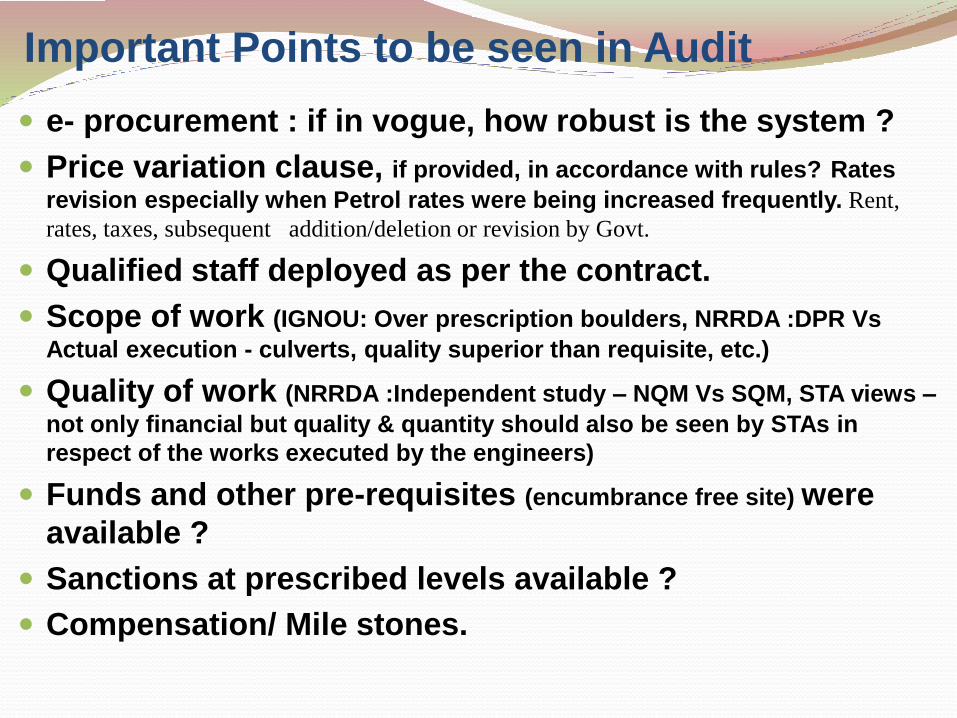

Important Points to be seen in Audit

e- procurement : if in vogue, how robust is the system ?

Price variation clause, if provided, in accordance with rules? Rates

revision especially when Petrol rates were being increased frequently. Rent,

rates, taxes, subsequent addition/deletion or revision by Govt.

Qualified staff deployed as per the contract.

Scope of work (IGNOU: Over prescription boulders, NRRDA :DPR Vs

Actual execution - culverts, quality superior than requisite, etc.)

Quality of work (NRRDA :Independent study – NQM Vs SQM, STA views –

not only financial but quality & quantity should also be seen by STAs in

respect of the works executed by the engineers)

Funds and other pre-requisites (encumbrance free site) were

available ?

Sanctions at prescribed levels available ?

Compensation/ Mile stones.

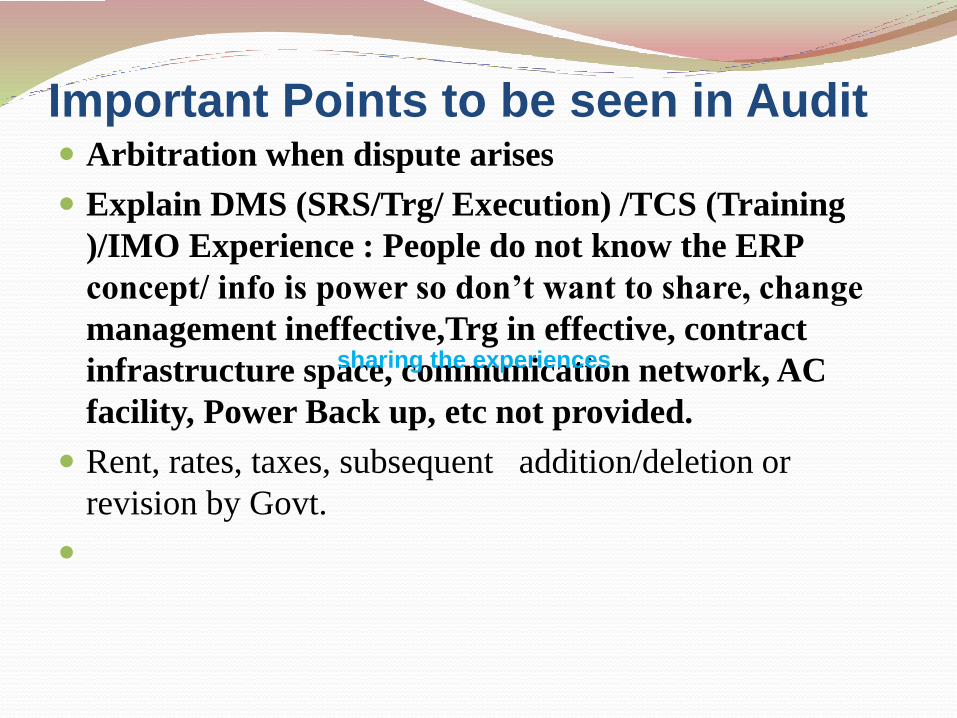

Important Points to be seen in Audit Arbitration when dispute arises

Explain DMS (SRS/Trg/ Execution) /TCS (Training

)/IMO Experience : People do not know the ERP

concept/ info is power so don’t want to share, change

management ineffective,Trg in effective, contract

infrastructure space, communication network, AC

facility, Power Back up, etc not provided.

Rent, rates, taxes, subsequent addition/deletion or

revision by Govt.

sharing the experiences

Thanks

An interaction on works procurement

and execution – sharing the experiences

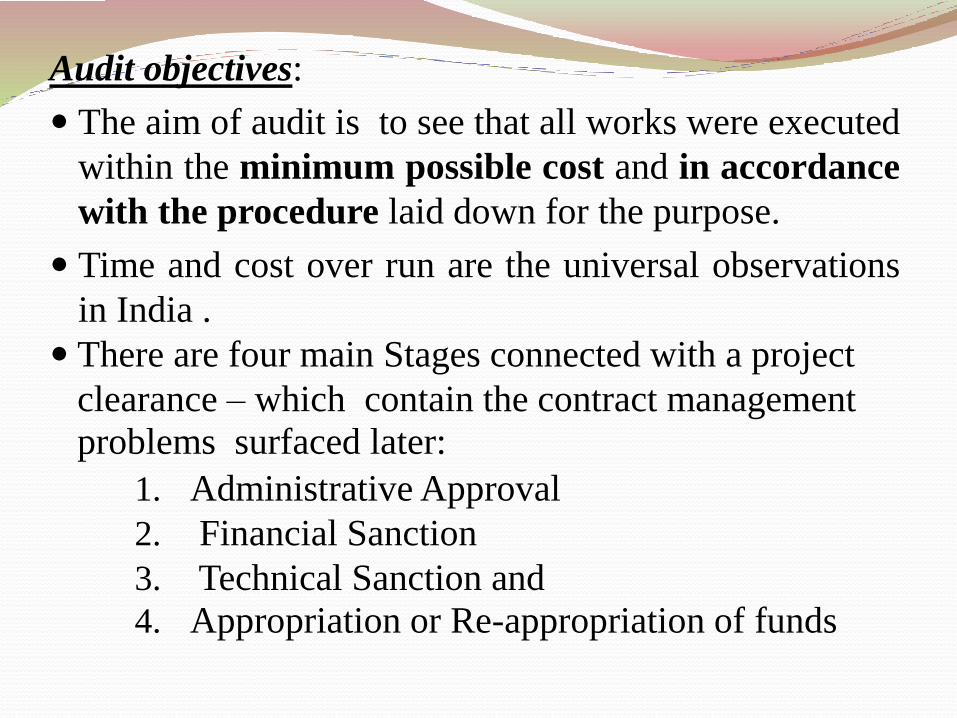

Audit objectives:

The aim of audit is to see that all works were executed

within the minimum possible cost and in accordance

with the procedure laid down for the purpose.

Time and cost over run are the universal observations

in India .

There are four main Stages connected with a project

clearance – which contain the contract management

problems surfaced later:

1. Administrative Approval

2. Financial Sanction

3. Technical Sanction and

4. Appropriation or Re-appropriation of funds

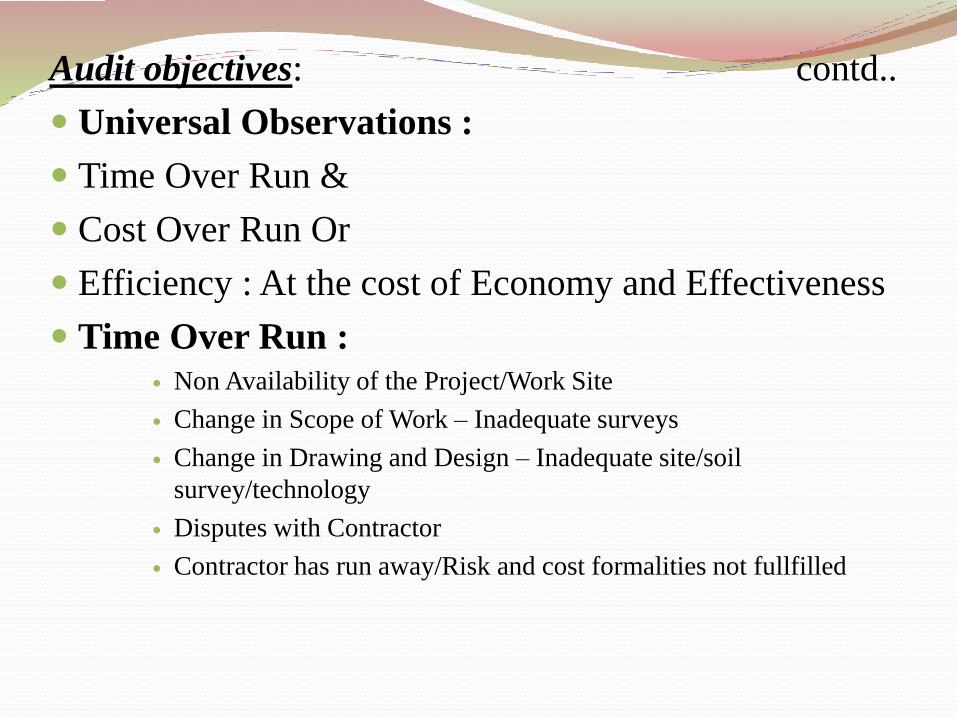

Audit objectives: contd..

Universal Observations :

Time Over Run &

Cost Over Run Or

Efficiency : At the cost of Economy and Effectiveness

Time Over Run : Non Availability of the Project/Work Site

Change in Scope of Work – Inadequate surveys

Change in Drawing and Design – Inadequate site/soil

survey/technology

Disputes with Contractor

Contractor has run away/Risk and cost formalities not fullfilled

Cost Over Run:

Adequate contractual Capacity not available in

the State

Adequate competition not generated :e-

procurement/tendering

Time Over Run

Disputes with Contractor : Arbitration

Turn key Projects :Defective agreements

Minimum possible cost:

Administrative approval (A/A): Necessity for the

work by the administrative department (Air

strip) . An approximate estimate and necessary

preliminary plans (land availability), Technical

estimate for the work to be prepared in advance.

Design and Drawing: To be based on proper field and site

surveys, necessary investigations (seldom found/normally

noticed at the execution stage in the form of large

deviations/variations in scope of work/quantities)

Road alignments based on transact walk (normally

dispute with forest department/land owners)

Proper soil survey in works (building , dams, canals

which do not come up timely or never used or

breached or washed away)

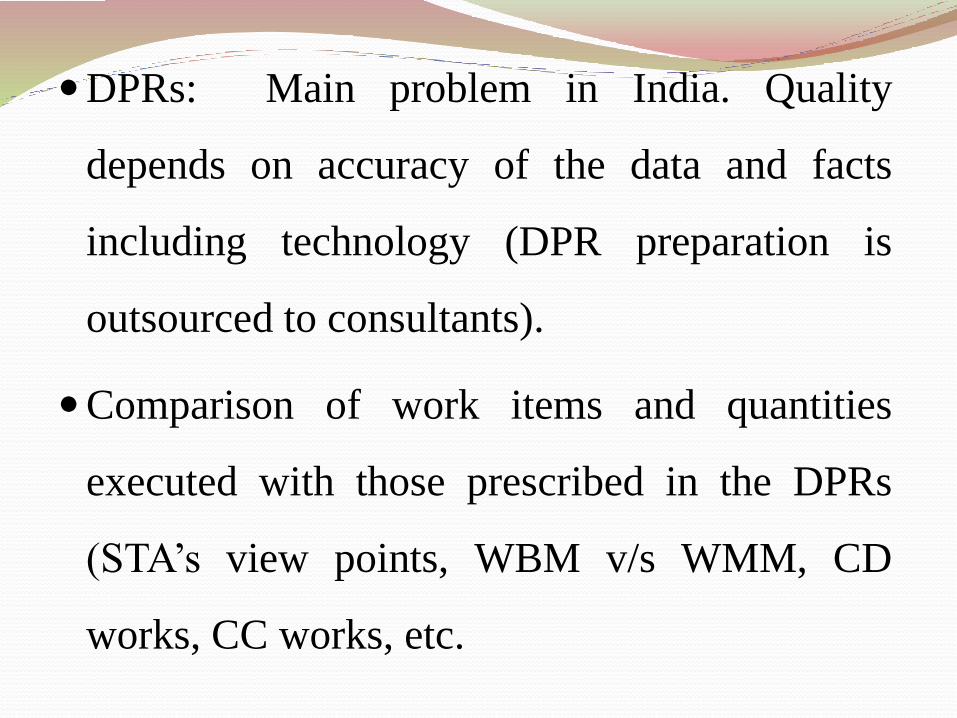

DPRs: Main problem in India. Quality

depends on accuracy of the data and facts

including technology (DPR preparation is

outsourced to consultants).

Comparison of work items and quantities

executed with those prescribed in the DPRs

(STA’s view points, WBM v/s WMM, CD

works, CC works, etc.

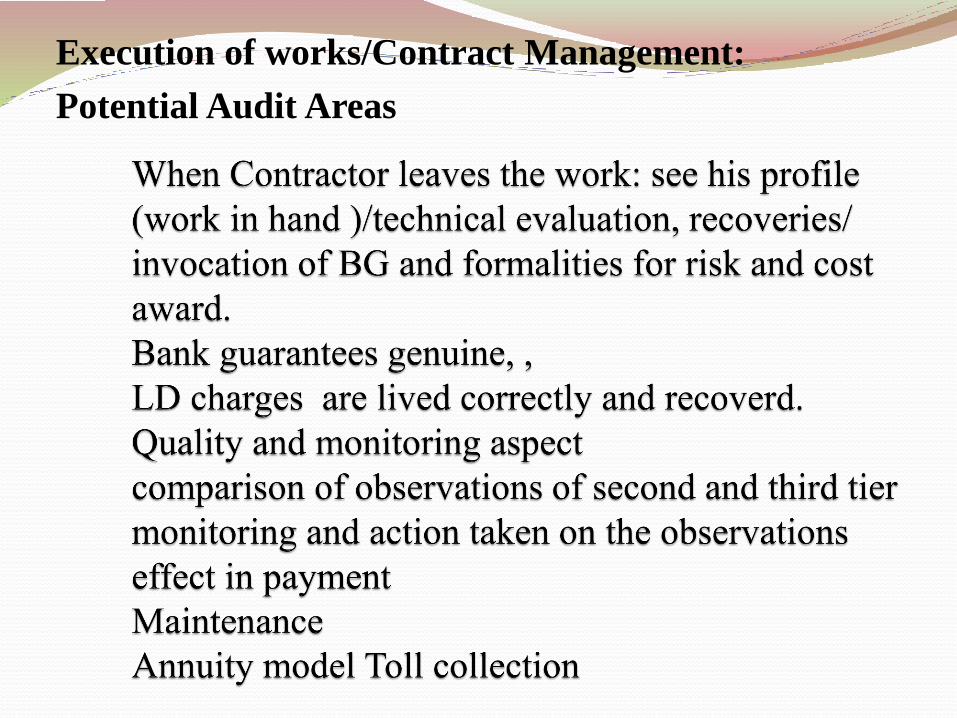

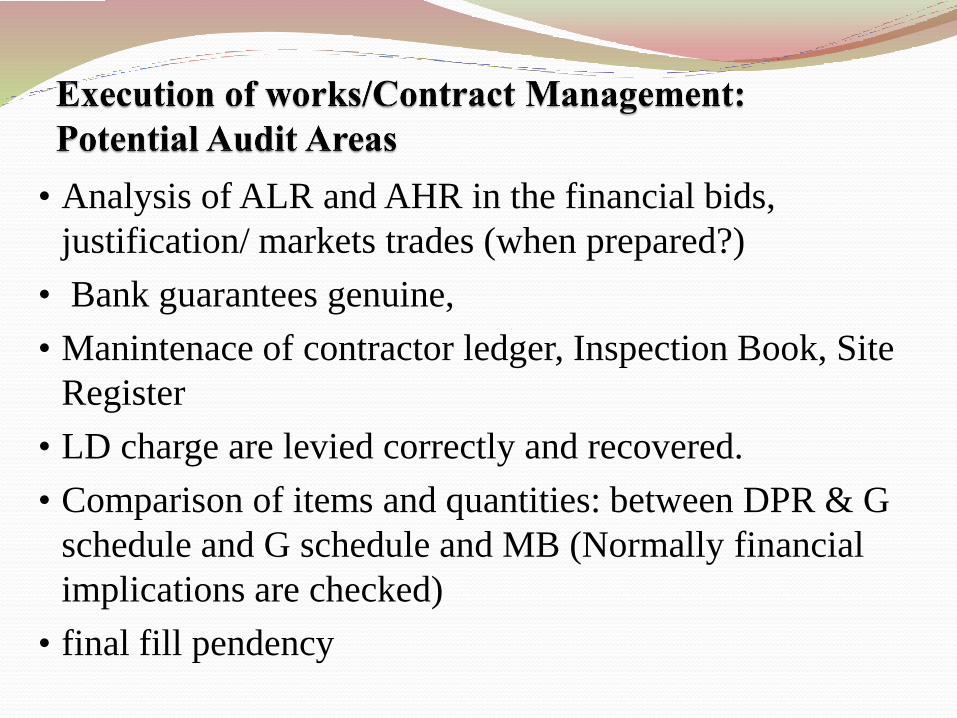

Execution of works/Contract Management:

Potential Audit Areas

• Analysis of ALR and AHR in the financial bids,

justification/ markets trades (when prepared?)

• Bank guarantees genuine,

• Manintenace of contractor ledger, Inspection Book, Site

Register

• LD charge are levied correctly and recovered.

• Comparison of items and quantities: between DPR & G

schedule and G schedule and MB (Normally financial

implications are checked)

• final fill pendency

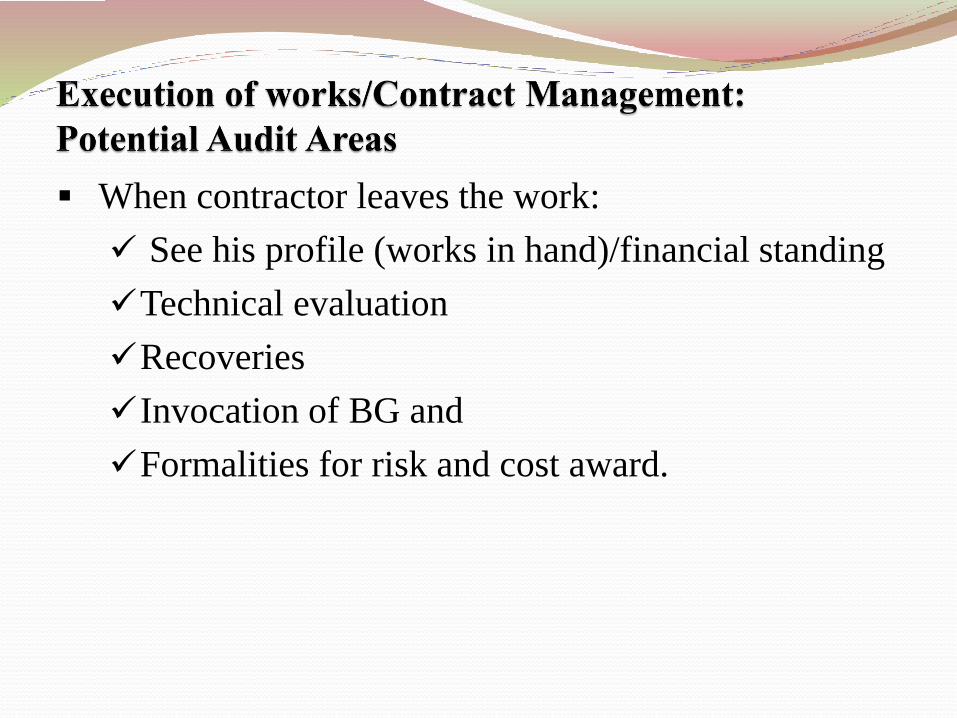

When contractor leaves the work:

See his profile (works in hand)/financial standing

Technical evaluation

Recoveries

Invocation of BG and

Formalities for risk and cost award.

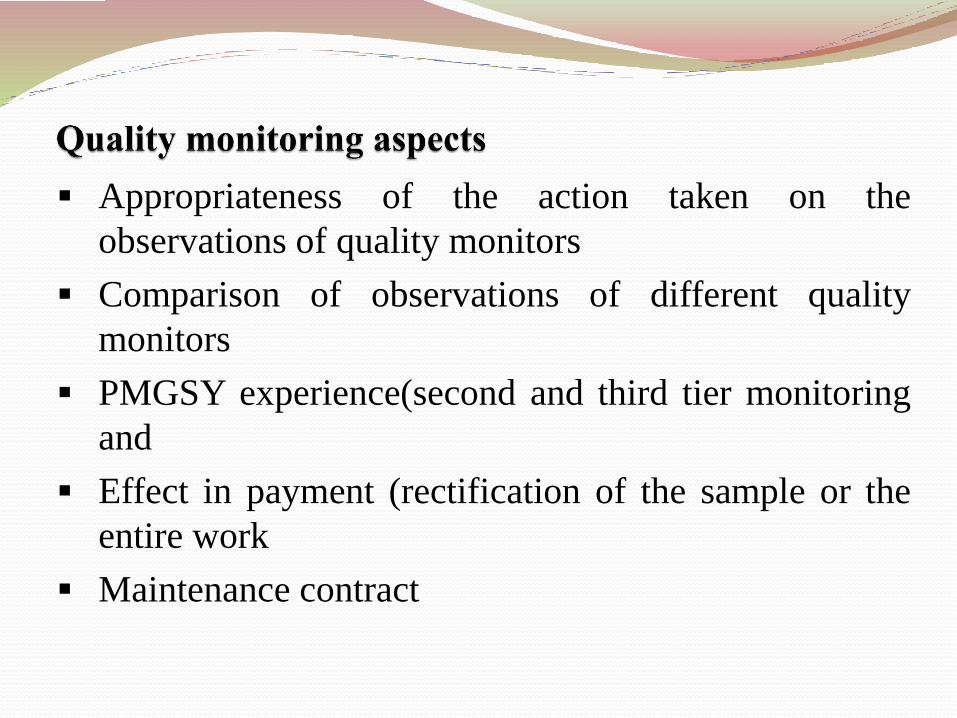

Appropriateness of the action taken on the

observations of quality monitors

Comparison of observations of different quality

monitors

PMGSY experience(second and third tier monitoring

and

Effect in payment (rectification of the sample or the

entire work

Maintenance contract

PPP New ways of Financing:

Huge infrasture being created

their subsequent Maintenance and

Renewal

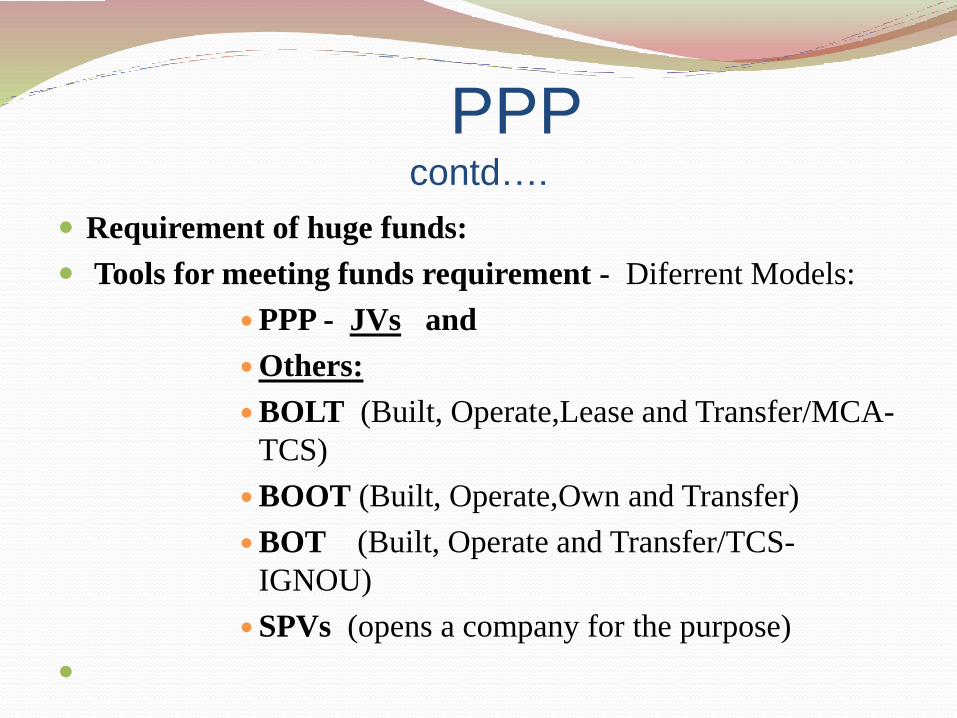

PPP contd….

Requirement of huge funds:

Tools for meeting funds requirement - Diferrent Models:

PPP - JVs and

Others:

BOLT (Built, Operate,Lease and Transfer/MCA-

TCS)

BOOT (Built, Operate,Own and Transfer)

BOT (Built, Operate and Transfer/TCS-

IGNOU)

SPVs (opens a company for the purpose)

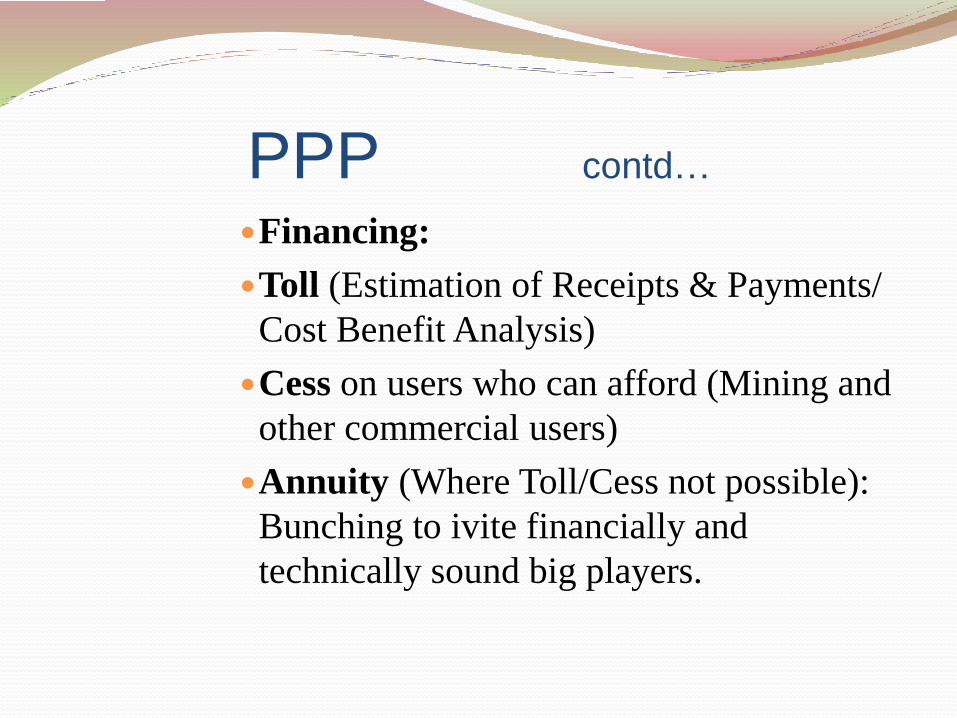

PPP contd…

Financing:

Toll (Estimation of Receipts & Payments/

Cost Benefit Analysis)

Cess on users who can afford (Mining and

other commercial users)

Annuity (Where Toll/Cess not possible):

Bunching to ivite financially and

technically sound big players.

Thank you

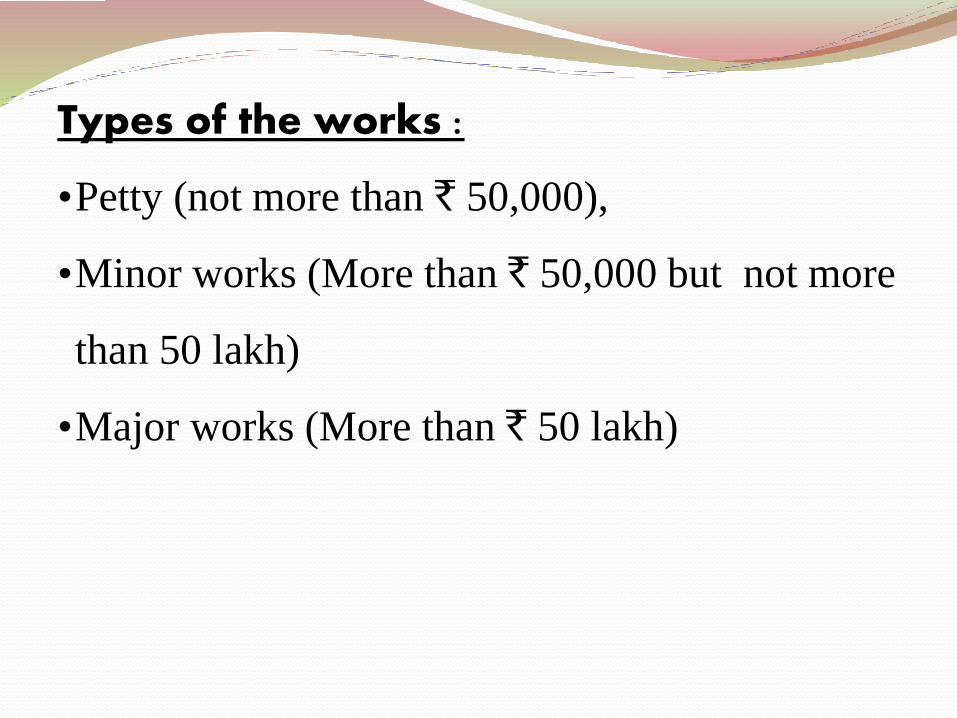

Types of the works :

•Petty (not more than ` 50,000),

•Minor works (More than ` 50,000 but not more

than 50 lakh)

•Major works (More than ` 50 lakh)

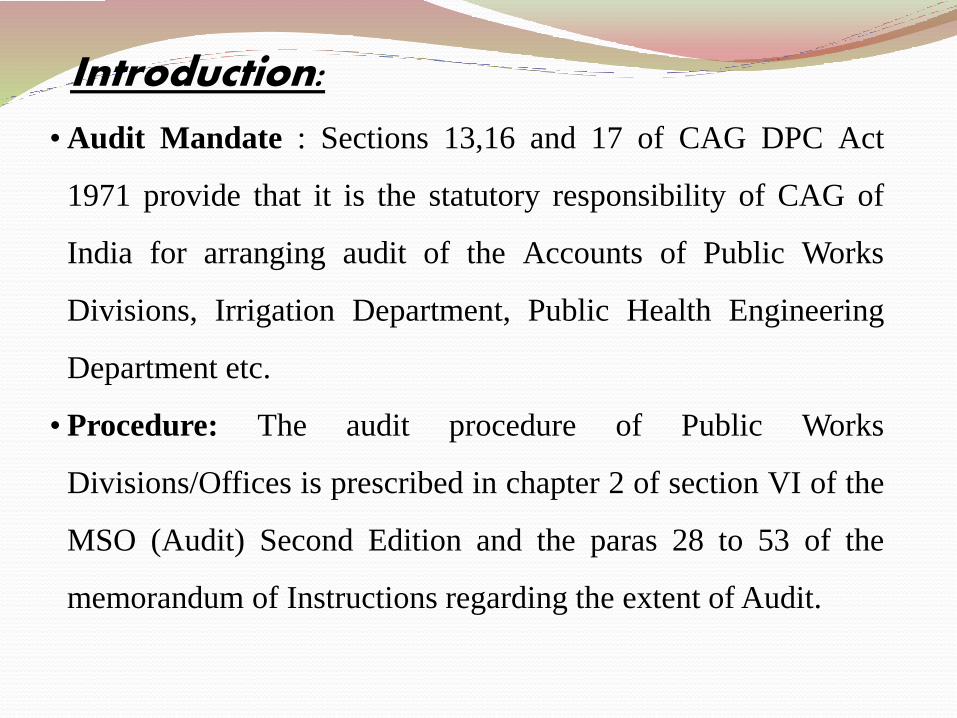

Introduction:

• Audit Mandate : Sections 13,16 and 17 of CAG DPC Act

1971 provide that it is the statutory responsibility of CAG of

India for arranging audit of the Accounts of Public Works

Divisions, Irrigation Department, Public Health Engineering

Department etc.

• Procedure: The audit procedure of Public Works

Divisions/Offices is prescribed in chapter 2 of section VI of the

MSO (Audit) Second Edition and the paras 28 to 53 of the

memorandum of Instructions regarding the extent of Audit.