Embed Size (px)

Citation preview

KU Leuven – Instituut voor de Overheid – Public Management Institute

Parkstraat 45 bus 3609 – B-3000 Leuven – Belgium

Tel: 0032 16 32 32 70 – Fax: 0032 16 32 32 67

[email protected] – www.instituutvoordeoverheid.be – www.publicmanagementinstitute.be

Financial management change in local governments:

empirical testing of a model

Paper for the 2012 EGPA Annual Conference

PSG XII: Public Sector Accounting and Financial Management

Leuven, Belgium

25/07/2012

Elke DEMEULENAERE, Katrien WEETS1 and Geert BOUCKAERT

KU Leuven – Public Management Institute2

1 The research findings outlined in this paper are based on the doctoral dissertation of Katrien Weets.

2 This text is based on research conducted within the frame of the Policy Research Centre on Governmental

organization in Flanders (SBOV II - 2007-2011), funded by the Flemish government. The views expressed herein

are those of the author(s) and not those of the Flemish government.

Financial management change: empirical testing of a model

KU Leuven – Public Management Institute 2

Abstract

Since the nineties and in line with international public sector changes, Flemish local governments

have been experiencing the push towards results-oriented public management. Essentially, local

governments’ performance is at stake and its improvement is assumed to benefit citizens. To this

end, results-oriented financial management is considered to be crucial. As such, the current research

project focuses on the integration of performance information in local governments’ financial cycle

and on the factors that facilitate this integration. This paper reports on the first endeavour in this

direction, namely the introduction of performance budgeting. More specifically, based on a large

scale survey, the extent to which Flemish municipalities have introduced (elements of) performance

budgeting is mapped. In this paper we especially want to elaborate on the case study in which the

explanatory power of the model of ter Bogt & van Helden (2000) on accounting change is explored.

This leads to an adapted and refined conceptual model and allows for the formulation of policy

recommendations. Moreover, it sets the ground for further research.

Research objectives 1

Integrating performance information in the financial cycle can be understood as a three-step

mechanism of measuring, incorporating and using performance information (Bouckaert and Halligan,

2008) in budgeting, accounting and auditing. Ideally, this integration realizes or follows from a strong

connection with the policy cycle (namely planning, monitoring an evaluating). Figure 1 visualizes the

three-step integration of performance information in both the financial and policy cycle. The

performance-oriented financial management system that would ideally follow from such an

integration, fits the ambitions of the financial and accounting dimension of New Public Management

(Hood, 1991), also labelled as New Public Financial Management (Guthrie, Olson and Humphrey,

1999).

This conceptualization of performance-oriented financial management gives away the scope and

ambitions of our research project with regard to local governments’ performance. However, this

paper will be confined to the results of a first research undertaking in this matter, namely the state of

the art of performance budgeting in Flemish municipalities and of the factors influencing this

practice. Of course, this mainly relates to the first phase of the policy and financial cycle: planning

and budgeting. Moreover, within the context of planning and budgeting, especially measurement

and incorporation of performance information is examined. This implies that the actual use of

Financial management change: empirical testing of a model

KU Leuven – Public Management Institute 3

performance information does not belong to the primary objectives of the research described here.

However, future research endeavours could address this use, not only concerning planning and

budgeting, but also regarding the second phase (monitoring and accounting) and third phase

(evaluating and auditing activities) of both the policy and financial cycle. Ultimately, when the field

has fully implemented these activities, the short-term impact and long-term effect of these practices

should be scrutinized.

PLANNING&

BUDGETING

MONITORING

&ACCOUNTING

EVALUATING&

AUDITING

Measuring

performance

information

Incorporating

performance

information

Using

performance

information

Figure 1 Integrating (measuring, incorporating and using) performance information in the financial cycle

(budgeting, accounting and auditing) and policy cycle (planning, monitoring and evaluating)

Performance budgeting in Flemish municipalities 2

This paper focuses on the practice of planning and budgeting and their interrelationship in Flemish

municipalities. Though performance budgeting has been defined in various ways to refer to similar or

various practices (Joyce & Sieg, 2000:3), there is a general agreement in literature that, increasingly,

performance is integrated in the budgeting practices of public organisations, though to different

degrees and in different ways (e.g. Guthrie et al. 1999; Pollitt & Bouckaert 2004). Globally speaking,

the practice of performance budgeting is described in three separate ways: (1) in a broad sense, it is

the supply of information in the budget document explaining what the organisation has done or

expects to do with the money put at her disposal (e.g. Jordan & Hackbart, 1999:69; Van Reeth, 2002;

Melkers & Willoughby, 1998:66); (2) in a narrow sense, it refers to a budget in which every increase

of resources is explicitly coupled to an increase in the number of products or services (e.g. Robinson

& Brumby, 2005:5; Young, 2003:12; Snell & Hayes, 1993:1; Garsombke & Schrad, 1999:9; Epstein,

1984:2). The allocation and financing aspect is essential to this view; (3) finally, according to the last

position, performance budgeting can be understood both in a broad and narrow sense, and sorted

Financial management change: empirical testing of a model

KU Leuven – Public Management Institute 4

into several ‘categories of performance budgeting’ (e.g. Schick, 2003:101-102; Shah & Shen,

2007:153; OECD, 2007;21-22).

Because relevant regulation at the time of the data collection was mainly confined to stipulations

concerning the integration of policy goals in the budget and their connection with budget allocations,

performance budgeting is understood in the broad sense described above. To picture to what extent

this has been introduced in the Flemish municipalities, a survey was carried out between November

2008 and February 2009. Labelled as “Management and Innovation in Local Governments”, it was

addressed to all municipal treasurers (n=308) and resulted in a response rate of 80% that appeared

to be representative to the population of Flemish municipalities (both regarding the geographical

spread and the scale of resident population). A full discussion of this survey is outside the scope of

this paper. Below, we confine ourselves to a summary.

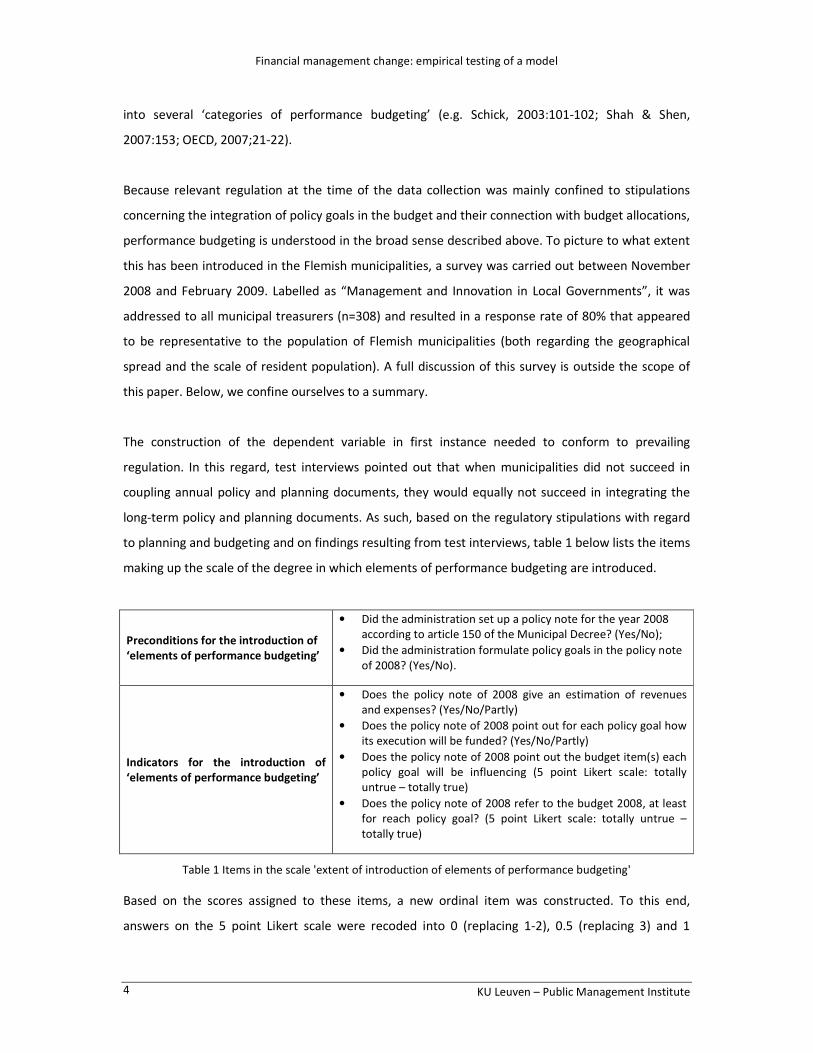

The construction of the dependent variable in first instance needed to conform to prevailing

regulation. In this regard, test interviews pointed out that when municipalities did not succeed in

coupling annual policy and planning documents, they would equally not succeed in integrating the

long-term policy and planning documents. As such, based on the regulatory stipulations with regard

to planning and budgeting and on findings resulting from test interviews, table 1 below lists the items

making up the scale of the degree in which elements of performance budgeting are introduced.

Preconditions for the introduction of

‘elements of performance budgeting’

• Did the administration set up a policy note for the year 2008

according to article 150 of the Municipal Decree? (Yes/No);

• Did the administration formulate policy goals in the policy note

of 2008? (Yes/No).

Indicators for the introduction of

‘elements of performance budgeting’

• Does the policy note of 2008 give an estimation of revenues

and expenses? (Yes/No/Partly)

• Does the policy note of 2008 point out for each policy goal how

its execution will be funded? (Yes/No/Partly)

• Does the policy note of 2008 point out the budget item(s) each

policy goal will be influencing (5 point Likert scale: totally

untrue – totally true)

• Does the policy note of 2008 refer to the budget 2008, at least

for reach policy goal? (5 point Likert scale: totally untrue –

totally true)

Table 1 Items in the scale 'extent of introduction of elements of performance budgeting'

Based on the scores assigned to these items, a new ordinal item was constructed. To this end,

answers on the 5 point Likert scale were recoded into 0 (replacing 1-2), 0.5 (replacing 3) and 1

Financial management change: empirical testing of a model

KU Leuven – Public Management Institute 5

(replacing 4-5). Answers on the two first questions in the indicators section of table 1 were recoded

into 0 (replacing “no”), 0.5 (replacing “partly”) and 1 (replacing “yes”). These recoded items

appeared to be sufficiently internally consistent (Cronbach Alpha = 0.73). By adding the

corresponding scores, a compound index concerning the link between the policy plan and the budget

document could be constructed (ranging from 0 to 4).

The final scale regarding the degree in which elements of performance budgeting are introduced, is

based on the answers of the questions formulated in table 1. This scale points out to what extent the

administration has already introduced ‘elements of performance budgeting’ and consists of several

phases a Flemish municipality should complete to be able to introduce ‘elements of performance

budgeting’. Three general phases are (1) the construction of a policy note, (2) the formulation of

policy goals in this note and (3) coupling financial information in the budgetary document with these

policy goals. Within this last stage, four substages are distinguished that point at the extent of

integration of policy goals and financial information in the budgetary document. Here, the compound

index mentioned above is used to position the municipalities. As such, the setup of the scale is

informed by a cumulative logic. Table 2 presents the format of this scale. In the right column, the

relative spread of the Flemish municipalities across the different stages is presented.

Some findings stand out from this table. For instance, 28% of the Flemish municipalities do not

formulate any policy goals at all. Further, 8% of them does not provide a link between policy

objectives and the budget. On the other hand, from the 63% of the administrations that do link policy

objectives to the budget, only 18% does this in profound way. As such, we could assert that the

introduction of performance budgeting in Flemish municipalities is rather modest. Of course, these

data are essentially based on the perceptions of members of the administrative top and, therefore, a

social desirability bias cannot be excluded. This would however suggest that the percentages in table

2 are overestimated.

Besides mapping the prevailing practice with regard to performance budgeting in Flemish

municipalities, the survey described above and the corresponding results (as pictured in table 2),

inform the examination of factors influencing the introduction of this new practice in local

governments. After describing the conceptual model used to describe the change processes in

planning and budgeting practices and to structure the findings, this utilization of survey results in the

case study will be explained.

Financial management change: empirical testing of a model

KU Leuven – Public Management Institute 6

Score Phase Operationalization %

0 No policy note Policy note = 0 12

1 Policy note without policy goals Policy note = 1

Policy goals = 0 16

2 Policy notes with policy goals

Without a link to the budget

Policy note = 1

Policy goals = 1

Link policy note – budget document =

0/0.5

8

3 Policy note with policy goals linked to the budget in a

limited way

Policy note = 1

Policy goals = 1

Link policy note – budget document =

1/1.5/2

24

4 Policy note with policy goals linked to the budget in a

moderate way

Policy note = 1

Policy goals = 1

Link policy note – budget document =

2.5/3

21

5 Policy note with policy goals linked to the budget in a

strong way

Policy note = 1

Policy goals = 1

Link policy note – budget document =

3.5/4

18

Table 2 Format of the scale of the degree in which elements of performance budgeting are introduced

Factors influencing financial management change: a conceptual model 3

The conceptual model on accounting change of ter Bogt and van Helden (2000) proves useful to

describe the change processes in planning and budgeting practices and to structure our findings. Ter

Bogt and van Helden base their research concerning accounting reforms in Dutch governments (such

as midsize municipalities) on three academic approaches: the institutional work of Burns and Scapens

(2000), the ‘Seven Cs’ model of Shields and Young (1989) and the behavioural theory of the firm of

Cyert and March (1963). Below we give a short description of the model. We end with an overview of

the propositions we derived from it.

A first variable in the model (see figure 3) is the presence or absence of external and/or internal

pressure. Ter Bogt and van Helden (2000), based on Cyert and March (1963), point at the fact that

when actors in an organization are satisfied with the existing procedures, there is little or no

reason/incentive to change. The authors also state that when actors in an organization notice that a

certain conduct leads to success, these actors will be inclined to reproduce this conduct and the

underlying procedures, i.e. not to change. As such, the presence of pressure to change is a first

demand to change the existing procedures within the organization.

Financial management change: empirical testing of a model

KU Leuven – Public Management Institute 7

Figure 2 Influencing variables according to ter Bogt and van Helden (2000:275)

The internal and external sources of pressure to change would, in turn, influence the culture and

goals of the organisation. Furthermore, the authors state that a stimulating and powerful leader

needs to propagate the necessity of change within the organisation. This is the initiator/stimulator.

He or she, also labelled as a ‘champion’ in change management literature, must convince the other

actors within the organisation of the necessity of change. Mostly, this “champion” will specify an

ideal concept of the change proposed, leaving the actual execution to others. According to ter Bogt

and van Helden (2000), this ‘champion’ influences the organisational culture, while his or her

conduct is in turn at least partly defined by this organisational culture. After all, he/she must take

into account the habits and customs within the organisation when estimating the feasibility of the

change trajectory.

Financial management change: empirical testing of a model

KU Leuven – Public Management Institute 8

Next, the change process is developed and executed. According to ter Bogt and van Helden (2000),

several technical and organisational enabling factors need to be present. The authors refer in this

matter to the ‘Seven Cs’ model of Shields and Young (1989). The choice for certain facilitating factors

would be defined by the ‘champion’ on the one hand, and the ‘organisational culture’ on the other,

which delineates the reference framework for the relevant stakeholders. In the end, the change

process results in the introduction of new formal financial instruments on the one hand and in

actual change of the financial procedures and practices on the other. However, the authors remark

that the extent in which the financial procedures and practices are actually changed is also largely

dependent on the prevailing organisational culture.

Finally, ter Bogt and van Helden (2000) identify two potential gaps: a ‘usage gap’ and a ‘development

gap’. This development gap refers to the difference between the ideal concept of change as initially

put forward and as finally executed. As such, it mainly concerns the technicalities of the change

process. Then again, the usage gap refers to the difference between the usage possibilities of the

new financial instruments and the extent in which they are actually used.

The authors admit that this model implies a certain simplification of the change processes of financial

systems in governmental organisations. They acknowledge that besides the relationships they

identify, there can be other, probably less important, relationships and that specific changes in the

variables can cause other changes. A large ‘development gap’, for example, can turn into an incentive

to start the search for new and better financial instruments. A large ‘usage gap’ can lead to a

stronger use of certain facilitating factors, for example the provision of training, or to a weakening of

the initial ambitions regarding the change process. This latter effect could, according to the authors

and mainly based on Cyert and March (1963), also appear in organisations whose members are

relatively satisfied with the existing financial instruments. As such, an organisation can settle for less

radical change of the existing set of financial instruments, because of its fit with the prevailing

organisational culture.

There are several reasons to apply the above described model. First, this model conceptualizes the

introduction of new financial instruments as a change process. As such, the model goes beyond the

mere mapping of organizational motives to introduce new instruments; it also pays attention to the

change dynamics within organisations. Second, the model does not only include the technical aspects

of the change process, but also the organisational ones. Changing financial instruments does also

Financial management change: empirical testing of a model

KU Leuven – Public Management Institute 9

require changing the organisational culture. This holistic approach of the change concept fits change

management literature and the vision that informs the Municipal Decree. Third, the research model

has already been applied on midsize municipalities. Despite historically grown differences and a

different municipal context, It could be stated that Dutch and Flemish municipalities are frequently

confronted with similar developments (Steen 2007). Moreover, Dutch municipalities are generally

always one or more steps ahead of their Flemish counterparts, at least with regard to financial

instruments. As such, the fact that this model has already been applied to Dutch municipalities offers

a unique opportunity to learn from their experiences and to test whether similar findings can be

recorded for the Flemish local governments examined.

A full discussion of the operationalization of the conceptual model of ter Bogt and van Helden (2000)

is outside the scope of this paper. However, in table 3 we summarize the propositions and note the

references that informed or guided the formulation of these propositions and their

operationalization. The next section elaborates on the case study that examined these propositions.

KU Leuven – Instituut voor de Overheid – Public Management Institute

Parkstraat 45 bus 3609 – B-3000 Leuven – Belgium

Tel: 0032 16 32 32 70 – Fax: 0032 16 32 32 67

[email protected] – www.instituutvoordeoverheid.be – www.publicmanagementinstitute.be

Concept P Elements of performance budgeting will be

introduced to a larger extent when…

References

Change pressure

1 the change trajectory is mainly driven by technical

motives.

Selznick (1957); Cyert & March (1963); March & Olsen (1976); Meyer & Rowan

(1977); Di Maggio & Powell (1983); Tolbert & Zucker (1983); Scott (1995); Staw

& Epstein (2000); Scott (2001); Rogers (2003); Lounsbury (2008); ter Bogt &

Scapens (2009); Van Roosbroek (2009)

2 actors are dissatisfied with existing planning and

budgeting practices.

Cyert & March (1963); Oliver (1997)

Organisational

culture

3

change initiatives along the line of ‘New Public

Management’ (NPM) have been implemented and

incorporated into procedures and practices.

Hofstede et al. (1990); Schein (1992); Osborne & Gaebler (1993); Trice & Beyer

(1993); Oliver (1997); Davies et al. (2000); Aardema (2002); van Helden &

Janssen (2003); Pollitt & Bouckaert (2004); Demuzere et al. (2008); Halligan

(2011); Kickert (2011); Hansen (2011) & Cheung (2011) 4

respondents evaluate the NPM agenda in a more

positive way.

Organisational

goals

5 to a large extent, future change initiatives are in line

with the current change trajectory.

Simon (1973); Covaleski & Dirsmith (1988); Oliver (1991); Verhoest (2002);

Rainey (2003)

6

actors feel less hindered in the pursuance of other

objectives and in the setup of other activities as a

consequence of time and resources invested in the

change trajectory.

Initiator /

Stimulator

7 one or more actors take(s) on a strong leadership role

in the change trajectory.

Shields & Young (1989); Rothwell (1994); Shields (1995); Bouckaert (1997);

Berman & Wang (2000); Hartley & Allison (2000); Newman et al. (2001); van

Helden & ter Bogt (2001); Bradford & Florin (2003); Painter et al. (2003); Ridder

et al. (2005); Windels (2007) 8

actors in non-financial positions take on a leadership

role in the change trajectory.

9 to a larger extent, members of the political and

administrative top support the change trajectory.

Enablers:

Continuous

Education

10 the municipality provides education concerning the

change trajectory.

Shields & Young (1989); Oliver (1997); Ridder et al. (2005), Housden (2000);

Newman et al. (2001); Windels (2007)

Enablers:

Compensation &

controls

11

to a larger extent, the municipality monitors the

change trajectory and provides feedback regarding

steps taken.

Burns & Stalkers (1961); Hall (1982); Shields & Young (1989); Oliver (1997);

12 to a larger extent, the municipality provides

incentives to get the change trajectory accepted.

Financial management change: empirical testing of a model

KU Leuven – Public Management Institute 11

Enablers:

Commitment

13 to a larger extent, employees support the change

trajectory.

Shields & Young (1989); Oliver (1997); Christiaens (1999); Ridder et al. (2005);

Sterck et al. (2007); Windels (2007);

14 the municipality allocates more resources to the

change trajectory.

15 to a larger extent, actors perceive the change

trajectory as a priority.

Enablers:

Change process 16

to a larger extent, the change trajectory is based on a

purposeful change strategy.

Greenwood & Hinings (1988 & 1996); Miller & Friessen (1984); Nadler &

Tushman (1989); Shields & Young (1989); Nadler et al. (1995)

Development gap 17

a municipality experiences or has experienced less

technical impediments in introducing elements of

performance budgeting.

Shields (1995)

Usage gap 18

to a larger extent, actors are convinced that the

information offered by introducing elements of

performance budgeting is or will actually be used.

Sterck et al. (2007)

Table 3 Propositions derived from the conceptual model of ter Bogt and van Helden (2000)

KU Leuven – Instituut voor de Overheid – Public Management Institute

Parkstraat 45 bus 3609 – B-3000 Leuven – Belgium

Tel: 0032 16 32 32 70 – Fax: 0032 16 32 32 67

[email protected] – www.instituutvoordeoverheid.be – www.publicmanagementinstitute.be

Factors influencing financial management change: a case study 4

To explain the extent in which elements of performance budgeting are introduced, an in depth

examination of the change processes in a few Flemish municipalities is carried out. Because past

research has pointed out that such change processes are mostly very complex (e.g. Burns and

Scapens, 2000; Burns and Vaivio, 2001), a case study was set up in which certain decisions and events

could be scrutinized in depth (Yin 2003). In the context of public management, a mix of research

methods, like surveys, literature studies, analyses of primary documents (e.g. budgets, annual

reports,…) and face-to-face interviews, is necessary to grasp the reality of the reforms.

Simultaneously, this mix enables compensating the weakness of one method with the strengths of

another. Within case, the information of the survey-research was also supplemented with data

gathered through documentary analysis and semi-structured face-to-face interviews. The

documentary analysis focused on the municipal long-term policy plans, long-term financial plans and

their annual counterparts. Moreover, semi-structured interviews were set up with the mayor, the

secretary, the treasurer, one or more aldermen, one or more member of the management team, one

or more head of department and other staff members (n=45, each interview lasted 2 hours on

average). To safeguard a balanced spread of the respondents across the organization, characteristics

of the different services was taken into account (i.e. history with policy planning, ‘hard’ or ‘soft’

sector, inside or outside service).

MUNICIPAL SIZE

LOWHIGH

BIG

SMALL

DEGREE OF

INTRODUCTION

POPULATION

SOFTWARE

POPULATION

SOFTWARE

BA

C D

Figure 3 Graphic representation of the case selection (case A, B, C & D)

The research design is a cross-case comparative case study (based on diverse cases). More

specifically, two larger and two smaller municipalities were selected. In each set, one municipality

Financial management change: empirical testing of a model

KU Leuven – Public Management Institute 13

had a high score and one had a low score on the dependent variable (i.e. based on the results from

the survey, see table 2 above). Besides size, municipal software to integrate financial and policy data

was held constant. After all, past research has shown that these factors influence the introduction of

management accounting (e.g. Ridder et al. 2005; Van Dooren 2005; Gomes et al. 2009). Moreover,

the provision of software in Flemish municipalities is mostly historically grown out of intermunicipal

companies. Therefore, only municipalities using the software application called ‘Olympus’ to

integrate financial and policy data (i.e. from one specific provider) are included in this research.

Figure 3 visualizes this research design.

First, within each set, both municipalities (i.e. both large or both small) were compared to each

other. As such, it was explored which factors lead to the diverging score on the dependent variable

(i.e. high or low). Second, across all cases, each concept was analysed regardless of the size of the

municipality. In this way, an attempt was made to generalize the explanatory power of the variables

examined. To this end, the dimensions of each concept and the position of the cases within each

dimension were visualized in one or more positioning maps (see figure 4). In each instance, it is

pointed out where we expect the cases to be positioned based on the formulated propositions. The

positioning maps are constructed in this way so that the bottom right quadrant always delineates the

position where cases are expected to have implemented performance budgeting in a large extent. Of

course, the data from the case study will point out whether this deductively based positioning is

correct. All positioning maps meet the following conditions: (1) dimensions are independent, (2) each

dimension has a certain order, (3) it is analytically possible to allocate cases to each quadrant and (4)

dimensions are derived from the propositions. Moreover, the allocation of cases to quadrants and,

hence, the position of the cases should be understood in a relative and not in an absolute way. In

other words, cases are positioned relative to other cases.

Finally, from the above it follows that cases are selected with different values for the dependent

variable (Y). As we have information regarding the values of this variable, the research design may be

qualified as Y-centered. This implicates according to Seawright & Gerring (2008:297) that this

research is exploratory-explanatory by nature. Selecting the cases based on the values of the

dependent variable (i.e. high or low), follows from the lack of empirical data with regard to the

independent variables. To meet the limitations of a cross-case analysis, a detailed in-depth study of

the within-case perspective is added (King et al. 1994:160). The advantage of this extra perspective is

that information is gathered not only regarding the influence of the independent variables on the

Financial management change: empirical testing of a model

KU Leuven – Public Management Institute 14

dependent variable, but also, if applicable, regarding the way how and the processes through which

this influence is exerted. In the next section, the findings from the case study are visualized and

discussed.

DIM

ENSI

ON

1

DIMENSION 2

Figure 4 Example of a positioning map

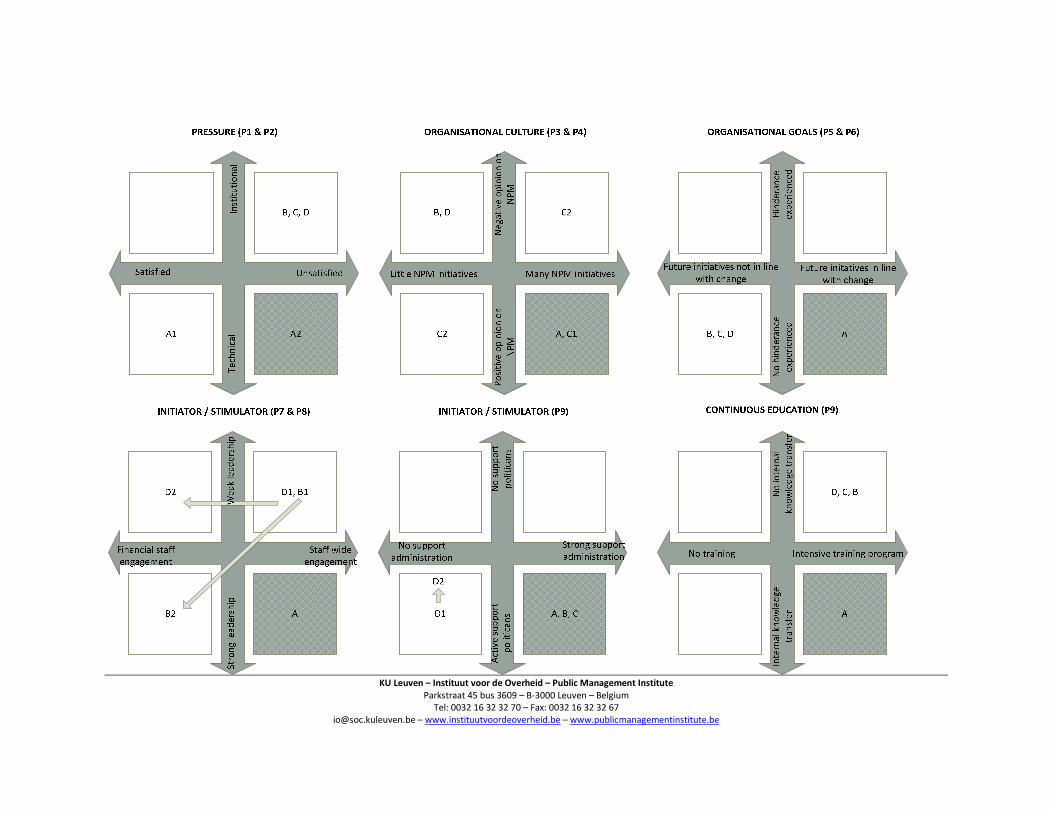

Factors influencing financial management change: empirical results 5

Below, the positioning maps visualize the different dimensions of each proposition, the bottom right

quadrant expected to be occupied by cases A and C (which are the cases with a high score on the

introduction of elements of performance budgeting) and the actual position of the four cases (based

on the data assembled in the case study). In general, cases A, B en D act as deductively expected.

After all, cases B and C (municipalities that introduced elements of performance budgeting to a lower

degree) are generally not positioned in the bottom right quadrant of the positioning maps, while

case A (a municipality that has introduced elements of performance budgeting to a high degree)

mostly is. On the other hand, case C (a small municipality that has introduced elements of

performance budgeting to a high degree), acts not as deductively expected. Indeed, looking at the

positioning maps, case C is generally not positioned in the bottom right quadrant. What is even more

striking, is that for the most part case C conforms to the positioning of cases B and D. As such, while

case C has obtained a high score with regard to the introduction of elements of performance

budgeting, the data obtained in the case study point out that case C acts as a municipality that did

introduce elements of performance budgeting to a lower extent. The positioning maps clearly

Financial management change: empirical testing of a model

KU Leuven – Public Management Institute 15

visualize the conformity in conduct between cases C, B and D on the one hand and the singular

position of case A.

To examine the possibility that case C was undeservedly classified as a municipality with a high level

of performance budgeting, we performed a quick scan of the way in which this municipality had

introduced elements of performance budgeting. An interview with the municipal treasurer set up in

the framework of this quick scan pointed out that in the budget document, policy objectives are

coupled with budget items. The reverse process however did not happen (correctly): budget articles

were not itemized across the different policy objectives and action plans. In other words, budget

articles are allocated to certain policy objectives as a whole. As such, the introduction of elements of

performance budgeting in municipality C seems to be a mere formalistic matter. Simultaneously, this

finding points out that our scale of the degree in which elements of performance budgeting are

introduced (see table 2) cannot discriminate between a formalistic and a non-formalistic

introduction. Therefore, to make sure that case A actually did introduce performance budgeting

elements to a high degree, a similar quick scan was performed in this municipality. This confirmed its

position as a case that does have the necessary budget registrations, that assembles budget

proposals and couples them to the goals structure on a decentralized basis, that itemizes budget

articles across objectives (or, vice versa, couples multiple budget articles to one objective) etcetera.

As such, it appears that case A has not been introducing elements of performance budgeting in a

formalistic manner.

Next, based on the cross-case analyses performed, the propositions put forward can be examined

(see table 3 above). Proposition one and two concerned the pressure to change. From the case study

it appears that the introduction of performance budgeting would indeed be enhanced by technical

motives (P1). Then again, concerning the satisfaction of employees (P2), the proposition had to be

rejected, as rather the reverse seemed to be true: when actors were satisfied with prevailing

budgeting and planning practices, elements of performance budgeting were introduced to a larger

extent. This could point at the beneficial influence of capacity built up (in casu with regard to

budgeting and planning practices) that would work as a self-reinforcing mechanism within the

change trajectory. Further research could shed more light on this aspect.

The first proposition within the concept organizational culture referred to the extent in which other

change initiatives along the lines of NPM were implemented and incorporated (P3). The case study

Financial management change: empirical testing of a model

KU Leuven – Public Management Institute 16

pointed out that especially initiatives in accordance with the policy component of ‘Decentralized

Government’ and ‘Community-owned Government’ (see Osborn and Gaebler, 2003) had a positive

influence on the introduction of performance budgeting (as opposed to initiatives regarding the

financial component of ‘Decentralized Government’ and ‘Customer-driven Government’). Next,

concerning the opinion of the actors with regard to NPM (P4), only the way in which the actors

evaluated the aspects ‘Community-owned Government’ and ‘Customer-driven Government’ (and not

‘Decentralized Government’) appeared to be relevant to the introduction of elements of

performance budgeting.

Concerning the concept organizational goals, the degree in which change initiatives planned were in

line with the change trajectory (P5) proved to have explanatory power regarding the degree of

performance budget elements introduced. Then again, the proposition regarding the extent in which

actors feel hindered in their accomplishment of other goals and activities due to the change

trajectory (P6) could not be confirmed. However, the corresponding motives do seem to be related

with the introduction of performance budgeting elements, as in cases B, C and D most respondents

said not to feel any hindrance, because, so far, only little time had been invested in the performance

budgeting change trajectory. In case A, on the other hand, employees actually felt their pressure of

work was heightened because of the change trajectory, but in their eyes, this had not disrupted their

daily work. Moreover, the strategic plan had, to a certain level, been embedded in daily practice, and

did, as such, rather serve as a guideline than as a disrupting element.

The initiator/stimulator concept is related to a first proposition concerning the extent in which

actors within the municipal organization have taken on a leadership role to implement the change

trajectory (P7). This seems necessary to introduce elements of performance budgeting to a large

extent. After all, cases in which there was no clear leader only introduced performance budgeting to

a low degree. However, the case study points out that a refinement is needed. After all, derived from

case A, not only the presence of a leader seems to be relevant, but especially how this leader

executes his role. More specifically, actively carrying out the change trajectory in the organization,

both during the decision-making process and the implementation phase, would prove particularly

beneficial to the change trajectory. Next, the extent in which also actors with non-financial functions

take on a leadership role (P8) appears to be relevant, as case A is the only one of the four selected

municipalities that actually succeeded in involving non-financial employees in the change trajectory.

Furthermore, the degree of support from the political and administrative top (P9), seems to be a

Financial management change: empirical testing of a model

KU Leuven – Public Management Institute 17

requisite to extensively introduce elements of performance budgeting. Secondly, it is necessary that

this support is explicit. In case D, for example, support from the political top was not perceived by

the administration; employees were quite on the contrary convinced that the political top did not

support the change trajectory. The reverse hols true for case B: while employees were convinced of

the political support, the political top acknowledged not to have championed the change trajectory.

These are both municipalities with a low level of elements of performance budgeting introduced.

Then again, in case A, both political and administrative top clearly supported the change trajectory,

both did so explicitly and, additionally, all employees actually perceived so.

Next, concerning the enabling factors, the first proposition relates to the extent in which training is

provided (P10). The case study points out that training is relevant. Moreover, a connection was

remarked between the nature of the training organized in cases C and D and the further

development of the change process in these municipalities. What discerns municipality A, is that in

this municipality training was provided both regarding policy and management matters (e.g. strategic

planning) and software-related matters (e.g. inputting data in ‘Olympus’). As such, it seems that both

types of training are relevant. Apart from this, case A also appeared to mobilize structures to enable

internal knowledge transfers. This too seems to be beneficial for the introduction of performance

budgeting elements.

Regarding compensation and controls, the extent in which incentives are provided was scrutinized

(P11). This proposition could not be confirmed. However, in this research only specific incentives

were examined in cases A and B. In these municipalities, employees are obliged to couple all board

and council proposals to policy objectives. If this coupling is lacking, the proposal is simply not

discussed. No other specific incentives were noticed. Moreover, this one explicit incentive found did

not seem to have any explanatory power. However, in case A, besides this formal incentive, informal

pressure is exerted by the municipal mayor to proceed with the change trajectory. This could point

out that besides formal incentives, informal ones should equally be taken into account.

Next, the extent in which the trajectory is monitored and feedback is provided (P12) proved to be

relevant. Then again, at first sight, employee support (P13) appeared not to be related to the

introduction of performance budgeting. However, in case A, specific attention was paid to the

employee support and throughout the trajectory, this support actually increased. However, further

examination should throw more light on the influence of this specific variable. Then again, the

Financial management change: empirical testing of a model

KU Leuven – Public Management Institute 18

influence of resources allocated to the change trajectory (P14) is multifaceted. First, regarding the

use of external consultants, there was no direct relationship with the introduction of elements of

performance budgeting. This however contrasts past research (cfr. Christiaens, 1999; Windels, 2007).

However, this could be ascribed to the angle of this research (namely management accounting, in

contrast with financial accounting) and the consultancy that corresponds with this. In this way, it

could be plausible that consultants within the domain of financial accounting have a more direct

impact on the extent and way of adopting a new instruments, than management accounting

consultants. Testing this proposition however exceeds the scope of this research and could be

addressed in future examinations.

In the study of Windels (2007), only the adoption of new management accounting instruments, as

put forward by relevant regulation, was scrutinized. The focus was not on the actual implementation

of these instruments in practice. However, inductively it could be asserted that case A diverges from

other cases in how this municipality treated external consultants hired. More specifically, only in case

A, the actors succeeded in keeping control over the change trajectory. Several respondents indicated

that this was thought to be very important. As such, the use of external consultants may not be

relevant an sich to the introduction of elements of performance budgeting, but to keep control over

the change trajectory is. Apart from this, the extent in which municipalities had one or more specific

functions to support the change trajectory seemed beneficial to this trajectory.

Finally, the extent in which other actors within the municipal organization spent time to the change

trajectory did not seem to be relevant. However, no single municipality where little time was spent

to the change trajectory obtained a high score regarding the introduction of elements of

performance budgeting. As such, this could be a necessary but insufficient condition. Otherwise, the

frequently slackening attention from other actors over time, could actually cause the low scores on

the introduction of performance budgeting. Seen in this way, the time spent by other actors would

directly affect the change trajectory. Indeed, respondents from case D pointed out that the lack of a

more intense coupling between objectives and budgets leaded several actors to wonder about the

added value of the change trajectory. As such, the engagement and initial enthusiasm from these

other actors decreased. In general, while this variable appears to have no direct relationship with the

introduction of performance budgeting elements, the time spent on the change trajectory does

however appear significant. A final proposition regarding ‘commitment’, refers to the extent in which

Financial management change: empirical testing of a model

KU Leuven – Public Management Institute 19

actors perceive the change trajectory as a priority (P15). A clear relationship between this variable

and the introduction of performance budgeting elements was found.

Concerning the change process, a purposeful change strategy (P16) appears to be fruitful to the

change trajectory. In the case study, the lack of an a priory defined change strategy seemed to cause

an unsystematic setup of the strategic plan and the corresponding policy notes, which, in turn,

caused several technical impediments. According to multiple respondents, these technical

impediments in turn hindered the organisation to move forward regarding the introduction of

performance budgeting.

Related to the concept of the development gap, is the extent in which a municipality experiences or

has experienced technical impediments (P17). This variable seems relevant to the introduction of

performance budgeting elements. There appears to be a connection with the extent in which training

is provided, the extent in which the trajectory is monitored and feedback is given, the degree in

which the changes are perceived as a priority matter, the extent in which the trajectory is based on a

purposeful strategy and, finally, the usage gap. Also, a refinement should be made, namely whether

the impediments actually disrupted the change trajectory. After all, while case A experienced

impediments, this municipality (contrary to the other ones), did not feel that this caused a disruption

of the change trajectory.

The usage gap consists of a first proposition, namely the extent in which actors think that the

information offered by introducing performance budgeting elements will be used or not (P18).

Concerning the use of this information for management purposes, case A is differentiated from other

municipalities by (1) the influence the change trajectory has on the decision-making process, (2) the

influence the change trajectory has on the cooperation between members of the political and

administrative top; (3) the influence the change trajectory has on the cooperation with other

organisations within the municipal territory. Concerning the use of this information for accountability

purposes, this research pointed out that case A was different because of the extent in which council

members actively refer to policy objectives in the explanations to the board. Concerning the use of

this information for the allocation of resources, in case A, as opposed to the other cases, there was

(1) an influence of the change trajectory on the budget setup process, both regarding administrative

and political aspects of this process and (2) an influence of the change trajectory on the division of

the resources available between the different sectors. In this way, information offered by introducing

Financial management change: empirical testing of a model

KU Leuven – Public Management Institute 20

performance budgeting elements is thought to be used in case A. As this case has a high level of

introducing performance budget elements, we conclude that this variable is relevant to this

introduction.

Conclusion 6

Based on the above outline of the findings of the case study carried out, this conclusion will first

formulate some remarks concerning the model used. Second, it will sum up the policy

recommendations that logically follow from this research. Third, future research endeavours are

explained.

Inductively, while carrying out this case study, some variables seemed to prove relevant to the

introduction of performance budgeting in the Flemish municipalities. However, these were not

incorporated in the original model of ter Bogt and van Helden (2000). First of all, the profiles of the

members of the political and administrative top appeared important. More specifically, future

research should take into account, for example, the external orientation, level of education and

motivation of administrative top members and, besides their level of education, the frequent

presence and involvement of political top members. In this context, it could also be worthwhile to

examine the nature of the political constellation. Next, and somewhat straightforward,

organisational characteristics are important: does the organisation have a lean structure, what is the

role of the management team, how does the organogram look like, are debate platforms constructed

etcetera. Concerning the process, for example, the presence of quick wins, the level of detail of the

municipal program, the existence of objectives regarding the internal functioning of the organisation

could equally be included in future research. Also, attention should be paid to environmental factors,

such as the financial(-economical) position of the municipality, prevailing regulation and other

factors. Furthermore, rethoric proved important.

A general critique on the model is its underestimation of the importance of ‘agents’ and their profile.

Another general remark is that environmental factors, such as the pressure to change, are not only

present at the start of the change trajectory, but also further down the line (e.g. changing regulation,

financial-economic crisis etcetera). To this end, and based on the research carried out, a revised

model of the one of ter Bogt and van Helden (2000) was constructed. Figure 5 illustrates this. Some

components were added (in italics), some were preserved and others were removed. Moreover, the

KU Leuven – Instituut voor de Overheid – Public Management Institute

Parkstraat 45 bus 3609 – B-3000 Leuven – Belgium

Tel: 0032 16 32 32 70 – Fax: 0032 16 32 32 67

[email protected] – www.instituutvoordeoverheid.be – www.publicmanagementinstitute.be

Financial management change: empirical testing of a model

KU Leuven – Public Management Institute 22

D, C

No

mo

nit

ori

ng

&

fee

db

ack

Incentives

A, B

Mo

nit

ori

ng

&

fee

db

ack

No incentives

COMPENSATION & CONTROLS (P11 & P12)

A1C, D2, B No

su

pp

ort

em

plo

ye

es

Involvement employees

D1, A2

Su

pp

ort

em

plo

ye

es

No involvement employees

COMMITMENT (P13 & P14)

D, BC

No

fu

nct

ion

s to

sup

po

rt c

ha

ng

e

External consultants

A

Sp

eci

fic

fun

ctio

ns

to

sup

po

rt c

ha

ng

e

No external consultants

COMMITMENT (P14)

C, B2, D2 No

n-p

rio

rity

Involvement other actors

B1, D1, A

Pri

ori

ty

No involvement other actors

COMMITMENT (P14 & P15)

C, D, B

No

ch

an

ge

str

ate

gy

(co

nte

nt)

Change strategy (process)

A

Ch

an

ge

str

ate

gy

(co

nte

nt)

CHANGE PROCESS (P16)

No change strategy

(process)

A

B, D, C

Dis

rup

tio

n o

f th

e

cha

ng

e p

roce

ss

No technical impediments

No

dis

rup

tio

n o

f th

e

cha

ng

e p

roce

ss

Development gap (P17)

Technical impediments

Financial management change: empirical testing of a model

KU Leuven – Public Management Institute 23

Financial management change: empirical testing of a model

KU Leuven – Public Management Institute 24

1

CHANGE PRESSURE

Presence of internal-technical pressure to change

ACTOR PROFILES CHANGE PROCESS TECHNICAL ORGANISATION

DEVELOPMENT GAP DEVELOPMENT GAP

POLITICAL TOP

ADMINISTRATIVE TOP

INITIATOR/STIMULATOR

INCENTIVES/MONITORING

COMMITMENT

• Active leadership role

• Non-financial involvement

• Pronounced political and

administrative support

TRAINING

• On policy and management

• On software

• Internal knowlegde transfer

• Formal incentives

• Informal steering

• Follow-up and feedback

• Consultants ‘controlled’ by municipality

• Trajectory is priority

• Specific functions

• Time invested by other actors

‘CHANGE PROCESS’

• Purposeful strategy

• Organisational improvement rhetoric

• Quick wins

IT-INFRASTRUCTURE

GOALS STRUCTURE

• Formulation of policy objectives

• Degree of coverage of policy

• Uniformity across sectors

• Level of detail

ORGANISATIONAL GOALS

ORGANISATIONAL CULTURE

ORGANISATIONAL STRUCTURE

• Congruence with future change

initiatives

• Debate platforms

• Sectoral working

O

M

G

E

V

I

N

G

S

F

A

C

T

O

R

E

N

Decentralization concerning policy

• Participation and communication

• Appreciation of participation and

communication

• Appreciation of customer

orietedness

• Extent confronted with technical

impediments

• Extent of actual disruption of the

change trajectory

• Used for management

• Used for accountability

• Used for allocation of resources

I

II

III

KU Leuven – Instituut voor de Overheid – Public Management Institute

Parkstraat 45 bus 3609 – B-3000 Leuven – Belgium

Tel: 0032 16 32 32 70 – Fax: 0032 16 32 32 67

[email protected] – www.instituutvoordeoverheid.be – www.publicmanagementinstitute.be

model is now divided into three boxes: (1) the cause of the change trajectory, (2) the change

trajectory and (3) the outcome of the trajectory. Finally, it is stressed that change trajectories of

financial instruments constitute an iterative process (see the arrow added from the lower box to the

upper box) and that environmental factors influence the whole change trajectory.

Policy recommendations that follow from this research are the following. Regarding the cause of the

change trajectory: (1) do not only emphasize regulations, but also the advantages for the

organisation, her functioning and her employees. Regarding the setup of the trajectory: (2) stimulate

the involvement of the board through training, systematic provision of information and the emphasis

on the need for input; (3) make sure that the profiles of the members of the management team fit

the change trajectory, through training and competences needed (for new staff) and make sure the

decisions of the management team are perceived as legitimate; (4) appoint a leader, preferably from

a policy service, and assure the involvement of other actors by means of a steering group; (5)

stimulate involvement of non-financial functions, by appointing a leader from a policy service and

setting up a steering group (consisting of political and administrative members); (6) pronounce the

support of political and administrative top; (7) provide training concerning policy and management

aspects, but also concerning software aspects. Stimulate internal knowledge transfer; (8) do not only

install formal incentives, but also informal ones; (9) pay attention to the follow-up and feedback; (10)

control the cooperation with the consultant; (10) create a supporting function; (11) stimulate other

actors to spend time; (12) stimulate that other actors perceive the trajectory as a priority; (13)

develop a change strategy that focuses on both technical and process aspects. To this end, map prior

to the changes which technical choices will be made and how the trajectory will be carried out in the

organisation. Enable quick wins and utilize an organizational improvement rhetoric.; (14) don’t let

the trajectory get halted on technical impediments; (15) frame future initiatives in line with the

change trajectory; (16) do not let the organisational structure and culture hinder the trajectory. With

regard to the result of the trajectory: (17) control the development gap by creating a purposeful

change strategy, by controlling the development of the trajectory and by establishing a close

cooperation with the software house; (18) control the usage gap, by using information for

management, accountability and allocation of resources.

In this paper, a study on the introduction of – what we have called – ‘elements of performance

budgeting’ in Flemish municipal organizations has been explained. Firstly, we examined to what

extent Flemish municipal organizations have introduced elements of performance budgeting.

Financial management change: empirical testing of a model

KU Leuven – Public Management Institute 26

Secondly, we explored to what extent the conceptual model presented by ter Bogt & van Helden

(2000) as operationalized by us, can account for the state of affairs regarding the introduction of

elements of performance budgeting in individual Flemish municipal organizations. Finally, taking the

adapted and refined conceptual model as our starting point, we have made policy recommendations

to managers within Flemish municipal organizations who want to introduce elements of performance

budgeting in their organization. Amongst other things, the research shows that the model of ter Bogt

& van Helden (2000) underestimates the importance of agents and their profile. Besides, we find

that, contrary to the impression that the model of ter Bogt & van Helden (2000) gives, environmental

factors influence the course of the change process throughout all phases of the change trajectory.

Finally, the research suggests a number of adjustments and refinements to the operationalization of

the concepts in the existing model.

In future research, we want to systematically build on these research findings and on the revised

model presented in this paper (see also the research objectives outlined at the beginning of this

paper). More specifically, a first question will be to what extent performance information is

measured, incorporated and used in local governments (Bouckaert and Halligan, 2008). Here, the

focus will be on the first two phases of the financial cycle (namely budgeting and accounting) and on

the link between both. Secondly, future research wants to examine to what extent factors described

in the revised model above facilitate this measurement, incorporation and use of performance

information. In this way, the focus will be extended from budgeting to accounting (and the link

between both). Moreover, the influence of the variables described should be further refined (in a

quantitative way) and tested on a large scale (contrary to the current exploratory research setup).

Moreover, not only the measurement and incorporation, but also the use of performance

information will be important. Finally, besides the Flemish municipalities, other local governments

will be scrutinized (namely the Public Centres for Social Welfare).

Bibliography 7

Aardema, H. (2002). Doorwerking van BBI. Evaluatie van een veranderingsbeweging bij de

Nederlandse gemeenten. Leusden: Bestuur & Management Consultants.

Adler, P.S. & Kwon, S.-W. (2002). Social capital: prospects for a new concept. The Academy of

Management Review, 27(1), pp. 17-40.

Anderson, P.F. (1982). Strategic planning and the Theory of the Firm. The Journal of Marketing, 46(2),

pp. 15-26.

Financial management change: empirical testing of a model

KU Leuven – Public Management Institute 27

Argote, L. (1999). Organizational learning: creating, retaining, and transferring knowledge. Kluwer

Academic Publishers. Boston MA.

Argote, L. & Greve, H.R. (2007). A behavioral theory of the firm – 40 years and counting: introduction

and impact. Organization Science, 18(3), pp. 337-349.

Augier, M. & Knudsen, T. (2004). The architecture and design of the knowledge organization. Journal

of knowledge management, 8(4), pp. 6-20.

Barley, S.R. & Tolbert, P.S. (1997). Institutionalization and structuration: studying the links between

action and institution. Organization Studies, 18(1), pp. 93-117.

Berman, E. & Wang, X. (2000). Performance Measurement in U.S. Counties: Capacity for Reform.

Public Administration Review, 60(5), pp. 409-420.

Beyer, J.M. & Trice, H.M. (1982). The utilization process: a conceptual framework and synthesis of

empirical findings. Administrative Science Quarterly, 27(4), pp. 591-622.

Boex, L.F.J., Martinez-Vazquez, J. & McNab, R.M. (2000). Multi-Year Budgeting : A Review of

International Practices and Lessons for Developing and Transitional Economies. Public Budgeting

& Finance, 20(2), pp. 91-112.

Bogt ter, H.J. & Helden van, J. (2000). Accounting change in Dutch government: Exploring the gap

between expectations and realizations. Management Accounting Research, 11, pp. 263-279.

Bogt ter, H.J. (2001). Politicians and output-oriented performance evaluation in municipalities.

European accounting review, 10(3), pp. 621-643.

Bogt ter, H.J. (2003). Performance evaluation styles in governmental organizations: how do

professional managers facilitate politicians’ work? Management accounting research, 14(4), pp.

311-332.

Bogt ter, H.J. (2004). Politicians in search of performance information? Survey research on Dutch

aldermen’s use of performance information. Financial Accountability & Management, 20(3), pp.

221-252.

Bogt ter, H.J. & Scapens, R.W. (2009). Performance Measurement in Universities: A Comparative

Study of Two A&F Groups in the Netherlands and the UK. Paper presented at the 7th ENROAC

Conference, Dundee – Scotland, 23-25 June, 2009.

Bouckaert, G. (1997). Proliferatie van lokale besturen: beleids- en beheersimplicaties. Res Publica,

Tijdschrift voor politologie, 39(1), pp. 109-123.

Bouckaert, G., Van Reeth, W., Auwers, T., & Verhoest, K. (1998). Handboek voor

doelmatigheidsanalyse – Prestaties begroten. Brussel: Ministerie van de Vlaamse Gemeenschap.

Bouckaert, G. & Van Nuffel, L. (2000). Financieel Overheidsmanagement: Internationale Tendensen

van begroting, boekhouding en audit. Brugge: die Keure.

Bouckaert, G., De Peuter, B. & Van Dooren, W. (2003). Meten en vergelijken van lokale bestuurlijke

ontwikkeling: een monitoringsysteem voor het lokaal bestuur in Vlaanderen. Brugge: die Keure.

Bouckaert, G. & Andriessens, E. (2003). Financiële meerjarenplanning in gemeenten: een

evaluatiestudie. Leuven: Steunpunt Bestuurlijke Organisatie Vlaanderen.

Bouckaert, G. (2006). Prestaties en prestatiemanagement in de publieke sector. Tijdschrift voor

Economie en Management, LI(3), pp. 237-265.

Financial management change: empirical testing of a model

KU Leuven – Public Management Institute 28

Bouckaert, G. & Halligan, J. (2008). Managing performance. International comparisons. London:

Routledge. 440 p.

Boyne, G.A. (2002) Public and private management: what's the difference? Journal of management

studies, 39(1), pp. 97-122.

Boyne, G., Gould-Williams, J., Law, J. & Walker, R. (2002). Plans, performance information and

accountability: the case of Best Value. Public Administration, 80(4), pp. 691-710

Bozeman, B. (2002). Public-Value Failure: When Efficient Markets May Not Do. Public Administration

Review, 62(2), pp. 145-161.

Bradford, M. & Florin, J. (2003). Examining the role of innovation diffusion factors on the

implementation success of enterprise resource the implementation success of enterprise

resource planning systems. International journal of accounting information systems, 4(3), pp. 205-

225.

Brignall, S & Modell, S. (2000). An institutional perspective on performance measurement and

management in ‘The New Public Sector’. Management Accounting Research, 11(3), pp. 281-306.

Bryson, J. (1995). Strategic planning for public and nonprofit organizations. A guide to strengthening

and sustaining organizational achievement. San Francisco: Jossey-Bass.

Budaüs, D. & Buchholtz, K. (1996). Controlling Local Government Cost and Performance: An

International Comparison. In Chan, J.L. et al. (Eds.). Research in Governmental and Nonprofit

Accounting, Vol. 9 (pp. 33-57). Greenwich, CT: JAI Press.

Burns, T., & Stalker, G. M. (1961). The management of innovation. London: Tavistock.

Burns, J. & Scapens, R.W. (2000). Conceptualizing management accounting change: an institutional

framework. Management accounting research, 11, pp. 3-25.

Burns, T.R. (2006). The sociology of complex systems: An overview of actor-system-dynamics theory.

World Futures, 62, pp. 411-440.

Caiden, N. (1988). Shaping things to come. Super-budgeters as heroes (and heroines) in the late-

twentieth century. In I. Rubin (Ed.), New directions in budget theory (pp. 43-58). Albany, NY: State

University of New York Press.

Chan, J.L. (1994). Accounting and Financial Management Reform in the United States Government:

An Application of Professor Lüder’s Contingency Model. In E. Bushor & K. Schedler (Eds.).

Perspectives on Performance Measurement and Public Sector Accounting (pp. 17-41). Berne et al:

Haupt.

Chan, J.L. (2003). Comparative international government accounting research (CIGAR) methodology:

issues and strategies. In: Montesinos, V. & Vela, J.M. (Ed). Innovations in Governmental

Accounting (pp. 23-29). Kluwer Academic Publishers.

Chenhall, R. H. (2003). Management control system design within its organizational context: Findings

from contingency-based research and directions for the future. Accounting, Organizations and

Society, 28(2-3), pp. 127-168.

Cheung, A.B.L. (2011). NPM in Asian countries. In T. Christensen & P. Lægreid (eds.). The Ashgate

Research Companion to New Public Management (pp. 131-145). Ashgate.

Christiaens, J. (1999) Financial accounting reform in Flemish municipalities: an empirical

investigation. Financial Accountability and Management, 15(1), pp. 21-40.

Financial management change: empirical testing of a model

KU Leuven – Public Management Institute 29

Collier, D. & Mahoney, J. (1996). Research Note – Insights and Pitfalls: Selection Bias in Qualitative

Research. World Politics, 49(1), pp. 56-91.

Covaleski, M. A., & Dirsmith, M. W. (1988). An institutional perspective on the rise, social

transformation, and fall of a university budget category. Administrative Science Quarterly, 33, pp.

562-587.

Cyert, R. M. and March, J. G. (1963). A Behavioral Theory of the Firm. Englewood Cliffs (N.J.), Prentice

Hall.

Davies, H.T.O., Nutley, S.M., & Mannion, R. (2000). Organizational Culture and Quality of Health Care.

Quality in Health Care, 9, pp. 111-119.

De Lancer Julnes, P. & Holzer, M. (2001). Promoting utilization of performance measures in public

organizations : an empirical study of factors affecting adoption and implementation. Public

Administration Review, 61(6), pp. 650-665.

Demuzere, S., Verhoest, K. & Bouckaert, G. (2008). Quality management in public sector

organizations: the role of managerial autonomy and organizational culture. EGOS 24th

Colloquium. Upsetting organizations. Nederland: Amsterdam. 10-12 juli 2008. 30 p.

Denhardt, K.G. & Aristigueta, M.P. (2008) Performance Management Systems: Providing

Accountability and Challenging Collaboration. In W. Van Dooren en S. van de Walle (Eds.).

Performance information in the public sector. How it is used. Palgrave MacMillan: Basingstoke.

Dequech, D. (2002). The demarcation between the “Old” and the “New” Institutional Economics:

recent complications. Journal of Economic Issues, 2, pp. 565-572.

DiMaggio, P.J., & Powell, W.W. (1983). The iron cage revisited: institutional isomorphism and

collective rationality in organizational fields. American Sociological Review, 48, pp. 147-160.

El-Batanoni, K. & Jones, R.H. (1996). Governmental Accounting in the Sudan. In Chan, J.L. et al. (Eds.).

Research in Governmental and Nonprofit Accounting, Vol. 9 (pp. 209-217). Greenwich, CT: JAI

Press.

Epstein, P. D. (1984). Using performance measurement in local government: A guide to improving

decisions, performance, and accountability. New York, NY: Van Nostrand Reinhold Company, Inc.

Garsombke, H. P. & Schrad, J. (1999). Performance measurement systems: Results from a city and

state survey. Government Finance Review, February.

Gavetti, G. & Levinthal, D.A. (2004). The strategy field from the perspective of management science:

divergent strands and possible integration. Management Science, 50(10), pp. 1309-1318.

Geddes, B. (1990). How the cases you choose affect the answers you get: selection bias in

comparative politics. Political Analysis, 2(1), pp. 131-150.

General Accounting Office (1997). Performance budgeting. Past initiatives offer insights for GPRA

implementation. G.A.O./AIMD. Washington D.C.: United States Governmental Accounting

Organization.

George, A.L. & Bennett, A. (2005). Case Studies and Theory Development in the Social Sciences. MIT

press (BCSIA studies in international security). 331p.

Gerring, J. (1999). What Makes a Concept Good? A Criterial Framework for Understanding Concept

Formation in the Social Sciences. Polity, 31(3) (Spring, 1999), pp. 357-393.

Financial management change: empirical testing of a model

KU Leuven – Public Management Institute 30

Gerring, J. (2004). What is a case study and what is it good for? American Political Science Review,

98(2), pp. 341-354.

Gerring, J. & Elman, C. (2006). Descriptive Inference: ‘What the Devil is Going On Around Here?’.

Paper presented at the annual conference of the American Political Science Association,

Philadelphia PA, 3 September.

Gerring, J. (2007). Case Study Research: Principles and Practices. Cambridge: Cambridge University

Press. 265 p.

Giddens, A. (1984). The constitution of society. Outline of the theory of structuration. Cambridge:

Polity Press. 402 p.

Godfrey, A.D., Devlin, P.J. & Merrouche C. (1996). Governmental Accounting in Kenya, Tanzania, and

Uganda. In Chan, J.L. et al. (Eds.). Research in Governmental and Nonprofit Accounting, Vol. 9 (pp.

193-208). Greenwich, CT: JAI Press.

Gomes, P.S., Fernandes, M.J, Carvalho, J.B. (2009). Explaining management accounting change in

Portuguese Local Government : a multi-theoretical approach. Paper presented at the 12th Biennial

CIGAR Conference. Modena – Italy, 28th-29th May 2009.

Gouldner, A.W. (1954). Patterns of Industrial Democracy. Free Press, New York.

Government Chief Social Researcher’s Office. (2004) . The Magenta Book – Guidance Notes for Policy

Evaluation and Analysis. London. Cabinet Office. Chapter 8 (17.03.2008, Policy Hub:

http://www.policyhub.gov.uk/magenta_book/index.asp).

Grant, R.M. (1996). Toward a knowledge-based theory of the firm. Strategic Management Journal,

17(10), pp. 109-122.

Greenwood, R. & Hinings, C. R. (1988). Design archetypes, tracks and the dynamics of strategic

change. Organization Studies, 9, pp. 293-316.

Greenwood, R. & Hinings, C.R. (1996). Understanding radical organizational change: bringing

together the old and the new institutionalism. Academy of Management Review, 21 (4), pp. 1022-

1054.

Greve, H.R. (2003). A behavioral theory of R&D expenditures and innovations: evidence from

shipbuilding. Academy of Management Journal, 46(6), pp. 685-702.

Guthrie, J., Olson, O. & Humphrey C. (1999). Debating Developments in New Public Financial

Management: The Limits of Global Theorising and Some New Ways Forward. Financial

Accountability and Management, 15(3-4), pp. 209-228.

Hall, R. (1982). Organizations: Structure and Process. Third edition. Englewood Cliffs, N.J.: Prentice-

Hall.

Hall, P.A. & Taylor, R.C.R. (1996). Political Science and the three new institutionalisms. Political

Studies, 44, pp. 936-957.

Halligan, J. (2011). NPM in Anglo-Saxon Countries. In T. Christensen & P. Lægreid (eds.). The Ashgate

Research Companion to New Public Management (pp. 83-96). Ashgate.

Hanssen, H.F. (2011). NPM in Scandinavia. In T. Christensen & P. Lægreid (eds.). The Ashgate

Research Companion to New Public Management (pp. 113-130). Ashgate.

Hart, D.M. (2004). “Business” is not an interest group: on the study of companies in American

national politics. Annual Review of Political Science, 7, pp. 47-69.

Financial management change: empirical testing of a model

KU Leuven – Public Management Institute 31

Hartley, J. & Allison, M. (2000) The Role of Leadership in the Modernization and Improvement of

Public Services. Public Money and Management, 20(2), pp. 35-40.

Hatry, H.P. (2002). Performance measurement: Fashions and fallacies. Public performance &

management review, 25(4), pp. 352-358.

Hedstrom, P. & Swedberg, R. (1998). Social Mechanisms: An Analytic Approach to Social Theory.

Studies in Rationality and Social Change. Cambridge: Cambridge University Press. 340 p.

Helden van, G.J. & ter Bogt, H.J. (2001). The application of businesslike planning and control in local

government: a field study of eight Dutch municipalities. Local Government Studies, 27(1), pp. 61-

86.

Helden van, G.J. & Jansen, E. P. (2003) New Public Management in Dutch Local Government. Local

Government Studies, 29(2), pp.1-88.

Helden van, J. (2005). Researching public sector transformation: the role of management accounting.

Financial Accountability & Management, 21(1), pp. 99-133.

Hirsch, P.M. & Lounsbury, M. (1997). Ending the family quarrel: toward a reconciliation of “Old” and

“New” Institutionalisms. American Behavioral Scientist, 40, pp. 406-418.

Ho, A. & Ni, A. (2005). Have cities shifted to Outcome-Oriented Performance Reporting? A content

analysis of city budgets. Public Budgeting & Finance, 25(2), pp. 61-83.

Hodgson, G.M. & Screpanti, E. (1991). Introduction to rethinking economics: markets, technology and

economic evolution. Edward Elgar. Aldershot. pp. 11-20.

Hodgson, G.M. (1993). The Economics of Institutions. International Library of Critical Writings in

Economics. Edward Elgar. 640p.

Hodgson, G.M. (2000). What is the essence of institutional economics? Journal of Economic Issues, 2,

pp. 317-329.

Hofstede, G. , Neuijen, B., Ohayv, D.D. & Sanders, G. (1990). Measuring Organizational Cultures: A

Qualitative and Quantitative Study across Twenty Cases. Administrative Science Quarterly, 35, pp.

286-316.

Housden, P. (2000) Turning Strategy into Practice: Organizational Development in the Modernization

of Local Government. Public Money and Management, 20(2), pp. 9-13.

Jackson, A. & Lapsley, I. (2003). The diffusion of accounting practices in the new “managerial” public

sector. International Journal of Public Sector Management, 16(5), pp. 359-372.

Jaruga, A. & Nowak, W.A. (1996). Toward a General Model of Public Sector Accounting Innovations.

In Chan, J.L. et al. (Eds.). Research in Governmental and Nonprofit Accounting, Vol. 9 (pp. 21-31).

Greenwich, CT: JAI Press.

Johansson, T. & Siverbo, S. (2009). Explaining the utilization of relative performance evaluation in

local government: a multi-theoretical study using data from Sweden. Financial Accountability &

Management, 25(2), pp. 197-224.

Jordan, M. & Hackbart, M. (1999). Performance budgeting and performance funding in the states: a

status assessment. Public Budgeting & Finance, 19(1), pp. 68-88.

Joyce, P.G. & Sieg, S. (2000). Using Performance Information for Budgeting: Clarifying the Framework

and Investigating Recent State Experience. Paper presented at the 2000 Symposium of the Center

Financial management change: empirical testing of a model

KU Leuven – Public Management Institute 32

for Accountability and Performance of the American Society for Public Administration, George

Washington University, Washington, D.C., February 11-12.

Joyce, P.G. (2003). Linking performance and budgeting. Opportunities in the Federal Budget Process.

Managing for Performance and Results series. IBM center for the Business of Government. 51 p.

Kettl, D.F. (1997). The global revolution in public management: Driving themes, missing links. Journal

of Policy Analysis and Management, 16(3), pp. 446-462.

Kickert, W.J.M. (2011) Public Management Reform in Continental Europe: National Distinctiveness. In