Embed Size (px)

Citation preview

Implementation of recommendations of Task

Force and Rationalization of Sugarcane Pricing

INDIAN SUGAR MILLS ASSOCIATION

Very relevant observations of Niti Ayog

“More often than not, the sugar industry gets saddled with high

inventories, leading to fall in prices below the cost of production and high

carrying costs and spoilage of sugar stocks, thus driving the industry to

sickness.

The sugarcane farmer, rather than benefiting from the high administered

prices of sugarcane, suffers distress caused by resource crunches with ex-

mills as they are unable to make timely payments for the crop.”

2

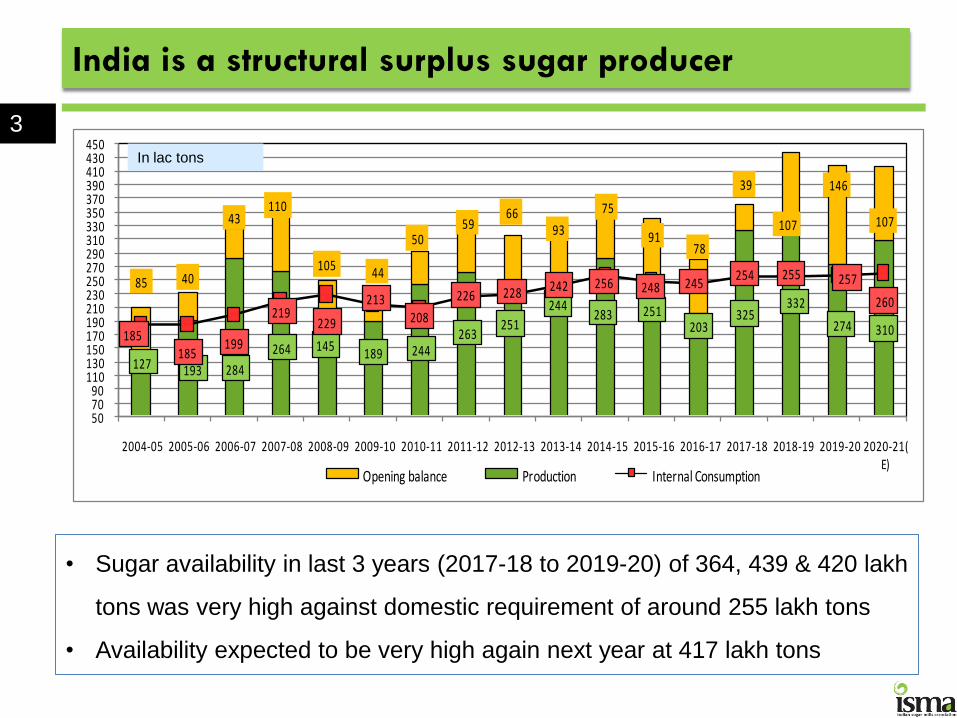

India is a structural surplus sugar producer

• Sugar availability in last 3 years (2017-18 to 2019-20) of 364, 439 & 420 lakh

tons was very high against domestic requirement of around 255 lakh tons

• Availability expected to be very high again next year at 417 lakh tons

3

127 193 284

264 145189 244

263251

244283 251

203325

332

274 310

85 40

43110

105 44

5059

6693

75

9178

39

107

146

107

185185

199

219229

213208

226 228 242 256 248 245254 255 257

260

507090

110130150170190210230250270290310330350370390410430450

2004-05 2005-06 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16 2016-17 2017-18 2018-19 2019-20 2020-21( E)

Opening balance Production Internal Consumption

In lac tons

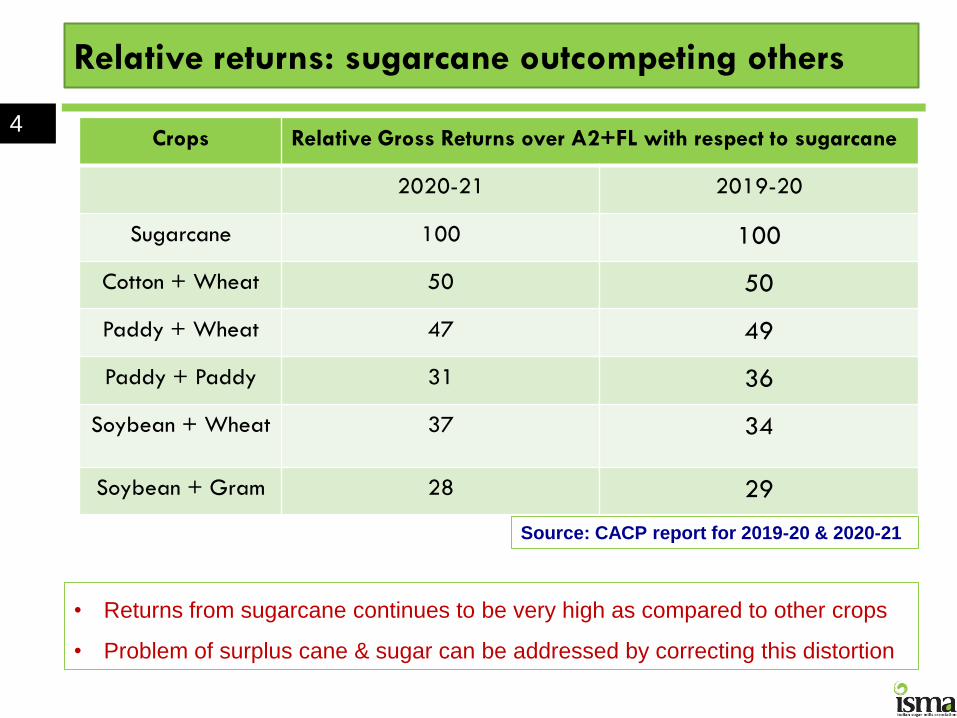

Relative returns: sugarcane outcompeting others

Crops Relative Gross Returns over A2+FL with respect to sugarcane

2020-21 2019-20

Sugarcane 100 100

Cotton + Wheat 50 50

Paddy + Wheat 47 49

Paddy + Paddy 31 36

Soybean + Wheat 37 34

Soybean + Gram 28 29

4

Source: CACP report for 2019-20 & 2020-21

• Returns from sugarcane continues to be very high as compared to other crops

• Problem of surplus cane & sugar can be addressed by correcting this distortion

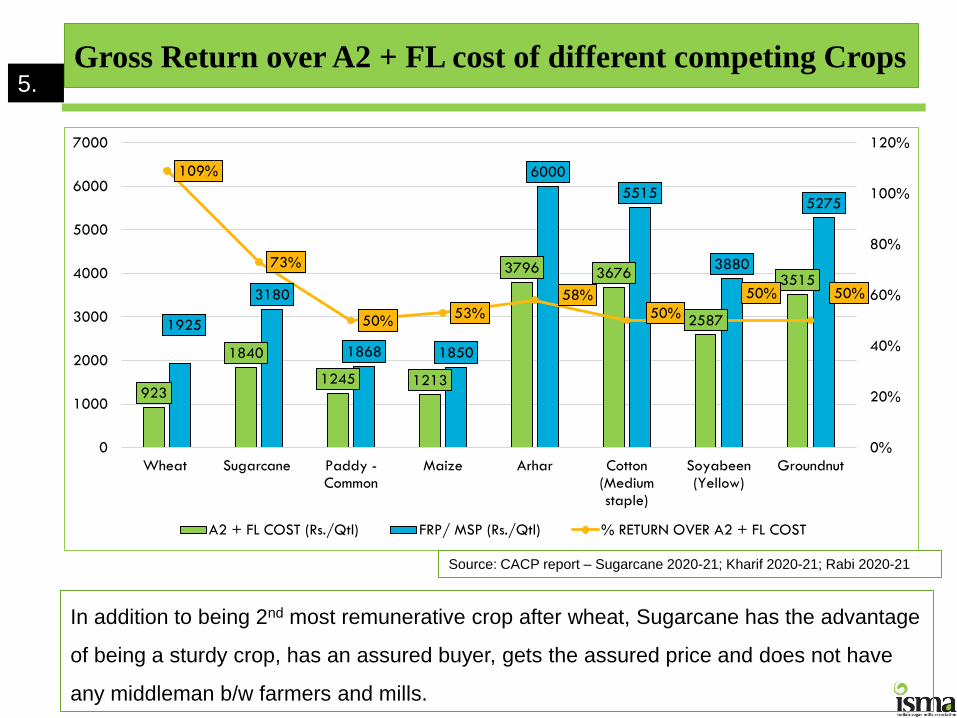

Gross Return over A2 + FL cost of different competing Crops

923

1840

1245 1213

3796 3676

2587

3515

1925

3180

1868 1850

6000

5515

3880

5275

109%

73%

50% 53%

58%

50%

50% 50%

0%

20%

40%

60%

80%

100%

120%

0

1000

2000

3000

4000

5000

6000

7000

Wheat Sugarcane Paddy - Common

Maize Arhar Cotton (Medium staple)

Soyabeen (Yellow)

Groundnut

A2 + FL COST (Rs./Qtl) FRP/ MSP (Rs./Qtl) % RETURN OVER A2 + FL COST

Source: CACP report – Sugarcane 2020-21; Kharif 2020-21; Rabi 2020-21

In addition to being 2nd most remunerative crop after wheat, Sugarcane has the advantage

of being a sturdy crop, has an assured buyer, gets the assured price and does not have

any middleman b/w farmers and mills.

5.

6

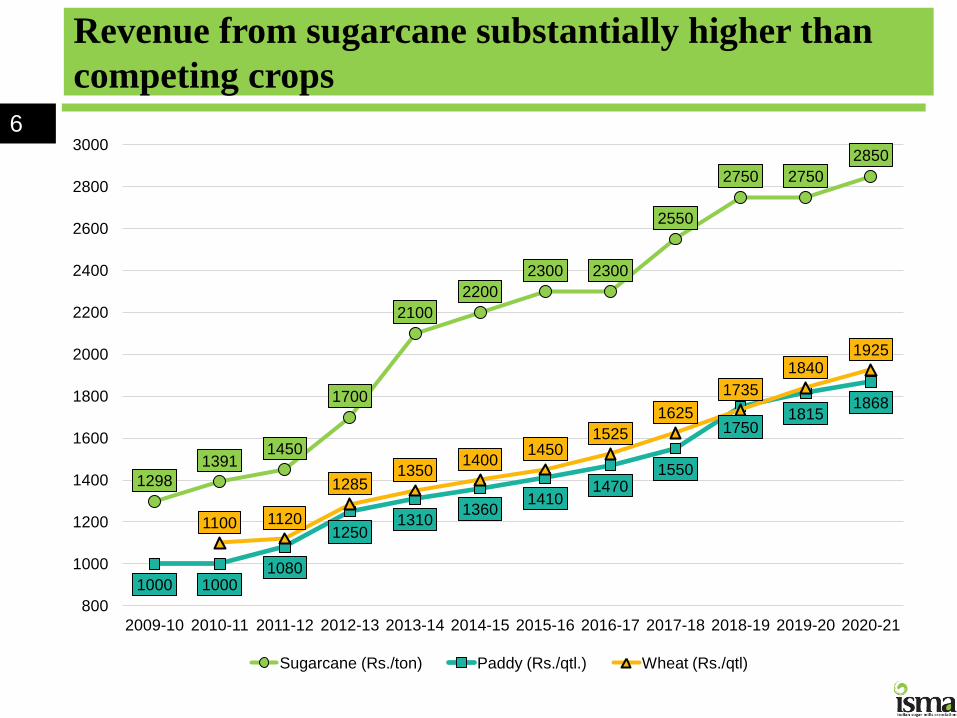

1298

1391 1450

1700

2100

2200

2300 2300

2550

2750 2750

2850

1000 1000 1080

1250 1310

1360 1410

1470 1550

1750 1815

1868

1100 1120

1285 1350

1400 1450

1525

1625

1735

1840 1925

800

1000

1200

1400

1600

1800

2000

2200

2400

2600

2800

3000

2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16 2016-17 2017-18 2018-19 2019-20 2020-21

Sugarcane (Rs./ton) Paddy (Rs./qtl.) Wheat (Rs./qtl)

Revenue from sugarcane substantially higher than

competing crops

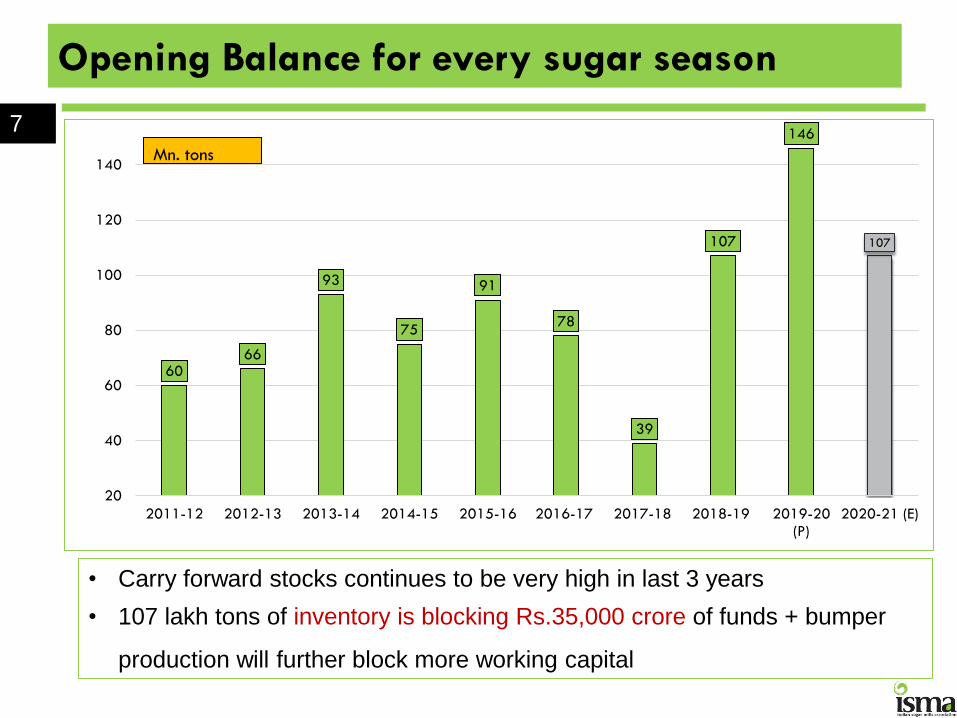

Opening Balance for every sugar season

60 66

93

75

91

78

39

107

146

107

20

40

60

80

100

120

140

2011-12 2012-13 2013-14 2014-15 2015-16 2016-17 2017-18 2018-19 2019-20 (P)

2020-21 (E)

Mn. tons

7

• Carry forward stocks continues to be very high in last 3 years

• 107 lakh tons of inventory is blocking Rs.35,000 crore of funds + bumper

production will further block more working capital

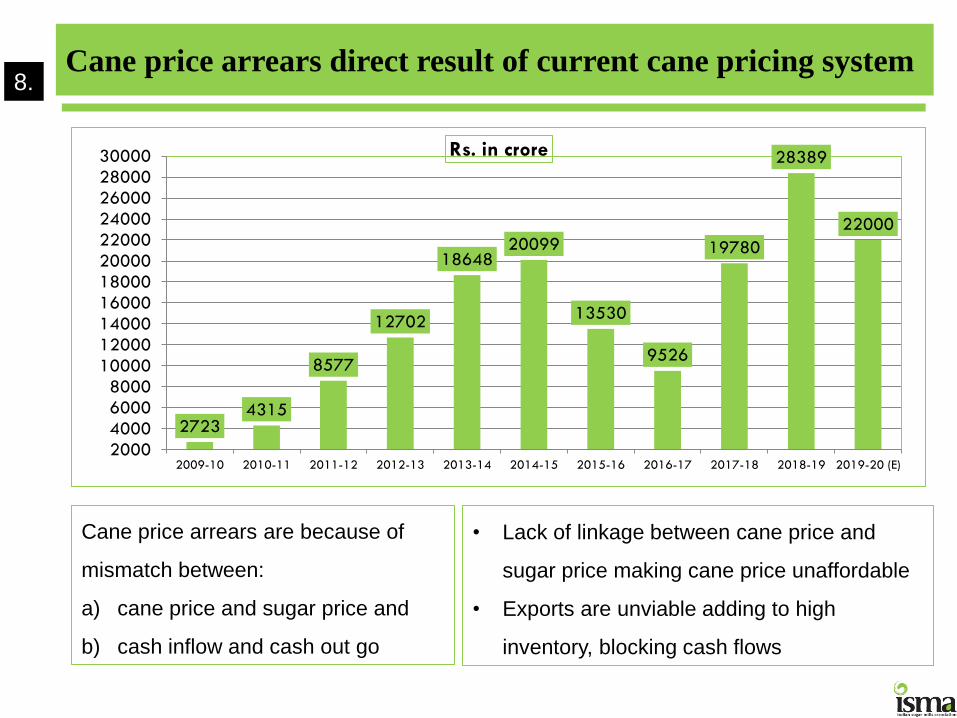

Cane price arrears direct result of current cane pricing system

2723 4315

8577

12702

18648 20099

13530

9526

19780

28389

22000

2000

4000

6000

8000

10000

12000

14000

16000

18000

20000

22000

24000

26000

28000

30000

2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16 2016-17 2017-18 2018-19 2019-20 (E)

Rs. in crore

Cane price arrears are because of

mismatch between:

a) cane price and sugar price and

b) cash inflow and cash out go

• Lack of linkage between cane price and

sugar price making cane price unaffordable

• Exports are unviable adding to high

inventory, blocking cash flows

8.

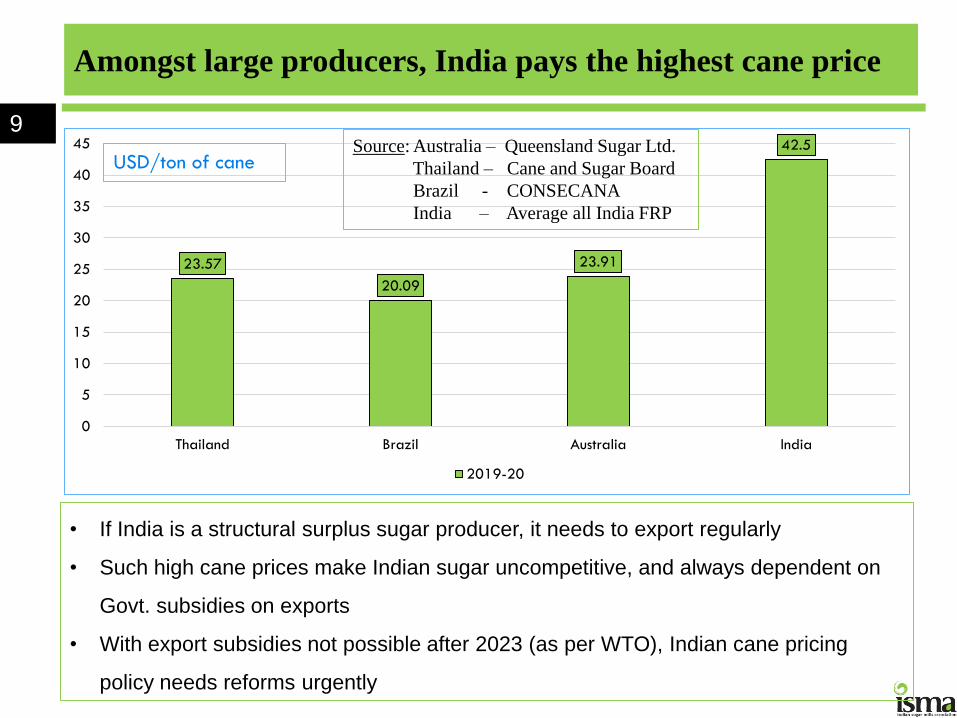

Amongst large producers, India pays the highest cane price

23.57

20.09

23.91

42.5

0

5

10

15

20

25

30

35

40

45

Thailand Brazil Australia India

2019-20

USD/ton of cane

9 Source: Australia – Queensland Sugar Ltd.

Thailand – Cane and Sugar Board

Brazil - CONSECANA

India – Average all India FRP

• If India is a structural surplus sugar producer, it needs to export regularly

• Such high cane prices make Indian sugar uncompetitive, and always dependent on

Govt. subsidies on exports

• With export subsidies not possible after 2023 (as per WTO), Indian cane pricing

policy needs reforms urgently

Indian cane pricing policy challenged in WTO

Brazil, Australia and Guatemala have complained against Indian sugar and

sugarcane policies in WTO

Complaint is also against high FRP

Stating FRP has “doubled in 9-10 years”

Causing surplus sugarcane production resulting in surplus Indian sugar

Causing global glut, depressing global prices

GOI’s legal experts feel there is need to amend Indian cane pricing policy

RSF along with PSF is WTO compliant

10

NITI AAYOG

RECOMMENDATIONS

11

MSP should cover costs/ FRP

Niti Ayog has said that

“MSP at ₹31/kg, …. does not even cover the cost of manufacture, given the FRP,

which is at a reasonably high floor of ₹275 per quintal (SAPs even higher). In

2017–18, the production cost for sugar was ₹3,580 per quintal (ISMA data)”

“One way of improving the liquidity situation of mills is to further raise the

Minimum Selling Price of sugar to Rs 33 per kg…… it would also help sugar

mills to cover the cost of production, including interest, maintenance costs etc.”

“Keeping in view the emerging developments, MSP for sugar should be

reviewed after six months of the notification.”

“If sugar prices in the market do not correspond to sugarcane FRP, then sugar

mills are left in a distressed state”

Above FRP has since been increased to Rs.285 per quintal

12

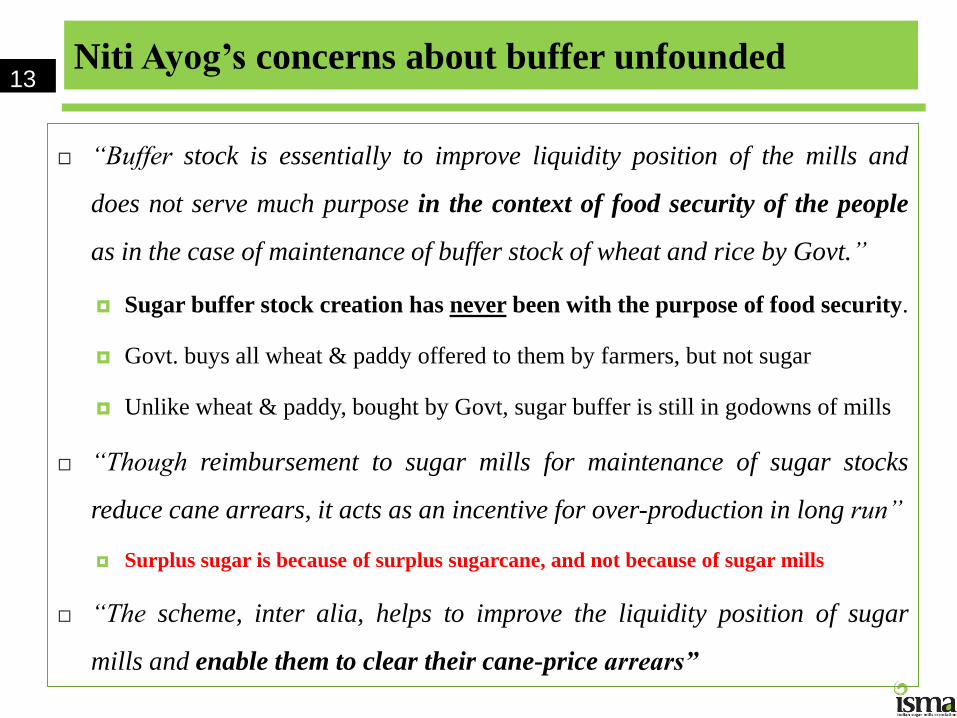

Niti Ayog’s concerns about buffer unfounded

“Buffer stock is essentially to improve liquidity position of the mills and

does not serve much purpose in the context of food security of the people

as in the case of maintenance of buffer stock of wheat and rice by Govt.”

Sugar buffer stock creation has never been with the purpose of food security.

Govt. buys all wheat & paddy offered to them by farmers, but not sugar

Unlike wheat & paddy, bought by Govt, sugar buffer is still in godowns of mills

“Though reimbursement to sugar mills for maintenance of sugar stocks

reduce cane arrears, it acts as an incentive for over-production in long run”

Surplus sugar is because of surplus sugarcane, and not because of sugar mills

“The scheme, inter alia, helps to improve the liquidity position of sugar

mills and enable them to clear their cane-price arrears”

13

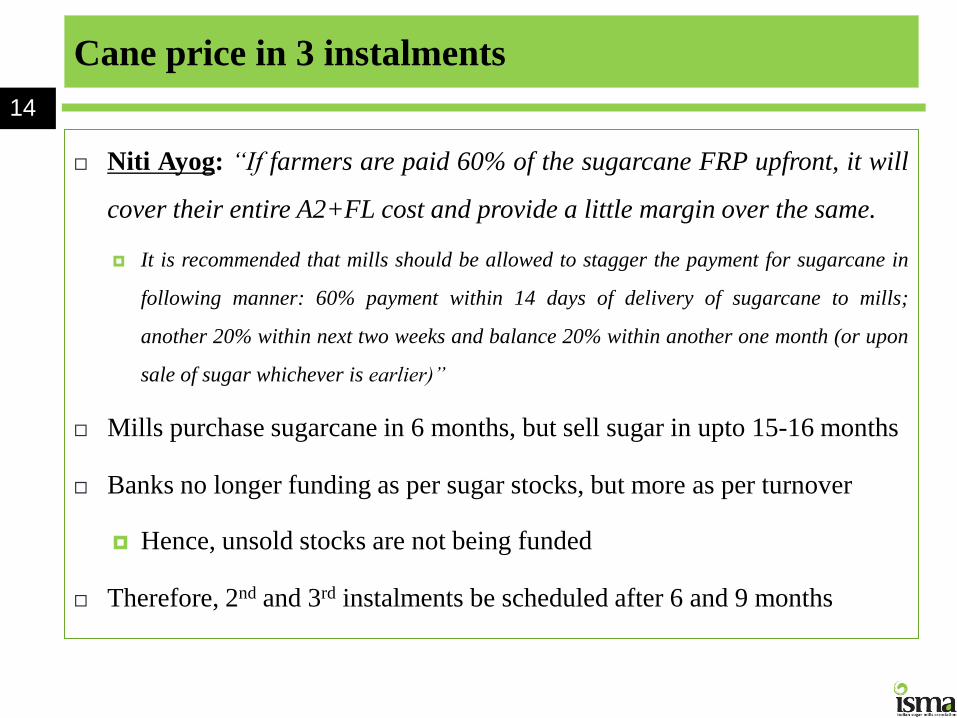

Cane price in 3 instalments

Niti Ayog: “If farmers are paid 60% of the sugarcane FRP upfront, it will

cover their entire A2+FL cost and provide a little margin over the same.

It is recommended that mills should be allowed to stagger the payment for sugarcane in

following manner: 60% payment within 14 days of delivery of sugarcane to mills;

another 20% within next two weeks and balance 20% within another one month (or upon

sale of sugar whichever is earlier)”

Mills purchase sugarcane in 6 months, but sell sugar in upto 15-16 months

Banks no longer funding as per sugar stocks, but more as per turnover

Hence, unsold stocks are not being funded

Therefore, 2nd and 3rd instalments be scheduled after 6 and 9 months

14

NITI AAYOG:

ON CANE PRICING

15

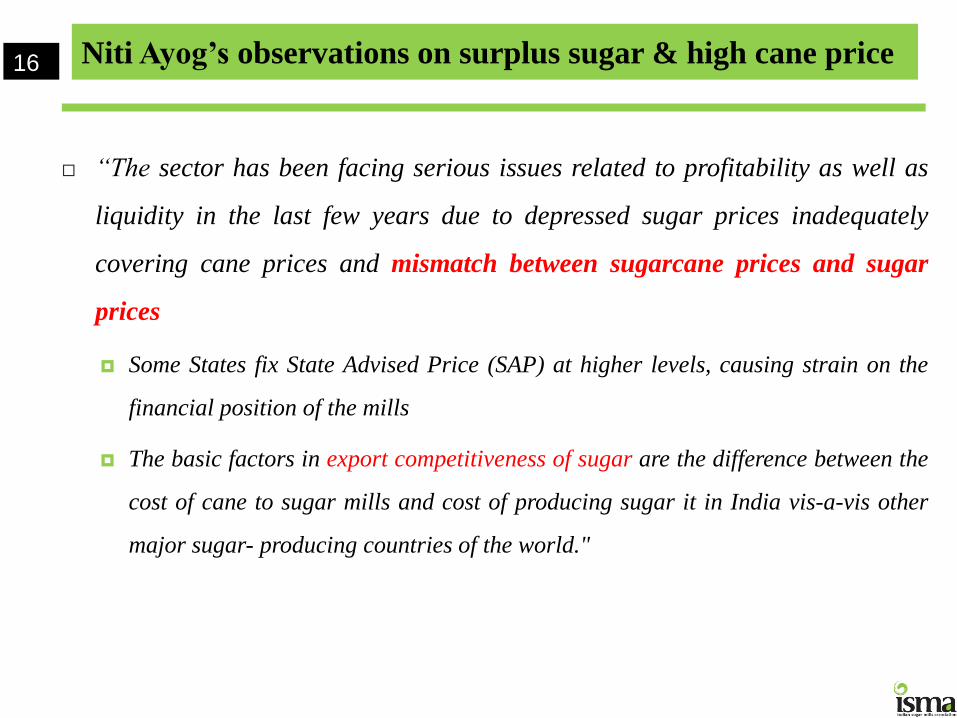

Niti Ayog’s observations on surplus sugar & high cane price

“The sector has been facing serious issues related to profitability as well as

liquidity in the last few years due to depressed sugar prices inadequately

covering cane prices and mismatch between sugarcane prices and sugar

prices

Some States fix State Advised Price (SAP) at higher levels, causing strain on the

financial position of the mills

The basic factors in export competitiveness of sugar are the difference between the

cost of cane to sugar mills and cost of producing sugar it in India vis-a-vis other

major sugar- producing countries of the world."

16

Niti Ayog’s observations on surplus sugar & high cane price

“Keeping sugar Industry healthy, needs major reform:

Serious policy distortions in sugar sector are continuing to result in excess sugar

production over domestic demand and rendered domestic prices highly

uncompetitive for trade.

Therefore, there is a need for complete restructuring of sugar industry in a phased

manner”

“To prevent the problem of arrears for sugarcane farmers and to keep the

sugar industry in sound financial health, sugarcane prices must be linked to

sugar prices”

“The (Rangarajan) Revenue Sharing Formula (RSF) needs to be introduced,

with a Price Stabilisation Fund (PSF) to protect farmers from receiving

prices below the FRP”

17

Rangarajan Committee formula

It inter-alia, in 2013, recommended for RSF, such that

Cane price @70% of revenue from sugar and primary by-products

Or @ 75% of revenue from sugar alone (5% weightage to primary by-products)

“The fundamental principle underlying sharing of the value created from

sugar and its by- products is that such value should be apportioned in the

relative share of costs incurred by farmers and millers.

An analysis of the costs incurred by sugarcane farmers and those incurred by

sugar mills suggests that this value-sharing ratio between farmers and millers

works out as 69:31 which, rounded off, can be taken as 70:30”

A scientific methodology was adopted to decide RSF, based on costs incurred

18

Niti Ayog’s recommendation of 80% unviable/ unnecessary

“The prices of sugarcane may need to be adjusted slightly upwards

keeping in view the improvement in recovery rates in the last few years

…….. formula can be 75% of sugar & by-products and 80% of sugar price”

RSF already accounts for higher recovery in calculation of cane price

As per RSF = (ex-mill sugar price) x (sugar recovery per ton of cane) x 75%

Increase in sugar recovery from 10.23% in 13-14 to 11.15% in 19-20 is

already included to give higher revenue and therefore higher cane price

Increase from 75% to 80% will give same benefit twice

Yield per hectare has also increased by 20-25% for the farmers

International Sugar Organisation (ISO) report of June 2019:

16 of the 22 countries have RSF, @ 62-66% of revenue from sugar & by-

products, so 70% for Indian RSF is already on higher side

19

Suggestions for funds for PSF

Niti Ayog: “Levy cess on sugar at Rs.50 per quintal for …… 3 years”

Under GST, all cesses abolished & sugar cess turned down by GST Council

Niti Ayog: “Dual pricing of sugar for industrial and household sector”

Can’t be implemented at factory gate

Niti Ayog: “In periods of high sugar price, part of the surplus generated

under RSF can be retained and deposited in the PSF”

Possible and will also ensure farmers get the FRP every year, and not too much

Niti Ayog: “The States that have been announcing State Advised Price,

should be urged to desist from doing so

Unless they are willing to bear additional costs of SAP upon themselves and not

forcing the mills to bear the load of sugarcane price above FRP”

20

ISMA’s SUBMISSIONS

21

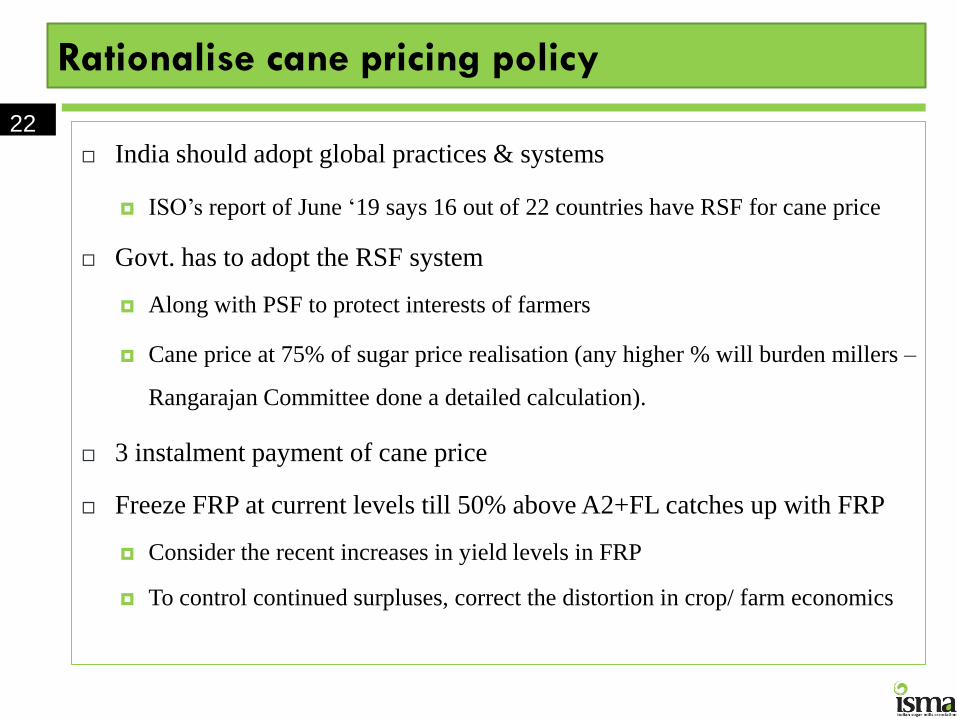

Rationalise cane pricing policy

India should adopt global practices & systems

ISO’s report of June ‘19 says 16 out of 22 countries have RSF for cane price

Govt. has to adopt the RSF system

Along with PSF to protect interests of farmers

Cane price at 75% of sugar price realisation (any higher % will burden millers –

Rangarajan Committee done a detailed calculation).

3 instalment payment of cane price

Freeze FRP at current levels till 50% above A2+FL catches up with FRP

Consider the recent increases in yield levels in FRP

To control continued surpluses, correct the distortion in crop/ farm economics

22

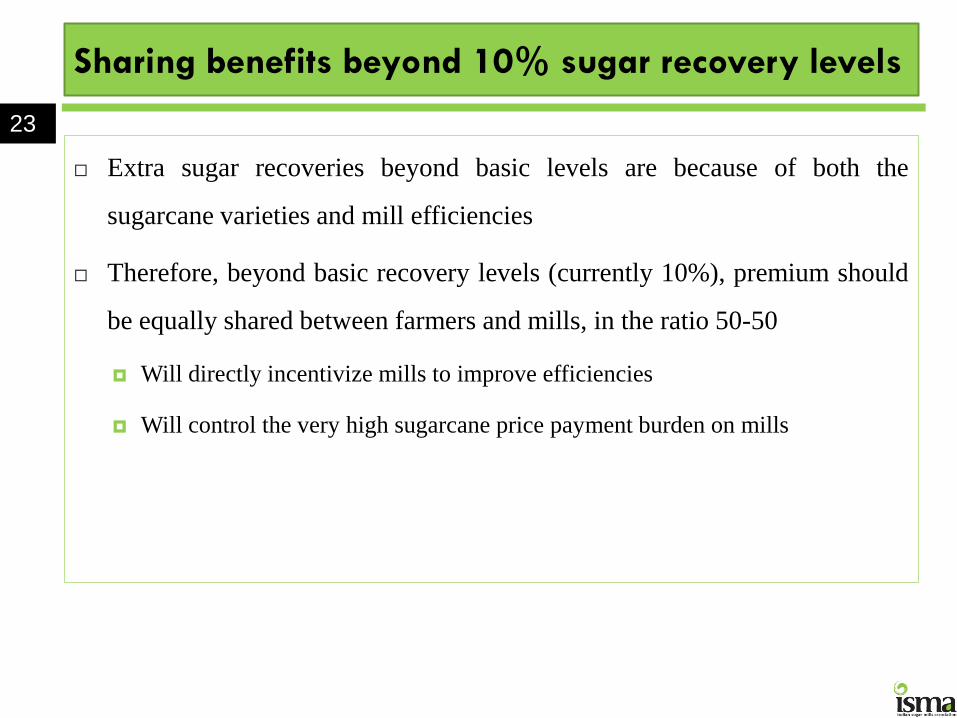

Sharing benefits beyond 10% sugar recovery levels

Extra sugar recoveries beyond basic levels are because of both the

sugarcane varieties and mill efficiencies

Therefore, beyond basic recovery levels (currently 10%), premium should

be equally shared between farmers and mills, in the ratio 50-50

Will directly incentivize mills to improve efficiencies

Will control the very high sugarcane price payment burden on mills

23

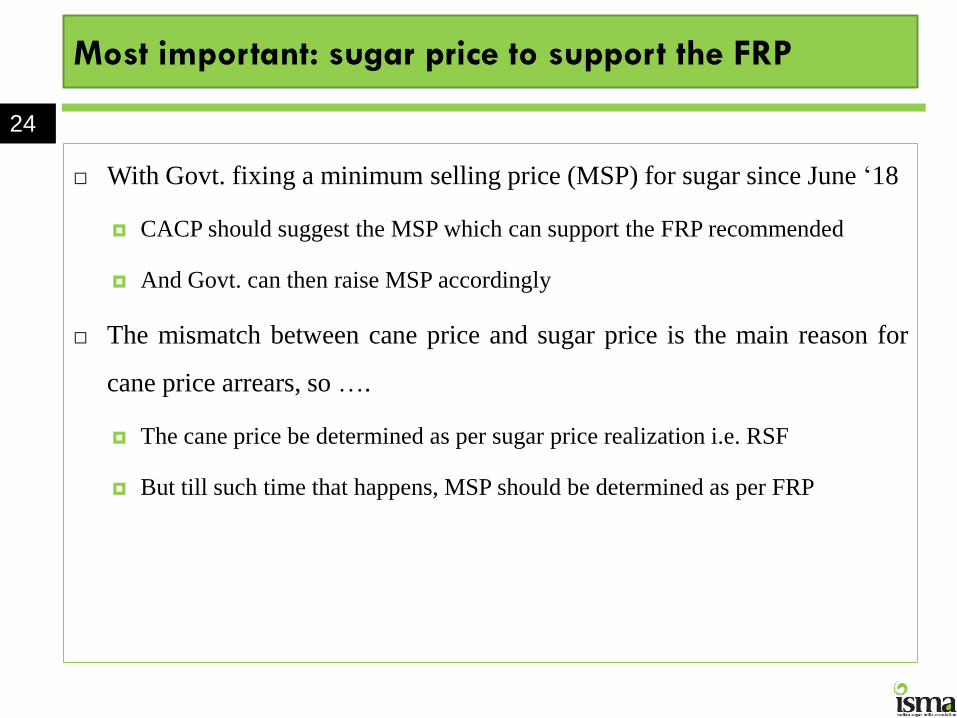

Most important: sugar price to support the FRP

With Govt. fixing a minimum selling price (MSP) for sugar since June ‘18

CACP should suggest the MSP which can support the FRP recommended

And Govt. can then raise MSP accordingly

The mismatch between cane price and sugar price is the main reason for

cane price arrears, so ….

The cane price be determined as per sugar price realization i.e. RSF

But till such time that happens, MSP should be determined as per FRP

24

Some other requests

Rebates for mechanical harvesting & binding material be revised

Non-cane material in mechanical harvesting increases by 12-14%

Rebate on biding material of 1% is too low as compared to actuals

Increase in base recovery from current 10% to 10.5%

With premium, rebates & discounts for higher & lower recoveries

Long term objectives of using sugarcane and molasses to produce

ethanol along with enough sugar for domestic requirement

The ad-hoc policies/schemes intending to temporarily discourage sugarcane

or give cash incentives for other crops should not be encouraged

Ethanol pricing formula be put out in the public domain

25.

Thank you