Embed Size (px)

Citation preview

Executive Summary China’s entry into the WTO opens up both opportunities as well as threats to the Indian

industry. Chinese entry shall increase the voice of developing nations in the WTO and

can enable them to have their demands of greater protection to domestic industries

accepted. India and China globally compete in the same export markets; Chinese entry

shall make Indian exports uncompetitive and threaten traditional Indian strongholds such

as textiles, tea and jewellery.

There is also the fear that Chinese goods may flood the Indian markets causing domestic

producers to go out of business. This fear, based on current data is largely unfounded as

there has been no perceptible increase in inflow of goods form China into India since the

easing of Quantitative Restrictions, over one year ago.

China is ahead of India both in terms of trade openness as well as its promised

commitment to further trade liberalization. China’s entry into the WTO shall force Indian

industry to become more competitive and shall pave the way for second-generation

market reforms in India. Labour market reforms, interest term structure reforms and basic

infrastructure reforms shall spur growth and competitiveness by cutting costs.

China’s huge market also becomes a potential market for Indian goods and increasing

domestic competitiveness can be leveraged by pushing exports.

Thus the potential for Indian industry to take advantage of the opportunity is large, but

needs to be backed up with forward- looking strategic policy initiatives form the

government. In a rapidly globalizing world economy there is no room for protectionism

and industry must compete based on its inherent strengths. Thus domestic industry needs

reforms in market structure to spur competiveness.

Introduction The WTO is a transnational organization that regulates trade between nations. It was

formed on the 1st of January 1995 by the Uruguay Pact countries. It has 142 countries as

its members. WTO provides a forum for trade negotiations, technical assistance and for

cooperation with other international organizations. The WTO wields tremendous

influence in shaping the course of world trade. Membership of the WTO, therefore,

enables nations to have a say in the framing of policies for their benefit.

India and China are emerging as the two largest markets in the world today. Foreign trade

has been one of the key factors fuelling high GDP growth rates (6.1% and 10.7%1

respectively for the years 1990 to 1999) in both these nations. In this context, the role of

the WTO as a body, which regulates and promotes trade assumes tremendous

significance for these countries.

India is a founder member of the WTO. The recent Doha summit of the WTO saw the

entry of China into the WTO. The entry of China had been held up because of

disagreements on the removal of trade barriers, which protect the Chinese domestic

industry from foreign competition. But all these disagreements have been resolved

through mutual bilateral agreements under the rules of the WTO.

China’s entry opens up a host of opportunities and threats for India. On one hand, it can

lend strength to the lobby of developing nations within the WTO. On the other, Chinese

industry will be able to compete in the Indian market on favourable terms.

This project will attempt to study the impact of China’s entry in the WTO on India by

examining the various issues and will also try to formulate a possible strategy so as to

optimise the gains accruing to India.

The present project allows us to use our skills towards good project planning and to apply

our knowledge of strategic issues to a dynamic environment involving deep structural

change.

1 Department of Economics and Statistics, Tata Services, Statistical outline of India, 2001, Bombay 241.

Literature Review China’s foreign trade increased explosively, from about $202 billion in the late 1970s to

$475 billion in 2000. By 2000 its share of total world trade had sextupled as compared

with 1977 and as early as 1995 China had become one of the top ten trading countries in

the world. Simultaneously, the total stock of foreign direct investment in China accounted

for almost a third of the cumulative foreign direct investment in all developing countries.

India’s share of total world exports was 0.6% compared to 3.5% of China.

China remains only shallowly integrated into the world economy in certain respects. The

foreign invested firms, which accounted for only about one-eighth of all manufacturing

output, were responsible for almost half of all of China's exports3. High tariffs and an

array of non-tariff barriers meant that some critical sectors of the Chinese economy

remain relatively insula ted from international competition.

Given this history of insularity from the world economy, the Chinese leadership has

increasingly come to the view that one of the principal benefits of becoming a member of

the World Trade Organization is the increased competition it would bring to China's

domestic market. Even though this would entail short-term economic costs, the Chinese

government has come to realize that economic reform and developing a market economy

is an imperative proposition.

During the 1990s, annual growth rates of U.S. merchandise exports to China averaged

16.1 percent 4. Even if annual growth rates in the next decade declined by half, U.S.

2 National Bureau of Asian Research 3 Lardy, Nicholas R., Issues in China’s WTO Accession, US-China Security review May 2001, p. 12. 4 Lau, Lawrence, J, New Estimates of the United States-China Bilateral Trade Balances, Institute for International Studies, Stanford University, April 1999, p. 22.

merchandise exports would reach $32 billion by 2005. Recent studies project that exports

of U.S. merchandise and services to China by 2005 would range from $27.8 to $36.5

billion with the entry of China into the WTO5.

In spite of being a member of the WTO, India still has barriers to trade to safeguard the

interests of domestic industry and trade. These restrictions are allowed by the WTO, but

have to be phased out gradually. The phasing out of the Quantitative Restrictions

coinciding with the entry of China into the WTO shall subject Indian industry to severe

competition. Indian industry has expressed concern that China would take advantage of

subsidized power, low-interest bank loans and lower labour costs in its own country to

dump its products in India. However, the fears of Chinese goods flooding the Indian

market and driving Indian industry out of business seem to be exaggerated. There was no

disproportionate rise in imports in 2000/01 because of the withdrawal of quantitative

restrictions 6.

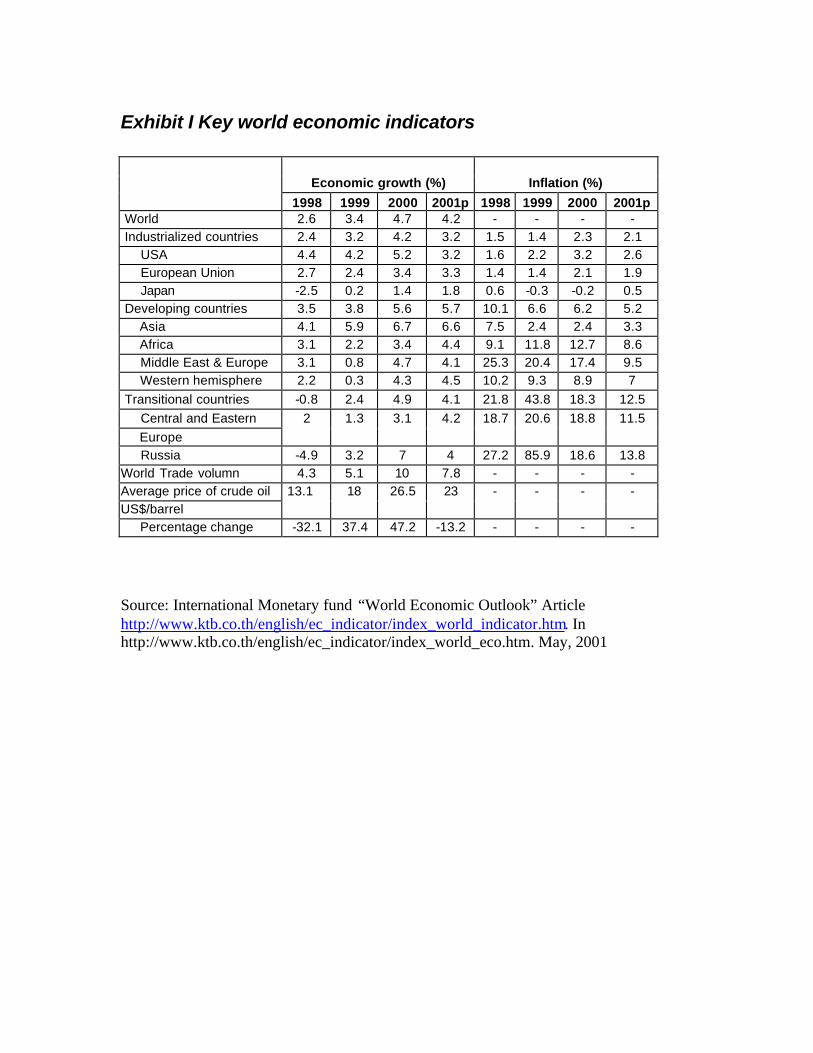

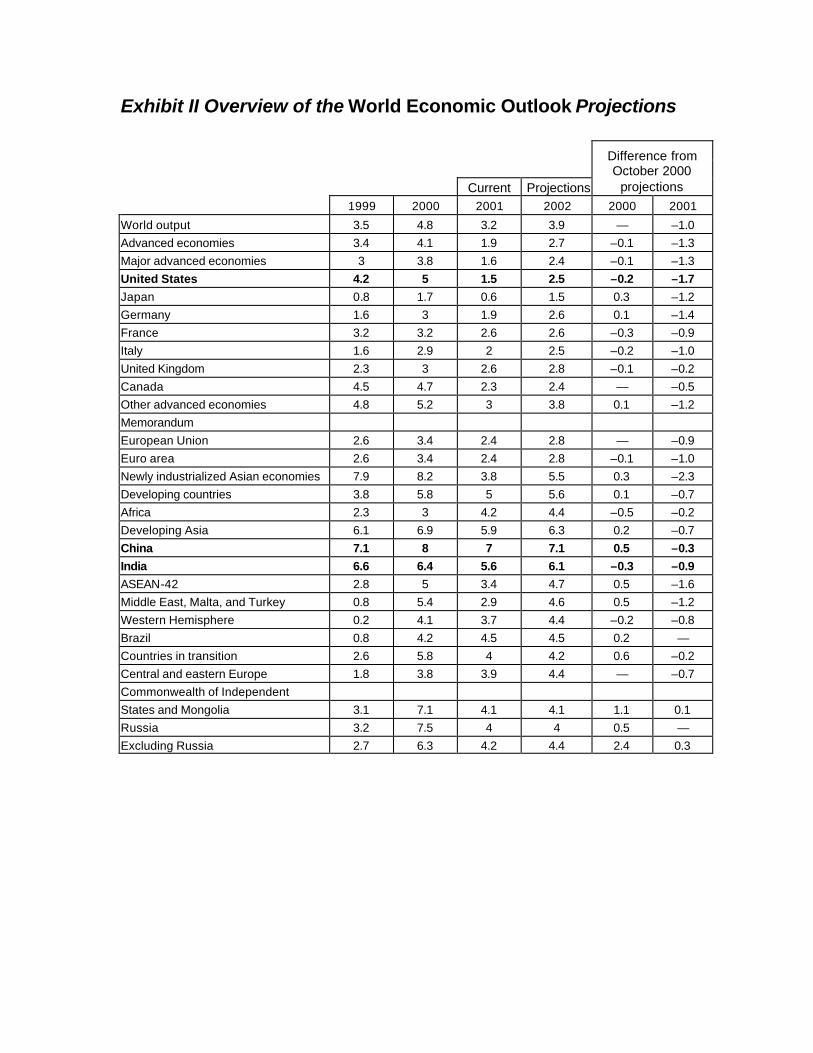

Global Economic Outlook Since October 2000 the prospects for global growth have weakened significantly, led by a

marked slowdown in the United States, a stalling recovery in Japan, and moderate growth 5 See Exhibit I 6 See Exhibit II

in Europe and in a number of emerging market countries7. Some slowdown from the

rapid rates of global growth of late 1999 and early 2000 was both desirable and expected,

especially in those countries most advanced in the cycle, but the downturn is proving to

be steeper than earlier thought. The revised projections of growth figures for the next two

years8 also indicate that the growth rates are likely to decrease. This data is indicative of a

Global recessionary scenario.

In such a situation nations are looking at spurring growth through increase in trade and

positive trade balances. China’s entry into the WTO at this juncture is expected to

increase the volume of international trade by up to 7%9.

Hence China’s entry into the WTO has far ranging implications not only for India but

also for the Global economy.

Terms of China’s Accession to the WTO The terms of an accession take two basic forms.

7 See Exhibit III 8 See Exhibit IV 9 National Bureau of Asian Research

Firstly there are the Schedules of commitments, which set out the full range of market

access obligations, which China, will be legally bound to grant to every Member when it

enters the WTO. The schedules cover tariffs and non-tariff measures applicable to

agricultural trade and industrial goods (commitments under the GATT), and services

(commitments under the General Agreement on Trade in Services, or GATS).

Secondly there are the Protocol and Working Party Report on the accession of China to

the WTO. These documents, which also include legally binding commitments, essentially

set out how China promises to fulfill her new WTO obligations. As well as containing

detailed descriptions of, and obligations relating to, China’s current and planned trade

and investment régimes, they detail a number of special provisions to which China will

be subject during the first years of her WTO Membership. These temporary derogations

from normal WTO rules are intended to reflect the unique challenge of incorporating

China into the world trading system. This is an economy in the midst of transition from

state ownership to the market based system; a country that has taken many measures to

introduce market economics, but where certain features of a state led economy still

prevail. Most notably, the protocol affords other Members special protection for their

own industries against damaging surges of exports from China.

The terms of accession detail the degree to which China will adopt the WTO rules and

agreements. These govern international trade in goods, agriculture and services, and

include provisions on many related areas such as trade related investment measures,

technical barriers to trade, sanitary and phytosanitary measures, intellectual property

protection, and government procurement.

Political Fallouts The WTO is presently sharply polarized between the developing and the developed

nations. The block of developing nations led by India are pressing for safeguards to

domestic industries from international competition and gradual phasing out of trade

restrictions 10. The developed nations on the other hand want faster phasing out of

restrictions and access of these markets to their industries. This polarization has, as

witnessed at the recent Doha summit prevented agreements from being reached on

strategic issues of Intellectual Property Rights and Quantitative restrictions.

China’s entry into WTO is in India’s interests as China shares India’s point of view on

various WTO issues. It has more diplomatic clout than India, and for the benefit of other

third world countries, might be able to break US and EU hegemony in the multilateral

organization. Thus, China's participation will increase the voice of the developing

countries, so that the rules for the new game at WTO may become more balanced and

more beneficial to the developing countries.

Another political implication of China’s entry is that bilateral sources of trade friction,

notably with regard to accused Chinese dumping of chemicals in India, will be easier to

resolve because China will be under the ambit of the WTO Dispute Settlement Body

China will also become more transparent about its rules and regulations on trade and

investment. All relevant economic data about the country will have to be provided to the

WTO's general council. In case WTO members consider these laws or regulations to be

unfair, a dialogue can be initiated with China under the WTO's dispute settlement

mechanism. This greater transparency in trade practices and advance information can be

utilized in planning countermeasures to unfavorable policies..

10 Interview with Satish Deodhar on 14th December

Economic Fallouts China’s entry into the WTO is a double-edged sword for India. India compares

unfavorably with respect to China on almost all the major Macro economic indicators11.

India’s share of world exports stands at a meagre 0.6%, while China enjoys a 3.5% share

of the total world exports. China is ahead of India both in terms of trade openness as well

as its promised commitment to further trade liberalization.

As per commitments made to the WTO, weighted average tariff rates in India in 2005

will be around 30%, while in the same time frame China will reduce average tariff rates

to 9.44%. Quantitative restrictions (QR) in India remain on 2,714 tariff lines and India is

seeking 3-4 year phase out period of QRs. China has committed itself to phasing most

QRs out by 2002 and the rest by 2005. While agricultural tariffs in India will be in range

of 0 to 300%, average tariff in China will be in the range of 17% by end 2004. Further

China has agreed to remove agricultural export subsidies.

It might turn out in the long run that China has offered to deliver much more than what it

actually can, but in the present situation this is pressurizing India to open up at a much

faster pace and compete with China for foreign investments. In order to understand the

impact of China’s entry on Indian trade we need to analyze respective trade figures and

their projected growth trends.

A region wise analysis of India’s imports and exports shows that the US accounts for

9%12 of India’s imports and 23%13 of India’s exports. This positive trade balance has

increased quite dramatically from the year 199514,after India joined the WTO.

11 See Exhibit V 12 See Exhibit VI 13 See Exhibit VII 14 See Exhibit VIII

A similar analysis of China-US trade figures15 show that the trade balance between them

has reached an all time high in China’s favor. With China now being a member of the

WTO, this trade balance is likely to rise even further. As a large proportion of India’s

exports are to the US, a growth in Chinese exports to the US is a major threat to the

Indian economy.

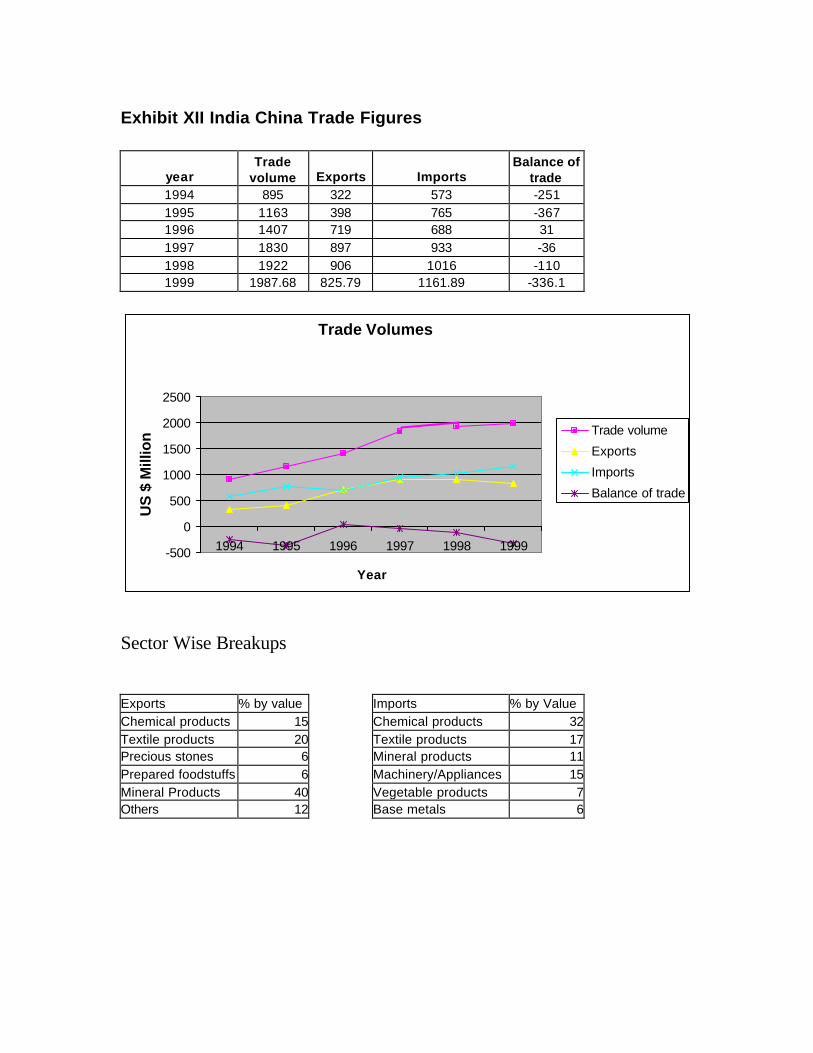

The effect on India-China bilateral trade is likely to be even more significant. The current

trade figures show a trade balance in China’s favor16. This balance is likely to move

upward after the entry of China into the WTO. Given the fact that China is one of the

largest suppliers of cheap labor- intensive goods in the world market, there are

apprehensions that cheap Chinese goods may flood the Indian market and spell disaster

for local manufacturers.

15 See Exhibit IX 16 See Exhibit X

Sector wise Analysis of Impacts

The major sectors that shall be impacted17 by China’s entry into the WTO are

Textiles

India has welcomed the move to facilitate China’s entry into the WTO in the hope that

the entry of China into the multilateral organization will increase the access of India’s

textiles into Chinese markets and China will also have to come out of its non-transparent

regime of export subsidies. The key question is whether China will get quota free access

in textiles, by January 1, 2005, when the clause in Agreement on Textile and Clothing

comes into force18. If China gets that, India will face more competition in textiles. In fact

the phasing-out of textile and apparel quotas by 2005 will enable China to wrest market

share from other low-cost Asian producers. The textile sector in India is already feeling

tremendous competitive pressure on their bottom line and many textile units are on the

verge of closure. With the easing of quantitative restrictions on imports in 2001, prices of

Chinese goods will ease further due to greater economies in exports.

Consumer Goods

The spur to competitiveness from lower tariffs will make Beijing an even more

formidable competitor in labor- intensive sectors such as shoes and toys. The Chinese are

exporting to India a wide range of low-cost consumer goods that have a mass market in

India such as kitchen-ware, textiles, electronic items, furniture, toys, cosmetics, footwear

and accessories. In fact in the last four years, there has been a deluge of cheap imports

from China – tyres, bicycles, watches and clocks, toys, plastics and dyes, and bulk drugs.

17 See Exhibit XI 18 Interview with G.S.Gupta on 14th December

In the very near future Indian scooter and motorcycle manufacturers are going to face

stiff competition from the Chinese. The sector that will be worst hit will be the small-

scale sector. The Chinese export import corporations are financially stronger, have more

efficient processes and turn out goods at extremely cheap prices. Armed with competitive

advantage of low price the Chinese are moving in new markets at a feverish pace and

Indian exports will also come under serious threat with the entry of China into the WTO.

Farm Products

China has committed to make agricultural import concessions. India has asked for lower

tariffs in 180 such commodities. As the Chinese get richer, their changing food habits

have made the country a net importer of farm products. Thanks to the green revolution

India’s agriculture generates surpluses, which needs places to be sold. Hence India’s

agricultural products shall find a ready market and benefit by China’s entry into the

WTO.

Information Technology Since 1991 India has discovered competitiveness in services, most notably in software.

While there is little bilateral business in this area at present, India’s InfoTech industry

will have to look beyond the West. China is determined to be a major player in the

coming revolution in InfoTech services like electronic commerce. There is hence a large

opportunity in this area for India to capitalize on its competitiveness and increase trade.

Recommendations In light of the threats as well as opportunities that present themselves after China’s

entry into the WTO, Indian policy makers need to take up a proactive approach

and formulate a long-term strategy for optimizing the benefits accruing to India.

The key measures in such a strategy would be

1. India must push for faster second generation economic reforms in the areas

of labour policies and power reforms. This would reduce the burden on

Indian industry and make Indian goods more competitive.

2. Greater attention also needs to be focused on developing basic

infrastructure, China is far ahead of India on this count and foreign

investors will move elsewhere unless the Government goes ahead with

reforms in this area

3. India must also pay greater attention to its trade relations with its Asian

neighbors and press for a larger role for SAARC19. The establishment of

SAFTA20 would go a long way towards boosting trade in the region

4. With the consumption cycle shortening, Indian industry it will have to

keep pace with international demand patterns. This means churning out

new products rapidly and gathering market intelligence.

5. India should not enter into investment- intensive areas. Instead low capital

requirement goods such as toys and home furnishings can be given a focus.

19 South Asian Association For Regional Cooperation 20 South Asian Free Trade Agreement

Conclusion

China’s entry into the WTO is viewed in India as a mixed blessing. On one

hand it helps India lend voice to its concerns in the WTO on the issue of

protecting domestic industry, but there are also large downsides as our exports

might become less competitive. There are also concerns that Chinese goods

would flood the Indian markets and spell doom for domestic producers.

China’s entry into the WTO also presents significant trade opportunities to

India as it gains access to the largest market in the world. Therefore, in order to

maximize its gains, India must adopt a forward looking strategy aimed both at

neutralizing Chinese competition by making Indian goods more competitive as

well as pushing Indian exports into China.

Exhibit I Key world economic indicators

Economic growth (%) Inflation (%)

1998 1999 2000 2001p 1998 1999 2000 2001p World 2.6 3.4 4.7 4.2 - - - - Industrialized countries 2.4 3.2 4.2 3.2 1.5 1.4 2.3 2.1 USA 4.4 4.2 5.2 3.2 1.6 2.2 3.2 2.6 European Union 2.7 2.4 3.4 3.3 1.4 1.4 2.1 1.9 Japan -2.5 0.2 1.4 1.8 0.6 -0.3 -0.2 0.5 Developing countries 3.5 3.8 5.6 5.7 10.1 6.6 6.2 5.2 Asia 4.1 5.9 6.7 6.6 7.5 2.4 2.4 3.3 Africa 3.1 2.2 3.4 4.4 9.1 11.8 12.7 8.6 Middle East & Europe 3.1 0.8 4.7 4.1 25.3 20.4 17.4 9.5 Western hemisphere 2.2 0.3 4.3 4.5 10.2 9.3 8.9 7 Transitional countries -0.8 2.4 4.9 4.1 21.8 43.8 18.3 12.5 Central and Eastern Europe

2 1.3 3.1 4.2 18.7 20.6 18.8 11.5

Russia -4.9 3.2 7 4 27.2 85.9 18.6 13.8 World Trade volumn 4.3 5.1 10 7.8 - - - - Average price of crude oil US$/barrel

13.1 18 26.5 23 - - - -

Percentage change -32.1 37.4 47.2 -13.2 - - - -

Source: International Monetary fund “World Economic Outlook” Article http://www.ktb.co.th/english/ec_indicator/index_world_indicator.htm. In http://www.ktb.co.th/english/ec_indicator/index_world_eco.htm. May, 2001

Exhibit II Overview of the World Economic Outlook Projections Current Projections

Difference from October 2000

projections 1999 2000 2001 2002 2000 2001

World output 3.5 4.8 3.2 3.9 — –1.0 Advanced economies 3.4 4.1 1.9 2.7 –0.1 –1.3 Major advanced economies 3 3.8 1.6 2.4 –0.1 –1.3 United States 4.2 5 1.5 2.5 –0.2 –1.7 Japan 0.8 1.7 0.6 1.5 0.3 –1.2 Germany 1.6 3 1.9 2.6 0.1 –1.4 France 3.2 3.2 2.6 2.6 –0.3 –0.9 Italy 1.6 2.9 2 2.5 –0.2 –1.0 United Kingdom 2.3 3 2.6 2.8 –0.1 –0.2 Canada 4.5 4.7 2.3 2.4 — –0.5 Other advanced economies 4.8 5.2 3 3.8 0.1 –1.2 Memorandum European Union 2.6 3.4 2.4 2.8 — –0.9 Euro area 2.6 3.4 2.4 2.8 –0.1 –1.0 Newly industrialized Asian economies 7.9 8.2 3.8 5.5 0.3 –2.3 Developing countries 3.8 5.8 5 5.6 0.1 –0.7 Africa 2.3 3 4.2 4.4 –0.5 –0.2 Developing Asia 6.1 6.9 5.9 6.3 0.2 –0.7 China 7.1 8 7 7.1 0.5 –0.3 India 6.6 6.4 5.6 6.1 –0.3 –0.9 ASEAN-42 2.8 5 3.4 4.7 0.5 –1.6 Middle East, Malta, and Turkey 0.8 5.4 2.9 4.6 0.5 –1.2 Western Hemisphere 0.2 4.1 3.7 4.4 –0.2 –0.8 Brazil 0.8 4.2 4.5 4.5 0.2 — Countries in transition 2.6 5.8 4 4.2 0.6 –0.2 Central and eastern Europe 1.8 3.8 3.9 4.4 — –0.7 Commonwealth of Independent States and Mongolia 3.1 7.1 4.1 4.1 1.1 0.1 Russia 3.2 7.5 4 4 0.5 — Excluding Russia 2.7 6.3 4.2 4.4 2.4 0.3

Exhibit III China: Macroeconomic Indicators

China's Economic Indicators, 1995-2000 1995 1996 1997 1998 1999 2000 Gross Domestic Product (GDP)

5,847.8 6,788.50 7,446.30 7,834.50 8,191.10 8,940.40

Real GDP growth (%) 10.5 9.6 8.8 7.8 7.1 8

Consumer price index (%) 17.1 8.3 2.8 0.8 -1.4 0.4

China's Industrial Output, 1995-2000 Gross value of industrial output 1995 1996 1997 1998 1999 2000Total industrial output 9,189.4 9,959.5 11,373.3 11,904.8 12,611.1 3,957.0% growth 20.3 16.6 13.1 10.8 11.6 9.9State-owned enterprises 3,122.00 3,617.30 3,596.80 3,362.10 3,557.10 1,403.20% growth 8.2 5.1 3.8 0.1 8.8 10.1Collective enterprises 3,362.30 3,923.20 4,334.70 4,573.00 4,460.70 330.1% growth 15.2 20.9 10.2 9.1 6 7.4Individual-owned enterprises 1,182.10 1,542.00 2,037.60 2,037.20 2,292.80 --% growth 51.5 20 15.4 14.7 14.4 --Other enterprises 1,523.10 1,658.20 2,098.20 2,727.00 3,296.20 1,028.70% growth 37.2 23.8 30.2 25.3 27.6 --

China's Financial Indicators, 1995-2000 1995 1996 1997 1998 1999 2000

Exchange rate * 8.4 8.3 8.3 8.3 8.3 8.3 Forex reserves ($bn)

73.6 105 139.9 145 154.7 165.6

Govt. revenue (total) 624.2 740.8 865.1 987.6 1,144.40 1,476.00 Tax revenue 603.8 691 823.4 926.3 1,068.30 1,266.00 Domestic debt 151.1 184.8 241.2 322.9 370.2 150* Foreign debt ($ bn) 106.6 116.3 131 146 151.8 -- Government deficit 58.2 53 58.2 92.2 174.4 259.8 SOURCES: National Bureau of Statistics, People’s Republic of China “PRC Main Economic Indicators” Article http://www.uschina.org/press/econmarch99.html. In uschina.org/press. 2 Feb, 2000

Exhibit VII Breakup of India’s Imports

Indian Imports: Region wise

31%

9%

3%32%

8%

7%

9% 1%

ECM Countries

E.F.T.A Countries

EAST EUROPE

ESCAP

REST OF ASIA &OCEANIAAFRICA

U.S.A

Legend: 1. E.C.M: European Common Market 2. E.F.T.A: European Free Trade Agreement 3. E.S.C.A.P: East, South and Central Asia-Pacific

Source: Ministry of Commerce and Industry, India “Annual Report, 2000-2001” Article http://commin.nic.in/doc/annual/App7.htm in commin.nic.in/doc/annual/App.htm Apr, 2001.

Exhibit VIII Breakup of India’s Exports

24%

1%

3%

1%

27%12%

5%

1%

23%

3%

ECM Countries

E.F.T.A

EAST EUROPEAN COUNTRIES

REST OF EUROPE

ESCAP

REST OF ASIA ANDOCEANIA

AFRICA

SOUTH AMERICA

U.S.A.

OTHER AMERICANAND CARRIBEANCOUNTRIES

India's Exports: Regionwise

Legend: 1. E.C.M: European Common Market 2. E.F.T.A: European Free Trade Agreement 3. E.S.C.A.P: East, South and Central Asia-Pacific

Source: Ministry of Commerce and Industry, India “Annual Report, 2000-2001” Article http://commin.nic.in/doc/annual/App5.htm in commin.nic.in/doc/annual/App.htm Apr, 2001.

Exhibit X Projected US-China Trade Figures

US Exports to China

01020304050

1995 2000 2005 2010

Years

$ B

illio

ns

US Exports toChina

Year $ Billions

1999 20.42000 222001 23.82002 25.72003 27.82004 302005 32.42006 352007 37.82008 40.82009 44.1

Source: K.C. Fung and Lawrence J. Lau, New Estimates of the United States-China Bilateral Trade Balances (Institute for International Studies, Stanford University, April 1999), p. 22.

Exhibit IX India US Trade Figures

Year Imports Exports Balance of Trade 1991 1,999.30 3,192.50 1,193.20 1992 1,917.10 3,779.80 1,862.70 1993 2,778.10 4,553.70 1,775.60 1994 2,294.00 5,309.50 3,015.50 1995 3,295.80 5,726.20 2,430.40 1996 3,328.30 6,169.50 2,841.20 1997 3,607.60 7,322.40 3,714.80 1998 3,564.40 8,237.20 4,672.80 1999 3,687.80 9,070.80 5,383.00 2000 3,662.80 10,686.50 7,023.70

India US Trade Figures

0.002,000.004,000.006,000.008,000.00

10,000.0012,000.00

1990 1995 2000 2005

Years

$ M

illio

ns

Imports ExportsBalance of trade

Source: U.S. Census Bureau “US-India Trade Statistics” Article http://www.indianembassy.org/indusrel/ind_us_trade_2000.html in http://www.indianembassy.org/indusrel Apr, 2001

Exhibit X US China Trade Figures

Year Imports Exports Trade Balance

1990 4.81 15.24 -10.431991 6.28 18.97 -12.691992 7.42 25.73 -18.311993 8.76 31.54 -22.781994 9.28 38.79 -29.501995 11.75 45.54 -33.791996 11.99 51.51 -39.521997 12.86 62.56 -49.701998 14.24 71.17 -56.931999 13.11 81.79 -68.682000 16.19 100.02 -83.83

Note: All figures in US $ Billions

US trade with China

-100.00

-50.00

0.00

50.00

100.00

150.00

1990

1992

1994

1996

1998

2000

Years

$ B

illio

ns Imports

ExportsTrade Balance

Source: U.S. Census Bureau “US-China Trade Statistics” Article http://www.census.gov/foreign-trade/balance/c5700.html in census.gov/foreign-trade/index.html Apr, 2001

Exhibit XII India China Trade Figures

year Trade

volume Exports Imports Balance of

trade 1994 895 322 573 -251 1995 1163 398 765 -367 1996 1407 719 688 31 1997 1830 897 933 -36 1998 1922 906 1016 -110 1999 1987.68 825.79 1161.89 -336.1

Trade Volumes

-500

0

500

1000

1500

2000

2500

1994 1995 1996 1997 1998 1999

Year

US

$ M

illio

n Trade volume

Exports

Imports

Balance of trade

Sector Wise Breakups

Exports % by value Imports % by Value Chemical products 15 Chemical products 32Textile products 20 Textile products 17Precious stones 6 Mineral products 11Prepared foodstuffs 6 Machinery/Appliances 15Mineral Products 40 Vegetable products 7Others 12 Base metals 6

Exports

% by value

15%

20%

6%6%

41%

12%

Chemicalproducts

Textile products

Precious stones

Preparedfoodstuffs

Mineral Products

Others

Imports

% by Value

32%

17%11%

15%

7%

6%

3%

9%

Chemicalproducts

Textile products

Mineral products

Machinery/Appliances

Vegetableproducts

Base metals

Assisi, Charles. “The misunderstood maharaja”, Express Investment Week, (9 November

1998), 18.

Bhargava, Anil. “Red Storm Rising”, Businessworld, (23 July 2001), 42.

Findlay, C., et al., Asia Pacific Air Transport: Challenges and Policy Reforms.

Singapore: Institute of Southeast Asian Studies, 1997.

[email protected] “PSU’s approved for disinvestment: Air India,” Article

divest.nic.in/psuapp/airindia.htm in divest.nic.in/index.htm. 17 May 2001.

Morrison, Steven; and Winston, Clifford. The Economic effects of Airline Deregulation.

Washington DC: The Blookings Institute, 1986.

Rao, D. Panduranga; and Rao, G. Venkata. Indian Airlines: A study of its performance.

New Delhi: Inter-India Publications, 1997.

Saraswati, Sujan Kumar. “Civil Aviation Environment in India”, Economic and Political

Weekly, (12 May 2001), 1639.

Taneja, Nawal K. The Commercial Airline Industry. Massachusetts: D.C. Health and

Company, 1976.

Exhibit I: Air India’s Present Financial Situation as on 31.3.20001

Paid up Capital Rs. 153.84 crores

Government of India Shareholding Rs. 153.84 crores (100%)

Net Worth Rs.401.97 crores

Net Profit/(Loss) Rs. (-) 37.63 crores

Number of Employees 17,169

Debt-to-equity ratio 10:1

1 [email protected] “PSU’s approved for disinvestment: Air India,” Article divest.nic.in/psuapp/airindia.htm in divest.nic.in/index.htm. 17 May 2001.