Embed Size (px)

Citation preview

Ilsue RohIlsue Roh

DCs’ IT Development and DCs’ IT Development and Remaining Challenges Remaining Challenges

10/10/2011 10/10/2011

2

ContentsContents

1. Korean IT Development Path

2. Success Factors of Korean IT Industry

3. Global IT Development Issues

4. Implementation of Policy Initiatives

ICT Development issues in Developing CountriesICT Development issues in Developing Countries

3

I. Korean IT Development I. Korean IT Development

PathPath

I. Korean IT Development I. Korean IT Development

PathPath

4

1. GDP Per Capita & Economic Growth

GDP ($)

5 Year Plan ofEconomic Development

5 Year Plan ofEconomic Development

67 U$67 U$

12,19612,196

1953

10,000

87 U$87 U$

1962

5,000

1996 1997

7,3557,355

2007

20,04520,045

1995

11,47111,471

Asian Financial Crisis

Asian Financial Crisis

1970 1980 2005

16,29116,291

20,000

2010

Export of 100 B. U$(87)Export of 100 B. U$(87)

Political Transition(88)Political Transition(88)

1987

GlobalFinancial Crisis

GlobalFinancial Crisis

IT Export of 100 B. U$(05)IT Export of 100 B. U$(05)

5

2. Growth Pattern of the Korean Economy

□ The Stage of Growth by innovation

- Labor oriented growth stage(1960 ~1970) :

- Capital oriented growth stage(1970 ~ 1990) :

- Innovation oriented growth stage(2000 ~ ) :

high tech. + Innovation

Years for Transition

UK 200 years

Japan 100 years

Korea 30 ~40 years

China 30 years

Natural Resources Based Economy ?

□ The Stage of Growth by innovation

- Labor oriented growth stage(1960 ~1970) :

- Capital oriented growth stage(1970 ~ 1990) :

- Innovation oriented growth stage(2000 ~ ) :

high tech. + Innovation

Years for Transition

UK 200 years

Japan 100 years

Korea 30 ~40 years

China 30 years

Natural Resources Based Economy ?

6

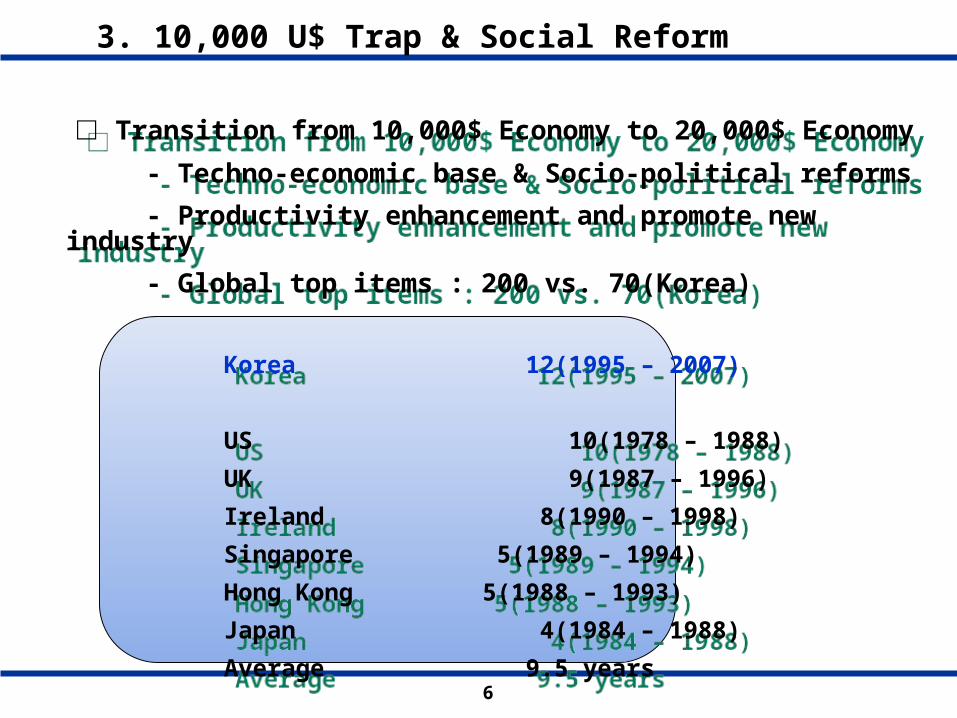

3. 10,000 U$ Trap & Social Reform

□ Transition from 10,000$ Economy to 20,000$ Economy

- Techno-economic base & Socio-political reforms

- Productivity enhancement and promote new industry

- Global top items : 200 vs. 70(Korea)

Korea 12(1995 – 2007)

US 10(1978 – 1988)

UK 9(1987 – 1996)

Ireland 8(1990 – 1998)

Singapore 5(1989 – 1994)

Hong Kong 5(1988 – 1993)

Japan 4(1984 – 1988)

Average 9.5 years

□ Transition from 10,000$ Economy to 20,000$ Economy

- Techno-economic base & Socio-political reforms

- Productivity enhancement and promote new industry

- Global top items : 200 vs. 70(Korea)

Korea 12(1995 – 2007)

US 10(1978 – 1988)

UK 9(1987 – 1996)

Ireland 8(1990 – 1998)

Singapore 5(1989 – 1994)

Hong Kong 5(1988 – 1993)

Japan 4(1984 – 1988)

Average 9.5 years

7

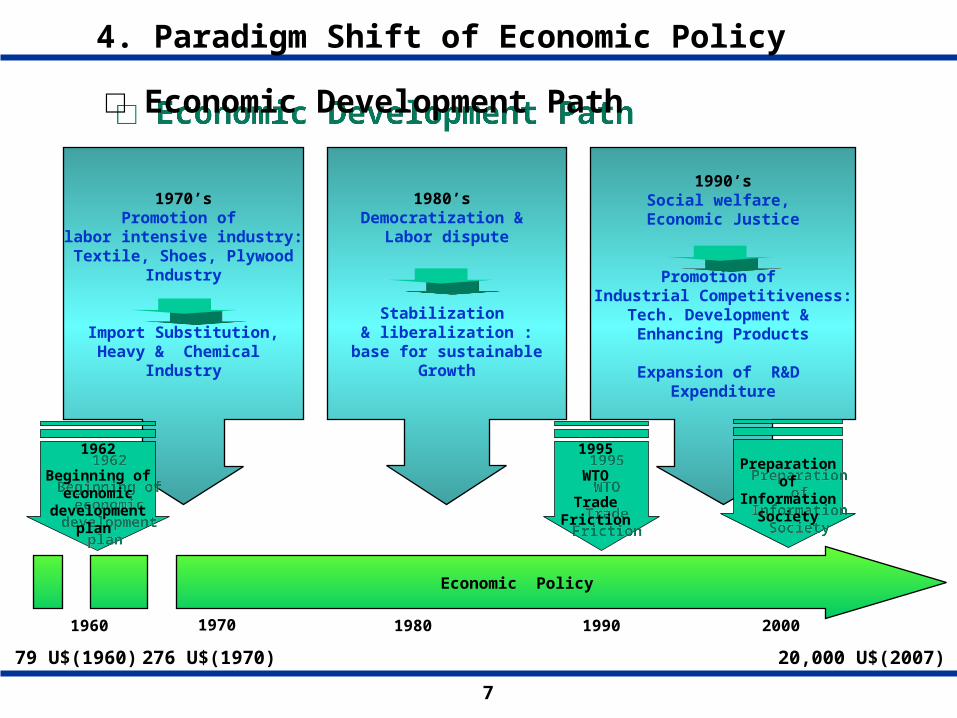

4. Paradigm Shift of Economic Policy

□ Economic Development Path □ Economic Development Path

Economic Policy

1970 1990 20001960

1970’sPromotion of

labor intensive industry:Textile, Shoes, Plywood

Industry

Import Substitution,Heavy & Chemical

Industry

1990’sSocial welfare,

Economic Justice

Promotion of Industrial Competitiveness:

Tech. Development & Enhancing Products

Expansion of R&D Expenditure

1980’s Democratization &

Labor dispute

Stabilization & liberalization :

base for sustainable Growth

1962

Beginning of economic

development plan

1962

Beginning of economic

development plan

1995

WTO

Trade Friction

1995

WTO

Trade Friction

276 U$(1970) 20,000 U$(2007)79 U$(1960)

Preparation of

Information Society

Preparation of

Information Society

1980

8

5. Paradigm Shift of Industry Policy

□ Industry Policy Drives to Innovation Drives □ Industry Policy Drives to Innovation Drives

Export-based Industry Policy

1980 1990 20001960

1970’s

Heavy & Chemical Industry

(Steel, Chemical, Machinery, Shipbuilding)

Mid 1990’s~

IT Industry

(DRAM(83), TDX(86),CDMA(96), LCD(97))

1980’s ~early 1990’s

Assembly &Processing Industry

(Electronics, Shipbuilding Automobile)

10 Mil. Mobile Phone Sub.(1998)1 Phone/ 1 House (1988)

Government Export Drive Private sector initiative

1970

9

’60s

Mechanics and electronics

tech. policy

’60s

Mechanics and electronics

tech. policy

Early ’80s

Beginning of IT Tech Policy

(launching TDX, Memory Chip,

PC project)

Early ’80s

Beginning of IT Tech Policy

(launching TDX, Memory Chip,

PC project)

Late ’80s

Beginning of industrial and

technology policy of

Mobile communications

Late ’80s

Beginning of industrial and

technology policy of

Mobile communications

’90s

Technology policy focused on

industrial policy

mid 90’s :CDMA

Late ’ 90 : ADSL, DTV, LCD

’90s

Technology policy focused on

industrial policy

mid 90’s :CDMA

Late ’ 90 : ADSL, DTV, LCD

Industry Policy

1980 1990 20001960

2000s ~

Technology policy nurturing

World class items

early 2000’s : Wibro, DMB

2000s ~

Technology policy nurturing

World class items

early 2000’s : Wibro, DMB

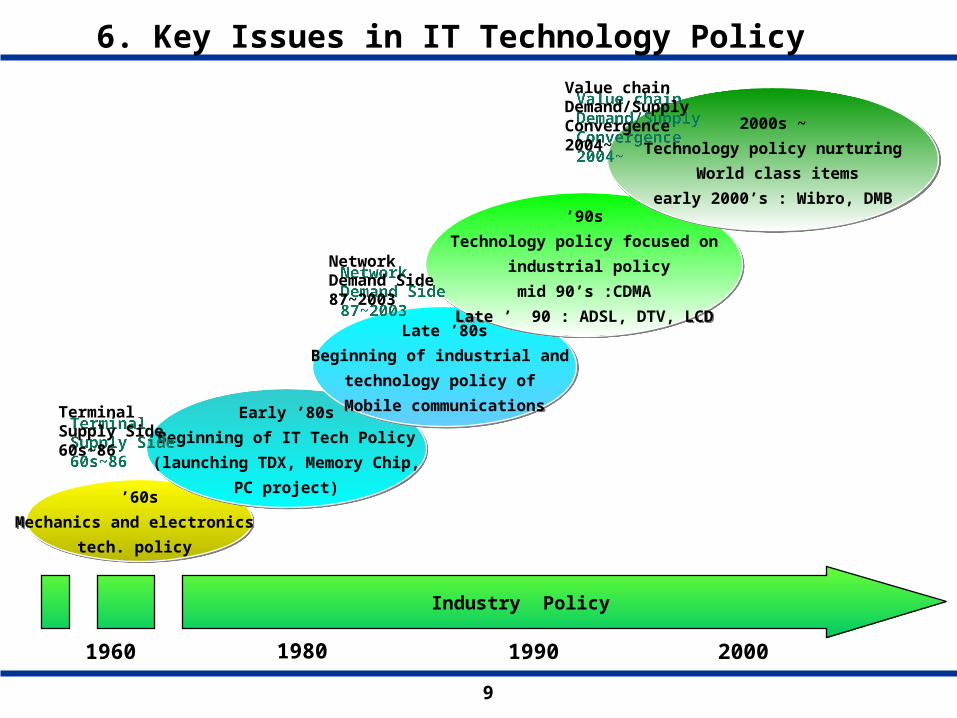

6. Key Issues in IT Technology Policy

TerminalSupply Side60s~86

TerminalSupply Side60s~86

NetworkDemand Side87~2003

NetworkDemand Side87~2003

Value chainDemand/Supply Convergence2004~

Value chainDemand/Supply Convergence2004~

10

7. Industrial Portfolio in 1980s

Growth

Profit

○ Automobile○ Automobile

○ Machinery○ Machinery

○ Electronics○ Electronics

○ Shipbuilding○ Shipbuilding

○ Construction○ Construction○ Textile

○ Textile

○ Chemical○ Chemical

○ Steel○ Steel

○ Precision Equipment

○ Precision Equipment ○ Precision

Chemistry

○ Precision Chemistry

Source : kang, Y. J. , KER, 2000

○ Leisure○ Leisure

AverageAverage

11

8. Industrial Portfolio in 1990s

Growth

Profit

○ Automobile○ Automobile

○ Machinery○ Machinery

○ Electronics○ Electronics

○ Shipbuilding○ Shipbuilding

○ Construction○ Construction

○ Textile○ Textile

○ Chemical○ Chemical

○ Steel○ Steel ○ Precision

Equipment

○ Precision Equipment

○ Precision Chemistry

○ Precision Chemistry

Source : kang, Y. J., KER, 2000

○ Computer○ Computer

○ Semi-Conductor○ Semi-Conductor

○ Leisure○ Leisure

AverageAverage

○ Business Service○ Business Service

12

9. Industrial Portfolio in 2000

Growth

Profit

○ Automobile○ Automobile

○ Machinery○ Machinery ○ Electronics

○ Electronics

○ Shipbuilding○ Shipbuilding

○ Construction○ Construction

○ Textile○ Textile

○ Chemical○ Chemical

○ Steel○ Steel

○ Precision Equipment○ Precision Equipment

○ Precision Chemistry ○ Precision Chemistry

Source : kang, Y. J., KER, 2000

○ Computer○ Computer

○ Semi- Conductor

○ Semi- Conductor

○ Communications Services

○ Communications Services

○ Communications Equipment

○ Communications Equipment

○ Leisure○ Leisure

AverageAverage

13

10. Positioning Changes of IT Industry

Growth

ProfitSource : kang, Y. J., KER, 2000

○ Electronics(90)○ Electronics(90)

○ Computer(90)○ Computer(90)

○ Semi-Conductor(98)○ Semi-Conductor(98)

○ Communications Services(90)

○ Communications Services(90)

○ Communications Equipment(98)

○ Communications Equipment(98)

AverageAverage

○ Computer(98)○ Computer(98) ○ Semi-Conductor(90)

○ Semi-Conductor(90)○ Electronics(98)

○ Electronics(98)

○ Communications Services(98)

○ Communications Services(98)

14

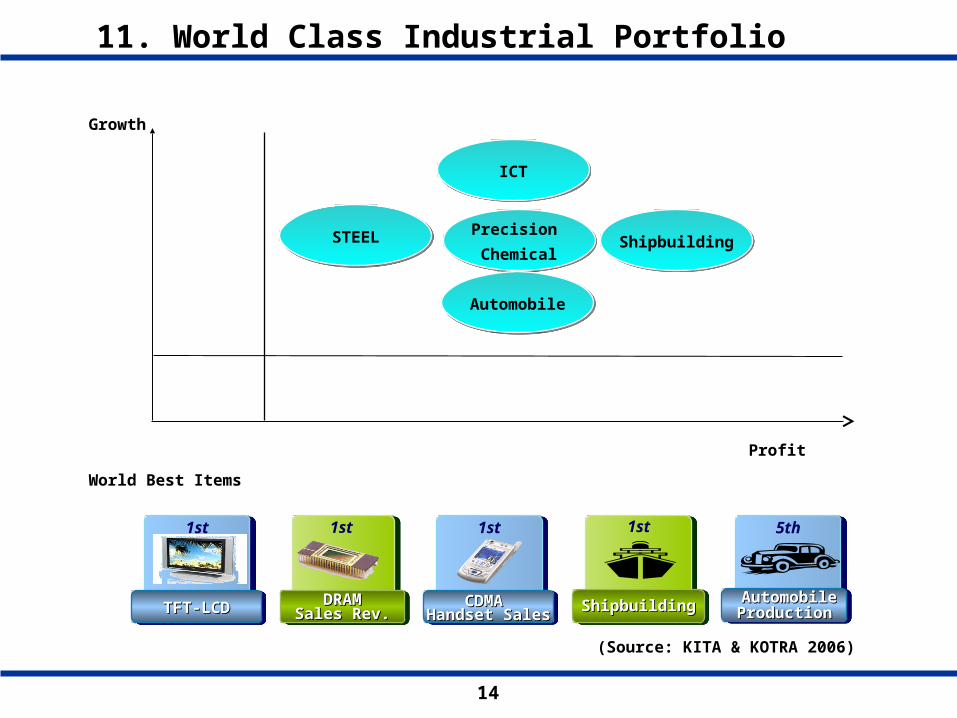

11. World Class Industrial Portfolio

Growth

Profit

STEELSTEEL

ICTICT

Precision

Chemical

Precision

Chemical

AutomobileAutomobile

ShipbuildingShipbuilding

DRAMDRAMSales Rev.Sales Rev.

DRAMDRAMSales Rev.Sales Rev.

1st

(Source: KITA & KOTRA 2006)

1st

CDMA CDMA Handset SalesHandset Sales

CDMA CDMA Handset SalesHandset Sales

Automobile Automobile ProductionProduction

Automobile Automobile ProductionProduction

5th

ShipbuildingShipbuildingShipbuildingShipbuilding

1st1st

TFT-LCDTFT-LCDTFT-LCDTFT-LCD

World Best Items

15

12. SWOT of Korean IT Industry

□ Strength : Mass Production, applied technology

Weakness : Source technology , S/W, global marketing

□ Strength : Mass Production, applied technology

Weakness : Source technology , S/W, global marketing

SS

○ CDMA & Mobile devices○ DTV, TFT-LCD○ STBox○ Semiconductor Tech.

○ CDMA & Mobile devices○ DTV, TFT-LCD○ STBox○ Semiconductor Tech.

WW

OO TT

○ Fiber, core tech. ○ S/W, Digital Contents○ Higher IT HR○ Product Planning & Marketing

○ Fiber, core tech. ○ S/W, Digital Contents○ Higher IT HR○ Product Planning & Marketing

○ Positioning global market○ Digital convergence btwn. telecom & broadcasting Industry ○ Increasing Internet user○ Worldclass IT Infra

○ Positioning global market○ Digital convergence btwn. telecom & broadcasting Industry ○ Increasing Internet user○ Worldclass IT Infra

○ Competition against foreign companies (Tech.)○ Follow up of developing countries (Wage) ○ Standardization Competition○ Strategic IPR Protection among advanced nations

○ Competition against foreign companies (Tech.)○ Follow up of developing countries (Wage) ○ Standardization Competition○ Strategic IPR Protection among advanced nations

16

13. Government’s R&D Investment Ratio

Ratio of private sector (Bil. U$)

Ratio of government sector(%)

DRAM, TDX, CDMA ?Machinery, Steel,

Chemical, shipbuilding,Automobile, electronics

Introduction P Catch up P Creative P

17

II. Success Factors of Korean II. Success Factors of Korean

IT IndustryIT Industry

II. Success Factors of Korean II. Success Factors of Korean

IT IndustryIT Industry

18

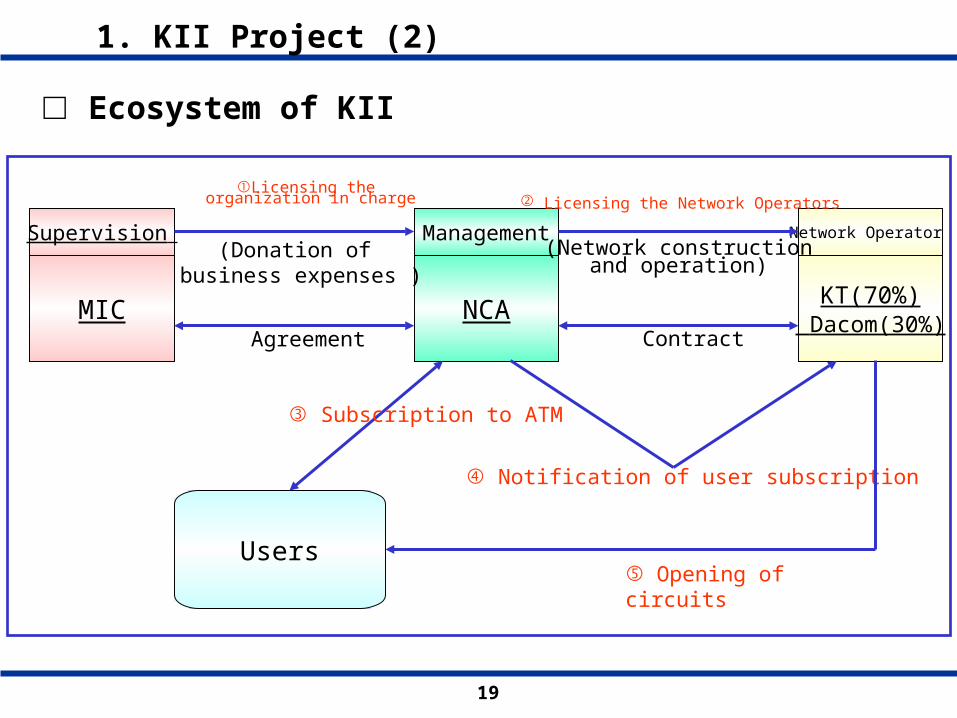

□ KII(Korea Information Infrastructure) Project

1. Background : • To enforce the national competitiveness • SOC in digital economy

2. Government strategy : • To take over the risk which might be resulted from large scale investment at the initial stage • To help the private sector to migrate smoothly to the information society 3. Main Players • MIC : Investment & project supervision • NCA(NIA) : Management on behalf of the government • KT and Dacom : Network installation and operation

1. KII Project (1)

19

□ Ecosystem of KII

1. KII Project (2)

Supervision

MIC

Management

NCA

Network Operator

KT(70%) Dacom(30%)

①Licensing the organization in charge

(Donation of business expenses )

Agreement

② Licensing the Network Operators

(Network construction and operation)

Contract

Users

③ Subscription to ATM

④ Notification of user subscription

⑤ Opening of circuits

20

1. KII Project (3)

Government

Users NetworkOperators

② Usage charge③ Contract charges = Usage charges + Deposit(Gov’t subsidy)

① Service provisioning

□ Financing for the KII

1. Government deposit to the operators account 2. Construction of KII by operators with the deposit 3. Government credit cleared as a part of contract charge(~40%)

4. Price differentiation • Group A: up to high Schools (70% of basic charges) • Group B: National and local governments Research, educational and cultural are institutuions Medical organization Medical insurance, non-profit organization(Basic charges) • Group C: others (130% of basic charges)

21

□ Internet Industry

1. Broadband internet apartment : • Highly urbanized population : 80% • Housing pattern : 50 % live in apartments • Internet cafe

2. Deregulation policy : • No entrance & price regulation, flat rate system

3. Facility-based competition • Hanaro telecom (ADSL, 1999) vs. cable modem service providers • KT (2000), major competition

4. Government’s role • Keeping price down • Strategic promotion in supplying PC and Internet • Keeping the demand of the user (e-education, e-trade)

2. Broadband Experience(1)

22

2. Broadband Experience(2)

* Hurry Psychology : faster speeder* Peer Pressure: intolerance for slower connection

□ Success Factors

* Enthusiastic Adoption of New Service * Various contents & Killer app.* Wholesale Demand: Internet Cafe

Cultural Acceptance

Demand

* Gov’t Initiatives : KII, Korea Information infra. e-Korea initiatives* Pro- Competition facility based competition Deregulation for ISP business* Certification System for Super High Speed Building

* Stiff Competition: 3 players, Price competition, facility based competition * Geographic Advantages: 50% of household in apartment complex* Dropping Network Costs: cost effective deployment, mass deployment and operating know-how

Policy & Regulation

Supply

23

□ Mobile Industry

1. Massive national R&D project - Successful establishment of government drive technology development system • Government : CDMA technology development project, Project Planning, roll assignment, funding, roadmap • Participants : Source tech. (Qualcom), commercial tech. (ETRI),

devices (Samsung, LGE, HE, Maxon) (devices), mobile

operator (SKT)

2. Selecting CDMA tech. : • GSM (industrialized tech.) • Early commercialization of CDMA Tech. : encouraging CDMA environment

3. Introducing competition & handset subsidy • 3rd telecom market reorganization • lower price & better services, explosive market demand & growth

3. Mobile Experience (1)

24

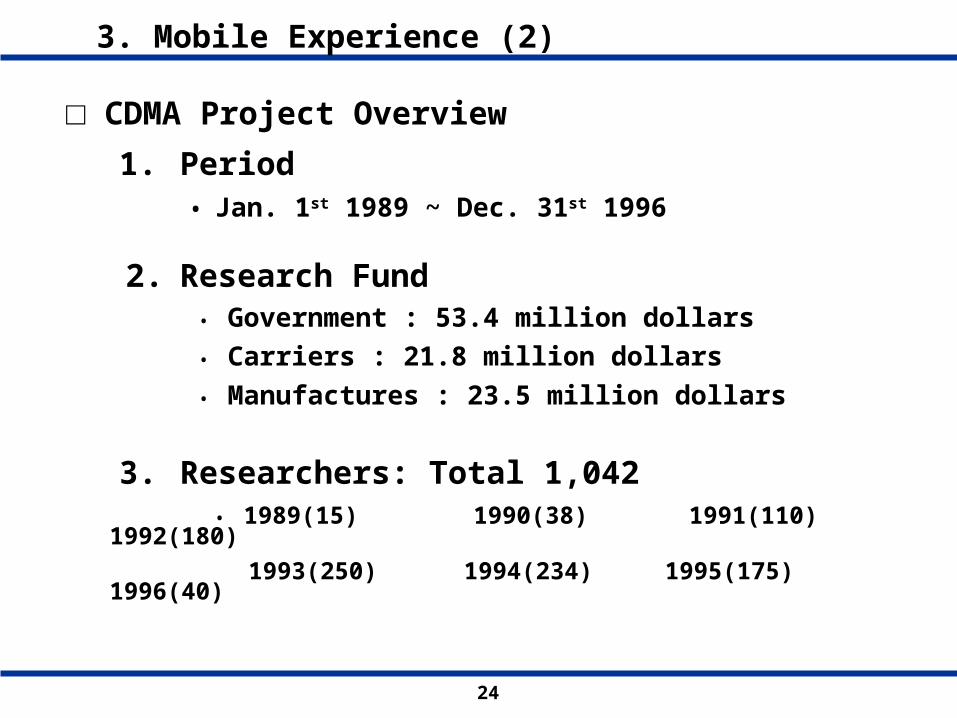

1. Period • Jan. 1st 1989 ~ Dec. 31st 1996

2. Research Fund • Government : 53.4 million dollars

• Carriers : 21.8 million dollars

• Manufactures : 23.5 million dollars

3. Researchers: Total 1,042 • 1989(15) 1990(38) 1991(110) 1992(180)

1993(250) 1994(234) 1995(175) 1996(40)

□ CDMA Project Overview

3. Mobile Experience (2)

25

QualcomQualcom ETRIETRI

System design/

dev. proto type

System design/

dev. proto typeJDA (Joint Development Agreement)JDA (Joint Development Agreement)

Joint research fund : 16.95 mil. U$Joint research fund : 16.95 mil. U$

DA (Designated Manufacturer)DA (Designated Manufacturer)

Infrastructure & Terminal Terminal

Royalty in advance : 8.50 mil. U$

Current royalty : domestic 6.0%

foreign 6.5%

Royalty in advance : 3.00 mil. U$

Current royalty : domestic 5.25%

foreign 5.75%

LGIC, Samsung, Hyundai Electronics Maxon

Dev. commercial system

Dev. commercial system

Source : ETRI, 2002

□ CDMA Joint Development Procedure

3. Mobile Experience (3)

26

Qualcomm

USA, Brazil, Argentina, China, India, Australia, Russia

SK Telecom(011)+ Shinsegi(017)

KT Freetel(016) + KT M.Com

LG PCS(019)

Foreign Mkt.

Others

ETRI

Samsung.

LG

Hyundai

Maxon

Telson

Hanwha

Pantech

Tech. Transfer

Royalty

Core Tech.

Parts Supplier

Domestic Suppliers

(First+Second)

Foreign Supplier

Manufacturers

PCS

Cellular

3. Mobile Experience (4)

□ The Structure of CDMA Industry

27

4. Success Story and its Effects

Economic effects

□ Unique Success Story and its Effects

Psychological effects

Better technology base

28

III. Global IT Development III. Global IT Development

issuesissues

III. Global IT Development III. Global IT Development

issuesissues

29

1. 3G Penetration Ratio

Source : ITU-D, 2010

□ The Rise of 3G

30

2. Global Mobile Subscription

Source : ITU-D, 2010

□ Growth Potential of Asia Pacific and Africa - Fast Growth in Asia Pacific - Greater potential in Africa

31

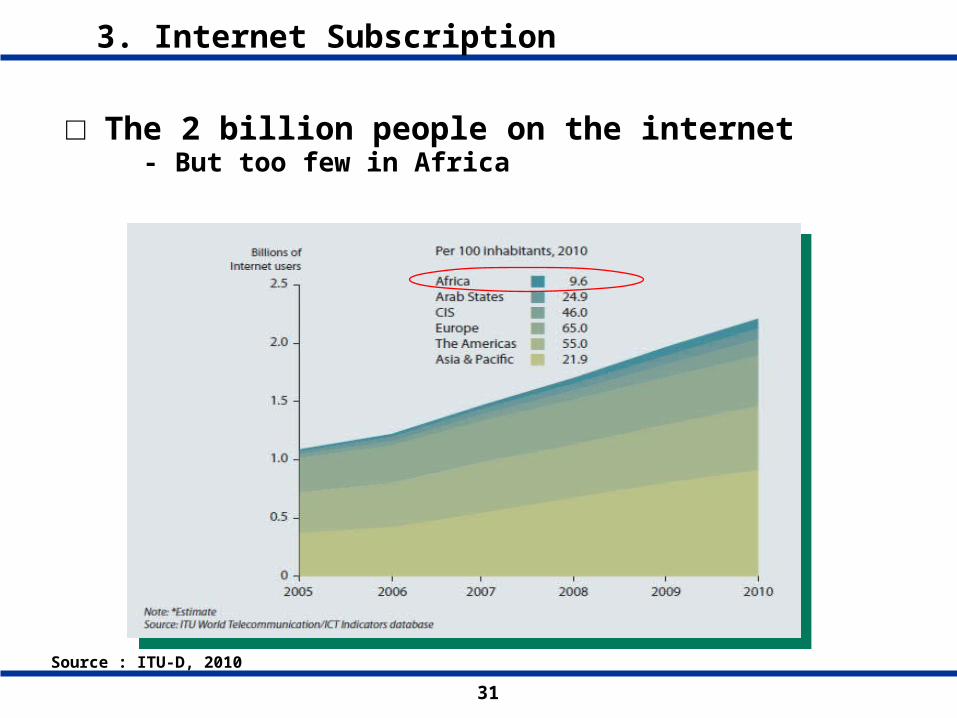

3. Internet Subscription

Source : ITU-D, 2010

□ The 2 billion people on the internet - But too few in Africa

32

4. Connecting Homes

Source : ITU-D, 2010

□ TV vs. Internet access

- Half a billion households worldwide (or 29.5%) have access to the Internet

33

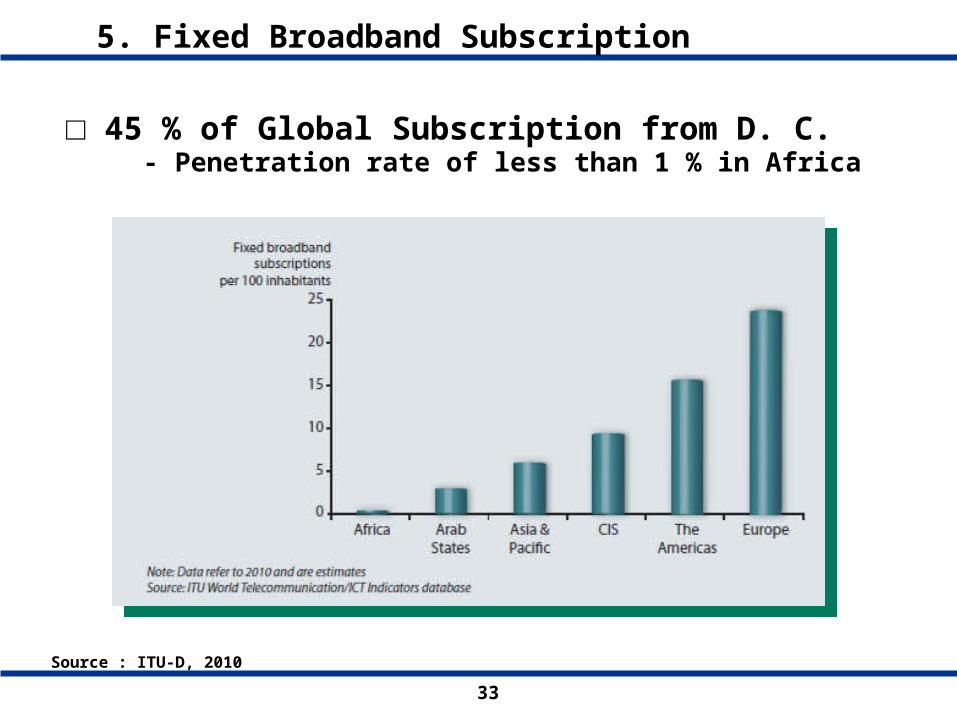

5. Fixed Broadband Subscription

Source : ITU-D, 2010

□ 45 % of Global Subscription from D. C. - Penetration rate of less than 1 % in Africa

34

6. Broadband Speed and Affordability

Source : ITU-D, 2010

□ Connection Speed and Average Price

35

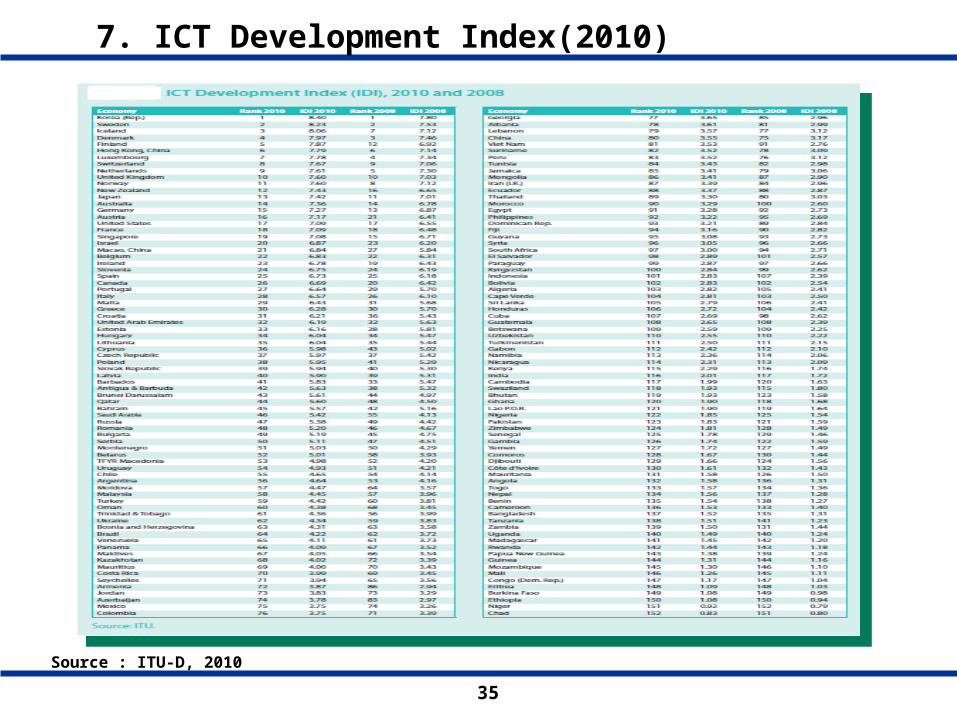

7. ICT Development Index(2010)

Source : ITU-D, 2010

36

8. IDI in Asia and Pacific(2010)

Source : ITU, 2010

37

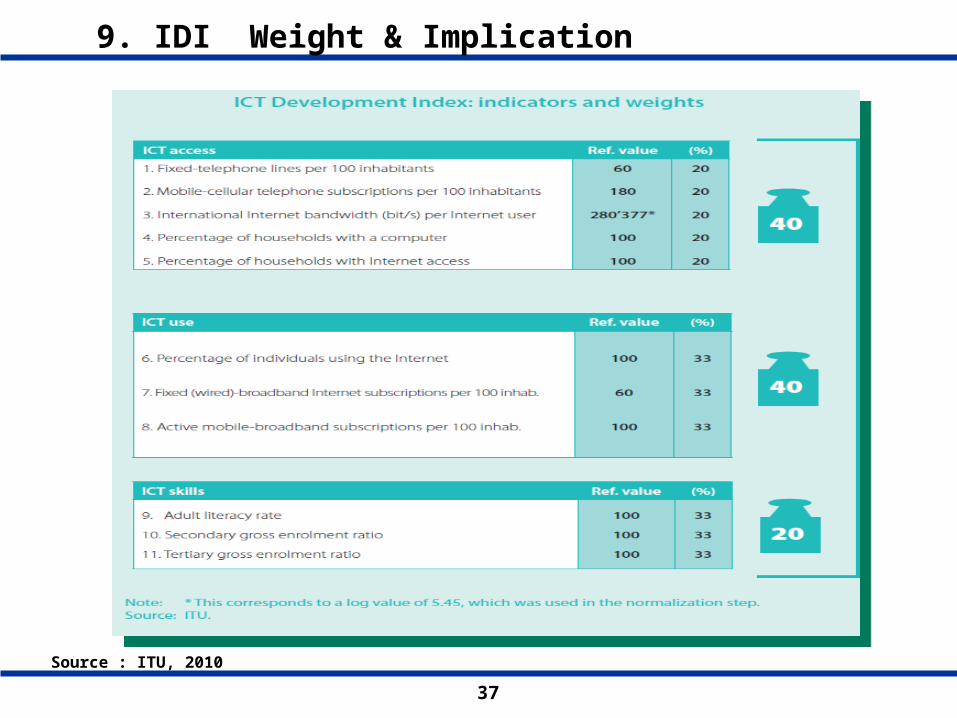

9. IDI Weight & Implication

Source : ITU, 2010

38

10. Economies by IDI (2010)

Source : ITU, 2010

39

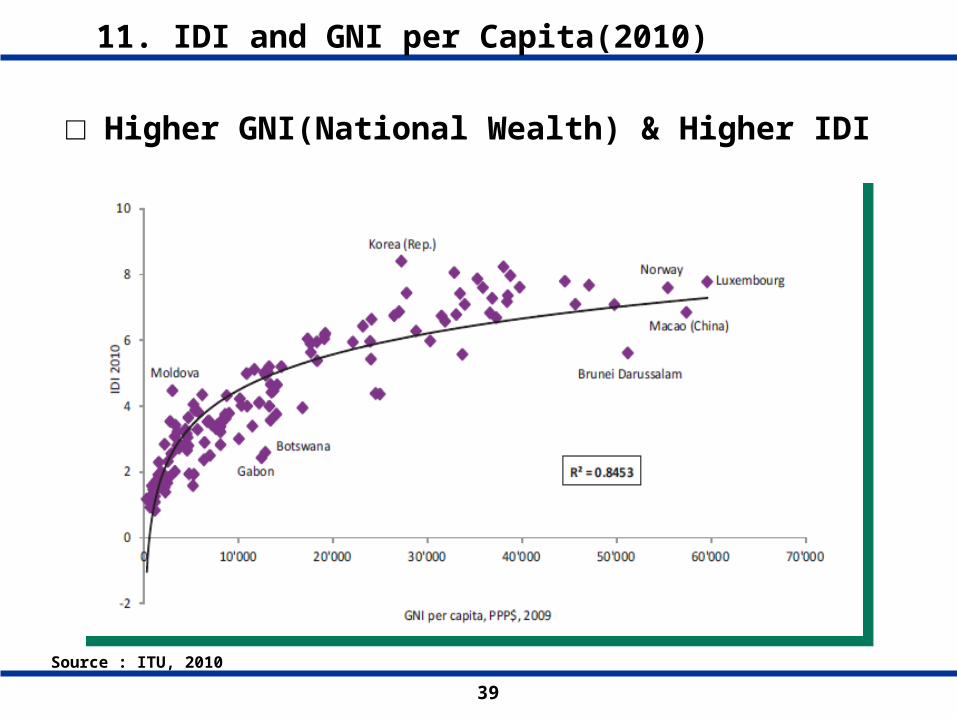

11. IDI and GNI per Capita(2010)

Source : ITU, 2010

□ Higher GNI(National Wealth) & Higher IDI

40

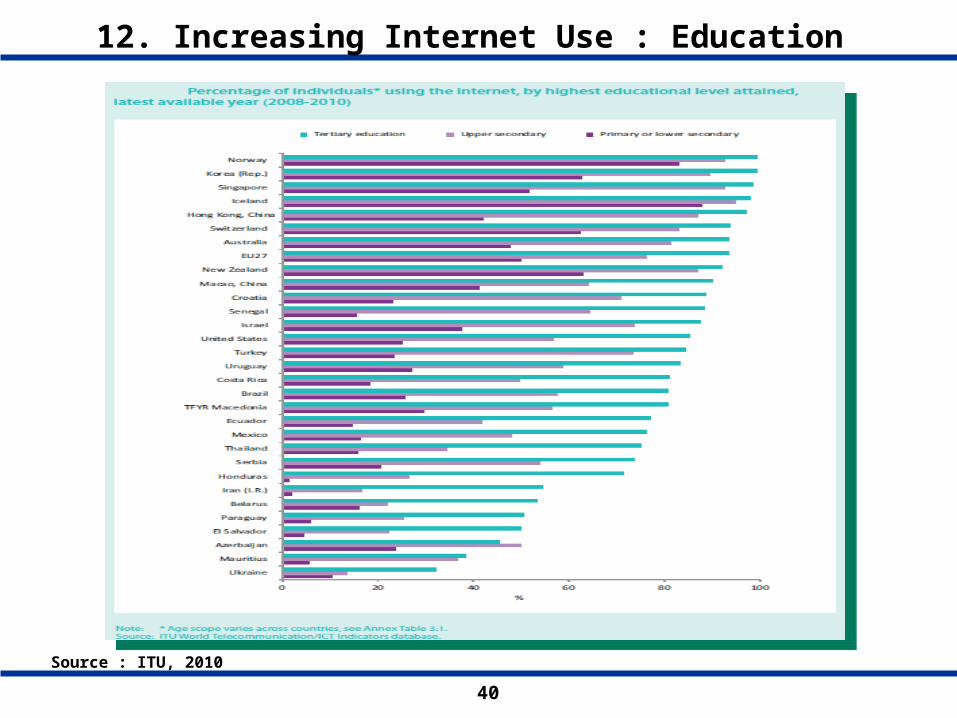

12. Increasing Internet Use : Education

Source : ITU, 2010

41

ICT as a Core Sector

ICT as an Enabler

Economic Development

Sustainable Industry

Competitive Knowledge Workers

Productivity

Social Equality

Education

13. Growth Engine

□ ICT is a Growth Engine of Socio-Economic Development

42

IV. Implementation of Policy IV. Implementation of Policy

InitiativesInitiatives

IV. Implementation of Policy IV. Implementation of Policy

InitiativesInitiatives

43

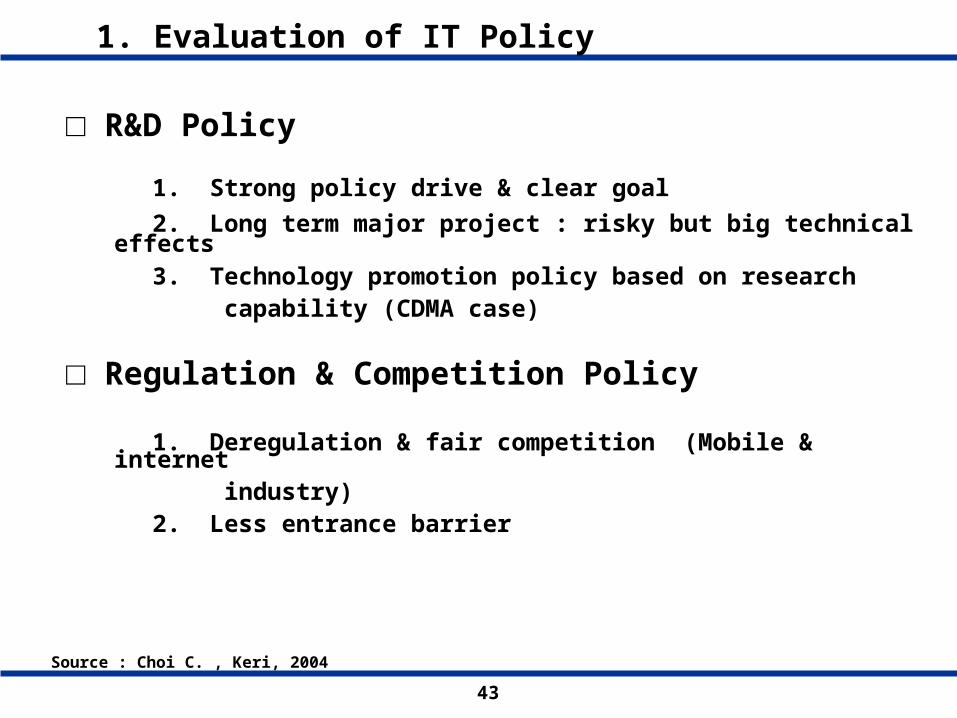

□ R&D Policy

1. Strong policy drive & clear goal

2. Long term major project : risky but big technical effects 3. Technology promotion policy based on research capability (CDMA case)

□ Regulation & Competition Policy 1. Deregulation & fair competition (Mobile & internet industry) 2. Less entrance barrier

1. Evaluation of IT Policy

Source : Choi C. , Keri, 2004

44

□ Corporation Policy

1. Evaluate the role of the major corporation in IT industry 2. Capability not Size

□ IT Policy

1. Deregulation & fair competition

2. Facility based competition 3. Emphasizing Frontier spirit for better industrial innovation

2. Evaluation of IT Policy

Source : Choi, C. K. , Keri, 2004

45

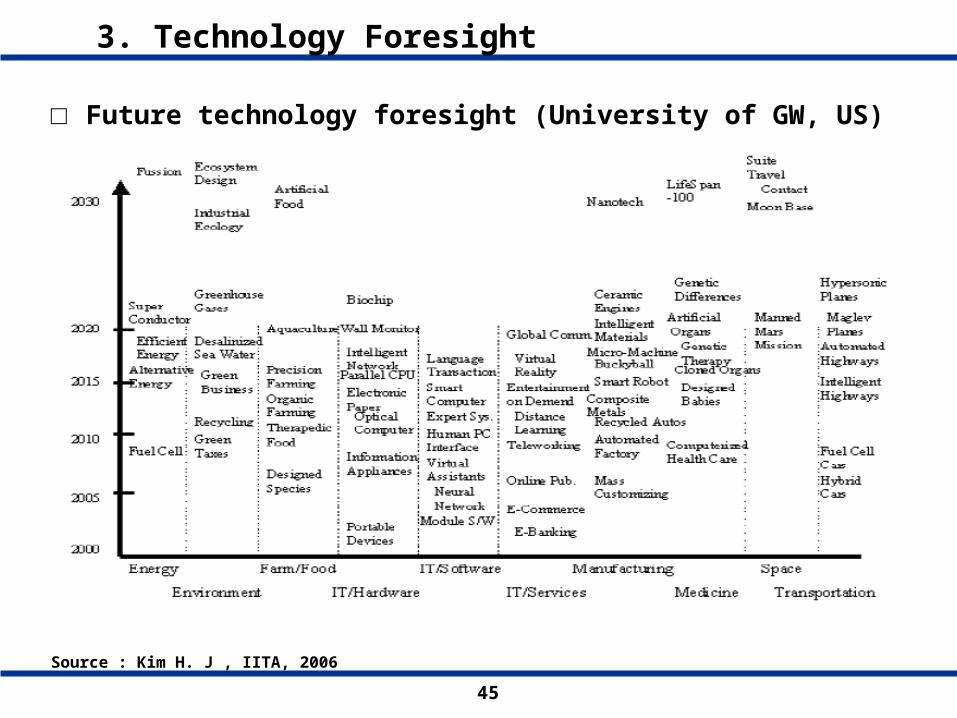

Source : Kim H. J , IITA, 2006

3. Technology Foresight

□ Future technology foresight (University of GW, US)

46

□ TEP & SIF 1. Techno-Economic Paradigm (TEP)

2. Socio-Institutional Framework (SIF)

- Good match

- Mismatch: structural crisis

4. New System

47

Thank You !Thank You !

Questionnaire

ETRI

Ilsue Roh

email : [email protected]

Phone: 82-42-860-1135