Embed Size (px)

Citation preview

FPS 2008 Organized by IBC: 23rd annual FPSO conference in this series

London, 3-4 December 2008

www.devonenergy.com 2 of 55NYSE: DVN www.devonenergy.com

An Operator’s Outlook for FPSOsin the Ultra Deepwater Gulf of Mexico

Peter Lovie

Devon Energy CorporationHouston, Texas

www.devonenergy.com 3 of 55

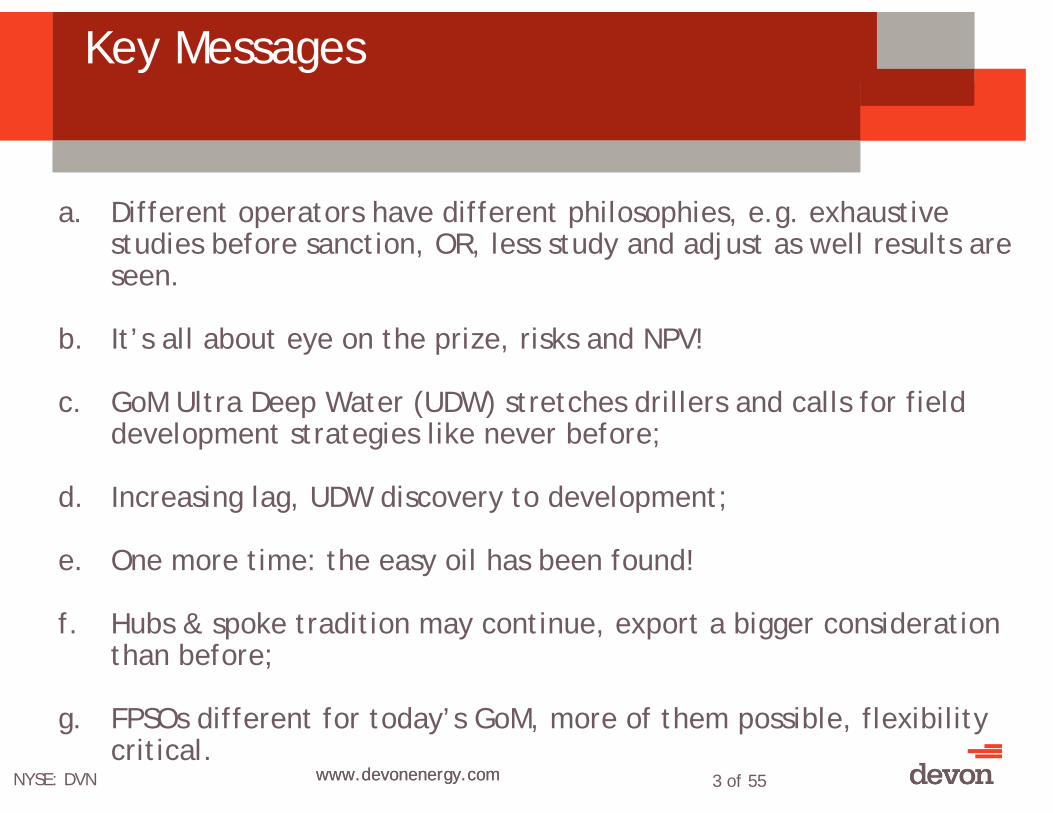

Key Messages

NYSE: DVN www.devonenergy.com

a. Different operators have different philosophies, e.g. exhaustivestudies before sanction, OR, less study and adjust as well results are seen.

b. It’s all about eye on the prize, risks and NPV!

c. GoM Ultra Deep Water (UDW) stretches drillers and calls for field development strategies like never before;

d. Increasing lag, UDW discovery to development;

e. One more time: the easy oil has been found!

f. Hubs & spoke tradition may continue, export a bigger consideration than before;

g. FPSOs different for today’s GoM, more of them possible, flexibility critical.

www.devonenergy.com 4 of 55

Today’s Agenda

1. Focus on production from remote prospects;

2. High stakes frontier: extreme physical, risk and financial challenges;

3. Highly prospective but risks slow sanction;

4. Huge drilling investments affecting facility choice;

5. Export issues – the coming shootout: pipelines and shuttle tankers;

6. Projecting what lies ahead for FPSOs in UDW GoM.

NYSE: DVN www.devonenergy.com

An idea of Devon’s frame of reference

www.devonenergy.com 5 of 55NYSE: DVN www.devonenergy.com

1. Focus on Production from Remote Prospects

Very deep wells far from shore over mountainous seabed

www.devonenergy.com 6 of 55

History in GoM

MMS/USCG approval in principle achieved in Record of Decision in December 2001 for FPSOs and shuttle tankers in US waters;

For service in US waters FPSOs can be built anywhere. In contrastshuttle tankers must be owned, built and crewed in US;

For the record, the first two FPSOs in GoM were in Mexican waters:1st FPSO 1989 Owned by Pemex1st FSO 1998 Charter from Modec2nd FPSO 2007 Charter from BW Offshore

Third FPSO in GoM - and first on US side - was contracted in 2007 toenter service in 2010.

NYSE: DVN www.devonenergy.com

GoM far behind the rest of the world in employing FPSOs

www.devonenergy.com 7 of 55NYSE: DVN www.devonenergy.com

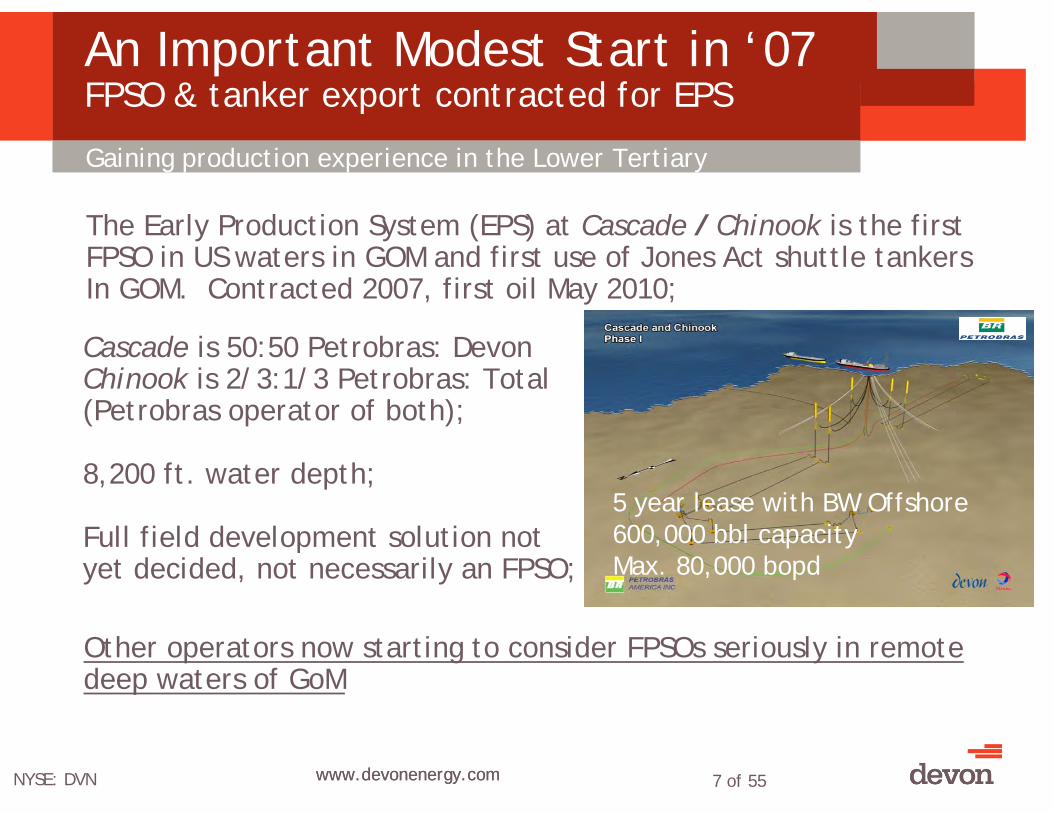

The Early Production System (EPS) at Cascade / Chinook is the firstFPSO in US waters in GOM and first use of Jones Act shuttle tankersIn GOM. Contracted 2007, first oil May 2010;

Cascade is 50:50 Petrobras: DevonChinook is 2/3:1/3 Petrobras: Total(Petrobras operator of both);

8,200 ft. water depth;

Full field development solution notyet decided, not necessarily an FPSO;

5 year lease with BW Offshore600,000 bbl capacityMax. 80,000 bopd

An Important Modest Start in ‘07FPSO & tanker export contracted for EPS

Other operators now starting to consider FPSOs seriously in remote deep waters of GoM

Gaining production experience in the Lower Tertiary

www.devonenergy.com 8 of 55NYSE: DVN www.devonenergy.com 8 of 69

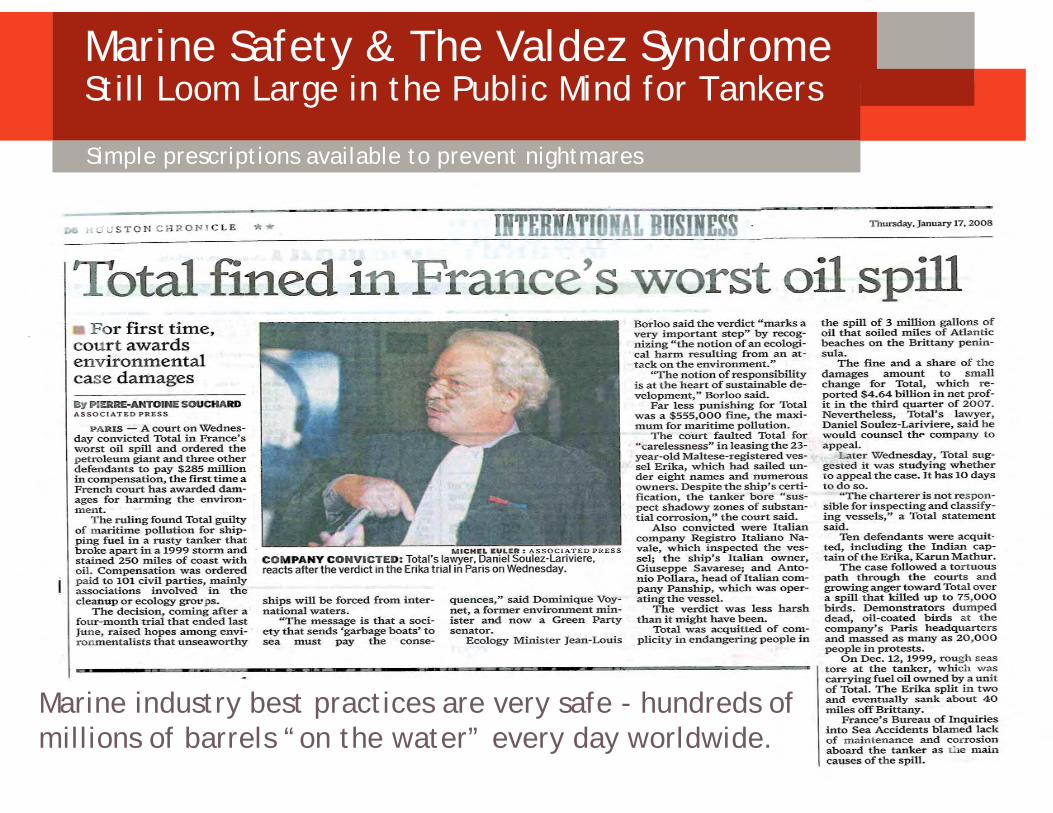

Marine industry best practices are very safe - hundreds of millions of barrels “on the water” every day worldwide.

Simple prescriptions available to prevent nightmares

Marine Safety & The Valdez SyndromeStill Loom Large in the Public Mind for Tankers

www.devonenergy.com 9 of 55

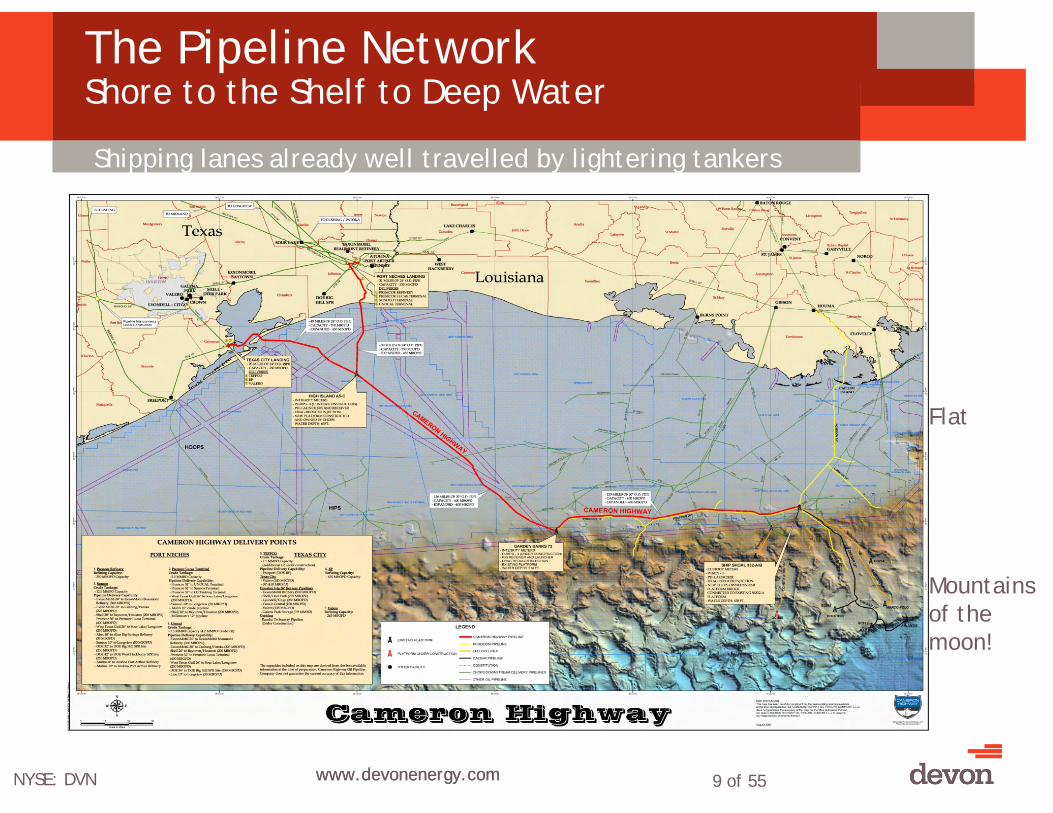

The Pipeline Network Shore to the Shelf to Deep Water

NYSE: DVN www.devonenergy.com

Flat

Mountains of the moon!

Shipping lanes already well travelled by lightering tankers

www.devonenergy.com 10 of 55NYSE: DVN www.devonenergy.com

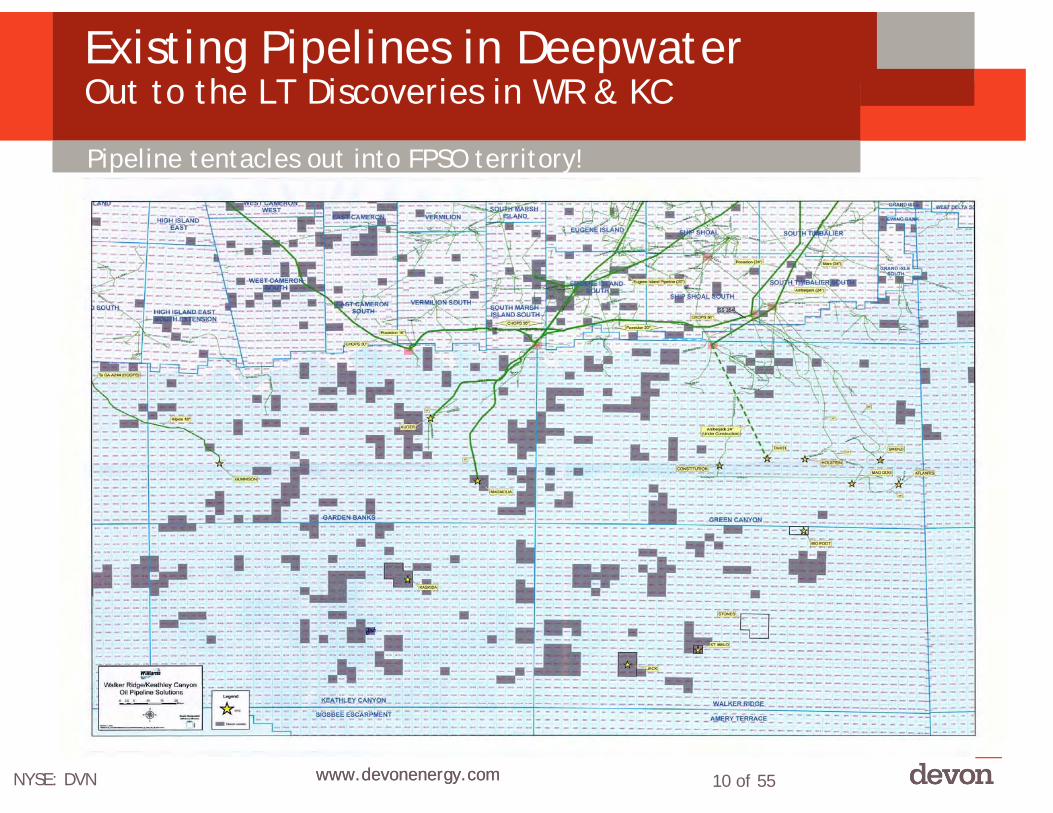

Existing Pipelines in DeepwaterOut to the LT Discoveries in WR & KC

Pipeline tentacles out into FPSO territory!

www.devonenergy.com 11 of 55NYSE: DVN www.devonenergy.com

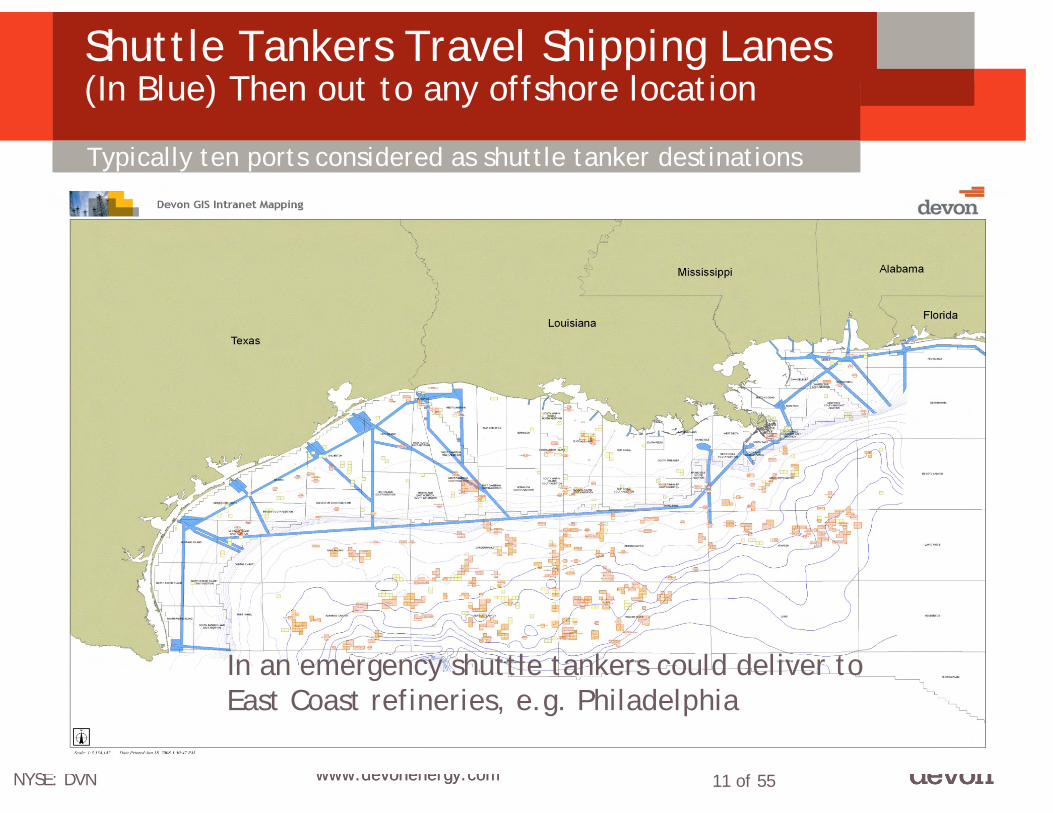

Typically ten ports considered as shuttle tanker destinations

In an emergency shuttle tankers could deliver to East Coast refineries, e.g. Philadelphia

Shuttle Tankers Travel Shipping Lanes(In Blue) Then out to any offshore location

www.devonenergy.com 12 of 55

For GoM, the Final Frontier.

For Devon, a Priority.

NYSE: DVN www.devonenergy.com

2. High Stakes Frontier:Extreme Physical, Risk andFinancial Challenges;

www.devonenergy.com 13 of 55

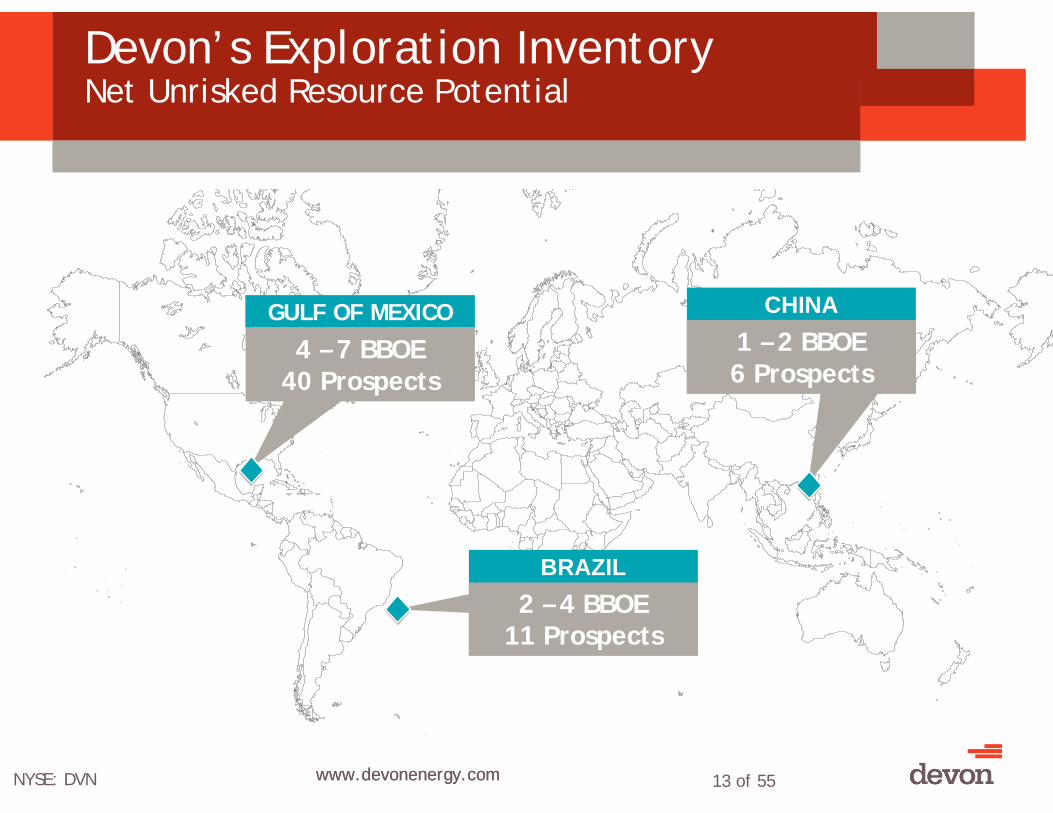

Devon’s Exploration InventoryNet Unrisked Resource Potential

NYSE: DVN www.devonenergy.com

GULF OF MEXICO CHINA

4 – 7 BBOE40 Prospects

2 – 4 BBOE11 Prospects

BRAZIL

1 – 2 BBOE6 Prospects

www.devonenergy.com 14 of 55

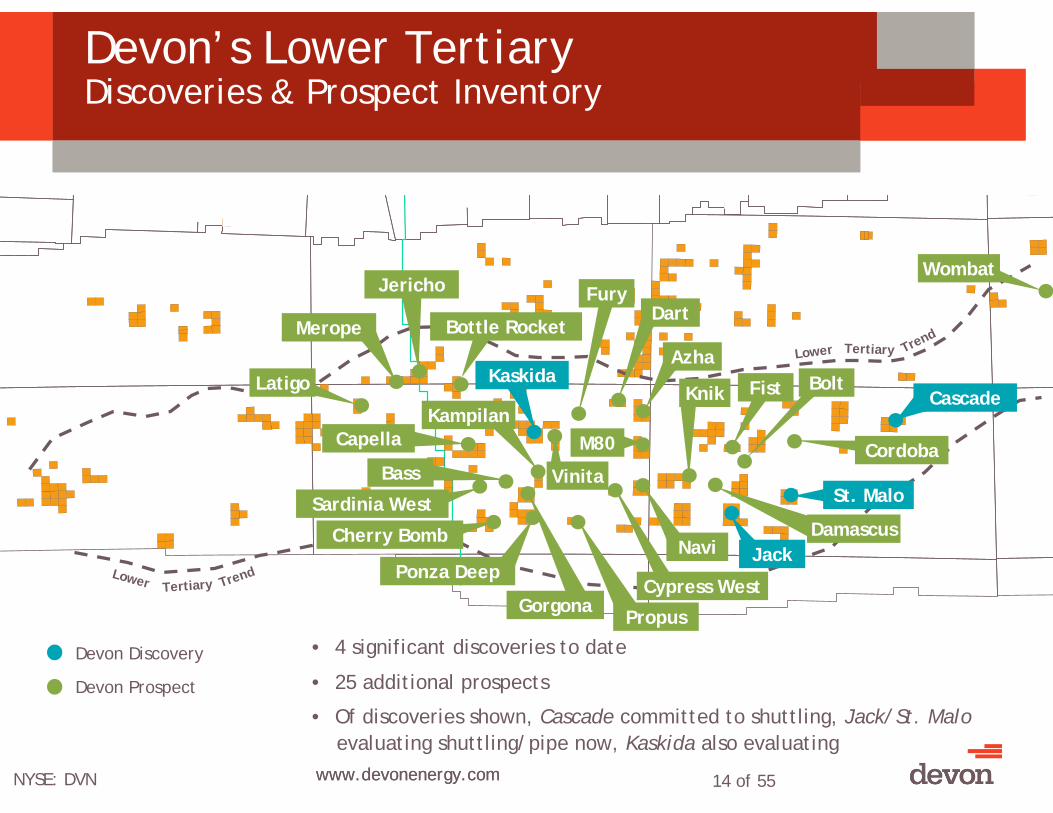

Devon’s Lower TertiaryDiscoveries & Prospect Inventory

NYSE: DVN www.devonenergy.com

TertiaryLower Trend

Trend

• 4 significant discoveries to date

• 25 additional prospects

• Of discoveries shown, Cascade committed to shuttling, Jack/St. Maloevaluating shuttling/pipe now, Kaskida also evaluating

Devon Discovery

Devon Prospect

Cascade

Jack

Kaskida

St. Malo

Merope

Cherry Bomb

Capella

Sardinia West

Propus

Bottle Rocket

Gorgona

Navi

Knik

M80

Jericho

Vinita

Cypress West

Bass

Azha

Dart

Latigo

TertiaryLower Trend Ponza Deep

FistKampilan

Bolt

FuryWombat

Damascus

Cordoba

www.devonenergy.com 15 of 55

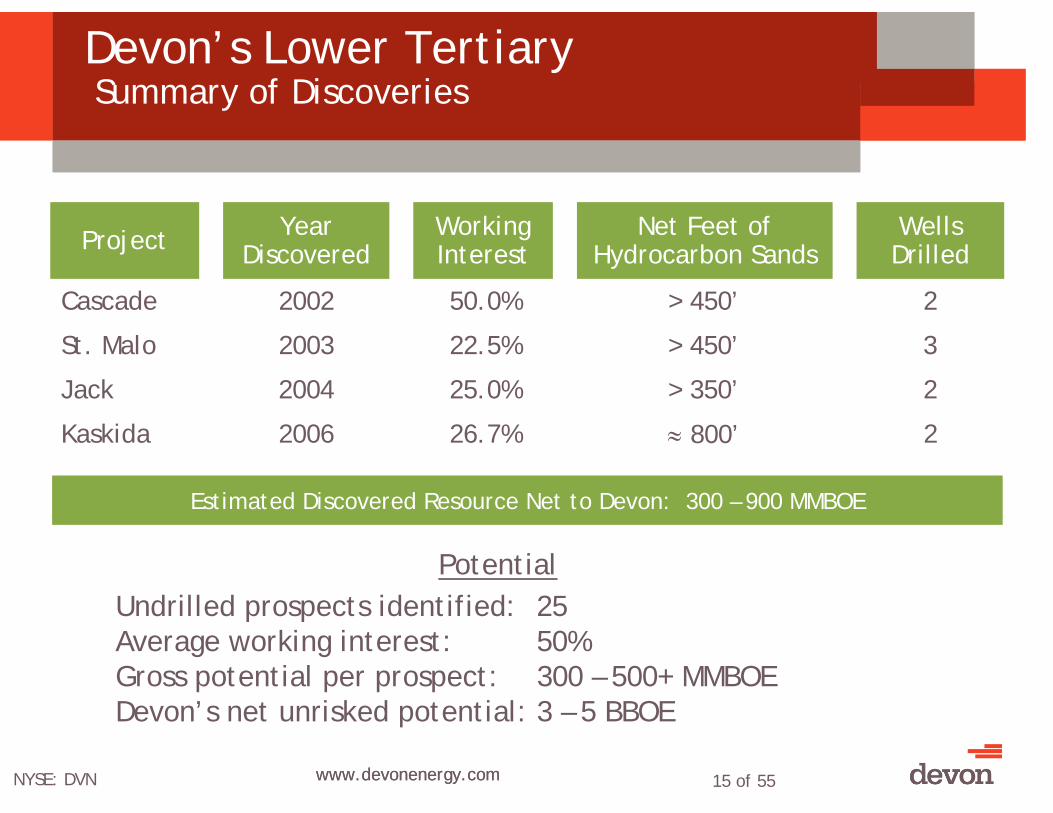

Project Year Discovered

Working Interest

Net Feet of Hydrocarbon Sands

Wells Drilled

Cascade 2002 50.0% > 450’ 2

St. Malo 2003 22.5% > 450’ 3

Jack 2004 25.0% > 350’ 2

Kaskida 2006 26.7% ≈ 800’ 2

NYSE: DVN www.devonenergy.com

Estimated Discovered Resource Net to Devon: 300 – 900 MMBOE

Devon’s Lower Tertiary Summary of Discoveries

Undrilled prospects identified: 25Average working interest: 50%Gross potential per prospect: 300 – 500+ MMBOEDevon’s net unrisked potential: 3 – 5 BBOE

Potential

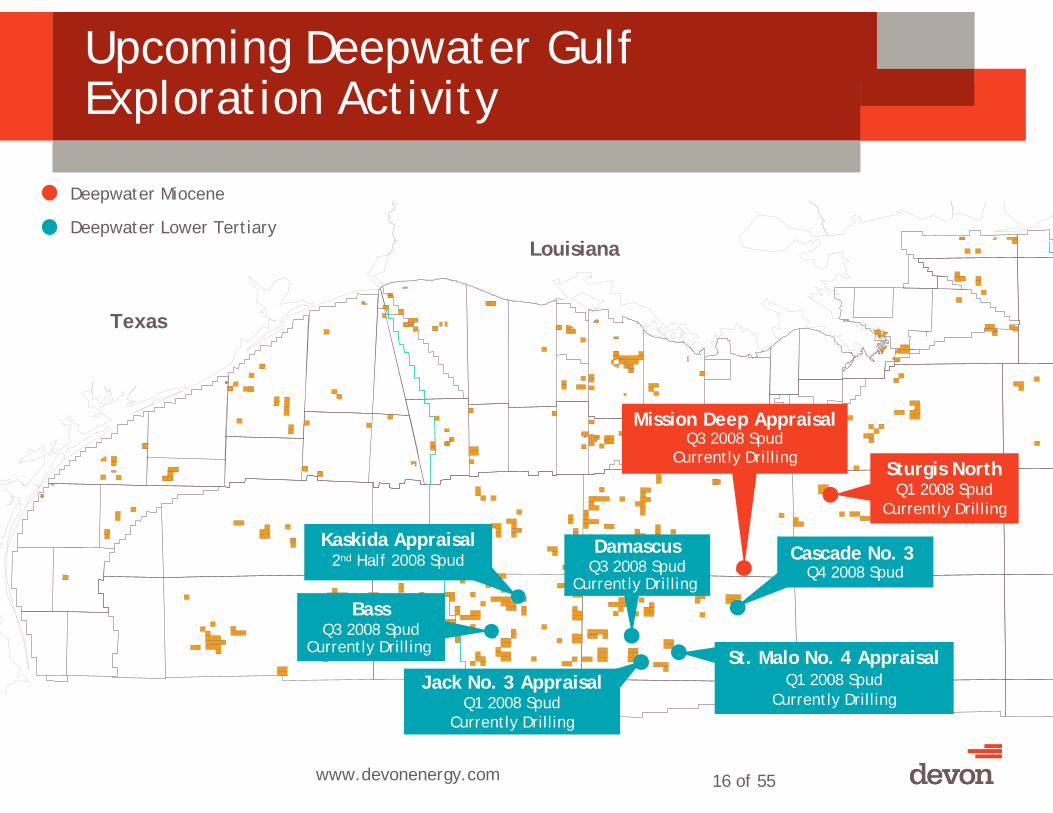

www.devonenergy.com 16 of 55

Texas

Louisiana

Upcoming Deepwater Gulf Exploration Activity

Jack No. 3 AppraisalQ1 2008 Spud

Currently Drilling

Sturgis NorthQ1 2008 Spud

Currently Drilling

Cascade No. 3 Q4 2008 Spud

Deepwater Miocene

Deepwater Lower Tertiary

St. Malo No. 4 AppraisalQ1 2008 Spud

Currently Drilling

Kaskida Appraisal2nd Half 2008 Spud

BassQ3 2008 Spud

Currently Drilling

Mission Deep AppraisalQ3 2008 Spud

Currently Drilling

DamascusQ3 2008 Spud

Currently Drilling

www.devonenergy.com 17 of 55

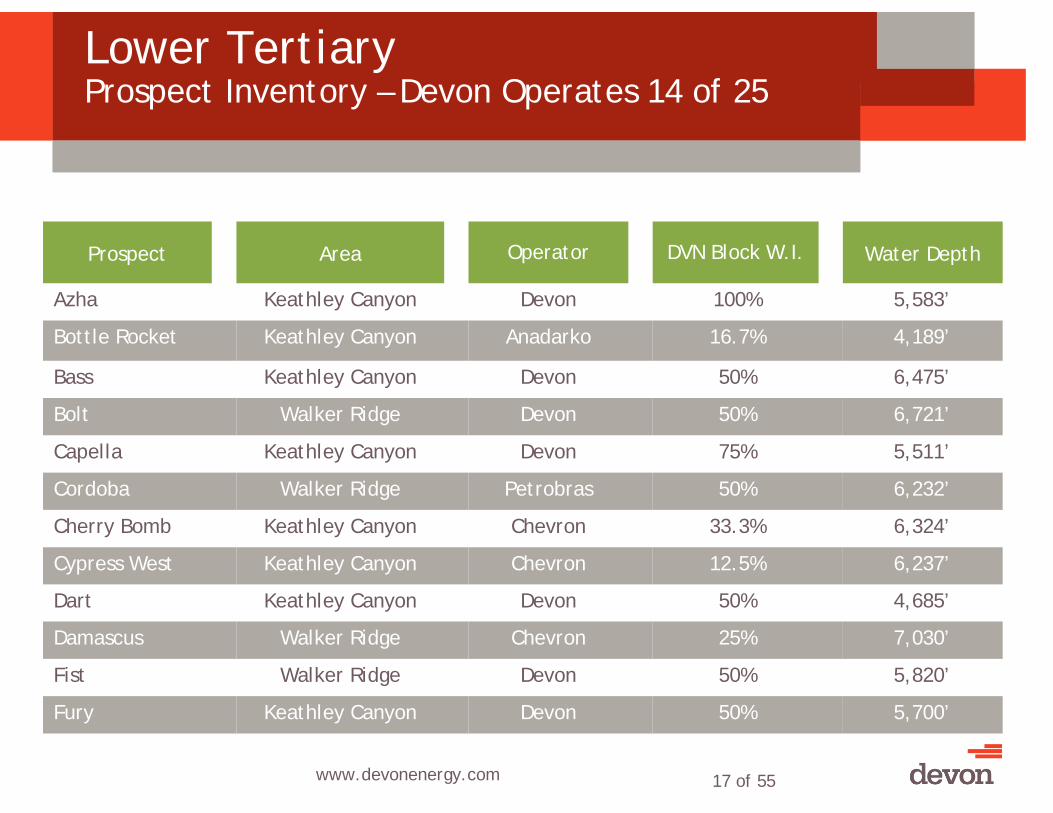

5,700’50%DevonKeathley CanyonFury

6,721’50%DevonWalker RidgeBolt

6,232’50%PetrobrasWalker RidgeCordoba

7,030’25%ChevronWalker RidgeDamascus

4,685’50%DevonKeathley CanyonDart

5,820’50%DevonWalker RidgeFist

6,237’12.5%ChevronKeathley CanyonCypress West

6,324’33.3%ChevronKeathley CanyonCherry Bomb

5,511’75%DevonKeathley CanyonCapella

6,475’50%DevonKeathley CanyonBass

4,189’16.7%AnadarkoKeathley CanyonBottle Rocket

5,583’100%DevonKeathley CanyonAzha

Prospect Water DepthDVN Block W.I.OperatorArea

Lower Tertiary Prospect Inventory – Devon Operates 14 of 25

www.devonenergy.com 18 of 55

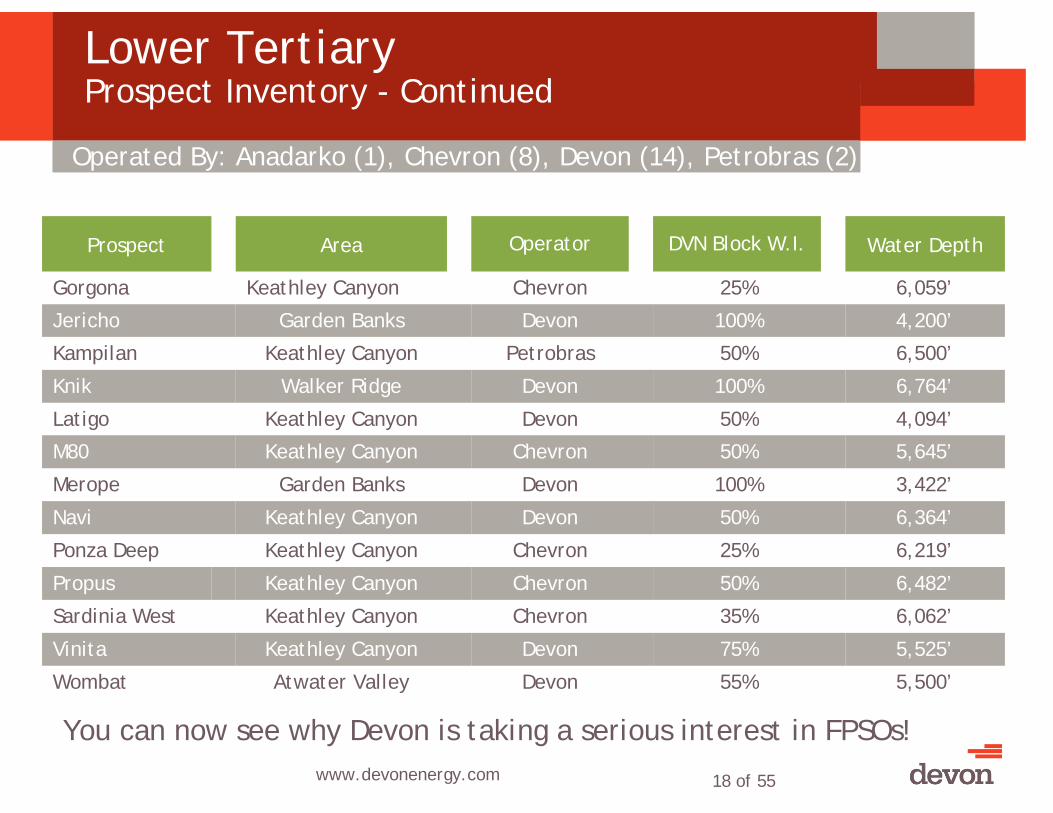

5,525’75%DevonKeathley CanyonVinita

6,059’25%ChevronKeathley CanyonGorgona

4,200’100%DevonGarden BanksJericho

6,500’50%PetrobrasKeathley CanyonKampilan

6,764’100%DevonWalker RidgeKnik

5,500’55%DevonAtwater ValleyWombat

6,062’35%ChevronKeathley CanyonSardinia West

6,219’25%ChevronKeathley CanyonPonza Deep

6,364’50%DevonKeathley CanyonNavi

3,422’100%DevonGarden BanksMerope

5,645’50%ChevronKeathley CanyonM80

4,094’50%DevonKeathley CanyonLatigo

Propus

Prospect

6,482’50%ChevronKeathley Canyon

Water DepthDVN Block W.I.OperatorArea

Lower Tertiary Prospect Inventory - Continued

You can now see why Devon is taking a serious interest in FPSOs!

Operated By: Anadarko (1), Chevron (8), Devon (14), Petrobras (2)

www.devonenergy.com 19 of 55NYSE: DVN www.devonenergy.com

3. Highly Prospective but Risks Slow Sanction

Devon truly open to different development options

www.devonenergy.com 20 of 55NYSE: DVN www.devonenergy.com

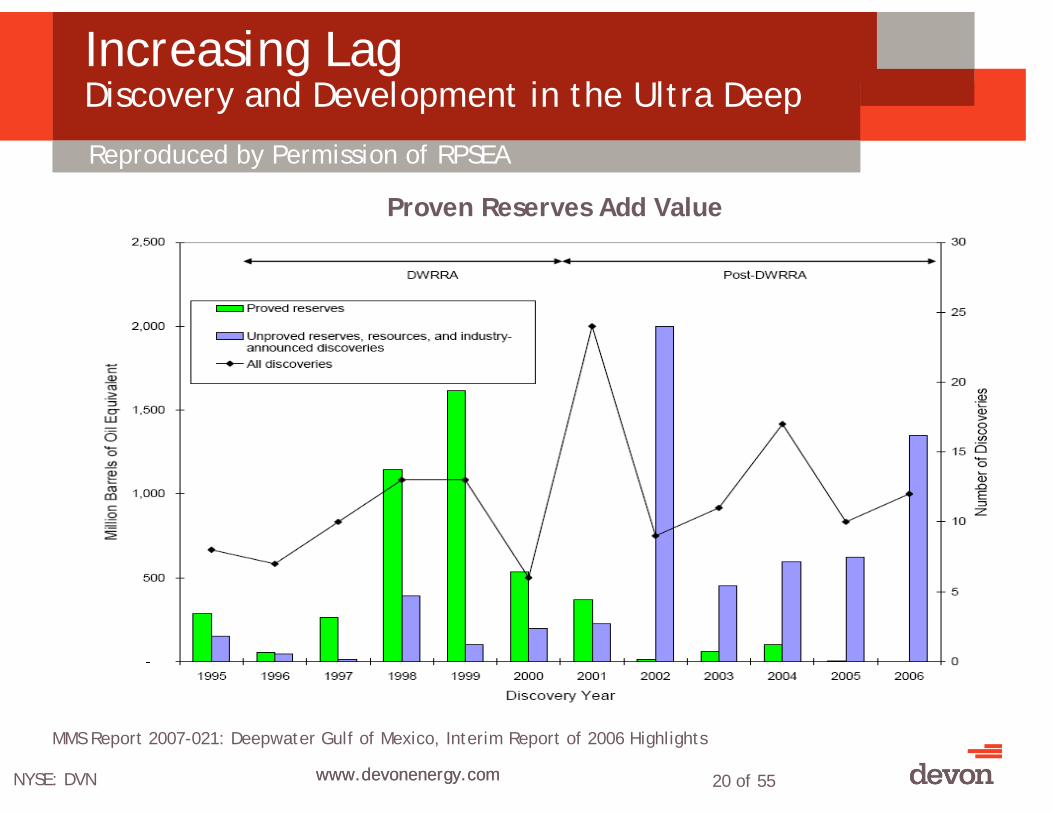

MMS Report 2007-021: Deepwater Gulf of Mexico, Interim Report of 2006 Highlights

Proven Reserves Add Value

Increasing Lag Discovery and Development in the Ultra Deep

Reproduced by Permission of RPSEA

www.devonenergy.com 21 of 55

Industry Pressures

• The US government for about two years has seen the slowdown in translating discoveries into booked reserves and royalty producing production;

• The industry sees the slow down too – planning is difficult, cannot take these risks without exhaustive work, witness Jack St. Malo;

• The US public presses for reduction of dependence on foreign oil(witness the election!);

• Devon like many operators in GoM has used various types of floaters in the past in different parts of the world;

• For the development choice to be an FPSO for GoM it has to be proven the optimum business choice.

www.devonenergy.com 22 of 55

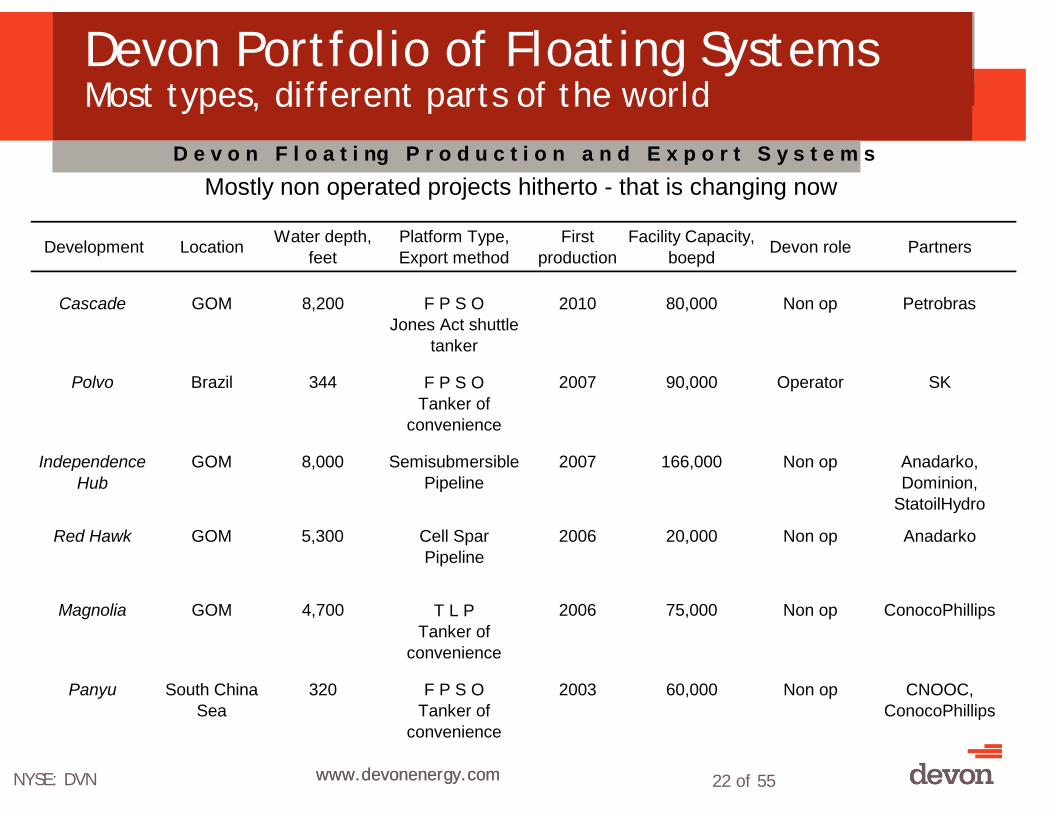

Devon Portfolio of Floating Systems Most types, different parts of the world

Development Location Water depth, feet

Platform Type, Export method

First production

Facility Capacity, boepd Devon role Partners

Cascade GOM 8,200 F P S O 2010 80,000 Non op Petrobras Jones Act shuttle

tanker

Polvo Brazil 344 F P S O 2007 90,000 Operator SKTanker of

convenience

Independence Hub

GOM 8,000 Semisubmersible Pipeline

2007 166,000 Non op Anadarko, Dominion,

StatoilHydro

Red Hawk GOM 5,300 Cell Spar Pipeline

2006 20,000 Non op Anadarko

Magnolia GOM 4,700 T L P 2006 75,000 Non op ConocoPhillipsTanker of

convenience

Panyu South China Sea

320 F P S O Tanker of

convenience

2003 60,000 Non op CNOOC, ConocoPhillips

D e v o n F l o a t i ng P r o d u c t i o n a n d E x p o r t S y s t e m sMostly non operated projects hitherto - that is changing now

NYSE: DVN www.devonenergy.com

www.devonenergy.com 23 of 55

Panyu FPSO - South China SeaExport: tanker of convenience

NYSE: DVN www.devonenergy.com 23 of 69

Operator: CNOOCCNOOC 51.0%Devon: 24.5%ConocoPhillips: 24.5%

Oil development at Panyu Block 4-260,000 bopd max320 ft. water depthFirst oil 4Q031,000,000 bbl storage

www.devonenergy.com 24 of 55

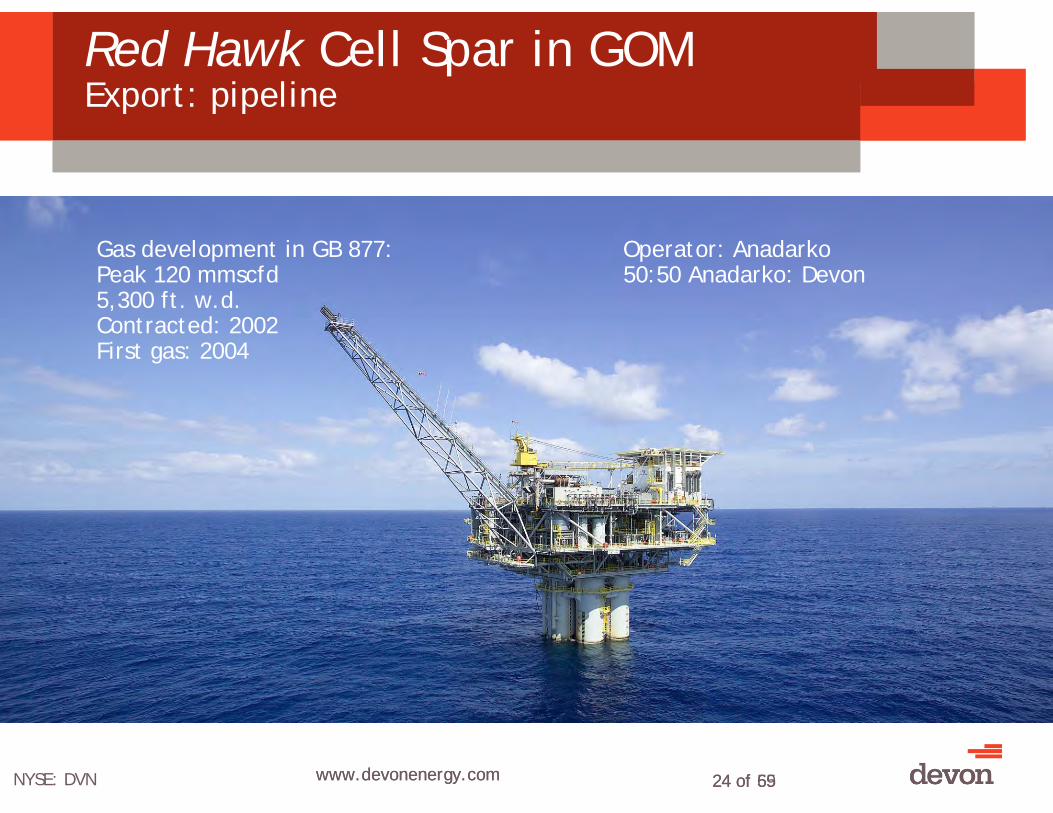

Red Hawk Cell Spar in GOMExport: pipeline

NYSE: DVN www.devonenergy.com 24 of 69

Gas development in GB 877: Operator: AnadarkoPeak 120 mmscfd 50:50 Anadarko: Devon5,300 ft. w.d.Contracted: 2002First gas: 2004

www.devonenergy.com 25 of 55

Magnolia TLP in GoMExport: pipeline

NYSE: DVN www.devonenergy.com 25 of 69

Oil development in GB 783 Operator: ConocoPhillips50,000 bopd capacity + 150 mmscfd 75: 25: ConocoPhillips: Devon4,700 ft. w.d. Discovery: May 1999First oil: November 2004

www.devonenergy.com 26 of 55

Polvo FPSO – BrazilExport: tanker of convenience

NYSE: DVN www.devonenergy.com 26 of 69

Oil development in BM-C-8: Operator: Devon90,000 bopd 60:40 Devon:SK344 ft. w.d. Leased FPSO from Prosafe1,500,000 bbl storage (7 years + options)Discovery: June 2004, first oil: July 2007

Shown en route, now producing

www.devonenergy.com 27 of 55

Devon is an Independent on Facility & Transportation

• Devon is an E&P company, i.e. has no refineries to feed;

• Devon owns neither an offshore pipeline company nor a shipping company;

• Every incentive therefore exists to objectively seek out the most cost efficient facility & transportation solution for Devon’s prospective developments in the ultra deep remote waters of the GoM!

• Rigorous internal debate, little/no bias pro/con FPSOs & shuttle tankers;

• Concept selection process slow and deliberate with Devon and itsPartners.

NYSE: DVN www.devonenergy.com

(pun intended)

www.devonenergy.com 28 of 55

Stating the Obvious?

• Some may feel GoM is prejudiced against FPSOs;

• But just like the rest of the world, the production solution is tailored to suit profitable production of oil and gas!

• Just happens to be difficult to arrive at the right economic technical and minimal risk choice in GoM for Lower Tertiary;

• Takes an unusually intense and protracted decision making process!!!

NYSE: DVN www.devonenergy.com

www.devonenergy.com 29 of 55NYSE: DVN www.devonenergy.com

4. Huge Drilling InvestmentsAffecting Facility Choice

Many Prospects;

Managing Mega Investments and Risks

www.devonenergy.com 30 of 55

Devon Deepwater Development (3D)Determining Plans to Produce & Deliver to Market

• Carefully crafted team: project sponsor, sponsor team, management team, multidiscipline project team (top management support);

• Been at it for a year;

• Developing strategy for Lower Tertiary prospect portfolio;

• Capex and Opex models developed for each case (facility configuration) for life of the field;

• Capex comparison with non operated Devon projects, e.g. Jack / St. Malo and Cascade data in progress;

• Gantt Charts completed for each development case, including exploration, appraisal, planning, execution, drilling & completions.

NYSE: DVN www.devonenergy.com

Running studies in team set up like for a mega project

www.devonenergy.com 31 of 55

Decision AnalysisReal Options Valuation (ROV). . the Process . .

• Framing of Development Options: Characterizing risks & uncertainties for “Difficult-to-Choose” options to lead to THE development option, so the TEAM, as a group, can:

– Clearly defines the decision problem;– Choose the options they would like to consider, and– Establish the means and measures (metrics i.e. ROR, NPV, etc)

they will consider when it comes time to make that choice.

• Reveals the sensitivities of the different options to the risks and uncertainties characterized above;

• Understanding & quantifying the impact of “More Information” (VOI – Value of Information exercise). Results not always intuitive!

NYSE: DVN www.devonenergy.com

Threading a way through a bewildering number of possibilities

www.devonenergy.com 32 of 55

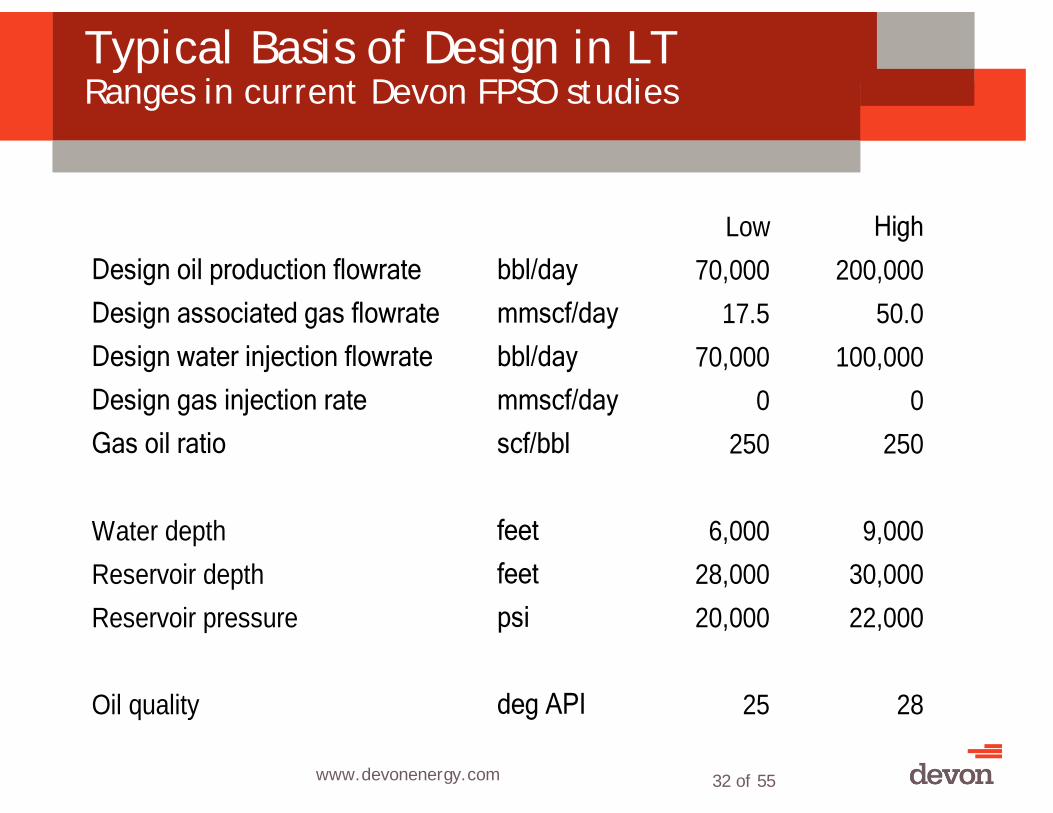

Typical Basis of Design in LT Ranges in current Devon FPSO studies

Low High

bbl/day 70,000 200,000mmscf/day 17.5 50.0bbl/day 70,000 100,000mmscf/day 0 0scf/bbl 250 250

Water depth feet 6,000 9,000Reservoir depth feet 28,000 30,000Reservoir pressure psi 20,000 22,000

Oil quality deg API 25 28

Design gas injection rate

Gas oil ratio

Design oil production flowrate

Design associated gas flowrate

Design water injection flowrate

www.devonenergy.com 33 of 55

5. Export Issues – the ComingShoot-out: Pipelines and Shuttle Tankers

Far from shore overmountainous terrain a new competition emerges

NYSE: DVN www.devonenergy.com

www.devonenergy.com 34 of 55

• Decades of tradition of tie ins of smaller reservoirs to deepwater hubs that process and feed a transportation system often with major oil company ownership;

• Same practical reasons hold today, looking ahead, may see sharedfacilities, profit motive for all;

• FSOG: Devon developed concept for hub storage in remote ultra deep waters of Walker Ridge and Keathley Canyon, ability to collect and process gas on deck;

• FPSO: Ability to serve as a hub may be a priority in FPSO capabilities, similar to FSOG.

NYSE: DVN www.devonenergy.com

Hubs and SpokesHistory Likely to Repeat Itself

Historic link between production and export to shore

www.devonenergy.com 35 of 55NYSE: DVN www.devonenergy.com 35 of 69

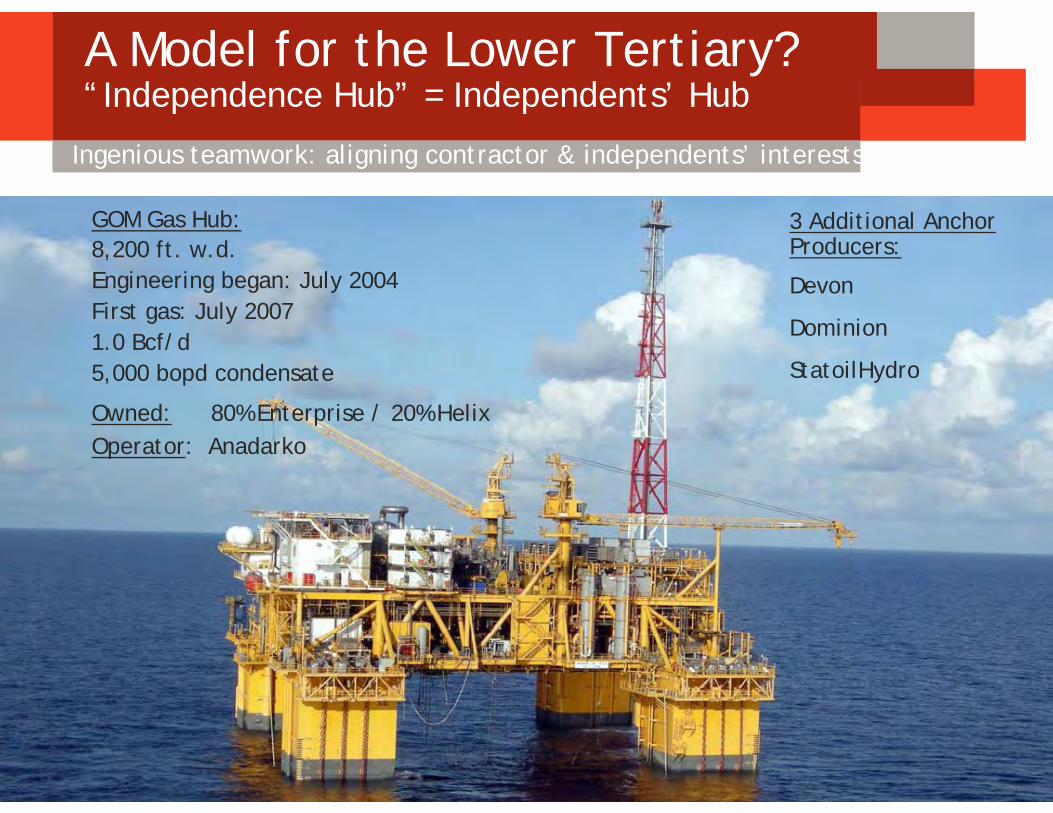

Ingenious teamwork: aligning contractor & independents’ interests

GOM Gas Hub:8,200 ft. w.d.Engineering began: July 2004 First gas: July 20071.0 Bcf/d5,000 bopd condensate

Owned: 80% Enterprise / 20% Helix Operator: Anadarko

3 Additional AnchorProducers:

Devon

Dominion

StatoilHydro

A Model for the Lower Tertiary?“Independence Hub” = Independents’ Hub

www.devonenergy.com 36 of 55NYSE: DVN www.devonenergy.com 36 of 69

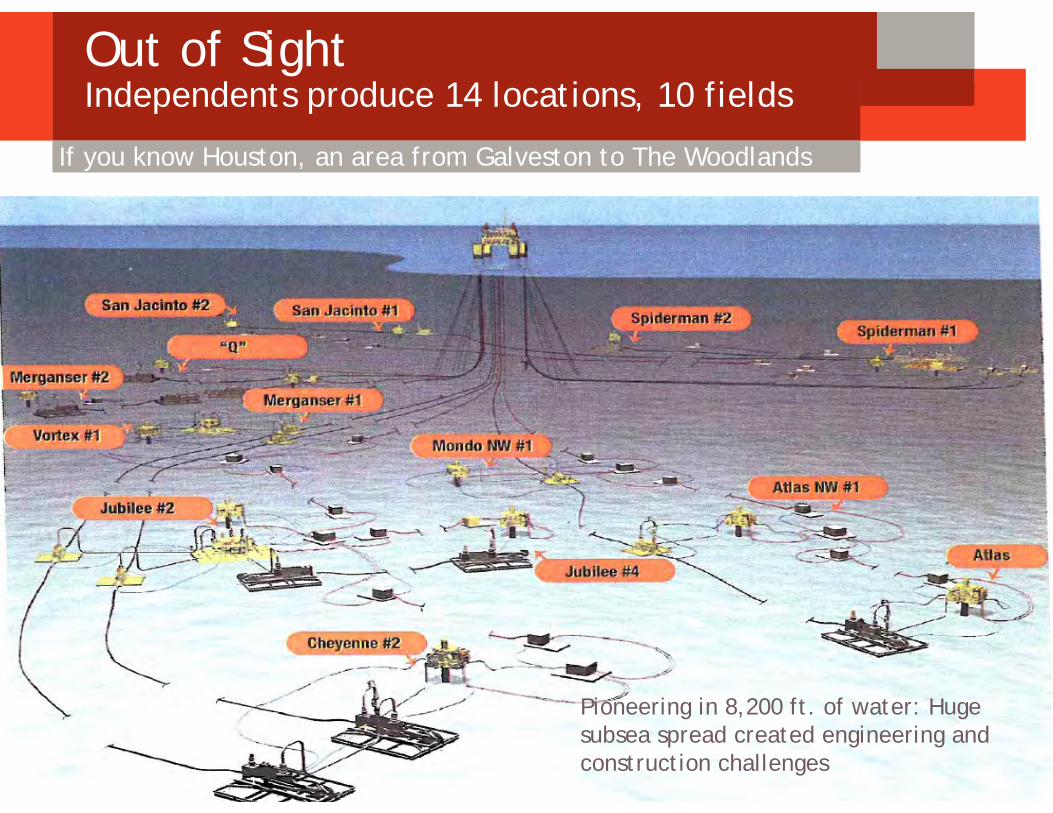

Out of SightIndependents produce 14 locations, 10 fields

Pioneering in 8,200 ft. of water: Huge subsea spread created engineering and construction challenges

If you know Houston, an area from Galveston to The Woodlands

www.devonenergy.com 37 of 55

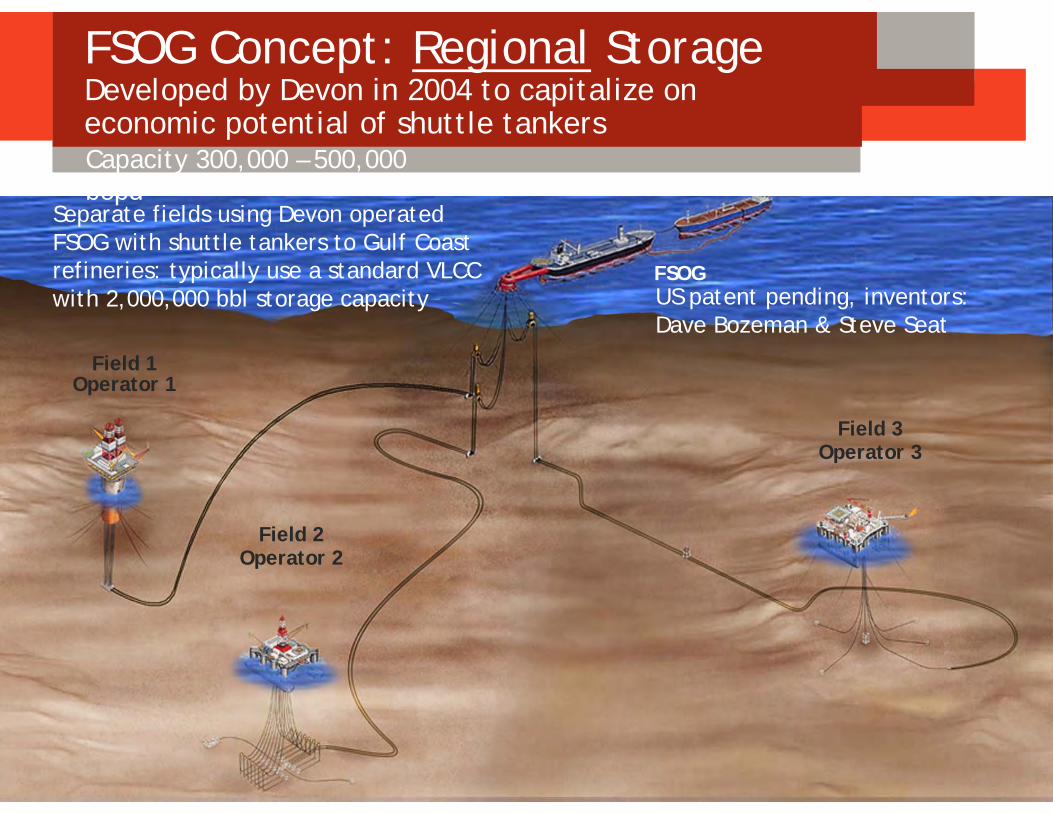

FSOG Concept: Regional StorageDeveloped by Devon in 2004 to capitalize on economic potential of shuttle tankers

NYSE: DVN www.devonenergy.com 37 of 69

Field 1Operator 1

Field 2Operator 2

Field 3Operator 3

FSOG

Separate fields using Devon operated FSOG with shuttle tankers to Gulf Coast refineries: typically use a standard VLCC with 2,000,000 bbl storage capacity US patent pending, inventors:

Dave Bozeman & Steve Seat

Capacity 300,000 – 500,000 bopd

www.devonenergy.com 38 of 55

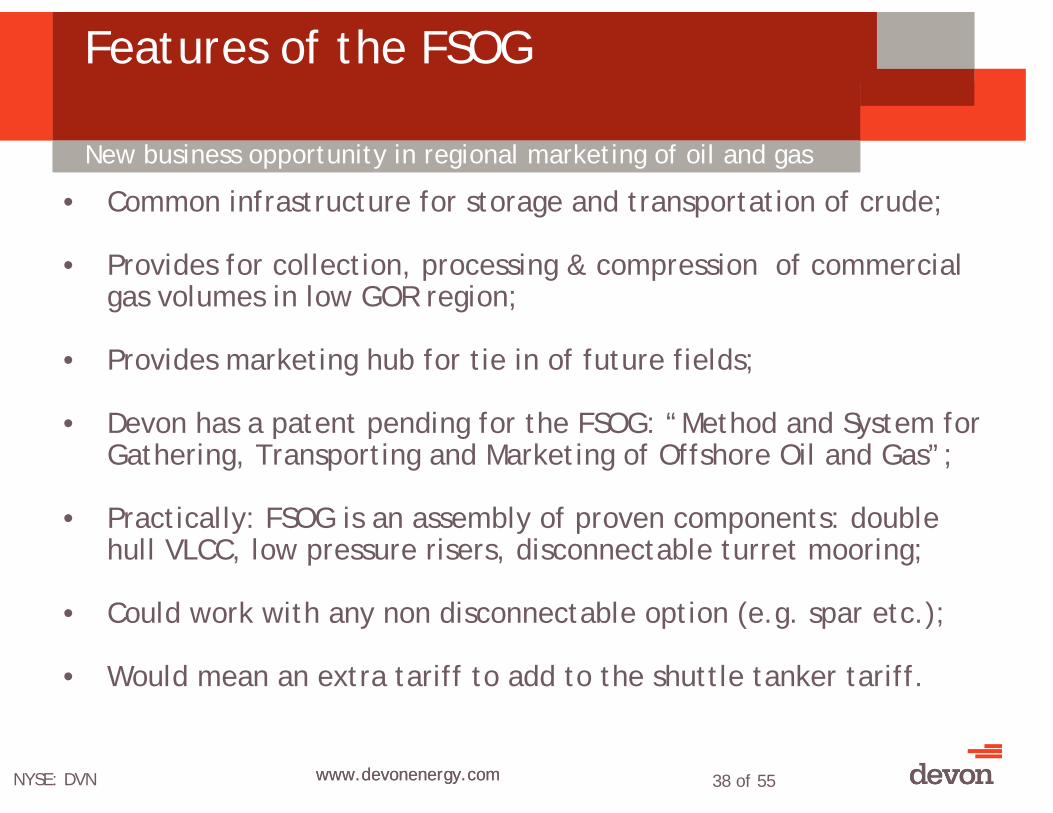

Features of the FSOG

• Common infrastructure for storage and transportation of crude;

• Provides for collection, processing & compression of commercialgas volumes in low GOR region;

• Provides marketing hub for tie in of future fields;

• Devon has a patent pending for the FSOG: “Method and System for Gathering, Transporting and Marketing of Offshore Oil and Gas”;

• Practically: FSOG is an assembly of proven components: double hull VLCC, low pressure risers, disconnectable turret mooring;

• Could work with any non disconnectable option (e.g. spar etc.);

• Would mean an extra tariff to add to the shuttle tanker tariff.

NYSE: DVN www.devonenergy.com

New business opportunity in regional marketing of oil and gas

www.devonenergy.com 39 of 55

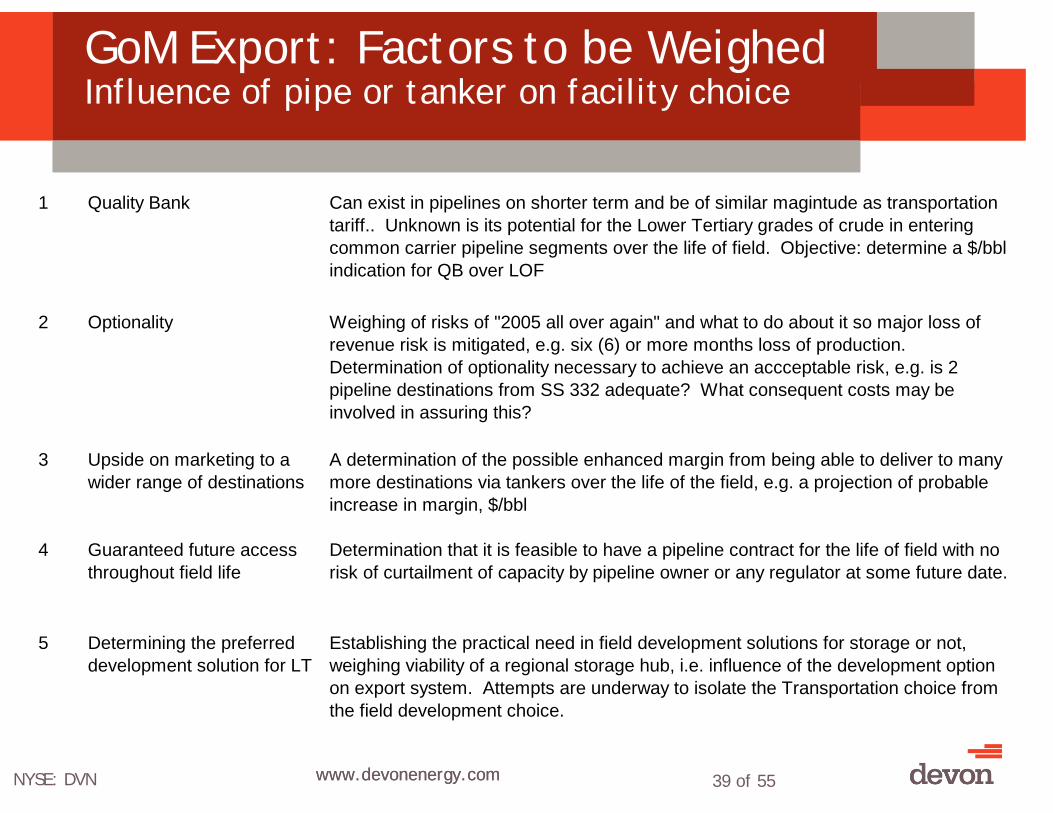

GoM Export: Factors to be WeighedInfluence of pipe or tanker on facility choice

1 Quality Bank Can exist in pipelines on shorter term and be of similar magintude as transportation tariff.. Unknown is its potential for the Lower Tertiary grades of crude in entering common carrier pipeline segments over the life of field. Objective: determine a $/bbl indication for QB over LOF

2 Optionality Weighing of risks of "2005 all over again" and what to do about it so major loss of revenue risk is mitigated, e.g. six (6) or more months loss of production. Determination of optionality necessary to achieve an accceptable risk, e.g. is 2 pipeline destinations from SS 332 adequate? What consequent costs may be involved in assuring this?

3 Upside on marketing to a wider range of destinations

A determination of the possible enhanced margin from being able to deliver to many more destinations via tankers over the life of the field, e.g. a projection of probable increase in margin, $/bbl

4 Guaranteed future access throughout field life

Determination that it is feasible to have a pipeline contract for the life of field with no risk of curtailment of capacity by pipeline owner or any regulator at some future date.

5 Determining the preferred development solution for LT

Establishing the practical need in field development solutions for storage or not, weighing viability of a regional storage hub, i.e. influence of the development option on export system. Attempts are underway to isolate the Transportation choice from the field development choice.

NYSE: DVN www.devonenergy.com

www.devonenergy.com 40 of 55

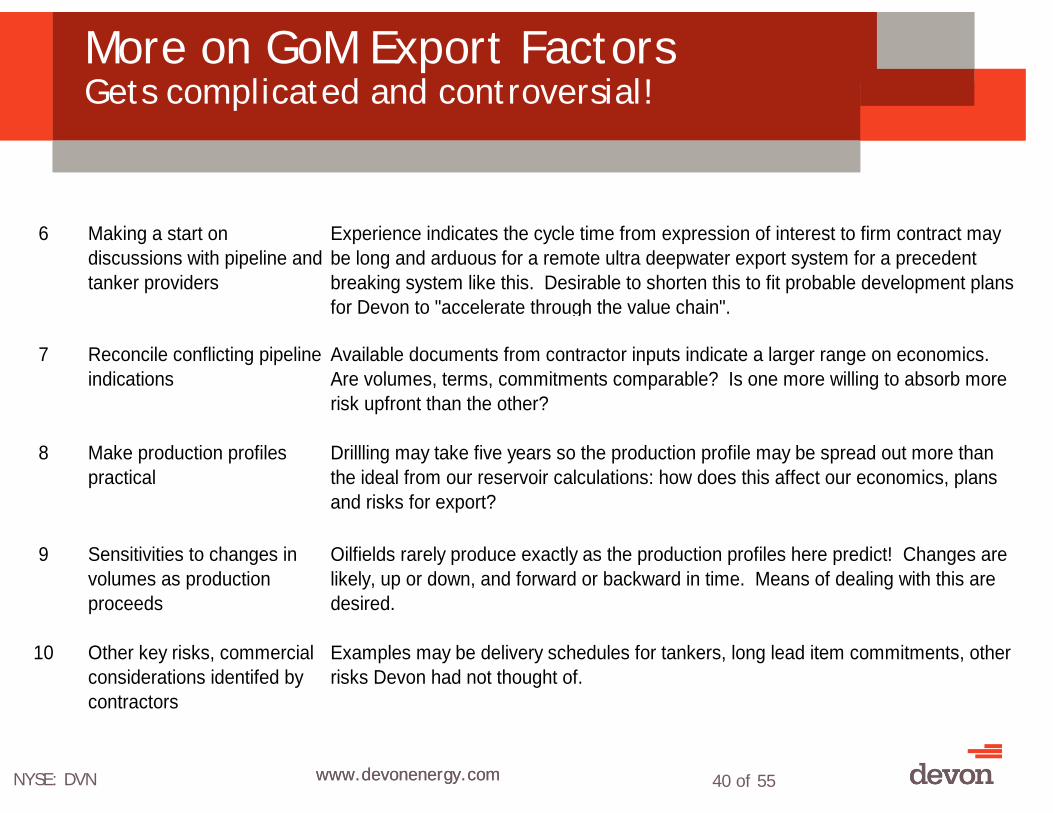

More on GoM Export FactorsGets complicated and controversial!

6 Making a start on discussions with pipeline and tanker providers

Experience indicates the cycle time from expression of interest to firm contract may be long and arduous for a remote ultra deepwater export system for a precedent breaking system like this. Desirable to shorten this to fit probable development plans for Devon to "accelerate through the value chain".

7 Reconcile conflicting pipeline indications

Available documents from contractor inputs indicate a larger range on economics. Are volumes, terms, commitments comparable? Is one more willing to absorb more risk upfront than the other?

8 Make production profiles practical

Drillling may take five years so the production profile may be spread out more than the ideal from our reservoir calculations: how does this affect our economics, plans and risks for export?

9 Sensitivities to changes in volumes as production proceeds

Oilfields rarely produce exactly as the production profiles here predict! Changes are likely, up or down, and forward or backward in time. Means of dealing with this are desired.

10 Other key risks, commercial considerations identifed by contractors

Examples may be delivery schedules for tankers, long lead item commitments, other risks Devon had not thought of.

NYSE: DVN www.devonenergy.com

www.devonenergy.com 41 of 55

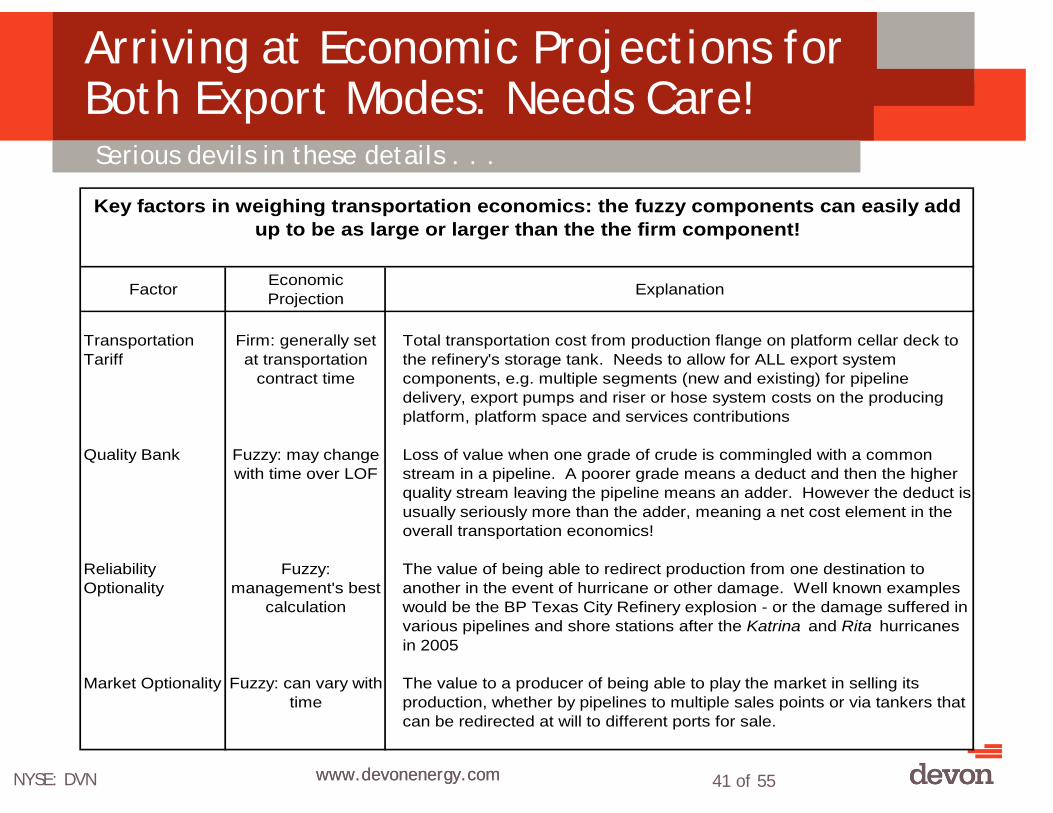

Arriving at Economic Projections for Both Export Modes: Needs Care!

Factor Economic Projection Explanation

Transportation Tariff

Firm: generally set at transportation

contract time

Total transportation cost from production flange on platform cellar deck to the refinery's storage tank. Needs to allow for ALL export system components, e.g. multiple segments (new and existing) for pipeline delivery, export pumps and riser or hose system costs on the producing platform, platform space and services contributions

Quality Bank Fuzzy: may change with time over LOF

Loss of value when one grade of crude is commingled with a common stream in a pipeline. A poorer grade means a deduct and then the higher quality stream leaving the pipeline means an adder. However the deduct is usually seriously more than the adder, meaning a net cost element in the overall transportation economics!

Reliability Optionality

Fuzzy: management's best

calculation

The value of being able to redirect production from one destination to another in the event of hurricane or other damage. Well known examples would be the BP Texas City Refinery explosion - or the damage suffered in various pipelines and shore stations after the Katrina and Rita hurricanes in 2005

Market Optionality Fuzzy: can vary with time

The value to a producer of being able to play the market in selling its production, whether by pipelines to multiple sales points or via tankers that can be redirected at will to different ports for sale.

Key factors in weighing transportation economics: the fuzzy components can easily add up to be as large or larger than the the firm component!

NYSE: DVN www.devonenergy.com

Serious devils in these details . . .

www.devonenergy.com 42 of 55

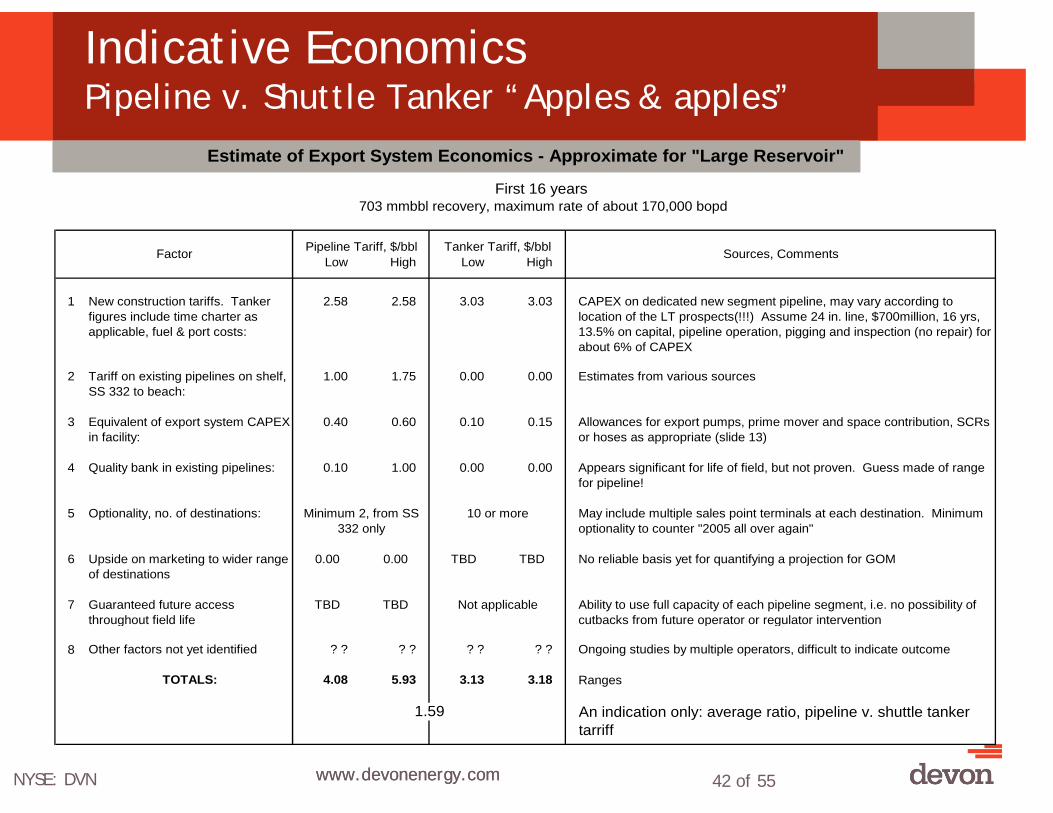

Indicative EconomicsPipeline v. Shuttle Tanker “Apples & apples”

Low High Low High

1 New construction tariffs. Tanker figures include time charter as applicable, fuel & port costs:

2.58 2.58 3.03 3.03 CAPEX on dedicated new segment pipeline, may vary according to location of the LT prospects(!!!) Assume 24 in. line, $700million, 16 yrs, 13.5% on capital, pipeline operation, pigging and inspection (no repair) for about 6% of CAPEX

2 Tariff on existing pipelines on shelf, SS 332 to beach:

1.00 1.75 0.00 0.00 Estimates from various sources

3 Equivalent of export system CAPEX in facility:

0.40 0.60 0.10 0.15 Allowances for export pumps, prime mover and space contribution, SCRs or hoses as appropriate (slide 13)

4 Quality bank in existing pipelines: 0.10 1.00 0.00 0.00 Appears significant for life of field, but not proven. Guess made of range for pipeline!

5 Optionality, no. of destinations: May include multiple sales point terminals at each destination. Minimum optionality to counter "2005 all over again"

6 Upside on marketing to wider range of destinations

0.00 0.00 TBD TBD No reliable basis yet for quantifying a projection for GOM

7 Guaranteed future access throughout field life

TBD TBD Ability to use full capacity of each pipeline segment, i.e. no possibility of cutbacks from future operator or regulator intervention

8 Other factors not yet identified ? ? ? ? ? ? ? ? Ongoing studies by multiple operators, difficult to indicate outcome

TOTALS: 4.08 5.93 3.13 3.18 Ranges

1.59 An indication only: average ratio, pipeline v. shuttle tanker tarriff

Minimum 2, from SS 332 only

Estimate of Export System Economics - Approximate for "Large Reservoir"

703 mmbbl recovery, maximum rate of about 170,000 bopd

Factor

Not applicable

10 or more

First 16 years

Pipeline Tariff, $/bbl Tanker Tariff, $/bbl Sources, Comments

NYSE: DVN www.devonenergy.com

www.devonenergy.com 43 of 55

A Sound Business Case Does Exist for FPSOs & Shuttle Tankers

• Shuttle tankers may indeed offer an economic benefit over pipelines for a large field in the Lower Tertiary: could amount to about a $Billion saving over field life;

• Aggregation of large enough volumes to enable an economic pipeline is more difficult in Lower Tertiary than closer to shore. Very difficult indeed for early production. Risks and economicscan favor tankers;

• Tankers offer future flexibility in changing destinations for maximum margin from production - and in event of hurricane damage can be directed to alternate delivery points;

• In the event of a field being a bust, tankers being redeployablemitigate risk on export service commitments. Pipelines are not good at being reeled up and redeployed!

NYSE: DVN www.devonenergy.com

If field production conditions allow it!

www.devonenergy.com 44 of 55NYSE: DVN www.devonenergy.com

6. Projecting what May Lie Aheadfor FPSOs in UDW GoM

Compared to a year ago, it’s starting to come into focus

www.devonenergy.com 45 of 55

Early Well Testing (EWT) ? And/or Early Production Systems (EPS) ?

• Gas cannot be flared in GoM – makes shorter term operations more difficult than in countries where there is some regulatory latitude for trials in new areas;

• Desirable to test wells for longer durations but assembling the spread is difficult and costly ;

• Smaller shorter term EPS, possibly on DP, has been debated in GoM but true added value to a field development often not there - or not conclusive;

• Dilemma of equipment being built if several multi-month (or one or two year) long commitments were available. The trick is stitching together enough of these to enable vessel construction;

• In spite of much discussion, no definitive EWT solution for GoMyet selected!

NYSE: DVN www.devonenergy.com

www.devonenergy.com 46 of 55

Is There Really a Case for an FPSOfor Full Field Development?

• Simultaneous with reserves that are deeper, higher pressured, more remote, requiring bigger CAPEX, the corporate need in these megaprojects intensifies to maintain capital discipline and project management discipline;

• So we could study it to death to mitigate risks - or take some risks with future flexibility at a premium;

• How to forge ahead? How to apply Devon’s mantra “accelerate through the value chain”?

• More GOM acceptance of FPSOs: the rise of the independents, plus arrival of serious non GoM experience (Petrobras, StatoilHydro);

• Conclusion: Circumstances now more favorable today for FPSOs in GoM than before, if they can be more flexible in capability & business basis;

NYSE: DVN www.devonenergy.com

www.devonenergy.com 47 of 55

Putting it Together . . .Devon’s Perspective (1 of 3)

a. For locations a long way out, over mountainous seabeds, pipeline routes much longer, more circuitous and more expensive than hitherto. Export economics thus may favor FPSOs;

b. Pressure to cut the cycle time to improve economics is counteredby risks of reservoirs performing differently from expectations;

c. Corporate goals of large independents may favor FPSOs: proving as they go along, e.g. EPS morphing into FFD;

d. Commitments on export pipelines are huge, tanker export easier to start quickly for remote areas and grow incrementally – again export system selection may favor FPSOs;

e. Drilling, well access, available technologies affect facility choice (e.g. dry trees and/or DVA, hence no FPSO);

f. Not conclusive that there must be a future for FPSOs for FFD in ultra deep in GoM;

NYSE: DVN www.devonenergy.com

www.devonenergy.com 48 of 55

Putting it Together . . .Devon’s Perspective (2 of 3)

g. Logic of Real Option Value decision process expedites steering acourse in uncertain waters (pun intended);

h. Rigorous internal debate, little/no bias pro/con FPSOs;

i. No export legacy of pipeline operation, shuttle tanker v. pipeline, relatively open competition;

j. Concept selection process slow and deliberate with Devon and itspartners;

k. Projecting the future fleet size of FPSOs for US GoM would require truly remarkable use of crystal balls on a biblical scale!!!

l. Would not expect a flood of FPSO orders for GoM.

NYSE: DVN www.devonenergy.com

www.devonenergy.com 49 of 55

Putting it Together . . .Devon’s Perspective (3 of 3)

m. For Devon’s 2008 portfolio of Lower Tertiary prospects in the UDW GoM, we can confirm considering FPSOs along the lines of:Technically: + EPS expandable to FFD

+ Suezmax newbuild;+ Disconnectable;

Commercially: + Studies on FPSOs for GoM underway;+ Early talks with contractors;+ Firm commitment dependent on well results;+ Premium on flexibility and speed;+ Bid process could proceed – or negotiation on hull

under construction – depending on progress;+ Linked to availability of shuttle tankers.

n. We do encourage exchange of ideas with contractors, expect them to make a reasonable profit, and understand paying for successful performance!

NYSE: DVN www.devonenergy.com

Thank You

www.devonenergy.com 51 of 55

Devon Core Values

Hire the best people

Always do the right thing

Deliver results

Be a team player

Be a good neighbor

NYSE: DVN www.devonenergy.com

www.devonenergy.com 52 of 55

Devon History

NYSE: DVN www.devonenergy.com

Founded as a private company in 1971

Became a public company in 1988

• Currently listed on the New York Stock Exchange under the ticker symbol DVN

Grown from 185 employees in 1981 to over 5,000 employees today

Established a portfolio to provide stableproduction and a solid platform for future growth

www.devonenergy.com 53 of 55

Devon Today

Proved reserves (12/31/07): ≈ 2.5 Billion BOE

Current production (Q2 2008): ≈ 643 MBOED

Oil & gas production (Q2 2008): 66% gas

34% oil & NGLs

Production profile (Q2 2008): 94% North America

Reserves / production ratio: ≈ 11 years

Enterprise value: ≈ $35 Billion

Largest U.S.-based independent oil and gas producer

www.devonenergy.com 54 of 55

Acknowledgements

My thanks is due to Devon management for permissionto freely discuss the issues here.

Recognition is also due to colleagues for their ideasand assistance in reviewing and assembling theinformation in this presentation:

Melany Boughman Dave BozemanScott CoodyJohn Heg

NYSE: DVN www.devonenergy.com

www.devonenergy.com 55 of 55

Questions?

[email protected] 713 265 6489 office

1 713 419 9164 cell

NYSE: DVN www.devonenergy.com