Embed Size (px)

Citation preview

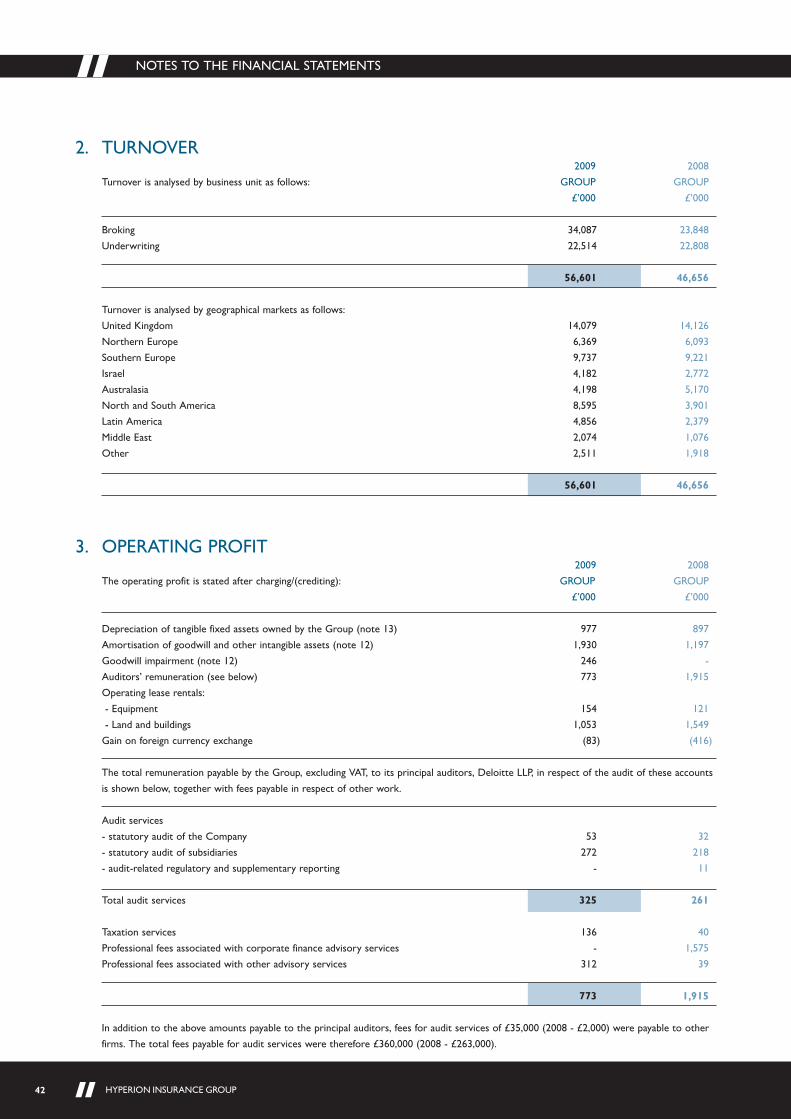

HYPERION INSURANCE GROUP LIMITED

REPORT & ACCOUNTS

YEAR ENDED 30 SEPTEMBER 2009

ARGENTINA

AUSTRALIA

BRAZIL

COLOMBIA

DUBAI

FINLAND

GERMANY

HONG KONG

ICELAND

INDIA

IRELAND

ISRAEL

ITALY

MEXICO

PUERTO RICO

SINGAPORE

SPAIN

SWEDEN

TAIWAN

UNITED KINGDOM

UNITED STATES

HYPERION INSURANCE GROUP LIMITED

REPORT & ACCOUNTS

YEAR ENDED 30 SEPTEMBER 2009

2008-2009 At A Glance 02

Chairman’s Statement 04

Chief Executive’s Review 06

Board Structure 08

Group Structure 10

Group Broking 11

Group Underwriting 21

Financial Statements 31

01HYPERION INSURANCE GROUP

CONTENTS

2008-2009 AT A GLANCE

£57,160,00GROUP REVENUE

£8,794,000EBITDA

£34,087,000BROKING REVENUE

£22,514,000UNDERWRITING REVENUE

448PEOPLE EMPLOYED

02 HYPERION INSURANCE GROUP

AT A GLANCE

2003 2004 2005 2006 2007 2008 2009

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

14.438

619

914

50 69102

175232

272

355408

383

448

1,759

5,170

2,245

6,787

Underwriting

Broking

3,659

10,478

6,606

13,689

8,894

17,990

14,228

19,17318,008

20,31822,808

23,848

22,514

34,087

3,691

1,3401,806

3,590 3,407

5,204

6,997

8,145

20.73027.399

34.10339.250

60

50

40

30

20

10

0

9,0008,0007,0006,0005,0004,0003,0002,0001,000

0

35,000

30,000

25,000

20,000

15,000

10,000

5,000

0

500

400

300

200

100

0

£ M

ILLI

ON

S£

‘000

£ ‘0

00N

umbe

r

48.030

57.160

8,0768,794

03HYPERION INSURANCE GROUP

AT A GLANCE

KEY FACTS• Founded in 1994 and headquartered in the City of

London, Hyperion is a fast expanding internationalinsurance company. Since its inception it has grown tobecome a leading global provider of specialist insurancesoperating on four key platforms: wholesale, retail,reinsurance broking and underwriting.

• Four main brands: CFC Underwriting, DUAL, Hendricks& CO GmbH and Howden.

• 42 offices in 21 countries employing over 440 people.

• Reported operating income of £57.2 million for thefinancial year ended 30 September 2009 and EBITDA(excluding exceptional items) of £8.8 million, up 19% and9% respectively on 2008.

2008-2009HIGHLIGHTSOCTOBER 2008• Group entered an exclusive partnership with a broker in

Korea.

DECEMBER 2008• Established a North American Property & Casualty

Division, with a team joining from Benfield CorporateRisks.

• Trebled size of International Property business withsignificant expansion in the Far East. Office opened inHong Kong.

FEBRUARY 2009• Offices opened in Taiwan as part of our expansion in the

Far East of our International Property business.

MAY 2009 • DUAL International announced a strategic partnership

between its Hong Kong office, DUAL Asia, and MSIGInsurance (Hong Kong) Ltd to provide financial linesproducts for mid market companies in Asia.

JUNE 2009 • Howden signs a deal to acquire Hendricks & CO

GmbH, the leading specialist Directors and Officers andCommercial Legal Expenses broker in Germany.

JULY 2009• Bob Van Gieson, former President and CEO of Arch

Insurance Company Europe appointed Chairman andCEO of DUAL International.

• CFC entered the Life Sciences market and launchedBioSurance™ R&D a blended policy designed specificallyfor research and development companies.

• Eric Fady appointed Finance Director of the Group. Ericwas previously Finance Director for Marsh EuropeMiddle East and Africa.

The Queen’s Award forEnterprise inInternational Tradereflects the Group’s fastgrowing global presence.

TERRITORIES AND PRODUCT LINES

The Hyperion Group currently operates in 22 countriesand 60% of our income comes from territories outside theUK. The Queen’s Award for Enterprise in InternationalTrade reflects the Group’s fast growing global presence.Hyperion is focused on providing specialist insuranceproducts to its clients. Some of our products:

Civil Sanctions and Regulatory Proceedings LiabilityCommercial CrimeCyber & Privacy LiabilityDirectors and Officers LiabilityEmployment Practice LiabilityEnvironmentalFinancial SpecialtiesGeneral CasualtyHealthcareInvestor ProtectionLawyersLife SciencesManagement LiabilityPension Trust LiabilityProfessional IndemnityProfessional LiabilityPropertyReal EstateSpecial RisksTechnologyTrustees Liability

04 HYPERION INSURANCE GROUP

CHAIRMAN’S STATEMENT

“This is an excellent set of results with strong organicgrowth supplemented by the acquisition of Hendricks, the largest independent D&O broker in Germany. ”

JOHN VAN KUFFELERCHAIRMAN

JOHN VAN KUFFELERCHAIRMAN

05HYPERION INSURANCE GROUP

CHAIRMAN’S STATEMENT

CHAIRMAN’S STATEMENTPERFORMANCEIn the year ended 30 September 2009 we saw continuedstrong growth, combined with a number of importantstrategic developments.

Group revenue increased by an impressive 19% and EBITDAby 7%. This is an excellent set of results as most of ourgrowth was organic rather than through acquisitions. Thenew teams we have attracted have allowed us to exploitnew areas of business which have played a strong part intaking our Group forward.

In particular, this has given the Group an ability to extractearnings from all points of the value chain aligned withproviding a hedge across the insurance cycle and a balanceacross our businesses.

Our strategy to enter new markets and grow our brandsglobally was enhanced with our acquisition of Hendricks &CO GmbH, the leading specialist in Directors and Officersand Commercial Legal Expenses broker in Germany inOctober 2009. This has propelled Howden Broking Groupinto a market leading position in Germany.

THE BOARDSince the year-end Tim Howden and Brian Marsh haveretired as non-executive Directors. Tim Howden had beena director since the company’s foundation in 1994 andprovided us with encouragement and wise counsel throughthe years. I would like to thank him for his considerablecontribution and wish him well in his retirement. BrianMarsh served as a director for 3 years but through BPMarsh & Partners PLC and was the original institutionalinvestor from the foundation of the company in 1994. Wewill miss his considerable insurance and business expertise,but I am pleased to announce that Jon Newman has joinedour Board as the nominee of BP Marsh & Partners PLC. Jonhas served on the Boards of a number of insurance relatedcompanies and is Finance Director of BP Marsh & PartnersPLC. His experience and expertise will be valuable to usgoing forward particularly as we get closer to our proposedIPO in 2012.

EMPLOYEESOur employees remain central to the success of Hyperion.Their dedication and hard work has been the principalreason for our success in 2009 and I would like to thankthem all for their considerable efforts.

OUTLOOKDespite soft markets, the new year has started with strongrevenue growth in both our broking and underwritingagency businesses and the outlook for us remains good as aresult of the strategic steps we achieved in 2009.

The ongoing support of our external shareholders is atestament to the strength of our business model. Following3i’s investment in April 2008, the Group still has £22m ofcommitted funds for acquisition. This, combined with theongoing success of our broking and underwriting divisions,places the Group in a strong position to make furtheracquisitions and achieve the growth which will place us in anexcellent position for our proposed IPO in 2012.

JOHN VAN KUFFELERCHAIRMAN

06 HYPERION INSURANCE GROUP

CHIEF EXECUTIVE’S REVIEW

“Hyperion has a distinctive business model, combiningwholesale, retail and reinsurance broking and underwritingagency businesses. Our ambition is to continue to build aworld beating specialist insurance business; to enhance theexisting entrepreneurial flair and continue to support ourability to attract and retain the very best people.”

DAVID HOWDENCHIEF EXECUTIVE

07HYPERION INSURANCE GROUP

CHIEF EXECUTIVE’S REVIEW

CHIEF EXECUTIVE’S REVIEWTHIS HAS BEEN AN EXCITING YEAR for theGroup against an extremely challenging financial market.Hyperion’s success over the years is due to its uniquestructure and distinctive culture which acts as a magnet fortalent. This enables us to create value for the Group andour employees which is key to our continued success.

Hyperion has a distinctive business model, combiningwholesale, retail and reinsurance broking and underwritingagency businesses. This simultaneously delivers us ascalable international platform offering global distributionand strong relationships with business producers andunderwriters.

OUR BUSINESSESBehind the overall success of the Group last year, all ourmain businesses traded extremely well.

BROKINGThe Group’s insurance broking operations reportedrevenues of £34.1 million – an increase of 43% on last year.Major developments which have contributed to the successof the Group included the following:• Establishment of a North American Property & Casualty

division, with a first-class team joining from BenfieldCorporate Risks.

• Trebling the size of our International Property businesswith significant expansion in the Far East. Offices wereopened in Hong Kong (December 2008) and Taiwan(February 2009), and in October 2008 the Groupentered into an exclusive partnership with an insurancebroker in South Korea (to be renamed Howden Korea).Howden will also open an office in Singapore shortly.Since the year-end we have been awarded a reinsurancebroking licence in Singapore.

• Impressive growth has also been achieved in Israel andSpain, achieving respectively a 23% and 21% increase inoperating income.

• On 1 October 2009 we acquired Hendricks & COGmbH, the leading specialist Directors and Officers andCommercial Legal Expenses broker in Germany. Thedeal propels us to be the D&O market leader inGermany.

UNDERWRITINGUnderwriting agencies DUAL International and CFCUnderwriting, both headquartered in London and VKUnderwriters based in Miami, all had a successful year.Total gross written premiums were £137 million, anincrease of 33% on the previous year. Major developmentsthat have contributed to these results – and willcontribute to the future growth of the underwritingagencies include:• DUAL International announced a strategic partnership

between its Hong Kong office, DUAL Asia, and MSIGInsurance (Hong Kong) Ltd, to provide financial linesproducts for mid market companies in Asia.

• In July 2009 Bob Van Gieson, former President and CEOof Arch Insurance Company Europe, was appointedChairman and CEO of DUAL International.

• In October 2009 Dual opened its first Irish branch inDublin.

• DUAL expanded its operations in Australia with theopening of an office in Brisbane to add to its existingoffices in Sydney, Perth and Melbourne.

• From 1 December 2009, DUAL Australia startedunderwriting solely on behalf of Lloyd’s (Arch Syndicate 2012).

• CFC had a particularly successful year with grosspremium income rising to £30 million and operatingprofit to £2.3 million representing increases of 22% and41.6% respectively.

• CFC entered the Life Sciences market in July 2009 bylaunching BiosuranceTM R&D, a blended policy specificallydesigned for research and development companies inthe Life Sciences industry.

These strategic developments are key to our future growthplans.

Our ambition is to continue to build a world beatingspecialist insurance business; to enhance the existingentrepreneurial flair and continue to support our abilityto attract and retain the very best people. Our successcan be attributed to our employees; our ability tocontinue to meet the insurance needs of our clients andour product and distribution expertise.

DAVID HOWDENCHIEF EXECUTIVE

08 HYPERION INSURANCE GROUP

BOARD STRUCTURE

BOARD STRUCTUREJOHN DE BLOCQ VAN KUFFELERNON-EXECUTIVE CHAIRMANJohn van Kuffeler joined Hyperion as non-executive Chairman in February 2009. He brings nearly 40 years of international financialservices experience to the role, and is also Chairman of Provident Financial PLC. He joined Provident Financial in 1991 as ChiefExecutive, and was appointed Executive Chairman in 1997, becoming non-executive Chairman in 2002. Prior to his career atProvident Financial he was Chief Executive of Brown Shipley, the investment banking group. Both Provident Financial and BrownShipley had significant insurance operations and van Kuffeler was also a non-executive director of the Medical Defence Union. Hewas also the Founder and former Chairman of Huveaux, the AIM listed political publishing & media group, and former Chairman ofEidos as well as two City based investment trusts. He is also an Advisory Board member of the Princes Trust and a former Councilmember of the CBI.

DAVID HOWDENCHIEF EXECUTIVEDavid has over 25 years’ experience in the Insurance industry. He is a leading expert in the field of Directors and Officers andProfessional Indemnity insurance both in London and the overseas markets.

David started his career as a broker at Alexander Howden in 1980. He founded the group in 1994 originally as a wholesale brokeremploying just 5 people. He has been the fundamental driving force behind its expansion into an international insurance groupoffering wholesale, retail, reinsurance and underwriting.

As Chief Executive, David’s focus is on leading the group’s M&A activities as well as directing and implementing the group’sstrategic growth and direction.

ERIC FADYGROUP FINANCE DIRECTOREric joined Hyperion in June 2008. His last role was as Finance Director for Marsh Europe Middle East and Africa from 2003 to2007, where he managed major projects to help the company adjust to the post Spitzer business world. Previously he was CFOand Vice President for Strategy Implementation for Dun & Bradstreet Europe & Middle East from 1999 to 2002 where hecontributed to the design of the company’s new business model and significantly improved their performance. Eric graduated fromRheims Business School, and began his career as an auditor with KPMG in France.

R.T. VAN GIESONEXECUTIVE DIRECTOR HYPERION AND CHAIRMAN & CEO DUAL INTERNATIONALBob was appointed Chairman and CEO of DUAL International in July 2009. Bob has over 40 years’ insurance experience and waspreviously President and CEO of Arch Insurance Company Europe. Bob successfully built Arch from a start-up operation into a$500m business. He was also Chairman of Arch Europe and sat on the board of its Lloyd’s Syndicate. Prior to his time with Arch,Bob worked for CNA Financial where he was responsible for five business units with a revenue base of $1 billion. Prior to CNA,Bob had a 29 year career at the Chubb Corporation. During this time he spent many years in Canada helping to build a strong andprofitable Canadian operation. He moved to London in 1990 and was responsible for European and Far Eastern operations. Hewas a driving force behind Chubb’s expansion and under his leadership it was established as a significant international player.

09HYPERION INSURANCE GROUP

BOARD STRUCTURE

LUIS MUÑOZ-ROJAS ENTRECANALESEXECUTIVE DIRECTORLuis is a founding Director of DUAL International. He opened the first DUAL operation in Madrid in August 1998, havingpreviously served as Director of GyC América, a reinsurance broking subsidiary of Gil y Caravajal (now part of Aon). During thattime Luis had considerable involvement in the Latin American territories. Luis began his insurance career in 1989 working withGyC & Partners, the British subsidiary of the GyC Group. Prior to this, he worked for Société Générale de France in variouscapacities and areas including foreign exchange.

EMILE WOOLFNON-EXECUTIVE DIRECTOREmile is a forensic and litigation support consultant with Kingston Smith Chartered Accountants. A qualified Accountant, formerChairman of ICAEW's Professional Indemnity Insurance Panel of Participating Insurers, Emile’s expertise covers technicalaccounting and audit issues, including independence, professional ethics and governance.

JONATHAN NEWMANNON-EXECUTIVE DIRECTORJonathan was appointed to the Hyperion Board in 2009. He is Group Director of Finance at BP Marsh & Partners PLC, and is achartered Management Accountant with more than 13 years’ experience in the financial services industry. He joined BP Marsh inNovember 1999 and was appointed Group Finance Director in December 2003.

DAVID WHILEMANNON-EXECUTIVE DIRECTORDavid is a Partner in the 3i Growth Capital business, investing up to €250m for stakes in market-leading businesses in the UK andacross Europe. He specialises in originating and leading investments into private companies seeking to accelerate their growth,both organically and through acquisition. Past investments include Foster & Partners, the global architects, Hayley ConferenceCentres and Morgan McKinley, the financial services business. David is a chartered accountant and prior to 3i worked in theinsolvency division within PricewaterhouseCoopers.

INSURANCE UNDERWRITING

AVANTSpain

CFC UNDERWRITINGUnited Kingdom

DUALAustralia

Germany

Hong Kong

Ireland

Italy

Spain

United Kingdom

VK UNDERWRITERSArgentina

Colombia

Mexico

Puerto Rico

United States

10 HYPERION INSURANCE GROUP

GROUP STRUCTURE

HYPERION INSURANCE GROUP

WHOLESALE, RETAIL & REINSURANCE BROKING

HOWDENBrazil

Dubai

Finland

Germany

Hong Kong

Iceland

India

Israel

Puerto Rico

Singapore

Spain

Sweden

Taiwan

United Kingdom

United States

40% GROUP INCOME13 TERRITORIES

18 OFFICES

60% GROUP INCOME15 TERRITORIES

24 OFFICES

11HYPERION INSURANCE GROUP

GROUP BROKINGINTRODUCTIONInsurance broking was the foundation of the HyperionInsurance Group with the formation of Howden InsuranceBrokers in 1994. From one operation in London, thenetwork of offices has grown to now number 24 worldwide.Over the past 16 years, the Group broking operations havegrown exponentially across the world as outstandinginsurance professionals have been identified in localterritories.

HOWDEN BROKING GROUPThe Howden Broking Group comprises wholesale, retailand reinsurance broking models, with its principalsubsidiary located at Lloyd’s of London. Retail brokersdistribute directly to the ultimate insured whereaswholesale brokers place business generated by otherinsurance brokers in the London and other internationalinsurance markets. Reinsurance broking is the process ofplacing insurance for insurance companies in order tospread the risk for the direct insurer. These methods ofbroking provide their own distinct advantages to the Groupand allow complete flexibility when entering a newterritory or product line.

Initially, the Group’s main focus was the two mutuallycompatible product lines of Professional Indemnityinsurance and Directors & Officers Liability insurance.However, client demand for the same professionalapproach to other insurance lines has grown. Howden hasbeen quick to meet these needs and is now a globalprovider of a range of specialist insurances.

HOWDEN OFFICES• Howden Insurance Brokers Limited – London, Leeds

and Taiwan• Howden Asia (Hong Kong) Limited – Hong Kong• Howden Asia Pte Ltd – Singapore• Howden Insurance Brokers LLC – Dubai• Howden Insurance Brokers India Private Limited –

Bangalore, Chennai, Hyderabad, Mumbai and New Delhi• Howden Insurance Brokers (2002) Limited - Tel Aviv• Howden Iberia SA – Barcelona, Madrid, Seville and

Valencia• Howden Insurance Brokers AB – Stockholm• Howden Insurance Brokers Oy – Helsinki• VK Howden LLC – Miami, Rio de Janeiro and San Juan• Howden Insurance Brokers Inc – Baltimore• Howden Corretora de Resseguros Ltda – Rio de Janeiro• Howden Iceland – Reykjavik• Hendricks & CO GmbH – Dusseldorf, Hamburg and

Munich

“We will aim to attractand recruit allindividuals, teams andbusinesses that weencounter who shareour passion for growthand desire to achieve. ”

TIM COLESCHIEF EXECUTIVE OFFICERHOWDEN BROKING GROUPAND HOWDEN INSURANCEBROKERS

HOWDEN BROKING GROUPDESPITE MARKET CONDITIONS, the Howden Broking Group recorded outstanding results with revenue increasing by 42.9% from £23.8 million to £31.4 million. This was achieved through organic growth alone. The EBITDA developed strongly too,increasing by 232%.

Strong growth was delivered by the Lloyd’s broker, which continued diversification of its product portfolio and territorial reach by attracting 2 teams. The first is an International Property team that has strong links with the Far East. The team led theestablishment of Howden Asia during the year, opening offices in Hong Kong, Taiwan and imminently, Korea and Singapore.

The second team to join is a North American Property and Casualty team which has firmly established Howden in the NorthAmerican marketplace, creating an exceptional platform for much greater growth.

Our retail operation in Dubai opened in April 2008 and enjoyed an excellent year.

Literally, a day after the financial year-end, Howden acquired Hendricks and CO GmbH, the market leading Directors and Officersliability broker in Germany.

In the coming year, we anticipate strong growth from all of our established operations. Our strategic drive will focus on developmentof our retail presence in Europe, particularly in the UK. In addition, we will continue to expand our operations in emerging markets,particularly in the Far East and Latin America. This will be complemented by further diversification of the product base of our GlobalWholesale and Reinsurance Practice. Most importantly, we will aim to attract and recruit all individuals, teams and businesses that weencounter who share our passion for growth and desire to achieve where others cannot.

12 HYPERION INSURANCE GROUP

GROUP BROKING - HOWDEN BROKING GROUP

13HYPERION INSURANCE GROUP

GLOBAL WHOLESALE &REINSURANCE PRACTICEOVERVIEWThe Global Wholesale and Reinsurance Practice comprises allHowden operations providing services to clients that requireaccess to product expertise and insurance markets beyondtheir domestic or direct markets. The practice serves clientsacross the world from bases in London, the USA and the FarEast. Its capabilities currently include Financial Lines, Property,Casualty and Binding Authorities. An important feature of thebusiness is its ability to instantly access markets globally,creating arbitrage opportunities and greatly broadening therange of placement solutions available to clients.

THE MARKETThe negative effects of a global recession and continued declineof insurance premiums in nearly all sectors were offset by a‘flight to quality’ by clients who often sought the expertise ofspecialist brokers and strong insurers based in established,competitive insurance markets. This was most notable forthose operations providing access to the London insurancemarket, all of whom enjoyed reinvigorated interest frominternational clients, particularly those seeking Financial Lines.Foreign exchange rates were also more favourable this year.

2008-2009 HIGHLIGHTSOur strategies of product and territorial diversification gainedfurther traction during the year. We acquired a team thatsubstantially increased our International Property capability. Italso led establishment of Howden operations in Hong Kong,Taiwan and imminently Korea and Singapore, creating in ashort time-frame, an excellent platform from which to further

develop in the Far East. We also acquired an outstandingNorth American Property and Casualty team which has firmlyestablished Howden in the North American market andprovided a base which is already developing further. Given theturmoil in financial markets, it was pleasing that our expertisein Financial Institutions was in much demand with the relevantindividuals and teams performing outstandingly, particularly inLatin America which had an exceptional year.

OUR PEOPLEWe were very pleased that so many outstanding peoplejoined our business throughout the year. It was particularlygratifying to experience our expansion in the Far East, NorthAmerica and Latin America. We will continue to target andattract exceptional people and teams, which are the key toour success.

THE FUTUREGrowth is the over-riding focus for the Global Wholesale andReinsurance Practice. The strategy for the coming year is tocapitalise on momentum gained in the regions in which wehave recently established. We will also continue to expand theproduct portfolio in order to provide more products andservices to our valued client-base. Most importantly, we willcontinue to develop a cohesive and aligned structure in whichclient focus and a team approach is promoted above all else.

PHILIP BONDMANAGING DIRECTORPROPERTY DIVISION

CHARLES LANGDALEMANAGING DIRECTORINTERNATIONAL

JOHN PLUMMERMANAGING DIRECTORNORTH AMERICANPROPERTY & CASUALTY

PATRICK GILHAMCHAIRMANINTERNATIONAL

GROUP BROKING - HOWDEN BROKING GROUP

DUBAITHE MARKETWith a population of 5.5 million people, the UAE has a totalgross written premium of US$5 billion, of which the LifeInsurance market comprises about 20%. Despite the slowdown in the economy the insurance industry continued togrow in the first half of 2008 but by the third quartervolumes started to decline sharply accompanied by a fall inprices as rates softened.

2008-2009 HIGHLIGHTSDespite a tough business environment and a challengingeconomic climate faced by our customers, we met ourbudgeted revenue of AED 4.5 million and produced a PBT ofover AED 1 million which far exceeded the budget.

OUR PEOPLEWe are very proud of our excellent team of just under 20people. Our professionals are highly motivated and businesssavvy with the operational staff having a high level oftechnical expertise. Our excellent record of client retentionand consistent growth in new business is proof of our team’scommitment to excellent efficiency and gaining new business.

THE FUTUREWhilst we will strive to increase our market share in theLiability and Financial Lines, we will continue to focus onbuilding volume from Medical Insurance, Employee Benefits,Property and Motor Insurance. New initiatives includeestablishing a legal entity in the Dubai International FinancialCentre and a branch in Abu Dhabi.

“Our excellent recordof client retention andconsistent growth innew business is proof ofour team’s commitmentto excellent efficiencyand gaining newbusiness. ”

ARVIND KASHYAPAMANAGING DIRECTORHOWDEN DUBAI

14 HYPERION INSURANCE GROUP

GROUP BROKING - HOWDEN BROKING GROUP

15HYPERION INSURANCE GROUP

GROUP BROKING - HOWDEN BROKING GROUP

INDIATHE MARKETThe size of the Non-Life insurance market in India is overINR 300 billion in gross written premiums and accounts for0.65% of the country’s GDP. Following the dismantling oftariffs by the IRDA (the regulatory authority in India) twoyears ago, fierce price competition amongst direct insurerscontinues. With adverse combined ratios, several insurersare beginning to feel the heat. While the sharpest fall inpricing has been witnessed in the property insurancesegment Liability and Health insurance too have seendownward trends.

It is expected that predatory pricing tendencies will continuefor a couple of years before the market stabilizes. Brokerswho are currently fighting for a small portion of the marketshare are eventually likely to emerge as an importantdistribution channel as the market matures.

2008-2009 HIGHLIGHTSIn our core Commercial Insurance business we crossed INR100 million income target and achieved a growth in income of18% compared to the previous year. We are privileged tocount some of the blue chip companies in India amongst ourcustomers, and have succeeded in adding several newcustomers. New business accounted for over 35% of incomein 2008-2009.

Regrettably, we have exited the Personal Lines insurancedistribution business that yielded losses due to a combinationof poor timing and lower than expected productivity.

OUR PEOPLEHowden is proud of the quality of its people and the way inwhich we work together to generate business value. As of 30September 2009, we have 55 people in our team.

Our professionals come from a multi-disciplinary background.The company has a campus recruitment programme andrecruits ‘management trainees’ from reputed businessschools. To retain and nurture talent, we place a strongemphasis on capability development and we have put in placevarious training programmes including induction modules.

THE FUTUREWe shall continue to seek growth in our core businessdespite a very soft local market. We expect to continue ourstrong income growth next year, driven largely by our threecore verticals – Financial Lines, large Property insurance andEmployee Benefits. New initiatives have been taken toenhance market share in large accounts and employeebenefits space. In line with our business plan our focus is onachieving our financial targets through investing in buildingthe right team.

“We are privileged tocount some of the bluechip companies in Indiaamongst our customers,and have succeeded inadding several newcustomers. ”

PRAVEEN VASHISHTAMANAGING DIRECTORHOWDEN INDIA

ISRAELTHE MARKETThe local insurance market in Israel is well developed,sophisticated and highly competitive and traditionallypremium rates have been very low in comparison to otherterritories. Despite the global economic crisis, growth hasslowed down but the economy has continued to grow bymore than 5%. Premium rates have levelled but some sectorsnotably financial institutions, have increased substantially.

Substantial claims, the continuous weakness of stock marketsand no Initial Public Offerings have given us a challengeparticularly as the largest D&O insurer in Israel.

2008-2009 HIGHLIGHTSDespite the volatility of the market, our year has beenexceptional, generating US$7 million in new premiumincome. We have achieved a 23% increase in income and a26% rise in profit year on year, an impressive performance.

We have broken the dominant position of one local player inMedical Malpractice now gaining a substantial market shareand we have become the market leader in insuring LifeScience companies.

OUR PEOPLEOur employees are passionate about the business and theirenergy, tenacity, drive and determination will bring continuedsuccess to our company.

As an insurance retailer, our success in building andmaintaining our relationship with our clients is fundamentalto our growth. All our account executives are trainedextensively and in the past 6 years we have obtained anaverage of over 50 new clients per quarter.

THE FUTUREWe will maintain our position as the leading business criticalinsurance broker in the region and enhance our market sharethrough our ability to build long-term relationships with newclients.

Our success in developing new product lines, includingMedical Malpractice and Product Liability together with LifeSciences gives us three strong products which will generategrowth going forward.

16 HYPERION INSURANCE GROUP

GROUP BROKING - HOWDEN BROKING GROUP

“ Despite the volatility of the market, our yearhas been exceptional,generating US$7million in new premium income. ”

DANNY SEVERCHAIRMANHOWDEN ISRAEL

SPAIN & PORTUGALTHE MARKETAs previously forecast the Spanish economy continues tosuffer from the effects of an economic crisis hampered also byits economic model based on real estate and constructionover the past decade. The impact of high unemployment, highpublic debt and stagnated growth for GDP (1.5%) in 2009,and (0.5%) in 2010 cannot be underestimated.

Although the impact has been felt in the insurance market itdoes not mirror the macro effect described above. Overallgrowth for 2009 is 1.7%, mainly driven by a 6.5% growth inLife Insurance, with a flat rate for Non-Life, and a (6.4%)decrease in Motor Insurance.

The future remains uncertain and will depend on the abilityof the Spanish economy to shift from its traditional incomesources.

2008-2009 HIGHLIGHTSThis year completes our original 3 year plan devised in 2006.Throughout this period we have created a platform forfuture growth with 4 locations in Spain and plans to expandin the North Region and in Lisbon. Our turnover of €25million with €3.25 million income is testament to theprofessional and dedicated team we have working for us.Overall a 560% growth across this period has beenimpressive.

In 2009 we have consolidated our position as market leaderin Private Medical Malpractice and Professional Indemnity and gained significant growth in two new areas, Surety andCivil Works Construction. Taking into account the difficultieswe face with Spain’s economy and our market we havecommissioned a team of specialists to expand into the creditinsurance arena.

OUR PEOPLEOur staff is renowned within the sector for its professionalismand creativity. The combination of autonomy, methodology,commitment, best practice, and providing a good workingenvironment makes us a highly desirable place to work.

THE FUTUREOur next 3 year plan aims to take the company to aprojected income above €6 million with a 20% profit rate.We will leverage the value of our team created during thepast 3 years and will also aim to continue to attract topindividuals.

“Our turnover of €25million with €3.25million income istestament to theprofessional anddedicated team wehave working for us. ”

JOSE-MANUEL GONZALEZ PEREZMANAGING DIRECTORHOWDEN IBERIA

17HYPERION INSURANCE GROUP

GROUP BROKING - HOWDEN BROKING GROUP

SWEDEN & FINLAND - NORDIC REGIONTHE MARKETThe Swedish insurance market is mature with most majorinternational brokers competing for business.

2008-2009 HIGHLIGHTSThe fierce competition driving down premiums has had anegative impact on our business. Our rating of AAA (Swedishbenchmark defined by Solidtet) has however, been maintainedand UC, Sweden’s leading Business and Credit Informationagency has assessed our risk as Class 5 the lowest risk.

We have won some exciting new business providing Boliden,Sweden’s largest mining company with Liability and MarineInsurance and Risk Management and we have developed a nichespeciality within trade credit and political risk insurance as wellas assisting companies who require export finance assistance.

OUR PEOPLEHowden AB is a well renowned insurance broker, whichhandles a broad range of large Swedish and internationalclients. We specialise in all lines of Corporate Non-Lifeinsurance including Trade Finance supporting cover. It istherefore paramount that we employ the best staff, with thenecessary expertise and experience, and operate within themost effective structure. We have strived to establish anextremely creative and innovative group of people, and toachieve the best balance between age and experience.

THE FUTUREOur ability to recruit the right people into a businessoperating in a highly competitive market is pivotal to meetour aim to grow our business by 30%.

18 HYPERION INSURANCE GROUP

GROUP BROKING - HOWDEN BROKING GROUP

THE MARKETMarket conditions in Finland remain challenging in view of theoverall situation in the liability insurance markets and therelatively new Act on Insurance Intermediaries, as well as theimpact of the global credit crisis; and in the case of Finland itsdependence on the export industry.

2008-2009 HIGHLIGHTSThe impact of the crisis has however, increased awareness inliability issues and insuring these risks. As the only pureliability specialist broker in Finland we have increased ourcustomer base by 30%. This is as a result of the increasedsales effort implemented in the early part of the year.Furthermore, the profitability of the company increasedsignificantly.

OUR PEOPLEHowden Oy team have achieved these results in a very toughenvironment and we intend to strengthen our team further.

THE FUTUREWe cannot see local insurance markets strengthening. Ourdirect contacts to international markets and our expertisegive us a clear advantage in our service to our clients.

In the forthcoming year Howden Oy will focus on increasingits co-operation with our Swedish sister company tofacilitate joint opportunities in the Nordic region. At thesame time we are searching for partners in other Nordiccountries so that in the near future we can have a trulyNordic Howden platform in place to exploit the weakness ofour competitors.

PASI HEIKKINEN MANAGING DIRECTORHOWDEN INSURANCEBROKERS OY - FINLAND

JESPER BRETZMANAGING DIRECTORHOWDEN INSURANCEBROKERS AB - SWEDEN

UNITED STATES / LATIN AMERICATHE MARKETMarket conditions in 2009 were marked by decliningpremiums and increasing competition. New capacitycontinues to enter the markets we serve which increases thechoice available to clients. New capacity providers typicallyhave ambitious premium targets and it is usually throughlower premiums that they hope to gain market share.

Whilst this market environment results in increasedcompetition and margin pressures, it also provides forinteresting opportunities. Insurers are more flexible and areseeking competitive advantage in the development of newproducts which we can often capitalize on.

2009-2010 HIGHLIGHTSThe biggest news during the fiscal year was the decision toalign our London and Latam based teams into a single globalwholesale unit offering clients worldwide market access. Bycombining the profit centers into a single unit we are able tobetter leverage markets on behalf of our clients and achievesuperior terms, conditions, and pricing.

Other highlights include: • We officially opened our office in Brazil and received our

SUSEP license to act as a local reinsurance intermediary inearly 2009

• We have reached a licensing/representation arrangementwith a local consultant in Mexico which will significantlyaid our “in country” marketing efforts

OUR PEOPLEOur firm is its people. Our insurance professionals are highlytechnical, with virtually all having amassed substantial brokingand underwriting experience in their careers. The technicalexpertise of our people, business producers, brokers andsupport staff is unmatched by any of our competitors whichprovides our firm with a strong competitive advantage in themarkets we serve.

Our Latam broking team and support service includeapproximately 12 people in 5 offices including personnelbased in Miami and London.

THE FUTUREWe expect to continue our regional and product expansionin Latin America as well as to launch additional productsincluding middle market property. Although marketconditions continue to be challenging we are optimistic aboutthe market opportunity given our focus on niches andrelentless focus on customer service and delivery.

“The technical expertise of our people,business producers,brokers and supportstaff is unmatched byany of our competitors.”

BOBBY VERNONMANAGING DIRECTORVK H OWDEN

19HYPERION INSURANCE GROUP

GROUP BROKING - HOWDEN BROKING GROUP

20 HYPERION INSURANCE GROUP

UNITED KINGDOMOur UK Retail operation’s strategic approach is that we aresector specialists who know insurance. Our focus onunderstanding a client’s sector and business results in aholistic approach to providing clients with the right productsat the right price, and underpins the structure andopportunity for long-term partnerships. We source acombination of insurances which fit specific requirements andwhich recognise the lifetime value of a client, from start-upbusinesses to recognised industry leaders. The structure ofthe team reflects our client-centric strategy and is currentlysplit into three key areas:

Howden Risk Partners occupies an increasingly dominantposition in the provision of bespoke management liabilityinsurance to the investment industry.

Professional Risks specialise in the provision of liabilityinsurances for a number of professions including engineers,insurance intermediaries and surveyors. We have beendeveloped in conjunction with professional memberassociations, leading insurers and specialist law firms tobespoke insurance packages which recognise the nuances ofrisk in individual professions.

Howden Affinity was significantly restructured, which haslaid the foundation for our future growth plans within thisarea. The business has expanded from being a specialist onlyin Complimentary Therapy and now includes a broadergroup of membership associations and franchise companies.

2008-2009 HIGHLIGHTSOur client focus has led us to listen and respond to ourclients’ buying needs for insurances other than those whichare core. As a result we have extended our capabilities toinclude a flexible, commercial, combined proposition to caterfor the varied needs of clients across our teams.

OUR PEOPLEThe division’s key capability is the quality of our people. Thisenables us to retain our existing clients and win new ones.As such, the division has made a number of key hires in thepast year; extending, strengthening and deepening ourexisting capabilities in line with emerging client needs.

THE FUTUREAlignment with client needs will define the development ofthe division’s capabilities and distribution platforms. Thiswill involve:• The acquisition of individuals and teams who exhibit the

Howden culture• A focus on marketing• Client research via the establishment of client boards• Benchmarking the Business in each sector against

competitors to understand changing market and sectordynamics

Whilst the UK retail business continues to operate within adiverse and competitive market, we are confident that ourcontinued focus on efficiency, sector specialism, and thequality of our people will deliver our ambitious growth plans.

GROUP BROKING - HOWDEN BROKING GROUP

“We have extended ourcapabilities to include aflexible, commercial,combined propositionto cater for the variedneeds of clients acrossour teams.”

MIKE LOBBMANAGING DIRECTORRETAIL

21HYPERION INSURANCE GROUP

GROUP UNDERWRITINGINTRODUCTIONThe underwriting arm of Hyperion was formed in 1998when the Group’s first underwriting agency, DUAL Ibérica,was established in Madrid. An underwriting agency has abinding (or delegated) authority given by an insurer to grantcover on the insurer’s behalf within certain pre-agreedparameters. Underwriting agency businesses act as a virtualinsurer, performing all of the functions typically performedby an insurer other than retaining the ultimate balancesheet risk. Hyperion operates underwriting agencybusinesses through Avant, CFC Underwriting, DUAL andVK Underwriters.

CFC UNDERWRITINGCFC Underwriting was established in 2000 to takeadvantage of growing technology industry risks and is basedin the Lloyd’s building in London. Although specialising inLiability insurance for technology businesses, it hasremained flexible in its approach to underwriting risk andhas developed new lines wherever an opportunity exists. Inthe USA, for example, it provides its broker clients with aLiability product designed to satisfy USA requirements forminimum insurance coverage of nursing homes.

DUALDUAL is the largest underwriting agency in Hyperion andconsists of eight offices in Germany, Italy, Spain, the UnitedKingdom, Hong Kong and Australia. These offices aresupported by a headquarters in London, DUAL International.Initially focusing on Directors & Officers and ProfessionalIndemnity, it has broadened its offering to brokers withPension Trustee Liability, Employment Practice Liability, andCommercial Crime and Fraud products. Its strategy hasalways been to sell insurance to low risk / low volatilityassureds focusing on profitable underwriting.

VK UNDERWRITERSThe origins of VK Underwriters date back to 2003, when a Miami-based intermediary established a contract tounderwrite Directors & Officers Liability insurance on behalfof several prominent insurance providers. Over the last fiveyears, the company has expanded its product offering toinclude a full suite of Liability products. VK Underwriterscontinues to focus on SME companies domiciled mostly inLatin America.

CFC UNDERWRITING OFFICE• CFC Underwriting Limited – London

DUAL OFFICES• DUAL International Underwriting Limited – London and

Hong Kong• DUAL Corporate Risks Limited – Dublin, London and

Manchester• DUAL Australia Pty. Limited – Brisbane, Melbourne,

Perth and Sydney• DUAL Deutschland GmbH – Cologne• DUAL Ibérica Riesgos Profesionales SA – Madrid• DUAL Italia SpA – Milan

VK UNDERWRITERS OFFICE• VK Underwriters – Bogota, Buenos Aires, Mexico City,Miami and Puerto Rico

DUAL INTERNATIONALDUAL’S CORE BUSINESS IS THE PROVISION of D&O Liability, Management Liability and Professional Indemnity insurance,principally to small to medium-sized enterprises and mid-market buyers in the UK, Europe, Australia and the Far East. In the last 5years DUAL has underwritten half a billion euros in premiums for our capacity providers, whilst delivering highly profitableunderwriting results.

The DUAL Group has enjoyed another strong year in a very challenging economic environment. GWP increased to €115 millionfrom €106 million in 2007-08. Rates continued to fall in most of our core product lines, albeit more slowly, but significant growthcame from new PI, D&O and Financial Lines initiatives in the UK, and from PI and Management Liability products in Australia.Over 44% of DUAL’s new premium income came from first-time buyers.

Our UK operation, DUAL Corporate Risks, launched its DUAL Focus product for mid-market Financial Lines D&O and PI and hasrecently recruited a respected team from ARGO-Heritage to expand this capability. It has just opened a new office in Dublin.

DUAL Australia became DUAL Asia Pacific with the opening of our Hong Kong office – our first in the Far East. It continues tooutperform its local competitors, with its fast, efficient product delivery and by providing service standards which others finddifficult to match.

DUAL Deutschland continues to grow well and to increase its profile in the local market. Its retention ratio of 90% is testament tothe superior service that the office provides to its German and Austrian clients. 85% of its new policy holders are first-time buyers.

In Southern Europe, the DUAL Ibérica and DUAL Italia offices performed well in extremely tough local conditions. DUAL Italiastands on the brink of an exciting new phase in its distribution plans, with its entry into bancassurance and the export of itsspecialist expertise into reinsurance solutions.

At the end of the year we welcomed VK Underwriters under the DUAL Group umbrella. VKU (formerly a division of Hyperion’sinsurance broking capability) underwrites Latin American and Caribbean business out of 5 offices, and brings welcomediversification to the DUAL Group – in product lines and territories, as well as in capacity providers.

22 HYPERION INSURANCE GROUP

GROUP UNDERWRITING - DUAL

“ In the last 5 yearsDUAL has underwrittenhalf a billion euros inpremiums for ourcapacity providers,whilst delivering highlyprofitable underwritingresults. ”

BOB VAN GIESONCHAIRMAN AND CHIEFEXECUTIVE OFFICER DUALINTERNATIONAL

23HYPERION INSURANCE GROUP

GROUP UNDERWRITING - DUAL

ASIA PACIFICTHE MARKET The Australian market maintains its position as one of thelargest Professional Lines markets in the world, totallingAUS$1.5 billion in insurance premiums.

The growth potential in the Professional Lines market, despitebeing competitive, remains buoyant (14% over the last 12months) due to the continuing rise in professions requiringPersonal Indemnity (PI) cover.

D&O and Management Liability has good growth potential asless than 10% of private companies purchase these forms ofinsurance. DUAL currently estimates its share of the marketto be between 6-7%.

The Asian market is however, considered less developed witha total market size of US$400 million. As Hong Kongrepresents over 25% of the market, the opening of an officethere is a logical entry point for our Asia Pacific expansion.

2008-2009 HIGHLIGHTSOur expansion geographically and in product developmentduring 2009 has been significant. A newly recruited team hasspearheaded our first major product expansion into theAccident and Health insurance market and we are nowoperating in Sydney, Melbourne, Perth, Brisbane and HongKong. Our gross premium base has increased by 26% duringthis period.

Our partnership with MSIG, one of the largest insurersthroughout Asia, will enable us to develop the AsianProfessional Lines market successfully.

OUR PEOPLEOur people are our strength and always will be. Over thelast 12 months, we have expanded our team from 28members to 35. We encourage a culture of “work hard, playhard”, a fact which has been key to our success and we havea strong commitment to invest in people and technology.

THE FUTUREThe expansion of DUAL in Asia Pacific continues to remain inline with the original plan prepared in 2004 which wouldinvolve an Asia Pacific Professional Lines capability focusing onthe mid-market. The plan for the future has now developedfurther for DUAL to be a Specialty Lines capability whilstcontinuing to focus on the mid market. In the coming yearswe will continue to expand our product range such as A&Halong with continuing our goal to build market share in theProfessional Lines market both in Asia and Australia.

“The expansion ofDUAL in Asia Pacificcontinues to remain inline with the originalplan prepared in 2004. ”

DAMIEN COATESMANAGING DIRECTORDUAL AUSTRALIA

GERMANYTHE MARKETThe German Non-Life insurance market’s value is around €55billion of gross written premium, of which D&O and Errors &Omissions (E&O) accounts for about €450 million. With anestimated 28 suppliers underwriting D&O, in a market which isonly 20 years old, it is highly competitive. The impact of thefinancial crisis has however, created a rise in D&O premiumsfor Financial Institutions and we are well placed to takeadvantage of this, helped by media coverage raising awarenessof the need for our product.

The SME market is underdeveloped and product penetrationstands at approximately 20% leaving us with an excellentopportunity for steady growth going forward. DUAL is alsoamong the few suppliers in Austria.

2008-2009 HIGHLIGHTSIn 2009, in testing market conditions, we succeeded inmeeting our planned budget. Our gross written premiumincome was approximately €10 million which demonstrates avery impressive achievement for a young business.

DUAL Deutschland’s reputation for expertise and knowledgeof the insurance market is well respected as is our exemplaryservice. Our market position is outstanding following theearly launch of our combined D&O/E&O product for FinancialInstitutions. With the support of Great Lakes/Munich Re, awell rated capacity provider, we are able to keep ahead of ourcompetitors.

OUR PEOPLEWe have been very successful in employing engaged, service-driven, highly motivated staff whose expertise covers keyareas including law, business administration and insurancescience, coupled with industry experience.

We maintain our fault-free, outstanding client service. Ourkey success is our people who understand that success isabout building and maintaining relationships with our clientsand their engagement and genuine enthusiasm is key togrowing our business going forward.

THE FUTUREThe German D&O and E&O market is still underdevelopedand gaining our market share will be a major objective as wellas continuing to build our presence in the Austrian market.We expect a continuation of the rapid increase in premiumvolume levels in these markets over the next years.

24 HYPERION INSURANCE GROUP

GROUP UNDERWRITING - DUAL

“Our gross writtenpremium income wasapproximately €10million whichdemonstrates a veryimpressive achievementfor a young business. ”

HEINER EICKHOFFMANAGING DIRECTORDUAL DEUTSCHLAND

ITALYTHE MARKETThe Italian market’s value of €95 billion GWP is sharedamong 246 insurance companies and 245,000 intermediaries.Banks largely dominate Life business whilst 76% of Non-Lifeand Non-Motor is placed by insurance agents with brokersaccounting for another 14% of the market share.

Recent laws based on EEC directives and new local insuranceregulations have significantly changed the market environmentincreasing the need for qualifications, transparency andresponsibility, aligning Italy with the most developed insurancemarkets and creating a fairer and more competitiveenvironment.

Market studies have demonstrated that Italian intermediariesbelieve that foreign insurers offering focused, specialisedinsurance solutions will be those most likely to dominate thedrive for growth, particularly in the PI arena.

2008-2009 HIGHLIGHTSSince its establishment, DUAL Italia has written more than€60 million of GWP with €12 million in 2009. Our ability tooffer tailor made sophisticated insurance solutions alongsideoff the shelf products resulted in the issue of 6,500 policies,an increase of 55% on the previous year.

Our strategy to build and reinforce our distribution networkhas come to fruition and now consists of 400 insuranceintermediaries of which 50 are agents.

This year DUAL Italia concluded two important reinsurancedeals enabling RSA Italy and UNIQA Protezione to issue their

own branded PI and D&O policies through their own networkof agents using DUAL’s products and expertise. Arch providesthe reinsurance capacity and DUAL Italia acts as a hub andspoke for any tailor made quotations and as a claims handler.

DUAL Italia is now unquestionably recognised as a marketleader in the Italian PI and D&O market.

OUR PEOPLEOur stated goals are to create innovative products, providehigh quality service, and retain and improve relationshipswith our distribution network. The only way to achieve thisis through employing and cultivating highly motivatedindividuals who want to achieve these goals with us andbelieve in our culture.

THE FUTUREGoing forward, we will focus on our ability to satisfy the needsof our distribution network, the quality of our products, andour brand awareness to maintain our enviable position as abenchmark company within the PI and D&O markets.

Our aim is to create a broad, diversified and loyal distributionbase alongside alternative distribution models includingreinsurance agreements with Italian companies. We are alsoexploring the potential of the emerging bancassurance D&Oand PI market. This represents an exciting opportunity forDUAL Italia going forward.

“DUAL Italia is nowunquestionablyrecognised as a marketleader in the Italian PIand D&O market. ”

MAURIZIO GHILOSSOMANAGING DIRECTORDUAL ITALIA

25HYPERION INSURANCE GROUP

GROUP UNDERWRITING - DUAL

SPAIN & PORTUGALTHE MARKETSpain and Portugal have both been strongly hit by the worldeconomic turmoil under which DUAL Ibérica has had totrade during the last year. Spain, in addition to the financialcrash, will need to recover from the bursting of anunprecedented housing market bubble.

Despite the difficult economic enviroment, the insuranceindustry has continued its constant softening trend. TheProfessional Liability insurance market appears once again tobe failing to take stock of the Spanish and Portugueseeconomy, and the forecast increase in the amount of claims.

2008-2009 HIGHLIGHTSDespite very competitive and aggressive market conditions,we have succeeded in achieving the budgeted revenuestream, €27.6 million in gross written premium. We haveachieved this by maintaining the prudent underwritingparameters established to ensure acceptable earnings fromprofit commissions.

Most of the strategic and commercial objectives defined atthe beginning of the year have been satisfactorily achieved.The shift to a portfolio in which non-construction relatedprofessionals have gained greater prominence is an impressiveachievement that has proven a key factor of success in thecurrent economic environment.

OUR PEOPLEDuring our 11 years of trading, the DUAL team has clearlydemonstrated an ability to meet budgets and maintain solidunderwriting parameters. This is a unique achievement in theSpanish and Portuguese market, and an enviable one from aglobal perspective.

We have only been able to achieve this success because ofthe outstanding levels of experience and expertise embodiedby our team.

THE FUTUREDUAL’s undeniable solid foundations will ensure we continueto maintain the levels of growth achieved over the last 11years. Our brand is based upon sustainable competitivedifferences and a strong commercial focus on new businessopportunities and is combined with a recognised reputationfor handling claims and an obsessive focus on underwritingprofitability.

DUAL is one of the leading choices in the market and ourchallenge is to make sure that we maintain this enviableposition.

26 HYPERION INSURANCE GROUP

GROUP UNDERWRITING - DUAL

“Despite verycompetitive andaggressive marketconditions, we havesucceeded in achievingthe budgeted revenuestream, €27.6 million ingross written premium.”

LUIS MUÑOZ-ROJASENTRECANALESMANAGING DIRECTORDUAL IBÉRICA

27HYPERION INSURANCE GROUP

GROUP UNDERWRITING - DUAL

UNITED KINGDOMTHE MARKETThe market continues to be broadly competitive particularlyin the commercial D&O and PI lines and we are witnessingsome sensible risk taking in the Financial Institutions lines. We believe this will continue for the rest of the year.

2008-2009 HIGHLIGHTSThere are a number of significant highlights to report duringthe past year.

Our gross written premium increased from £30 million to£43 million, an increase of 43% on the previous year.

Unfortunately, due to the large reserves for solicitors’ claimsin the year, the Profit Commission received in December washowever, significantly lower than in previous years. GWP forD&O increased from £20 million to £27 million (up 31%) andPI from £10 million to £16 million (up 66%).

During the year we launched our Broker RelationshipManagement Programme. This will enable us to betterunderstand the needs of our key brokers and identify andrealise new business opportunities with them.

We opened the doors to our Dublin office in November2009 and have successfully recruited two ex AIGunderwriters and Brian Martin will head up this operation.

The DUAL Focus product was launched during the year withGWP of £3 million being written. In October two ex ARGOunderwriters Liz Hanlon and Beth Whybrow joined us. GWP

is expected to grow from £3 million to £7.8 million in2009/2010.

We have repositioned our Manchester office as a NationalBusiness Unit. This will be responsible for the growth anddevelopment of all high volume/low premium initiatives. Thiswill enable our more specialist underwriters in London tofocus on more complex risks with a higher GWP value.

OUR PEOPLEDUAL has welcomed a significant number of new people intothe company this year, notably boosting our size and capacityacross all departments.

It is at the core of our philosophy that we invest in people ofthe highest quality, expertise and motivation in order toremain competitive in such difficult market conditions.

THE FUTUREOur success has always been founded upon offering asuperior service to our brokers and delivering excellentunderwriting results for our capital providers.

Predictions are that 2010 will remain a highly challengingmarket, with cautious economic forecasts and increased PIclaims activity. However, by sticking closely to our focusedunderwriting strategy we will continue to increase oursuccess and perform with strength.

“Our gross writtenpremium increasedfrom £30 million to£43 million, an increaseof 43% on the previousyear. ”

RUSSELL KILPATRICKMANAGING DIRECTORDUAL CORPORATE RISKS

UNITED KINGDOM (CFC)THE MARKETThe market has softened for all of our product lines over thelast five years, but the overall market size has grown as a resultof increasing market penetration. We expect continued growthin each of our key product lines over the next three years.

2008-2009 HIGHLIGHTSCFC had another very successful year with growth in revenue of22% and profit of 41% against the backdrop of a global recessionand a very competitive insurance market. However, the mostsignificant achievement during this period was the developmentof scalability in a number of different areas leaving the businessextremely well positioned to deliver on the exciting growthplans which form the next phase of our development.

One of our core values is to be 'product-obsessed' and thisinvolves regular reviews of our products and services. We havehoned our product development and launch processes and arewell positioned to refresh existing products and launch newones into multiple countries very quickly. This is fast becominga major source of competitive advantage and at the beginningof the year we re-packaged and re-launched our entireproduct range. Since then we developed and launched a highlyinnovative insurance product targetting drug developmentcompanies, entered the D&O insurance market and launched anew product suite, MedSuranceTM, which focuses on small longterm care facilities. The re-launch of the existing products andthe introduction of several new ones represented a significantinvestment for CFC, but it was just one of several large-scaleinvestments during the year.

The launch of our new internal computer system, NERD has

had a significant impact on our business providing us withgreat efficiencies and producing superior managementinformation that will drive better informed business decisionsgoing forward.

CFC has also developed online delivery of small businessinsurance via insurance brokers, developing and licensingonline systems to brokers in a number of countries that theyare able to 'white-label' as their own. We provide thesesystems at very low cost to brokers who manage securebooks of homogeneous business, or to brokers who areprepared to invest considerably in online marketing.

The combination of these two new systems enables us notonly to provide insurance brokers with a powerful and uniquetool but we can transact business on a ‘no-touch’ basisallowing us to enter the micro business insurance marketwithout incurring the high costs associated with distribution.As a result, we will benefit from economies of scale.

OUR PEOPLEWe now employ 32 people who are all based in London. Thecompany benefits from a strong management team with agreat deal of experience of the London and internationalinsurance markets. Significant emphasis is placed onenhancing the service and product culture of the business byemploying highly motivated, top calibre people.

THE FUTURESince its formation in 2000, CFC has achieved great success.The initiatives we have successfully implemented this yearwill provide the foundation to accelerate our growth.

28 HYPERION INSURANCE GROUP

GROUP UNDERWRITING - CFC UNDERWRITING

“CFC had anothervery successful yearwith growth inrevenue of 22% andprofit of 41% againstthe backdrop of aglobal recession and avery competitiveinsurance market. ”

DAVID WALSHMANAGING DIRECTORCFC UNDERWRITING

29HYPERION INSURANCE GROUP

GROUP UNDERWRITING - VK UNDERWRITERS

LATIN AMERICA & THE CARIBBEANTHE MARKET As expected, 2008-2009 presented challenges for businessgrowth. While there was some notable stability and increasein pricing for financial institution products the general trendremained a downward one, liability premiums, professional,management and general alike. New entrants into the LatinAmerica and Caribbean markets create new competitorswhose need to grow and diversify their business putssignificant pressure on pricing. The increased presence ofmultinational companies in the reinsurance arena createsgreater retention of risk and less facultative reinsuranceopportunities. These factors combine to influence “fac”underwriters to become more aggressive in their acquisitionand retention of business, thereby further perpetuating thedownward pressure on pricing.

2008-2009 HIGHLIGHTSVK Underwriters successfully concluded its spin-off andincorporation into Dual International. We secured separateMGA Licenses in Florida, which sets the stage fordevelopment into the North America liability market. Havingopened a new subsidiary in San Juan, Puerto Rico, with theincorporation of a General Agency to service Puerto Rico,we are positioning ourselves for a smooth and successfulemergence into neighbouring Caribbean countries. We alsohave increased our capacity for Professional Liability andsigned an agreement to begin offering Crime Insurance.

OUR PEOPLE All of our underwriters possess a vast amount of technicalknowledge coupled with extensive, practical experience inthe markets they serve. With the incorporation of oursubsidiary in Puerto Rico we have invested significantly inhuman resources and attracted both a recognized andrespected senior manager and the most seasonedProfessional Indemnity manager in Latin America.

Fortifying the core to our success, we have been fortunate inattracting people who are committed to providing outstandinglevels of service to both our clients and capacity providerpartners.

THE FUTUREThroughout 2009 and 2010 we will look to consolidate andleverage our now robust distribution and underwritingnetwork in Latin America and the Caribbean. We also planto initiate our underwriting operations in the US market.

In addition to pricing trends, two areas of concern that weplan to monitor closely are terms and conditions and trendsin liability awards. A combination of continued downwardpricing, increases in liability awards and enhanced terms andconditions will cause greater strain on profitability. And thismust be controlled in the weak investment incomeenvironment.

Although market conditions continue to be challenging andcompetitive , we remain optimistic about the ability of ourpeople to continue to deliver for our clients, capacityproviders and shareholders.

“Fortifying the core toour success, we havebeen fortunate inattracting people whoare committed toproviding outstandinglevels of service to bothour clients and capacityprovider partners. ”

MATT KELLYCHIEF UNDERWRITING OFFICERVK UNDERWRITERS

30 HYPERION INSURANCE GROUP

HYPERION INSURANCE GROUP LIMITED

FINANCIAL STATEMENTS

YEAR ENDED 30 SEPTEMBER 2009

Directors’ report 32 - 35

Statement of directors’ responsibilities 35

Independent auditors’ report 36

Consolidated profit and loss account 37

Consolidated statement of total recognised gains and losses 37

Consolidated and company balance sheets 38

Consolidated cash flow statement 39

Reconciliation of net cash flow to movement in net funds 39

Notes to the consolidated financial statements 40 - 61

Hyperion contact details 62 - 64

31HYPERION INSURANCE GROUP

FINANCIAL STATEMENTS

The directors submit their report and audited financial statements

for Hyperion Insurance Group Limited (“the Company”) together

with the consolidated financial statements of the Group for the year

ended 30 September 2009.

PRINCIPAL ACTIVITYThe principal activity of the Company during the year was that of a

holding and investment company for a group of insurance

intermediaries. The Group’s trading operations comprise wholesale and

retail insurance broking, reinsurance broking and underwriting agencies.

REVIEW OF THE BUSINESSThe Board is pleased to report that, against an extremely

challenging financial market background, the Group reported 19%

growth in operating income to £57.2m (2008 - £48.0m). EBITDA

excluding exceptionals was £8.8m, up 7% (2008 - £8.2m). Operating

profit, before exceptional items, was £5.9m (2008 - £6.0m).

Excluding profit commissions, operating income increased by 38%

and EBITDA excluding exceptionals grew by £6.4m. Profit

commissions were down by £5.6m in 2009 as expected in light of

the overall economic turmoil.

The Group’s broking operations reported revenues of £34.1m

(2008 - £23.8m). This 43% increase reflects further growth in

International and North America Property following the recruitment

of two teams in London as well as solid growth in Israel and Spain

and new offices in South East Asia and Latin America, partially offset

with the impact of further declines in premiums and brokerage, and

the impact of weak Sterling. Against this difficult background, the

Group’s broking operations reported profits of £4.6m (2008 - £0.6m)

and this reflects the maturity of the broking group as many of the

initiatives undertaken in the past start to pay off.

DUAL International’s underwriting agency operations had a

successful year. Gross written premium increased by 34% to £107m

and total revenues excluding profit commission by 43% to £14.9m.

This result reflects solid underlying growth. Whilst all DUAL offices

reported satisfactory results except DUAL Asia, which started to

trade only in May 2009, particularly strong performances were

achieved in the UK, Australia and Italy.

CFC, the Group’s other underwriting agency operation, had a very

successful year. Gross written premiums increased by 34% to

£30.0m, and profit after tax rose 44% to £1.7m.

Including VK Underwriters, the Group’s other underwriting agency

based in Miami, the total gross written premiums for the

underwriting agencies was £142m.

During the year, the Group raised £3m of additional working capital

through a shareholder loan facility, and also secured shareholder loan

note financing of €4.5m for the acquisition of Hendricks & Co GmbH,

of which €3m was received before year end. This loan note is the first

utilisation of the £25m funding committed in March 2008 by 3i,

supported by other major shareholders.

The Group’s trading operations are geographically diverse, with

different market positions and strong specialities. A number of

recently established businesses have yet to complete their initial

development phase. During the year the Group established

operations in five new countries; we now have 45 offices in 22

countries with over 600 employees across the Group including

associates. The management focus is on revenue and profit against

historic and budgeted performance levels, and in the DUAL and

CFC businesses, there is close monitoring of the underlying

underwriting performance. The Group also monitors revenue and

profit per employee, staff costs as a proportion of revenue and

overall brokerage as a percentage of premiums.

FUTURE DEVELOPMENTSWhilst the market background remains difficult, there is evidence

that premium and commission rates are beginning to stabilise and

that overseas earnings are improving following the weakening of

Sterling against a number of currencies. These place the Group in a

strong position and the prospects for its continued growth are very

positive.

RESULTS AND DIVIDENDSThe loss of the Group for the year after taxation and minority

interests amounted to £14,000 (2008 - profit of £1.2m). The loss of

the Company was £4.6m (2008 - profit of £2.5m). No equity

dividends were paid during the year (2008 - £nil). The subsidiary

and associated undertakings included within the Group are

disclosed in notes 14 and 15 to these financial statements.

CHARITABLE DONATIONSDuring the year to 30 September 2009 the Group made cash

donations of £14,000 (2008: £nil) for the benefit of charitable causes.

POST BALANCE SHEET DATE EVENTSOn 1 October 2009, the Group’s subsidiary Howden Broking Group

Limited completed the acquisition of 75% of the issued shares in

Hendricks & Co GmbH, the leading D&O insurance broker in

Germany. This is the first major acquisition since 3i acquired a

minority stake in the Group in March 2008. The acquisition of

Hendricks & Co GmbH is an important development in the further

expansion of the Group’s international broking network.

The Group is currently obtaining approval for a license in Singapore,

has just opened a Dual office in Ireland, and is in the process of

negotiating the sale of JK Buckenham Limited.

DIRECTORS’ REPORT

32 HYPERION INSURANCE GROUP

DIRECTORS’ REPORT

DIRECTORSThe directors who served during the year are listed below:

J P de Blocq van Kuffeler Chairman (appointed 1 February 2009)

D P Howden Chief Executive

L I Muñoz-Rojas Entrecanales

E R Fady

T S Howden

E H Woolf

D A Whileman

R T Van Gieson (appointed 22 July 2009)

R J R Elias (resigned 31 January 2009)

S J Crowther (resigned 20 July 2009)

B P Marsh (resigned 11 November 2009)

DIRECTORS AND OFFICERS LIABILITYINSURANCEThe Company has purchased insurance to cover directors’ and officers’

liability, as permitted by section 233 of the Companies Act 2006.

CORPORATE GOVERNANCEHyperion is committed to maintaining high standards of corporate

governance. We recognise that good governance helps the business to

deliver our strategy and safeguard shareholders’ long term interests.

We believe that the Combined Code provides a useful guide and we

apply these principles as appropriate to a group of our size.

In addition to the Chairman, the Board currently comprises four

executive directors, and five non-executive directors who bring an

appropriate balance of experience and knowledge, whereby the Board’s

decision making cannot be dominated by an individual or small group.

AUDIT, REMUNERATION AND INVESTMENTCOMMITTEESThe Board has delegated certain responsibilities to Committees that are

described below, all of which have formally constituted terms of

reference. It does not consider that the Group is of sufficient size to

justify the establishment of a permanent Nomination Committee and all

matters relating to Board appointments are therefore dealt with by the

Board itself, or by a subcommittee specifically formed for that purpose.

Audit Committee

The Audit Committee comprises three non-executive directors and

is chaired by Emile Woolf. The Committee meets at least four times

a year. Meetings are attended, by invitation, by the Company’s

external auditors, the finance director and members of his staff,

compliance officers and internal audit.

The Committee’s role is to assist the Boards of the Company and

its subsidiaries in fulfilling their responsibilities with regard to

accounting policies, internal control, financial reporting functions,

risk assessment, compliance and related matters.

Remuneration Committee

The Remuneration Committee comprises four non-executive

directors and is chaired by John van Kuffeler. The Committee meets

at least four times a year. Meetings are attended by the Chief

Executive and by the Group Human Resources manager. Other

individuals and external advisers may be invited to attend for all or

part of any meeting as and when appropriate.

The Committee’s overall responsibility is to balance the various

interests of shareholders, the Company and its employees, with the

aim of ensuring that the Company, through its remuneration policy

is able to attract, retain and motivate management and senior staff

of appropriate experience and expertise.

INTERNAL CONTROL & RISK MANAGEMENTThe Board is responsible for maintaining a sound system of internal

control and risk management, and for reviewing its effectiveness to

safeguard shareholders’ investments and Group assets. There is no

absolute means of preventing material loss and/or misstatement,

and the Group’s internal controls reflect a balanced judgement,

taking into account the direct costs of controls as well as the

indirect costs of being over-bureaucratic, which provide reasonable

assurance against material loss and/or misstatement.

The Group’s internal controls are tested and key business risks are

evaluated on a continuing basis, using Internal Audit, Compliance,

and other relevant expertise. The Group maintains insurance cover

against certain risks, including fidelity insurance.

THE BOARDThe Board is responsible for maintaining effective control over

significant strategy, financial, organisational, legal and regulatory

matters. It meets at least six times a year. Management supply the

Board with appropriate and timely information and the directors are

free to seek any further information they consider necessary.

PRINCIPAL BUSINESS RISKS AND UNCERTAINTIESThe Group’s operations specialise in business critical liability

insurance such as professional indemnity insurance, directors and

officers’ liability insurance and related products. The Group is

thus exposed to the cyclical factors that affect the insurance

market, and premiums and commissions. Whilst its underwriting

agency operations are not directly responsible for claims, claims

costs do affect the level of profit commission that the Group

receives.

Further, the Group’s international focus (which is one of its most

important strengths) exposes its revenues to currency fluctuations,

mainly sterling/dollar and sterling/euro. The Group has floating-rate

borrowings in Sterling, US dollars, Australian dollars and Euros and

is therefore also exposed to interest rate movements in those

DIRECTORS’ REPORT (CONTINUED)

33HYPERION INSURANCE GROUP

DIRECTORS’ REPORT

currencies. The Group has put in place appropriate hedging

strategies to manage this risk.

The Group is ambitious and seeks to grow by means of acquisitions

and organic growth. Such activities are inherently uncertain,