Embed Size (px)

Citation preview

REPORt & ACCOUNtS 2012

HYPERION INSURANCE GROUP

Highlights 8

Group Timeline 10

At a Glance 12

Group Footprint 14

Chairman’s Statement 16

Chief Executive’s Review 18

Board Structure 24

Howden Broking Group 26

DUAL Group 30

Corporate Social Responsibility Policy 34

Risk Management 38

ConSoLiDATED FinAnCiAL STATEMEnTS 42

Directors’ Report 44

independent Auditor’s Report 50

Consolidated income Statement 51

Consolidated Statement of Comprehensive income 53

Consolidated Statement Financial Position 54

Consolidated Statement of Changes in Equity 55

Consolidated Cash Flow Statement 56

notes to the Consolidated Accounts 57

CoMPAny FinAnCiAL STATEMEnTS 98

notes to the Company Financial Statements 100

CoMPAny ConTACTS 104

Cover:

olympic marathon runners pass Hyperion’s head office in London

CONtENtS

The Matthew Harding Trophy for the Lloyd’s of London Football Tournament.

2012 Champions: Howden.

At the heart of the Group’s success is the quality of our people.

The Group’s vision is to be an independent, innovative, courageous,

dynamic, great company, and that vision will continue to be delivered

by attracting the best people and empowering them to make us

insurance partners of choice for clients.

Hyperion Insurance Group was founded in 1994 and is headquartered in the City

of London. Beginning life as an insurance broker, the Group is now an international

insurance intermediary group with divisions in broking and underwriting.

In 2012 the Group turned 18, and received its second Queen’s Award for Enterprise

in International Trade.

18 YEARS

32

5

In 2012, over 1200 employees in our operations around the world were

responsible for delivering our record growth. Their energy, innovation and

entrepreneurialism continues to drive the Group’s success.

1200EMPLOYEES

4

Hyperion Insurance Group companies serve clients around the world from

67 offices in 28 countries across Europe, the Middle East, Asia Pacific

and the Americas.

28COUNTRIES

76

• HyperionInsuranceGroupacquiredtheoperationsofAccetteInsuranceGroupinSingapore,HongKong,Malaysia,ThailandandthePhilippinesinNovember2011andinIndonesiainJuly2012.

• DUALlaunchedTamesisDUAL,specialtyexcessoflossreinsurancebusinesssupportedwithcapacityfromLloyd’sofLondon,inNovember2011.

• HyperionInsuranceGroupLimitedwaslistedintheSundayTimesBuyoutTrack100asoneof theUK’sfastestgrowingcompanies,andintheSundayTimesInternationalTrack200asoneoftheUK’scompanieswiththefastestgrowinginternationalsales.

• InApril2012HyperionInsuranceGroupwasawardeditssecondQueen’sAwardforEnterpriseinInternationalTrade.

• HyperionInsuranceGroupacquiredWindsorLimitedinJuly2012.Windsor’sLloyd’sbrokingbusinesswaslegallyintegratedintoHowdenInsuranceBrokersLimitedinOctober2012.

• DUALopenedofficesinSingaporeinMay2012,AustriainJune2012,andNewYorkinAugust2012.

• DUALwasnamedUnderwritingAgencyoftheYearattheBritishInsuranceAwardsinJuly2012.

• HowdenBrokingGroupacquiredamajority stakeinBrazilianbrokerConsetSegurosin September2012.

HIGHlIGHtS

Howden’s Madrid office welcomes clients and colleagues to thank them for their

support and partnership

67 offices 28 countries

1200 employees

98

1110

1995 19961994 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

1994 2008 2010 20121996 2004

DUAL Australia, Sydney

2002

DUAL Corporate Risks, London

Davidoff Howden, Israel

Howden Risk

Partners, London

InternationalProperty Services

Team Stage 2

North American Property & Casualty

Team

Howden, Dubai

DUAL Iberica,Barcelona

InternationalProperty Services

Team Stage 1

VK Howden LLC,Miami

Howden Insurance

Brokers Inc., Baltimore

DUAL Australia,Perth

Howden, Singapore

Howden, Korea

Dual Corporate

Risks, Ireland

DUAL New Zealand

Accette GroupSouth-East Asia

Tamesis DUAL, London

Broking activity of Davidoff Insurance

Brokers, Israel

Broking activity ofPYV Ltd, London

Howden SpecialityUnderwriters,

Miami

1998

DUAL International

DUAL Iberica, Madrid

Howden Iberia, Madrid

Howden Pangborn (‘HP’) formed

(25% investment by BP Marsh, 75% by

David Howden andMark Pangborn)

2000

CFCUnderwriting

Howden OY,Helsinki

Howden,Iceland

DUAL Italia, Milan

Spear Gulland,London

2006

DUAL Deutschland, Cologne

DUAL Australia, Melbourne

DUAL Corporate Risks, Manchester

Howden, India

Holm & Co – later renamed

Howden Insurance Brokers AB,

Sweden

Hendricks, Germany

Howden, Taiwan

Howden, Brazil

Howden, Hong Kong

DUAL Asia, Hong Kong

VK Underwriters, Miami and Latin America

DUAL Australia, Brisbane

DUAL Singapore

DUAL New York

Accette Indonesia

Windsor Limited, UK

Conset Seguros, Brazil

DUAL Austria

1994 2008 2010 20121996 2004

DUAL Australia, Sydney

2002

DUAL Corporate Risks, London

Davidoff Howden, Israel

Howden Risk

Partners, London

InternationalProperty Services

Team Stage 2

North American Property & Casualty

Team

Howden, Dubai

DUAL Iberica,Barcelona

InternationalProperty Services

Team Stage 1

VK Howden LLC,Miami

Howden Insurance

Brokers Inc., Baltimore

DUAL Australia,Perth

Howden, Singapore

Howden, Korea

Dual Corporate

Risks, Ireland

DUAL New Zealand

Accette GroupSouth-East Asia

Tamesis DUAL, London

Broking activity of Davidoff Insurance

Brokers, Israel

Broking activity ofPYV Ltd, London

Howden SpecialityUnderwriters,

Miami

1998

DUAL International

DUAL Iberica, Madrid

Howden Iberia, Madrid

Howden Pangborn (‘HP’) formed

(25% investment by BP Marsh, 75% by

David Howden andMark Pangborn)

2000

CFCUnderwriting

Howden OY,Helsinki

Howden,Iceland

DUAL Italia, Milan

Spear Gulland,London

2006

DUAL Deutschland, Cologne

DUAL Australia, Melbourne

DUAL Corporate Risks, Manchester

Howden, India

Holm & Co – later renamed

Howden Insurance Brokers AB,

Sweden

Hendricks, Germany

Howden, Taiwan

Howden, Brazil

Howden, Hong Kong

DUAL Asia, Hong Kong

VK Underwriters, Miami and Latin America

DUAL Australia, Brisbane

DUAL Singapore

DUAL New York

Accette Indonesia

Windsor Limited, UK

Conset Seguros, Brazil

DUAL Austria

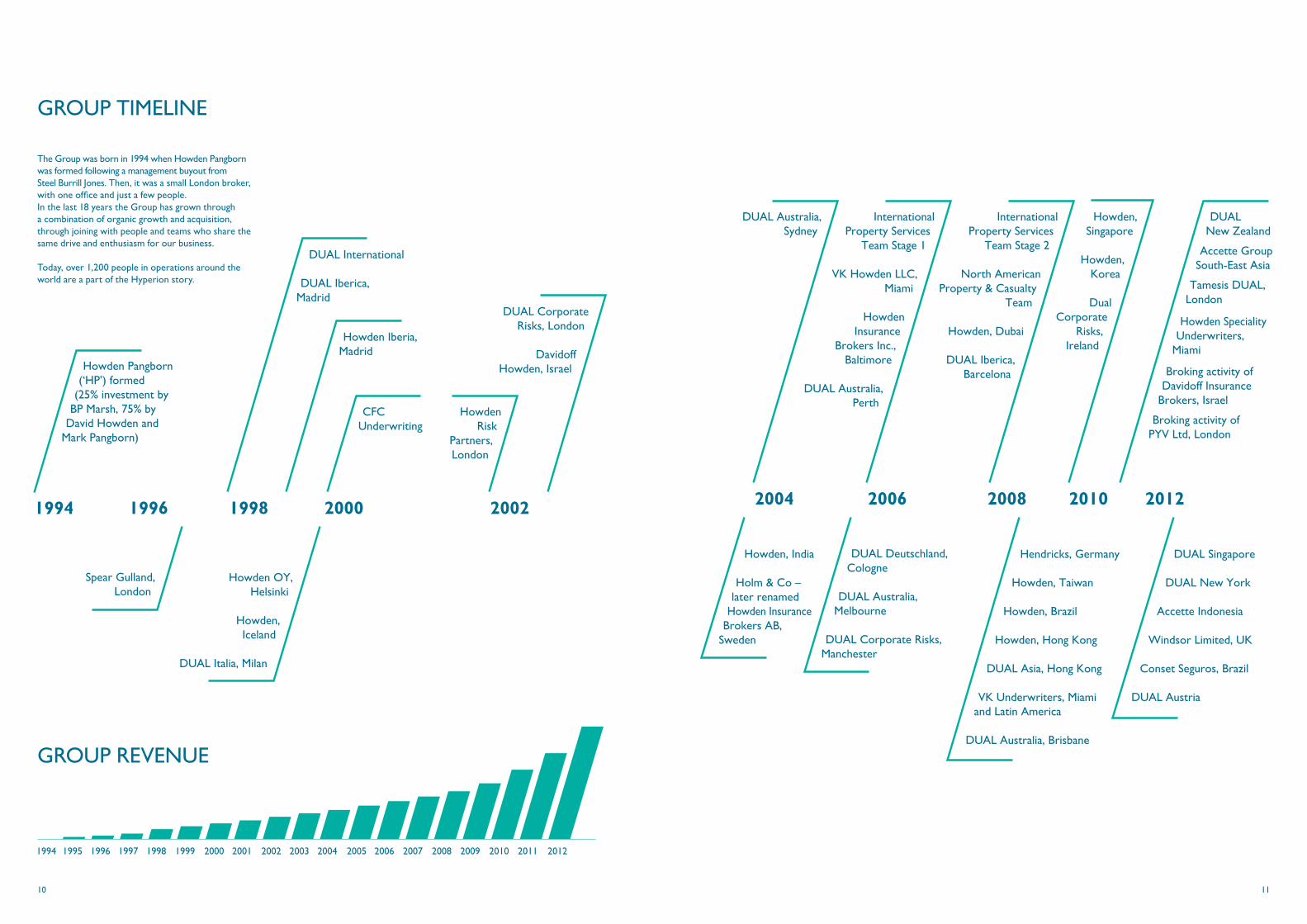

GROUP tImElINE

GROUP REvENUE

TheGroupwasbornin1994whenHowdenPangbornwasformedfollowingamanagementbuyoutfrom SteelBurrillJones.Then,itwasasmallLondonbroker,withoneofficeandjustafewpeople.Inthelast18yearstheGrouphasgrownthrough acombinationoforganicgrowthandacquisition,throughjoiningwithpeopleandteamswhosharethesamedriveandenthusiasmforourbusiness.

Today,over1,200peopleinoperationsaroundtheworldareapartoftheHyperionstory.

1312

EBITDABEFoRE non-RECURRinG iTEMS AnD ACqUiSiTion CoSTS

£20.6m

mARGIN: 18.6%

HYPERION At A GlANCE

AVERAGENUMBEROFEMPLOYEES 1,020

FEESANDCOMMISSION:BROKING£75.1m

EARNINGS PER SHAREFRoM ConTinUinG oPERATionS BEFoRE FAiR VALUE ADJUSTMEnTS, non-RECURRinG CoSTS AnD ACqUiSiTion CoSTS

15.0 PEnCE

GROUP REvENUE£111m

GROSSWRITTENPREMIUM:UNDERWRITING£228m

20

40

60

80

100

120

£m

0‘11 ‘12‘10‘09

‘09 ‘09 ‘09 ‘09

5

10

15

20

25

£m

0‘09 ‘10 ‘11 ‘12

200

400

1200

1000

800

600

0‘09 ‘10 ‘11 ‘12

10

20

40

30

50

60

70

80

£m

0‘09 ‘10 ‘11 ‘12

50

100

150

200

250

£m

0‘09 ‘10 ‘11 ‘12

2

4

14

12

10

8

6

16

0‘09 ‘10 ‘11 ‘12

Revenueofcontinuingoperationshasincreasedby 42%to£111m(continuingoperations)andEBITDA isup40%(excludingnon-recurringandacquisition costsanddiscontinuedoperations)to£20.6m.

OUR PROdUCtS

HOWDENBROKINGGROUPincome by Product

Property 21%

Professional indemnity 20%

Directors and officers 18%

GL, PL, EL 9%

Accident and Health 4%

Employee Benefits 4%

BBB 3%Marine 3%

Clinical Trials 2%2%

Energy

CAR/EAR 6%

Treaty, Medical Malpractice, Fi Crime, Motor Fleet, Surety, Aviation, Personal Lines1% each

dUAl GROUP GWP by Product

Directors and officers 33%

Financial institution Crime 5%

BBB, Property and Treaty each 2%

General Liability 1%

Accident and Health 4%

Marine 7% Professional indemnity 45%

1514

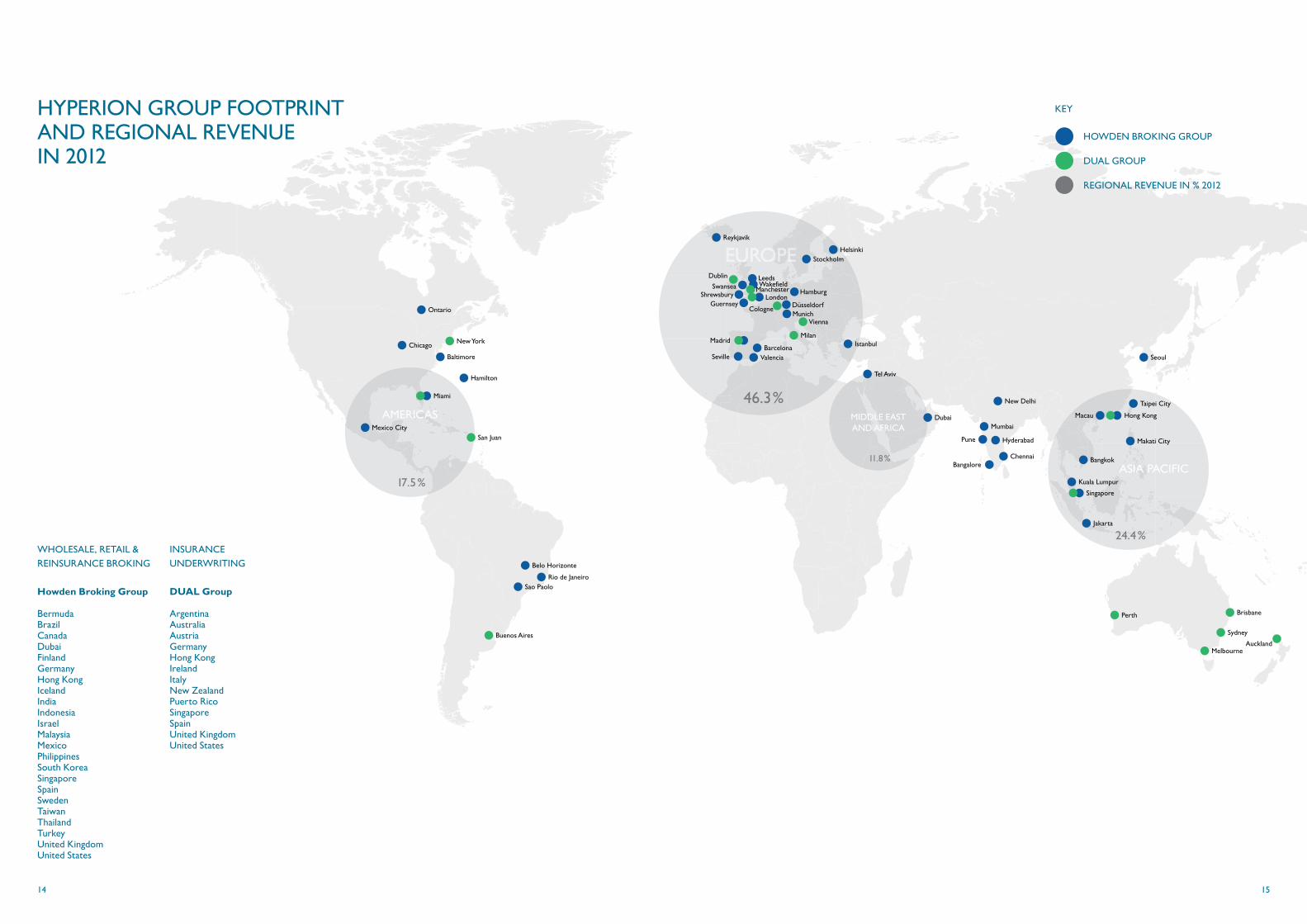

HYPERIONGROUPFOOTPRINTANd REGIONAl REvENUE IN 2012

KEY

HOWDENBROKINGGROUP

dUAl GROUP

REGIONAl REvENUE IN % 2012

WHOLESALE,RETAIL&

REINSURANCEBROKING

Howden Broking Group

BermudaBrazilCanadaDubaiFinlandGermanyHongKongIcelandIndiaIndonesiaIsraelMalaysiaMexicoPhilippinesSouthKoreaSingaporeSpainSwedenTaiwanThailandTurkeyUnitedKingdomUnitedStates

INSURANCE

UNDERWRITING

DUAL Group

ArgentinaAustraliaAustriaGermanyHongKongIrelandItalyNewZealandPuertoRicoSingaporeSpainUnitedKingdomUnitedStates

16

InSeptember2012,HowdenBrokingGroupacquiredamajoritystakeinBrazilianbrokerConsetSeguros.WithofficesinRiodeJaneiro,SaoPaoloandBeloHorizonte,andanexcellentreputationinthemarket,theacquisitionofConsetgivesHowdenafootholdinanotherimportantandgrowingglobalmarket. Afterinvestinginthecompanyasastart-upin2000,inApril2012theGroupsoldits59.5%stakeinCFCUnderwritingLimitedtoaconsortiumofprivateinvestorsandthemanagementteamforatotalof£20.8million. DUALhascementeditspositionasthelargestinternationalcoverholderatLloyd’s,andwithofficeopeningsinAustria,NewYorkandSingaporehasperformedextremelywellandiswellpositionedforfurthergrowth.

FINANCE,GOVERNANCE ANd OPERAtIONAl StRENGtHTherequirementtofinancetheacquisitionofWindsorwhilstprotectingouremployeeshareholdingssawtheGroupsecurefinancingof£90mduringoneofthelongestandworstfinancialcrisesinhistory,andisagreattestamenttothestrengthofHyperion’sbusinessmodel.EvenwiththisfinancingtheGrouphasconservativelevelsofdebt.

AcrucialpartoftheGroup’sstrategicdirectionisthestrengthoftheHyperionBoardanditsabilitytoguidetheGroupintothefuture,andIwasdelightedtowelcomeLordForsythtotheBoardinSeptember2012.Hisbackgroundandexperiencewillbeinvaluabletous.

Ongoinginvestmentinourmanagementandinfrastructuretoimprovetheagilityandeffectivenessofouroperationshasalsoseensignificantdevelopments.ThenewrolesofDeputyCEOforDUAL,CorporateandLegalDirectorforHowdenBrokingGroupandGlobalHRDirectorforHyperionarenotablestepsthathavebeenmadetoaddstrengthanddepthtoourmanagementteams. dIvIdENd2012hasbeenayearofsignificantinvestmentsinnewinitiativesandthefurtherdevelopmentofourinfrastructure,butthestronggrowthinrevenueandprofitabilityallowedustopayanincreaseddividendof3.1pencepershare(2011–2.8pence)toshare- holdersontheRegisteron30thSeptember2012.

PEOPlETheGroup’sabilitytoattractqualitypeople,businessesandteamshasresultedinanumberofimportantnewinitiatives;theacquisitionofWindsorinJuly2012andthelaunchofDUAL’sSpecialistLiabilitydivisioninNovember2012areexamplesfrombothsidesoftheGroupwhereHyperionhasbeenthepartnerofchoice.AttractingtherightpeopleisalsoattheheartofHyperion’sacquisitions,which,asaguidingprinciple,arebaseduponjoiningwithlike-mindedpeoplewherethesumofwhatwecandelivertogetherisgreaterthanthatwhichwecandeliveralone.Theabilitytoquicklyrealisesynergiesandvalueforourclients,shareholdersandemployeesistheresult,asevidenced,forexample, bytheperformanceofourbrokingoperationsinAsiaandourstart-upunderwritingoperationin NewZealand.

Theeffectivenessandefficiencywithwhichweintegratebusinessesisoneofourgreatoperationalstrengths.ParticularmentionthisyearmustgotothecentraloperationsteamsinvolvedinintegratingWindsor;theyhaveworkedextremelyhardtobringtheLloyd’sbrokingbusinessestogetherandwearealreadybeginningtoseethebenefitsfromthis.

ThenumberofemployeesintheGrouphaspassed1,000forthefirsttime,andtheevidenceoftheircontributioncontinuestopresentitselfintheexternalrecognitionthattheGrouphasreceivedthisyearforbothitsfinancialperformanceandthequalityofitsactivities.In2012,HyperionfeaturedintheSundayTimesBuyoutandInternationalTracks,placingusamongstthefastestgrowingcompaniesintheUK.Foritsstrategy,growthandcommitmenttocustomerneeds,DUALwasnamedUnderwritingAgencyoftheYearattheBritishInsuranceAwards;andfinally,forcontinuousachievement,theGroupwonitssecondQueen’sAwardforEnterpriseinInternationalTrade.

MythanksgotoeachoftheGroup’semployeesfortheirhardworkandsupportinwhathasbeenaveryspecialyearfortheGroup.

JOHNVANKUFFELERCHAiRMAn

CHAIRMAN’S StAtEmENt2012hasbeenanextremelyimportantyearintheevolutionofHyperionInsuranceGroup.Wehaveexpandedourgeographicreachwithacquisitionsandstart-upoperationsinanumberoftheworld’smajorgrowtheconomies,andthecompletionofHyperion’slargestacquisitiontodate.

Thesedevelopmentsandaverystrongperformancefromboththeunderwritingandbrokingarmshaveproduceda42%increaseinrevenueanda40%increaseinEBITDAonprioryear(excludingnon-recurringandacquisitioncostsanddiscontinuedoperations).

Akeyperformanceindicator,andunderpinningtheGroup’ssustainablelong-termgrowth,isourorganicrevenuegrowth.Thisyearourorganicrevenuegrowthforcontinuingoperationswas12%-anexcellentresultinthefaceoftheongoingchallengespresentedbytheglobaleconomy.

PERFORMANCEAt30thSeptember2012,totalrevenueofcontinuingoperationswas£111m(£78min2011),andEBITDAwas£20.6m(£14.7min2011). StrongperformancesfromouroperationsinthefastergrowingpartsoftheworldandtheabilityoftheGrouptoquicklytransformnewinitiativesandinnovationintorevenueandprofitabilityhavebeennotablecontributorstotheseresults.

ACQUISITIONSANDSTRATEGICdEvElOPmENtThecompletionoftheacquisitionofspecialistLloyd’sbrokinggroup,WindsorLimited,inJuly2012,constitutedHyperion’slargestacquisitiontodate.Windsor’s220staffhavejoinedHowdenBrokingGroup,bringingwiththemcomplementarystrengthswhichaddsignificantbreadthtothecombinedbrokingarm’scapabilities,bydeliveringmoretoboththeUKretailpropositionandtoourglobalwholesaleandreinsuranceproposition.IamalsopleasedtowelcomemanyoftheWindsordirectorsandseniormanagementasHyperionshareholders.

TheacquisitionofAccetteInsuranceGroup’soperationsinSingapore,HongKong,Thailand,MalaysiaandthePhilippinesinNovember2011,andinIndonesiainJuly2012,hasprovidedanexcellentplatformforgrowthinsomeofthefastestgrowingeconomiesinSouthEastAsia.

JoHn VAn KUFFELER Chairman, Hyperion insurance Group

17

18

DAViD HoWDEn Chief Executive, Hyperion insurance Group

CHIEFExECUTIVE’SREVIEW

2012hasbeenalandmarkyearforHyperion.TheGrouphaspassedanumberofsignificantmilestones,notleastoftheseisthatinNovembertheGroupturned18.Thisfinancialyearhasseentwelvemonthsofachievementsanddevelopmentsfittingofour‘comingofage’.MostnotablewasouracquisitionofWindsorforanenterprisevalueof£94.7m,byfarourlargestacquisitiontodate,creatingwithHowdenaninternationalbrokinggroupofover1,000staff,operatingfrom47officesin22countries.

ThisyearsawGrouprevenuebreakingthe£100mmark.Significantly,priortotheacquisitionofWindsorwemadeamajordivestmentwiththesaleof CFCUnderwriting,nettingusaprofitofover£20mforour59.5%share,andfocusingourunderwritingactivityunderDUAL.

ItwaswithgreatprideinthepeoplewhoworkintheGroupthatIlearnedinAprilthatwewerewinnersofoursecondQueen’sAwardforInternationalTrade.WhenIlookbackatthecompanywewerein2007,whenwelastwontheQueen’sAward,itisinterestingtoseehowfarwehavecome.Atthetime,Hyperionhadjust355employeesin25officesand13countriesproducingrevenueof£34.1mandoperatingprofitofalittleunder£6m.

Thisyearwehavewontheawardforcontinuousachievementininternationaltradeoverasixyearperiod,withoverseasearningsgrowthofover250%.Ourrevenueandprofitsaretreblewhattheywerewhenwewonourfirstaward,representingaCompoundAnnualGrowthRateovertheperiodof22%.Thisrelentlessfocusonprofitablegrowthhasseen42%revenuegrowthfor2012to£111mand40%growthinEBITDAto£20.6m(excludingnon-recurringandacquisitioncostsanddiscontinuedoperations).Importantly,ourEBITDAmarginremainsstrongat18.6%forcontinuingoperations,evenwiththecostsofinitiativeslinkedtofuturegrowthengines,recruitingadditionalspecialists,andinvestingininfrastructure.Producingtheseresultsareover1,200peoplein67officesin28countriesacrossourbrokingandunderwritingoperations.

Thefoundationofourgrowthhasalwaysbeen,andwillcontinuetobeorganic.TheGroup’sorganicgrowthof12%in2012isanexcellentachievementinthecurrenteconomicclimate.NeverthelesstheacquisitionofbusinesseswhichwillthemselvesbehighgrowthaspartoftheGrouphasalwaysbeenakeyelementofourstrategy.Therearetwocriticaldriversofouracquisitionactivity:firstly,wejoinwithlike-mindedbusinessesandteamswithwhomweshareanoutlookandgoals.WeachievethisbecauseeveryonewepartnerwithhasinvariablytradedforsometimewithapartoftheGroup.Secondly,wemakeacquisitionsandenterintopartnershipswherethesumofthepartsissignificantlygreaterthantheirseparatevalues,andwherewecandelivermoretoourclientstogether.

Wecontinuetofocusonincreasingourprofitabilityasapercentageofourrevenue.CombiningWindsorwithHowdennotonlyprovidesourclientswithabroaderrangeofservicesandgreaterdepthofexpertise,butalsocreatesabrokinggroupofscalewiththeabilityforsuperioroperatingmargins.Likewise,whilstDUAL’sprimaryfocusisonunderwritingprofit,ithasdemonstrateditsabilitywithincreasedgeographicreachandproductdiversitytocreateoperationalefficienciesanddeliveranoperatingmarginofjustunder20%.

19

20

INSURER

INSURED

Economic Value Chain

Retail Broker

UnderwritingAgency

Wholesaleand

Reinsurance Broker

39%

32%29%

vISION ANd StRAtEGYMuchhaschangedthen!Importantlythough,muchhasalsoendured.AttheheartoftheGrouphasalwaysbeenthevisionthatwewanttobeanindependent,innovative,courageous,dynamic,greatcompany,andthatwewillachievethisbyattractingthebestpeopleandempoweringthemtomakeusinsurancepartnersofchoiceforclients.Thisisourculture,whichisattheheartofourgrowth. TheGroup’svisionisimplementedthroughfourareasofstrategy–ourfocusontheoptimalperformanceofouroperatingplatformsandthequalityofourdistribution,thedepth,breadthandinnovationofourspecialistproductsandourrelativemarketpositions,beingpartnersofchoiceforclients,insurersandbrokerstheworldover,andinvestinginanddevelopingtherightpeopletodeliverthebestsolutions.

PROCESSESANDDISTRIBUTIONUnderpinningourstrategyandgrowthisouruniqueinsurancedistributionmodel.Hyperionisatrueinsuranceintermediarygroup,withdistinctbrokingandunderwritingagencyarmsoperatingindependentlyofoneanother.Themodelisimportantfortwomainreasons,bothrelevantagainstthebackdropofthecontinuingglobaleconomicdifficulties.Firstly,ourstructurerecognisesandrespondstothespectrumofclientinsuranceneedsandenablestheGrouptocaptureagreaterproportionoftheeconomicvaluechain.Secondly,thedistinctplatformsprovideanaturalhedgeinearnings,reducingvolatilityoverthemarketcycle,whichhasallowedtheGrouptogrowprofitablythroughoutour18yearsthroughhardandsoftinsurancemarketsandpeaksandtroughsofeconomiccycles.

THEBALANCEOFOURMODEL

GroupRevenue

Ourdistributionplatformhasgrownsignificantly.WhenwelastwontheQueen’sAwardDUALhadjustsevenofficesinfivecountriesandpremiumincome hadexceeded£60mforthefirsttime.TodayDUALhas19officesin13countries,andhaswritten£228minpremium(up24%onprioryear)withanEBITDAof£9.9m(up20%onprioryear).HowdenBrokingGrouphasexpandedfrom19officesin10countries,withrevenueof£27.7mto47officesin22countrieswithrevenueexceeding£75m(up58%onprioryear)andanEBITDAof£12.1m(up42%onprioryear).OurcontinuedfocusonthegeographicbalanceoftheGrouphasseenasignificantshiftsincewewonourfirstQueen’sAward,whenjustover70%ofourrevenuecamefromEurope,lessthan10%camefromAsiaPacific,andlessthan10%fromtheAmericas. In2012,activitydrivingthegeographicbalanceofourdistributionisinevidenceinabundance:

• theacquisitionoftheAccetteInsuranceGroupoperationsinSouthEastAsiahasgivenusaplatformoffourteenretailbrokingofficesinAsiaandhascreatedatruepan-regionalnetworktosupportourclients;

• theacquisitionofamajoritystakeinwellregardedBrazilianretailbrokerConsetSeguroshasgiventheBrokingGroupitsfirstretailfootholdinLatinAmerica;

• alignmentofourunderwritingoperationsintheUSandLatinAmerica,withtherebrandingofVKUnderwritersandHSUtoDUALhascreatedastrongplatformforfocusedgrowth;

• officeopeningsinNewYork,AustriaandSingaporehaveextendedtheinternationalreachofDUAL,andhaveconnectedourcapacityproviderswithnewmarketsandmorebrokerswithnewcapacity;

• theacquisitionofWindsorhasextendedtheBrokingGroup’sUKretailfootprint,broughtnewwholesalebrokingrelationshipstothegroupfrommarketssuchasLatinAmericaandAustralia,andextendedbothourwholesaleandretailbrokingplatformswiththeadditionofnewcapabilitiessuchasMarineandAviation.

The Hyperion Strategy

Products and Positions

Processes and Distribution

People andOrganisations

Partnersof choice

Ourexpansiononprioryear,particularlyinemergingmarkets,isshowninthegraphsbelow.

FeesandCommissions2011and2012(£’000s)

Ourtechnologicaldistributioncapabilitiesarealsoacontinuedfocusfordevelopment;asanexample,DUALhascontinuedtoinvestinonlineplatformsviawhichitsbrokerscantransactmid-marketbusinesseffectivelyandefficiently.Withover30%ofDUAL’sbusinessnowtransactedonline,ourinvestmentinourtechnologicaldistributionisanimportantelementforthefuture.

Comparisonofregionalrevenue

5.000

10.000

20.000

15.000

25.000

30.000

0United

Kingdom2011Americas Europe Middle and

East AfricaAsia Pacific

2012

2006

70.3%

9.4% 10.8%

9.0%

2012

46.3%

17.5% 11.8 %

24.4%

21

2322

PROdUCtS ANd POSItIONS WhenwewonourfirstQueen’sAward78%ofourincomecamefromourtraditionalexpertiseinProfessionalIndemnityandDirectors’andOfficers’Insurance.Thisfellto60%lastyear,andforthe2012financialyeartheselinesaccountforjustover50%ofourincome.Ourtraditionallinescontinuetoshowgoodgrowth,butfurtherbalancehasbeenbroughtbytheintroductionofnewspecialistteamswhohavejoinedthebrokingarmsuchastheInternationalandNorthAmericanProperty,EnergyandMarineteamsandTamesisDUAL,launchedinNovember2011.

COMPARISONOFINCOMEBYPRODUCT

Hyperion Income 2006

Hyperion Income 2012

Withratescontinuingtochallengeinsomeareas,DUAL’srelentlessfocusonunderwritingforprofitanddeliveringlong-termprofitabilitytoitscapacityprovidershasseenmuchofitsgrowthcomefromnewproductsandnewmarkets.Alongsideitsnewoperations,continuedinnovationhasseenthelaunchofninenewproductsthisyear.

ByinvestinginnewoperationsaroundtheworldDUALhasgrownfromoneofficeinMadridin1998intotheworld’slargestglobalunderwritingagencyandisnowLloyd’slargestinternationalcoverholder,providingover£150mofpremiumtoLloyd’s.51%ofDUAL’sincomecomesfromEurope,and49%fromoutsideEurope,with36%ofthatfromAsiaPacific.ThesuccessofDUALisitsability,bycreatinganinternationaldistributionplatform,toaccessforitscapacityprovidersthelocalsmalltomid-marketbusinessthatisinherentlymoreprofitable,aswellasitsabilitytodevelopmarkets,evidencedbythefactthat40%ofDUAL’snewbusinessarefirsttimebuyers.

TheacquisitionofWindsorhasaddedanumberofadditionalareasofexpertisetotheBrokingGroup’sproductportfolio,withMarine,Aviation, PharmaceuticalandBindercapabilities,amongstothers,joiningthegroup.ThecombinedWindsorandHowdenProfessionalIndemnitydivisionisoneofthelargestspecialistteamsintheLondonmarket,placingover£140mofpremiumintotheLondonmarketandemployingover100people.

AsHyperioncelebratesits18thbirthdaysoanumberofournewinitiativescelebratetheirfirst;afteropeningtogiveourinsurersaccesstotheprofitablelocalGeneralLiabilitymarket,ourNewZealandunderwritingoperationturnedoneinMarch,havingachievedprofitabilitywithinsevenmonths. InNovember2012,TamesisDUAL,ouruniquespecialtyexcessoflossunderwritingagency,hadasuccessfulfirstyearwritingahighlyprofitablebookofover£20mpremium.

PARTNERSOFCHOICETheGroup’sabilitytocreatemeaningful,long-lastingrelationshipswithourpartners–betheyclients,employees,shareholders,capacityproviders,orbrokers–isvital.

Importantly,retentionratesremainhighinbothbrokingandunderwriting,asinvestmentinclientserviceremainscentrestage.Ourclientsarekey toourgrowth,asweexpandbothgeographicallyandinourproductcapabilitiesinlinewiththeirneeds. OurexpansioninLatinAmerica,forexample,ispartly drivenbytheinternationalrequirementsofourclients inSpain,whereourbusinessesarelisteningtotheirclientsanddevelopingtheirpropositionaccordingly.

In2006,DUALwasbackedbyArch.In2010,Hiscoxalsobecameamajorpartner,andtodayDUALhasrelationshipswith15othercapacityproviders,bringingbalance,breadthanddepthtotheunderwritingarm.Thisyear,amongstothers,Libertybecameamajorcapacityprovider,andDUAL’ssuccessfulpartnershipwithMSIGinAsiahascontinued withournewventureinSingaporegivingusaccesstothedevelopingmarketsofSouthEastAsia.

PEOPlE ANd ORGANISAtIONSWehavewelcomedmanypeopletotheGroupin2012,boththosewhohavejoinedusasaresultofacquisitionsandthosewhohavejoinedusaspartofspecialistteamsorasindividuals.

ThedevelopmentofourHRfunctionisextremelyimportant,andhastakenasignificantstepwiththerecruitmentofaGlobalHeadofHRtoleadthedeliveryofimprovedadministration,service,traininganddevelopment,andfurtherconsistencyacrossouroperations.

ThefutureoftheGroupliesnotonlyinourabilitytoattracttalentbutalsoinourabilitytodevelopit,andsoaspartofthisgoal,ourFutureLeadersProgrammewaslaunchedin2012,with21youngmanagersfromacrossourinternationaloperationsselectedtotakepartinaweek-longresidentialleadershipcourse.

Hyperionhasalwaysbeenanentrepreneurialbusinessinthetruesenseoftheword,andsoitisimportantthattodaywehaveover220employeesholdingsharesintheGroup,representingover60%ofourshareholderbase.

TheformationoftheHyperionCharityCommitteeishelpingtobringawell-deservedfocustothemanycharitableinitiativesthatHyperionemployeestakepartinandsupport.AMatchFundingschemeandtheinauguralInvestingintheCommunityAwardswerebothlaunchedin2012,andIwasparticularlypleasedtoseethevolumeandqualityofsubmissionsfortheAwards.HyperionalsosupportstheLloyd’sofLondonCommunityProgramme,andasignificantnumberofourLondon-basedstaffaregivinguptheirowntimetosupporttheinitiative.

OUTLOOKAfteranotherdifficultyearfortheglobaleconomy,withthedebtcrisisweighingheavilyonEuropeandtheeffectsofthecontinueddownturndampeningeventhehigh-growthemergingmarkets,ouroperationshaveperformedextremelywell. Thissuccessisachievedbyfocusingondoingtherightbusinesstherightway,bymakingtherightconnectionswithinsurers,brokersandclients,andbycontinuingtoinnovateandchallenge.

TheacquisitionofWindsorhasgivenHowdenBrokingGroupscale,andwithitssignificantgeographicreachanddepthandbreadthofexpertiseweareextremelywellpositionedtostandshouldertoshoulderwithourglobalcompetitorsaswecontinuetogrowthebusiness.

DUAL,namedUnderwritingAgencyoftheYearattheBritishInsuranceAwardsin2012,haslaunchedimportantnewoperationsandcontinuestodevelopnewproducts.Alongsidetherestructuringofitscapacityarrangementsandthestrengthofitsrelationshipswithitscapacityprovidersitiswellpositionedtocontinuetoprovideitsinsurerpartnerswithaccesstonewmarketsandtodeliverfurtherprofitablegrowthasaspecialtylinesunderwritingagency.

Withtheworld’sinsurancemarketsinthemiddleof afurtherwaveofconsolidation,ourrobustyetagilemodelalsopositionsuswelltowelcomemorelike-mindedindividuals,teamsandbusinessestotheGroup.

DuringdifficulttimesourbusinessesarebuildingstrongfoundationsforwhatIbelieveisabrightfuture.Therewillbechallenges,andthefocusforthecomingyearwillbetointegratethebusinesseswehaveacquiredandactivatethevaluethattheyandournewinitiativescancreate.

So,theGroupisverydifferentin2012towhatitwaswhenwewonourfirstQueen’sAward,butinsomewaysitisverysimilar:financialresultsandawardsalikearedeliveredandwonbypeople,andthisisjustthesametodayasitwasin2007.Mythanksthen, gotoourpartnersfortheircontinuedsupport, ourclientsfortheirloyalty,andtoeachofthe1,200peopleinthegroupformakingHyperionsuchafantasticplacetowork.

DAVIDHOWDENCHiEF ExECUTiVE, HyPERion inSURAnCE GRoUP

General Liability 2%

Professional indemnity 40%Financial

institutions 7%

Reinsurance 5%Property 3%

other 2%Medical Malpractice 3%

Directors and officers 38%

Professional indemnity 39%

Property 15%

General Liability 5%

Accident and Health (PA) 4%

other 3%

BBB 3%Employee Benefits 3%

Marine 3%

Product Liability, Employers’ Liability, Medical Malpractice, Treaty, Motor Fleet, Clinical Trials, Surety, Energy, CAR/EAR, Aviation, each1%

Directors and officers 24%

1. ERiC FADy, Group Finance Director, and DAViD HoWDEn, Chief Executive,collect Hyperion’s Sunday Times international Track 200 ranking

2. DAViD HoWDEn, STAnLEy Ko, Managing Director of Howden’s retail operation in Hong Kong, and members of the team

1.

2.

4.

1.

2.

3.

6.

8.7.

1.JOHNDEBLOCQVANKUFFELER non-ExECUTiVE CHAiRMAn

JohnvanKuffelerjoinedHyperionasNon-ExecutiveChairmaninFebruary2009bringingnearly40years’ofinternationalfinancialservicesexperiencetotherole.HejoinedProvidentFinancialin1991asChiefExecutive,andwasappointedChairmanin1997.PriortohiscareeratProvidentFinancialhewasChiefExecutiveofBrownShipley,theinvestmentbankinggroup.BothProvidentFinancialandBrownShipleyhadsignificantinsuranceoperationsandJohnwasalsoaNon-ExecutiveDirectoroftheMedicalDefenceUnion,theFounderandformerChairmanofDodsGroup,theAIMlistedpoliticalpublishingandmediagroup,andformerChairmanofEidosaswellastwoCitybasedinvestmenttrusts.HeisalsoChairmanofMarlinFinancialGroup,anAdvisoryBoardmemberofthePrince’sTrust,andaformerCouncilmemberoftheCBI.

2.ERICFADY GRoUP FinAnCE DiRECToR

EricjoinedHyperioninJune2008.HislastrolewasasFinanceDirectorforMarshEurope,MiddleEastandAfricafrom2003to2007,wherehemanagedmajorprojectstohelpthecompanyadjusttothepostSpitzerbusinessworld.PreviouslyhewasCFOandVicePresidentforStrategyImplementationforDun&BradstreetEurope&MiddleEastfrom1999to2002wherehecontributedtothedesignofthecompany’snewbusinessmodelandsignificantlyimprovedtheirperformance.EricgraduatedfromRheimsManagementSchool,andbeganhiscareerasanauditorwithKPMGinFrance.

3.LUISMUÑOZ-ROJASENTRECANALES ExECUTiVE DiRECToR

LuisisafoundingDirectorofDUALInternational. HeopenedthefirstDUALoperationinMadridinAugust1998,havingpreviouslyservedasDirectorofGyCAmérica,areinsurancebrokingsubsidiaryof GilyCaravajal(nowpartofAon).DuringthattimeLuishadconsiderableinvolvementintheLatinAmericanterritories.Luisbeganhisinsurancecareerin1989workingwithGyC&Partners,theBritishsubsidiaryoftheGyCGroup.

4.DAVIDHOWDEN CHiEF ExECUTiVE

DavidstartedhiscareerasabrokeratAlexanderHowdenin1980.HefoundedtheGroupin1994originallyasawholesalebrokeremployingjustfivepeople.Hehasbeenthefundamentaldrivingforcebehinditsexpansionintoaninternationalinsurancegroupofferingwholesale,retailandreinsurancebroking,andunderwriting.AsChiefExecutive,David’sfocusisonleadingtheGroup’sM&AactivitiesaswellasdirectingandimplementingtheGroup’sstrategicgrowthanddirection.

5.EMILEWOOLF non-ExECUTiVE DiRECToR

EmileisaCharteredAccountantandindependentinsuranceandlitigationconsultant.HeisformerChairmanofthePracticeInsuranceRequirementsCommitteeoftheInstituteofCharteredAccountantsinEnglandandWales,andofitsPanelofParticipatingInsurers.InparallelwithalongcareerprovidingExpertWitnessreportsontheconductofprofessionalaccountantsandauditors,heisaregularcolumnistin‘Accountancy’,thejournaloftheInstitute,andisoneoftheprofession’smostrespectedauthorsandlecturers.HewasthefounderoftheEmileWoolfColleges,whichtrainaccountantsinmanycountriesworld-wide.

6.DAVIDWHILEMAN non-ExECUTiVE DiRECToR

DavidisaPartnerinthe3iGrowthCapitalbusiness,investingupto€250mforstakeholdersinmarket-leadingbusinessesintheUKandacrossEurope.Hespecialisesinoriginatingandleadinginvestmentsintoprivatecompaniesseekingtoacceleratetheirgrowth,bothorganicallyandthroughacquisition.PastinvestmentsincludeFoster&Partners,theglobalarchitects,HayleyConferenceCentresandMorganMcKinley,thefinancialservicesbusiness.Davidisacharteredaccountantandpriorto3iworkedintheinsolvencydivisionwithinPricewaterhouseCoopers.

BOARDSTRUCTURE

7.JONATHANNEWMAN non-ExECUTiVE DiRECToR

JonathanwasappointedtotheHyperionBoardin2009.HeisGroupDirectorofFinanceatBPMarsh&PartnersPLC,aventurecapitalgroupthatspecialisesininvestingininsuranceintermediaries,andisacharteredManagementAccountantwithmorethan13years’experienceinthefinancialservicesindustry.HejoinedBPMarshinNovember1999andistheirnomineeDirectorontheboardsofseveralinvesteecompanies.

8.LORDFORSYTHOFDRUMLEAN non-ExECUTiVE DiRECToR

LordForsythwasappointedtotheHyperionBoardinSeptember2012.HeisaformerDeputyChairmanofEvercorePartnersInternationalandofJPMorganinLondon.PriortojoiningRobertFleming&Co.as aDirectorin1997hewasaCabinetMinisterandservedintheGovernmentsleadbyMargaretThatcherandJohnMajorformorethanadecade. HeisalsoaDirectorofJ&JDenholm,NBNKInvestments,theCentreforPolicyStudies,andSafor.

5.

2524

HowdenBrokingGroupisaninternationalbrokinggroupcomprisingretailoperationsacrossEurope,AsiaandtheAmericas,andaglobalwholesaleandreinsurancepracticebuiltaroundkeyglobalplacementandproductionhubs.

TheGrouporiginatedin1994asastart-upinsurancebrokerinLondon.Itisnowaninternationalspecialistbrokerwith47officesin22countriesandmorethan1000employees,distributingthroughretail,wholesaleandreinsurancechannels.

Revenue:£75.1m–increase58%EBITDA:£12.1m–increase42%

Numberofoffices:47Numberofcountrieswithoperations:22Numberofemployees:1,000+

Revenuedistributionchannels:retail59%, wholesale/reinsurance41%

2012wasamomentousyearforHowdenBrokingGroup;itwasayearofimportantstrategicinvestmentsinourdistributionplatform,anddeliveryofaverystrongperformancewithrevenuesup58%andEBITDA(excludingnon-recurringitemsandacquisitioncosts)increasing42%onprioryear.Howden’sretailoperationsperformedextremelywell,presentingcloseto30%EBITDAgrowthcollectively.OurWholesaleandReinsurancepracticehadatougheryearbutstilldeliveredagoodresult,withnewinitiativesperformingexceptionallywellandcontributingstronglytoouroverallgrowth.

Ourpriorityfocusonemergingmarketssawsignificantdevelopmentsinthepasttwelvemonths:

• InNovember2011wecompletedtheacquisitionoffiveoftheAccetteInsuranceGroup’soperations(Singapore,HongKong,Thailand,MalaysiaandthePhilippines)withthesixthjoiningHowdeninJuly2012(Indonesia).Thishas createdanoutstandingplatformforretaildistributionintheextremelyimportantemergingmarketsofSouthEastAsia,complementingouralreadysignificantwholesaleandreinsurancedistributionacrosstheregion.ThebusinessesrebrandedasHowdenandhaveintegratedwell,combininghighqualitylocalexpertisewiththebrokinggroup’sinternationalreach.Togetherweareabletodelivergreaterinnovation,expertiseandservicetoourclients.HowdennowhasexcellentmomentuminAsiaandveryexcitingplansforthefuture.Itisinterestingtonotethatin2012HowdenhasalmostasmanypeopleworkinginouroperationsinAsiaasworkedinthewholeofHyperionwhenwewonourfirstQueen’sAwardin2007.Almost20%ofrevenuenowcomesfromAsiaPacific.

• InSeptember2012HowdenestablisheditsfirstretailoperationinLatinAmericawiththeacquisitionofamajorityshareinConsetSegurosinthefast-growingBrazilianinsurancemarket.Consetisanextremelywell-respectedbrokerspecialisingininsurancesolutionsfortheconstructionindustry.ThebusinessisanimportantstrategicadditiontotheHowdennetwork,complementingbothourreinsurancedistributionacrossLatinAmerica,aswellastheserviceweprovidetoourSpanishretailclientsoperatingacrosstheregion.

Theproportionofbrokingincomegeneratedfromemergingmarketswillcontinuetogrowfastasaresultoftheseimportantacquisitions,futureinitiativesandthestrongorganicgrowthweanticipate.

HOWDENBROKINGGROUP

The Howden pack at the Lloyd’s of London Rugby Sevens

REVENUEBYREGION2012

43%

22% 15%

18%

2726

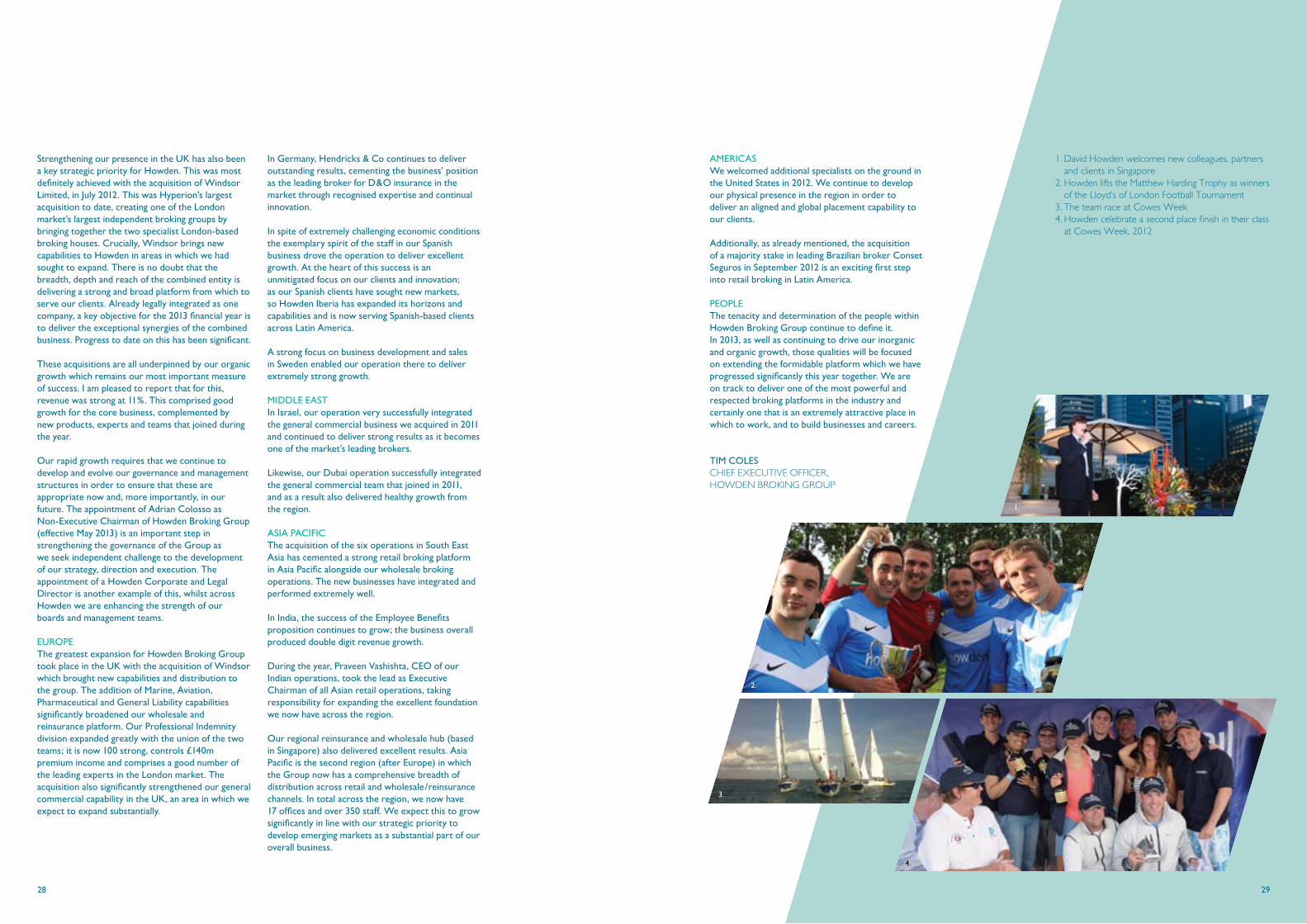

StrengtheningourpresenceintheUKhasalsobeenakeystrategicpriorityforHowden.ThiswasmostdefinitelyachievedwiththeacquisitionofWindsorLimited,inJuly2012.ThiswasHyperion’slargestacquisitiontodate,creatingoneoftheLondonmarket’slargestindependentbrokinggroupsbybringingtogetherthetwospecialistLondon-basedbrokinghouses.Crucially,WindsorbringsnewcapabilitiestoHowdeninareasinwhichwehadsoughttoexpand.Thereisnodoubtthatthebreadth,depthandreachofthecombinedentityisdeliveringastrongandbroadplatformfromwhichtoserveourclients.Alreadylegallyintegratedasonecompany,akeyobjectiveforthe2013financialyearistodelivertheexceptionalsynergiesofthecombinedbusiness.Progresstodateonthishasbeensignificant.

Theseacquisitionsareallunderpinnedbyourorganicgrowthwhichremainsourmostimportantmeasureofsuccess.Iampleasedtoreportthatforthis,revenuewasstrongat11%.Thiscomprisedgoodgrowthforthecorebusiness,complementedby newproducts,expertsandteamsthatjoinedduringtheyear.

Ourrapidgrowthrequiresthatwecontinuetodevelopandevolveourgovernanceandmanagementstructuresinordertoensurethattheseareappropriatenowand,moreimportantly,inourfuture.TheappointmentofAdrianColossoasNon-ExecutiveChairmanofHowdenBrokingGroup(effectiveMay2013)isanimportantstepinstrengtheningthegovernanceoftheGroupas weseekindependentchallengetothedevelopment ofourstrategy,directionandexecution.TheappointmentofaHowdenCorporateandLegalDirectorisanotherexampleofthis,whilstacrossHowdenweareenhancingthestrengthofourboardsandmanagementteams.

EUROPE ThegreatestexpansionforHowdenBrokingGrouptookplaceintheUKwiththeacquisitionofWindsorwhichbroughtnewcapabilitiesanddistributiontothegroup.TheadditionofMarine,Aviation,PharmaceuticalandGeneralLiabilitycapabilitiessignificantlybroadenedourwholesaleandreinsuranceplatform.OurProfessionalIndemnitydivisionexpandedgreatlywiththeunionofthetwoteams;itisnow100strong,controls£140mpremiumincomeandcomprisesagoodnumberoftheleadingexpertsintheLondonmarket.TheacquisitionalsosignificantlystrengthenedourgeneralcommercialcapabilityintheUK,anareainwhichweexpecttoexpandsubstantially.

InGermany,Hendricks&Cocontinuestodeliveroutstandingresults,cementingthebusiness’positionastheleadingbrokerforD&Oinsuranceinthemarketthroughrecognisedexpertiseandcontinualinnovation.

InspiteofextremelychallengingeconomicconditionstheexemplaryspiritofthestaffinourSpanishbusinessdrovetheoperationtodeliverexcellentgrowth.Attheheartofthissuccessisan unmitigatedfocusonourclientsandinnovation; asourSpanishclientshavesoughtnewmarkets, soHowdenIberiahasexpandeditshorizonsandcapabilitiesandisnowservingSpanish-basedclientsacrossLatinAmerica.

Astrongfocusonbusinessdevelopmentandsales inSwedenenabledouroperationtheretodeliverextremelystronggrowth.

mIddlE EAStInIsrael,ouroperationverysuccessfullyintegratedthegeneralcommercialbusinessweacquiredin2011andcontinuedtodeliverstrongresultsasitbecomesoneofthemarket’sleadingbrokers.

Likewise,ourDubaioperationsuccessfullyintegratedthegeneralcommercialteamthatjoinedin2011, andasaresultalsodeliveredhealthygrowthfromtheregion.

ASIAPACIFICTheacquisitionofthesixoperationsinSouthEastAsiahascementedastrongretailbrokingplatform inAsiaPacificalongsideourwholesalebrokingoperations.Thenewbusinesseshaveintegratedandperformedextremelywell.

InIndia,thesuccessoftheEmployeeBenefitspropositioncontinuestogrow;thebusinessoverallproduceddoubledigitrevenuegrowth.

Duringtheyear,PraveenVashishta,CEOofourIndianoperations,tooktheleadasExecutiveChairmanofallAsianretailoperations,takingresponsibilityforexpandingtheexcellentfoundationwenowhaveacrosstheregion.

Ourregionalreinsuranceandwholesalehub(basedinSingapore)alsodeliveredexcellentresults.AsiaPacificisthesecondregion(afterEurope)inwhichtheGroupnowhasacomprehensivebreadthofdistributionacrossretailandwholesale/reinsurancechannels.Intotalacrosstheregion,wenowhave 17officesandover350staff.Weexpectthistogrowsignificantlyinlinewithourstrategicprioritytodevelopemergingmarketsasasubstantialpartofouroverallbusiness.

1. David Howden welcomes new colleagues, partners and clients in Singapore2. Howden lifts the Matthew Harding Trophy as winners of the Lloyd’s of London Football Tournament3. The team race at Cowes Week4. Howden celebrate a second place finish in their class at Cowes Week, 2012

AmERICASWewelcomedadditionalspecialistsonthegroundintheUnitedStatesin2012.Wecontinuetodevelopourphysicalpresenceintheregioninordertodeliveranalignedandglobalplacementcapabilitytoourclients.

Additionally,asalreadymentioned,theacquisition ofamajoritystakeinleadingBrazilianbrokerConsetSegurosinSeptember2012isanexcitingfirststepintoretailbrokinginLatinAmerica.

PEOPlEThetenacityanddeterminationofthepeoplewithinHowdenBrokingGroupcontinuetodefineit. In2013,aswellascontinuingtodriveourinorganicandorganicgrowth,thosequalitieswillbefocusedonextendingtheformidableplatformwhichwehaveprogressedsignificantlythisyeartogether.Weareontracktodeliveroneofthemostpowerfulandrespectedbrokingplatformsintheindustryandcertainlyonethatisanextremelyattractiveplaceinwhichtowork,andtobuildbusinessesandcareers.

tIm COlESCHiEF ExECUTiVE oFFiCER, HoWDEn BRoKinG GRoUP

4.3.

1.

2.

4.

3.

28 29

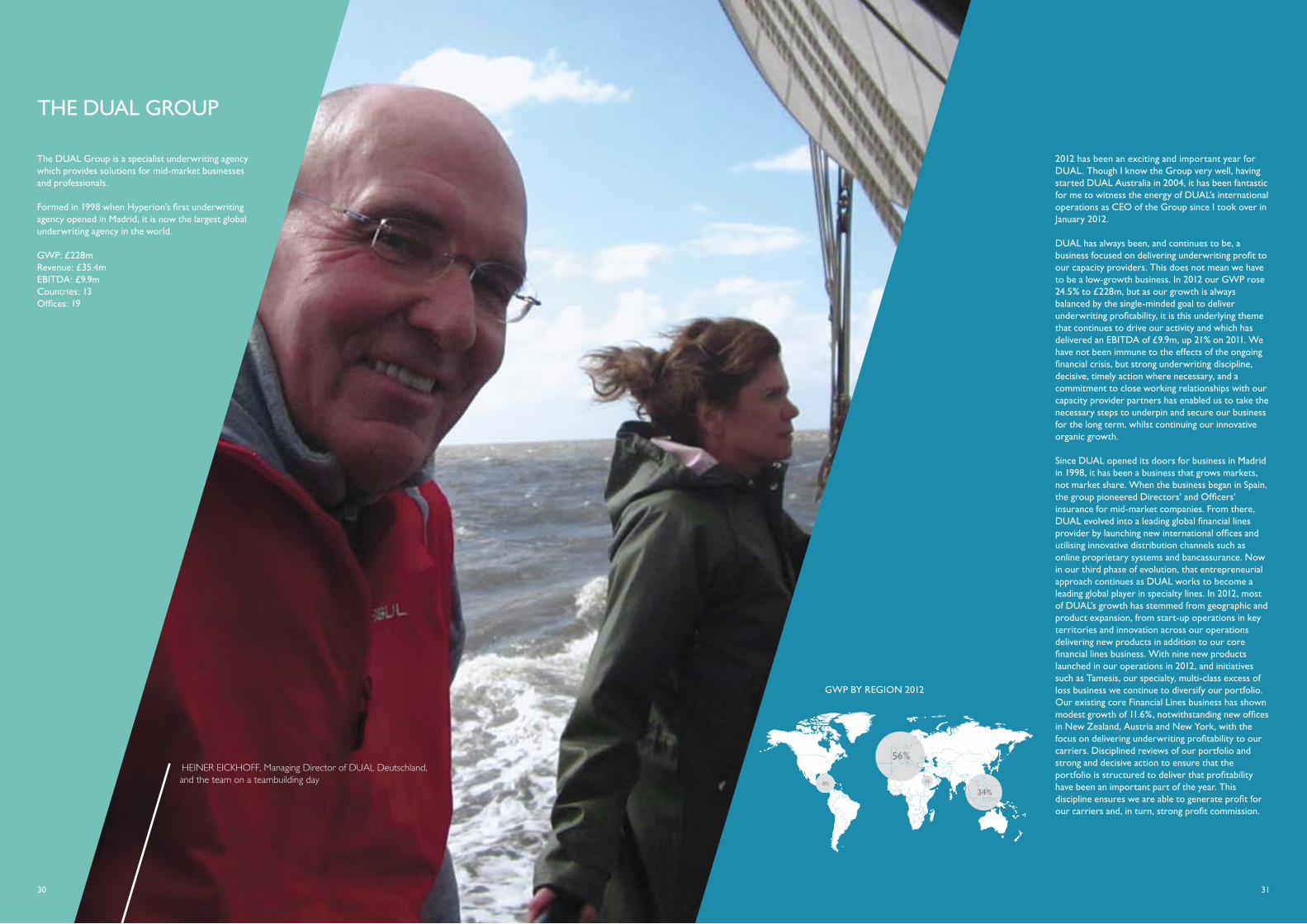

tHE dUAl GROUP

TheDUALGroupisaspecialistunderwritingagencywhichprovidessolutionsformid-marketbusinessesandprofessionals.

Formedin1998whenHyperion’sfirstunderwritingagencyopenedinMadrid,itisnowthelargestglobalunderwritingagencyintheworld.

GWP:£228mRevenue:£35.4mEBITDA:£9.9mCountries:13Offices:19

HEinER EiCKHoFF, Managing Director of DUAL Deutschland, and the team on a teambuilding day

2012hasbeenanexcitingandimportantyearforDUAL.ThoughIknowtheGroupverywell,havingstartedDUALAustraliain2004,ithasbeenfantasticformetowitnesstheenergyofDUAL’sinternationaloperationsasCEOoftheGroupsinceItookoverinJanuary2012.

DUALhasalwaysbeen,andcontinuestobe,abusinessfocusedondeliveringunderwritingprofittoourcapacityproviders.Thisdoesnotmeanwehavetobealow-growthbusiness.In2012ourGWProse24.5%to£228m,butasourgrowthisalwaysbalancedbythesingle-mindedgoaltodeliverunderwritingprofitability,itisthisunderlyingthemethatcontinuestodriveouractivityandwhichhasdeliveredanEBITDAof£9.9m,up21%on2011.Wehavenotbeenimmunetotheeffectsoftheongoingfinancialcrisis,butstrongunderwritingdiscipline,decisive,timelyactionwherenecessary,andacommitmenttocloseworkingrelationshipswithourcapacityproviderpartnershasenabledustotakethenecessarystepstounderpinandsecureourbusinessforthelongterm,whilstcontinuingourinnovativeorganicgrowth.

SinceDUALopeneditsdoorsforbusinessinMadridin1998,ithasbeenabusinessthatgrowsmarkets,notmarketshare.WhenthebusinessbeganinSpain,thegrouppioneeredDirectors’andOfficers’insuranceformid-marketcompanies.Fromthere,DUALevolvedintoaleadingglobalfinanciallinesproviderbylaunchingnewinternationalofficesandutilisinginnovativedistributionchannelssuchasonlineproprietarysystemsandbancassurance.Nowinourthirdphaseofevolution,thatentrepreneurialapproachcontinuesasDUALworkstobecomealeadingglobalplayerinspecialtylines.In2012,mostofDUAL’sgrowthhasstemmedfromgeographicandproductexpansion,fromstart-upoperationsinkeyterritoriesandinnovationacrossouroperationsdeliveringnewproductsinadditiontoourcorefinanciallinesbusiness.Withninenewproductslaunchedinouroperationsin2012,andinitiativessuchasTamesis,ourspecialty,multi-classexcessoflossbusinesswecontinuetodiversifyourportfolio.OurexistingcoreFinancialLinesbusinesshasshownmodestgrowthof11.6%,notwithstandingnewoffices inNewZealand,AustriaandNewYork,withthefocusondeliveringunderwritingprofitabilitytoourcarriers.Disciplinedreviewsofourportfolioandstronganddecisiveactiontoensurethattheportfolioisstructuredtodeliverthatprofitabilityhavebeenanimportantpartoftheyear.Thisdisciplineensuresweareabletogenerateprofitforourcarriersand,inturn,strongprofitcommission.

GWPBYREGION2012

56%

8% 3%

34%

3130

32 33

AttheheartofDUALaretherelationshipswebuildwithourcapacityprovidersandourbrokers.In2012wehaverelationshipswith17capacityprovidersand2,200brokersaroundtheworld,andourresults arebuiltonthestrengthofthoserelationships,oldandnew.

Followingtheappointmentofabroker,wehaverestructuredourcapacityarrangementsinordertoensurewereceiveanincreasedshareoftheunderwritingprofitsofthebusinesswecontrol,andin2012,inadditiontoourlongstandingpartnershipswithArch,HiscoxandMSIGonourFinancialLinesportfolio,wewerepleasedtowelcomeLibertyandBarbicantoaddfurtherstrengthanddepthtoourcapacity.WewerealsodelightedtoextendoursuccessfulrelationshipwithMSIGinAsiaPacificwiththelaunchofDUALinSingaporegivingusaccesstotheexcitingSouthEastAsianmarkets.OurpartnershipwithLibertyintheAmericasisalsoaveryimportantdevelopmentwhichgivesusaccesstothelargestFinancialLinesmarketintheworld.

Theimportanceofourmanyrelationshipswithbrokersandagentshasbeenadriverforourcontinuedinvestmentinthedevelopmentofouronlineproprietarysystemstoensuretheefficienttransactionofmid-marketbusiness.Thevalueofthisinvestmenttothebrokersweworkwithisevidencedbythe30%ofour100,000policieswhicharenowtransactedonline.

Inthesamevein,crucialtoDUAL’smodelandcontinuedprofitablegrowthisthestrengthofourinfrastructure,whichmustbedisciplinedandrobusttoallowouroperationstheflexibilitytogetonwithdeliveringqualityunderwritingandtodelivernewproductswithafasttimetomarket.

AspartofthisprocesswehavefurtherstrengthenedourunderwritingoversightfunctionwiththerecruitmentofaDeputyCEOwhohastheresponsibilitytocontinuetoimproveunderwritingprofitabilityacrosstheGroup.TheappointmentofaChiefActuarywillalsosupportthedeliveryofthisgoalinthe2013financialyear.

EUROPEOurEuropeanoperationshavehadastrongyearinthefaceofthesoftmarketandfinancialcrisis.Theyhavedonethisthroughacombinationofdisciplinedportfoliomanagementandinnovation,withseveralimportantnewinitiativesmakingasignificantcontribution.

InItaly,strongprofitablegrowthhasbeendrivenbycontinuedinnovationinproductsanddistribution. ApartnershipwiththeItalianPostOffice’sinsurancearmtodistributefinanciallinesproductsthroughitsbranchnetworkwasaparticularhighlightandanotherexample,followinglastyear’sground-breakingdealwithoneofthecountry’sleadingbankinggroups,ofourabilitytoprovideourcarrierswithaccesstonewmarkets.Additionally,thecreationandlaunchofanonlinePublicOfficials’LiabilityInsurancesolutionhasbeenanimportantareaofdevelopmentcontributingtoefficientgrowth.

InSpain,despiteconsiderableeconomicpressures,strongmanagementdecisionsontheportfoliohaveresultedinagoodyearfortheSpanishoperationandleavethebusinesswellpositionedtobuildonitssolidfoundation.

OuroperationinGermanyextendeditsreachbyopeningabranchinVienna,Austria,tobuildonthebusinessitalreadyhasintheregion.Thisinitiativehasbeenextremelywellreceivedbyourbrokerpartnersandisalreadybeginningtodeliverstrongresults.Newproductshavealsohelpedcontribute toanexcellentyearforDUALinGermany.

TheUKbusinesseshavealsohadanexcitingyear. ThelaunchofTamesisDUALsawtheintroductionof auniqueunderwritingagencytotheLondonmarket. Aspecialtyexcessoflossbusinesswritingamixedandflexibleportfolioofshort-tailbusiness,Tamesishasgivenusaccesstoanewareaofthemarket.TappingintothestrengthoftheDUALinfrastructurethebusinesshasbeenfast-to-market,andcelebrateditsfirstbirthdayinNovember2012.NewproductlauncheswithintheexistingLondonbusinesshavebeencomplementedbytheadditionofawell-knownspecialistGeneralLiabilityteamjustaftertheendofthefinancialyear.Thislaunchcombinesmarket-leadingexpertisewiththeglobaldistributionnetworkofDUAL,andwillbeofgreatbenefittoboththeLondonandinternationaloperationsasitbeginstowriteUKandinternationalbusiness.

ASIAPACIFICAsiaPacificcontinuestobeagrowthengine.WhenHyperionwonitsfirstQueen’sAwardin2007theregionaccountedfor15%ofourGWP;now,in2012,theregioncontributes34%.

InAustralia,theoldestofourAsiaPacificoperations,innovationcontinuesapacewithnewCyber,CrimeandStandaloneStatutoryLiabilityproductslaunchedduringtheyear.Theworkputinoverthelast18monthstoourAccidentandHealthpropositionisalsobeginningtobearfruit,withsignificantgrowthintheproductcontribution.Amajormilestonewasrecentlypassedwhenthe15,000thpolicywasboundonlinethroughourproprietarysystem,keepingusattheforefrontoftechnologicaldevelopmentsinlinewithourbrokerpartners’needs.

OurNewZealandoperationcelebrateditsfirstbirthdayinMarchafterhittingthegroundrunningin2011.ThebusinesshasgivenusaccesstotheprofitableNewZealandGeneralLiabilitymarketandhasperformedstronglyin2012.

ThesuccessofourpartnershipwithMSIGinourHongKongoperationhasseentheteamextendthepropositionthroughthelaunchofanewDUALoperationinSingapore,andthedevelopmentofbothbusinessesisnowamajorfocus.

AmERICASTherestructuringandalignmentofHyperion’sunderwritingoperationsinNorthandLatinAmericaunderasinglebrand,DUAL,wasamajordevelopment in2012.BringingtheformerVKUnderwritersandHSUbusinessestogetherhascreatedastrongfoundation,andcombinedwithourglobalpartnershipwithLibertyInternational,DUALformsanexcitingplatformfromwhichwecanentertheworld’sbiggestfinanciallinesmarket.Additionally,theopeningofanewoperationinNewYorkfurtherextendsourfootprintintheregionandgivesusapresenceinthisimportantglobalinsurancehub.

PEOPlEThefinalwordmustgotothepeoplewhohavebuiltDUAL.In2007therewere95ofus.Today190peopleareresponsiblefortheseexcellentresultsfromoperationsaroundtheworld.TheircontributionhasbeenrecognisednotonlyinDUAL’scontributiontoHyperion’sQueen’sAward,butalsowhenDUALwasnamedUnderwritingAgencyoftheYearattheBritishInsuranceAwards.

Werecruitspecialistunderwritersandspecialistoperationsexperts.Ourinfrastructureisstrongandenablesourinternationaloperationstokeepdeliveringinnovativesolutionsandgrowingmarketswhilstprovidingqualityinformationtoourcapacityproviders.Thestrengthofourpartnershipsbeginswiththestrengthofourpeople,andIamincrediblyproudofthemall.

dAmIEN COAtES CHiEF ExECUTiVE oFFiCER, DUAL inTERnATionAL

1. PAUL FERRiS, DUAL’S Chief Underwriting officer, collects the British insurance Award for Underwriting Agency of the year

2. The DUAL new Zealand team line up for the Rangitoto half marathon3. DAMiEn CoATES, CEo of DUAL international, and LUiS MUÑoZ-RoJAS,

Executive Director, Hyperion, at the top of Almanzor in Spain

1.

2. 3.

INtROdUCtIONCorporateSocialResponsibilityisoftheutmostimportancetoHyperion.WeunderstandthatitpositivelyaffectsourGroup,ouremployeesandthelocalcommunity.HyperionthereforestrivestofulfilallaspectsofitsCSRPolicy,aswellascontinuallyreviewingitandsettingtargetsforfutureimprovements.ThePolicyissetoutinasimplestructureundertheheadings:Environment,CommunityandCharity,Welfare,Employees,andSuppliersandCustomers.ThisapproachmakesthePolicyaccessibletoallofouremployeesandcustomers,allowingboththesuccessfulapplicationofthePolicy,aswellascriticalassessmentandfeedbackfromourcustomersandinvestors.

ENvIRONmENtHyperioniscommittedtoreducinganynegativeimpactsontheenvironmentitmayproducewhereverpossible.Asacompanyweexpectinvolvementandenvironmentalresponsibilityfromallofouremployees,andencourageourassociatesandsupplierstostrivetowardshighenvironmentalstandardsalso.

CORPORATESOCIALRESPONSIBILITYPOLICY

Ourenvironmentalcommitments:

• Recycling paper and other waste materials. –Paperandmixedrecyclingbinsareprovidedin ouroffices,andweactivelyencourage employeestoreducewasteandrecycle wheneverpossible. –Thecompanyalsorecyclesbatteriesandink andtonercartridges.

• To use environmentally responsible materials and sources. – SourcingFSCandrecycledpaperforuseinall ofourprinters.

• To increase energy efficiency. –Usingenergyefficientlightingwhereverpossible, includingmotionsensorlightsinourLondon officeswhichswitchoffautomaticallywhenthey arenotneeded. –Runninga‘SwitchOff’campaign;encouraging employeestoturnofftheircomputersand otherelectricalequipmentwhenitisnotinuse.

• To reduce our carbon footprint. –Reducingtravelwherepossiblebyusing teleconferencing. –Providingbikeshedsforouremployeesatour Londonoffices.

• To reduce wastefulness. – Encouragingduplexprintingstandardisedto reducepaperuse.

–Reducingprintingwhereverpossible: encouragingemployeesnottoprintemails.

–Donatingoldequipmentandfurnituretocharity wherepossible,orrecyclingitifnot.

– FollowingtheHeadOfficemoveto 16Eastcheapduringthe2011/12financialyear, anysurplusfurnitureatBevisMarksHousewas donatedtocharityviaClearEnvironment.

COmmUNItY ANd CHARItYHyperion’sCharityCommitteeensuresthatthecompanyhasapositiveinfluenceinthelocalcommunitieswhereitsdifferentdivisionsarebased.Thisisbasedonanawarenessofthelocalculture,whichallowsthecompanytorespectthelocalcommunityandgivebacktoitinapositiveandappropriatemanner.

Hyperionalsostrivestohaveapositivesocialinfluenceonawiderscalebyactivelyencouragingcharitablecommitmentsfromemployees,andacrossitsvariousdivisionsworldwide.Ratherthanselectacharityforthecompanytocommittoasawhole,Hyperionpreferstoencourageitsemployeestosupportcharitiesthattheyarepassionateabout,inordertomaximisetheinvolvementofallstaffandincreasethediversityofcharityandcommunityworkundertaken.

Ourcommitmentsandachievements:

• Runninga‘Give-As-You-Earn’schemeforemployees.

• Operating‘MatchFundraising’(upto£250)foremployees.

• Hyperion’s‘InvestingintheCommunityAward’.Employeescanpitchideasforcommunityprojectsthattheywouldliketorun,andthetoptwowillbeselectedandawarded£5,000eachtoputtowardstheirprojects.

• HyperionisinvolvedintheLloyd’sofLondonCommunityProgramme.

INvEStING IN tHE COmmUNItYHyperion’sInvestingintheCommunityAwardwaslaunchedinJuly2012andallsubmissionswerejudgedbytheGroupManagementTeam(“GMT”)atthebeginningofSeptember2012.SummaryofAward:Tosupportthosewhoarepassionateaboutlocalcauses,twoawardsof£5,000werecreatedtobegiventotwoprojectsthatclearlymakeapositivecontributiontotheirlocalcommunity,enhancingandimprovingthequalityoflivesofthosewholivethere.TheCharityCommitteemetduringAugust2012toreviewthesubmissionsforthisawardandmadethefollowingrecommendationswhichwereapprovedbytheGMT:

2012WINNERS:

• PHIl dAvIS, Vimba, Dewe Project – Zimbabwe AcharitywhichregeneratesrundownschoolsinZimbabwe,Africa.TheawardwillallowthecharitytoinstallasolarwaterpumpinoneoftheirschoolsnorthofHararetoensurethechildrenhaveclean,safedrinkingwater,whichinturnwillalsoallowthemtolearnhowtogrowgrainandvegetables.

• MATTBAKER, Projekt Nepal e.v – Nepal ApartnershipbetweentwoschoolsinGermanyandNepal.TheawardwillallowtheteamtocompletetheconstructionoftwonewclassroomsatJanaSudharLowerSecondarySchoolinNepal;aschoolforchildrenfromlowincomefamilies.

Submissionswerejudgedontheircontributiontothelocalcommunityandthelevelofsupportalreadyshownbythememberofstafffortheinitiative.

MATT BAKER, Associate Director, Howden (UK), visits Jana Sudhar Lower Secondary School in nepal

3534

WELFAREHyperioncomplieswiththeEqualityAct2010intheUKandwithequivalentlegislationinothercountriesinordertoprovideacommonstandardforallofitsemployees.Webelieveinequalopportunitiesforall,regardlessofrace,religion,gender,ageordisability.OurPolicyisdesignedtoensurethateveryoneisgiventhesameconsiderationwhentheyapplyforjobs,andthattheyenjoythesametraining,careerdevelopmentandprospects.

Hyperionaimstoprovideasupportiveandwelcomingworkplaceenvironment,andhasinplacetheHyperionFamilyFriendlyProposition,whichoutlinesproceduresformaternity,paternityandadoptionleaveinordertomaximiseouremployees’possibilitiesforincorporatingfamilyandwork,andalsodetailsholiday,annualleaveandleaveintheeventofemergencysituations.

Intheeventofsicknessorincapacity,Hyperionhasinplacedetailedproceduresastopaidleaveandhealthserviceprovisions,takingintospecialconsiderationthosewhomaybeaffectedbymediumtolongtermleave,andaimingtoaccommodatetoneedswhereverpossible,incompliancewiththeDisabilityDiscriminationAct.Hyperionalsoofferssupportforitsemployeesthroughtheprovisionofacounsellingservicewhereitisthoughttobeappropriate.

Wearecommittedtomaintainingthehigheststandardofintegrity,opennessandaccountabilityinouroperations.WehaveproceduresinplacetoensurecompliancewiththeBriberyAct2010,andhaveinplaceaWhistleblowingPolicywhichsetsoutspecificproceduresforemployeestoundertakeinordertoreportconcerns.HyperionalsooperatesDisciplinaryandGrievanceprocedures.

HyperionalsocomplieswiththeHealthandSafetyatWorkAct1974intheUK,andrunsriskassessmentproceduresinordertomaximisesafetyandsecurityforouremployees.ThisincludesrunningDSEassessmentsforallofouremployeesbasedinofficeenvironments.

EmPlOYEESTheBoardrecognisesthatHyperion’scontinuingsuccessdependsonitsemployeesanditsabilitytocreatepolicieswhichattract,motivateandretainemployeesofthehighestcalibre.BasedontheseprinciplesHyperionensuresthatthereisregularcommunicationwithemployeesabouttheprogressofthecompany;holdingregularmeetings,sendingoutregularnewslettersandprovidingagroupintranetforemployees.

Hyperionoperatespayandrewardpolicieswhichcommittofairandequitablestrategiesfortheremunerationofitsemployees,andindoingsotakefullaccountofmarkettrends.Payandrewardsareregularlybenchmarkedtoensurethattheyarecontinuallyimprovinginlinewithresults.Weuseatotalrewardsapproachwhichprovidesamixtureoffinancialandnon-financialrewards,andbenefitsandincentivesvaryinaccordancewithlocalcultureandpractice.

Hyperionbelievesininvestinginouremployeesinordertocontinuallyimproveourstandardsandtomaintainourcompetitiveadvantageandprofessionalism.Wethereforenotonlyofferfullsupporttoemployeeswhowishtoundergotraining,butactivelyencourageitamongstourstaff.OurFutureLeadersProgrammeisaimedatidentifyingthosewiththepotentialtobefutureleaderswithinHyperion,andtoprovidethemwithappropriatetrainingtodevelopandenhancetheirexistingskills. SUPPlIERS ANd CUStOmERSBeingcommittedtohighstandardsacrossthewholeofitsoperations,Hyperiontakescarefulconsiderationoveritssuppliers.ThereareProcurementPoliciesandTermsofBusinessAgreementsinplace,whicharereviewedinordertoensurethatoursuppliersmeettherequirementsexpected.

ThecorevaluesofHyperionInsuranceGroupcompanieshaveclientfocusattheircentre,andtheGroup’sbusinessprocessesandproceduresaredevelopedandrefinedinlinewithfeedbackinordertoensurewearealwaysdeliveringthehighestqualityservicepossible.

1. 2.

3.

1. / 2. PHiL DAViS taking part in the Marathon des Sables in support of Vimba

3. The Howden team line up for the Great City Race in London

3736

RISKMANAGEMENT

RisksrelatingtoHyperion’sbusinesscouldaffectitadverselybycausingfinancialresultstobemateriallydifferentoroperationaloutcomestobeoutoflinewithmanagement’sexpectations.UnderHyperion’sriskmanagementframework,risksareidentified,managedandreportedeitherlocallyoronagroupbasis.Wherenewrisksareencountered,theyareassessedagainstcriteriaapprovedbytheBoardtocoverthepotentialimpactoftheriskandthelikelihoodofitsoccurrence.Theriskwillbeconsideredforitseffectonstrategy,operations,financesorreputationandwhethertheyareexternalorinternal.

Allrisksareassignedanownerwhohasresponsibilityforensuringthattheriskismanagedandmonitoredovertime.Ownershipforcontrolactivitiesandactionsshouldalsobeassignedtoclarifyresponsibilitiesandaccountabilities.Riskmonitoringandreportingapplicationsexisttoensurerisklevelsaremaintainedwithinstatedriskappetitesandtolerancelevels,toevaluatetheriskadjustedperformanceoftheCompanyanditsbusinessunitsandtoprovidedecisionsupportinformationforvariousriskmanagementdecisions.

Thefollowingisalistofthemainrisks withcommentontheirmitigation:

FINANcIAL RIsks

THESIZEOFOURDEBTAt30thSeptember2011,wehadcurrentandnon-currentborrowingsof£25.8m.Duringtheyearto30thSeptember2012,thisamountroseto£81.0mpartlyasaresultofenteringintofurtherdebttofinancethecashportionoftheconsiderationtoacquireWindsorandtorefinanceexistingGroupdebt.WeagreedfinancialandothercovenantsinconnectionwiththefacilityenteredintoinJuly2012.Thehigherlevelofdebtandgearingthatresultswillleadtoincreasedinterestcharges,andcovenantrequirementsmayrestrictourabilitytoobtainotherfundingtofundmatterssuchasadditionalacquisitions,capitalexpendituresandgeneralrequirementsforworkingcapital.Thisinturnmayreducetheavailabilityofcashfordividendstoshareholdersandcorporatepurposes.

OURABILITYTOMAKEINTEREST ANd CAPItAl PAYmENtS Ourabilitytopayinterestandcapitalpaymentsandrefinanceourexistingdebtdependsoncashflowgeneratedfromoperations.Generationofcashflowdependsongeneralfinancial,economic,competitiveandregulatoryfactorsthatarebeyondthecontrolofHyperionmanagement.Ifcashflowisinadequatetoservicethedebtthenwemayneedtoreduceacqui- sitionactivityorcapitalexpenditure.Thismayinturnrestrictourabilitytorefinancethedebtatmaturity.

Notwithstandingthefinancialinstrumentsthatwehavetoprotectusfromcertainchangesininterestrates,anincreaseininterestratesmayaffectourfinancialresultsandreducethevalueofcashbalances.

OURHOLDINGOFFOREIGNExCHANGECURRENCY WeconductalargeproportionofourbusinessincurrenciesotherthanSterlingwhichouraccountsarereportedin.Ourresultsandcashflowsarethereforeexposedtomovementsinforeigncurrencyexchangerates.OurmainexposuresaretoUSDollar,Euro,AustralianDollarandCanadianDollar.IntheUK,partofourrevenueisinforeigncurrencies;howeverourexpensesareborneinSterling.Wemitigatetheriskbybuyingfinancialinstrumentstohelpprotectagainstexposuresthatwecanpredictwithreasonableaccuracy.Asaprofitablebusiness,however,astrongpoundagainstremainingforeigncurrencyexposuresproducesalowerprofitinourconsolidatedaccounts.

RECEIPTOFFOREIGNCURRENCYDIVIDENDSAsaholdingcompanywithUKandoverseassubsidiaries,wemaynotbeabletoreceivedividendsinsufficientamountstomeetthegroup’scashflowrequirements.UKsubsidiariesmayhaveregulatoryrequirementsforholdingofcapitaltomeetrequirementsformaintainingadequatefinancialresources.Overseassubsidiariesmayhavesimilarrequirements,orlocalfundingrequirementsthatmaypreventthemfrompayingdividends.Inthesecases,ourrequirementforfuturecashmayincrease.

OUR ACCOUNtING ASSUmPtIONS ANd EStImAtESWeprepareourfinancialstatementsinaccordancewithInternationalFinancialReportingStandards(IFRS).Wearerequiredtomakeassumptionsandjudgmentalestimatesthataffectthereportedamountsofassetsandliabilitiesandthedisclosureofcontingentassetsandliabilitiesatthedateofourfinancialstatements.Wereviewtheseassumptionsandjudgmentalestimatesincludingthoserelatedtocarryingvalueofgoodwillinacquiredentities,revenuerecognition,derivativeliabilities,contingentliabilitiesandtaxation.Althoughwemakeassumptionsthatwebelievearerealistic,actualresultscoulddifferfromestimatesandthiscouldaffecttheGroup’sfinancialresults.

INsURANce RIsks

OURCOMPETITIVEPLACEINTHEMARKETTheinsurancemarketisintenselycompetitive.Wecompetewithglobalandlocalbrokersandinsurancecompaniesanddependontheprovisionofgoodservice,competitivepricingandsuperiorproductfeatures.Ourcompetitionmayhavealongertermrelationshipwiththeirclientsthanwehaveandgreaterfinancialandtechnicalresources.Theymayalsohavealargerbrandingandstrongerinternationalofficenetwork,bettercostmarginsandasuperiorrangeofservicesandofferlowerpricesforinsurancecoverage.Lowerpremiumratesmayinturnadverselyaffectouroperatingincomeandprofitmargin.Ourbusinessstrategyhelpsustomitigatethisrisk.

ECONOMICFACTORSAFFECTING OURBUSINESSAseconomicactivityincreasesandreduces,thedemandforinsurancecoveragegenerallyrisesandfalls.Thesechangesaffectbrokerageandcommissionsearnedbyus.Examplesofmeasurementofeconomicactivityarebusinesses’turnover,balancesheetvaluesandnumberofpeopleemployed.Companiesbecominginsolventandceasingtradingmayresultinlossofclients.Insolvenciesintheinsuranceindustrymayrestrictourabilitytoplacebusiness.Reducedactivitymayalsocauseareductioninclients’appetiteforbuyinginsuranceprotectionwhereitisadiscretionaryspend.Inturn,reduceddemandmaycausepricestoreducethroughcompetition,whichcanbecyclicalovertime.Althoughourbusinessstrategyhelpsustomitigatethisrisk,itislargelyoutsideourcontrol.

OURINTEGRATIONWITHACQUIREDCOmPANIES FollowingtheacquisitionsofbothAccettein2011andWindsorin2012,weundertookanintegrationplantoobtainbusinesssynergiesandcostbenefitsfromtheseacquisitions.Theanticipatedbenefitsoftheseacquisitionsdependonhowsuccessfulweareincompletingtheintegrationplaneffectively.Significantmanagementtimehasbeenspentontheintegrationofoperationstorealisethebenefitsbutavoidanydisruptiontothebusinessoftheintegratedcompanies.

TheresultoftheWindsoracquisitionisasignificantlylargerbaseintheUKwhichdemandsmoremanagementtime.Itisimportanttomaintainstaffmoraleandretentionratesatalllevelswhilstintegratingthecultures.Theassumptionsmadeaboutclientretentionandnewbusinessmayprovetobeincorrect.Thetaskofmaintainingexistingsystemsandseekingasuitablebusinesssystemforfutureuse,avoidingduplication,willabsorbfurthermanagementresource.Wealsohavetoco-ordinatetheseparatelocationsforthebusinessandoptimisespaceplanningandtechnologyusebetweentheselocations.Whilstmanagementtimeisspentinreducingtherisksofprojectfailure,theremaybeunforeseenfactorsthatcauseadditionalexpenseordelayinintegrationandsomeofthesemaybeoutsideourcontrol.

Inthelongertermwemaynotbeabletoachievetheincreaseintheprofitmarginsweseekbyincreasingoperatingincomeandcontrollingcostlevelseffectivelywhilstmeetingourclients’servicerequirements.

3938

41

LeGAL AND ReGULAToRy RIsks

Wemaybesubjecttolegalandregulatoryissuesthat,onceconcluded,mayaffectourfinancialresultsadversely.Wemayreceiveclaimsinrelationtoerrorsandomissions(‘E&O’)inplacingorunderwritinginsuranceordealingwithclaims.ItisnotalwayspossibletopreventerrorsandomissionsoccurringanddamagesunderE&Oclaimsmaycauseourfinancialpositiontobeadverselyaffected,aswellasdivertingmanagementtimeandcausingreputationaldamage.Wepurchaseinsurancetocovertheseclaimsandithasnotbeenmateriallydepleted.Lawsuitsmayarisefromcorporateactionsthataredisputedbythirdparties.

Weaccruefortheseexposurestotheextentthatlossesareprobableandcanbereasonablyestimated.TheseaccrualsareadjustedovertimeaccordingtodevelopmentsanddetailsoflegalissuesarecontainedinthenotestotheConsolidatedFinancialStatements.

Ourbusinessissubjecttoahighdegreeofregulationfromgovernmentsortheiragenciesandthismaylimitourgrowthorharmourfinancialresults.Thecostofcomplianceincreaseswiththequantityandtypesofinsuranceproductsthatweplaceforclientsorunderwrite.Alsoasweexpand,wearerequiredtoobtainlicencesincountriesinwhichwetradeandcountriesthathavemorestrictregulatoryregimesneedtohavemoreresourcededicatedtocompliancematters.Inconnectionwithunderwriting,wemayhavetocomplywithregulationsaffectingtheinsurersforwhichweactascoverholders.

Innovationsinregulatingourindustrythatcouldhaveanimpactonourfinancialresultsincludeadditionalregulations,suchastheFSA’sproposedchangesinclientmoneyruleswhichwillrequiremorefinancestaffresourcetoimplementandfurtherexpansionofdirectsellingofinsurancebyinsurancecompanies.

oUR oPeRATIoNs

Werelyonhighlytrainedandexperiencedstafftoundertakebrokingandunderwritingbusiness.Thebusinessismanagedbydirectorswhohavemanyyearsofexperienceandexpertise.Lossofpersonnelcouldhaveadisruptiveimpactonourabilitytomanageourbusinesseffectivelyandtofulfilourstrategyandplans.Weareinahighlycompetitivemarketfortalentandneedtoretainstaffoncerecruited.Anylossofkeystaffcouldthereforeadverselyaffectouroperatingresultsandprofitability.Theadequacyofemploymentcontracts,effectivenessofourappraisalandtrainingprogrammeandcompletenessofsuccessionplansarereviewedregularly.

Ourinformationtechnologysystemsareakeypartofourbusinessandanydisruptionofsystemsorthesupportinginfrastructureandnetworkscouldadverselyaffectouroperations,incomeandfinancialresults.Inparticular,wearecarefulthatanychangesinthesystemsforrecordinginsurancetransactionsareplannedandtestedthoroughlytoaddresstheriskofoverrunsoftimeorcost.Wealsotakespecificmeasurestoensurethatsecurityofpersonaldataismaintained.

Asnotedaboveourglobaloperationsaresubjecttoeconomic,financial,regulatory,legalandmarketrisksasnotedabove.OverseasofficesmayexperiencetheserisksmoreseverelythantheUK,forinstancebylackingthestafftobuildthebusinessinacompetitivemarket.Subsidiariesmaybesubjecttopoorereconomicconditionsleadingtoaworsecreditcontrolenvironment,inflationoflocalcostsorlocalcurrencyfluctuations.Also,overseasregulatoryandtaxationprovisionscouldresultinrestrictionstoourtrading,additionaltaxburdenandlimitationsontheamountofdividendsthatcanbepaidtotheparentcompany.

Aswellasnaturalandman-madedisasterscausingvolatilityinfinancialmarketsanddisruptingtheinsurancemarketsinwhichwetrade,theymayaffectouroperationsdespitelocalbusinesscontinuity anddisasterrecoveryplanning,causingfurtherfinancialloss.

Wedependonouroperationstoensureclientsatisfactionandifweareunabletooperate,thelossofclientsatisfactioncouldresultinharmtoourbusinessandfinancialresults.Inparticular,akeypartofoperationsisthehandlingofclientmoneyandensuringthatitistreatedproperlyandinaccordancewithregulations.

Inacquiringordisposingofbusinesses,weneedtoidentifysuitableopportunitiesforacquisitionandnegotiatefavourabletermsandcompletetransactions.Werelyonourduediligenceprocesstounderstandthenatureofallliabilities,bothrealandcontingentthatthetargetcompanyissubjectto.However,toenableeffectiveintegrationwithacquiredcompanies,weneedtorealisethefullbusinessbenefitsasnotedabove,orotherwisethefullfinancialbenefitwillnotoccur.Inturn,thisreliesonsatisfactorygrowthandprofitableoperationsofthecompaniesweacquire.

Wemayalsorelyonthirdpartiestoprovideoutsourcedservices.Thisincludespaymentserviceswithbanks,payroll,archivingandLondonInsuranceMarketprocessing,andfailureofthesethirdpartiesdespiteourduediligencepriortoemployingthemcouldresultinfinanciallossorregulatorypenaltiesanddamageourbusinessanditsreputation.

40

Steering the Howden boat at Cowes Week GARETH ABBoTT, Account Executive,

Howden insurance Brokers (UK)

FINANCIALSTATEMENTS

42 43

44 45

Directors’ rePort

GrouP Directors’ rePort for the year enDeD 30 sePtember 2012

The Directors submit their report and audited financial statements for Hyperion Insurance Group Limited (“the Company”) together with the consolidated financial statements of the Group for the year ended 30 September 2012.

Principal activitiesThe principal activity of the Company during the year was that of a holding and investment company for a group of insurance intermediaries. The Group’s trading operations comprise wholesale and retail insurance broking, reinsurance broking and underwriting agencies.

review of business

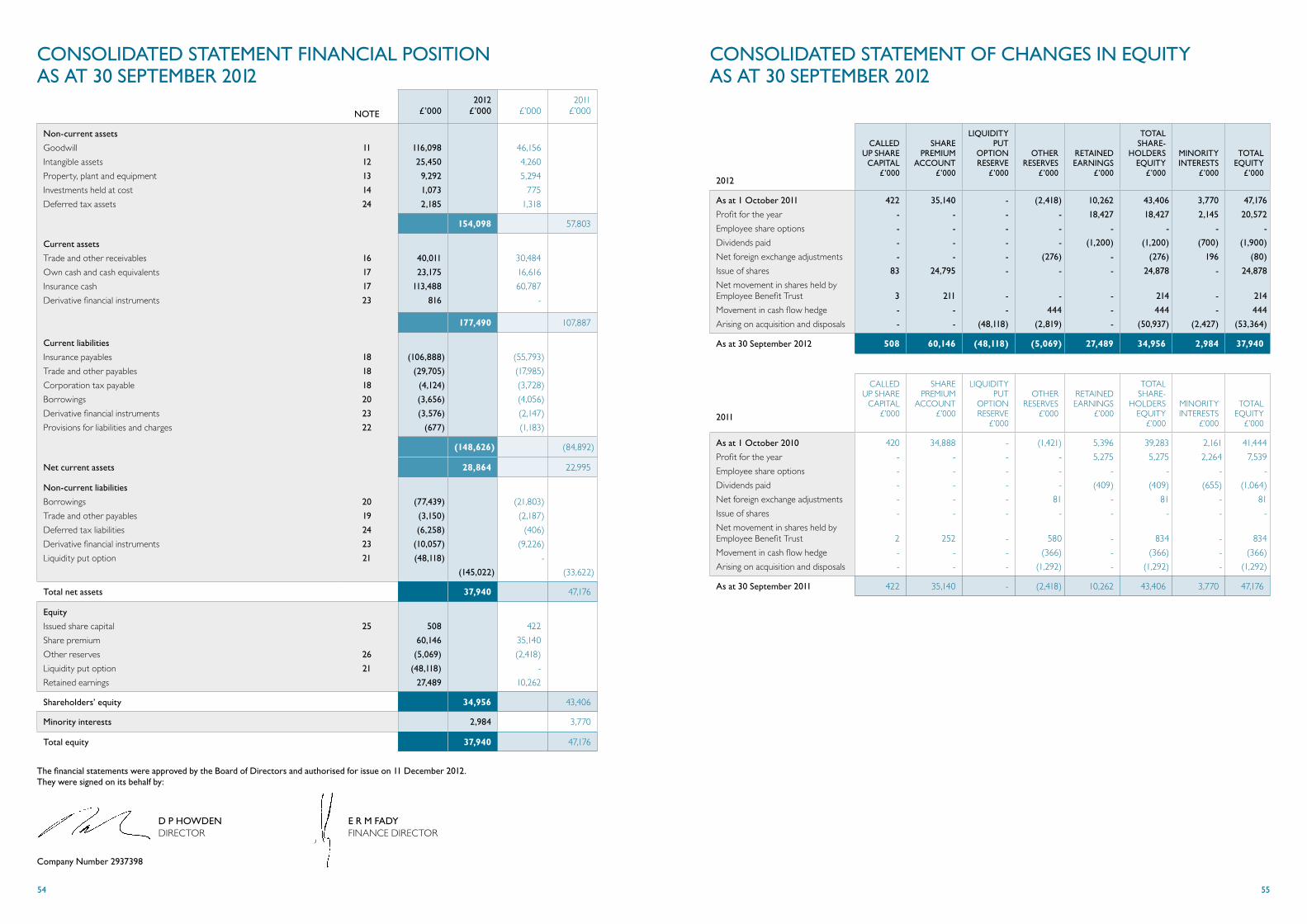

Financial reviewThe Group’s financial statements include a consolidated income statement, consolidated statement of comprehensive income, consolidated statement of financial position and consolidated cash flow statement for the year ended 30 September 2012, together with comparative figures for the year ended 30 September 2011.

The Group has adopted International Financial Reporting Standards (“IFRS”) as the basis of preparation of its consolidated accounts. The statutory accounts of individual companies within the Group continue to be prepared in accordance with local accounting standards and in this regard the balance sheet for the parent company, Hyperion Insurance Group Limited, has been prepared in accordance with UK Generally Accepted Accounting Principles (“UK GAAP”).

The consolidated income statement has been prepared in accordance with IFRS. The segmental analysis of the Group identifies the approach adopted by the Group in assessing its financial performance and the following comments are probably more easily interpreted by reference to note 3.

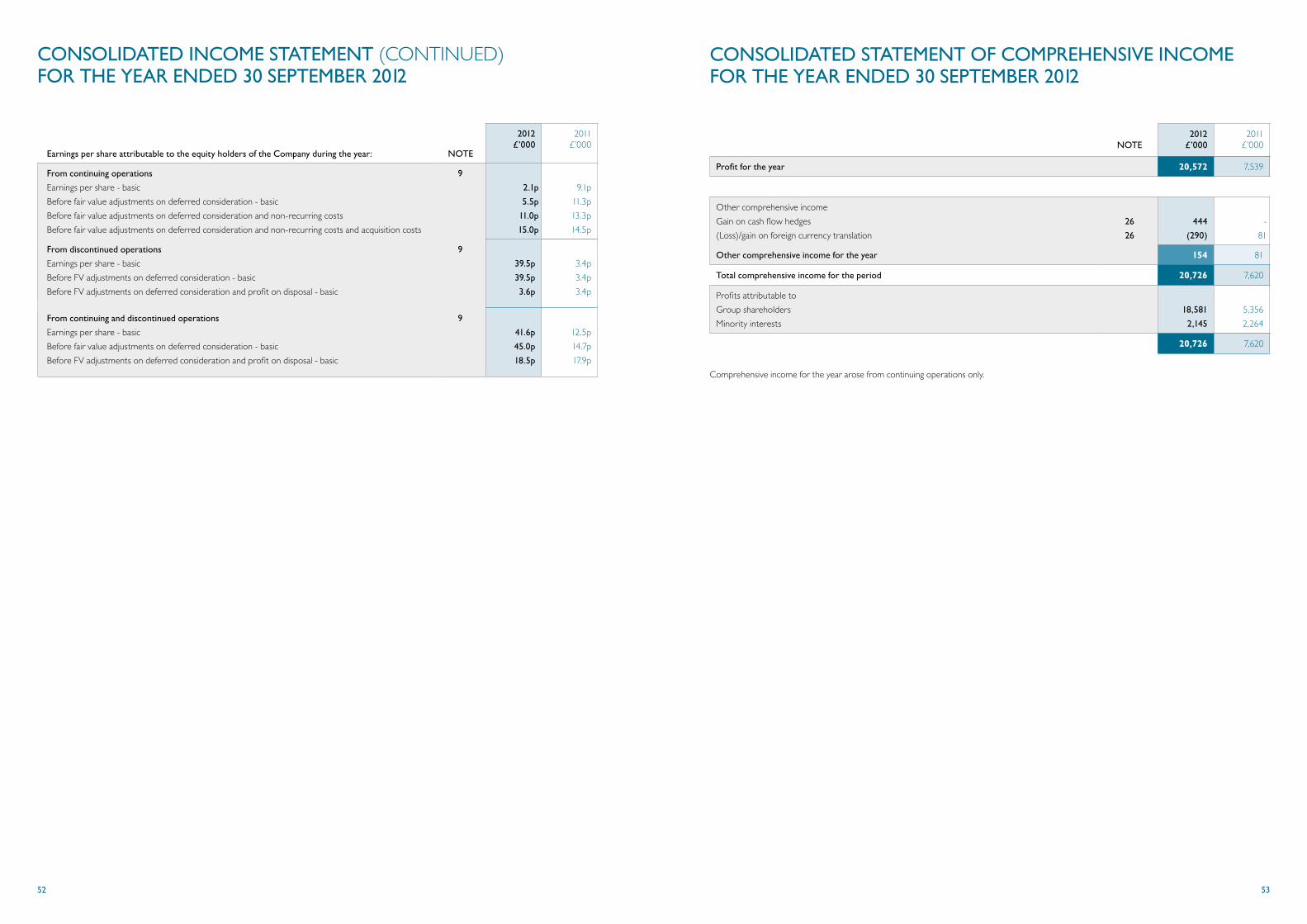

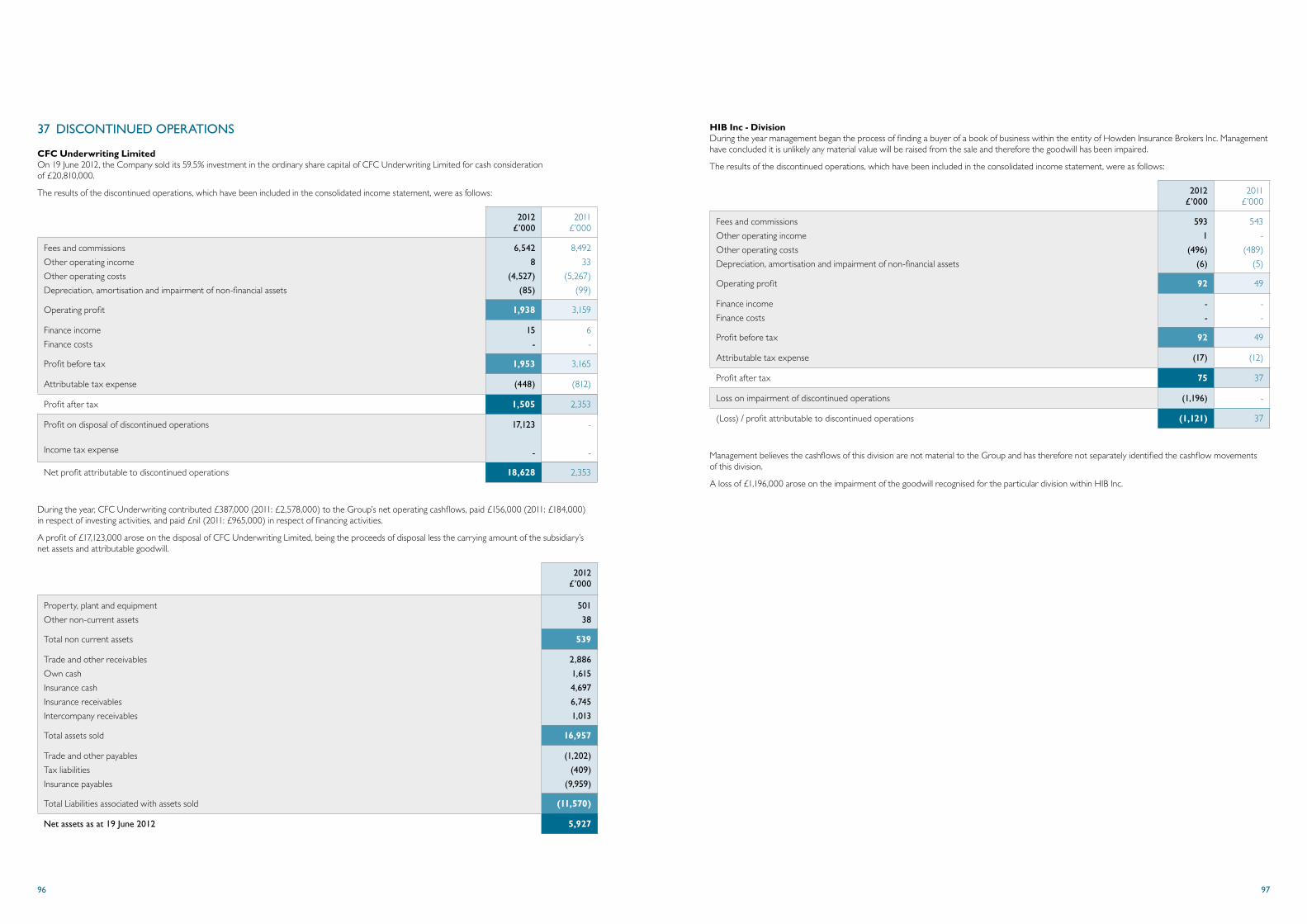

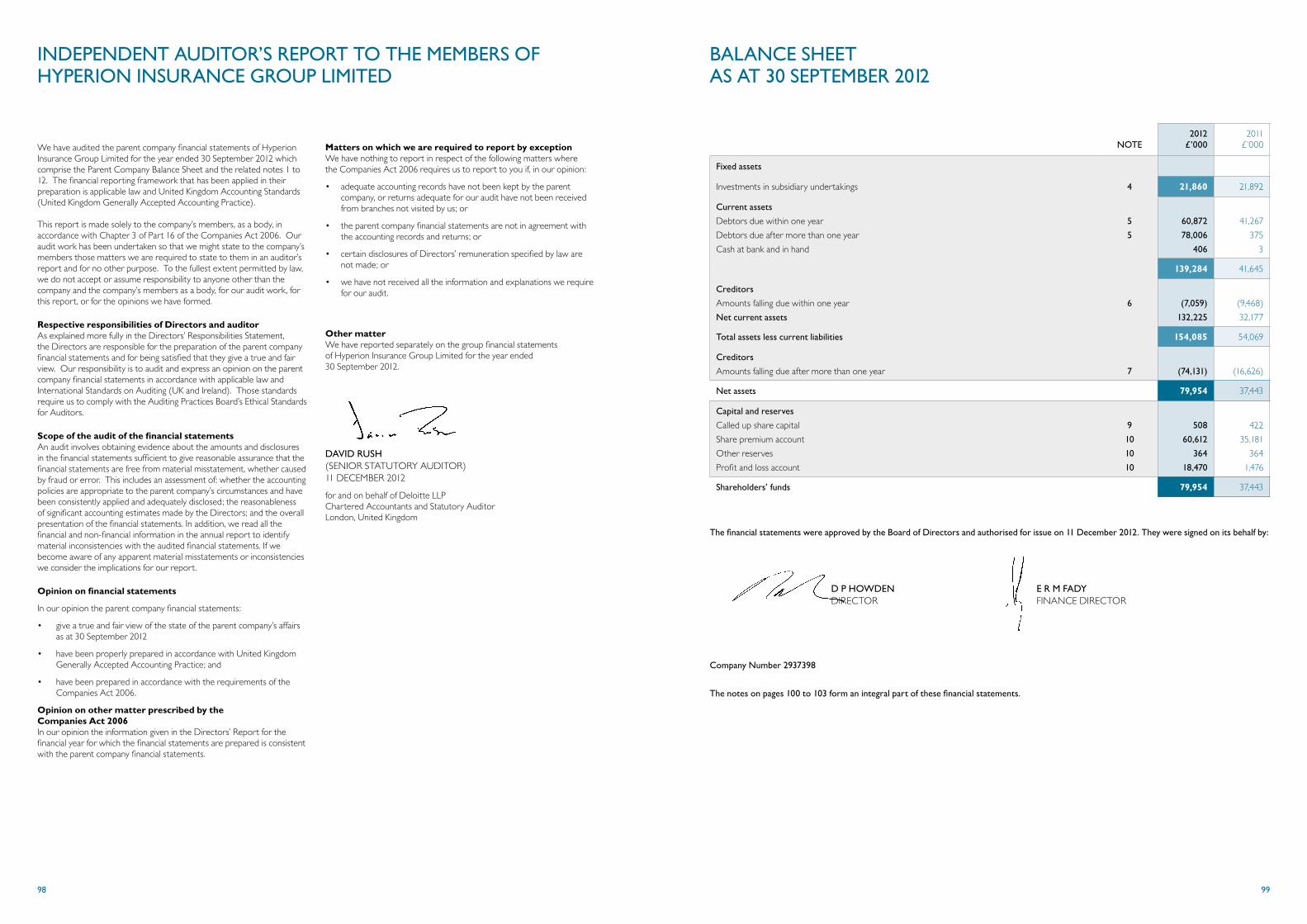

Discontinued OperationsDuring the year the Group sold to a consortium of new investors its 59.5% interest in CFC Underwriting Limited (“CFC”), which it had held since the establishment of CFC in 2000. The CFC sale was concluded, following FSA consent, on 19 June 2012. The Group disposed its entire 59.5% interest in CFC for cash consideration of £20.8m. For the year ended 30 September 2012, a profit of £1.5m was recorded for the discontinued operation, compared to a net profit of £2.4m in the previous financial year. The profit on disposal of CFC was £17.1m.

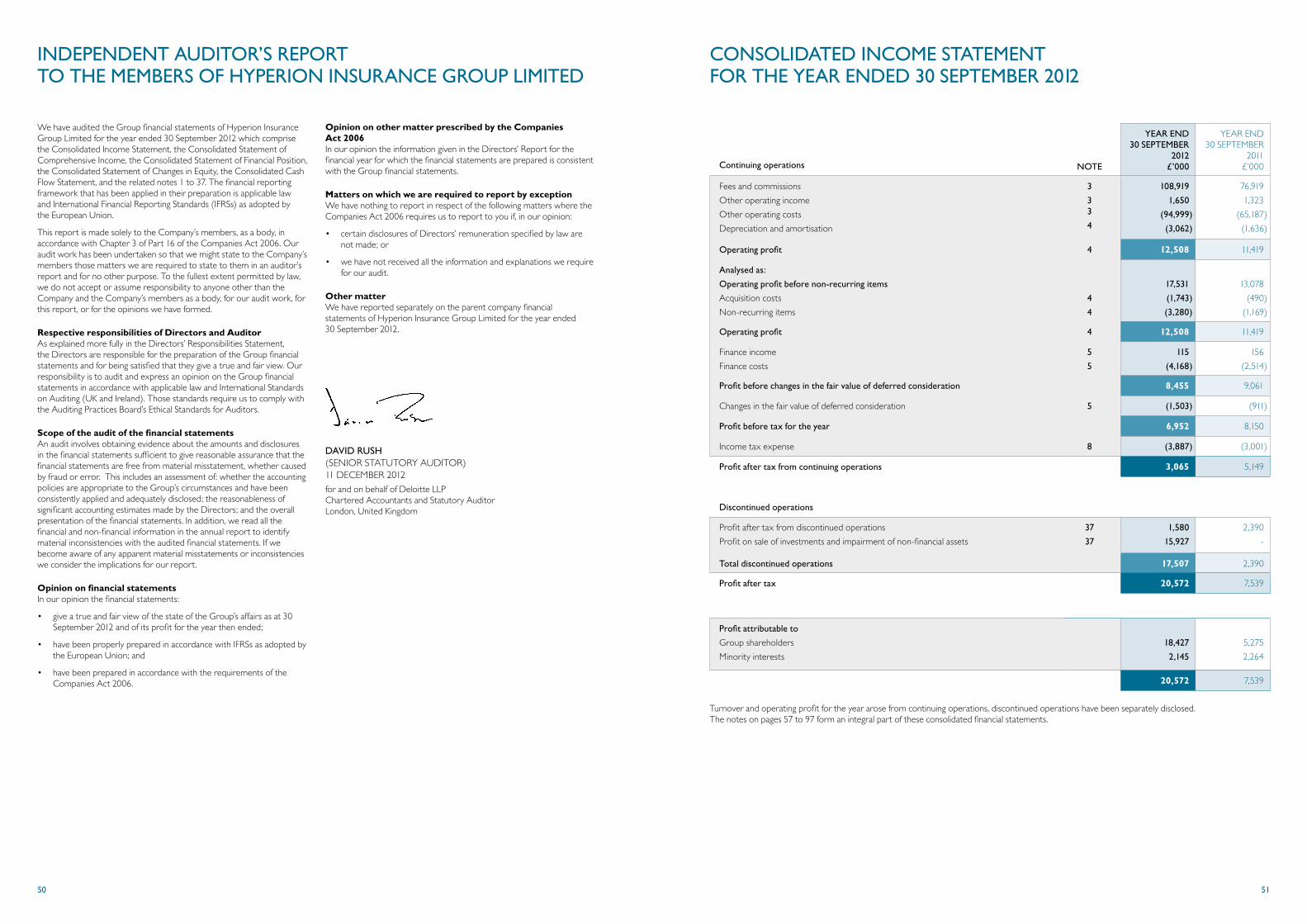

Continuing OperationsThe Board is pleased to announce that the Group reported a 42% growth in fees and commissions to £108.9m (2011: £76.9m). Group EBITDA (Earnings before Interest, Tax, Depreciation and Amortisation) excluding acquisition costs and non-recurring items was £20.6m, up 40% (2011: £14.7m). Group operating profit, before acquisition costs and non-recurring items was £17.5m (2011: £13.1m). Acquisition costs and non-recurring items are separately identified to provide greater understanding of the Group’s underlying performance. Further analysis of these items can be found in the Group’s accounting policies. Group profit before tax was £7.0m compared to £8.2m in 2011.

Howden Broking Group reported revenues of £74.8m (2011: £47.3m), representing overall growth of £27.5m (58%) compared to prior year. EBITDA was £12.1m (2011: £8.4m).

DUAL International reported revenue increased by £4.6m to £34.2m and its EBITDA increased from £8.2m to £9.9m. Gross written premiums increased by 24% to £227.8m. This includes exceptional costs of £1.7m incurred in the write-off of a business critical system as there has been a significant change in the extent and manner in which the system is

expected to be used in the future, such that previously capitalised costs are not expected to provide further benefit.

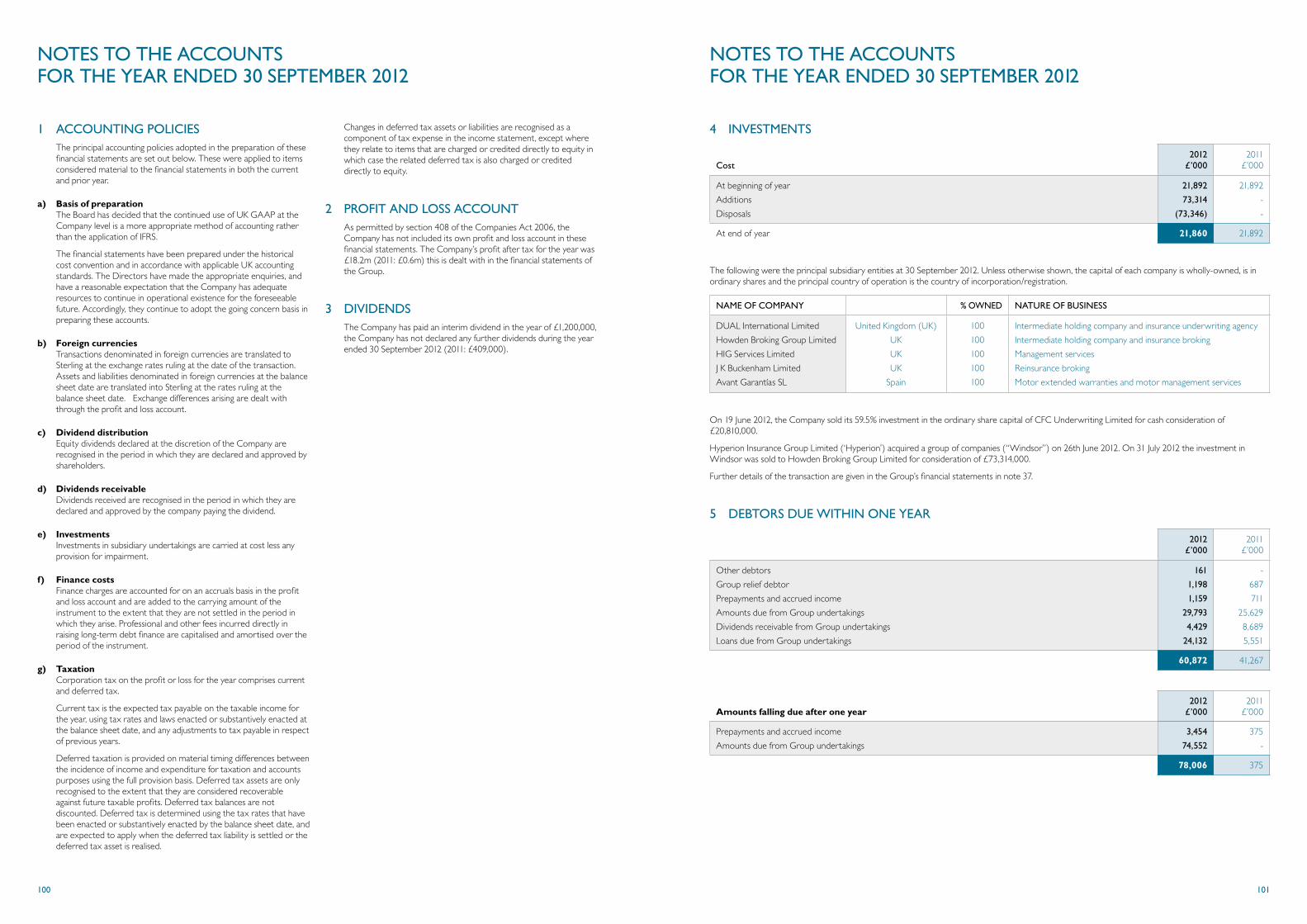

Acquisitions and growthOn 3 November 2011 Howden Broking Group Limited completed, following regulatory approvals, the acquisition of a 75% interest in the Accette Insurance Group, Asia’s largest independent insurance broker, through a newly-incorporated company called HBG Asia Holdings Limited.

During the year the Group also completed its largest acquisition to date with the agreed takeover of Windsor Limited and its subsidiaries, a specialist insurance broking group providing insurance broking services to companies in the UK and overseas, which was concluded following FSA consent on 3 July 2012.

On 28 September 2012 Howden Broking Group Limited acquired 51% of the shares in Conset Seguros, a Brazilian retail insurance broker specialising in the construction industry.

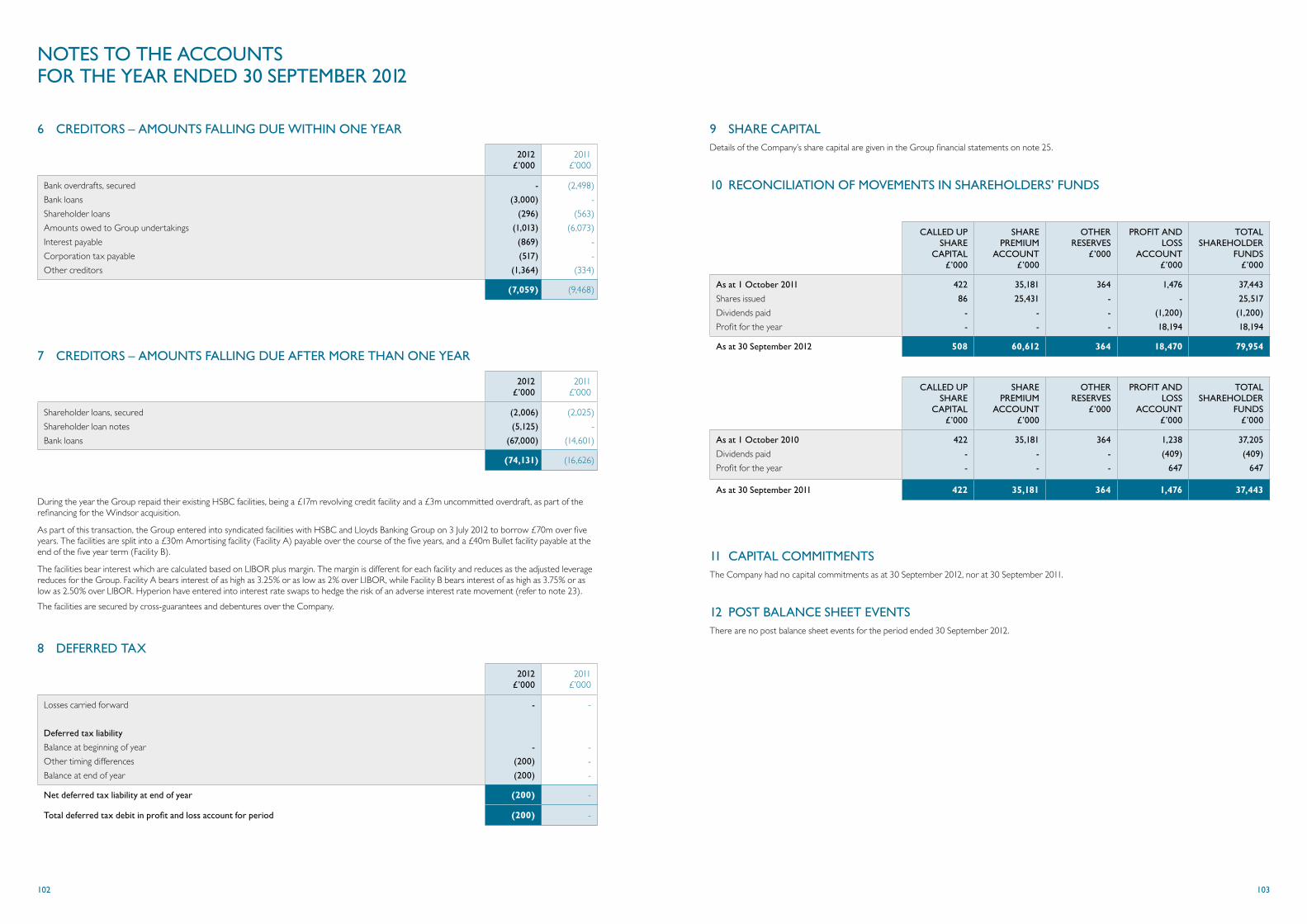

DividendsThe profit of the Group for the year after taxation and minority interests amounted to £18.4m (2011: £5.3m). Equity dividends were paid during the year amounting to £1.2 million (2011: £409,000).

the boarD

The Board is responsible for maintaining effective control over the Group’s significant strategic, financial, organisational, legal and regulatory matters. It meets at least six times a year. Management supply the Board with appropriate and timely information and the Directors are free to seek any further information they consider necessary.

DirectorsThe Directors who served during the year are listed below:

J P de Blocq van Kuffeler Chairman D P Howden Chief Executive E R M Fady L I Muñoz-Rojas Entrecanales J S Newman D A Whileman E H Woolf R T Van Gieson (resigned 27 April 2012) Lord Forsyth (appointed 20 September 2012)

Directors’ inDemnities

The Company has made qualifying third party indemnity provisions for the benefit of its Directors which were made during the year and remain in force at the date of this report.

corPorate Governance

Hyperion is committed to maintaining high standards of corporate governance. We recognise that good governance helps the business to deliver our strategy and safeguard shareholders’ long-term interests. We believe that the UK Corporate Governance Code provides a useful guide and we apply these principles as appropriate to a group of our size.

The Board has a schedule of matters specifically reserved for its decision.

Matters requiring Board approval include Group strategy and planning, structure and capital, financial reporting and controls, key business policies (including the remuneration policy), Board membership and other appointments.

The Board currently comprises three Executive Directors and five Non-Executive Directors (including the Chairman) with an appropriate balance of experience and knowledge. As a result, the Board‘s decision-making processes cannot be dominated by an individual or small group.

Mr. Whileman and Mr. Newman represent on the Company’s Board the shareholding interests of, respectively, 3i Group plc (including its managed funds) and BP Marsh & Company Limited. The Board believes that the presence of Mr. Whileman and Mr. Newman on the Board is appropriate and in the interests of shareholders generally and does not detract from their independence on any relevant issue. Mr. de Blocq van Kuffeler (the Chairman of the Board), Mr. Woolf (the senior independent non-executive Director), and Lord Forsyth are independent of any of the Company’s major shareholders. While Mr. Woolf has been a Director of the Company since 1999, the Board believes that his presence on the Board and as Chairman of the Audit Committee continues to be appropriate and in the interests of shareholders generally, having regard to his particular expertise and relevant experience in relation to his role.

The Directors have access to independent professional advice at the Company’s expense, where deemed necessary, to discharge their responsibilities as Directors. The Directors also have access to the advice and services of the Company Secretary.

accountability anD auDit

The Board has overall responsibility for the Group’s systems of internal control and for reviewing their effectiveness.

The implementation and maintenance of the risk management and internal control systems are the responsibility of the Executive Directors and senior management. The systems are designed to manage, rather than eliminate, the risk of failure to achieve business objectives and can provide reasonable, but not absolute, assurance against material misstatement or loss.

Relations with shareholdersThe Board ensures that a satisfactory dialogue with major investors and employee shareholders takes place. Each of the Company’s major investors is represented on the Board by a Director.

Conflicts of interestThe Company’s Articles of Association permit the Board to authorise potential conflicts of interest. Authorisation of any such conflicts may only be given by Directors who have no interest in the matter being considered. The Board has procedures in place to review actual and potential conflicts of interest.

Messrs Howden, Muñoz-Rojas Entrecanales, Newman and Whileman represent the interests of the Company’s four largest shareholders and their interests have been notified to the Company.

Committees of the BoardThe Board has delegated certain responsibilities to Committees that are described below, all of which have formally constituted terms of reference.