Embed Size (px)

DESCRIPTION

Hedge Funds in Strategic Asset Allocation Lyxor White Paper March 2014

Citation preview

WHITE PAPER - ISSUE #11

L Y X O R R E S E A R C H

HEDGE FUNDS IN STRATEGIC ASSET ALLOCATION

ZÉLIA CAZALET

Quantitative ResearchLyxor Asset Management

BAN ZHENG

Quantitative ResearchLyxor Asset Management

M A R C H 2 0 1 4

713967B_221076 White Paper N°11.indd 1 18/03/14 11:56

H E D G E F U N D S I N S T R AT E G I C A S S E T A L L O C AT I O N

I S S U E # 1 1 - M A R C H 2 0 1 4L Y X O R R E S E A R C H

<< 2

713967B_221076 White Paper N°11.indd 2 18/03/14 11:56

H E D G E F U N D S I N S T R AT E G I C A S S E T A L L O C AT I O N

I S S U E # 1 1 - M A R C H 2 0 1 4L Y X O R R E S E A R C H

3 >>

Foreword

Total assets under management for the hedge fund industry reached an all-time highof USD 2.6 trillion in 20131. With lower expectations for traditional assets, many institu-tional investors, including pension funds and corporate, are lending increasing allocation toalternative assets to secure both performance and resilience for their portfolios. As a result,hedge funds are now growing faster than any other type of asset. They are expected to reachUSD 3.3 trillion by 2015 with a compound annual growth rates of around 15%2.

This 11th white paper looks at hedge funds from a new perspective, in the context ofStrategic Asset Allocation (SAA). We see the growth of the assets managed the industry asan implicit consequence of the different approach taken with regard to hedge fund invest-ments.

Numerous studies using pre-2008 data have shown the benefits of adding hedge fundsto SAA. Hedge funds were previously considered to be a stand-alone asset which shouldaccount for a small percentage of overall portfolios. Now, in the aftermath of the financialcrisis, a new paradigm has appeared: hedge funds are becoming mature investmentstyles exhibiting significant and persistent performance divergence both witheach other and when compared to traditional assets.

As such, hedge fund strategies should be disaggregated into sensible sub-categories whichshould naturallymigrate from a stand-alone asset into the broader equity and bondasset-mix. In this context, we propose a reassessment of the relationship between hedgefund strategies and traditional markets to introduce an updated SAA framework withhedge funds.

To highlight the above points, this paper addresses the following structural questions:

• What are the stylized facts of hedge fund performance in the post-2008environment?

• How should we classify hedge funds in order to better reflect their truecharacteristics?

• What is the best way to integrate the new classification process into a SAAapproach?

We hope you will find this article both interesting and useful in practice.

Jean-Marc StengerChief Investment Officer for Alternative Investments

1Hedge Fund Research database, 2013.2The New Challenge for Hedge Funds: Operational Excellence, Boston Consulting Group, 2013.

713967B_221076 White Paper N°11.indd 3 18/03/14 11:56

H E D G E F U N D S I N S T R AT E G I C A S S E T A L L O C AT I O N

I S S U E # 1 1 - M A R C H 2 0 1 4L Y X O R R E S E A R C H

<< 4

713967B_221076 White Paper N°11.indd 4 18/03/14 11:56

H E D G E F U N D S I N S T R AT E G I C A S S E T A L L O C AT I O N

I S S U E # 1 1 - M A R C H 2 0 1 4L Y X O R R E S E A R C H

5 >>

Executive Summary

Introduction

Alternative investments, including hedge funds, have grown faster than non-alternativesand have now surpassed their 2007 levels. For this reason, institutional investors expectto increase allocations to alternative classes, especially hedge funds. It seems that manyinvestors are still following the traditional approach to examining their SAA with hedgefunds because many academic and empirical studies are based on pre-2008 data.

As the performance of hedge funds is becoming less homogeneousthan in the past, it is of the utmost importance to re-examine theSAA with hedge funds.

In our investment philosophy, hedge funds can be regarded as (equity or bond) betaproviders or pure alpha generators. Intelligent use of beta provider hedge funds allows moreefficient risk diversification compared to traditional assets. Moreover, it is worthwhileto introduce some pure alpha generator hedge funds to generate uncorrelated absolutereturn. To take advantage of these benefits, we propose a new process for classifyinghedge funds into two families: equity/bond substitutes and diversifiers. To take intoaccount economic periodicity, we then propose a regime switching mean-variance model fordetermining the hedge fund allocation in strategic asset allocation.

A new vision of hedge funds after the subprime crisis

• Hedge funds are more resilient than traditional assets during crisis peri-ods.

• In the post-2008 environment, it is no longer possible to consider hedgefunds as a single asset class.

Many academic studies show that hedge funds are generally more resilient than equities andbonds in extreme periods, with hedge fund losses being three times lower than the largestfalls suffered by equities. In addition, hedge fund returns are very positive in comparisonwith the biggest losses made by bonds.

Moreover, several studies report homogeneous attractive hedge fund performance foralmost all hedge fund strategies using data from before the subprime crisis in 2008. Thishomogeneity allows investors to consider hedge funds as a single asset class in strategic assetallocation. Nevertheless, many differences between strategies appeared during the subprime

713967B_221076 White Paper N°11.indd 5 18/03/14 11:56

H E D G E F U N D S I N S T R AT E G I C A S S E T A L L O C AT I O N

I S S U E # 1 1 - M A R C H 2 0 1 4L Y X O R R E S E A R C H

<< 6

crisis period. For instance, Equity Hedge suffered from big losses whereas Macro faredbetter. The difference between hedge fund strategies in terms of performance and volatilityhas persisted since 2008.

A new process for classifying heterogeneous hedge funds

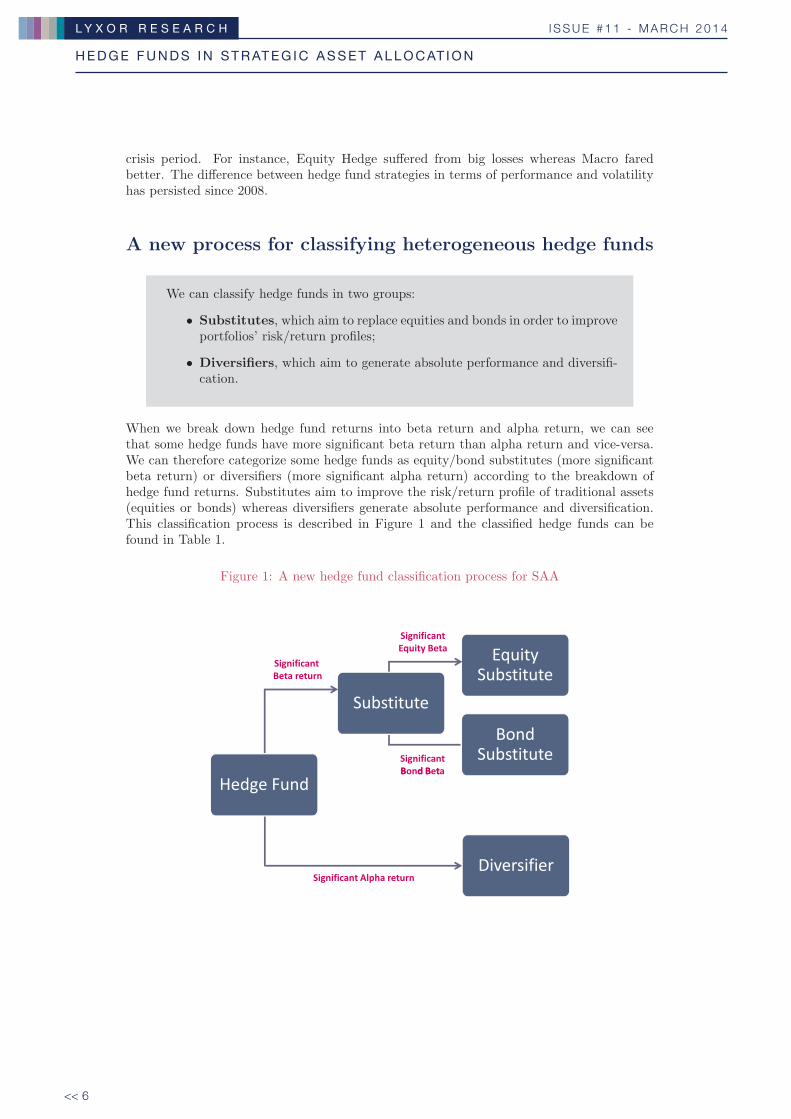

We can classify hedge funds in two groups:

• Substitutes, which aim to replace equities and bonds in order to improveportfolios’ risk/return profiles;

• Diversifiers, which aim to generate absolute performance and diversifi-cation.

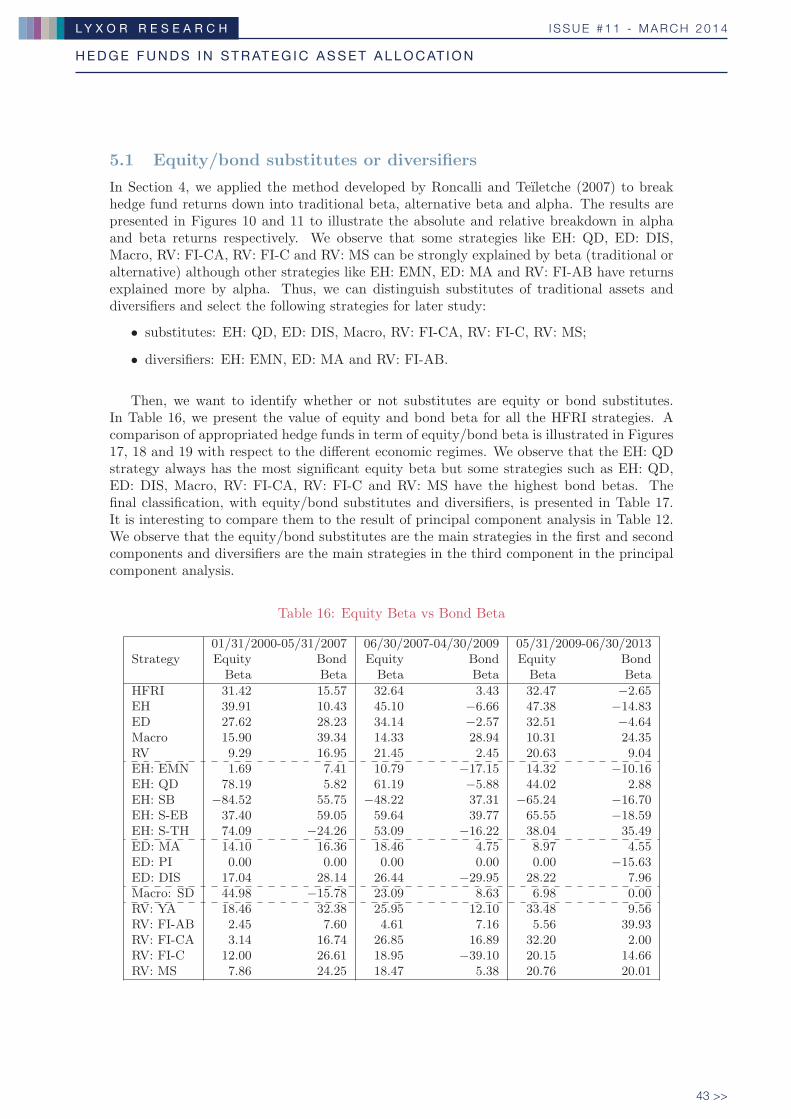

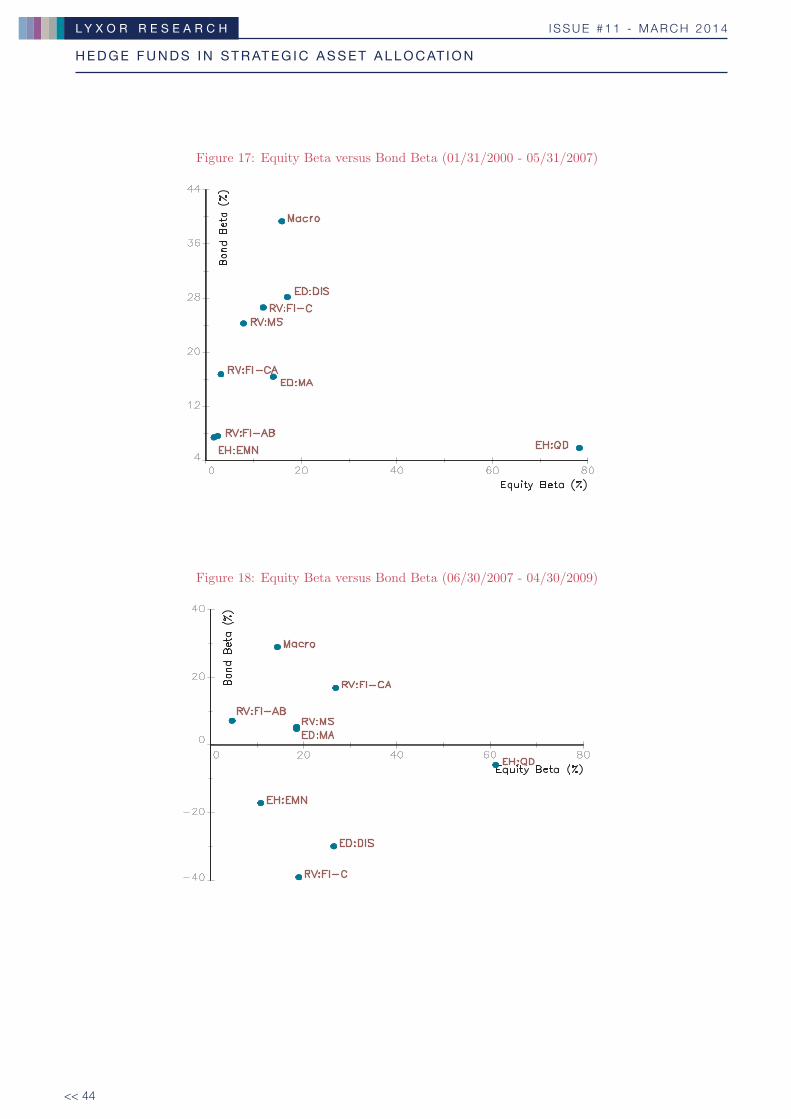

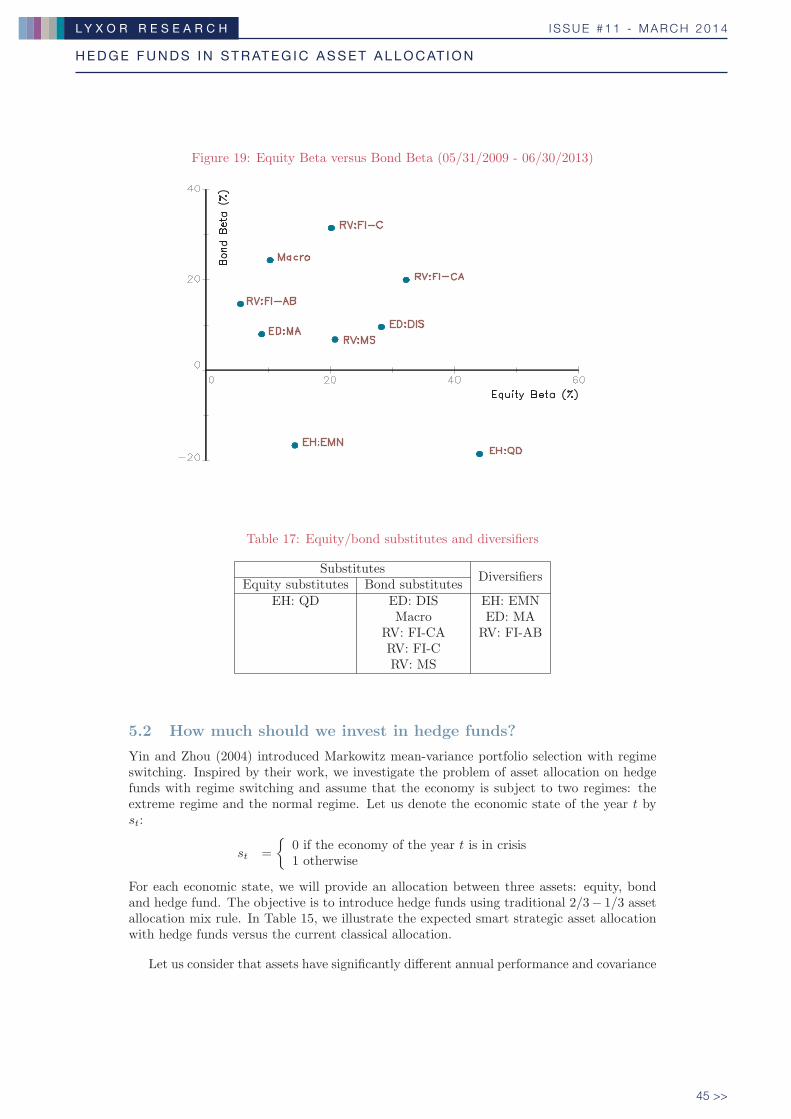

When we break down hedge fund returns into beta return and alpha return, we can seethat some hedge funds have more significant beta return than alpha return and vice-versa.We can therefore categorize some hedge funds as equity/bond substitutes (more significantbeta return) or diversifiers (more significant alpha return) according to the breakdown ofhedge fund returns. Substitutes aim to improve the risk/return profile of traditional assets(equities or bonds) whereas diversifiers generate absolute performance and diversification.This classification process is described in Figure 1 and the classified hedge funds can befound in Table 1.

Figure 1: A new hedge fund classification process for SAA

������������� ���

����������� � �

�������������������

����������

���������������

��������������

��������

���������� �����������

����� ����

�����������

713967B_221076 White Paper N°11.indd 6 18/03/14 11:56

H E D G E F U N D S I N S T R AT E G I C A S S E T A L L O C AT I O N

I S S U E # 1 1 - M A R C H 2 0 1 4L Y X O R R E S E A R C H

7 >>

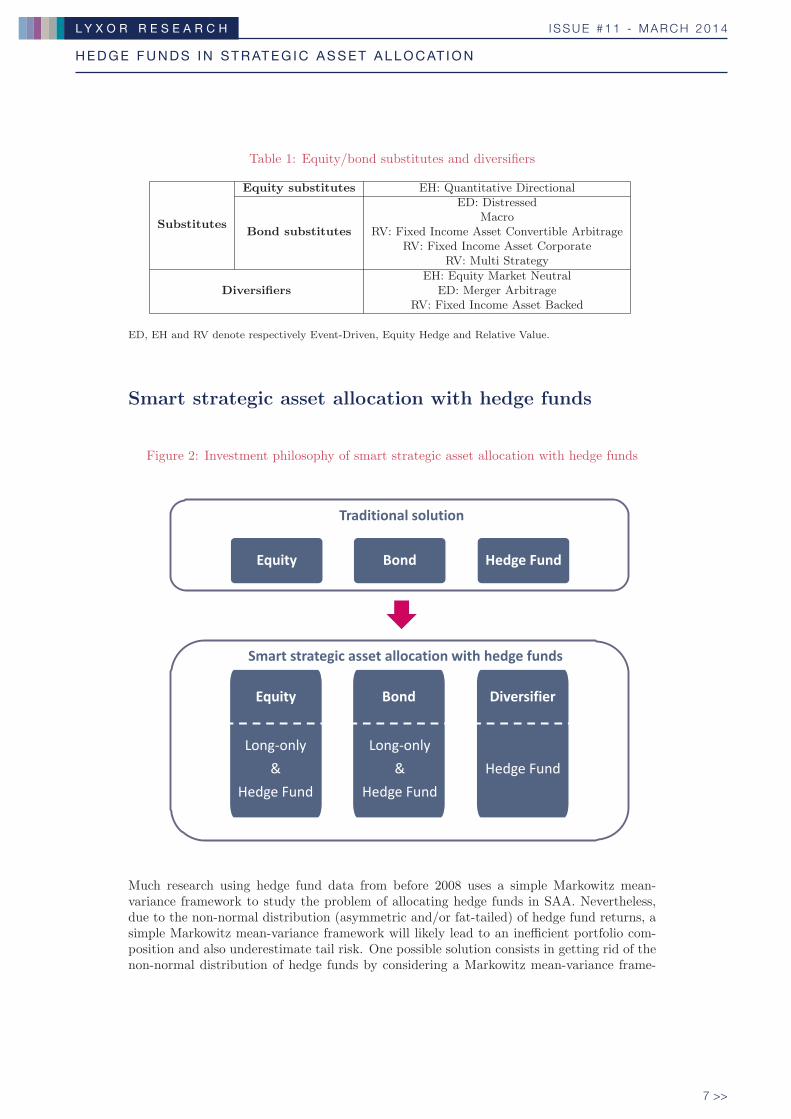

Table 1: Equity/bond substitutes and diversifiers

Substitutes

Equity substitutes EH: Quantitative Directional

Bond substitutes

ED: DistressedMacro

RV: Fixed Income Asset Convertible ArbitrageRV: Fixed Income Asset Corporate

RV: Multi Strategy

EH: Equity Market NeutralDiversifiers ED: Merger Arbitrage

RV: Fixed Income Asset Backed

ED, EH and RV denote respectively Event-Driven, Equity Hedge and Relative Value.

Smart strategic asset allocation with hedge funds

Figure 2: Investment philosophy of smart strategic asset allocation with hedge funds

���������� �������

��� ���� ����� ����

������������ ���� ������������� ����� �����

��� ���� �����������

����������

����� ����

����������

����� ��������� ����

Much research using hedge fund data from before 2008 uses a simple Markowitz mean-variance framework to study the problem of allocating hedge funds in SAA. Nevertheless,due to the non-normal distribution (asymmetric and/or fat-tailed) of hedge fund returns, asimple Markowitz mean-variance framework will likely lead to an inefficient portfolio com-position and also underestimate tail risk. One possible solution consists in getting rid of thenon-normal distribution of hedge funds by considering a Markowitz mean-variance frame-

713967B_221076 White Paper N°11.indd 7 18/03/14 11:56

H E D G E F U N D S I N S T R AT E G I C A S S E T A L L O C AT I O N

I S S U E # 1 1 - M A R C H 2 0 1 4L Y X O R R E S E A R C H

<< 8

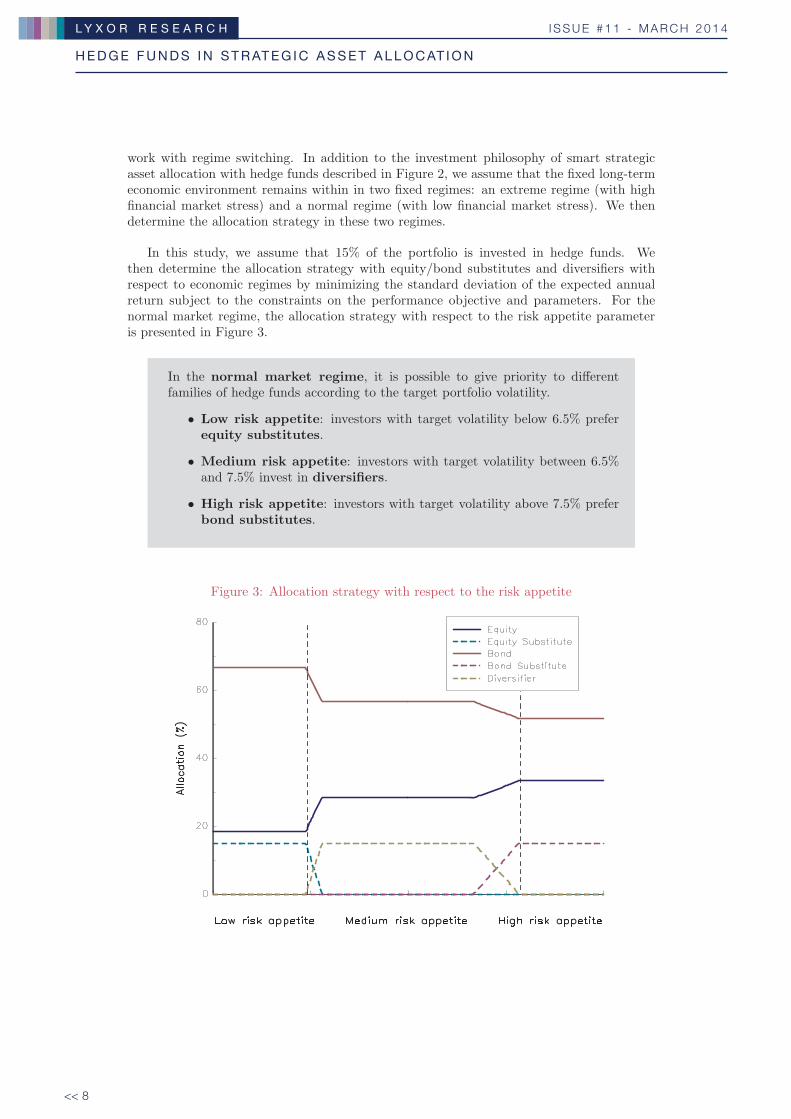

work with regime switching. In addition to the investment philosophy of smart strategicasset allocation with hedge funds described in Figure 2, we assume that the fixed long-termeconomic environment remains within in two fixed regimes: an extreme regime (with highfinancial market stress) and a normal regime (with low financial market stress). We thendetermine the allocation strategy in these two regimes.

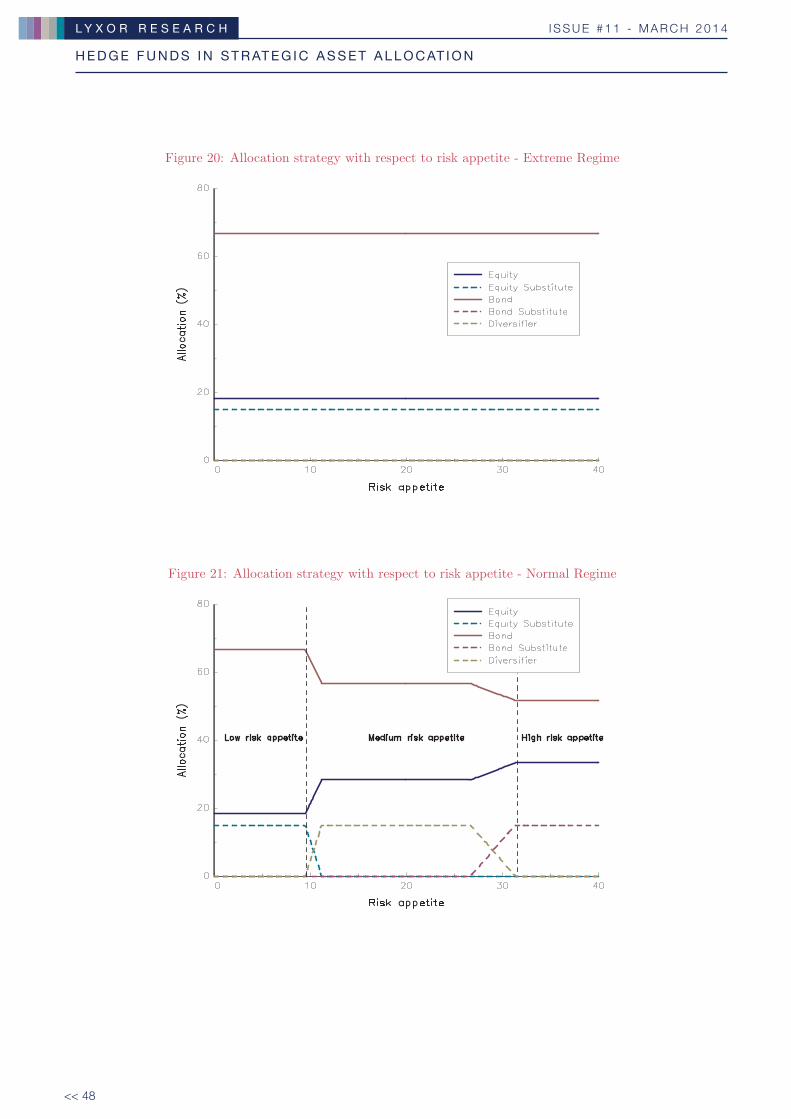

In this study, we assume that 15% of the portfolio is invested in hedge funds. Wethen determine the allocation strategy with equity/bond substitutes and diversifiers withrespect to economic regimes by minimizing the standard deviation of the expected annualreturn subject to the constraints on the performance objective and parameters. For thenormal market regime, the allocation strategy with respect to the risk appetite parameteris presented in Figure 3.

In the normal market regime, it is possible to give priority to differentfamilies of hedge funds according to the target portfolio volatility.

• Low risk appetite: investors with target volatility below 6.5% preferequity substitutes.

• Medium risk appetite: investors with target volatility between 6.5%and 7.5% invest in diversifiers.

• High risk appetite: investors with target volatility above 7.5% preferbond substitutes.

Figure 3: Allocation strategy with respect to the risk appetite

713967B_221076 White Paper N°11.indd 8 18/03/14 11:56

H E D G E F U N D S I N S T R AT E G I C A S S E T A L L O C AT I O N

I S S U E # 1 1 - M A R C H 2 0 1 4L Y X O R R E S E A R C H

9 >>

Conclusion

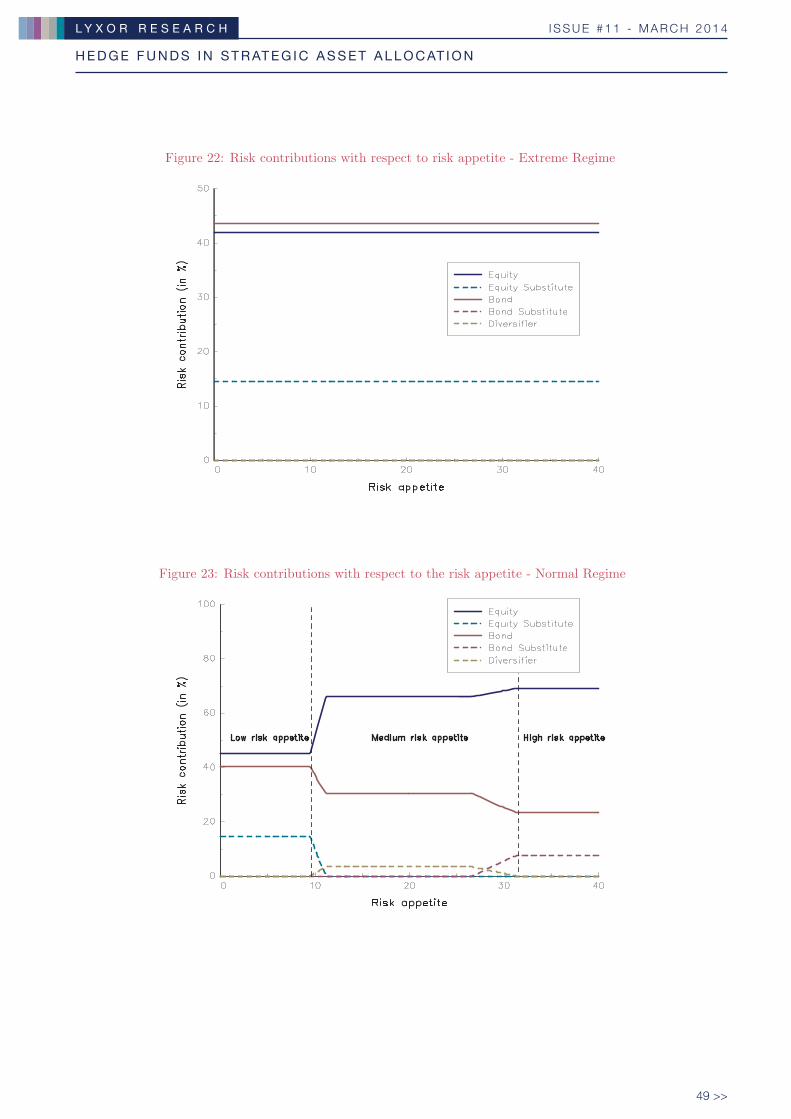

Hedge funds are attractive investment tools, but are more sophisticated than traditionalassets and therefore require more investment expertise. Hedge funds have become noticeablymore mature in recent years, meaning that it is time to reassess hedge fund investments inSAA. The granularity of hedge funds allows us to evaluate and classify them according totheir sensitivity to common risk factors. Hedge funds can be classified into equity/bondsubstitutes and diversifiers. Taking into account the non-normal distribution of hedge fundreturns and economic periodicity, a regime switching Markowitz model is applied to examineportfolio allocation in an extreme market regime and a normal market regime. We show thatinvestors should choose equity substitutes in an extreme market regime, while in a normalmarket regime, it is recommended for investors to use equity substitutes, diversifiers andbond substitutes if they are aiming for low, medium and high volatility respectively.

713967B_221076 White Paper N°11.indd 9 18/03/14 11:56

H E D G E F U N D S I N S T R AT E G I C A S S E T A L L O C AT I O N

I S S U E # 1 1 - M A R C H 2 0 1 4L Y X O R R E S E A R C H

<< 10

713967B_221076 White Paper N°11.indd 10 18/03/14 11:56

H E D G E F U N D S I N S T R AT E G I C A S S E T A L L O C AT I O N

I S S U E # 1 1 - M A R C H 2 0 1 4L Y X O R R E S E A R C H

11 >>

Table of Contents

1 Introduction 13

2 Hedge fund overview 152.1 Hedge fund databases . . . . . . . . . . . . . . . . . . . . . . . . 15

2.1.1 Biases in database construction . . . . . . . . . . . . . . 152.1.2 Private hedge funds databases and indices . . . . . . . . 16

2.2 Stylized facts of hedge funds . . . . . . . . . . . . . . . . . . . . 172.2.1 Basic statistics of hedge fund indices . . . . . . . . . . . 182.2.2 Survivorship bias . . . . . . . . . . . . . . . . . . . . . . 202.2.3 Abnormal distribution and fat tail risk . . . . . . . . . . 212.2.4 Performance persistence . . . . . . . . . . . . . . . . . . 222.2.5 Auto-correlation . . . . . . . . . . . . . . . . . . . . . . 232.2.6 Cross-correlation with traditional assets . . . . . . . . . 24

2.3 Quantitative classification of hedge funds . . . . . . . . . . . . . 26

3 Investment vehicles 283.1 Single hedge funds and managed account platforms . . . . . . . 283.2 Funds of hedge funds and multi-strategy funds . . . . . . . . . . 293.3 Hedge fund indices replicators . . . . . . . . . . . . . . . . . . . 30

4 Benefits and risks of hedge funds investments 314.1 Benefits of hedge funds investments . . . . . . . . . . . . . . . . 31

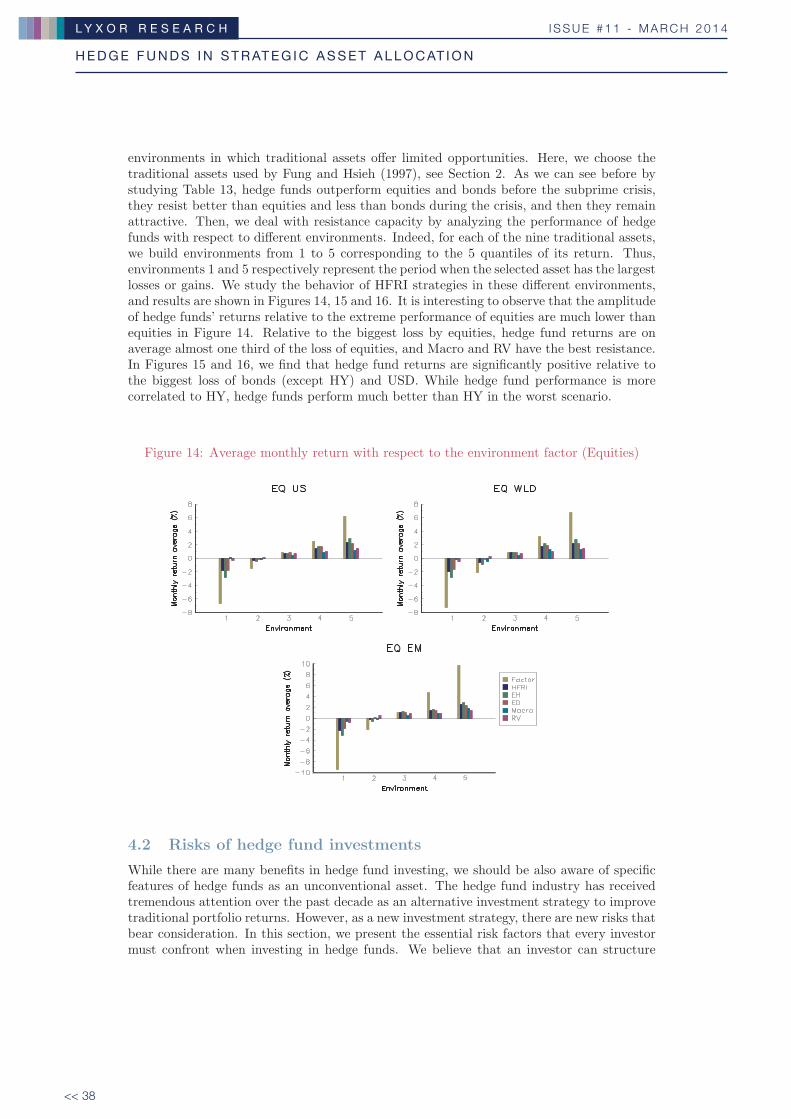

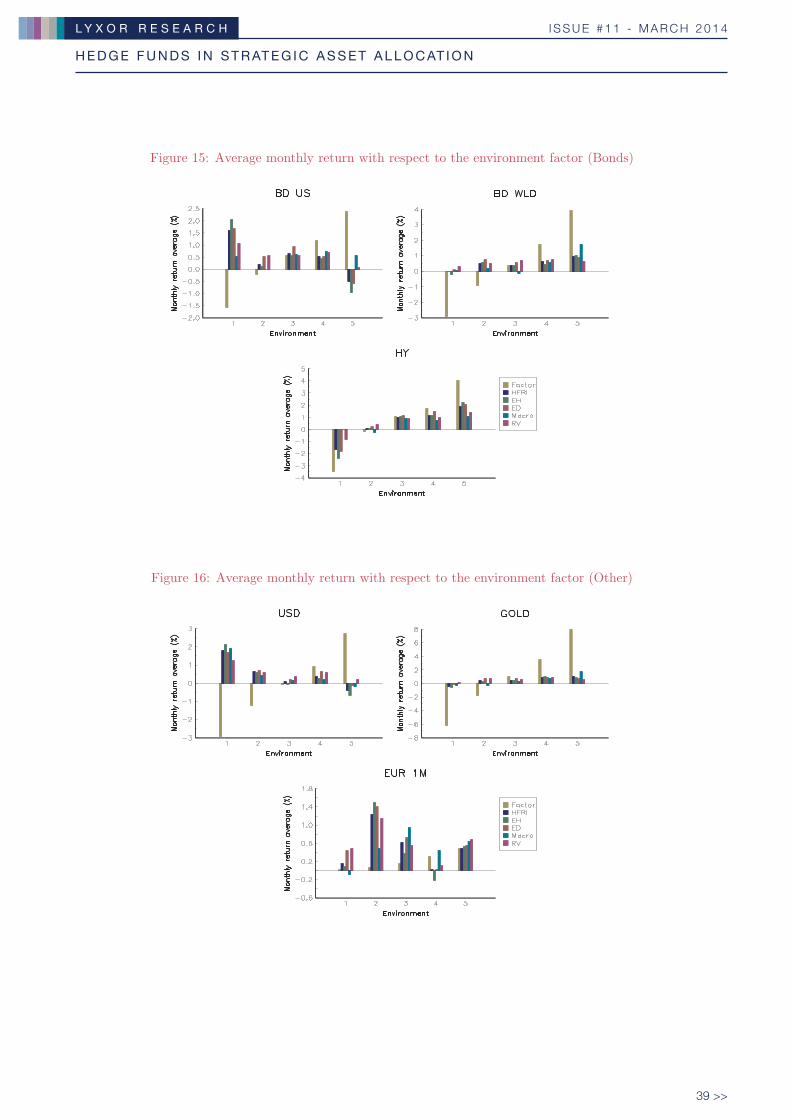

4.1.1 Significant risk-adjusted return . . . . . . . . . . . . . . 314.1.2 Efficient diversification of risks . . . . . . . . . . . . . . . 324.1.3 Resistance to market environments . . . . . . . . . . . . 37

4.2 Risks of hedge fund investments . . . . . . . . . . . . . . . . . . 38

5 Smart strategic asset allocation with hedge funds 415.1 Equity/bond substitutes or diversifiers . . . . . . . . . . . . . . 435.2 How much should we invest in hedge funds? . . . . . . . . . . . 45

6 Conclusion 50

A Comparison of classification in different databases 52

B Markowitz mean variance model with regime switching 53

Sans titre-2 1 19/03/14 11:50

H E D G E F U N D S I N S T R AT E G I C A S S E T A L L O C AT I O N

I S S U E # 1 1 - M A R C H 2 0 1 4L Y X O R R E S E A R C H

<< 12

713967B_221076 White Paper N°11.indd 12 18/03/14 11:56

H E D G E F U N D S I N S T R AT E G I C A S S E T A L L O C AT I O N

I S S U E # 1 1 - M A R C H 2 0 1 4L Y X O R R E S E A R C H

13 >>

From Niche to Mainstream: A New Approach

to Utilizing Hedge Funds in Strategic Asset

Allocation

Zelia CazaletQuantitative Research

Lyxor Asset Management, [email protected]

Ban ZhengQuantitative Research

Lyxor Asset Management, [email protected]

March 2014

Abstract

Over recent decades, the hedge fund industry has expanded rapidly. Its developmenthas enabled the creation of a new asset class in its own right. Hedge funds have becomemore attractive in recent years, especially for family offices and institutional investors.The objective of this paper is to provide a comprehensive overview of hedge funds in themost detailed way possible and propose an innovative approach to placing hedge fundsin strategic asset allocation (SAA). Using the HFR database, we review the stylizedfacts, benefits and risks of hedge funds. We propose a new method of classifying hedgefunds as equity/bond substitutes and diversifiers. We then examine SAA in extremeand normal regimes using the Markowitz mean-variance model with regime switching.

Keywords: Hedge fund, strategic asset allocation, Markowitz, regime switching.

JEL classification: G11.

1 Introduction

Hedge funds have experienced explosive growth in recent decades and assets under manage-ment in the global hedge fund industry totalled USD 2.6 trillion in 2013 according to HedgeFund Research. Nonetheless, they needed time to emerge from the shadows and to becomea very attractive asset class in recent decades. The key principles of the first single-hedgefund were introduced by the statistician Karsten in his book Scientific Forecasting publishedin 1931. However, the creation of the first large hedge fund by Jones did not occur until1949. His investment process combined long positions in undervalued stocks and short po-sitions in overvalued ones, adding leverage by financing long positions from short sales andintroducing performance-linked fees (20% of realized profits). It was not until 1966 that anewspaper article written by Loomis described this process and introduced the term hedgefund for the first time (Lhabitant, 2006).

After that, the alternative industry experienced strong growth during the huge bullmarket of the 1950s and 1960s. Caldwell (1995) reports that a 1968 SEC survey found that140 out of 215 investment partnerships were probably hedge funds. Many of the futureindustry leaders started their funds during this period such as Warren Buffett’s Omaha-based Buffett Partnership, the first fund of hedge fund Walter J. Schloss’s WJS Partners

713967B_221076 White Paper N°11.indd 13 18/03/14 11:56

H E D G E F U N D S I N S T R AT E G I C A S S E T A L L O C AT I O N

I S S U E # 1 1 - M A R C H 2 0 1 4L Y X O R R E S E A R C H

<< 14

and the George Soros’ Quantum Fund. Nevertheless, hedge funds went through a difficultperiod from the end of 1960s to the beginning of 1980s. Their popularity revived againin 1986 thanks to an article by Rohrer entitled Institutional Investor. He highlighted theoutperformance of Julian Roberton’s Tiger Fund campared with the S&P 500 over the firstsix years of its existence. Julian Roberton’s investment was based on macroeconomic analysis(occasionally without a hedging policy) and on allocation to financial derivatives such asfutures and options. This strategy is referred to as global macro which had great success inthe late 1980s thanks to the weak US dollar, the rise of equity markets, commodity marketsand interest rates and the fall of bond market.

Then, like most other traditional asset classes, hedge funds were severely hurt by finan-cial crises such as the crash of October 1987, the Gulf war in 1990, the European currencycrisis in 1992 and 1993 or the Mexico crisis in 1994. However, hedge funds recover bet-ter and faster than financial markets as a whole. Thus, during this period, many newstrategies emerged including credit arbitrage, distressed debt, fixed income, quantitative,multi-strategy etc. In addition, many institutional investors such as pension and endow-ment funds began to allocate a greater portion of their portfolios to hedge funds achievingvery attractive performance (Swensen, 2000).

In 1998, the collapse of Long Term Capital Management (LTCM) which was founded byMeriwether and run by future Nobel Laureates Scholes and Merton, represents a landmark inthe evolution of the hedge fund industry. It acted as a wake-up call for all markets regardingthe need for greater transparency and better practices. Hedge funds sharply reduced theirleverage, agreed to provide their investors with greater transparency, and improved their riskmanagement. During the subprime mortgage crisis in 2007 and 2008, despite a double-digitloss for the Credit Suisse/Tremont hedge fund index, hedge funds outperformed the globalequity market. Meanwhile, the fraud by Madoff Investment Securities LLC in 2008 droveregulators to impose a tighter and more stringent regulatory framework requiring extendedhedge fund registration and reporting. Increased regulation aimed at protecting investorsin recent years is seen as boosting investor confidence and adding value to the hedge fundindustry.

Due to their eventful history, hedge funds have become a key investment vehicle inmodern finance. They represent an important financial instrument in the growing alternativeinvestment market. Recently, alternative investments have experienced higher growth thannon-alternative investments. Farrell et al. (2008) show that compound annual growth ratesare 14.2% and 1.9% respectively for alternative investments and non-alternative investmentsfrom 2000 to 2007. Erzan et al. (2012) state that alternative investments have grown fasterthan non-alternatives over the last six years and have surpassed peak 2007 levels. Theyreport that assets under management in hedge funds reached USD 2.25 trillion at the end of2012 and are expected to reach USD 3−4.9 trillion in 2013. They also show that institutionalinvestors expect to increase allocations to hedge funds as well as other alternative classessuch as private equity or real estate.

In spite of major growth in investment in hedge funds and academics’ increasing interestin this subject, there is still much to be done in this area of research. Unlike the case oftraditional assets, few investors have a detailed overview of hedge funds in terms of theirstylized facts, benefits, risks and especially their role in SAA. In this paper, we hope toprovide an overview of these subjects and propose a new hedge fund allocation process inSAA using a regime switching mean-variance model.

713967B_221076 White Paper N°11.indd 14 18/03/14 11:56

H E D G E F U N D S I N S T R AT E G I C A S S E T A L L O C AT I O N

I S S U E # 1 1 - M A R C H 2 0 1 4L Y X O R R E S E A R C H

15 >>

Our paper is organized as follows. In Section 2, we provide an overview of the hedgefund industry. We present different hedge fund databases and study the stylized factsand quantitative classification of hedge funds using the HFR database. Then, we examinedifferent hedge fund investment vehicles in Section 3. In Section 4, we present the benefitsand risks of investing in hedge funds. Section 5 is dedicated to proposing an innovativeapproach to classifying hedge funds as equity/bond substitutes and diversifiers. It thenexamines the SAA in extreme regime and normal regimes using Markowitz’s mean-varianceportfolio selection with regime switching.

2 Hedge fund overview

In what follows, we present the main characteristics of hedge funds. In the first paragraph,we introduce different databases used by investors and academics and their respective clas-sification methods. We then present the basic statistics on HFRI indices and their stylizedfacts such as fat-tail risk, performance persistence, auto-correlation and cross-correlationwith traditional assets. We conclude this section with a quantitative classification.

2.1 Hedge fund databases

Studying the statistics and stylized facts of hedge funds requires the gathering of good in-formation about the hedge fund industry. It is necessary as a minimum to have data on thereturns and the qualitative investment styles of hedge funds. Hedge funds do not have apublic organization which officially collects this type of information. Meanwhile, fund man-agers voluntarily release monthly return information to the specialised databases to whichpractitioners and academics must pay a subscription to gain access rights. The databaseproviders also offer other services like hedge fund indices which are widely used in the in-dustry. However, we must be careful because these databases and their respective indicesdo not exactly represent the whole hedge fund universe. All these databases and indices canbe built according to different methodologies. It is important to highlight existing biasesto be taken into account in statistical analysis before choosing the appropriate database tostudy.

2.1.1 Biases in database construction

In this paragraph, we list different biases in database construction that we have to keep inmind before doing any statistical analysis.

First we look at the selection bias. Hedge funds are private investment solutions andhave no obligation to report their performance. They only have to communicate theirperformance to their own investors. There is no public organization which officially collectsthis type of data. Hedge funds decide for themselves what to communicate in prospectusesand voluntarily provide information about their performance if they need more visibility.Thus, while small funds with good performance are eager to report their performance,bad funds do not want to report their performance since they do not wish to suffer fromcompetition. Moreover, famous large funds with exceptional performance are not interestedin this visibility. As a result, the selection bias is linked to the data sources and may beamplified in the proprietary construction of databases. Indeed, some databases follow certainreporting rules such as minimum assets under management and performance records. The

713967B_221076 White Paper N°11.indd 15 18/03/14 11:56

H E D G E F U N D S I N S T R AT E G I C A S S E T A L L O C AT I O N

I S S U E # 1 1 - M A R C H 2 0 1 4L Y X O R R E S E A R C H

<< 16

lack of representativeness and homogeneity of database construction rules and the selectivereporting rules of some hedge funds lead to partial representation of the whole hedge fundindustry by each database.

Another important bias is the survivorship bias which is often mentioned in many re-search papers. The survivorship bias results from the tendency to exclude “dead funds”from statistical study when their performance is no longer reported. A fund is supposed tobe dead when it is liquidated, closed, merged or simply when it stops reporting. Althoughsome researchers only focus on live funds which are surviving funds on the date of the study,it is biased to analyze the behavior of the whole hedge fund world over a long period byusing live funds. Many studies have been carried out on this subject with the database ofmutual funds or hedge funds (Malkiel, 1995, Elton et al., 1996, Brown and Goetzmann, 1997,Ackermann et al., 1999, Brown et al., 1999, Fung and Hsieh, 2000, Liang, 2000, Agarwal etal., 2013, Aiken et al., 2013).

Hedge fund databases also face a backfill bias. When a hedge fund is added to a database,its manager can choose whether or not to report its returns over the incubation periodprior to the date of submission. Hence, there is a bias resulting from the fact that fundswith satisfying performance over the incubation period report their returns whereas fundswith disappointing performance prefer to provide returns only after the submission date.Moreover, for some hedge funds, there is a time lag between the realisation time and thereporting time. Liang (2000) documents the backfill bias by discovering that the same fundin several databases has not reported its return since the same date. Barry (2003) highlightsdifferent backfill durations in each database.

Finally, since hedge funds often invest in illiquid assets for which market prices are notreadily available, we may face liquidity bias in hedge fund databases due to the smoothing ofprices in the valuation process (Cici et al., 2011). To account for liquidity bias, Getmanskyet al. (2004) propose an approach to uncover the unobserved (“true”) returns which aresupposed to be serially uncorrelated contrary to the serially correlated observed returns.However, Ammann et al. (2011, 2013) investigate liquidity bias but find it to be very small.

2.1.2 Private hedge funds databases and indices

In this paragraph, we present different hedge fund databases. We can find details of variousdatabases in Brooks and Kat (2002) and Lhabitant (2006). Here, we only deal with thedatabases most frequently used by investors and academics. We then compare their differentclassification methods and define the usual hedge fund strategies.

The Hedge Fund Research (HFR) database has reported the performance net of fees ofnearly 7, 000 funds and funds of funds since 1990. It has also built 32 HFRI indices which areequally weighted indices. These HFRI indices aim to reflect the hedge fund industry globallyor by strategies and are widely used by practitioners. The HFRI indices are the most popularindices which benchmark the total hedge funds industry with almost 2, 200 funds (providedby Hedge Fund Research, Inc. in August 2013). HFR also proposes HFRX indices which aredaily investable and transparent indices of the hedge fund industry. Recently, they createdHFRU indices which are benchmarks for UCITS hedge funds.

The TASS or Lipper database contains the performance of 7, 500 live funds and fundsof funds plus more than 11, 000 dead funds. The relative indices are the 14 value-weighted

713967B_221076 White Paper N°11.indd 16 18/03/14 11:56

H E D G E F U N D S I N S T R AT E G I C A S S E T A L L O C AT I O N

I S S U E # 1 1 - M A R C H 2 0 1 4L Y X O R R E S E A R C H

17 >>

CSFB/Tremont indices. They result from the joint venture between Credit Suisse FirstBoston, a leading investment bank, and Tremont Advisor Inc., a financial services companyspecialised in hedge fund consulting. There are 13 indices which correspond to 13 hedge fundstrategies reported in the TASS database. They also propose the Credit Suisse/TremontHedge Fund Index which is a benchmark of the hedge fund industry.

The Morningstar Center for International Securities and Derivatives Markets (CISDM)database has reported the performance of more than 5, 000 live hedge funds, funds of fundsand CTAs since 1994. It was formerly Managed Account Reports (MAR) database whichwas highly recognized by academics. Eleven indices are constructed in this database: CISDMFund of Fund index, eight individual CISDM Hedge Fund Strategy Indices representing themedian performance of relative funds, the CISDM Equal Weighted Hedge Fund Index andCISDM CTA Equal Weighted Index reflecting the average performance of all hedge fundsand CTAs.

The EurekaHedge database was created by ABN Amro and Eurekahedge Fund Advi-sor. This database refers to about 6, 700 funds and 2, 800 funds of funds. Like other dataproviders, they offer a benchmark for the hedge fund industry with the Eureka Hedge FundIndex which is an equally-weighted index. They also build geographical indices for NorthAmerica, Europe, Asia, Latin America and Emerging Markets. More recently, they haveproposed indices for UCITS hedge funds, long-only absolute return funds and funds of funds.

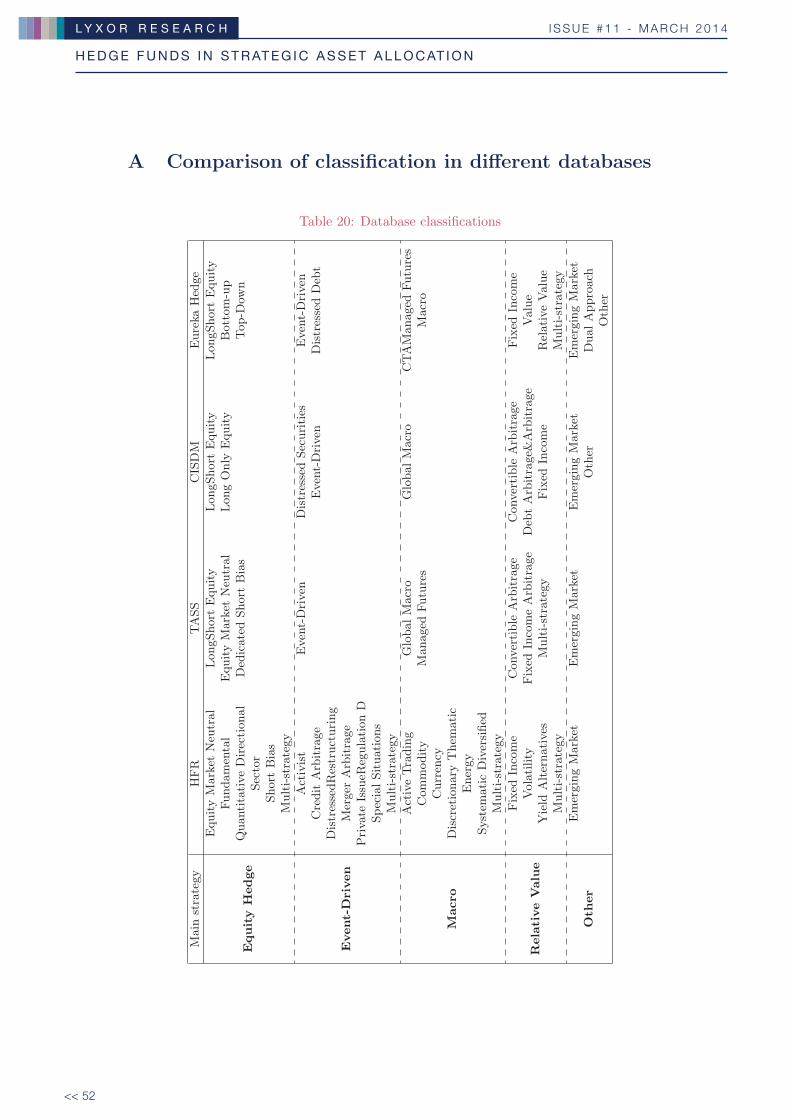

As mentioned above, each data provider is in possession of its own database and itspersonalized benchmarks. Qualitative classification methods vary from one database toanother and depends completely on the interpretation of each data provider. In Table 20in Appendix A, we present strategies and sub-strategies classified in the databases of HFR,TASS, CISDM and Eurekahedge and try to match their classifications for a better overview.All hedge funds are classified in four main strategies: Equity Hedge, Event-Driven, Macroand Relative Value. The Equity Hedge strategy corresponds to an investment strategy withlong and short positions in equity or equity derivatives securities. The Event-Driven strategytakes positions on companies concerned by corporate events. The Macro strategy runs CTAsor applies macroeconomic analysis to take bets on the major risk factors such as currencies,interest rates, stock indices and commodities. The Relative Value strategy is characterizedby the fact that the manager simultaneously purchases a security expected to appreciateand short sells a related security expected to depreciate.

Despite all the biases mentioned above, hedge fund databases provide a remarkable sourceof information to understand the behavior of hedge funds. In what follows, we decide to usethe HFR database in our study which is the most frequently referenced by investors andpractitioners (Jagannathan et al., 2010, Cumming et al., 2012, Joenvaara and Kosowski,2013, etc.).

2.2 Stylized facts of hedge funds

In this section, we present a comprehensive study of the stylized facts of hedge funds usingthe HFR database from January 2000 to June 2013. We provide basic statistics of hedgefund indices and we illustrate the characteristics on hedge funds such as survivorship bias,abnormal distribution and fat-tail risk, performance persistence, auto-correlation and cross-correlation with traditional assets. In what follows, we facilitate notation by using theabbreviations of the hedge fund indices referenced in Table 2.

713967B_221076 White Paper N°11.indd 17 18/03/14 11:56

H E D G E F U N D S I N S T R AT E G I C A S S E T A L L O C AT I O N

I S S U E # 1 1 - M A R C H 2 0 1 4L Y X O R R E S E A R C H

<< 18

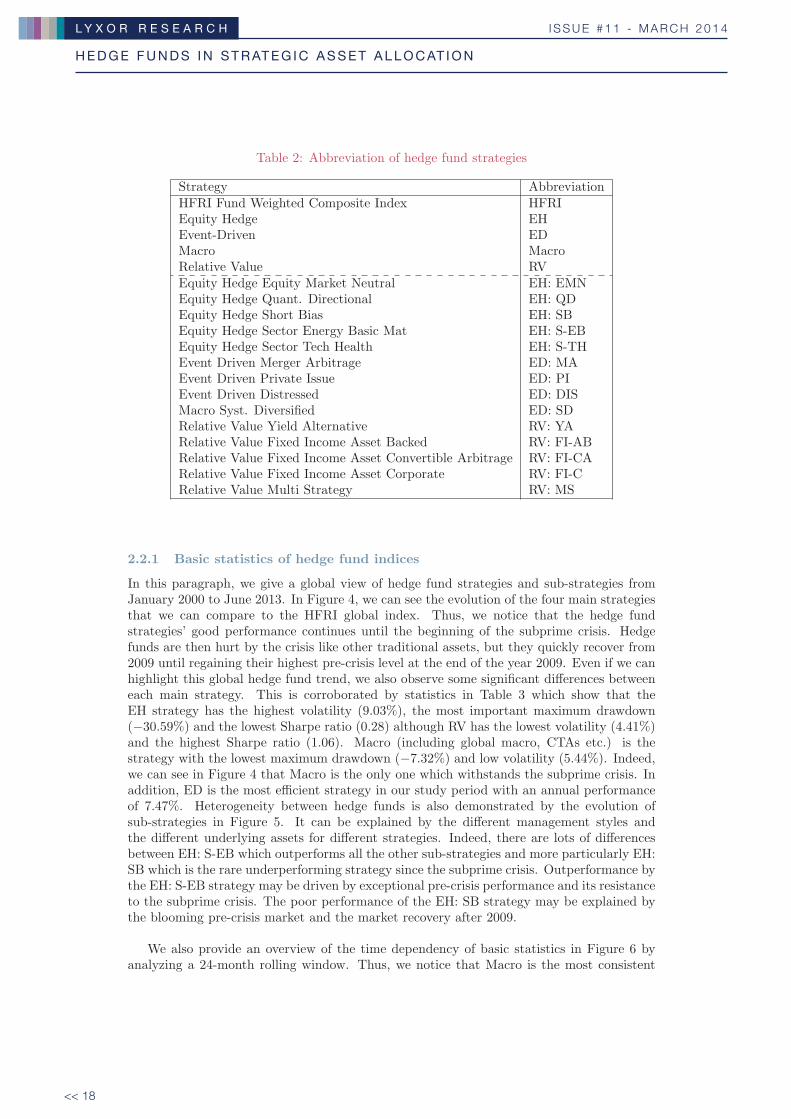

Table 2: Abbreviation of hedge fund strategies

Strategy AbbreviationHFRI Fund Weighted Composite Index HFRIEquity Hedge EHEvent-Driven EDMacro MacroRelative Value RVEquity Hedge Equity Market Neutral EH: EMNEquity Hedge Quant. Directional EH: QDEquity Hedge Short Bias EH: SBEquity Hedge Sector Energy Basic Mat EH: S-EBEquity Hedge Sector Tech Health EH: S-THEvent Driven Merger Arbitrage ED: MAEvent Driven Private Issue ED: PIEvent Driven Distressed ED: DISMacro Syst. Diversified ED: SDRelative Value Yield Alternative RV: YARelative Value Fixed Income Asset Backed RV: FI-ABRelative Value Fixed Income Asset Convertible Arbitrage RV: FI-CARelative Value Fixed Income Asset Corporate RV: FI-CRelative Value Multi Strategy RV: MS

2.2.1 Basic statistics of hedge fund indices

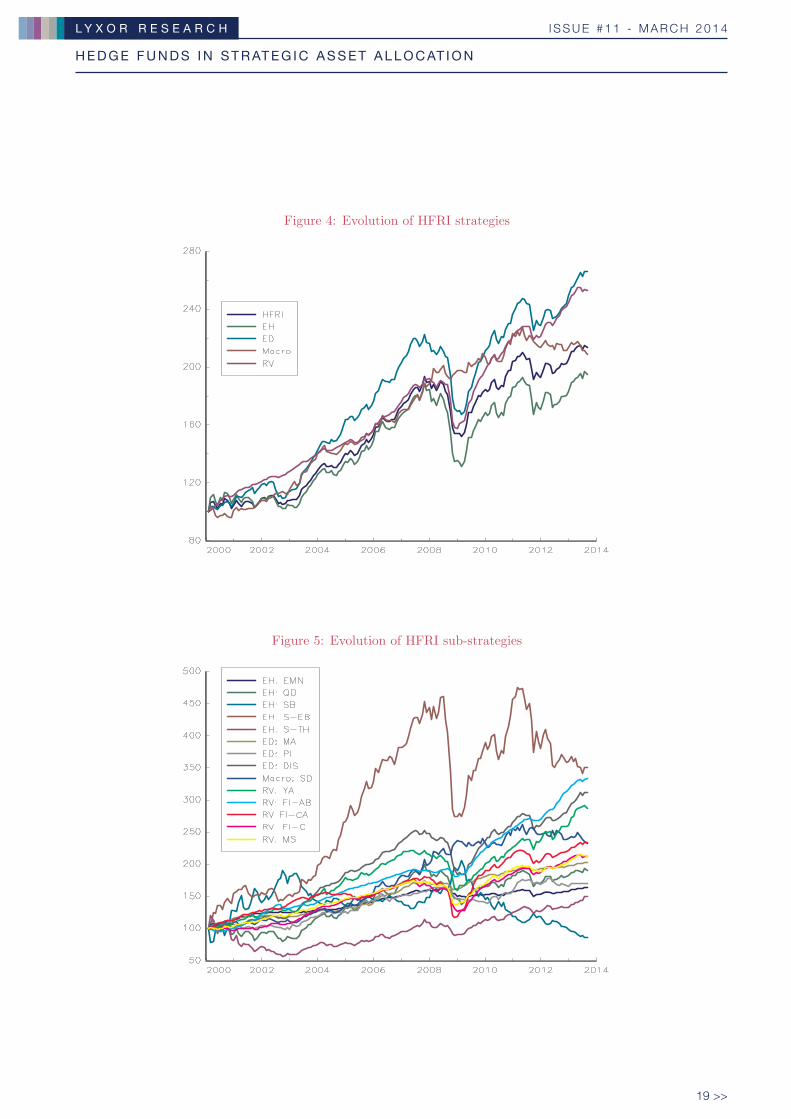

In this paragraph, we give a global view of hedge fund strategies and sub-strategies fromJanuary 2000 to June 2013. In Figure 4, we can see the evolution of the four main strategiesthat we can compare to the HFRI global index. Thus, we notice that the hedge fundstrategies’ good performance continues until the beginning of the subprime crisis. Hedgefunds are then hurt by the crisis like other traditional assets, but they quickly recover from2009 until regaining their highest pre-crisis level at the end of the year 2009. Even if we canhighlight this global hedge fund trend, we also observe some significant differences betweeneach main strategy. This is corroborated by statistics in Table 3 which show that theEH strategy has the highest volatility (9.03%), the most important maximum drawdown(−30.59%) and the lowest Sharpe ratio (0.28) although RV has the lowest volatility (4.41%)and the highest Sharpe ratio (1.06). Macro (including global macro, CTAs etc.) is thestrategy with the lowest maximum drawdown (−7.32%) and low volatility (5.44%). Indeed,we can see in Figure 4 that Macro is the only one which withstands the subprime crisis. Inaddition, ED is the most efficient strategy in our study period with an annual performanceof 7.47%. Heterogeneity between hedge funds is also demonstrated by the evolution ofsub-strategies in Figure 5. It can be explained by the different management styles andthe different underlying assets for different strategies. Indeed, there are lots of differencesbetween EH: S-EB which outperforms all the other sub-strategies and more particularly EH:SB which is the rare underperforming strategy since the subprime crisis. Outperformance bythe EH: S-EB strategy may be driven by exceptional pre-crisis performance and its resistanceto the subprime crisis. The poor performance of the EH: SB strategy may be explained bythe blooming pre-crisis market and the market recovery after 2009.

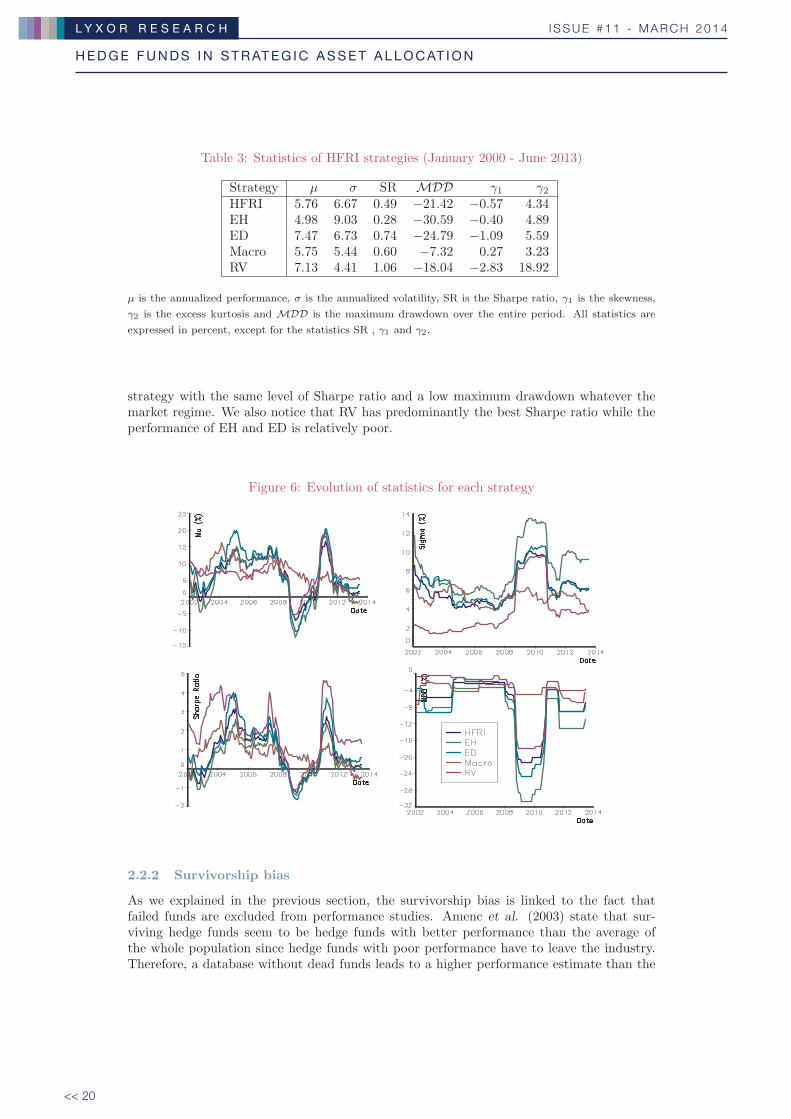

We also provide an overview of the time dependency of basic statistics in Figure 6 byanalyzing a 24-month rolling window. Thus, we notice that Macro is the most consistent

713967B_221076 White Paper N°11.indd 18 18/03/14 11:56

H E D G E F U N D S I N S T R AT E G I C A S S E T A L L O C AT I O N

I S S U E # 1 1 - M A R C H 2 0 1 4L Y X O R R E S E A R C H

19 >>

Figure 4: Evolution of HFRI strategies

Figure 5: Evolution of HFRI sub-strategies

713967B_221076 White Paper N°11.indd 19 18/03/14 11:56

H E D G E F U N D S I N S T R AT E G I C A S S E T A L L O C AT I O N

I S S U E # 1 1 - M A R C H 2 0 1 4L Y X O R R E S E A R C H

<< 20

Table 3: Statistics of HFRI strategies (January 2000 - June 2013)

Strategy μ σ SR MDD γ1 γ2HFRI 5.76 6.67 0.49 −21.42 −0.57 4.34EH 4.98 9.03 0.28 −30.59 −0.40 4.89ED 7.47 6.73 0.74 −24.79 −1.09 5.59Macro 5.75 5.44 0.60 −7.32 0.27 3.23RV 7.13 4.41 1.06 −18.04 −2.83 18.92

μ is the annualized performance, σ is the annualized volatility, SR is the Sharpe ratio, γ1 is the skewness,

γ2 is the excess kurtosis and MDD is the maximum drawdown over the entire period. All statistics are

expressed in percent, except for the statistics SR , γ1 and γ2.

strategy with the same level of Sharpe ratio and a low maximum drawdown whatever themarket regime. We also notice that RV has predominantly the best Sharpe ratio while theperformance of EH and ED is relatively poor.

Figure 6: Evolution of statistics for each strategy

2.2.2 Survivorship bias

As we explained in the previous section, the survivorship bias is linked to the fact thatfailed funds are excluded from performance studies. Amenc et al. (2003) state that sur-viving hedge funds seem to be hedge funds with better performance than the average ofthe whole population since hedge funds with poor performance have to leave the industry.Therefore, a database without dead funds leads to a higher performance estimate than the

713967B_221076 White Paper N°11.indd 20 18/03/14 11:56

H E D G E F U N D S I N S T R AT E G I C A S S E T A L L O C AT I O N

I S S U E # 1 1 - M A R C H 2 0 1 4L Y X O R R E S E A R C H

21 >>

real performance of the hedge fund industry. It is only recently that a few hedge-funddatabases have maintained historical data on dead funds. It is partly for legal reasons andpartly because the primary users of these databases are investors seeking to evaluate existingmanagers they can invest in. In the case where databases contain dead as well as live funds,studies have concluded that the impact of the survivorship bias can be substantial.

Malkiel (1995) and Elton et al. (1996) estimate the survivorship bias for mutual fundsby comparing the difference between average annual performances of all funds and survivingfunds and discover that the survivorship bias is much higher than estimated by Grinblattand Titman (1989). The survivorship bias in hedge funds is usually higher than in mutualfunds because of the higher turnover rate of hedge funds. Survivorship bias in hedge fundsis studied by Ackermann et al. (1999), Park et al. (1999), Brown et al. (1999) and Fung andHsieh (2000) and is estimated to be around 3% per year. Liang (2000) points out that thedifference in estimated survivorship bias is due to the compositional difference of databasesand different study periods. For example, the TASS database has a higher survivorship biasthan the HFR database because it has a default rate that is higher than HFR’s. Ibbotson etal. (2011) provide a more accurate estimate of survivorship bias of 5.13% per year withoutthe backfill data which confirms the high survivorship observed by Aggarwal and Jorison(2010). Eleanor Xu et al. (2011) study survivorship bias using a database from 1994 to 2009but they do not find survivorship bias to be notably significant during the global financialcrisis.

Survivorship bias makes risk management in hedge funds particularly challenging. Lo(2001) shows that although this ”survivorship bias” may not be too extreme for any givenfund, it affects the entire cross-section of funds and its impact is compounded over time inthe returns of each survivor, hence the end result can be enormous for the unwary investorseeking to construct an optimal portfolio of hedge funds.

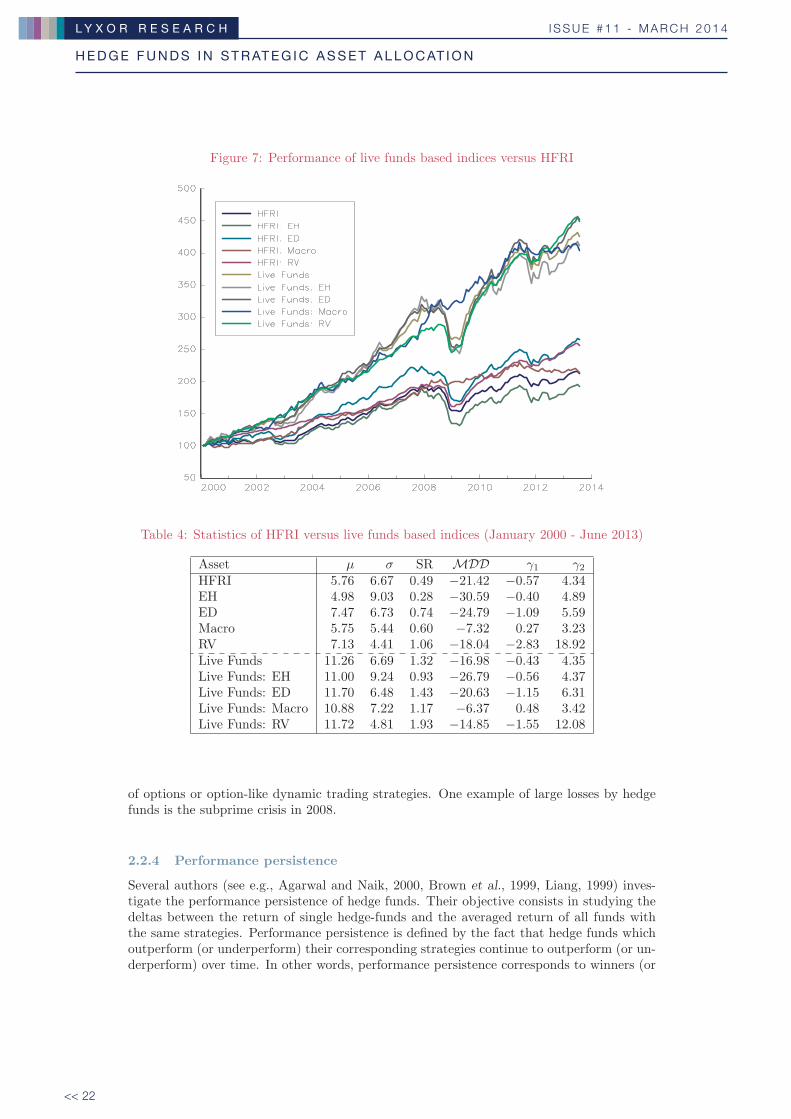

As we have a complete list of live funds in the HFR database at the end of June 2013, weare curious to compare our equally weighted indices of these live funds with HFRI indices.The evolution of equally weighted indices of these live funds compared to HFRI indices isshown in Figure 7. The comparison of their basic statistics is given in Table 4. We observethat, in general, live funds outperform all hedge funds by around 6% which is significantlyhigher than the level estimated using the database before the subprime crisis. Moreover, wealso observe that the performance of HFRI indices is more volatile than live funds. Thesefacts highlight the profound impact of the subprime crisis on the hedge fund industry.

2.2.3 Abnormal distribution and fat tail risk

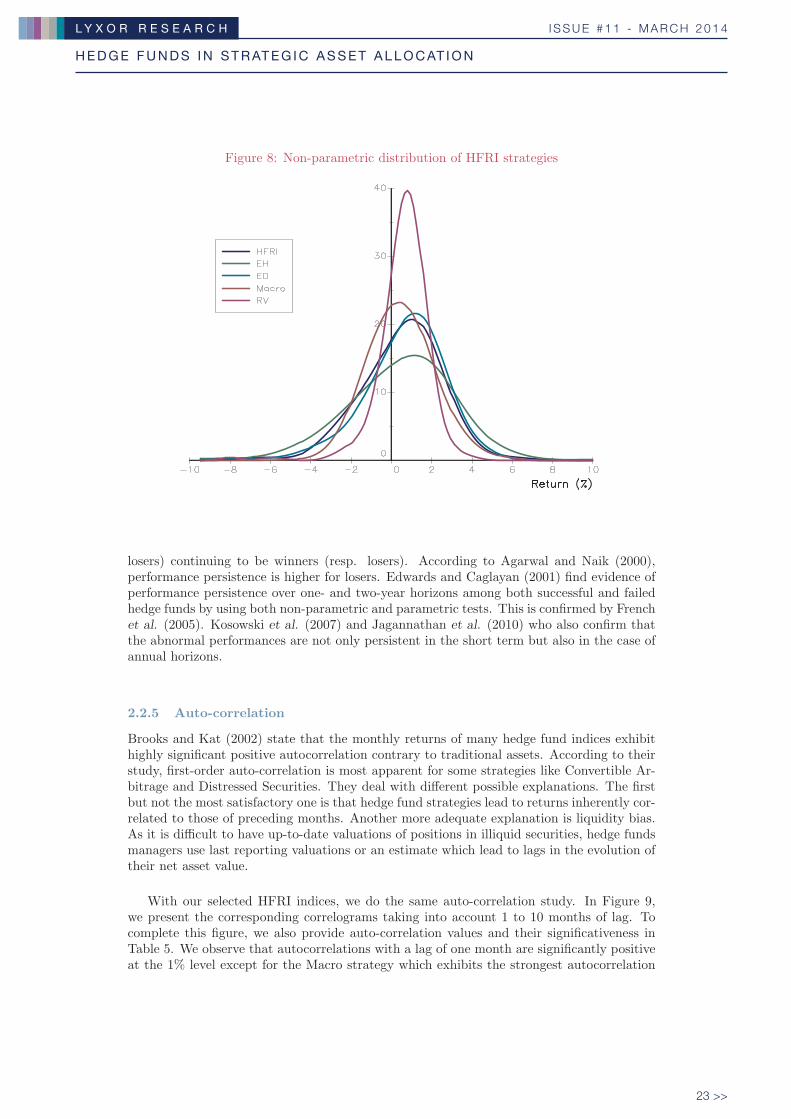

According to Brooks and Kat (2002), any hedge fund strategy return distributions are notnormal and exhibit negative skewness and positive excess kurtosis. According to our basicstatistics previously presented in Table 3, it is especially true for all main strategies, exceptMacro with a skewness of 0.27 and a positive kurtosis of 3.23. Thus, the majority of strategydistributions are leptokurtic with fat left-tails. The probability of having extreme returnsis quite high, especially for negative returns. We confirm this result by estimating thenon-parametric distributions of the annualized returns of the four main sub-strategies. Wepresent them in Figure 8 and we notice that RV is the most leptokurtic strategy, Macroshows an almost normal distribution while ED and EH are characterized by very fat left-tails. These observations are consistent with the skewness and kurtosis statistics presentedearlier. The non-normal payoffs of hedge funds are due to various reasons such as the use

713967B_221076 White Paper N°11.indd 21 18/03/14 11:56

H E D G E F U N D S I N S T R AT E G I C A S S E T A L L O C AT I O N

I S S U E # 1 1 - M A R C H 2 0 1 4L Y X O R R E S E A R C H

<< 22

Figure 7: Performance of live funds based indices versus HFRI

Table 4: Statistics of HFRI versus live funds based indices (January 2000 - June 2013)

Asset μ σ SR MDD γ1 γ2HFRI 5.76 6.67 0.49 −21.42 −0.57 4.34EH 4.98 9.03 0.28 −30.59 −0.40 4.89ED 7.47 6.73 0.74 −24.79 −1.09 5.59Macro 5.75 5.44 0.60 −7.32 0.27 3.23RV 7.13 4.41 1.06 −18.04 −2.83 18.92Live Funds 11.26 6.69 1.32 −16.98 −0.43 4.35Live Funds: EH 11.00 9.24 0.93 −26.79 −0.56 4.37Live Funds: ED 11.70 6.48 1.43 −20.63 −1.15 6.31Live Funds: Macro 10.88 7.22 1.17 −6.37 0.48 3.42Live Funds: RV 11.72 4.81 1.93 −14.85 −1.55 12.08

of options or option-like dynamic trading strategies. One example of large losses by hedgefunds is the subprime crisis in 2008.

2.2.4 Performance persistence

Several authors (see e.g., Agarwal and Naik, 2000, Brown et al., 1999, Liang, 1999) inves-tigate the performance persistence of hedge funds. Their objective consists in studying thedeltas between the return of single hedge-funds and the averaged return of all funds withthe same strategies. Performance persistence is defined by the fact that hedge funds whichoutperform (or underperform) their corresponding strategies continue to outperform (or un-derperform) over time. In other words, performance persistence corresponds to winners (or

713967B_221076 White Paper N°11.indd 22 18/03/14 11:56

H E D G E F U N D S I N S T R AT E G I C A S S E T A L L O C AT I O N

I S S U E # 1 1 - M A R C H 2 0 1 4L Y X O R R E S E A R C H

23 >>

Figure 8: Non-parametric distribution of HFRI strategies

losers) continuing to be winners (resp. losers). According to Agarwal and Naik (2000),performance persistence is higher for losers. Edwards and Caglayan (2001) find evidence ofperformance persistence over one- and two-year horizons among both successful and failedhedge funds by using both non-parametric and parametric tests. This is confirmed by Frenchet al. (2005). Kosowski et al. (2007) and Jagannathan et al. (2010) who also confirm thatthe abnormal performances are not only persistent in the short term but also in the case ofannual horizons.

2.2.5 Auto-correlation

Brooks and Kat (2002) state that the monthly returns of many hedge fund indices exhibithighly significant positive autocorrelation contrary to traditional assets. According to theirstudy, first-order auto-correlation is most apparent for some strategies like Convertible Ar-bitrage and Distressed Securities. They deal with different possible explanations. The firstbut not the most satisfactory one is that hedge fund strategies lead to returns inherently cor-related to those of preceding months. Another more adequate explanation is liquidity bias.As it is difficult to have up-to-date valuations of positions in illiquid securities, hedge fundsmanagers use last reporting valuations or an estimate which lead to lags in the evolution oftheir net asset value.

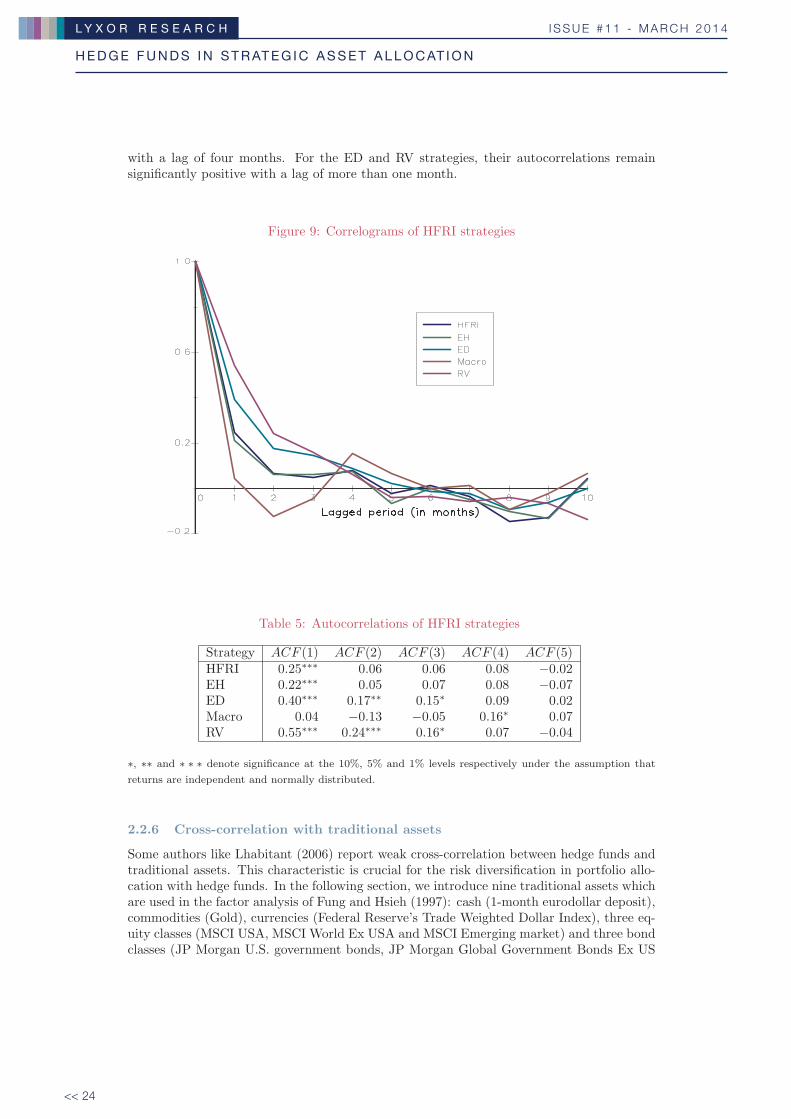

With our selected HFRI indices, we do the same auto-correlation study. In Figure 9,we present the corresponding correlograms taking into account 1 to 10 months of lag. Tocomplete this figure, we also provide auto-correlation values and their significativeness inTable 5. We observe that autocorrelations with a lag of one month are significantly positiveat the 1% level except for the Macro strategy which exhibits the strongest autocorrelation

713967B_221076 White Paper N°11.indd 23 18/03/14 11:56

H E D G E F U N D S I N S T R AT E G I C A S S E T A L L O C AT I O N

I S S U E # 1 1 - M A R C H 2 0 1 4L Y X O R R E S E A R C H

<< 24

with a lag of four months. For the ED and RV strategies, their autocorrelations remainsignificantly positive with a lag of more than one month.

Figure 9: Correlograms of HFRI strategies

Table 5: Autocorrelations of HFRI strategies

Strategy ACF (1) ACF (2) ACF (3) ACF (4) ACF (5)HFRI 0.25∗∗∗ 0.06 0.06 0.08 −0.02EH 0.22∗∗∗ 0.05 0.07 0.08 −0.07ED 0.40∗∗∗ 0.17∗∗ 0.15∗ 0.09 0.02Macro 0.04 −0.13 −0.05 0.16∗ 0.07RV 0.55∗∗∗ 0.24∗∗∗ 0.16∗ 0.07 −0.04

∗, ∗∗ and ∗ ∗ ∗ denote significance at the 10%, 5% and 1% levels respectively under the assumption that

returns are independent and normally distributed.

2.2.6 Cross-correlation with traditional assets

Some authors like Lhabitant (2006) report weak cross-correlation between hedge funds andtraditional assets. This characteristic is crucial for the risk diversification in portfolio allo-cation with hedge funds. In the following section, we introduce nine traditional assets whichare used in the factor analysis of Fung and Hsieh (1997): cash (1-month eurodollar deposit),commodities (Gold), currencies (Federal Reserve’s Trade Weighted Dollar Index), three eq-uity classes (MSCI USA, MSCI World Ex USA and MSCI Emerging market) and three bondclasses (JP Morgan U.S. government bonds, JP Morgan Global Government Bonds Ex US

713967B_221076 White Paper N°11.indd 24 18/03/14 11:56

H E D G E F U N D S I N S T R AT E G I C A S S E T A L L O C AT I O N

I S S U E # 1 1 - M A R C H 2 0 1 4L Y X O R R E S E A R C H

25 >>

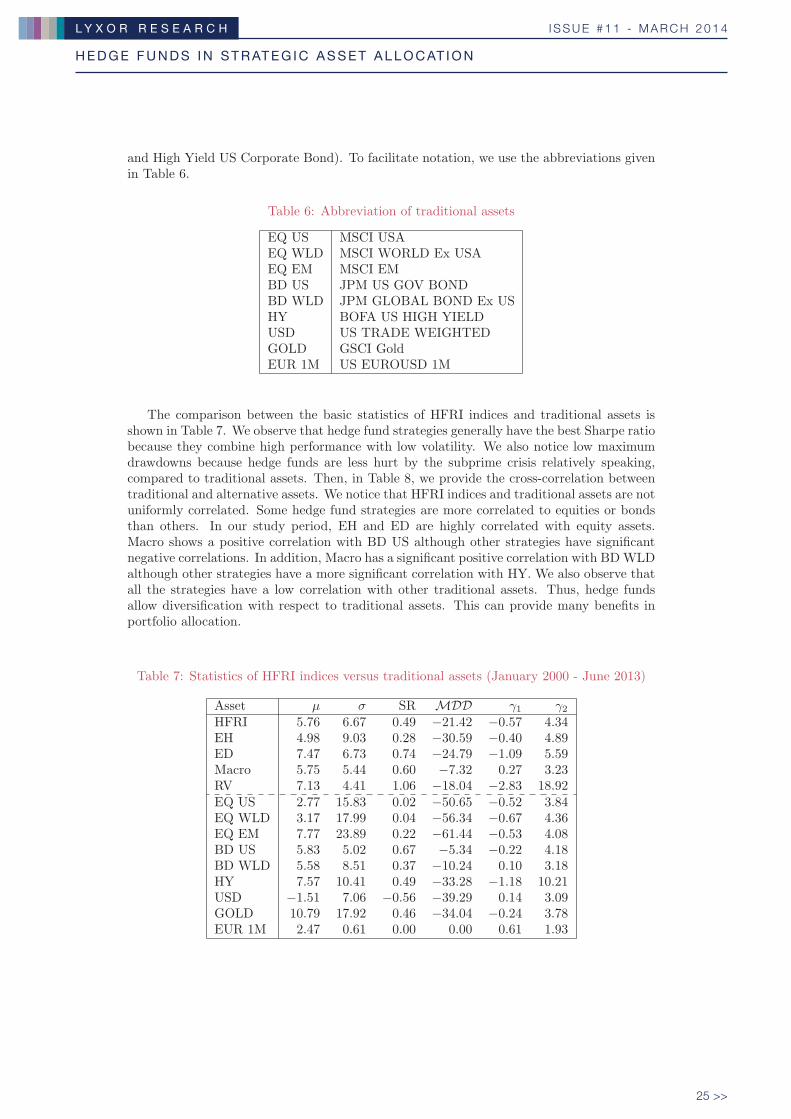

and High Yield US Corporate Bond). To facilitate notation, we use the abbreviations givenin Table 6.

Table 6: Abbreviation of traditional assets

EQ US MSCI USAEQ WLD MSCI WORLD Ex USAEQ EM MSCI EMBD US JPM US GOV BONDBD WLD JPM GLOBAL BOND Ex USHY BOFA US HIGH YIELDUSD US TRADE WEIGHTEDGOLD GSCI GoldEUR 1M US EUROUSD 1M

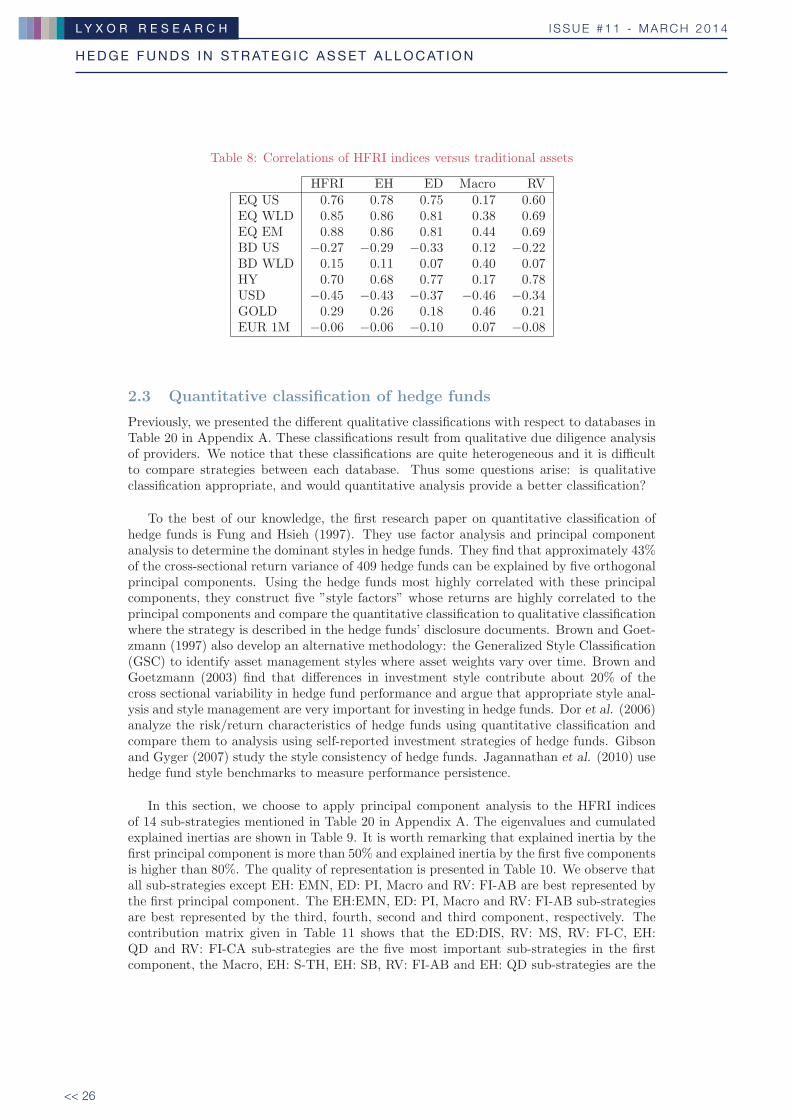

The comparison between the basic statistics of HFRI indices and traditional assets isshown in Table 7. We observe that hedge fund strategies generally have the best Sharpe ratiobecause they combine high performance with low volatility. We also notice low maximumdrawdowns because hedge funds are less hurt by the subprime crisis relatively speaking,compared to traditional assets. Then, in Table 8, we provide the cross-correlation betweentraditional and alternative assets. We notice that HFRI indices and traditional assets are notuniformly correlated. Some hedge fund strategies are more correlated to equities or bondsthan others. In our study period, EH and ED are highly correlated with equity assets.Macro shows a positive correlation with BD US although other strategies have significantnegative correlations. In addition, Macro has a significant positive correlation with BDWLDalthough other strategies have a more significant correlation with HY. We also observe thatall the strategies have a low correlation with other traditional assets. Thus, hedge fundsallow diversification with respect to traditional assets. This can provide many benefits inportfolio allocation.

Table 7: Statistics of HFRI indices versus traditional assets (January 2000 - June 2013)

Asset μ σ SR MDD γ1 γ2HFRI 5.76 6.67 0.49 −21.42 −0.57 4.34EH 4.98 9.03 0.28 −30.59 −0.40 4.89ED 7.47 6.73 0.74 −24.79 −1.09 5.59Macro 5.75 5.44 0.60 −7.32 0.27 3.23RV 7.13 4.41 1.06 −18.04 −2.83 18.92EQ US 2.77 15.83 0.02 −50.65 −0.52 3.84EQ WLD 3.17 17.99 0.04 −56.34 −0.67 4.36EQ EM 7.77 23.89 0.22 −61.44 −0.53 4.08BD US 5.83 5.02 0.67 −5.34 −0.22 4.18BD WLD 5.58 8.51 0.37 −10.24 0.10 3.18HY 7.57 10.41 0.49 −33.28 −1.18 10.21USD −1.51 7.06 −0.56 −39.29 0.14 3.09GOLD 10.79 17.92 0.46 −34.04 −0.24 3.78EUR 1M 2.47 0.61 0.00 0.00 0.61 1.93

713967B_221076 White Paper N°11.indd 25 18/03/14 11:56

H E D G E F U N D S I N S T R AT E G I C A S S E T A L L O C AT I O N

I S S U E # 1 1 - M A R C H 2 0 1 4L Y X O R R E S E A R C H

<< 26

Table 8: Correlations of HFRI indices versus traditional assets

HFRI EH ED Macro RVEQ US 0.76 0.78 0.75 0.17 0.60EQ WLD 0.85 0.86 0.81 0.38 0.69EQ EM 0.88 0.86 0.81 0.44 0.69BD US −0.27 −0.29 −0.33 0.12 −0.22BD WLD 0.15 0.11 0.07 0.40 0.07HY 0.70 0.68 0.77 0.17 0.78USD −0.45 −0.43 −0.37 −0.46 −0.34GOLD 0.29 0.26 0.18 0.46 0.21EUR 1M −0.06 −0.06 −0.10 0.07 −0.08

2.3 Quantitative classification of hedge funds

Previously, we presented the different qualitative classifications with respect to databases inTable 20 in Appendix A. These classifications result from qualitative due diligence analysisof providers. We notice that these classifications are quite heterogeneous and it is difficultto compare strategies between each database. Thus some questions arise: is qualitativeclassification appropriate, and would quantitative analysis provide a better classification?

To the best of our knowledge, the first research paper on quantitative classification ofhedge funds is Fung and Hsieh (1997). They use factor analysis and principal componentanalysis to determine the dominant styles in hedge funds. They find that approximately 43%of the cross-sectional return variance of 409 hedge funds can be explained by five orthogonalprincipal components. Using the hedge funds most highly correlated with these principalcomponents, they construct five ”style factors” whose returns are highly correlated to theprincipal components and compare the quantitative classification to qualitative classificationwhere the strategy is described in the hedge funds’ disclosure documents. Brown and Goet-zmann (1997) also develop an alternative methodology: the Generalized Style Classification(GSC) to identify asset management styles where asset weights vary over time. Brown andGoetzmann (2003) find that differences in investment style contribute about 20% of thecross sectional variability in hedge fund performance and argue that appropriate style anal-ysis and style management are very important for investing in hedge funds. Dor et al. (2006)analyze the risk/return characteristics of hedge funds using quantitative classification andcompare them to analysis using self-reported investment strategies of hedge funds. Gibsonand Gyger (2007) study the style consistency of hedge funds. Jagannathan et al. (2010) usehedge fund style benchmarks to measure performance persistence.

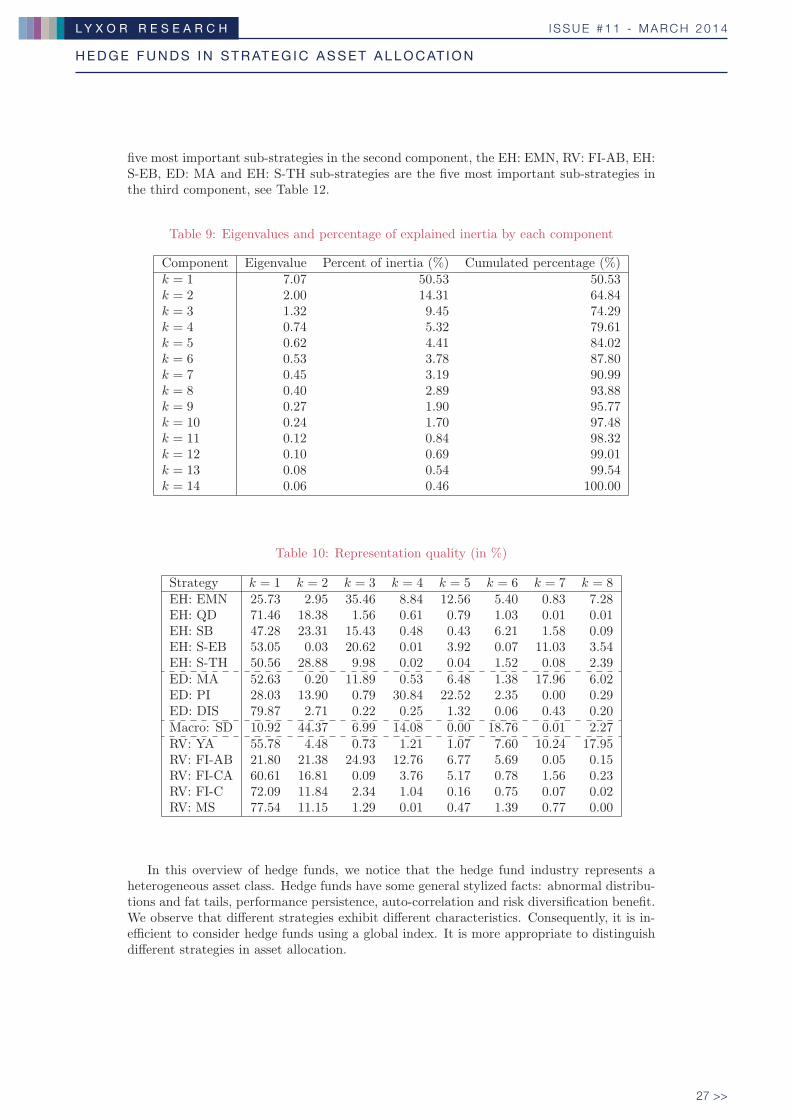

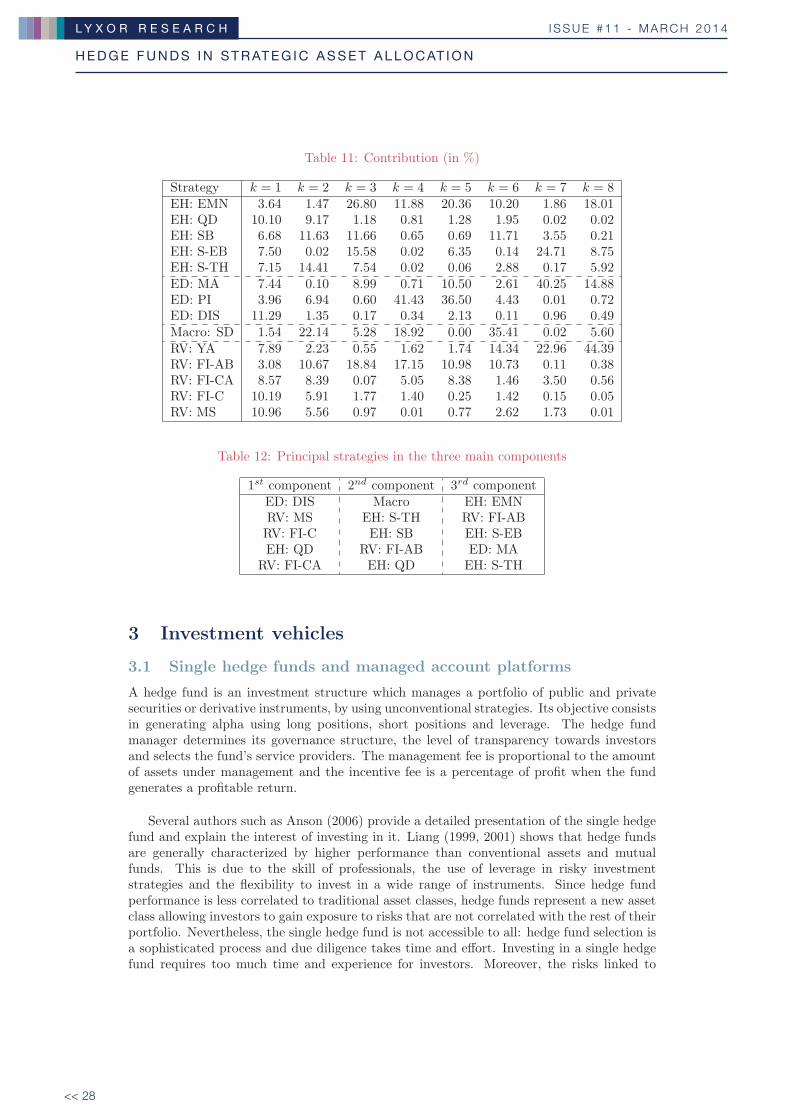

In this section, we choose to apply principal component analysis to the HFRI indicesof 14 sub-strategies mentioned in Table 20 in Appendix A. The eigenvalues and cumulatedexplained inertias are shown in Table 9. It is worth remarking that explained inertia by thefirst principal component is more than 50% and explained inertia by the first five componentsis higher than 80%. The quality of representation is presented in Table 10. We observe thatall sub-strategies except EH: EMN, ED: PI, Macro and RV: FI-AB are best represented bythe first principal component. The EH:EMN, ED: PI, Macro and RV: FI-AB sub-strategiesare best represented by the third, fourth, second and third component, respectively. Thecontribution matrix given in Table 11 shows that the ED:DIS, RV: MS, RV: FI-C, EH:QD and RV: FI-CA sub-strategies are the five most important sub-strategies in the firstcomponent, the Macro, EH: S-TH, EH: SB, RV: FI-AB and EH: QD sub-strategies are the

713967B_221076 White Paper N°11.indd 26 18/03/14 11:56

H E D G E F U N D S I N S T R AT E G I C A S S E T A L L O C AT I O N

I S S U E # 1 1 - M A R C H 2 0 1 4L Y X O R R E S E A R C H

27 >>

five most important sub-strategies in the second component, the EH: EMN, RV: FI-AB, EH:S-EB, ED: MA and EH: S-TH sub-strategies are the five most important sub-strategies inthe third component, see Table 12.

Table 9: Eigenvalues and percentage of explained inertia by each component

Component Eigenvalue Percent of inertia (%) Cumulated percentage (%)k = 1 7.07 50.53 50.53k = 2 2.00 14.31 64.84k = 3 1.32 9.45 74.29k = 4 0.74 5.32 79.61k = 5 0.62 4.41 84.02k = 6 0.53 3.78 87.80k = 7 0.45 3.19 90.99k = 8 0.40 2.89 93.88k = 9 0.27 1.90 95.77k = 10 0.24 1.70 97.48k = 11 0.12 0.84 98.32k = 12 0.10 0.69 99.01k = 13 0.08 0.54 99.54k = 14 0.06 0.46 100.00

Table 10: Representation quality (in %)

Strategy k = 1 k = 2 k = 3 k = 4 k = 5 k = 6 k = 7 k = 8EH: EMN 25.73 2.95 35.46 8.84 12.56 5.40 0.83 7.28EH: QD 71.46 18.38 1.56 0.61 0.79 1.03 0.01 0.01EH: SB 47.28 23.31 15.43 0.48 0.43 6.21 1.58 0.09EH: S-EB 53.05 0.03 20.62 0.01 3.92 0.07 11.03 3.54EH: S-TH 50.56 28.88 9.98 0.02 0.04 1.52 0.08 2.39ED: MA 52.63 0.20 11.89 0.53 6.48 1.38 17.96 6.02ED: PI 28.03 13.90 0.79 30.84 22.52 2.35 0.00 0.29ED: DIS 79.87 2.71 0.22 0.25 1.32 0.06 0.43 0.20Macro: SD 10.92 44.37 6.99 14.08 0.00 18.76 0.01 2.27RV: YA 55.78 4.48 0.73 1.21 1.07 7.60 10.24 17.95RV: FI-AB 21.80 21.38 24.93 12.76 6.77 5.69 0.05 0.15RV: FI-CA 60.61 16.81 0.09 3.76 5.17 0.78 1.56 0.23RV: FI-C 72.09 11.84 2.34 1.04 0.16 0.75 0.07 0.02RV: MS 77.54 11.15 1.29 0.01 0.47 1.39 0.77 0.00

In this overview of hedge funds, we notice that the hedge fund industry represents aheterogeneous asset class. Hedge funds have some general stylized facts: abnormal distribu-tions and fat tails, performance persistence, auto-correlation and risk diversification benefit.We observe that different strategies exhibit different characteristics. Consequently, it is in-efficient to consider hedge funds using a global index. It is more appropriate to distinguishdifferent strategies in asset allocation.

713967B_221076 White Paper N°11.indd 27 18/03/14 11:56

H E D G E F U N D S I N S T R AT E G I C A S S E T A L L O C AT I O N

I S S U E # 1 1 - M A R C H 2 0 1 4L Y X O R R E S E A R C H

<< 28

Table 11: Contribution (in %)

Strategy k = 1 k = 2 k = 3 k = 4 k = 5 k = 6 k = 7 k = 8EH: EMN 3.64 1.47 26.80 11.88 20.36 10.20 1.86 18.01EH: QD 10.10 9.17 1.18 0.81 1.28 1.95 0.02 0.02EH: SB 6.68 11.63 11.66 0.65 0.69 11.71 3.55 0.21EH: S-EB 7.50 0.02 15.58 0.02 6.35 0.14 24.71 8.75EH: S-TH 7.15 14.41 7.54 0.02 0.06 2.88 0.17 5.92ED: MA 7.44 0.10 8.99 0.71 10.50 2.61 40.25 14.88ED: PI 3.96 6.94 0.60 41.43 36.50 4.43 0.01 0.72ED: DIS 11.29 1.35 0.17 0.34 2.13 0.11 0.96 0.49Macro: SD 1.54 22.14 5.28 18.92 0.00 35.41 0.02 5.60RV: YA 7.89 2.23 0.55 1.62 1.74 14.34 22.96 44.39RV: FI-AB 3.08 10.67 18.84 17.15 10.98 10.73 0.11 0.38RV: FI-CA 8.57 8.39 0.07 5.05 8.38 1.46 3.50 0.56RV: FI-C 10.19 5.91 1.77 1.40 0.25 1.42 0.15 0.05RV: MS 10.96 5.56 0.97 0.01 0.77 2.62 1.73 0.01

Table 12: Principal strategies in the three main components

1st component 2nd component 3rd componentED: DIS Macro EH: EMNRV: MS EH: S-TH RV: FI-ABRV: FI-C EH: SB EH: S-EBEH: QD RV: FI-AB ED: MA

RV: FI-CA EH: QD EH: S-TH

3 Investment vehicles

3.1 Single hedge funds and managed account platforms

A hedge fund is an investment structure which manages a portfolio of public and privatesecurities or derivative instruments, by using unconventional strategies. Its objective consistsin generating alpha using long positions, short positions and leverage. The hedge fundmanager determines its governance structure, the level of transparency towards investorsand selects the fund’s service providers. The management fee is proportional to the amountof assets under management and the incentive fee is a percentage of profit when the fundgenerates a profitable return.

Several authors such as Anson (2006) provide a detailed presentation of the single hedgefund and explain the interest of investing in it. Liang (1999, 2001) shows that hedge fundsare generally characterized by higher performance than conventional assets and mutualfunds. This is due to the skill of professionals, the use of leverage in risky investmentstrategies and the flexibility to invest in a wide range of instruments. Since hedge fundperformance is less correlated to traditional asset classes, hedge funds represent a new assetclass allowing investors to gain exposure to risks that are not correlated with the rest of theirportfolio. Nevertheless, the single hedge fund is not accessible to all: hedge fund selection isa sophisticated process and due diligence takes time and effort. Investing in a single hedgefund requires too much time and experience for investors. Moreover, the risks linked to

713967B_221076 White Paper N°11.indd 28 18/03/14 11:56

H E D G E F U N D S I N S T R AT E G I C A S S E T A L L O C AT I O N

I S S U E # 1 1 - M A R C H 2 0 1 4L Y X O R R E S E A R C H

29 >>

hedge funds cover not only traditional risks but also management risk or transparency risk.We can find many studies on these specific risks of hedge funds, for example, Boyson (2003),Foster and Young (2008, 2010).

Remark 1 Investors can invest in exchange quoted hedge fund companies to benefit fromhedge fund performance. Apart from Man Group quoted on the London Stock Exchange since1994, more hedge funds have been quoted on stock exchanges since October 2006, firstly inthe Netherlands, then in the UK and the USA in 2007. The largest funds such as BrevanHoward, Winton Capital, Polygon and Och-Ziff are quoted on stock exchanges based on afraction ranging from 10% to 30% of their capital, see (Teıletche, 2010).

To facilitate the investment in hedge funds, some companies provide investors with amanaged account platform which is an investment structure run by the sponsor (includingthe managed account provider, client and independent board of directors) to manage assetsby using transparent hedge fund exposures. The managed account can be fully customizedto the sponsors’ specific needs and restrictions. All operational aspects are handled by theservice providers chosen by the sponsor of the managed account. The managers are restrictedto managing the investor’s assets with the selected hedge funds. The sponsor chooses in-dependent third-party providers to carry out certain operational tasks such as valuation oraccounting services and is responsible for the operational oversight of the managed account(e.g. risk management, monitoring investment limits, cash management, reporting, legal,compliance, tax, etc.).

Managed accounts have gained great popularity over the last decade or so. The ap-peal of managed accounts lies in easier access to professional managers, a higher degree ofcustomization, better liquidity, greater transparency, more tax efficiencies and stronger anti-fraud ability than single hedge funds. Giraud (2005) argues that, thanks to independentvaluation and risk monitoring, managed account platforms offer a higher level of protec-tion against potential fraudulent activities within a hedge fund structured around a privatepartnership.

3.2 Funds of hedge funds and multi-strategy funds

A fund of hedge funds is an investment vehicle with exposures in several different hedgefunds. Its objective consists in capturing the performance of the hedge fund industry whilehaving better risk diversification than a single hedge fund. To do this, the fund of hedge fundmanager manages the selection of single hedge funds, portfolio construction and portfoliomanagement.

The added value of funds of hedge funds is the selection process used by single hedgefund managers which enables investors to achieve good performance with diversified risks.Due diligence and analysis of risks, correlations and behaviors are essential for the selectionprocess. Liang (1999) argues that funds of hedge funds offer investors greater returns thanmutual funds. Lamm (1999) shows that adding hedge funds to conventional portfoliossignificantly improves a portfolio’s risk-adjusted return performance via diversification andlow correlation with other asset classes. They state that portfolios of hedge funds are inreality a conservative investment and can replace bonds and cash as a defensive vehicle whenequity prices decline. Gregoriou and Rouah (2002) outline the benefits of including hedgefunds and funds of hedge funds in pension fund portfolios.

713967B_221076 White Paper N°11.indd 29 18/03/14 11:56

H E D G E F U N D S I N S T R AT E G I C A S S E T A L L O C AT I O N

I S S U E # 1 1 - M A R C H 2 0 1 4L Y X O R R E S E A R C H

<< 30

A specific fund of hedge funds is the investable hedge fund index fund which selects fundsto deliver the performance of the reference hedge fund index. To construct an investable andliquid index, hedge funds must agree to accept the terms including provisions for redemptionsthat some managers may consider too onerous to be acceptable. Hence, investable hedgefund indices do not represent the total universe of hedge funds.

Recently, some debates has occured on the representability and the eligibility for UCITSIII of investable hedge fund indices. Amenc and Martellini (2003) provide detailed evidenceof strong heterogeneity in the information conveyed by competing indices and attempt toprovide remedies to the problem suggesting a methodology designed to help build a ”purestyle index” or ”index of the indices” for a given style. Martellini et al. (2004) borrowthe concept of factor replicating portfolios from asset pricing literature and apply it to thebenchmarking of hedge fund style returns. Their results suggest that it is actually possibleto construct representative investable indices based on a limited number of funds, exceptperhaps in the case of Equity Market Neutral strategy. Lhabitant (2006) argues that ex-isting investable hedge fund indices are fundamentally different from indices of traditionalassets and they do not fulfil the three basic criteria required to become UCITS III eligible -sufficient diversification, ability to serve as an adequate benchmark and appropriate publi-cation, hence, he suggests excluding existing hedge fund indices from the list of UCITS IIIeligible assets.

In spite of scepticism about their representability, investable hedge fund indices havegrown in numbers over the recent years and are widely available through a number ofproviders, for example, HFR, S&P, FTSE, Dow Jones Credit Suisse (former CS/Tremont),MSCI, etc. Lhabitant (2006) states that assets linked to investable hedge fund indicesexceeded USD 12 billion in 2006. Credit Suisse reports that aggregate assets under man-agement of its investable hedge fund indices totalled to approximately USD 55 billion onAugust 1, 2003.

The fund of hedge funds can be also regarded as a multi-manager fund which mayinvest in a single strategy or multi-strategies. There are also multi-strategy funds whichare special single hedge funds diversifying risks in different strategies and often differentportfolio managers. Normally, multi-strategy funds cost slightly less than funds of hedgefunds but offer less flexibility in portfolio allocation.

3.3 Hedge fund indices replicators

Instead of reflecting the performance of actual hedge fund indices with the most represen-tative exposures, a hedge fund indices replicator uses the statistical approach to replicatehedge fund indices using various investable financial assets. This method makes the indexinvestable and the replicated portfolio can in principle be very representative. A hedgefund indices replicator is built on the research of Hasanhodzic and Lo (2007) who argue thepossibility of creating passive replicating portfolios or clones using liquid exchange-tradedinstruments that provide similar risk exposures at lower cost but greater transparency.

In contrast to traditional investments such as stocks and bonds, hedge-fund returns havemore complex risk exposures that yield additional and complementary sources of risk pre-mium. Amenc et al. (2007) suggest that it is only through the introduction of new adaptedeconometric techniques allowing for a parsimonious statistical estimation of the dynamicand/or non-linear functions relating underlying factors to hedge fund returns that hedge

713967B_221076 White Paper N°11.indd 30 18/03/14 11:56

H E D G E F U N D S I N S T R AT E G I C A S S E T A L L O C AT I O N

I S S U E # 1 1 - M A R C H 2 0 1 4L Y X O R R E S E A R C H

31 >>

fund replication could be turned from an attractive concept into a workable investmentsolution. Amenc et al. (2009) find that going beyond the linear case does not necessarily en-hance replication power and confirm the findings in Hasanhodzic and Lo (2007) who explainthat the performance of the replicating strategies is systematically inferior to that of the ac-tual hedge funds. Giamouridis and Vrontos (2007) find that dynamic covariance/correlationmodels construct portfolios with lower risk and higher out-of-sample risk-adjusted realizedreturn. Roncalli and Teıletche (2007) investigate the implications of substituting standardrolling-window regressions, which appear ad-hoc, with more efficient methodologies such asKalman filter. They show that shortfall risk seems less important than with hedge fundindices and regression-based-trackers and propose a new breakdown of hedge fund perfor-mance into alpha, traditional beta and alternative beta. Cazalet and Roncalli (2011) studythe application of shrinkage methods to improve hedge fund replication.

4 Benefits and risks of hedge funds investments

Hedge funds are entering the mainstream because they introduce a compelling new money-management paradigm which is embraced by many investors. Investors can gain manybenefits from hedge funds that traditional assets cannot offer, for example, significant risk-adjusted return, diversification of risks and better resistance to market environments. Nev-ertheless, we should be aware of the specific risks related to hedge funds investing includingmarket risk or management risk.

4.1 Benefits of hedge funds investments

4.1.1 Significant risk-adjusted return

Investors are always curious about whether hedge funds can offer significant positive returns.In order to answer this question, researchers apply different methods to look into the risk-adjusted return of hedge funds. Ackermann et al. (1999) first use a single-factor modelto estimate the alpha. They study a large data sample from 1988 to 1995 and find thathedge funds consistently outperform mutual funds. Edwards and Caglayan (2001) run amulti-factor model to estimate the risk-adjusted excess returns of hedge funds. By studyinga sample of hedge funds during the 1990-1998 period, they find that hedge funds on averagehave significantly positive excess returns equalling 8.52% annually and these returns have aclose relationship with the type of hedge fund strategies.

Fung and Hsieh (1997) explain that hedge funds often use derivatives and follow dynamictrading strategies. Therefore, the traditional linear method may offer limited help withestimating the performance of hedge funds. In recent studies, researchers begin to includenon-linear exposure to standard asset classes in new models. Fung and Hsieh (2004) use anABS (Asset-Based Style) model similar to the APT (Arbitrage Pricing Theory) risk-factormodel to study the performance of hedge funds. In the ABS model, three trend-followingrisk factors, two equity-oriented risk factors and two bond-oriented risk factors have beenidentified 3. They find that these seven hedge fund risk factors can explain the systematic riskof hedge funds more meaningfully than the traditional linear regression model. In order toinvestigate two major market shocks: the LTCM debacle (September 1998) and the Internet

3According to the recent research of David A. Hsieh, he adds MSCI emerging market index as theemerging market risk factor in the model.

713967B_221076 White Paper N°11.indd 31 18/03/14 11:56

H E D G E F U N D S I N S T R AT E G I C A S S E T A L L O C AT I O N

I S S U E # 1 1 - M A R C H 2 0 1 4L Y X O R R E S E A R C H

<< 32

bubble (March 2000), they split the data period into 3 subperiods: Jan 1994-Sep 1998,Apr 2000-Dec 2002 and Jan 1994-Dec 2002, and find that three hedge fund indices (HFRI,TASSAVG, MSCI) exhibit significant alpha for all sub-periods. Ammann et al. (2011)propose a factor model whose risk factors are selected using a stepwise regression approachand compare it to the factor model proposed by Fung and Hsieh (2004). They estimatethe alpha of hedge funds using a rolling-window regression approach with the Lipper/TASSdatabase over the 1994-2008 period but they do not systematically find the decreasing alphaof hedge funds over time which is reported by Fung et al. (2008) and Zhong (2008) over the1994-2004 period.

In order to solve the difficulties in evaluating the significance and persistence of hedgefund returns, Kosowski et al. (2006) employ a robust bootstrap method and Bayesianapproach which were applied by Busse and Irvine (2006) to mutual funds in order to estimatethe performance of hedge funds. They confirm that the abnormal performance of top hedgefunds cannot be attributed to luck and that abnormal hedge fund performance persists atannual horizons.

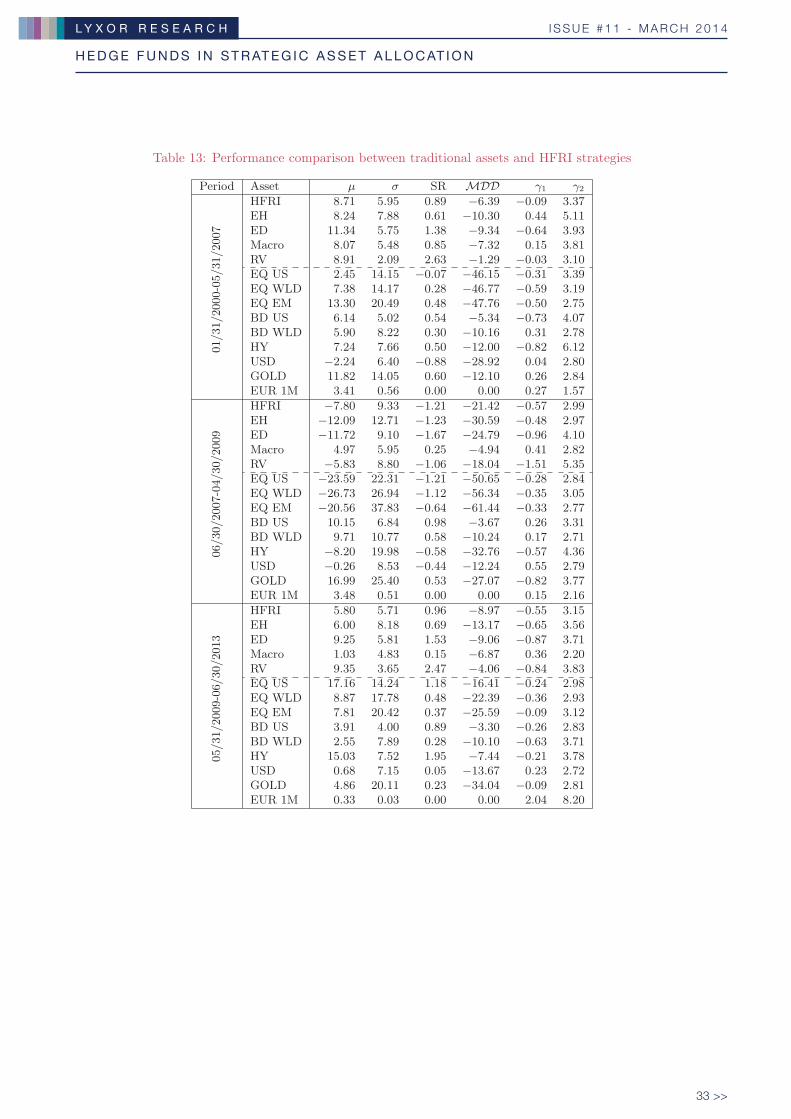

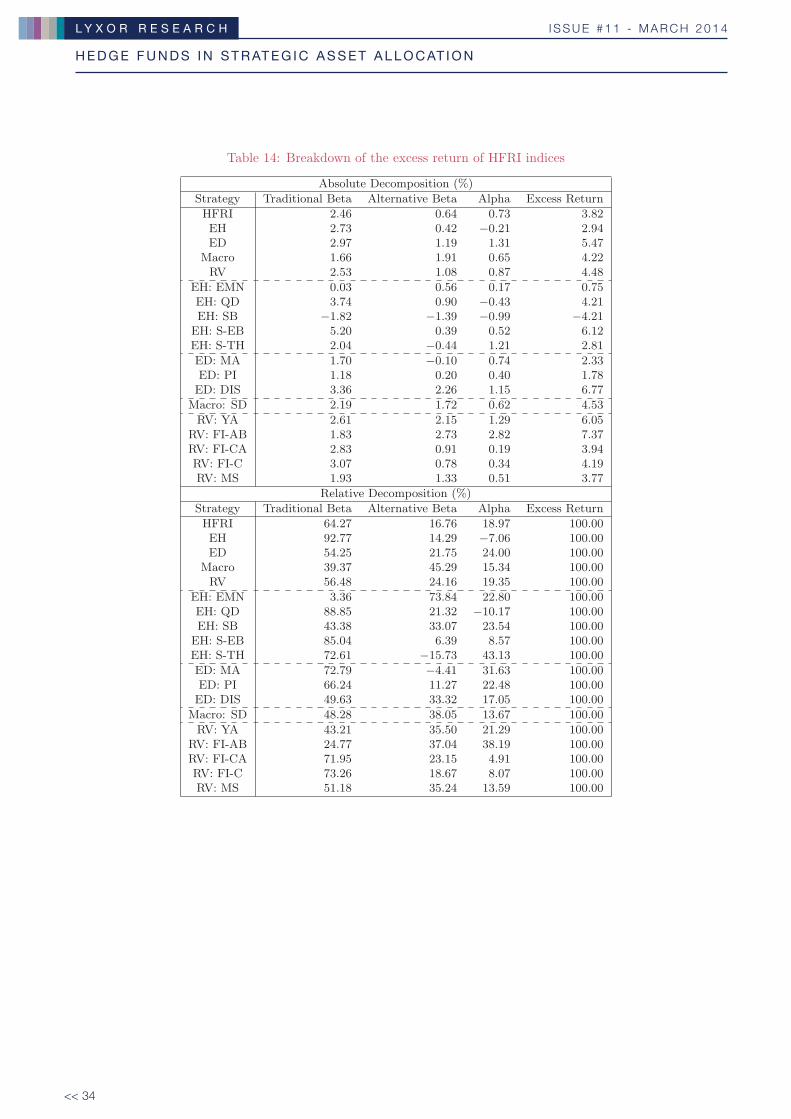

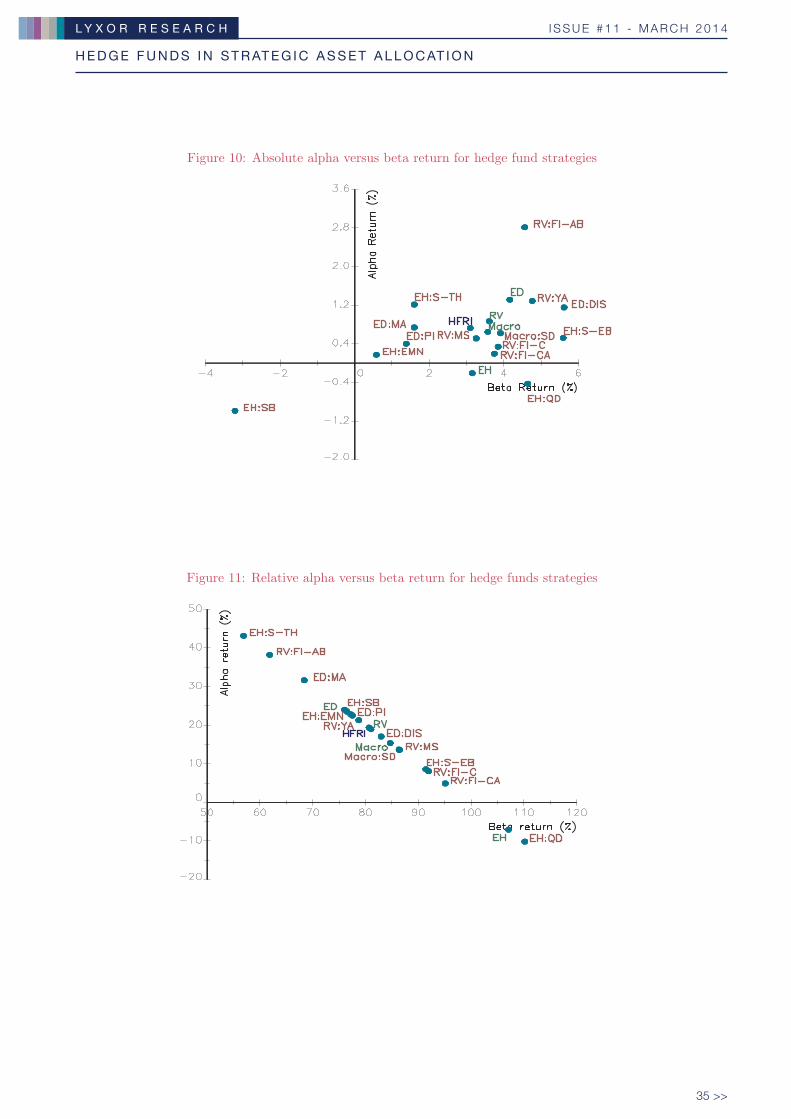

To study the significant risk-adjusted return with HFRI indices, we first compare theperformance of hedge funds during different periods to the nine traditional assets of Fungand Hsieh (1997). We provide the corresponding statistics in Table 13. Before the subprimecrisis, the performance of hedge funds was better than equity and bond performance withhigher returns and lower volatility. However, during the crisis, most hedge funds sufferedmajor losses except for the Macro strategy (including CTA, currency trading, etc.). Althoughhedge funds withstood the crisis better than equities but less well than bonds (except highyield bond), the performance of hedge funds after the crisis is not significantly better thanbefore the crisis but remains attractive to investors since they outperform bonds and exhibitlower volatility than equities. Roncalli and Teıletche (2007) propose breaking hedge fundperformance down into cash, traditional beta, alternative beta and alpha. By applying theirmethod, we show the relative and absolute breakdown of excess returns in Table 14 and weillustrate the results in Figures 10 and 11. We find that the alpha of most hedge funds issignificantly positive. But there are some differences between strategies. Some of them arecharacterized by a high relative percentage of alpha such as EH: S-TH, RV: FI-AB or ED:MA, whereas others display a high level of beta such as EH: QD, RV: FI-CA or RV: FI-C.

4.1.2 Efficient diversification of risks

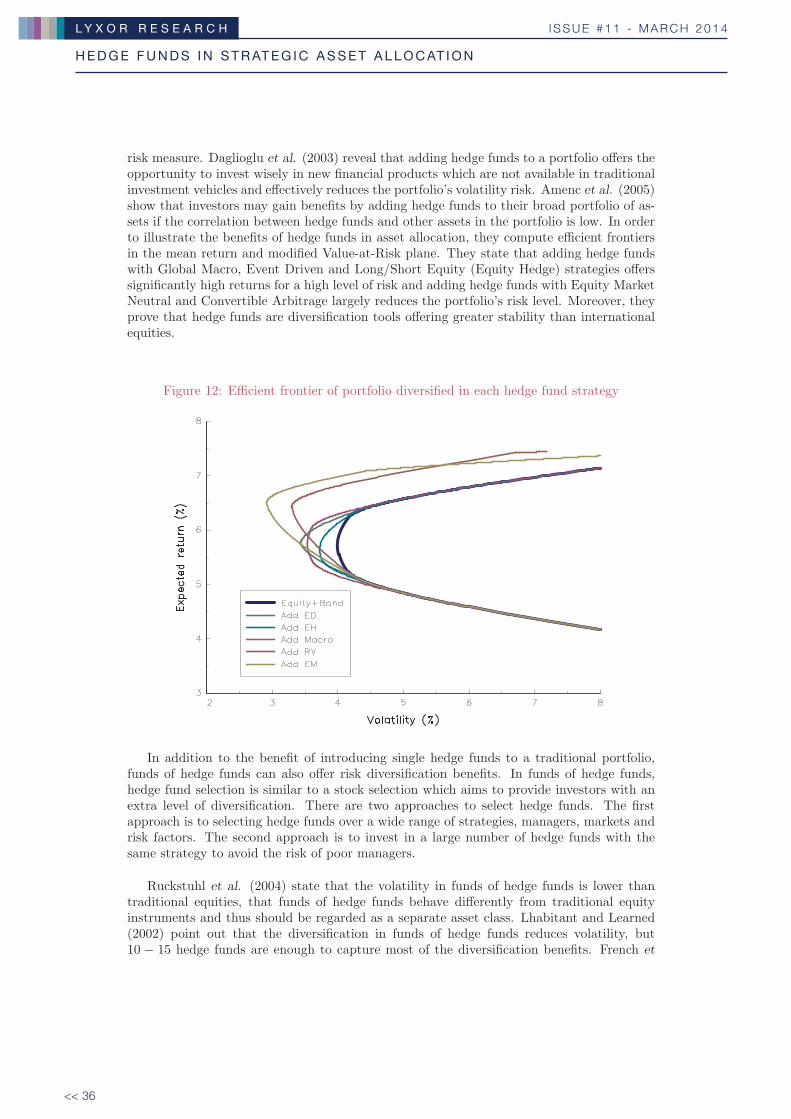

Apart from attractive risk-adjusted returns, hedge funds offer benefits in terms of risk di-versification when added to a traditional portfolio. Liang (1999) shows that hedge fundshave a higher efficiency line than mutual funds, which contradicts the widely held view thathedge funds are risky investments. Signer and Favre (2002) compare most of the existingacademic literature on the benefits of hedge funds in portfolio construction. They find thatthe benefits of hedge funds are justified by a shift in the efficiency line in the mean-varianceenvironment which is a standard process in the traditional portfolio management theory.Using the HFR database and historical data for equities/bonds, we present the shift of theMarkowitz efficient frontier by adding hedge funds to the traditional equity/bond portfolioin Figure 12. We observe that including hedge funds in traditional portfolios improves therisk/return profile. Since most hedge funds always have a significant negative skewness (seeTable 13), some studies introduce new methods to evaluate the benefits of hedge funds moreprecisely. Signer and Favre (2002) propose a new risk measure (Modified Value-at-Risk) andconfirm that adding hedge funds offers benefits in term of risk-adjusted returns with the new

713967B_221076 White Paper N°11.indd 32 18/03/14 11:56

H E D G E F U N D S I N S T R AT E G I C A S S E T A L L O C AT I O N

I S S U E # 1 1 - M A R C H 2 0 1 4L Y X O R R E S E A R C H

33 >>

Table 13: Performance comparison between traditional assets and HFRI strategies

Period Asset μ σ SR MDD γ1 γ2

01/31/2000-05/31/2007

HFRI 8.71 5.95 0.89 −6.39 −0.09 3.37EH 8.24 7.88 0.61 −10.30 0.44 5.11ED 11.34 5.75 1.38 −9.34 −0.64 3.93Macro 8.07 5.48 0.85 −7.32 0.15 3.81RV 8.91 2.09 2.63 −1.29 −0.03 3.10EQ US 2.45 14.15 −0.07 −46.15 −0.31 3.39EQ WLD 7.38 14.17 0.28 −46.77 −0.59 3.19EQ EM 13.30 20.49 0.48 −47.76 −0.50 2.75BD US 6.14 5.02 0.54 −5.34 −0.73 4.07BD WLD 5.90 8.22 0.30 −10.16 0.31 2.78HY 7.24 7.66 0.50 −12.00 −0.82 6.12USD −2.24 6.40 −0.88 −28.92 0.04 2.80GOLD 11.82 14.05 0.60 −12.10 0.26 2.84EUR 1M 3.41 0.56 0.00 0.00 0.27 1.57

06/30/2007-04/30/2009

HFRI −7.80 9.33 −1.21 −21.42 −0.57 2.99EH −12.09 12.71 −1.23 −30.59 −0.48 2.97ED −11.72 9.10 −1.67 −24.79 −0.96 4.10Macro 4.97 5.95 0.25 −4.94 0.41 2.82RV −5.83 8.80 −1.06 −18.04 −1.51 5.35EQ US −23.59 22.31 −1.21 −50.65 −0.28 2.84EQ WLD −26.73 26.94 −1.12 −56.34 −0.35 3.05EQ EM −20.56 37.83 −0.64 −61.44 −0.33 2.77BD US 10.15 6.84 0.98 −3.67 0.26 3.31BD WLD 9.71 10.77 0.58 −10.24 0.17 2.71HY −8.20 19.98 −0.58 −32.76 −0.57 4.36USD −0.26 8.53 −0.44 −12.24 0.55 2.79GOLD 16.99 25.40 0.53 −27.07 −0.82 3.77EUR 1M 3.48 0.51 0.00 0.00 0.15 2.16

05/31/2009-06/30/2013

HFRI 5.80 5.71 0.96 −8.97 −0.55 3.15EH 6.00 8.18 0.69 −13.17 −0.65 3.56ED 9.25 5.81 1.53 −9.06 −0.87 3.71Macro 1.03 4.83 0.15 −6.87 0.36 2.20RV 9.35 3.65 2.47 −4.06 −0.84 3.83EQ US 17.16 14.24 1.18 −16.41 −0.24 2.98EQ WLD 8.87 17.78 0.48 −22.39 −0.36 2.93EQ EM 7.81 20.42 0.37 −25.59 −0.09 3.12BD US 3.91 4.00 0.89 −3.30 −0.26 2.83BD WLD 2.55 7.89 0.28 −10.10 −0.63 3.71HY 15.03 7.52 1.95 −7.44 −0.21 3.78USD 0.68 7.15 0.05 −13.67 0.23 2.72GOLD 4.86 20.11 0.23 −34.04 −0.09 2.81EUR 1M 0.33 0.03 0.00 0.00 2.04 8.20

713967B_221076 White Paper N°11.indd 33 18/03/14 11:56

H E D G E F U N D S I N S T R AT E G I C A S S E T A L L O C AT I O N

I S S U E # 1 1 - M A R C H 2 0 1 4L Y X O R R E S E A R C H

<< 34

Table 14: Breakdown of the excess return of HFRI indices

Absolute Decomposition (%)

Strategy Traditional Beta Alternative Beta Alpha Excess Return

HFRI 2.46 0.64 0.73 3.82EH 2.73 0.42 −0.21 2.94ED 2.97 1.19 1.31 5.47

Macro 1.66 1.91 0.65 4.22RV 2.53 1.08 0.87 4.48

EH: EMN 0.03 0.56 0.17 0.75EH: QD 3.74 0.90 −0.43 4.21EH: SB −1.82 −1.39 −0.99 −4.21

EH: S-EB 5.20 0.39 0.52 6.12EH: S-TH 2.04 −0.44 1.21 2.81

ED: MA 1.70 −0.10 0.74 2.33ED: PI 1.18 0.20 0.40 1.78ED: DIS 3.36 2.26 1.15 6.77

Macro: SD 2.19 1.72 0.62 4.53

RV: YA 2.61 2.15 1.29 6.05RV: FI-AB 1.83 2.73 2.82 7.37RV: FI-CA 2.83 0.91 0.19 3.94RV: FI-C 3.07 0.78 0.34 4.19RV: MS 1.93 1.33 0.51 3.77

Relative Decomposition (%)

Strategy Traditional Beta Alternative Beta Alpha Excess Return

HFRI 64.27 16.76 18.97 100.00EH 92.77 14.29 −7.06 100.00ED 54.25 21.75 24.00 100.00

Macro 39.37 45.29 15.34 100.00RV 56.48 24.16 19.35 100.00

EH: EMN 3.36 73.84 22.80 100.00EH: QD 88.85 21.32 −10.17 100.00EH: SB 43.38 33.07 23.54 100.00

EH: S-EB 85.04 6.39 8.57 100.00EH: S-TH 72.61 −15.73 43.13 100.00

ED: MA 72.79 −4.41 31.63 100.00ED: PI 66.24 11.27 22.48 100.00ED: DIS 49.63 33.32 17.05 100.00

Macro: SD 48.28 38.05 13.67 100.00

RV: YA 43.21 35.50 21.29 100.00RV: FI-AB 24.77 37.04 38.19 100.00RV: FI-CA 71.95 23.15 4.91 100.00RV: FI-C 73.26 18.67 8.07 100.00RV: MS 51.18 35.24 13.59 100.00

713967B_221076 White Paper N°11.indd 34 18/03/14 11:56

H E D G E F U N D S I N S T R AT E G I C A S S E T A L L O C AT I O N

I S S U E # 1 1 - M A R C H 2 0 1 4L Y X O R R E S E A R C H

35 >>

Figure 10: Absolute alpha versus beta return for hedge fund strategies

Figure 11: Relative alpha versus beta return for hedge funds strategies

713967B_221076 White Paper N°11.indd 35 18/03/14 11:56

H E D G E F U N D S I N S T R AT E G I C A S S E T A L L O C AT I O N

I S S U E # 1 1 - M A R C H 2 0 1 4L Y X O R R E S E A R C H

<< 36

risk measure. Daglioglu et al. (2003) reveal that adding hedge funds to a portfolio offers theopportunity to invest wisely in new financial products which are not available in traditionalinvestment vehicles and effectively reduces the portfolio’s volatility risk. Amenc et al. (2005)show that investors may gain benefits by adding hedge funds to their broad portfolio of as-sets if the correlation between hedge funds and other assets in the portfolio is low. In orderto illustrate the benefits of hedge funds in asset allocation, they compute efficient frontiersin the mean return and modified Value-at-Risk plane. They state that adding hedge fundswith Global Macro, Event Driven and Long/Short Equity (Equity Hedge) strategies offerssignificantly high returns for a high level of risk and adding hedge funds with Equity MarketNeutral and Convertible Arbitrage largely reduces the portfolio’s risk level. Moreover, theyprove that hedge funds are diversification tools offering greater stability than internationalequities.

Figure 12: Efficient frontier of portfolio diversified in each hedge fund strategy

In addition to the benefit of introducing single hedge funds to a traditional portfolio,funds of hedge funds can also offer risk diversification benefits. In funds of hedge funds,hedge fund selection is similar to a stock selection which aims to provide investors with anextra level of diversification. There are two approaches to select hedge funds. The firstapproach is to selecting hedge funds over a wide range of strategies, managers, markets andrisk factors. The second approach is to invest in a large number of hedge funds with thesame strategy to avoid the risk of poor managers.

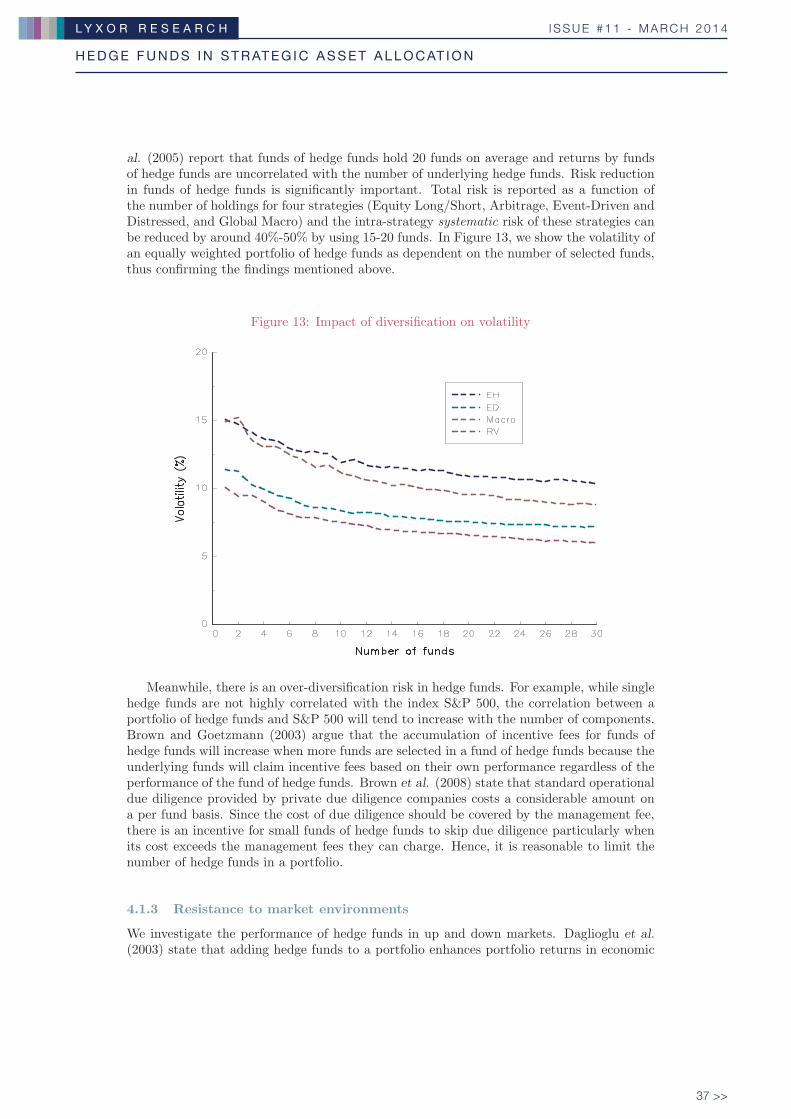

Ruckstuhl et al. (2004) state that the volatility in funds of hedge funds is lower thantraditional equities, that funds of hedge funds behave differently from traditional equityinstruments and thus should be regarded as a separate asset class. Lhabitant and Learned(2002) point out that the diversification in funds of hedge funds reduces volatility, but10 − 15 hedge funds are enough to capture most of the diversification benefits. French et

713967B_221076 White Paper N°11.indd 36 18/03/14 11:56

H E D G E F U N D S I N S T R AT E G I C A S S E T A L L O C AT I O N

I S S U E # 1 1 - M A R C H 2 0 1 4L Y X O R R E S E A R C H

37 >>