Embed Size (px)

Citation preview

The Somh AfriCtlulustitllte ofClllIrtered ACCOIIl/tllut... Circular ../2007(Replacing 11/2006)

GUIDELINE ON FEES FOR AUDITSDONE ON BEHALF OF THEAUDITOR-GENERAL

The A uditor-General has confirmed that the charge out rates set out in the .0Iannexure to this circular are considered to be appropriate for audit workperf0n11ed by members on behalf of the Auditor-General. These ratesapply from I April 2007 to 3 I March 2008.

The Auditor-General determined these rates after consultation with the .02

Standing Committee on the Auditor-General (SCoAG). In addition, whendiscussing the rates with the Auditor-General, representatives of theSouth African Institute of Chartered Accountants (SAICA) takecognisance of the state of the economy Government's Budgetary Policy,and the steps taken by Government to contain the rate of inflation.

The revised scale stal1s with an hourly rate of R69 (2006: R66) for .03monthly earnings of R2 500 (2006: R2 500) and includes rates formonthly earnings of .lIp to R50 000 (2006: R50 000). The. rate formonthly earnings of R50 000 is R I 308 (2006: Rr 258) The rate forpartners has been increased from RI 321 to RI 374 per hour and forspecialists from R I 387 to R I 442 per hour.

Rates are calculated by dividing the monthly earnings by recoverable .04hours and multiplying by a factor of 2.75 (2006: 2.75) to accommodateoverhead costs. The recoverable hours factor in the increasing trainingrequirements. The rate per category continues to be calculated using themidpoint of the earnings.

Fees should be based on the time spent on audits. Time records should be .05kept for individualstaff or grades of staff and should indicate the actualtime spent on the audit. Where fee estimatesare given to a client, suchestimates should be based on time expected to be spent on audits, on thebasis of past experience. Should it be necessaryto spend more time thanexpected as a result of exceptional circumstances, such as unforeseenproblems requiring additional work to be perfonlled to express anopinion, the Auditor-General should be advised prior to any work beingcarried out. The increase in fees for these circumstances should be

negotiated with the Audit Controller. In the absence of such exceptional

Issued February 2007

CIRCULAR ../2007 FEES/ A UD ITOR-G EN ERA L

circumstances, the increase in fees for the current year as compared to thefees for the previous year, is limited to 10% (2006: 10%).

.06 Members are reminded that invoices to the Auditor-General must be

accompanied by a schedule sening out the monthly earnings category foreach employee. the associated rate and number of hours charged inrespect of that invoice. Supporting schedules sening out the compositionof the monthly eamings category of each employee. in terms of the itemslisted in the annexure, must be available for inspection by the Auditor-General. at members' offices.

.07 Professional liability for a member performing work on behalf of theAuditor-General is limited to a maximum of two (2) times the fees billedfor the specific work.

.08 Members are exh0l1ed to review their audit approaches to ensure that upto date techniques are used so as to reduce to a minimum the time spenton audits. The audit approach should be in line with the IntemationalStandards of Auditing and lake into account the Auditor-Generalguidelines as indicated in Directive 1Notice 544 of 2006. issued 10 April2006. in tenm of the Public Audit Act. However. auditors should carryout their duties free from any restrictions whatsoever.

.09 It is acceptable practice for public sector clients to make interim paymentson account of fees. Such interim fees should not exceed the total fees for

time spent up to the date of rendering the account.

., I0 These rates are only applicable to audit work performed by members onbehalf of the Auditor-General, as they are based on factors existing in thisenvironment. Fees for other work perfonned for government departmentsshould be negotiated directly with the department concerned. -'

JohannesburgFebruary 2007

I S SehooleExecutive President

Issued Febnaary 2007 2

FEES/AUDITOR-GENERAL CIRCULAR ../2007

Annexure

RATES FOR AUDITS DONE ON BEHALF OF THE AUDITOR-GENERALPERIOD: 1 APRIL 2007 TO 31 MARCH 2008RA TES (excluding Value Added Tax)

PARTNERS

SPECIALISTS (maximum)RI 374 per hourR 1 442 per hour

ST AFF

3 Issued February 2007

MONTHLY EARNINGS RATE PER HOURR R

1500 and more 691700 and more 741900 and more 793 100 and more 843300 and more 893500 and more 97:) 800 and more 1044 100 and more 1124400 and more 1214700 and more 1285000 and more 1365300 and more 1445600 and more 1525900 and more 1606200 and more 1686600 and more 1807000 and more 1907400 and more 1927800 and more 1998200 and more 2098600 and more 2189000 and more 2299400 and more 2399800 and more 254

(continuedon page4)

CIRCULAR ../2007 FEES/AUDITOR-GENERAL

d fJ 3)

Fee increases

In the absence of exceptional circumstances, the fees should be in linewith the economic indicators and should not exceed the previous year'sfee for comparativework by more than ]0% (2006: -10%). Before thecommencement of the audit, auditors should perform the normal riskassessment to detennine whether there have been any changes in the riskprofile of the client. Where there is a change in the circumstances thatmight affect the audit fee, this change should be discussed with the

Issued February 2007 4

- - -

-0-

MONTHLY EARNINGS RATE PER HOURR R

10600 and more 27411400 and more 29312200 and more 31313 000 and more 33313800 and more 35514600 and more 37415400 and more 39416200 and more 41417000 and more 43417800 and more 45318600 and more 47419400 and more 49420 200 and more 51421000 and more 53421 800 and more 55322 600 and more 57423 400 and more 59424 200 and more 61425 000 and more 6.......).)25 800 and more 68526 600 and more 70627 400 and more 72728 200 and more 76]3a 000 and more 8]732 500 and more 88335 000 and more 94837 500 and more ] 0]440 000 and more 108042500 and more I 14445000 and more 121047500 and more ] 27550 000 and more ] 308

FEES/AUDITOR-GENERAL CIRCULAR ../2007

Auditor-General. All audit fees should be motiv~ted and negotiated withthe Auditor-General prior to any additional work being perfonned.

Monthly earningsMonthly eamings include the total cost of the employee's remunerationpackage and are limited to the following:

. Basic salary;. Travel allowance (as pal1of the salary structure);· Housing allowance/subsidy (as part of the salary structure);· Annual bonus (guaranteed pOl1iononly);· Fringe benefit on the use of a company vehicle (as part of the salarystructure);· Computer allowance, irrespective of whether it is a salary sacrifice ornot. The allowance should not necessarily be included in payslip;. Propol1ionate amount of annual subscriptions payable to SAICAand/or the Independent RegulatOlYBoard for Auditors;. Company contributions to l~ledicalaid fund, pension fund, providentfund, group life insurance and unemployment insurance fund;. Entel1ainment allowance (as part of the salary structure).

Should any unceJ1ainty exist in respect of the composition of employees'packages, the SAICA Project Director - Public Sector should becontacted.

Reimbursement of expensesClaims should comply with the requirements as stipulated in theGuideline on audits conducted 0/1 behalf of the Auditor-General. TheGuideline can be obtained from the Auditor-General.

# 147947

5 Issued Febno31)' 2007

Tile South African institute ofChartcrcd Accollntants Circulnr 11/2006

(Rl:plncing 612006)

GUIDELINE ON FEES FOR AUDITSDONE ON BEHALF OF THEAUDITOR-GENERAL

The Auditor-General has confinned that the charge out rates set out in thc .01annexure to this circular :!fe considered to be appropriate for audit workperfonned by members on bchalfoflhe Auditor-General for 1006/7.

These rates apply from 1 April 2006 1031 March 2007. Members should .02invoice the Audilor-Gem:ral for the difference between the ch3rge outr31esin the annexure and the interim rates in Circular 6/2006 for the workdone IDldbilled for the period from I April 2006 10the date of issu3nce ofthis circular.

It should be noted that the Auditor-Genera] delermines these rates in .03consultation with its Oversight Mechanism. In addition, when discussingthe rJtes with the Auditor-Genera], representatives of the South AfricanInstitute ofCharlered Accountants (SAICA) take cognisance of the stateof the economy, Government's budgetary policy, and the steps taken bygovemmentto contain tJlerate of inflation.

The revised scale starts with an hourly rale of R66 (2005: R62) for .04monthly e3rnings of R2 500 (2005: R2 500) and includes rates formonthly e3mings of up to RSO 000 (2005: R40 OOO). The rate formonthly e3mings of R50 000 is R I 258 (2005: R988 for monthlyearnings of R40 000). The rate for p3rtners has been incrcased fromR I 037 to RI 321 per hour and for specialists from RI 089 to RI 387 perhour.

Rates are calculated by dividing the monthly earnings by recoverable .05hours and multiplying by a factor of 2,75 (2005: 2,70) to accommodateoverhead costs. The recoverable hours have been revised owing to theimpact of the training requirements. The rate per category continues to bec3lcuJated with the midpoint of tJle"earnings.

Fees should be based on the time spent on audits. Time records should be .06kept for individual staff or grades of staff and should indicate the actualtime spent on the audit Where fee estimates are given to a cJient, suchestimates should be based on time expected to be spent on audits, on lhebasis Dfpast experience. Should it be necessary to spend more time than

Is.ued July ~006

CIRCULAR 11/2006 FEES/A UDITOR-GENERAL

expected as a resull 01' exceptional circumstances, such as unforeseenproblems requiring additional work to be performed 10enable the auditor10express an opinion, Ihe Auditor-General should be advised prior 10anywork being calTied oul. The increase in fees for these circumstancesshould be negotiated with the Audit Controller. In the absence of suchexceptional circumstances, the increase in fees for the cUlTent yearincluding the imp3ct of the International Standards of Auditing, ascompared 10 the fees for Ihe previous year, is limited to 10% (2005:10%).

.07 Members are reminded that invoices 10 the Audilor-Generul musl beaccomp;:miedb)' a schedule selling oul Lhemonthly earnings category foreach employee, the assoei31ed rute and number of hours charged inrespect of that invoice. Supporting schedules selting out the compositionof the monthly earnings calegol)' of each employee, in terms ofthe ilemslisted in the m1nCxure,must be available for inspection by the Audilor-General, at members' offices.

.08 Professional liability for a member performing work on behalf of theAuditor-Generul is limited to a ma..'\imumoft\vo (2) times the fees billedfor the specific work.

.09 Members are exhorted to review their audit approaches 10ensure that up10dale techniques 3re used so as to reduce to n minimum the time spenton audiLs. The audit approach should be in line with the InlemationalStandards of Auditing and take inlo account the Auditor-Generalguidelines as indicated in Directive) Notice 544 of2006, issued 10April2006, in U~rmsof the Public Audit Act. However, auditors should carl)'ouLtheir duLiesfree from any restricLionswhalsoever.

.)0 It is acceptable pructice for public secLorclienls to make interimpayrncnls on account of fees. Such interim fees should not e.xceed theloilll fees for time spent up to the date of rendering the account.

"sued July 2006 2

FEES! AUDITOR-GENERAL cmCULAR 11/2006

These ro1!esaic.only applicable \0 audit work perfonned by members on .J 1behalr of the Auditor-Generul, as they are based on factors existing in thisenvironment. Fees for other work perfonned for government departmentsshould be negotiated directly with the department concerned.

JohannesburgJuly 2006

I S SehooleExecutive President

3 bsucd July 2006

cmCULAR 1112006 FEES/A UDITOR-GENERAL

AIUlcxure

RATES FOR AUDITS DONE ON BEHALF OF THE AUDITOR-GENERALPEIllOD: 1 APRil.. 2006 TO 31 MARCH 2007RATES (cxcluding Value AdlJed Tax)

PARTNERSSPECIALISTS (ma.,imum)

R I 321 per hourR I 387 per hour

STAFF

4

MONTHLY EARNINGS RATE PER HOURR R

2500 and more 662700 and more 712900 and more 763 100 and more 813300 and more 863500 and more 933800 and more 1004100 and more 1084400 and more 1164700 and more 1235000 and more 1315300 nnd more 1385600 and more 1465900 and more 1546200 and more 1626600 and more 1737000 and more 1837400 and more 1857800 and more 1918200 and more 2018600 and more 2109000 and more 2209400 and more 2309800 and more 244

(continued on page 4)

FEES/AUDITOR-GENERAL CIRCULAR 11/2006

d Ii

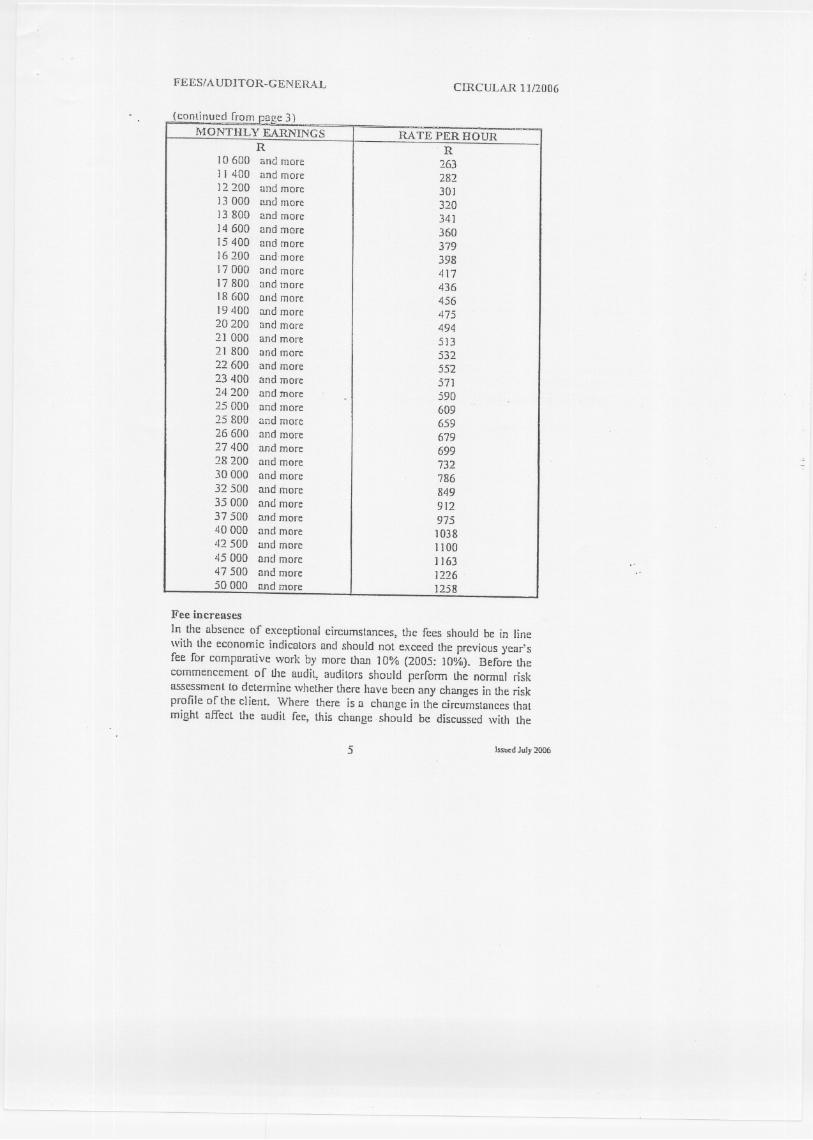

Fee increases

In the absence of exceptional circumstances, the fees should be in linewith the economic indicalors and should not exceed Ihe previous year'sfee for compnrative work by more than ] 0% (2005: 10%). Before thecommencemenL of [he audit., audilors should perform the nonnal riskassessment to determine whether there have been any changes in the riskprofile orLhe client. Where there is a change in the circumstances thaimight affect Ihe audit fec, this change. should be discussed with Lhe

5 IssuedJuJy2006

m -._.., ...t.:._....,

MONTHLY EARNINGS RATE PER HOURR R

10600 and more 26311400 nnd more 282]2200 and more 30]]3000 and more 32013800 and more 34114 600 and more 36015400 and more 37916200 and more 39817000 and more 41717800 and more 43618600 [lndmore 45619400 and more 47520 200 and more 4942] 000 and more 51321800 and more 53222 600 and more 55223400 and more 57124 200 and more . 59025 000 and more 60925 800 nnd more 65926 600 and more 67927 400 and more 69928 200 and more 73230 000 and more 78632 500 and more 84935 000 and more 91237 500 and more 97540 000 and more 103842 500 and more 110045 000 and more ] 16347 500 and more 122650 000 and more 1258

cmcUL..-\.R 11/2006 FEES/AUDITOR-GENERAL

Auditor-General. All audit fees should be mutivated and negotiated withthe Auditor-General prior to any additional work being perfonned.

Monthly enrningsMonthly earnings include the total cost of the employee's remunerationpackagc and are limited to thc following:

· Basic salary;· Travel allowance (as part of the salary structure);. Housing allowance/subsidy (as part of the salary structure);Annual bonus (guarantced portion only);Fringe benefit on the use of a company vehicle (as part of the salarystructure);. Computer allowance, irrespective of whether it is a salary sacrifice ornot. The allowance should not necessarily be included in payslip;. Proportionate amount of annual subscriptions payable to SAICAand/or the Independent Regulatory board for Auditors;· Company contributions to medical aid fund, pension fund, providentfund, group life insurance nnd unemployment insurance fund;· Enterlainment allowance (as part of the salary structure).

Should any uncertainty exist in respect of the composition of employees'packages, the SAICA Project Director - Public Sector should beconlacted.

Reimbursement of expensesClaims should comply with the requirements as stipulated in theGuideline 01/Audits COl/ducted 011Behalf oJ the Auditor-Gel/eral. TheGuideline was updated by the Auditor-General in September 2003 andcan be obtained ITomthe Auditor-General.

Issued July :!0D6 6