Embed Size (px)

Citation preview

APRJ - 699

Applied Project

A Strategic Analysis of

Petroleum Refining Infrastructure in Canada

Wayne Dosman

Coach: Dr. Oliver Mack

Word Count: 19,093

Date Due: March 31, 2013

A Strategic Analysis of Petroleum Refining Infrastructure In Canada

Page 1

Abstract

Canada continues to be economically dependent on refined petroleum products even as

the world moves to constrain their use of fossil fuels. Canada has a long history of

producing more crude oil than we consume however little attention is given to the

strategic importance of the integrated supply network that gathers, transports, refines

and distributes the finished goods. The refining industry in Canada has gone through a

30 year reduction in the number refineries in production and recently various market

anomies have become more pronounced.

This study considers the research question whether this consolidated infrastructure will

be able to meet the future needs of Canadians? I use a qualitative case study format

and publicly available secondary data. The data is analyzed applying three approaches

to strategic management, an industry analysis to captured the industry’s structural

components, a competitive forces analysis that identifies the industry’s dominate forces

and a system dynamics analysis to explore how the system responds to two situations

that occur in the industry.

The industry analysis identifies major elements of the petroleum industry’s structure and

relates these elements to a review of the Canadian industry’s current structure. We

identify four major elements, crude oil slate, mid-stream infrastructure, refinery

configuration and capacity, and product slate demand as elements that structurally

shape the industry. We then review the composition of these elements in Canada’s

refining infrastructure. This review revealed Canada’s refining infrastructure is organized

into four regional supply orbits, each having defining features. These features create

substantially different constraints and requirements for each orbit. Production capacity

shortfalls, product production/demand gaps and significant mid-stream constraints were

identified in two supply orbits.

The competitive forces analysis reviewed the competitive forces surrounding the

downstream refineries which captured crude slate producers as suppliers and refined

product users as buyers. This analysis revealed that the industry’s competitive

structure consists of low buyer and supplier power while refiners possess some

bargaining power under specific mid-stream constraint circumstances. Competitor

rivalry is moderate as although an oligopoly structure exists that is conducive for intense

price competition, the lack of excess capacity and threat of imports limit refiners pricing

power. The threat of new entrants is high as although incumbents enjoy various barriers

to entry, these barriers are mitigated by existing capacity and product shortfalls, and the

diseconomies of scale that exist in certain markets. The threat of substitutes was

A Strategic Analysis of Petroleum Refining Infrastructure In Canada

Page 2

considered moderate as although some substitutes have successfully displaced refined

products in the electricity generation market and to certain extent the home heating

market, access to infrastructure and price performance trade-offs currently leave them

less attractive in the transportation industry. Substitutes are a long run threat however

and could motivate companies to hedge their long run exposure by limiting capacity

acquisitions to meet current needs.

Systems dynamics principals were used to schematically represent the stocks and flows

we identified in the industry and competitive analyses. The industry schematic was then

used to quantitatively examine how the system would response to two situations that

the industry confronts, an unanticipated refinery shut down and whether to acquire

additional capacity. In the refinery shut down situation we found that in supply orbit with

mid-stream constraints, adequate inventory levels were critical to maintaining the

reliability of supply. In orbits with access to deep water ports or waterways, inventory

levels were not as critical as imports could replace production given adequate

transportation time horizons. In the capacity addition decision we found that confidence

in the long run expected return on capital is the crucial determinant in deciding to

acquire capacity. Demand can change much faster than the extended process of adding

capacity and as such industry often overprovides capacity. Adding excessive capacity in

periods of reduced demand can trigger price wars, reducing industry profitability and

possibly leading to periods of closing marginally profitable refineries. As minor capacity

demand shortfalls can be covered by imports, over capacity situations can be more

harmful to industry profitability than under capacity situations.

The study concludes that the Canadian Refining Infrastructure can meet Canada’s

future needs however consideration should be given to three recommendations.

Midstream options should be added to the Western and Ontario supply orbits to reduce

dependence on existing midstream pipelines. A strategic petroleum reserve of refined

petroleum products should be maintained in supply orbits with constrained midstream

options. Capacity should be added in the Ontario, Western and possibly Quebec orbits

to meet demand expectations however consideration should be given to strategically

located small scale refineries.

A Strategic Analysis of Petroleum Refining Infrastructure In Canada

Page 3

Table of Contents

ABSTRACT .............................................................................................................................................................. 1

TABLE OF FIGURES ................................................................................................................................................. 4

1.0 INTRODUCTION ................................................................................................................................................ 5

1.1 SIGNIFICANCE OF THE CANADIAN REFINING INDUSTRY ................................................................................................... 5

1.2 RESEARCH QUESTIONS ............................................................................................................................................. 7

1.3 RESEARCH DESIGN AND APPROACH ............................................................................................................................ 7

1.4 SCOPE AND ASSUMPTIONS ........................................................................................................................................ 8

2.0 REVIEW OF RELATED THEORY .......................................................................................................................... 9

2.1 INDUSTRY AND COMPETITIVE ANALYSIS ..................................................................................................................... 10

2.2 SYSTEM DYNAMICS ................................................................................................................................................ 12

3.0 ANALYSIS ....................................................................................................................................................... 14

3.1 - INDUSTRY ANALYSIS ............................................................................................................................................. 14

3.2 - COMPETITIVE FORCES ANALYSIS ............................................................................................................................. 53

3.3 - SYSTEM DYNAMICS ANALYSIS ................................................................................................................................ 61

4.0 RECOMMENDATIONS AND CONCLUSIONS ..................................................................................................... 72

REFERENCES ......................................................................................................................................................... 77

APPENDIX 1 – ACRONYMS, UNITS AND CONVERSION FACTORS .......................................................................... 84

A Strategic Analysis of Petroleum Refining Infrastructure In Canada

Page 4

Table of Figures FIGURE 1 - 2009 TOTAL FINAL CONSUMPTION FOR CANADA .............................................................................. 5

FIGURE 2 - REFINING INFRASTRUCTURE SUPPLY NETWORK ............................................................................... 8

FIGURE 3 - DETERMINANTS OF COMPETITIVE FORCES ..................................................................................... 11

FIGURE 4 - PROJECTION OF CANADIAN CRUDE OIL PRODUCTION ..................................................................... 16

FIGURE 5 - PRODUCT YIELDS OF REFINERY CONFIGURATIONS USING HEAVY OIL FEEDSTOCK .......................... 19

FIGURE 6 - EXPECTED YIELD OF A CRACKING REFINERY ................................................................................. 20

FIGURE 7 - CANADIAN DOMESTIC REFINED PRODUCT SALES (2011) ................................................................ 20

FIGURE 8 - CANADIAN DOMESTIC SALES OF RPP 2002 - 2011 ........................................................................ 21

FIGURE 9 - CANADIAN PRODUCT DEMAND ...................................................................................................... 22

FIGURE 10 - MAJOR ELEMENTS OF REFINING SUPPLY NETWORK ..................................................................... 22

FIGURE 11 - REFINERY CAPACITY VERSES NUMBER OF REFINERIES ................................................................ 23

FIGURE 12 - OWNERSHIP OF CANADIAN REFINERY CAPACITY .......................................................................... 24

FIGURE 13 - THROUGHPUT CAPACITY OF CANADIAN REFINERIES ..................................................................... 25

FIGURE 14 - SUMMARY OF CANADIAN REFINED PRODUCTS PRODUCTION IN 2011 ............................................ 26

FIGURE 15 - CANADIAN REFINERY UTILIZATION ............................................................................................... 27

FIGURE 16 - 2011 REGIONAL CAPACITY VERSES DEMAND .............................................................................. 28

FIGURE 17 - CANADIAN SUPPLY ORBITS ......................................................................................................... 29

FIGURE 18 - SUMMARY OF MARITIME REFINED PRODUCTS PRODUCTION IN 2011 (BPD).................................... 30

FIGURE 19- MARITIME REFINERY CONFIGURATIONS CAPACITY ........................................................................ 32

FIGURE 20 - PRODUCT DEMAND MIX CANADA VERSE MARITIME ...................................................................... 33

FIGURE 21 - MARITIME PRODUCT DEMAND ..................................................................................................... 33

FIGURE 22 - SUMMARY OF QUEBEC ORBITS REFINED PRODUCTS PRODUCTION IN 2011 (BPD) ......................... 35

FIGURE 23 – QUEBEC ORBITS CAPACITY ....................................................................................................... 37

FIGURE 24 - CANADA VERSES QUEBEC'S PRODUCT DEMAND MIX ................................................................... 37

FIGURE 25 - QUEBEC PRODUCT DEMAND GROWTH ........................................................................................ 38

FIGURE 26 - QUEBEC'S PRODUCT BALANCE.................................................................................................... 39

FIGURE 27 – SUMMARY OF ONTARIO'S REFINED PRODUCT PRODUCTION IN 2011 (BPD) ................................... 40

FIGURE 28 - ONTARIO ORBIT'S CAPACITY ....................................................................................................... 42

FIGURE 29 - CANADA VERSES ONTARIO'S PRODUCT DEMAND MIX ................................................................... 42

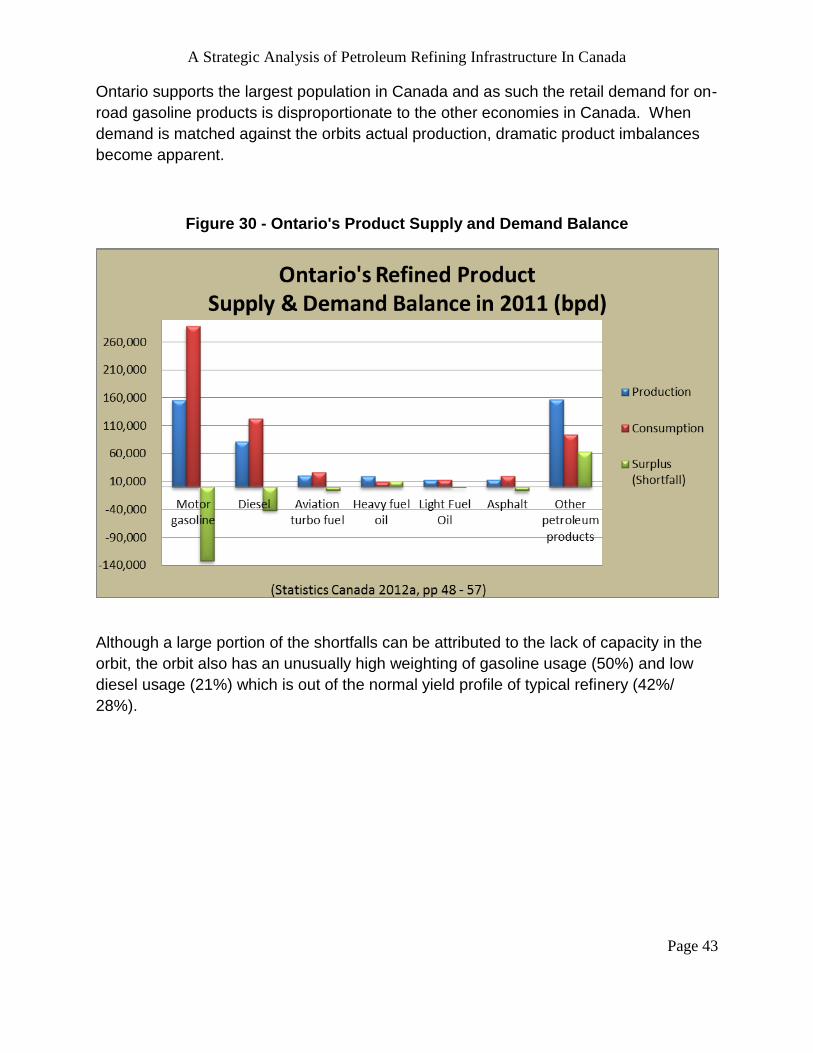

FIGURE 30 - ONTARIO'S PRODUCT SUPPLY AND DEMAND BALANCE ................................................................. 43

FIGURE 31 - ONTARIO'S PRODUCT DEMAND GROWTH ..................................................................................... 44

FIGURE 32 - WESTERN ORBIT'S REFINED PRODUCT PRODUCTION IN 2011 (BPD) ............................................. 45

FIGURE 33 - WESTERN ORBIT CAPACITY ........................................................................................................ 47

FIGURE 34 - CRUDE UPGRADERS CAPACITY ................................................................................................... 48

FIGURE 35 - CANADA VERSES WESTERN'S PRODUCT DEMAND MIX .................................................................. 49

FIGURE 36 - WESTERN'S PRODUCT DEMAND GROWTH ................................................................................... 50

FIGURE 37 - WESTERN'S PRODUCT BALANCE ................................................................................................. 50

FIGURE 38 - SALIENT FEATURES OF SUPPLY ORBITS ...................................................................................... 51

FIGURE 39 - COMPETITIVE FORCES IN THE REFINING INDUSTRY ....................................................................... 60

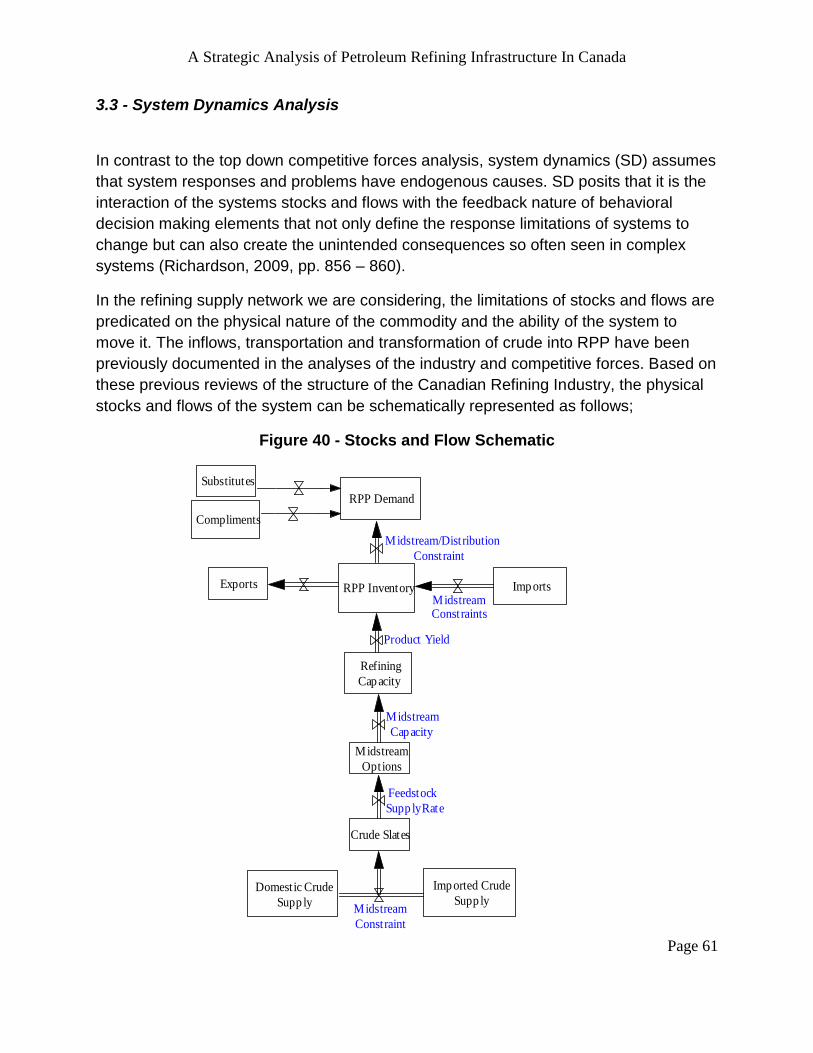

FIGURE 40 - STOCKS AND FLOW SCHEMATIC .................................................................................................. 61

FIGURE 41 - REFINERY SHUTDOWN CAUSAL MAP ........................................................................................... 63

FIGURE 42 - ONTARIO'S ORBIT SHUTDOWN RESPONSE ................................................................................... 65

FIGURE 43 - INVENTORY RESPONSE TO SHUTDOWN ........................................................................................ 65

FIGURE 44 - CAPACITY ACQUISITION CAUSAL MAP .......................................................................................... 67

FIGURE 45 - IMPERIAL OILS DIVISIONAL RETURN ON CAPITAL EMPLOYED ......................................................... 68

A Strategic Analysis of Petroleum Refining Infrastructure In Canada

Page 5

1.0 Introduction

1.1 Significance of the Canadian Refining Industry

In spite of the growing negative sentiment towards products from crude oil being a

major source of greenhouse gas emissions, global energy demand continues to grow

each year and refined petroleum products continues to be the dominate source that

supplies the growing demand for energy.

British Petroleum’s’ (BP) Statistical Review of World Energy estimates global energy

demand grew 2.5% in 2011 which is also approximately equal to the 10 year average

growth in global energy demand (BP, 2012, p. 2). Within the mix of energy sources that

fuel this demand, oil continues to be the dominate source of energy. Even though oil’s

2011 global growth of 600 thousand barrels per day (0.7% growth) was less than the

growth in total energy demand, oil is still the largest energy source in the mix providing

41.3% of the global total final consumption of energy in 2009 (IEA, 2012, p. 28).

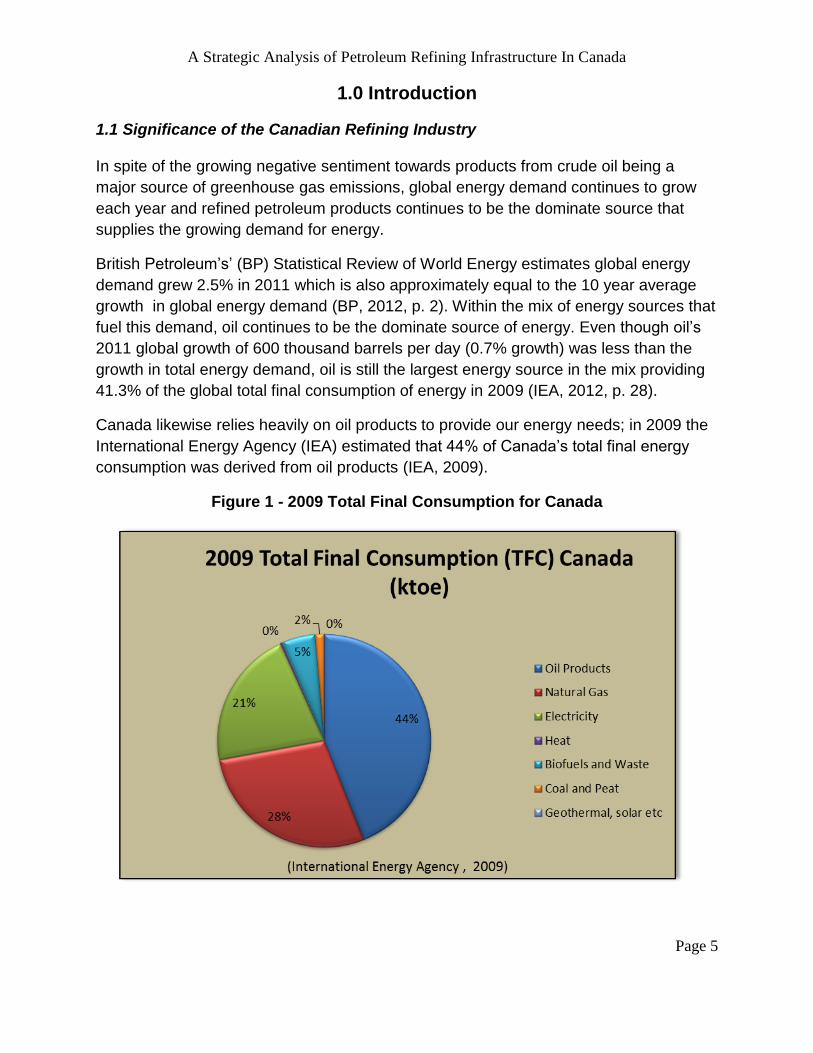

Canada likewise relies heavily on oil products to provide our energy needs; in 2009 the

International Energy Agency (IEA) estimated that 44% of Canada’s total final energy

consumption was derived from oil products (IEA, 2009).

Figure 1 - 2009 Total Final Consumption for Canada

A Strategic Analysis of Petroleum Refining Infrastructure In Canada

Page 6

Canada’s dependence oil products’ is actually growing at a faster rate than our demand

for energy. Over the past ten years, our primary energy consumption increased 8.9%

(Statistics Canada, 2012b) at the same time when oil consumption increased 12.1%

(Statistics Canada, 2012, 2003).

Barring a dramatic increase to the cost of GHG emissions, the worlds’ heavy reliance on

refined petroleum products (RPP) is expected to continue well into the future. Changes

in the global energy mix are slow to change due to the magnitude of the infrastructure

investments currently in place and the higher costs of substitute energy sources.

Canada has a long history of producing more crude oil than it needs’, BP estimated that

in 2011 Canada produced more than 1.2 million barrels of oil per day (bpd) more than it

consumed (BP, 2012a). However, crude oil is of little value itself as it is only after

refining that crude oil in vast quantities that it has an economic use. The use of RPP

permeates every market of the Canadian economy so much that any small disruption

has an immediate and negative cascading effect throughout the economy.

Notwithstanding the economic dependence that the Canadian economy has on RPP,

the industry itself makes a significant value added contribution to domestic production

while providing high paying jobs for the Canadian economy. A 2011 Conference Board

of Canada report estimated that a 10% loss in domestic refining capacity would reduce

GDP by four billion dollars and 38,300 person-years of employment over a five year

period (Conference Board of Canada, 2011, p.31). Given Canada’s economic

dependence on RPP, the production of a secure reliable supply of RPP into the

Canadian marketplace should be managed as a critical strategic resource.

The refining industry in Canada has gone through a 30 year period of reducing the

number of producing refineries even though demand constantly grew. Demand has

been balanced by building larger refineries in fewer locations and increasing throughput

utilization rates. This strategy has resulted in an industry which has historically been

reliable but is highly concentrated in specific locations across Canada. Over the past

ten years, various fundamental changes have emerged in the Petroleum Industry which

has changed the supply and demand dynamics of the North American market. These

changes seem to be manifesting in various market anomalies not previously

experienced:

- Gasoline shortages are becoming more regular occurrences even in oil

rich Western Canada (CBC News, July 28, 2010).

- Despite crude oil being structured as a financial traded global

commodity, large price differentials are developing between

A Strategic Analysis of Petroleum Refining Infrastructure In Canada

Page 7

benchmark oil prices such as West Texas Intermediate (WTI) and

Brent Oil (Sharples, 2012).

- Although Canada produces 1.2 million barrels per day more than they

consume, 40% of the crude oil refined in Canada is imported.

Moreover, imported crude oil is purchased at Brent Oil prices while the

crude that Canada exports is sold at the discounted WTI price or at the

further discounted heavy oil prices like Western Canadian Select

(CAPP, 2012a).

At this point in time, it is unclear whether these events are isolated occurrences or

harbingers of greater events yet to come.

1.2 Research Questions

Bearing in mind economic significance of RPP relative to the changes in concentration

of production infrastructure and the recent appearance of market anomalies this

research paper will explore the following primary question:

Will Canada’s existing Petroleum Refinery Infrastructure meet the future needs of

Canadians?

In pursuing this question, several sub questions and hypotheses arise:

Sub- Question 1) Does Canada’s existing refining infrastructures provide secure,

reliable and efficient production or do these legacy assets present an economic risk?

Hypothesis 1) Refining infrastructure in Canada is a Legacy Cost.

Sub- Question 2) Do large economies of scale refineries provide a more appropriate fit

to Canada’s energy needs than strategically placed smaller scale refineries?

Hypothesis 2) Smaller scale modern refineries located close to major centers can

provide efficient economies to the existing network with less concentration risk.

1.3 Research Design and Approach

The research design will be a qualitative research case study format using reliable

publicly available secondary data (Leedy, 2008, p. 135). The purpose of the research

process will be to resolve the research questions by identifying emergent patterns from

the data being analyzed using three different approaches to strategic management,

those being:

A Strategic Analysis of Petroleum Refining Infrastructure In Canada

Page 8

1) An Industry Analysis Approach.

2) A Competitive Forces Approach.

3) A System Dynamics Approach.

In the Industry Analysis, the existing industry structure will be explored using data

collected from secondary sources for supply, demand, refinery capacity, ownership and

throughput data on the Canadian petroleum refinery industry. This data is available

through various governmental, national and international petroleum agencies

segregated at the national and provincial levels. All sources used will be accessed

through their respective sources websites. The data will be used to identify current

supply and demand balances, identify potential constraints and excesses, and identify

emergent patterns.

We will then use the information and data from the industry analysis section to analyse

the competitive forces that exist in this market and to establish causal relationships that

can be used to build a qualitative causal map model of refinery infrastructure.

1.4 Scope and Assumptions

In considering the scope of the Petroleum Refining Infrastructure, we will establish the

boundaries of the infrastructure to include the availability of the feedstocks, the delivery

systems used to move feedstocks to refineries, refineries, the distribution and marketing

networks of RPP, and the quantities demanded of RPP (Briggs, Tolliver and

Szmerekovsky, 2012, p.2). Throughout this study we will define this chain as the

Petroleum Refining Infrastructure Supply Network (Slack, Chambers & Johnson, 2010,

p. 375).

Figure 2 - Refining Infrastructure Supply Network

In establishing the scope boundaries we will make the following assumptions throughout

this report:

Demand for RPP will not be severely disrupted by innovation

technologies, public policy or changing societal norms other than trends

which currently exist.

A Strategic Analysis of Petroleum Refining Infrastructure In Canada

Page 9

International imports of RPP will not flood global markets with below cost

production from overcapacity and Canadian refineries can profitability

competitive with imports.

Crude slates will continue to be available internationally and domestically

without any unanticipated long run disruptions.

Taxation and government policy changes are material to the refining

industry but have not been considered within this scope.

In setting this scope and making these assumptions, there are material limitations which

could change the current supply and demand determinants:

Factors external to Canada are important and will impact the supply

demand determinants of this industry such as international capacity

additions, crude oil macro-political events, disruptive technologies, or

application of existing technologies in regions not currently employing

them.

Taxing of externalities may dampen demand or reduce energy intensity

resulting in long run demand destruction.

Innovation could make the price/performance trade-off of substitutes more

attractive.

Crude oil slate changes rapidly altering cost curve and mix of light

oil/heavy oil. Upstream activities can alter downstream operations

significantly by pushing volumes of newly discovered oil through the

supply network.

It is the intention of this study to provide a baseline framework based on current trends

and emergent patterns from which such risks and variables external to this study can be

explored.

2.0 Review of Related Theory

Strategy is a far reaching topic and the breath of its academic literature is broad.

Mintzberg, Ahlstrand, and Lampel identify ten schools of strategy that have evolved.

This study will focus on the more traditional school of positioning. The positioning school

relies on a more systematic, analytical approach to problem solving (Mintzberg,

Ahlstrand, and Lampel, 1998). In that regard, the Industry Analysis will detail the refining

A Strategic Analysis of Petroleum Refining Infrastructure In Canada

Page 10

industry’s physical structure and supply/demand balances, Porter’s Five Competitive

Forces will be used to establish the intensity of the industry’s forces and finally we will

use these findings to build a system dynamics model that can be used to qualitatively

examine market situations within the industry.

2.1 Industry and Competitive Analysis

The positioning school argues that industry structure should drive strategy as there

exists’ certain generic strategic positions in each industry which provide a sustainable

competitive advantage. Taking an industry top down perspective, this school developed

sets of analytical tools to match the right strategy to context of the industry and its

competitors. Included in this school is Porters’ theory on competitive analysis,

competitive advantage and the value chain (Mintzberg, Ahlstrand, and Lampel, 1998.

pp. - 94–106) which forms the foundation for much of this school.

The concept that industry structure impacts differences in levels of industry profitability

is rooted in Industrial Organization Economics and the Theories of Monopoly and

Perfect Competition. It has long been observed that industries with a single dominating

firm often generate above average profits and profitability between industries vary

dramatically. Although the macro-environment that businesses operate in have many

important external factors that influence profitability all industries operate in the same

macro environment hence understanding what influences profitability in the industry

environment is an important first step in strategy formation. The balance between

meeting customer demand through the intensity of competition and supplier bargaining

power results a particular level of industry profitability. It is the examination of the

structure of these relationships that gave rise to the positioning school and Porters

theory of competitive forces (Grant, 2008, pp. 66 -71).

It has been argued that an industry’s environment is a minor determinant of a firm

profitability and that inter-firm differences are much greater influence than industry

profitability. Notwithstanding that effect on profitability by industry may be more

diminished than originally thought, industry analysis is still regarded as primary step in

understanding competition and in predicting the effect that changes in an industry will

have on profitability (Grant, 2008, p. 98).

Porter proposes that it is the interactions of five competitive forces that shape the

structure and profitability of any industry. The five forces of competition are Internal

Industry Rivalry, Threat of New Entrants, Treat of Substitutes, Bargaining Power of

Suppliers and the Bargaining Power of Buyers. Competitive forces arise from the

industry’s distinctive economic and technical characteristics and each force has specific

A Strategic Analysis of Petroleum Refining Infrastructure In Canada

Page 11

determinants which govern that forces influence or power on the industry. We have

summarized some of these determinants in the following charts.

Figure 3 - Determinants of Competitive Forces

(Porter, 2008, pp. 80-86).

Porter stresses that it is the interaction of the relative strengths of these forces that

shapes industry profitability. Consequently, it is the strongest competitive forces that are

most important to strategy formation however these prominent influencers are not

always obvious (Porter, 2008, p. 80).

A Strategic Analysis of Petroleum Refining Infrastructure In Canada

Page 12

In understanding the interaction of these forces in an industry, a strategist can identify

opportunities or weaknesses in the industry structure to reposition their competitive

strategies, distinguish short term aberrations from structural market changes or identify

industry-transforming potential (Porter, 2008, pp.88-90).

Porter also cautions that it is important not to mistake industry attributes for competitive

forces. He explains that each industry has specific elements which influence the forces

but in themselves are not forces. Examples of such industry factors are technology,

complementary products, government and growth rate (Porter, 2008, p.86).

It has been argued that Porter’s five force frameworks is too narrow a view of industry

grouping (Grant, 2008, p 98). It has also been argued that where substitutes limit

profitability complements increase industry profitability and often expands an industries

market. Complements are often considered to be a sixth competitive force (Grant, 2008,

p 98).

2.2 System Dynamics

System Dynamics (SD) originated in the 1950’s by Jay Forrester in his seminal paper

“Industrial Dynamics” (Forrester, 1958). As did Michael Porter, Jay Forrester drew on

industrial organization economics and engineering disciplines along with the then recent

computing advances to proposed that industrial stock-flow-feedback designs can be

used to model business management decisions in complex systems using computer

based simulations. He found that such system models explained the unexpected

results often seen in complex systems better than the causal linear explanations in use

at that time.

System dynamics (SD) is a framework to examine the interaction of decisions with a

system structure as it changes over time. SD models look endogenously at a system to

establish causal relationships which can be used to understand how the system

operates and responds to various changes. Systems can be as large as an industry or

an economy or a much smaller grouping such as a firm. Systems are viewed as

bounded causally closed systems with continuous quantities flowing in and out (rates),

supported by various stocks (inventory or levels) that have feedback loops and circular

causal relationships. Exogenous changes are viewed as either causal loops that should

be added to the system or as triggers which modify conditions within the system

resulting in system adaptation. Models can be computer simulations expressing

relationships within the system using coupled, nonlinear, first-order differential

A Strategic Analysis of Petroleum Refining Infrastructure In Canada

Page 13

equations however they can also be expressed schematically using causal maps to

qualitatively capture the interactions between the stocks, flow and causal feedback

structure of the system (Richardson, 2009, pp. 856 -860).

SD is particularly useful in identifying elements within a system that will react to a

change or in identifying a problem and isolating the interaction of physical and

behavioral elements causing the problem. Wolstenholme suggests that successful

system thinking is predicated on being able to see the whole system in context of its

interconnections to the environment. In that regard, he suggests that the establishment

and understanding the boundaries of systems and their linkages to the physical

environment is a critical component to understanding complex systems (Wolstenholme,

2003).

John Sterman indicates that in systems time delayed responses often create oscillations

in matching production with demand. The resulting overshooting or undershooting of

demand can result in instability which explains the cyclical long term expansions and

contractions of certain industries (Sterman, 2000, pp. 791 – 800). In his 1999 MIT

doctoral thesis, Taylor found that long run capacity cycles in the pulp and paper industry

can be explained by capacity acquisition delays that create oscillations in capacity. The

pulp and paper industry shares many similar characteristics with the petroleum industry,

commodity price variations with growth, long supply chains with physical constraints and

capacity is added in large quantities with long capacity acquisition delays. Taylor found

that a four year acquisition delay in capacity lead to short run price and utilization

oscillations within a 14 year long capacity cycle (Sterman, 2000, pp. 824 -828).

SD has a long history of being applied to the dynamic systems of energy markets dating

back to the early 1970’s in the designing of various energy models used by the United

States Department of Energy such as COAL1 & 2, FOSSIL 1 & 2, the IDEAS

(Integrated Dynamic Energy Analysis Simulation) and the DOE’s current model, the

National Energy Model System or NEMS (EIA, 2009; DOE, 1997). All these models

were developed based on academic work by scholars such as Roger Naill, John

Sterman, George Richardson and Eric Wolstenholme, among others, each of which

have a long list of published contributions to SD.

We will use a SD qualitative model to explore the physical structure of the industry and

that systems feedback response to specific changes.

A Strategic Analysis of Petroleum Refining Infrastructure In Canada

Page 14

3.0 Analysis

3.1 - Industry Analysis

An understanding of the factors that influences profitability in any industry starts with

examining the relationship between what customers demand and the competing

interests of industry incumbents, the industry’s suppliers and producers of substitute

goods (Grant, 2008, p. 80). The structure of these relationships can be established by

examining the industry’s supply and demand trends, by identifying trends that are

changing in the industry structure and by reviewing the industry’s existing competitors

(Grant, 2008, p. 81). Analyzing these relevant structural components of supply, demand

and competition in an industry is typically completed concurrent with a competitive

forces analysis however we have separated the industry analysis to capture the

physical SD elements of stocks, flows, capacity and delays that exist in the industry.

To bring forward the information necessary for the competitive forces and SD analysis

we will first review the major elements of the petroleum industry as they relate to

Canadian refining infrastructure and then review the relevant structure of Canadian

Industry.

3.1.1 Major Elements of the Petroleum Industry Structure

The petroleum industry activities have traditionally been segregated into three

segments, the “upstream” exploration and production (E&P) of crude oil, the

“midstream” segment that transports crude oil and RPP, and the “downstream” refining

and marketing segments (Briggs, Tolliver and Szmerekovsky, 2012, p.2).

There are four key elements of this supply network that combine to determine refining

infrastructure efficiency, crude oil slates, midstream transportation options, refinery

configuration and product demand (Natural Resources Canada, 2008, pp. 20-33). We

will discuss the significance of each of these elements separately.

Crude Oil Slate

The slate of available crude oil (crude) provides the feedstock for refineries. Not all

crude is equal in the process of refining oil. Crude is found in varying viscosities and

can have numerous heavy metals and chemicals suspended in the emulsion. The

industry convention it to characterise crude by its viscosity, also referred to as specific

A Strategic Analysis of Petroleum Refining Infrastructure In Canada

Page 15

density or weight, and its sulfur content. Only specific refinery designs (configurations)

can process heavy or light, sweet or sour crude efficiently. Consequently, crude

supplies are segregated by weight and sulfur content and streamed to refineries that are

best suited to their characteristics based on the configuration of the refinery and the

desired yield of products (Natural Resources Canada, 2008, pp. 21-24).

The convention used by the industry to categorize crude oil viscosity is the American

Petroleum Institute’s specific gravity scale measured in degrees API. The industry

refers to light oil as being greater than 30o API, medium oil is between 27o to 30o API

and heavy oil is less than 27o API (CAPP, 2012a, p. 2). In 2011, 29% of the 3 million

barrels of Canadian crude oil production was light or medium weight and 71% was

considered heavy (CAPP, 2012a, p. 37)

Crude oil containing high sulfur content is referred to as “sour” while “sweet” crude has

low sulfur content. Sulfur content is measured as a percentage of the total volume with

sweet oil having a sulfur content of less than or equal to 0.5% and sour being above

0.5% (CAPP, 2012a, p. 2) . Sulfur is undesirable in crude oil as most refined products

are combusted resulting in the sulfur reformulating into the pollutant sulfur dioxide.

Governments continue to increase standards on polluting externalities such as sulfur.

Crude oil containing higher sulfur levels is priced at a discount to offset the additional

processing costs of removing the sulfur. Consequently, refineries are willing to pay more

for light, sweet crude than for sour heavy crude.

There are two major global standards for crude against which other crude oils are

graded and priced. West Texas Intermediate (WTI) is the primary benchmark for US

crude while North Sea Brent Oil (Brent) has become the standard for foreign oil. The

standard characteristics for WTI is an API of 40o and sulfur content of 0.5% or less while

Brent has an API of 37o and a sulfur content of 1.0%. From a refiners cost point of view

Brent should be priced less than WTI as a barrel of Brent requires more desulfurization

and refining to produce the same products as WTI however due to supply spikes from

the US Midwest and increases in Western Canadian production, WTI has traded at a

substantial discount to Brent for the past couple of years. Prior to 2005 Brent traded at a

slight discount to WTI (EIA, 2012a).

In Canada crude oil production is trending towards more heavy oil. Regionally, Western

Canada contributes 91% of all crude oil produced in Canada with the remaining majority

of Eastern Canada’s production found offshore of Atlantic Canada. Western Canadian

production totaled 2,743,000 barrels of crude oil per day in 2011 consisting of 80%

heavy and 20% light oil. Although, much of Western Canada’s production is heavy oil,

approximately 30% of it (705,000 b/d) is upgraded within Western Canada into light

synthetic oil which has refining characteristics similar to light sweet conventional, i.e.

A Strategic Analysis of Petroleum Refining Infrastructure In Canada

Page 16

greater than 30o API and less than 0.5% sulfur. The Canadian Association of

Petroleum Producers 2012 Market Forecast (CAPP, 2012a, p.37) projects growth in

both heavy and light oil production to result in total production of 3,942,000 bpd (61%)

by 2017. The majority of this growth is projected to be in heavy oil production which

CAPP has projected to grow 1,270,000 bpd (69%) over the five years ending in 2017.

Atlantic Canada oil production is light and medium oil and primarily produced offshore.

Production from existing East Coast producing fields is expected to decline by 25% over

the next five years, at which time the offshore heavy oil Hebron field is expected to go

into production to partially offset the light oil declining production (CAPP, 2012a, p. 37).

Figure 4 - Projection of Canadian Crude Oil Production

(CAPP, 2012a, p. 37)

The trend towards more heavy oil production and the asymmetrical distribution of

production across Canada creates significant logistic challenges. A substantial portion

of the oil product demand in Canada comes from Central Canada (Quebec and Ontario)

while almost all production is in the West. Existing refineries in the east are configured

for light oil refining which is the most expensive feedstock. Despite Canada producing

more than a million barrels of crude per day than it consumes, the location of the

production does not align with the location of demand. Consequently, vast quantities of

crude production or RPP need to be physically moved to meet Canada’s daily demand.

A Strategic Analysis of Petroleum Refining Infrastructure In Canada

Page 17

Mid-stream Infrastructure

Crude oil can be transported on land by pipelines, railway cars and trucks or by water

using barges or tanker ships. Inland production of crude oil is collected from the

wellhead and transported by pipeline through a field gathering system or trucked to

centralized storage tanks where it is treated, measured and stored for shipping. Once

the crude oil characteristics are determined, it is shipped through a trunk or

transmission pipeline system to a refinery or coastal port willing to purchase it. There

are more than 250,000 kilometers of field gathering pipelines and over 100,000

kilometers of transmission lines in Canada (CEPA, 2012a).

Refineries that are located close to water can receive crude by barge or large tanker

ships. Refineries with coastal water access compete with all other coastal refineries for

crude which making them a price taker of world oil prices. Inland refiners are also

typically price takers of world prices however in instances when supply dramatically

increases and outpaces the pipeline infrastructure in place to transport it, they can have

more leverage to reduce prices. Refineries with access to deep water ports compete

internationally in purchasing their crude feedstock or selling RPP’s making large

complex refineries more feasible than in inland areas as they have more options to buy

and sell.

Trucking and the use of rails cars provides flexibility to the delivery and distribution

networks. Although they are the most expensive options, they are just as critical to the

other cheaper systems as it is the combination of all three methods that makes the

global network reliable in delivering 90 million barrels of oil based products to end users

each day.

Depending on the distance and location, the transportation costs of moving a barrel of

crude or RPP over comparable distances is lowest by pipeline, then open water

shipping, followed by shipping by inland waterways, rail then trucking. Generally

speaking, open water is slightly higher than pipelines, inland waterways are moderately

higher that open water, rail is 3 to 5 times higher than pipelines with truck transportation

costs being the most expensive but over shorter distances trucking provides a

reasonable solution. The toll rate for transporting a barrel of light crude from Edmonton,

Alberta to Sarnia, Ontario in the Enbridge Mainline pipeline is $3.95 while the toll rate

from Portland, Maine to Sarnia is $4.40 (CAPP, 2012a, p.40). Rail costs from Alberta to

the East Coast can be from $12.00 to $15.00 per barrel (EIA, 2012c).

Once refined, products are shipped by pipeline, ship, rail or truck to local distribution

terminals. In the east coast Maritime region, almost all RPP are delivered by ships and

barges however in the rest of Canada it is efficient for pipelines, rail and trucks to

combine in product distribution. Due to the refinery consolidation in the Canadian

A Strategic Analysis of Petroleum Refining Infrastructure In Canada

Page 18

Industry, in many markets only one terminal is available for all marketers for loading. In

these areas, products exchange agreements are common where a refiner in one area

agrees to provide product to a competitor in that area where they do not have a refinery.

Most of the product distribution network is owned by the larger refiners, Shell, Imperial

Oil, Suncor, Ultramar, Federated Co-op, Husky and Chevron (Natural Resources

Canada, 2008, pp. 28-30).

Inventory of RPP is stored at local distribution terminals or at strategically located

storage terminals. Refiners build up inventory of crude and RPP to absorb

unanticipated supply disruptions, refinery shutdowns, regular refinery maintenance

(turnarounds) and seasonal variations in product demand. Inventory hold levels are

quite different from region to region in Canada (Natural Resources Canada, 2008, pp.

33-34).

The marketing and retailing of RPP is carried out by numerous companies and

intermediaries however they can be segregated into integrated refiner marketers or

independent marketers, companies which do not won a refinery. Of the existing eleven

companies that own refineries, nine are refiner-marketers. Refiner-marketers controlled

26% of the gasoline service stations in 2010 and 16% is under the control of the top

three, Shell, Suncor and Imperial Oil. Independent operators own the remaining 74% of

which between 15- 25% of the market is owned by a half dozen larger independent

retailers (M.J. Ervin & Associates, 2011, pp. 8-10).

Refineries

Refineries are designed with different processing configurations to efficiently refine

different weights of crude into products. Heavier crudes require more elaborate

chemical and thermal refining to optimize product yield. Refineries are categorized into

three general configurations (Natural Resources Canada, 2008, pp. 23-24);

1) Topping plants consists of crude distillation unit (CDU) and normally has a

catalytic reformer. These plants are designed to efficiently handle light sweet

crudes and condensates. Although they can process heavier crudes into

asphalt and heavy fuel oil, they are not efficient in processing heavy fuels into

lighter refined products such as gasoline.

2) Cracking refineries take the heavier middle streams of gas oils from a CDU

and “cracks” the complex gas compounds into simpler, lighter gasoline and

distillates compounds using a combination of chemical catalysts, high

temperatures and pressure.

A Strategic Analysis of Petroleum Refining Infrastructure In Canada

Page 19

3) Coking refineries processes the heaviest streams of oil and thermally cracks

the carbon bonds in heavy oils into lighter compounds using a coker or a

coker plus hydrocracker (fluid catalytic cracking unit - FCCU). Coker’s and

hydrocrackers allow the refinery to process heavier crude slates while still

yielding a high amount of lighter products. Coker’s and hydrocrackers can

operate independent of CDU complexes to upgrade heavy oil before shipping

the crude for further refining. Heavy oil upgraders create a lighter, sweeter

feedstock known as synthetic oil which has refining characteristics similar to

WTI and therefore command a higher price when sold to refineries.

In addition to these three basic configurations, each process may be paired with a

“hydrotreating” unit to reduce the sulfur and nitrogen content in crude. With the lower

sulfur content standards required by regulations more hydrotreating units are being

added to refineries as they are capable of removing up to 95% of the sulfur contained in

crude (Natural Resources Canada, 2008, p. 23-24).

These different refining configurations yield different products percentages dependant

on the weight of the crude inputted. For example, using heavy oil as a feedstock would

yield different percentage yields in each configuration.

Figure 5 - Product Yields of Refinery Configurations Using Heavy Oil Feedstock

(National Resources Canada, 2012)

Although there is some flexibility in designing the configuration to yield a higher ratio of

gasoline to distillates, or visa versa, this flexibility is limited and after a certain point

production must be increased to produce the amount of product required. Typically, a

cracking refinery will yield the following product percentages;

A Strategic Analysis of Petroleum Refining Infrastructure In Canada

Page 20

Figure 6 - Expected Yield of a Cracking Refinery

(CEPA, 2012b)

Product Slate Demand

Refining crude produces a wide array of products however it is also necessary to match

the production of products to the demand for the products.

Figure 7 - Canadian Domestic Refined Product Sales (2011)

Motor gasoline 42.00%

Diesel fuel oil 28.45%

Aviation turbo fuel, kerosene type 5.62%

Heavy fuel oil 4.59%

Petro-chemical feedstock 4.16%

Asphalt 3.84%

Light fuel oil 3.19%

Other petroleum products 2.87%

Petroleum coke 1.67%

Lubricating oils and greases 1.03%

Propane and propane mixes 1.00%

Butane and butane mixes 0.89%

Stove oil, kerosene 0.56%

Naphtha specialties 0.06%

Aviation gasoline 0.06%

Aviation turbo fuel, naphtha type 0.01%

Total RPP 100.00%

(Statistics Canada, 2012, p 11)

A Strategic Analysis of Petroleum Refining Infrastructure In Canada

Page 21

Balancing refinery configurations with the availability of crude feedstock to yield the

appropriate amounts RPP demanded requires careful planning. More often the process

yield excess which cannot be fully utilized within a supply region, the most prudent

method to clear the market of a product surplus is to sell and transport it out of the

region.

Over the past ten years, domestic sales of RPP have grown in aggregate 195,949 bpd

from 1,622,227 bpd in 2002 to 1,818,175 bpd in 2011. Although this represents a

12.1% growth (Statistics Canada, 2012, 2003) or 1.15% Compounded Average Annual

Growth Rate (CAGR) over a ten year period (Gitman and Hennessey, 2008, p. 318),

domestic demand exhibits substantial annual variation.

Figure 8 - Canadian Domestic Sales of RPP 2002 - 2011

Although the demand for RPP is obviously being influenced by economic growth, other

issues such as societal initiatives directed towards reducing energy intensity and the

growing awareness of the environmental damage caused by Green House Gases

dampen the growth expectations of the RPP.

The rate of growth in the use of individual products has been uneven. Over the past ten

years, national gasoline sales have increased 11.7% while diesel sales have increased

A Strategic Analysis of Petroleum Refining Infrastructure In Canada

Page 22

33%. The use of heavy fuel oil is down 33%, light fuel oil is down 27% but asphalt is up

26.7%.

Figure 9 - Canadian Product Demand

Summary

The relative volume of different products that the process of refining crude yields is a

function of the crude slate inputted into the refinery and the configuration of the refinery.

Different crude slates used as feedstock will produce different product yields in different

configurations.

Figure 10 - Major Elements of Refining Supply Network

Crude Oil

Slate

Mid-stream

Options

Refinery

Configuration

and Capacity

Product

Slate

Yield

Refined

Product

Demand

A Strategic Analysis of Petroleum Refining Infrastructure In Canada

Page 23

Matching a source of crude to a particular refinery’s product yield to satisfy product

demand is challenging especially given the long lead times involved in adjusting the

physical components of this chain to demand which can respond to environmental

changes much quicker.

3.2.1 Industry Structure in Canada

Refining infrastructure in Canada has undergone constant restructuring over the past 40

years. Since 1970, the number of operating refineries has dropped from 49 to just 18

producing refineries today (CAPP, 2012b). This reduction of the number of refineries in

Canada was not a function of reduced demand for refined products but was undertaken

to take advantage of economies of scale in the production of refined products. In spite

of this 61% drop in the number of refineries, the refining capacity in Canada has

increased 47% during this same time period (BP, 2012a).

Figure 11 - Refinery Capacity Verses Number of Refineries

This reduction in the number of operating refineries has concentrated the ownership

control of these refineries. The remaining 18 operating refineries are owned by 11

companies; two companies control 43% of Canada’s refining capacity while largest five

refinery owners control 80% (CAPP, 2012a).

A Strategic Analysis of Petroleum Refining Infrastructure In Canada

Page 24

Figure 12 - Ownership of Canadian Refinery Capacity

Company Capacity

(bpd) % Total

Capacity

Imperial Oil 516,000 25.67%

Suncor 350,000 17.41%

Irving Oil 300,000 14.93%

Ultramar 265,000 13.18%

Shell Canada 175,000 8.71%

Five Largest Refiners 1,606,000 79.90%

Next six owners 404,000 20.10%

Total Canadian Capacity 2,010,000 100.00%

(CAPP, 2012a, pp. 39-40)

Vertically integrated oil companies own 57% of the refining capacity, 18.7% are State

Owned Enterprises (SOE) while the remaining are independent of upstream production

although some have downstream retail marketing outlets .

Further complicating this oligopoly structure is the regional concentration of these large

refineries:

- 67% of Western Canada’s refinery capacity is owned by three

companies,

- 84% of Ontario’s capacity is owned by three companies,

- 100% of Quebec’s capacity is owned by two companies while,

- 83% of the Maritime Provinces capacity is owned by two companies.

In addition to the concentration of ownership, in certain regions of Canada, individual

large refineries produce a disproportionate share of the regions RPP. The Ultramar

265,000 bpd refinery in Levy, Quebec represents 67% of Quebec’s throughput capacity

and without it operating Quebec would require 225,000 bpd of petroleum products from

outside Quebec and Ontario would require an additional 40,000 bpd that Quebec

refineries currently provide.

A Strategic Analysis of Petroleum Refining Infrastructure In Canada

Page 25

Industry defines throughput capacity as the volume of crude oil and feedstock that can

fed into the distillation unit which is sometimes referred to as the charge capacity of the

refinery (EIA, 2012b). Refineries can operate continuously 24/7 however about 5% of

operating time is consider necessary for annual maintenance. Consequently, refineries

that operate at 95% utilization are considered as being at full capacity. Refined product

outputs can confuse the issue as refining increases the volume of output by as great as

Figure 13 - Throughput Capacity of Canadian Refineries

Capacity Percent of

Western Capacity (bpd) Total

Husky Prince George 12,000 0.59%

Chevron Burnaby 55,000 2.72%

BC Capacity 67,000 3.31%

Imperial Oil Edmonton 187,000 9.23%

Shell Scotford 100,000 4.94%

Suncor Edmonton 135,000 6.66%

Husky Lloydminister 29,000 1.43%

Alberta Capacity 451,000 22.27%

Regina Consumers Co-Op 100,000 4.94%

Moose Jaw Refinery 15,000 0.74%

Saskatchewan Capacity 115,000 5.68%

Western Capacity 633,000 31.25%

Ontario Capacity

Nova Sarnia 78,000 3.85%

Suncor Sarnia 85,000 4.20%

Shell Sarnia 75,000 3.70%

Imperial Oil Sarnia 120,000 5.92%

Imperial Oil Nanicoke 120,000 5.92%

Ontario Capacity 478,000 24.37%

Quebec Capacity Ultramar Levis 265,000 13.08%

Suncor Montreal 130,000 6.42%

Total Quebec Capacity 395,000 19.50%

Maritime Capacity North Atlantic Newfoundland 115,000 5.68%

Imperial Oil Dartmouth 89,000 4.39%

Irving Oil Saint John 300,000 14.81%

Total Maritime Capacity 504,000 24.88%

Total Canadian Capacity 2,010,000 100.00%

(CAPP, 2012a, pp. 39-40)

A Strategic Analysis of Petroleum Refining Infrastructure In Canada

Page 26

7% (volumetric gain) resulting in some refineries operating for short periods of time at

over 100% of capacity if output volumes of refined products are being compared to

capacity. Although refineries are routinely maintained and debottlenecked, no new

refineries have been built in Canada since 1984 (Natural Resources Canada, 2008,

p.25)

In 2011, Canada extracted over 3 million bpd of crude production of which

approximately 1.8 million bpd was used to meet the countries total demand for RPP.

Figure 14 - Summary of Canadian Refined

Products Production in 2011

Canada

Crude Slates

Light/Medium Conventional 689,544

Upgraded Synthetic 705,000

Heavy Oil 1,610,712

Total Orbit Domestic Supply 3,005,256

Crude Imports (Domestic) 326,140

Crude Imports (International) 679,581

Crude Exports - 2,342,427

Inventory Build (draw) 9,617

Other Feedstock 144,251

Refinery Charge Production 1,822,418

Volumetric Gains 87,863

Refinery output Production 1,910,281

Refined Imports 262,237

Refined Exports 387,870

Adjustments/Interprovincial 33,526

Net Refined Products 1,818,174

Demand

Gasoline 762,485

Diesel 517,289

Heavy Fuel 86,730

Other Fuels 451,670

Total Demand 1,818,174

(Statistics Canada, 2012, p. 28-29)

A Strategic Analysis of Petroleum Refining Infrastructure In Canada

Page 27

On the surface the market appears to be a well-balanced market operating at 91% of

capacity (1,822,418/ 2,010,000 bpd) with the excess crude being exported. At a 91%

utilization rate refineries should be able to maintain a regular maintenance schedule and

operate at profitable levels. Over the past ten years the industry has maintained

utilization at 88% to 95% of available capacity.

Figure 15 - Canadian Refinery Utilization

Canada is a large country and the physical movements of large quantities of volatile

fluids create natural constraints which must be considered. It is expensive and

dangerous to move large quantities by rail or truck. Consequently, the lack of natural

deep water seaways or pipelines has created partially isolated regional zones of supply

and demand in Canada. When regional differences between capacities demand for

products are considered, specific regional imbalances begin to emerge.

A Strategic Analysis of Petroleum Refining Infrastructure In Canada

Page 28

Figure 16 - 2011 Regional Capacity Verses Demand

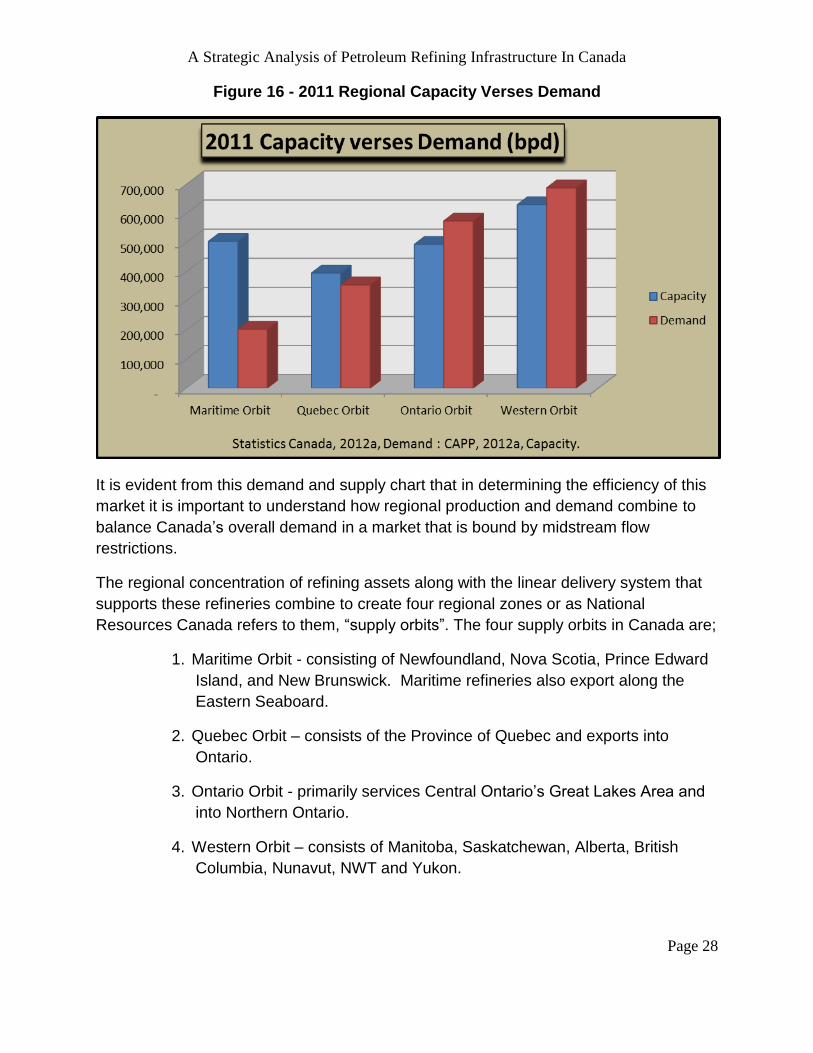

It is evident from this demand and supply chart that in determining the efficiency of this

market it is important to understand how regional production and demand combine to

balance Canada’s overall demand in a market that is bound by midstream flow

restrictions.

The regional concentration of refining assets along with the linear delivery system that

supports these refineries combine to create four regional zones or as National

Resources Canada refers to them, “supply orbits”. The four supply orbits in Canada are;

1. Maritime Orbit - consisting of Newfoundland, Nova Scotia, Prince Edward

Island, and New Brunswick. Maritime refineries also export along the

Eastern Seaboard.

2. Quebec Orbit – consists of the Province of Quebec and exports into

Ontario.

3. Ontario Orbit - primarily services Central Ontario’s Great Lakes Area and

into Northern Ontario.

4. Western Orbit – consists of Manitoba, Saskatchewan, Alberta, British

Columbia, Nunavut, NWT and Yukon.

A Strategic Analysis of Petroleum Refining Infrastructure In Canada

Page 29

Figure 17 - Canadian Supply Orbits

(Natural Resources Canada, 2012).

Each orbit has different sources of crude feedstock and each have developed unique

resources to refine petroleum products. Although nationally the demand for petroleum

products is balanced relative to production, regionally each orbit has significantly

different characteristics along the supply network. For example:

- The Maritime’s refine much more finished products than they consume

and as their refineries has access to ocean ports, the excess refined

products are exported to the US seaboard and into the Arctic.

- Ontario’s demand is greater than their production while Quebec’s

production is greater than demand. Consequently, Quebec’s

overproduction balances some of Ontario’s shortfall.

- Alberta extracts more crude than all of Canada can use however as

limited pipeline capacity is available flowing east and west, most of the

excess crude is exported to the US. Alberta also refines more RPP

than they consume and although their surplus is transported and

consumed in the supply orbit it is not sufficient to meet the orbits total

demand.

In order to provide a more transparent understanding of interrelationships of these orbits

we will examine the supply network in each orbit.

A Strategic Analysis of Petroleum Refining Infrastructure In Canada

Page 30

Maritime Supply Orbit

The Maritime supply orbit includes the provinces of Newfoundland, Nova Scotia, Prince

Edward Island, and New Brunswick. The three refineries in this orbit provides enough

refined products to meet all of the orbits domestic demand and export the surplus to the

Eastern Seaboard of the United States and into the Arctic.

The defining feature of this market is that their access to deep water ports provides a

flexible cost effective gateway to foreign markets not only for importing crude but also

for exporting finished products. The following production summary chart reflects the

orbits supply, production and demand structure whereas domestic crude which

originates from within the orbit accounts for 20% of the total crude input into refineries.

Figure 18 - Summary of Maritime Refined Products Production in 2011 (bpd)

Maritime Orbit

Crude Slates

Light/Medium Conventional 83,543

Upgraded Synthetic 0

Heavy Oil 2,712

Total Orbit Supply 86,255

Crude Imports (Domestic) -

Crude Imports (International) 325,035

Crude Exports -

Inventory Build (draw) 5,222

Other Feedstock 10,648

Refinery Charge Production 427,160

Volumetric Gains 20,617

Refinery Production 447,777

Refined Imports 39,427

Refined Exports 238,768

Adjustments/Interprovincial - 46,376

Net Refined Products 202,060

Demand

Gasoline 61,956

Diesel 48,542

Heavy Fuel 32,848

Other Fuels 58,714

Total Demand 202,060

(Statistics Canada, 2012a, p. 28-29)

A Strategic Analysis of Petroleum Refining Infrastructure In Canada

Page 31

Exports excluded, domestic crude could provide 45% of domestic consumption, with

volumetric gains taken into consideration. The surplus production from the refineries

allowed for 53% of the refined products to be exported out of the country and a net

16,000 bpd to be transferred to Ontario and Quebec’s orbits.

Crude Slates

The supply of crude in the Atlantic orbit is a mix of domestic production and imported

crude. During 2011, 83,500 bpd of light and medium crude and 2,700 bpd of heavy

crude were provided domestically, primarily from offshore production. Domestic crude

production provided about 45% of the orbits domestic demand. An additional 325,000

bpd was imported to meet the remaining 115,000 bpd domestic demand and provide

the feedstock for the 238,768 bpd of refined products exported out of the orbit. In 2011,

60% of the imported oil came from OPEC nations, primarily Saudi Arabia, Nigeria and

Angola, 15% came from the North Sea and the remaining came from numerous smaller

sources.

Of the 427,000 bpd of crude processed, 99% was a light or medium blend with the

remaining being a conventional heavy oil. The orbits typically maintains a crude

inventory of between 4 to 6 million barrels providing a 10 to 15 day supply of feedstock

or enough to meet domestic demand for 20 to 30 days (Statistics Canada, 2012, p 28).

This orbits access to deep water ports provides the Atlantic refineries with the ability to

purchase crude from multiple global sources. This optionality allows them to tailor the

purchases of their crude slate to an ideal mix that optimizes the yield of their refining

configuration and satisfy this orbits atypical demand for medium weight finished

products. This ability to pick and choose whatever supply source can provide the best

weight of crude for the refinery configuration historically was considered an advantage

as they were able to but product to best utilize their fixed cost design, rather than having

to design more complex refineries to produce the middle and heavier product slate that

the orbit demanded. However over the past number of years, this flexibility in crude

slate comes at a price as it must purchase crude based on Brent Petroleum prices

which has been trading at a 15 to 20 dollar premium to WTI prices.

Midstream delivery and distribution

Imported crude is delivered through sea faring vessels which dock at seaports and then

piped short distances to the orbits three refineries. No crude is transported in or out of

the orbit through pipelines. Waterways provide world access through the Atlantic

Ocean and the St Lawrence Seaway provides waterway access to Quebec and Ontario

supply orbits.

A Strategic Analysis of Petroleum Refining Infrastructure In Canada

Page 32

Refined products are primarily distributed through ships and barges to terminals and

storage facilities, from which products are typically trucked to end users. The inventory

of refined products held in storage terminals, range from 6 to 7 million barrels which is

sufficient to meet domestic and import demand for 15 to 18 days or domestic demand

for 32 to 38 days.

Refineries

The Atlantic supply orbit has three refineries, two larger complexes which provide over

80% of the orbits refined products and a smaller plant which also processes heavy oils

and produces the orbits asphalt supply.

Figure 19- Maritime Refinery Configurations Capacity

Capacity (bpd) % Total Configuration

North Atlantic – Newfoundland 115,000 22.82% CDU+Reformer/Cracker/Hydrotreating

Imperial Oil Dartmouth 89,000 17.66% CDU+Reformer/Cracking/hydrotreating/Asphalt

Irving Oil Saint John 300,000 59.52% CDU+ Reformer/Cracking/Hydrotreating

Maritime Orbit Capacity 504,000 100.00%

(CAPP, 2012a, p. 39- 40)

Utilization in 2011 was 85% of capacity however over the past 10 years has averaged

90% of capacity. Domestic demand was 202,060 bpd in 2011 which represents 40% of

orbits capacity, so even if one refinery went out of production domestic demand could

still be satisfied from the remaining refineries without depleting inventories. The surplus

output is exported primarily to the US however some surplus is transported to the

Quebec and Ontario orbits and supplies the east coast of the Canadian Arctic.

Product Demand

Atlantic Canada has historically had a somewhat atypical demand profile as their large

refining capacity has developed a reliance on heavy fuels for electricity generating

plants and middle distillates for home heating. The orbits reliance on heavier fuel

products can be easily recognized in a comparison with Canada’s aggregate domestic

product consumption mix.

A Strategic Analysis of Petroleum Refining Infrastructure In Canada

Page 33

Figure 20 - Product Demand Mix Canada Verse Maritime

In the past it was cost effective to use heavier oil based sources for electricity and home

heating however recently these uses are being displaced by lower cost natural gas. This

shift to substitute products is reflected the in the negative demand trends in heavy fuel

oil and stove kerosene (included in “Others”) over the past 10 years.

Figure 21 - Maritime Product Demand

A Strategic Analysis of Petroleum Refining Infrastructure In Canada

Page 34

The orbit is self-sufficient in its ability to produce all the different RPP that it uses except

for lubricating oil and greases of which it must import about 1000 bpd. The Maritime’s

orbits excess capacity and ability to sell off unused surplus can efficiently manage any

changes to its domestic demand structure or short term disruption in production.

A Strategic Analysis of Petroleum Refining Infrastructure In Canada

Page 35

Quebec Supply Orbit

The Quebec supply orbit consists of the province of Quebec. There are two refineries in

this orbit which provides sufficient production capacity to satisfy the orbits demand.

Quebec does not produce any crude consequently 92% of its required feedstock is

imported from outside of Canada, 7% is from the Maritime orbit and a small amount has

recently found its way from Western Canada.

Figure 22 - Summary of Quebec Orbits Refined

Products Production in 2011 (bpd)

Quebec

Crude Slates

Light/Medium Conventional 0

Upgraded Synthetic 0

Heavy Oil 0

Total Orbit Supply 0

Crude Imports (Domestic)

26,429

Crude Imports (International) 302,528

Crude Exports 0

Inventory Build (draw) 4,810

Other Feedstock 15,634

Refinery Charge Production 349,401

Volumetric Gains 4,581

Refinery Gross Production 353,982

Refined Imports 85,407

Refined Exports 56,804

Adjustments/Interprovincial - 28,084

Net Refined Products 354,501

Demand

Gasoline 154,728

Diesel 90,799

Heavy Fuel 22,360

Other Fuels 86,614

Total Demand 354,501

(Statistics Canada, 2012a, p. 38-39)

Crude Slates

As previously mentioned, Quebec’s supply of crude is 92% imported crude and 8% from

domestic supply. The domestic supply is primarily from offshore Atlantic production

A Strategic Analysis of Petroleum Refining Infrastructure In Canada

Page 36

however about 3,000 bpd is from the Western Orbit bring brought through Ontario.

Approximately 302,000 bpd was imported from outside of Canada to meet domestic

demand. OPEC nations, primarily Algeria and Angola, accounted for 53% of the

imported supply, the North Sea provided 16%, and the remaining came from numerous

smaller sources.

Of the 349,000 bpd of crude used, 86% was a light sweet blend, 13% was conventional

heavy oil and a small amount of synthetic crude was processed. Crude inventory levels

are maintained between 7 to 9 million barrels which is sufficient to provide 15 to 20

day’s supply of feedstock for the refineries.

Midstream delivery and distribution

Quebec has good waterway access to global markets through the St. Lawrence Seaway

and also has good pipeline access to feedstock from Northeast US and from Montreal

into Ontario. As the size of vessels that can access the Seaway is limited, it is often cost

effective for crude to be transported by pipeline or unit train. The Seaway is impassable

at time during the winter months which necessitates a higher level of inventory during

winter. In 2011 almost half of the crude used in refining was transported to the refineries

by pipeline.

A 240,000 bpd pipeline moves crude from Montreal, Quebec to Sarnia, Ontario

(Enbridge’s Line 9). Originally, the line was designed to transport Western crude to

Montreal however it was reversed in 1999 to help balance feedstock demands in

Ontario. Enbridge has applied to once again reverse this line in 2014 and increase its

flow capacity to 300,000 bpd to accommodate the transportation of Western crude to

Montreal (Enbridge, 2012). Supplying 200,000 plus bpd of WTI priced western crude to

Montreal would be expected to immediately displace the higher Brent Oil priced

imported oil and dramatically reduce this orbits dependence on the 300,000 bpd of

imported oil.

Refined products are distributed through barges, local area pipelines and trucks to

terminals and storage facilities, from which products are typically trucked to end users.

The Trans Northern Pipeline (TNPL) is a 132,600 bpd refined product transmission line

from Montreal to the Toronto area and Ottawa. This line allows RPP from Montreal

refineries and global imports arriving at Montreal via the Seaway access to the southern

Ontario market.

Inventory of refined products held in storage and terminals ranges from 11 to 12.5

million barrels which is sufficient to meet demand for 30 to 36 days.

A Strategic Analysis of Petroleum Refining Infrastructure In Canada

Page 37

Refineries

Quebec only has two refineries and both are required to meet the orbits demand for

RPP. Both refineries have cracking units while the Suncor plant also has an asphalt

plant.

Figure 23 – Quebec Orbits Capacity

Capacity (bpd) % Total Configuration

Ultramar Levis 265,000 67.09% CDU/Cracking/Reformer/Hydrotreating

Suncor Montreal 130,000 32.91% CDU/ Reformer/Cracking/hydrotreating/Asphalt

Quebec Orbit Capacity 395,000 100.00%

( CAPP, 2012a, pp.39-40)

Utilization in 2011 was 89% of capacity however over the past 10 years has averaged

93% of capacity. Domestic demand was 354,501 bpd in 2011 which is more than any

one refinery can provide.

Product Demand

The mix of products demanded in Quebec emulates the aggregated Canadian Product Mix with some minor variations.

Figure 24 - Canada Verses Quebec's Product Demand Mix

A Strategic Analysis of Petroleum Refining Infrastructure In Canada

Page 38

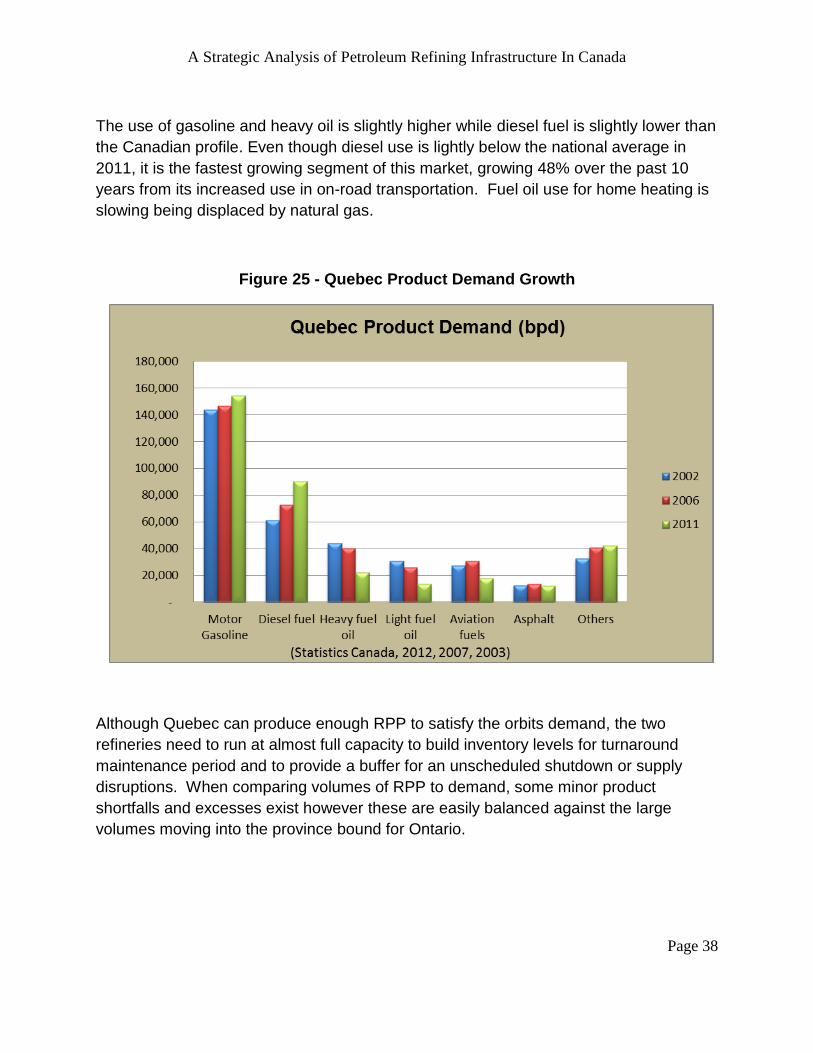

The use of gasoline and heavy oil is slightly higher while diesel fuel is slightly lower than

the Canadian profile. Even though diesel use is lightly below the national average in

2011, it is the fastest growing segment of this market, growing 48% over the past 10

years from its increased use in on-road transportation. Fuel oil use for home heating is

slowing being displaced by natural gas.

Figure 25 - Quebec Product Demand Growth

Although Quebec can produce enough RPP to satisfy the orbits demand, the two

refineries need to run at almost full capacity to build inventory levels for turnaround

maintenance period and to provide a buffer for an unscheduled shutdown or supply

disruptions. When comparing volumes of RPP to demand, some minor product

shortfalls and excesses exist however these are easily balanced against the large

volumes moving into the province bound for Ontario.

A Strategic Analysis of Petroleum Refining Infrastructure In Canada

Page 39

Figure 26 - Quebec's Product Balance

Even though the orbit is close to being self-sufficient in its ability to produce enough

RPP to meet demand, over 142,000 bpd of RPP was brought into the province and over

189,000 bpd was shipped out. This large volume of product movement is required for

various reasons:

- About 150,000 bpd of RPP is received and transferred into the

Ontario’s market to balance Ontario’s demand.

- RPP movement is needed to balance out the daily, weekly and

seasonal timing of the demand for certain types of products and

building inventories to meet these requirements in Quebec and Ontario

orbits.

- As Quebec refineries approach their operating capacity, there is a lack

of flexibility in the product yields. This lack of slack creates some

production excesses and shortfalls of products that need to be traded

off through exports or interprovincial transfers.

Moving products increase the costs of the system and can add $2 to $10 per barrel

depending on how it is transported and where it sold.

A Strategic Analysis of Petroleum Refining Infrastructure In Canada